aqip budget improvement team - colorado mountain...

TRANSCRIPT

Colorado Mountain College

AQIP Budget Improvement

Team

April 13, 2009

Team Members Steve Boyd, Purchasing and Contracts Manager, Central Services Technology Geek Extraordinaire Jan Krueger, Budget/Finance Manager, Central Services Carol Richards, Accounts Manager, Alpine Karen Silverman, Accounts Manager, Aspen Scribe

Mike Simon, Timberline Campus Chief Executive Officer, Vice President of Colorado Mountain College Team Leader

Team Sponsors Linda English, Chief Financial Officer, Central Services Joe Maestas, Aspen Campus Chief Executive Officer, Vice President of College Mountain College

Table of Contents

Team Members ............................................................................... Inside Front Cover Background Information ........................................................................................... .2 Key Elements Relationship Graph…(Figure #1) ............................................. 3 Project Statement ...................................................................................................... 4 Operational Definitions .............................................................................................. 5 Current Process Annual Budget Process Flow…(Figure #2) ..................................................... 8 Current Budget Formula Narrative ................................................................ 9 Data Gathering Results CLT Survey Results …(Figures #3 – 7) ............................................................ 14 Other Colleges Survey Results…(Figure #8) .................................................. 17 Development of Improvement Theory and Implementation Plan .......................... 19 Changes to be Instituted ................................................................................ 19 Costs Involved ................................................................................................ 19 Anticipated Positive Results…(Figure #9) ...................................................... 21 Recommendations ................................................................................................... 22 Link to AQIP Criteria ....................................................................................... 24 Force Field Analysis…(Figure #10) .................................................................. 25 Schedule of Zero‐Based Budgeting (Tree Diagram)…(Figure #11) ......................... 26 Engrafting Improvements into System .................................................................... 27 Timeline for Implementation of Zero‐Based Budgeting (Gantt)…(Figure #12) ....... 28 Ideas for Future Team Improvements ..................................................................... 29 CLT Group Feedback ................................................................................................ 30 Thank You and Acknowledgements ......................................................................... 31 Appendix .................................................................................................................. 32

Survey and Responses from CLT…(Figure #13) .......................................... 33 Survey and Responses from Outside Colleges…(Figure #14) ..................... 41 CLT Focus Group Survey and Response ...................................................... 51 Sample Rotation Schedule…(Figure #15) ................................................... 52 LaFaive Testimony Re: Zero Based Budgeting ............................................ 53

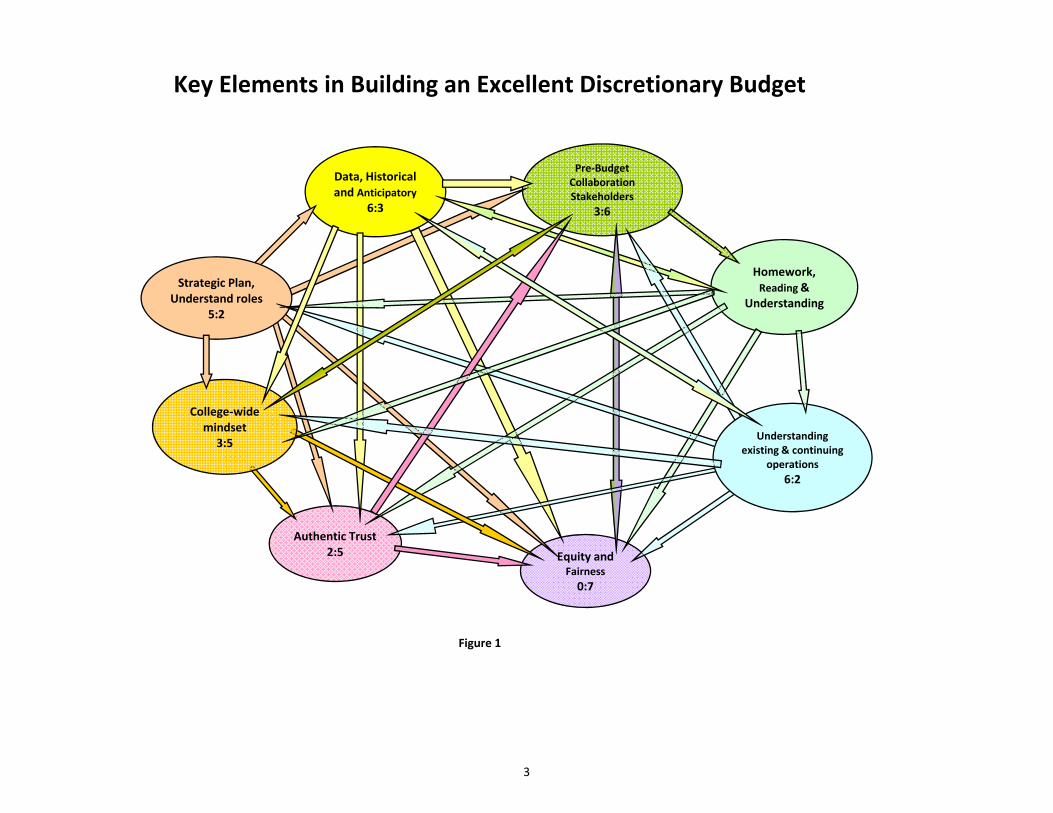

Budget Improvement Team Background Information Under our current budgeting processes serious issues are raised over the allocation of funding, the relationship of the funding to our strategic goals, and the resulting determination of the effectiveness of our spending. Additionally, since some units cannot accomplish their operating goals while remaining within their budgets, it was suggested that a review of our process be made to determine if there are areas where significant improvements can be achieved. We prepared a Relations diagram (Figure 1) to determine the most influential factors affecting the budget development. We found that reliable, trustworthy and uniform data were most important in the process. Understanding our current and future operations and being prepared for the discussions were the next most critical components. All of these factors suggest that training and well defined computations as well as standardized processes will significantly improve the ultimate budgets. The team decided that there were two sources where focal points could be identified. Internally, the College Leadership Team (CLT) participates at the highest level in developing and reviewing the budgets. Externally, other similar colleges must go through budget processes also. We prepared a Survey of the CLT members. This was followed up by a focus group discussion once an area of concentration was identified. We also prepared a phone survey of similar colleges which were identified by Dr. Meeta Goel. Not all colleges responded to our survey request but those which did offered meaningful insights. Both of these surveys and the results are part of this report. The direction that these results most clearly pointed toward was an overall change in our funding allocation/budget building methods. The conclusions are that we need to move away from the use of the current “drivers” and to a method which will more closely align funding with our strategic goals.

2

Data, Historical and Anticipatory

6:3

Pre‐Budget Collaboration Stakeholders

3:6

Homework, Reading &

Understanding

Strategic Plan, Understand roles

5:2

Key Elements in Building an Excellent Discretionary Budget

Figure 1

Authentic Trust2:5 Equity and

Fairness0:7

Understanding existing & continuing

operations6:2

College‐wide mindset

3:5

3

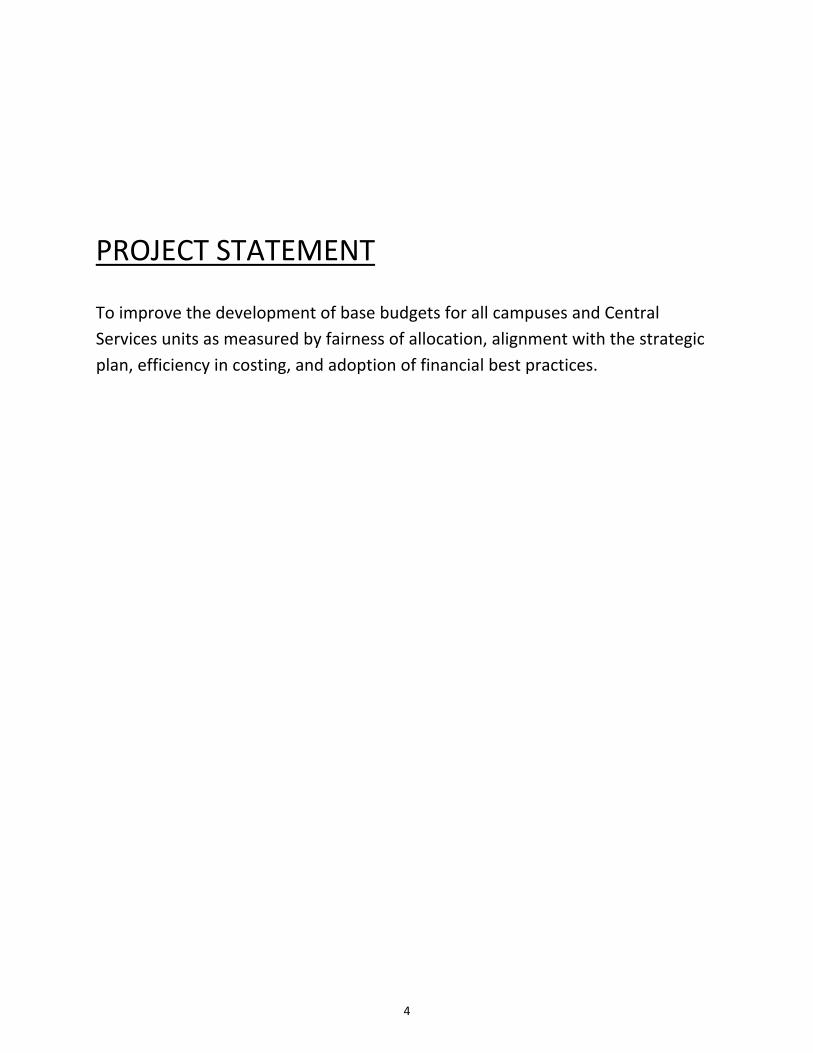

PROJECT STATEMENT To improve the development of base budgets for all campuses and Central Services units as measured by fairness of allocation, alignment with the strategic plan, efficiency in costing, and adoption of financial best practices.

4

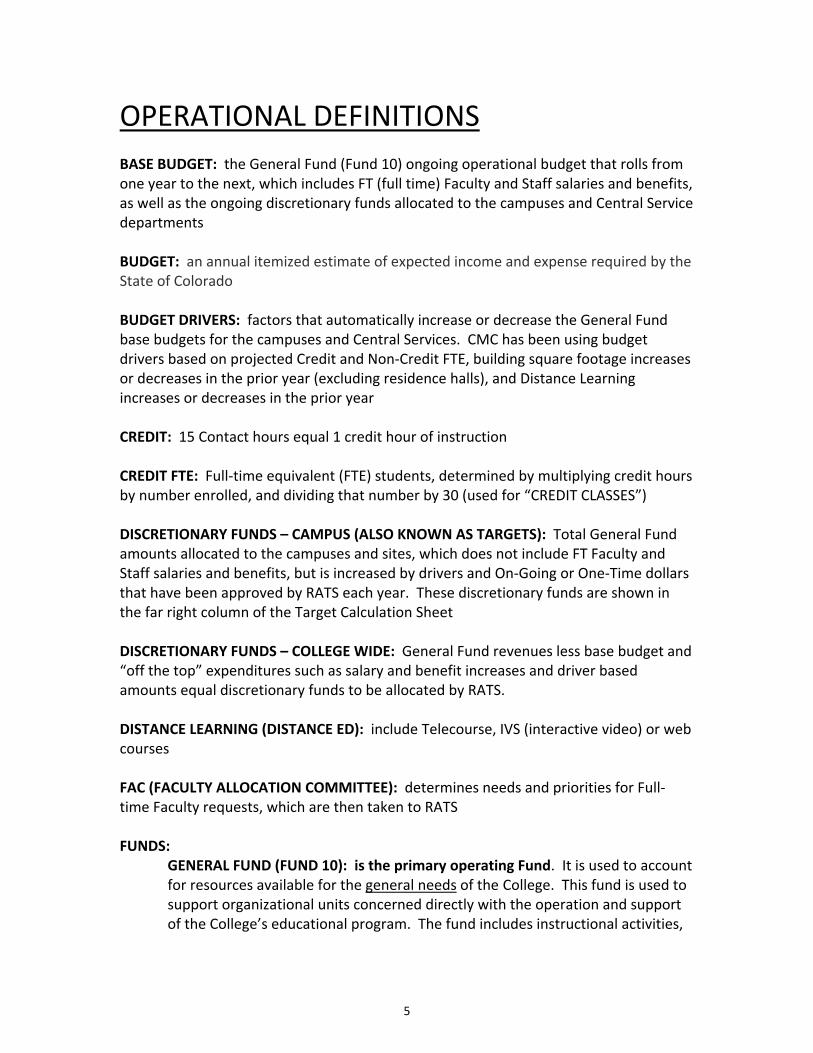

OPERATIONAL DEFINITIONS BASE BUDGET: the General Fund (Fund 10) ongoing operational budget that rolls from one year to the next, which includes FT (full time) Faculty and Staff salaries and benefits, as well as the ongoing discretionary funds allocated to the campuses and Central Service departments BUDGET: an annual itemized estimate of expected income and expense required by the State of Colorado BUDGET DRIVERS: factors that automatically increase or decrease the General Fund base budgets for the campuses and Central Services. CMC has been using budget drivers based on projected Credit and Non‐Credit FTE, building square footage increases or decreases in the prior year (excluding residence halls), and Distance Learning increases or decreases in the prior year CREDIT: 15 Contact hours equal 1 credit hour of instruction CREDIT FTE: Full‐time equivalent (FTE) students, determined by multiplying credit hours by number enrolled, and dividing that number by 30 (used for “CREDIT CLASSES”) DISCRETIONARY FUNDS – CAMPUS (ALSO KNOWN AS TARGETS): Total General Fund amounts allocated to the campuses and sites, which does not include FT Faculty and Staff salaries and benefits, but is increased by drivers and On‐Going or One‐Time dollars that have been approved by RATS each year. These discretionary funds are shown in the far right column of the Target Calculation Sheet DISCRETIONARY FUNDS – COLLEGE WIDE: General Fund revenues less base budget and “off the top” expenditures such as salary and benefit increases and driver based amounts equal discretionary funds to be allocated by RATS. DISTANCE LEARNING (DISTANCE ED): include Telecourse, IVS (interactive video) or web courses FAC (FACULTY ALLOCATION COMMITTEE): determines needs and priorities for Full‐time Faculty requests, which are then taken to RATS FUNDS:

GENERAL FUND (FUND 10): is the primary operating Fund. It is used to account for resources available for the general needs of the College. This fund is used to support organizational units concerned directly with the operation and support of the College’s educational program. The fund includes instructional activities,

5

student services, learning resource centers, operation and maintenance of physical facilities, institutional support and related activities of the College.

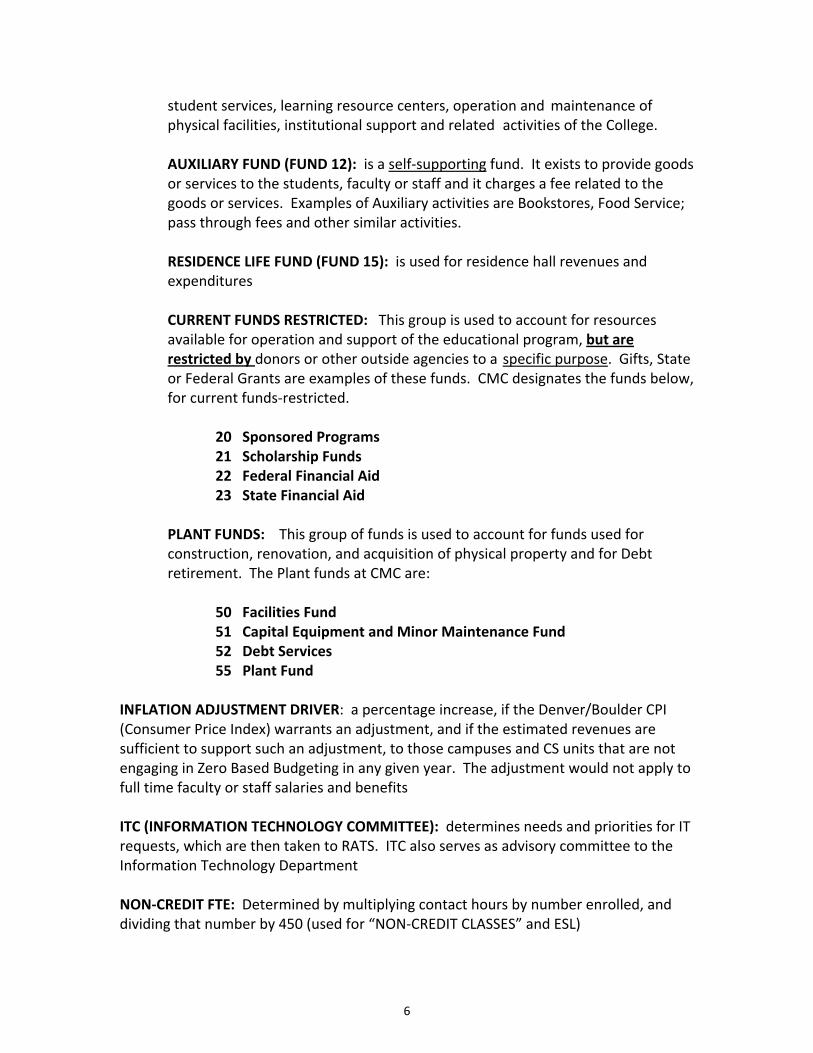

AUXILIARY FUND (FUND 12): is a self‐supporting fund. It exists to provide goods or services to the students, faculty or staff and it charges a fee related to the goods or services. Examples of Auxiliary activities are Bookstores, Food Service; pass through fees and other similar activities.

RESIDENCE LIFE FUND (FUND 15): is used for residence hall revenues and expenditures

CURRENT FUNDS RESTRICTED: This group is used to account for resources available for operation and support of the educational program, but are restricted by donors or other outside agencies to a specific purpose. Gifts, State or Federal Grants are examples of these funds. CMC designates the funds below, for current funds‐restricted.

20 Sponsored Programs 21 Scholarship Funds 22 Federal Financial Aid 23 State Financial Aid

PLANT FUNDS: This group of funds is used to account for funds used for construction, renovation, and acquisition of physical property and for Debt retirement. The Plant funds at CMC are:

50 Facilities Fund 51 Capital Equipment and Minor Maintenance Fund

52 Debt Services 55 Plant Fund

INFLATION ADJUSTMENT DRIVER: a percentage increase, if the Denver/Boulder CPI (Consumer Price Index) warrants an adjustment, and if the estimated revenues are sufficient to support such an adjustment, to those campuses and CS units that are not engaging in Zero Based Budgeting in any given year. The adjustment would not apply to full time faculty or staff salaries and benefits ITC (INFORMATION TECHNOLOGY COMMITTEE): determines needs and priorities for IT requests, which are then taken to RATS. ITC also serves as advisory committee to the Information Technology Department NON‐CREDIT FTE: Determined by multiplying contact hours by number enrolled, and dividing that number by 450 (used for “NON‐CREDIT CLASSES” and ESL)

6

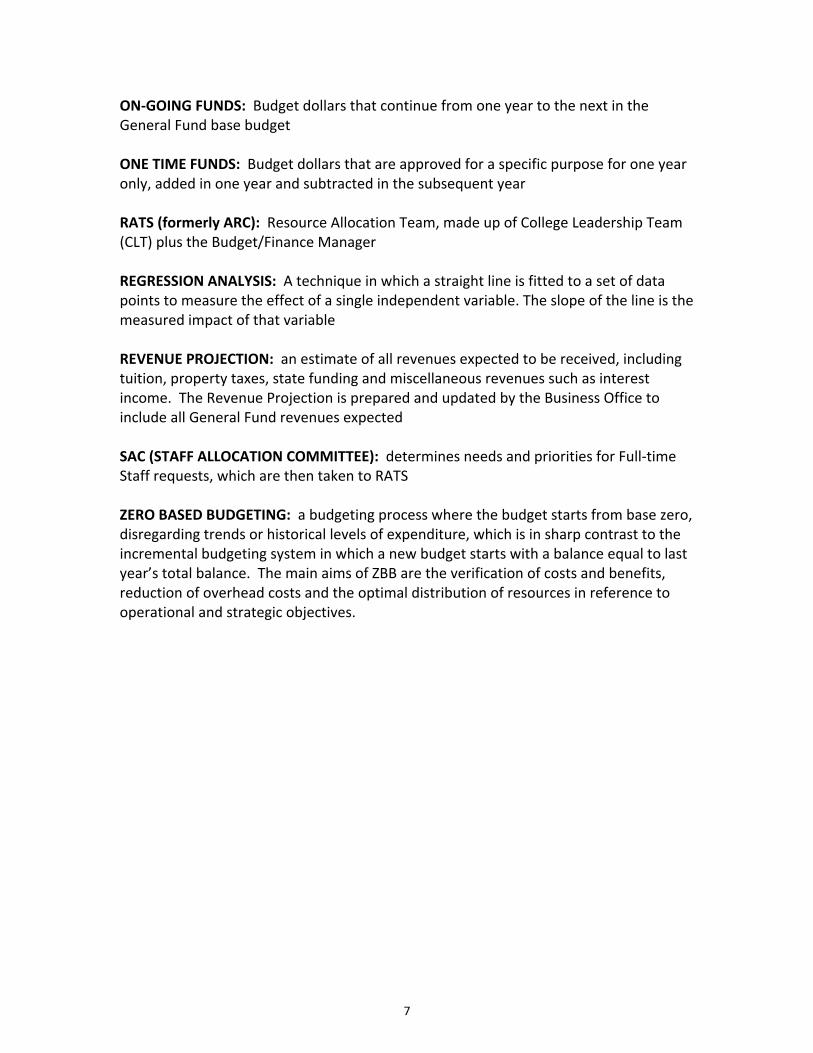

ON‐GOING FUNDS: Budget dollars that continue from one year to the next in the General Fund base budget ONE TIME FUNDS: Budget dollars that are approved for a specific purpose for one year only, added in one year and subtracted in the subsequent year RATS (formerly ARC): Resource Allocation Team, made up of College Leadership Team (CLT) plus the Budget/Finance Manager REGRESSION ANALYSIS: A technique in which a straight line is fitted to a set of data points to measure the effect of a single independent variable. The slope of the line is the measured impact of that variable REVENUE PROJECTION: an estimate of all revenues expected to be received, including tuition, property taxes, state funding and miscellaneous revenues such as interest income. The Revenue Projection is prepared and updated by the Business Office to include all General Fund revenues expected SAC (STAFF ALLOCATION COMMITTEE): determines needs and priorities for Full‐time Staff requests, which are then taken to RATS ZERO BASED BUDGETING: a budgeting process where the budget starts from base zero, disregarding trends or historical levels of expenditure, which is in sharp contrast to the incremental budgeting system in which a new budget starts with a balance equal to last year’s total balance. The main aims of ZBB are the verification of costs and benefits, reduction of overhead costs and the optimal distribution of resources in reference to operational and strategic objectives.

7

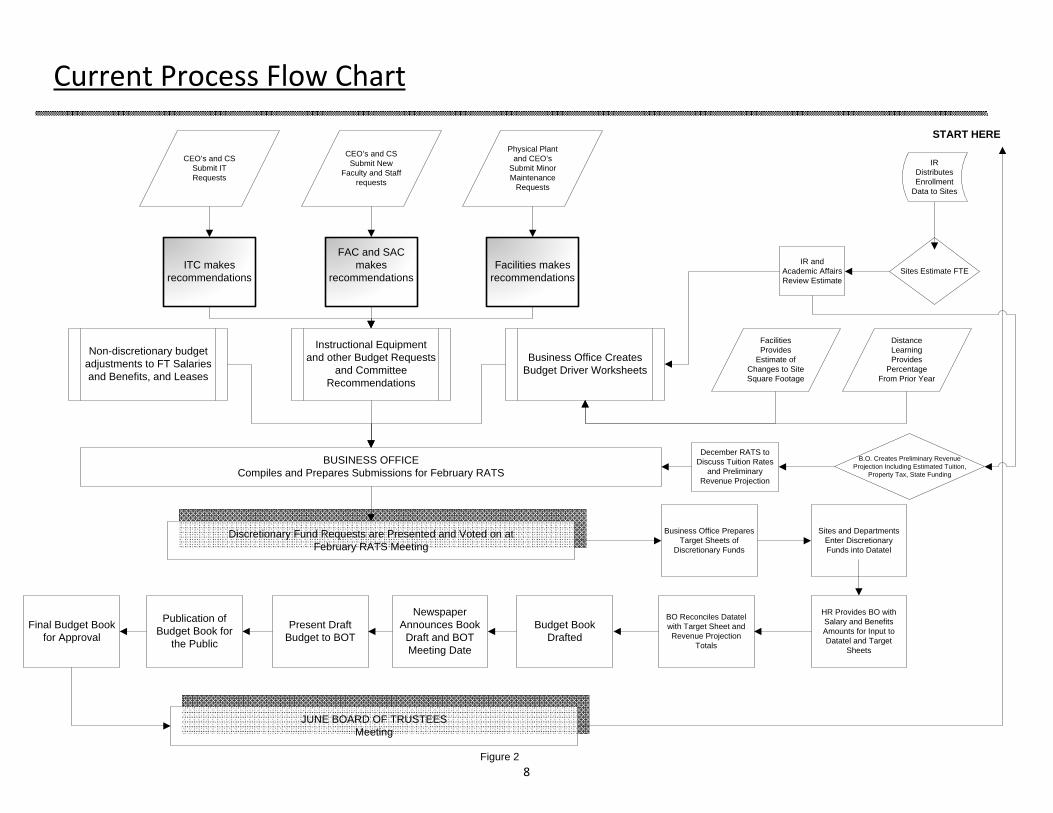

Sites Estimate FTEITC makes recommendations

FAC and SAC makes

recommendationsFacilities makes

recommendations

B.O. Creates Preliminary Revenue Projection Including Estimated Tuition,

Property Tax, State Funding

IR Distributes Enrollment

Data to Sites

IR and Academic Affairs Review Estimate

CEO’s and CS Submit IT Requests

CEO’s and CS Submit New

Faculty and Staff requests

Physical Plant and CEO’s

Submit Minor Maintenance

Requests

START HERE

BUSINESS OFFICECompiles and Prepares Submissions for February RATS

Discretionary Fund Requests are Presented and Voted on at February RATS Meeting

Business Office Prepares Target Sheets of

Discretionary Funds

Sites and Departments Enter Discretionary Funds into Datatel

HR Provides BO with Salary and Benefits Amounts for Input to Datatel and Target

Sheets

BO Reconciles Datatel with Target Sheet and Revenue Projection

Totals

Budget Book Drafted

Newspaper Announces Book

Draft and BOT Meeting Date

Present Draft Budget to BOT

Publication of Budget Book for

the Public

Final Budget Book for Approval

Non-discretionary budget adjustments to FT Salaries and Benefits, and Leases

Instructional Equipment and other Budget Requests

and Committee Recommendations

Business Office Creates Budget Driver Worksheets

Distance Learning Provides

Percentage From Prior Year

Facilities Provides

Estimate of Changes to Site Square Footage

JUNE BOARD OF TRUSTEESMeeting

December RATS to Discuss Tuition Rates

and Preliminary Revenue Projection

Current Process Flow Chart

Figure 28

Current Budget Process Narrative

COLORADO MOUNTAIN COLLEGE NEW BUDGET FORMULA NARRATIVE DESCRIPTION

FOR FISCAL YEAR '98/99 AND BEYOND This document should replace the "proposed budget formula" document which was discussed at ARC last summer. The basic background of the formula is to establish a base budget for each site, determine "drivers" to be used to allocate (plus or minus) additional dollars from year to year and to pull full time faculty dollars out of the site budget process and into a central pot for faculty allocation. Distance education dollars will also be subject to the formula allocation. The District Office budget will be historical with a staffing review done every five years. We believe it is important to keep a new formula simple so that it can be understood throughout the college. Following are the details of each segment of the formula. 1. Determine Base: a. The 97/98 budget is the base for each campus with full‐time faculty dollars (object code 603

plus fringes) being pulled out of the total and put in a central pot. b. Full‐time faculty positions (current and future) will be reviewed by a college‐wide committee

to determine where the need for full‐time faculty is at any given time. If the committee feels as though additional full‐time positions are needed they would come to ARC with a request for additional funding.

c. District Office bases will also be equal to the 97/98 budget. Any part of full time faculty being

paid out of district office will be reallocated to the central pot as well. If a department within district office has a need for a budget increase they may submit a request for additional funding to ARC as was done in the past.

d. Annual salary adjustments will continue to be funded on top of the location budget. 2. Define Drivers: a. FTE b. Non‐Credit c. Square Footage We talked about using headcount as a driver, but felt as though most of the courses offered which drive up the headcount would be covered in the non‐credit category. We thought this would be a duplication if we made non‐credit one of the drivers.

9

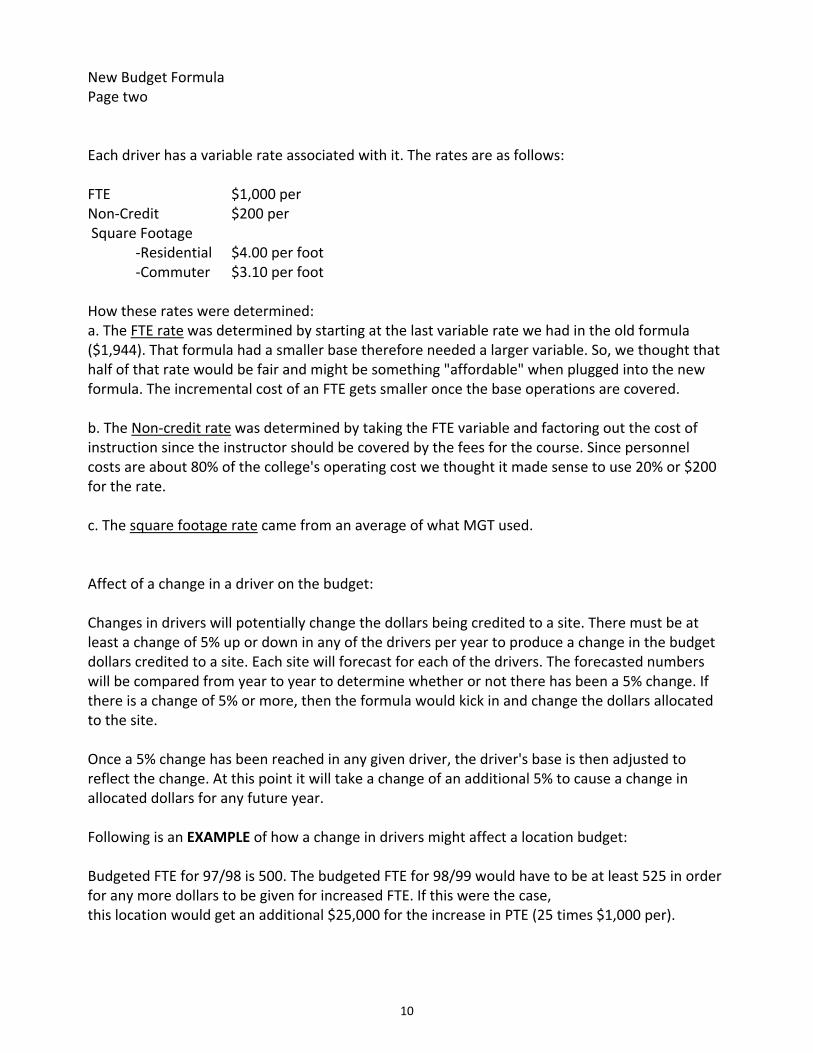

New Budget Formula Page two Each driver has a variable rate associated with it. The rates are as follows: FTE $1,000 per Non‐Credit $200 per Square Footage

‐Residential $4.00 per foot ‐Commuter $3.10 per foot

How these rates were determined: a. The FTE rate was determined by starting at the last variable rate we had in the old formula ($1,944). That formula had a smaller base therefore needed a larger variable. So, we thought that half of that rate would be fair and might be something "affordable" when plugged into the new formula. The incremental cost of an FTE gets smaller once the base operations are covered. b. The Non‐credit rate was determined by taking the FTE variable and factoring out the cost of instruction since the instructor should be covered by the fees for the course. Since personnel costs are about 80% of the college's operating cost we thought it made sense to use 20% or $200 for the rate. c. The square footage rate came from an average of what MGT used. Affect of a change in a driver on the budget: Changes in drivers will potentially change the dollars being credited to a site. There must be at least a change of 5% up or down in any of the drivers per year to produce a change in the budget dollars credited to a site. Each site will forecast for each of the drivers. The forecasted numbers will be compared from year to year to determine whether or not there has been a 5% change. If there is a change of 5% or more, then the formula would kick in and change the dollars allocated to the site. Once a 5% change has been reached in any given driver, the driver's base is then adjusted to reflect the change. At this point it will take a change of an additional 5% to cause a change in allocated dollars for any future year. Following is an EXAMPLE of how a change in drivers might affect a location budget: Budgeted FTE for 97/98 is 500. The budgeted FTE for 98/99 would have to be at least 525 in order for any more dollars to be given for increased FTE. If this were the case, this location would get an additional $25,000 for the increase in PTE (25 times $1,000 per).

10

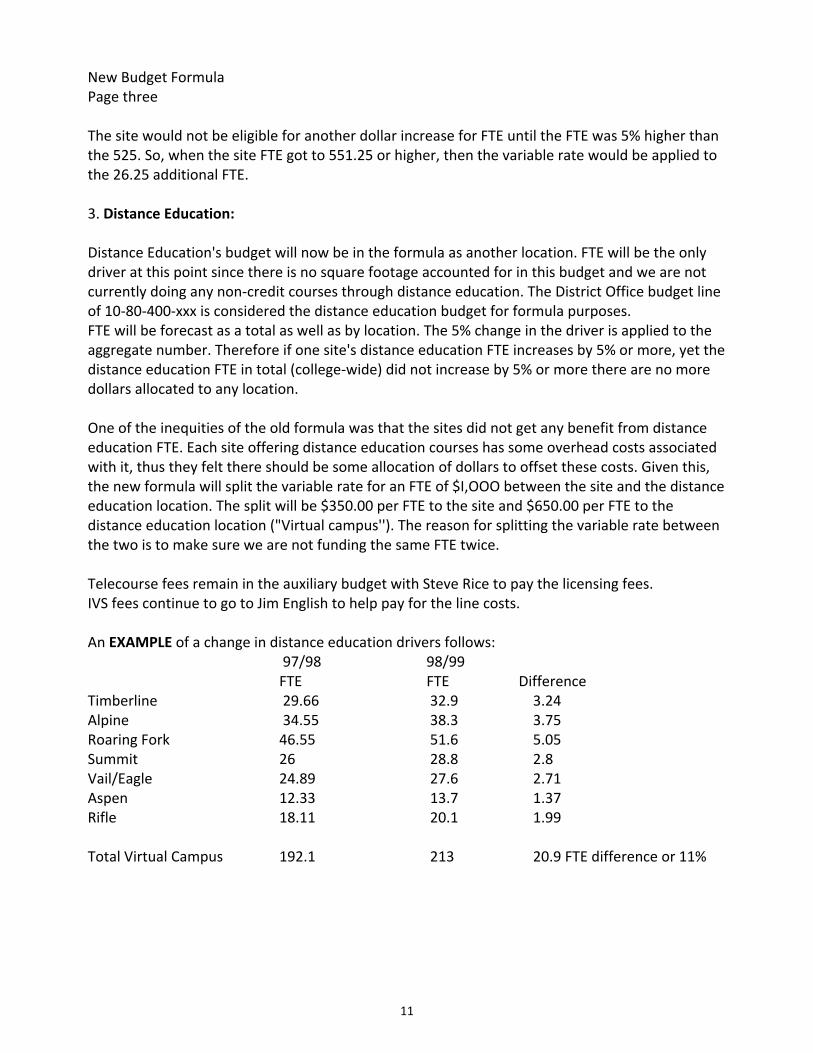

New Budget Formula Page three The site would not be eligible for another dollar increase for FTE until the FTE was 5% higher than the 525. So, when the site FTE got to 551.25 or higher, then the variable rate would be applied to the 26.25 additional FTE. 3. Distance Education: Distance Education's budget will now be in the formula as another location. FTE will be the only driver at this point since there is no square footage accounted for in this budget and we are not currently doing any non‐credit courses through distance education. The District Office budget line of 10‐80‐400‐xxx is considered the distance education budget for formula purposes. FTE will be forecast as a total as well as by location. The 5% change in the driver is applied to the aggregate number. Therefore if one site's distance education FTE increases by 5% or more, yet the distance education FTE in total (college‐wide) did not increase by 5% or more there are no more dollars allocated to any location. One of the inequities of the old formula was that the sites did not get any benefit from distance education FTE. Each site offering distance education courses has some overhead costs associated with it, thus they felt there should be some allocation of dollars to offset these costs. Given this, the new formula will split the variable rate for an FTE of $I,OOO between the site and the distance education location. The split will be $350.00 per FTE to the site and $650.00 per FTE to the distance education location ("Virtual campus''). The reason for splitting the variable rate between the two is to make sure we are not funding the same FTE twice. Telecourse fees remain in the auxiliary budget with Steve Rice to pay the licensing fees. IVS fees continue to go to Jim English to help pay for the line costs. An EXAMPLE of a change in distance education drivers follows:

97/98 98/99 FTE FTE Difference

Timberline 29.66 32.9 3.24 Alpine 34.55 38.3 3.75 Roaring Fork 46.55 51.6 5.05 Summit 26 28.8 2.8 Vail/Eagle 24.89 27.6 2.71 Aspen 12.33 13.7 1.37 Rifle 18.11 20.1 1.99 Total Virtual Campus 192.1 213 20.9 FTE difference or 11%

11

New Budget Formula Page four The change in the total FTE (11%) is what determines a change in the dollar allocations. The variable is split between the sites and the Virtual campus. Following is how the allocation would work ‐note that differences from the previous page have been rounded to the nearest whole FTE: Timberline $ 1,050 (3 x $350) Alpine 1,400 (4 x $350) Roaring Fork 1,750 (5 x $350) Summit 1,050 (3 x $350) Vail/Eagle 1,050 (3 x $350) Aspen 350 (1 x $350) Rifle 700 (2 x $350) Virtual $ 13,650 (21 x $650) Total New$$ $ 21,000 (21 x $1,000) The new FTE base for the Virtual campus would now be 213. Not until the FTE projection reaches 223.65 (5% increase) will there be another allocation of funds to either the Virtual campus or any other site.

12

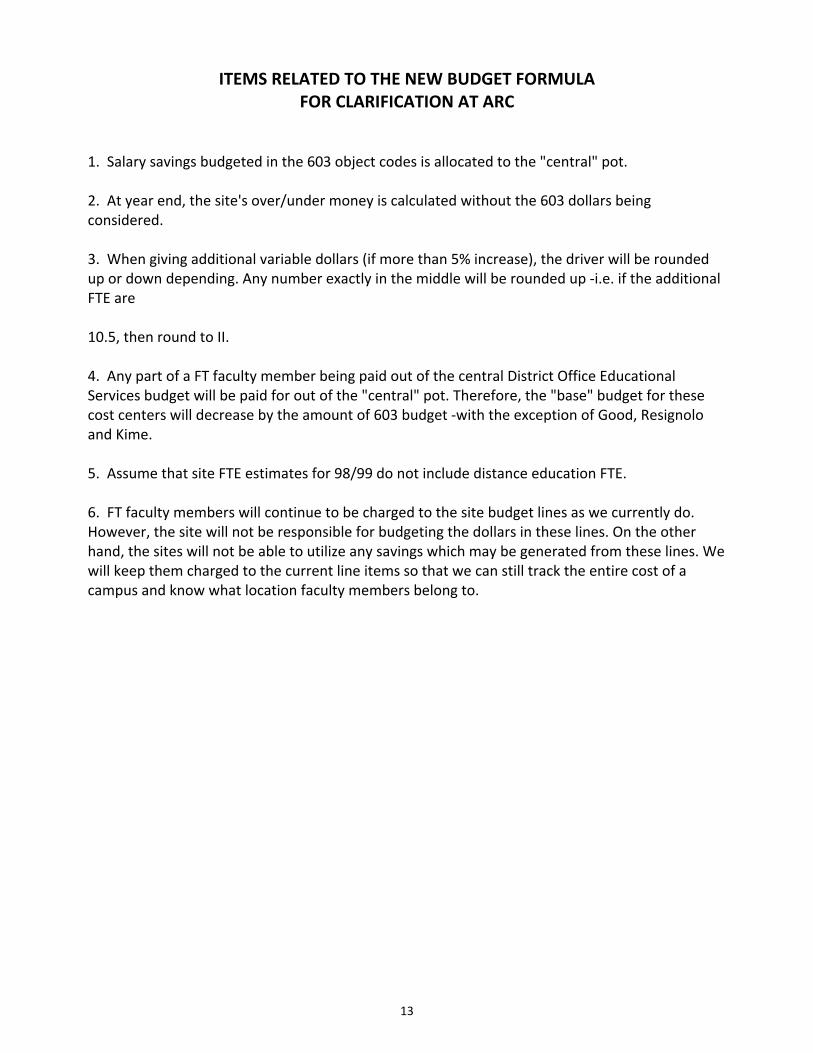

ITEMS RELATED TO THE NEW BUDGET FORMULA

FOR CLARIFICATION AT ARC 1. Salary savings budgeted in the 603 object codes is allocated to the "central" pot. 2. At year end, the site's over/under money is calculated without the 603 dollars being considered. 3. When giving additional variable dollars (if more than 5% increase), the driver will be rounded up or down depending. Any number exactly in the middle will be rounded up ‐i.e. if the additional FTE are 10.5, then round to II. 4. Any part of a FT faculty member being paid out of the central District Office Educational Services budget will be paid for out of the "central" pot. Therefore, the "base" budget for these cost centers will decrease by the amount of 603 budget ‐with the exception of Good, Resignolo and Kime. 5. Assume that site FTE estimates for 98/99 do not include distance education FTE. 6. FT faculty members will continue to be charged to the site budget lines as we currently do. However, the site will not be responsible for budgeting the dollars in these lines. On the other hand, the sites will not be able to utilize any savings which may be generated from these lines. We will keep them charged to the current line items so that we can still track the entire cost of a campus and know what location faculty members belong to.

13

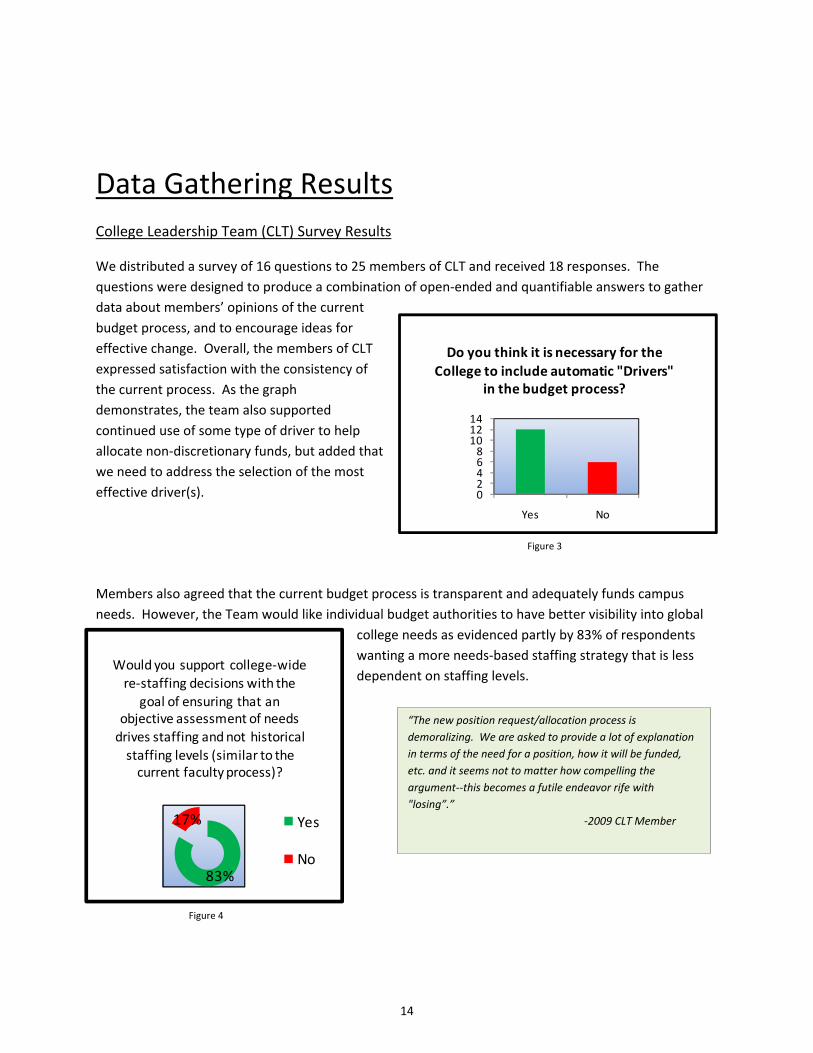

Data Gathering Results College Leadership Team (CLT) Survey Results

We distributed a survey of 16 questions to 25 members of CLT and received 18 responses. The questions were designed to produce a combination of open‐ended and quantifiable answers to gather data about members’ opinions of the current budget process, and to encourage ideas for effective change. Overall, the members of CLT expressed satisfaction with the consistency of the current process. As the graph demonstrates, the team also supported continued use of some type of driver to help allocate non‐discretionary funds, but added that we need to address the selection of the most effective driver(s).

Members also agreed that the current budget process is transparent and adequately funds campus needs. However, the Team would like individual budget authorities to have better visibility into global

college needs as evidenced partly by 83% of respondents wanting a more needs‐based staffing strategy that is less dependent on staffing levels.

02468

101214

Yes No

Do you think it is necessary for the College to include automatic "Drivers"

in the budget process?

83%

17%

Would you support college‐wide re‐staffing decisions with the

goal of ensuring that an objective assessment of needs

drives staffing and not historical staffing levels (similar to the

current faculty process)?

Yes

No

“The new position request/allocation process is demoralizing. We are asked to provide a lot of explanation in terms of the need for a position, how it will be funded, etc. and it seems not to matter how compelling the argument‐‐this becomes a futile endeavor rife with "losing”.”

‐2009 CLT Member

Figure 3

Figure 4

14

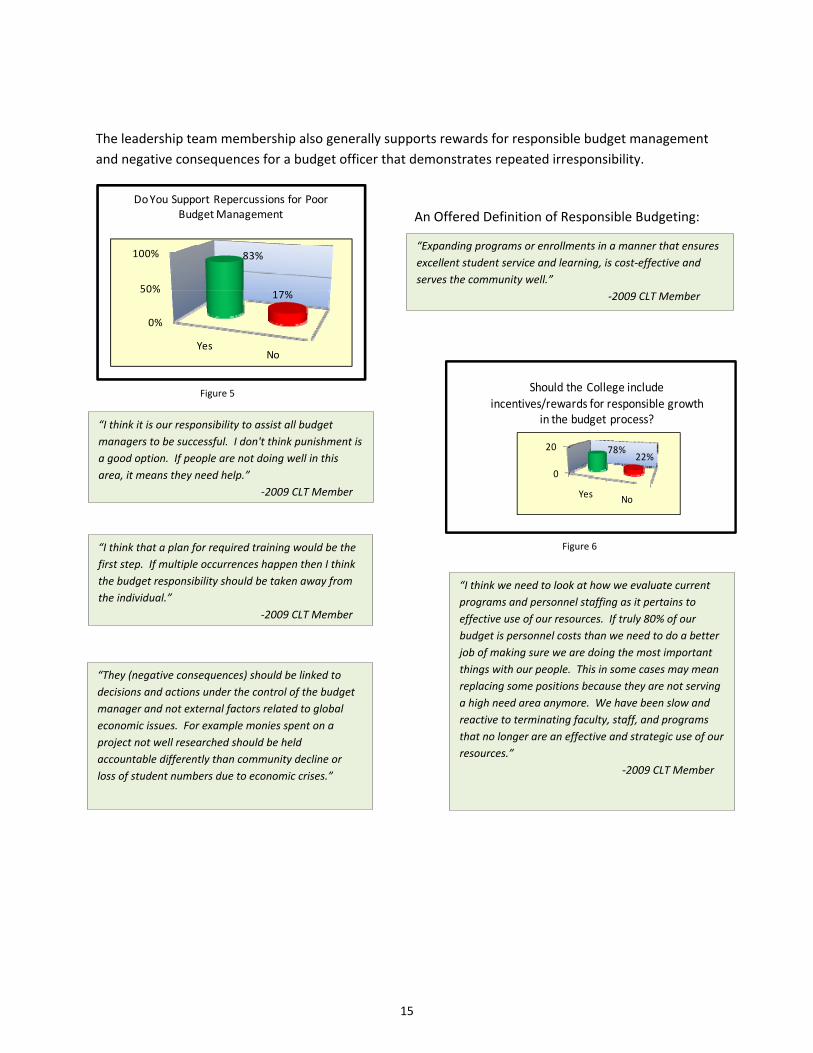

The leadership team membership also generally supports rewards for responsible budget management and negative consequences for a budget officer that demonstrates repeated irresponsibility.

0%

50%

100%

YesNo

83%

17%

Do You Support Repercussions for Poor Budget Management

0

20

Yes No

78%22%

Should the College include incentives/rewards for responsible growth

in the budget process?

“Expanding programs or enrollments in a manner that ensures excellent student service and learning, is cost‐effective and serves the community well.” ‐2009 CLT Member

An Offered Definition of Responsible Budgeting:

“I think it is our responsibility to assist all budget managers to be successful. I don't think punishment is a good option. If people are not doing well in this area, it means they need help.” ‐2009 CLT Member

“I think that a plan for required training would be the first step. If multiple occurrences happen then I think the budget responsibility should be taken away from the individual.”

‐2009 CLT Member

“They (negative consequences) should be linked to decisions and actions under the control of the budget manager and not external factors related to global economic issues. For example monies spent on a project not well researched should be held accountable differently than community decline or loss of student numbers due to economic crises.”

“I think we need to look at how we evaluate current programs and personnel staffing as it pertains to effective use of our resources. If truly 80% of our budget is personnel costs than we need to do a better job of making sure we are doing the most important things with our people. This in some cases may mean replacing some positions because they are not serving a high need area anymore. We have been slow and reactive to terminating faculty, staff, and programs that no longer are an effective and strategic use of our resources.”

‐2009 CLT Member

Figure 5

Figure 6

15

We provided several important characteristics of the budget process below and asked CLT members to rate each on a scale of 1 to 4; where a 4 needs the most attention. The control chart below represents their input, ranked from left to right with the most opportunity to improve on the left side of the graph.

3.1 3.1

3.0

2.9

2.8 2.82.8

2.7

2.6

2.5

2.42.3

2.0

2.2

2.4

2.6

2.8

3.0

3.2

College‐wide perspective

Uses staff expertise

Aligns resources

with strategic plan

Is consistent and uses

reliable data

Responsive to economy

Easy to understand

Adequately funds new initiatives

Responsive to community

Aligns with T2R2

Generates flexible budget

Funds campus neeeds

Is Transparent

Average Ratings of Current Budget Process

Needs Improvement Excellent

“Individual requests, no matter how large or small, are given fair consideration. It's not terribly stressful ‐‐ largely because we have experienced a number of years with stable to surplus funding.” ‐2009 CLT Member

Figure 7

16

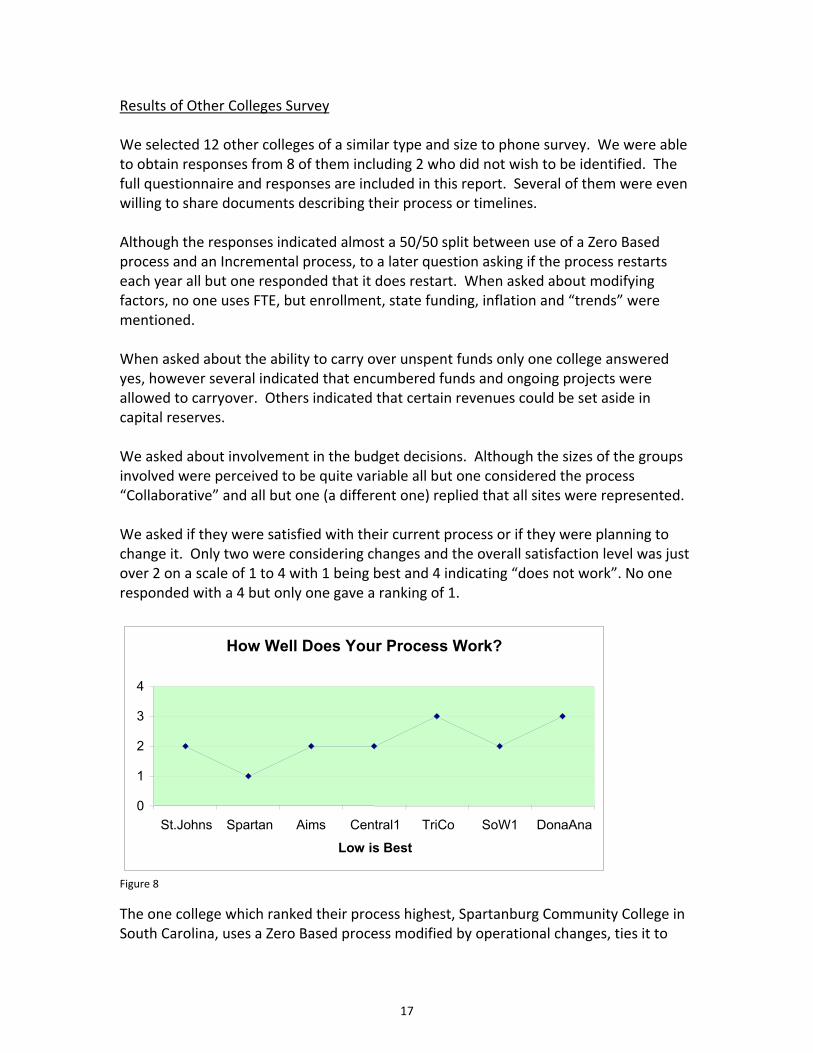

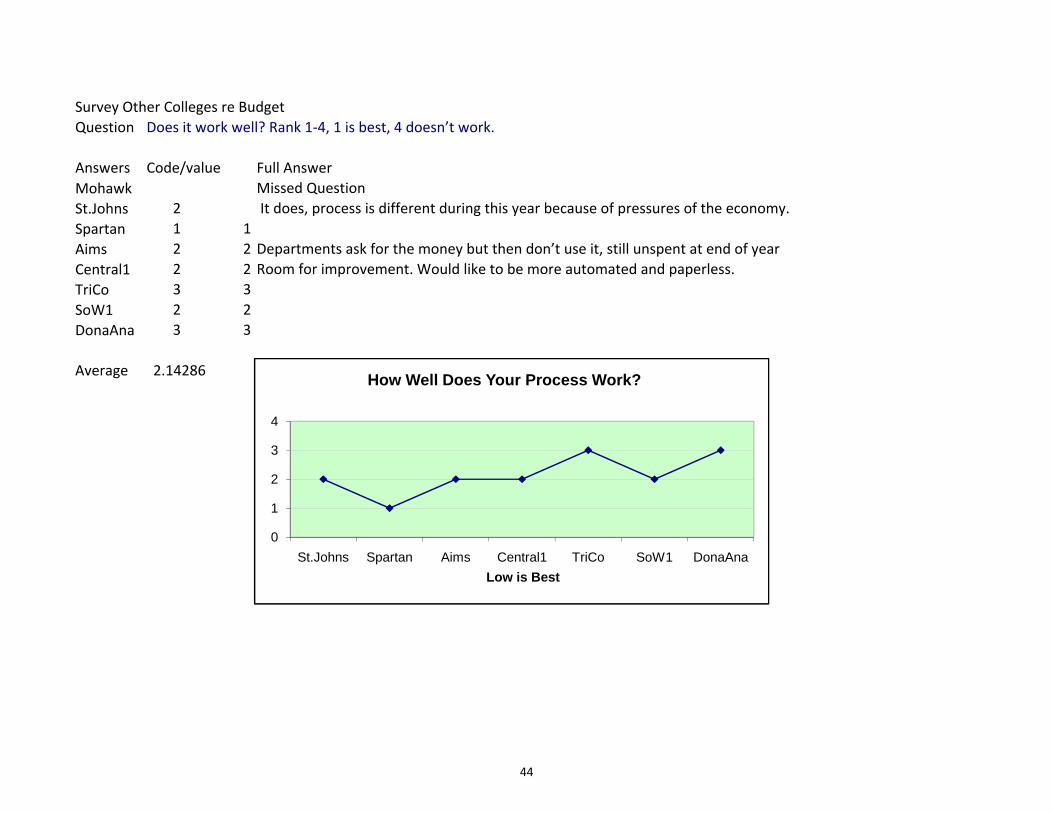

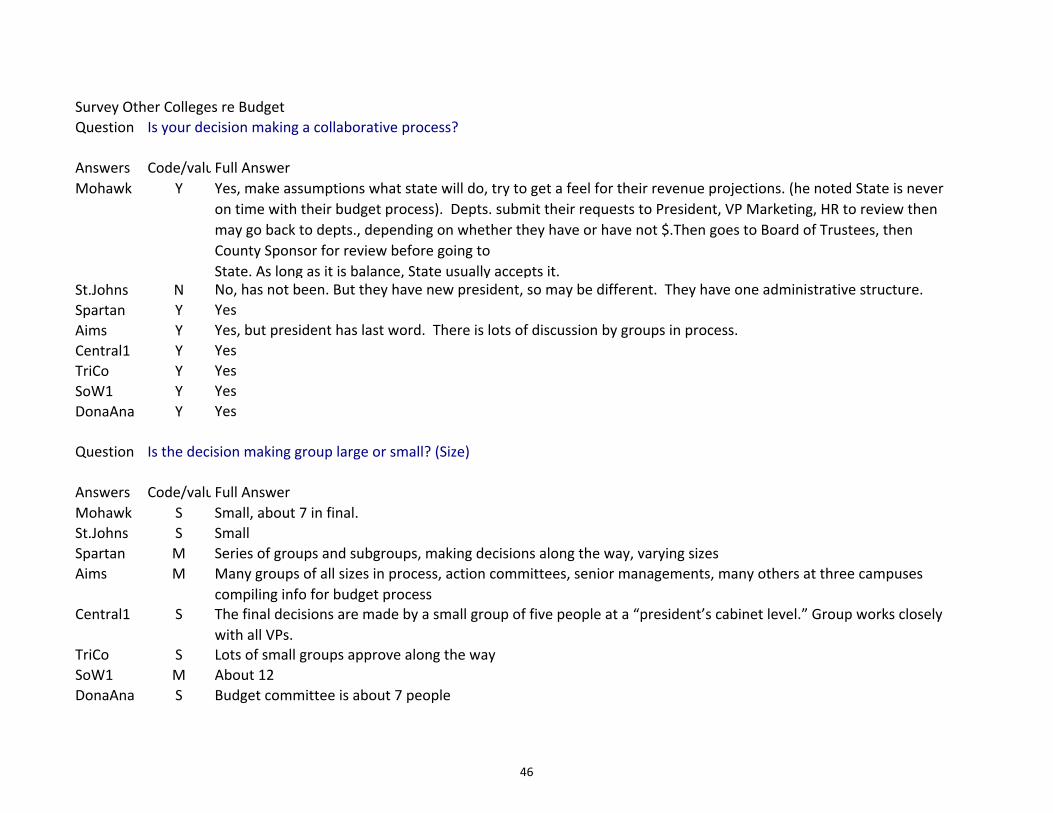

Results of Other Colleges Survey We selected 12 other colleges of a similar type and size to phone survey. We were able to obtain responses from 8 of them including 2 who did not wish to be identified. The full questionnaire and responses are included in this report. Several of them were even willing to share documents describing their process or timelines. Although the responses indicated almost a 50/50 split between use of a Zero Based process and an Incremental process, to a later question asking if the process restarts each year all but one responded that it does restart. When asked about modifying factors, no one uses FTE, but enrollment, state funding, inflation and “trends” were mentioned. When asked about the ability to carry over unspent funds only one college answered yes, however several indicated that encumbered funds and ongoing projects were allowed to carryover. Others indicated that certain revenues could be set aside in capital reserves. We asked about involvement in the budget decisions. Although the sizes of the groups involved were perceived to be quite variable all but one considered the process “Collaborative” and all but one (a different one) replied that all sites were represented. We asked if they were satisfied with their current process or if they were planning to change it. Only two were considering changes and the overall satisfaction level was just over 2 on a scale of 1 to 4 with 1 being best and 4 indicating “does not work”. No one responded with a 4 but only one gave a ranking of 1.

How Well Does Your Process Work?

0

1

2

3

4

St.Johns Spartan Aims Central1 TriCo SoW1 DonaAna

Low is Best

Figure 8

The one college which ranked their process highest, Spartanburg Community College in South Carolina, uses a Zero Based process modified by operational changes, ties it to

17

their strategic plan, is very inclusive and collaborative and devotes a full day to establishing plan objectives. They monitor the budget closely during the year balancing the needs of departments when changing conditions warrant. Two areas that produced almost completely uniform responses were Strategic Goals and Over Spending. When asked about tying strategic goals to budgets all but one replied “Yes”. St. Johns River CC is even working on a software package to link the two processes. Various methods were referenced to accomplish this correlation. Although very few indicated that a formal process was in place to hold someone accountable for budget results everyone responded that overspending was not allowed. Comments included “not possible” “closely watched” “explained” “transfers requested”. To see each college’s individual responses, please see the appendix. If you wish to review the materials supplied by the other colleges please see a team member.

18

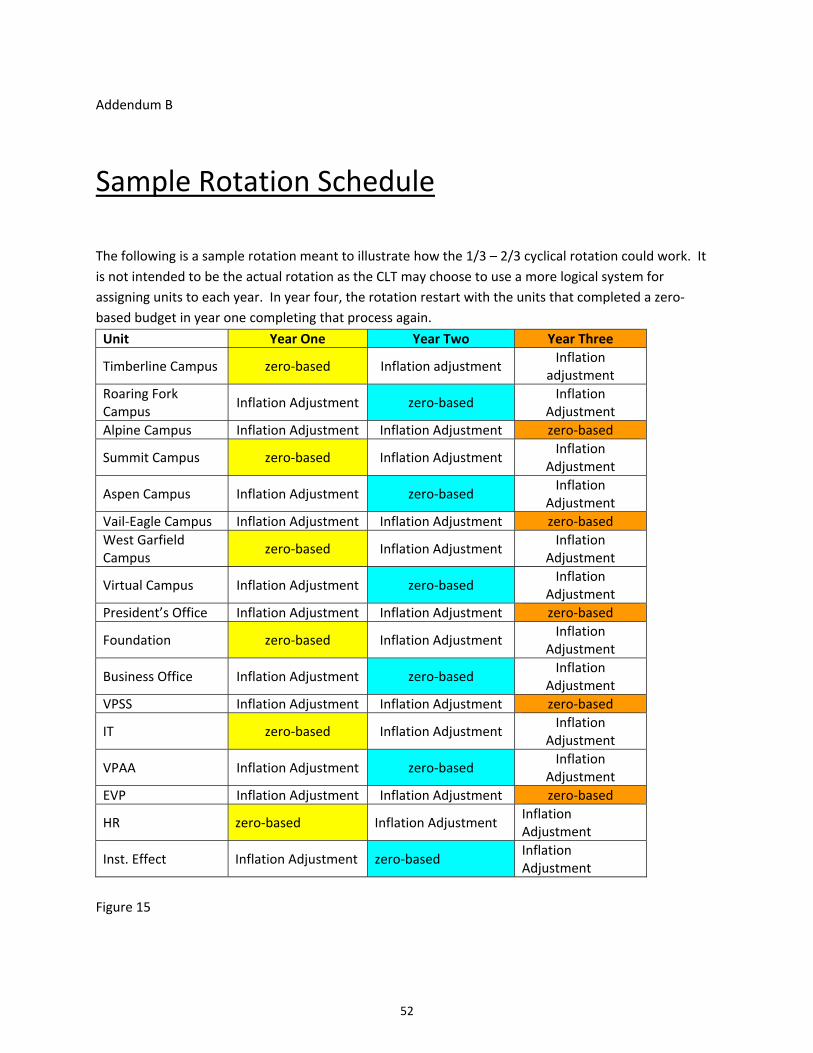

Improvement Theory Zero‐based budgeting will improve the development of base budgets for campuses and

Central Services (CS) units as measured by alignment with strategic plan, standardization and transparency of spending decisions, and adoption of financial best practices among similar units.

Changes in System

Implementing this improvement theory will result in substantial and wide‐reaching changes in the College’s budget system. As with any epochal change, implementing zero‐based budgeting will mark a new period of financial planning distinctive from the current paradigm. As is often the case with a change of this magnitude, we anticipate a relatively tempestuous time as people become familiar and eventually comfortable with the new paradigm. The fundamental changes in the system include the following:

• Discontinuation of current drivers for campus base budgets

• Detailed review of CS units’ base budgets on cyclical basis

• One‐third of campuses and CS units produce a zero‐based budget each year

• The other two‐thirds of campuses and CS units receive a budget increase based upon an “inflation adjustment” driver for years when they are not preparing a zero‐based budget

• President/CEO and CFO (and/or designees) determine the standard inflation adjustment during the revenue projection process

• More sophisticated cost‐center‐specific data analysis utilized for budget development

• Inefficiencies ended and best practices implemented system wide

Each of these changes is described in detail in the Recommendations section of this report.

Costs of Improvement

Adopting the zero‐based budgeting approach will have no costs of improvement except for “time costs”.

Time Costs

Implementing a new budget process requires significant investment of personnel time to develop standardized templates for presenting each budget, accepted and well

19

defined data sets, documentation standards, and operational definitions. Once preliminary work is completed, training curriculum must be developed ensuring that people preparing budgets clearly understand and can implement the process for their unit(s). It will require personnel time to deliver training to those staff members who will be developing zero‐based budgets. Lastly, campus and CS unit leaders will need to implement a zero‐based budget process, which likely will require more time to develop and apply data and project costs relative to the current process.

• Time to develop zero‐based model and guiding principles o Operational definitions of key concepts o Development of data sets relevant to specific cost centers o Regulations for what expenses are included and those that are not (i.e., fixed

costs) o Standardized templates for presenting budget (probably Excel spreadsheets) o Relevant equations and accepted calculations

• “Training” staff time to develop curriculum

• Campus and CS unit leadership time to receive training (including training staff time)

• Campus and CS units time to complete a zero‐based budget

Cost Savings

In a survey of the College Leadership Team, 89.5 percent responded that the current process “does not work” or “needs improvement” in aligning financial resources with the College strategic plan. Assuming the College will continue to have finite financial resources, it is clear that budget decisions that do not align with the strategic plan have a real cost in terms of limiting the College’s ability to fund projects and programs that will contribute to reaching strategic goals. By requiring that each cost center in a budget demonstrate alignment with the College mission, vision or strategic plan, zero‐based budgeting will drive alignment thus enabling the achievement of those goals as quickly and efficiently as possible. The current system does not readily identify and encourage the adoption of financial best practices. By allowing inefficiencies or poor decision making to continue, the current budget process perpetuates incalculable costs. For instance, if a campus realizes savings by developing a more efficient approach to scheduling adjunct faculty members and other locations do not replicate that approach, the College is missing an opportunity to realize cost savings. In a zero‐based environment, the innovation would be apparent in the documentation of the first campus’ budget proposal. Other campuses that had

20

not adopted the innovation would then have an opportunity to implement the new approach and save costs or defend why it is not possible in their environment/situation.

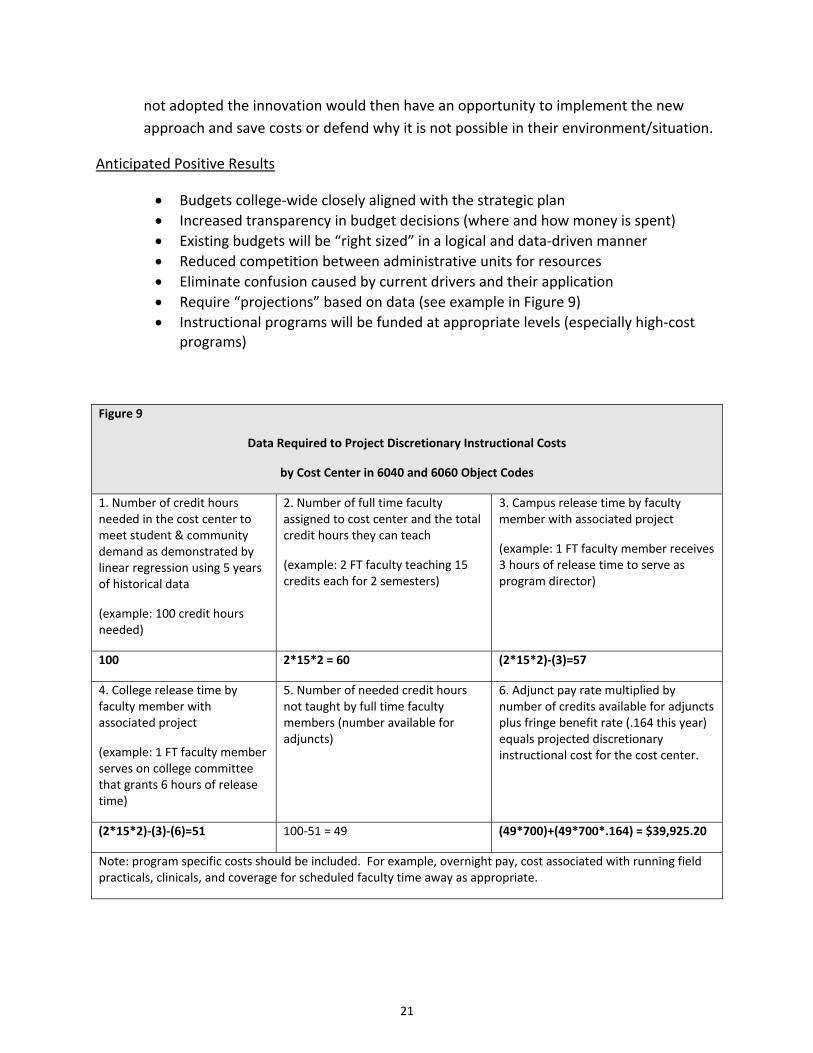

Anticipated Positive Results

• Budgets college‐wide closely aligned with the strategic plan • Increased transparency in budget decisions (where and how money is spent) • Existing budgets will be “right sized” in a logical and data‐driven manner • Reduced competition between administrative units for resources • Eliminate confusion caused by current drivers and their application • Require “projections” based on data (see example in Figure 9) • Instructional programs will be funded at appropriate levels (especially high‐cost

programs)

Figure 9

Data Required to Project Discretionary Instructional Costs

by Cost Center in 6040 and 6060 Object Codes

1. Number of credit hours needed in the cost center to meet student & community demand as demonstrated by linear regression using 5 years of historical data

(example: 100 credit hours needed)

2. Number of full time faculty assigned to cost center and the total credit hours they can teach

(example: 2 FT faculty teaching 15 credits each for 2 semesters)

3. Campus release time by faculty member with associated project

(example: 1 FT faculty member receives 3 hours of release time to serve as program director)

100 2*15*2 = 60 (2*15*2)‐(3)=57

4. College release time by faculty member with associated project

(example: 1 FT faculty member serves on college committee that grants 6 hours of release time)

5. Number of needed credit hours not taught by full time faculty members (number available for adjuncts)

6. Adjunct pay rate multiplied by number of credits available for adjuncts plus fringe benefit rate (.164 this year) equals projected discretionary instructional cost for the cost center.

(2*15*2)‐(3)‐(6)=51 100‐51 = 49 (49*700)+(49*700*.164) = $39,925.20

Note: program specific costs should be included. For example, overnight pay, cost associated with running field practicals, clinicals, and coverage for scheduled faculty time away as appropriate.

21

Recommendations Narrative Feedback from College Leadership Team members clearly identified campus budget drivers as the aspect of the budget process most in need of change. None of the colleges that responded to the team’s telephone survey utilized anything resembling “drivers” in their budget process. Half of those respondents use some form of zero‐based budgeting as the foundation of their budget development process. Consequently, the team strongly recommends that Colorado Mountain College adopt zero‐based budgeting for campus and CS base budgets. Under the current system, CS units automatically receive the same funding each year and engage in the discretionary funds process (RATS) to increase that funding. At present, there is no systematic process for reviewing a CS unit’s budget decisions. The current system does not ensure alignment with the strategic plan, review efficacy of consultants and conferences, determine if the unit is implementing best practices, or reduce a unit’s budget level for programs/activities that are not efficient or effective. In order to correct the above shortfalls in the current paradigm, the team’s recommendation is that CS units engage in zero‐based budgeting on the same cyclical rotation as campuses.

Zero‐based budgeting is a method in which all expenditures must be justified (which includes strategic plan alignment). Because it requires significant documentation and review of data, zero‐based budgeting can be more time intensive than other approaches (see Appendix: The Pros and Cons of Zero‐Based Budgeting). To address this potentiality, the team recommends that only one‐third of campuses and CS units complete a zero‐based budget each year. The team’s recommendation is that, for those years when they do not complete a zero‐based budget, campuses or CS units receive an increase in budget based upon an “inflation adjustment” driver. The President and CFO and/or their designees will determine the percentage of increase used for the driver as part of the revenue projection process. As noted in the cost savings section of this report, the current drivers for campus budgets were ranked either “does not work” or “needs improvement” by a large majority of the CLT. In a focus group with a cross‐section of the CLT that included a number of VP/Campus CEOs, this finding was strongly reinforced. Guided by this information, the team recommends the elimination of current drivers for campus budgets. Going forward, campuses cyclically will complete a zero‐based budget or receive an increase based upon the “inflation adjustment” driver.

22

In order to fully realize the utility of zero‐based budgeting it is critical that the College adopt consistent data points for determining costs, financial operational definitions, and accepted methodology for documenting anticipated expenses. Sophisticated cost‐center‐specific data analysis will be developed, enabling effective determination of best practices. It is also important the College Leadership Team (or ad hoc subcommittee) determine how budgets will relate to the Strategic Plan and a mutually agreed upon rubric for that relationship by cost center. By taking this recommendation, the College will avoid each unit applying the strategic plan to their expenses in different manners, which would make reviewing them very difficult.

The College will need to implement required training on developing a zero‐based budget for budget officers that includes standard operating procedures, accountability on spending, operational definitions, standardized spreadsheets with equations, and accepted methodology for projecting costs.

The team recommends no change to the revenue projection, base general fund carry forward, and discretionary funding process (i.e., RATS).

Bulleted List of Recommendations

• Adopt zero‐based budgeting for Campus and CS budgets • Create a schedule where one‐third of campuses and CS units complete a zero‐

based budget each year • Institute an “inflation adjustment” driver to adjust the base budgets of those

campuses and CS units that are not completing a zero‐based budget that year • Eliminate the use of current drivers for creating campus budgets • Create an ad hoc committee that includes the members of this AQIP team and

other key administrators and charge it with developing consistent data points for determining costs, financial operational definitions, and accepted methodology for documenting anticipated expenses

• Create an ad hoc committee (with some membership overlap with the one above, but not complete overlap) to develop and implement training on how to develop, document, and defend a zero‐based budget

• CLT or a subcommittee develop approved rubric for associating costs to the College strategic plan

• Require training for budget officers on zero‐based budgeting

23

Link to AQIP Criteria • Mission and Integrity: By adopting a zero‐based budget model, most spending

within the College will be tied directly to the Strategic Plan, which is based upon our mission. Budget officers will be called upon in the review process to defend how their anticipated spending in most cost centers ties to the College strategic plan.

• Preparing for the Future o Measuring Effectiveness: In order to truly measure the effectiveness of the

budget process in preparing the College for the future, it is vitally important that we have a shared understanding of how resources are allocated and expended. By infusing consistency throughout the budgeting process, we will position the College to implement best practices throughout the district and effectively allocate resources to support growth. Zero‐based budgeting can be the mechanism for achieving these ends.

o Supporting Institutional Operations: If campuses and CS units are not adequately funded to fulfill their individual missions, it is difficult to imagine how the institution as a whole can fulfill its strategic plan and ultimately its vision.

• Student Learning and Effective Teaching o Understanding Students’ and Other Stakeholders’ Needs: Each location and

department/division serves students and stakeholders who have unique needs. Zero‐based budgeting will allow the College to be responsive to those needs in a much more efficient manner than the current, somewhat blunt, approach of relying upon historical funding levels (CS) or drivers (campuses).

24

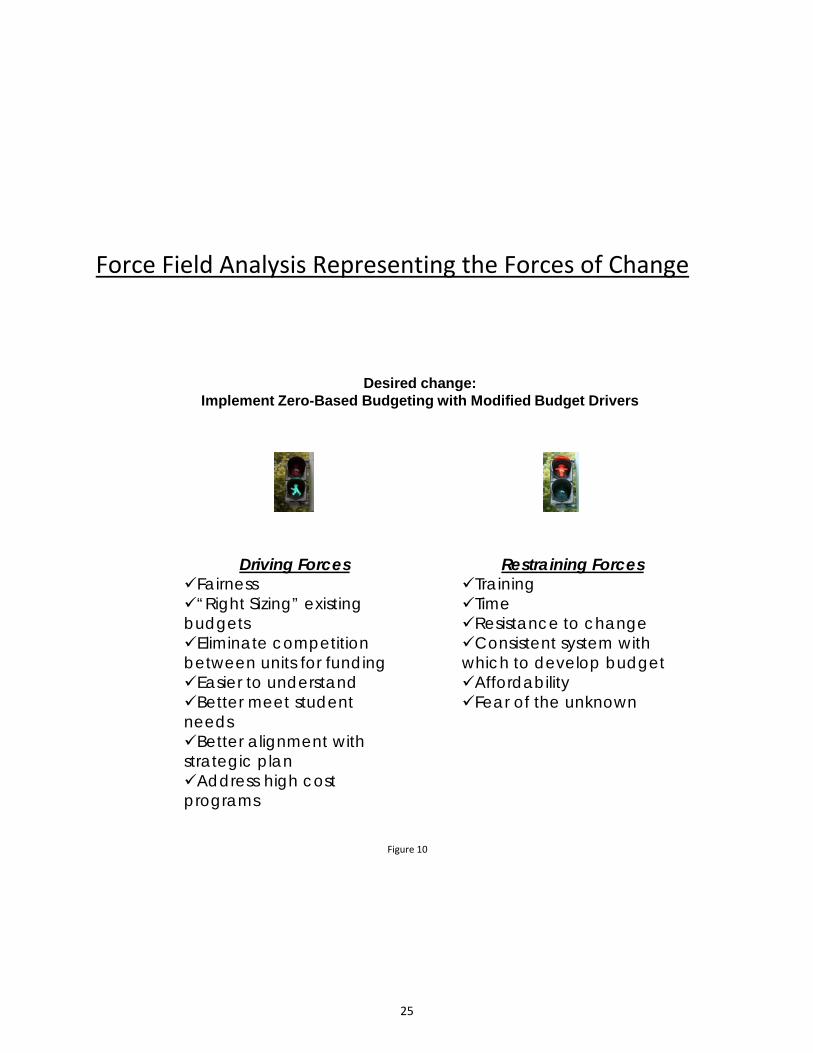

Force Field Analysis Representing the Forces of Change

Desired change: Implement Zero-Based Budgeting with Modified Budget Drivers

Driving ForcesFairness“Right Sizing” existing budgetsEliminate competition between units for fundingEasier to understandBetter meet student needsBetter alignment with strategic planAddress high cost programs

Restraining ForcesTrainingTimeResistance to changeConsistent system with which to develop budgetAffordabilityFear of the unknown

Figure 10

25

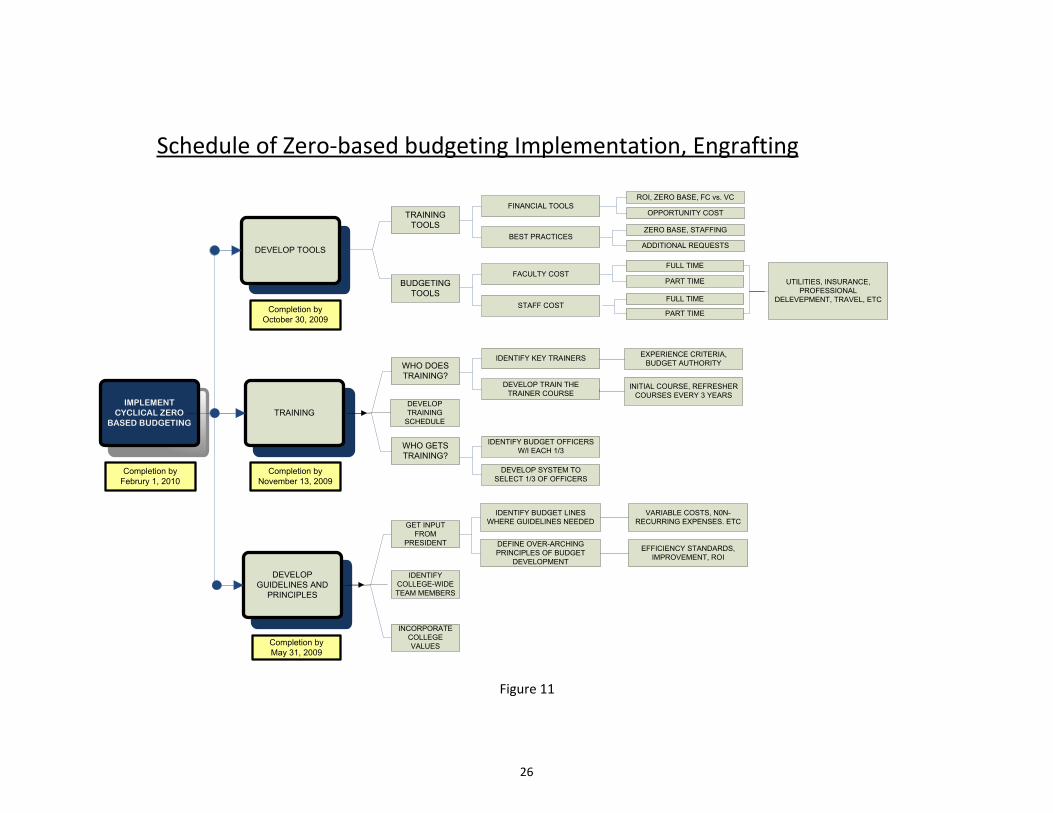

IMPLEMENT CYCLICAL ZERO

BASED BUDGETING

DEVELOP TOOLS

DEVELOP GUIDELINES AND

PRINCIPLES

TRAINING

GET INPUT FROM

PRESIDENT

INCORPORATE COLLEGE VALUES

TRAINING TOOLS

BUDGETING TOOLS

WHO DOES TRAINING?

WHO GETS TRAINING?

IDENTIFY COLLEGE-WIDE TEAM MEMBERS

IDENTIFY KEY TRAINERS

DEVELOP TRAIN THE TRAINER COURSE

IDENTIFY BUDGET OFFICERS W/I EACH 1/3

DEVELOP SYSTEM TO SELECT 1/3 OF OFFICERS

IDENTIFY BUDGET LINES WHERE GUIDELINES NEEDED

DEFINE OVER-ARCHING PRINCIPLES OF BUDGET

DEVELOPMENT

EFFICIENCY STANDARDS, IMPROVEMENT, ROI

FINANCIAL TOOLS

BEST PRACTICES

FACULTY COST

STAFF COST

FULL TIME

PART TIME

FULL TIME

PART TIME

UTILITIES, INSURANCE, PROFESSIONAL

DELEVEPMENT, TRAVEL, ETC

EXPERIENCE CRITERIA, BUDGET AUTHORITY

INITIAL COURSE, REFRESHER COURSES EVERY 3 YEARS

ROI, ZERO BASE, FC vs. VC

OPPORTUNITY COST

ZERO BASE, STAFFING

ADDITIONAL REQUESTS

VARIABLE COSTS, N0N-RECURRING EXPENSES. ETC

Completion by May 31, 2009

DEVELOP TRAINING

SCHEDULE

Completion by Februry 1, 2010

Completion by November 13, 2009

Completion by October 30, 2009

Schedule of Zero‐based budgeting Implementation, Engrafting

Figure 11

26

ENGRAFTING THE IMPROVEMENTS INTO THE SYSTEM We recommend the formation of an ad hoc committee made up of key administrators, Business Office, and the AQIP Budget Team to develop norms and set guidelines for documenting anticipated expenses. This group will meet frequently prior to the start of the traditional budget process. Once this information is in place, those with budget responsibilities, such as Campuses, CEO’s, and Budget Managers, will be trained on developing budgets with the new format. Due to the 3 year rotation system, it will take some time before all the results are in. However, there are ways to start measuring the success or failure of the project. The Budget Team will survey both the “Zero‐Base” group and those on the alternate year schedules to get their opinions about the new budget process. A mid‐year review will be conducted as well. These results will be shared with CLT and evaluated. The budget team will then conduct an annual survey for the next 3 years and share the results with CLT. Financial data with a comparison of prior year’s results will be readily available. New recommendations for improvement may come as a result of all these actions. It is anticipated that the new process will result in less variation in over or under spending by each unit at the end of each fiscal year. This will be tracked by the Business Office and report each year end.

27

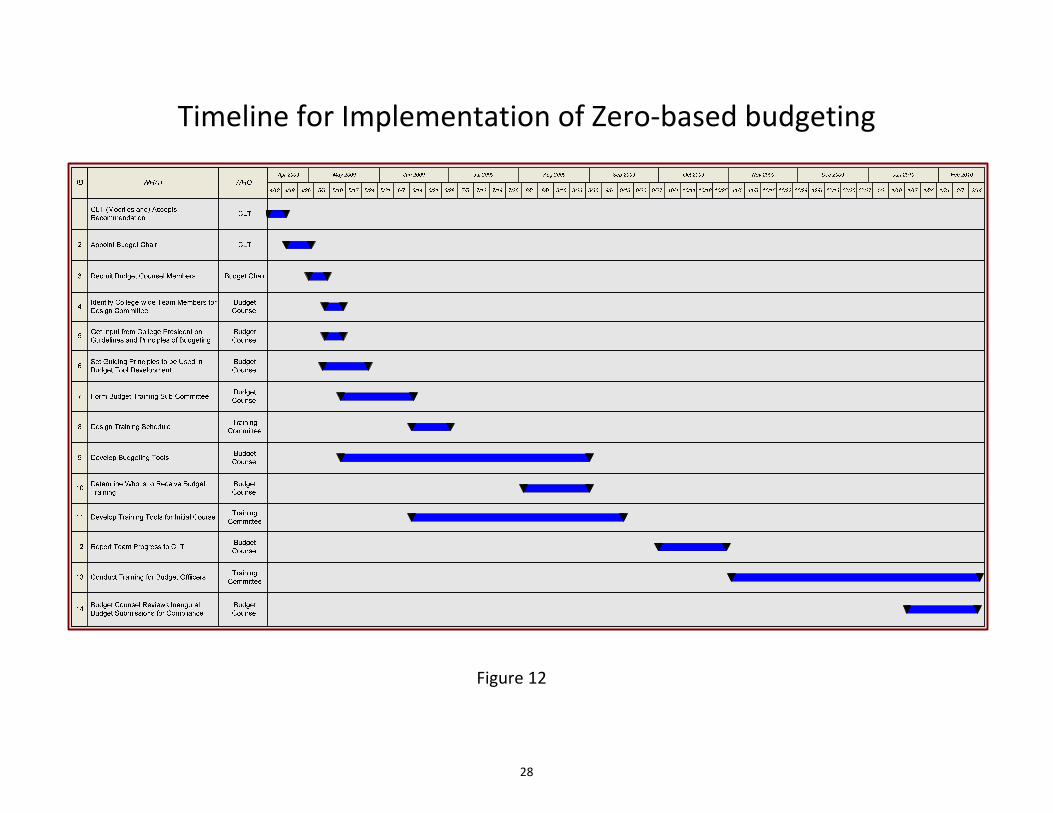

Timeline for Implementation of Zero‐based budgeting

Figure 12

28

Ideas for Future Team Improvements To determine if there should be an assessment system in place to encourage accurate budget controls Modifications to the current full time staff salary savings program Improvements in reports, making them more user‐ friendly Strategies for creating larger, innovation funding pools Working out appropriate balance between high and low cost programs, by campus

29

College Leadership Team Feedback

Team Name: BUDGET IMPROVEMENT TEAM Date: April 13, 2009 Sponsors: Linda English, Joe Maestas

Ideas for Improvement: Support Adopt zero‐based budgeting for Campus and CS budgets ______ Create a schedule for 1/3 of campuses and CS units to complete a zero‐based budget each year ______ Institute an “inflation adjustment” driver to adjust the base budgets to those campuses and CS units that are not completing a zero‐based budget that year ______ Eliminate the use of current drivers for creating campus budgets ______ Create an ad hoc committee that includes the members of this AQIP team, and other key administrators, charging it with developing consistent data points for determining costs, financial operational definitions, and accepted methodology for documenting anticipated expenses ______ Create an ad hoc committee (with some membership overlap with the one above, but not complete overlap) to develop and implement training on how to develop, document and defend a zero‐based budget ______ CLT or a subcommittee develop approved rubric for associating costs to the College Strategic Plan ______ Require training for budget officers on zero‐based budgeting ______ Team Feedback Meeting – Date:__________ Sponsors: Linda English, Joe Maestas Leader: Mike Simon

30

With Thanks…

The AQIP Budget Team wishes to thank the following people and organizations for sharing their time and effort and knowledge: Meeta Goel, Ph.D., and Lin Stickler for their valuable research. Stanley Jensen, Ph.D., for his expertise in taking us through this process. CLT team for answering the surveys and attending our In‐Focus group. Our Co‐Sponsors, Linda English and Joe Maestas, for their wisdom and patience, and without whom we could never have completed this project. Those individuals at our offices who helped as well as backed us up, during many absences, including Anne Maclean and Rebecca Arrington for their help on the cover. The staff at Edwards for their continual hospitality and delicious meals.

The Colleges who shared their own budget processes with us, including Aims Community College (CO), Dona Ana Community College (NM), Mohawk Valley Community College (NY), Spartanburg Community College (SC), St Johns River Community College (FL), Tri‐County Technical College (SC) and several others who wished not to be identified.

31

Appendix

32

Comments from CLT Survey

What do you like the most about the current budget process (list no more than 3 items)?

1

2 1. Open process 2. Good discussion 3. Most seemed reasonable and balanced in decision‐making

3 ‐It is very inclusive regarding decision‐making for allocation of resources ‐It allows campuses to retain most of their auxillary budget dollars each year (roll‐over) ‐It is moving closer to alignment with strategic plan

41. The information provided by the Business Office 2. The colloborative process used

51. It is starting to become more aligned with the Strategic Plan. 2. It is to a large degree open and transparent.

6 opportunity to request dollars with justification relatively easy to read

7 1. There is campus and Central Services representation for making budget decisions. 2. Anyone can ask for funds 3. We generally think in a college wide perspective when making budget decisions.

8 Seeing thebudter as a whole Undertanding other campuses needs

9 1. We have discretionary funds (most schools don't) 2. It is a group process where people can be heard 3. In most cases, people do seem to have a college‐wide perspective when making decisions

10 1. The ability to provide input into what is funded. 2. That we are fortunate to have money to fund many requests. 3. The spirit of team and helping each other out, cross functional and across campuses.

11 Linda does a good job of managing our budget.

12The people involved treat others respectfully The timeline is usually well communicated and reasonable

13Individual requests, no matter how large or small, are given fair consideration. It's not terribly stressful ‐‐ largely because we have experienced a number of years with stable to surplus funding.

14 We are moving towards aligning the budget to our goals.

15 The presentation/explanation of each request

16 We get it done with wide ranging involvement.

17‐ the preliminary review of technology requests by the IT Council (ITC), and the resulting short list of items that end up at RATS. The ITC is made up of college‐wide representatives, and as such this preliminary review and trimming process produces a li

18Collaborative and open ‐ no back‐room agreements and surprises That faculty allocation and ITC have already determined priorities before they come to RATS That we are in a better place of openness and trust than in past years

Figure 13

33

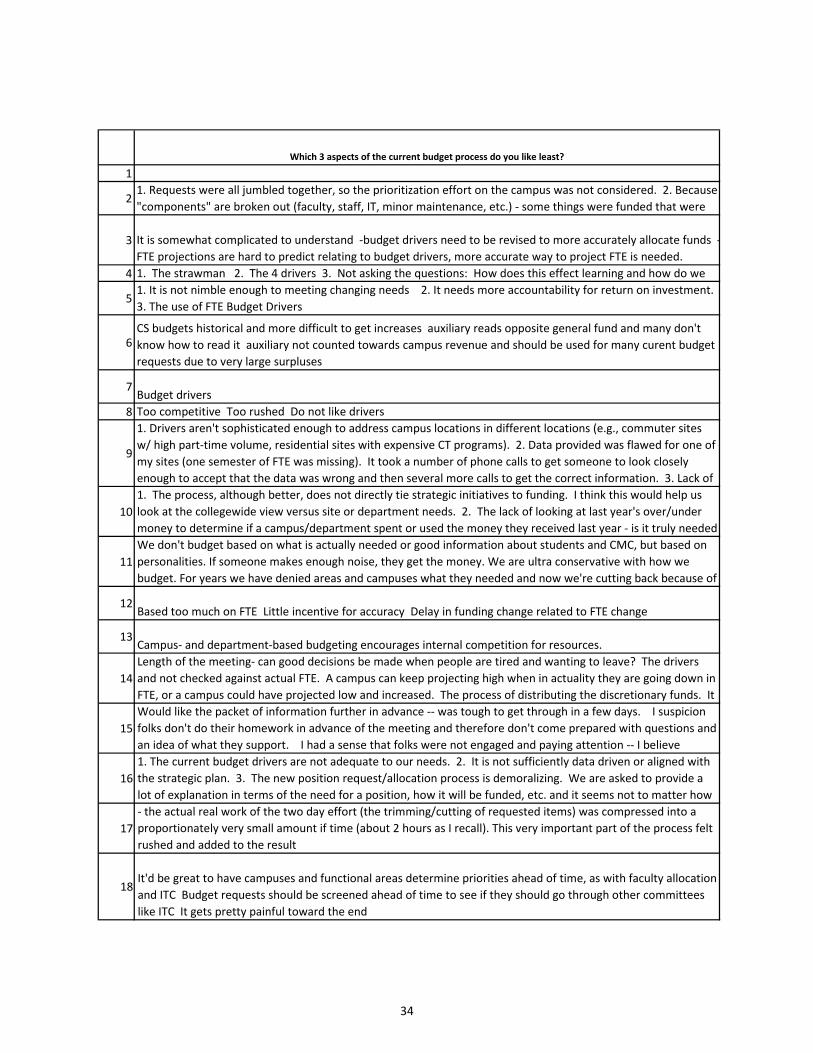

Which 3 aspects of the current budget process do you like least?

1

21. Requests were all jumbled together, so the prioritization effort on the campus was not considered. 2. Because "components" are broken out (faculty, staff, IT, minor maintenance, etc.) ‐ some things were funded that were

3 It is somewhat complicated to understand ‐budget drivers need to be revised to more accurately allocate funds ‐FTE projections are hard to predict relating to budget drivers, more accurate way to project FTE is needed.

4 1. The strawman 2. The 4 drivers 3. Not asking the questions: How does this effect learning and how do we

51. It is not nimble enough to meeting changing needs 2. It needs more accountability for return on investment. 3. The use of FTE Budget Drivers

6CS budgets historical and more difficult to get increases auxiliary reads opposite general fund and many don't know how to read it auxiliary not counted towards campus revenue and should be used for many curent budget requests due to very large surpluses

7Budget drivers

8 Too competitive Too rushed Do not like drivers

9

1. Drivers aren't sophisticated enough to address campus locations in different locations (e.g., commuter sites w/ high part‐time volume, residential sites with expensive CT programs). 2. Data provided was flawed for one of my sites (one semester of FTE was missing). It took a number of phone calls to get someone to look closely enough to accept that the data was wrong and then several more calls to get the correct information. 3. Lack of

101. The process, although better, does not directly tie strategic initiatives to funding. I think this would help us look at the collegewide view versus site or department needs. 2. The lack of looking at last year's over/under money to determine if a campus/department spent or used the money they received last year ‐ is it truly needed

11We don't budget based on what is actually needed or good information about students and CMC, but based on personalities. If someone makes enough noise, they get the money. We are ultra conservative with how we budget. For years we have denied areas and campuses what they needed and now we're cutting back because of

12Based too much on FTE Little incentive for accuracy Delay in funding change related to FTE change

13Campus‐ and department‐based budgeting encourages internal competition for resources.

14Length of the meeting‐ can good decisions be made when people are tired and wanting to leave? The drivers and not checked against actual FTE. A campus can keep projecting high when in actuality they are going down in FTE, or a campus could have projected low and increased. The process of distributing the discretionary funds. It

15Would like the packet of information further in advance ‐‐ was tough to get through in a few days. I suspicion folks don't do their homework in advance of the meeting and therefore don't come prepared with questions and an idea of what they support. I had a sense that folks were not engaged and paying attention ‐‐ I believe

161. The current budget drivers are not adequate to our needs. 2. It is not sufficiently data driven or aligned with the strategic plan. 3. The new position request/allocation process is demoralizing. We are asked to provide a lot of explanation in terms of the need for a position, how it will be funded, etc. and it seems not to matter how

17‐ the actual real work of the two day effort (the trimming/cutting of requested items) was compressed into a proportionately very small amount if time (about 2 hours as I recall). This very important part of the process felt rushed and added to the result

18It'd be great to have campuses and functional areas determine priorities ahead of time, as with faculty allocation and ITC Budget requests should be screened ahead of time to see if they should go through other committees like ITC It gets pretty painful toward the end

34

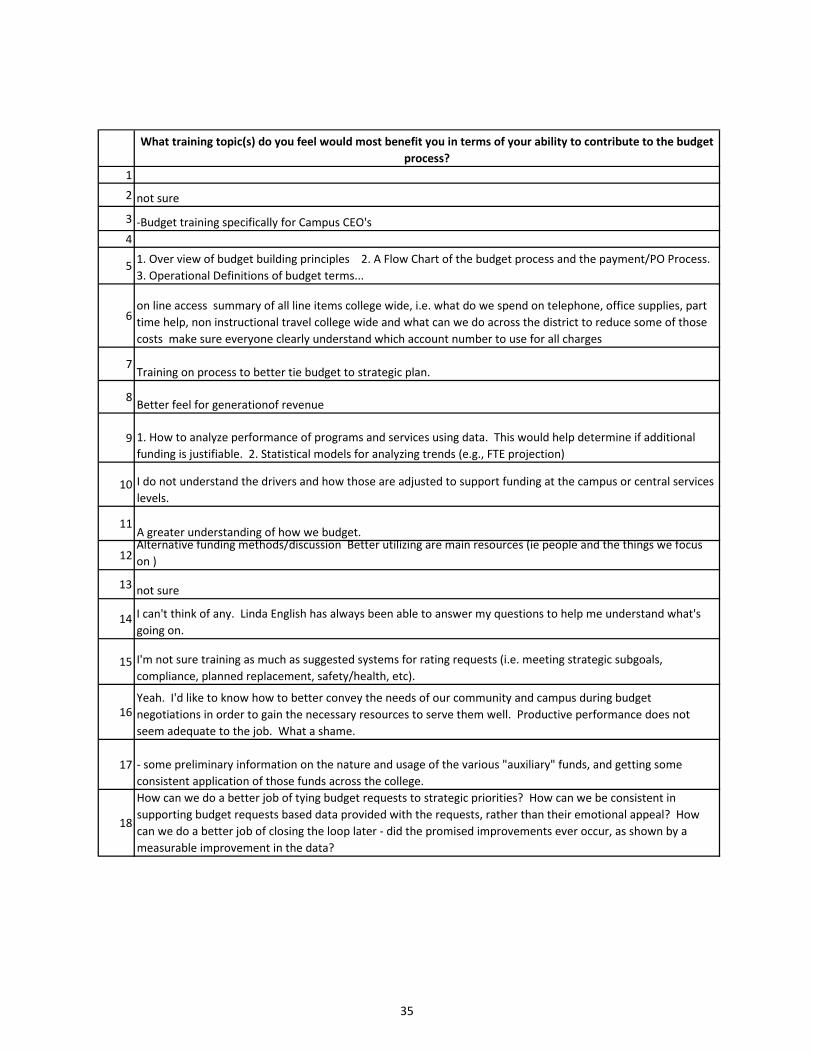

What training topic(s) do you feel would most benefit you in terms of your ability to contribute to the budget process?

1

2 not sure

3 ‐Budget training specifically for Campus CEO's4

5 1. Over view of budget building principles 2. A Flow Chart of the budget process and the payment/PO Process. 3. Operational Definitions of budget terms...

6on line access summary of all line items college wide, i.e. what do we spend on telephone, office supplies, part time help, non instructional travel college wide and what can we do across the district to reduce some of those costs make sure everyone clearly understand which account number to use for all charges

7Training on process to better tie budget to strategic plan.

8Better feel for generationof revenue

9 1. How to analyze performance of programs and services using data. This would help determine if additional funding is justifiable. 2. Statistical models for analyzing trends (e.g., FTE projection)

10 I do not understand the drivers and how those are adjusted to support funding at the campus or central services levels.

11A greater understanding of how we budget.

12Alternative funding methods/discussion Better utilizing are main resources (ie people and the things we focus on )

13 not sure

14 I can't think of any. Linda English has always been able to answer my questions to help me understand what's going on.

15 I'm not sure training as much as suggested systems for rating requests (i.e. meeting strategic subgoals, compliance, planned replacement, safety/health, etc).

16Yeah. I'd like to know how to better convey the needs of our community and campus during budget negotiations in order to gain the necessary resources to serve them well. Productive performance does not seem adequate to the job. What a shame.

17 ‐ some preliminary information on the nature and usage of the various "auxiliary" funds, and getting some consistent application of those funds across the college.

18

How can we do a better job of tying budget requests to strategic priorities? How can we be consistent in supporting budget requests based data provided with the requests, rather than their emotional appeal? How can we do a better job of closing the loop later ‐ did the promised improvements ever occur, as shown by a measurable improvement in the data?

35

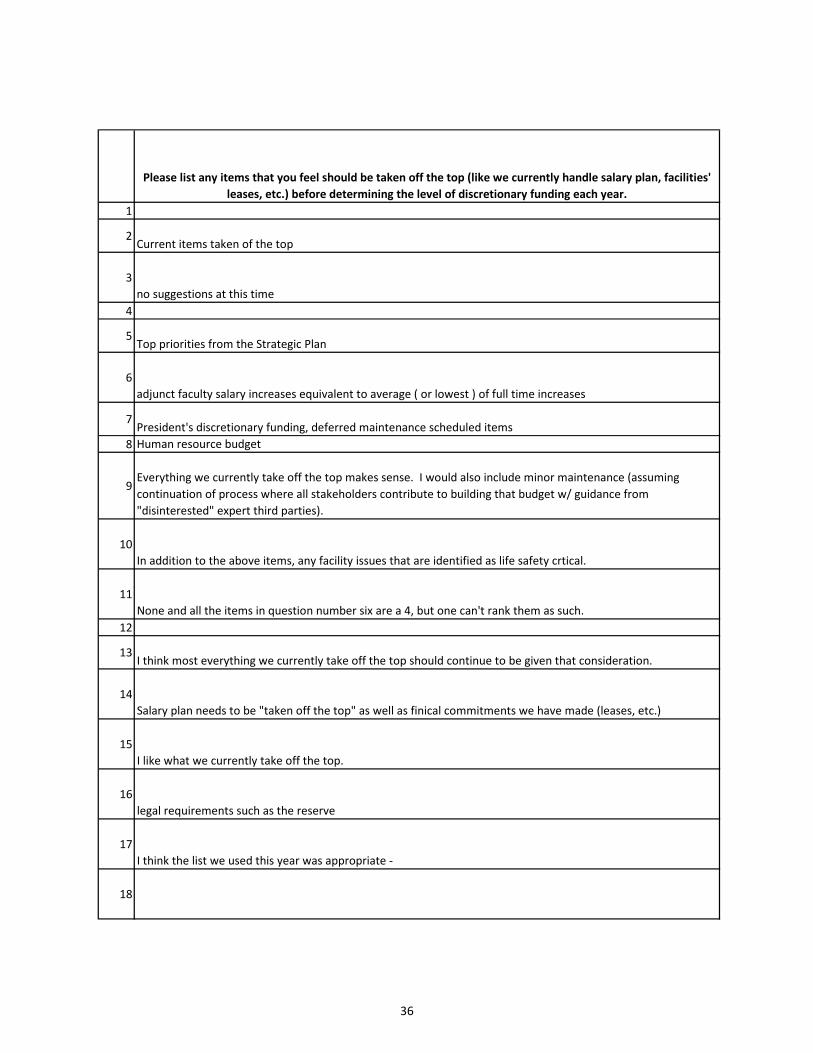

Please list any items that you feel should be taken off the top (like we currently handle salary plan, facilities' leases, etc.) before determining the level of discretionary funding each year.

1

2Current items taken of the top

3no suggestions at this time

4

5Top priorities from the Strategic Plan

6adjunct faculty salary increases equivalent to average ( or lowest ) of full time increases

7President's discretionary funding, deferred maintenance scheduled items

8 Human resource budget

9Everything we currently take off the top makes sense. I would also include minor maintenance (assuming continuation of process where all stakeholders contribute to building that budget w/ guidance from "disinterested" expert third parties).

10In addition to the above items, any facility issues that are identified as life safety crtical.

11None and all the items in question number six are a 4, but one can't rank them as such.

12

13I think most everything we currently take off the top should continue to be given that consideration.

14Salary plan needs to be "taken off the top" as well as finical commitments we have made (leases, etc.)

15I like what we currently take off the top.

16legal requirements such as the reserve

17I think the list we used this year was appropriate ‐

18

36

If you answered no to the previous question, can you recommend another mechanism for building campus base budgets (please briefly describe below)?

1

2

3

4

I am not sure what would be appropriate. I don't think the current process allows for growth nor does it support any type of student support services to assist our student population. Now, I am sure that some will say I am wrong, but my argument is that we do not offer services up front for our students. I think if we had more opportunities in our labs, mentoring and tutoring, base camp we would see more of our students complete their

5Building and SQ. foot drivers ... yes FTE Driver estimates ... no

6

7I think that it might be time to get rid of drivers and have campuses (including distance learning) come forth with individual requests for additional funding when they feel they need it. I would hope that this would then neutralize the competition surrounding FTE or any other metric we might use.

8 Zero based budget system

9I think the square footage and distance education drivers make sense. Credit/ESL and Non‐Credit FTE seem too blunt. I think some sort of zero‐base process makes sense if it were coupled with perhaps some combination of drivers to address needs like high‐cost programs, high proportion of part‐time students, etc.

10

11

12

13

14

15

16 Zero based budgeting has been tossed around. Surely there are best practices that we could emulate....whether it includes drivers or not.

17

18

37

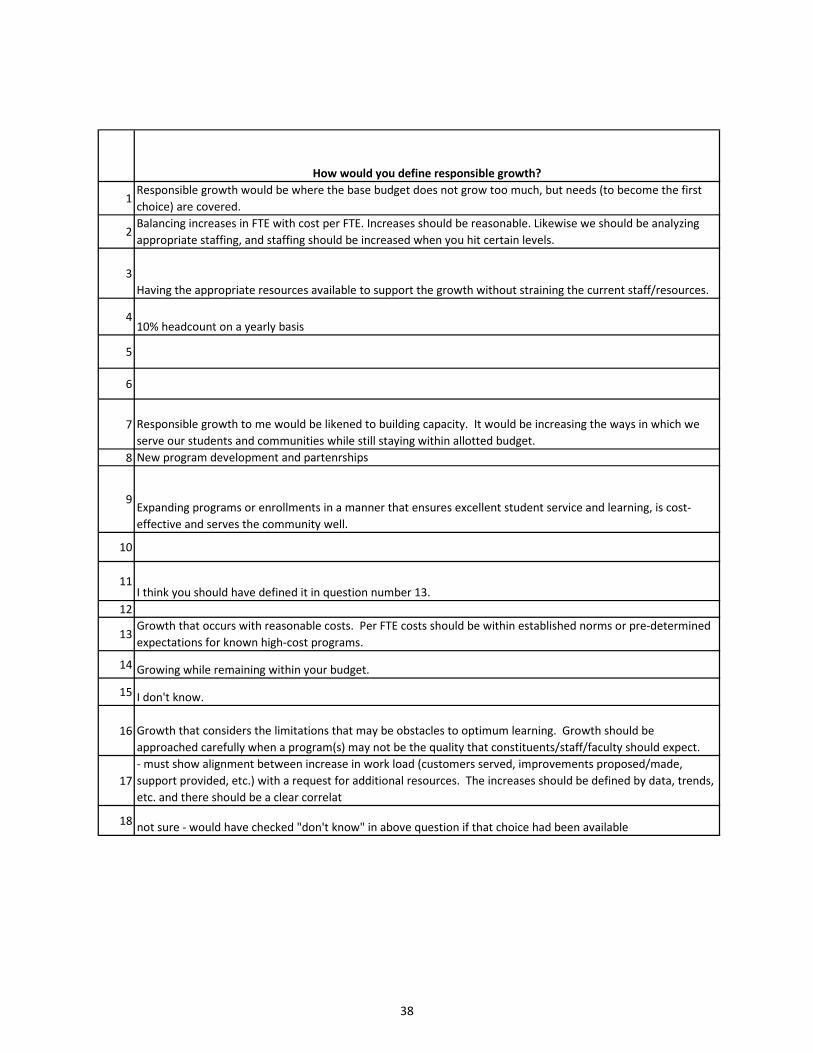

How would you define responsible growth?

1Responsible growth would be where the base budget does not grow too much, but needs (to become the first choice) are covered.

2Balancing increases in FTE with cost per FTE. Increases should be reasonable. Likewise we should be analyzing appropriate staffing, and staffing should be increased when you hit certain levels.

3Having the appropriate resources available to support the growth without straining the current staff/resources.

410% headcount on a yearly basis

5

6

7 Responsible growth to me would be likened to building capacity. It would be increasing the ways in which we serve our students and communities while still staying within allotted budget.

8 New program development and partenrships

9Expanding programs or enrollments in a manner that ensures excellent student service and learning, is cost‐effective and serves the community well.

10

11I think you should have defined it in question number 13.

12

13Growth that occurs with reasonable costs. Per FTE costs should be within established norms or pre‐determined expectations for known high‐cost programs.

14 Growing while remaining within your budget.

15 I don't know.

16 Growth that considers the limitations that may be obstacles to optimum learning. Growth should be approached carefully when a program(s) may not be the quality that constituents/staff/faculty should expect.

17‐ must show alignment between increase in work load (customers served, improvements proposed/made, support provided, etc.) with a request for additional resources. The increases should be defined by data, trends, etc. and there should be a clear correlat

18 not sure ‐ would have checked "don't know" in above question if that choice had been available

38

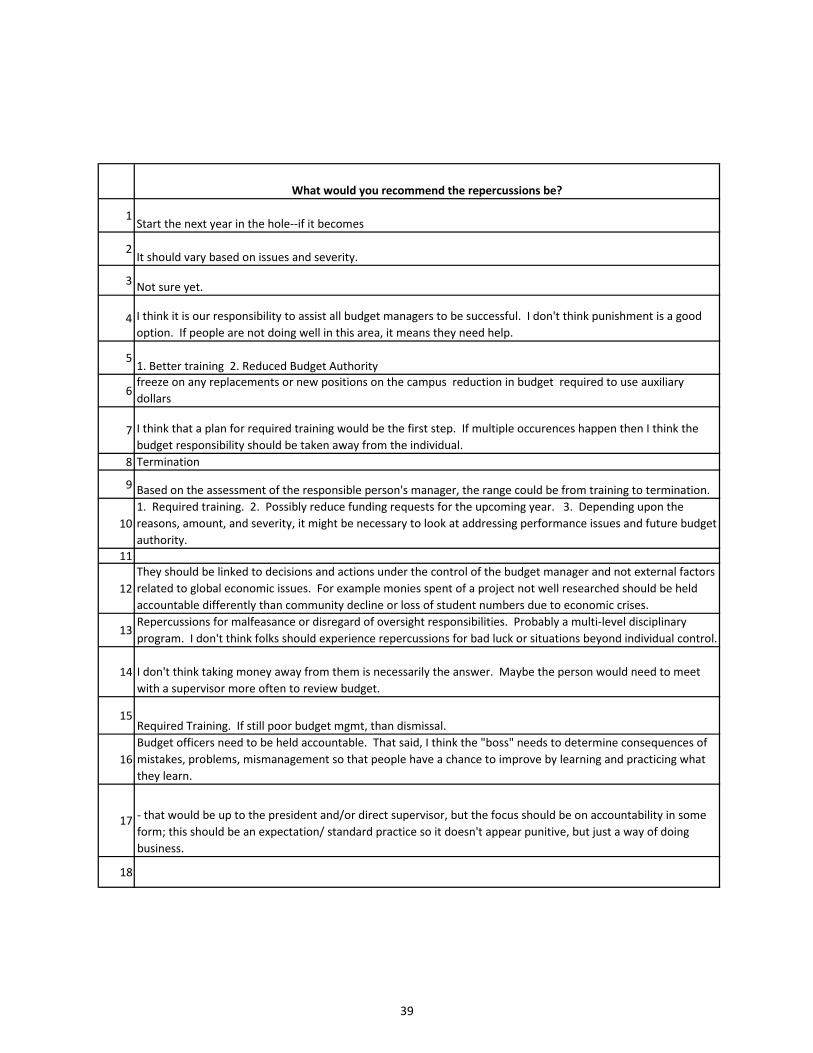

What would you recommend the repercussions be?

1Start the next year in the hole‐‐if it becomes

2It should vary based on issues and severity.

3 Not sure yet.

4 I think it is our responsibility to assist all budget managers to be successful. I don't think punishment is a good option. If people are not doing well in this area, it means they need help.

51. Better training 2. Reduced Budget Authority

6freeze on any replacements or new positions on the campus reduction in budget required to use auxiliary dollars

7 I think that a plan for required training would be the first step. If multiple occurences happen then I think the budget responsibility should be taken away from the individual.

8 Termination

9 Based on the assessment of the responsible person's manager, the range could be from training to termination.

101. Required training. 2. Possibly reduce funding requests for the upcoming year. 3. Depending upon the reasons, amount, and severity, it might be necessary to look at addressing performance issues and future budget authority.

11

12They should be linked to decisions and actions under the control of the budget manager and not external factors related to global economic issues. For example monies spent of a project not well researched should be held accountable differently than community decline or loss of student numbers due to economic crises.

13Repercussions for malfeasance or disregard of oversight responsibilities. Probably a multi‐level disciplinary program. I don't think folks should experience repercussions for bad luck or situations beyond individual control.

14 I don't think taking money away from them is necessarily the answer. Maybe the person would need to meet with a supervisor more often to review budget.

15Required Training. If still poor budget mgmt, than dismissal.

16Budget officers need to be held accountable. That said, I think the "boss" needs to determine consequences of mistakes, problems, mismanagement so that people have a chance to improve by learning and practicing what they learn.

17 ‐ that would be up to the president and/or direct supervisor, but the focus should be on accountability in some form; this should be an expectation/ standard practice so it doesn't appear punitive, but just a way of doing business.

18

39

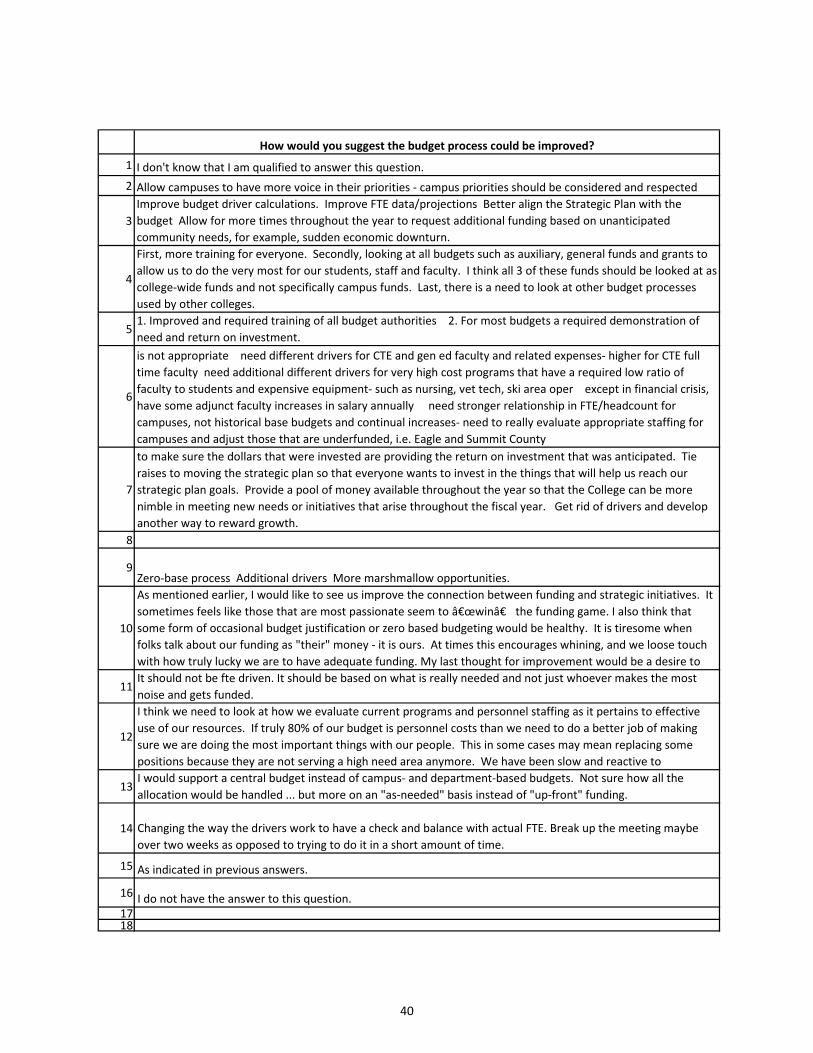

How would you suggest the budget process could be improved?

1 I don't know that I am qualified to answer this question.

2 Allow campuses to have more voice in their priorities ‐ campus priorities should be considered and respected

3Improve budget driver calculations. Improve FTE data/projections Better align the Strategic Plan with the budget Allow for more times throughout the year to request additional funding based on unanticipated community needs, for example, sudden economic downturn.

4

First, more training for everyone. Secondly, looking at all budgets such as auxiliary, general funds and grants to allow us to do the very most for our students, staff and faculty. I think all 3 of these funds should be looked at as college‐wide funds and not specifically campus funds. Last, there is a need to look at other budget processes used by other colleges.

51. Improved and required training of all budget authorities 2. For most budgets a required demonstration of need and return on investment.

6

is not appropriate need different drivers for CTE and gen ed faculty and related expenses‐ higher for CTE full time faculty need additional different drivers for very high cost programs that have a required low ratio of faculty to students and expensive equipment‐ such as nursing, vet tech, ski area oper except in financial crisis, have some adjunct faculty increases in salary annually need stronger relationship in FTE/headcount for campuses, not historical base budgets and continual increases‐ need to really evaluate appropriate staffing for campuses and adjust those that are underfunded, i.e. Eagle and Summit County

7

to make sure the dollars that were invested are providing the return on investment that was anticipated. Tie raises to moving the strategic plan so that everyone wants to invest in the things that will help us reach our strategic plan goals. Provide a pool of money available throughout the year so that the College can be more nimble in meeting new needs or initiatives that arise throughout the fiscal year. Get rid of drivers and develop another way to reward growth.

8

9Zero‐base process Additional drivers More marshmallow opportunities.

10

As mentioned earlier, I would like to see us improve the connection between funding and strategic initiatives. It sometimes feels like those that are most passionate seem to “winâ€� the funding game. I also think that some form of occasional budget justification or zero based budgeting would be healthy. It is tiresome when folks talk about our funding as "their" money ‐ it is ours. At times this encourages whining, and we loose touch with how truly lucky we are to have adequate funding. My last thought for improvement would be a desire to

11It should not be fte driven. It should be based on what is really needed and not just whoever makes the most noise and gets funded.

12

I think we need to look at how we evaluate current programs and personnel staffing as it pertains to effective use of our resources. If truly 80% of our budget is personnel costs than we need to do a better job of making sure we are doing the most important things with our people. This in some cases may mean replacing some positions because they are not serving a high need area anymore. We have been slow and reactive to

13I would support a central budget instead of campus‐ and department‐based budgets. Not sure how all the allocation would be handled ... but more on an "as‐needed" basis instead of "up‐front" funding.

14 Changing the way the drivers work to have a check and balance with actual FTE. Break up the meeting maybe over two weeks as opposed to trying to do it in a short amount of time.

15 As indicated in previous answers.

16 I do not have the answer to this question.1718

40

Phone Survey of colleges about Budget process College name

Person contacted & position

Person doing the interview

Can you describe the type of budget process you use? (examples: Zero Based or Incremental )

Does it work well? Rank 1-4, 1 is best, 4 doesn’t work.

Is your budget tied to your Strategic Plan?

How do you assure that?

Is your decision making a collaborative process?

Is the decision making group large or small? (Size)

Does the decision making group include leadership from all campuses?

Does the process completely restart each year or is there a modification from the prior year factored in?

What types of modifying factors do you use? (drivers)

Can you carry over any unspent funds or is funding strictly “use it or loose it”?

If you have any carry over, how do you allocate those funds or are they held in reserve for future needs?

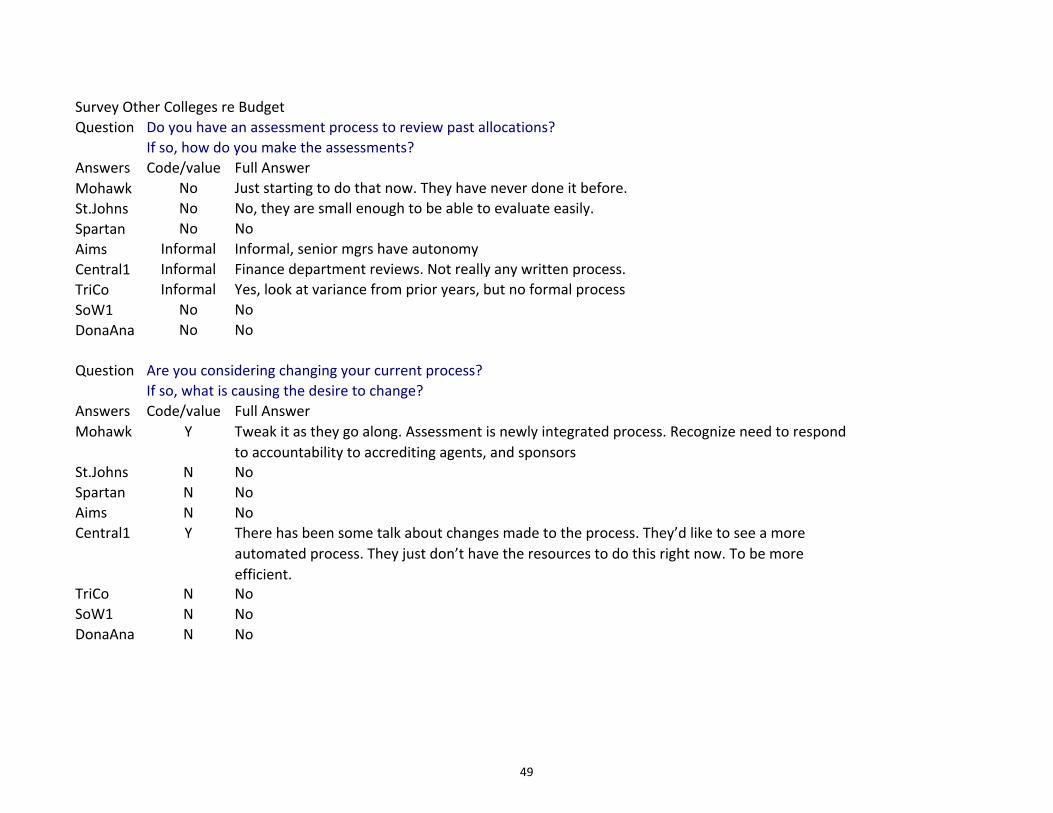

Do you have an assessment process to review past allocations?

If so, how do you make the assessments?

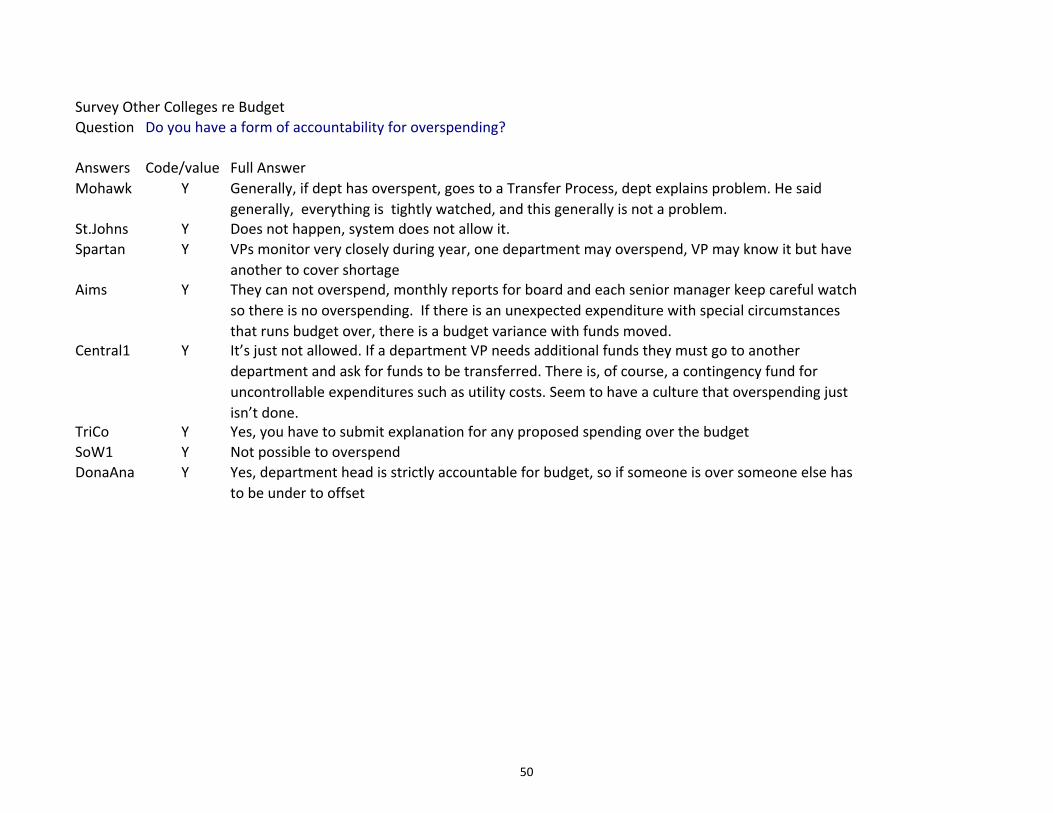

Do you have a form of accountability for overspending?

Are you considering changing your current process?

If so, what is causing the desire to change?

Do you have a visual diagram or written description of your process that you would be willing to send us?

If other colleges participating in this survey want to get the results, do we have your permission to share with them?

If this college wants the results, get the necessary information.

Figure 14 41

DonaAna No

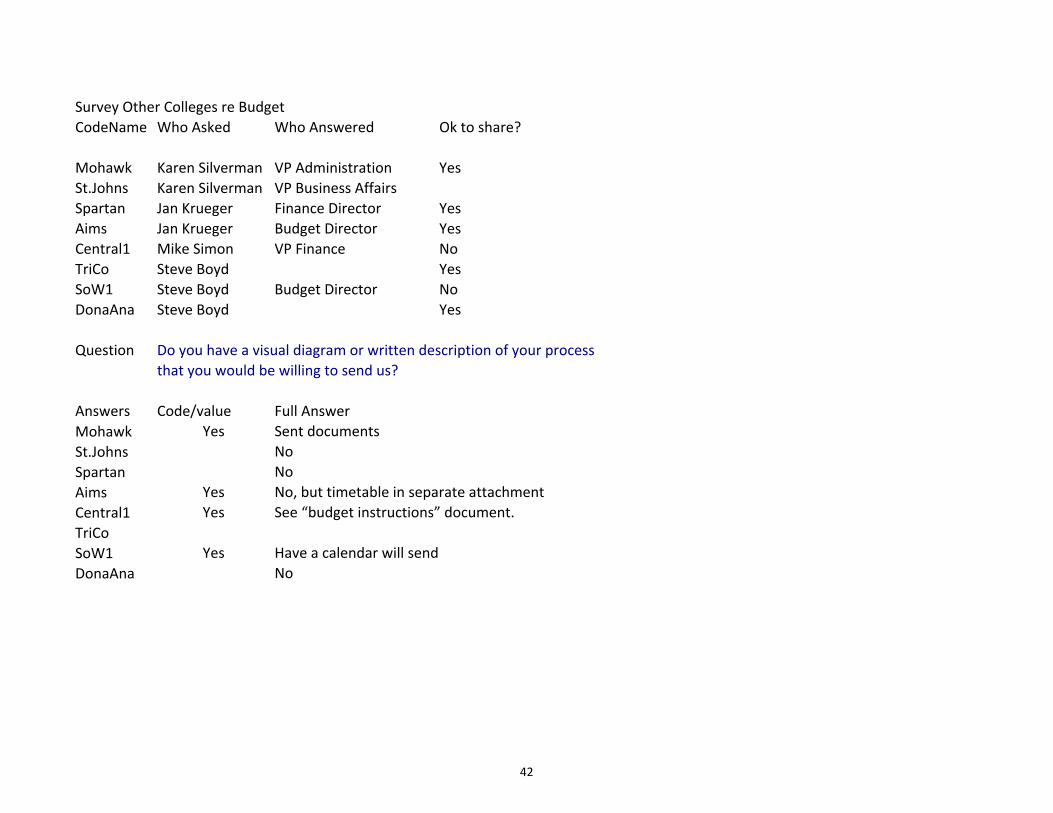

Survey Other Colleges re BudgetCodeName Who Asked Who Answered Ok to share?

Mohawk Karen Silverman VP Administration YesSt.Johns Karen Silverman VP Business AffairsSpartan Jan Krueger Finance Director YesAims Jan Krueger Budget Director YesCentral1 Mike Simon VP Finance NoTriCo Steve Boyd YesSoW1 Steve Boyd Budget Director NoDonaAna Steve Boyd Yes

Question Do you have a visual diagram or written description of your process that you would be willing to send us?

Answers Code/value Full AnswerMohawk Yes Sent documentsSt.Johns NoSpartan No

Yes No, but timetable in separate attachment AimsCentral1 Yes See “budget instructions” document.TriCoSoW1 Yes Have a calendar will send

42

Survey Other Colleges re BudgetQuestion Can you describe the type of budget process you use? (examples: Zero Based or Incremental )

Answers Code/valu Full AnswerMohawk I Incremental within limitsSt.Johns Z Mix, but Is changing. They were given the budget, now have to justify. (the woman I spoke with when I first

called, said it was mostly zero based, but becoming a mix)Spartan Z Zero based, hold prior year’s allocation harmless, add or delete new expenses or cost savings, identified through

planning process, departments determine needs or savings, VP may cut if discontinuance. There are series of meetings, if cost savings identified, savings go into general pot for reallocation, ties to planning, gives opportunity to identify needs

Aims I IncrementalCentral1 Z Basically a zero based budget process, however don’t detail every expenditure. Start from scratch each year.

Commented that their budget process is pretty straight forward because there is not a lot of wiggle room for how to spend money. Bare bones budget.

TriCo Z Each dept starts with zero and makes new budget. Budget manager usually starts with budget number from last d difiyear and modifies as necessary

SoW1 I IncrementalDonaAna I Start from last year’s budget, then submit each department gathers requests for increases and decreases, sends

them to budget committee for approval

Question Does the process completely restart each year or is there a modification from the prior year factored in?

Answers Code/valu Full AnswerMohawk R Yes, When the actuals do come in, will review and re‐evaluate (But he had said their process was incremental

within limits).St.Johns R Begins with requests from all depts.,.and looks at prior numbers.Spartan R Base for revenue, add or subtract, nothing automatic, fixed cost bases, each must identify needs Aims R YesCentral1 R Restarts each year.TriCo R RestartSoW1 M ModificationDonaAna R Restart

43

Survey Other Colleges re BudgetQuestion Does it work well? Rank 1‐4, 1 is best, 4 doesn’t work.

AnswersMohawk

Code/value Full AnswerMissed Question

St.JohnsSpartanAims

212

12

It does, process is different during this year because of pressures of the economy.

Departments ask for the money but then don’t use it, still unspent at end of yearCentral1TriCo

23

23

Room for improvement. Would like to be more automated and paperless.

SoW1DonaAna

23

23

Average 2.14286 How Well Does Your Process Work?

0

1

2

3

4

St.Johns Spartan Aims Central1 TriCo SoW1 DonaAnaLow is Best

How Well Does Your Process Work?

44

yet.y

Survey Other Colleges re BudgetQuestion Is your budget tied to your Strategic Plan?

How do you assure that?AnswersMohawk

Code/vY

alue Full AnswerYes Send documents to Dept. heads, with current strategic plan(09/10) and a word document asking them

which goals they are striving for. Asks if they are changing, adding new positions, etc.

St.Johns Y Yes tie back decisions to budget line items. Both strategic plan and budget in computer, and they are creating a software that will allow the 2 areas to talk to each other. Not on line with it yet.

Spartan Y Yes One day a year set aside to plan objectives and strategies, costs identified, sub‐group prioritizes, rolls into process

Aims Y Yes Board sets goals, senior management determines percentage of staff going toward board set goals. They make sure to fund strategic plan goals. Dan has only been there 10 months, he does not know

Central1 Y Yes They have college strategic goals and objectives and Unit Plan Initiatives . Units are departments.Funding from departments for Unit Plan Initiatives must be supported with Unit Plan documentation on a form called “Special Project Funding Request” when submitting their budgets to the finance dept. Institutional effectiveness handles any follow‐up assessment of this.

TriCo N Not reallySoW1 Y Yes Committee meetingsDonaAna Y Yes Only have budget categories that are consistent with the college goals

45

u

DonaAna Y Yes

Question

u

DonaAna S Budget committee is about 7 people

Survey Other Colleges re BudgetQuestion Is your decision making a collaborative process?

Answers Code/val Full AnswerMohawk Y Yes, make assumptions what state will do, try to get a feel for their revenue projections. (he noted State is never

on time with their budget process). Depts. submit their requests to President, VP Marketing, HR to review then may go back to depts., depending on whether they have or have not $.Then goes to Board of Trustees, then County Sponsor for review before going toState. As long as it is balance, State usually accepts it.

St.JohnsSpartan

NY

No, has not been. But they have new president, so may be different. They have one administrative structure.Yes

Aims Y Yes, but president has last word. There is lots of discussion by groups in process. Central1 Y YesTriCo Y YesSoW1 Y Yes

Is the decision making group large or small? (Size)

Answers Code/val Full AnswerMohawk SSt.Johns S

Small, about 7 in final.Small

Spartan M Series of groups and subgroups, making decisions along the way, varying sizesAims M Many groups of all sizes in process, action committees, senior managements, many others at three campuses

compiling info for budget process Central1 S The final decisions are made by a small group of five people at a “president’s cabinet level.” Group works closely

with all VPs.TriCo S Lots of small groups approve along the waySoW1 M About 12

46

e

DonaAna Yes Yes

e

DonaAna

Survey Other Colleges re BudgetQuestion Does the decision making group include leadership from all campuses?

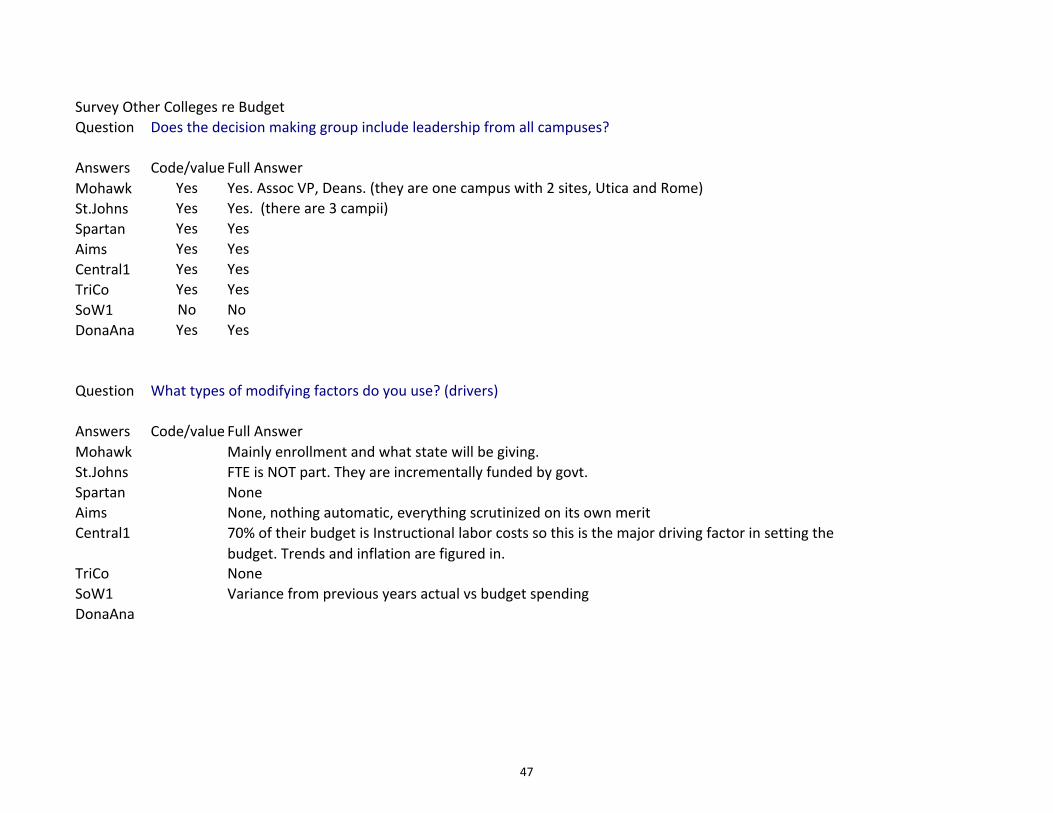

Answers Code/valu Full AnswerMohawk Yes Yes. Assoc VP, Deans. (they are one campus with 2 sites, Utica and Rome)St.Johns Yes Yes. (there are 3 campii)Spartan Yes YesAims Yes YesCentral1 Yes YesTriCo Yes YesSoW1 No No

Question What types of modifying factors do you use? (drivers)

Answers Code/valu Full AnswerMohawk Mainly enrollment and what state will be giving.St.Johns FTE is NOT part. They are incrementally funded by govt.Spartan None AimsCentral1

None, nothing automatic, everything scrutinized on its own merit 70% of their budget is Instructional labor costs so this is the major driving factor in setting the budget. Trends and inflation are figured in.

TriCo NoneSoW1 Variance from previous years actual vs budget spending

47

Answers Code/value Full Answer

Survey Other Colleges re BudgetQuestion Can you carry over any unspent funds or is funding strictly “use it or loose it”?

Mohawk No They cannot use what they did not spend for next year. They can use only if monies were already

St.JohnsSpartan

YesNo

encumbered.can carry forward , No

Aims No No, goes into construction fund for capital projects. Oil and gas revenues also set aside for capital projects

Central1TriCo

NoNo

No. Lose it.No carryover

SoW1DonaAna

Question

NoNo

If you have

Use it or Lose itCarry over only on projects that are in process

any carry over, how do you allocate those funds

AnswersMohawk

St.Johns

or are theyCode/value

held in reserve for future needs?Full Answer If there were revenues that were over, they go into a fund balance. May call upon them, especially if they know state funding may decrease.have option of moving $ to plant facility, etc. , depends.They can be held for future needs.

SpartanAims