area 2 gwinnett county council leadership treasurer training cathy wendholt-mcdade georgia pta...

TRANSCRIPT

Area 2 Gwinnett County Council Leadership Treasurer Training

Cathy Wendholt-McDade

Georgia PTA Treasurer

The PTA Audit• Certify the accuracy of the records of the

financial officer.

• Assure the membership that resources/funds are being managed in a businesslike manner within the membership approved budget.

• Required to be in good standing with Georgia PTA and for bonding insurance.

Audit FAQs

• Does the audit have to be completed by a CPA?

• Do we have to pay someone to do our audit?

• Can we write checks during the audit?

Once the audit is complete…• Auditor presents report to the Executive

Committee• Executive Committee presents the report to the

membership at the first meeting of the school year to adopt the report

• Copy of audit report (all 3 pages) is submitted to the state office no later than September 30th.

• Gross receipts for the year are filed on the appropriate federal tax form with the IRS.

IRS Form 990

• All Not For Profits, regardless of income, required to file a Form 990

• Failure to file for three years, automatic revocation of tax exempt status– 990 N – Electronic Postcard

• Receipts less than $50,000

– 990 EZ• Receipts less than $500,000 and assets less

than $1.25 million

IRS Form 990 NCompleting the e-Postcard requires the seven items listed below:

1.Employer identification number (EIN)2.Fiscal year3.Legal name and mailing address4.Any other names the organization uses5.Name and address of a principal officer6.Web site address if the organization has one7.Confirmation that the organization’s annual gross receipts are normally $50,000 or less

990 FAQs

• When is my 990 due?

• Who is responsible for completing?

• Who is responsible for sending in to IRS?

• Who signs the return?

Online Resources

Internal Revenue Service

www.irs.gov

GuideStar

www.guidestar.org

National Center for Charitable Statistics

http://nccsdataweb.urban.org

The Budget Process• Budget Committee prepares proposed

budget– Calendar of programs and projects

– Realistic estimates of the costs

– How will you fund programs

• Present proposed budget to Board of Directors

• Present proposed budget to General Membership for approval

• New budget each year

Things to Consider before Fundraising

• Don’t just fundraise to fundraise!

• Membership Approval

• Carry over

• 3 to 1 Rule

• http://www.irs.gov/charities/index.html

Things To Remember

• Dues Transmittal

• Insurance Premium

• Incorporation Fees

Insurance

What does a fidelity bond policy cover?Protects the cash of the PTA unit against theft, fraud and embezzlement

Who should be covered under this policy?

Anyone in your PTA who has access to or handles money (e.g. Treasurer, President, Fundraising chair)

Other Insurance Coverage• GENERAL LIABILITY: Protects all members in case they

are held legally liable for bodily injury or property damage to another person that resulted from a covered event.

• DIRECTORS & OFFICERS LIABILITY: Covers protection if an officer or member of PTA is sued for not living up to the responsibilities and duties assumed as a member of PTA.

• PROPERTY: Covers property owned by the PTA - Laptop, merchandise for fundraiser, Fall Festival Booths, etc.

• ACCIDENT MEDICAL: Provides medical payment for injuries sustained at a PTA event.

Donations• Contributions to the PTA are tax deductible in full

if no service or other benefit is received in return.

• Single cash contributions in excess of $250 require a receipt documenting the charitable donation to the PTA.

• If the donor claims the value of a non-cash contribution of $250 or more, the PTA is required to furnish a written acknowledgement as well, following similar guidelines for cash contributions. However, the PTA is not required to, and should not, place a value on the contributed item(s) for the donor.

Treasurer’s Responsibilities• Write checks as authorized by the PTA/PTSA

president in accordance with the adopted budget ;

• Have checks signed by 2 people: the treasurer and 1 other person. (Individuals authorized to sign checks shall not be related to each other;

• Always issue a receipt for cash received;• Maintain a full and accurate account of the

receipts and disbursements in the books belonging to your PTA/PTSA;

• Reconcile the bank statements monthly and have the statements reviewed, signed and dated by the president and another PTA member (not related to the treasurer);

• Have records available at all meetings;• Provide a written financial statement at all

PTA/PTSA meetings;• Present an annual report of the financial condition

of the organization;• Have the accounts examined annually at the end of

the school year or upon the change of treasurer by an auditor or committee

Treasurer’s Responsibilities

• Never sign a blank check;• Pay all bills by check – never by cash;• Never deposit funds of this PTA in a personal

account or a school account;• Electronic banking

Treasurer’s Responsibilities

Treasurer’s File• Bylaws

• Budget

• Last Audit Report

• Checkbook register/Cancelled checks (voids too)

• Signed Cash Verification Forms/Deposit slips

• Authorized Check Request Forms/Receipts

• Bank statements, bank books Cash receipts

• All PTA/PTSA meeting minutes

• Treasurer and Secretary reports

• Annual Financial Report

• Copy of last tax return filed

Internal controls

The cornerstone of all your PTA’s financial

transactions.

Most only require one person to create, the risk of fraud increases due to lack of checks and balances.

Ensure that you have proper internal controls in place to mitigate that risk.

Internal controls

Factors necessary:

Board of directors commitment

Sound policies and/or procedures

regarding the segregation of duties

Compliance with and review of the

policies/procedures in place

Internal controls

Factors necessary:

Policies/procedures should be in writing

Segregation of Duties

Internal controls

Factors necessary: Segregation of Duties:

• A person(s)* who does not have the

authority to approve payments receive

invoices

• The person(s)* who can approve payment

should not be able to cut checks or enter

invoices into the accounting system

Internal controls

Factors necessary:

Review on a monthly basis all bank

statements and bank reconciliations by

someone who does not have access to

authorize or enter invoices

Maintain a filing system for proper and

complete storage of all necessary

documentation

Internal controls

Factors necessary: Be organized and consistent

Review internal control policies/

procedures annually

Ensure proper training for personnel

or volunteers

Regardless of how automated the process, without effective internal controls in place, there will be opportunity for fraud to occur.

Risk

Risk

For fraud to occur, only three things are needed: opportunity

pressure

rationalization

FRAUDIf you believe that fraud has occurred, which generally involves stolen or misappropriated assets like cash, property, or equipment; you should contact your Council, District and State PTA.

Online Bill Payment

Helps improve visibility and transparency of the accounts payable process through automation and electronic record-keeping

Helps eliminate lost or misfiled documents

Reduces process and data entry errors through document capture and financial process automation

Eliminates check printing, signing, and

mailing

Online Bill Payment

Allows access to financial documents

anytime, anywhere

Helps eliminate check fraud

Forces second approval of vendor payments

Can increase productivity and lower costs

through paperless document imaging, auto-

mated bill routing, and integrated online bill

payment

Online Bill Payment

But…. fraud could still occur the same way it could if

using checks.

Online Bill Payment

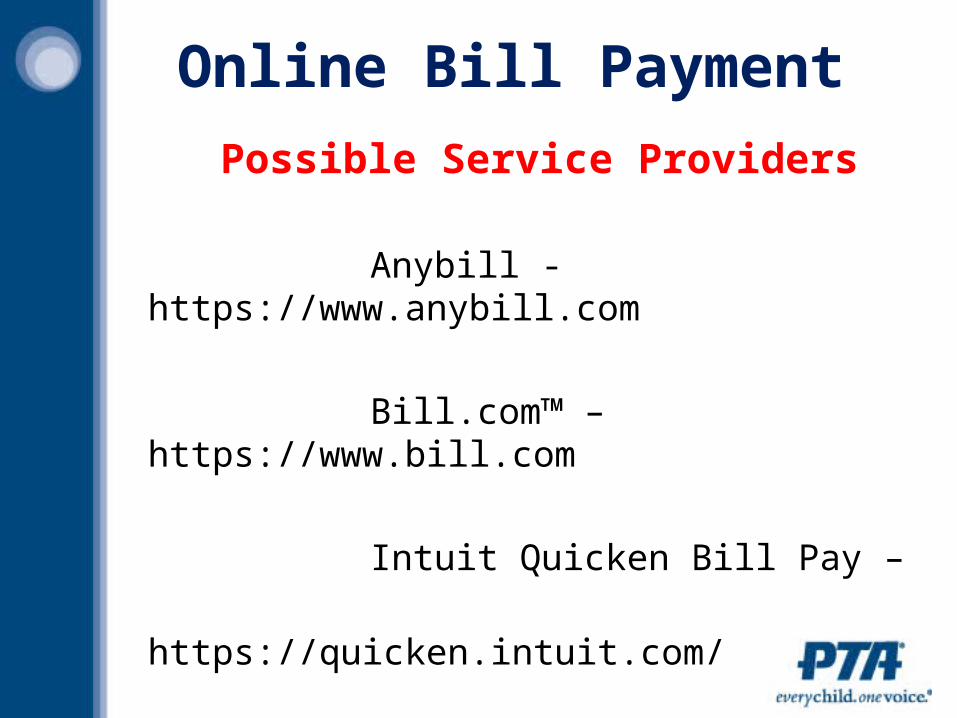

Possible Service Providers

Anybill - https://www.anybill.com

Bill.com™ – https://www.bill.com

Intuit Quicken Bill Pay –

https://quicken.intuit.com/

Online Banking

Recommended Account Controls

Train volunteers on policies and procedures

Consult with your bank to see what security

options are available

No shared user names and passwords

Assign two individuals as administrators

Set user online access levels by roles and

responsibility

Online Banking

Recommended Account Controls

Review user online access levels regularly

Delete online user IDs as soon as a person

resigns his or her position

Set up alerts to notify persons of payments

initiated or deposits made

Allow read-only access to individuals who

should be monitoring the bank account

Online Banking

Recommended Security Settings

Keep an updated antivirus application

Keep your passwords and user IDs secure

Select a strong password and do not give

your password or bank ID to anyone

Never respond to or open internet links or

attachments in unsolicited emails, especially

ones that appear to come from your bank

Using Credit Cards for Bill Payments

Have credit card policies and procedures in place

State by whom and for what it can be used

and cardholder responsibilities

Have cardholders sign a statement

- they have received the credit card

- have read and agree to the terms and

conditions of the credit card policy

Get a credit card that will allow limits by user

-limits set by board of directors

Using Credit Cards for Bill Payments

Have credit card policies and procedures in place

Get a credit card that will allow limits by user

-limits set by board of directors

Set up an approval process

-all credit card receipts are received

-all charges have been pre-approved

Make sure expense reports are signed/dated

-card holder -designated approver

Using Credit Cards for Bill Payments

Have credit card policies and procedures in place

Make sure the cards of all former volunteers

are destroyed and deactivated immediately

upon termination

Assign a person who does not have a

company card to review receipts and

reconcile them to the credit card statement

Use of ATM/Debit, Gift, or Deposit Only Cards

National PTA highly recommends that the

use of debit or gift cards not be used as a

form of payment.

Deposit only ATM cards are acceptable if

your bank offers this service.

Deposit Only Cards

Deposit only ATM cards can be requested for

volunteers, which allow them to make deposits

only

Each card has a unique card number and

individual personal identification number (PIN)

Deposit cards can be used at any deposit-

taking ATM that is affiliated with your bank

Accepting Credit Cards

When a local PTA decides to accept credit

cards as a form of payment, a review of internal

controls will need to be conducted to ensure

policies/procedures are in place.

Accepting Credit Cards

Best Practices Do not transmit cardholder’s credit card data

by e-mail, mail or fax

Do not store credit card data for customers on

paper or electronically in an unsecured area

Do not store PIN or CVV2/CVC2/CID numbers

Do not share user ID’s

Accepting Credit Cards

Best Practices

Never disclose any cardholder’s data without

their consent

Store all documents containing credit card data in a secure place which PTA solely controls

Ensure that the person processing the

transaction is properly trained in best practices

Accepting Credit CardsBest Practices

Each person who has access to credit card

information is responsible for protecting it

Keep documentation for each transaction so

that disputed charges do not become a problem

When a refund is necessary, the refund must be credited only to the same account from which the purchase/donation was made

Accepting Credit Cards PTA’s Responsibilities

Must comply with Payment Card Industry Data Security Standards (PCI DSS)

These standards protect the PTAs from issues of liability and fraud

PCI Data Security Standards can be located at:

http://www.pcisecuritystandards.org/securitystandards/pci_dss.shtml

Thank you for having me here today

Cathy Wendholt-McDadeGeorgia PTA Treasurer

[email protected] Baker St., NE

Atlanta, GA 30308-3366Phone: 404-659-0214 or 1-800-PTA-TODAY