apresentação do powerpointir.marfrig.com.br/en/documentos/3776_results... · achievement of...

TRANSCRIPT

2Q15 Earnings

August 12, 2015

Strategic Vision

GREATER VALUE TO

SHAREHOLDERS

FULL SUPPORT OF CONTROLLING SHAREHOLDERS

STAGE

EXAMPLES

VALUE LEVERAGE

FOCUS TO WINProfitable growth and global leadership in foodservice

Adjusting the capital structure and reducing borrowing costs

Continuous operational improvement and increased operating cash flow

• Productivity Agenda

• Streamlining of Beef Brazil production units

• Improved sales • mix Brazil

• Pursuit of synergies

• Sale ofMoy Park

• Liability Management

Prioritizing organic growth opportunities

- Keystone- Beef

1

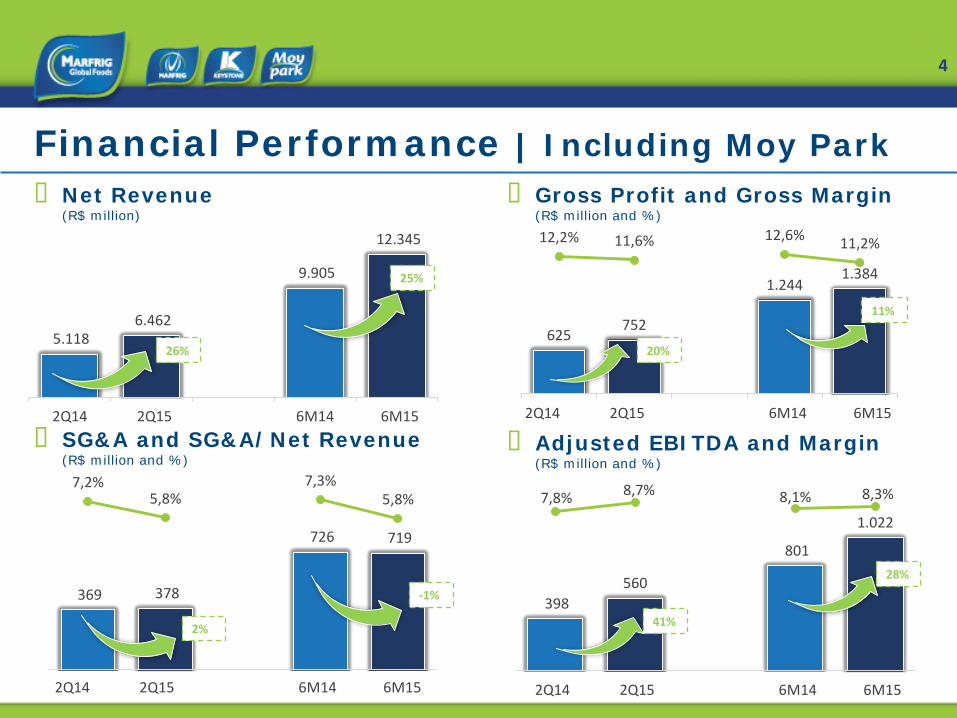

Highlights in 2Q15� Strong growth in net revenue (+26%) and Adjusted EBITDA (+41%) on

2Q14¹;

� EBITDA Margin expansion at all business units, with combined1 Adjusted EBITDA of 8.7%;

� Positive free cash flow of R$136 million in the quarter and R$48 million year to date;

� Keystone’s adjusted EBITDA grew 20% in USD, driven by robust growth in Asia and continuous growth in Key Accounts;

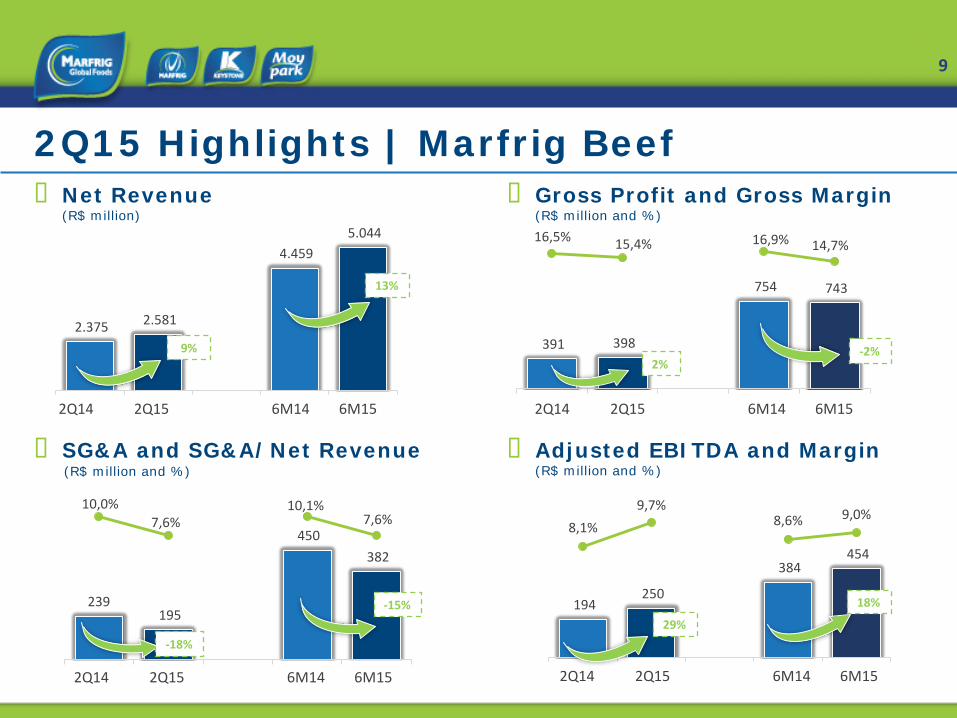

� Marfrig Beef’s Adjusted EBITDA margin stood at 9.7%, due to a better sales mix and higher operating efficiency;

� Opening-up of the US and Chinese markets to Brazilian beef;

� Sale of Moy Park for approximately US$1.5 billion;

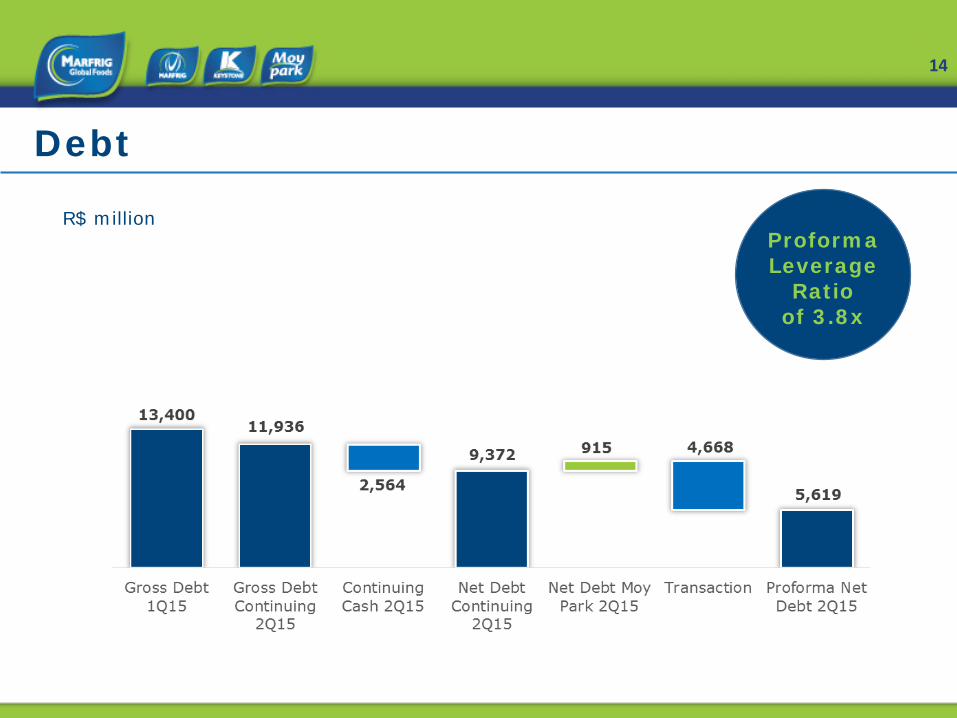

� On a proforma basis (considering the Moy Park divestment), financial leverage ended 2Q15 at 3.8x.

1 Includes Moy Park for comparison purposes, not audited.

2

Achievement of Guidance

Note: (1) In BRL based on the exchange rates of R$2.70/US$1.00 and R$4.30/£1.00.(2) Adjusted by non-recurring events.(3) Operating cash flow after investments, variations in working capital, interest expenses and income tax.

Target Range2015 (1)

6M15Achieved

Net Revenue R$23 to25billion

R$12.3billion

AdjustedEBITDA Margin (2) 8.0% - 9.0% 8.3%

CAPEX R$650million

R$339million

Free Cash Flow toShareholders (3)

R$100 to R$200 million

R$48million

3

398 560

801

1.0227,8% 8,7% 8,1% 8,3%

2T14 2T15 1S14 1S152Q14 2Q15 6M14 6M15

625752

1.2441.384

12,2% 11,6% 12,6% 11,2%

2T14 2T15 1S14 1S152Q14 2Q15 6M14 6M15

369 378

726 719

7,2%5,8%

7,3%5,8%

2T14 2T15 1S14 1S152Q14 2Q15 6M14 6M15

5.118 6.462

9.905

12.345

2T14 2T15 1S14 1S152Q14 2Q15 6M14 6M15

Financial Performance | Including Moy Park� Net Revenue

(R$ million)

� SG&A and SG&A/Net Revenue(R$ million and %)

� Gross Profit and Gross Margin(R$ million and %)

� Adjusted EBITDA and Margin(R$ million and %)

26%

25%

11%

28%

41%

20%

2%

-1%

4

294 415

595 759

7,8%8,8%

8,2% 8,3%

2T14 2T15 1S14 1S15

3.789 4.728

7.265

9.099

2T14 2T15 1S14 1S15

Financial Performance | Continuing Operations� Net Revenue

(R$ million)

� Adjusted EBITDA and Margin(R$ million and %)

25%

25%

41%

27%

� Profile of Continuing Ops.

� Revenue Breakdown

Approximately 33,000 employees

46 commercial, production and distribution units

Operational presence

in 11 countries in the Americas, Asia and Oceania

Serving clients with our products in approx.

100 countries

45%

42%

13%

Business

KeystoneBeef BrasilBeef Intr. Ops.

63%

22%

15%

CurrencyUSD

BRL

Other

2Q14 2Q15 6M14 6M15

2Q14 2Q15 6M14 6M15

51%

41%

8%

ProductOther

Fresh

Processed

5

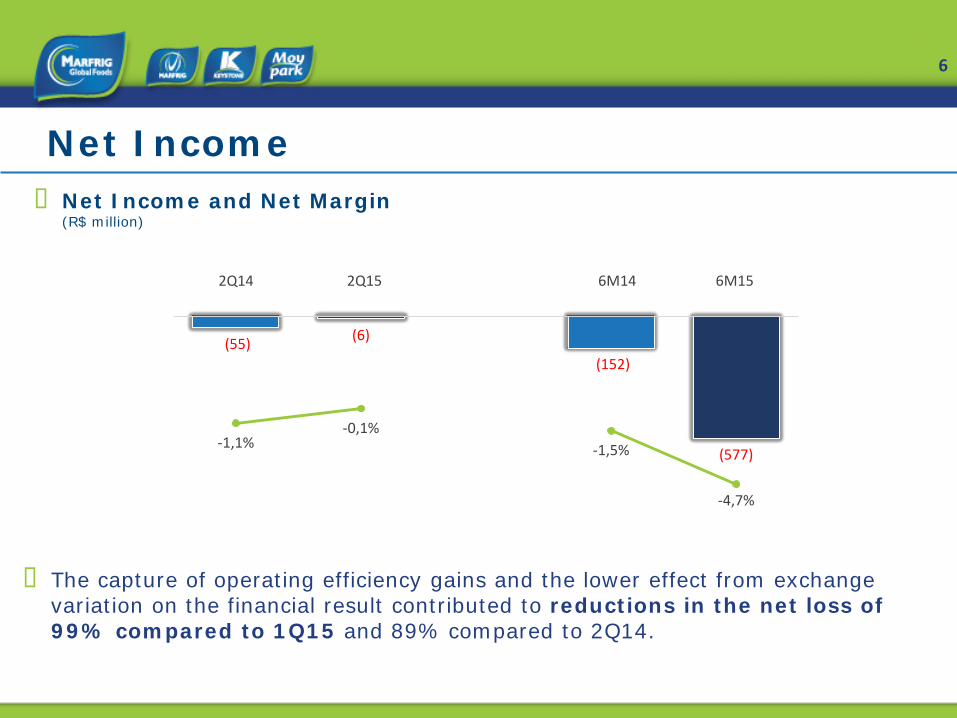

Net Income� Net Income and Net Margin

(R$ million)

� The capture of operating efficiency gains and the lower effect from exchange variation on the financial result contributed to reductions in the net loss of 99% compared to 1Q15 and 89% compared to 2Q14.

(55) (6)

(152)

(577)-1,1%

-0,1%-1,5%

-4,7%

2T14 2T15 1S14 1S152Q14 2Q15 6M14 6M15

6

36 53

83 99 5,7%

7,6%6,8% 7,3%

2T14 2T15 1S14 1S152Q14 2Q15 6M14 6M15

45 54

92 102

7,1%7,7% 7,5% 7,5%

2T14 2T15 1S14 1S152Q14 2Q15 6M14 6M15

8

17

26 32

1,3%2,4% 2,1% 2,4%

2T14 2T15 1S14 1S152Q14 2Q15 6M14 6M15

634 698

1.223 1.359

2T14 2T15 1S14 1S152Q14 2Q15 6M14 6M15

2Q15 Highlights | Keystone� Net Revenue

(USD million)

� SG&A and SG&A/Net Revenue(USD million and %)

� Gross Profit and Gross Margin(USD million and %)

� Adjusted EBITDA and Margin(USD million and %)

10%

11%

47%

18%

20%

11%

109%

25%

7

2T14 2T152Q14 2Q15

211 226

3747

2T14 2T152Q14 2Q15

471 500

163198

2T14 2T15

EUA APMEA

2Q14 2Q15

Operating Performance | Keystone

� Total Volume (‘000 ton)

� Net Revenue(USD million)

25% 22%

7% 6%

� Net Revenue Key Accounts (1)

(USD million)

19%

(1) Processed, value-added products

137

163

10%

634698

10%

248272

USA

8

194 250

384 454

8,1%9,7%

8,6% 9,0%

2T14 2T15 1S14 1S15

239195

450 382

10,0%7,6%

10,1%7,6%

2T14 2T15 1S14 1S15

391 398

754 743

16,5% 15,4% 16,9% 14,7%

2T14 2T15 1S14 1S15

2Q15 Highlights | Marfrig Beef� Net Revenue

(R$ million)

� SG&A and SG&A/Net Revenue(R$ million and %)

� Gross Profit and Gross Margin(R$ million and %)

� Adjusted EBITDA and Margin(R$ million and %)

29%

18%

-2%2%

-15%

-18%

2.375 2.581

4.459 5.044

2T14 2T15 1S14 1S15

9%

13%

2Q14 2Q15 6M14 6M15

2Q14 2Q15 6M14 6M15

2Q14 2Q15 6M14 6M15

2Q14 2Q15 6M14 6M15

9

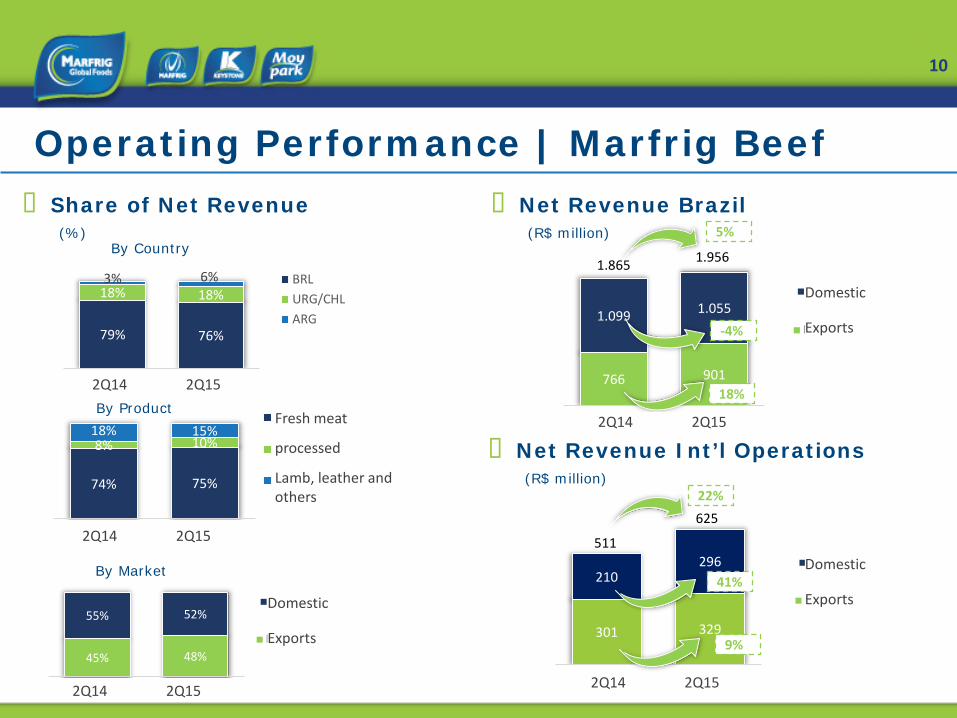

Operating Performance | Marfrig Beef� Share of Net Revenue

(%)By Country

By Product

By Market

79% 76%

18% 18%3% 6%

2T14 2T15

BRLURG/CHLARG

74% 75%

8% 10%18% 15%

2T14 2T15

Carne in natura

Processados

Ovinos, Couro,Outros

45% 48%

55% 52%

2T14 2T15

Exportação

MercadoInterno

� Net Revenue Brazil (R$ million)

� Net Revenue Int’l Operations(R$ million)

766 901

1.099 1.055

2T14 2T15

Exportação

MercadoInterno

301 329

210296

2T14 2T15

Exportação

MercadoInterno

1.865 1.956

625

511

-4%

18%

5%

41%

9%

22%

2Q14 2Q15

2Q14 2Q15

2Q14 2Q15

2Q14 2Q15

2Q14 2Q15

Fresh meat

processed

Lamb, leather and others

Domestic

Exports

Domestic

Exports

Domestic

Exports

10

Operating Performance | Marfrig Beef� Slaughter Volume

(‘000 head)

Total Brazil

� Capacity Utilization(% of authorized capacity in operation)

� Temporary closure of 5 of the 15 slaughtering plants, or approximately 29% of the total authorized capacity in operation.

� The objective is to achieve capacity utilization of 90-95%.

� Conclusion of the restructuring of production units.

1.562 1.555

1S14 1S15

1.220 1.206

1S14 1S15

-0.5% -1.1%

66,9%

82,9%

1T15 2T15

65,0%

74,9%

1S14 1S15

6M14 6M15 6M14 6M15

6M14 6M151Q15 2Q15

11

353 373

2T14 2T15

Domestic Market | Beef Brasil� Food Service share in Total

Domestic Revenue(R$ million)

1.098 1.055

6%

Others

Food Service

� Fresh and Processed Meat� Net Revenue

(R$ million)

� Volume('000 ton)

� Average Price(R$/Kg)

79 70 70

2T14 1T15 2T15

-11%

861852

873

2T14 1T15 2T15

10,9512,14 12,50

2T14 1T15 2T15

14%

1%

2Q14 2Q15

2Q14 1Q15 2Q15

2Q14 1Q15 2Q15

2Q14 1Q15 2Q15

12

343

261293

2T14 1T15 2T15

7365

78

2T14 1T15 2T15

Exports | Beef Brasil� Market Share Fresh Meat

(% Volume (1))

� Export Volume('000 ton)

� Share of Exports(% Beef Brasil Revenue )

� Export Revenue(USD million)

7%

-14%

41% 41%

46%

2T14 1T15 2T15

19.0%19.9%

20.6%19.8%

21.6%

14,0%15,0%16,0%17,0%18,0%19,0%20,0%21,0%22,0%

0

200

400

600

800

2T14 3T14 4T14 1T15 2T15

(1) Secex

2Q14 1Q15 2Q15

2Q14 1Q15 2Q152Q14 1Q15 2Q15

2Q14 3Q14 4Q14 1Q15 2Q15

13

Debt

R$ millionProforma Leverage

Ratio of 3.8x

14

2,564

450 1,066

246 196 677 757

3,0142,392

2,993

145

6,317

Cash 3Q15 4Q15 1Q16 2Q16 2016 2017 2018 2019 2020 2021

Short Term R$ 2.0 bn

Debt Maturity Schedule excl. Moy Park

R$ million

(1) Cash to be received from the sale of Moy Park.

3,753(1)

15

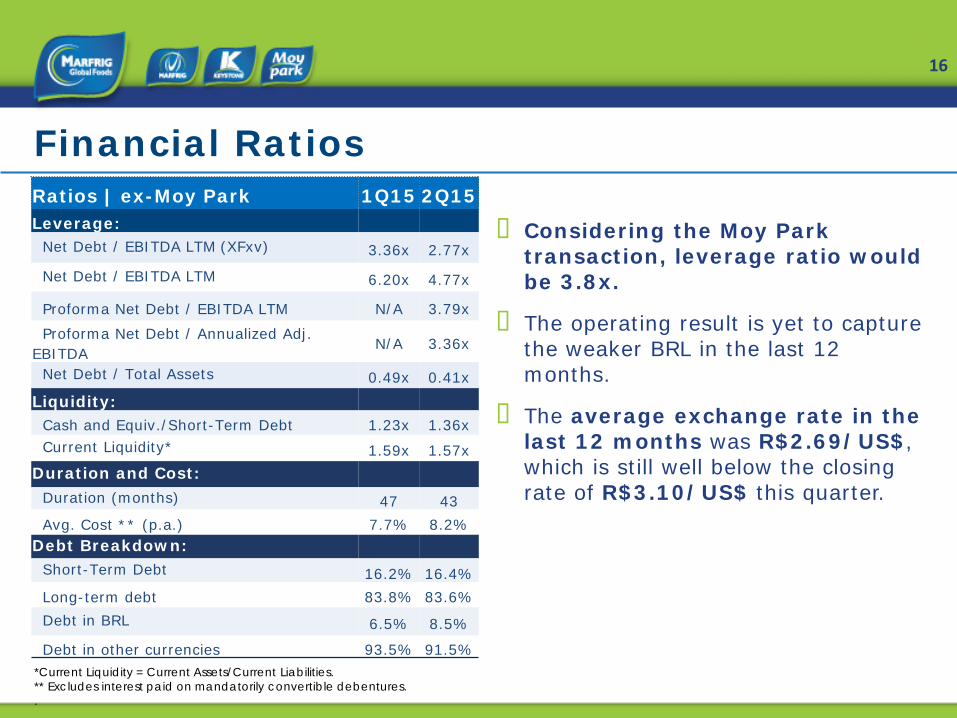

� Considering the Moy Park transaction, leverage ratio would be 3.8x.

� The operating result is yet to capture the weaker BRL in the last 12 months.

� The average exchange rate in the last 12 months was R$2.69/US$, which is still well below the closing rate of R$3.10/US$ this quarter.

*Current Liquidity = Current Assets/Current Liabilities.** Excludes interest paid on mandatorily convertible debentures..

Financial RatiosRatios | ex-Moy Park 1Q15 2Q15Leverage:

Net Debt / EBITDA LTM (XFxv) 3.36x 2.77x

Net Debt / EBITDA LTM 6.20x 4.77x

Proforma Net Debt / EBITDA LTM N/A 3.79xProforma Net Debt / Annualized Adj.

EBITDAN/A 3.36x

Net Debt / Total Assets 0.49x 0.41xLiquidity:

Cash and Equiv./Short-Term Debt 1.23x 1.36xCurrent Liquidity* 1.59x 1.57x

Duration and Cost:Duration (months) 47 43Avg. Cost ** (p.a.) 7.7% 8.2%

Debt Breakdown:Short-Term Debt 16.2% 16.4%Long-term debt 83.8% 83.6%Debt in BRL 6.5% 8.5%

Debt in other currencies 93.5% 91.5%

16

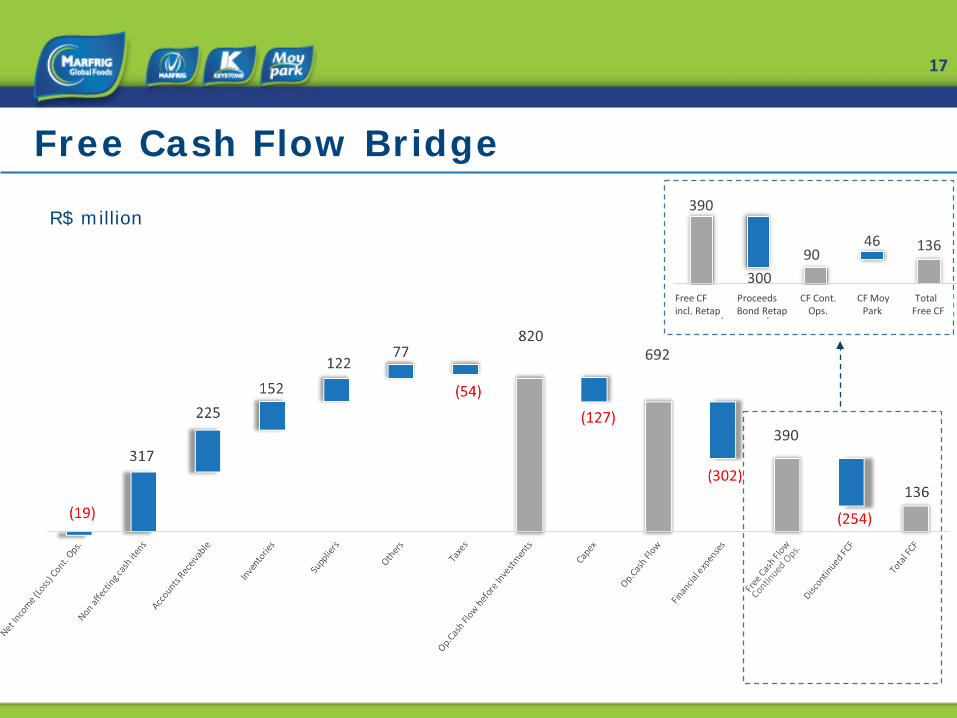

390

30090

46 136

FC LivreIncl. Retap

RecursosRetap

FC Op.Cont.

FC MoyPark

FC LivreTotal

Free Cash Flow Bridge

R$ million

Free CF Proceeds CF Cont. CF Moy Total incl. Retap Bond Retap Ops. Park Free CF

17

Closing Remarks

� We generated strong free cash flow, transformed Marfrig Beef Brazil andsigned an agreement to sell Moy Park.

� The strategic decision to divest Moy Park leaves Marfrig with a stronger focuson the foodservice channel, which offers excellent opportunities for growth inthe key markets of Asia and the United States.

� This transaction significantly reduces Marfrig’s net debt, which ended thequarter with a ratio of Pro-Forma Net Debt to EBITDA from ContinuingOperations of 3.8x in 2Q15.

� Cash generation in the quarter confirms our determination and financialdiscipline, and was the result of our pursuit of increased operating efficiencyand better working capital management.

18

Closing Remarks

� Marfrig Beef posted margin of 9.7%, driven by greater efficiency, improvedsales mix and continuous improvement in the management of costs andexpenses. The second-quarter results only partially reflect these changes,since many are still in the implementation phase.

� The opening up of the U.S. and Chinese markets to Brazilian beef importsshould generate volume growth in the medium term. We have already begunshipments to China and hope to make our first shipments to the United Statesbefore year-end.

� Marfrig Beef’s international operations continue to make a positive contributionto the division's results.

19

Closing Remarks

� Keystone continues to contribute to free cash flow, posting accelerated growthand benefitting from its impeccable reputation for customer service andexecution excellence in its industrial operations.

� Strategically, Marfrig's priorities are:

� expanding Keystone's food service business in both Asia and the United States;

� optimizing production capacity at Marfrig Beef;

� growing beef exports from Brazil; and

� strengthening the capital structure and increasing free cash flow.

20

This material is a presentation of general information about Marfrig GlobalFoods S.A. and its consolidated subsidiaries (jointly the “Corporation”) on thedate hereof. The information is presented in summary form and does notpurport to be complete.

No representation or warranty, either expressed or implied, is made regardingthe accuracy or scope of the information herein. Neither the Company nor anyof its affiliated companies, consultants or representatives undertake anyresponsibility for any losses or damages arising from any of the informationpresented or contained in this presentation. The information contained in thispresentation is up to date as of June 30, 2015, and, unless stated otherwise, issubject to change without prior notice. Neither the Corporation nor any of itsaffiliated companies, consultants or representatives have signed anycommitment to update such information after the date hereof. Thispresentation should not be construed as a legal, tax or investmentrecommendation or any other type of advice.

The data contained herein were obtained from various external sources andthe Corporation has not verified said data through any independent source.Therefore, the Corporation makes no warranties as to the accuracy orcompleteness of such data, which involve risks and uncertainties and aresubject to change based on various factors.

This presentation includes forward-looking statements. Such statements donot constitute historical fact and reflect the beliefs and expectations of theCorporation’s management. The words “anticipates,” “hopes,” “expects,”“estimates,” “intends,” “projects,” “plans,” “predicts,” “projects,” “aims” andother similar expressions are used to identify such statements.

Although the Corporation believes that the expectations and assumptionsreflected by these forward-looking statements are reasonable and based onthe information currently available to its management, it cannot guaranteeresults or future events. Such forward-looking statements should beconsidered with caution, since actual results may differ materially from thoseexpressed or implied by such statements. Securities are prohibited from beingoffered or sold in the United States unless they are registered or exempt fromregistration in accordance with the U.S. Securities Act of 1933, as amended(“Securities Act”). Any future offering of securities must be made exclusivelythrough an offering memorandum. This presentation does not constitute anoffer, invitation or solicitation to subscribe or acquire any securities, and nopart of this presentation nor any information or statement contained hereinshould be used as the basis for or considered in connection with any contractor commitment of any nature. Any decision to buy securities in any offeringconducted by the Corporation should be based solely on the informationcontained in the offering documents, which may be published or distributedopportunely in connection with any security offering conducted by theCompany, depending on the case.

Disclaimer

IR Contacts

Website

www.marfrig.com.br/ri

Address

Avenida Chedid Jafet, 222 Bloco A 5º andar -São Paulo - SP SP: +55 (11) 3792-8650

Telephone

@