argus bitumen€¦ · · 2017-06-08pockets of bitumen 60/70 demand emerged, including from north...

TRANSCRIPT

Copyright © 2017 Argus Media Ltd

Pockets of bitumen 60/70 demand emerged, including from north

Africa, but most markets were slow with summer holidays

and falling crude and fuel oil prices hitting buying activity.

Domestic requirements in Mediterranean exporting coun-

tries like Italy, Spain and Greece remained at seasonally low

levels, before an expected rise from September onwards.

But export activity was boosted by a surge in Moroccan

import demand. That was thanks to the continued shutdown

of the Samir refinery in Mohammedia, with no prospect for

a restart before October at the earliest, amid deep financial

problems affecting the company.

In Europe cargo export price levels relative to fob R t-

Bitumen prices at key locations $/t

Low High

Domestic prices

Northern Germany 300 316 +1

Northern France 344 361 +1

Hungary 333 344 +1

Italy 305 316 +1

South Korea 714 741 nc

Indonesia 430 430 -6

Singapore 415 425 nc

terdam high-sulphur fuel oil quotes were assessed $15-20/t Export prices Delivery method stronger in the -$5/t to +$10/t range, reflecting full utilisa- Poland-Germany truck, ex ref 272 283 -10

tion of regional bitumen tanker fleets, shipments into the Hungary-Romania truck, ex ref 277 294 -10

new Dagenham terminal in southeast England and arbitrage Italy cargo fob 206 210 -11

nean market. Ivory Coast cargo fob 260 270 -9

Bahrain prices dropped to nearly a seven-year low at Iran cargo fob 280 290 nc

$325/t fob. Singapore prices also saw a fall, trading at Singapore cargo fob 335 345 -10

around $340/t. The gap between high-sulphur fuel oil 180cst Taiwan cargo fob 315 325 -10

Singapore and bitumen 80/100 widened to nearly $100/t impacting Delivered cargo prices cfr

negotiations in the region.

Iranian prices are also expected to see a downward price Mediterranean Gebze, Turkey, bulk 241 251 -15

revision next week, with traders expecting to see a mini- North Africa Alexandria, bulk 253 263 -15

mum of $15/t downward revision to vacuum bottom feed- East Africa Mombasa, drum 403 413 nc

stock prices. West Africa Lagos, bulk 309 319 -13

South China coast 355 400 -12

Argus Bitumen Europe, Africa, Middle East and Asia-Pacific prices and commentary

Incorporating Argus Asphalt Report

Issue 17-033| Friday 2 Jun 2017

Summary Price

interest in moving cargoes into a strengthening Mediterra-

North Sea Dated vs Rotterdam domestic $/bl East China coast 350 410 -12 North China coast 345 350 -15

North Sea Dated

80

Rotterdam domestic

70

60

50

40

30

28 Nov 16 06 Mar 17 29 May 17 21 Jun 17

CONTENTS

Key bitumen prices 1

Map of waterborne bitumen prices 2

Northwest and central Europe 3-4

Mediterranean 5-6

Sub-Saharan Africa 7-8

Asia-Pacific and Middle East 9-13

Bitumen news 14-16

Issue 17-033| Friday 2 Jun 2017

Argus Bitumen

A O I M P I S, FO

Copyright © 2017 Argus Media Ltd Page 2 of 16

High

Rotterdam, Netherlands

-5

+10

+18

Spain -15 -10 +2

Italy -15 -10 +8

Greece -10 -5 +4

Albania -35 -25 +5

Morocco -50 -40 +5

Ivory Coast +40 +50 +10

rotterdam

$220/t

Italy

$208/t

Albania

$191/t

Spain

$208/t

Greece

$213/t

South Korea

$305/t

Morocco

$176/t

Ivory coast

$266/t

bahrain

$325/t

Iran

$285/t

Singapore

$340/t

taiwan

$320/t

thailand

$320/t

CARGO FLOWS

The continued shutdown of the 220,000 b/d Samir refinery

in Mohammedia amid financial difficulties drew a surge of

export cargoes into Morocco.

The 6,654 DWT Asphalt Summer was scheduled to arrive

in Mohammedia on 25 August with a cargo from the Agio

Theodori terminal in Greece, the first of four such planned

consignments from the Greek terminal to Moroccan ports.

At least one of the cargoes is to be delivered into the Nador

terminal in eastern Morocco.

Europe and Africa cargo export differentials to HSFO $/t

Waterborne markets, differential to HSFO $/t Mediterranean cargo freight rates $/t

Low High ±

Rotterdam

Italy

Ivory Coast 75

50

25

Spain

Greece Aspropyrgos-Corinth-Gebze-Mersin 30 35 nc

Tarragona-Ghazaouet 30 40 nc

Livorno-Rades 45 55 nc

Mohammedia-Ghazaouet 30 40 nc

Aspropyrgos-Corinth-Alexandria 40 50 nc

0

-25

-50

-75

05 Sep 16 09 Jan 17 01 May 17 21 Jun 17

Mideast Gulf to Africa freight rates $/t

Low High ±

Bandar Abbas/Jebel Ali-Mombasa (drums) 40 50 nc

Bandar Abbas/Jebel Ali-Dar es Salaam (drums) 40 50 nc

Bandar Abbas/Jebel Ali-Djibouti (drums) 40 50 nc

Copyright © 2017 Argus Media Ltd Page 3 of 16

Issue 17-033| Friday 2 Jun 2017

Argus Bitumen

N ANd N A p A N A

summary Cargo export price levels relative to fob Rotterdam high-sul-

phur fuel oil quotes were assessed $15-20/t stronger in the

-$5/t to +$10/t range, reflecting full utilisation of regional

bitumen tanker fleets, shipments into the new Dagenham

terminal in southeast England and arbitrage interest in mov-

ing cargoes into a strengthening Mediterranean market.

uk

The UK market remained slow as the August holiday period

hit paving activity. Prices were assessed £10/t down at £255-

270/t on an ex-works basis in southern England.

The downward price move was partly linked to antici-

pated Trafigura-supplied truck flows from the new Stolthaven

Dagenham terminal in the river Thames in east London. The

terminal received a fresh bitumen cargo, shipped from La

Coruna, Spain, on board the Theodora on 20 August after the

first cargo was discharged there on 9 August.

France/Benelux The French market was especially quietly and thinly dis-

cussed in the August holiday period, while Benelux markets

were expected to start becoming active from the last week

of August after the restart of mixed asphalt plants after

usual summer holiday period shutdowns.

Prices held steady after recent intra-month losses reg-

istered in Belgium and the Netherlands. Low-prices truck

export flows were heading for Germany from Benelux. A

bitumen cargo was being moved on board the 5,897 DWT

tanker Iver Action from Antwerp to Mostaganem, Algeria,

arriving 28 August.

Germany Falling HSFO prices and weak August demand meant the

domestic bitumen market was muted.

Official prices for some domestic refinery volumes stayed

at €320-330/t ex-works, but price assessments stayed sub-

stantially below those values, reflecting actual selling prices

by most suppliers. Significant rebates were being offered on

official prices to stimulate business.

Low priced imports have been coming into Germany from

Antwerp as well as Poland where export prices to Germany

slipped to around €250/t ex-works.

Tight infrastructure budgets were hitting bitumen

demand in Germany, estimated at least 10pc down on last

year.

Next year could see improved demand because of an

expected rise in spending on infrastructure.

Northwest and central Europe bitumen prices

€/t $/t

Low High ± Low High ±

Domestic prices, fob

Southern UK £/t 255 270 -10 399 423 -12

Rotterdam, Netherlands 240 260 nc 266 289 +0

Antwerp, Belgium 240 260 nc 266 289 +1

Northern Germany 270 285 nc 300 316 +1

Northeast Germany 265 280 nc 294 311 +1

Southern Germany 260 275 nc 289 305 +1

Southwest Germany 260 275 nc 289 305 +1

Western Germany 265 280 nc 294 311 +1

Hungary 300 310 nc 333 344 +1

Romania 295 310 -8 327 344 -7

Czech Republic 280 300 nc 311 333 +1

Export prices, fob

Poland-Germany (truck) 245 255 -10 272 283 -10

Czech Republic-Germany (truck) 260 270 nc 289 300 +1

Poland-Romania (truck) 245 255 -5 272 283 -5

Hungary-Romania (truck) 250 265 -10 277 294 -10

Rotterdam (cargo) 212 227 -2

Domestic prices, delivered

Southern UK £/t 270 280 -10 423 438 -13

Brussels 250 270 nc 278 300 +1

Northern France 310 325 nc 344 361 +1

Central France 315 330 nc 350 366 +1

Crude and refined products

Low High ±

Urals cif Rotterdam $/bl 42.44 46.06 -2.25

Fuel oil 3.5%S, fob RMG barge $/t 203.75 231.00 -20.00

Fuel oil straight-run 0.5% fob cargo $/t 275.00 300.50 -13.62

Fuel oil straight-run M-100 cif cargo $/t 212.75 239.00 -20.00

Vacuum gasoil 0.5%S cif cargo $/t 329.75 353.50 -14.12

Czech republic/poland/Hungary Demand in the Czech Republic was steady with some regular

demand for bitumen from construction work. The supply

situation was more than keeping pace with demand.

Market participants said there had been no impact on

bitumen supply from a fire at the Litvinov refinery which has

halted petrochemical production. The fire at the petrochem-

ical plant has not directly affected the 103,000 b/d refinery.

Cheaper Polish imports have been offered into the Czech

market, undercutting local supplies as domestic demand in

Copyright © 2017 Argus Media Ltd Page 4 of 16

Issue 17-033| Friday 2 Jun 2017

Argus Bitumen

N and n p n

Poland remains so poor, pushing product out for export.

Hungarian trucked bitumen flows to Poland were indi-

cated around €245/t ex-works.

romania Domestic road construction activity and bitumen require-

ments remained at low levels, with August proving to be a

weak month because of hot weather restricting asphalt pav-

ing work while the holiday period has also had a dampening

impact on project activity.

While road construction projects are still expected to

generate sizeable bitumen requirements during September

and October, a 20pc downward revision in the 2015 calendar

year Romanian government road construction budget — an-

nounced in mid-August — was expected to reduce the rate

of activity and dampen overall bitumen consumption this

autumn. The budget cut amounted to around 1bn Romanian

New Leu (€220mn), with the cut likely to discourage some

banks from lending for Romanian infrastructure projects.

Price levels continued to slip, with Serbian export flows

to Romania from the Pancevo refinery indicated around

€250/t ex-refinery. Hungarian export prices slipped to €255-

265 ex-refinery, with €8-10/t discounts applied on some

sales to large customers. The bulk of Polish export flows to

Romania were being sold at around €250/t ex-refinery, €5/t

lower than the previous week, although even lower prices

were heard.

Domestic truck sales from the Rompetrol refinery in

Ploiesti were assessed in the €295-310/t ex-refinery range,

€5-10/t down on previous levels.

Balkans

Export volumes from the Serbian refinery in Pancevo were

Germany: North vs South $/t

Northern Germany Southern Germany

400

350

300

250

200

28 Nov 16 06 Mar 17 29 May 17 21 Jun 17

reported at prices down to around €220/t ex-refinery for

truck shipments to Bulgaria and €215/t for flows to FYROM

(Macedonia).

Supplies from the Hellenic Petroleum refinery in Thessa-

loniki, northern Greece, into Bulgaria were indicated around

$250/t (€220-225/t), with those truck shipments being

made at $12/t premiums to fob Mediterranean HSFO quotes.

Bosnia-Herzegovina export flows from the Bosanski Brod

refinery were reported at $235-24/t (€210-215/t) ex-refinery

for Pen 50/70, 70/100 and 160/220 grades.

While stiff competition was bearing down on regional

price levels, export availability from Serbia was being re-

stricted by domestic demand for highway project work.

Bulgarian bitumen demand, much of it in the form of

polymer-modified bitumen, is expected to be stepped up

from end-August/early September after the holiday season.

Total bitumen consumption in the country is expected to

jump to around 170,000t this year after dropping to 120,000t

in 2014, from 140,000t in 2013. The main bulk of bitumen

requirements are for work on sections of the Struma and

Maritza highways. Prices for standard PMB grades used in

Bulgaria were indicated at €360-365/t ex-works from Serbia,

but as high as €450/t ex-works Burgas, Bulgaria.

The 83,000 b/d Thessaloniki refinery is to be shut for a

few days in the first half of September for maintenance

work, although the shutdown is not expected to impact on

bitumen availability (see news section).

portugal Buoyant bitumen demand in Portugal means there will be no

export cargoes available from the Viana do Castelo terminal

— close to the Galp bitumen-producing refinery in Oporto in

the north of the country — until October at the earliest.

scandinavia Norwegian bitumen consumption jumped by around 40pc

year on yearin the month of June, underlining a bullish per-

formance during the first half of 2015 (see news).

A planned September shutdown at Shell’s 70,000 b/d

Fredericia refinery in Denmark is expected to impact bitu-

men availability on that market, but potentially also flows

from the refinery into Norway.

The Swedish bitumen market has been stable this year,

with estimated consumption remaining in the 450,000-

500,000t range with construction activity back under way

throughout August after the usual shutdown in July.

Copyright © 2017 Argus Media Ltd Page 5 of 16

Issue 17-033| Friday 2 Jun 2017

Argus Bitumen

M A A MA MM A

Summary While domestic requirements in Mediterranean exporting

countries like Italy, Spain and Greece remained at season-

ally low levels, before an expected rise from September

onwards, export activity was boosted by a surge in Moroccan

import demand. That was in turn to the continued shutdown

of the Samir refinery in Mohammedia, with no prospects for

a restart before October at the earliest, amid deep financial

problems affecting the company.

Cargo activity to Morocco from Greece, Italy and Spain,

coupled with sizeable continuing flows into Egypt and Alge-

ria, were a factor — along with falling high-sulphur fuel oil

prices — in driving down discounts to Mediterranean fuel oil

quotes. Italian export discounts were assessed at $10-15/t,

versus $15-25/t previously, with some volumes reportedly

offered at flat to $5/t discounts to fuel oil quotes – although

some volumes were still being sold around $20/t discounts.

Greek exports were indicated at $5-10/t discounts to fuel

oil and Spanish volumes at $10-15/t. Moroccan and Albanian

assessed discounts also narrowed, although Morocco is for

now purely an importer, while no Albanian export cargoes

were reported being offered.

The regional cargo market strength meant there was less

interest in arbitrage exports to the US, while the Mediter-

ranean continued to attract flows from northwest Europe.

Movements to Saudi Arabia continue, with a trading firm

looking for a tanker to move 5,000-7,000t of bitumen from

Ravenna, Italy, to Jubail or Yanbu for prompt to early Sep-

tember shipment, although no booking was yet made.

Morocco

The continued shutdown of the 220,000 b/d Samir refinery

in Mohammedia amid financial difficulties (see news), with

Italy domestic less bitumen fuel oil blendstock value $/t

300

250

200

150

100

50

28 Nov 16 06 Mar 17 29 May 17 21 Jun 17

Mediterranean bitumen prices

Local currency/t $/t

Low High ± Low High ±

Domestic prices, fob Italy 275 285 nc 305 316 +1

Southern France (delivered) 315 330 nc 350 366 +1

Northeast Spain 340 360 nc 377 400 +2

Southwest Spain 320 340 nc 355 377 +1

Izmit, Turkey 684 684 nc 237 237 -9

Izmir, Turkey 684 684 nc 237 237 -9

Batman, Turkey 712 712 nc 247 247 -9

Kirikkale, Turkey 712 712 nc 247 247 -9

Export prices, fob $/t Differential to HSFO

Italy -15 -10 +8 206 210 -11

Greece -10 -5 +4 210 216 -15

Spain -15 -10 +2 206 210 -16

Albania -35 -25 +5 186 196 -14

Morocco -50 -40 +5 170 180 -14

Delivered cargo prices, cfr Alexandria, Egypt 253 263 -15

Gebze-Mersin, Turkey 241 251 -15

Ghazaouet, Algeria 222 232 -15

Rades, Tunisia 253 263 -11

Economics Mid ±

Bitumen’s value as a fuel oil blendstock $/t 174 nc

Crude and refined products, 15-21 Aug

Low High ± Basrah Light fob Sidi Kerir $/bl 38.29 41.91 -2.12

Urals cif Augusta $/bl 43.09 46.66 -2.28

Iran Heavy fob Sidi Kerir $/bl 40.37 43.94 -2.83

Fuel oil 3.5% fob $/t 207.25 233.75 -18.88

VGO 0.5% fob $/t 319.50 345.00 -14.88

no prospect of an early restart, drew a surge in cargo export

business to the country. Morocco is usually a net bitumen

exporter, with its two bitumen units at Mohammedia having

420,000 t/yr of combined production capacity.

Traders and ship brokers expect the refinery to remain

shut at least until October, meaning bitumen cargo import

flows are set to continue. A crude tanker was awaiting dis-

charge at Mohammedia, but it was unclear if and when the

volume can be moved into the refinery to enable its restart.

The 6,654 DWT Asphalt Summer was scheduled to arrive

in Mohammedia on 25 August with a cargo from the Agio

Theodori terminal in Greece, the first of four such planned

consignments from the Greek terminal to Moroccan ports.

At least one of the cargoes is to be delivered into the Nador

terminal in eastern Morocco. Additionally, a cargo was

Copyright © 2017 Argus Media Ltd Page 6 of 16

Issue 17-033| Friday 2 June 2017 Argus Bitumen

M A A MA MM A

moved from Cadiz to Mohammedia on board the 4,999 DWT

Sunpower, arriving 17 August, while a Spanish refiner moved

a cargo on board the Castillo de Pambre on 19-20 August

into Laayoune in the disputed territory of Western Sahara

governed by Morocco.

Turkey

Political uncertainty and its impact on construction sec-

tor activity is set to continue after Turkish President Recep

Tayyip Erdogan announced snap elections will be held on 1

November. That followed inconclusive elections in June that

were followed by the inability of Turkish political parties to

form a governing coalition.

The lack of government has badly impacted decision-

making and fund allocation for road and other infrastructure

projects in recent months, forcing down bitumen demand

as some projects have been halted and others slowed by

contractors worried about payment for project work.

Discounts to some customers below published levels

helping to discourage imports. One buyer said such discounts

in some cases now amounted to levels up to TL100/t for

larger orders.

Tupras published prices remained by 21 August at latest

levels set on 15 August after TL21/t price cuts. In dollar

terms, prices for pen 50/70 and 70/100 bitumen supplied

domestically from Tupras refineries in Izmit and Izmir fell

over the week by $8-9/t to the $235-240/t range.

Some import cargoes were still arriving, with a 4,500t

cargo moved on board the Lagan into Gebzel, to be fol-

lowed by another cargo on board an undisclosed vessel for

end-August arrival. A separate cargo shipment on board the

Iver Agile was reported being made by a trader into storage

tanks in Mersin.

Spain Bitumen demand levels remained low during the holiday

period in August, but there was still some road construc-

tion work generating some bitumen requirements before an

expected resumption in activity from September onwards.

A busy construction period is expected in the run-up to the

general election on 20 December.

The planned maintenance shutdown for about a month

from early September of crude and vacuum distillation,

as well as other units, at the Cepsa refinery in Huelva is

expected to impact bitumen production. Although stocks are

likely to be built up ahead of the turnaround, market avail-

ability is likely to be impacted as the autumn road paving

season gets under way in Spain coinciding with a surge in

export business to Morocco.

Algeria

There was a continued steady stream of import shipments

into the busy Algerian market. The Black Shark discharged

a cargo into Skikda on 17-18 August, to be followed by the

Iver Brilliant on 18-20 August, while the Sonatrach vessel Ain

Zeft moved a cargo from Tarragona to Oran and then Skikda

is an apparent two-port discharge, arriving in Skikda on 20

August.

Argus Asia-Pacific and Middle East Bitumen 2015

2-4 September 2015 • Singapore

3 days with the industry’s most senior executives

from across the world

Italy domestic and Mediterranean HSFO barges $/t

600 Italy domestic HSFO Med

500

400

300

200

100

28 Nov 16 06 Mar 17 29 May 17 21 Jun 17

www.argusmedia.com

Copyright © 2017 Argus Media Ltd Page 7 of 16

Issue 17-033| Friday 2 June 2017 Argus Bitumen

SUB-SAHARAN A A AR N AR

$/t Low High ±

Summary East African buying was expected to pick up after an antici-

pated drop in Iranian export prices on 22 August, while the

South African market was entering a three-month period

that is likely to see substantial demand for numerous road

Sub-Saharan Africa bitumen prices

Local currency/t

Low High ±

Domestic prices, fob

South Africa 5,000 5,500 nc 388 427 -5

projects. Import/export prices $/t

Ivory Coast, fob Abidjan (export, cargo) 260 270 -9

West Africa Nigeria, cfr Lagos (import cargo) 309 319 -13

Market activity remained thin, with no enquiries for cargoes Ghana, cfr Takoradi-Tema (import, cargo) 340 370 nc

or tankers to move bulk bitumen from Mediterranean or Kenya, cfr Mombasa (import, drums) 403 413 nc

northwest European export terminals to destinations in west Tanzania, cfr Dar es Salaam (import, drums) 403 413 nc

Africa. Price levels were pushed lower by another drop in Freight rates $/t

HSFO prices, but bitumen export price spreads versus HSFO Abidjan-Lagos-Warri-Port Harcourt (cargo) 35 45 nc

strengthened. Abidjan-Takoradi-Tema (cargo) 30 40 nc

There was still low-level interest in moving bitumen in Tarragona-Lagos-Warri-Port Harcourt (cargo) 100 130 nc

containers into regional outlets. A recent enquiry for 3,000t Bandar Abbas-Jebel Ali-Mombasa (drums) 40 50 nc

of bulk bitumen into Nouakchott, Mauritania, could not be Bandar Abbas-Jebel Ali-Dar es Salaam (drums) 40 50 nc

fulfilled because of lack of terminal facilities to receive the Bandar Abbas-Jebel Ali-Djibouti (drums) 40 50 nc

cargo. There were subsequently reports that bitutainer vol-

umes were being sought instead, responding to anticipated

demand for work on the Mauritanian section of the Trans-

West African Coastal Highway from Mauritania to Nigeria.

There were no signs of a recovery in Nigerian construc-

tion activity that would generate bitumen demand and

import business, with the country’s new government still

preoccupied with sweeping changes in government depart-

ments. Falling crude oil prices are also cutting available

funds for investment in infrastructure and other areas.

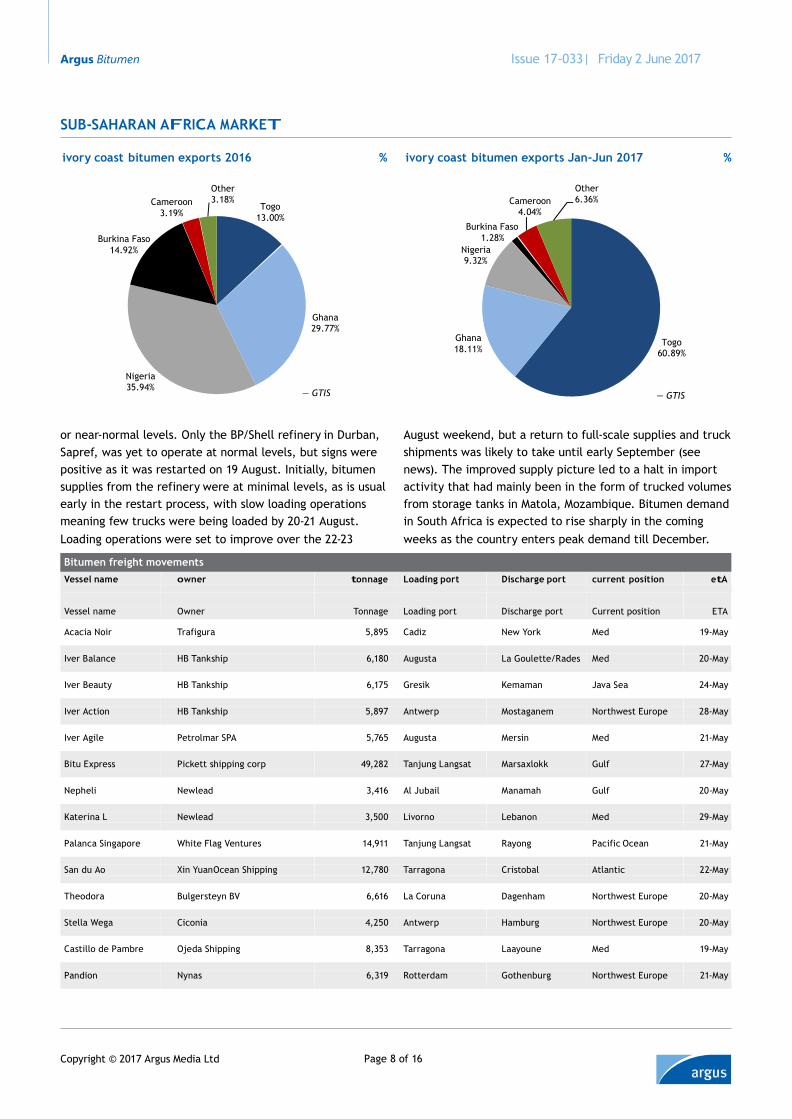

Fresh data indicated that the pattern of Ivory Coast

exports had radically changed over the past year, while the

overall volumes remain low (see p8). Export shipments from

the exporting country, all of them made from the SMB bitu-

men refinery and terminal complex at Abidjan, to Nigeria

and Ghana fell sharply in the first half of 2015 to 9,320t and

Asphalt del West Africa and fuel oil fob Med $/t

18,110t respectively. Those levels were down from 35,940t in

the first six months of last year for Nigeria-bound flows and

29,770t for volumes shipped to Ghana. By contrast Ivory

Coast flows to Togo jumped over the year to 60,880t from

13,000t, indicating a switch to movements into a deep-water

terminal in Lome from which small parcels are then moved

to regional outlets.

east Africa

A sharp drop in Iranian domestic vacuum bottom prices –

amounting to $15-30/t — was expected to be announced at

the start of the new Iranian calendar month, correspond-

ing with 22 August. That was in turn expected to result in

declines in bitumen export prices from the country to east

African and other destinations.

The extent of the likely fall will depend in part on

currency movements, with the US dollar remaining strong

500

400

300

200

100

West Africa waterborne, cfr Med HSFO against the Rial. Some traders were already offering

drummed Iranian export cargoes at prices down to $325-330/

t fob Bandar Abbas in anticipation of the VB price cuts, but

buyers were holding back from making any orders as they

awaited lower priced offers from across the market.

There were regular requests for volumes into Dar es

Salaam, but no firm deals were being made for import of

drummed bitumen consignments from Iran.

South Africa Bitumen availability from South African refineries was im-

28 Nov 16 06 Mar 17 29 May 17 21 Jun 17 proving as nearly all refineries were now running at normal

Copyright © 2017 Argus Media Ltd Page 8 of 16

Issue 17-033| Friday 2 June 2017 Argus Bitumen

SUB-SAHARAN A A AR N AR

ivory coast bitumen exports 2016 % ivory coast bitumen exports Jan-Jun 2017 %

Burkina Faso

14.92%

Cameroon

3.19%

Other

3.18%

Togo

13.00%

Cameroon

4.04%

Burkina Faso

1.28%

Nigeria 9.32%

Other

6.36%

Ghana

29.77%

Ghana

18.11%

Togo

60.89%

Nigeria

35.94% — GTIS

— GTIS

or near-normal levels. Only the BP/Shell refinery in Durban,

Sapref, was yet to operate at normal levels, but signs were

positive as it was restarted on 19 August. Initially, bitumen

supplies from the refinery were at minimal levels, as is usual

early in the restart process, with slow loading operations

meaning few trucks were being loaded by 20-21 August.

Loading operations were set to improve over the 22-23

August weekend, but a return to full-scale supplies and truck

shipments was likely to take until early September (see

news). The improved supply picture led to a halt in import

activity that had mainly been in the form of trucked volumes

from storage tanks in Matola, Mozambique. Bitumen demand

in South Africa is expected to rise sharply in the coming

weeks as the country enters peak demand till December.

Bitumen freight movements

Vessel name owner tonnage Loading port Discharge port current position etA

Vessel name

Owner

Tonnage

Loading port

Discharge port

Current position

ETA

Acacia Noir

Trafigura

5,895

Cadiz

New York

Med

19-May

Iver Balance

HB Tankship

6,180

Augusta

La Goulette/Rades

Med

20-May

Iver Beauty

HB Tankship

6,175

Gresik

Kemaman

Java Sea

24-May

Iver Action

HB Tankship

5,897

Antwerp

Mostaganem

Northwest Europe

28-May

Iver Agile

Petrolmar SPA

5,765

Augusta

Mersin

Med

21-May

Bitu Express

Pickett shipping corp

49,282

Tanjung Langsat

Marsaxlokk

Gulf

27-May

Nepheli

Newlead

3,416

Al Jubail

Manamah

Gulf

20-May

Katerina L

Newlead

3,500

Livorno

Lebanon

Med

29-May

Palanca Singapore

White Flag Ventures

14,911

Tanjung Langsat

Rayong

Pacific Ocean

21-May

San du Ao

Xin YuanOcean Shipping

12,780

Tarragona

Cristobal

Atlantic

22-May

Theodora

Bulgersteyn BV

6,616

La Coruna

Dagenham

Northwest Europe

20-May

Stella Wega

Ciconia

4,250

Antwerp

Hamburg

Northwest Europe

20-May

Castillo de Pambre

Ojeda Shipping

8,353

Tarragona

Laayoune

Med

19-May

Pandion

Nynas

6,319

Rotterdam

Gothenburg

Northwest Europe

21-May

Copyright © 2017 Argus Media Ltd Page 9 of 16

Issue 17-033| Friday 2 Jun 2017

Argus Bitumen

AND MIDDLE A MA MM A

singapore Singapore penetration (pen) 60/70 fob prices widened

further this week to high-sulphur fuel oil 180cst prices by

around $100/t further denting buying interest.

Singapore prices for second-half September loading car-

goes were assessed $10/t lower at $335-345/t fob. Singapore

prices dropped to a six-month low, last trading at these

levels in early March of this year.

A 4,000t cargo was concluded at $340/t fob Singapore to

Vietnam. The buyer will take the delivery of the spot cargo

towards the middle of September. Another 3,200t cargo deal

to an Indonesian buyer was concluded at around $390/t cfr

Indonesia, this netbacks to around $330-335/t fob Singapore.

Buying remains weak across the region as the fall in

crude prices and corresponding drop in the fuel oil prices

made buyers nervous. North Sea prices are trading at a

nearly eight-month low. The weakness of regional currencies

against the US dollar has also slowed down the negotiation

process. The Central bank of Vietnam devalued the Dong

earlier this week by 1pc. This is the second devaluation for

the year of the currency.

One regional producer has already started to offer lower

priced cargoes out of Singapore. The offer price to buyers

was at around $320-325/t fob, but no deals were concluded.

One Singapore based producer is expected to have lower

production of bitumen for October as well. The producer

had halved its production of bitumen for September and is

producing less in August as well.

Trade focus is also shifting more towards end-September

and early October, although buyers pointed out that they

will be in no rush to commit to October volumes.

With the decline in cargo prices, Singapore pen 60/70

and 80/100 tank truck prices were lowered by $33/t at $330-

340/t ex-refinery. Buyers did not commit to truck volumes

Singapore pen 60/70: drummed and bulk $/t

Singapore pen 60/70 drums waterborne

Asia bitumen prices

Local currency/t $/t

Low High ± Low High ± Domestic prices, fob

South Korea 844,955 876,907 +10,114 714 741 nc

Mumbai, India 30,035 32,034 -700 460 490 -18

Mumbai, India

(drums) 33,134 35,134 -700 507 538 -20

Thailand 11,719 12,252 +100 330 345 nc

Indonesia 5,950,000 5,950,000 nc 430 430 -6

Singapore 583 598 +6 415 425 nc

Singapore-Malaysia

ex-ref 464 478 -40 330 340 -32

Japan 53,000 60,000 nc 427 484 +2

Waterborne, fob

Iran 280 290 nc

Iran (drums) 345 380 nc

Bahrain 123 123 -9 325 325 -25

Singapore 471 485 -9 335 345 -10

Singapore (drums) 745 759 +7 530 540 nc

Thailand 11,187 11,542 +95 315 325 nc

South Korea 355,023 366,857 -19,150 300 310 -20

Taiwan 10,227 10,552 -174 315 325 -10

Waterborne, cfr

North China coast 2,206 2,238 -58 345 350 -15 East China coast 2,238 2,621 -38 350 410 -12 South China coast 2,270 2,557 -40 355 400 -12

Northern Vietnam (drums) 540 550 nc

Southern Vietnam (drums) 540 560 nc

Economics Mid ±

Bitumen’s value as fuel oil blendstock, Singapore 208 -25

Crude and refined products

Low High ± Dubai fob Dubai $/bl 45.33 48.50 -3.11

Basrah Light fob Basrah $/bl 44.30 47.18 -2.91

Banoco Arab Medium $/bl 43.70 46.67 -3.72

Fuel oil HS 180cst fob Singapore $/t 230.00 255.75 -22.25

Fuel oil HS 380cst fob Singapore $/t 224.25 248.50 -21.38

Gasoil 0.5% fob Singapore $/bl 54.35 57.25 -1.92

700

600

500

Singapore pen 60/70 waterborne from Singapore due to weak demand. One Singapore based

refiner is expected to revise its tank truck prices either on

22 August or early next week. A Singapore refinery had of-

fered to importers at $335/t ex-refinery.

400

300

200

28 Nov 16 06 Mar 17 29 May 17 21 Jun 17

Malaysia Paving activities had slowed down thanks to poor demand

coupled with high tank inventory.

Domestic prices had moved lower by 75 ringgit/t ($18/t)

and were in the 1,400-1,440 ringgit/t range. Domestic refin-

Copyright © 2017 Argus Media Ltd Page 10 of 16

Issue 17-033| Friday 2 Jun 2017

Argus Bitumen

AND MIDDLE A MAR C MM AR

Bitumen freight, 15-21 Aug $/t

Singapore-east Australia

135

145

nc Singapore-west Australia 85 90 nc

Singapore-Gresik, Indonesia 40 45 nc

Singapore-south China 51 56 -0.5

Singapore-east China 61 71 -0.5

Thailand-south China 51 56 -0.5

Thailand-east China 61 71 -0.5

Thailand-east Australia 147 151 nc

Thailand-west Australia 91 96 nc

Taiwan-Ho Chi Minh, Vietnam 42 45 nc

Taiwan-Haiphong, Vietnam 38 40 nc

South Korea-east China 31 35 -0.5

South China-Haiphong, Vietnam 35 37 nc

Prices at China main refineries

Area Province Refinery Grade Contract

price Yn/t

±

Posted

price Yn/t

±

Contract

price $/t

Posted

price $/t

Northwest Xinjiang Petrochina Karamay AH-70, AH-90, AH-110, AH-130 3,150 -100 3,250 -50 493 508

AH-100, AH-140, AH-180 3,150 -100 3,250 -50 493 508

Sinopec Tahe 90-A 3,250 -50 3,300 -50 508 516

90-B 3,250 -50 3,300 -50 508 516

Shannxi Sinopec Xi’an AH-90 2,950 -50 3,100 nc 461 485

Northeast Liaoning Petrochina Liaohe AH-70, AH-90, AH-110, AH-100, AH-140 2,900 nc 3,050 nc 454 477

Panjin Northern AH-90, AH-110, AH-100, AH-140 2,900 -100 3,050 -50 454 477

North Hebei Petrochina Qinhuangdao AH-70, AH-90 2,900 nc 3,000 -50 454 469

Central Henan Sinopec Luoyang AH-90 2,950 -100 3,050 -100 461 477

East Shandong CNOOC asphalt AH-70, AH-90 2,800 -200 3,150 -100 438 493

Sinopec Qilu 70 -A 2,800 -200 2,850 -200 438 446

90 -A, 70-B 2,750 -200 2,800 -200 430 438

90-B 2,700 -200 2,750 -200 422 430

Zhejiang Sinopec Zhenhai 70-A, 90-A 2,750 nc 2,800 nc 430 438

70-B, 90-B 2,700 nc 2,750 nc 422 430

Petrochina Wenzhou AH-70, AH-90 2,650 nc 2,750 nc 415 430

Shanghai Sinopec Shanghai AH-70 2,700 -50 2,900 -100 422 454

Jiangsu CNOOC Taizhou AH-70, AH-90 2,900 -150 3,150 -100 454 493

Sinopec Jinling 70-A, 90-A 2,700 -50 2,900 -100 422 454

Petrochina Xingneng 70-A, 90-A 2,700 -100 2,800 -150 422 438

Jangyin Alpha 70-A, 90-A 2,700 -100 2,800 -150 422 438

South Guangdong Sinopec Maoming 70-A, 90-A 2,750 nc 2,900 -100 430 454

Sinopec Guangzhou 70-A, 90A 2,750 nc 2,900 -100 430 454

Petrochina Gaofu AH-70, AH-90 2,750 nc 2,900 -100 430 454

West Sichuan CNOOC Luzhou AH-70, AH-90 3,600 nc 3,650 nc 563 563

Thailand

Thai export prices were stable this week at $315-325/t fob.

The weakening of the Thai Baht did not impact the

bitumen market as improved domestic demand with more

construction tender projects for the third quarter of the

year were approved.

A domestic producer had received a bid of $300/t for

5,000t from south China buyer, but Thai refineries had no

plans to export for September as domestic demand was

expected to pick up further.

Domestic prices were stable at $330-345/t fob with lim-

ited availability for August. An upward price revision on the

domestic prices was expected for September loadings.

eries were offering cargoes at 1,400-1,440 ringgit/t. An in-

ternational trader who had imported 50,000t from Spain for

August had offered tank truck cargoes to dealers at $345/t

ex-Langsat last week, but was met with limited response. It

was unknown if any volumes had been sold this week.

Indonesia

Increased disbursement of construction funds from the Indo-

nesian government had improved domestic demand from last

week, with increased lifting from contractors. Full demand

was expected to pick up only from end of September when

more budget funds are expected to be released.

Copyright © 2017 Argus Media Ltd Page 11 of 16

Issue 17-033| Friday 2 Jun 2017

Argus Bitumen

AND MIDDLE A MA MM A

A domestic importer had purchased 3,200t for Septem-

ber at $390/t cfr Makassar from a Singapore refinery. This

netbacks to $330/t fob, taking freight of around $60/t. The

importer was looking to purchase another 5,000t from an-

other Singapore refinery with a buying price idea of $340/t

fob and another 5,000t from a Malaysian refinery, which had

offered to the importer at $320/t, with no deal concluded.

The domestic importer who had previously locked down

August term cargoes from Singapore refineries had negoti-

ated to only receive partial shipment from its purchase due

to high tank inventory at its terminals.

Another domestic importer bought 3,200t mid-end

September cargo of India origin from a Singapore trader

at $380/t cif east Indonesia. The importer is to pay a 5pc

import tax, this netbacks to around $399/t cif. With freight

estimated at $60-70/t from India to eastern Indonesia ports,

the cargo netbacks to $329-339/t fob India.

south korea Tracking the decline in the regional market, South Korea

pen grade 60/70 and 80/100 were assessed lower by $20/t at

$300-310/t fob.

A mid-sized refiner concluded the sale of its three spot

cargoes earlier this week via tender. The tender may have

concluded at around $285-288/t fob, a premium of around

$25/t to hsfo 180 on 19 August.

With the drop in domestic prices in China, importers said

that they will be able to buy South Korean cargoes at around

$310/t fob. Two mid-sized refiners are expected to issue sell

tenders next week.

Vietnam Domestic demand had not picked up from previous weeks.

The state-owned refiner bought 4,000t cargo from Singa-

Delivered cargoes: North and South China $/t

Australia import cargo prices $/t

Low High ±

Thailand fob (Class 170)

350

360

-10

Thailand fob (Class 320) 350 360 -10

Singapore fob (Class 170) 350 360 -10

Singapore fob (Class 320) 370 375 -10

pore at $340/t fob for mid-September delivery.

Other domestic importers were looking to purchase a

4,500t shared vessel of Taiwanese cargoes for second-half

September and October with buying price ideas at $370-390/

t cfr north Vietnam. This netbacks to $325-345/t fob Taiwan,

taking freight and insurance costs at $40-45/t to Ho Chi Minh

or Haiphong depending on ullage availability by then. No

deals had been concluded.

Other domestic importers buying idea hovered at $320-

330/t fob Singapore, with no deals concluded due to limited

cargo availability form Singapore. Domestic sellers were

continuing to sell bitumen below imported price for July and

August to create space in their tanks.

taiwan

Tracking the decline in regional prices, Taiwan bulk cargo

prices were down by $11/t at $315-325/t fob.

Paving activities were stable due to good weather but a

typhoon was expected to arrive this weekend. The domes-

tic producer who had sold 20,000-30,000t for its domestic

market kept its domestic prices stable at 17,500 TWD/t.

The producer was expected to have a downward revision on

its domestic price next week as there have been lesser

construction projects available. A private supplier which had

started negotiation for October cargoes had not finalized

its October volume availability. Limited ullage availability

in all Vietnam ports had resulted in some loading delays for

August cargoes.

600

550

500

450

400

350

300

North China

South China china Import cargoes to China were down by another $15/t to

$345-350/t cfr north China, down by $13/t to $350-410/t cfr

east China and down by $13 /t to $355-400/t cfr south China.

The market was lower during the week as crude and

fuel oil values continued to fall. Domestic refiners reduced

prices by 50-200 Yuan/t, as production volumes remain

high due to better margins when compared with fuel oil or

petroleum coke. Large-scale construction activities have

not fully started and consumption is still not high to balance

28 Nov 16 06 Mar 17 29 May 17 21 Jun 17 the output. The lower-than-expected consumption is partly

Copyright © 2017 Argus Media Ltd Page 12 of 16

Issue 17-033| Friday 2 Jun 2017

Argus Bitumen

ASIA- A I I AND M AS MA MM A

Iranian export sales through the IME, 15-20 Aug

Grade Seller Price $/t Packing Volume t Destination

60/70

Fara Shimi Rooz

330

Bulk

5,000

Export by ship from Bandar Abbas

MTA Holding 405 Drum 6,000 Export by ship from Bandar Abbas

Ayegh Hesar Mehran 310 Bulk 200 Export by ship or truck, supply ex-Tehran

Shimi Tejarat Naghsh Jahan 308 Bulk 2,000 Export by ship or truck, supply ex-Esfahan

Kimiya Sanat Aradan 320 Bulk 300 Export by ship or truck, supply ex-Aradan

Ayegh Bam Bastan 300 Bulk 500 Export by ship or truck, supply ex-Eshtehard

Matin Saz Faal 315 Bulk 200 Export by ship or truck, supply ex-Kordestan

Bam Gostaran 309 Bulk 100 Export by ship or truck, supply ex-Oromieh

RK Refining & Energy 305 Bulk 1,000 Export by ship or truck, supply ex-Tabriz

Ayegh Esfahan 380 Bulk 3,000 Export by ship from Bandar Abbas

Azar Davam Yol 300 Bulk 1,000 Export by ship or truck, supply ex-Tabriz

Poyandegan Fan & Tejarat 272 Bulk 700 Export by ship or truck, supply ex-Esfahan

Negin Gum Pars 315 Bulk 440 Export by ship or truck, supply ex-Tabriz

85/100 Shimi Tejarat Naghsh Jahan 308 Bulk 2,000 Export by ship or truck, supply ex-Esfahan

Exchange rate 1$ = 29,860 rials

because of rainy weather in east and south China, and also

partly due to the crunched funding support from local gov-

ernment. Some projects, especially those sponsored by local

government, have been delayed for lack of funds released

by the local government. Market participants are bearish on

the price, explaining that the big price gap between fuel oil

and bitumen may push bitumen prices to go down further to

narrow the gap.

One mid-sized South Korean refiner was awarded its

September tender, to sell a total of three cargoes to Chinese

importer. The awarded price of $285-288/t fob price is lower

than recent market levels, likely to compensate for the last

expensive cargoes to the importer. The low priced tender

has further dampened buying interest.

A state-controlled refiner is believed to have sold two

September cargoes each 5,000t, one to Vietnam and one to

Indonesia. Both the cargoes are from its Maoming refinery.

The refiner has not decided the export volume for Septem-

ber cargoes from its Zhenhai refinery.

Australia

Paving activities have been slow during the winter season

with lesser purchasing ideas from domestic importers.

Domestic demand was expected to pick up from Octo-

ber which would start the new road project works. Some

US cargoes were being offered in the Australia market, no

firm deals were concluded. Buyers pointed out that the

current volatility in the Asian market is too risky to commit

to US cargoes. Buyers also pointed out that they continue

to receive competitive priced C spec cargoes from North

Asia, explaining that the premium to pen grade cargoes from

southeast Asia may start to narrow. Tracking the decline in

regional prices, Thai C 170 and C 320 prices were assessed

lower by $10/t at $350-360/t fob and Singapore C 170 was

assessed lower by $10/t at $350-360/t fob and C 320 was as-

sessed lower by $10 at $370-375/t fob.

India State-owned refiners revised the bitumen bulk and drum

prices lower by 700 rupees/t ($10/t) in the 15 August price

revision.

The next price revision is expected on 31 August of bulk

and drum cargoes. Weakening of the Indian rupee to the US

dollar will be one of the factors that is expected to impact

the price revisions.

Domestic demand in India remains weak as road projects

have seen slower progress due to the ongoing wet weather

in the country. Demand may start to pick up once weather

conditions improve. Market participants expect buying to

pick up from mid-September.

Bahrain State-owned refiner BAPCO revised the prices downward by

$25/t at $325/t fob Sitra on Thursday.

Falling bitumen cargo prices in the Mediterranean market

has kept the arbitrage open to the Gulf market.

The refiner loaded nearly 2,000t on tank trucks to Qatar

and around 9,000t vessel cargoes to the UAE, Saudi and

Qatar market.

Iran

The export market remained relatively quiet this week as

anticipation grew on the upcoming price revision by state-

owned NIOC of the vacuum bottom feedstock price.

Copyright © 2017 Argus Media Ltd Page 13 of 16

Issue 17-033| Friday 2 Jun 2017

Argus Bitumen

ASIA- A I I AND MIDDLE EAST MARkET OMM N A

Market participants are expecting the VB feedstock to be

revised downwards between $15-30/t. The downward

revision is due to the fall in crude and fuel oil prices. NIOC is

expected to announce the new price on Saturday or Sunday.

In anticipation of the downward price revision some sup-

pliers were already offering drum and bulk cargoes lower by

$10-15/t fob, but no deals were concluded. Buyers preferred

to wait and not commit to any cargoes this week.

The rial continued to remain weak against the US dollar

and was trading in the 33,450-33,650/$1 range.

Fewer deals were concluded on the Iran Mercantile

Exchange (IME). Jey Oil and Pasargad Oil did not supply any

cargoes on the IME.

Trading activities were limited and cargoes were moved

to Vietnam, Indonesia, Bangladesh, Myanmar and Sudan.

Bulk demand was weak in the UAE and Oman due to warm

weather. A small 500mt packed bitumen deal for India was

concluded at $345/t fob Bandar Abbas.

Bulk cargos were steady at $279-290/t fob Bandar Abbas

by some producers and traders this week. A 1,200t of pen

60/7 was concluded at $284/t fob Bandar Abbas and another

1,000t bulk cargo was sold at $285/t fob Bandar Abbas to the

UAE.

Another 1,000t bulk cargo was settled on local currency

basis at 9,450,000 rials/t fob Bandar Abbas (about $284/t fob

Bandar Abbas based on free market exchange rate).

Drums cargoes were flat at $340-360/t fob Bandar Abbas

for cash payments and at $365-380/t fob Bandar Abbas for

credit payments this week. Some producers and traders

offered their cargoes at 11,200,000-11,700,000/t fob Bandar

Abbas (about $339-355/t fob Bandar Abbas based on a free

market exchange rate). IME costs include of brokerage fee is

$1.06/t.

Iran local market

Vacuum bottom feedstock prices were steady this week,

although demand was low and limited VB cargoes were sold.

Domestic buying interest was weak due to warm weather

and producers sold 31,985t in the domestic market.

Jey Oil kept prices stable and they sold 13,506t of pen

60/70 and 85/100 at 9,080 rials/kg ex-Esfahan this week.

Pasargad Oil prices were also firm this week, they settled

8,319t of pen 60/70 and 85/100 at 9,680 rials/kg ex-Tehran

and 2,414t of pen 60/70 at 10,070 rials/kg ex-Shiraz. Another

1,953t of pen 60/70 and 85/100 was sold at 9,080 rials/kg

ex- Arak. It sold cargoes from its Tabriz, Tehran and Bandar

Abbas plants as well.

Iranian Vacuum Bottom prices from NIOC*

Refinery Volume t Rials/kg $/t

Low High Low High Bandar Abbas 1,900 7,913 7,913 236 236

Esfahan 3,720 7,536 7,536 225 225

Shiraz 1,000 7,913 7,913 236 236

Tehran 9,730 7,536 7,588 225 226

Tabriz 2,350 7,536 7,536 225 225

Arak

* Exclusive of the 9pc tax for domestic sales and 14pc duty for export sales

Iranian domestic sales through the IME

Grade Volume t Price rials/kg 60/70 26,759 9,080-10,070

85/100 5,226 9,070-9,534

40/50 3,596 9,769

MC-250 1,812 13,294-14,180

Emulsion Rapid 50 7,866

Emulsion Slow no supply

Exchange rate 1$ = 29,860 rials

Jey Oil $/t

Total purchased quantity up to 2000t up to 4000t 2.00

4200t up to 7000t 3.50

7300t up to 10,000 5.00

10,500t and above 7.00

Jey Oil discount $/t

Total purchase and 100pc advance payment 2,000 up to 5,000t 5.00

5200t and above 7.00

Jey Oil $/t

Total purchase and loaded quantity 15,200t up to 30,000t 2.00

30,500t up to 60,000t 3.50

61,000t up to 100,000 5.00

102,000t and above 7.00

Pasargad Oil discount $/t

Discount, cash payment and loading within 45 days 0 up to 2000t 4.00

2,000t up to 5,000t 6.00

5,000t and above 8.00

Pasargad Oil discount $/t

In case of withdrawal 5 May 35,000t and above 4.00

Copyright © 2017 Argus Media Ltd Page 14 of 16

Issue 17-033| Friday 2 Jun 2017

Argus Bitumen

N

Sapref Durban refinery restarts after delays The 180,000 b/d Sapref refinery in Durban, operated jointly

by Shell and BP, restarted 19 August after extended delays

that followed a scheduled maintenance shutdown.

Loadings of bitumen from the refinery are still slow, but

they are expected to be ramped up over the coming week-

end. The return to full-scale refinery and loading operations

after full shutdowns at Sapref usually takes up to two weeks.

The refinery was fully shut for scheduled maintenance

work that was to have lasted from 20 April to 30 June, but

the restart has been plagued by repeated technical hitches

and delays, helping — along with other refinery problems

and shutdowns in South Africa — to dramatically tighten

domestic bitumen supplies.

No sign of restart at Morocco refinery

There is no sign of a restart at the 220,000 b/d Mohammedia

refinery in Morocco despite the delivery of a 1mn bl crude

cargo in the week starting 17 August and another 1mn bl

cargo sitting offshore.

Refinery operator Samir, which is majority owned by

Saudi Arabian private sector company Corral, has not

updated the Casablanca stock exchange since the delivery.

Trading in its shares was suspended on 6 August, and the

firm said refining operations had stopped because ―the sup-

ply of crude oil to the refinery has been delayed due to the

international market situation and the company's financial

difficulties‖. The company owes over $1bn to the Moroccan

government in taxes.

Repeated attempts by Argus to contact the company for

comment have been unsuccessful. Shipping market partici-

pants also say they have been unable to reach the firm.

The STI Spiga left Mohammedia on 17 August, after

discharging crude, while the Delta Tolmi is moored offshore.

But product traders do not expect the refinery to restart

until at least October, pointing to the financial straits Samir

finds itself in. This timeline would tally with a schedule for

refinancing discussions. On 11 August, Samir said it would

adopt a financing plan drawn up by the Attijari Bank and in-

crease the company's capitalisation. But the board is not due

to meet until 8 September to convene a shareholder meeting

on 12 October.

The financial problems at Samir do not come out of the

blue. Last December, it issued a profits warning follow-

ing the collapse in crude prices. The refiner is obliged to

maintain a strategic stock of 4mn bl of crude, in addition to

operating stocks. It said the fall in the value of this inven-

tory since July meant it would make a loss in 2014. That loss

amounted to 3.4bn dirhams ($350mn). Earlier this year, the

refiner restructured its debt with a Moroccan bank, and an-

nounced loans from an arm of the Islamic Development Bank

and US finance group Carlyle.

The Mohammedia refinery — the only one in Morocco —

primarily supplies the domestic products and LPG markets,

but around 25pc of its output is exported. It produces over

7,000 b/d of bitumen, some of which is exported.

Shell's Godorf refinery to undergo maintenance

Shell will halt production of motor fuels and heating oil at

its 170,000 b/d Godorf refinery in the west of Germany in

September because of maintenance work.

It is unclear which units will undergo maintenance, or

how long the stoppage will last. The last planned shutdown

of the Godorf refinery was in September 2014.

Godorf refinery is part of Shell's Rheinland Refinery

complex that also includes the 140,000 b/d Wesseling refin-

ery. There is no stop of production planned for Wesseling in

September.

Total plans Antwerp maintenance in October

Total is planning to shut down a desulphurisation unit and

a reformer throughout October at its 308,000 b/d Antwerp

refinery in Belgium.

The desulphurisation unit is used to reduce sulphur

content in gasoil. The shutdown of the reformer will lead to

higher straight-run naphtha output from the plant.

The refinery had a full turnaround shutdown in 2013.

Argus direct Web | Mobile | Alerts

Argus Direct is the next generation platform

from Argus Media. It is the premium way to

access our reports, prices, market insight,

fundamentals data and markets.

To learn more, visit our website

or contact your account representative.

argusmedia.com/direct

Copyright © 2017 Argus Media Ltd Page 15 of 16

Issue 17-033| Friday 2 Jun 2017

Argus Bitumen

N S

Norway’s oil product sales down in July Norway’s

oil product sales fell by 2.4pc in July compared with a year

earlier, as deliveries of gasoline and middle dis- tillates

more than offset rises in diesel used for motor fuel.

Bitumen imports rose 40pc year on year to 47,458t in

June, reflecting a rising trend seen this year.

Total product sales in July were 147,000 b/d, according

to preliminary data released by Statistics Norway (SSB).

Norway bitumen imports t

January

11,274

February 3,807

March 7,299

April 25,686

May 59,276

June 74,193

July 47,458

Source: Statistics Norway (SSB)

Hellenic plans short Thessaloniki shutdown

Hellenic Petroleum will shut its 83,000 b/d Thessaloniki

refinery for a turnaround during September.

No further details were provided by the company for a

turnaround that is expected to last for a few days during the

first half of the month and is not expected to affect supplies

of oil products from the refinery.

Data revision boosts Spanish asphalt demand

A second data revision in as many months by the Spanish

strategic reserve Cores has boosted demand for asphalt

products versus the corresponding periods in 2014.

The reserve upwardly revised 2015 demand, after having

Argus Media Blog

http://blog.argusmedia.com

Subscribe to our blog for expert updates and analysis on the latest developments in the global oil industr y

Market Reporting

Consulting

illuminating the markets Events

previously revised down consumption data for 2014.

Spain consumed 97,266 tonnes of asphalt products in

June said Cores, up by 8pc compared with a year earlier.

Over the first six months of the year Spain has seen 477,285t

of demand, up by 33pc compared with the first half of 2014.

Cores defines bitumen and asphalt products as "bitumen,

asphalt, petroleum bitumen and any other secondary prod-

ucts".

Cores has upwardly revised its data for the first five

months in 2015. Previously it had said Spanish demand for

asphalt products in the January to May period stood at

304,499t, but this has now increased to 380,019t. The re-

serve also revised its data for 2014 downwards in July. It said

demand for 2014 was 885,205t, down from a level of 1.3mn t

given previously. The years before 2014 remain unchanged.

The new figures mean 2014 was the lowest level of asphalt

product demand on record and the only year with less than

1mn t of demand since Cores' records began in 1997.

The reserve publishes demand and distribution data,

which it receives from the member companies that pay its

costs. In 2014 that was integrated firm Repsol, which pays

32pc of Cores' fees, followed by refiner Cepsa, which pays

22pc, and BP, Spain's Galp and retailer Disa, which pay 10pc,

9pc and 7pc, respectively. Another 20pc of Cores' revenues

is made up of smaller firms.

Despite the upwards revision to 2015 data, it is still the

second lowest level of consumption for the period on record.

In the first six months of 2013 Spain consumed 618,924t.

In 2008 — before the onset of Spain's financial crisis — the

country saw 1.1mn t of demand, underlying the fragile state

of any economic recovery in the country.

Construction activity figures from the EU's statistics

service Eurostat — which include all building projects in the

country — show a small increase in June of 0.6pc compared

with the same month a year earlier. But provisional data on

civil engineering activity — road, rail and other large scale

state works — shows an increase of 2.9pc compared with

June 2014. This means Spanish civil engineering activity has

now grown in each month since September.

Petronas profit hit by falling prices, lower sales

Profit at Malaysia’s state-owned oil firm Petronas fell sharply

in the second quarter because of lower oil prices and a

decline in crude and LNG sales.

Petronas made a profit of 11.1bn ringgit ($2.7bn) during

April-June, down by 47.4pc from 21.1bn ringgit a year earlier.

Profit in the first half of 2015 fell by 43.5pc to 22.5bn ringgit.

The firm produced 2.28mn b/d of oil equivalent (boe/d)

Issue 17-033| Friday 2 Jun 2017

Argus Bitumen

N S

in the second quarter, up by 3.2pc from 2.21mn boe/d a year

earlier, supported by higher crude and condensate output in

Malaysia, Iraq and Azerbaijan.

Output on an entitlement basis edged down to 1.56mn

boe/d from 1.59mn boe/d over the period. But sales fell,

with crude sales dropping by 2pc from a year earlier to

580,000 b/d and oil product sales dipping by 6pc to 780,000

b/d on lower trading and marketing volumes respectively.

The firm’s capital investment totalled 19.8bn ringgit in

the quarter, up by 48pc from the same period last year, fol-

lowing its October purchase of a 15.5pc stake in the BP-led

Shakh Deniz gas and condensate field in the Azeri sector

of the Caspian Sea from Norway’s state-controlled oil firm

Statoil for $2.25bn. Domestic spending on the $27bn Rapid

refinery and petrochemical project in southern Malaysia and

an expansion at Bintulu LNG also contributed to quarterly

investment.

Crude prices will remain under pressure because of

modest global oil demand growth and abundant Opec and

non-Opec supply, Petronas said. It warned its full-year per-

formance is likely to be hit by prolonged lower oil prices and

modest global economic growth.

Argus direct Web | Mobile | Alerts Argus Direct provides immediate

access to market moving news,

intelligent analysis and robust

price assessments, wherever.

www.argusmedia.com/direct

Argus Bitumen Methodology Argus uses a precise and transpar- ent methodology to assess prices in all the markets it covers. The latest version of the Argus Bitumen mthodology can be found at: www.argusmedia.com/methodology For a hard copy, please email [email protected], but please note that methodologies are updated frequently and for the latest version, you should visit the internet site.

arGUs BIOFUeLs

Contents:

Methodology overview 2

Price assessments — introduction 6

Spot prices 6

Reference prices 8

Spot ethanol price assessments 8

Forward price assessments and swaps 9

Last Updated: janUary 2015

The most up-to-date Argus Biofuels methodology is available on www.argusmedia.com

Argus Bitumen is published by Argus Media Ltd.

Registered office

Argus House, 175 St John St, London, EC1V 4LW

Tel: +44 20 7780 4200 Fax: +44 20 7681 3458

email: [email protected]

ISSN: 2057-6749

Copyright notice

Copyright © 2017 Argus Media Ltd.

All rights reserved. All intellectual property

rights in this publication and the information

published herein are the exclusive property of

Argus and/or its licensors and may only be used

under licence from Argus. Without limiting the

foregoing, by reading this publication you agree

that you will not copy or reproduce any part of

its contents (including, but not limited to, single

prices or any other individual items of data) in

any form or for any purpose whatsoever without

the prior written consent of Argus.

Trademark notice

ARGUS, ARGUS MEDIA, the ARGUS logo, ARGUS

BITUMEN, other ARGUS publication titles and

ARGUS index names are trademarks of Argus

Media Ltd. Visit www.argusmedia.

com/trademarks for more information.

Disclaimer

The data and other information published

herein (the ―Data‖) are provided on an ―as

is‖ basis. Argus makes no warranties, express

or implied, as to the accuracy, adequacy,

timeliness, or completeness of the Data or

fitness for any particular purpose. Argus shall

not be liable for any loss or damage arising

from any party’s reliance on the Data and

disclaims any and all liability related to or

arising out of use of the Data to the full extent

permissible by law.

Publisher Adrian Binks Chief executive Neil Bradford Global compliance officer Jeffrey Amos Commercial manager Jo Loudiadis Editor in chief Ian Bourne

Managing editor

Peter Ramsay

Editor Jonathan Weston Tel: +44 20 7199 5779 [email protected]

Customer support and sales Technical queries [email protected] All other queries [email protected]

London, UK Tel: +44 20 7780 4200

Astana, Kazakhstan Tel: +7 7172 54 04 60

Beijing, China Tel: +86 10 8535 7682

Dubai Tel: +971 4434 5112

Moscow, Russia Tel: +7 495 933 7571

Rio de Janeiro, Brazil Tel: +55 21 2548 0817

Singapore Tel: +65 6496 9966

Tokyo, Japan Tel: +81 3 3561 1805

Argus Media Inc, Houston, US Tel: +1 713 968 0000

Argus Media Inc, New York, US Tel: +1 646 376 6130

Petroleum

illuminating the markets