applied value steel quarterly report q4 2016 · applied value steel quarterly report – q4 2016 q4...

TRANSCRIPT

Applied Value Steel

Quarterly Report –

Q4 2016

Q4 2016

Applied Value Empire State Building 350 Fifth Avenue, Suite 5400 New York, NY 10118 Phone: +1 646 336 4971 Fax: +1 646 733 9191 www.appliedvaluegroup.com

1 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Strategy, Finance & Organization

Operations Management

Sourcing & Procurement Management

Research, Development & Engineering Management

Marketing & Sales Management

IT Efficiency Management

Questions or Comments – Please Contact

North America: Ryan Huff | [email protected] | +1 914 907 0781

Asia: Jason Yang | [email protected] | +86 138 1864 9865

Europe: Anders Dahlberg | [email protected] | +46 704 269 262

The Steel Report is published quarterly for the benefit of our clients

in steel consuming industries.

Applied Value is a professional services firm which offers expertise

in six key practice areas.

2 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Automotive OEM

White Goods OEM

Automotive OEM

Global Engineering

Global Construction

Industrial Products

4 Food Producers

Heavy Truck OEM

Defense/Heavy Truck

Security Solutions

Heavy Truck OEM

Heavy Truck OEM

Truck Tier 1

Lifting OEM

Intntl. Engineering

Intntl Consumer Goods OEM

European Engineering

Automotive OEM

Scand. Engineering

Scand. Construction

Applied Value has 10+ years of experience working with clients in

numerous industries involved in various facets of steel purchasing.

10 million tons

1 million tons

0.1 million tons

0.01 million tons

Control

of Data

Fact-based

Negotiations

Leverage

Creation

Manage Steel

Component Costs

Risk

Management

Macroeconomic

Factors on Global

Steel Trade

Game

Changers Client Annual

Consumption

3 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Our organization supports clients globally from 3 offices.

Countries where Applied

Value has performed case

work over the last ten years

Shanghai New York

Stockholm

New York

Empire State Building

350 Fifth Avenue

Suite 5400

New York, NY 10118

USA

Phone: +1 646 336 4971

Shanghai

Suite 1906, No. 819

West Nanjing Road

Shanghai 200041

China

Phone: +86 21 5213 6390

Stockholm

Linnégatan 18, Floor 8

PO Box 5047

SE-102 41 Stockholm

Sweden

Phone: +46 8 562 787 00

4 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Market Conditions by Region

Stock Price Development of Major Steel Companies

Steel Production Costs

US Market Fundamentals Deep-Dive

5 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

The US steel market weakened throughout Q3, while EU prices

stayed relatively flat, and CN prices showed some recovery.

Executive Summary

• North America Summary:

– After peaking in June from a supply driven rally, US Flat prices teetered and have turned downwards as the market corrects itself

– US flat prices are expected to be constrained through Q4 due to weakened demand, low utilization, and threats of potential circumvention of imports

• Europe Summary:

– EU Flat prices were relatively stable in Q3 in a period of seasonally slow buying activity, countered by domestic supply disruptions

– EU steel prices are expected to remain firm through Q4 on tight supply, lower import threats and rising raw material costs

• China Summary:

– Chinese HR steel prices recovered in Q3 on rising input costs and fear of further anti-dumping actions

– Chinese steel prices are likely to decline in the near term as mills fail to hit established production-cut targets and demand remains weak

• Raw Materials Summary

– While Scrap and Iron Ore prices face downward pressures, Met Coal prices remain strong on disrupted supply from China and Australia

This issue’s special section focuses on a deep dive of the US Steel Market Fundamentals

Market Conditions by Region

6 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016 Market Conditions by Region

Commodity Latest Price

(Sep)

Last 3

Months

Trend

(Forward) Major Individual Market Drivers

Flat

US $613/MT -12% ▲Anti-dumping; Idling; Coking Coal

▼Weak Demand; Circumvention of Imports; Economy

EU €432/MT -1% ▲Tight Supply; Lower Imports; Coking Coal; Auto Demand

▼Economic Uncertainty; Brexit; Scrap

CN $428/MT +12% ▲Coking Coal; Consolidation; Export Market;

▼Property Markets; Purchasing Strategies; Domestic Demand

SS

US $2,138/MT +5%

▲Raw Material Surcharges; Declining Supply; Demand

▼Oversupply; Economic Outlook EU $2,372/MT +8%

CN $1,955/MT +10%

Plate

US $617/MT -14%

▲Trade Cases

▼Lackluster Demand; High Inventories; Declining Coil Prices EU $534/MT -9%

CN $389/MT +8%

Bar

US $673/MT -1%

▲Improved Construction Demand

▼Scrap; High Inventories; Excess Supply EU $502/MT +10%

CN $356/MT +16%

Pipe/

Tube

US $948/MT +1% ▲Trade Cases; Rising EU Coil Prices

▼Weak Demand; Declining US Coil Prices EU $600/MT -5%

OCTG US $865/MT 0% ▲Rig Count; Anti-dumping

▼Weak Oil Prices

Global Steel Price & Trend Summary.

▲ Tightened Supply

▲ Coking Coal

▲ Anti-dumping

▼ Scrap

▼ Economic Uncertainty

▼ Brexit

▼ Weak Demand

Overall Market Drivers

7 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

85

95

105

115

Jun 16 Jul 16 Aug 16 Sep 1680

100

120

140

160

180

200

Jun 16 Jul 16 Aug 16 Sep 16

BDI 41.5%

CRB -6.1%

USD/EUR -0.2%

Indexed Input Costs Jul 2016 – Sep 2016

Scrap -9.2%

Iron Ore 13.3%

Indexed Flat Steel Prices Jul 2016 – Sep 2016

Coking Coal 80.2%

Global steel prices started to decrease in North America and Europe

while Asian prices have steadily rebounded.

Europe

-1.4%

Asia

10.9%

NA

-12.0%

Market Conditions by Region

Source: AMM, Capital Link Shipping, CRU, HSBC, Bloomberg, Oanda, SBB, AV

Analysis

8 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

71.9% 70.2%

60%

70%

80%

90%

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

0.0

1.0

2.0

3.0

250

500

750

1,000

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

mM

T I

mp

ort

ed

US

D/M

T

Flat Steel Imports US Price China Price

5,214

4,512

3,500

4,500

5,500

6,500

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

‘000 M

T

US Flats Steel Prices

After peaking in June from a supply driven rally, US Flat prices

teetered and have turned downwards as the market corrects itself.

US Service

Center

Inventory

US Mill

Capacity

Utilization

US vs. China

Price &

US Flat

Imports

US Scrap

Steel Price

(+)

(+)

(+)

Source: US Census Bureau, CRU

Source: AMM

Source: AISI, SBB

496

708

909

613

300

500

700

900

1100

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16 Mar 17

Hot Rolled Coated

US: 613

China: 428 Imports: 2.4

Previous Year’s Data

Latest Data

Source: CRU

US

D/M

T

Source: CRU, Applied Value analysis

Market Conditions by Region

• Mill utilization continued to slip in Q3, approaching the 70%, a

mark not seen since November 2015 when HR prices dipped to

historical lows below $400/MT

• Antidumping has effectively restricted import competition. Imports

are down by 19% Y-o-Y between Jan-July 2016 while the US-CN

price delta has averaged over $250/MT since May

• US HR and HDG prices turned around as market fundamentals

did not support the rally; prices have already dropped by 12% and

8%, respectively, since June, driven by seasonally quiet summer

activity, insufficient capacity idling and lower mill utilization

• US scrap prices

dropped another

15% Q-o-Q, due to

weak demand and

US mills cancelling

scrap orders in

response to falling

utilization

• After a ten-month

fall, US SSC

inventories began

to rise in July as

buyers sought

lower prices and

shorter lead times

231 231

100

200

300

400

500

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/G

T

9 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

• Upward drivers

– Antidumping: Trade cases have substantially limited import threats, particularly from China. Imports of Chinese CRC and HDG dwindled to only 140 kMT and 9 kMT in H1 2016, respectively, from over 300 kMT and 525 kMT in H1 2015

– Mill Outages: Current YTD planned outages at ArcelorMittal and AK Steel have helped to mildly improve domestic oversupply. However, AM’s Indiana Harbor is scheduled to come on line in Q4

– Coking Coal: Coking coal prices have shot up by 109% since the beginning of the year, as weather and infrastructure problems at certain mines and railways disrupted supply in China and Australia

• Downward drivers

– Weak Demand: Demand in the US Auto industry started to decline. Light weight vehicle sales decreased by 1% in Aug. and the downward trend is expected to persist through Q4; demand from Construction also started to cool off as US construction spending remained flat in July and housing starts missed expectations in August

– Supply-Driven Price Rally: Market demand indicators did not support the H1 price rally. Thus, the market has begun to correct itself and mill utilization has been continuously decreasing since June in spite of mill outages

– Circumvention Imports: The major US mills have requested that the US DOC investigate China over allegations of circumventing import duties on CRC and HDG products by processing HRC in Vietnam. CRC imports from Vietnam skyrocketed to over 150 kMT in H1 2016, up from 8 kMT in H1 2015; however, the anti-circumvention investigation process will be complex and time consuming, and could extend to other countries, such as Taiwan

– Disappointing Economy: US Q2 GDP growth was 1.1%, well below previous estimates in the range of 2~3%. Meanwhile, Manufacturing PMI slipped to 51.4 in September despite expectations it would hit 52.0; private fixed investment, including residential and business spending, dropped to 3.2% in Q2, the lowest rate in seven years. The disappointing economic performance also delayed the Fed’s decision to raise interest rates in September

– Big River Steel: Arkansas-based Big River Steel opened in September, with an estimated annual production capacity of 1.5 mMT at utilization of around 60%~70%

– Scrap: Scrap prices are expected to remain pressured, as weak demand for steel is keeping steelmakers’ demand for scrap low. Several mills have started to cancel outstanding scrap orders

US flat prices are expected to be constrained through Q4 as the

market continues to correct itself.

Market Conditions by Region

10 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

200 190

100

150

200

250

300

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

EU

R/M

T

0.0

0.5

1.0

1.5

2.0

2.5

250

350

450

550

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

mM

T Im

po

rte

d

EU

R/M

T

Flat Steel Imports EU Price China Price

EU Flat prices were relatively stable in Q3 in a period of seasonally

slow buying activity, countered by domestic supply disruptions.

German

Sheet

Inventory

W. Europe

HR Steel

Production /

Consumption

EU vs. China

Price & EU

Flat Imports

European

Scrap

Prices

(-)

(-)

(+)

Source: CRU, Applied Value analysis China: 379

EU: 432 Imports: 1.7

Source: SBB

Source: CRU

Source: CRU, Eurofer

Market Conditions by Region

Previous Year’s Data

Latest Data

Source: World Steel

1,273 1,323

1,000

1,200

1,400

1,600

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

‘000 M

T

383

510

432

572

200

300

400

500

600

700

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16 Mar 17

Hot Rolled Coated

European Flats Prices E

UR

/MT

as buyers stocked up while expecting tight supply in the short term

• EU Flat imports rebounded to 1.7mMT in July despite trade action

taken against China in May. However, the spread between EU and

Chinese prices has shrunk by ~46% to 53 EUR/MT since June,

further diminishing import threats and supporting domestic prices

continues to

correct itself

• European scrap

fell 10% further in

Q3, following a

spike in May due

to a temporary

supply shortage.

Prices have since

stabilized at ~190

EUR/MT

• German sheet

inventories peaked

in July at a 2-year

high of 1.4 mMT,

• EU HR prices fell just 1% in Q3, relative to the 12% decline in

US prices. The EU market was more disciplined during the rally

as HR prices only rose 30% (vs. 56% in the US) during Q2. EU

prices have leveled off at ~430 EUR/MT whereas the US market

0.96 0.93

0.88

0.92

0.96

1.00

1.04

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

11 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

• Upward drivers

– Tight Supply: Material shortages, due to disrupted supply and reported diminishing imports in August/September, have pushed mill lead times far out into late December / early January, especially for CR and Coated steel

– Lower Imports: The impact from trade actions against China is being reported in the market as a shrinking price spread between EU and China. This has allowed domestic producers to gain some of the market share lost to imports

– Coking Coal: Coking coal prices sky-rocketed by 109% since the beginning of the year. 80% of that growth took place in Q3 and is linked to a 60-day reduction in statutory working days at Shanxi mines in China, as well as a series of global supply disruptions owed to weather and infrastructure problems in China and Australia

– Manufacturing Growth: The Eurozone Manufacturing Index (PMI) rose to 52.6 in September, beating market expectations and signaling an increased pace of manufacturing production. According to the European Automobiles Manufacturers Association (ACEA), August demand for new light commercial vehicles is up 35.8% Y-o-Y, driven mainly by Italian, Spanish and German markets

– Consolidation: A potential merger between steel mills ThyssenKrupp and Salzgitter announced in August would create the second largest steel producer in Europe, with combined annual production capacity of ~ 17mMT. The resulting consolidation would enable better control over production and overcapacity. On the other hand, talks for merging Tata Steel’s EU operations with TK have slowed down as Tata and trade unions try to solve a £15B pension funding deficit

• Downward drivers

– Economic Growth: The EU GDP growth rate of 0.3% in Q2 of 2016 is down Y-o-Y from 0.4% in Q2 of 2015

– Brexit: Continues to be viewed as a deterrent for investments, due to the uncertainty that still surrounds both the political and trade environments

– Raw Materials: Despite net positive price movements since the beginning of 2016, EU scrap prices have fallen 27% since May, eroding most of the price gains observed up until then. Iron Ore prices, in spite of climbing by 29% in Q3, remain at historically low levels

Market Conditions by Region

EU steel prices are expected to remain firm through Q4 on tight

supply and lower import threats.

12 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

202 234

100

200

300

400

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

Chinese

Scrap

Prices

Chinese Steel

Production /

Consumption

(-)

(+)

Chinese

Imports /

Exports

Source: China Customs Statistics.

Chinese Flats Steel Prices

Source: CRU, Applied Value analysis.

Chinese HR steel prices recovered in Q3 on rising input costs and

fear of further anti-dumping actions.

Source: SBB, China Scrap.

Source: World Steel

US

D/M

T

Previous Year’s Data

Latest Data

328

463 428

599

200

300

400

500

600

700

800

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16 Mar 17

US

D/M

T

Hot Rolled Coated

• Chinese HR prices rose 12% in Q3 on rising input costs and

planned mill outages. HDG prices fell 5% in July due to abundant

inventories after trade actions, but have since recovered by 4% on

stronger exports to Southeast Asia

Market Conditions by Region

1.02 1.11

9.73 9.01

0.0

2.5

5.0

7.5

10.0

12.5

Aug 14 Feb 15 Aug 15 Feb 16 Aug 16

MM

T

Import Volume Export Volume

• Despite the

absence of

anticipated stimulus

measures, Chinese

Q3 prices were

supported by an

18% rebound in

scrap prices

and an 80% spike

in coal prices

• Chinese HR prices

also benefitted

from a temporary

planned capacity

reduction of 21 mMT before the G20 summit

• Amid global antidumping, Chinese exports are up 7% Y-o-Y.

Much of the volume displaced by AD in the Americas is being

offset by an increase in export volume to other Asian countries

1.10 1.10

1.00

1.05

1.10

1.15

1.20

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

13 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Chinese steel prices are likely to decline in the near term as mills fail

to hit established production-cut targets and demand remains weak.

Market Conditions by Region

• Upward drivers

– Coking Coal: Coking coal prices sky-rocketed by 109% since the beginning of the year. 80% of that growth took

place in Q3 and is linked to a 60 day reduction in statutory working days at Shanxi mines in China, as well as a series

of global supply disruptions owed to weather and infrastructure problems in China and Australia

– Consolidation: Baosteel Group and Wuhan Iron & Steel Group announced the start of talks at the end of June. If the

state-controlled companies integrate their operations, they would become the world’s No. 2 steelmaker after

ArcelorMittal. The prospect of the merger is fuelling optimism about an end to the glut of steel supply

– Exports: Despite losing the ability to export to North America due to AD, China’s exports to other Asian countries

have increased by 17% y-o-y, more than offsetting the displaced volume. Mills have indicated that export prices could

increase in order to avoid further AD investigations, although US mills have requested that the US DoC investigate

China over allegations of circumventing import duties on CRC and HDG products by processing HRC in Vietnam

• Downward drivers

– Property Market: The People’s Bank of China has indicated that it is going to curb financing in the property sector,

as housing prices and the number of unsold residential properties continues to increase following stimulus actions.

These actions are likely to lead to reduction in construction activity

– New Purchasing Strategies: With prices beginning to trend downwards, many buyers are either adopting a just-in-

time approach to inventory, or plan to deplete current inventory levels in anticipation of lower prices on the horizon

– Weak Domestic Demand: Demand is set to decrease as government stimulus has recently waned. However, this

effect could be delayed in the near-term due to seasonality

– End of Idling: Many mills have taken advantage of the recent surge in steel prices to boost production and even to

revitalize unprofitable mills. Furthermore, the increasingly attractive margins have incentivized regional governments

to delay production-cut plans and keep workers employed

14 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

2.65 2.79

0

2

4

6

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/m

mB

tu

Stainless Steel Prices – US / Europe / China

2,161

2,414

1,900

2,138

2,372

1,955

1,500

2,000

2,500

3,000

3,500

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16 Mar 17

US

D/M

T

US CR 304 EU CR 304 China CR 304

9,898 10,026

6,000

10,000

14,000

18,000

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/M

T

2,370

1,938

1,800

2,000

2,200

2,400

2,600

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/M

T

54 55

0

50

100

150

200

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/M

T

Nickel

Chromium

Natural Gas

(+)

(+)

(+)

Source: SBB, Applied Value analysis

Iron Ore

(+)

Stainless prices increased globally during Q3 2016, largely driven

by rising raw material surcharges.

result of higher nickel costs

• In September, the US Department of Commerce announced

preliminary dumping margins of 63.86% and 76.64% in its

antidumping investigation of imports of stainless steel sheet and

narrow strip from China

Source: LME Settlement and 3-Month Futures

Source: AMM

Source: SBB

Source: IMF Previous Year’s Data

Latest Data

• US stainless prices rose by 5% in Q3 as higher raw material

surcharges provided boosts to most grades. Supply has

continued to tighten in the US stainless sheet market since the

start of 2016, thanks to declining imports resulting from AD

against China

• European stainless

prices increased by

8% in Q3, fueled

by rising alloy

surcharges as well

as gradual positive

momentum created

by healthy demand

from some end-use

sectors

• Chinese stainless

prices maintained

an upward trend,

increasing by 10%

during Q3 as a

Market Conditions by Region

15 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Plate Prices – US / Europe / China

732 729

700

725

750

775

800

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

BU

SD

15.19 14.46

38.59 39.55

36

37

38

39

40

10

15

20

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

Mill

ion B

arr

els

/

Day

USA OPEC

202 204

190

195

200

205

210

Jun 14 Dec 14 Jun 15 Dec 15 Jun 16

IND

EX

(1

985 =

100)

US Defense

Spending

Crude Oil

Production

Baltic Dry

Index

(+)

(+)

(+)

Source: AMM, SBB, Applied Value analysis

US

Shipbuilding

& Repairs

(+)

After seven straight months of increasing prices, NA & EU Plate

prices collapsed in Q3 on high inventories and lackluster demand.

Source: FRED

Source: EIA

Source: BLS

Source: Capital Link Shipping

889 763

0

500

1,000

1,500

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16Previous Year’s Data

Latest Data

Market Conditions by Region

• US plate prices fell 14% in Q3, the largest decline seen in all

global markets. Demand from major consumers of plate steel,

such as US defense spending, Oil production and Shipbuilding

remained weak in Q3, and suppliers have been offering steep

USA OPEC

exacerbated the effect of the summer slowdown on demand,

sending prices down 9% Q-o-Q

• China’s prices increased 8% in Q3, driven by price hikes

announced by several major Chinese mills in August due to

stronger domestic coil prices

573

496

329

617

534

389

200

400

600

800

1,000

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16 Mar 17

US

D/M

T

US EU China

discounts to try to

attract new orders

• US plate prices had

begun to decline in

Q3. SSCs began to

stock imported

material in an

environment

weakened by

rumors of AD duties

on plate imports

from Brazil and

South Africa

• High EU plate

inventories

16 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

• Chinese rebar shot up 16% in Q3, supported by increased

futures prices, production cuts related to the G20 summit in

Hangzhou, an acceleration of construction activity prior to the

cold winter weather and rising scrap prices

2.06

1.82

1.75

1.85

1.95

2.05

2.15

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/L

B

231 250 225

213 202

234

100

200

300

400

500

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/M

T

US EU China

5.70 7.32

2.00

6.00

10.00

14.00

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/L

B

Bar Prices

Despite a relatively tight historical correlation, Global Merchant Bar

price trends have diverged across NA, EU and CN during Q3.

Ferrochrome

Nickel

Scrap Steel

Price

Source: AMM, SBB, CRU, Applied Value Analysis

Source: AMM, SBB

Molybdenum

Source: LME

Source: AMM

742 673

570

313

840

738

502

356 200

400

600

800

1,000

1,200

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16 Mar 17

US

D/M

T

US Merchant Bar EU Merchant Bar

China Rebar SBQ (US) Source: SBB

(+)

(+)

(+)

(+)

Market Conditions by Region

Previous Year’s Data

Latest Data

• US Merchant Bar prices remained relatively flat, declining just

1% over Q3 due to weak buying activity, seasonally slow

demand and declining scrap surcharges. Cheaper scrap and

slightly higher

9,898 9,978

5,000

10,000

15,000

20,000

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/M

T

inventories are

also pressuring

SBQ prices

downwards

• EU merchant bar

prices dropped

10% in Q3 on

weakened EU

scrap prices,

sluggish demand

and intense

domestic

competition as a

result of excess

supply

17 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

88 84

454 368

0

500

1,000

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

KM

T

OCTG imports Pipe/Tube Imports

WTI Crude Oil

& Natural Gas

Signals that the Oil & Gas industry is in early stages of recovery

were not enough to preserve OCTG Q-o-Q price momentum in Q3.

42.9

44.7

2.8 2.79

6.7

4.3

0

3

6

9

12

0

40

80

120

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/m

mB

tu

US

D/b

arr

el

Crude Oil Natural Gas US Natural Gas EU

Rig Count

848 508

1,137 937

200

600

1,000

1,400

1,800

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US Global excl. US/CAN

HR

Source: AMM, SBB, EIA

Source: Baker Hughes

• US domestic OCTG prices remained flat in Q3 as crude oil prices

slid backwards to $45/bbl. However, US rig count increased by

22% over the same period, signalling a possible recovery for the

industry and demand for OCTG products

• Despite preliminary

Source: IMF, Index Mundi, EIA

Pipe/Tube/OCTG Prices

US Pipe/Tube/

OCTG Imports

(+)

(+)

(+)

(+)

Source: US Census Bureau

Previous Year’s Data

Latest Data

Market Conditions by Region

duties levelled by

the DOJ on

OCTG imports

from several

countries in Q2,

OCTG imports

remained flat in

Q3

• After a sharp 23%

increase in late

April and early

May, EU welded

tube prices have

corrected

downwards 5% in Q3, settling at $600/MT

• EU welded tube prices decreased by 5% in Q3 as the market

remained quiet and there were limited buying activities

496 613

430 485

200

400

600

800

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/M

T

US HR EU HR

Source: CRU

904

1,048

827

948

567 600

717

865

400

600

800

1000

1200

1400

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16 Mar 17

US

D/M

T

US Import OCTG US Domestic OCTG

US Welded Tube EU Welded Tube

18 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

173

313

0

125

250

375

500

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/M

T

76 93

40

80

120

160

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

MT

Wire Rod Prices

North American and European Wire Rod prices fell in Q3, driven by

weak scrap prices and import competition in both markets.

Steel Billet

Scrap Steel

Price

Source: SBB (Mesh Quality), Applied Value Analysis

Source: AMM, Euroforge, SBB

U.S. Wire Rod

Imports

Source: LME

571

449

289

551

432

357

200

300

400

500

600

700

800

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16 Mar 17

US

D/M

T

N. America Europe China (FOB Export)

Source: US Census Bureau

(+)

(–)

(+)

Market Conditions by Region

Previous Year’s Data

Latest Data

• NA and EU Wire rod prices have fallen 7% and 17%,

respectively as a result of seasonally weak demand, particularly

from the construction sector

• US Domestic mills have started to lower prices in Q3 to be more competitive

against wire rod

imports, despite a

9% reduction in

import volume in

Q3

• Rapidly declining

EU scrap prices in

Q3 cut much of

the support for

inflated wire rod

prices in Q2

• EU Wire Rod

Producers’ efforts

to initiate AD

investigations against Belarus, Russia, Turkey and Ukraine in

Q2 have so far failed to gain traction

• Chinese export prices for wire rod rallied 17% in Q3 before

weak market sentiment and buyer uncertainty began to curtail

this rise

231 250

225 213 202

234

150

250

350

450

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/M

T

US EU China

19 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

The CME HRC Futures Forward Curve suggests that steel prices will

continue to slide further, finishing the year at $540-$560/MT.

Trading History of Steel Product Futures

Price: USD/MT Volume: kMT

• The CME HRC Futures Forward Curve

currently implies that prices will decline

another 8-10% through the end of the

year, settling at ~$560-$550/MT and

could potentially decrease further in Q1

2017

• Trading volume reached 89 kMT in

August, the highest level since February.

However, cumulative trade volume for

2016 is only ~570kMT for the first 9-

months, down 24% from the same period

last year

• The HRC futures remain in

backwardation, although this has eased

since the end of June. Settlement prices

for December continued to decline, from

$605-$595/MT in Q2 to $560-$550/MT

• LME Billet Futures have remained largely

flat over the last few months, without

immediate reaction to the recent

downturn felt in the rest of the steel

market

Note: volumes are exchange traded volumes, i.e. they exclude the

“off exchange” OTC (over-the-counter) volumes

Source: CME, CRU

CRU HR Price History and CME HRC Futures

0

200

400

600

Sep 14 Dec 14 Mar 15 Jun 15 Sep 15 Dec 15 Mar 16 Jun 16 Sep 16

3-Month 15-Month Spot

LME Billet Futures – 3 months & 15 months futures (avg of Ask and Bid)

Price: USD/MT

Source: LME

Market Conditions by Region

0

30

60

90

120

150

300

400

500

600

700

800

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16 Mar 17 Sep 17

HR Prices and Futures Volume

20 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Market Conditions by Region

Stock Price Development of Major Steel Companies

Steel Production Costs

US Market Fundamentals Deep-Dive

21 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

The US CR margin above HR reached unprecedented levels in Q3,

indicating price adjustments on the horizon.

US Steel Market Fundamentals Deep-Dive

Source: CRU, SBB, Applied Value Analysis

$0

$50

$100

$150

$200

$250

$300

$0

$200

$400

$600

$800

$1,000

$1,200

US CR Margin above HR US HR US CR

US HRC, CRC Prices and Spread 2010 – Sep 2016 USD/MT

• Between 2010 and 2015, the spread between US CR and HR remained within a range of $120 - $140/MT

• In 2016, the spread surpassed the historical average by ~65%, driven by a more pronounced increase in

CR prices during the steel market run-up in H1 of 2016

• As the market starts to normalize, the spread can be expected to return to the historical average level

2010 2011 2012 2013 2014 2015 2016 YTD

$127 $117 $121 $122 $139 $139 $210

The spread reached

an all time high of

$246/MT in August

Average

Margin

This quarter’s special section will deep-dive the market fundamentals of the US steel market

Spread

USD/MT

22 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

$0

$200

$400

$600

$800

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Spread US HR Base Scrap

Historical data suggests when the delta between HR and scrap

prices exceeds $370/MT, HR prices will adjust downward.

• Historically, HR prices have a strong correlation to the spread between HR and scrap prices

− If the delta reaches above $370~$400/MT, HR prices will correct downward to account for lower input costs

• The current price gap is at $391/MT, HR prices are expected to continue the downward trend without

strong market support

US Steel Market Fundamentals Deep-Dive

HRC, Scrap

prices USD/MT

US HRC, Scrap Prices and Spread 2010 – Sep 2016

Spread = $626/MT

Aug 08, subprime crisis

Spread = $416/MT

May 10, 6 months

price drop

Spread = $516/MT

Apr 11, 7 months price

decrease

Spread = $377

May 14, global commodity

price collapse, price not

recovered yet

Spread = $447

Jun 16, prices

started to drop

consistently for 3

consecutive months

HRC, Scrap

spread USD/MT

23 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Several key factors influencing the market were assessed to

determine the anticipated future direction of US steel prices.

Macroeconomics End-Use Industry

Performance Mill Profitability

Competition is centered around

domestic steel producers

Domestic buyers of steel must pay

higher price for raw materials

Lowers production and thus supply,

providing upward pressure on price

Overhead costs are not covered

and employees are laid off

Producers can create upward

momentum on prices and margins

Not based on market fundamentals

and sometimes prices do not stick

1 2 3

The disappointing US

economic performance

during most of 2016

suggests a general

slowdown in industrial

activities, including the

overall steel industry

Impacted by the overall

bearish consumer spending

outlook, key steel end-use

industries have shown signs

of weak demand, with some

industries more afflicted

than others

US Steel Market Fundamentals Deep-Dive

Most US mills have

benefited from both

increased steel prices and

sluggish input costs in H1.

Customers could become

more aggressive negotiating

price reductions in Q4

24 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

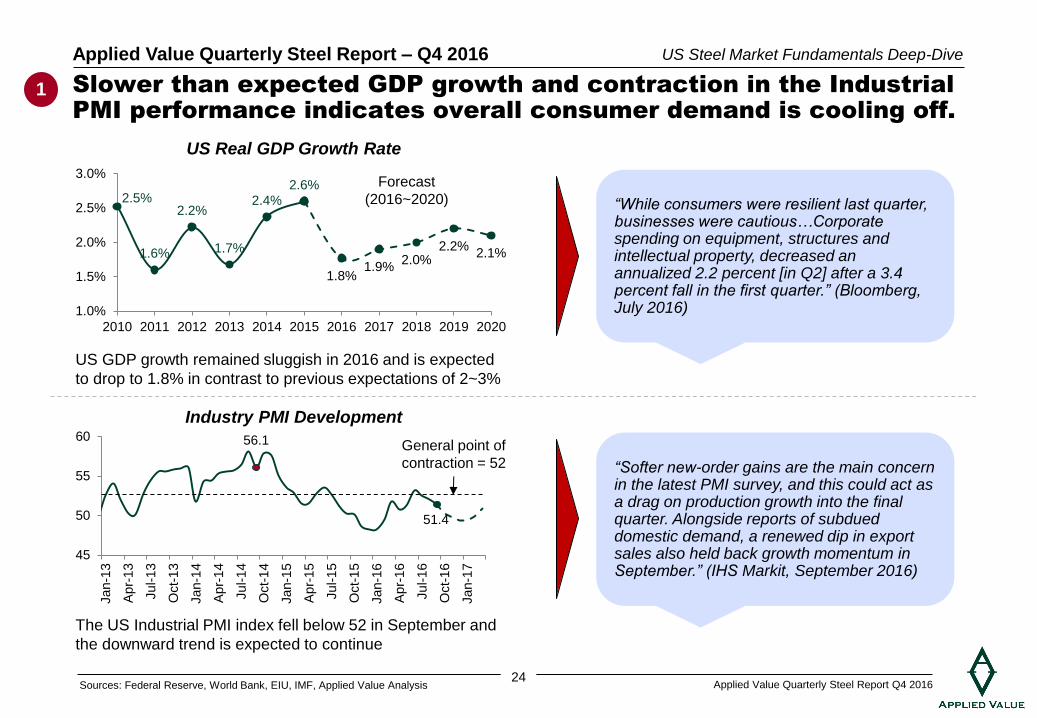

“While consumers were resilient last quarter, businesses were cautious…Corporate spending on equipment, structures and intellectual property, decreased an annualized 2.2 percent [in Q2] after a 3.4 percent fall in the first quarter.” (Bloomberg, July 2016)

Slower than expected GDP growth and contraction in the Industrial

PMI performance indicates overall consumer demand is cooling off.

US Real GDP Growth Rate

Industry PMI Development

1

2.5%

1.6%

2.2%

1.7%

2.4% 2.6%

1.8% 1.9%

2.0% 2.2%

2.1%

1.0%

1.5%

2.0%

2.5%

3.0%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

56.1

51.4

45

50

55

60

Jan-1

3

Apr-

13

Jul-1

3

Oct-

13

Jan-1

4

Apr-

14

Jul-1

4

Oct-

14

Jan-1

5

Apr-

15

Jul-1

5

Oct-

15

Jan-1

6

Apr-

16

Jul-1

6

Oct-

16

Jan-1

7

Forecast

(2016~2020)

US GDP growth remained sluggish in 2016 and is expected

to drop to 1.8% in contrast to previous expectations of 2~3%

The US Industrial PMI index fell below 52 in September and

the downward trend is expected to continue

US Steel Market Fundamentals Deep-Dive

“Softer new-order gains are the main concern in the latest PMI survey, and this could act as a drag on production growth into the final quarter. Alongside reports of subdued domestic demand, a renewed dip in export sales also held back growth momentum in September.” (IHS Markit, September 2016)

Sources: Federal Reserve, World Bank, EIU, IMF, Applied Value Analysis

General point of

contraction = 52

25 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

End sector demand from the automotive industry has started to cool

off as a peak has been reached; construction spending remained flat.

-40%

-30%

-20%

-10%

0%

10%

20%

30%

0.0

0.5

1.0

1.5

2.0

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16

Th

ou

san

ds

US Light Weight Vehicle Sales M-o-M Growth

Sales

Million units

US Light Weight Vehicle Sales US Construction Spending

• U.S. Light Weight Vehicle Sales posted a 1%

decline for August

• Major carmakers stated that a peak was reached

and consumer demand has started to soften

• Subprime car loans are hitting 17.5% in 2016, the

highest rate since 19.6% in 2007

2

M-o-M

Growth Rate

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

950

1,000

1,050

1,100

1,150

1,200

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16

Total Construction Spending M-o-M Growth

Spending

BUSD

M-o-M

Growth Rate

US Steel Market Fundamentals Deep-Dive

• US construction spending has remained flat

• Overall construction spending has also under-

performed market expectations

• In addition, the construction machinery sector is

expected to see a 15% decline y-o-y in 2016 and

another 10% in 2017

Sources: Federal Reserve, Bureau of Labor Statistics, Precision Economics,

Applied Value Analysis

26 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

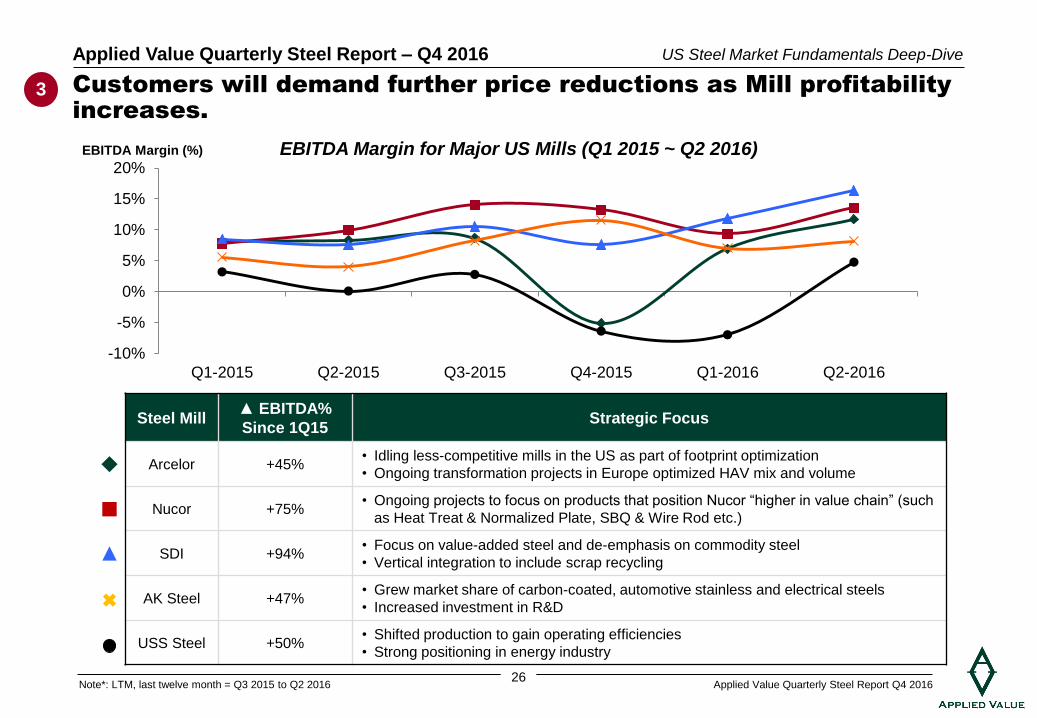

Steel Mill ▲ EBITDA%

Since 1Q15 Strategic Focus

Arcelor +45% • Idling less-competitive mills in the US as part of footprint optimization

• Ongoing transformation projects in Europe optimized HAV mix and volume

Nucor +75% • Ongoing projects to focus on products that position Nucor “higher in value chain” (such

as Heat Treat & Normalized Plate, SBQ & Wire Rod etc.)

SDI +94% • Focus on value-added steel and de-emphasis on commodity steel

• Vertical integration to include scrap recycling

AK Steel +47% • Grew market share of carbon-coated, automotive stainless and electrical steels

• Increased investment in R&D

USS Steel +50% • Shifted production to gain operating efficiencies

• Strong positioning in energy industry

Customers will demand further price reductions as Mill profitability

increases.

-10%

-5%

0%

5%

10%

15%

20%

Q1-2015 Q2-2015 Q3-2015 Q4-2015 Q1-2016 Q2-2016

3

EBITDA Margin for Major US Mills (Q1 2015 ~ Q2 2016)

Note*: LTM, last twelve month = Q3 2015 to Q2 2016

US Steel Market Fundamentals Deep-Dive

EBITDA Margin (%)

27 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

60%

65%

70%

75%

80%

Dec 15 Mar 16 Jun 16 Sep 16

Circumvention Imports Domestic Overcapacity HRC/CRC Spread

Current

Situation

Aggressive trade cases against

imports on a global level particularly

against China

Major US mills started to cut

production via plant idling to fight off

overcapacity

HRC/CRC Spread is well above

marginal production costs driven by

increased demand of CR, e.g. Auto

industry

Reality

Check

• Imports from China have been cut

out of the US

• However, CR and HDG imports to

the US from Vietnam skyrocketed in

recent months

• Despite announced mill outages, US

mill capacity utilization kept falling in

Q3, indicating ineffective capacity

cuts

− AM's Indiana Harbor facility will

resume operations in Q4

− Big River Steel started operating

in Sep

• Typical cost of processing HR into

CR is ~$60-100/MT

• Current spread is at $233/MT

• As the spread remains significantly

higher than the cost, more CR

production capacity will be added

• The spread can be expected to

decrease

US steel prices will continue to normalize and follow the current

downward trend driven by three major supply-driven factors.

0

50

100

150

200

250

Jan-15 Jul-15 Jan-16 Jul-16

China

Vietnam

CR and HDG imports to US

from China and Vietnam KST

US Mill Capacity

Utilization

US CR HR Spread

(Sep 2016) USD/MT

Decreased utilization rate despite idled capacity

613 80

153 845

0

300

600

900

HR Price ConversionCosts

Add.Spread

CR Price

28 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Market Conditions by Region

Stock Price Development of Major Steel Companies

Steel Production Costs

US Market Fundamentals Deep-Dive

29 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

While Scrap and Iron Ore prices face downward pressures, Met Coal

prices remain strong on disrupted supply from China and Australia.

• Scrap

− US Scrap prices retreated by 15% in Q3. After the Q2 buying spree (44% price jump), the idling

of several facilities has resulted in mills not running out of scrap inventories, which has slowed

buying activity. The decrease in domestic HRC prices added downward pressure to Scrap prices

− EU Scrap prices dropped 27% Q-o-Q in Q3, as supply continues to exceed demand and export

prices into Turkey decreased. Turkish demand for scrap softened after domestic rebar and semis

prices declined, causing mills’ importing activity to slow down. The behavior of HRC prices in EU

and Turkish import demand will dictate Scrap price movements

• Iron Ore

− Iron Ore prices climbed back 23%. However, prices already began to soften on a bearish steel

outlook. In addition, Chinese mills have been pivoting towards billets in lieu of Iron Ore, as

domestic billets prices have tanked by ~19% since April. Furthermore, the spike in metallurgical

coal prices and its subsequent diminishing effect on mills’ margins have caused buyers to slow

their procurement activity. Some restocking activity in early Q4 could relieve prices

• Coking Coal

− Coking Coal prices surged 80% in Q3, mainly due to limited supply from China. The rally has

been triggered in part by Beijing’s decision to limit coal mines operating days to 276 or fewer a

year. In addition, recent heavy rains in the key mining province of Shanxi have significantly

reduced the number of available roads and damaged other transportation infrastructure, curbing

local supplies. Cargoes from Australia’s New South Wales region also saw disruptions due to

weather and infrastructure problems at certain mines and railways. There is no significant

downside pressure in the short term

Steel Production Costs

Current Market Update Q4 Forecast

30 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

2017 HR production costs are projected to be slightly higher than

2016 based on limited recovery in raw material markets.

80% self-sufficiency of iron ore and coking coal

Integrated Mill Cost Changes YOY (HRB)

Source: Applied Value analysis, SBB, WSD, Goldman Sachs, Morgan Stanley,

Australian Treasury

Note: Other Metallics includes Pig Iron (purchased), Scrap and Direct Reduced Iron

Mini-mill

Mini-Mill Cost Changes YOY (HRB)

2014 – 2015 Changes 2015 – 2016F Changes

– Iron Ore: -44%

– Coking Coal: -23%

– Scrap: -39%

– Natural Gas: -39%

– Iron Ore: -5%

– Coking Coal: +25%

– Scrap: -11%

– Natural Gas: -10%

Steel Production Costs

2016F – 2017F Changes

– Iron Ore: -11%

– Coking Coal: +15%

– Scrap: +7%

– Natural Gas:+22%

31 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

US HR production costs are expected to decrease slightly to

$486/MT in 2016, before mildly bouncing back in 2017 to $492/MT.

US Integrated Mill Hot-Rolled Production Cost

80% self-sufficiency of iron ore and coking coal

Steel Production Costs

Source: Applied Value analysis, SBB, WSD, Goldman Sachs, Morgan Stanley,

Australian Treasury

32 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

US HDG production costs are expected to remain stable in 2016 before

a slight increase to $708/MT in 2017, driven by tight zinc supply.

US Integrated Mill HDG Production Cost

80% self-sufficiency of iron ore and coking coal

Steel Production Costs

Source: Applied Value analysis, SBB, WSD, Goldman Sachs, Morgan Stanley, Australian

Treasury

33 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

European HR steel production costs have maintained mostly stable

in 2016 vs 2015, but projections indicate a €9/MT increase in 2017.

2014 – 2015 Changes 2015 – 2016F Changes

– Iron Ore: -44%

– Coking Coal: -22%

– Scrap: -18%

– Natural Gas: -7%

– Iron Ore: -5%

– Coking Coal: +19%

– Scrap: -12%

– Natural Gas: -10%

Steel Production Costs

2016F – 2017F Changes

– Iron Ore: -11%

– Coking Coal: +15%

– Scrap: +11%

– Natural Gas: +20%

100% external purchase of iron ore and coking coal

Integrated Mill Cost Increases YOY (HRB)

Source: Applied Value analysis, SBB, WSD, Goldman Sachs, Australian Treasury,

Credit Suisse

Note: Other Metallics includes Pig Iron (purchased), Scrap and Direct Reduced Iron

34 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

European integrated mill HR production costs are expected to hold

firm in 2016, but to rise by €9/MT in 2017 due to rising Coal prices.

EU Integrated Mill Hot-Rolled Production Cost

100% external purchase of iron ore and coking coal

Steel Production Costs

Source: Applied Value analysis, SBB, WSD, Goldman Sachs, Australian Treasury,

Credit Suisse

35 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

European integrated mill HDG production costs are expected to

remain stable y-o-y in 2016 but see a 4% increase in 2017.

EU Integrated Mill Hot-Dip Galvanized Production Cost

100% external purchase of iron ore and coking coal

Steel Production Costs

Source: Applied Value analysis, SBB, WSD, Goldman Sachs, Australian Treasury,

Credit Suisse

36 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

€200

€190

150

200

250

300

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

EU

R/ M

T

$240 $245

150

250

350

450

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D / M

T

$298 $305

$200

$300

$400

$500

$600

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D / M

T

$231 $220

150

250

350

450

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D / G

T

US Scrap prices softened in Q3 and fell by 15% in September, while

EU Scrap prices corrected the dramatic increase seen in Q2.

Source: SBB (Semi-Finished / Slab / Latin America export FOB LA)

Source: American Metal Market (Scrap, ferrous, No. 1 bundles – Consumers) Source: SBB (Scrap / Shredded / N.Europe domestic delivered)

Source: SBB (Brazil export FOB Ponta da Madeira)

Previous Year’s Data Latest Data

Slabs Pig Iron

Ferrous Scrap US Ferrous Scrap Europe

Steel Production Costs

-5% -5%

+2% +2%

37 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

$54 $56

20

40

60

80

100

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D / M

T

$1,766

$2,344

1,000

1,500

2,000

2,500

3,000

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D / M

T

$80

$159

50

100

150

200

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D / M

T

278

291

260

270

280

290

300

Jul 14 Jan 15 Jul 15 Jan 16 Jul 16

Coking Coal prices surged 80% in Q3, due to supply disruptions from

Northern China and Australia which triggered a global buying spree.

Source: SBB (SGX 62% Fe Iron Ore cash-settled swaps - CFR Tianjin port)

Source: SBB, London Metal Exchange Source: BLS PPI. 1983 = 100

Source: SBB (Hard Coking Coal/Australia export FOB)

Iron Ore Coking Coal

Zinc Limestone – Producer Price Index

Previous Year’s Data Latest Data

Steel Production Costs

+33% +5%

+99% +4%

38 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

€19.75

€12.65

10

15

20

25

30

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

Eu

ro / M

WH

$2.76 $2.94

1

2

3

4

5

6

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

D/m

mB

tu

$7.30 $7.23

6.0

6.5

7.0

7.5

8.0

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

US

cen

ts /

KW

H

Energy prices in the US and N. Europe have started showing a trend

of recovery, while energy prices in S. Europe remain depressed.

Source: US Energy Information Administration (Industry retail price)

Source: IMF (Natural Gas spot price at the Henry Hub terminal in Louisiana) Source: EEX (EGIX Germany)

Source: EEX (KWK-Index Germany), Nordpool

-1%

+1% -35%

Electricity US

Natural Gas US Natural Gas Germany

Previous Year’s Data Latest Data

Steel Production Costs

€28.35

€24.79

€20.50

€28.50

5

15

25

35

45

Sep 14 Mar 15 Sep 15 Mar 16 Sep 16

Eu

ro /

MW

H

Central Europe Northern Europe

Electricity Europe

Central Europe: -13%

Northern Europe: +39%

39 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Market Conditions by Region

Stock Price Development of Major Steel Companies

Steel Production Costs

US Market Fundamentals Deep-Dive

40 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

2016 Q3 major developments in the steel industry.

• Current improved steel price and spreads in China are expected to spill over to Japan and improve the NSSMC’s profitability with a lag

• POSCO posted a profit margin of 11.9% for Q2, the highest in four years thanks to the increased sales ratio of high quality steel

• JFE sees marginal improvement in export spread and also expects domestic demand to pick up in 2H, led by autos and construction

• Baosteel and Wugang revealed mega-merger plans; the new giant would unseat Hebei Steel as China’s biggest steel producer

• Angang continued cost-cutting efforts and expects a stable margin outlook in Q3 and Q4

• US Steel posted a narrower net loss and improved its full-year guidance for a key earnings metric

• AK Steel swung to a profit as the steelmaker reduced its exposure to spot prices and focused on more profitable coated products

• Severstal’s Q2 results were strong and in line with expectations, reflecting the recent hike in steel prices

• Thyssenkrupp reported a 34% slide in net profit for Q3, weighed down by drops in global steel and material prices from a year ago

• Tata Steel posted a 10% increase in net loss for the fiscal Q1 as a slowdown in demand and losses at its U.K. business hurt margins

• Voestalpine expects earnings to increase, helped by higher prices in its longer-term contracts and increasing orders from the oil & gas sector

• Evraz has suffered a plunge in revenue and profit as it suffers a hangover from the global steel crisis

Stock Price Development of Major Steel Companies

41 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Despite the steel spread recovery losing momentum recently, lagged

prices will support operating results in a seasonally slow period.

• South Africa's Competition Commission says

ArcelorMittal to pay r1.5 billion fine for its

involvement in cartels – Reuters 22/Aug/2016

• ArcelorMittal reports Q2 2016 and half year

2016 results: operating income of $1.9 billion

in Q2. EBITDA of $1.8 billion in Q1 2016,

nearly double as compared to $0.9 billion in

Q1 – ArcelorMittal 29/Jul/2016

• ArcelorMittal and Marcegaglia submit offer to

acquire Ilva with the intention of increasing

Ilva's primary utilisation rate. Crude steel

production aims to rise to over 6 million tonnes

per annum by 2020.Major capital expenditure

programme aimed at enhancing Ilva's asset

capabilities – SBB 30/Jun/2016

• United Steelworkers members have ratified a

new contract with ArcelorMittal USA. Contract

sets terms of employment for nearly 14,000

hourly production, maintenance, office, and

technical workers through Sept 1, 2018

– Reuters 23/Jun/2016

Stock Price Development of Major Steel Companies

Recent Headlines:

Source: Thomson Reuters

ArcelorMittal (MT): Two-Year Stock Price

USD

0

2

4

6

8

10

12

14

16

18

20

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

42 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Current improved steel price and spreads in China are expected to

spill over to Japan and improve the NSSMC’s profitability with a lag.

• NSSMC is on track to generate 20 billion

yen ($192 million) pretax profit abroad in the

current year through March 2017, seeing

group pretax profit plunging 35% to 130

billion yen this fiscal year

– Reuters 02/Sep/2016

• NSSMC reports financial results for the

quarter ended June 30, 2016 posting

revenues of USD 9,740.49 million and Net

Earnings of USD -135.64 million. Gross

margins narrowed from 13.12% to 9.96%

compared to the same period last year,

EBITDA margins contrated to 6.09% from

9.95% – NSSMC 22/Jul/2016

• NSSMC together with Sumitomo

Corporation signed the renewal of a master

agreement for line pipe with BP. This long

term agreement is effective from July 1,

2016 for 5 years with an option to extend

another 5 years – NSSMC 22/Jul/2016

Stock Price Development of Major Steel Companies

Recent Headlines:

Nippon Steel & Sumitomo Metal Corporation (5401) Two-Year Stock Price

1600

2000

2400

2800

3200

3600

4000

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Source: Thomson Reuters

YEN

43 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

POSCO posted a profit margin of 11.9% for Q2, the highest in four

years, thanks to the increased sales ratio of high quality steel.

Stock Price Development of Major Steel Companies

Recent Headlines: POSCO (PKX): Two-Year Stock Price

USD • POSCO has established an automotive steel

plate production line with an annual output of

450,000 tons in Thailand, the largest car

producing country in Southeast Asia

– Business Korea 1/Sep/2016

• POSCO plans to take legal action against the

U.S. government's decision to slap anti-

dumping duties at nearly 60 percent on hot-

rolled flat steel products imported from Korea

– The Korea Times 7/Aug/2016

• POSCO opened Technical Service Center

Laboratories in Suzhou, China. Through this,

POSCO will be able to respond to its global

clients in a more timely manner and add value

to its steel products – POSCO 12/Jul/2016

• POSCO posted 678.5 billion won in operating

profit on a consolidated basis during the 2nd

quarter. A recorded profit margin of 11.9%, the

highest in four years, was thanks in part to the

increased sales ratio of high quality steel

– POSCO 21/Jul/2016

30

40

50

60

70

80

90

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Source: Yahoo Finance

44 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

JFE sees marginal improvement in export spread and expects

domestic demand to pick up in 2H, led by autos and construction.

Stock Price Development of Major Steel Companies

Recent Headlines: JFE Steel Corporation (5411): Two-Year Stock Price

YEN • JFE announced that it has signed an

agreement with Thyssenkrupp Steel to

cross-license advanced forming

technologies for automobile steel sheets,

including high tensile steel

– JFE 23/Aug/2016

• JFE reported an operating loss of ¥4bn, a

recurring loss of ¥13bn, and a net loss of

¥12bn for 1Q earnings – JFE 29/Jul/2016

• JFE announced that it will provide hot coils,

plates and UOE pipes to the unincorporated

consortium of Greek pipe manufacturer

CPW and Marubeni-Itochu Steel that won a

contract to supply steel materials to the TAP

project in Europe. JFE Steel will serve as

one of the project’s major subcontractors –

JFE 8/Jul/2016

1,200

1,700

2,200

2,700

3,200

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Source: Thomson Reuters

45 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Baosteel and Wugang revealed mega-merger plans that would

unseat Hebei Steel as China’s biggest steel producer.

Stock Price Development of Major Steel Companies

Recent Headlines: Baosteel Group (600019): Two-Year Stock Price

RMB • Zhanjiang steel project is fully completed with

No. 2 blast furnace successful ignition for trial

operation – Baosteel 18/Jul/2016

• Baosteel plans to cut its crude steelmaking

capacity over the next two years as part of its

efforts to push through supply-side reform

– Reuters 12/Jul/2016

• Baosteel Group and Wugang Group, two of

the China's largest steelmakers, are together

planning to restructure, their listed units said

in separate stock exchange filings

– Reuters 27/Jun/2016

3

4

5

6

7

8

9

10

11

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Source: Yahoo Finance

46 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Angang continued cost-cutting efforts and expects a stable margin

outlook in Q3 and Q4.

Stock Price Development of Major Steel Companies

Recent Headlines: Ansteel (000898): Two-Year Stock Price

RMB • Angang reported financial results for Q2:

Revenues of CNY 14,071 million, Net

Earnings of CNY 915 million; Gross

margins widened from 11.51% to 16.64%

compared to the same period last year,

EBITDA margins now 8.93% from 9.13%

– Yahoo! Finance 5/Sep/2016

• Angang Steel and Angang Energy

conservation entered into the energy

management contracts. Estimated total

construction cost is approximately

RMB213.7 million – Reuters 23/Aug/2016

• The EU on imposed anti-dumping

measures against some China and Russia

steel makers including Angang following

industry complaints from the European

Steel Association

– European Union 4/Aug/2016

• Ansteel has evinced interest in setting up a

steel plant in Andhra Pradesh at a cost of

Rs 3,000 crore

– The Times of India 26/Jun/2016

2

3

4

5

6

7

8

9

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Source: Yahoo Finance

47 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

US Steel posted a narrower net loss and improved its full-year

guidance for a key earnings metric.

• US Steel sued the state of Michigan, saying

the Michigan Department of Environmental

Quality illegally enacted a rule in June that

calls for the company to submit a plan for

meeting sulfur dioxide compliance

standards – US Steel 1/Sep/2016

• Ontario Steel Investments submitted formal

bid for US Steel Canada. Total proposed

purchase price was not disclosed

– Reuters 9/Aug/2016

• The Occupational Safety and Health

Administration has fined US Steel $170,000

after an investigation showed the company

exposed workers to asbestos hazards in

February and March – WTAE 8/Aug/2016

• US Steel reported a Q2 net loss of $46

million, compared to a Q2 2015 net loss of

$261 million, and a Q1 2016 net loss of

$340 million – US Steel 26/Jul/2016

• US Steel will idle plants in Ohio, Texas and

Alabama as it continues to cut costs amid a

global glut that has driven down prices

– WSJ 18/Mar/2016

Stock Price Development of Major Steel Companies

Recent Headlines: US Steel (X): Two-Year Stock Price

USD

0

10

20

30

40

50

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Source: Yahoo Finance

48 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

AK Steel swung to a profit as the steelmaker reduced its exposure

to spot prices and focused on more profitable coated products.

• AK Steel entered into global settlement

agreement with Magnetation LLC and its

affiliates in chapter 11 bankruptcy. AK

Steel agreed to make cash contribution of

$37.5 million to Magnetation's chapter 11

estate – Reuters 29/Aug/2016

• AK Steel reported its financial results for

Q2 2016: Net income of $17.3 million,

compared to a net loss of $64.0 million a

year ago; Adjusted EBITDA of $99.3

million, more than doubled from the year

ago quarter; Adjusted EBITDA margin

improved to 6.7% from 2.8% a year ago

– AK Steel 26/Jul/2016

Stock Price Development of Major Steel Companies

Recent Headlines: AK Steel (AKS): Two-Year Stock Price

USD

0

2

4

6

8

10

12

14

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Source: Yahoo Finance

49 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

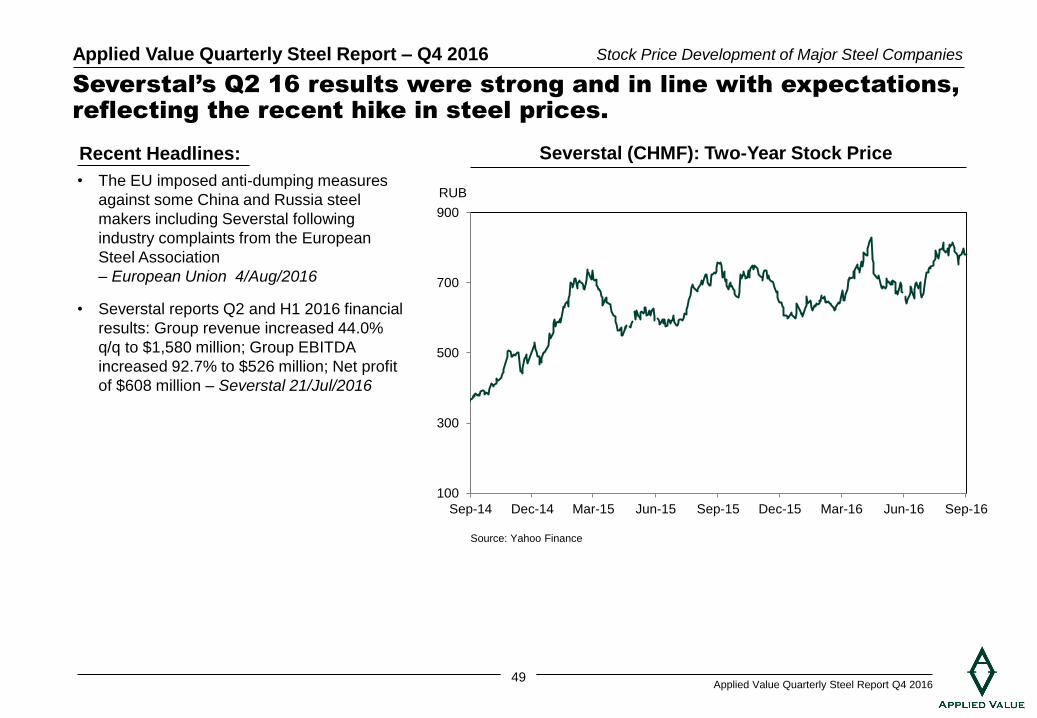

• The EU imposed anti-dumping measures

against some China and Russia steel

makers including Severstal following

industry complaints from the European

Steel Association

– European Union 4/Aug/2016

• Severstal reports Q2 and H1 2016 financial

results: Group revenue increased 44.0%

q/q to $1,580 million; Group EBITDA

increased 92.7% to $526 million; Net profit

of $608 million – Severstal 21/Jul/2016

Stock Price Development of Major Steel Companies

Recent Headlines: Severstal (CHMF): Two-Year Stock Price

RUB

Severstal’s Q2 16 results were strong and in line with expectations,

reflecting the recent hike in steel prices.

100

300

500

700

900

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Source: Yahoo Finance

50 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Thyssenkrupp reported a 34% slide in net profit for Q3, weighed

down by drops in global steel and material prices from a year ago.

• Several thousand steel workers at

Thyssenkrupp protested management's

plans for a merger of its European steel

business with that of Tata Steel as well as

possible site closures

– Reuters 31/Aug/2016

• Thyssenkrupp wants to come up with a

new, aggressive cost-cutting plan for its

steelmaking division by May, probably

including the closure of some plants that

would violate a labour agreement

-Reuters 12/Aug/2016

• Thyssenkrupp reported Q3 2016 financial

results: Sales fell 12%, to €9.87 billion; Net

profit was €130 million compared with €199

million during the same period last year;

Adjusted EBIT was down 45% y-o-y, at €91

million – WSJ 11/Aug/2016

• ThyssenKrupp confirmed that it is in talks

with Tata Steel and other steel groups over

a potential tie-up, giving the strongest

indication yet that the German company

would help drive a new wave of expected

consolidation in the beleaguered European

steel sector – WSJ 11/Jul/2016

Stock Price Development of Major Steel Companies

Recent Headlines: ThyssenKrupp AG (TKA): Two-Year Stock Price

EUR

12

16

20

24

28

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Source: Yahoo Finance

51 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Tata Steel posted a 10% increase in net loss for the fiscal Q1 as a

slowdown in demand and losses at its U.K. business hurt margins.

• India's leading steelmakers - JSW Steel,

Tata, Essar Steel and Steel Authority of

India, have sought an extension of the

minimum import price (MIP) imposed on

steel by six months to a year, as the

current MIP regime is due to end

– The Times of India 3/Aug/2016

• Tata Steel is expected to pause the sale

of most of its UK business, including Port

Talbot. However, it will proceed with the

sale of its speciality steel-making

business, which employs 2,000 people in

Hartlepool, Rotherham and Stocksbridge

– BBC 7/Jul/2016

• Tata Steel has entered into discussions

with strategic players in the steel industry

to explore the feasibility of collaborations

through a potential joint venture

– Tata Steel 7/Jul/2016

Stock Price Development of Major Steel Companies

Recent Headlines: Tata Steel (TATASTEEL): Two-Year Stock Price

RS

150

250

350

450

550

650

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Source: Yahoo Finance

52 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

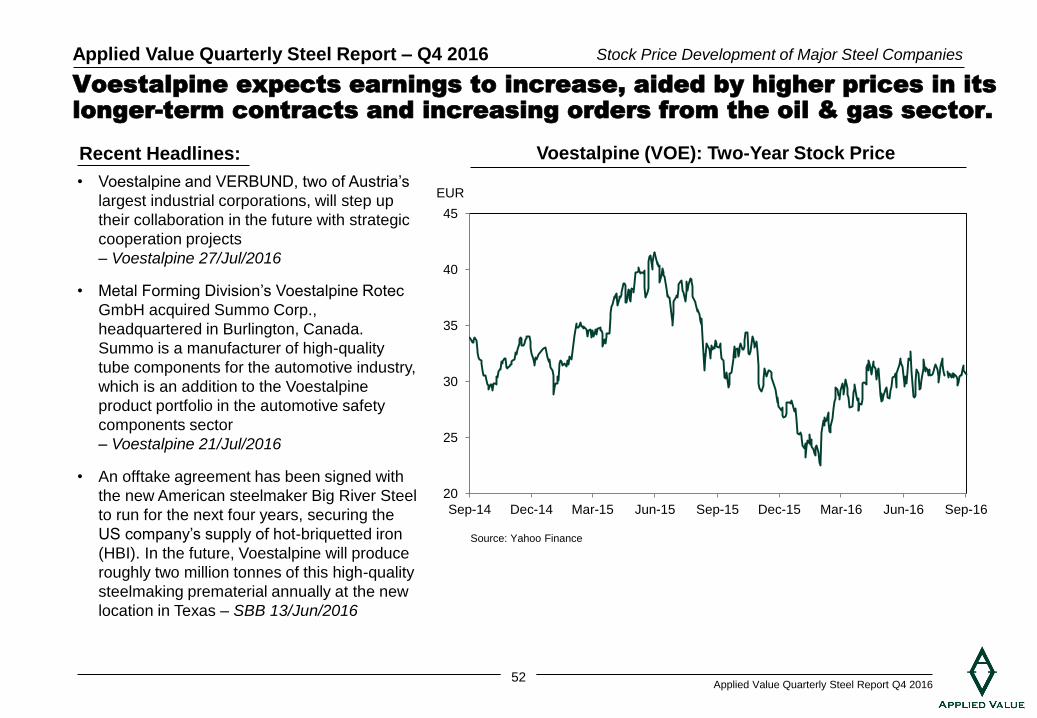

Voestalpine expects earnings to increase, aided by higher prices in its

longer-term contracts and increasing orders from the oil & gas sector.

Stock Price Development of Major Steel Companies

Recent Headlines: Voestalpine (VOE): Two-Year Stock Price

EUR • Voestalpine and VERBUND, two of Austria’s

largest industrial corporations, will step up

their collaboration in the future with strategic

cooperation projects

– Voestalpine 27/Jul/2016

• Metal Forming Division’s Voestalpine Rotec

GmbH acquired Summo Corp.,

headquartered in Burlington, Canada.

Summo is a manufacturer of high-quality

tube components for the automotive industry,

which is an addition to the Voestalpine

product portfolio in the automotive safety

components sector

– Voestalpine 21/Jul/2016

• An offtake agreement has been signed with

the new American steelmaker Big River Steel

to run for the next four years, securing the

US company’s supply of hot-briquetted iron

(HBI). In the future, Voestalpine will produce

roughly two million tonnes of this high-quality

steelmaking prematerial annually at the new

location in Texas – SBB 13/Jun/2016

20

25

30

35

40

45

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Source: Yahoo Finance

53 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Gerdau reported disappointing results for Q2 2016, a fall that was

triggered primarily by lower revenue generation.

Stock Price Development of Major Steel Companies

Recent Headlines: Gerdau S.A (GGB): Two-Year Stock Price

USD • Sand Springs Railway, a managed affiliate

of OmniTRAX, is acquiring the Gerdau mill

site in Sand Springs, Okla. Sand Springs

Railway Company provides freight service

between Sand Springs and Tulsa

– Digital Journal 1/Sept/2016

• Competition Commission of India: CCI

approves formation of joint venture between

Gerdau S.A., Sumitomo Corporation and

the Japan Steel Works Ltd

– Reuters 23/Aug/2016

• Gerdau hopes to keep reducing leverage in

dollar terms until end of year; its mills in

Brazil reached a utilization rate of 75

percent capacity in Q2, compared to 65

percent in Q1 – Reuters 10/Aug/2016 Source: Thomson Reuters

0

1

2

3

4

5

6

7

8

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

54 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Nucor’s Q2 performance benefited from a stronger global economic

outlook and improved market conditions.

Stock Price Development of Major Steel Companies

Recent Headlines: Nucor Corporation (NUE): Two-Year Stock Price

USD • Total tons shipped to outside customers

were 6,457,000 tons in Q2 2016, a 5%

increase from Q1 2016 –

Reuters 21/Jul/2016

• Nucor announced that it has agreed to

acquire Joy Global's steel plate mill

in Longview, Texas, for approximately $29

million. The mill produces carbon and alloy

plate products with heat-treating capabilities

and has an annual capacity of 180,000 tons

– Nucor 20/Jul/2016

• Kinder Morgan announced that it had

reached a US$900-million deal to provide

in-plant services to five Nucor plants. The

plants are located in Decatur, Alabama;

Hertford, North Carolina; Berkeley, and

South Carolina. There are two plants at

Blytheville, Arkansas – Platts 7/Jul/2016 Source: Thomson Reuters

30

35

40

45

50

55

60

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

55 Applied Value Quarterly Steel Report Q4 2016

Applied Value Quarterly Steel Report – Q4 2016

Evraz has suffered a plunge in revenue and profit, partially a result

of a hangover from the global steel crisis.

Stock Price Development of Major Steel Companies

Recent Headlines: Evraz Group S.A. (EVR.L) : Two-Year Stock Price

GBP • Evraz’s Q2 crude steel output fell 10%

quarter-on-quarter to 3.2 million tonnes

due to planned repair at one of its

furnaces

– The Moscow Times 19/Jul/2016

• Bushveld Minerals has updated on

conditional purchase agreement with

Evraz for Vametco – Reuters 15/Jul/2016

• EVRAZ NTMK has announced the start

of a new blast furnace construction

project in in Nizhny Tagil

– Evraz 14/Jul/2016

• EVRAZ has started the production of TSI

wheelsets together with Slovenian

company SZ-VIT. Wheelset is a new

product for EVRAZ, and it is

characterized by high marketability

among the key European rail operators

and manufacturers of freight wagons

– Evraz 23/Jun/2016

Source: Thomson Reuters