asset securitization. introduction the purpose of this lecture is to introduce - the asset-backed...

TRANSCRIPT

ASSET SECURITIZATION

Introduction

The purpose of this lecture is to introduce

- the asset-backed securities market;

- the evolution of asset securitization;

- asset-backed securities deal structures;

- the role of players;

- briefly presents pricing models; and

- real estate securitization

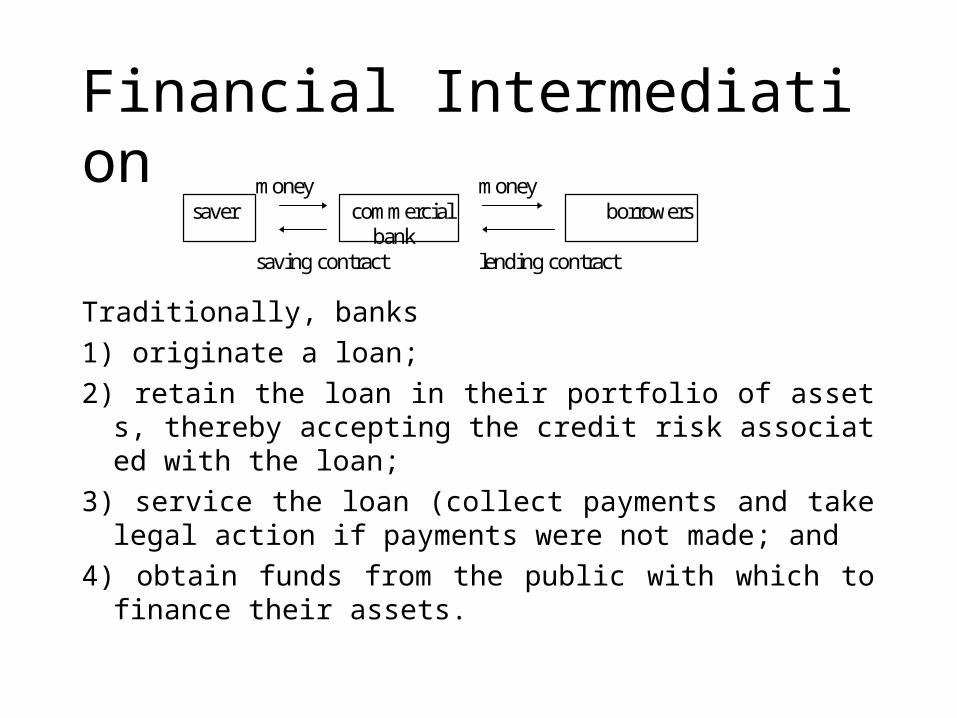

Financial Intermediation

Traditionally, banks

1) originate a loan;

2) retain the loan in their portfolio of assets, thereby accepting the credit risk associated with the loan;

3) service the loan (collect payments and take legal action if payments were not made; and

4) obtain funds from the public with which to finance their assets.

money moneysaver commercial borrowers

banksaving contract lending contract

Problems

1. Asset/liability mismatching

2. liquidity mismatching

3. institutional mismatching

Asset Securitization

Recently, banks

1) originate a loan;

2) sell the loan to an investment banking firm that creates a security backed by the pool of loans;

3) the investment bankers obtain credit risk insurance for the pool of loans from an insurance company;

4) the investment banker can sell the right to serve the loan to another bank or a company specializing in servicing loans; and

5) the investment banking firm can sell the securities to individual and institutional investors.

Asset Securitizationlending money money money

originator trust underwriter

lending security security

contract

borrowers credit investors

enhancement

payments payments

server

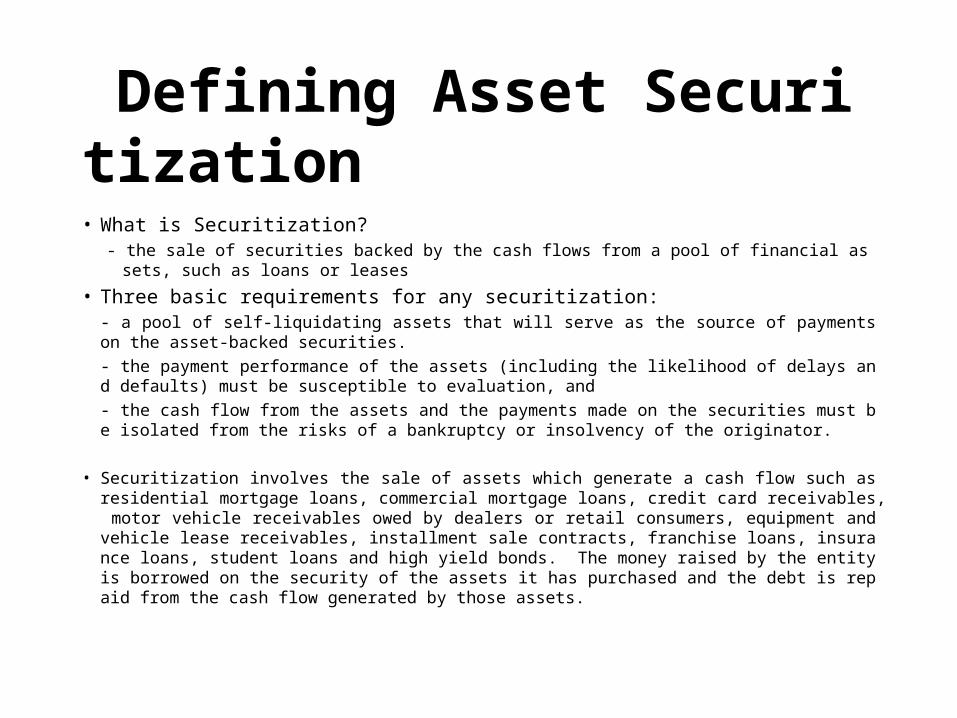

Defining Asset Securitization

• What is Securitization?- the sale of securities backed by the cash flows from a pool of financial assets, such as loans or le

ases

• Three basic requirements for any securitization:- a pool of self-liquidating assets that will serve as the source of payments on the asset-backed securities.

- the payment performance of the assets (including the likelihood of delays and defaults) must be susceptible to evaluation, and

- the cash flow from the assets and the payments made on the securities must be isolated from the risks of a bankruptcy or insolvency of the originator.

• Securitization involves the sale of assets which generate a cash flow such as residential mortgage loans, commercial mortgage loans, credit card receivables, motor vehicle receivables owed by dealers or retail consumers, equipment and vehicle lease receivables, installment sale contracts, franchise loans, insurance loans, student loans and high yield bonds. The money raised by the entity is borrowed on the security of the assets it has purchased and the debt is repaid from the cash flow generated by those assets.

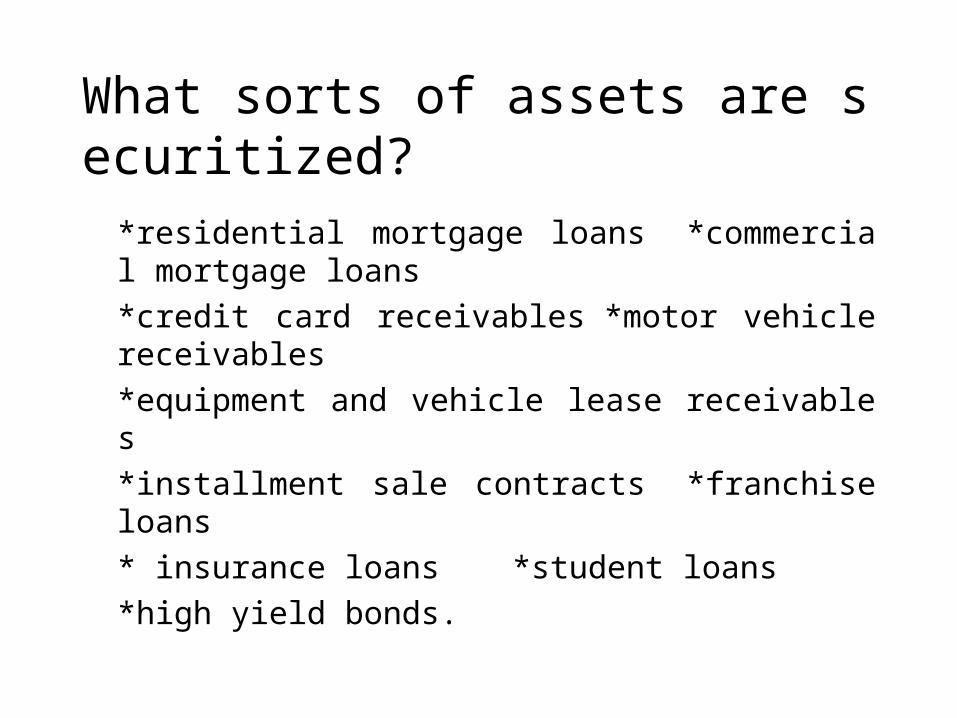

What sorts of assets are securitized?

*residential mortgage loans *commercial mortgage loans

*credit card receivables *motor vehicle receivables

*equipment and vehicle lease receivables

*installment sale contracts *franchise loans

* insurance loans *student loans

*high yield bonds.

The evolution of asset securitization

• late 1970s and early 1980s

• 1982

• 1983, SEC

• 1984, Secondary Mortgage Market Enhancement Act

• 1986, Real Estate Mortgage Investment Conduits

• 1992

• 1993, Financial Asset Securitization Investment Trust

Real Estate Mortgage Investment Conduits

• An alternative for pool owners who want to issue a multi-class security, but can't take on debt or need to sell the mortgages

- Created in 1986 by Tax Reform Act

- Separate legal entity for tax purposes

- Tax-favored entity for issuing CMOs

- Pool owners sell mortgages to the REMIC

- Can take many forms - trust, corporation, partnership

- Can use any type of security - pass-through, debt

- Investors only pay tax on interest income

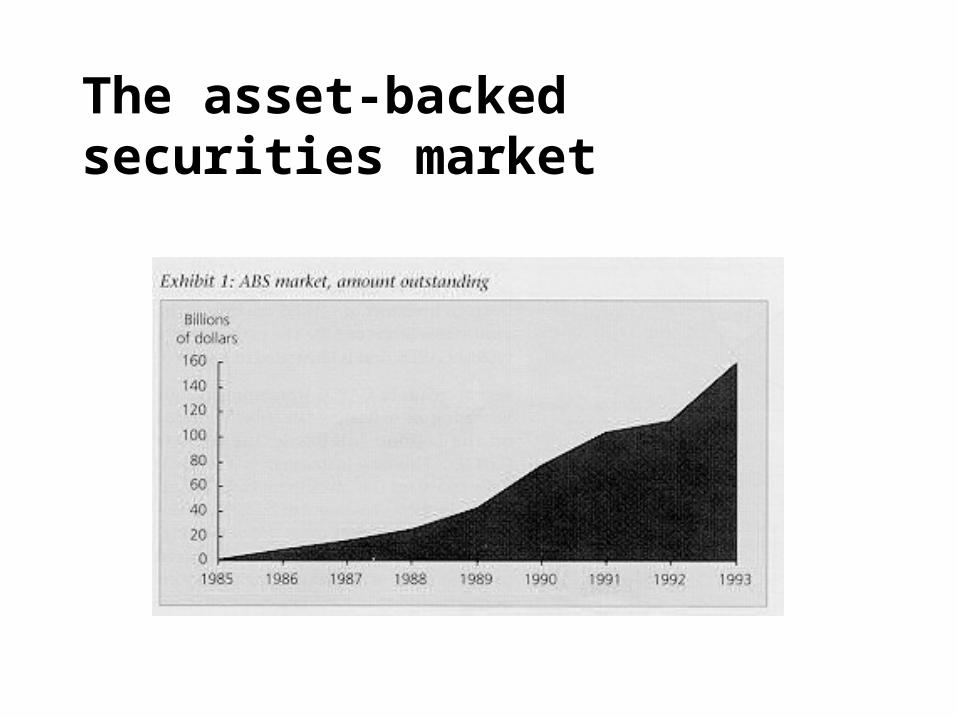

The asset-backed securities market

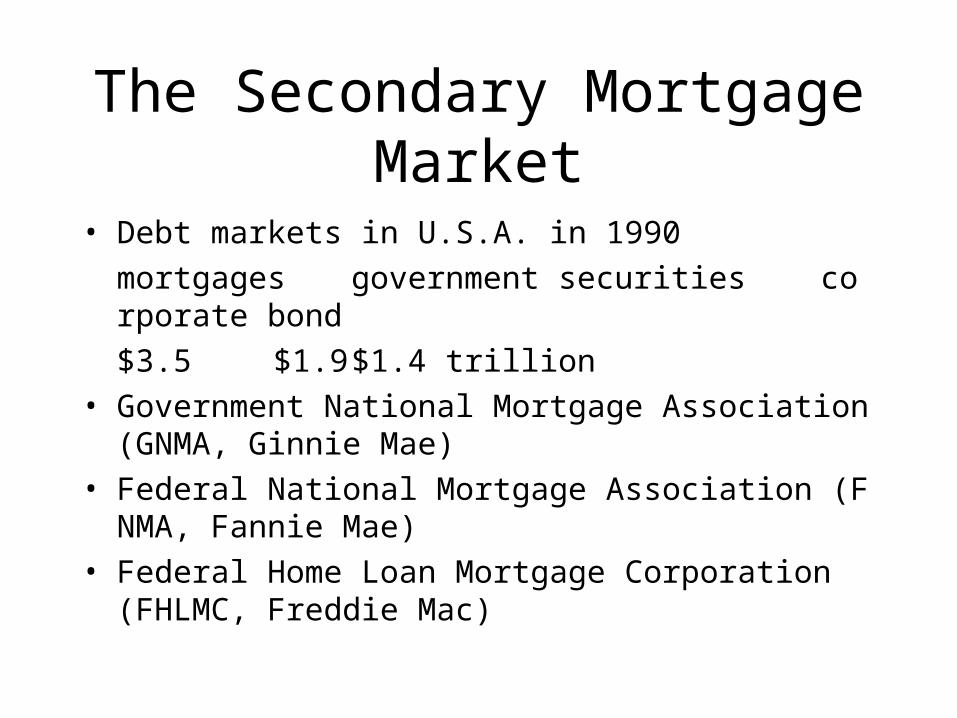

The Secondary Mortgage Market

• Debt markets in U.S.A. in 1990

mortgages government securities corporate bond

$3.5 $1.9 $1.4 trillion

• Government National Mortgage Association (GNMA, Ginnie Mae)

• Federal National Mortgage Association (FNMA, Fannie Mae)

• Federal Home Loan Mortgage Corporation (FHLMC, Freddie Mac)

The Secondary Mortgage Market

Origination of Passthrough by Agency(in million)

Year GNMA FNMA FHLMC Private firms Total1984 28,097 18,684 13,546 6,273 68,5841985 45,980 38,829 23,649 6,916 117,3591986 101,433 100,198 60,566 13,163 277,3461987 94,929 75,018 63,229 18,576 253,7391988 55,248 39,777 54,878 20,699 172,5901989 57,190 73,518 69,764 12,010 214,4711990 64,651 73,815 96,695 14,341 251,492

Source: Freddie Mac, Secondary MortgageMarkets, 1991

Holdings of Mortgage-Backed Securities

Percentage Distribution of Holdings of Mortgage-Backed Securities byInstitutionsThrifts 23.40%Banks 21.0%Pension Funds 9.7%Life insurance companies 14.4%Dealers, mutual funds, asset managers, etc. 31.5%

Asset-Backed Securities Issuance Issuance amount by collateral (in billion)

Collateral typeYear Autos Credit cards Home

equityOthers Total

1985 898.6 0 0 338.3 1236.91986 9473 0 0 617.6 10090.61987 6372.2 2410 0 1208.7 9990.91988 5497.8 7420 0 2276.1 15193.91989 7823.6 11112 2700.2 2912.5 24548.31990 11632.6

28%22731

54%5499.9

13%1963.9

5%41827.4

*1991 11240.5 16342 8820.5 2928.4 39331.4Total 52938.3 60015 17020.6 12245.5 142219.4* Through September 1991Source: Data supplied by the first Boston Corporation

Benefits to issuers

1) Obtaining a lower cost of funds

2) More efficient use of capital

3) Better asset/liability management

4) Enhancing financial performance

5) Diversification of sources

Benefits to investors and borrowers

• To investors:

– reduced credit risk. a) it is backed by a diversified pools of loans, and

b) there is credit enhancement.

– returns are also improved.

• To borrowers: reduce the lending rates.

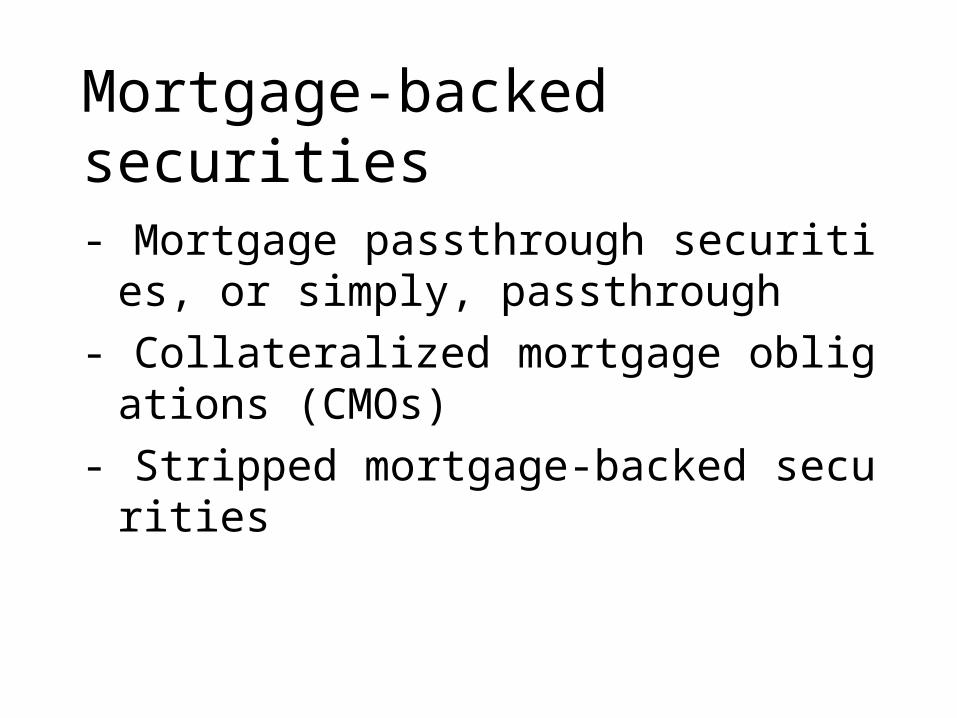

Mortgage-backed securities

- Mortgage passthrough securities, or simply, passthrough

- Collateralized mortgage obligations (CMOs)

- Stripped mortgage-backed securities

Mortgage Passthrough Securities

- Most popular form of mortgage-backed security

- Represents sale of mortgages

- Taxed only at investor level

- Commits to pay P,I, and prepayments each month as received

- "Modified" pass through guarantees timely payment

- Greatest volume issued by FNMA, FHLMC and GNMA surrogates

- Private entities also issue

- Swap program provided more options to originators

Collateralized Mortgage Obligations

- Debt instrument secured by pool of mortgages

- Appeals to investors who can't tolerate prepayment

- A Derivative: different from the underlying mortgages even though CMO distributions are derived from the mortgages

- Issued in multiple maturities or tranches

- Cash flow is distributed in sequential order (A,B,C,Z tranches)

- A method for issue debt, reduce prepayment risk and shift remaining prepayment risk to the investor

- Quoted with a stated maturity within a range

- Overcollateralized

Stripped mortgage-backed securities

- Issuer retains ownership

- I is paid based on a coupon rate of interest (IO), P is passed through as it is received from normal amortization and prepayments (PO)

- Some overcollateralization is required

- Prepayment potential important to investor

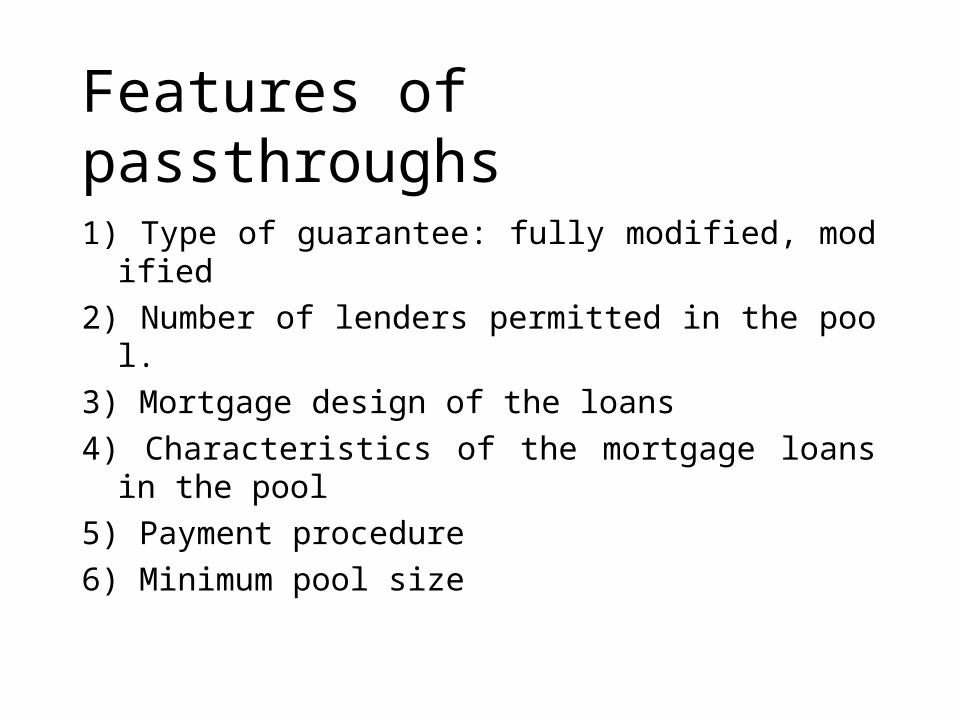

Features of passthroughs

1) Type of guarantee: fully modified, modified

2) Number of lenders permitted in the pool.

3) Mortgage design of the loans

4) Characteristics of the mortgage loans in the pool

5) Payment procedure

6) Minimum pool size

Cash flows of mortgage-backed securities

1) interest

2) scheduled principal repayment

3) payments in excess of the regularly scheduled principal repayment

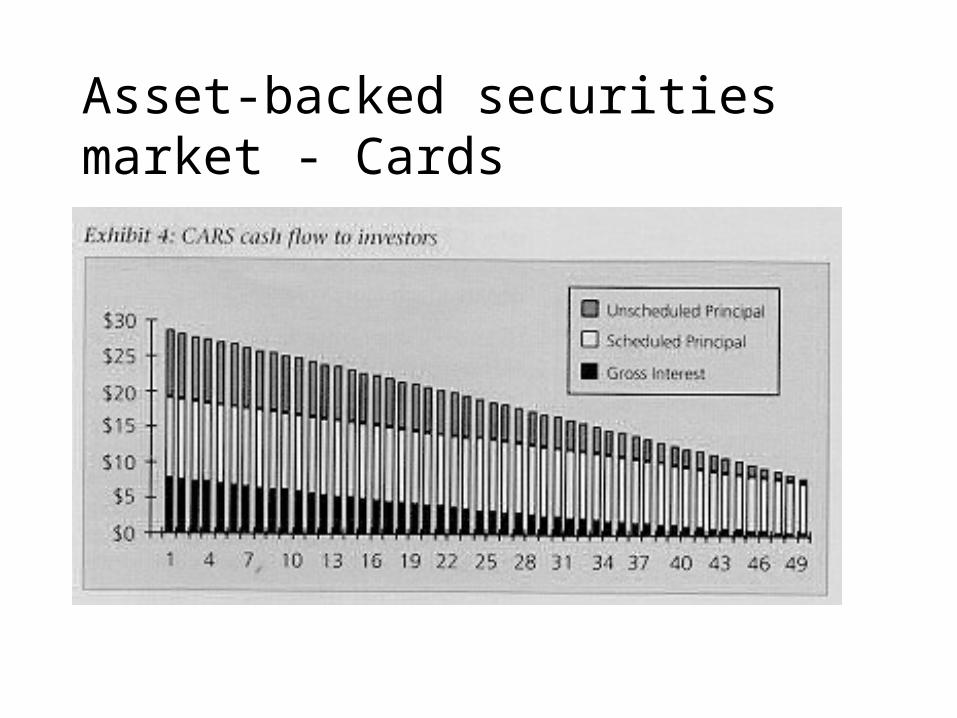

Asset-backed securities market - Cards

Asset-backed securities market - Cards

Role of players

a. collateral/borrower

b. origination

c. servicing: often by originator

d. credit-enhancement:

e. Special Purpose Trust:

f. investors

g. underwriters

h. rating agency

i. government

Role of an investment bank

• An investment bank provides consultants to a broad spectrum of issues, including corporate, bankruptcy, regulatory, securities, and security-interest questions.

• An investment bank serves as an representative of issuers and underwriters in the public and private sale of securities secured by a variety of nonmortgage assets.

Evaluation of mortgage-backed securities

Pricing is a function of:

- interest rate risk

- default

- risk of delayed payment

- prepayment possibilities

- PSA model

- FHA prepayment experience

- empirical models

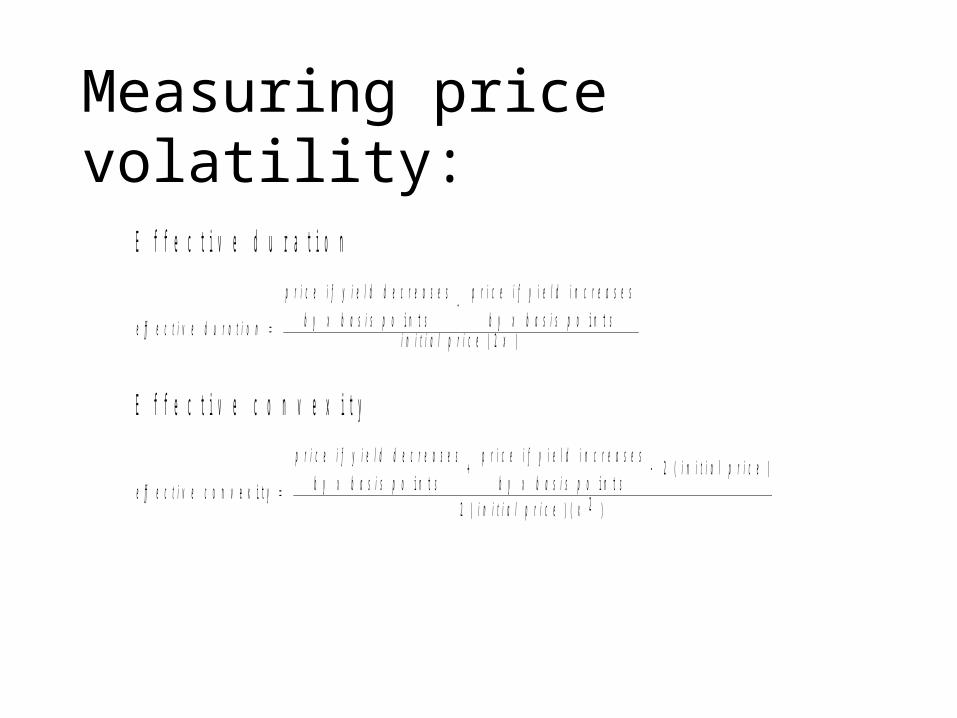

Measuring price volatility:

E f f e c t i v e d u r a t i o n

e ff e c t i v e d u r a t i o n

p r i c e i f y i e l d d e c r e a s e s

b y x b a s i s p o s

p r i c e i f y i e l d i n c r e a s e s

b y x b a s i s p o si n i t i a l p r i c e x

i n t i n t( )2

E f f e c t i v e c o n v e x i t y

e ff e c t i v e c

p r i c e i f y i e l d d e c r e a s e s

b y x b a s i s p o s

p r i c e i f y i e l d i n c r e a s e s

b y x b a s i s p o si n i t i a l p r i c e

i n i t i a l p r i c e x o n v e x i t y

i n t i n t

( )

( ) ( )

2

2 2

Price/Yield Relationship for a Callable bond - negative convexity

price

yield

The Option pricing methodology

callable bond price

= noncallable bond price -call option rice

Option-adjusted spread methodology

pS

CF

r oas

ts

si

i

tts

S

0

1

1

360

1

1

1

( )

Total return framework

( ) . t o t a l f u t u r e d o l l a r sp r i c e o f t h e p a s s t h r o u g h

n o o f m o n t h s i n h o r i z o n

1

1

T h e n t h e e f f e c t i v e a n n u a l y i e l d i s

( )1 1 2 1 t o t a l m o n t h l y r e t u r n

定義• 證券化 (securitization)-

簡言之 , 凡是以發行證券直接在資本市場上籌措資金的叫做證券化 . 或言 , 利用發行證券的形式到資本市場籌措資金 , 而投資人對標的資產的未來現金流量具有求償權 .

• 不動產證券化 (Real Estate Securitization)

利用發行證券的形式來轉化不動產單一固定性的投資為流動性高的證券投資 . 使得不動產的投資由直接的物權關係轉為間接的債權關係 . 資金得由證券的形式由資本市場注入不動產市場 .

為何有不動產證券化• The bringing together of sources and uses of capital is the

core to the finance function. In a world of costless transactions, suppliers of capital would be able to identify and meet users in need of debt and equity to carry out their investment objectives or development plans.

• However, the world of real estate finance and investment is far different from the world described above.

• Financial instruments and other devices have been developed by financial intermediaries to facilitate the necessary transactions.

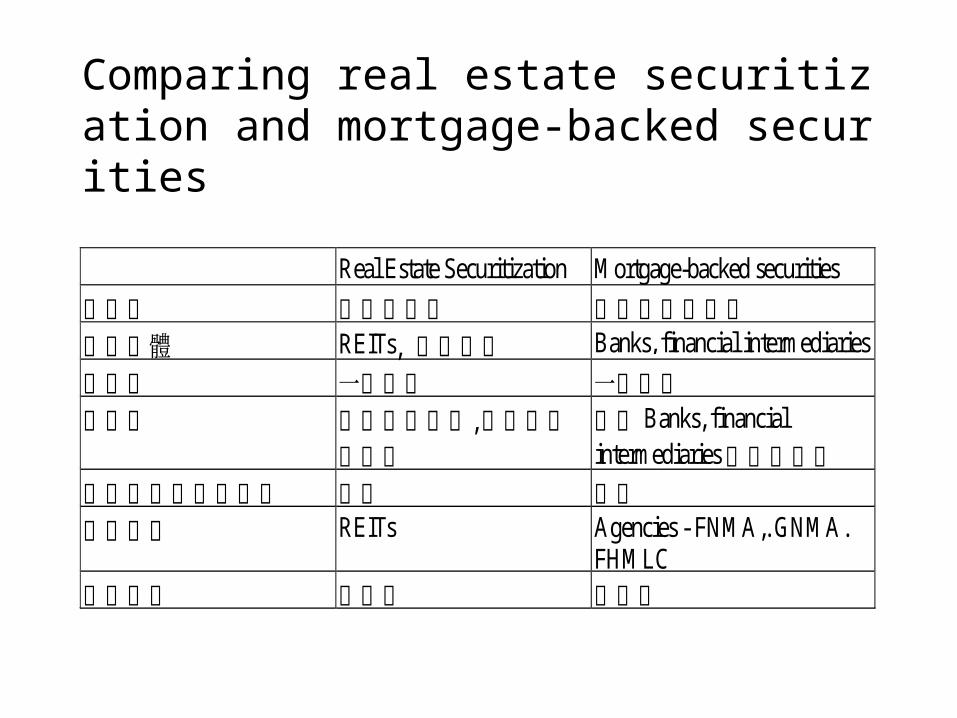

Real Estate Securitization Mortgage-backed securities

標的物 不動產本身 不動產抵押債券經營主體 REITs, 信託公司 Banks, financial intermediaries

投資者 一般大眾 一般大眾受益者 不動產開發商,不動產經

營業者疏導 Banks, financialintermediaries的資金壓力

對不動產市場的影響 直接 間接運作方式 REITs Agencies - FNMA,. GNMA.

FHMLC證券形式 權益形 債券形

Comparing real estate securitization and mortgage-backed securities

不動產證券化的特性•投資單位化•權益可分割•權益可轉移 - 次級市場存在 ,流通性高

•以證券形式表彰權益 : 投資人權益是以證券形式表示而非以物權 ,即不動產產權持分來表彰

不動產證券化的目的• 導入資本市場資金於不動產市場上• 促使不動產經營透明化及效率提高

不動產證券化的優點• To the whole economy

– 促進不動產開發– 促進資金的有效利用– 健全不動產市場機能

• To developer– 取得資金– 提高經營績效

• To investors– 多一個投資的管道 ,分散風險– 提高投資的流通性

美國的不動產證券化•主要 (常見 )型態• Real Estate Investment Trusts (REITs)

• Real Estate Limited Partnerships (RELPs)

Forms of ownership germane to financing real property

I. Individual ownership II. Co-ownership

III. Group ownership - joint tenancy

A. Partnerships - tenancy in common

1.general, 2.limited - tenancy by the entirety

B.Corporations

1.Ordinary - collapsible, noncollapsible

2.S corporation

C. Real estate investment trusts

D. Joint venture

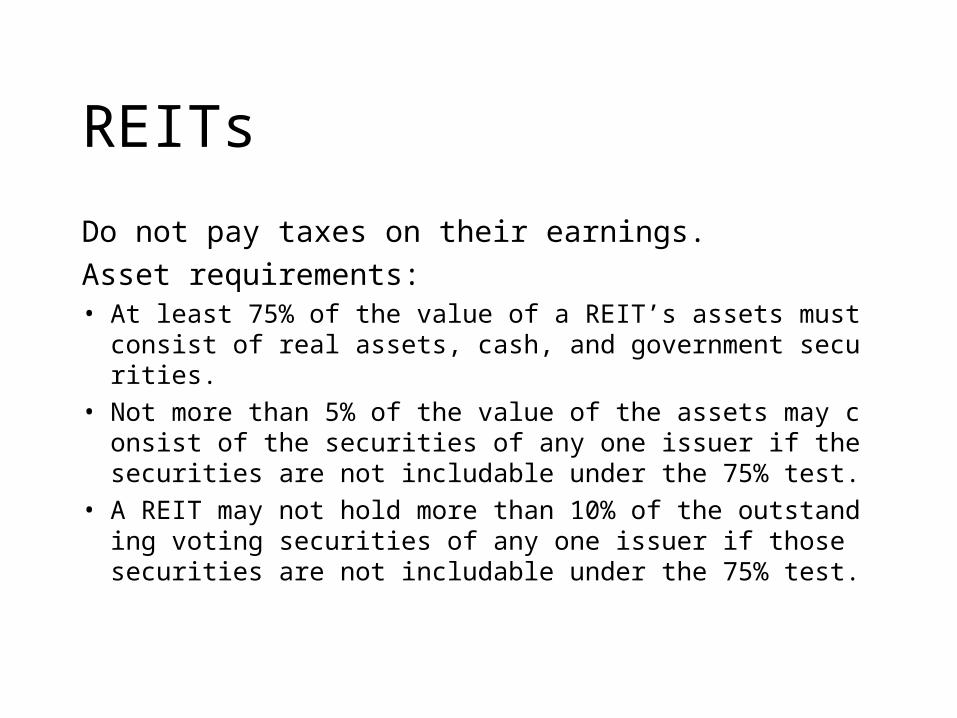

REITs

Do not pay taxes on their earnings.

Asset requirements:• At least 75% of the value of a REIT’s assets must consist o

f real assets, cash, and government securities.

• Not more than 5% of the value of the assets may consist of the securities of any one issuer if the securities are not includable under the 75% test.

• A REIT may not hold more than 10% of the outstanding voting securities of any one issuer if those securities are not includable under the 75% test.

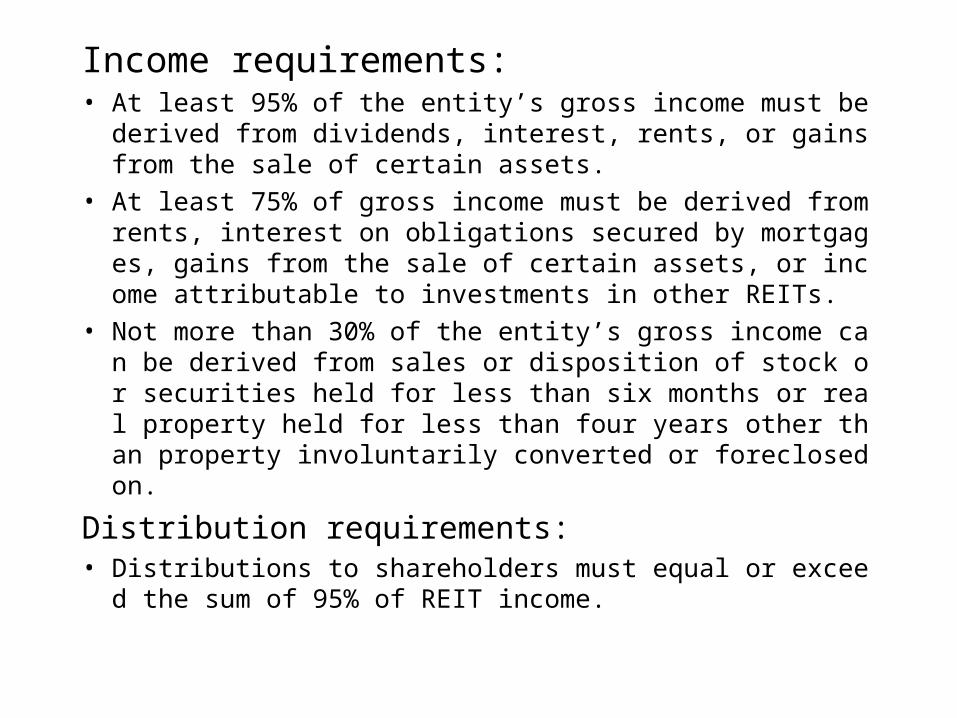

Income requirements:• At least 95% of the entity’s gross income must be derived fro

m dividends, interest, rents, or gains from the sale of certain assets.

• At least 75% of gross income must be derived from rents, interest on obligations secured by mortgages, gains from the sale of certain assets, or income attributable to investments in other REITs.

• Not more than 30% of the entity’s gross income can be derived from sales or disposition of stock or securities held for less than six months or real property held for less than four years other than property involuntarily converted or foreclosed on.

Distribution requirements:• Distributions to shareholders must equal or exceed the sum of

95% of REIT income.

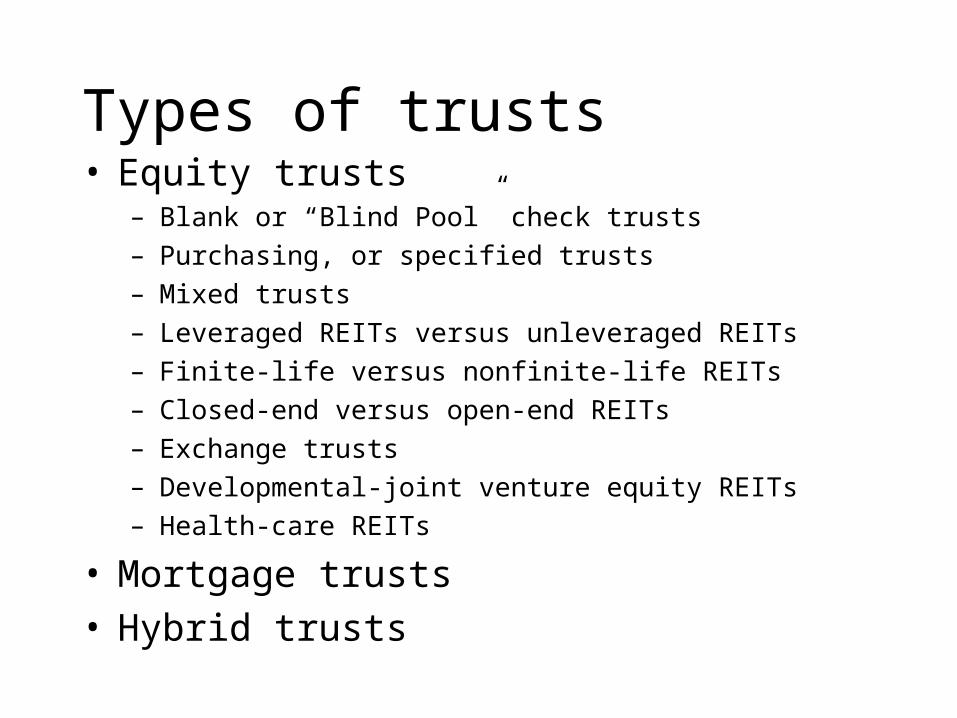

Types of trusts• Equity trusts

– Blank or “Blind Pool” check trusts

– Purchasing, or specified trusts

– Mixed trusts

– Leveraged REITs versus unleveraged REITs

– Finite-life versus nonfinite-life REITs

– Closed-end versus open-end REITs

– Exchange trusts

– Developmental-joint venture equity REITs

– Health-care REITs

• Mortgage trusts• Hybrid trusts

REIT 實行架構

underwriting

購買不動產(equity trusts)

投資金額 投資 不動產融資受益憑證 收益 (mortgage trusts)

Hybrid trusts

買賣

投資銀行

投資者 REITs

次級市場

日本的不動產證券化• 信託型不動產證券化1. 由不動產公司將土地建築物分售給投資者2. 投資者將持有之共同持分權信託給信託銀行 , 信託銀行

發給受益憑證3. 信託銀行委予不動產 ( 經理 ) 公司經營4. 不動產 ( 經理 ) 公司負責經營管理 , 出租建築物以收取租

賃費 , 再轉給信託銀行5. 信託銀行按持分分錢給投資者6. 最後 , 信託銀行可出售土地建築物 , 再將錢分給投資者• 組合型不動產證券化

日本信託型不動產證券化實行架構

繳交投資款 土地建築物分售

發給受益憑證支付收益 將共有持分權信託支付出售價款

支付租賃費 委託經營

支付租賃費 分租

不動產公司投資者

信託銀行不動產公司承租戶

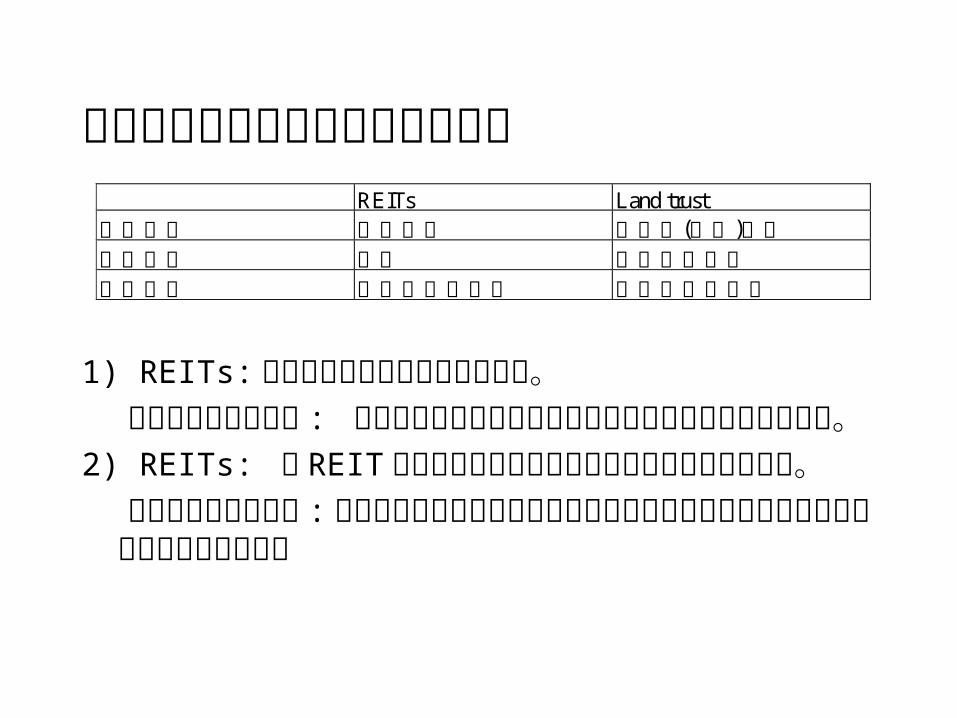

美日兩國不動產證券化運作之比較

1) REITs: 先募集資金再找不動產投資標的。 信託型不動產證券化 : 先有不動產﹐將所有權細分後﹐

再以證券型態賣給投資者。2) REITs: 以 REIT 方式發行之憑證可在公開市場轉售﹐流

動性極佳。 信託型不動產證券化 : 有價證券之定義中不含不動產信

託的有價證券﹐故而無法在公開市場轉售﹐流動性差

REITs Land trust信託本質 金錢信託 不動產(實物)信託信託財產 現金 不動產所有權信託目的 不動產證券投資 不動產開發經營

我國的案例• 財神酒店• 太平洋鳳蝶計劃• 歐洲共同仕場

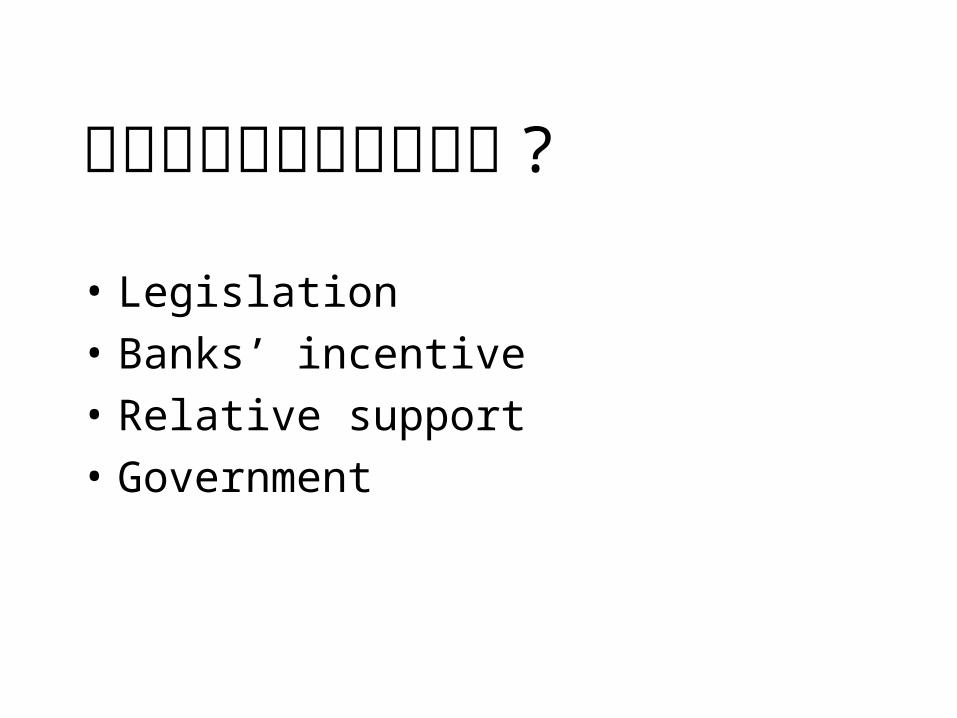

我們需要不動產證券化嗎 ?

• Legislation

• Banks’ incentive

• Relative support

• Government

我國發展不動產證券化之探討• REIT, land trust, which is better?• 法令制度的配合

– 制定信託法 , 信託業法– 修正證券交易法– 相關稅法的配合

• 遊戲規則的建立– 投資者– 信託公司– 不動產開發商– 不動產經營管理商– Investment bankers