at kearney powertrain 2025 study summary vpublish-1.pptx

TRANSCRIPT

P t i 2025A global study on the passenger car powertrain market towards 2025

Powertrain 2025

May 2012Study summary

A.T. Kearney Global Powertrain Team

Study introduction

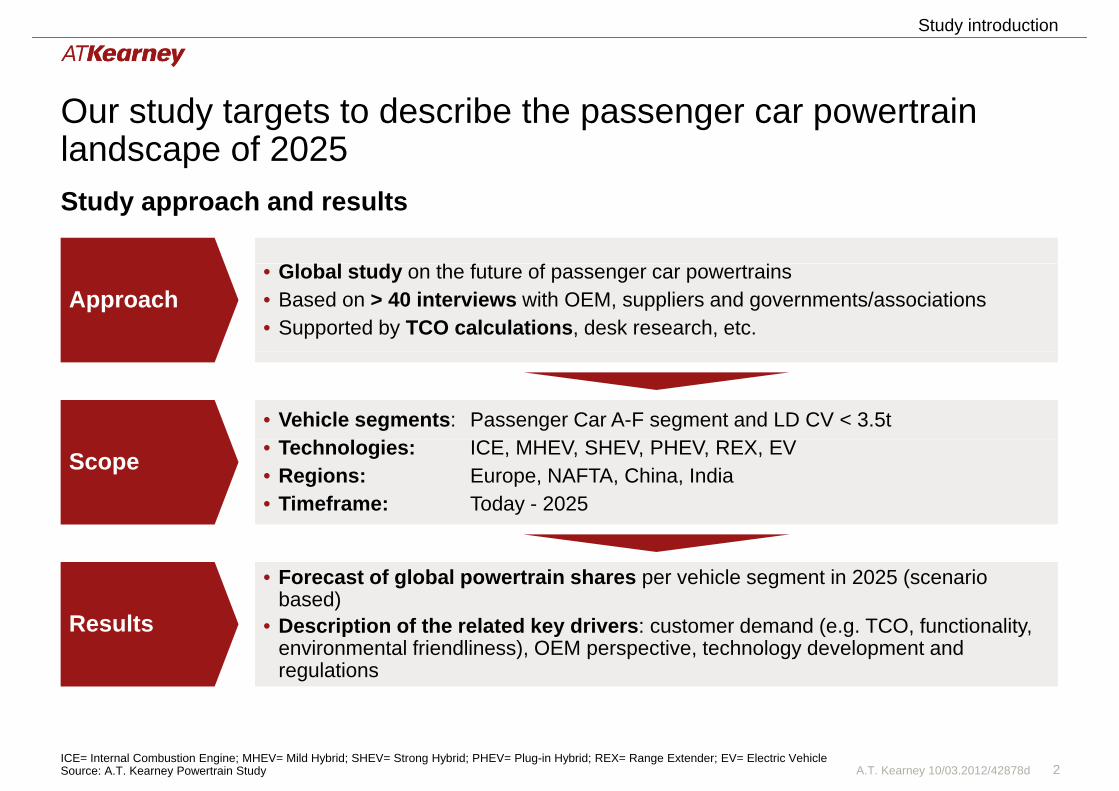

Our study targets to describe the passenger car powertrain landscape of 2025Study approach and results

G f fApproach

• Global study on the future of passenger car powertrains• Based on > 40 interviews with OEM, suppliers and governments/associations• Supported by TCO calculations, desk research, etc.

• Vehicle segments: Passenger Car A-F segment and LD CV < 3.5t

Scope • Technologies: ICE, MHEV, SHEV, PHEV, REX, EV• Regions: Europe, NAFTA, China, India• Timeframe: Today - 2025

R l

• Forecast of global powertrain shares per vehicle segment in 2025 (scenario based)

Results • Description of the related key drivers: customer demand (e.g. TCO, functionality, environmental friendliness), OEM perspective, technology development and regulations

A.T. Kearney 10/03.2012/42878d 2ICE= Internal Combustion Engine; MHEV= Mild Hybrid; SHEV= Strong Hybrid; PHEV= Plug-in Hybrid; REX= Range Extender; EV= Electric VehicleSource: A.T. Kearney Powertrain Study

Study introduction

Seven vehicle segments are in scope of the study; three major ones will be in the focus of this summaryVehicle segments

Basic(e.g. Fiesta)

Compact(e.g. Golf)

Lower Medium(e.g. A4)

Upper-Medium (e.g. 5-series)

Large & Luxury SUV LD (<3.5t) g y(e.g. 7-series) (e.g. Explorer)

( )(e.g. F-series)

A.T. Kearney 10/03.2012/42878d 3Source: A.T. Kearney Powertrain Study

= in focus of summary

Study introduction

The 2025 powertrain landscape is driven by boundary conditions, customer demand and OEM strategies

Boundary conditions

Drivers of the future powertrain landscape

Boundary conditionsHow do macro parameters impact powertrain developments?

Regulation Technology Fuel pricesRegulation Technology Fuel prices

Customer demandWhat do customers want?• Total costs of ownership

OEM strategyWhat do OEM plan to offer?• Technology strategyo a cos s o o e s p

• Functionality• Environmental friendliness

ec o ogy s a egy• Development status• SOP/ramp-up planning

All presented results are related to the “Moderate” scenario of the study (represents most likely development from today’s perspective)

A.T. Kearney 10/03.2012/42878d 4

(represents most likely development from today’s perspective)

Source: A.T. Kearney Powertrain Study

Boundary conditions

Future regulation will be a key driver for the electrification of the powertrain landscape Boundary conditions: Regulation Scenarios 2025

2025

CO2 limits • 75 g/km average(-38% cp to 2015)

• 102 g/km (54,5mpg; -43% cp to 2015)

• 112 g/km (-36% cp. to 2015)

• 130 g/km( 38% cp. to 2015)

• Binding segment specific limits

43% cp. to 2015)

• Binding segment specific limits

to 2015)

• Binding segment specific limits

• Fleet average limit

Taxation/ subsidies

• Moderate CO2-based tax

• Tax exemptions for EV/PHEV1

• Tax exemptions for EV/PHEV1

• Subsidies for EV in

• Low CO2-based tax

• No subsidies

the basic segment

E-only driving

• Some “e-only”-driving zones • No “e-only”-driving zonesg

zones

A.T. Kearney 10/03.2012/42878d 51. Stable total tax amount is assumed, i.e. if EV/PHEV are excluded from vehicle tax, the tax for other powertrains rises accordinglySource: A.T. Kearney Powertrain Study

Basic Segment Profile

The average customer in the Basic segment is very cost sensitive, but “Green Lifestyle” becomes more important

Customer groups & driving pattern Customer Demand

Basic: Customer Demand 2025

TCO Funct. EF1

Relevance

Customer groups & driving pattern Customer Demand

• TCO very important in the basic segment

• Low acquisition price and economical running

Relevance

Green lifestyle

FamiliesSinglesCar-sharingfleets • Low acquisition price and economical running

cost equally important

• Functionality and environmental friendliness comparably low in importance

12k km p.a.Long distance

20% p y p

• Only exception is “Green Lifestyle” customer group with limited TCO relevance and major affinity to “small, hip and green” vehicles, esp. EV

Urban40%

40%

20%

EVsExtra urban

A.T. Kearney 10/03.2012/42878d 61. Environmental friendlinessSource: A.T. Kearney Powertrain Study

Basic Segment Profile

In the Basic segment ICE will remain most beneficial in terms of acquisition costs and competitive in terms of TCO

TCO p a

Basic: Powertrain Assessment 2025

Functionality & Environmental

Functionality• Strong hybrid with best functionality score

TCO p.a.

Example Gasoline

yfriendliness

2.560€Strong hybrid with best functionality score

• EV with disadvantages in range and advantages in e-only driving capability

1.790€ 1.840€ 1.890€

• Gasoline with significantly lower acquisition

Environmental friendliness• EV with highest environmental friendliness

scores

EVGasoline Strong HEV

Gasoline Mild HEV

Gasoline

• Gasoline with significantly lower acquisition cost than HEV variants

• Acquisition cost in often more important than TCO due to limited purchasing power

• Strong hybrids with low CO2 emissions (71-77 g/km) and good green image communication

• EV with additional TCO of ~ €60/month

A.T. Kearney 10/03.2012/42878d 7Source: A.T. Kearney Powertrain Study

FinancingFuelOthers (vehicle tax, maintenance, VAT)

Basic Segment Profile

OEMs focus on improvement of conventional ICE and EVs for premium customers

Powertrain landscape 2025 (Moderate)OEM Strategy

Basic: OEM Strategy and Powertrain landscape 2025

Strategic assessment• Strategies mostly focused on low-cost improve-

ment measures for ICEs and mild hybrids

Powertrain landscape 2025 (Moderate)OEM Strategy

EV

18%ment measures for ICEs and mild hybrids

• In addition strong focus on EV for city usage pattern (“Green Lifestyle”)

ICE66%8%MHEV

8%SHEV

• High ICE share driven by (initial) cost sensitive customers

Examples HEV/EV• E-Smart

– EV

ICE

customers

• High EV share mainly used by “Green Lifestyle” customers

Li it d h f MHEV d SHEV

– SOP 2012

• E-Up!– EV

• Limited share of MHEV and SHEV– SOP 2013

A.T. Kearney 10/03.2012/42878d 8Source: A.T. Kearney Powertrain Study

Compact Segment Profile

The Compact segment has the most diverse customer group of all segments – everything is important…Compact: Customer Demand 2025

Customer groups & driving pattern Customer Demand

TCO Funct. EF1

Relevance

Customer groups & driving pattern Customer Demand

• Large segment with high bandwidth of customer types (families, singles, all age groups)

Relevance

Green lifestyle

FamiliesSingles Eldersgroups)

• Vehicle for most versatile usage patterns, typically only household vehicle for full range of activities

14k km p.a.Urban

25%Long distance

activities

• High importance of TCO in this segment

• However, premium customers in this segment with relevant functionality and environmental45%

30%25%

with relevant functionality and environmental friendliness requirements

45%Extra urban

A.T. Kearney 10/03.2012/42878d 91. Environmental friendlinessSource: A.T. Kearney Powertrain Study

Compact Segment Profile

In the Compact segment, TCO of ICE and hybrids will be very close together – in other criteria HEV/EV winCompact: Powertrain Assessment 2025

TCO p a Functionality & Environmental

Functionality• PHEVs with best functionality score (best

TCO p.a.

Example Diesel

yfriendliness

3.590€PHEVs with best functionality score (best active driving performance through electric engine, highest combined range and technological attractiveness)

2.420€2.460€2.330€2.260€

Environmental friendliness• EV and REX with highest environmental

friendliness scores

Diesel PHEV

Diesel Strong

HEV

Diesel Mild HEV

Diesel EV

• ICE with lowest TCO but very close to electrified powertrains, especially PHEV with competitive TCO

• EV with additional costs of ~ €100/month

friendliness scores

• PHEVs with very low CO2 emissions (~43g/km) and strong green image communication

• EV with additional costs of ~ €100/month

A.T. Kearney 10/03.2012/42878d 10Source: A.T. Kearney Powertrain Study

FuelOthers (vehicle tax, maintenance, VAT) Financing

Compact Segment Profile

The Compact segment powertrain landscape 2025 reflects the diversity of customer requirementsCompact: OEM Strategy and Powertrain landscape 2025

Powertrain landscape 2025 (Moderate)OEM StrategyStrategic assessment• Diverse picture of OEM strategies ranging from

MHEV and SHEV to PHEV

Powertrain landscape 2025 (Moderate)OEM Strategy

9%REX ICE

EV

10%

MHEV and SHEV to PHEV

• Also initial models of REX and EV for premium customers

9%

PHEV

35%

20%

Examples HEV• Peugeot 3008

– Diesel HEV • Very diverse powertrain landscape

MHEVSHEV

14%12%

– SOP 2011

• Toyota Prius– Gasoline PHEV

y p p• ICE with highest share but also broad

hybridization• High EV share mainly used by “Green

– SOP 2012 Lifestyle” customers

A.T. Kearney 10/03.2012/42878d 11Source: A.T. Kearney Powertrain Study

Upper Medium Segment Profile

In the Upper Medium segment, functionality and environmental friendliness will be of highest importanceUpper Medium: Customer Demand 2025

Customer groups & driving pattern Customer Demand

TCO Funct. EF1

Relevance

Customer Group 1 (60%)

Customer groups & driving pattern Customer Demand

Long distance12k km p.a.

• Segment with highest share of fleet vehicles, and highest overall mileage of all vehicle

RelevanceUrban

45%

35%20%

Extra urban

Long distance

Private user

segments

• Functionality with high importance due to comfort and driving experience requirements

Customer Group 2 (40%)25k km p.a.

• Environmental friendliness with high importance due to social pressure and fleet buyer’s requirements

TCO ith l i t

Urban

40%

20%40%

Long distance

Commercial user • TCO with low importance40% Extra urban user

A.T. Kearney 10/03.2012/42878d 121. Environmental friendlinessSource: A.T. Kearney Powertrain Study

Upper Medium Segment Profile

In terms of functionality, PHEVs will beat all other powertrain due to superior comfort and driving experienceUpper Medium: Powertrain Assessment 2025

Functionality TCO & Environmental friendliness

TCO• Very low differences between powertrain TCO

Functionality TCO & Environmental friendliness

Criteria WeightAcceleration

ScoreVery low differences between powertrain TCO

• E.g. Diesel with €3,470 p.a. and Diesel PHEV with €3,650 p.a.

Acceleration

Torque

Pure electric driving

Plug-inHEV

St Environmental friendliness• All HEV variants beat pure combustion engines

in terms of environmental friendliness

driving

NVH

Range (combined)1 Mild

StrongHEV

• Especially PHEVs with very low CO2 emissions (~60g/km) and strong green image communication

( )

Towing capacity

Technology tt ti

HEV

ICEattractiveness

A.T. Kearney 10/03.2012/42878d 131. Penalty for EV/REX, as minimum range (>300 km) is critical for customer acceptance in Upper-mediumSource: A.T. Kearney Powertrain Study

Upper Medium Segment Profile

PHEVs will dominate the 2025 Upper Medium powertrain landscapeUpper Medium: OEM Strategy and Powertrain landscape 2025

Powertrain landscape 2025 (Moderate)OEM StrategyStrategic assessment• Visible SHEV and PHEV strategy to achieve

CO limits and fulfill customer requirements

Powertrain landscape 2025 (Moderate)OEM Strategy

MHEVREX ICE

1%10%

1%CO2 limits and fulfill customer requirements (first PHEV launches planned for 2014+)

E l HEV

SHEV17%

1%1%

71%Examples HEV• BMW 5 Series HEV

– GasolineSOP 2011

PHEV71%

– SOP 2011

• Mercedes E HEV– Diesel– SOP 2012

• High PHEV share due to functionality advantages, green image and achievement of segment’s CO2 limits (roughly equal between Gasoline and Diesel)1SOP 2012 Gaso e a d ese )

A.T. Kearney 10/03.2012/42878d 14Source: A.T. Kearney Powertrain Study

The Future Powertrain Landscape

Until 2025, almost 60% of all new vehicles in Europe will use an electrified powertrain with a focus on PHEV

Powertrain volumes PC Changes towards 2025

The future Powertrain Landscape: Europe

(%) ICE• Significant decrease in marketshare• Remaining volumes mainly in cost sensitive smaller

vehicle segments12%7%1%2% vehicle segments

MHEV• Peak probably before 2020, decrease in share with

growing relevance of SHEV and PHEVP t ti l t b “ t d d i t” t d

14%

15% 24%

2%4%

• Potential to become “standard equipment” towards 2025

SHEV• Peak around 2020, decrease in share with growing 8%

11%12%99%

, g gimportance of PHEV

PHEV• Increases in importance between towards 2020 and

gains significant marketshares towards 202541%

50%

gains significant marketshares towards 2025• Combines high customer benefit with low CO2

emissions especially for larger vehicles

EV/REX20252011 2020

A.T. Kearney 10/03.2012/42878d 15

• Moderate growth until 2020 but especially EVs with double-digit share in 2025 mainly in Basic and Compact segment

Source: A.T. Kearney Powertrain Study

ICEPHEV MHEVREX SHEVEV

The Future Powertrain Landscape

In NAFTA, focus of electrification towards 2025 will be on affordable MHEV and SHEV solutionsThe future Powertrain Landscape: NAFTA

Powertrain volumes PC Changes towards 2025(%)

7%3%4%

3% 2%

ICE• Significant decrease in marketshare• Remaining volumes mainly in cost sensitive smaller

vehicle segments4%

20%10%

14%vehicle segments

MHEV• Peak around 2020 due to low costs solution to reduce

fuel consumptionP t ti l t b “ t d d i t” t d12%

20%97%

26%• Potential to become “standard equipment” towards

2025

SHEV• Struggles to gain major market shares compared to

37%45%

gg g j pMHEV (low end) and PHEV (upper end)

PHEV• Increases in importance between towards 2020 and

gains significant marketshares towards 2025

20252011 2020

gains significant marketshares towards 2025• Combines high customer benefit with low CO2

emissions especially for larger vehicles

EV/REX

A.T. Kearney 10/03.2012/42878d 16Source: A.T. Kearney Powertrain Study

EV MHEVREX ICEPHEV SHEV• Slow growth until 2020 and moderate growth towards

2025

The Future Powertrain Landscape

China will see the largest EV share but also have a large share of more affordable SHEV powertrainsThe future Powertrain Landscape: China

Powertrain volumes PC Changes towards 2025(%)

14%7%

ICE• Significant decrease in marketshare• Remaining volumes mainly in cost sensitive smaller

vehicle segments14%

17%

10%

20%

vehicle segments

MHEV• Peak around 2020 due to low costs solution to reduce

fuel consumptionP t ti l t b “ t d d i t” t d

24%100% 29%

• Potential to become “standard equipment” towards 2025

SHEV• Strong growth towards 2025 as affordable alternative

42%

10%

g gcompared to PHEV and EV

• Benefits from comparably low battery prices in China

PHEVI i i t b t t d 2020 d

20202011 2025

26% • Increases in importance between towards 2020 and gains significant marketshares towards 2025

• Benefits from comparably low battery prices in China

EV/REX

A.T. Kearney 10/03.2012/42878d 17Source: A.T. Kearney Powertrain Study

SHEVPHEV ICEMHEVREXEV• Moderate growth until 2020 but especially EVs with

double-digit share in 2025 mainly in Basic segment (governmental subsidies)

The Future Powertrain Landscape

India’s powertrain landscape will remain to be dominated by conventional ICE with a growing share of MHEVThe future Powertrain Landscape: India

Powertrain volumes PC Changes towards 2025(%) ICE

• Remains dominating powertrain type towards 2025• Will see significant technology improvements resulting

in emission and f el cons mption red ction

1%4% 1%7%

in emission and fuel consumption reduction

MHEV• Gains double-digit market shares towards 2025 as low

costs solution to further reduce fuel consumption

14%17%

costs solution to further reduce fuel consumption

SHEV• Moderate growth until 2025 due to comparably high

costs and limited buying power of customers81%

100%

PHEV• Some very minor marketshare in luxury segment

EV/REX

81% 75%

• No market share towards 2025

202520202011

A.T. Kearney 10/03.2012/42878d 18Source: A.T. Kearney Powertrain Study

MHEV ICESHEVPHEVREXEV

Contacts

Our global powertrain team is looking forward to discussion the study results with youAuthors

Dr. Götz Klink (Stuttgart, Germany): [email protected]

Stephan Krubasik (Munich, Germany): [email protected]

Dr. Thomas Weber (Frankfurt, Germany): [email protected]

Stephen Mickelson (Southfield, USA): [email protected]

Stephen Dyer (Shanghai, China): [email protected]

Manish Mathur (Gurgaon, India): [email protected]

The authors would like to thank Alexander Wünsch (Berlin, Germany) and Astrid Peine (Düsseldorf, Germany) for their valuable contributions to the study!

A.T. Kearney 10/03.2012/42878d 19Source: A.T. Kearney

A.T. Kearney is a global team of forward-thinking, collaborative partners that delivers immediate, meaningful results and long-term transformative advantage to clients.

Si 1926 h b d d i CEO d i h ld’ l di i i

Americas Atlanta Chicago Detroit Mexico City San Francisco Toronto

Since 1926, we have been trusted advisors on CEO-agenda issues to the world’s leading organizations across all major industries and sectors. A.T. Kearney’s offices are located in major business centers in 39 countries.

Americas AtlantaCalgary

Chicago Dallas

DetroitHouston

Mexico CityNew York

San FranciscoSão Paulo

TorontoWashington, D.C.

Asia Pacific BangkokBeijing

Hong KongJakarta

Kuala LumpurMelbourne

MumbaiNew Delhi

SeoulShanghai

SingaporeSydney

Tokyo

Europe Amsterdam Berlin BrusselsBucharest

BudapestCopenhagenDüsseldorfFrankfurt

HelsinkiIstanbulKievLisbon

LjubljanaLondonMadridMilan

MoscowMunichOsloParis

PragueRomeStockholmStuttgart

ViennaWarsawZurich

Ab Dh bi J h bMiddle East and Africa

Abu DhabiDubai

JohannesburgManama

Riyadh

A.T. Kearney 10/03.2012/42878d 20