asia pacific healthcare outlook focus : australia analysis of best opportunities 24 th february 2010

TRANSCRIPT

Asia Pacific Healthcare OutlookFocus : Australia

Analysis of Best Opportunities

24th February 2010

2

1. Overview of Healthcare Market: Key Takeaways

2. In-depth Sectoral Analysis, APAC and Australia

3. Summary: Best Opportunity Analysis, Australia

Agenda

3

Global Healthcare Market: 2009

• US and Europe were impacted in a major way by global crisis

• Asia also slowed down but not as much as the West

• Valuations were low and M&A was high, many smaller Biotech companies struggled

• Major organizational restructuring occurred, along with portfolios being reassessed

• Recovery of the markets to a large extent with strong growth in Asia

• Start of major patent expiries

• M&A activity down in the West but could be important in Asia, restructuring will continue

• Asia becoming increasingly important as a market and outsourcing hub

• 5Ps to drive market: Preventive, Preemptive, Personalized, Predictive, Personal Responsibility

Global Healthcare Market: 2010-12

Setting the Scene Outlook for Healthcare Industry from 2010-12

Source: Frost & Sullivan

4

23.9%23.9%

27.2%27.2%

23.2%23.2%

26.4%26.4%

CAGR12.2%CAGR12.2%

CAGR6.5%

CAGR6.5%

Global & APAC Healthcare Revenues US$ Bn, 2009-2012

• By 2015 APAC could represent ~40% of global market!Source: Frost & Sullivan

Rest of the World

APAC

Global vs. Apac: The New Frontier By 2012 APAC expected to be close to 27% of global market

5

Asia Pacific Market : 2009

• Slowing down of GDP in mature markets – Japan took a big hit

• Global consolidation left a difficult mess for integration on a local level – job losses and portfolio realignment

• Price cutting and playing the margins game

• The bubble burst for Medical Tourism

• Asia started to set up infrastructure for offshoring and outsourcing for US/EU companies

Asia Pacific Market : 2012

• A shift in the center of the world economically and strategically to Asia

• Asia to move from export led development to consumption led growth

• APAC the fastest growing pharma market and API production hub

• Increased government attention to primary and community based healthcare.

• Increased use of mobile technology in healthcare service delivery

Asia is However Transitionaing Moving toward a Multi–Polar World Order

Source: Frost & Sullivan

6

Australian Healthcare MarketBy 2012, Australia is estimated to be almost 5% of the APAC market

Australian Healthcare Revenues, US$ Bn, 2009-2012

Source: Frost & Sullivan

7

1. Overview of Healthcare Market: Key Takeaways

2. In-depth Sectoral Analysis, APAC and Australia

3. Summary: Best Opportunity Analysis, Australia

Agenda

8

Unresolved political and regulations issues Quality concern of generics & counterfeits

Government tenders favour local manufacturers

24.6% 28.5%

APAC Pharmaceuticals MarketEarlier diagnosis improves disease management and length of therapy

Note: All figures are rounded; the base year is 2009. Source: Frost and SullivanNote: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

Market Drivers

Market Restraints

Long term use of multiple and specialized drugs for the ageing population

Government support for generics and biosimilars

Enhanced diagnosis and management in oncology, cardiovascular, pain etc

CAGR6.6 %

CAGR6.6 %

CAGR12.9 %CAGR12.9 %

Pharma Revenues, US$ Bn, 2009-2012

APAC Share

750825 866 909

9

Saturated market with low unmet needs

Government attempts to restrain PBS expenditure & BPS reforms

• Growing demand for lifestyle diseases drugs in an aging population e.g. cancer, cardiovascular, diabetes

• Uptake of new, expensive drugs

• Strong government support for generics

Australia Pharmaceuticals MarketMature market driven by lifestyle diseases

Pharmaceuticals Revenues, US$ Bn, 2009-2012

Market Drivers

Market Restraints

Source: Frost & Sullivan

10

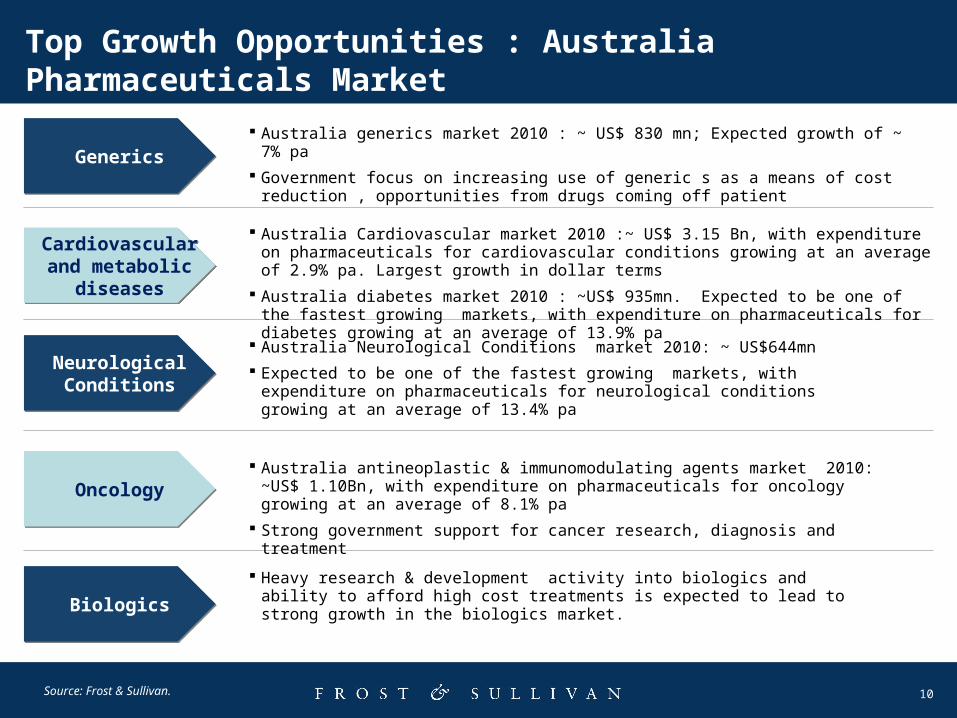

Australia Cardiovascular market 2010 :~ US$ 3.15 Bn, with expenditure on pharmaceuticals for cardiovascular conditions growing at an average of 2.9% pa. Largest growth in dollar terms

Australia diabetes market 2010 : ~US$ 935mn. Expected to be one of the fastest growing markets, with expenditure on pharmaceuticals for diabetes growing at an average of 13.9% pa

0

0

Source: Frost & Sullivan.

GenericsGenerics

Cardiovascular and metabolic

diseases

Cardiovascular and metabolic

diseases

Neurological Conditions

Neurological Conditions

OncologyOncology

Australia Neurological Conditions market 2010: ~ US$644mn

Expected to be one of the fastest growing markets, with expenditure on pharmaceuticals for neurological conditions growing at an average of 13.4% pa

Top Growth Opportunities : Australia Pharmaceuticals Market

Australia generics market 2010 : ~ US$ 830 mn; Expected growth of ~ 7% pa

Government focus on increasing use of generic s as a means of cost reduction , opportunities from drugs coming off patient

Australia antineoplastic & immunomodulating agents market 2010: ~US$ 1.10Bn, with expenditure on pharmaceuticals for oncology growing at an average of 8.1% pa

Strong government support for cancer research, diagnosis and treatment

BiologicsBiologics

Heavy research & development activity into biologics and ability to afford high cost treatments is expected to lead to strong growth in the biologics market.

11

•Regulatory and reimbursement hurdles

•Lack of sufficient distribution networks

•Inadequate training/certification for allied staff

APAC Medical Devices MarketTransition to a mindset of monitoring

23.8%23.8%

25.8%25.8%

Market Drivers

Market Restraints

•Safety, accuracy, efficiency, cost

•Silver industry devices

•Convergence of devices and pharma products

Medical Devices Revenues, US$ Bn, 2009-2012

APAC Share

CAGR5.8%

CAGR5.8%

CAGR10.2%CAGR10.2%

Note: All figures are rounded; the base year is 2009. Source: Frost and SullivanNote: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

12

Medical Devices Revenues, US$ Bn, 2009-2012

Government’s commitment to reduce elective surgery waiting time

Increasing number of joint replacement procedures due to ageing population

Expansion of private health insurance results in demand for better medical care

Market Drivers

Increased medical device safety concerns could slow device approval cycle

Development of new technologies will replace conventional treatment methods.

Market Restraints

Australian Medical Devices MarketDemand for better quality of healthcare driving growth

Note: All figures are rounded; the base year is 2009. Source: Frost and SullivanNote: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

13

High cost of genomics and proteomics tests

Mutually exclusive target customers

Reimbursement issues

APAC Clinical Diagnostics Market Shift in business model from instrumentation to service revenues

17.8%17.8%

18.5%18.5%

Market Drivers

Market Restraints

Lab automation

Home care monitoring

Emphasis on early detection

Clinical Diagnostics Revenues, US$ Bn, 2009-2012

APAC Share

CAGR7.3%

CAGR7.3%

CAGR6%

CAGR6%

Note: All figures are rounded; the base year is 2009. Source: Frost and SullivanNote: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

14

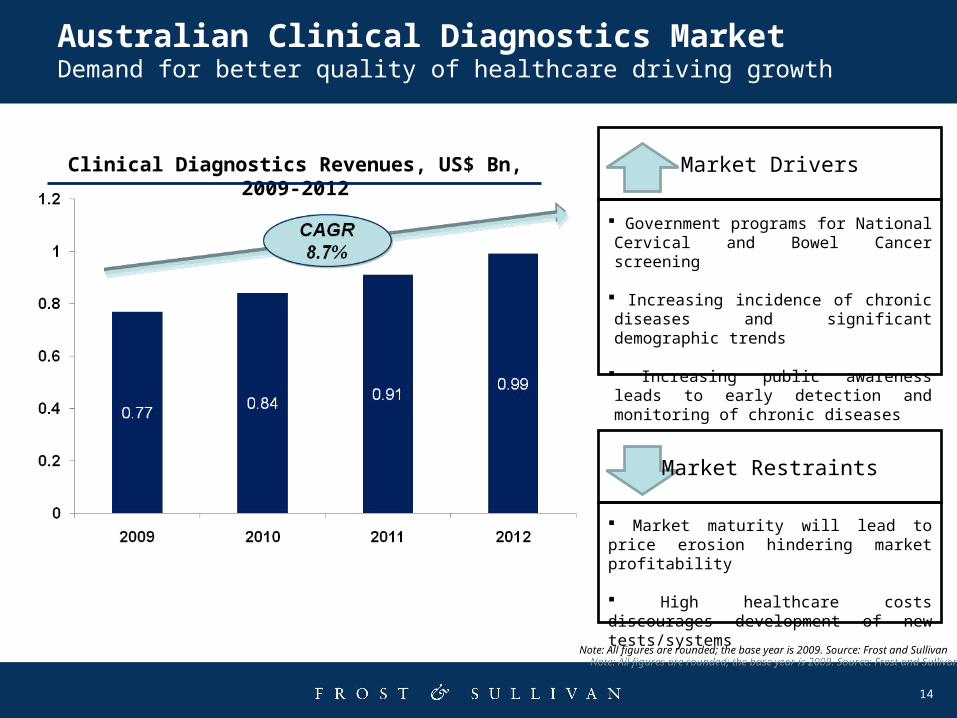

Clinical Diagnostics Revenues, US$ Bn, 2009-2012

Government programs for National Cervical and Bowel Cancer screening

Increasing incidence of chronic diseases and significant demographic trends

Increasing public awareness leads to early detection and monitoring of chronic diseases

Market Drivers

Market maturity will lead to price erosion hindering market profitability

High healthcare costs discourages development of new tests/systems

Market Restraints

Australian Clinical Diagnostics MarketDemand for better quality of healthcare driving growth

Note: All figures are rounded; the base year is 2009. Source: Frost and SullivanNote: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

15

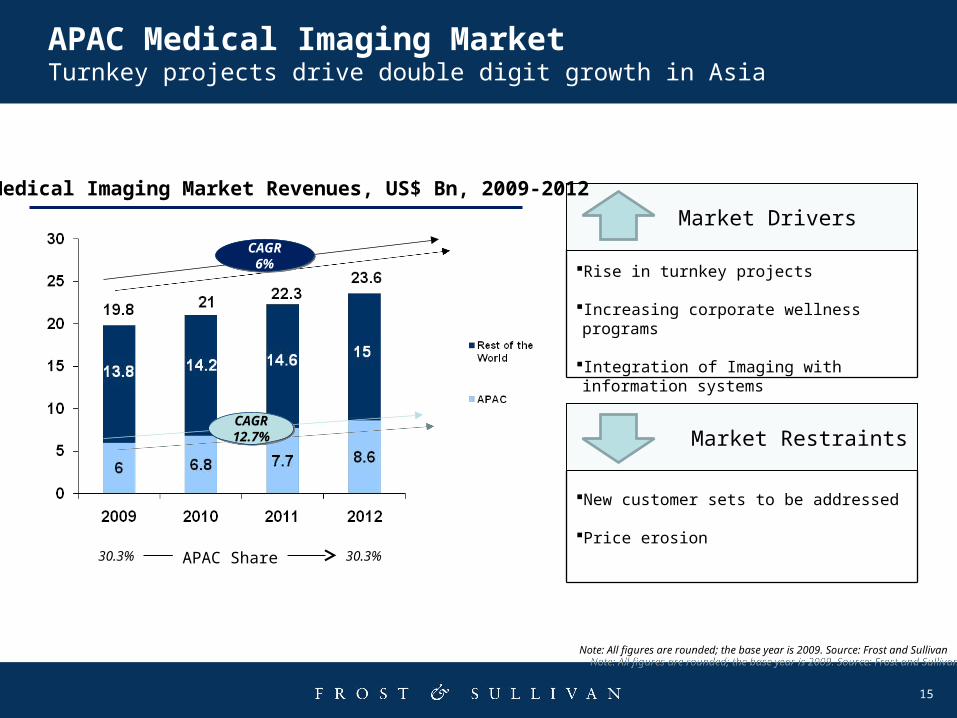

APAC Medical Imaging MarketTurnkey projects drive double digit growth in Asia

Market Drivers

Market Restraints

Rise in turnkey projects

Increasing corporate wellness programs

Integration of Imaging with information systems

New customer sets to be addressed

Price erosion

CAGR6%

CAGR6%

CAGR12.7%CAGR12.7%

Medical Imaging Market Revenues, US$ Bn, 2009-2012

Note: All figures are rounded; the base year is 2009. Source: Frost and SullivanNote: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

APAC Share30.3% 30.3%

16

Medical Imaging Revenues, US$ Bn, 2009-2012

Increase in patient demand

Increase in the number of Medicare funded diagnostic imaging services

Increasing competition in the diagnostic imaging services sector

Government initiatives such as BreastScreen

Market Drivers

Market saturation due to high penetration of medical imaging modalities

Increasing pricing pressure

Market Restraints

Australian Medical Imaging MarketDigital imaging to drive growth

Note: All figures are rounded; the base year is 2009. Source: Frost and SullivanNote: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

17

PACSPACS

Australian PACS market in 2010: ~US$ 49 million; CAGR: 9.0%

Focus by healthcare providers to integrate imaging with IT and integrate PACS with

the hospital information system to improve efficiency and quality of healthcare

Increasing demand for cardiology PACS and orthopedics PACS solutions outside the

radiology department

Top Growth Opportunities

CR/DR CR/DR

Australian CR/DR market in 2010: ~US$ 66 million ; CAGR: 10.0%

Teleradiology - Shortages of radiologists require better information sharing and the

need to share and transfer reports and images

Increase in the number of diagnostic imaging procedures. Around 15 million diagnostic

imaging procedures performed in Australia. Around 3 million procedures performed in

the public hospitals.

Note: All figures are rounded; the base year is 2009. Source: Frost and SullivanNote: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

18

Top Growth Opportunities

Note: All figures are rounded; the base year is 2009. Source: Frost and SullivanNote: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

SMBGSMBG

Australian self monitoring of blood glucose (SMBG) devices market in 2010: ~US$ 150

million; CAGR: 6.0

Increasing public awareness about diabetes and the need for glucose monitoring

Strong government support in form of initiatives such as National Diabetes Services

Scheme

The total number of diabetic patients registered with NDSS has increased to 897, 867

at a CAGR of 9.8% in the period 2002-2008

Minimally Invasive Surgery

Minimally Invasive Surgery

Increase in day surgery procedures - In 2009, around 57% of total patient separations

in hospitals were same day separations.

Number of day procedures in 2009: ~4.8 million; CAGR: 4.5%

Gastrointestinal endoscopy (around 0.64 million), Arthroscopy (0.14 million) are among

the top 5 high volume procedures in Australia

Technological advancement, benefits to hospitals (economic savings) and patient

benefits (shorter stay in hospital, reduction in risk of acquiring hospital infections)

19

Interoperability

Integration

Lack of skilled resources

*Life Sciences & Healthcare IT includes: Software, Hardware, IT services

Asia Pacific Lifesciences and Health IT MarketInteroperability challenges hinder adoption

14.5%14.5%

15.7%15.7%

Market Drivers

Market Restraints

Operational efficiency Strong and sustained demand for healthcare services

Consumer demand for quality and access to information

Lifesciences & Healthcare IT, US$ Bn, 2009-2012

CAGR7%

CAGR7%

CAGR11.3%CAGR11.3%

APAC Share

50.654.6

58.4 62.5

Note: All figures are rounded; the base year is 2009. Source: Frost and SullivanNote: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

20

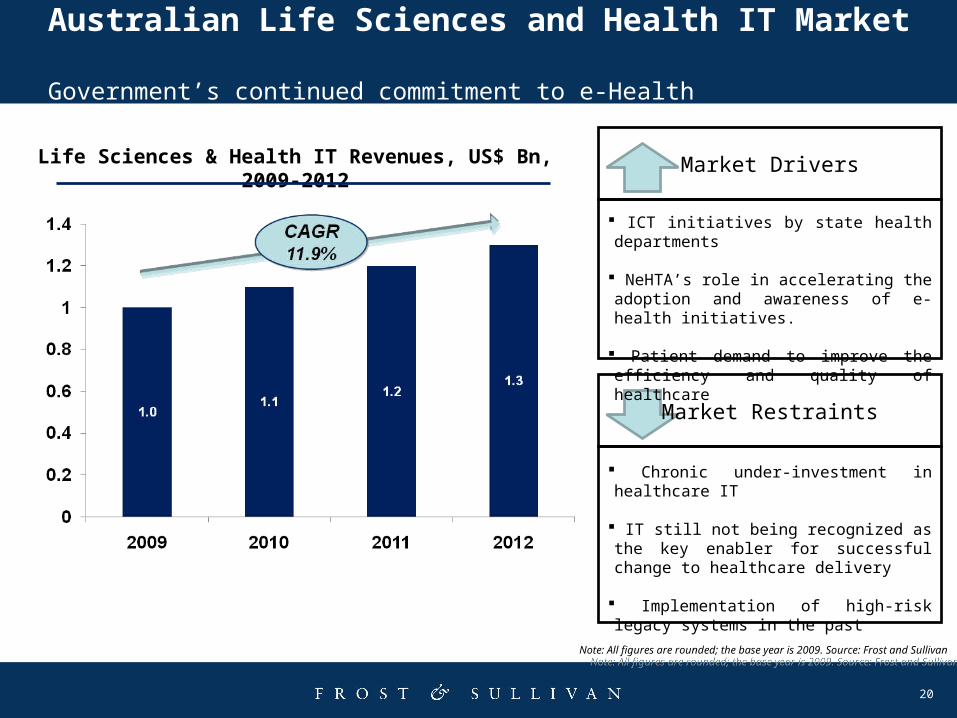

Australian Life Sciences and Health IT Market Government’s continued commitment to e-Health

Life Sciences & Health IT Revenues, US$ Bn, 2009-2012

ICT initiatives by state health departments

NeHTA’s role in accelerating the adoption and awareness of e-health initiatives.

Patient demand to improve the efficiency and quality of healthcare

Market Drivers

Chronic under-investment in healthcare IT

IT still not being recognized as the key enabler for successful change to healthcare delivery

Implementation of high-risk legacy systems in the past

Market Restraints

Note: All figures are rounded; the base year is 2009. Source: Frost and SullivanNote: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

21

0

0

0

Clinical IT SystemsClinical IT Systems

Spending on departmental systems (radiology, cardiology, pharmacy, acute care, etc,) 2010: ~US$ 160 mn; CAGR: 15.3%

Modernization of the healthcare system, implementation of more accurate and reliable systems and shift from lengthy to short and more clinically intense hospital stays is driving investment in departmental systems.

Spending on infrastructure, interoperability and EHR solutions: ~US$ 45mn; CAGR: ~17.3%

State eHealth programs such as Healthelink (NSW Health) and government’s commitment to development of the right technology necessary to deliver the best e-health system is accelerating the growth in this segment.

Top Opportunities – Australian Life Sciences and Health IT Market

Solutions for Patient and Revenue Cycle

Management

Solutions for Patient and Revenue Cycle

Management

Spending on patient and revenue cycle management solutions 2010: ~US$ 104 mn; CAGR: 6.1%

The steps taken by healthcare facilities to improve the quality and outcome of healthcare, reduce the administrative burden, and adopt a more standardized approach towards application of information systems is the key driver for this market segment.

Patient administration solutions being adopted in public hospitals in South Australia (careconnect.sa), Western Australia (eHealthWA) and Victoria (HealthSMART).

Note: All figures are rounded; the base year is 2009. Source: Frost and SullivanNote: All figures are rounded; the base year is 2009. Source: Frost and Sullivan

22

1. Overview of Healthcare Market : Key Takeaways

2. In-depth Sectoral Analysis, APAC and Australia

3. Summary: Best Opportunity Analysis, Australia

Agenda

23

Time

Gro

wth Home-based

care

Personalized medicine

POCT/Self Monitoring

Clinical IT

Endoscopy

Administrative IT

EMR/EHR

INNOVATIONTRIGGER

SUPERGROWTH

NORMALISATION LEADERSHIP

Source: Frost & Sullivan.

Where to place your bets in 2010- 2012 : Australia

Biologics

Joint replacement

Oncology, Diabetes

Cardiovascular

Thank You