anuja kumari. “the process of ensuring access to financial services and timely and adequate credit...

TRANSCRIPT

ANUJA KUMARI

“The process of ensuring access to financial services and timely and adequate credit where needed by vulnerable groups such as weaker sections and low income groups at an affordable cost” The Committee on Financial Inclusion

2008

FINANCIAL INCLUSION ENVISAGES

Providing Financial Facilities TO

Hitherto excluded /Disadvantaged group AT

Affordable Cost

Financial Services Include

Deposits

Credits

Ancillary Services Include: Remittances

Insurances

Face to Face Advice

For inclusive growth

A necessity for sustainable overall economic growth

Lift financial condition & standard of life of underprivileged

Empower un served & underserved sections of society

In developed economies, focus is on small population

In developing economies (India), focus is on excluded majority

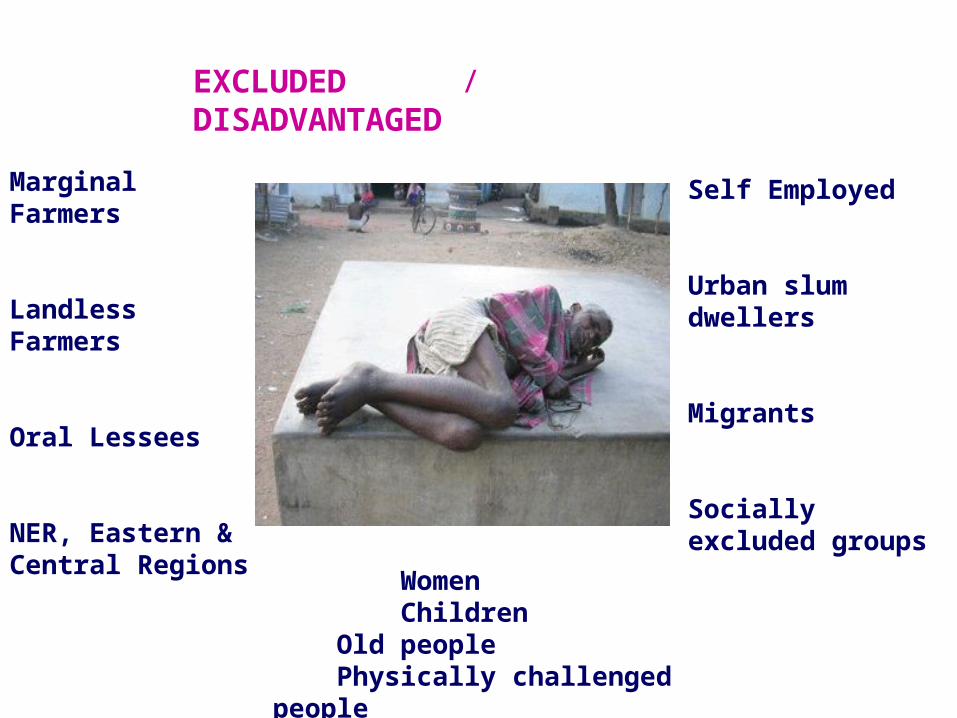

Marginal Farmers

Landless Farmers

Oral Lessees

NER, Eastern & Central Regions

Self Employed

Urban slum dwellers

Migrants

Socially excluded groups

Women Children

Old people Physically challenged people

EXCLUDED / DISADVANTAGED

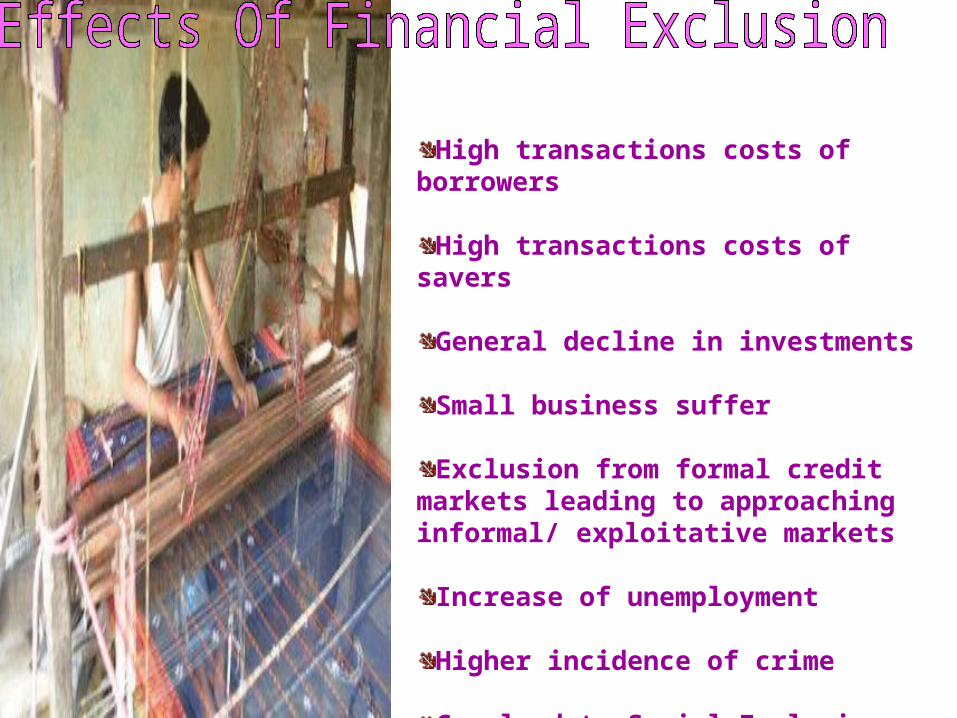

High transactions costs of borrowers

High transactions costs of savers

General decline in investments

Small business suffer

Exclusion from formal credit markets leading to approaching informal/ exploitative markets

Increase of unemployment

Higher incidence of crime

Can lead to Social Exclusion

Remote, hilly & sparsely populated areas with poor infrastructure and difficult physical accessLack of awareness, low income, social exclusion, illiteracy

Distance from bank branch, branch timings, Cumbersome Documentation /procedures.

unsuitable products Higher transaction cost

Ease of availability of informal credit

KYC – documentary proof of identity/ address

Rich have no compassion for poor

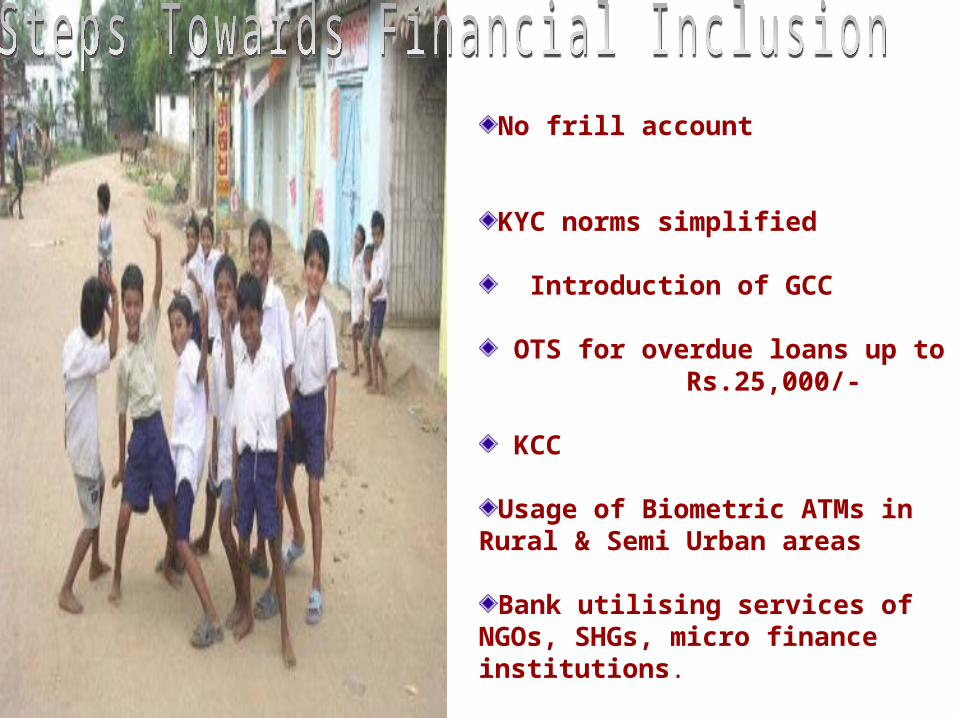

No frill account

KYC norms simplified

Introduction of GCC

OTS for overdue loans up to Rs.25,000/-

KCC

Usage of Biometric ATMs in Rural & Semi Urban areas

Bank utilising services of NGOs, SHGs, micro finance institutions.

Bank accounts – check in account

Immediate Credit

Savings product

Insurance – Healthcare

Mortgage

Financial advisory services

Entrepreneurial credit

Services of business facilitators/ correspondents (BC) for extending banking services

Credit Counselling & financial education

Multilingual website w.r.t. information on Banking

Banks to identify households with no bank accounts & to open at least one account per house

Revamping of RRBs and cooperative banks

Banks with insurance companies to provide, disability & health cover.

Target group for Financial Education

School /college children, women, rural/ urban poor, defence personnel, senior citizens

Funds for Financial inclusion

Micro Finance Development and Equity Fund

Financial Inclusion Fund for Development and Promotional Interventions

Financial Inclusion Technology Fund to meet cost of technology

Geographical coverage

5.2% villages have Bank branch

Farmers coverage-

Out of 119 million farmers, small and marginal farmers are 97.7 million (82.1 %)

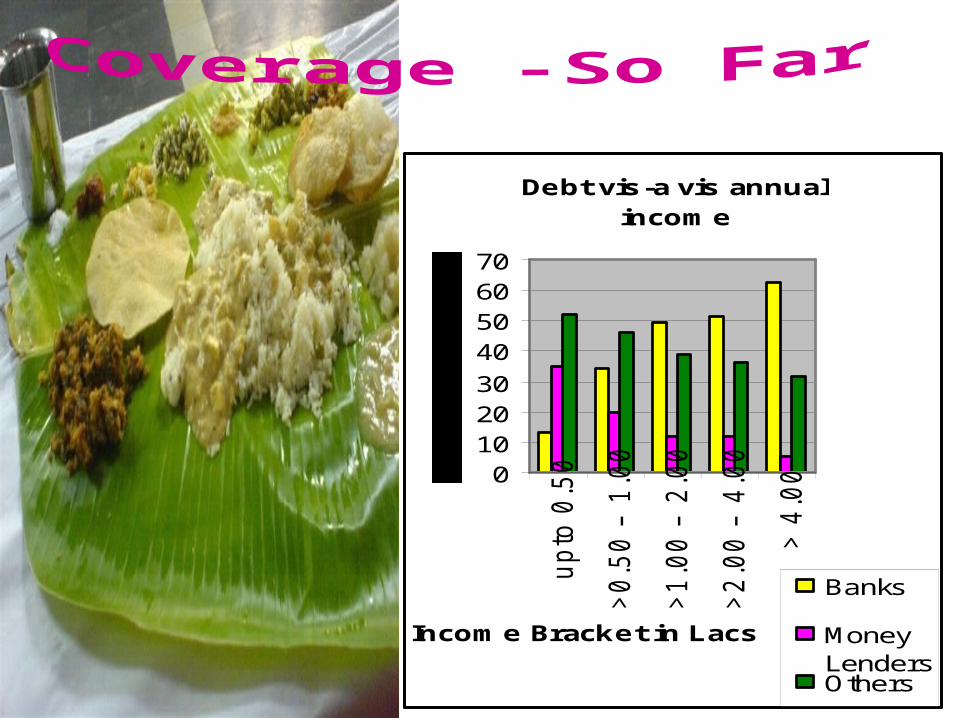

Debt vis-a vis annual income

0102030

40506070

upto

0.5

0

>0.5

0 –

1.0

0

>1.0

0 –

2.0

0

>2.0

0 –

4.0

0

> 4

.00

Income Bracket in Lacs

Banks

MoneyLendersOthers

Scaling up of activities

Transaction cost too high

Appropriate business model yet to evolve

BC model too restrictive

Limitation of cash delivery point

Lack of Interest / Involvement of Big Technology Players

The union budget 2009-10, has underlined the need to strengthen the mechanisms for inclusive growth for creating about 12 million new work opportunities per year, reduce the proportion of people living below poverty line to less than half from current levels by 2014 and to ease the delivery mechanism for primary health care facilities with a view to improve the preventive and curative health care in the country

Appropriate Technology

Appropriate and Efficient Delivery model

Mainstream Banks’ determination and involvement

Strong Collaboration among Banks

Technical Service Provider, BC Services

Involvement of all

Liberalisation of BC model

Banking services to every village with a population of over 2000 at least once a week on regular basis by March 2011

State Govts to ensure development of Infrastructure where penetration by the formal banking system is required

Generate awareness of the various banking policies and regulations relating to the common person

Expedite use of IT solutions for various financial products like NREGA