asia insurance (philippines) corporation statement.pdfasia insurance (philippines) corporation...

TRANSCRIPT

Asia Insurance(Philippines)CorporationFinancial StatementsAs at and for the years ended December 31, 2012 and 2011

Asia Insurance (Philippines) Corporation

Statements of Financial PositionDecember 31, 2012 and 2011

(All amounts in Philippine Peso)

Notes 2012 2011

A S S E T S

CASH AND CASH EQUIVALENTS 6 243,862,773 352,117,028

RECEIVABLES, net 7 215,821,345 159,834,675

AVAILABLE-FOR-SALE SECURITIES 8 92,231,585 91,079,476

HELD-TO-MATURITY SECURITIES 8 382,623,710 225,595,876

REINSURANCE RECOVERABLE ON UNPAID LOSSES 9 361,832,955 411,023,340

DEFERRED REINSURANCE PREMIUMS 9 87,977,043 74,734,336

DEFERRED ACQUISITION COSTS, net 9 84,849,495 61,940,595

INVESTMENT PROPERTY, net 10 28,862,371 30,617,981

PROPERTY AND EQUIPMENT, net 11 15,634,660 12,966,262

DEFERRED INCOME TAX ASSETS, net 12 17,364,947 15,145,999

OTHER ASSETS 9,492,465 8,869,155Total assets 1,540,553,349 1,443,924,723

LIABILITIES AND EQUITY

LOSSES AND CLAIMS PAYABLE 9 462,630,931 500,360,754

RESERVE FOR UNEARNED PREMIUMS 9 188,973,910 159,658,774

DUE TO REINSURERS AND CEDING COMPANIES 20 121,981,621 60,106,616

FUNDS HELD FOR REINSURERS 20 27,026,004 34,131,914

COMMISSIONS PAYABLE 34,362,509 23,130,504

ACCOUNTS PAYABLE AND OTHER LIABILITIES 13 60,783,097 49,235,190Total liabilities 895,758,072 826,623,752

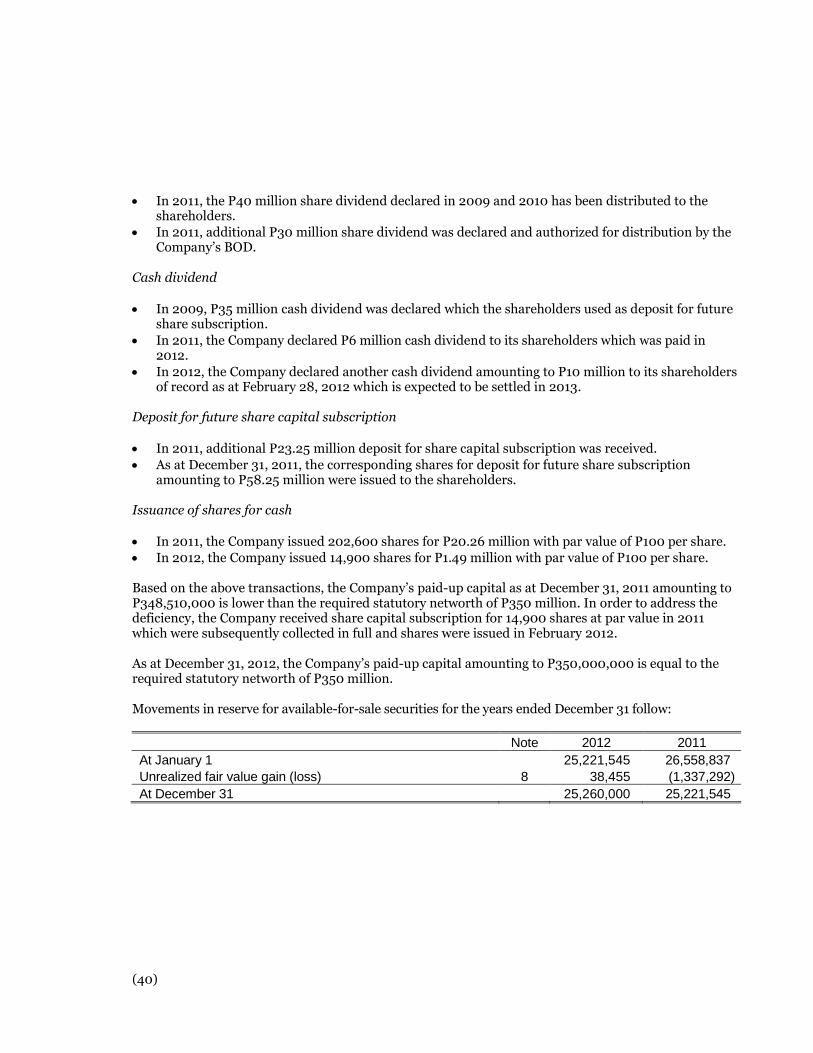

SHARE CAPITAL 14 350,000,000 348,510,000

CONTRIBUTED SURPLUS 14 500,000 500,000

FAIR VALUE RESERVE ON AVAILABLE-FOR-SALESECURITIES 25,260,000 25,221,545

RETAINED EARNINGS 269,035,277 243,069,426Total equity 644,795,277 617,300,971Total liabilities and equity 1,540,553,349 1,443,924,723

(The notes on pages 1 to 52 are an integral part of these financial statements)

Asia Insurance (Philippines) Corporation

Statements of Total Comprehensive IncomeFor the years ended December 31, 2012 and 2011

(All amounts in Philippine Peso)

Notes 2012 2011UNDERWRITING INCOME

Premiums written, net of returns 473,629,315 423,741,378Reinsurance premiums ceded 20 (201,973,903) (192,267,087)Premiums retained 271,655,412 231,474,291Increase in reserve for unearned premiums, net 9 (16,072,428) (4,705,502)Premiums earned 255,582,984 226,768,789Commissions earned 20 48,715,412 51,185,319Other underwriting income 1,945,784 2,811,070

GROSS UNDERWRITING INCOME 306,244,180 280,765,178UNDERWRITING EXPENSES

Commissions and other underwriting expenses 9,20 119,368,402 115,294,015Losses and claims, net 9,20 112,957,481 95,468,673

232,325,883 210,762,688NET UNDERWRITING INCOME 73,918,297 70,002,490INVESTMENT AND OTHER INCOME (EXPENSES)

Interest income 15 31,458,647 25,587,917Rent 10 4,005,022 3,866,381Gain on sale of investments 2,942,069 -Dividend 8 1,865,806 1,132,441Foreign exchange loss, net 4 (19,758,574) (78,270)Miscellaneous 2,712,429 573,756

23,225,399 31,082,225NET UNDERWRITING AND INVESTMENT INCOME 97,143,696 101,084,715GENERAL AND ADMINISTRATIVE EXPENSES

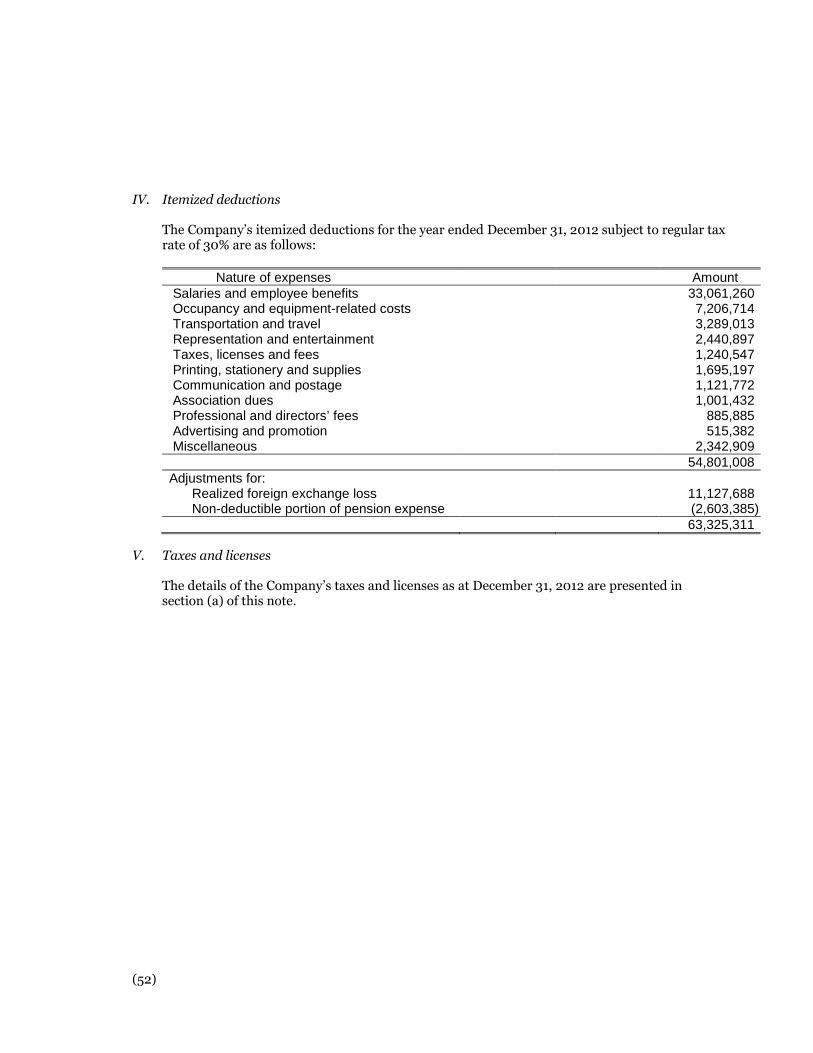

Salaries and employee benefits 16 33,061,260 31,083,473Occupancy and equipment-related costs 7,206,714 7,087,070Transportation and travel 3,289,013 3,088,094Representation and entertainment 2,440,897 4,241,074Printing, stationery and supplies 1,695,197 1,373,853Taxes, licenses and fees 1,240,547 1,615,910Communication and postage 1,121,772 1,115,225Association dues 1,001,432 892,910Professional and directors’ fees 20 885,885 855,750Advertising and promotion 515,382 503,510Miscellaneous 2,342,909 2,348,441

54,801,008 54,205,310INCOME BEFORE INCOME TAX 42,342,688 46,879,405PROVISION FOR INCOME TAX 12,18 (6,376,837) (9,733,260)NET INCOME FOR THE YEAR 35,965,851 37,146,145

OTHER COMPREHENSIVE INCOMENet change in fair value of available-for-sale securities 38,455 (1,337,292)

TOTAL COMPREHENSIVE INCOME FOR THEYEAR 36,004,306 35,808,853

(The notes on pages 1 to 52 are an integral part of these financial statements)

Asia Insurance (Philippines) Corporation

Statements of Changes in EquityFor the years ended December 31, 2012 and 2011

(All amounts in Philippine Peso)

Sharecapital

(Note 14)

Contributedsurplus

(Note 14)

Deposit for futureshare capitalsubscription

(Note 14)

Fair value reserveon available-for-sale securities

(Note 14)

Retained earnings(Notes 14)

Total equityAppropriated UnappropriatedBalances at January 1, 2011 200,000,000 500,000 35,000,000 26,558,837 40,000,000 241,923,281 543,982,118Comprehensive income

Net income for the year - - - - - 37,146,145 37,146,145Other comprehensive income

Changes in fair value ofavailable-for-sale investments - - - (1,337,292) - - (1,337,292)

Total comprehensive income for the year - - - (1,337,292) - 37,146,145 35,808,853Transactions with owners

Cash dividend - - - - - (6,000,000) (6,000,000)Share dividend 70,000,000 - - - (40,000,000) (30,000,000) -Issuance of shares for cash 20,260,000 - - - - - 20,260,000Deposit for future share capital subscription - - 23,250,000 - - - 23,250,000Issuance of shares from deposit for future

share subscription 58,250,000 - (58,250,000) - - - -Total transactions with owners 148,510,000 - (35,000,000) - (40,000,000) (36,000,000) 37,510,000Balances at December 31, 2011 348,510,000 500,000 - 25,221,545 - 243,069,426 617,300,971Comprehensive income

Net income for the year - - - - - 35,965,851 35,965,851Other comprehensive income

Changes in fair value ofavailable-for-sale investments - - - 38,455 - - 38,455

Total comprehensive income for the year - - - 38,455 - 35,965,851 36,004,306Transactions with owners

Cash dividend - - - - - (10,000,000) (10,000,000)Issuance of shares for cash 1,490,000 - - - - - 1,490,000

Total transactions with owners 1,490,000 - - - - (10,000,000) (8,510,000)

Balances at December 31, 2012 350,000,000 500,000 - 25,260,000 - 269,035,277 644,795,277

(The notes on pages 1 to 52 are an integral part of these financial statements)

Asia Insurance (Philippines) Corporation

Statements of Cash FlowsFor the years ended December 31, 2012 and 2011

(All amounts in Philippine Peso)

Notes 2012 2011CASH FLOWS FROM OPERATING ACTIVITIES

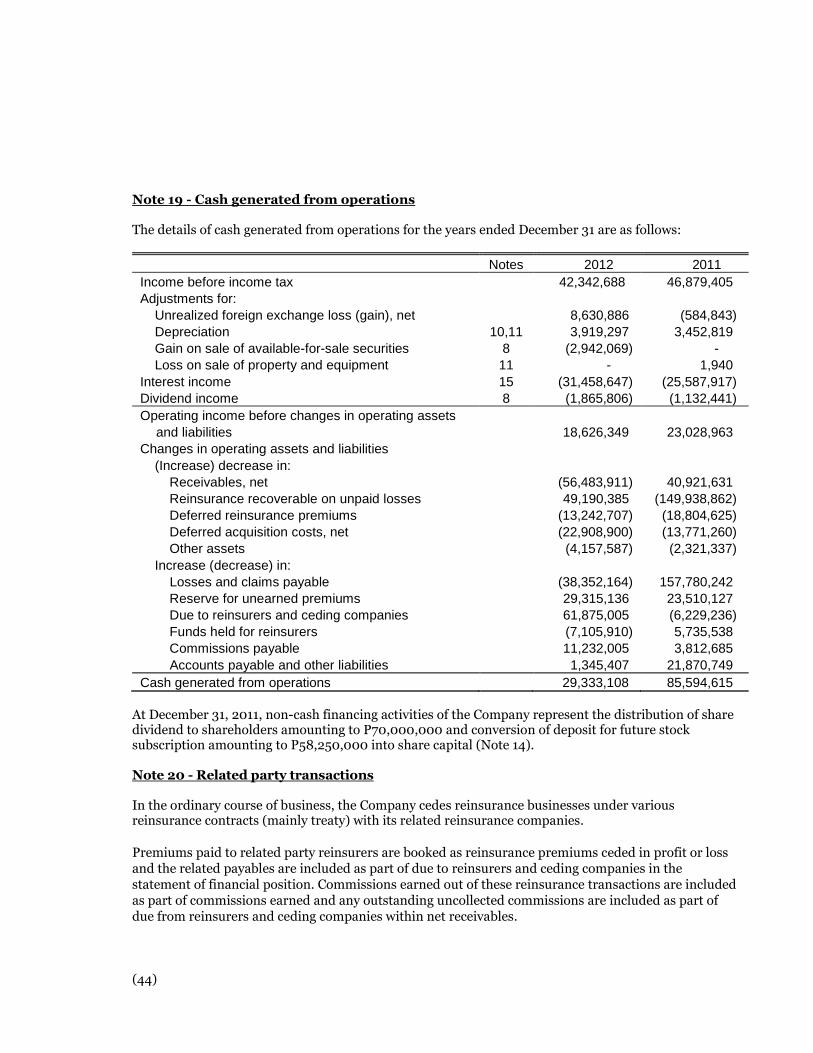

Cash generated from operations 19 29,333,108 85,594,615Interest received on cash and cash equivalents 13,847,911 8,089,504Income tax paid (745,697) (1,124,963)Net cash from operating activities 42,435,322 92,559,156

CASH FLOWS FROM INVESTING ACTIVITIES

Acquisitions of:

Property and equipment 11 (4,629,585) (2,246,643)Available-for-sale securities 8 (5,063,685) (2,000,000)Held-to-maturity securities 8 (189,611,036) (110,908,067)

Proceeds from:

Disposal of available-for-sale securities 8 4,241,960 2,000,000Maturities of held-to-maturity securities 8 27,482,702 66,021,457Disposal of property and equipment - 4,000

Interest received 18,458,238 19,870,968Dividends received 1,686,355 1,132,441Income tax paid (4,315,811) (2,844,631)Net cash used in investing activities (151,750,862) (28,970,475)

CASH FLOWS FROM FINANCING ACTIVITIES

Cash dividends paid 14 - (6,000,000)Deposit for future share capital subscription 14 - 23,250,000Issuance of share capital 14 1,490,000 20,260,000Net cash from financing activities 1,490,000 37,510,000

EFFECTS OF EXCHANGE RATE CHANGES ON CASHAND CASH EQUIVALENTS (428,715) -

NET (DECREASE) INCREASE IN CASH ANDCASH EQUIVALENTS (108,254,255) 101,098,681

CASH AND CASH EQUIVALENTS 6January 1 352,117,028 251,018,347December 31 243,862,773 352,117,028

(The notes on pages 1 to 52 are an integral part of these financial statements)

Asia Insurance (Philippines) Corporation

Notes to Financial StatementsAs at and for the years ended December 31, 2012 and 2011(All amounts are shown in Philippine Peso unless, otherwise stated)

Note 1 - General information

Asia Insurance (Philippines) Corporation (the “Company”) was incorporated and registered with thePhilippine Securities and Exchange Commission (SEC) primarily to engage in selling non-life insurancepolicies on fire, marine cargo, motor vehicle, casualty, surety bond, personal accident, comprehensivegeneral liability, engineering lines and miscellaneous insurances.

The Company’s registered office, which is also its principal place of business, is located at the15th Floor, Tytana Plaza, Plaza Lorenzo Ruiz, Binondo, Manila.

The Company has 79 employees as at December 31, 2012 (2011 - 71).

The financial statements have been approved and authorized for issuance by the Company’s Board ofDirectors on April 26, 2013. There were no material events that occurred subsequent to April 26, 2013until April 30, 2013.

Note 2 - Summary of significant accounting policies

The principal accounting policies adopted in the preparation of these financial statements are set outbelow. These policies have been consistently applied to both years presented, unless otherwise stated.

2.1 Basis of preparation

The financial statements of the Company have been prepared in accordance with Philippine FinancialReporting Standards (PFRS). The term PFRS in general includes all applicable PFRS, PhilippineAccounting Standards (PAS) and interpretations of the Philippine Interpretations Committee (PIC),Standing Interpretations Committee (SIC) and International Financial Reporting InterpretationsCommittee (IFRIC) which have been approved by the Financial Reporting Standards Council (FRSC)and adopted by SEC.

The financial statements have been prepared under the historical cost convention, as modified by therevaluation of available-for-sale securities.

The preparation of financial statements in conformity with PFRS requires the use of certain criticalaccounting estimates. It also requires management to exercise its judgment in the process of applyingthe Company’s accounting policies. The areas involving a higher degree of judgment or complexity, orareas where assumptions and estimates are significant to the financial statements are disclosed inNote 3.

(2)

Changes in accounting policy and disclosures

A number of new PFRS standards, amendments to existing PFRS standards and IFRIC interpretationsare effective for annual periods beginning January 1, 2012 and onwards. The adoption of these standards,amendments and interpretations, to the extent applicable to the Company’s operations, transactions andbalances, did not have or are not expected to have a significant impact on the Company’s financialstatements except as set out below:

PAS 1 (Amendment), Financial Statement Presentation - Other Comprehensive Income (effectiveJuly 1, 2012). The main change resulting from these amendments is a requirement for entities togroup items presented in other comprehensive income on the basis of whether they are potentiallyreclassifiable to profit or loss subsequently (reclassification adjustments). The amendments do notaddress which items are presented in other comprehensive income. The Company will apply theamendment beginning January 1, 2013. The adoption is not expected to have a significant impacton the financial statements but will result in changes in presentation in the statement of totalcomprehensive income.

PAS 19 (Amendment), Employee Benefits (effective January 1, 2013). These amendments eliminatethe corridor approach and calculate finance costs on a net funding basis. They would also requirerecognition of all actuarial gains and losses in other comprehensive income as they occur and of allpast service costs in profit or loss. The amendments replace interest cost and expected return on planassets with a net interest amount that is calculated by applying the discount rate to the net definedbenefit liability (asset). The Company will apply the amendment beginning January 1, 2013. At aminimum, the adoption of the amendment will result into the recognition of unrecognized actuariallosses amounting to P1,364,297 (Note 17) in other comprehensive income.

PFRS 9, Financial Instruments (effective January 1, 2015). This new standard addresses theclassification, measurement and recognition of financial assets and financial liabilities. It replacesthe parts of PAS 39 that relate to the classification and measurement of financial instruments.PFRS 9 requires financial assets to be classified into two measurement categories: those measuredat fair value and those measured at amortized cost. The determination is made at initialrecognition. The classification depends on the Company’s business model for managing itsfinancial instruments and the contractual cash flow characteristics of the instrument. For financialliabilities, the standard retains most of the PAS 39 requirements. The main change is that, in caseswhere the fair value option is taken for financial liabilities, part of the fair value change due to anentity’s own credit risk is recorded in other comprehensive income rather than profit or loss, unlessthis creates an accounting mismatch. The Company is yet to assess the full impact of PFRS 9 andintends to adopt this standard beginning January 1, 2015. The Company will also consider theimpact of the remaining phases of PFRS 9 when issued.

PFRS 13, Fair Value Measurement (effective January 1, 2013). This new standard aims to improveconsistency and reduce complexity by providing a clarified definition of fair value and a singlesource of fair value measurement and disclosure requirements for use across PFRS. Therequirements, which are largely aligned between IFRS and US GAAP, do not extend the use of fairvalue accounting but provide guidance on how it should be applied where its use is alreadyrequired or permitted by other standards within IFRS. The Company is yet to assess the full impactof PFRS 13 and intends to adopt the standard beginning January 1, 2013.

(3)

There are no other applicable and relevant standards, amendments and interpretations which areeffective beginning January 1, 2012 and adopted by the Company, and those issued but are not yeteffective as at December 31, 2012 that have or expected to have a significant impact on the Company’sfinancial statements during and at the end reporting period.

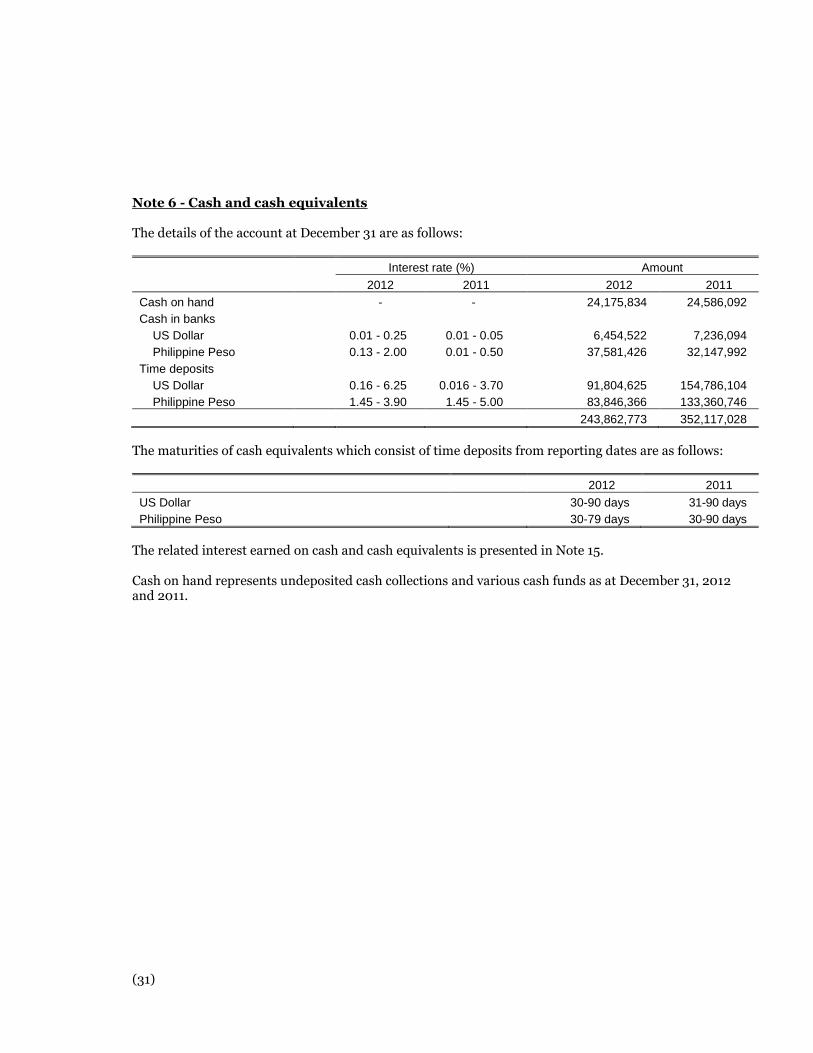

2.2 Cash and cash equivalents

Cash and cash equivalents include cash on hand, deposits held at call with banks, and other short-termhighly liquid investments with original maturities of three months or less from the date of acquisitionand are subject to an insignificant risk of changes in value.

2.3 Financial assets

2.3.1 Classification

The Company classifies its financial assets in the following categories: loans and receivables, held-to-maturity securities, at fair value through profit or loss and available-for-sale securities. Theclassification depends on the purpose for which the financial assets were acquired.

Management determines the classification of its financial assets at initial recognition. The Companyhas no investments classified as at fair value through profit or loss during and at the end of eachreporting period.

Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that arenot quoted in an active market.

The Company’s loans and receivables comprise cash and cash equivalents and receivables in thestatement of financial position.

Held-to-maturity securities

Held-to-maturity securities are non-derivative financial assets with fixed or determinable paymentsand fixed maturities for which management has the positive intention and ability to hold to maturity.

Available-for-sale securities

Available-for-sale securities are non-derivative financial assets that are either designated in thiscategory or not classified in any of the other categories.

2.3.2 Initial recognition and derecognition

Regular-way purchases and sales of financial assets are recognized on trade date (i.e., the date on whichthe Company commits to purchase or sell the asset). Financial assets are initially recognized at fairvalue plus transaction costs that are directly attributable to their acquisition.

Financial assets are derecognized when the contractual right to receive cash flows from the financialassets has ceased to exist or where the Company has transferred substantially all risks and rewards ofownership.

(4)

2.3.3 Subsequent measurement

Available-for-sale securities are subsequently carried at fair value.

Loans and receivables and held-to-maturity securities are subsequently carried at amortized cost usingthe effective interest method.

Gains and losses arising from changes in the fair value of available-for-sale securities are recognizeddirectly in equity, until the financial asset is derecognized or impaired at which time the cumulativegain or loss previously recognized in equity is recognized in profit or loss. Interest earned on thesesecurities is recognized using the effective interest rate in profit or loss. Dividends on available-for-saleequity instruments are recognized in profit or loss when the Company’s right to receive payment isestablished. Changes in the fair value of monetary securities denominated in foreign currency andclassified as available-for-sale are analyzed between translation differences resulting from changes inamortized cost of security and other changes in the carrying amount of the security. The translationdifferences are recognized in the profit or loss, and other changes in carrying amount are recognized inequity. Changes in the fair value of monetary securities classified as available-for-sale and non-monetary securities classified as available-for-sale are recognized in equity.

2.3.4 Impairment of financial assets

Assets classified as loans and receivables and held-to-maturity securities

The Company assesses at each reporting date whether there is objective evidence that a financial assetor group of financial asset is impaired. Individually significant financial asset is tested for impairmentif there are indicators of impairment. Impairment is measured on a portfolio basis when there isindication of impairment in a group of similar assets (with similar credit characteristics) andimpairment cannot be identified with an individual asset within the group. An asset that is deemedimpaired on an individual basis is not subsequently included in any group of assets that is tested forimpairment on a portfolio basis.

For purposes of a collective evaluation of impairment, financial assets are grouped on the basis ofsimilar credit risk characteristics (i.e., on the basis of the Company’s credit rating process thatconsiders asset type, industry, geographical location, collateral type, past-due status and other relevantfactors). Those characteristics are relevant to the estimation of future cash flows for groups of suchassets by being indicative of the debtor’s ability to pay all amounts due according to the contractualterms of the assets being evaluated.

Historical loss experience is adjusted on the basis of current observable data to reflect the effects ofcurrent conditions that did not affect the period on which the historical loss experience is based and toremove the effects of conditions in the historical period that do not currently exist. The methodologyand assumptions used for estimating future cash flows are reviewed regularly to reduce any differencesbetween loss estimates and actual loss experience.

The amount of impairment loss is measured as the difference between the financial asset’s carryingamount and the present value of estimated future cash flows discounted at the asset’s original effectiveinterest rate (recoverable amount). Impairment loss is recognized in profit or loss and the carryingamount of the asset is reduced through the use of an allowance account.

(5)

An impairment charge is reversed subsequently by adjusting the allowance account if the decrease inimpairment loss can be related objectively to an event occurring after the impairment loss isrecognized. The amount of reversal is recognized against impairment losses in profit or loss.

Loans and receivables are written-off in the year in which they are determined to be uncollectible.Loans and receivables are determined to be uncollectible after exerting effort to collect the accountsand upon approval by the Company’s Board of Directors.

Assets classified as available-for-sale

The Company assesses at the end of each reporting period whether there is objective evidence thatavailable-for-sale debt securities are impaired using similar criteria and process applied to financialassets carried at amortized cost as described above.

For equity investments classified as available-for-sale, a significant or prolonged decline in the fairvalue of the security below its cost is an objective evidence that the assets are impaired. A decline inthe fair value of the instrument by more than 20 percent is considered significant and a period of 12months or greater is considered to be a ‘prolonged’ decline. If any such evidence exists for available-for-sale equity securities, the cumulative loss - measured as the difference between the acquisitioncost and the current fair value, less any impairment loss on that financial asset previously recognizedin profit or loss - is removed from equity and recognized in profit or loss. Impairment losses onequity investment are not reversed in profit or loss. Increases in fair value after impairment arerecognized directly in equity.

2.4 Financial liabilities

2.4.1 Classification and measurement

The Company classifies its financial liabilities in the following categories: at fair value through profit orloss and at amortized cost. The classification depends on the purpose for which the financial liabilitieswere acquired or incurred. Management determines the classification of its financial instruments atinitial recognition.

The Company’s financial liabilities include financial instruments that are carried at amortized cost.These include commissions payable and accounts payable and other liabilities (excluding taxespayable).

The Company has no financial liabilities classified at fair value through profit or loss during and at theend of each reporting period.

2.4.2 Initial recognition and derecognition

Financial liabilities are initially recognized at fair value of the consideration received plus transactioncosts. A financial liability is derecognized when the obligation under the liability is discharged orcancelled, or has expired.

2.4.3 Subsequent measurement

Financial liabilities at amortized cost are subsequently measured at amortized cost using the effectiveinterest method.

(6)

2.5 Determination of fair value

The Company classifies its fair value measurements using a fair value hierarchy that reflects thesignificance of the inputs used in making the measurements. The fair value hierarchy has the followinglevels:

Level 1 - Quoted prices (unadjusted) in active markets for identical assets or liabilities. This levelincludes listed equity securities and debt instruments on exchanges (for example, PhilippineStock Exchange, Inc., Philippine Dealing and Exchange Corp., etc.).

Level 2 - Inputs other than quoted prices included within Level 1 that are observable for the asset orliability, either directly (i.e., as prices) or indirectly (i.e., derived from prices).

Level 3 - Inputs for the asset or liability that are not based on observable market data (unobservableinputs). This level includes equity investments and debt instruments with significantunobservable components.

The fair value for financial instruments traded in active markets at the reporting date is based on theirquoted market price or dealer price quotations, without any deduction for transaction costs. Whencurrent bid and asking prices are not available, the price of the most recent transaction providesevidence of the current fair value as long as there has not been a significant change in economiccircumstances since the time of the transaction.

For all other financial instruments not listed in an active market, the fair value is determined by usingappropriate valuation techniques. Valuation techniques include discounted cash flow analyses,comparison to similar instruments for which market observable prices exist, option pricing models,and other relevant valuation models.

2.6 Offsetting of financial instruments

Financial assets and liabilities are offset and the net amount reported in the statement of financialposition when there is a legally enforceable right to offset the recognized amounts and there is anintention to settle on a net basis, or realize the asset and settle the liability simultaneously.

2.7 Insurance contracts

2.7.1 Recognition and measurement

Short-term insurance contracts of the Company include property and casualty insurance contracts.

For all these contracts, premiums are recognized as revenue as follows:

Direct business

Gross premiums written are recognized at the inception date of the risks underwritten and are earnedover the period of cover in accordance with the incidence of risk using the 24th method. The portion ofthe gross premiums written that relates to the unexpired periods of the policies at year-end is presentedas reserve for unearned premiums in the statement of financial position.

(7)

Inward reinsurance business

Gross premiums written are recognized based on the date of notification by the ceding companies andare earned over the period of cover in accordance with the incidence of risk using the 24th method.The portion of the gross premiums written that relates to the unexpired periods of the policies at year-end is presented as reserve for unearned premiums in the statement of financial position.

2.7.2 Losses and claims payable

Losses and claims payable are recognized when the contracts are entered into and the premiums arecharged. Loss and claims adjustment expenses are recognized in profit or loss based on the estimatedliability for compensation owed to contract holders or to third parties damaged by the contract holders.They include direct and indirect claim settlement costs arising from events that have occurred up to thereporting date even if they have not yet been reported to the Company [i.e., incurred but not reported(IBNR)]. The Company does not discount its liabilities for unpaid claims. Liabilities for unpaid claimcosts including those for incurred but not reported are estimated and accrued. The liabilities forunpaid claims are based on the estimated ultimate cost of settling the claims using the input ofassessment for individual cases reported to the Company. The method of determining such estimatesand establishing reserves is continually reviewed and updated. Changes in estimates of claim costsresulting from the continuous review process and differences between estimates and payments forclaims are recognized as income or expenses in the year in which the estimates are changed orpayments are made. Estimated recoveries on settled and unsettled claims are evaluated in terms ofestimated realizable values of the salvage recoverable and deducted from the liability for unpaid claims.Outstanding claims and IBNR losses are presented in the statement of financial position as part oflosses and claims payable.

2.7.3 Reinsurance commission

Reinsurance commission is initially deferred upon acceptance of the premium cession by reinsurersand earned in proportion to premium revenue recognized. Reinsurance commission is presented ascommissions earned in the statement of total comprehensive income.

2.7.4 Acquisition costs

Costs that vary with and are primarily related to the acquisition of new and renewal insurance contractssuch as commissions are deferred and charged to expense in proportion to premium revenuerecognized. Unamortized acquisition costs are shown in the statement of financial position as deferredacquisition costs.

Reinsurance commissions are deferred and deducted from the applicable deferred acquisition costs, andrecognized in profit or loss using the same amortization method as the related acquisition costs.

(8)

2.7.5 Liability adequacy test

At each reporting date, liability adequacy tests are performed to ensure the adequacy of the contractliabilities, net of related deferred acquisition costs (DAC). In performing these tests, current best estimateof future contractual cash flows and claims handling and administration expenses, as well as investmentincome from the assets backing such liabilities, are used. Any deficiency is immediately charged to profitor loss initially by writing-off DAC and by subsequently establishing a provision for losses arising fromliability adequacy tests (the unexpired provision). There were no deficiencies recognized in profit or lossduring reporting periods. Any DAC written off as a result of this test cannot be subsequently reinstated.

2.7.6 Reinsurance contracts held

Contracts entered by the Company with reinsurers which compensate the Company for losses on one ormore contracts issued and meet the classification requirements for insurance contracts are classified asreinsurance contracts held. Insurance contracts entered into by the Company under which the contractholder is another insurer (inward reinsurance) are classified as insurance contracts. Contracts that donot meet these classification requirements are classified as financial contracts.

The benefits to which the Company is entitled under its reinsurance contracts held are recognized asreinsurance assets. These assets consist of reinsurance recoverable on paid losses, due from reinsurersand ceding companies and funds held by ceding companies (classified within receivables) andreinsurance recoverable on unpaid losses.

The Company assesses its reinsurance assets for impairment annually. If there is objective evidencethat the reinsurance asset is impaired, the Company reduces the carrying amount of the reinsuranceasset to its recoverable amount and recognizes that impairment loss in profit or loss. The Companygathers the objective evidence that a reinsurance asset is impaired using the same policies adopted forfinancial assets held at amortized cost. The impairment loss is also calculated following the samemethod used for these financial assets. These policies are described in Note 2.3 (e).

Reinsurance liabilities are primarily premiums payable for reinsurance contracts and are recognized asan expense upon recognition of related premiums. These liabilities pertain to due to reinsurers andceding companies and funds held for reinsurers.

Amounts recoverable from or due to reinsurers are measured consistently with the amounts associatedwith the reinsured insurance contracts and in accordance with terms of each reinsurance contract.

2.7.7 Receivables and payables related to insurance contracts

Receivables and payables, such as premium receivable, losses and claims payable and commissionspayable, are recognized when the right to receive payment is established or when the obligation becomesdue. These include amounts due to and from agents, brokers and insurance contract holders.

If there is objective evidence that the insurance receivable is impaired, the Company reduces thecarrying amount of the insurance receivable accordingly and recognizes that impairment loss in profitor loss. The Company gathers the objective evidence that an insurance receivable is impaired using thesame policies adopted for loans and receivables. The impairment loss is also calculated under the samemethod used for these financial assets. These policies are described in Note 2.3 (e).

(9)

2.7.8 Salvage and subrogation reimbursements

Some insurance contracts permit the Company to sell usually damaged property acquired in settling aclaim (i.e., salvage). The Company also have the right to pursue third parties for payment of some or allcosts (i.e., subrogation).

Subrogation reimbursements are also considered as an allowance in the measurement of the insuranceliability for claims and are charged against losses and claims payable when the liability is settled. Theallowance is the assessment of the amount that can be recovered from the action against the liable thirdparty.

The total salvage and subrogation reimbursements as at December 31, 2012 amount to P2,042,224(2011 - P520,000).

2.8 Investment properties

Properties held for long term rental yields or for capital appreciation or for both, are classified asinvestment properties. These properties are initially measured at cost, which includes transaction costs,but excludes day to day servicing costs. Replacement cost is capitalized if it is probable that futureeconomic benefits associated with the item will flow to the Company and the cost of the item can bereliably measured. Subsequently, at each report date, investment properties, except for land, arecarried at cost less accumulated depreciation and impairment loses, if any. Land is carried at cost lessany impairment in value.

Depreciation of investment property is computed using the straight-line method over its useful life. Theestimated useful life and the depreciation method is reviewed periodically to ensure that the period andthe method of depreciation is consistent with the expected pattern of economic benefits from items ofinvestment properties. The estimated useful life of the investment properties is 25 years.

Transfers are made to investment property when there is a change in use, evidenced by ending of owneroccupation, commencement of an operating lease to another party or ending of construction ordevelopment. There were no transfers made to investment property during and at the end of eachreporting period.

Investment property is derecognized when it has been disposed of or when permanently withdrawnfrom use and no future benefit is expected from its disposal. Any gain or loss on the retirement ordisposal of investment property is recognized in profit or loss in the year of derecognition.

Rental income from investment property is recognized in profit or loss on a straight-line basis over thelease term. Lease incentives are recognized as an integral part of the total rent income. Expenses withregard to investment property are treated as ordinary operating expenses and are recognized whenincurred.

(10)

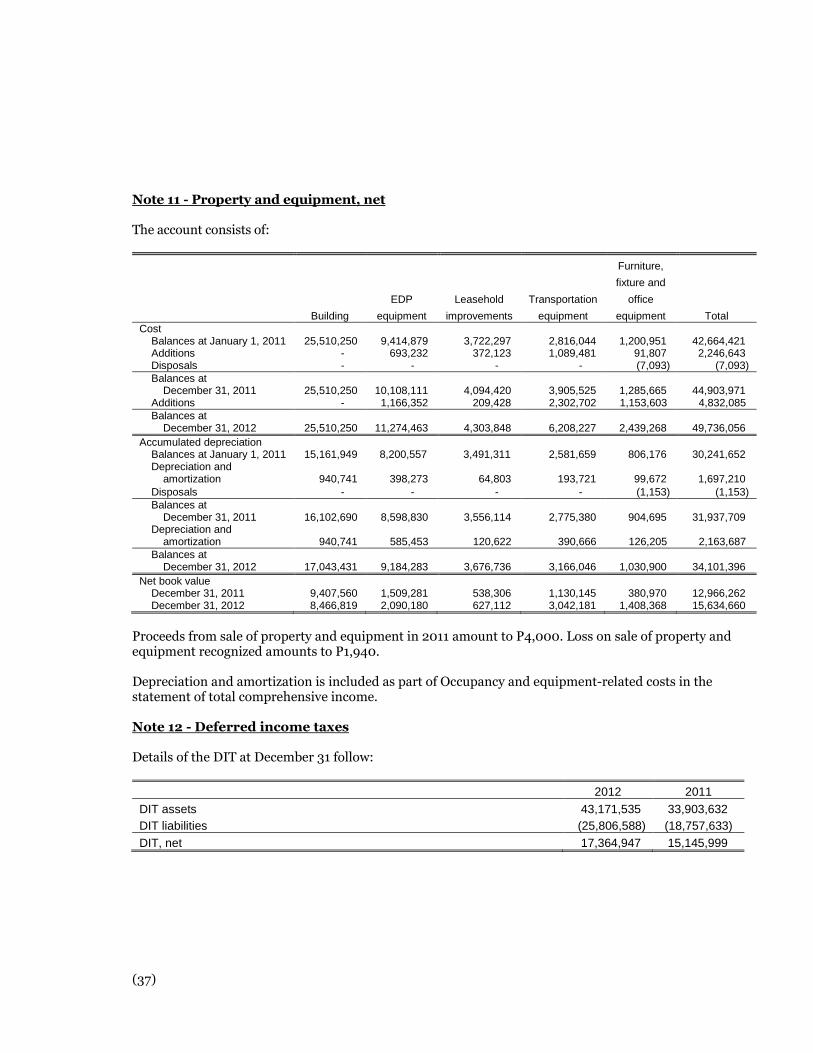

2.9 Property and equipment

Property and equipment are stated at historical cost less accumulated depreciation and amortization andany impairment in value. Historical cost includes expenditures that are directly attributable to theacquisition of items. Subsequent costs are included in the asset’s carrying amount or recognized as aseparate asset, as appropriate, only when it is probable that economic benefits associated with the itemwill flow to the Company and the cost of the item can be measured reliably. All other repairs andmaintenance are charged to profit or loss during the period in which they are incurred.

Depreciation and amortization are calculated using the straight-line method to allocate their cost to theirresidual values over their estimated useful lives as follows:

Building 27 yearsEDP equipment 5 yearsTransportation equipment 5 yearsFurniture, fixtures and office equipment 5 to 7 years

Leasehold improvements5 years or lease term, whichever is

shorter

The assets’ residual values and useful lives are reviewed, and adjusted as appropriate, at each reportingdate.

An asset’s carrying amount is written down immediately to its recoverable amount if the asset’scarrying amount is greater than its estimated recoverable amount. The recoverable amount is thehigher of an asset’s fair value less costs to sell and value in use.

An item of property and equipment is derecognized upon disposal or when no future economic benefitsare expected from its use or disposal at which time the cost and their related accumulated depreciationare removed from the accounts. Gains and losses on disposals are determined by comparing proceedswith carrying amount and are recognized in profit or loss.

2.10 Impairment of non-financial assets

Assets that are subject to depreciation or amortization, such as property and equipment and investmentproperty, are reviewed for impairment whenever events or changes in circumstances indicate that thecarrying amount may not be recoverable. An impairment loss is recognized for the amount by which theasset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of anasset’s fair value less costs to sell and value in use. For purposes of assessing impairment, assets aregrouped at the lowest levels for which there are separately identifiable cash flows (cash-generating units).Value in use requires the Company to make estimates of future cash flows to be derived from a particularasset, and discount them using a pre-tax market rate that reflects current assessments of the time value ofmoney and the risks specific to the asset.

2.11 Income taxes

Current income tax

The current income tax charge is calculated on the basis of the tax laws enacted or substantivelyenacted at the reporting date. Management periodically evaluates positions taken in tax returns withrespect to situations in which applicable tax regulation is subject to interpretation and establishesprovisions where appropriate on the basis of amounts expected to be paid to the tax authorities.

(11)

Deferred income tax

Deferred income tax (DIT) is provided in full, using the liability method, on temporary differencesarising between the tax bases of assets and liabilities and their carrying amounts in the financialstatements. DIT is determined using the tax rates (and laws) that have been enacted or substantivelyenacted by the reporting date and are expected to apply when the related DIT asset is realized or theDIT liability is settled.

DIT assets are recognized for all deductible temporary differences, carry-forward of unused tax losses(net operating loss carryover or NOLCO) and unused tax credits to the extent that it is probable thatfuture taxable profits will be available against which the temporary differences can be utilized. DITliabilities are recognized in full for all taxable temporary differences, except to the extent that thedeferred tax liability arises from the initial recognition of goodwill.

DIT assets and liabilities are offset when there is a legally enforceable right to offset current tax assetsagainst current tax liabilities and when the DIT assets and liabilities relate to income taxes levied by thesame taxation authority and where there is an intention to settle the balances on a net basis.

DIT expense or credit included in provision for income tax is recognized for the changes during theyear in the DIT assets and liabilities.

2.12 Provisions

Provisions for legal claims are recognized when the following are present:

the Company has a present legal or constructive obligation as a result of past events; it is more likely than not that an outflow of resources will be required to settle the obligation; and the amount has been reliably estimated. Provisions are not recognized for future operating losses.

Provisions are measured at the present value of the expenditures expected to be required to settle theobligation using a pre-tax rate that reflects current market assessments of the time value of money andthe risks specific to the obligation. The increase in the provision due to the passage of time isrecognized as interest expense.

2.13 Pension liability

The liability recognized in the statement of financial position in respect of defined benefit pension planis the present value of the defined benefit obligation at the reporting date less the fair value of planassets, together with adjustments for unrecognized actuarial gains or losses and past service costs. Thedefined benefit obligation is calculated annually by independent actuaries using the projected unitcredit method. The present value of the defined benefit obligation is determined by discounting theestimated future cash outflows using interest rates of government bonds that are denominated in thecurrency in which the benefits will be paid, and that have terms to maturity which approximate theterms of the related pension liability.

Actuarial gains and losses arising from experience adjustments and changes in actuarial assumptions inexcess of the greater of 10% of the value of plan assets or 10% of the defined benefit obligation arerecognized in profit or loss over the employees’ expected average remaining working lives.

(12)

Past service costs are recognized immediately in profit or loss, unless the changes to the pension plan areconditional on the employees remaining in service for a specified period of time (the vesting period). Inthis case, the past-service costs are amortized on a straight-line basis over the vesting period.

The unrecognized pension liability (transition liability) is amortized over five years.

2.14 Equity

Common shares are classified as equity.

2.15 Deposit for future share subscription

Deposit for future share subscription represent funds received by the Company with a view to applyingthe same as payment for a future additional issuance of shares either from its authorized but unissuedshares, from a proposed increase in authorized share capital, or as additional paid-in capital. Uponapplication, the amount will be credited to share capital for the par value of the shares and sharepremium for the amount in excess of the par value.

2.16 Dividend distribution

Dividend distribution to the Company’s shareholders is recognized as a liability in the Company’sfinancial statements in the period in which the dividends are approved by the Company’s Board ofDirectors.

2.17 Revenue recognition

Revenue is recognized to the extent that it is a probable that the economic benefits will flow to theCompany and the revenue can be reliably measured. The following specific recognition criteria mustalso be met before revenue is recognized:

Premium revenue

Premiums from short-duration insurance contracts are recognized as revenue over the period of thecontracts using the 24th method, except for marine cargo where the provision for unearned premiumspertain to the premiums for the last two months of the year. The portion of the premiums written thatrelate to the unexpired periods of the policies at reporting date is accounted for as reserve for unearnedpremiums in the statement of financial position. The related reinsurance premiums that pertain to theunexpired periods at reporting date are accounted for as deferred reinsurance premiums presented inthe statement of financial position. The net changes in these accounts between reporting dates areincluded in the determination of net premium earned.

Commission income

Reinsurance commissions are recognized as revenue over the period of the contracts using the24th method, except for marine cargo where the deferred reinsurance commission pertains to thepremiums for the last two months of the year. The portion of the commissions that relates to theunexpired periods of the policies at the reporting date is accounted for as deferred reinsurancecommissions and offset against deferred acquisition costs in the statement of financial position.

(13)

2.18 Leases

Leases where a significant portion of the risks and rewards of ownership are retained by the lessor areclassified as operating leases. Payments made under operating leases are charged to profit or loss on astraight-line basis over the period of the lease.

Properties leased out under operating leases are included in investment properties in the statement offinancial position. Rental income under operating leases is recognized in profit or loss on a straight-line basis over the period of the lease.

2.19 General and administrative expenses

General and administrative expenses are recognized when incurred.

2.20 Foreign currency transactions and translation

Functional and presentation currency

Items included in the financial statements are measured using the currency of the primary economicenvironment in which the Company operates (the “functional currency”). The Company’s financialstatements are presented in Philippine Peso, which is the Company’s functional and presentationcurrency.

Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange ratesprevailing at the dates of the transaction. Foreign exchange gains and losses resulting from thesettlement of such transactions and from the translation of monetary assets and liabilities denominatedin foreign currencies are recognized in profit or loss.

2.21 Related party transactions and relationships

Related party relationships exist when one party has the ability to control, directly, or indirectlythrough one or more intermediaries, the other party or exercises significant influence over the otherparty in making financial and operating decisions. Such relationships also exist between and/or amongentities which are under common control with the reporting enterprise, or between and/or among thereporting enterprise and its key management personnel, directors, or its shareholders. In consideringeach possible related party relationship, attention is directed to the substance of the relationship, andnot merely the legal form.

2.22 Events after the reporting date

Post year-end events that provide additional information about the Company’s position at the reportingdate (adjusting events) are reflected in the financial statements. Post year-end events that are notadjusting events are disclosed in the notes to the financial statements when material.

(14)

Note 3 - Critical accounting estimates, assumptions and judgments

The Company makes estimates and assumptions that affect the reported amounts of assets andliabilities within the next financial year. Estimates, assumptions and judgments are continuallyevaluated and are based on historical experience and other factors, including expectations of futureevents that are believed to be reasonable under the circumstances. The estimates, assumptions andjudgments that have significant risk of causing a material adjustment to the carrying amounts of assetsand liabilities within the next financial year are discussed below.

3.1 Critical accounting estimates and assumptions

The ultimate liability arising from claims made under insurance contracts (Note 9)

The estimation of the ultimate liability arising from claims made under insurance contracts is theCompany’s most critical accounting estimate. Management makes best estimate of its insuranceliability at reporting date using adjuster’s report and other available information relating to claims.However, there are several sources of uncertainty that need to be considered in the estimate of theliability that the Company will ultimately pay for such claims. The major uncertainties are thefrequency of claims due to the contingencies covered and the timing of benefit payments.

The Company considers that it is impracticable to discuss with sufficient reliability the possibleeffects of sensitivities surrounding the ultimate liability arising from claims made under insurancecontracts as the major uncertainties may differ significantly. With this, it is reasonably possible,based on existing knowledge, that the outcomes within the next fiscal year are different fromassumptions could require a material adjustment to the carrying amount of the asset or liabilityaffected including reserve for outstanding losses and related insurance balances.

The carrying value of losses and claims payable as at December 31, 2012 amounts to P462,630,931(2011 - P500,360,754). IBNR claims, gross of reinsurance, as at December 31, 2012 amount toP7,447,073 (2011 - P4,181,825). Net claims and losses during the year amount to P100,797,976(2011 - P89,337,414).

3.2 Critical accounting judgments

Impairment of available-for-sale securities (Note 8)

The Company determines that available-for-sale securities are impaired when there has been asignificant or prolonged decline in the fair value below its cost for equity securities. For debt securities,available-for-sale financial assets are impaired when an objective evidence of impairment is present.The determination of what is significant or prolonged decline or objective evidence of impairmentrequires judgment. Impairment may be appropriate when there is evidence of deterioration in thefinancial health and near-term business outlook of the investee or issuer, including factors such asindustry and sector performance, changes in technology, and financing and operational cash flows.

As at reporting date, the Company has no recognized impairment in available-for-sale securities.

(15)

Classification to held-to-maturity securities (Note 8)

The Company follows the guidance of PAS 39 in classifying non-derivative financial assets with fixed ordeterminable payments and fixed maturity as held-to-maturity. This classification requires significantjudgment. In making this judgment, the Company evaluates its intention and ability to hold suchinvestments to maturity. If the Company fails to keep these investments to maturity other than for thespecific circumstances - for example, selling an insignificant amount close to maturity - it will berequired to reclassify the entire class as available-for-sale. The investments would therefore bemeasured at fair value and not amortized cost.

If the entire class of held-to-maturity investments is tainted, the carrying amount of investment wouldincrease by P8,770,396 (2011 - P18,610,943 increase) with a corresponding entry in reserve foravailable-for-sale securities in the equity section of the statement of financial position.

Impairment of reinsurance assets (Notes 7 and 9)

The Company reviews reinsurance assets at each reporting period to assess whether an allowance forimpairment should be recorded in profit or loss. In particular, judgment by management is required indetermining the amount and timing of future cash flows in establishing the level of allowance required.The amount and timing of recorded expenses for any period would differ if the Company madedifferent judgment. An increase in allowance for impairment losses would increase recorded expensesand decrease net income.

As at reporting date, the Company has no recognized impairment in reinsurance assets.

Recoverability of deferred income taxes (Note 12)

Management reviews at each reporting date the carrying amounts of DIT assets. The carrying amountof DIT assets is reduced to the extent that is no longer probable that sufficient taxable profit will beavailable against which the related tax assets can be utilized. Management believes that sufficienttaxable profit will be generated to allow all of the recognized DIT assets to be utilized.

The balance of DIT assets amounted to P43,171,535 (2011 - P33,903,632).

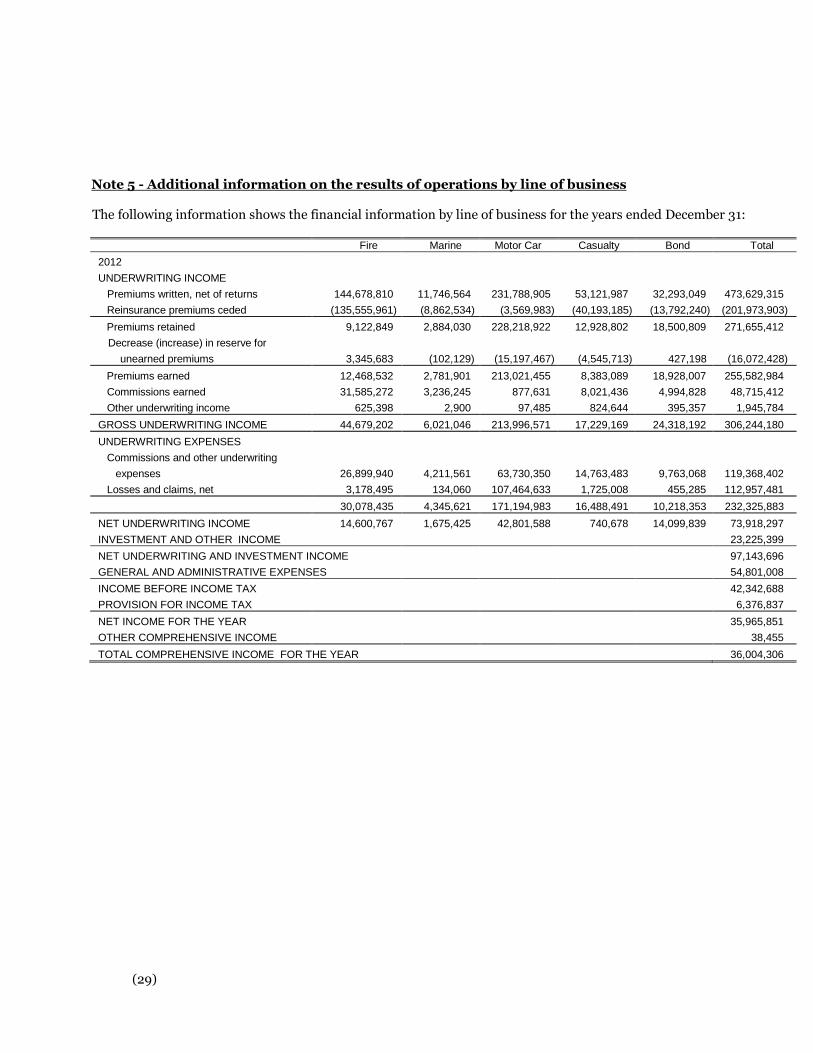

Note 4 - Insurance and financial risk and capital management

This section summarizes the Company’s insurance and financial risks and the way the Companymanages them, including the Company’s capital management objectives.

4.1 Insurance risk

Insurance is a form of contract whereby periodic payments (also known as insurance premiums) aremade to an insurance company, in order to provide an individual or business compensation in theevent of property loss or damage. The risk under any one insurance contract is the uncertainty aboutan unfavorable outcome in a given situation. Insurance risk is uncertainty over the likelihood of aninsured event occurring, the quantum of the claim, or the time when claims payments will fall due.

The principal risk the Company is facing under insurance contracts is when the actual claims andbenefit payments exceeds the carrying amount of the insurance liabilities. This could happen whenthere are numerous claims that occur in a particular period and the actual payment exceeds theestimated amount.

(16)

Factors that aggravate insurance risk include reduction in rates of premium, geographical location, andtype of industry covered. One way of reducing insurance risk is by transfer and sharing of risk.

The Company has developed its insurance underwriting strategy to expand the type of insurance riskaccepted in order to attain premium income growth and above-average underwriting profit.

4.1.1 Casualty insurance contracts

Frequency and severity of claims

The frequency and severity of claims can be affected by several factors. Estimated inflation is also asignificant factor due to the long period typically required to settle these cases. Another factor is thepolitical and economic stability of the country which resulted to numerous theft claims. The Companymanages these risks through its well-designed underwriting strategy, adequate reinsurancearrangements and proactive claims handling.

The underwriting strategy attempts to ensure that the underwritten risks are well diversified in termsof type and amount of risk, industry and geography in order to spread possible losses fairly between theCompany (retention) and the reinsurers.

Management continues to review the loss experience and premium payment record of existing agenciesto identify and weed out the bad agencies and motivate the good agencies to produce more business.

Sources of uncertainty in the estimation of future claim payments

The claims outstanding provision is the estimated ultimate cost of all claims and the related claimshandling expenses in respect of events up to the accounting date less amounts already paid.

The provision will relate to all events that have occurred up to the accounting date, whether or not theCompany has been notified of the claims in question before the close of the accounting period. Thelatter category of claims is referred to as IBNR claims.

It is impossible for an insurance company to predict its outstanding claims provisions with 100%accuracy. Yet this item is probably the most significant figure in the accounts. If it is understated, theCompany may distribute assets or otherwise act in a way that could lead to severe financial problems,and possible insolvency, when claims come to be paid.

The provision for reported claims and IBNR claims are the Company’s estimate of the amount which itwill have to pay at year-end.

The estimated cost of claims includes direct expenses to be incurred in settling claims, net of theexpected subrogation value and other recoveries. The Company takes all reasonable steps to ensurethat it has appropriate information regarding its claims exposures.

4.1.2 Property insurance contracts

Frequency and severity of claims

For property insurance contracts, climatic changes give rise to more frequent and severe extremeweather events (for example, flooding, typhoons, etc.) and their consequences.

(17)

Cost of rebuilding properties, replacement or indemnity for contents and time taken to restartoperations for business interruption are the key factors that influence the level of claims under thesepolicies. The greatest likelihood of significant losses on these contracts arises from storm or flooddamage.

The Company has the right to re-price the risk on renewal. It also has the ability to impose deductiblesand reject fraudulent claims. Moreover, it has the right not to accept a certain risk by not engaging inany form of hazardous enterprise at all. These contracts are underwritten by reference to thecommercial replacement value of the properties and contents insured, and claim payment limits arealways included to cap the amount payable on occurrence of the insured event.

Sources of uncertainty in the estimation of future claims payments

Treaty cession limits and underwriting strategies are being implemented to protect the Company andreinsurers from high exposures to possible losses. Property claims are analyzed separately for itsexposures and risk accumulation. This is estimated within the definition of the crest zone exposures.The shorter settlement period for these claims allows the Company to achieve a higher degree ofcertainty about the estimated cost of claims.

4.1.3 Marine insurance contracts

Marine insurance contract covers marine cargo

All marine insurance policies issued are covered by the Company’s reinsurance program. TheCompany sees to it that the name of the vessel is stated to determine whether the vessel is acceptableand to ensure that it is insuring a shipment that is loaded in a sea worthy vessel.

Sources of uncertainty in the estimation of future claims payments

For marine claims, it is the marine adjusters who make valuations and recommendations for theestimated loss reserves including direct expenses, subrogation value and recoveries that will beincurred in settling the claims. The Company sees to it that the underwriting guidelines in accepting amarine risk is being implemented to mitigate exposure to an amount which is beyond the Company’scapacity to write involving one vessel.

4.1.4 Sensitivities

The general insurance claims provision is sensitive to the Company’s past claims developmentexperiences. The sensitivity of certain variables like legislative change, uncertainty in the estimationprocess, etc., is not possible to quantify. Furthermore, because of delays that arise between occurrenceof a claim and its subsequent notification and eventual settlement, the outstanding claims provisionsare not known with certainty at the reporting date.

Consequently, the ultimate liabilities will vary as a result of subsequent developments. Differencesresulting from reassessments of the ultimate liabilities are recognized in subsequent financialstatements.

(18)

The Company provides for estimated IBNR losses based on the actual reported losses during the firstmonth subsequent to yearend. A sensitivity analysis was performed based on the standard deviation inIBNR for the past three years covering claims filed during the first month of each year for lossesincurred for the previous year.

Change in IBNR Effect on pre-tax incomeDecember 31, 2012 +/- 10% +/- 772,155December 31, 2011 +/- 41% +/- 1,718,461

4.2 Financial risk

The Company is exposed to financial risk through its financial assets and financial liabilities. Themost important components of this financial risk are market risk, credit risk and liquidity risk.

4.2.1 Market risk

Interest rate risk

This is the type of risk that the Company primarily faces due to the nature of its financial assets andliabilities. The interest rate risk is the only financial risk that has a materially different impact acrossthe assets and liabilities categorized in the Company’s asset liability management framework.

Cash flow interest rate risk is the risk that the future cash flows of a financial instrument will fluctuatebecause of changes in market interest rates. Fair value interest rate risk is the risk that the value of afinancial instrument will fluctuate because of changes in market interest rates.

The Company is exposed to fair value interest rate risk, the risk that the value of a financial instrumentwill fluctuate because of changes in market interest rate, because of debt securities held by theCompany and classified on the statement of financial position as available-for-sale (Note 8). Asensitivity analysis was performed based on a reasonable possible shift in interest rate year on year onthe Company’s debt securities. If interest rates increased/decreased by 216 basis points in 2012 (2011 –17 basis points), with all other variables held constant, the fair value reserve shown in equity woulddecrease/increase by P1,821 (2011 - P25,416).

The Company’s investments in government securities which are held-to-maturity (Note 8) bear fixedinterest rates and therefore the Company is not exposed to fair value and cash flow interest risk onthese securities.

(19)

Foreign currency risk

The insurance business of the Company is mostly denominated in local currency.

Currency exposures arise primarily from the holding of monetary assets denominated in US Dollar.The Company does not enter into derivatives to manage foreign currency risks.

The Company’s foreign currency assets and liabilities as at December 31 are as follows:

Notes 2012 2011

Assets (in US Dollar)Cash and cash equivalents 6

Cash in banks 156,694 164,726

Time deposits 2,228,700 3,449,969

Available-for-sale securities 8 1,008,740 1,010,326

Held-to-maturity securities 8 4,185,000 1,975,000

Reinsurance recoverable on unpaid losses 2,056,961 2,921,450

Total assets 9,636,095 9,521,471

Liability

Losses and claims payable 2,018,448 2,975,000

Net asset 7,616,647 6,546,471

Peso equivalent 313,744,923 287,573,378

The exchange rate of US Dollar into Philippine Peso is P41.192 (2011 - P43.928).

For the years ended December 31, the Company’s foreign exchange (losses) gains are as follows:

2012 2011

Unrealized foreign exchange (loss) gain (8,630,886) 584,843Realized foreign exchange (loss) gain (11,127,688) (663,113)

(19,758,574) (78,270)

A sensitivity analysis was performed on the US Dollar denominated assets and liabilities. Thefluctuation rate is based on the historical movement of US Dollar year on year.

Year Change in currencyEffect on pre-tax income in

Philippine Peso

2012 +/- 6.00% +/- 21,841,8822011 +/- 0.10% +/- 281,331

Price risk

The Company is exposed to price risk in respect of equity securities classified as available-for-salesecurities.

Net change in fair value of available-for-sale equity securities would increase/decrease by P12,430,350(2011 - P2,570,844) as a result of an increase/decrease of 32% (2011 - 7%) in market prices which isbased on the average historical fluctuation in the stock price index year on year.

(20)

4.2.2 Credit risk

Credit risk management, risk limit and mitigation policies

(i) Insurance and reinsurance receivable balances

The Company structures the levels of credit risk it accepts by placing limits on its exposure to a singlecounterparty, or group of counterparty, and to geographical and industry segments. Such risks aresubject to an annual or more frequent review. Limits on the level of credit risk by category andterritory are approved annually by the Board of Directors.

Reinsurance risk is used to manage insurance risk. This does not, however, discharge the Company’sliability as primary insurer. If a reinsurer fails to pay a claim for any reason, the Company remainsliable for the payment to the policyholder. The creditworthiness of reinsurers is considered on anannual basis by reviewing their financial strength prior to finalization of any contract. For facultativereinsurers, only approved companies are being used after taking into consideration their paying habitand reciprocal business.

Key areas where the Company is exposed to credit risk are:

reinsurers’ share of insurance liabilities; amounts due from reinsurers in respect of claims already paid; amounts due from insurance contract holders; and amounts due from insurance intermediaries.

(ii) Available-for-sale and held-to-maturity debt securities

One of the Company’s primary investment objectives is to seek the preservation of its portfolio bymitigating the credit risk which is the risk of loss due to failure of the issuer to make good on itsobligation when maturity becomes due. This is mitigated by investing in safe securities anddiversifying its investment portfolio so that the failure of any one issuer would not materially affect thecash flow of the Company. Within the guidelines provided by the Insurance Commission (IC), theCompany’s Investment Committee ensures that the Company invests in allowable categories ofinvestment instruments and provided limitation as to the percentage of the portfolio which can beinvested in certain category. Presently, the Company has heavily invested in government securities.

For time deposits and debt securities, external ratings such as those provided by Philippine RatingServices Corporation (Philratings) and Standard & Poor (S&P) or their equivalent are used by theCompany for managing credit risk exposures. Investments in these deposits and securities are viewedas a way to gain better credit quality mix and at the same time, maintain a readily available source tomeet funding requirements.

(21)

Maximum exposure to credit risk

Credit risk exposures relating to financial assets at December 31 are as follows:

2012 2011

Cash and cash equivalents (excluding cash on hand) 219,686,939 327,530,936

Receivable arising from insurance contractsPremium receivable 61,870,942 53,151,648Reinsurance recoverable on paid losses 130,391,975 85,525,687

Due from reinsurers and ceding companies 5,460,729 5,020,333

Funds held by ceding companies 4,880,417 4,091,641

Other loans and receivablesAccounts receivable 9,663,611 9,255,490Accrued interest income 4,745,489 4,248,247

Accrued rental income 266,553 -Refundable deposits 69,700 69,700Security fund 24,929 24,929

Available-for-sale debt securities 51,825,921 54,990,169Held-to-maturity securities 382,623,710 225,595,876

Allowance for impairment on premium receivable amounts to P1,553,000 as at December 31, 2012 and2011.

Credit quality of receivables arising from insurance contracts and other loans and receivables

Amounts in thousands

Neither pastdue norimpaired

(1-30 days)

Past due but not impairedOverdue

andimpaired

Grosscarryingamount

31-180days

181-360days

More than360 days

December 31, 2012Receivable arising from insurance

contractsPremium receivable 11,348 35,764 10,063 3,143 1,553 61,871Reinsurance recoverable on paid

losses 18,217 64,614 10,487 37,074 - 130,392Due from reinsurers and ceding

companies 931 150 127 4,253 - 5,461Funds held by ceding companies - 1,802 41 3,037 - 4,880

Other loans and receivables -Accounts receivable 2,834 830 449 5,551 - 9,664Accrued interest income 376 4,369 - - - 4,745Accrued rental income 267 - - - - 267Refundable deposits - - - 70 - 70Security fund - - - 25 - 25

33,683 88,632 16,018 77,489 1,553 217,375

(22)

Amounts in thousands

Neither pastdue norimpaired

(1-30 days)

Past due but not impairedOverdue

andimpaired

Grosscarryingamount

31-180days

181-360days

More than360 days

December 31, 2011Receivable arising from insurance

contractsPremium receivable 12,814 33,227 3,039 2,519 1,553 53,152Reinsurance recoverable on paid

losses 840 7,612 3,974 73,100 - 85,526Due from reinsurers and ceding

companies 569 1,994 522 1,935 - 5,020Funds held by ceding companies - 486 128 3,478 - 4,092

Other loans and receivablesAccounts receivable 2,778 1,285 1,806 3,386 - 9,255Accrued interest income 2,735 1,352 161 - - 4,248Refundable deposits - - - 70 - 70Security fund - - - 25 - 25

19,736 45,956 9,630 84,513 1,553 161,388

Credit quality of cash and cash equivalents, available-for-sale and held-to-maturity securities

A+ to AAA* BB- to BB+** Unrated*** Total

December 31, 2012

Available-for-sale securities

Debt securities-US Dollars - 51,825,921 - 51,825,921

Held-to-maturity securities

Treasury bonds and notes

Philippine Peso - 103,654,350 - 103,654,350

US Dollar - 174,019,683 - 174,019,683

Corporate bonds - 30,980,737 - 30,980,737

Short-term time deposits - - 73,968,940 73,968,940

- 308,425,374 73,968,940 382,623,710

Cash and cash equivalents

Universal bank 124,511,930

Commercial bank 58,788,578

Thrift bank 36,309,436

Rural bank 76,995

219,686,939

(23)

A+ to AAA* BB- to BB+** Unrated*** Total

December 31, 2011

Available-for-sale securities

Debt securities-US Dollars - 54,990,169 - 54,990,169

Held-to-maturity securities

Treasury bonds and notes

Philippine Peso - 89,521,881 - 89,521,881

US Dollar - 85,061,671 - 85,061,671

Corporate bonds - 38,977,622 - 38,977,622

Short-term time deposits - - 12,034,702 12,034,702

- 213,561,174 12,034,702 225,595,876

Cash and cash equivalents

Universal bank 210,947,857

Commercial bank 22,458,963

Thrift bank 94,124,116

327,530,936* Based on Philratings** Based on Standard & Poor’s rating

***Unrated short term deposits and corporate bonds are issued by local commercial and universal banks.

The credit quality of cash and cash equivalents is based on the Bangko Sentral ng Pilipinasclassification of banks operating in the Philippines based on total resources. The remaining balance ofcash and cash equivalents as at December 31, 2012 represents cash on hand of P24,175,834(2011 - P24,586,092).

Unrated counterparties, however, have no history of default.

(24)

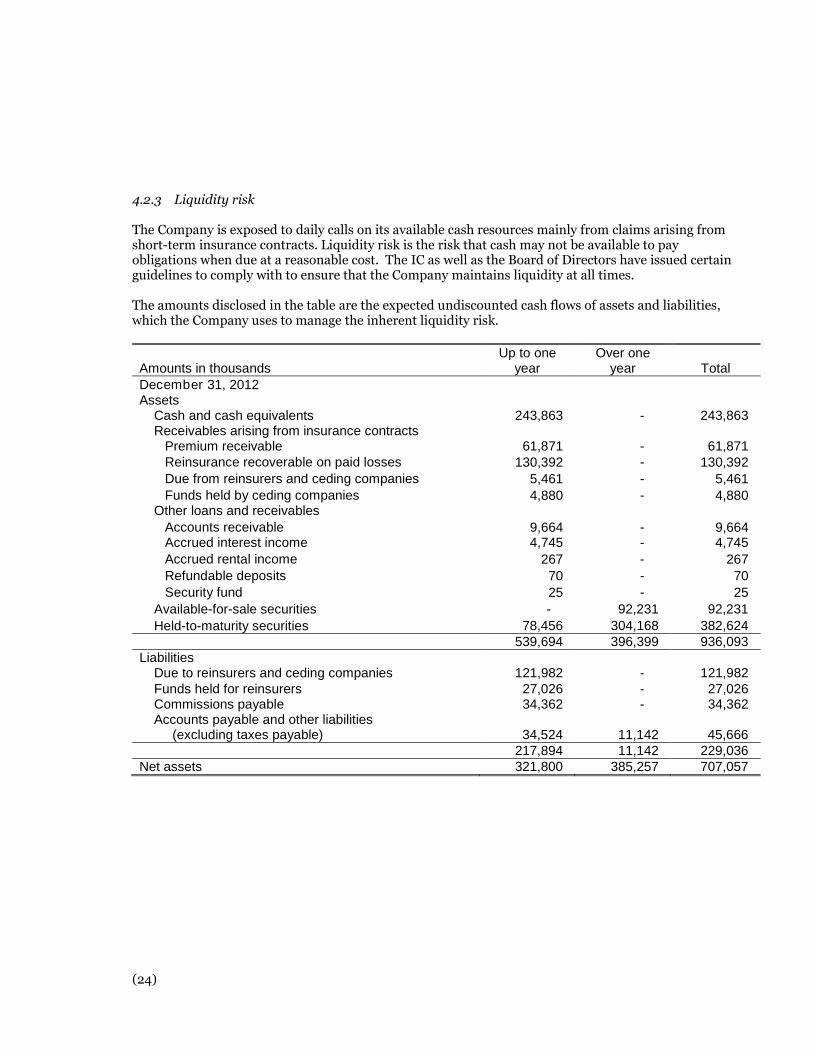

4.2.3 Liquidity risk

The Company is exposed to daily calls on its available cash resources mainly from claims arising fromshort-term insurance contracts. Liquidity risk is the risk that cash may not be available to payobligations when due at a reasonable cost. The IC as well as the Board of Directors have issued certainguidelines to comply with to ensure that the Company maintains liquidity at all times.

The amounts disclosed in the table are the expected undiscounted cash flows of assets and liabilities,which the Company uses to manage the inherent liquidity risk.

Amounts in thousandsUp to one

yearOver one

year TotalDecember 31, 2012Assets

Cash and cash equivalents 243,863 - 243,863Receivables arising from insurance contracts

Premium receivable 61,871 - 61,871Reinsurance recoverable on paid losses 130,392 - 130,392Due from reinsurers and ceding companies 5,461 - 5,461Funds held by ceding companies 4,880 - 4,880

Other loans and receivables

Accounts receivable 9,664 - 9,664Accrued interest income 4,745 - 4,745

Accrued rental income 267 - 267Refundable deposits 70 - 70Security fund 25 - 25

Available-for-sale securities - 92,231 92,231

Held-to-maturity securities 78,456 304,168 382,624539,694 396,399 936,093

LiabilitiesDue to reinsurers and ceding companies 121,982 - 121,982Funds held for reinsurers 27,026 - 27,026Commissions payable 34,362 - 34,362Accounts payable and other liabilities

(excluding taxes payable) 34,524 11,142 45,666217,894 11,142 229,036

Net assets 321,800 385,257 707,057

(25)

Amounts in thousandsUp to one

yearOver one

year Total

December 31, 2011Assets

Cash and cash equivalents 352,117 - 352,117

Receivables arising from insurance contractsPremium receivable 53,152 - 53,152

Reinsurance recoverable on paid losses 85,526 - 85,526

Due from reinsurers and ceding companies 5,020 - 5,020Funds held by ceding companies 4,092 - 4,092

Other loans and receivables

Accrued interest income 4,248 - 4,248

Accounts receivable 9,255 - 9,255

Refundable deposits 70 - 70

Security fund 25 - 25Available-for-sale securities - 91,079 91,079

Held-to-maturity securities 19,495 206,101 225,596532,996 297,180 830,180

LiabilitiesDue to reinsurers and ceding companies 60,107 - 60,107Funds held for reinsurers 34,132 - 34,132Commissions payable 23,131 - 23,131Accounts payable and other liabilities

(excluding taxes payable) 29,091 8,538 37,629146,461 8,538 154,999

Net assets 386,539 288,641 675,180

4.3 Fair value of financial assets and financial liabilities

The Company’s available-for-sale financial assets measured at fair value amounting to P90.67 millionand P89.5 million in 2012 and 2011, respectively, are classified as Level 1.

There are no significant financial instruments that fall under Level 2 and Level 3 categories in 2012 and2011.

(26)

The table below summarizes the carrying amounts and fair values of those financial assets andliabilities at December 31 that are not presented in the statement of financial position at fair value.

2012 2011Carrying

value Fair valueCarrying

value Fair valueFinancial assets

Cash and cash equivalents 243,862,773 243,862,773 352,117,028 352,117,028

Receivables 14,770,282 14,770,282 13,598,366 13,598,366Held-to-maturity securities 382,623,710 391,394,106 225,595,876 244,206,819

Financial liabilitiesCommission payable 34,362,509 34,362,509 23,130,504 23,130,504Accounts payable and other liabilities

(excluding taxes payable) 45,665,902 45,665,902 37,629,673 37,629,673

The method and assumptions used by the Company in estimating the fair value of financialinstruments are as follows:

Cash in banks and cash equivalents

The estimated fair value of interest bearing deposits is based on discounted cash flows using prevailingmoney market interest rates for debts with similar credit risk and remaining maturity.

Receivables

The estimated fair value of loans and receivables represents the discounted amount of estimated futurecash flows expected to be received. Expected cash flows are discounted at current market rates todetermine fair value. Due to short term nature of the receivables, the carrying amount approximatesfair value.

Held-to-maturity and available-for-sale securities

Fair values of held-to-maturity and available-for-sale securities are based on market prices orbroker/dealer price quotations. Where this information is not available, fair value is estimated usingquoted market prices for securities with similar credit, maturity and yield characteristics.

Financial liabilities

The estimated fair value of liabilities with no stated maturity is the amount repayable on demand.

4.4 Capital management

The Company’s objectives when managing capital are:

to comply with the minimum capitalization requirement, Margin of Solvency (MOS) andRisk-Based Capital (RBC) model set by the IC;

to safeguard the Company’s ability to continue as a going concern so that it can continue to providesecurity for its policyholders, returns for shareholders and benefits for other stakeholders; and

to maintain a strong capital base to support the development of its business.

(27)

The Company calculates its capital as equity as shown in the statement of financial position.

The Company maintains a certain level of capital to ensure solvency margin in excess of regulatoryrequirements, which in turn, protects its policyholders.

To ensure compliance with these externally imposed capital requirements, it is the Company’s policy toassess its position, at least on a quarterly basis, against set minimum capital requirements. TheCompany elevates any requirement for additional capital infusion to its shareholders to address anyforeseen capital deficiency.

The level of MOS is monitored by the Company’s management, employing the procedures based on theguidelines developed by the IC.

The Company also manages its capital through its compliance with the following regulatoryrequirements:

4.4.1 Fixed capitalization

In September 2006, the Department of Finance issued Order 27-06 increasing the capitalizationrequirements for insurance and reinsurance companies on a staggered basis for the five years endedDecember 31, 2006 up to 2011. Depending on the level of foreign ownership in the insurance company,the minimum statutory net worth and minimum paid-up capital requirements vary. The statutory networth includes the Company’s paid-up capital, capital in excess of par value, contingency surplus,retained earnings and revaluation increments as may be approved by the IC. The minimum paid-upcapital is pegged at 50% of the minimum statutory net worth.

The IC, in accordance with Department Order 27-2006 and Circular Letter 26-2008, required non-lifecompanies existing, operating, or otherwise doing business in the Philippines with more than fortypercent (40%) but less than sixty percent (60%) foreign equity to possess minimum paid-up capital ofP350 million as at December 31, 2012 and 2011, respectively (Note 14).

The Company is compliant with this requirement of the IC.

4.4.2 Risk-based capital

In October 2006, the IC issued Insurance Memorandum Circular No.7-2006 adopting the risk-basedcapital framework for non-life insurance industry to establish the required amounts of capital to bemaintained by insurance companies in relation to their investment and insurance risks. Every non-lifeinsurance company is annually required to maintain a minimum RBC ratio of 100% and not fail thetrend test. The insurance company will be subjected to the corresponding regulatory intervention uponits failure to meet the minimum RBC ratio.

The following table shows how the RBC ratio compliance was determined by the Company:

2012 2011

Net worth 644,795,277 617,300,971

RBC requirement 358,075,148 347,953,590

RBC ratio 180% 177%

The Company is compliant with this requirement of the IC.

(28)

4.4.3 Margin of solvency requirements

Under the Insurance Code, a non-life insurance Company doing business in the Philippines shall maintainat all times a MOS equal to P500,000 or 10% of the total amount of its net premiums written during thepreceding year, whichever is higher. The MOS shall be the excess of the value of its admitted assets (asdefined under the Insurance Code), exclusive of its paid-up capital over the amount of its liabilities,reserve for unearned premiums and reinsurance reserves.

Reserve for unearned premiums determined in accordance with the Insurance Code for purposes of MOSamounts to P109,931,696 (2011 - P93,345,792).

The estimated amount of non-admitted assets as at December 31 as defined in the Insurance Codeconsists of the following:

2012 2011

Deferred acquisition costs, net 84,849,495 61,940,595

Receivables 23,553,119 16,195,870

Available-for-sale securities - 2,500,000

Property and equipment, net 4,450,548 1,511,114

Other assets 9,492,464 10,780,359

122,345,626 92,927,938

The final amounts of MOS can only be determined after the accounts of the Company have beenexamined by the IC specifically as to admitted and non-admitted assets as defined in the Insurance Code.