$asqteacher 20080423 1240 - wikispacesvespereconomics.wikispaces.com/file/view/frq+practice.pdf ·...

TRANSCRIPT

Microeconomic FRQ’s

20071. A patent gives inventors the exclusive right to produce and market a product for a period of time. GCR Company is a profit-

maximizing firm. It has a patent for a unique antispyware computer program called Aspy.a. Assume that GCR is making economic profit. Draw a correctly labeled graph and show the profit-maximizing price and

quantity.b. Assume that the government imposes a lump-sum tax on GCR.

i. What will happen to output and market price? Explainii. What will happen to GCR’s profits?

c. Assume instead that the government grants a per-unit subsidy to GCR for Aspy.i. What will happen to output and market price? Explain.

ii. What will happen to GCR’s profits?d. Now assume that GCR’s patent on Aspy expires. What will happen to GCR’s economic profits in the long run?

Explain.

Scoring guidelines and answersP MC

ATCP*

MR D

Q* Qa. 4 pts. – 1 for correct graph; 2 for profit-maximizing Q and P where MR = MC; 1 for showing that P>ATC at Q*b. 3 pts. – 2 – profit-maximizing P and Q will not change b/c a lump-sum tax doesn’t affect MC. It would only affect ATC, shifting

it upward. 1 pt. for saying that profits will decreasec. 3 pts. – 2 – Q increases and P decreases b/c MC curve shifts down (to right) – subsidy makes it cheaper to produce b/c it gives

producers $$$ for each one they produce; 1 pt. for saying profits will increased. 2 pts –profits will fall in the long-run b/c new firms will enter the market

2.# of unskilled workers

hiredQuantity of radiosproduced (per day)

0 01 202 453 604 705 756 797 80

Assume that HZRad Company produces clock radios as shown in the short-run production function in the table above. HZRad can sell allthe clock radios it produces at a market price of $20 each and can hire all the unskilled labor it needs at a wage of $90 per day per worker.Assume also that labor is the only variable input.

a. Using the specific information above, draw a correctly labeled graph of HZRad’s current supply curve for unskilled labor.b. What is HZRad’s profit-maximizing output level? Explain.c. Suppose that HZRad is the 1st company to use a new technology that increases the productivity of its unskilled workers.

i. How will the new technology affect the quantity of labor HZRad hires? Explain.ii. How will the new technology affect the wage paid to HZRad’s unskilled workers?

Scoring guidelines and answersWagerate

90 SL

Q of workers

a. 1 pt for graph – horizontal supply curve at $90 wage rate & correctly labeled axesb. 2 pts – 1 for identifying profit-maximizing output as 75 (or between 75 and 79) – profits are maximized where MR=MC; the MC ofthe 5th worker is $90; the MR from the 5th worker is 5 units x $20 = $100; the MC of the 6th worker is $90 but the MR = 4 units x $20 =$80. So 5 workers should be hired, producing 75 units. The marginal revenue product for the 5th worker is greater than $90 but the MRPfor the 6th worker is less than $90.c. 3 pts – 2 – Quantity of workers hired will increase b/c marginal product of labor increases at each input level OR D curve for laborshifts to right; 1 pt – wages remain constant

3. Two bus companies, Roadway and Rankin Wheels, operate a route from Greensboro to Spring City, transporting a mix of passengersand freight. They must file their schedules with the local transportation board each year and cannot alter them during that year. Thoseschedules are revealed only after both companies have filed. Each company must choose between an early and a late departure. Therelevant payoff matrix appears below, with the first entry in each cell indicating Roadway’s daily profit and the second entry in each cellindicating Rankin Wheels’ daily profit.

Rankin WheelsEarly Late

Roadway --Early $1000; $900 $950; $850Roadway – Late $750; $650 $700; $800

a. In which market structure do these firms operate? Explain.b. If Roadway chooses an early departure, which departure time is better for Rankin Wheels?c. Identify the dominant strategy for Roadway.d. Is choosing an early departure a dominant strategy for Rankin Wheels? Explain.e. If both firms know all of the information in the payoff matrix but do not cooperate, what will be Rankin Wheels’ daily

profit?Scoring guidelines and answers

a. 1 pt – market is an oligopoly b/c there are only 2 firms and their actions are mutually interdependentb. 1 pt. – early departurec. 1 pt – Roadway’s dominant strategy is early departure since, regardless of Rankin’s departure time, Roadway makes more $$ w/

an early departured. 2 pts. – early departure is NOT a dominant strategy for Rankin b/c, if Roadway chooses a late departure, Rankin is better off

choosing a late departure.e. 1 pt. -- $900 – both firms have an incentive to adopt an early departure strategy; it is Roadway’s dominant strategy as they’re

better off w/ early no matter what; therefore, since it is in Roadway’s interest to depart early, Rankin knows they will make moreprofit by also departing early b/c they’ll make $900 rather than $850

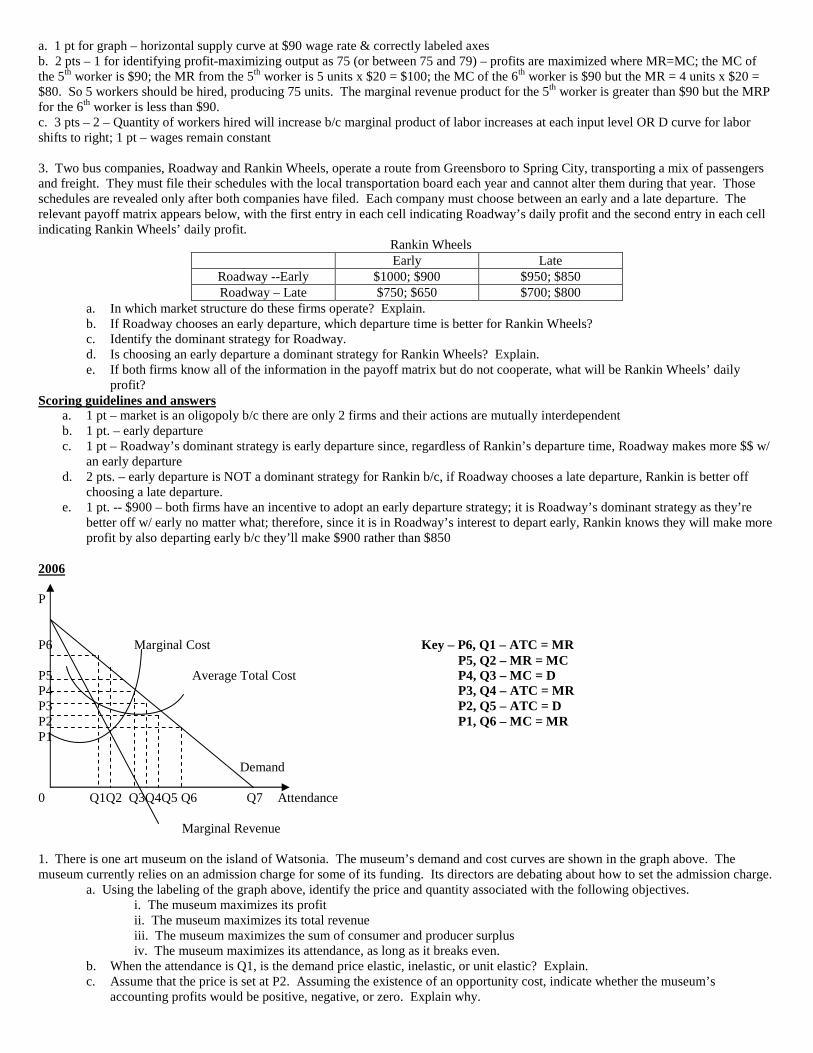

2006

P

P6 Marginal Cost Key – P6, Q1 – ATC = MRP5, Q2 – MR = MC

P5 Average Total Cost P4, Q3 – MC = DP4 P3, Q4 – ATC = MRP3 P2, Q5 – ATC = DP2 P1, Q6 – MC = MRP1

Demand

0 Q1Q2 Q3Q4Q5 Q6 Q7 Attendance

Marginal Revenue

1. There is one art museum on the island of Watsonia. The museum’s demand and cost curves are shown in the graph above. Themuseum currently relies on an admission charge for some of its funding. Its directors are debating about how to set the admission charge.

a. Using the labeling of the graph above, identify the price and quantity associated with the following objectives.i. The museum maximizes its profitii. The museum maximizes its total revenueiii. The museum maximizes the sum of consumer and producer surplusiv. The museum maximizes its attendance, as long as it breaks even.

b. When the attendance is Q1, is the demand price elastic, inelastic, or unit elastic? Explain.c. Assume that the price is set at P2. Assuming the existence of an opportunity cost, indicate whether the museum’s

accounting profits would be positive, negative, or zero. Explain why.

d. Assume that the government decides the museum should charge no admission and agrees to subsidize the museum for anylosses.

i. Using the labeling in the graph, identify the museum’s attendance under that circumstance.ii. Would the outcome be allocatively efficient? Explain.

Scoring guidelines and answers1. a. 4 pts.

i. P5, Q2ii. P3, Q4

iii. P4, Q3iv. P2, Q5

b. 2 pts. – demand is elastic at Q1 b/c MR > 0 OR Q1 is to the left of the midpoint OR Q1 is in the upper half of the demandcurve

c. 2 pts. – accounting profits are positive b/c economic profits are 0, opportunity costs are present and economic profits =accounting profits – opportunity costs

d. 3 pts – Q7, the outcome is not allocatively efficient b/c MC > B or MSC > MSB

Short-run total cost functionQuantity produced Total Cost in dollars

0 201 272 383 534 725 956 122

2. The table above gives the short-run total cost function for a typical firm in a perfectly competitive industry.a. What is the dollar value of the firm’s total fixed cost?b. Calculate the marginal cost of producing the first unit of output.c. If the price the firm receives for its product is $20, indicate the firm’s profit-maximizing quantity of output and explain

how you determined your answer.d. Given your results in part (c), explain what will happen to the number of firms in the industry in the long run.e. Assume that this firm operates in a constant-cost industry and has reached long-run equilibrium. If the government

imposes a per-unit tax of $2, indicate what will happen to the firm’s profit-maximizing output in the long run.

Scoring guidelines and answers2. a. TFC = $20

b. MC for the first unit = $7c. 2 pts. – profit maximizing output = 4 units (or between 4 and 5 units) b/c MR > MC for all units until Q = 5d. 2 pts. – number of firms will increase b/c profits will cause new firms to enter the industrye. there is no change in the profit-maximizing output

P Supply

Pe

Demand0

Qe Quantity of Land for residential development (acres)

3. The supply and demand for land for residential development is shown in the diagram above. The land supplied for suchdevelopment comes from privately held open-space land or privately held farmland.

a. Redraw the graph above and show how an increase in income will affect the equilibrium price and quantity of landconverted into residential development, assuming that land for residential development is a normal good.

b. Redraw the graph above and show how a decrease in government per-unit subsidies to farmers will affect theequilibrium price and quantity of land converted into residential development.

c. Assume that the conversion of open-space land and farmland imposes costs on the general population, which can nolonger enjoy the scenic vistas.

i. Indicate whether the marginal social cost of converting land is greater than, less than, or equal to the marginalprivate cost of converting land.

ii. Explain whether the private market quantity of land converted into residential development is socially optimal.

Scoring guidelines and answers3. 2 pts. – a. 1 for rightward shift of the demand curve, equilibrium price and quantity increasesb. 2 pts. – rightward shift of supply curve, equilibrium price decreases and quantity increasesc. 2 pts. – MSC > MPC, the conversion of land to residential development is not socially optimum b/c MSC > MSB

20051. Bestmilk, a typical profit-maximizing dairy firm, is operating in a constant-cost, perfectly competitive industry that is in long-runequilibrium.a. Draw correctly-labeled side by side graphs for the dairy market and for Bestmilk showing the following: price and output for theindustry and price and output for Bestmilk.b. Assume that milk is a normal good and consumer income falls. Assume that Bestmilk continues to produce. On your graph in part a,show the effect of the decrease in income on each of the following in the short-run: price and output in the industry, price and output forBestmilk, area of loss or profit for Bestmilk.c. Following the decrease in consumer income, what must be true for Bestmilk to continue to produce in the short-run?d. Assume that the industry adjusts to a new long-run equilibrium. Compare the following between the initial and the new long-runequilibrium: price in the industry, output of a typical firm, the number of firms in the dairy industry.

Scoring guidelines and answersMC ATC

P S P

P1 P1 MR1

P2 P2 MR2D1

D2

Q2 Q1 Q q2 q1 QINDUSTRY BESTMILK

a. 4 pts. – 1 for graph of industry, 1 for industry P & Q, 1 for horizontal D for Bestmilk, 1 for equilibrium Q where P=MC=ATC.b. 4 pts. – 1 for decrease in D, 1 for decrease in market (industry) P and Q, 1 for change to new lower profit-maximizing P and Q forBestmilk, 1 for shading the area of loss for Bestmilkc. 1 for stating that P>AVC, or TR>TVC, or stating that losses are less than total fixed costsd. 3 pts. – 1 for stating that price returns to original long-run equilibrium price, 1 for stating that output of a typical firm returns tooriginal profit-maximizing quantity, 1 for stating that there is a decrease in the # of firms.

Supply + taxP

A13 B Supply12 C F

D G Demand11

E10

80 100 Q

2. The graph above shows the market for a good that is subject to a per-unit tax. The letters in the graph represent the enclosed areas.a. Using the labeling on the graph, identify each of the following: equilibrium price and quantity before the tax, area representingconsumer surplus before the tax, area representing producer surplus before the tax.b. Assume that the tax is now imposed. Based on the graph, does the price paid by the buyers rise by the full amount of the tax? Explain.c. Using the labeling on the graph, identify each of the following after the imposition of the tax: net price received by the sellers, amountof tax revenue, area representing consumer surplus, area representing deadweight loss.

Scoring guidelines and answers

ATC intersects MR1at ATC’s minimum;line from q2 intersectsATC; shaded arearepresents lossfollowing D decrease

a. 3 pts. – 1 pt. for P = $12 and Q = 100 units; 1 pt. for identifying consumer surplus before the tax (CS = A+B+C+F); 1 pt. foridentifying producer surplus before the tax (PS = D+E+G = $100)b. 2 pts. – 1 pt. for stating that the price paid by the buyers does not increase by the full amount of the tax; 1 pt. for correct explanation: Pincreases by $1 and the tax is $2 per unit.c. 4 pts. – 1 pt. for identifying the net price received by the sellers, $11; 1 pt. for identifying the tax revenue, B+C+D or $160; 1 pt. foridentifying consumer surplus, A; 1 pt. for identifying deadweight loss, F+G or $20.

3. P&L is a profit-maximizing shirt manufacturing firm. The firm can sell all the shirts it can produce to retailers at a price of $20 each.P&L can hire all the workers it wants at a market wage of $120 per day per worker. The table below shows the firm’s short-runproduction function.

# of workers # of shirts per day0 01 102 253 454 605 726 807 858 82

a. In what kind of market structure does this firm sell its output? How can you tell?b. In what kind of market structure does this firm hire its workers? How can you tell?c. Calculate the marginal revenue product of the 3rd worker. Show your work.d. How many workers should the firm hire to maximize profit? Explain.

Scoring guidelines and answers

a. 2 pts. – 1 pt. for identifying perfect competition; 1 pt. for correct explanation, price is constant or the firm is a price takerb. 2 pts. – 1 pt. for identifying perfect competition; 1 pt. for correct explanation, price is constant or the firm is a price taker in the

labor marketc. 2 pts. – 1 pt. for stating the MRP is $400; 1 pt. for showing the calculation: MRP = P x MP so MRP = $20 x 20 = $400d. 2 pts. – 1 pt. for indicating 6 workers, or in between 6 and 7 workers; 1 pt. for correct explanation: MRP > Wage for 6th worker

but MRP < Wage for 7th worker (7th worker adds 5 shirts so 5 x $20 (P of shirt) = $100; wage for 7th worker is $120)

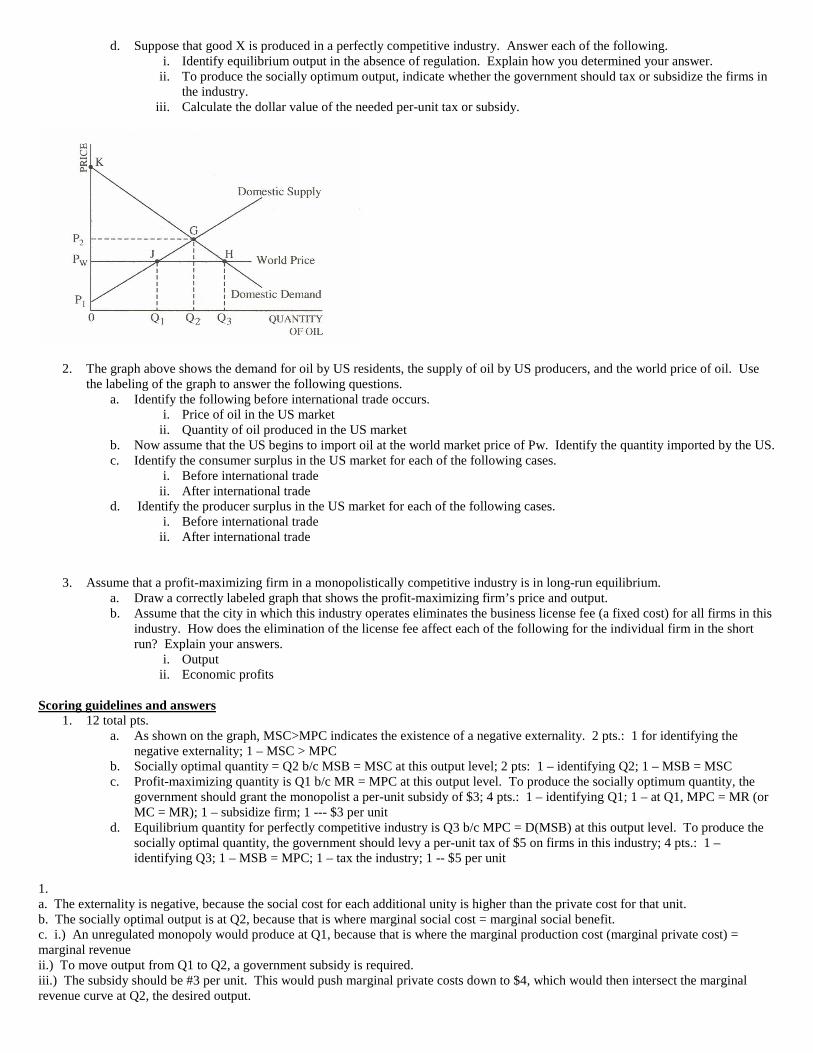

2004

1. The production of good X creates an externality. The following questions are based on the graph above, which show s themarginal revenue, marginal social benefit, marginal private cost, and marginal social cost associated with the production of goodX.

a. Is the externality positive or negative? Explain.b. Using labeling from the graph above, identify the socially optimum output. Explain how you determined your answer.c. Suppose that good X is produced by a profit-maximizing monopoly. Answer each of the following.

i. Using labeling from the graph above, identify the unregulated firm’s output. Explain how you determinedyour answer.

ii. To produce the socially optimum output, indicate whether the government should tax or subsidize the firm.iii. Calculate the dollar value of the needed per-unit tax or subsidy.

d. Suppose that good X is produced in a perfectly competitive industry. Answer each of the following.i. Identify equilibrium output in the absence of regulation. Explain how you determined your answer.

ii. To produce the socially optimum output, indicate whether the government should tax or subsidize the firms inthe industry.

iii. Calculate the dollar value of the needed per-unit tax or subsidy.

2. The graph above shows the demand for oil by US residents, the supply of oil by US producers, and the world price of oil. Usethe labeling of the graph to answer the following questions.

a. Identify the following before international trade occurs.i. Price of oil in the US market

ii. Quantity of oil produced in the US marketb. Now assume that the US begins to import oil at the world market price of Pw. Identify the quantity imported by the US.c. Identify the consumer surplus in the US market for each of the following cases.

i. Before international tradeii. After international trade

d. Identify the producer surplus in the US market for each of the following cases.i. Before international trade

ii. After international trade

3. Assume that a profit-maximizing firm in a monopolistically competitive industry is in long-run equilibrium.a. Draw a correctly labeled graph that shows the profit-maximizing firm’s price and output.b. Assume that the city in which this industry operates eliminates the business license fee (a fixed cost) for all firms in this

industry. How does the elimination of the license fee affect each of the following for the individual firm in the shortrun? Explain your answers.

i. Outputii. Economic profits

Scoring guidelines and answers1. 12 total pts.

a. As shown on the graph, MSC>MPC indicates the existence of a negative externality. 2 pts.: 1 for identifying thenegative externality; 1 – MSC > MPC

b. Socially optimal quantity = Q2 b/c MSB = MSC at this output level; 2 pts: 1 – identifying Q2; 1 – MSB = MSCc. Profit-maximizing quantity is Q1 b/c MR = MPC at this output level. To produce the socially optimum quantity, the

government should grant the monopolist a per-unit subsidy of $3; 4 pts.: 1 – identifying Q1; 1 – at Q1, MPC = MR (orMC = MR); 1 – subsidize firm; 1 --- $3 per unit

d. Equilibrium quantity for perfectly competitive industry is Q3 b/c MPC = D(MSB) at this output level. To produce thesocially optimal quantity, the government should levy a per-unit tax of $5 on firms in this industry; 4 pts.: 1 –identifying Q3; 1 – MSB = MPC; 1 – tax the industry; 1 -- $5 per unit

1.a. The externality is negative, because the social cost for each additional unity is higher than the private cost for that unit.b. The socially optimal output is at Q2, because that is where marginal social cost = marginal social benefit.c. i.) An unregulated monopoly would produce at Q1, because that is where the marginal production cost (marginal private cost) =marginal revenueii.) To move output from Q1 to Q2, a government subsidy is required.iii.) The subsidy should be #3 per unit. This would push marginal private costs down to $4, which would then intersect the marginalrevenue curve at Q2, the desired output.

d. i.) A perfectly competitive firm would produce at an equilibrium output of Q3, because that is where their marginal private cost =demand.ii.) To move output from Q3 to Q2, the government should tax the industry.iii.) A $5 tax is needed, which would move the marginal private cost curve up to $12. This makes the marginal private cost intersect thedemand curve at the desired output of Q2.

2. 8 total pts.a. As shown on the graph, P2 and Q2 were the price and quantity of oil before trade in the US market; 2 pts.: 1 each –

identifying P2 and Q2b. The amount of oil imported into the US market after trade would be equal to Q3 – Q1. US production drops to Q1 but

quantity demanded rises to Q3; 1 pt – identifying (q3 – Q1) or H-J c. The triangle P2KG represents consumer surplus before trade, while triangle PwKH represents consumer surplus after

trade (1 pt. each)d. The triangle P1P2G represents producer surplus before trade, while triangle P1PwJ represents producer surplus after

trade (1 pt. each)e. The triangle JGH shows the net gain in total surplus from trade (1 pt)

3. 8 pts.a. The correct graph for a monopolistically competitive firm will show a downward-sloping D curve with a downward-

sloping MR curve below it. The firm’s price and output would be found at the equality of MR and MC. In the long-run, the ATC curve is tangent to the demand curve and equal to price directly above the output level at which MR =MC. (see graph below); 4 pts.: 1 – graph w/ downward-sloping D curve w/ correctly labeled axes; 1 – downward-sloping MR curve below the D curve; 1 – Q from MR = MC and P from D directly above Q; 1 – long-run equilibriumAC (or ATC) tangent to D at Q

b. When the fixed cost decreases, MC is not affected so that the output and price remain constant. Economic profitincreases since ATC falls; 4 pts.: 1 – individual firm’s output does not change; 1 – license fee is a fixed cost, thus itdoes not affect the firm’s marginal cost; 1 – economic profits increase; 1 – explanation

a. (graph)

b. i.) output would not change; Output is determined by the point where marginal revenue equals marginal cost. If fixed costschange, the average total cost decreases but marginal cost does not change.

ii.) Profits increase. The firm moves from earning normal or zero economic profit to earning an economic profit. The averagetotal cost curve decreases below the demand curve. Demand remains the same and since output doesn’t change, price staysthe same. The cost though is now below price and the firm is making an economic profit.

2004 – Form B

1. Due to a new technology, Brunelle, Inc. enjoys monopoly power. Brunelle does not engage in price discrimination.a. Explain why the demand curve lies above the marginal revenue curve.b. Assume that Brunelle is earning short-run economic profits. Using a correctly labeled graph, show the following for

Brunelle.i. Profit-maximizing level of output, labeled as Q*

ii. Profit-maximizing price, labeled as P*iii. Economic profits as a shaded area

c. If Brunelle wants to maximize its total revenues instead of profits, using the graph from part b show the following.

i. Revenue-maximizing level of output labeled as Qrii. Revenue-maximizing price, labeled as Pr

d. Given your answer in part b, indicate whether Brunelle is producing the allocatively efficient level of output. Explain.e. Explain what wil happen to Brunelle’s demand curve as other firms adopt the same technology.

2. In each part below, assume that the government imposes a per-unit sales tax and that the supply curve is upward-sloping.a. In industry X, consumers buy the same quantity no matter what the price is.

i. Using a correctly labeled graph, show what happens to the quantity sold when the tax is imposed.ii. How will the burden of the tax be distributed between buyers and sellers?

b. In industry Y, the market demand curve is perfectly elastic.i. Using a correctly labeled graph, show what happens to the price of the good that he consumers pay when the

tax is imposed.ii. How will the burden of the tax be distributed between buyers and sellers?

c. In industry Z, the market demand curve is downward-sloping. Using a correctly labeled graph, shad the area thatrepresents total tax revenues.

3. The diagram above shows the domestic supply and demand for good X in the country of Placonia.a. If the current world price of good X is Pw, does Placonia export or import good X? Explain.b. Given your answer in part a, indicate the quantity of good X that Placonia exports or imports.c. Assume that the government of Placonia imposes a tariff on good X, increasing the price from Pw to Pt. Using labels in

the graph, indicate the change in each of the following in Placonia.i. Consumer surplus

ii. Producer surplusd. Indicate how employment in the domestic industry that produces good X is affected by the tariff.

Scoring guidelines and answers1. 9 pts.

a. 1 pt. – Brunelle must lower its price on all units to sell additional units. Thus, the additional revenue from the last unitsold is the price minus the loss on units that would otherwise sell at a higher price.

b. 4 pts:1 – correctly labeled graph w/ downward-sloping D and MR below demand; 1 – for Q* at MC=MR; 1 – for P* at the heightof the demand curve above MC=MR; 1 – for shading the correct area of profit (P* - ATC)Q*c. 2 pts: 1 – for identifying Qr at MR=0; 1 – for identifying Pr at the height of the demand curve above Qrd. 1 pt. – Brunelle is not producing the allocatively efficient level of output b/c P>MC (MSB > MSC)e. 1 pt. – Brunelle’s demand curve will shift inward to the left

1. a.) As Brunelle, Inc enjoys monopoly power, its demand curve is the demand curve for the industry and is thereforedownsloping. Brunelle needs to lower the price of its product in order to sell more output, but this lower price also applies to allprevious units of output produced, resulting in a marginal revenue curve that is lower than its demand curve.

b.) (see graph)c.) As shown above, total revenue is maximized at the level of output which MR = 0 and the Pr is the price level of this quantity

along the demand curve.d.) No it is not. At Q*, Brunelle is producing at a price that is above the marginal cost the firm faces (P>MC). In this scenario,

there is an underallocation of resources, as society is willing to pay more for the good than it is for other uses of the money.e.) Shift inward to the left

2. 6 pts.a. 2 pts: 1 – perfectly inelastic demand curve showing that Q does not change; 1 – since producers can raise the price by

the full amount of the tax, the tax falls entirely on buyers

b. 2 pts.: 1 – horizontal demand curve showing that price does not change; 1 – the tax falls entirely on sellers since theycan’t charge more and thus must absorb the entire amount of the tax

c. 2 pts.: 1 – for shifting either the supply or the demand curve inward to the left; 1 – for shading the correct profits area

2. a.: i.) the tax makes the supply curve shift to the left. But since the demand is perfectly inelastic, the quantity sold does notchange.ii.) As seen in the graph, the burden falls entirely on consumers.b. i.) As the supply curve shifts to the left, the quantity sold decreases from Q1 to Q2 in the graph.

ii.) As seen in the graph, the burden of tax falls entirely on suppliers of the good.c. The tax revenue is shown in the graph above. Goods are sold at P2 and Q2. The tax paid is (P2 – P0) for each unit sold. The quantitysold is Q2. So the total tax revenue is (P2 – P0) x Q2

3. 6 pts:a. 2 pts: 1 – Placonia imports the good; 1 – the domestic opportunity cost of producing good X is higher than the world

price (Pw) for unit JN. Or they can get it cheaper at the world priceb. 1 pt. – They import 300 (350 – 50) units or JN units

c. 2 pts: 1 – consumer surplus decreases from PwNH to PtMH, or a decrease of MNPwPt; producer surplus increases byJKPtPw

d. 1 pt: Employment would increase b/c domestic production of good X increases in Placonia

a.) Placonia imports good X because its domestic equilibrium price is higher than the world price, therefore it would be inclined tobuy good X cheaper from abroad.

b.) Placonia imports 300 units of good x (quantity demanded at point N (350) minus quantity supplied at point J (50))c.) i. consumer surplus would change from area NHPw to area MHPt ( a net change of PtMNPw); ii – producer surplus would

change by area PtKJPwd.) Because of the tariff, more of good X will be produced domestically, therefore employment in the industry will increase.

2003

1. J & P Company operates in a perfectly competitive market for smoke alarms. J & P is currently earning short-run positive economicprofits.

a. Using correctly labeled side-by-side graphs for the smoke alarm market and J &P Company, indicate each of thefollowing for both the market and the J & P Company.

i. Priceii. Output

b. In the graph in part for J & P, indicate the area of economic profits that J & P Company is earning in the short run.c. Using a new set of correctly labeled side-by-side graphs for the smoke alarm market and J & P Company, show what

will happen in the long run to each of the following.i. Long-run equilibrium price and quantity in the market

ii. Long-run equilibrium price and quantity for J & P Companyd. Assume that purchases of smoke alarms create positive externalities. Draw a correctly labeled graph of the smoke

alarm market.i. Label the market equilibrium quantity as Qm

ii. Label the socially optimum equilibrium quantity as Qse. identify one government policy that could be implemented to encourage the industry to produce the socially optimum

level of smoke alarms.

2. a. Draw a correctly labeled graph showing a typical monopoly that is maximizing profit and indicate each of the following.i. Price

ii. Quantity of outputiii. Profit

b. describe and explain the relationship between the monopolist’s demand curve and marginal revenue curve.c. Label each of the following on your graph in part a

i. Consumer surplusii. Deadweight loss

3. Assume that Company XYZ is a profit-maximizing firm that hires its labor in a perfectly competitive labor market and sells itsproduct in a perfectly competitive output market.

a. Define the marginal revenue product of labor (MRPl).b. Using correctly labeled side-by-side graphs, show each of the following.

i. The equilibrium wage in the labor marketii. The labor supply curve the firm faces

iii. The number of workers the firm will hirec. Company XYZ develops a new technology that increases its labor productivity. Currently this technology is not

available to any other firm. For Company XYZ, explain how the increased productivity will affect each of thefollowing.

i. Wage ratesii. Number of workers hired

Scoring guidelines and answers

1. 12 pts:a. 4 pts.: 1 – market graph w/ downward-sloping D curve and an upward-sloping S curve; 1 – correctly labeling

equilibrium P and Q for market; 1 – for the firm graph (horizontal D or P curve); 1 – applying MR = MC to findequilibrium quantity (MR must be logically consistent with demand curve)

The market graph should have a downward-sloping demand curve and an upward-sloping supply curve with an equilibriumprice and quantity clearly labeled. The firm graph should have a perfectly elastic (horizontal) demand curve at the

equilibrium market price. The firm’s profit-maximizing quantity is found at the intersection of this demand or marginalrevenue curve with the firm’s marginal cost curve.

b. 1 pt.: showing the area of economic profit (above) for the firm (must use P, ATC, and q); The firm’s profits arerepresented by the rectangle that has a height or (vertical distance) of P – ATC multiplied by the firm’s profit-maximizing output or q.

c. 4 pts.:i. 2 pts.: 1 – showing an increase in supply on market graph (resulting from entry of new firms); 1 –

showing both a lower P and a higher Q due to an increase in supplyii. 2 pts.: 1 – downward shift in the firm’s demand curve (P or MR or D); 1 – for q (for firm) where P = min

ATC for firm

With profits being earned, new firms will enter the smoke alarm market. The market supply will increase(shift to the right) and the equilibrium price will fall and quantity will increase. As the market price falls, thefirm has a downward shift in its horizontal demand curve. The process continues until price of output hasfallen to the minimum of the average total cost of the firm.

d. 2 pts: 1 – showing that Qs > Qm; 1 – having 2 marginal benefit curves: one with and one without the positiveexternality

With a positive consumption externality in the market for smoke alarms, the demand curve with marginal social benefitsshould lie above the demand curve with only marginal private benefits. Thus, the socially optimal output level will exceedthe output level produced by an unregulated private market.

e. 1 pt. for any of the following: subsidize sellers or buyers, mandatory smoke alarm system, or tax relief; To increase themarket output to the socially optimal output, the government could subsidize the consumption or production of smokealarms.

2. 7 pts.a. 4 pts.: 1 – correctly labeled graph w/ downward-sloping D curve and marginal revenue curve below demand; 1 –

indicating Q at MR = MC; 1 – finding the appropriate P on the demand curve directly above MR = MC output; 1 ---area of profit (must use P, ATC, and Q)

For the monopolist, a correctly labeled graph should show a downward-sloping demand curve with a marginal revenuecurve that lies below the demand curve. The monopolist’s profit-maximizing output is found at the intersection of marginalrevenue and marginal cost. The price is found on the demand curve, above the quantity produced. The firm’s profits arerepresented by the rectangle that has a height (or vertical distance) of P – ATC multiplied by the profit-maximizing output orQ.

b. 1 pt. – the monopolist must lower its price on all units to sell additional quantities so MR < P; Marginal revenue is lessthan price since to sell additional units of output, the monopolist must lower price on all units of output sold.

c. 2 pts.: 1 – indicating correct area for consumer surplus; 1 – correct area for deadweight loss; Consumer surplus is thearea bounded vertically by the difference between the demand curve (willingness to pay) and monopolist’s price overthe number of units sold by the monopolist. The deadweight loss from monopoly is the combination of consumer andproducer surplus that is lost when comparing the monopoly output to the output that would be produced undercompetitive conditions (where P – MC).

3. 7 pts.a. 1 pt. – definition: the additional revenue from hiring an additional worker or MRP = MP x MR or MRP = MP x P; The

marginal revenue product of labor is the change in total revenue associated with the change in output following a unitchange in the employment of labor; MRP of labor = MR (or P of output) x MPP of labor

b. 4 pts.: 1 – correctly labeled labor market graph showing equilibrium wage; 1 – firm graph indicating downward-slopingdemand (MRPl) curve; 1 – horizontal labor supply curve for the firm; 1 – showing quantity of labor for the firm at theintersection of labor supply and labor demand

The perfectly competitive labor market will have a downward-sloping labor demand curve and an upward-sloping laborsupply curve. There will be an equilibrium wage and quantity of labor. The firm will be a wage taker and have a perfectlyelastic labor supply at the market wage rate. The firm’s labor demand curve is its marginal revenue product of labor curve.Thus, the profit-maximizing firm will hire the amount of labor associated with the intersection of its marginal revenueproduct of labor curve and its horizontal labor supply curve. The firm will pay each unit of labor the market wage.

c. 2 pts.: 1 – wage rate for the firm remains constant at the original wage.; 1 – the number of workers hired by XYZincreases b/c XYZ’s MRP increases or labor demand curve shifts to the right.; With an increase in labor productivitythat affects only Company XYZ there will be no perceptible change in labor market. The equilibrium wage stays thesame. Company XYZ will have an outward shift in its marginal revenue product of labor (or labor demand) curve,leading to more employment at the unchanged market wage.

20023.The table below shows total utility in utils that a utility-maximizing consumer receives from consuming two goods: apples andoranges.

Apples OrangesQuantity Total utility Quantity Total Utility0 0 0 01 20 1 302 35 2 503 45 3 654 50 4 755 52 5 80

Assume that apples cost $1 each, oranges cost $2 each, and the consumer spends the entire income of $7 on apples and oranges.a. Using the concept of marginal utility per dollar spent, identify the combination of apples and oranges the consumer will

purchase. Explain your reasoning.b. With the prices of apples and oranges remaining constant, assume that the consumer’s income increases to $12.

Identify each of the following.i. The combination of apples and oranges the consumer will now purchase.

ii. The total utility the consumer will receive from consuming the combination in (i)c. with income remaining at $12, assume the price of oranges increases to $4 each. Identify each of the following.

i. The combination of apples and oranges the consumer will now purchase.ii. The total utility the consumer will receive from consuming the combination in (i)

Scoring and answer3 6 pts.

a. 2 pts.: 1 – 3 apples and 2 oranges; 1 --marginal analysis: equalization of MU/$ or 10/1 (apples) = 20/2(oranges); student may not simply use the maximizing of total utility for the explanation.; The utility-maximizing consumer will exhaust her income, purchasing quantities of each good such that for eachcommodity the marginal utility of the last unit purchased divided by the price of the commodity is equal. Thisconsumer will purchase 3 apples and 2 oranges. The marginal utility per dollar of each commodity is equal:10/$1 for apples and 20/$2 for oranges. (Marginal utility of 2nd orange = 20 divided by price of $2; marginalutility of 3rd apple is 10 divided by price of $1)

b. 2 pts.: 1 – 4 apples and 4 oranges; 1 – 50 + 75 = 125 utils; With the increase in income, the consumer will nowpurchase 4 apples and oranges and have 125 utils (50 from apples and 75 from oranges)

c. 2 pts.: 1 – 4 apples and 2 oranges; 1 – 50 + 50 = 100 utils: With the increase in the price of oranges, theconsumer will now purchase 4 apples and 2 oranges and have 100 utils (50 from apples and 50 from oranges)

2002 Form B

1. Assume that two firms are operating with identical cost schedules, but one firm is in a perfectly competitive industry,and the other is in a monopolistically competitive industry.

a. Using two correctly labeled graphs, show the long-run equilibrium price and output levels for each of thesetwo firms.

b. Compare the long-run equilibrium price and output levels for these two firms.

c. What level of economic profit will each firm earn in the long run? Why do these results occur?d. For each of the two firms at the equilibrium quantity, indicate whether the firm’s demand curve is perfectly

elastic, elastic, unit elastic, inelastic, or perfectly inelastic. How can you tell?

Scoring and answers

15 pointsa. 6 pts.: 1 each – two graphs with appropriate cost curves; 1 each – Q indicated for each firm where MR = MC;

1 each – P for each firm read off the correct D curve at correct Q; see graphs above. The long-run equilibriumprice and quantity are labeled Pm and Qm, for the monopolistically competitive firm and Pc and Qc for theperfectly competitive firm.

b. 2 pts.: 1 – P in perfect competition is lower than P in monopolistic competition; 1 – Q in perfect competition issmaller than Q in monopolistic competition; The perfectly competitive firm has a lower price and a largerquantity of output than the monopolistically competitive firm.

c. 3 pts.: 1 – firm in perfect competition earns zero economic profit; 1 – firm in monopolistic competition earnszero economic profit; 1 – entry of new firms increases industry output, individual firm’s output decreases,prices will fall to level of ATC; Each of these firms will earn zero economic profits in the long run. With nobarriers to entry, the existence of positive economic profits or economic losses motivates the entry or exit offirms in and out of the industry, forcing prices to the level of average costs.

d. 4 pts.: 1 – for perfectly competitive firm, D is perfectly elastic; 1 – b/c P is constant, the % change in P is 0; 1– for the monopolistically competitive firm, demand is elastic; MR is positive in the elastic portion of the Dcurve; Demand is perfectly elastic for the perfectly competitive firm because price is constant, making thepercentage change in price zero for any change in quantity. For the monopolistically competitive firm, demandis elastic because MR is positive at Qm.

20011. a. Assume that a profit-maximizing firm in a perfectly competitive industry is earning economic profits. For a given market

price, draw a correctly labeled graph and show each of the following for a typical firm in this perfectly competitive industry.i. Marginal revenue

ii. Outputiii. Economic profits

b. using the information given in (a), draw correctly labeled side-by-side graphs for the industry and a typical firm.i. Given the existence of economic profits of the typical firm, show on the graphs how the industry adjusts in the

long run and explain the process that leads to the long-run equilibrium.ii. Show on the graphs each of the following for the industry and for the typical firm in long-run equilibrium:

price, output

c. Now assume that the government sets a price that is less than the equilibrium price but greater than average variable cost.Indicate how each of the following will change for the typical firm and explain why the change occurs.

i. Marginal revenueii. Level of output

iii. Short-run total costiv. Short-run total revenue

3. Sparkle Car Wash is a profit-maximizing firm with the following production information.Number of workers Number of Cars Washed Per Day

0 01 152 35

3 604 755 856 80

a. With which worker is marginal product maximized?b. Identify and define the economic principle that explains why marginal product eventually decreases.c. Explain why Sparkle would never hire the sixth worker.d. If Sparkle charges $6 for washing a car, what is the maximum daily wage that Sparkle would be willing to pay the

fourth worker?

Scoring and answers1. The firm has a perfectly elastic (horizontal) marginal revenue curve that is equal to the market price. The firm produces the

output level where marginal revenue equals marginal cost. The economic profit of the firm is the area bounded by the quantityproduced multiplied by the difference between price and average total cost ( P – ATC) at that output level.With economic profits, new firms will enter the industry. The market supply will shift outward with the entry of firms, andmarket price will fall. The process continues until a long-run equilibrium is established. At this equilibrium, the market price isequal to the minimum of the long-run average cost of the typical firm. Each firm produces where P=MR=MC, which is the levelof output that corresponds to the minimum of the long-run average cost. The firm makes zero economic profits.A price control below the long-run equilibrium price but above the firm’s average variable cost will result in short-runproduction. Since the price has fallen, the firm’s marginal revenue falls. The firm’s output level, where MR = MC, will alsodecrease. Since the firm is producing less output, total cost falls. Since both the firm’s price and quantity have fallen, totalrevenue falls.

a. 3 pts: 1 – a horizontal MR curve; 1 – show and indicate that output should be where MR = MC; 1 – show the areaof profit as the rectangle whose width is the distance between 0 and the equilibrium quantity and whose height isthe distance between the P(AR) and ATC at that quantity.

b. 5 pts. total:i. 3 pts.: 1 – showing correctly side-by-side graphs of the firm and the market, both correctly labeled; 1 –

showing a market supply curve shifting out and a market price decreasing with this price being used in thefirm graph; 1 – explaining that w/ economic profits, more firms enter the market

ii. 2 pts.: 1 – showing the industry equilibrium price and quantity. Students can either use a vertical linefrom the x axis to the equilibrium pt. and one from the equilibrium pt. to the y axis (labeling each) or elsethey can mark the equilibrium pt. w/ a letter and somehow indicate that that pt. represents the equilibrium;1 – showing the long-run equilibrium price and quantity for the firm at the minimum ATC, indicating itvia either of the methods discussed above

c. 4 pts.:i. 1 – indicating that MR has fallen b/c P has been lowered

ii. 1 – indicate that output has fallen b/c MR = MC is at a lower qiii. 1 – indicating that total costs fell b/c output felliv. 1 – indicating that price AND quantity fell

2.3. Worker #3 has the highest marginal product (60 – 35 = 25 cars washed). With additional workers the marginal product falls.

This is consistent with the Law of Diminishing Returns. That law states that as more units of a variable input (labor) areemployed with a fixed input, output will eventually increase at a decreasing rate. The sixth worker would never be hired sincethe marginal product of that worker is negative (80 – 85 = -5 cars). A firm would never hire a unit of an input that reduces totaloutput. The firm would be willing to pay the fourth worker as much as its marginal revenue product or $90 per day found bymultiplying the price of a car wash by the number of cars washed by the fourth worker ($6 x 15 cars = $90 per day). 5 pointstotal

a. 1 – 3rd workerb. 1 – diminishing marginal returns; 1 – definition of diminishing marginal returns that includes both variable and

fixed inputsc. 1 – negative marginal product for 6th workerd. 1 -- $90