apipa 20091 statistical sampling for auditors jeanne h. yamamura cpa, mim, phd

TRANSCRIPT

APIPA 2009APIPA 2009 11

STATISTICAL SAMPLING FOR

AUDITORS

Jeanne H. Yamamura

CPA, MIM, PHD

APIPA 2009APIPA 2009 22

OBJECTIVESOBJECTIVES Review of sampling conceptsReview of sampling concepts Types of samplingTypes of sampling

Attribute samplingAttribute sampling StepsSteps Nonstatistical attribute samplingNonstatistical attribute sampling Compliance auditingCompliance auditing

Monetary unit samplingMonetary unit sampling StepsSteps Nonstatistical monetary unit sampling Nonstatistical monetary unit sampling

Classical samplingClassical sampling Ratio estimationRatio estimation Difference estimationDifference estimation

APIPA 2009APIPA 2009 33

AUDIT SAMPLINGAUDIT SAMPLING

Application of an audit procedure to less Application of an audit procedure to less than 100% of the items in a populationthan 100% of the items in a population Account balanceAccount balance Class of transactionsClass of transactions

Examination “on a test basis”Examination “on a test basis” Key: Sample is intended to be Key: Sample is intended to be

representative of the population.representative of the population.

APIPA 2009APIPA 2009 44

SAMPLING RISKSAMPLING RISK

Possibility that the sample is NOT Possibility that the sample is NOT representative of the populationrepresentative of the population

As a result, auditor will reach WRONG As a result, auditor will reach WRONG conclusionconclusion

Decision errorsDecision errors Type I – Risk of incorrect rejectionType I – Risk of incorrect rejection Type II – Risk of incorrect acceptanceType II – Risk of incorrect acceptance

APIPA 2009APIPA 2009 55

TYPE I – RISK OF TYPE I – RISK OF INCORRECT REJECTIONINCORRECT REJECTION

Internal controlInternal control: Risk that sample : Risk that sample supports conclusion that control is NOT supports conclusion that control is NOT operating effectively when it really isoperating effectively when it really is AKA – Risk of underreliance, risk of AKA – Risk of underreliance, risk of

assessing control risk too highassessing control risk too high

Substantive testingSubstantive testing: Risk that sample : Risk that sample supports conclusion that balance is NOT supports conclusion that balance is NOT properly stated when it really isproperly stated when it really is

APIPA 2009APIPA 2009 66

TYPE II – RISK OF TYPE II – RISK OF INCORRECT ACCEPTANCEINCORRECT ACCEPTANCE

Internal controlInternal control: Risk that sample : Risk that sample supports conclusion that control is supports conclusion that control is operating effectively when it really isn’toperating effectively when it really isn’t AKA – Risk of overreliance, risk of assessing AKA – Risk of overreliance, risk of assessing

control risk too lowcontrol risk too low

Substantive testingSubstantive testing: Risk that sample : Risk that sample supports conclusion that balance is supports conclusion that balance is properly stated when it really isn’tproperly stated when it really isn’t

APIPA 2009APIPA 2009 77

WHICH RISK POSES THE WHICH RISK POSES THE GREATER DANGER TO AN GREATER DANGER TO AN AUDITOR?AUDITOR?

Risk of incorrect rejectionRisk of incorrect rejection EfficiencyEfficiency

Risk of incorrect acceptanceRisk of incorrect acceptance EffectivenessEffectiveness

Auditor focus on Type IIAuditor focus on Type II Also provides coverage for Type IAlso provides coverage for Type I

APIPA 2009APIPA 2009 88

NONSAMPLING RISKNONSAMPLING RISK

Risk of auditor errorRisk of auditor error Sample wrong populationSample wrong population Fail to detect a misstatement when applying audit Fail to detect a misstatement when applying audit

procedureprocedure Misinterpret audit resultMisinterpret audit result

Controlled through Controlled through Adequate trainingAdequate training Proper planningProper planning Effective supervisionEffective supervision

APIPA 2009APIPA 2009 99

SAMPLE SIZE FACTORSSAMPLE SIZE FACTORS

Desired level of assurance Desired level of assurance (confidence level)(confidence level)

Acceptable defect rate (tolerable Acceptable defect rate (tolerable error)error)

Historical defect rate (expected Historical defect rate (expected error)error)

APIPA 2009APIPA 2009 1010

CONFIDENCE LEVELCONFIDENCE LEVEL

Complement of sampling riskComplement of sampling risk 5% sampling risk, 95% confidence level5% sampling risk, 95% confidence level

How much reliance will be placed on test How much reliance will be placed on test resultsresults

The greater the reliance and the more severe The greater the reliance and the more severe the consequences of Type II error, the higher the consequences of Type II error, the higher the confidence level neededthe confidence level needed

Sample size increases with confidence level Sample size increases with confidence level (decreases with sampling risk)(decreases with sampling risk)

APIPA 2009APIPA 2009 1111

TOLERABLE ERROR AND TOLERABLE ERROR AND EXPECTED ERROREXPECTED ERROR

““Precision” – the gap between tolerable Precision” – the gap between tolerable error and expected errorerror and expected error

AKA Allowance for sampling riskAKA Allowance for sampling risk Sample size increases as precision Sample size increases as precision

decreasesdecreases

APIPA 2009APIPA 2009 1212

WHEN DO YOU SAMPLE?WHEN DO YOU SAMPLE?

Inspection of tangible assets, e.g., Inspection of tangible assets, e.g., inventory observationinventory observation

Inspection of records or documents, e.g., Inspection of records or documents, e.g., internal control testinginternal control testing

Reperformance, e.g., internal control Reperformance, e.g., internal control testingtesting

Confirmation, e.g., verification of AR Confirmation, e.g., verification of AR balancesbalances

APIPA 2009APIPA 2009 1313

WHEN IS SAMPLING WHEN IS SAMPLING INAPPROPRIATE?INAPPROPRIATE?

Selection of all items with a particular Selection of all items with a particular characteristic, e.g., all disbursements > characteristic, e.g., all disbursements > $100,000$100,000

Testing only one or a few items, e.g., Testing only one or a few items, e.g., automated IT controls, walk throughsautomated IT controls, walk throughs

Analytical proceduresAnalytical procedures ScanningScanning InquiryInquiry ObservationObservation

APIPA 2009APIPA 2009 1414

WALKTHROUGHSWALKTHROUGHS

Designed to provide evidence regarding the Designed to provide evidence regarding the design and implementation of controlsdesign and implementation of controls

Can provide some assurance of operating Can provide some assurance of operating effectiveness BUTeffectiveness BUT Depends on nature of control (automated or Depends on nature of control (automated or

manual)manual) Depends on nature of auditor’s procedures to test Depends on nature of auditor’s procedures to test

control (also includes inquiry and observation control (also includes inquiry and observation combined with strong control environment and combined with strong control environment and adequate monitoring)adequate monitoring)

Walkthough = sample of 1Walkthough = sample of 1

APIPA 2009APIPA 2009 1515

STATISTICAL VS STATISTICAL VS NONSTATISTICAL SAMPLINGNONSTATISTICAL SAMPLING

Statistical samplingStatistical sampling Statistical computation of sample sizeStatistical computation of sample size Statistical evaluation of resultsStatistical evaluation of results

Nonstatistical samplingNonstatistical sampling Sample sizes should be approximately the Sample sizes should be approximately the

same (AU 350.22)same (AU 350.22) Sample sizes must be sufficient to support Sample sizes must be sufficient to support

reliance on controls and assertions being reliance on controls and assertions being testedtested

APIPA 2009APIPA 2009 1616

WHEN IS SAMPLING WHEN IS SAMPLING NONSTATISTICAL?NONSTATISTICAL?

If sample size determined judgmentallyIf sample size determined judgmentally If sample selected haphazardlyIf sample selected haphazardly If sample results evaluated judgmentallyIf sample results evaluated judgmentally

APIPA 2009APIPA 2009 1717

TYPES OF SAMPLINGTYPES OF SAMPLING

Attribute samplingAttribute sampling Monetary unit samplingMonetary unit sampling Classical variables samplingClassical variables sampling

APIPA 2009APIPA 2009 1818

ATTRIBUTE SAMPLINGATTRIBUTE SAMPLING

Used to estimate proportion of a Used to estimate proportion of a population that possesses a specific population that possesses a specific characteristiccharacteristic

Most commonly used for T of CMost commonly used for T of C Can also be used for dual purpose Can also be used for dual purpose

testing (T of C and Substantive T of T)testing (T of C and Substantive T of T)

APIPA 2009APIPA 2009 1919

MONETARY-UNIT MONETARY-UNIT SAMPLINGSAMPLING

AKA probability proportional to size AKA probability proportional to size (PPS) sampling, cumulative monetary (PPS) sampling, cumulative monetary unit samplingunit sampling

Used to estimate dollar amount of Used to estimate dollar amount of misstatementmisstatement

APIPA 2009APIPA 2009 2020

CLASSICAL VARIABLES CLASSICAL VARIABLES SAMPLINGSAMPLING

Uses normal distribution theory to identify Uses normal distribution theory to identify amount of misstatementamount of misstatement

Useful when large number of differences Useful when large number of differences expectedexpected Smaller sample size than MUSSmaller sample size than MUS

Effective for both overstatements and Effective for both overstatements and understatementsunderstatements

Can easily incorporate zero balancesCan easily incorporate zero balances

APIPA 2009APIPA 2009 2121

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 1 NO. 1

APIPA 2009APIPA 2009 2222

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 1NO. 1

TestTest Involves Involves Sampling?Sampling?

Attribute / Variable / MUS / NAAttribute / Variable / MUS / NA

11 YesYes Attribute (ST of T)Attribute (ST of T)

22 NoNo NANA

33 YesYes Attribute (T of C)Attribute (T of C)

44 NoNo NANA

55 NoNo NA (Could be MUS if large NA (Could be MUS if large population)population)

66 NoNo NANA

APIPA 2009APIPA 2009 2323

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 1NO. 1

TestTest Involves Involves Sampling?Sampling?

Attribute / Variable / MUS / NAAttribute / Variable / MUS / NA

77 YesYes Attribute (T of C)Attribute (T of C)

88 YesYes MUSMUS

99 NoNo NANA

1010 YesYes Attribute (T of C/ST of T)Attribute (T of C/ST of T)

1111 NoNo NANA

APIPA 2009APIPA 2009 2424

STEPS IN STATISTICAL STEPS IN STATISTICAL ATTRIBUTE SAMPLING ATTRIBUTE SAMPLING APPLICATIONAPPLICATION

PlanningPlanning1.1. Determine the test objectivesDetermine the test objectives2.2. Define the population characteristicsDefine the population characteristics3.3. Determine the sample sizeDetermine the sample size

PerformancePerformance4.4. Select sample itemsSelect sample items5.5. Perform the auditing proceduresPerform the auditing procedures

EvaluationEvaluation6.6. Calculate the resultsCalculate the results7.7. Draw conclusionsDraw conclusions

APIPA 2009APIPA 2009 2525

STEP 1: DETERMINE THE STEP 1: DETERMINE THE TEST OBJECTIVESTEST OBJECTIVES

Objective for T of CObjective for T of C: To determine the : To determine the operating effectiveness of the internal operating effectiveness of the internal controlcontrol Support control risk assessment below Support control risk assessment below

maximummaximum

Identify controls to be tested and Identify controls to be tested and understand why they are to be testedunderstand why they are to be tested

APIPA 2009APIPA 2009 2626

TESTS OF CONTROLSTESTS OF CONTROLS

Concerned primarily withConcerned primarily with Were the necessary controls performed?Were the necessary controls performed? How were they performed?How were they performed? By whom were they performed?By whom were they performed?

Appropriate when documentary evidence Appropriate when documentary evidence of performance existsof performance exists

APIPA 2009APIPA 2009 2727

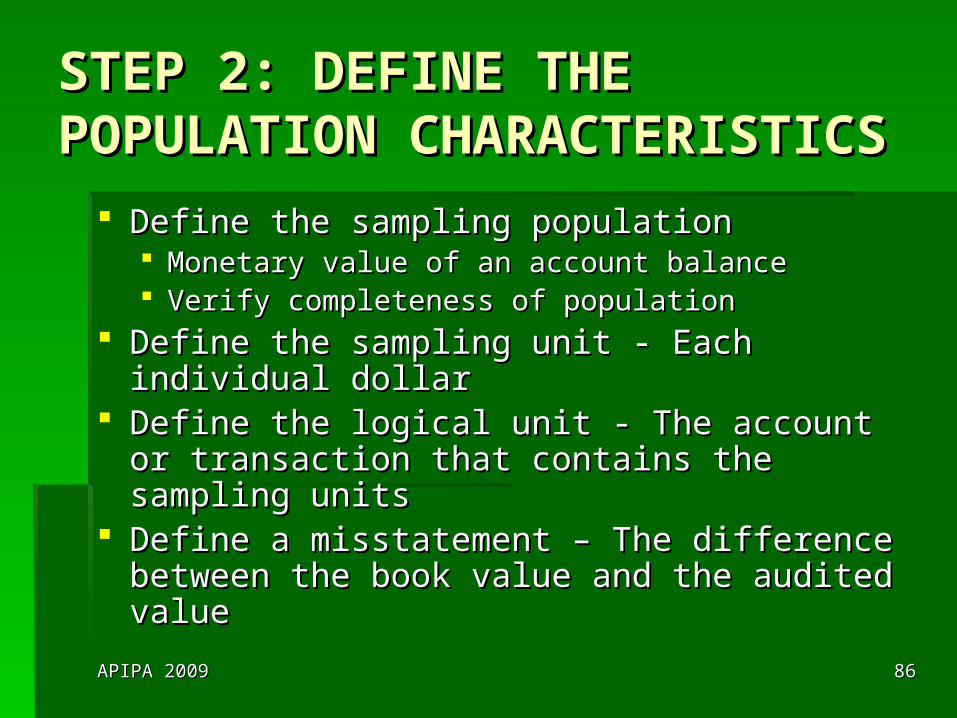

STEP 2: DEFINE THE STEP 2: DEFINE THE POPULATION POPULATION CHARACTERISTICSCHARACTERISTICS

Define the sampling populationDefine the sampling population AssertionAssertion CompletenessCompleteness

Define the sampling unitDefine the sampling unit Determined by available recordsDetermined by available records

Define the control deviation conditionsDefine the control deviation conditions

APIPA 2009APIPA 2009 2828

STEP 3: DETERMINE THE STEP 3: DETERMINE THE SAMPLE SIZESAMPLE SIZE

Determine factorsDetermine factors Desired confidence level (direct)Desired confidence level (direct) Tolerable deviation rate (inverse)Tolerable deviation rate (inverse) Expected population deviation rate (direct)Expected population deviation rate (direct)

Desired confidence levelDesired confidence level If planning to rely on controls, would be 90 to If planning to rely on controls, would be 90 to

95%95% Significance of account and importance of Significance of account and importance of

assertion affected by control being testedassertion affected by control being tested

APIPA 2009APIPA 2009 2929

STEP 3: DETERMINE THE STEP 3: DETERMINE THE SAMPLE SIZESAMPLE SIZE

Tolerable deviation rateTolerable deviation rate Maximum deviation rate that auditor willing to Maximum deviation rate that auditor willing to

accept and still consider control effectiveaccept and still consider control effective Control would be relied uponControl would be relied upon

Why any errors acceptable?Why any errors acceptable? Control deviation = MisstatementControl deviation = Misstatement

Assessed importance of controlAssessed importance of control Tolerable Tolerable deviation ratedeviation rate

Highly importantHighly important 3-5%3-5%

Moderately importantModerately important 6-10%6-10%

APIPA 2009APIPA 2009 3030

STEP 3: DETERMINE THE STEP 3: DETERMINE THE SAMPLE SIZESAMPLE SIZE

Expected population deviation rateExpected population deviation rate Rate expected to exist in populationRate expected to exist in population Based on prior years’ results or pilot sampleBased on prior years’ results or pilot sample If expected population deviation rate > If expected population deviation rate >

tolerable rate, DO NOT TESTtolerable rate, DO NOT TEST

SAMPLE SIZE TABLESSAMPLE SIZE TABLES

APIPA 2009APIPA 2009 3131

STEP 3: DETERMINE THE STEP 3: DETERMINE THE SAMPLE SIZESAMPLE SIZE

Testing multiple attributes on the same Testing multiple attributes on the same samplesample Select largest sample size and audit all of Select largest sample size and audit all of

them for all attributesthem for all attributes Result is some overauditing BUT may take Result is some overauditing BUT may take

less time than trying to remember which less time than trying to remember which sample items need to be tested for which sample items need to be tested for which attribute attribute

APIPA 2009APIPA 2009 3232

FINITE POPULATION FINITE POPULATION CORRECTION FACTORCORRECTION FACTOR

When population size < 500When population size < 500 Apply finite population correction factorApply finite population correction factor

√√1-(n/N)1-(n/N) Where n = sample size from table and N = Where n = sample size from table and N =

number of units in populationnumber of units in population

APIPA 2009APIPA 2009 3333

STEP 4: SELECT THE STEP 4: SELECT THE SAMPLE ITEMSSAMPLE ITEMS

Sample must be selected to be Sample must be selected to be representative of the populationrepresentative of the population

Each item must have an equal Each item must have an equal opportunity of being selectedopportunity of being selected

APIPA 2009APIPA 2009 3434

STEP 4: SELECT THE STEP 4: SELECT THE SAMPLE ITEMSSAMPLE ITEMS

Random number selectionRandom number selection Unrestricted random sampling without Unrestricted random sampling without

replacement (once selected cannot be replacement (once selected cannot be selected again)selected again)

APIPA 2009APIPA 2009 3535

STEP 4: SELECT THE STEP 4: SELECT THE SAMPLE ITEMSSAMPLE ITEMS

Random number tableRandom number table Need to documentNeed to document

Correspondence: relationship between Correspondence: relationship between population and random number tablepopulation and random number table

Route: selection path, e.g., up or down columns, Route: selection path, e.g., up or down columns, and right to left (must be consistent)and right to left (must be consistent)

Starting point: starting row, column, digitStarting point: starting row, column, digit Stopping point: to enable adding more sample Stopping point: to enable adding more sample

items if neededitems if needed

APIPA 2009APIPA 2009 3636

RANDOM NUMBER TABLE RANDOM NUMBER TABLE ILLUSTRATIONILLUSTRATION

Select a sample of 4 items from prenumbered Select a sample of 4 items from prenumbered canceled checks numbered from 1 to 500. canceled checks numbered from 1 to 500. Start at row 5, column 1, digit starting position Start at row 5, column 1, digit starting position 1. Select three-digit numbers. Items selected 1. Select three-digit numbers. Items selected are:are: 145 (sample item #1)145 (sample item #1) 516 (discard because checks numbers do not 516 (discard because checks numbers do not

exceed 500)exceed 500) 032 (sample item #2)032 (sample item #2) 246 (sample item #3)246 (sample item #3) 840 (discard)181 (sample item #4)840 (discard)181 (sample item #4)

APIPA 2009APIPA 2009 3737

RANDOM NUMBER TABLE RANDOM NUMBER TABLE ILLUSTRATIONILLUSTRATION

To minimize discards, table numbers > 500 can To minimize discards, table numbers > 500 can be reduced by 500 to produce a sample item be reduced by 500 to produce a sample item within the population boundary of 1 to 500. The within the population boundary of 1 to 500. The four sample items selected are:four sample items selected are: 145 (sample item #1)145 (sample item #1) 016 (sample item #2 = 516 – 500 = 016)016 (sample item #2 = 516 – 500 = 016) 032 (sample item #2)032 (sample item #2) 246 (sample item #3)246 (sample item #3) 340 (sample item #4 = 840 – 500 = 340)340 (sample item #4 = 840 – 500 = 340)

APIPA 2009APIPA 2009 3838

RANDOM NUMBER TABLE RANDOM NUMBER TABLE ILLUSTRATIONILLUSTRATION

Select 4 sales invoices numbered from 5000 to Select 4 sales invoices numbered from 5000 to 12000. Start at row 21, column 2, digit starting 12000. Start at row 21, column 2, digit starting point 1. Rather than use a 5-digit number, point 1. Rather than use a 5-digit number, which produces a large number of discards, which produces a large number of discards, add a constant to get a population with 4 digits. add a constant to get a population with 4 digits. If a constant of 3000 is used, the usable If a constant of 3000 is used, the usable numbers selected from 2000 to 9000 are:numbers selected from 2000 to 9000 are: 6,043 (sample item #1 = 3043 + 3000)6,043 (sample item #1 = 3043 + 3000) 10,120 (sample item #2 = 7120 + 3000)10,120 (sample item #2 = 7120 + 3000) 10,212 (sample item #3 = 7212 + 3000)10,212 (sample item #3 = 7212 + 3000) 5,259 (sample item #4 = 2259 + 3000)5,259 (sample item #4 = 2259 + 3000)

APIPA 2009APIPA 2009 3939

STEP 4: SELECT THE STEP 4: SELECT THE SAMPLE ITEMS - EXCELSAMPLE ITEMS - EXCEL

Excel Excel Select ToolsSelect Tools Select Data AnalysisSelect Data Analysis Select SamplingSelect Sampling

APIPA 2009APIPA 2009 4040

STEP 4: SELECT THE STEP 4: SELECT THE SAMPLE ITEMS - EXCELSAMPLE ITEMS - EXCEL

APIPA 2009APIPA 2009 4141

STEP 4: SELECT THE STEP 4: SELECT THE SAMPLE ITEMSSAMPLE ITEMS

Input RangeInput Range Enter the references for the range of data that contains the population of Enter the references for the range of data that contains the population of

values you want to sample. Microsoft Excel draws samples from the first values you want to sample. Microsoft Excel draws samples from the first column, then the second column, and so on.column, then the second column, and so on.

LabelsLabels Select if the first row or column of your input range contains labels. Clear Select if the first row or column of your input range contains labels. Clear

if your input range has no labels; Excel generates appropriate data labels if your input range has no labels; Excel generates appropriate data labels for the output table.for the output table.

Sampling MethodSampling Method Click Click PeriodicPeriodic or or RandomRandom to indicate the sampling interval you want. to indicate the sampling interval you want. PeriodPeriod Enter the periodic interval at which you want sampling to take place. The Enter the periodic interval at which you want sampling to take place. The

periodperiod-th value in the input range and every -th value in the input range and every periodperiod-th value thereafter is -th value thereafter is copied to the output column. Sampling stops when the end of the input copied to the output column. Sampling stops when the end of the input range is reached.range is reached.

APIPA 2009APIPA 2009 4242

STEP 4: SELECT THE STEP 4: SELECT THE SAMPLE ITEMSSAMPLE ITEMS

Number of SamplesNumber of Samples Enter the number of random values you want in the Enter the number of random values you want in the

output column. Each value is drawn from a random output column. Each value is drawn from a random position in the input range, and position in the input range, and any number can be any number can be selected more than onceselected more than once..

Output RangeOutput Range Enter the reference for the upper-left cell of the output Enter the reference for the upper-left cell of the output

table. Data is written in a single column below the cell. table. Data is written in a single column below the cell. If you select If you select PeriodicPeriodic, the number of values in the , the number of values in the output table is equal to the number of values in the output table is equal to the number of values in the input range, divided by the sampling rate. If you select input range, divided by the sampling rate. If you select RandomRandom, the number of values in the output table is , the number of values in the output table is equal to the number of samples.equal to the number of samples.

APIPA 2009APIPA 2009 4343

STEP 4: SELECT THE STEP 4: SELECT THE SAMPLE ITEMSSAMPLE ITEMS

Systematic selectionSystematic selection Determine sampling interval = Population / Sample Determine sampling interval = Population / Sample

SizeSize Ensure population is in random orderEnsure population is in random order Select random starting number (within first interval)Select random starting number (within first interval)

Better to use multiple random starting points to reduce risk Better to use multiple random starting points to reduce risk of missing systematic deviationsof missing systematic deviations

Select every nth itemSelect every nth item Continue sample selection until population is Continue sample selection until population is

exhausted exhausted (Last sample selected + sampling interval) > Last item in (Last sample selected + sampling interval) > Last item in

populationpopulation In other words, don’t stop when desired sample size In other words, don’t stop when desired sample size

reachedreached

APIPA 2009APIPA 2009 4444

STEP 5: PERFORM THE STEP 5: PERFORM THE AUDITING PROCEDURESAUDITING PROCEDURES

Conduct planned audit proceduresConduct planned audit procedures What if?What if?

Voided documents - if properly voided, not a Voided documents - if properly voided, not a deviation; replace with new sample itemdeviation; replace with new sample item

Unused or inapplicable documents – replace Unused or inapplicable documents – replace with new sample itemwith new sample item

Inability to examine sample item – deviationInability to examine sample item – deviation Stopping test before completion – large Stopping test before completion – large

number of deviations detectednumber of deviations detected

APIPA 2009APIPA 2009 4545

STEP 5: PERFORM THE STEP 5: PERFORM THE AUDITING PROCEDURESAUDITING PROCEDURES

Deviations observedDeviations observed Investigate nature, cause, and consequence Investigate nature, cause, and consequence

of every exceptionof every exception Unintentional error? Or fraud?Unintentional error? Or fraud? Monetary misstatement resulted?Monetary misstatement resulted? Cause – misunderstanding of instructions? Cause – misunderstanding of instructions?

Carelessness?Carelessness? Effect on other areas?Effect on other areas?

APIPA 2009APIPA 2009 4646

STEP 6: CALCULATE STEP 6: CALCULATE RESULTSRESULTS

Summarize deviations for each controlSummarize deviations for each control Calculate sample deviation rate and Calculate sample deviation rate and

computed upper deviation ratecomputed upper deviation rate Sample deviation rate + Allowance for Sample deviation rate + Allowance for

sampling risk = Computed upper deviation sampling risk = Computed upper deviation raterate

Statistical sampling results evaluation tablesStatistical sampling results evaluation tables

APIPA 2009APIPA 2009 4747

STEP 7: DRAW STEP 7: DRAW CONCLUSIONSCONCLUSIONS

If Computed Upper Deviation Rate > If Computed Upper Deviation Rate > Tolerable Rate, control is ineffective and Tolerable Rate, control is ineffective and cannot be relied upon.cannot be relied upon.

If Computed Upper Deviation Rate < If Computed Upper Deviation Rate < Tolerable Rate, control is effectiveTolerable Rate, control is effective

APIPA 2009APIPA 2009 4848

EVALUATION OF EVALUATION OF EXPOSUREEXPOSURE

In a sample of 25 manual control In a sample of 25 manual control operations from a population of 3,000 operations from a population of 3,000 control operations, 1 deviation was control operations, 1 deviation was identified. The sample was designed with identified. The sample was designed with an expectation that 0 deviations would be an expectation that 0 deviations would be found.found.

Looking up the results (in 90% Looking up the results (in 90% confidence level table): Computed upper confidence level table): Computed upper error limit = 14.7%error limit = 14.7%

APIPA 2009APIPA 2009 4949

EVALUATION OF EVALUATION OF EXPOSUREEXPOSURE

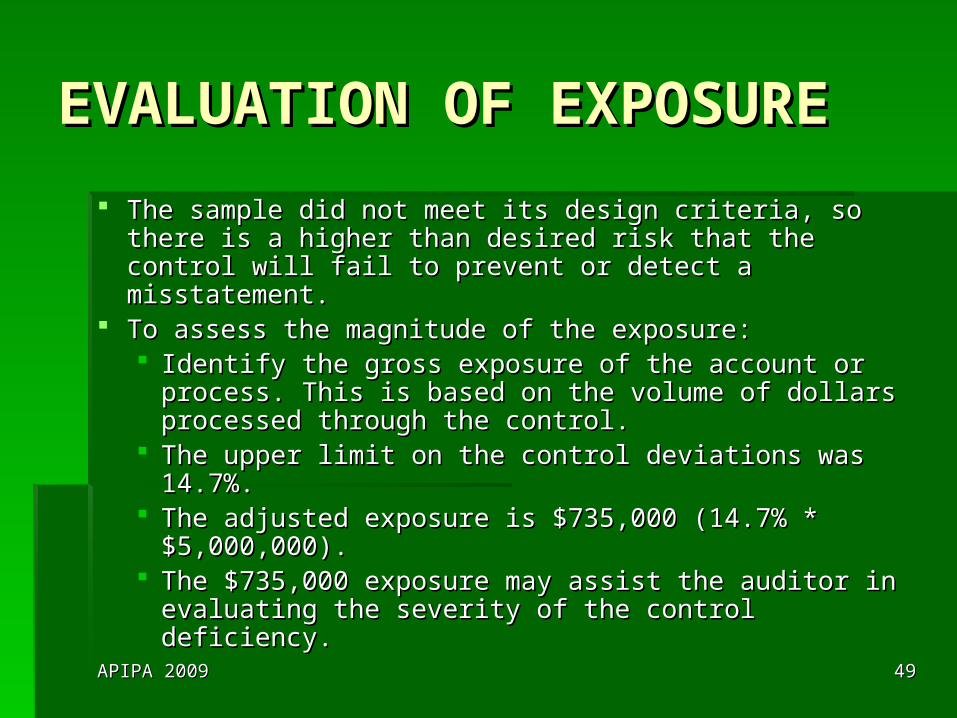

The sample did not meet its design criteria, so there is The sample did not meet its design criteria, so there is a higher than desired risk that the control will fail to a higher than desired risk that the control will fail to prevent or detect a misstatement.prevent or detect a misstatement.

To assess the magnitude of the exposure:To assess the magnitude of the exposure: Identify the gross exposure of the account or Identify the gross exposure of the account or

process. This is based on the volume of dollars process. This is based on the volume of dollars processed through the control.processed through the control.

The upper limit on the control deviations was 14.7%.The upper limit on the control deviations was 14.7%. The adjusted exposure is $735,000 (14.7% * The adjusted exposure is $735,000 (14.7% *

$5,000,000).$5,000,000). The $735,000 exposure may assist the auditor in The $735,000 exposure may assist the auditor in

evaluating the severity of the control deficiency.evaluating the severity of the control deficiency.

APIPA 2009APIPA 2009 5050

IN-CLASS EXERCISES IN-CLASS EXERCISES NO. 2 & NO. 3NO. 2 & NO. 3

APIPA 2009APIPA 2009 5151

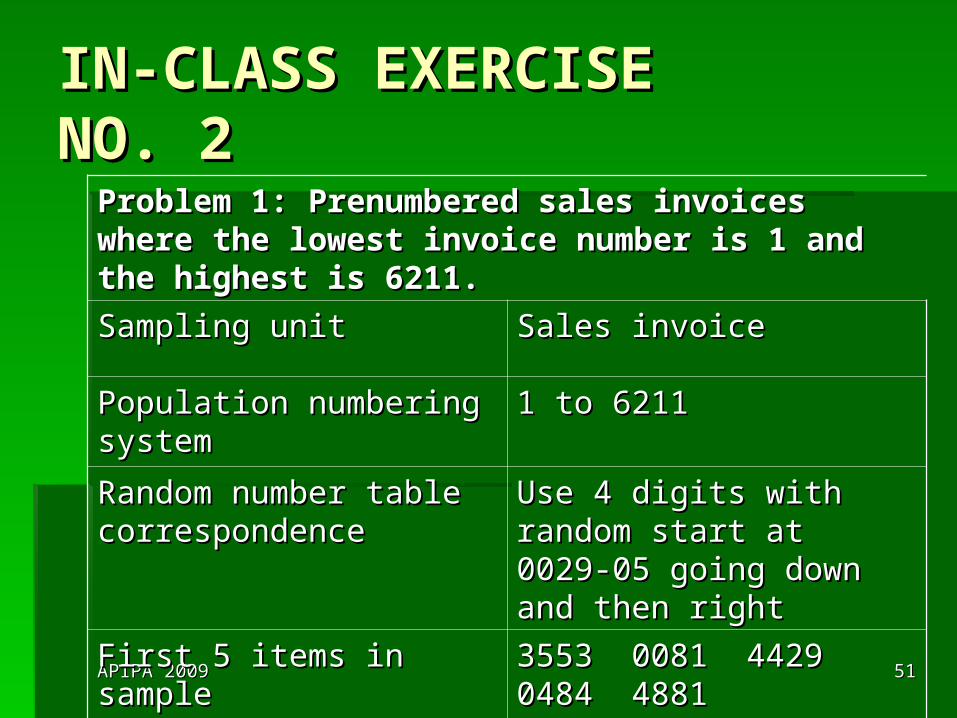

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 2NO. 2

Problem 1: Prenumbered sales invoices where the Problem 1: Prenumbered sales invoices where the lowest invoice number is 1 and the highest is 6211.lowest invoice number is 1 and the highest is 6211.

Sampling unitSampling unit Sales invoiceSales invoice

Population numbering Population numbering systemsystem

1 to 62111 to 6211

Random number table Random number table correspondencecorrespondence

Use 4 digits with random Use 4 digits with random start at 0029-05 going down start at 0029-05 going down and then rightand then right

First 5 items in sampleFirst 5 items in sample 3553 0081 4429 0484 3553 0081 4429 0484 48814881

APIPA 2009APIPA 2009 5252

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 2NO. 2

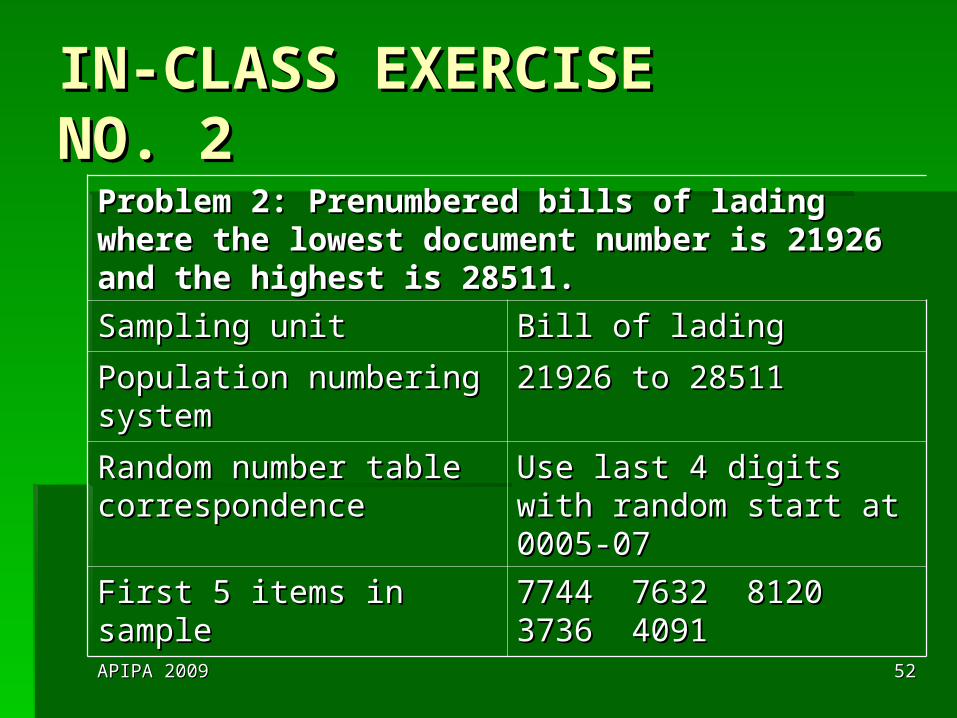

Problem 2: Prenumbered bills of lading where the Problem 2: Prenumbered bills of lading where the lowest document number is 21926 and the highest is lowest document number is 21926 and the highest is 28511.28511.

Sampling unitSampling unit Bill of ladingBill of lading

Population numbering Population numbering systemsystem

21926 to 2851121926 to 28511

Random number table Random number table correspondencecorrespondence

Use last 4 digits with Use last 4 digits with random start at 0005-07random start at 0005-07

First 5 items in sampleFirst 5 items in sample 7744 7632 8120 3736 7744 7632 8120 3736 40914091

APIPA 2009APIPA 2009 5353

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 2NO. 2

Problem 3: Accounts Receivable on 10 pages with 60 lines per Problem 3: Accounts Receivable on 10 pages with 60 lines per page except the last page, which has only 36 full lines. Each page except the last page, which has only 36 full lines. Each line has a customer name and an amount receivable.line has a customer name and an amount receivable.

Sampling unitSampling unit Each lineEach line

Population numbering Population numbering systemsystem

9 * 60 = 540 + 36 = 576 9 * 60 = 540 + 36 = 576 lineslines

Add 2000 (2001 to 2576)Add 2000 (2001 to 2576)

Random number table Random number table correspondencecorrespondence

Use last 4 digits with Use last 4 digits with random start at 00040-01 random start at 00040-01 going down and then rightgoing down and then right

First 5 items in sampleFirst 5 items in sample 2240 2055 2094 2087 2240 2055 2094 2087 26082608

APIPA 2009APIPA 2009 5454

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 2NO. 2

Problem 4: Prenumbered invoices in a sales journal where each month Problem 4: Prenumbered invoices in a sales journal where each month starts over with number 1. (Invoices for each month are designated by starts over with number 1. (Invoices for each month are designated by the month and document number.) There is a maximum of 20 pages the month and document number.) There is a maximum of 20 pages per month with a total of 185 pages for the year. All pages have 75 per month with a total of 185 pages for the year. All pages have 75 invoices except for the last page for each month.invoices except for the last page for each month.

Sampling unitSampling unit Page of invoicesPage of invoices

Population numbering systemPopulation numbering system Starting with January, first page is Starting with January, first page is 1 (up to 185)1 (up to 185)

Random number table Random number table correspondencecorrespondence

Random start at 0008-03 going Random start at 0008-03 going down then right, subtract random down then right, subtract random number from next 1000number from next 1000

First 5 items in sampleFirst 5 items in sample 4000 – 3982 = 18; 7000 – 6847 = 4000 – 3982 = 18; 7000 – 6847 = 153; 5000 - 4956 = 44; 6000 – 153; 5000 - 4956 = 44; 6000 – 5985 = 15; 5000 – 4941 = 595985 = 15; 5000 – 4941 = 59

APIPA 2009APIPA 2009 5555

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 3NO. 3

For which of these auditing procedures can For which of these auditing procedures can attribute sampling be conveniently used?attribute sampling be conveniently used?

11 NoNo

22 NoNo

33 NoNo

44 YesYes

5a5a YesYes

5b5b YesYes

APIPA 2009APIPA 2009 5656

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 3NO. 3

For which of these auditing procedures can For which of these auditing procedures can attribute sampling be conveniently used?attribute sampling be conveniently used?

5c5c YesYes

5d5d YesYes

5e5e YesYes

66 YesYes

APIPA 2009APIPA 2009 5757

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 3NO. 3

2. Considering the audit procedures to be 2. Considering the audit procedures to be performed, what is the most appropriate performed, what is the most appropriate sampling unit for conducting most of the audit sampling unit for conducting most of the audit sampling tests?sampling tests?

Sales invoiceSales invoice

APIPA 2009APIPA 2009 5858

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 3NO. 3

For each T of C or ST of T, identify the attribute For each T of C or ST of T, identify the attribute being tested and the exception condition.being tested and the exception condition.

AttributeAttribute Exception ConditionException Condition

4. Existence of the sales 4. Existence of the sales invoice number in the invoice number in the sales journalsales journal

No record of the sales No record of the sales invoice number in the invoice number in the sales journalsales journal

5a. Amount and other 5a. Amount and other data in MF agree with data in MF agree with the sales journal entrythe sales journal entry

The amount recorded in The amount recorded in the MF differs from the the MF differs from the amount recorded in the amount recorded in the sales journal.sales journal.

APIPA 2009APIPA 2009 5959

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 3NO. 3

For each T of C or ST of T, identify the attribute For each T of C or ST of T, identify the attribute being tested and the exception condition.being tested and the exception condition.

AttributeAttribute Exception ConditionException Condition

5b. Amount and other 5b. Amount and other data on the duplicate data on the duplicate sales invoice agree with sales invoice agree with the sales journal entrythe sales journal entry

Customer name and Customer name and account number on the account number on the invoice differ from the invoice differ from the information recorded in the information recorded in the sales journalsales journal

APIPA 2009APIPA 2009 6060

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 3NO. 3

For each T of C or ST of T, identify the attribute For each T of C or ST of T, identify the attribute being tested and the exception condition.being tested and the exception condition.

AttributeAttribute Exception ConditionException Condition

5b. Evidence that 5b. Evidence that pricing, extensions, and pricing, extensions, and footings are checked footings are checked (initials and correct (initials and correct amounts).amounts).

Lack of initials indicating Lack of initials indicating verification of pricing, verification of pricing, extensions, and footings.extensions, and footings.

APIPA 2009APIPA 2009 6161

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 3NO. 3

For each T of C or ST of T, identify the attribute For each T of C or ST of T, identify the attribute being tested and the exception condition.being tested and the exception condition.

AttributeAttribute Exception ConditionException Condition

5c. Quantity and other 5c. Quantity and other data on the bill of lading data on the bill of lading agree with the duplicate agree with the duplicate sales invoice and sales sales invoice and sales journaljournal

Quantity of goods shipped Quantity of goods shipped differs from quantity on differs from quantity on sales invoicesales invoice

APIPA 2009APIPA 2009 6262

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 3NO. 3

For each T of C or ST of T, identify the attribute For each T of C or ST of T, identify the attribute being tested and the exception condition.being tested and the exception condition.

AttributeAttribute Exception ConditionException Condition

5d. Quantity and other 5d. Quantity and other data on the sales order data on the sales order agree with the duplicate agree with the duplicate sales invoicesales invoice

Quantity on the sales Quantity on the sales order differs from quantity order differs from quantity on the duplicate sales on the duplicate sales invoiceinvoice

5e. Quantity and other 5e. Quantity and other data on the customer data on the customer order agree with the order agree with the duplicate sales invoiceduplicate sales invoice

Product number and Product number and description on the description on the customer order differ from customer order differ from information on the information on the duplicate sales invoiceduplicate sales invoice

APIPA 2009APIPA 2009 6363

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 3NO. 3

For each T of C or ST of T, identify the attribute For each T of C or ST of T, identify the attribute being tested and the exception condition.being tested and the exception condition.

AttributeAttribute Exception ConditionException Condition

5e. Credit is approved5e. Credit is approved Lack of initials indicating Lack of initials indicating credit approvalcredit approval

6. For recorded sales in 6. For recorded sales in the sales journal, the file the sales journal, the file of supporting documents of supporting documents includes a duplicate includes a duplicate sales invoice, BL, sales sales invoice, BL, sales order, and customer order, and customer order.order.

BL is not attached to the BL is not attached to the duplicate sales invoice duplicate sales invoice and the customer order.and the customer order.

APIPA 2009APIPA 2009 6464

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 3NO. 3

See Solution

APIPA 2009APIPA 2009 6565

STEPS IN NONSTATISTICAL STEPS IN NONSTATISTICAL ATTRIBUTE SAMPLING ATTRIBUTE SAMPLING APPLICATIONAPPLICATION

PlanningPlanning1.1. Determine the test objectivesDetermine the test objectives2.2. Define the population characteristicsDefine the population characteristics3.3. Determine the sample sizeDetermine the sample size

PerformancePerformance4.4. Select sample itemsSelect sample items5.5. Perform the auditing proceduresPerform the auditing procedures

EvaluationEvaluation6.6. Calculate the resultsCalculate the results7.7. Draw conclusionsDraw conclusions

APIPA 2009APIPA 2009 6666

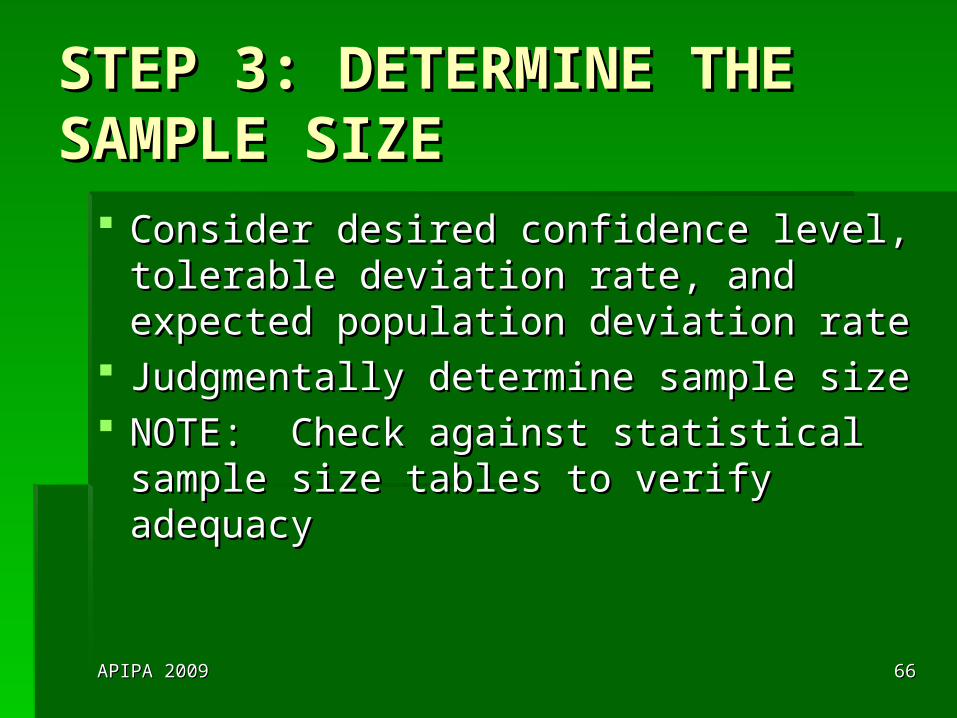

STEP 3: DETERMINE THE STEP 3: DETERMINE THE SAMPLE SIZESAMPLE SIZE

Consider desired confidence level, Consider desired confidence level, tolerable deviation rate, and expected tolerable deviation rate, and expected population deviation ratepopulation deviation rate

Judgmentally determine sample sizeJudgmentally determine sample size NOTE: Check against statistical sample NOTE: Check against statistical sample

size tables to verify adequacysize tables to verify adequacy

APIPA 2009APIPA 2009 6767

STEP 3: DETERMINE THE STEP 3: DETERMINE THE SAMPLE SIZESAMPLE SIZE

Guidelines for nonstatistical sample sizes for tests Guidelines for nonstatistical sample sizes for tests of controlsof controls

If any errors found, increase sample size or If any errors found, increase sample size or increase control riskincrease control risk

Desired level of controls relianceDesired level of controls reliance Sample sizeSample size

LowLow 15-2015-20

ModerateModerate 25-3525-35

HighHigh 40-6040-60

APIPA 2009APIPA 2009 6868

STEP 4: SELECT SAMPLE STEP 4: SELECT SAMPLE ITEMSITEMS

Random sampleRandom sample Systematic sample (with random start)Systematic sample (with random start) Haphazard selectionHaphazard selection

Still desire representative sampleStill desire representative sample Avoid unusual, large, first or lastAvoid unusual, large, first or last

APIPA 2009APIPA 2009 6969

STEP 6: CALCULATE THE STEP 6: CALCULATE THE RESULTSRESULTS

No computed upper deviation rateNo computed upper deviation rate If sample deviation rate > expected If sample deviation rate > expected

population deviation rate, control not population deviation rate, control not effectiveeffective

APIPA 2009APIPA 2009 7070

COMPLIANCE AUDITINGCOMPLIANCE AUDITING

Performance of auditing procedures to Performance of auditing procedures to determine whether an entity is complying with determine whether an entity is complying with specific requirements of laws, regulations, or specific requirements of laws, regulations, or agreementsagreements

Governmental entities and other recipients of Governmental entities and other recipients of governmental financial assistancegovernmental financial assistance Compliance with laws and regulations that materially Compliance with laws and regulations that materially

affect each major federal assistance programaffect each major federal assistance program

APIPA 2009APIPA 2009 7171

COMPLIANCE AUDITING OF COMPLIANCE AUDITING OF FEDERAL ASSISTANCE FEDERAL ASSISTANCE PROGRAMSPROGRAMS

Definition of population for testing of an Definition of population for testing of an internal control procedure that applies to internal control procedure that applies to more than one programmore than one program Define items from each major program as a Define items from each major program as a

separate population, ORseparate population, OR Define all items to which control is applicable Define all items to which control is applicable

as a single populationas a single population Second choice usually more efficientSecond choice usually more efficient

APIPA 2009APIPA 2009 7272

COMPLIANCE AUDITING - COMPLIANCE AUDITING - EXAMPLEEXAMPLE

Federal financial assistance for Island Federal financial assistance for Island CityCity Three major federal financial assistance Three major federal financial assistance

programsprograms Four nonmajor programsFour nonmajor programs

Control: Transaction review to ensure Control: Transaction review to ensure that only legally allowable costs are that only legally allowable costs are charged to each programcharged to each program

APIPA 2009APIPA 2009 7373

COMPLIANCE AUDITING - COMPLIANCE AUDITING - EXAMPLEEXAMPLE

More efficient to select one sample from More efficient to select one sample from population of all transactions (major and population of all transactions (major and nonmajor programs)nonmajor programs)

Confidence level = 95%Confidence level = 95% Tolerable deviation rate = 9%Tolerable deviation rate = 9% Expected population deviation rate = 1%Expected population deviation rate = 1% Sample size: 51Sample size: 51 1 allowable deviation1 allowable deviation

APIPA 2009APIPA 2009 7474

SMALL POPULATIONS AND SMALL POPULATIONS AND INFREQUENTLY OPERATING INFREQUENTLY OPERATING CONTROLSCONTROLS

Small Population Sample Size TableSmall Population Sample Size Table

Control Frequency and Control Frequency and Population SizePopulation Size

Sample SizeSample Size

Quarterly (4)Quarterly (4) 22

Monthly (12)Monthly (12) 2-42-4

Semimonthly (24)Semimonthly (24) 3-83-8

Weekly (52)Weekly (52) 5-95-9

APIPA 2009APIPA 2009 7575

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 4 NO. 4

APIPA 2009APIPA 2009 7676

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 4NO. 4

Selected Payroll T of CSelected Payroll T of C

1. Examine the time card 1. Examine the time card for approval of a for approval of a supervisorsupervisor

Moderately critical – Moderately critical – affects E/O of S& W affects E/O of S& W

2. Account for a 2. Account for a sequence of payroll sequence of payroll checks in the payroll checks in the payroll journaljournal

Very critical – affects E/O Very critical – affects E/O of S&Wof S&W

3. Recompute hours on 3. Recompute hours on the time cardthe time card

Moderately critical – Moderately critical – affects V of S&Waffects V of S&W

APIPA 2009APIPA 2009 7777

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 4NO. 4

4. Compare the 4. Compare the employee name in the employee name in the payroll journal to payroll journal to personnel recordspersonnel records

Very critical – affects Very critical – affects E/O - affects E/O of S& E/O - affects E/O of S& W; also an area subject W; also an area subject to fraud to fraud

5. Review OT charges 5. Review OT charges for approval of a for approval of a supervisorsupervisor

Moderately critical – Moderately critical – affects E/O and V of affects E/O and V of S&WS&W

APIPA 2009APIPA 2009 7878

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 4NO. 4

Selected Cash Disbursement T of CSelected Cash Disbursement T of C

6. Examine voucher for 6. Examine voucher for supporting invoices, supporting invoices, receiving reports, etc.receiving reports, etc.

Very critical – affects Very critical – affects E/O of purchase E/O of purchase transactionstransactions

7. Examine supporting 7. Examine supporting documents for evidence documents for evidence of cancellation (“paid”)of cancellation (“paid”)

Moderately critical – Moderately critical – affects validity of affects validity of purchase transactions purchase transactions and relates to double and relates to double paymentpayment

APIPA 2009APIPA 2009 7979

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 4NO. 4

Selected Cash Disbursement T of CSelected Cash Disbursement T of C

8. Ascertain whether 8. Ascertain whether cash discounts were cash discounts were takentaken

Least critical – affects V Least critical – affects V of purchase of purchase transactions; amounts transactions; amounts usually minorusually minor

9. Review voucher for 9. Review voucher for clerical accuracyclerical accuracy

Moderately critical – Moderately critical – affects V of purchase affects V of purchase transactionstransactions

APIPA 2009APIPA 2009 8080

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 4NO. 4

Selected Cash Disbursement T of CSelected Cash Disbursement T of C

10. Agree purchase 10. Agree purchase order price to invoiceorder price to invoice

Moderately critical – Moderately critical – affects V of purchase affects V of purchase transactionstransactions

APIPA 2009APIPA 2009 8181

MONETARY UNIT MONETARY UNIT SAMPLINGSAMPLING

Uses attribute sampling theory to express Uses attribute sampling theory to express conclusions in dollar amountsconclusions in dollar amounts Estimates the percentage of monetary units in a Estimates the percentage of monetary units in a

population that might be misstatedpopulation that might be misstated Multiples the percentage by an estimate of how Multiples the percentage by an estimate of how

much the dollars are misstatedmuch the dollars are misstated

Developed by auditorsDeveloped by auditors Assumes little or no misstatementsAssumes little or no misstatements Designed primarily to test for overstatementsDesigned primarily to test for overstatements

APIPA 2009APIPA 2009 8282

ADVANTAGESADVANTAGES

When no misstatements expected, When no misstatements expected, results in smaller (more efficient) sample results in smaller (more efficient) sample size than classical variables samplingsize than classical variables sampling

No need to compute/identify standard No need to compute/identify standard deviationdeviation

Automatically stratifies sampleAutomatically stratifies sample

APIPA 2009APIPA 2009 8383

DISADVANTAGESDISADVANTAGES

Zero or negative balances must be tested Zero or negative balances must be tested separatelyseparately

Assumes audited amount of sample Assumes audited amount of sample items is not in error by more than 100%items is not in error by more than 100%

When more than 1 or 2 misstatements When more than 1 or 2 misstatements found, allowance for sampling risk may found, allowance for sampling risk may be overstatedbe overstated Auditor more likely to reject balance and Auditor more likely to reject balance and

overauditoveraudit

APIPA 2009APIPA 2009 8484

STEPS IN MONETARY UNIT STEPS IN MONETARY UNIT SAMPLING APPLICATIONSAMPLING APPLICATION

PlanningPlanning1.1. Determine the test objectivesDetermine the test objectives2.2. Define the population characteristicsDefine the population characteristics3.3. Determine the sample sizeDetermine the sample size

PerformancePerformance4.4. Select sample itemsSelect sample items5.5. Perform the auditing proceduresPerform the auditing procedures

EvaluationEvaluation6.6. Calculate the resultsCalculate the results7.7. Draw conclusionsDraw conclusions

APIPA 2009APIPA 2009 8585

STEP 1: DETERMINE THE STEP 1: DETERMINE THE TEST OBJECTIVESTEST OBJECTIVES

Substantive testingSubstantive testing: To test the : To test the reasonableness of an amount, i.e., that reasonableness of an amount, i.e., that an amount is fairly statedan amount is fairly stated

To test the assertion that no material To test the assertion that no material misstatements exist in an account misstatements exist in an account balance, class of transactions, or balance, class of transactions, or disclosure component of the financial disclosure component of the financial statementsstatements

APIPA 2009APIPA 2009 8686

STEP 2: DEFINE THE STEP 2: DEFINE THE POPULATION POPULATION CHARACTERISTICSCHARACTERISTICS

Define the sampling populationDefine the sampling population Monetary value of an account balanceMonetary value of an account balance Verify completeness of populationVerify completeness of population

Define the sampling unit - Each individual Define the sampling unit - Each individual dollardollar

Define the logical unit - The account or Define the logical unit - The account or transaction that contains the sampling unitstransaction that contains the sampling units

Define a misstatement – The difference Define a misstatement – The difference between the book value and the audited valuebetween the book value and the audited value

APIPA 2009APIPA 2009 8787

STEP 3: DETERMINE THE STEP 3: DETERMINE THE SAMPLE SIZESAMPLE SIZE

Determine factors (effect on sample size)Determine factors (effect on sample size) Desired confidence level (direct)Desired confidence level (direct)

To increase confidence, more work is required! To increase confidence, more work is required! (larger sample size)(larger sample size)

Tolerable misstatement (inverse)Tolerable misstatement (inverse) Expected misstatement (direct)Expected misstatement (direct) Population size (direct)Population size (direct)

APIPA 2009APIPA 2009 8888

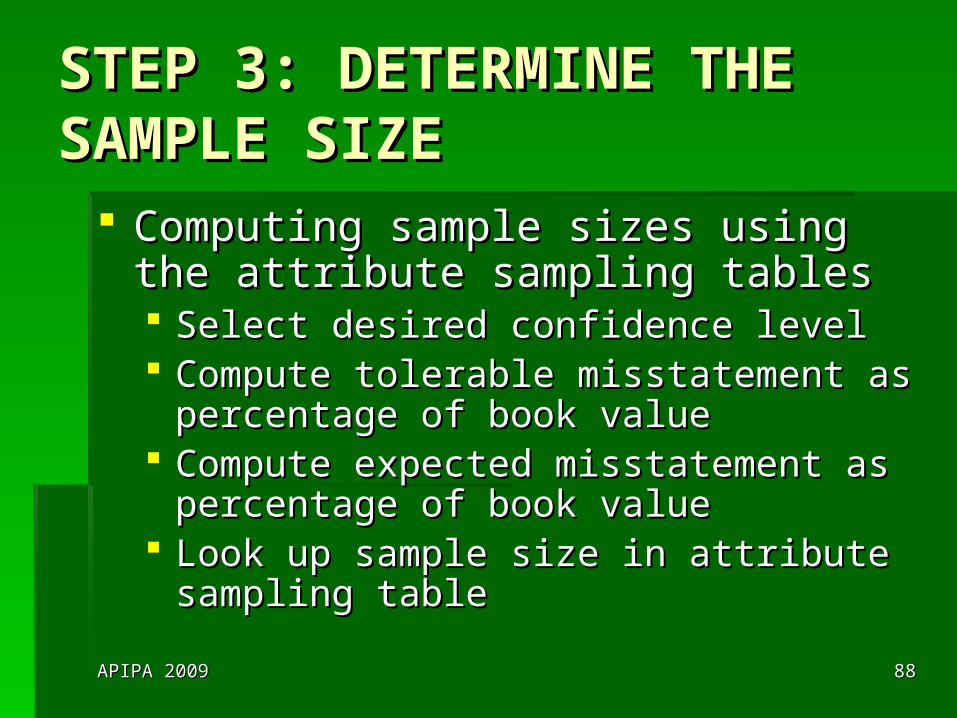

STEP 3: DETERMINE THE STEP 3: DETERMINE THE SAMPLE SIZESAMPLE SIZE

Computing sample sizes using the Computing sample sizes using the attribute sampling tablesattribute sampling tables Select desired confidence levelSelect desired confidence level Compute tolerable misstatement as Compute tolerable misstatement as

percentage of book valuepercentage of book value Compute expected misstatement as Compute expected misstatement as

percentage of book valuepercentage of book value Look up sample size in attribute sampling Look up sample size in attribute sampling

tabletable

APIPA 2009APIPA 2009 8989

STEP 4: SELECT THE STEP 4: SELECT THE SAMPLE ITEMSSAMPLE ITEMS

Systematic selection approach called Systematic selection approach called probability proportional to size (PPS)probability proportional to size (PPS)

Calculate sampling intervalCalculate sampling interval Book value / sample sizeBook value / sample size

From random start (within first interval), From random start (within first interval), select every nth dollarselect every nth dollar Logical unit included only once even if Logical unit included only once even if

includes more than one sample unitincludes more than one sample unit

APIPA 2009APIPA 2009 9090

STEP 5: PERFORM THE STEP 5: PERFORM THE AUDITING PROCEDURESAUDITING PROCEDURES

Conduct planned audit procedures on Conduct planned audit procedures on logical unitslogical units

What if?What if? Missing document – consider to be a Missing document – consider to be a

misstatementmisstatement

APIPA 2009APIPA 2009 9191

STEP 6: CALCULATE STEP 6: CALCULATE RESULTSRESULTS

Projected misstatement: Projection of Projected misstatement: Projection of the errors to the populationthe errors to the population

Upper limit on misstatement: Adds an Upper limit on misstatement: Adds an allowance for sampling risk to the allowance for sampling risk to the projected misstatementprojected misstatement

APIPA 2009APIPA 2009 9292

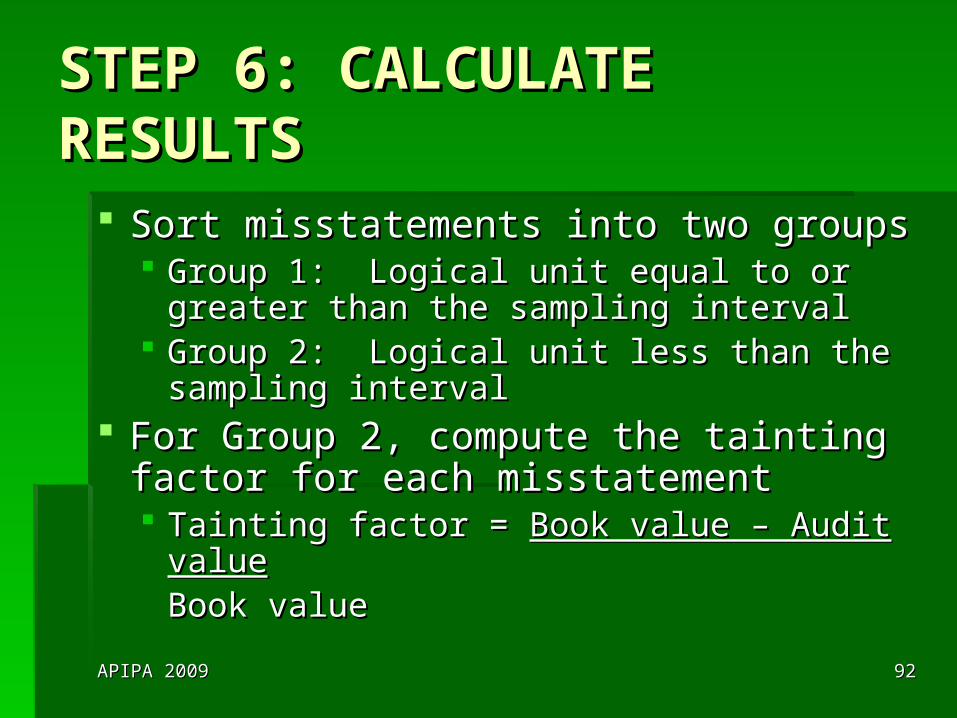

STEP 6: CALCULATE STEP 6: CALCULATE RESULTSRESULTS

Sort misstatements into two groupsSort misstatements into two groups Group 1: Logical unit equal to or greater Group 1: Logical unit equal to or greater

than the sampling intervalthan the sampling interval Group 2: Logical unit less than the sampling Group 2: Logical unit less than the sampling

intervalinterval For Group 2, compute the tainting factor For Group 2, compute the tainting factor

for each misstatementfor each misstatement Tainting factor = Tainting factor = Book value – Audit valueBook value – Audit value

Book valueBook value

APIPA 2009APIPA 2009 9393

STEP 6: CALCULATE STEP 6: CALCULATE RESULTSRESULTS

Place the Group 2 items in rank order by Place the Group 2 items in rank order by tainting factor (from largest to smallest)tainting factor (from largest to smallest)

Compute the projected misstatementCompute the projected misstatement Calculate the upper limit increments (using the Calculate the upper limit increments (using the

Monetary Unit Sampling – Confidence Monetary Unit Sampling – Confidence Factors for Sample EvaluationFactors for Sample Evaluation table)table)

Calculate upper misstatement for each Group 2 Calculate upper misstatement for each Group 2 itemitem

Add differences for Group 1Add differences for Group 1 Total = Upper misstatement limitTotal = Upper misstatement limit

APIPA 2009APIPA 2009 9494

STEP 6: CALCULATE STEP 6: CALCULATE RESULTS - EXAMPLERESULTS - EXAMPLE

Book value = $3,100,000Book value = $3,100,000 Tolerable misstatement = $150,000Tolerable misstatement = $150,000 Expected misstatement = $25,000Expected misstatement = $25,000 Desired confidence level = 95%Desired confidence level = 95% Tolerable misstatement rate = Tolerable misstatement rate =

4.8%,round to 5%4.8%,round to 5% Expected misstatement rate = .8%, round Expected misstatement rate = .8%, round

to 1%to 1%

APIPA 2009APIPA 2009 9595

STEP 6: CALCULATE STEP 6: CALCULATE RESULTS - EXAMPLERESULTS - EXAMPLE

Sample size = 93Sample size = 93 Sampling interval = $33,333Sampling interval = $33,333 Expected misstatement = $25,000Expected misstatement = $25,000

APIPA 2009APIPA 2009 9696

STEP 6: CALCULATE STEP 6: CALCULATE RESULTS - EXAMPLERESULTS - EXAMPLE

ItemItem Book ValueBook Value Audited ValueAudited Value DifferenceDifference

Item 1 12,000 3,120 8,880

Item 2 35,000 32,000 3,000

Item 3 1,400 0 1,400

Item 4 45,200 41,000 4,200

Item 5 740 555 185

APIPA 2009APIPA 2009 9797

STEP 6: CALCULATE STEP 6: CALCULATE RESULTS - EXAMPLERESULTS - EXAMPLE

ItemItem Book ValueBook Value Audited ValueAudited Value DifferenceDifference

Group 1: BV > SI (33,333)

Item 2 35,000 32,000 3,000

Item 4 45,200 41,000 4,200

7,200

APIPA 2009APIPA 2009 9898

STEP 6: CALCULATE STEP 6: CALCULATE RESULTS - EXAMPLERESULTS - EXAMPLE

ItemItem DifferenceDifference Book ValueBook Value Tainting Tainting FactorFactor

Group 2: BV < SI (33,333)

Item 1 8,880 12,000 .74

Item 3 1,400 1,400 1.0

Item 5 185 740 .25

APIPA 2009APIPA 2009 9999

STEP 6: CALCULATE STEP 6: CALCULATE RESULTS - EXAMPLERESULTS - EXAMPLE

ItemItem Tainting Tainting FactorFactor

Sampling Sampling IntervalInterval

Projected Projected Misstatement Misstatement

(Tainting (Tainting Factor * SI)Factor * SI)

Item 3 1.0 33,333 33,333

Item 1 .74 33,333 24,666

Item 5 .25 33,333 8,333

APIPA 2009APIPA 2009 100100

STEP 6: CALCULATE STEP 6: CALCULATE RESULTS - EXAMPLERESULTS - EXAMPLE

ItemItem Projected Projected MisstatementMisstatement

95% Upper 95% Upper Limit Limit

IncrementIncrement

Upper Upper MisstatementMisstatement

Item 3 33,333 3.0 99,999

Item 1 24,666 1.7 41,932

Item 5 8,333 1.5 12,500

154,431

APIPA 2009APIPA 2009 101101

STEP 6: CALCULATE STEP 6: CALCULATE RESULTS - EXAMPLERESULTS - EXAMPLE

ItemItem Projected Projected MisstatementMisstatement

95% Upper 95% Upper Limit Limit

IncrementIncrement

Upper Upper MisstatementMisstatement

Group 2 154,431

Group 1 7,200

Upper Misstatement Limit 161,631

APIPA 2009APIPA 2009 102102

STEP 7: DRAW STEP 7: DRAW CONCLUSIONSCONCLUSIONS

If Upper Misstatement Limit > Tolerable If Upper Misstatement Limit > Tolerable Misstatement, balance is materially Misstatement, balance is materially misstated.misstated.

If Upper Misstatement Limit If Upper Misstatement Limit >> Tolerable Tolerable Misstatement, balance is not materially Misstatement, balance is not materially misstatedmisstated

APIPA 2009APIPA 2009 103103

IN-CLASS EXERCISES IN-CLASS EXERCISES NO. 5 TO NO. 6NO. 5 TO NO. 6

APIPA 2009APIPA 2009 104104

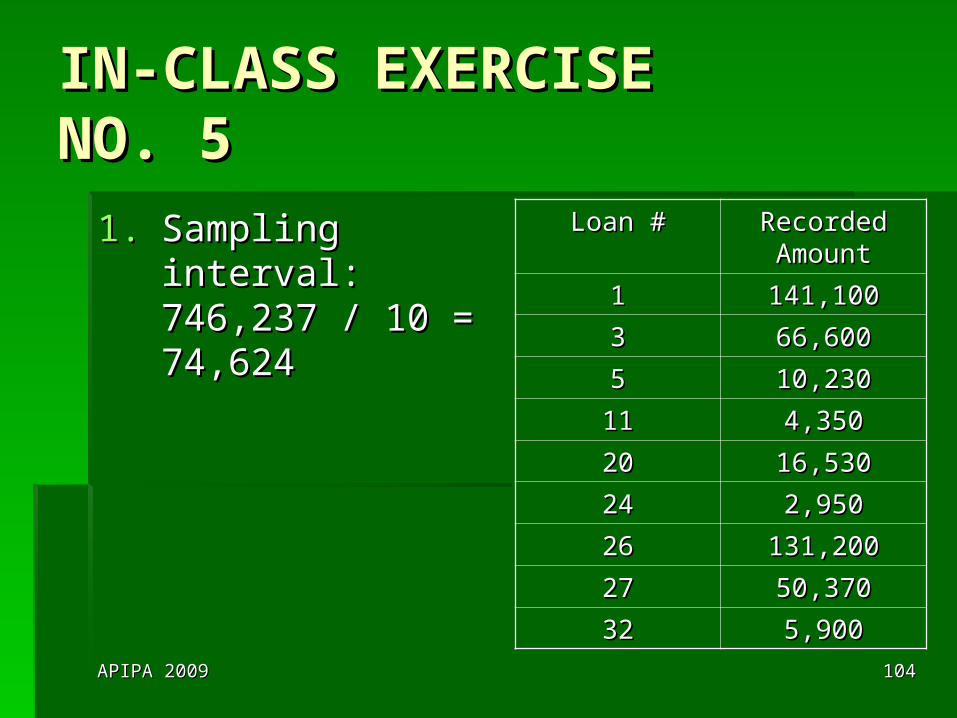

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 5NO. 5

1.1. Sampling interval: Sampling interval: 746,237 / 10 = 746,237 / 10 = 74,62474,624

Loan #Loan # Recorded Recorded AmountAmount

11 141,100141,100

33 66,60066,600

55 10,23010,230

1111 4,3504,350

2020 16,53016,530

2424 2,9502,950

2626 131,200131,200

2727 50,37050,370

3232 5,9005,900

APIPA 2009APIPA 2009 105105

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 5NO. 5

2.2. Sampling items always included:Sampling items always included:

The loans > the sampling intervalThe loans > the sampling interval

Loan #1 – 141,100Loan #1 – 141,100

Loan #26 – 131,200Loan #26 – 131,200

APIPA 2009APIPA 2009 106106

IN-CLASS EXERCISEIN-CLASS EXERCISENO. 6NO. 6

Recorded amount of accounts receivable = Recorded amount of accounts receivable = $400,000$400,000

Tolerable misstatement: $20,000; 20,000 / Tolerable misstatement: $20,000; 20,000 / 400,000 = 5%400,000 = 5%

Risk of incorrect acceptance: 5%Risk of incorrect acceptance: 5% Expected misstatements: 0Expected misstatements: 0

Sample size = 59Sample size = 59 Sampling interval = 400,000 / 59 = 6,780Sampling interval = 400,000 / 59 = 6,780

APIPA 2009APIPA 2009 107107

IN-CLASS EXERCISEIN-CLASS EXERCISENO. 6NO. 6

ErrorError Recorded Recorded AmountAmount

Audit Audit AmountAmount

DifferenceDifference Tainting Tainting %%

11 400400 320320 8080 20%20%

22 500500 00 500500 100%100%

33 7,0007,000 6,5006,500 500500 NANA

APIPA 2009APIPA 2009 108108

IN-CLASS EXERCISEIN-CLASS EXERCISENO. 6NO. 6

ErrorError Tainting Tainting %%

Sampling Sampling IntervalInterval

Projected Projected Misstate-Misstate-mentment

Upper Upper Limit Limit IncrementIncrement

Upper Upper Limit Limit Misstate-Misstate-mentment

Logical unit BV < Sampling IntervalLogical unit BV < Sampling Interval

22 100100 6,7806,780 6,7806,780 1.71.7 11,52611,526

11 2020 6,7806,780 1,3561,356 1.51.5 2,0342,034

APIPA 2009APIPA 2009 109109

IN-CLASS EXERCISEIN-CLASS EXERCISENO. 6NO. 6

ErrorError Tainting Tainting %%

Sampling Sampling IntervalInterval

Projected Projected Misstate-Misstate-mentment

Upper Upper Limit Limit IncrementIncrement

Upper Upper Limit Limit Misstate-Misstate-mentment

Logical unit BV > Sampling IntervalLogical unit BV > Sampling Interval

33 NANA NANA 500500 NANA 500500

Basic Precision: 3.0 * 6,780 = 20,340Basic Precision: 3.0 * 6,780 = 20,340

APIPA 2009APIPA 2009 110110

IN-CLASS EXERCISEIN-CLASS EXERCISENO. 6NO. 6

ErrorError Tainting Tainting %%

Sampling Sampling IntervalInterval

Projected Projected Misstate-Misstate-mentment

Upper Upper Limit Limit IncrementIncrement

Upper Upper Limit Limit Misstate-Misstate-mentment

Logical unit BV < Sampling IntervalLogical unit BV < Sampling Interval 13,56013,560

Logical unit BV > Sampling IntervalLogical unit BV > Sampling Interval 500500

Basic PrecisionBasic Precision 20,34020,340

Upper Misstatement LimitUpper Misstatement Limit 34,40034,400Conclusion: The account is materially misstated. The upper misstatement limit of 34,400 exceeds the tolerable misstatement of 20,000.

APIPA 2009APIPA 2009 111111

NONSTATISTICAL SAMPLING NONSTATISTICAL SAMPLING – BALANCE TESTING– BALANCE TESTING

Differences inDifferences in Identifying individually significant itemsIdentifying individually significant items Determining sample sizeDetermining sample size Selecting sample itemsSelecting sample items Calculating sample resultsCalculating sample results

APIPA 2009APIPA 2009 112112

IDENTIFYING INDIVIDUALLY IDENTIFYING INDIVIDUALLY SIGNIFICANT ITEMSSIGNIFICANT ITEMS

Selected due to large sizeSelected due to large size Tested 100%Tested 100% Results similar to PPS selectionResults similar to PPS selection For example, selecting all items > For example, selecting all items >

$100,000$100,000

APIPA 2009APIPA 2009 113113

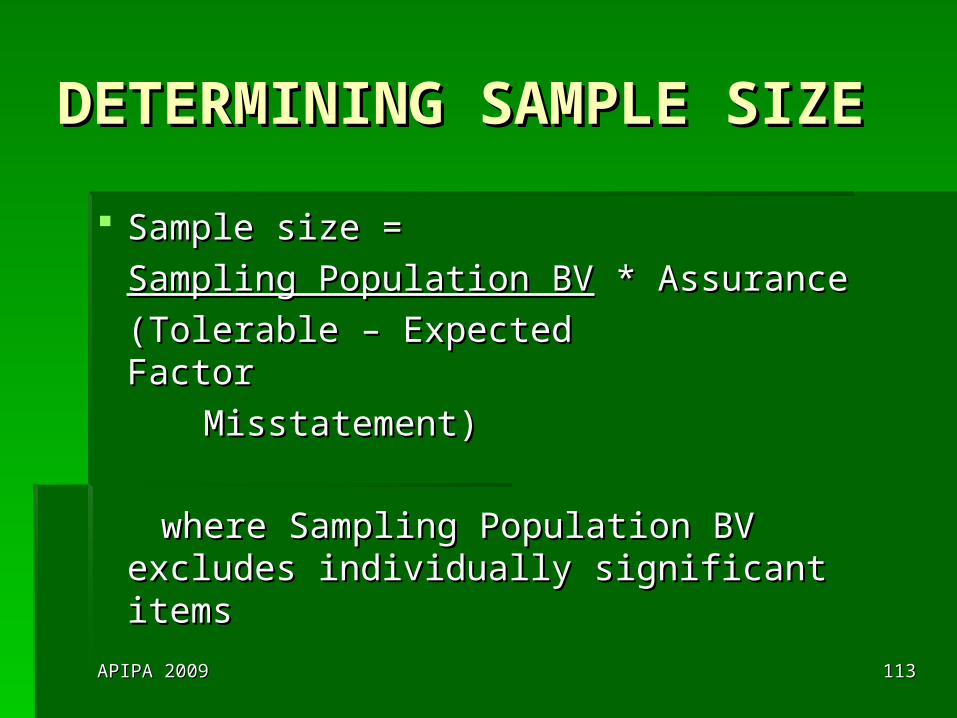

DETERMINING SAMPLE DETERMINING SAMPLE SIZESIZE

Sample size = Sample size =

Sampling Population BVSampling Population BV * Assurance * Assurance

(Tolerable – Expected Factor(Tolerable – Expected Factor

Misstatement)Misstatement)

where Sampling Population BV excludes where Sampling Population BV excludes individually significant itemsindividually significant items

APIPA 2009APIPA 2009 114114

DETERMINING SAMPLE DETERMINING SAMPLE SIZESIZE

Assessment Assessment of RMMof RMM

Desired Level of Confidence – Assurance FactorsDesired Level of Confidence – Assurance Factors

MaximumMaximum Slightly below Slightly below maximummaximum

ModerateModerate LowLow

MaximumMaximum 3.0 2.7 2.3 2.0Slightly below Slightly below maximummaximum

2.7 2.4 2.0 1.6

ModerateModerate 2.3 2.1 1.6 1.2LowLow 2.0 1.6 1.2 1.0

APIPA 2009APIPA 2009 115115

DETERMINING SAMPLE DETERMINING SAMPLE SIZE - EXAMPLESIZE - EXAMPLE

Book value = $3,100,000Book value = $3,100,000 Individually significant items = $1,500,000Individually significant items = $1,500,000 Tolerable misstatement = $150,000Tolerable misstatement = $150,000 Expected misstatement = $25,000Expected misstatement = $25,000 Desired confidence level = MaximumDesired confidence level = Maximum Risk of MM = MaximumRisk of MM = Maximum Sample size = Sample size = 1,600,0001,600,000 * 3.0 * 3.0

(150,000 – 25,000)(150,000 – 25,000) = 38.4, round to 39= 38.4, round to 39

APIPA 2009APIPA 2009 116116

SELECTING SAMPLE SELECTING SAMPLE ITEMSITEMS

Random selectionRandom selection Systematic selectionSystematic selection Haphazard selectionHaphazard selection

APIPA 2009APIPA 2009 117117

CALCULATING SAMPLE CALCULATING SAMPLE RESULTSRESULTS

Sample misstatement MUST be Sample misstatement MUST be projected to populationprojected to population

Two acceptable methodsTwo acceptable methods Apply sample misstatement ratio to Apply sample misstatement ratio to

population (ratio estimation)population (ratio estimation) Apply average misstatement $ of each item Apply average misstatement $ of each item

in sample to all items in population in sample to all items in population (difference estimation)(difference estimation)

APIPA 2009APIPA 2009 118118

CLASSICAL SAMPLINGCLASSICAL SAMPLING

Ratio estimationRatio estimation Difference estimationDifference estimation

APIPA 2009APIPA 2009 119119

RATIO ESTIMATIONRATIO ESTIMATION

Sample misstatements = $19,000Sample misstatements = $19,000 Sample book value = $175,000Sample book value = $175,000 Sample error rate = 10.9%, round to 11%Sample error rate = 10.9%, round to 11% Total population BV = $1,840,000Total population BV = $1,840,000 Projected misstatement = $1,840,000 * Projected misstatement = $1,840,000 *

11% = $202,40011% = $202,400 Compare projected misstatement to Compare projected misstatement to

tolerable misstatementtolerable misstatement

APIPA 2009APIPA 2009 120120

DIFFERENCE ESTIMATIONDIFFERENCE ESTIMATION

Sample misstatements = $19,000Sample misstatements = $19,000 # of sample items with misstatements = 5# of sample items with misstatements = 5 Average misstatement per sample item = Average misstatement per sample item =

$3,800$3,800 # items in population = 256# items in population = 256 Projected misstatement = $3,800 * 256 = Projected misstatement = $3,800 * 256 =

$972,800$972,800 Compare projected misstatement to tolerable Compare projected misstatement to tolerable

misstatementmisstatement

APIPA 2009APIPA 2009 121121

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 7NO. 7

APIPA 2009APIPA 2009 122122

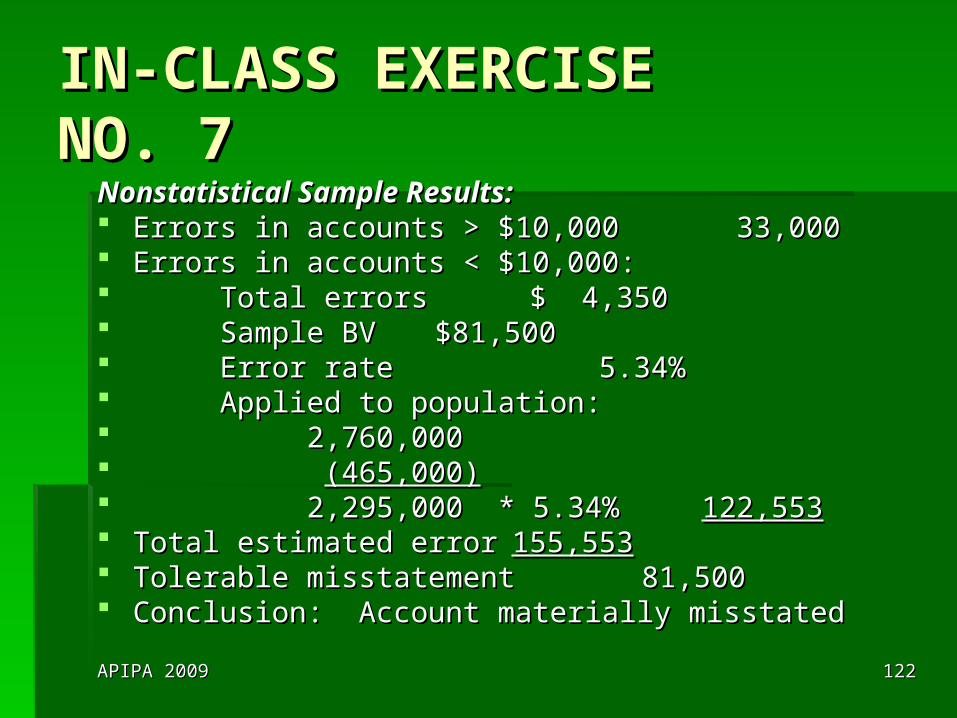

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 7NO. 7

Nonstatistical Sample Results:Nonstatistical Sample Results: Errors in accounts > $10,000Errors in accounts > $10,000 33,000 33,000 Errors in accounts < $10,000:Errors in accounts < $10,000: Total errorsTotal errors $ 4,350 $ 4,350 Sample BV Sample BV $81,500 $81,500 Error rate Error rate 5.34% 5.34% Applied to population:Applied to population: 2,760,0002,760,000 (465,000)(465,000) 2,295,000 * 5.34%2,295,000 * 5.34% 122,553122,553 Total estimated errorTotal estimated error 155,553155,553 Tolerable misstatementTolerable misstatement 81,500 81,500 Conclusion: Account materially misstatedConclusion: Account materially misstated

APIPA 2009APIPA 2009 123123

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 7 - PPSNO. 7 - PPS

PPS Sample Results:PPS Sample Results: Accounts receivable recorded Accounts receivable recorded

balance: balance: $2,760,000$2,760,000 Accounts > $10,000 (tested Accounts > $10,000 (tested

separately)separately) ( (465,000465,000)) Accounts receivable populationAccounts receivable population

– – PPSPPS $2,295,000$2,295,000 Tolerable misstatementTolerable misstatement $ 81,500$ 81,500

APIPA 2009APIPA 2009 124124

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 7 - PPSNO. 7 - PPS

Sample and sampling interval: Sample and sampling interval:

Tolerable rate: 81,500 / 2,295,000 = 3.55%, Tolerable rate: 81,500 / 2,295,000 = 3.55%, round to 4%round to 4%

Expected rate: 0Expected rate: 0

5% risk of overreliance (since IR and CR are 5% risk of overreliance (since IR and CR are both high)both high)

Sample size: 74Sample size: 74

Sampling interval: 2,295,000 / 74 = 31,014Sampling interval: 2,295,000 / 74 = 31,014

APIPA 2009APIPA 2009 125125

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 7 - PPSNO. 7 - PPS

RecordedValue

AuditedValue

Difference Tainting %

Item 12 5,120 4,820 300 5.85

Item 19 485 385 100 20.6

Item 33 1,250 250 1,000 80

Item 35 3,975 3,875 100 25.2

Item 51 1,850 1,825 25 1.4

Item 59 4,200 3,780 420 10

Item 74 2,405 0 2,405 100

APIPA 2009APIPA 2009 126126

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 7 - PPSNO. 7 - PPS

# of Overstatement Misstatements 5% Upper Limit Increment

0 3.00

1 4.75 1.75

2 6.30 1.55

3 7.76 1.46

4 9.16 1.40

5 10.52 1.36

6 11.85 1.33

7 13.15 1.30

APIPA 2009APIPA 2009 127127

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 7 - PPSNO. 7 - PPS

Tainting%

SamplingInterval

ProjectedMisstatement

Upper LimitFactor

UpperMisstatement

Item 74 100 31,014 31,014 1.75 54,275

Item 33 80 31,014 24,811 1.55 38,457

Item 35 25.2 31,014 7,816 1.46 11,411

Item 19 20.6 31,014 6,389 1.40 8,944

Item 59 10 31,014 3,101 1.36 4,218

Item 12 5.85 31,014 1,814 1.33 2,413

Item 51 1.4 31,014 434 1.30 564

120,282

APIPA 2009APIPA 2009 128128

IN-CLASS EXERCISE IN-CLASS EXERCISE NO. 7 - PPSNO. 7 - PPS

Items < Sampling Interval:Items < Sampling Interval: 120,282 120,282 Items > Sampling Interval: NoneItems > Sampling Interval: None Basic precision: 3.0 * 31,014 = Basic precision: 3.0 * 31,014 = 93,04293,042 Upper misstatement limit =Upper misstatement limit = 213,324213,324 Conclusion: Account is materially misstated. Conclusion: Account is materially misstated.

Upper misstatement limit 213,324 > tolerable Upper misstatement limit 213,324 > tolerable misstatement 81,500misstatement 81,500

APIPA 2009APIPA 2009 129129

RESOURCESRESOURCES

Audit Sampling: An Introduction, 3Audit Sampling: An Introduction, 3rdrd Edition, Guy, Carmichael & WhittingtonEdition, Guy, Carmichael & Whittington

Audit Guide: Audit Sampling, New Edition Audit Guide: Audit Sampling, New Edition as of May 1, 2008, AICPAas of May 1, 2008, AICPA

Auditing & Assurance Services, 6Auditing & Assurance Services, 6thth Edition, Messier, Glover, & PrawittEdition, Messier, Glover, & Prawitt

Auditing & Assurance Services, 12Auditing & Assurance Services, 12thth Edition, Arens, Elder & BeasleyEdition, Arens, Elder & Beasley

APIPA 2009APIPA 2009 130130

THE END!THE END!