asset/liability management pensions and other post employment benefits

DESCRIPTION

Asset/Liability Management Pensions and Other Post Employment Benefits. State Association of County Retirement Systems (SACRS) February 6, 2007 Navigating Public Pensions & OPEB with Liability Driven Investments Ryan Labs (www.ryanlabs.com) Sean McShea [email protected] - PowerPoint PPT PresentationTRANSCRIPT

1Ryan Labs Asset Management Asset/Liability Management

Asset/Liability Management Pensions and Other Post Employment Benefits

State Association of County Retirement Systems (SACRS)February 6, 2007

Navigating Public Pensions & OPEBwith Liability Driven Investments

Ryan Labs (www.ryanlabs.com)

Sean McShea [email protected] Adair [email protected] Johnson [email protected]

2Ryan Labs Asset Management Asset/Liability Management

Pension & OPEB: Problems

Problems:

1. Under Funding

2. Higher Net Costs (Accrued Liabilities)

3. Higher Contributions

4. Compounding in reverse (Negative Leverage)

5. CPI & COLA inflation < Medical inflation

6. Demographics

7. Mortality tables

8. Sunset communities vs. Sunrise communities

3Ryan Labs Asset Management Asset/Liability Management

Pension & OPEB: Crisis In Public Plans

Causes:

1. Silo effect (optimization in isolation)

2. Agency problem (no one in charge)

3. Morality issues (wealth transfer)

4. Asset Only Framework (mean variance models)

5. Actuarial Smoothing (No economic content)

6. Pro forma Accounting Return Assumptions

7. Lack of Financial Economics in pension practices

8. Peer Group (Beauty Contest)

4Ryan Labs Asset Management Asset/Liability Management

Solution Framework

Objectives Fund liabilities at lowest relative cost

Fund liabilities at lowest relative risk

Enhance Financial Statements

Enhance Credit Rating

Rules GASB 25, GASB 45

Teams Assets v. Liabilities

Playing field Present Value

Time Annual Financial Statements

Scoreboard Custom Liability Index

5Ryan Labs Asset Management Asset/Liability Management

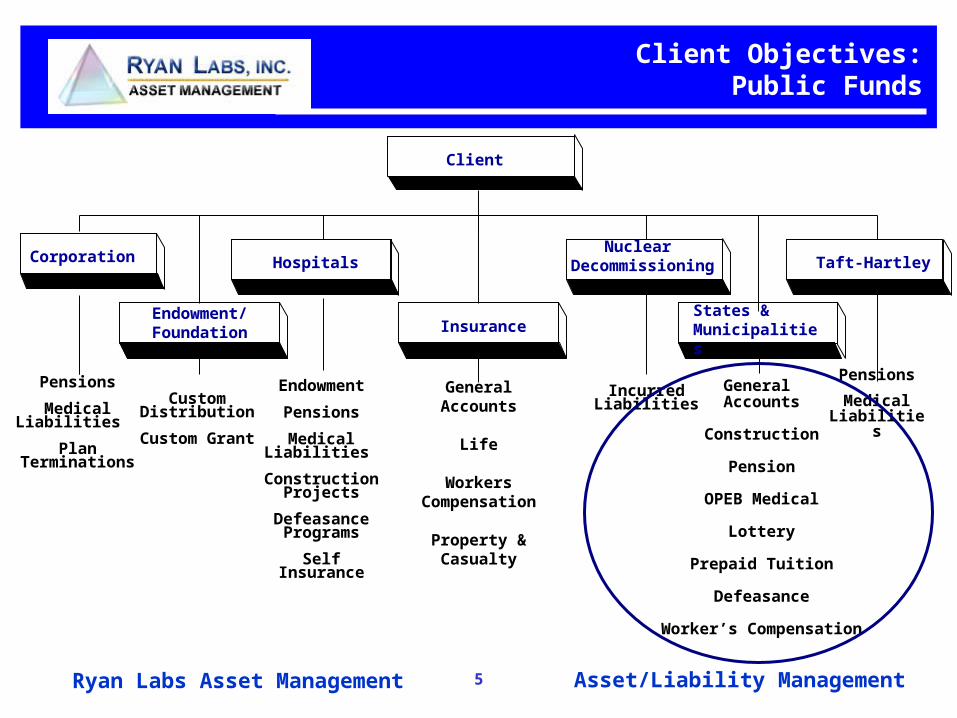

Client Objectives:Public Funds

Endowment

Pensions

Medical Liabilities

Construction Projects

Defeasance Programs

Self Insurance

Client

Pensions

Medical Liabilities

Pensions

Medical Liabilities

Plan Terminations

General Accounts

Life

Workers Compensatio

n

Property & Casualty

Custom Distribution

Custom Grant

General Accounts

Construction

Pension

OPEB Medical

Lottery

Prepaid Tuition

Defeasance

Worker’s Compensation

Incurred Liabilities

Nuclear Decommissioning

States &Municipalities

Taft-HartleyHospitals

InsuranceEndowment/Foundation

Corporation

6Ryan Labs Asset Management Asset/Liability Management

Government will not default on it promise

Prefunding ensures intergenerational fairness

Current stakeholder pays fair share current cost

Future stakeholder pays only for future cost

Minimize current costs by capturing equity risk premium

Protect the municipal bond rating and bonding capacity

Participants exchange direct for deferred compensation

Stakeholders own the pro rata share of balance sheet

Public Plans:Assumptions

7Ryan Labs Asset Management Asset/Liability Management

1. Benefit Management

Current benefits, Benefit enhancements

2. Contribution strategy

% of active payroll

Constrained by budget

3. Asset Allocation

Capture equity risk premium (Reduce cost)

Avoid risk

Public Plans:Three Key Levers

8Ryan Labs Asset Management Asset/Liability Management

Teams: Asset/Liability Watch (December 2006)

2006: Good year !!

9Ryan Labs Asset Management Asset/Liability Management

Assets vs. Liabilities Funding Volatility (December 2006)

10Ryan Labs Asset Management Asset/Liability Management

Risk: Risk is Based on the Objective

Risk is best defined as NOT meeting the client objective:

No Risk = Assets Match Liabilities

High Risk = Assets Don’t Match Liabilities

(Surplus Volatility)

Low Risk = Assets Behave Like Liabilities

Return of Portfolio – Return

of ObjectiveNew Sharpe Ratio =

STD (Portfolio Return – Objective Return)

11Ryan Labs Asset Management Asset/Liability Management

GASB 25 versus FASB 87/158(Difference between Public & Private)

Private versus Public

Authority FASB (Norwalk, CT) GASB (Norwalk, CT)

Inception 1973 1984

Mission Financial reporting

Output Useful, transparent information

Focus Point in time snapshotsOngoing

View in perpetuity

Bankruptcy Settlement focus Remote

Solvency Increased focus Not reported

Users Shareholders Stakeholders

12Ryan Labs Asset Management Asset/Liability Management

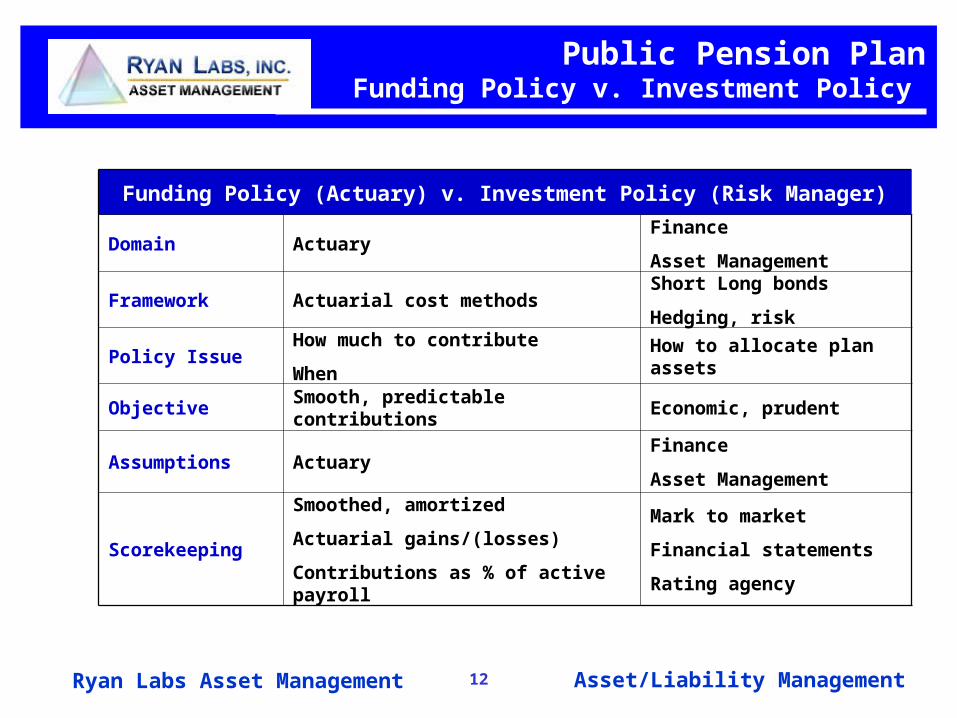

Public Pension PlanFunding Policy v. Investment Policy

Funding Policy (Actuary) v. Investment Policy (Risk Manager)

Domain ActuaryFinance

Asset Management

Framework Actuarial cost methodsShort Long bonds

Hedging, risk

Policy IssueHow much to contribute

When

How to allocate plan assets

ObjectiveSmooth, predictable contributions

Economic, prudent

Assumptions ActuaryFinance

Asset Management

Scorekeeping

Smoothed, amortized

Actuarial gains/(losses)

Contributions as % of active payroll

Mark to market

Financial statements

Rating agency

13Ryan Labs Asset Management Asset/Liability Management

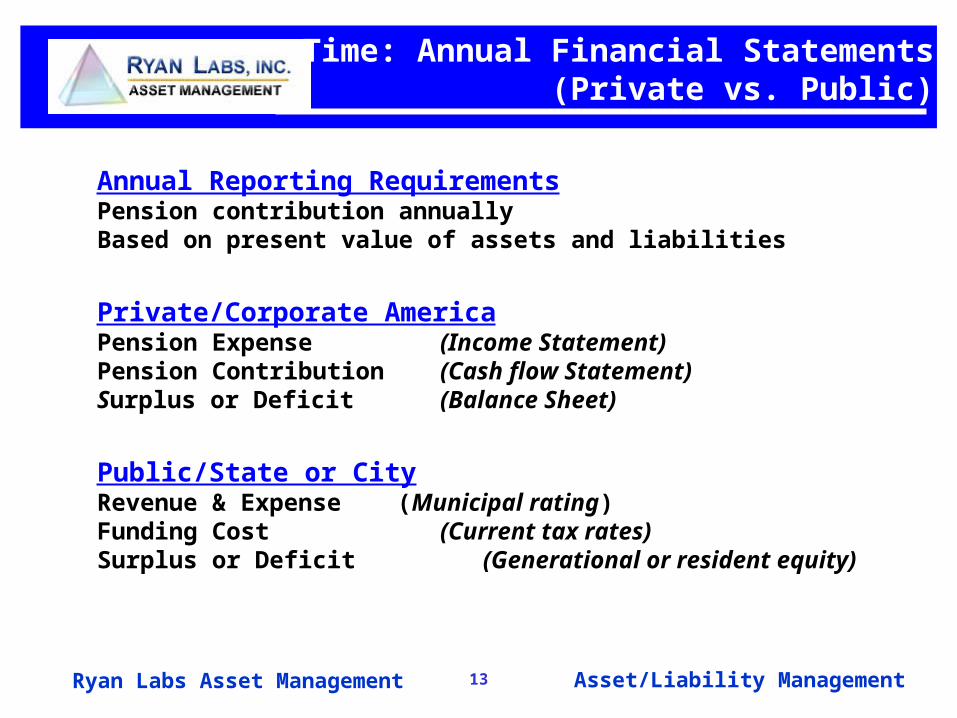

Time: Annual Financial Statements(Private vs. Public)

Annual Reporting RequirementsPension contribution annuallyBased on present value of assets and liabilities

Private/Corporate AmericaPension Expense (Income Statement) Pension Contribution (Cash flow Statement)Surplus or Deficit (Balance Sheet)

Public/State or CityRevenue & Expense (Municipal rating)Funding Cost (Current tax rates)Surplus or Deficit (Generational or resident equity)

14Ryan Labs Asset Management Asset/Liability Management

Rules: GASB 43 & 45(Non Pension Related Liabilities)

OPEB Other post employment benefits

GASB 43 Financial Reporting for Post Employment Benefit Plans Other Than pension plans

Requires accrual of liabilitiesReplaces pay-as-you go basis

GASB 45 Requires accrual of OPEB expense

15Ryan Labs Asset Management Asset/Liability Management

Playing Field: Time FrameLong Term Horizon v. Solvency

Public Plans : Horizon (10 to 20 year horizons)Prevailing Pension practiceSmoothing Assets (5, 10, 15 years)Amortization of Liabilities (15 to 30 years)Fully funding (assumes asset allocation return of 8%)Assumes Sponsorship Longevity

Private : Economic SolvencyBest Practice methodologyFair Value of Assets and Liabilities (Basel II)No smoothing100% interest rate drivenMark to Mark Valuation on Assets vs. Liabilities

16Ryan Labs Asset Management Asset/Liability Management

Playing Field: Solvency / Present Value $

Future value (Projected benefit payments)Inflation, COLAS, MortalityLabor costs/demographicsPlan designDon't know the future value of assets

Present valueDetermines funding adequacyRequired by SEC/FASB/PPA 2006100% interest rate drivenPriced using yield curve

17Ryan Labs Asset Management Asset/Liability Management

Public Fund Risk: Unpleasant Issues

Public Pension & OPEB PlansBankruptcy Taxpayer will pay

Stakeholders Taxpayers may escape deficits

Long Term FocusIntergenerational risk sharing

LT focus captures rewards without commensurate risks

Risk (Traditional)Annual contributions as a percent of active payroll or tax revenue

Smoothing Smoothing masks risk

18Ryan Labs Asset Management Asset/Liability Management

Problem: Investment ProcessPrevailing Practice vs. Best Practice

Current Actuarial Models and Methods

Current practice is not best practice

Financial Economic models expose flaws in standard modes

Calls for revision of actuarial training and practice

Financial Economics and Actuarial PracticeTony Day

Presented at The Great Controversy: Current Pension Actuarial Practice in Light of Financial Economics Symposium

Sponsored by the Society of ActuariesVancouverJune 2003

19Ryan Labs Asset Management Asset/Liability Management

Problem: Pro Forma ReturnsRisk Premium Review

75 Years, Starting Dec.

1925

Prospects January

2006 Starting Dividend Yield 5.40% (a) 1.94%

Growth in Real Dividends 1.00% 1.00%

Change in Valuation Levels* 1.70% ?????

Cumulative Real Return 8.10% 2.94%±

Less Starting Bond Real Yield 3.70% (b) 2.10% (c)

Less Bond Valuation Change**

-0.40% ?????

Cumulative Risk Premium 4.70% 0.84%

(a) Dividend Yield of S&P 500 Index(b) 3.7% yield, less an assumed 1926 inflation expectation of zero(c) The yield on US government inflation-indexed bonds

Based on Ibbotson data and First Quadrant research

20Ryan Labs Asset Management Asset/Liability Management

Generational Equality (Fair share of costs)

Pro Forma mechanism transfers risk ($1 equity > $1 bonds)

Reward is captured today, risk is transferred to the future

Smoothing feels good but contains no “economic” content

Current practice favors current management, taxpayers, plan participants, politicians, at the expense of future shareholders and stakeholders (taxpayers).

Source: Risk Transfer in Public Pension Plans, Jeremy Gold, PRC WP 2002-18, 2002, Pension Research CouncilThe Wharton School, University of Pennsylvania

Problem: StakeholderCurrent vs. Future

21Ryan Labs Asset Management Asset/Liability Management

Sub Optimal Decision Making

Benefit leakage (wage / pension negotiation)

Asset Allocation focused on asset only framework

Granting of valuable options (DROPS, skim funds)

Costly financing options (i.e. Pension Obligation Bonds)

Wealth transfer devices (i.e. Infrastructure Securitization)

Source: Risk Transfer in Public Pension Plans, Jeremy Gold, PRC WP 2002-18, 2002, Pension Research CouncilThe Wharton School, University of Pennsylvania

Problem for StakeholdersExpected Returns

22Ryan Labs Asset Management Asset/Liability Management

Actuarial Flaw: (Benefit Management & Funding)

Single Discount Rate

(Assumes “horizontal” term structure)

Not fully determined by market interest rates

(Usually 100 to 400 plus basis points too high)

Present Value calculation performed annually

(Usually the month plus delinquent)

Liability Term Structure not visible

(Short, Intermediate, Long, Very Long)

Problem: Actuarial Valuations (Mispricing Liabilities)

23Ryan Labs Asset Management Asset/Liability Management

Robert North, Chief Actuary of New York City

Actuarial methods based on actuarial interest rate (AIR)

Ignores financial economics

North ratio: NYCRS 70% Funded ($14 B deficit)

2005 CAFR : NYCRS 99% Funded (No deficit)

Source: Life & Pensions magazine, March 2006

Problem: DisclosureA New York City Pension Story

24Ryan Labs Asset Management Asset/Liability Management

Problem : Generic Indexes(Mean Variance Models)

Mean Variance Models based on Generic Indexes

Represent the market (Lehman Aggregate, S&P 500)(Subjective methodology)(Potential bias = Investment Banking, Trading)

NOT based on client liability schedule(Unique to each client)

Does NOT represent clients’ true objective

25Ryan Labs Asset Management Asset/Liability Management

Scoreboard: Custom Liability Index

Goal Measure growth, size, shape of liabilities

Features Market value, yield, duration, returns

Return Total return, index levels

Performance Money management index

Quantifies asset allocation

26Ryan Labs Asset Management Asset/Liability Management

Solutions: Adopt Liability Benchmark

27Ryan Labs Asset Management Asset/Liability Management

Structure Difference Liabilities vs. LB Aggregate

Duration Cell Port (% ) YTW MDUR Port (% ) YTW MDUR Port (% ) YTW MDURSHORT (0.00 - 0.50) 1.8 5.0 0.2 0.4 2.3 0.3 1.3 2.6 0.00.5 - 1.5 4.3 4.9 0.9 7.4 5.1 1.2 -3.1 -0.2 -0.21.51 - 2.5 4.4 4.7 1.9 10.9 4.9 1.9 -6.5 -0.2 0.02.51 - 3.5 4.4 4.6 2.9 9.1 5.0 2.9 -4.7 -0.4 -0.13.51 - 4.5 4.5 4.5 3.9 19.1 5.2 4.0 -14.6 -0.7 -0.14.51 - 5.5 4.5 4.4 4.9 18.8 5.5 5.0 -14.3 -1.1 -0.2LMTD (0.51 - 5.50) 22.0 4.6 2.9 65.3 5.2 3.5 -43.2 -0.6 -0.65.51 - 6.5 4.4 4.5 5.8 15.1 5.3 5.8 -10.7 -0.8 0.06.51 - 7.5 4.4 4.6 6.8 5.5 5.1 6.9 -1.1 -0.5 -0.17.51 - 8.5 4.3 4.6 7.8 2.5 5.0 7.6 1.8 -0.4 0.18.51 - 9.5 4.3 4.7 8.8 1.9 5.0 8.8 2.3 -0.4 0.09.51 - 10.5 4.2 4.7 9.7 1.2 5.1 9.6 2.9 -0.4 0.1INTER (5.51 - 10.50) 21.6 4.6 7.7 26.3 5.2 6.6 -4.7 -0.6 1.110.51 - 11.5 4.0 4.7 10.7 1.5 5.4 10.7 2.5 -0.6 0.011.51 - 12.5 3.9 4.8 11.7 2.5 5.6 11.7 1.4 -0.8 0.012.51 - 13.5 3.7 4.8 12.6 2.2 5.4 12.7 1.5 -0.5 0.013.51 - 14.5 3.6 4.9 13.6 1.2 5.5 13.5 2.4 -0.6 0.114.51 - 15.5 3.4 4.9 14.6 0.2 5.6 14.4 3.2 -0.7 0.215.51 - 16.5 3.3 4.9 15.6 0.3 4.9 15.8 3.0 0.0 -0.216.51 - 17.5 3.1 4.9 16.5 0.0 0.0 0.0 3.1 4.9 16.517.51 - 18.5 3.0 4.9 17.5 0.0 5.1 17.6 3.0 -0.2 -0.118.51 - 19.5 2.8 4.9 18.5 0.0 0.0 0.0 2.8 4.9 18.519.51 - 20.5 2.7 4.9 19.5 0.0 0.0 0.0 2.7 4.9 19.5LONG (10.51 - 20.50) 33.5 4.8 14.7 8.0 5.4 12.3 25.5 -0.6 2.420.51 - 21.5 2.5 4.8 20.5 0.0 0.0 0.0 2.5 4.8 20.521.51 - 22.5 2.4 4.8 21.4 0.0 0.0 0.0 2.4 4.8 21.422.51 - 23.5 2.3 4.8 22.4 0.0 0.0 0.0 2.3 4.8 22.423.51 - 24.5 2.1 4.8 23.4 0.0 0.0 0.0 2.1 4.8 23.424.51 - 25.5 2.0 4.8 24.4 0.0 0.0 0.0 2.0 4.8 24.425.51 - 26.5 1.8 4.8 25.3 0.0 0.0 0.0 1.8 4.8 25.326.51 - 27.5 1.7 4.7 26.3 0.0 0.0 0.0 1.7 4.7 26.327.51 - 28.5 1.6 4.7 27.3 0.0 0.0 0.0 1.6 4.7 27.328.51 - 29.5 0.8 4.7 28.2 0.0 0.0 0.0 0.8 4.7 28.229.51 - 30.5 0.5 4.7 29.3 0.0 0.0 0.0 0.5 4.7 29.3VLONG (20.51 - 30.50) 17.6 4.8 23.9 0.0 0.0 0.0 17.6 4.8 23.9ULTRA (30.51+) 3.5 4.7 36.2 0.0 0.0 0.0 3.5 4.7 36.2TOTAL 100.0 4.7 12.7 100.0 5.2 5.0 0.0 -0.5 7.7

Note: YTW = Yield To WorstMdur = Modified Duration

DifferenceLehman AggregateTotal Lives

28Ryan Labs Asset Management Asset/Liability Management

Solution:First Steps

Reduce Risk, Protect Expected ROA

29Ryan Labs Asset Management Asset/Liability Management

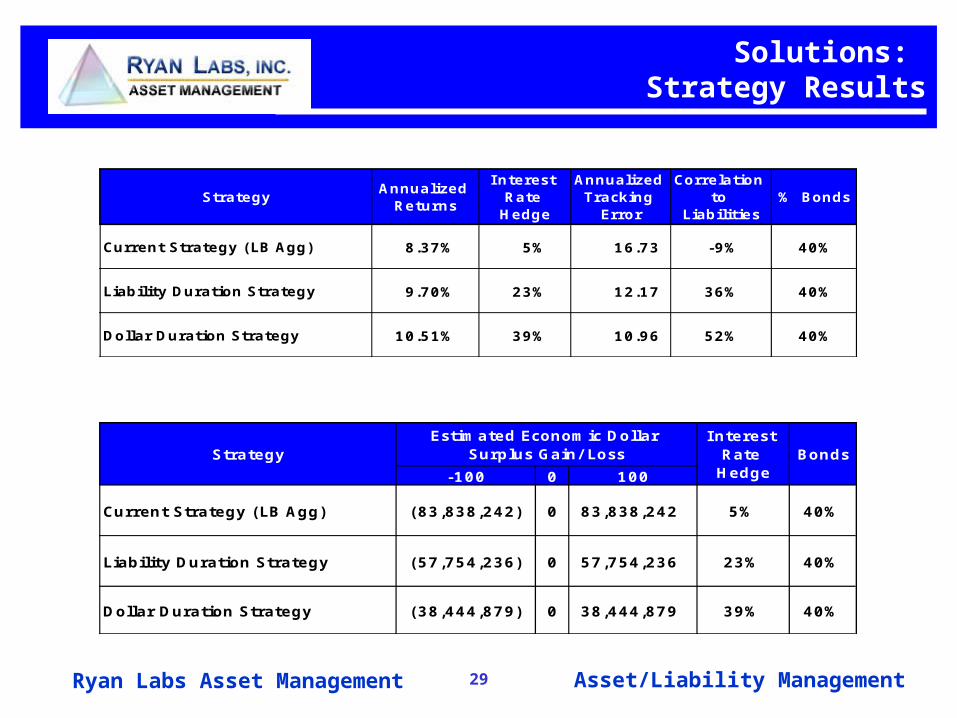

Solutions: Strategy Results

1 8.37% 5% 16.73 -9% 40%

2 9.70% 23% 12.17 36% 40%

3 10.51% 39% 10.96 52% 40%Dollar Duration Strategy

Current Strategy (LB Agg)

Annualized Returns

Liability Duration Strategy

% BondsCorrelation

to Liabilities

StrategyAnnualized Tracking

Error

Interest Rate Hedge

-100 0 100

0 Current Strategy (LB Agg) (83,838,242) 0 83,838,242 5% 40%

1 Liability Duration Strategy (57,754,236) 0 57,754,236 23% 40%

2 Dollar Duration Strategy (38,444,879) 0 38,444,879 39% 40%

Estimated Economic Dollar Surplus Gain/ LossStrategy

I nterest Rate Hedge

Bonds

30Ryan Labs Asset Management Asset/Liability Management

Scoreboard: Custom Liability Index

Goal Measure growth, size, shape of liabilities

Features Market value, yield, duration, returns

Return Total return, index levels

Performance Money management index

Quantifies asset allocation

31Ryan Labs Asset Management Asset/Liability Management

Benefits

Represents client objective (funding target)

Supports strategic & tactical asset allocation

Benchmark for asset management

Benchmark for performance measurement

Benchmark for risk management control

Foundation for risk budgeting

Solution: Custom Liability Index

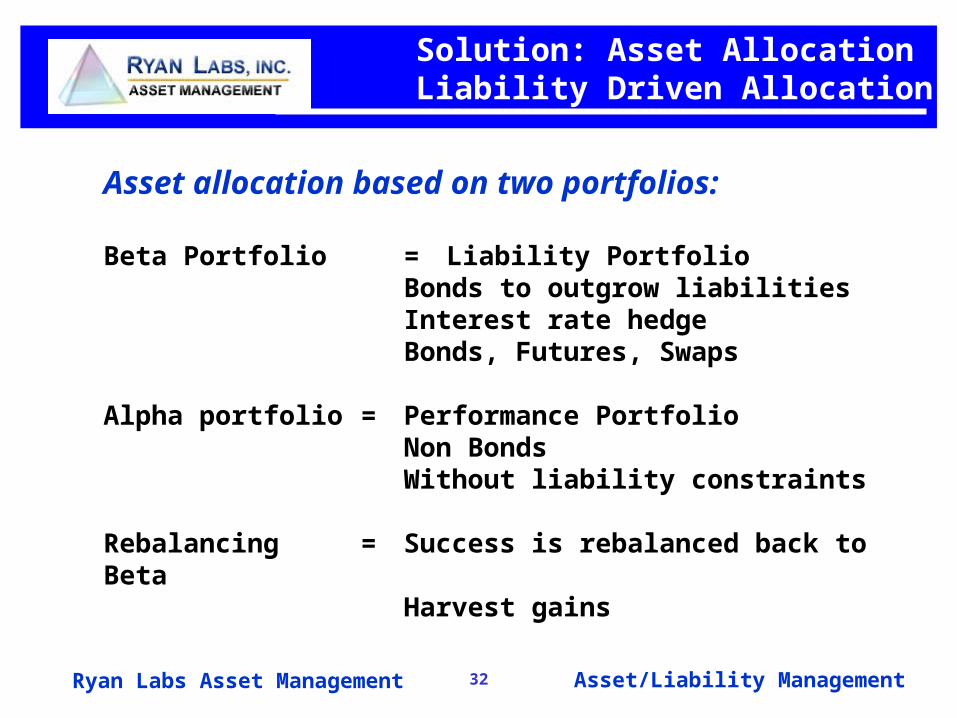

32Ryan Labs Asset Management Asset/Liability Management

Asset allocation based on two portfolios:

Beta Portfolio = Liability PortfolioBonds to outgrow liabilitiesInterest rate hedgeBonds, Futures, Swaps

Alpha portfolio = Performance PortfolioNon BondsWithout liability constraints

Rebalancing = Success is rebalanced back to BetaHarvest gains

Solution: Asset Allocation Liability Driven Allocation

33Ryan Labs Asset Management Asset/Liability Management

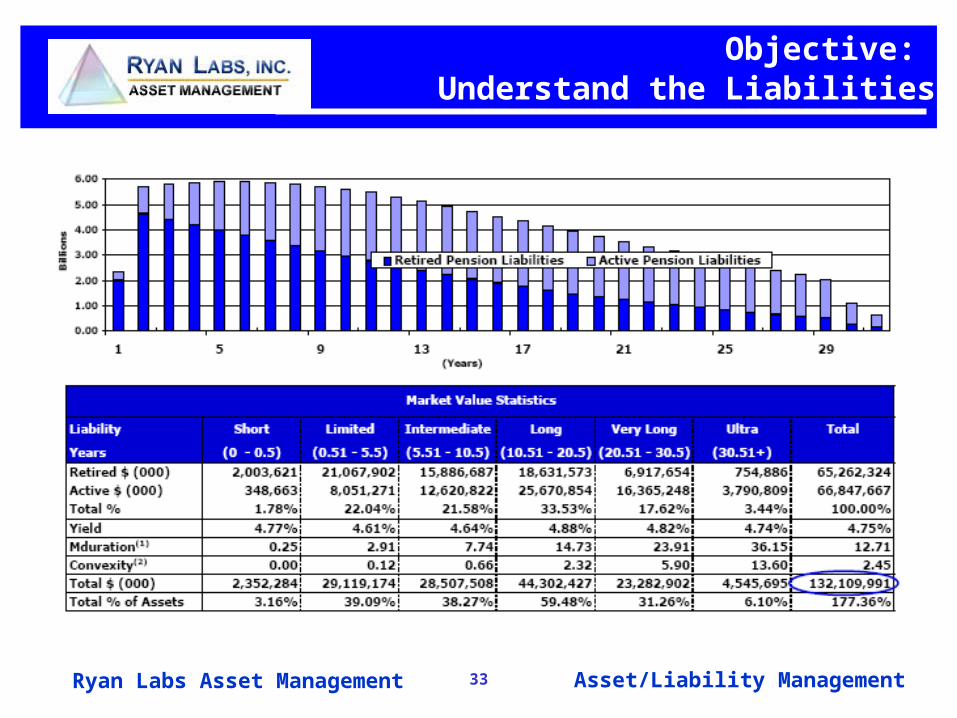

Objective: Understand the Liabilities

34Ryan Labs Asset Management Asset/Liability Management

Problem: Negative Leverage

35Ryan Labs Asset Management Asset/Liability Management

Solution: New Approach(New methodologies)

Transparency

Fair Value Accounting

Asset/Liability Management

Focus on Asset Allocation (Strategic/Tactical)

Alternative Asset Classes (Low correlation)

36Ryan Labs Asset Management Asset/Liability Management

Liability Risk

Asset Mix Risk

Active Risk

Traditional Approach LDI Approach

Source: Leo de Bever, Ontario Teachers' Pension

Solution: New Approach(New methodologies)

37Ryan Labs Asset Management Asset/Liability Management

Solution: Move Away From Single Focused Strategies

Source: First Quadrant/Research Affiliates

38Ryan Labs Asset Management Asset/Liability Management

Ryan Labs: Assets vs. Liabilities Monitor

The information presented herein was compiled from sources believed to be reliable. It is intended for illustrative purposes only, and is furnished without responsibility for completeness or accuracy.Past performance does not guarantee future results.

••

• ••

• •• •

••

• • • • • • • •• • • • •

•

6%

8%

10%

12%

14%

16%

6%

8%

10%

12%

14%

16%

0 2 4 6 8 10 12 14 16 18 20 22 24Volatility of Total Return (STD)

Twenty Year Returns - Period ending 12/31/05

Sources: Ryan Labs, Inc.- Standard & Poor's Corporation - Lehman Brothers - Merrill Lynch - Morgan Stanley Capital International - Frank Russell Company - Financial Times - Wilshire Asset Management - Crandall, Pierce & Company

AnnualizedReturn

•

••

••

••

•

•

•

•

• •

•

••

•

AnnualizedReturn

Ryan Labs5yr. Treasury

6.95%

Short Intermediate Long Very Long

Ryan Labs2yr. Treasury

6.16%

LehmanAggregate

7.88%

Ryan LabsLiability11.07%

Ryan Labs LiabilityIndex is represented by

the Treasury STRIPcurve (1 thru 25 years)

Merrill LynchYankee8.63%

Ryan Labs10yr. Treasury

7.58%

Ryan Labs6 mo. Bill 5.24%

FInancial TimesEquity Pacific

7.30%

Wilshire SmallCap Growth

12.00%

Ryan Labs3yr. GIC

6.75%

Merrill LynchHigh Yield

9.26%

Wilshire LargeCap Value

12.15%

S&P 50011.93%

P&I Asset10.61%

MSCI EAFE10.00%

Russell 200011.17%

Ryan Labs30yr. Treasury

8.79%

Assets vs. Liabilities Monitor(Last 20 years ending 2005)

39Ryan Labs Asset Management Asset/Liability Management

••

••

••

•••

••

••••• • • •

• • • • • •

-6%

-4%

-2%

0%

2%

4%

-6%

-4%

-2%

0%

2%

4%

0 2 4 6 8 10 12 14 16 18 20 22 24 26

Ann

ualiz

ed E

xces

s R

etur

ns v

s. R

yan

Labs

Lia

bilit

y In

dex

(%) A

nnualized Excess R

eturns vs. Ryan Labs Liability Index (%

)

Ryan Labs3yr. GIC

••

••

•

•

•

••

•

•

•

•

••

•

•

Ryan Labs5yr. Treasury

Merrill LynchHigh Yield

Merrill LynchConvertible

FInancial TimesEquity Pacific

LehmanAggregate

Ryan LabsLiability Index

P&I Asset

Ryan Labs LiabilityIndex is a proxy

for pension plans

Merrill LynchYankee

Wilshire LargeCap Growth

Ryan Labs10yr. Treasury

Wilshire LargeCap Value

MSCI EAFE

Russell 2000

Ryan Labs6 mo. Bill

Ryan Labs2yr. Treasury

Ryan Labs30yr. Treasury

LehmanGC Long

S&P 500

Annualized Tracking Error (TE) vs. Ryan Labs Liability Index (%)

Asset/Liability Return DifferenceAnd Tracking Error (Last 20 years)

Asset/Liability Return Difference

40Ryan Labs Asset Management Asset/Liability Management

Solution: Equity Correlation to Liabilities

Equity Correlations to Liabilities

Time HorizonAnnualized

Return on S&P 500

Annualized Return on

Liabilities (1)

Correlation

(S&P v. Liabilities)

1950 to 1960 16.16 1.54 (0.20)

1960 to 1970 8.18 1.47 0.21

1970 to 1980 8.44 4.73 0.25

1980 to 1990 13.94 13.69 0.40

1990 to 2000 17.44 11.24 0.26

2000 to 2002 (17.12) 10.71 (0.60)

2002 to 2004 19.45 6.17 0.02

2004 to 2006 10.21 5.95 (0.19)

(1) RL Treasury Long Index from 1949 to 1990, RL Liability Index from1991 to 2006,

41Ryan Labs Asset Management Asset/Liability Management

Solution: Next Steps

1. Adopt Liability Driven Investment strategy

2. Design Custom Liability Index

3. Document economic solvency

4. Document cash flow budgeting

5. Segregate Liability portfolio

6. Segregate performance portfolio

7. Reduce deficit, harvest gains back to liabilities

8. Grow surplus

9. Monitor risk

10. Document, Document, Document

42Ryan Labs Asset Management Asset/Liability Management

Solution: Small Steps

1. Move from prevailing practice to best practice

2. Create economic and actuarial reporting

3. Replace Policy benchmark with Liability benchmark

4. Understand limitations of peer group analysis

5. Structure fixed income to liabilities

6. Segregate Surplus (performance portfolio)

7. Positive story to trustees and rating agencies

8. Protect defined benefit pension plans