asset securitization report

TRANSCRIPT

AssetsecuritizationThe Premier Guide to Asset and Mortgage-Backed Securitization REPORT

AUGUST 2012Volume 12, Number 8

StructuredFinanceNews.com

WITH THE EUROPEAN DATAWAREHOUSE, ANYONE CAN SEE WHAT’S BEHIND THE REGION’S ABS. WILL IT BE ENOUGH TO REVIVE THE MARKET?

REVEALTHE FULL

C1_ASRAug12 1 8/2/2012 6:31:36 PM

C2_ASRAug12 2 7/30/2012 3:11:12 PM

ACONTENTS

COlumN23 The “Single Agency Security” Proposal

The ASF recently released a white paper entitled “Discussion of a Proposed Single Agency Security” that outlines the issues to be addressed in effectively merging the securities markets of Fannie Mae and Freddie Mac to reduce “TBA market inefficiencies.” This month’s column will discuss the implications of unresolved issues raised by the report.

>> by Bill Berliner

ABS 6 Basel II Proposal to Shift Market to More Rational Framework 9 Will New Regs Push ABS to Electronic Platforms? 16 The Return of SBA Loan ABS 20 Consolidation Shakes Up CLO Ranks 22 Univision Remains the Most Held Name in CLOs 24 Competing Funding Markets Push Private ABS to Fringes 25 After Maiden Lane, Supply Drought

mBS26 Rates and Govt. Programs to Boost

Near-Term Prepays

GlOBAl 28 GRAND Restructuring Aims to Make All Bondholders Winners

10 COvEr STOry

>> by Felipe Ossa

The Full RevealWiTh The euRopean DaTaWaRehouse, anyone Can see WhaT’s BehinD The Region’s aBs. Will iT Be enough ToRevive The MaRkeT?

www.StructuredFinanceNews.com // August 2012 �

003_ASRAug12 1 8/2/2012 6:32:02 PM

To improve on the extensive deal data covered in Asset Securitization

Report, we would like you to try out ASR Scorecards, an online

database designed to help you search for deals inside our crucial

scorecard data with 2 modes: DEALS and RANKINGS. You will not

only get current deal information but full deal listings from 2007.

Go to http://www.structuredfi nancenews.com/asr_scorecards

for a free 30-day trial and see for yourself what you’ve been missing.

TALKING ABOUTEVERYONE’S

LOOK WHATOne State Street Plaza, 27th Floor, New York, NY 10004

EditorialEditor: Karen Sibayan

[email protected]; 212.803.8735

Senior Editor/Europe: Nora [email protected]; 817.471.8272

Editor/Emerging Markets: Felipe [email protected]; 212.803.8709

ContributorsSally Ann Runyan • Bonnie McGeer

Group Editorial Director, Banking & Capital MarketsRichard Melville

[email protected]; 212.803.8679

Editorial Director, Capital Markets Newsletter GroupAllison Bisbey

[email protected]; 212.803.8271

PublishingEVP/Managing Director, Capital Markets Division: Mike Stanton

212.803.6552

Group Advertising Director: Harry Nikpour212.803.8638

Associate Publisher: Louis Fugazy212.803.8773

Marketing Manager: Megan Stalnaker212.803.8843

Circulation Sales: Dennis Strong212-803-8372

Reprint Sales Manager: Godfrey Livermore212.803.8351

Production & FulfillmentExec. Dir. of Creative Services: Sharon Pollack

Art Director: Scott Valenzano

Group Marketing Director: Edward Hanasik

Exec. Dir. of Manufacturing: Stacy Ferrara

Production Manager: Barbara W. Lau

Distribution Manager: Michael Candemeres

Distribution Coordinator: Brian Alexander

Fulfillment Manager: Tijana Jovanovic

Chief Executive Officer: Douglas J. ManoniChief Financial Officer: Rebecca Knoop

Executive Vice President and Managing Director, Banking and Capital Markets: Karl Elken

Executive Vice President and Managing Director, Professional Services and Technology: Bruce Morris

Executive Vice President, Chief Content Officer: David Longobardi

Executive Vice President, Marketing Solutions Adam Reinebach

Senior Vice President, Human Resources and Office Management: Ying Wong

Vice President, Finance: Jamie Brokowsky

Reproduction or electronic forwarding of this productis a violation of federal copyright law!

Site licenses are available — please call Customer Service 1.800.221.1809 or [email protected]

Subscription InformationPhone: 800.221.1809 212.803.8333

Bulk subscription US/Canada $2,259Annual Rate (48 issues) International $2,359 Fax: 212.803.1592

[email protected] Securitization Report - (ISSN # 1547-3422) Vol. 12, No. 8, is published monthly by SourceMedia, One State Street Plaza, 27th Floor, New York, NY 10004. Postmaster: Send address changes to Asset Securitization Report, SourceMedia, One State Street Plaza, 27th Floor, New York, NY 10004. All rights reserved. Photocopy permission is available solely through SourceMedia, One State Street Plaza, 27th Floor, New York, NY 10004. For back issues and bulk distribution needs, please contact Customer Service at (800) 221-1809 or e-mail: [email protected] Securitization Report is a general-circulation publication. No data herein is or should be construed to be a recommendation for the purchase, retention or sale of securities, or to provide investment advice of the companies mentioned or ad-vertised. SourceMedia, its subsidiaries and its employees may, from time to time, purchase, own, or sell securities or other investment products of the companies discussed or advertised in this publication. ©2012 Asset Securitization Report and SourceMedia, Inc. All rights reserved.

AssetsecuritizationThe Premier Guide to Asset and Mortgage-Backed Securitization REPORT

ecuritizationRT

� Asset Securitization Report // August 2012

004_ASRAug12 1 8/2/2012 6:32:22 PM

A Warehouse with a Mission

EDITOR’S LETTER

Scheduled to launch later this year, the European DataWarehouse will, for the first time, house loan-level data on a wide range of loans backing the region’s ABS. The European Central Bank is the information repository’s biggest client and champion.

In this month’s cover story, Felipe Ossa looks at the hows and whys of the new project. Although the U.S.’s mortgage sector is more advanced in terms of providing this type of

data to investors, what the Europeans have been able to demonstrate is how regulators and the private sector can work closely together to give securitization a fighting chance in today’s dysfunctional markets.

Despite initial resistance to the initiative — the Dutch banks have said they would not be shareholders in the warehouse — many European securitization players are ready to push forward, with RMBS the first asset class to have collateral loaded in.

On the home front, John Hintze reports that the new 700-page Basel proposal with com-ments due on Sept. 7 holds pleasant surprises for the securitization industry. Laurie Good-man, the head of RMBS strategy at broker-dealer Amherst Securities, said the requirements in this new version provide a more rational framework than either the one regulators pro-posed last year or, prior to that, the ratings-based approach.

What’s more, John explains that the proposal’s less severe capital charges for lower-rated ABS should result in banks shifting their investments to these securities, which offer them a considerable yield pick-up.

Elsewhere in securitization, Nora Colomer tackles an asset class that is experiencing a revival after a long hiatus — small business loan ABS. Nonbank lenders, who filled the void left by commercial banks in this business, need securitization to increase their access to fund-ing and to grow their lending volumes. Nora explores the motivation for these issuers and how the securitization of loans from a component of this market — the SBA 7(a) loans — was dormant until nine months ago, when the first of three deals appeared.

There’s action in other classes of securitized products as well. In his other story, John says that traditional private ABS issuers, at least the bigger ones, are tapping banks and 144A in-vestors. That’s because issuers have more options, with rated ABS deals back in fashion and bank financing more readily available.

Because of this, the private market is now hosting smaller deals backed by “off-the-run” and less common asset classes including music library receivables, delinquent tax returns and truck leases.

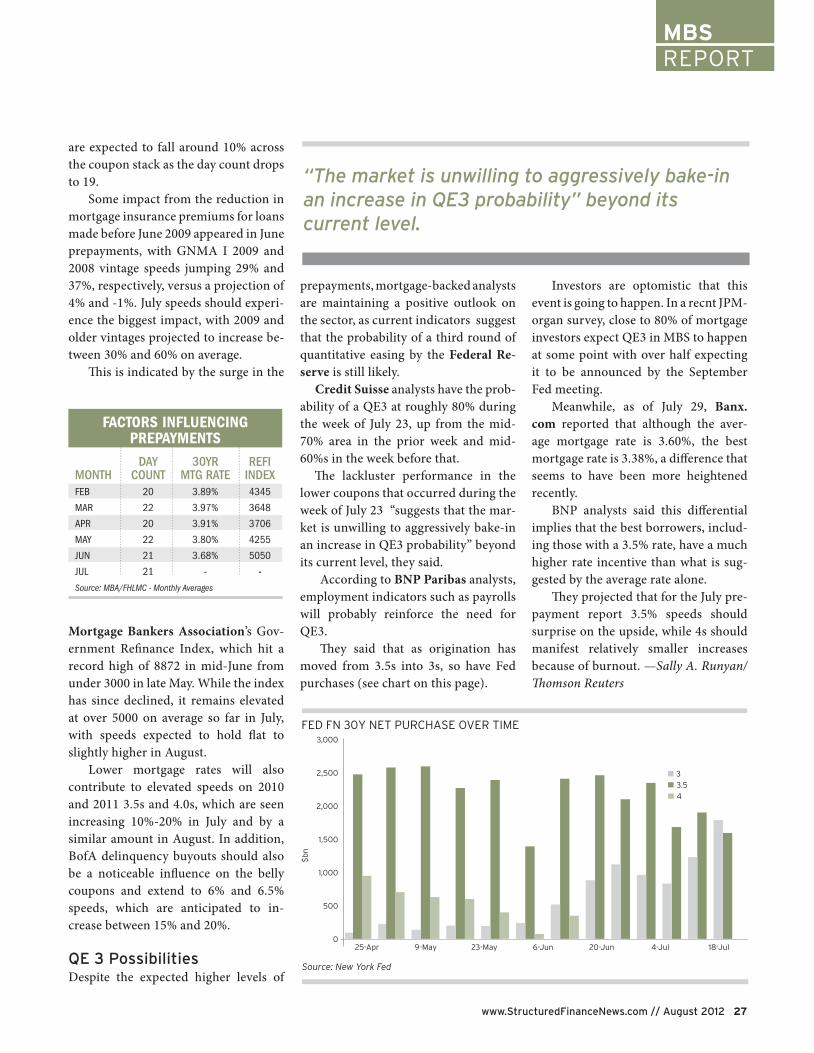

While smaller assets are capturing some attention, much of the structured finance conver-sation still turns on agency securities and where they’re headed.

The American Securitization Forum recently released a white paper that outlines issues behind the proposal to create a single security by merging Fannie and Freddie’s issuance platforms.

Bill Berliner in his column says that the underlying object of creating one security is to lessen the pricing disadvantage that has torpedoed Freddie’s ability to price and securitize loans.

Bill discusses the implication of making these two separate entities issue one type of product and concludes that allowing the GSEs to separately determine their pricing is still the best way.

—Karen Sibayan, Editor

www.StructuredFinanceNews.com // August 2012 �

005_ASRAug12 1 8/2/2012 6:32:40 PM

ABSREPORT

F or years, U.S. banks, and especial-ly the largest ones, have dreaded the seemingly inevitable arrival

of new and more burdensome regula-tory capital requirements. U.S. banking regulators’ proposal to revamp those re-quirements, issued in mid-June, should dispel many of their fears, although the proposal is likely to result in extra work for U.S. banks and may put them at a dis-advantage to global competitors in the ABS market.

Comments on the 700-page proposal, which is split into three parts, are due by Sept. 7. While few industry comments have been filed, early observers are pleasantly surprised by the proposal’s language.

“This is far more rational than ei-ther the initial formula the regulators proposed last year, or the ratings-based approach a while ago,” said Laurie Good-man, head of Amherst Securities Group’s RMBS strategy team.

Under the new formula, capital charges are based on the riskiest of the underlying loans in a securitization, the credit enhancement of the bonds and the portion of the deal the bond takes up rel-ative to other deal tranches. Goodman said many higher-rated bonds in a secu-ritization will face more punitive capital charges, and many lower-rated bonds will face less capital charges.

Focusing on CMBS, Deutsche Bank Se-curities research analysts David Zhou and Harris Trifon noted that risk weightings will be higher for all but the most subordi-nated bonds. In fact, the risk weighting for a ‘BB’-rated CMBS increases to more than 600% under the proposal from the 200% imposed by the Basel I-based rules in use today, the widest risk-weighting difference between the two regulatory regimes (see chart on next page).

As a result, the capital charges for ‘AAA’-rated CMBS originated since 2010 will average $447.43 million under cur-rent rules and $449.23 million under the proposal. As the rating drops, the proposal’s capital charges increase to several times the current Basel I charg-es. The risk weightings for both sets of rules converge for ‘B’-rated bonds at $3,181.15, and for lower-rated bonds the Basel I risk weightings start to exceed those under the proposal.

“Although the magnitude of the risk-weighting increases is severe for many legacy securities, the actual amount of ad-ditional capital that will need to be held is manageable given the size of the market,” the analysts noted in a July 25 report.

The proposal’s lesser capital charges for lower-rated ABS should result in banks shifting their investments to those securities and provide them with a sig-nificant pick up in yield for investing in those bonds, Goodman said.

In an analysis of the proposed rules published June 15, she noted three posi-

tive impacts. For one, they move banks away from relying on a ratings-based ap-proach to determine regulatory risk cap-ital and thus their reliance on the rating agencies, which have been criticized for their role in the recent financial crisis. In addition, the proposed rule would en-able banks to hold “well-enhanced” se-curities with reasonable capital charges, without worrying about rating agency actions. And third, because the proposal imposes risk weightings for bonds rated less than ‘BB’ that are significantly less than the 100% risk weighting under the ratings-based approach, a bank selloff of those securities with large ratings-based capital charges is far less likely.

“I think this proposal removes that fear, which is very, very important,” Goodman said, adding that such a selloff could drive down RMBS prices, even though it may make sense to hold those securities from an economic risk/return standpoint.

Not a Slam DunkNevertheless, there are bound to be chal-

More Rational Framework with New Basel Proposal

lenges, some perhaps significant, that are buried deep in the proposal. For that reason, the and the were quick to request a comment-period extension on June 22.

“These proposals would be the most material changes to U.S. capital standards since 1989 and will have significant immediate and ongoing impact on the nature of financial services in the United States…bankers need sufficient time to evaluate the operational complexities of the proposals and understand their significant impact,” the two trade groups stated in a joint letter.

Some complications have already emerged. principal and leader of & Touche’s rities practice, said there are a “couple of pretty significant implications” from the banking regulators’ proposal. For one, as currently written, it would ramp up banks’ compliance and monitoring obligations for activity in their trading books to levels resembling those in their banking book. That is a potentially difficult requirement given the likelihood of the short-term and more frequent nature of those trades.

1400%

RIS

K W

EIG

HT

CMBS RISK WTHE MOST SUBORDINATE BONDS

SOURCE: DEUTSCHE BANK, TREPP, BLOOMBERG FINANCE LP

� Asset Securitization Report // August 2012

006_ASRAug12 1 8/2/2012 6:33:06 PM

ABSREPORT

tive impacts. For one, they move banks away from relying on a ratings-based ap-proach to determine regulatory risk cap-ital and thus their reliance on the rating agencies, which have been criticized for their role in the recent � nancial crisis. In addition, the proposed rule would en-able banks to hold “well-enhanced” se-curities with reasonable capital charges, without worrying about rating agency actions. And third, because the proposal imposes risk weightings for bonds rated less than ‘BB’ that are signi� cantly less than the 100% risk weighting under the ratings-based approach, a bank sello� of those securities with large ratings-based

“I think this proposal removes that fear, which is very, very important,” Goodman said, adding that such a sello� could drive down RMBS prices, even though it may make sense to hold those securities from an economic risk/return standpoint.

Nevertheless, there are bound to be chal-

lenges, some perhaps signi� cant, that are buried deep in the proposal. For that rea-son, the American Bankers Associationand the Financial Services Roundtablewere quick to request a comment-period extension on June 22.

“� ese proposals would be the most material changes to U.S. capital standards since 1989 and will have signi� cant im-mediate and ongoing impact on the na-ture of � nancial services in the United States…bankers need su� cient time to evaluate the operational complexities of the proposals and understand their signi� cant impact,” the two trade groups stated in a joint letter.

Some complications have already emerged. Alok Sinha,principal and leader of Deloitte & Touche’s banking and secu-rities practice, said there are a “couple of pretty signi� cant implications” from the bank-ing regulators’ proposal. For one, as cur-rently written, it would ramp up banks’ compliance and monitoring obligations for activity in their trading books to levels resembling those in their banking book. � at is a potentially di� cult requirement given the likelihood of the short-term and more frequent nature of those trades.

“Banks typically don’t have the same underlying compliance and monitoring processes on their trading book side, so putting those mechanisms in place would be challenging,” Sinha said.

He added that increasing requirements for the trading book may be an attempt to reduce the regulatory capital arbitrage between holding the same assets in the trad-ing book versus the banking book. However, if the change results in less trading book activity, “there may be low-er liquidity, and it could be

harder to price these transactions.”Sinha explained that the banking

regulators’ proposal is broadly aligned with the approach to Basel III imple-mentation that regulators outside the U.S. are taking, although certain require-ments emanating from Dodd-Frank im-pose some noteworthy and potentially

problematic di� erences. For instance, the Dodd-Frank proposal imposes a 20% risk weighting � oor, a requirement of Dodd-Frank as well as the Basel I rules, even for very highly rated securities that may otherwise warrant lower risk weightings. � e proposal also disallows the use of ratings in determining capital requirements.

Basel III essentially retains the amended Basel II capital rules, com-monly known as Basel 2.5. European regulators have been faster to adopt this version, which does not impose a � oor and allows the use of third-party ratings in capital calculations.

As a result, the largest U.S. banks will have to calculate their capital require-ments based on both the “standardized” and the “advanced” approaches — laid out respectively in the second and third parts of the proposal — to determine minimum regulatory capital require-ments. Dodd-Frank then requires them to take the higher of the two.

“So Basel I e� ectively never goes away for U.S. banks,” Sinha said, adding that running parallel regulatory-capital calculations will impose additional op-erational costs on U.S. banks and poten-tially higher capital costs as well. “If, over time, the actual capital requirements cal-culated using Basel 2.5 drop below the � oor from Basel I or Basel III standard-ized approach, because the portfolio’s risk is coming down, the bank’s capital requirement won’t be able to drop below that � oor. So it could put them at a com-petitive disadvantage.”

As a result of these changes, banks will almost certainly have to restructure

“This is far more rational than either the initial formula the regulators proposed last year, or the ratings-based approach a while ago.”

1400%

1200

1000

800

600

400

200

0

AAA AA A BBB BB B

RIS

K W

EIG

HT

CMBS RISK WEIGHT WILL BE HIGHER FOR ALL BUT THE MOST SUBORDINATE BONDS

Basel I (Current) Basel III

SOURCE: DEUTSCHE BANK, TREPP, BLOOMBERG FINANCE LP

Basel I (Current) Basel III

TkTkTk

LAURIE GOODMAN

www.StructuredFinanceNews.com // August 2012 �

007_ASRAug12 2 8/2/2012 6:33:37 PM

ABSREPORT

their portfolios, and that will impact the prices of different ABS assets. BradHintz, an equity research analyst at San-ford Bernstein, said that as the pricing of assets holding higher regulatory capital weightings changes, the economics of investing in these assets will also change. However, banks will likely hold onto some low-return businesses to service clients who are also active in higher-re-turn businesses.

It is still too early to forecast changes in market participants’ behavior as a re-sult of the proposed rules, Hintz said. “As prices change in the market place and weak competitors drop out of the business, there will almost certainly be a second and third round of adjustments,” he said.

Nevertheless, the initial impact of proposed provisions that are statutorily mandated by Dodd-Frank is fairly clear. On the plus side, while the proposed rules do not necessarily lower capital re-quirements, they’ll make ABS portfolios more manageable than the ratings-based approach because portfolio managers will no longer have to ascertain the per-ceptions of the rating agencies about a security, Amherst Securities noted. In-stead, they will be able to focus more on its future performance.

The 20% floor, however, could be a disadvantage for the largest U.S. banks, since they are competing against finan-cial institutions from outside the U.S. that will use the ratings-based approach and have no such floor. Those competitors may be able to hold less capital against assets with the same risk weightings.

Collins AmendmentAnother potentially problematic provision required by Dodd-Frank is referred to as the “Col-lins Amendment,” named after Senator Susan Collins (R-Me.). The provision requires that capi-tal requirements derived from the advanced approach are not less than the standardized ap-proach — essentially the Basel I require-ments — or quantitatively lower than the requirements in effect for the modified Ba-sel I requirements for insured depository institutions when the bill was enacted.

Consequently, the largest banks must calculate their capital requirements using both the standardized and advanced ap-

proaches to determine which approach requires the greater amount of capital. If the more risk-sensitive advanced approach generates a lower requirement, then the amount of capital required by the standard-ized approach applies. The banks must opt for the capital required by the advanced ap-proach if its tally is higher.

Jason Kravitt, a partner at Mayer Brown, said that to make the comparison between the two approaches, banks must calculate them from the “ground up” to all their assets. The Collins Amendment then requires them to compare the totals for regulatory purposes. However, banks must also choose the appropriate meth-od for day-to-day business decisions, whether it’s pursuing a certain deal or buying a new line of business.

“The dilemma for management is, How do we decide if we’re going to do

a deal … which capital rule do we look at to decide whether it’s too much capital or the right amount’?” Kravitt said.

One argument is that the two approaches should be compared when making a decision in every transaction, and in making the decision the method requiring the most

capital should be chosen, Kravitt said. However, since the advanced approach is more risk-sensitive, it is arguably a more rational way to price products and make other business decisions, since it is a more accurate measure of risk and could result in a more efficient use of capital.

“Each bank will have to weigh the plusses and minuses of the two approach-es,” Kravitt said. It is likely that banks re-quired to use the advanced approach will opt to utilize that method when making business decisions if early indications that the two approaches yield similar amounts prove to be the case. Kravitt explained that the fact that the advanced approach for securitization has the same 20% floor as the standardized approach reinforces the likelihood of this outcome. He added that in any case most banks will keep ex-tra capital as a buffer in the event the ap-proaches do yield different outcomes.

“If the standardized approach comes out a bit higher, it probably won’t be that much higher, and adding some extra cap-ital should take care of it,” Kravitt said.

Higher CostsRunning parallel capital calculations in perpetuity for each of a bank’s lines of business, portfolios or individual assets is bound to result in material operational costs. Although smaller banking institu-tions will use only the standardized ap-proach, the biggest U.S. banks, which hold a majority of banks’ assets in the U.S., are likely to see the cost of calculating regula-tory capital remain at elevated levels.

Having more impact will be increases

in the cost of regulatory capital and the risk-based capital charges assigned to both traditional and non-traditional banking activities. Economic capital has traditionally been the dominant factor for banks when evaluating whether to pursue transactions or make other decisions, such as when to grant loans or what investments to make, said Scott Stengeling and outside counsel for the Securitization Forumand liquidity committee.

“It is clear that while in the past economic capital received more emphasis than regulatory capital in a credit committee’s decision making, looking ahead regulatory capital is going to occupy an equal if not more important position,” Stengel said. “In addition, management

JAson KrAvitt

The factors would appear to be in place. The Dodd-Frank Wall Street Reform and Consumer Protection Act’s Volcker Rule places new restrictions on the big Wall Street banks’ bond inventories that, along with new Basel III capital rules, should increasingly push trading of fixed-income, including ABS, to electronic markets.

the prospect of their arrival has already resulted in major changes among Wall Street’s biggest market makers. Data compiled by the Bank plummeting to approximately $40 billion today from $250 billion in 2008.

ketAxessnoted that dealer balance sheets for fixed income have reduced significantly since the credit crisis in 2008.

ing to electronic trading as an alternative solution for identifying liquidity,” he said. “We’ve added regional dealers and dealers that specialize in structured products trading to help our investor clients source more liquidity.”

CMBS last November and ABS earlier in 2011. Violante

Will New Regs Push ABS to Electronic Platforms?“The dilemma for management is, ‘How do we decide if we’re going to do a deal … which capital rule do we look at to decide whether it’s too much capital or the right amount’?”

� Asset Securitization Report // August 2012

008_ASRAug12 3 8/2/2012 6:34:03 PM

ABSREPORT

a deal … which capital rule do we look at to decide whether it’s too much capital or the right amount’?” Kravitt said.

One argument is that the two approaches should be compared when making a decision in every transaction, and in making the decision the method requiring the most

capital should be chosen, Kravitt said. However, since the advanced approach is more risk-sensitive, it is arguably a more rational way to price products and make other business decisions, since it is a more accurate measure of risk and could result in a more efficient use of capital.

“Each bank will have to weigh the plusses and minuses of the two approach-es,” Kravitt said. It is likely that banks re-quired to use the advanced approach will opt to utilize that method when making business decisions if early indications that the two approaches yield similar amounts prove to be the case. Kravitt explained that the fact that the advanced approach for securitization has the same 20% floor as the standardized approach reinforces the likelihood of this outcome. He added that in any case most banks will keep ex-tra capital as a buffer in the event the ap-proaches do yield different outcomes.

“If the standardized approach comes out a bit higher, it probably won’t be that much higher, and adding some extra cap-ital should take care of it,” Kravitt said.

Running parallel capital calculations in perpetuity for each of a bank’s lines of business, portfolios or individual assets is bound to result in material operational costs. Although smaller banking institu-tions will use only the standardized ap-proach, the biggest U.S. banks, which hold a majority of banks’ assets in the U.S., are likely to see the cost of calculating regula-tory capital remain at elevated levels.

Having more impact will be increases

in the cost of regulatory capital and the risk-based capital charges assigned to both traditional and non-traditional banking ac-tivities. Economic capital has traditionally been the dominant factor for banks when evaluating whether to pursue transactions or make other decisions, such as when to grant loans or what investments to make, said Scott Stengel, a partner at King & Spald-ing and outside counsel for the American Securitization Forum’s regulatory capital and liquidity committee.

“It is clear that while in the past eco-nomic capital received more emphasis than regulatory capital in a credit com-mittee’s decision making, looking ahead regulatory capital is going to occupy an equal if not more important position,” Stengel said. “In addition, management

will be focusing more and more on what revenues a business unit will be able to generate in order to justify the regula-tory cost of capital associated with it.”

According to Amherst Securities, there are other reasons the proposal could cause market participants some heartache, including the fact that it doesn’t account for deal features such as overcollateralization, excess spread or payment priority, all of which could provide capital relief. However, Good-man and her colleagues wrote that they are sympathetic to regulators seeking to incorporate “complex structural issues in a simple formula.”

Amherst also criticized the proposal for not taking into account the purchase price of a security. For example, if the se-

curity is purchased at a discount that effec-tively provides a cushion to absorb losses, that discount “should be counted as a credit enhancement and provide capital relief,” the report said.

A third contention noted by Amherst is the proposal’s harsh capital treatment of re-securitizations, which comprise por-tions of existing securitizations. Simple “re-REMICs” often have cash flows that could have been “created in the context or the original deal” and consequently deserve the same capital treatment, the brokerage firm noted.

“You’re actually improving the credit quality of these securities through re-secu-ritization, and there’s no reason to penal-ize them as much as the proposal does,” Goodman said. — John Hintze

The factors would appear to be in place. The Dodd-FrankWall Street Reform and Consumer Protection Act’s Vol-cker Rule places new restrictions on the big Wall Streetbanks’ bond inventories that, along with new Basel IIIcapital rules, should increasingly push trading of fixed-income, including ABS, to electronic markets.

None of those requirements have been finalized, butthe prospect of their arrival has already resulted in ma-jor changes among Wall Street’s biggest market mak-ers. Data compiled by the New York Federal ReserveBank showed primary dealers’ corporate bond holdingsplummeting to approximately $40 billion today from$250 billion in 2008.

Lou Violante, structured products manager at Mar-ketAxess, an electronic bond-trading platform, hasnoted that dealer balance sheets for fixed income havereduced significantly since the credit crisis in 2008.

“In this challenging environment, investors are turn-ing to electronic trading as an alternative solution foridentifying liquidity,” he said. “We’ve added regionaldealers and dealers that specialize in structured prod-ucts trading to help our investor clients source moreliquidity.”

MarketAxess began trading non-agency RMBS andCMBS last November and ABS earlier in 2011. Violante

said the private firm does not release its own volumenumbers. However, it appears to be well positioned tobenefit from investors’ needs for ways to trade relative-ly illiquid structured fixed-income products that may beless readily available from the big Wall Street firms’ tra-ditional market-making desks.

In fact, some major players in the capital marketshave taken notice. Columbia Management, Fidelity In-vestment Management, Street Global Advisors andmore than a half dozen Wall Street dealers are report-edly in early-stage discussions about creating a newmarketplace for bonds. Whether that platform will tradeABS could not be clarified by press time.

A spokesperson at BlackRock said the big moneymanager intends “to expand into MBS and ABS overtime,” but its current focus is investment grade corpo-rates. In mid-July, BlackRock held a live trading sessionwith members of its Aladdin Trading Network, which isdesigned to let large buy-side investors trade directlywith one another and bypass the Wall Street firms.

BlackRock, with $3.7 trillion under management,has said the network is not intended to replace the WallStreet market makers, although it has been controver-sial on the Street because it could put downward pres-sure on commissions. — John Hintze

Will New Regs Push ABS to Electronic Platforms?

www.StructuredFinanceNews.com // August 2012 �

009_ASRAug12 4 8/2/2012 6:34:24 PM

010_ASRAug12 1 8/2/2012 6:35:04 PM

With the european DataWarehouse, anyone Can see What’s BehinD the region’s aBs.

Will it Be enough to revive the Market?

By Felipe ossa

RevealThe Full

y the end of this year, RMBS issuers keen on obtaining funding from the European Central Bank, as well as those already using these securities as collateral in sale and repurchase agreements, will need to input data on the underlying mortgages into the newly created European DataWarehouse, known pithily as ED.

Deadlines for securitizations backed by other kinds of assets are further down the road, and there is a grace period for all asset classes, but the point is clear: As it now stands, if you want to use ABS you’ve either issued or hold as collateral in ECB funding, be prepared to lodge loan-level information with ED.

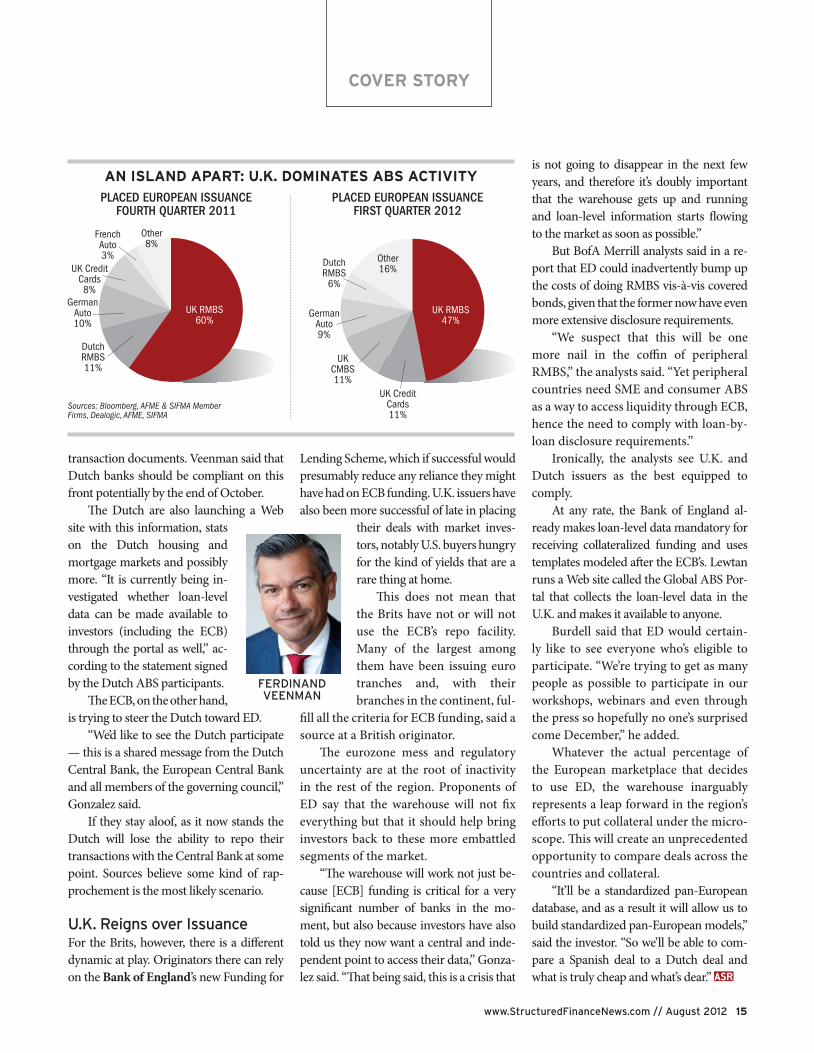

This may not be a big enough incentive to ensure the participation of the entire European securitization market, particularly in ED’s early stages. Dutch originators have expressed reservations about how the project has been organized, and U.K. banks are not as beholden to the ECB for funding as are their peers on the continent.

ED’s champions, though, say that it will bring a major boost in transparency, which should help lure investors back into a Europe that in the days before the crisis provided scant infor-mation about collateral, especially as compared to certain segments of the U.S. securitization market.

The most visible booster is the ECB itself. By dangling the carrot of its repo window in front of issuers and anyone else holding ABS deals, the bank is sending a loud signal to the market-place. But the ECB will also be a customer of the warehouse. Having already taken shiploads of collateral from ABS issuers in Europe, it would naturally like to know itself what’s in there.

“To be fair, organizations like the European Central Bank, as well as most central banks to-day, were not designed to do the things that the market is asking them to do currently,” said Paul Burdell, director of the European DataWarehouse. “However, the European Central Bank saw an absolute need for transparency in ABS, and from this came the loan-level data initiative.”

The loan-level data initiative was essentially the precursor to ED. The process of establishing loan-level data requirements for European securitizations began in 2009 as an effort to correct what many saw as major deficits in market transparency.

“In [European] securitizations until now, most of the data that came was at the aggregate level,” said Usman Ismail, executive vice president at Lewtan Technologies. “And for matters of transparency, to be able to do a true analysis and understand the risk of the transaction, you need data at the loan level.” Beyond combined stats such as weighted average coupon and aver-

BB

www.StructuredFinanceNews.com // August 2012 11

011_ASRAug12 2 8/2/2012 6:35:42 PM

ers have not been disclosed yet, but Burdell said ED expected to make an announcement in this area shortly.

He added that the European DataWarehouse is essentially a utility: “It’s open to anyone; anyone can become a shareholder or a user.”

Its profit margin is based on costs plus 5%–10%. “The profit that it’s making is not only to cover itself but to reinvest in itself so that technology is continually enhanced to keep up with market developments,” Burdell said.

Both those downloading from and those uploading to ED will pay a fee.

“The fee structure or the fees paid by data providers and users of ED still need to be agreed, but the premise is that they will be set by the pricing committee,” Burdell added.

The committee will be made up of originators, investors, rating agencies and other ABS market players and will be overseen by the European Central Bank and several other national central banks.

“Investors will likely pay less than originators, similarly for current shareholders,” Burdell said. “Everyone was invited to be a shareholder, and when we set the pricing on the equity we tried to price it at such a level that incentivized buyers by offering large discounts on services that ED will provide in the future.”

He added that the larger the number of participants, the lower the cost of the fees — a characteristic feature of how a utility is run.

TemplatesThe templates for each asset class were created with the help of the technical working groups. All are available on the ECB’s Web site. The one for RMBS, for instance, contains approximately 157 fields for details on the underlying mortgage

COVER STORY

age maturity, individual loans in a typi-cal pool remained largely a mystery.

These deficiencies came to the atten-tion of the European Central Bank, espe-cially, as Burdell noted, when a closer re-lationship with the sector fed the need for a more meticulous understanding of the collateral underpinning transactions.

“During the crisis in 2007–2008, with the collapse of Lehman and some of the Icelandic banks, we were seeing transpar-ency failings in the European ABS mar-ket,” said Fernando Gonzalez, chairman of the ECB technical working group on

the ABS loan-level initiative and head of the risk strategy section at the ECB.

Soon after, the ECB started to receive large amounts of ABS collateral from banks with few options for funding. “We launched the loan-level initiative to im-prove this situation,” Gonzalez added. “It’s not only a risk management issue for us to even better understand the ABS se-curities we’ve taken as collateral, but it’s a transparency initiative for the market. It should also, quite naturally, give investors that have left the market confidence to re-look at ABS as an investible asset class and in turn help it to reactivate itself.”

As investors in Europe have largely stayed away from ABS, originators con-tinue to retain a sizable portion of their deals. (See graph at right.)

The loan-level initiative involved six technical working groups, each focusing on a different asset class: RMBS, CMBS, SME securitizations, auto loan deals, leasing ABS and transactions backed by consumer finance assets.

Some views of what should be in ED have been shaped by experience with loan-level data in the U.S.

An investor familiar with the European DataWarehouse said U.S. structured finance inves-tors are accustomed to the sort of loan-level data that will be available in ED largely because of non-agency RMBS and the level of detail typically disclosed in that sector. The information flow there did not come from an ED-style warehouse with participation from a variety of market participants, but rather was harvested, standardized and supplied by data providers CoreLogic and

Lender Processing Services, according to market sources.

ED is the culmi-nation of a more di-rected approach.

“To better achieve the objectives, what the Eurosystem thought was that you bring confidence to the market by having a single platform for the market, so that all the information of the Europe-an ABS market is contained in one place with the same standards for everyone,” said Gonzalez. “We didn’t want to have a balkanization of the ABS market.”

Also, the ECB itself want-ed to have a single counter-party for such a platform, he added.

Nuts & BoltsED is open to the 27 countries that make up the European Union in addition to non-EU countries that are part of the

European Economic Area, namely Iceland, Liechtenstein and Norway. This goes well beyond the 17 EU states that share the euro as their currency.

The warehouse had its first issuance of shares earlier this summer, with 15 in-vestors buying in, consisting “largely of global banks and institutions,” according to a press release distributed July 9. The statement added that “proceeds from the placement will be used to finalize the build-out of ED as well as to provide the business with ongoing working capital.” Sapient Global Markets is building the software, while NTT Europe will provide the hardware and backup service for ED. Morrison & Foerster and Noerr have both been legal advisors to the project.

The names of the present sharehold-

Paul Burdell

We didn’t want to have a balkanization of the ABS market.

TOugh SEll: EuROpEan STRuCTuREd FinanCE iSSuanCE

180.0

160.0

140.0

120.0

80.0

60.0

40.0

20.0

0.0

2009:Q1

2009:Q2

2009:Q3

2009:Q4

2010:Q1

2010:Q2

2010:Q3

2010:Q4

2011:Q1

2011:Q2

2011:Q3

2011:Q4

2012:Q1

Sources: Bloomberg, AFME & SIFMA Member Firms, Dealogic, AFME, SIFMA

PlacedRetained

12 Asset Securitization Report // August 2012

012_ASRAug12 3 8/2/2012 6:36:08 PM

ers have not been disclosed yet, but Bur-dell said ED expected to make an an-nouncement in this area shortly.

He added that the European Data-Warehouse is essentially a utility: “It’s open to anyone; anyone can become a sharehold-er or a user.”

Its profit margin is based on costs plus 5%–10%. “The profit that it’s mak-ing is not only to cover itself but to re-invest in itself so that technol-ogy is continually enhanced to keep up with market develop-ments,” Burdell said.

Both those downloading from and those uploading to ED will pay a fee.

“The fee structure or the fees paid by data providers and users of ED still need to be agreed, but the premise is that they will be set by the pricing com-mittee,” Burdell added.

The committee will be made up of orig-inators, investors, rating agencies and other ABS market players and will be overseen by the European Central Bank and several other national central banks.

“Investors will likely pay less than origi-nators, similarly for current shareholders,” Burdell said. “Everyone was invited to be a shareholder, and when we set the pricing on the equity we tried to price it at such a level that incentivized buyers by offering large discounts on services that ED will provide in the future.”

He added that the larger the number of participants, the lower the cost of the fees — a characteristic feature of how a utility is run.

TemplatesThe templates for each asset class were created with the help of the technical working groups. All are available on the ECB’s Web site. The one for RMBS, for in-stance, contains approximately 157 fields for details on the underlying mortgage

loans. But not all fields are mandatory. Many fields are applicable only to

specific jurisdictions. For instance, the last field in the RMBS template reflects an idiosyncrasy of Spanish RMBS — asking whether a borrower is contencioso. This denotes a status in which legal proceed-ings have begun against the homeowner, typically when the borrower is in arrears for more than a few months.

“Originators have had a year participating in the de-velopment of the RMBS loan-level template and some more time for providing input to the consumer loan and auto loan TWGs,” said Steve Gandy,head of securitization at Ban-co Santander and a member of the RMBS, auto loan and consumer finance working

groups. “In that process, the ECB has given plenty of time to the market to un-derstand the template requirements and figure out if there were any gaps in the system. We did a gap analysis ourselves among our various units to determine if there were any information elements that were missing.”

Gandy declined to say whether Santander was a shareholder in ED.

Calendar The deadlines for deals to remain eligible to be used as collateral in ECB repos vary by asset class: for RMBS, loan-level data must be provided by December 1, 2012; for ABS backed by loans to small and medium enterprises and for commercial mortgage-backed securities, it is Janu-ary 1, 2013; and for consumer finance ABS, leasing ABS and auto loan ABS, the deadline is January 1, 2014.

There is a nine-month phasing-in pe-riod from the dates above. Where loan-level data are incomplete on that date, they must gradually be completed in the course of that transition period.

If a deal isn’t fully compliant but re-mains in the system, there is a way for investors to immediately gauge whether all the required data is in there and sub-mitted on time.

Burdell said there will be a scoring system that will reflect whether the orig-inator or other data provider on a trans-action submitted comprehensive infor-mation, with the right kind of data in its corresponding field in accordance with the ECB eligibility criteria. The higher the score, the more complete the infor-mation. “This will be a quality assurance score,” he added. “It will let investors know that a quality assurance process has been applied to the data.”

As it currently stands, scores are combinations of A–D and 1–4, with A1 denoting full compliance and D4 slapped on a deal where a good number of the fields are noncompliant for any num-ber of reasons, according to the ECB Web site. For pur-poses of the scor-ing system, the nine month grace period for completing the template is divvied into three phases of three months each.

Gonzalez said that the score will not determine the haircut that the ECB applies to a deal for collateralized funding, but he added that the Eurosystem reserves the right to change or modify its haircut schedule when it deems that doing so is necessary.

Mixed Get NixedBarred from ED — and by extension the repo window — is any transaction backed by pools of different kinds of as-sets. Heterogeneous ABS will remain eli-gible until March 31, 2014.

In an early July report, Bank of America Merrill Lynch said this pol-

COVER STORY

FerNaNdoGoNzalez

Also, the ECB itself want-ed to have a single counter-party for such a platform, he

ED is open to the 27 countries that make up the European Union in addition to non-EU countries that are part of the

European Economic Area, namely Iceland, Liechtenstein and Norway. This goes well beyond the 17 EU states that share the euro

The warehouse had its first issuance of shares earlier this summer, with 15 in-vestors buying in, consisting “largely of global banks and institutions,” according to a press release distributed July 9. The statement added that “proceeds from the placement will be used to finalize the build-out of ED as well as to provide the business with ongoing working capital.”

is building the will provide

the hardware and backup service for ED. Noerr have

both been legal advisors to the project. The names of the present sharehold-

STeve GaNdy

2012:Q1

www.StructuredFinanceNews.com // August 2012 13

013_ASRAug12 4 8/2/2012 6:36:38 PM

icy shift will weigh on the Italian market, where mixed collateral is more common, particularly in lease ABS. “The use-by date of these deals from the Eurosystem collat-eral point of view is limited by the end of March 2014,” said BofA Merrill analysts.

For deals that are eligible and entered into the warehouse, the data will still not be clean enough for immediate use by some investors, sources said.

“If investors don’t use it directly, they’ll use it indirectly,” an investor familiar with the European DataWarehouse said. “You can imagine cottage industries developing around this — people offering services to analyze the data, process it, clean it up.”

Ismail said that Lewtan — which was part of a group of companies that had lost the bid to Sapient to build the ware-house’s software — is prepared to collect, scrub and normalize the data from the

warehouse and put it into a format that people can use.

“If there’s any experience we’ve learned over the years it’s that people will conform to a particular template, but it still won’t be normalized against issuers and services,” Ismail said. “Someone has got to take the trouble to normalize it; otherwise it will be useless.”

Burdell said that ED will “check the validity of data to make sure everything is in the right order according to the ECB templates, but it’s not an auditor.”

Basically, it is a matter of ensuring that the right information goes in the proper field.

“ED is not designed to do anything intelligent with the data,” he added. “[But] as part of maintaining excep-tional service, ED will have an external

firm come in regularly to re-view and report on its opera-tions, methods and processes against agreed and contracted minimum service levels.”

The warehouse’s impact has been assured by the ECB’s active involvement, sources said. The bank will, after all, be one of its largest customers, given all the ABS it has already taken on as collateral for funding eurozone banks.

“Having a data warehouse like this, and the ECB using its position as one of its largest users, I think will have a very positive effect on the market in terms of standardizing loan-level requests, get-ting originators who might have been reluctant to provide this detail or to do the necessary investments to provide it,” said Santander’s Gandy.

The eurozone’s monetary authority, however, will not own a piece of ED.

“The ECB itself will not be a share-holder, but it will be an active observer [as well as] a client. Our position is one of support and a catalyzer of change so as to equip the ABS market with the nec-essary tools to develop and reactivate it-self,” Gonzalez said.

Mitigating ImpactBut the project may not have the impact it could have, given that, for now, a significant portion of the market is being kept alive by lenders in the Netherlands and the U.K. (See pie chart on the next page.) The for-mer group is reticent to participate, while the latter is not as dependent on ECB fund-ing as eurozone banks and therefore may not feel as compelled to participate.

For instance, there have been reports that Dutch banks/issuers are staying out of the warehouse because of how ED was set up and the charg-ing of fees. The truth is more nuanced, though this area of the market — and not a negli-gible one in the past year or so — is not exactly embracing the

warehouse either.“Dutch issuers at this point in time

don’t want to participate in funding the warehouse, but they haven’t said that they wouldn’t upload their data to the ware-house,” said Ferdinand Veenman, a partner at the corporate finance group at KPMGand advisor to the soon-to-be-launched Dutch Securitisation Association.

In a joint statement on the matter, 10 Dutch issuers of ABS — among them ABN AMRO, ING and Rabobank — as well as the Holland Financial Centresaid they sent a letter to the ECB con-veying that they “fully subscribe to the objectives of the European Central Bank of restoring confidence and facilitating investment in the structured finance markets across Europe and that they agree that requiring loan-level data be-ing made available to investors will con-tribute to meeting these objectives.”

But, at the same time, the signatories were still discussing their participation in the warehouse with the ECB. “The Dutch issuers have raised their concerns regarding the information that was pro-vided in respect of the funding, func-tioning and objectives of the European DataWarehouse,” they said.

Veenman said that Dutch origina-tors — which are overwhelmingly RMBS issuers — have come together to come up with a single standard for mortgage-backeds. The goal is to have investor re-ports issued on a monthly basis for RMBS and to have the same table of contents and main definitions in the prospectuses and

transaction documents. Veenman said that Dutch banks should be compliant on this front potentially by the end of October.

The Dutch are also launching a Web site with this information, stats on the Dutch housing and mortgage markets and possibly more. “It is currently being investigated whether loan-level data can be made available to investors (including the ECB) through the portal as well,” according to the statement signed by the Dutch ABS participants.

The ECB, on the other hand, is trying to steer the Dutch toward ED.

“We’d like to see the Dutch participate — this is a shared message from the Dutch Central Bank, the European Central Bank and all members of the governing council,” Gonzalez said.

If they stay aloof, as it now stands the Dutch will lose the ability to repo their transactions with the Central Bank at some point. Sources believe some kind of rapprochement is the most likely scenario.

U.K. Reigns over IssuanceFor the Brits, however, there is a different dynamic at play. Originators there can rely on the Bank of England

COVER STORY

UsMan IsMaIl

Dutch issuers at this point in time don’t want to participate in funding the warehouse, but they haven’t said that they wouldn’t upload their data.

Sources: Bloomberg, AFME & SIFMA Member Firms, Dealogic, AFME, SIFMA

DutchRMBS11%

German Auto10%

UK Credit Cards8%

FrenchAuto

Placed

14 Asset Securitization Report // August 2012

014_ASRAug12 5 8/2/2012 6:37:08 PM

For instance, there have been reports that Dutch banks/issuers are staying out of the warehouse because of how ED was set up and the charg-ing of fees. The truth is more nuanced, though this area of the market — and not a negli-gible one in the past year or so — is not exactly embracing the

“Dutch issuers at this point in time don’t want to participate in funding the warehouse, but they haven’t said that they wouldn’t upload their data to the ware-

Ferdinand Veenman, a partner at the corporate finance group at KPMGand advisor to the soon-to-be-launched Dutch Securitisation Association.

In a joint statement on the matter, 10 Dutch issuers of ABS — among them

Rabobank — as Holland Financial Centre

said they sent a letter to the ECB con-veying that they “fully subscribe to the objectives of the European Central Bank of restoring confidence and facilitating investment in the structured finance markets across Europe and that they agree that requiring loan-level data be-ing made available to investors will con-tribute to meeting these objectives.”

But, at the same time, the signatories were still discussing their participation in the warehouse with the ECB. “The Dutch issuers have raised their concerns regarding the information that was pro-vided in respect of the funding, func-tioning and objectives of the European

Veenman said that Dutch origina-tors — which are overwhelmingly RMBS issuers — have come together to come up with a single standard for mortgage-backeds. The goal is to have investor re-ports issued on a monthly basis for RMBS and to have the same table of contents and main definitions in the prospectuses and

transaction documents. Veenman said that Dutch banks should be compliant on this front potentially by the end of October.

The Dutch are also launching a Web site with this information, stats on the Dutch housing and mortgage markets and possibly more. “It is currently being in-vestigated whether loan-level data can be made available to investors (including the ECB) through the portal as well,” ac-cording to the statement signed by the Dutch ABS participants.

The ECB, on the other hand, is trying to steer the Dutch toward ED.

“We’d like to see the Dutch participate — this is a shared message from the Dutch Central Bank, the European Central Bank and all members of the governing council,” Gonzalez said.

If they stay aloof, as it now stands the Dutch will lose the ability to repo their transactions with the Central Bank at some point. Sources believe some kind of rap-prochement is the most likely scenario.

U.K. Reigns over IssuanceFor the Brits, however, there is a different dynamic at play. Originators there can rely on the Bank of England’s new Funding for

Lending Scheme, which if successful would presumably reduce any reliance they might have had on ECB funding. U.K. issuers have also been more successful of late in placing

their deals with market inves-tors, notably U.S. buyers hungry for the kind of yields that are a rare thing at home.

This does not mean that the Brits have not or will not use the ECB’s repo facility. Many of the largest among them have been issuing euro tranches and, with their branches in the continent, ful-

fill all the criteria for ECB funding, said a source at a British originator.

The eurozone mess and regulatory uncertainty are at the root of inactivity in the rest of the region. Proponents of ED say that the warehouse will not fix everything but that it should help bring investors back to these more embattled segments of the market.

“The warehouse will work not just be-cause [ECB] funding is critical for a very significant number of banks in the mo-ment, but also because investors have also told us they now want a central and inde-pendent point to access their data,” Gonza-lez said. “That being said, this is a crisis that

is not going to disappear in the next few years, and therefore it’s doubly important that the warehouse gets up and running and loan-level information starts flowing to the market as soon as possible.”

But BofA Merrill analysts said in a re-port that ED could inadvertently bump up the costs of doing RMBS vis-à-vis covered bonds, given that the former now have even more extensive disclosure requirements.

“We suspect that this will be one more nail in the coffin of peripheral RMBS,” the analysts said. “Yet peripheral countries need SME and consumer ABS as a way to access liquidity through ECB, hence the need to comply with loan-by-loan disclosure requirements.”

Ironically, the analysts see U.K. and Dutch issuers as the best equipped to comply.

At any rate, the Bank of England al-ready makes loan-level data mandatory for receiving collateralized funding and uses templates modeled after the ECB’s. Lewtan runs a Web site called the Global ABS Por-tal that collects the loan-level data in the U.K. and makes it available to anyone.

Burdell said that ED would certain-ly like to see everyone who’s eligible to participate. “We’re trying to get as many people as possible to participate in our workshops, webinars and even through the press so hopefully no one’s surprised come December,” he added.

Whatever the actual percentage of the European marketplace that decides to use ED, the warehouse inarguably represents a leap forward in the region’s efforts to put collateral under the micro-scope. This will create an unprecedented opportunity to compare deals across the countries and collateral.

“It’ll be a standardized pan-European database, and as a result it will allow us to build standardized pan-European models,” said the investor. “So we’ll be able to com-pare a Spanish deal to a Dutch deal and what is truly cheap and what’s dear.” ASR

COVER STORY

FeRdInandVeenman

An ISlAnd ApART: U.K. dOmInATES ABS ACTIVITY

UK RMBS47%

UK Credit Cards11%

UKCMBS11%

German Auto9%

DutchRMBS

6%

Other16%

Sources: Bloomberg, AFME & SIFMA Member Firms, Dealogic, AFME, SIFMA

UK RMBS60%

DutchRMBS11%

German Auto10%

UK Credit Cards8%

FrenchAuto3%

Other8%

Placed euroPean IssuanceFourth Quarter 2011

Placed euroPean IssuanceFIrst Quarter 2012

www.StructuredFinanceNews.com // August 2012 15

015_ASRAug12 6 8/2/2012 6:37:39 PM

ABSREPORT

C ommercial banks, still busy with the business of tidying up their portfolios and shrinking balance

sheets, are slowly getting back to small business lending. However, the void cre-ated by their long absence has been in-creasingly filled by both smaller regional banks and nonbank lenders. It’s the latter that are driving securitization because it increases their access to funding, allow-ing them to grow lending volumes.

“Banks are significantly more com-fortable with their willingness to lend to us if they believe there is a permanent takeout,” said Barry Sloane, chairman, president and chief executive of Newtek Business Services, a nonbank financial firm that lends to small businesses. “For example, if there is securitization for the loans that can be funded with equity in our warehouse lines of credit, banks are more generous.”

A monthly analysis of 1,000 loan applications by small businesses on Bi-z2Credit.com found that approvals by banks with at least $10 billion of assets totaled 11.1%, up from 10.6% in May 2012. June’s approval rate was also up significantly from 8.9% in June 2011.

The index showed that the alternate lending approval rate such as that from nonbank financials was at 62.9%, posting a small decrease from a peak of 63.2% in May 2012.

Newtek is one of two issuers in the past nine months that completed a secu-ritization of small-business loans. Both-deals securitized the unguaranteed por-tion of the U.S. SBA’s 7(a) loans.

The SBA does not lend money di-

rectly to small-business owners. In-stead, a small-business borrower applies for an SBA-backed loan at a local bank, credit union, Certified Development Co. (CDC) or other specialized lender. The lender then provides the actual loan to the borrower.

Under its 7(a) program, the SBA guarantees a portion of the loan rang-ing from 50%-85%, depending on the program, limiting the lender’s risk and exposure. This helps lenders become comfortable making loans that they might otherwise not approve. The pro-gram offers government guarantees of up to $5 million on loans made by com-mercial lenders to borrowers that face challenges obtaining financing.

The DealsNewtek completed the securitization and sale of $20.5 million of the unguar-anteed portion of the 7(a) program loans in January.

The deal added on to the $23 million deal Newtek closed in December 2010 to the securitization of $23 million in SBA loans that closed in December 2010.

That deal was followed by another completed in June 2012 by a newcomer to the space: Hana Financial, a nonbank direct lender that in addition to SBA loans, specializes in factoring, inventory financing, trade finance, equipment leas-ing, home mortgages and commercial real estate loans. Hana securitizated and sold $26.6 million of the non-guaranteed

The Return of Small Business Loan Securitization After a long hiatus, three securitizations of the non-guaranteed portion of Small Business Administration (SBA) 7a loans executed over the last nine months mark a return of the sector.

portions of SBA small-business loans. Guggenheim Securities

both deals.John Wade

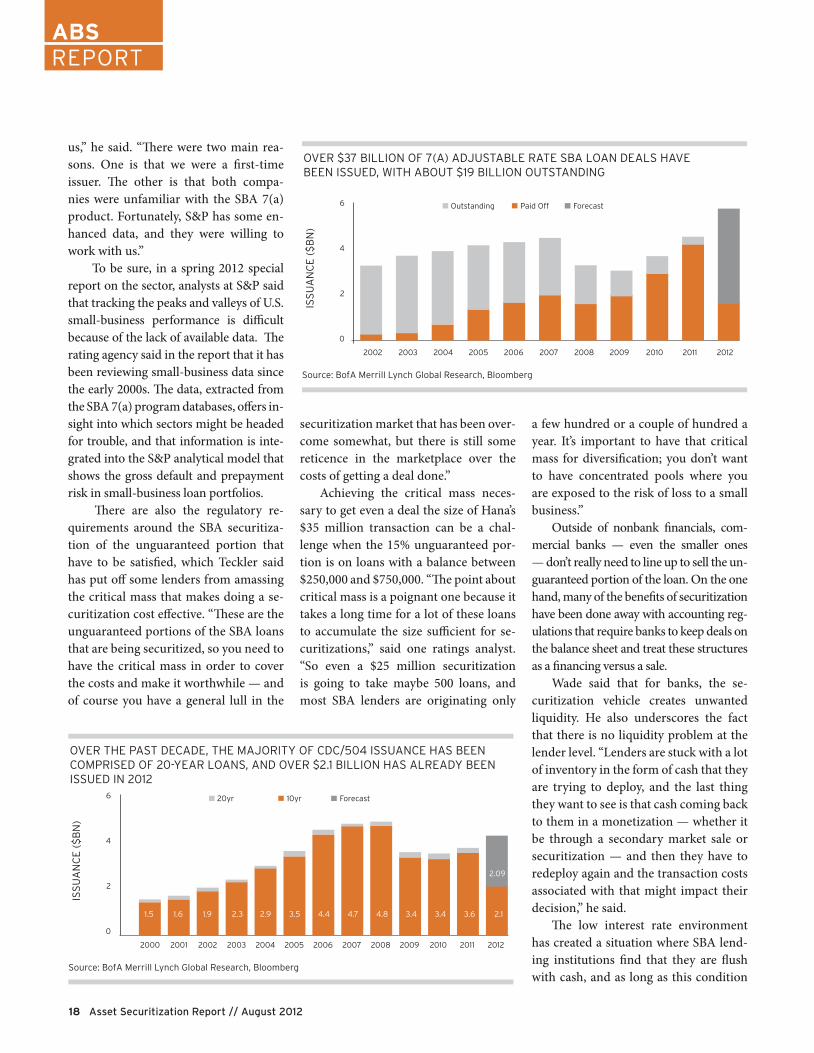

Analyst with the Office of Capital Access at the SBA, said that roughly $10.3 billion of loans have been approved in the SBA flagship 7(a) loan guarantee program in the last nine months. Additionally, lending volumes for the fiscal year 2012 in 7(a) are on track to come in somewhere around the ball park of $14 billion, he said.

“Our program is such that as you approach the end of the fiscal year everyone seems to throw everything, including the kitchen sink, in for approval,” he said.

Of that volume, Wade said that the SBA has seen sales in the secondary market of the guarantee piece tracking at about $2 billion to $2.2 billion, which means that roughly a fifth and up to a quarter of the loans that are approved and disbursed have made their way into the secondary market where the guaranteed piece is sold.

“The guaranteed portions of SBA 7(a) loans are being sold in the secondary market and that market is very buoyant and the premiums are running very high,” said vides counsel for in the SBA programs and other federal agencies that provide capital to small businesses. “The nonbanks and banks are availing themselves of the secondary market for the guaranteed portion and doing well with it.”

The trend for the unguaranteed portion has been toward these smaller-sized deals. Hana’s deal securitized 247 loans while the Newtek deal securitized 400 loans. Still, Wade believes that these deals are still considered good-sized securitizations.

Since nonbanks don’t have a source of deposits, they also look at securitiza

16 Asset Securitization Report // August 2012

016_ASRAug12 1 8/2/2012 6:38:14 PM

ABSREPORT

Newtek completed the securitization and sale of $20.5 million of the unguar-anteed portion of the 7(a) program loans

The deal added on to the $23 million deal Newtek closed in December 2010 to the securitization of $23 million in SBA loans that closed in December 2010.

That deal was followed by another completed in June 2012 by a newcomer

, a nonbank direct lender that in addition to SBA loans, specializes in factoring, inventory financing, trade finance, equipment leas-ing, home mortgages and commercial real estate loans. Hana securitizated and sold $26.6 million of the non-guaranteed

Business portions of SBA small-business loans. Guggenheim Securities managed

both deals.John Wade, a Financial

Analyst with the Office of Capital Access at the SBA, said that roughly $10.3 billion of loans have been approved in the SBA flagship 7(a) loan guarantee program in the last nine months. Additionally, lending volumes for the fiscal year 2012 in 7(a) are on track to come in somewhere around the ball park of $14 billion, he said.

“Our program is such that as you ap-proach the end of the fiscal year everyone seems to throw everything, including the kitchen sink, in for approval,” he said.

Of that volume, Wade said that the SBA has seen sales in the secondary market of the guarantee piece tracking at about $2 billion to $2.2 billion, which means that roughly a fifth and up to a quarter of the loans that are approved and disbursed have made their way into the secondary market where the guaran-teed piece is sold.

“The guaranteed portions of SBA 7(a) loans are being sold in the second-ary market and that market is very buoy-ant and the premiums are running very high,” said Martin Teckler, who pro-vides counsel for Bingham McCutchen in the SBA programs and other federal agencies that provide capital to small businesses. “The nonbanks and banks are availing themselves of the secondary market for the guaranteed portion and doing well with it.”

The trend for the unguaranteed portion has been toward these smaller-sized deals. Hana’s deal securitized 247 loans while the Newtek deal securitized 400 loans. Still, Wade believes that these deals are still considered good-sized se-curitizations.

Since nonbanks don’t have a source of deposits, they also look at securitiza-

tion of the unguaranteed portions as an opportunity to finance themselves more readily. “The use of securitization as a

takeout for these businesses isn’t new, but the market for securitization by the partici-pants in the SBA 7(a) pro-gram was kind of dormant until the recent transactions took place,” Teckler said.

The last deal to takeout a sizeable portion of unguar-anteed SBA 7(a) loans was a $304 million deal that CIT

completed in 2007. Today, however, none of the lender participants in the SBA loan program have expressed an interest in doing a securitization deal of that magnitude, Wade said.

These bigger commercial banks have historically been a cata-lyst for the larger -scale deals, and they don’t get excited un-less the volumes are significant. The biggest impediment to do-ing future securitizations from a financial institution perspec-tive is that there is no more sale treatment at this point and that it is just financing, Sloane said. That situation takes most of the depositories out of the market to do se-curitization, and they were the biggest participants.

“It’s not that they aren’t going to make loans; it’s that they aren’t looking to securitize them and instead will opt to put them on their portfolio,” Sloane said. “For entities like us that are nonbank lenders, securitization is the be all and end all. It puts us on an even playing field with the depository institutions if we are able to secure the long-term financing.”

Sloane anticipates that securitization will help Newtek grow its originations to $125 million of financings this year from $100 million in 2011. “We antici-pate $200 million worth of loans to small businesses in 2013, and we anticipate in-

creasing our line of credit, and securiti-zation is part of that,” he said.

James Kim, senior vicepresident of small-business lending at Hana Finan-cial, said that securitization is a tool that the company plans to increasingly use.

He explained that for each SBA 7(a) loan made, Hana must pay 25% of that loan on its books. “Our annual volume growth equates to about $100 million, and for every $100 million, we must hold $25 million of the volume we generate on our books — our capital gets tied up onto the 25% portion that is unguaran-teed,” he said. “With securitization we are able to securitize this 25% of the un-guaranteed portion and thereby receive the necessary liquidity to make addi-tional loans.”

Hana worked on its June deal for nearly a year, and Kim said that much of the holdup on the deal was getting it rated. The company eventually received an ‘A’ rating from Standard & Poor’s but prior to S&P the company first en-gaged DBRS and then with Moody’s Investors Service,which were not able to rate the deal because of insuffi-

cient data on the sector. DBRS, for instance, has rated deals

with a component of small-business leases and factoring transactions, but the rating agency said that analyzing the SBA strips required data and a better un-derstanding of how the product works to develop the criteria to help define the credit levels required.

These companies are also relatively small, which means that the operational risks in a securitization will be perceived to be higher; therefore, either some ad-ditional mitigation will be necessary or the rating agency may just not be able to get to the rating level they sought.

“The unfortunate situation was that initially they didn’t want to work with

MarTin Teckler

Barry Sloane

www.StructuredFinanceNews.com // August 2012 17

017_ASRAug12 2 8/2/2012 6:38:45 PM

ABSREPORT

us,” he said. “There were two main rea-sons. One is that we were a first-time issuer. The other is that both compa-nies were unfamiliar with the SBA 7(a) product. Fortunately, S&P has some en-hanced data, and they were willing to work with us.”

To be sure, in a spring 2012 special report on the sector, analysts at S&P said that tracking the peaks and valleys of U.S. small-business performance is difficult because of the lack of available data. The rating agency said in the report that it has been reviewing small-business data since the early 2000s. The data, extracted from the SBA 7(a) program databases, offers in-sight into which sectors might be headed for trouble, and that information is inte-grated into the S&P analytical model that shows the gross default and prepayment risk in small-business loan portfolios.

There are also the regulatory re-quirements around the SBA securitiza-tion of the unguaranteed portion that have to be satisfied, which Teckler said has put off some lenders from amassing the critical mass that makes doing a se-curitization cost effective. “These are the unguaranteed portions of the SBA loans that are being securitized, so you need to have the critical mass in order to cover the costs and make it worthwhile — and of course you have a general lull in the

securitization market that has been over-come somewhat, but there is still some reticence in the marketplace over the costs of getting a deal done.”

Achieving the critical mass neces-sary to get even a deal the size of Hana’s $35 million transaction can be a chal-lenge when the 15% unguaranteed por-tion is on loans with a balance between $250,000 and $750,000. “The point about critical mass is a poignant one because it takes a long time for a lot of these loans to accumulate the size sufficient for se-curitizations,” said one ratings analyst. “So even a $25 million securitization is going to take maybe 500 loans, and most SBA lenders are originating only

a few hundred or a couple of hundred a year. It’s important to have that critical mass for diversification; you don’t want to have concentrated pools where you are exposed to the risk of loss to a small business.”

Outside of nonbank financials, com-mercial banks — even the smaller ones — don’t really need to line up to sell the un-guaranteed portion of the loan. On the one hand, many of the benefits of securitization have been done away with accounting reg-ulations that require banks to keep deals on the balance sheet and treat these structures as a financing versus a sale.

Wade said that for banks, the se-curitization vehicle creates unwanted liquidity. He also underscores the fact that there is no liquidity problem at the lender level. “Lenders are stuck with a lot of inventory in the form of cash that they are trying to deploy, and the last thing they want to see is that cash coming back to them in a monetization — whether it be through a secondary market sale or securitization — and then they have to redeploy again and the transaction costs associated with that might impact their decision,” he said.

The low interest rate environment has created a situation where SBA lend-ing institutions find that they are flush with cash, and as long as this condition

remains this way they will look to deploy capital with the understanding that they really don’t want it back right away, Wade said. “Securitization exists to increase the velocity of money back into the lending channel,” he said. “I think people will start doing this [more] as we see a rise in level of interest rate, but it isn’t coming any time soon.”

504 LoansAnother potential catalyst for securitization from the SBA’s small-business lending programs, is the temporary 504 Refinancing Program, which was established to allow small-business owners to refinance up to 90% of the appraised value of available collateral.

The temporary program, established in October 2011 as a Small Business Jobs Act and American Recovery Reinvestment Act initiative, is authorized to provide $7.5 billion. It will be available until Sept. 27. Borrowers can finance up to 90% of the appraised value of available collateral, which could include fixed

Issu

an

cE

($b

n)

OvER $37 bIllIOn Of 7(a) adjusTablE RaTE sba lOan dEals havEbEEn IssuEd, wITh abOuT $19 bIllIOn OuTsTandIng

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Outstanding Paid Off forecast

source: bofa Merrill lynch global Research, bloomberg

6

4

2

0

Issu

an

cE

($b

n)

OvER ThE PasT dEcadE, ThE MajORITy Of cdc/504 IssuancE has bEEncOMPRIsEd Of 20-yEaR lOans, and OvER $2.1 bIllIOn has alREady bEEnIssuEd In 2012

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

20yr 10yr forecast

source: bofa Merrill lynch global Research, bloomberg

6

4

2

0

1.5 1.6 1.9 2.3 2.9 3.5 4.4 4.7 4.8 3.4 3.4 3.6 2.1

2.09

fInancdEfaul

source:

1,800

1,600

1,400

1,200

1,000

800

600

400

200

0

18 Asset Securitization Report // August 2012

018_ASRAug12 3 8/2/2012 6:39:23 PM

ABSREPORT

a few hundred or a couple of hundred a year. It’s important to have that critical mass for diversi� cation; you don’t want to have concentrated pools where you are exposed to the risk of loss to a small

Outside of nonbank � nancials, com-mercial banks — even the smaller ones — don’t really need to line up to sell the un-guaranteed portion of the loan. On the one hand, many of the bene� ts of securitization have been done away with accounting reg-ulations that require banks to keep deals on the balance sheet and treat these structures

Wade said that for banks, the se-curitization vehicle creates unwanted liquidity. He also underscores the fact that there is no liquidity problem at the lender level. “Lenders are stuck with a lot of inventory in the form of cash that they are trying to deploy, and the last thing they want to see is that cash coming back to them in a monetization — whether it be through a secondary market sale or securitization — and then they have to redeploy again and the transaction costs associated with that might impact their

� e low interest rate environment has created a situation where SBA lend-ing institutions � nd that they are � ush with cash, and as long as this condition

remains this way they will look to deploy capital with the understanding that they really don’t want it back right away, Wade said. “Securitization exists to increase the velocity of money back into the lend-ing channel,” he said. “I think people will start doing this [more] as we see a rise in level of interest rate, but it isn’t coming any time soon.”

504 LoansAnother potential catalyst for securi-tization from the SBA’s small-business lending programs, is the temporary 504 Re� nancing Program, which was estab-lished to allow small-business owners to re� nance up to 90% of the appraised value of available collateral.

� e temporary program, established in October 2011 as a Small Business Jobs Act and American Recovery Rein-vestment Act initiative, is authorized to provide $7.5 billion. It will be available until Sept. 27. Borrowers can � nance up to 90% of the appraised value of avail-able collateral, which could include � xed

assets acceptable to SBA (for example: commercial or residential real property). � is allows borrowers with more than 10% equity to be able to obtain addition-al proceeds to pay for eligible business expenses.

In April, SBA expanded the program parameters by allowing any business with a commercial mortgage that is two or more years old to re� nance its debt, regardless of maturity. � e program was put together to create liquidity in the � rst mortgage loans that are tied to SBA’s long-term 504 loan program.

� ere is much interest in averting a situation where the September dead-line for the program’s authorization is