annual report 2014 · 2019-03-13 · koç group [s turnover omprises 8% of turkeys total gdp, and...

TRANSCRIPT

Annual Report 2014

1

Table of Contents

Section I : Independent Audit Report on the Annual Report 2 General Information 4 Yapı Kredi Faktoring in Brief 5 Chairman’s Letter 6 Board of Directors, Senior Management and Company Organization 7 Provided Financial Rights and R&D 8 Company Activities and Important Developments Regarding Activities 9-11 Future Outlook 11 Audit Information, Lawsuits, Subsidiaries and Affiliates, General Assembly Meetings 12 Yapı Kredi Bank 13 Financial Highlights 14 Dividend Distribution Policy, Risks and Risk Assessment Report of the Board of Directors, Miscellaneous 15 Affiliated Company Report 16

Section II : Financial tables as of 31 December 2014 and independent audit report 17-70

2

3

Section I

Introduction

4

General Information Company Title : Yapı Kredi Faktoring A.Ş. Annual Report Period : 01/01/2014 – 31/12/2014 Trade Registry Number : 417822 Mersis Number : 8638636782157842 Capital : 31,916,695 TL Address : Büyükdere Caddesi Yapı Kredi Plaza A Blok Kat:14 Levent, İstanbul /

Türkiye Phone / Fax Number : 212 371 99 99 / 212 371 99 00 Website : www.yapikredifaktoring.com.tr Number of Employees : 114 Branches : There are 10 branches: Adana, Ankara, Antalya, Beyoğlu, Bursa, Eminönü,

Güneşli, İzmir, Kadıköy, Kartal.

Adana Branch Reşatbey Mahallesi Atatürk Caddesi A Blok No:18/1 Kat:7 Semih Rüstem İş Merkezi Seyhan / Adana Phone : (0322) 459 04 91 Ankara Branch Atatürk Bulvarı No: 93 Kat: 5 Kızılay - Ankara Phone: (0312) 435 93 36 Antalya Branch Kızıltoprak Mahallesi Aspendos Bulvarı YKB Şubesi No:35 Antalya Phone: (0242) 312 75 40

Bursa Branch Ulubatlı Hasan Bulvarı No: 59 Osmangazi - Bursa Phone: (0224) 271 41 15

İzmir Branch Gazi Bulvarı No: 3 Egehan Kat: 4 Pasaport - İzmir Phone: (0232) 441 20 71

Shareholder Structure

Shareholders Share Ratio Amount (TL)

Yapı ve Kredi Bankası A.Ş. % 99,95 31.901.499

Temel Ticaret ve Yatırım A.Ş. % 0,04 11.393

Yapı Kredi Finansal Kiralama A.O. % 0,01 3.799

Koç Yapı Malzemeleri A.Ş. % 0,00 2

Zer Madencilik ve Dayanıklı Mallar

Yatırım Pazarlama A.Ş. % 0,00 2

%100,0 31.916.695

Beyoğlu Branch İnönü Mah. Cumhuriyet Cad. No:67A Kat:2 Şişli / İstanbul Phone: (0212) 232 77 94

Eminönü Branch Aşirefendi Cad.No:31 Sultanhamam / Eminönü İstanbul Phone: (0212) 514 36 73

Güneşli Branch Osmaniye Mah. Marmara Forum Alışveriş Merkezi B Blok (Marmara Forum Garden Office) 3.Kat No:OF-40 Bakırköy İstanbul Phone: (0212) 422 02 42

Kadıköy Branch Kozyatağı Mah.Ş.Mehmet Fatih Öngül Sok.No:1 Kat:4 Kadıköy İstanbul Phone: (0216) 362 37 30

Kartal Branch Mustafa Kemal Caddesi Şehit Gazi Sok.Adalet Sarayı arkası Hukukçular Towers - A BLok Kat : 17 Kartal İstanbul Phone: (0216) 510 60 46

5

Yapı Kredi Faktoring in Brief

Yapı Kredi Faktoring, has been the leader in the sector for the past 14 years based on the total turnover criterion. As Turkey’s leading and innovative factoring company, Yapı Kredi Faktoring boasts a solid position in the market through its strong performance, well-established structure and high quality service mentality. As the leader of the Turkish factoring market, Yapı Kredi Faktoring has 16.86% market share in total transaction volume and 14.76% in export factoring. Yapı Kredi Faktoring provides nation-wide factoring services through its Istanbul Head Office and branches located Adana, Ankara, Antalya, Beyoğlu, Bursa, Eminönü, Güneşli, İzmir, Kadıköy and Kartal. Yapı Kredi Bank and notably the synergy created by the close relationship with the bank’s nation-wide sales and services organization constitutes one of the most important service and competition advantages of Yapı Kredi Faktoring. The service points of Yapı Kredi Bank with its more than 1000 branches provide a comprehensive reach. Yapı Kredi Faktoring is a member of Factors Chain International (FCI), whose headquarters is located in Amsterdam, and also a member of the Association of Financial Institutions. Yapı Kredi Faktoring has been among the leading companies in the Best Export Factoring Companies ranking prepared globally by the FCI since 2002. In 2014, the Company service quality was considered to be ‘‘perfect’’ and the company was 2. in the ranking. Relying on its strong position in both the domestic and international markets, Yapı Kredi Faktoring displays superior activity performance through its correctly defined strategies, provides sustainable quality in factoring services via its competent and experiences team and produces strategic solutions that are specific to its customer portfolio. Thanks to its strong capital structure, extensive experience, proven service quality and expert human resources, Yapı Kredi Faktoring has been the number 1 company in the sector based on its total factoring turnover for the past 14 years.

6

Chairman’s Letter

As the uninterrupted leader of the sector with its total volume of transaction since 2001, Yapı Kredi Faktoring also

maintained its leadership in 2014.

Esteemed Shareholders, 2014 has been a year that confirmed the downward trend in global growth. Developed nations other than the United States faced a significant growth problem. On the other hand, the opinion that it would also be difficult for emerging markets to catch up with the growth rates of previous years became more widespread. This perception was further confirmed with the sharp fall in oil prices towards the end of the year and it is unlikely that it will change any time soon. This led to a sharp differentiation between oil importing and oil exporting countries among developing markets and brought along significant potential in favour of the first group, of which Turkey is a part. After failing to reach its desired results in 2014, Turkey started 2015 with fresh hope with the effect of the sharp fall in oil prices. Positioned as the country to derive the most benefit from the fall in oil prices, Turkey has not yet been able to reflect this positive situation on to asset prices and its real economy. Despite the tough competition conditions prevailing in financial markets, Yapı Kredi Faktoring has not compromised its superior customer-oriented service mentality and continued to successfully implement its healthy growth strategy in 2014 as well. Yapı Kredi Faktoring realized 15 per cent of the transaction volume in total export factoring of the sector in 2014 and maintained its uninterrupted leadership since 2001 with 16.86% market share. Of the total transaction volume, which reached 19.6 billion liras with 26 per cent increase, 85 per cent came from domestic factoring transactions and 15 per cent from international factoring transactions. With revenues attaining 161 million TL in 2014, Yapı Kredi Faktoring continued to benefit from the nationwide branch network of Yapı Kredi as it pursued its activities. Producing customer and market-oriented functional solutions and designing products that are customized according to needs in a quick fashion and at high quality standards lie at the heart of Yapı Kredi Faktoring’s service approach. While representing Yapı Kredi Faktoring’s corporate culture in the best manner, this approach also supports its growth and progress in all business processes. Moreover, included among the ‘‘Best Export Factoring Companies’’ in the world by Factors Chain International (FCI) since 2002, Yapı Kredi Faktoring took the 2. place in this ranking in 2014. Yapı Kredi Faktoring has also been awarded the global distinction of having ‘‘perfect service quality’’ by the FCI. Having assumed such an important mission as expanding the market by means of encouraging the dissemination of factoring transactions across the country and in all segments, Yapı Kredi Faktoring continues to make significant progress in terms of grassroots dissemination through its strong capital structure, its reputation in the sector and its comprehensive funding capabilities. At Yapı Kredi Faktoring, our prime responsibility for 2015 is to maintain our leadership by delivering an exemplary activity performance and to set the example for the sector as the first choice of customers via the comprehensive financial services that we offer. As we move forward with our healthy growth strategy, I would like to extend my gratitude to our customers for their unyielding confidence in us, to our shareholders for their continuous support and to our employees, who have a great share in this success, for their diligent efforts. Faik Açıkalın Chairman of the Board

7

Board of Directors, Senior Management and Company Organization

Board of Directors Internal Control Nilay Özbir

Internal Audit Pınar Adıyaman Demirtaş

General Manager

M. Coşkun Bulak

Credit Underwriting and Risk Monitoring

Atilla Kurban

Product Development and Monitoring Can Özyurt

Sales Işıl Eskici

Financial Planning and Financial Affairs

Zeynep Emecen Kandemir

Treasury and Foreign Relations S. Suhan Kaptan

Operations, IT and Administrative Affairs

Rengin Altınok

Board of Directors Faik Açıkalın Chairman Carlo Vivaldi Vice - Chairman Feza Tan Member Marco Iannaccone Member Nurgün Eyüboğlu Member M. Coşkun Bulak Member (General Manager)

Senior Management M.Coşkun Bulak General Manager Atilla Kurban Assistant General Manager - Credit Underwriting and Risk Monitoring Işıl Eskici Assistant General Manager - Sales Rengin Altınok Assistant General Manager - Operations, IT and Administrative Affairs Can Özyurt Vice President - Product Development and Monitoring S. Suhan Kaptan Vice President - Treasury and Foreign Relations Zeynep Emecen Kandemir Vice President - Financial Planning and Administration

8

Financial Rights Provided to Members of the Board and Senior Executives

The total amount of benefits such as per diems, fees, premiums, bonuses and dividends offered to Members of the Board and Senior Executives is 2,148,527 TL. The total amount of allowances, travel, accommodation and representation expenses as well as in-kind and in-cash means, insurance and similar indemnities paid to Members of the Board and Senior Executives is 268,878 TL.

Company Research and Development Activities The Company conducts research and marketing activities in order to widen its customer base and to develop its existing customer portfolio.

9

Company Activities and Important Developments Regarding Activities

Sales At Yapı Kredi Faktoring, our aim is to sustain the strong and reliable presence of our company with an increasing volume by means of establishing a sustainable and growing relationship with our customers. The Sales Department of Yapı Kredi Faktoring actively serves both domestic and international markets with the diversified range of products it offers to its customers. Yapı Kredi Faktoring achieved a total factoring turnover of 19,6 billion TL in 2014, 15% of which came from international transactions with the remaining 85% consisting of domestic transactions. As the leader of the sector based on the criterion of total turnover generated within the total sector for 14 consecutive years, Yapı Kredi Faktoring achieved a market share of 16,86% in 2014. Moreover, while Yapı Kredi Faktoring has been among the ‘‘Best Export Factoring Companies’’ selected by Factors Chain International (FCI) since 2002, in 2014 it ranked the second among FCI members world wide and its service quality was deemed to be perfect. Yapı Kredi Faktoring closely follows the developments in the market and the sector. The company added 1.556 new customers to its portfolio in 2014. Yapı Kredi Faktoring offers its services under four segments, namely Corporate, Commercial, SME and Supplier Group (suppliers and key industries), and through 10 branches. While the company achieved progress in 2014 in terms of the number of transactions and active customers through the services it offers in all segments and sectors, the increasing trend is expected to continue in 2015. Efficiency is expected to increase through new system investments to be made in 2015. More than 1000 Yapı Kredi Bank branches across the country constitute the most important distribution channel of the company in addition to its own sales organization. The company aims to continue serving and focusing on its potential and current customers in all segments and products through its ever-growing synergy with Yapı Kredi.

Credit Underwriting and Risk Monitoring Yapı Kredi Faktoring manages its credit risk with an emphasis on ‘effective risk management’ within the framework of its principal field of activity and supports sales activities with a view to fulfilling the company’s common goals. Special care is paid to avoiding high risk transactions that can tarnish the company’s reputation. Credit limits are determined by taking into account the financial structure and activity cycle of the customer and based on a payment schedule that is structured in advance in compliance with the customer’s commercial need. Risk policies that are in compliance with Yapı Kredi group are followed in monitoring and managing credit risk. In 2014, the number of employees working in credit underwriting, risk monitoring and intelligence units was increased, all relevant procedures were updated, the scope of audit processes and reporting activities was expanded and significant improvements were achieved in order to manage credit risk more effectively. Risk related reports are produced at regular intervals and the information is shared with the senior management as well as the Board of Directors. A total of 5,284 ‘credit underwriting proposals’ were evaluated and credit underwriting opinions were provided in 2014. While the non-performing credit ratio was 2.8% as of the end of 2014, it continued to be lower than the factoring sector average of 4.3% (according to BRSA data).

10

Product Development and Monitoring The Product Development and Monitoring Department assists the formulation of marketing strategies to gain new customers and to build long-term customer relations and ensures effective communication with Yapı Kredi Bank, which is the main shareholder. In addition, cooperation opportunities are developed in order for Yapı Kredi Faktoring to reach much wider customer masses by relying on the synergy created with Yapı Kredi Bank. Contributing to sustainable growth by means of developing solutions that are suitable for customer needs and closely monitoring and reporting on the progress in customer performance is also among the principal fields of work of this department. The department is also in charge of the Company’s Corporate Communication activities such as media, advertisement-promotion, meeting and seminar organization.

Treasury and Foreign Relations Funding activities are carried out by the Treasury and Foreign Relations Department. The objective of the Treasury Department is to meet the needs of customers without exposing them to the risks in the market. The general strategy of the Treasury Department is to effectively manage the Company’s asset and liability structure by protecting it from interest rate, liquidity and foreign exchange risks. Yapı Kredi Faktoring’s reputation vis-à-vis credit institutions and foreign factoring companies has always been at a very high level. Therefore, the Company boasts a wide portfolio of banks and credit opportunities.

Financial Planning and Administration The Financial Planning and Administration Department measures the Company’s performance on the basis of revenue, profitability and turnover in order to ensure that the Company reaches the corporate performance targets and to monitor these targets by taking into account the interest rate risk, market risk and operational risks. The Department secures compliance with BRSA regulations and the principles, policies and procedures of UFRS and the group and ensures that the accounting systems are also structured in harmony with these regulations. Moreover, it supports the Company’s strategic targets by means of carrying out assessments pertaining to the Company’s financial situation and providing relevant data in order to facilitate the decision-making process within the Company.

11

Operations, IT and Administrative Affairs

The administration, which previously functioned under the Financial Affairs Administration, was restructured in 2014 in the form of Operation, Information Technologies and Administrative Affairs administration to serve under a separate Deputy General Manager from an organizational point of view. In order to support the Company’s strategic growth and sales activities, minimize operational risk and to structure the appropriate services and the accompanying projects within the diverse product portfolio to work with the 10 branches and the growing number of active customers, it fulfils the following functions and organized its 2014 activities within this framework.

Managing and realizing the operational functioning of the organization (customer services, operational risk,

administrative activities within and outside the organization),

Formulating changes in practical rules and controls to ensure efficiency in the workings of Headquarters

Departments and Branches,

Minimizing Operational Risk related losses and taking action with regard to preventive measures,

Managing both system-related and infrastructure requirements through Information Technologies Management

and determining IT development requirements to the Company’s risk, service and sales related activities,

Creating project plans for 2015 in conjunction with relevant departments in line with the Company’s growth

targets and structuring projects.

The number of employees was increased in order to be able to fulfil these activities. As of 2014, the department serves with 21 staff members on the Operation side and 3 on the Information Technologies Management side. The department conducts all of its activities by means of carrying the ‘Customer-oriented operational service’ mentality onto operations. The investments to be made in the system in 2015 have been determined and work is on-going in line with the priorities that reflect the company’s growth strategy.

Internal Control and Internal Audit The Internal Control and Internal Audit departments strive to ensure the efficiency of the Internal Control System within the company by carrying out continuous controls on the company’s activities and operations with a view to determine and assess risks. Their independence within the organization has been ensured by rendering them answerable to the Board of Directors. The Internal Control and Internal Audit departments notify the Board of Directors of the findings they obtain as a result of their activities and matters of significance four times a year via the Audit Committee. The Audit Committee is assigned to responsible for monitoring the efficiency and adequacy of internal systems on behalf of the Board of Directors and ensuring that audit activities are sustained in a consolidated fashion. Moreover, the Internal Audit staff members have the responsibility of assessing the compliance of the activities conducted by the company within the framework of compliance controls with the legal responsibilities stipulated in the regulations published by the Banking Regulation and Supervision Agency and the Financial Crimes Investigation Board.

Future Outlook “Maintaining Leadership”

Yapı Kredi Faktoring successfully fulfilled one of its most important objectives in 2014 by becoming the sector leader. With its strong financial structure, high level of reliability and vast financing opportunities, Yapı Kredi Faktoring aims to sustain its leader position in the market with its long tradition of customer-oriented service approach. Yapı Kredi Faktoring's objective is to maintain sustainable development by means of widening its customer base as much as possible through the growing cooperation opportunities stemming from Yapı Kredi Bank and UniCredit network.

12

Audits by Regulatory Bodies and Independent Auditor

Yapı Kredi Faktoring is audited by an independent audit firm on a quarterly basis. In 2014, no public audit was made in the Company.

Lawsuits Filed against the Company

There is no lawsuit filed against the Company that may affect its financial status or operations.

Affiliates and Subsidiaries

The Company maintained its shares in Yapı Kredi Emeklilik in 2014.

Shares Amount (TL) Yapı Kredi Emeklilik A.Ş. 0.04% 26,593

26,593

In 2014, Yapı Kredi Faktoring donated TL 200,000 to Vehbi Koç Foundation, and TL 1,860 to Turkish Education Foundation, amounting to TL 201,860 in donations.

Extraordinary Assembly of Shareholders within the Period

Pursuant to Article 8 of the Articles of Association and Article 505 of Turkish Commercial Code, on 4 December 2014, the Extraordinary General Assembly has granted, with majority vote, to the Board of Directors the authority to issue debt instruments up to the maximum limit allowed in relevant regulations in accordance with the provisions of TCC and other regulations, and to determine the terms and conditions for such issuances, for a 15-month period.

13

Yapı Kredi Bank

As the fourth largest private bank in Turkey and one of the most well-established and robust players in its sector, Yapı Kredi

has been sustainably strengthening its positioning since its establishment in 1944 through a customer-centric banking

approach and focus on innovation.

Yapı Kredi serves 10.6 million customers through a widespread and multi-channel service network. The Bank operates from

more than 1,000 branches across Turkey with over 18.500 employees. Yapı Kredi offers its products and services via its

state-of-the-art alternative distribution channels (ADCs), including 3,606 ATMs (5th largest, with 7.1% market share),

innovative online banking (market leader with 13.1%), pioneering mobile banking (market leader with 11.6%), 3 award-

winning call centers, and 500,000 POS terminals. These ADCs handle 83% of total banking transactions.

Yapı Kredi is a fully integrated financial services group supported by domestic and international subsidiaries. Yapı Kredi Bank

renders banking services such as retail banking (including individual banking, SME banking, and card-payment systems),

corporate and commercial banking, and private banking and asset management. The Bank’s operations are supported by

domestic subsidiaries specializing on portfolio management, investment, financial leasing and factoring; and by foreign

banking subsidiaries in Netherlands, Russia and Azerbaijan.

For Yapı Kredi, 2014 was of particular and special importance as it marked the Bank’s 70th anniversary. Over the past 70

years, Yapı Kredi has always broken new ground in line with its “Dedication to Deliver” philosophy and customer-centric

approach.

In 2014, Yapı Kredi total assets increased by 22% annually to TL 195 billion. Yapı Kredi further accelerated its contribution

to the financing of the Turkish economy. Accordingly, total cash and non-cash loan volume increased by 27% reaching TL

174.3 billion, increasing its ranking among private banks in Turkey by 1 notch to 3rd place.

In 2014, total loan book reached TL 125.5 billion with 26% annual growth compared to sector growth of 18%. Accordingly,

the Bank increased its market share in total loans by 70 bps to 10.2%. Remixing of loan book continued towards more

profitable segments including TL company loans (+50% annually), general-purpose loans (+46% annually) and SME loans

(+49% annually). In 2014, Yapı Kredi maintained its leader position in credit cards. During the same period, total deposit

book reached TL 107.6 billion with 22% annual growth, more than twice the sector growth of 10%. This resulted in a gain of

90 bps in total deposit market share to 10.0%.

Yapı Kredi’s successful performance is supported by various subsidiaries, each among the leading companies in their

sectors. Yapı Kredi Leasing maintains its sector leadership with 18.3% market share. Yapı Kredi Asset Management (18.0%

market share in mutual funds) and Yapı Kredi Invest (7.4% market share in equity transaction volume) are the second

largest players in their respective sectors. The Bank maintained its 26-year leadership in credit cards with a market share of

20.8% in outstanding volume, 18.6% in issuing volume, 20.0% in POS volume, and 17.9% in number of cards.

81.80% of Yapı Kredi’s shares are owned by Koç Financial Services, a 50%-50% joint venture between UniCredit Group and

Koç Group. The remaining 18.20% is publicly traded on Borsa Istanbul, and Global Depositary Receipts that represent the

Bank’s shares are quoted on the London Stock Exchange.

Koç Group, founded in 1926, is the largest conglomerate in Turkey with its turnover, exports and 81 thousand employees.

Koç Group’s turnover comprises 8% of Turkey’s total GDP, and it exports comprise 10% of Turkey’s total exports.

UniCredit Group, with roots dating back to 1473, is a systematically important European financial institution based in Italy.

The Group has a widespread network of 9,000 branches and 148 thousand employees in 22 countries.

14

Financial Highlights

Turnover (million USD) 2014 2013 2012

Domestic 7,184 5,443 4,149

International 1,273 2,049 2,001

Export 1,269 2,044 1,994

Import 4 5 7

Total 8,457 7,492 6,150 Balance Sheet & Income Statement Major Accounts (thousand TL)

2014 2013 2012

Factoring receivables (net)

2,774,764

2,149,220 1,650,735

Total assets 2,813,932 2,196,454 1,791,190

Factoring payables 5,155 6,843 10,675

Shareholders' equity 232,986 263,545 219,654

Net profit 44,837 149,335 53,342

Factoring revenue 160,868 119,426 156,492

Interest income 145,046 104,996 137,461

Commission income 15,822 14,430 19,031

Total Assets (thousand TL)

2014 2,813,932

2013 2,196,454

2012 1,791,190

Factoring Receivables, net (thousand TL)

2014 2,774,764 2013 2,149,220 2012 1,650,735 Total Turnover (million USD)

2014 8.457

2013 7,492

2012 6,150

Shareholder's Equity (thousand TL)

2014 232,986

2013 263,545

2012 219,654

Factoring Revenue (thousand TL)

2014 160,868 2013 119,426 2012 156,492

15

Profit Distribution Policy

The Company distributes profits in accordance with the provisions of Turkish Commercial Code, current tax legislation, and other relevant regulations as well as the provisions of its Articles of Incorporation regarding profit distribution. Article 18 of the Articles of Association provides detailed information about the Company's profit distribution policy. In this respect, the General Assembly is authorized to pass resolutions on whether the dividend distribution shall be in cash or in the form of capital increase, whereupon bonus shares will be issued to shareholders or if part of the distribution shall be in cash and part in the form of capital increase, taking into consideration the Company’s growth targets as well as its financing requirements. After setting aside first dividend and first legal reserves from net profits as mandated by Article 18 of the Articles of Association; the General Assembly may make the decision to distribute a portion or the entire remaining amount as secondary dividends or reserve it as extraordinary reserves. Profit distribution policy must comply with the medium and long-term growth targets of the Company. The Board of Directors may review said policy, if necessary, depending on national and international economic conditions.

Risks and Risk Assessment Report of the Board of Directors

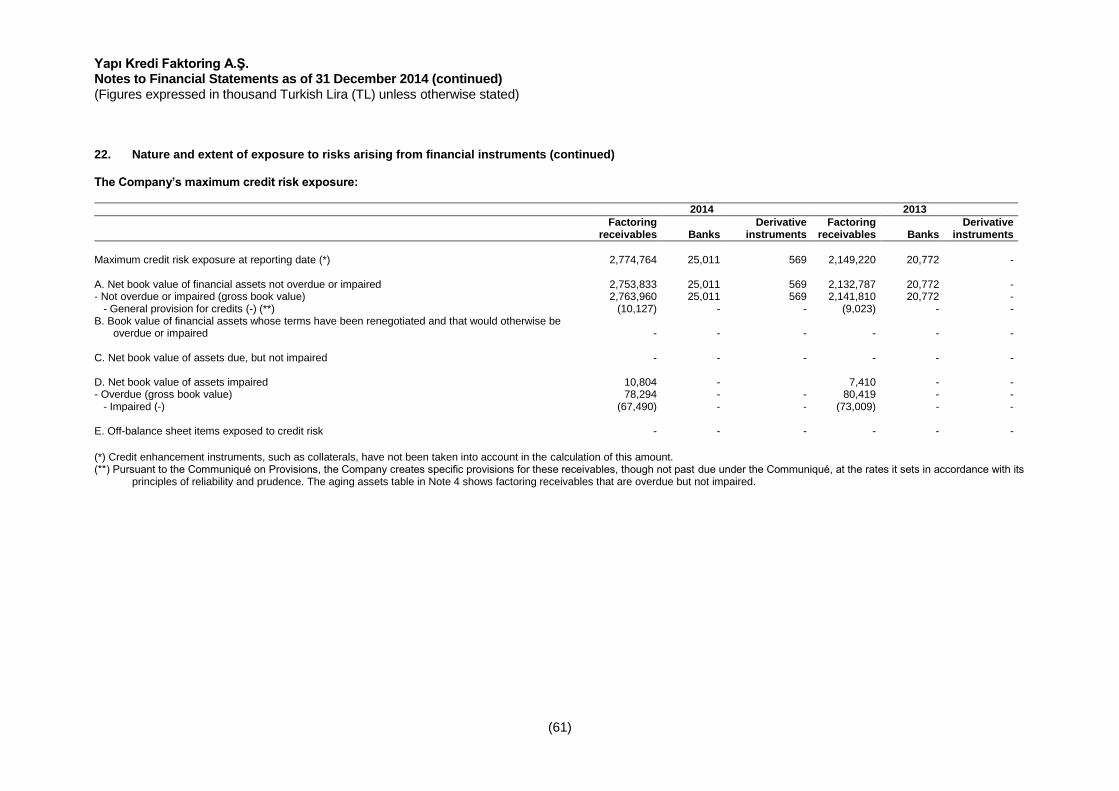

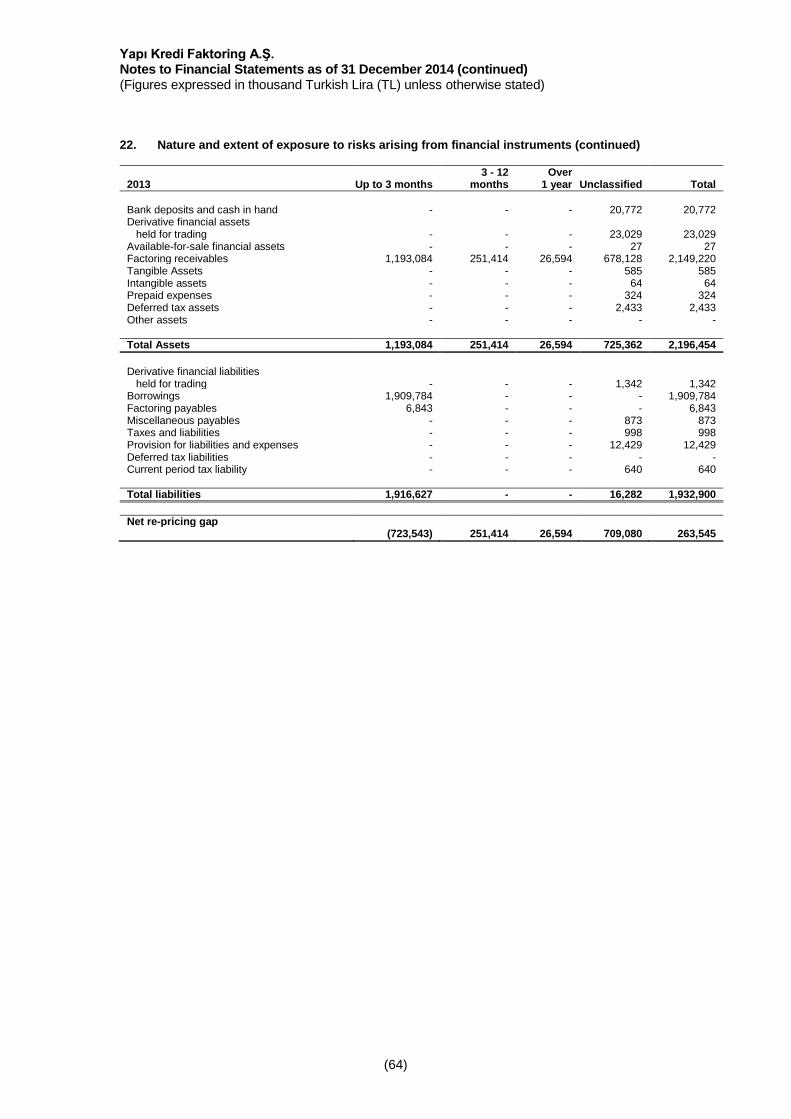

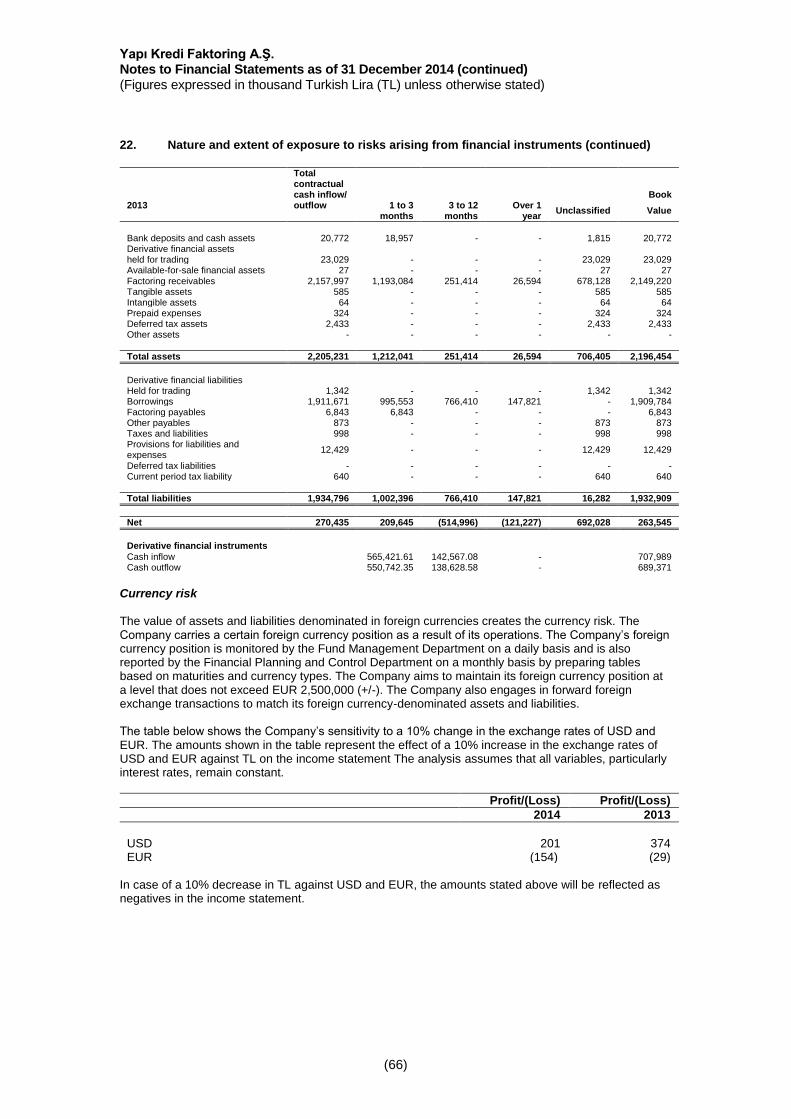

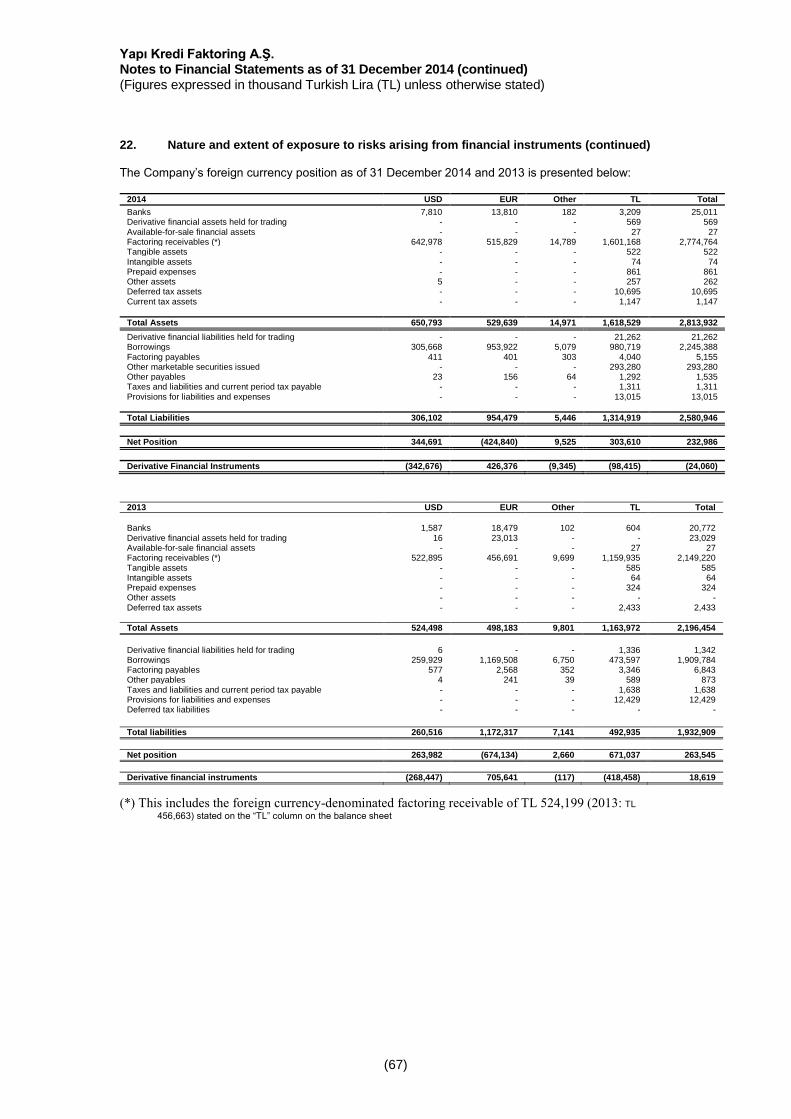

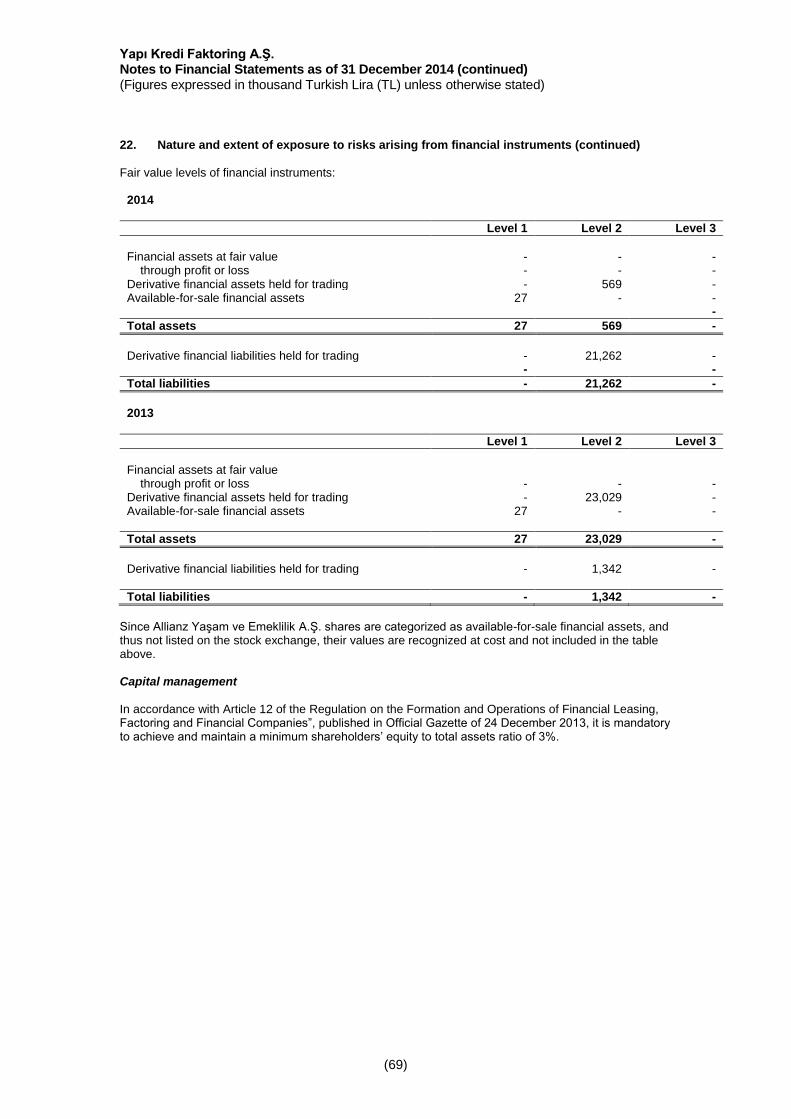

As no significant risk was identified during 2014, the Board of Directors has not drawn up a risk assessment report. On the other hand, credit risk, market risk, interest rate risk, liquidity risk, foreign exchange risk and other risk-related matters are discussed in detail in Article 22 under the Notes to the Independent Auditor’s Report.

Miscellaneous

As of 16 February 2015, Carlo Vivaldi has resigned as Board Member and Deputy CEO, and was succeeded by Niccoló Ubertalli, effective from the same date. As of 1 February 2015, Ekin Arca Kırelli was appointed as Assistant General Manager, replacing Zeynep Emecan Kandemir who has resigned as Director of Financial Planning & Financial Affairs as of 31 January 2015. As of 1 February 2015, Pınar Adıyaman Demirtaş has resigned as Director of Internal Audit, and was succeeded by Aba Kantarcı, effective from the same date.

16

Affiliated Company Report, Prepared in Accordance with Article 199 of the Turkish Commercial Code

According to Article 199 of the Turkish Commercial Code No. 6102, which came into effect on July 2012, Yapı Kredi Faktoring A.Ş. Board of Directors is obligated to prepare a report regarding relations with the controlling company and its affiliated companies, within the first three months of the relevant operating year and to indicate the conclusion part of mentioned report in its annual report. Necessary explanations regarding transactions made by Yapı Kredi Faktoring A.Ş. with related parties can be found in Note 21 of the financial report. The report issued by Yapı Kredi Faktoring A.Ş. Board of Directors on 20 February 2015 states that: “It is concluded that, in all transactions made by Yapı Kredi Faktoring A.Ş. with the controlling company and the companies affiliated to the controlling company in 2014, according to situations and conditions known to us and prevailing at the time, the related transaction was made or related measure were taken or refrained from being taken, an appropriate consideration for each transaction has been provided and there is no measure taken or refrained from being taken, which may cause the company to suffer losses and that in this context, there is no transaction or measure which may require balancing."

17

Section II

Financial Statements as of 31 December 2014

and Independent Auditor's Report

18

19

20

Table of Contents Page

Balance Sheet ................................................................................................................................................................... 21-22

Off-Balance Sheet Items .................................................................................................................................................. 23

Income Statement .................................................................................................................................................... 24

Shareholders’ Equity Profit and Loss Account Statement ................................................................................................ 25

Changes in Shareholders’ Equity ..................................................................................................................................... 26

Cash Flow Statement .................................................................................................................................................... 27

Profit Distribution Statement ............................................................................................................................................ 28

Explanatory Notes Regarding Financial Statements......................................................................................................... 29-70

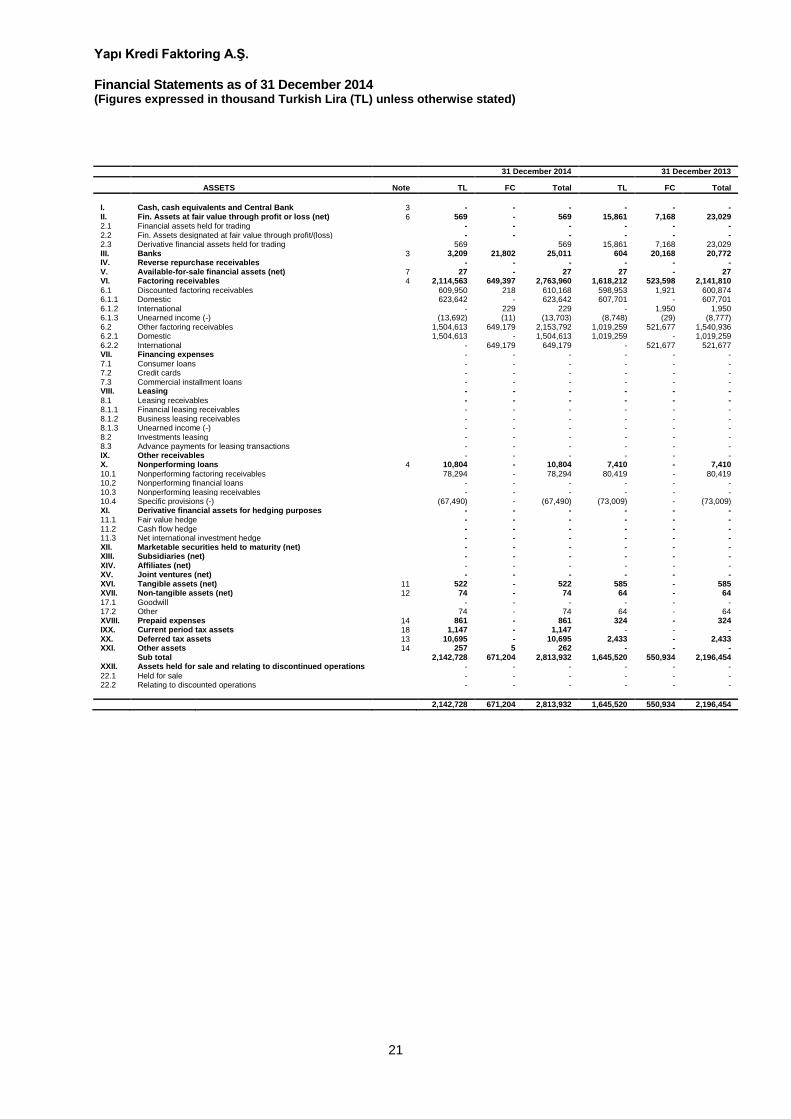

Yapı Kredi Faktoring A.Ş. Financial Statements as of 31 December 2014 (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

21

31 December 2014 31 December 2013

ASSETS Note TL FC Total TL FC Total

I. Cash, cash equivalents and Central Bank 3 - - - - - - II. Fin. Assets at fair value through profit or loss (net) 6 569 - 569 15,861 7,168 23,029 2.1 Financial assets held for trading

- - - - - -

2.2 Fin. Assets designated at fair value through profit/(loss)

- - - - - - 2.3 Derivative financial assets held for trading

569

569 15,861 7,168 23,029

III. Banks

3 3,209 21,802 25,011 604 20,168 20,772 IV. Reverse repurchase receivables

- - - - - - V. Available-for-sale financial assets (net) 7 27 - 27 27 - 27 VI. Factoring receivables 4 2,114,563 649,397 2,763,960 1,618,212 523,598 2,141,810

6.1 Discounted factoring receivables

609,950 218 610,168 598,953 1,921 600,874 6.1.1 Domestic

623,642 - 623,642 607,701 - 607,701

6.1.2 International

- 229 229 - 1,950 1,950 6.1.3 Unearned income (-)

(13,692) (11) (13,703) (8,748) (29) (8,777)

6.2 Other factoring receivables

1,504,613 649,179 2,153,792 1,019,259 521,677 1,540,936 6.2.1 Domestic

1,504,613 - 1,504,613 1,019,259 - 1,019,259

6.2.2 International

- 649,179 649,179 - 521,677 521,677 VII. Financing expenses

- - - - - -

7.1 Consumer loans

- - - - - - 7.2 Credit cards

- - - - - -

7.3 Commercial installment loans

- - - - - - VIII. Leasing

- - - - - -

8.1 Leasing receivables

- - - - - - 8.1.1 Financial leasing receivables

- - - - - -

8.1.2 Business leasing receivables

- - - - - - 8.1.3 Unearned income (-)

- - - - - -

8.2 Investments leasing

- - - - - - 8.3 Advance payments for leasing transactions

- - - - - -

IX. Other receivables

- - - - - - X. Nonperforming loans 4 10,804 - 10,804 7,410 - 7,410

10.1 Nonperforming factoring receivables

78,294 - 78,294 80,419 - 80,419 10.2 Nonperforming financial loans

- - - - - -

10.3 Nonperforming leasing receivables

- - - - - - 10.4 Specific provisions (-)

(67,490) - (67,490) (73,009) - (73,009)

XI. Derivative financial assets for hedging purposes

- - - - - - 11.1 Fair value hedge

- - - - - -

11.2 Cash flow hedge

- - - - - - 11.3 Net international investment hedge

- - - - - - XII. Marketable securities held to maturity (net)

- - - - - -

XIII. Subsidiaries (net)

- - - - - - XIV. Affiliates (net)

- - - - - -

XV. Joint ventures (net)

- - - - - - XVI. Tangible assets (net) 11 522 - 522 585 - 585 XVII. Non-tangible assets (net) 12 74 - 74 64 - 64

17.1 Goodwill

- - - - - - 17.2 Other

74 - 74 64 - 64

XVIII. Prepaid expenses 14 861 - 861 324 - 324 IXX. Current period tax assets 18 1,147 - 1,147 - - - XX. Deferred tax assets 13 10,695 - 10,695 2,433 - 2,433 XXI. Other assets 14 257 5 262 - - -

Sub total

2,142,728 671,204 2,813,932 1,645,520 550,934 2,196,454

XXII. Assets held for sale and relating to discontinued operations - - - - - - 22.1 Held for sale

- - - - - -

22.2 Relating to discounted operations

- - - - - -

2,142,728 671,204 2,813,932 1,645,520 550,934 2,196,454

Yapı Kredi Faktoring A.Ş. Financial Statements as of 31 December 2014 (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

22

31 December

2014 31 December

2013

Liabilities Note TL FC Total TL FC Total

I. Derivative financial liabilities held for trading 9 21,262 - 21,262 1,336 6 1,342 II. Loans received 5 980,719 1,264,669 2,245,388 473,597 1,436,187 1,909,784 III. Factoring payables

4,040 1,115 5,155 3,346 3,497 6,843

IV. Leasing payables

- - - - - - 4.1 Financial leasing payables

- - - - - -

4.2 Business leasing payables

- - - - - - 4.3 Other

- - - - - -

4.4 Deferred financial leasing expenses ( - )

- - - - - - V. Marketable securities issued (net)

293,280 - 293,280 - - -

5.1 Bills 5 293,280 - 293,280 - - - 5.2 Asset-backed securities

- - - - - -

5.3 Bonds

- - - - - - VI. Other liabilities 8 1,292 243 1,535 589 284 873 VII. Other liabilities

- - - - - -

VIII. Derivative financial liabilities for hedging purposes

- - - - - - 8.1 Fair value hedge

- - - - - -

8.2 Cash flow hedge

- - - - - - 8.3 Net international investment hedge

- - - - - -

IX. Taxes and liabilities due 18 1,311 - 1,311 998 - 998 X. Provision for liabilities and expenses

13,015 - 13,015 12,429 - 12,429

10.1 Provision for reorganization

- - - - - 10.2 Provision for employee benefits 10 1,238 - 1,238 913 - 913

10.3 Other provisions 10 11,777 - 11,777 11,516 - 11,516 XI. Deferred income

- - - - - -

XII. Current period tax liabilities 18 - - - 640 - 640 XIII. Deferred tax liability 13 - - - - - - XIV. Subordinated loans

- - - - - -

Sub total

1,314,919 1,266,027 2,580,946 492,935 1,439,974 1,932,909

XV. Liabilities for property and equipment held for sale and related to discontinued operations (net) - - - - -

15.1 Held for sale

- - - - - - 15.2 Related to discounted operations

- - - - - -

XVI. Shareholders’ equity 15 232,986 - 232,986 263,545 - 263,545 16.1 Paid-in capital

31,917 - 31,917 31,917 - 31,917

16.2 Capital reserve

97,223 - 97,223 - - - 16.2.1 Share premium

- - - - - -

16.2.2 Share cancellation profits

- - - - - - 16.2.3 Other capital reserves

97,223 - 97,223 - - -

16.3 Other comprehensive accumulated income or expenses not to be re-classified in case of profit / loss (10) - (10) 12 - 12

16.4 Other comprehensive accumulated income or expenses to be re-classified in case of profit / loss - - - - - -

16.5 Profit reserves

29,642 - 29,642 51,921 - 51,921 16.5.1 Legal reserves

25,220 - 25,220 17,780 - 17,780

16.5.2 Statutory reserves

- - - - - - 16.5.3 Extraordinary reserves

4,422 - 4,422 34,141 - 34,141

16.5.4 Other profit reserves

- - - - - - 16.6 Profit / loss

74,214 - 74,214 179,695 - 179,695

16.6.1 Profit / loss carried forward

29,377 - 29,377 30,360 - 30,360 16.6.2 Current period net profit / loss

44,837 - 44,837 149,335 - 149,335

Total Liabilities 1,547,905 1,266,027 2,813,932 756,480 1,439,974 2,196,454

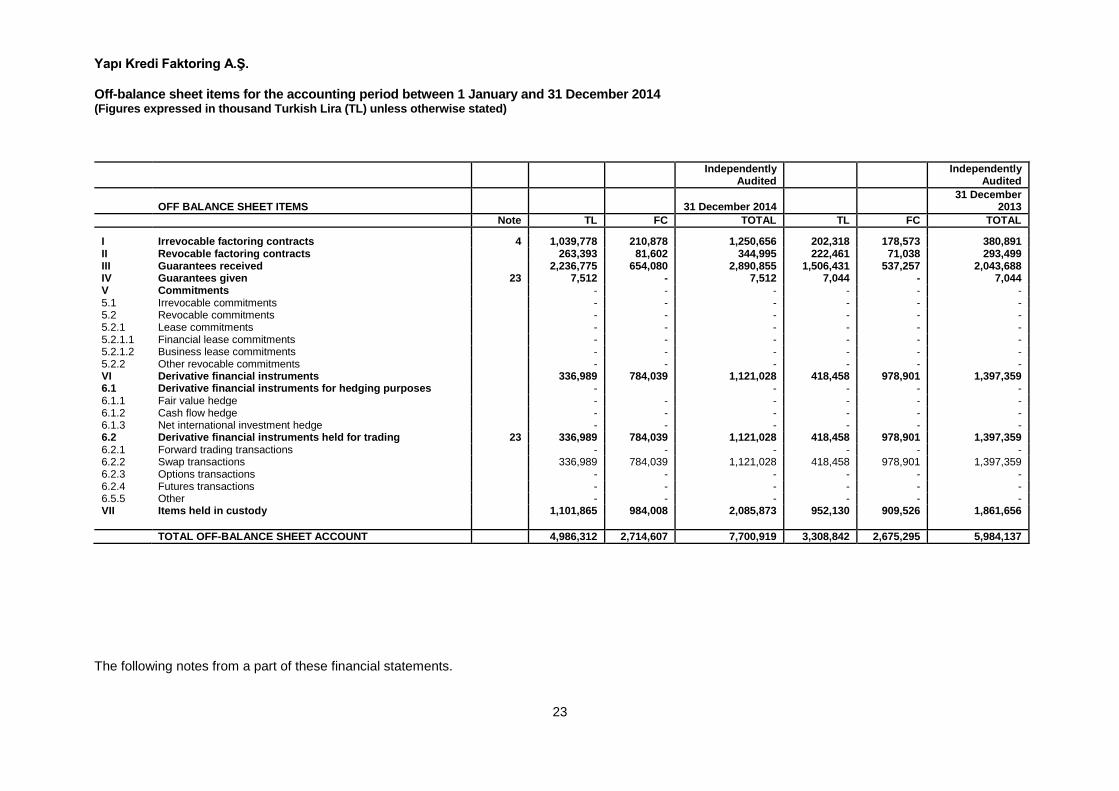

Yapı Kredi Faktoring A.Ş. Off-balance sheet items for the accounting period between 1 January and 31 December 2014 (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

The following notes from a part of these financial statements.

23

Independently Audited

Independently Audited

OFF BALANCE SHEET ITEMS

31 December 2014

31 December 2013

Note TL FC TOTAL TL FC TOTAL

I Irrevocable factoring contracts 4 1,039,778 210,878 1,250,656 202,318 178,573 380,891 II Revocable factoring contracts

263,393 81,602 344,995 222,461 71,038 293,499

III Guarantees received

2,236,775 654,080 2,890,855 1,506,431 537,257 2,043,688 IV Guarantees given 23 7,512 - 7,512 7,044 - 7,044 V Commitments

- - - - - -

5.1 Irrevocable commitments

- - - - - - 5.2 Revocable commitments

- - - - - -

5.2.1 Lease commitments

- - - - - - 5.2.1.1 Financial lease commitments

- - - - - -

5.2.1.2 Business lease commitments

- - - - - - 5.2.2 Other revocable commitments

- - - - - -

VI Derivative financial instruments

336,989 784,039 1,121,028 418,458 978,901 1,397,359 6.1 Derivative financial instruments for hedging purposes

-

- - - -

6.1.1 Fair value hedge

- - - - - - 6.1.2 Cash flow hedge

- - - - - -

6.1.3 Net international investment hedge

- - - - - - 6.2 Derivative financial instruments held for trading 23 336,989 784,039 1,121,028 418,458 978,901 1,397,359 6.2.1 Forward trading transactions

- - - - - -

6.2.2 Swap transactions

336,989 784,039 1,121,028 418,458 978,901 1,397,359 6.2.3 Options transactions

- - - - - -

6.2.4 Futures transactions

- - - - - - 6.5.5 Other

- - - - - -

VII Items held in custody

1,101,865 984,008 2,085,873 952,130 909,526 1,861,656

TOTAL OFF-BALANCE SHEET ACCOUNT

4,986,312 2,714,607 7,700,919 3,308,842 2,675,295 5,984,137

Yapı Kredi Faktoring A.Ş. Income Statement for the accounting period between 1 January and 31 December 2014 (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

The following notes constitute a part of the accompanying financial statements.

24

INCOME AND EXPENSE ITEMS Independently Audited Independently Audited Note 31 December 2014 31 December 2013

I. INCOME FROM OPERATING ACTIVITIES

160,868 119,426

FACTORING INCOME 16 160,868 119,426

1.1 Interest Received From Factoring Receivables

145,046 104,996 1.1.1 Discounts

56,362 32,934

1.1.2 Other

88,684 72,062 1.2 Factoring Fees and Commissions 15,822 14,430 1.2.1 Discounts

5,088 4,058

1.2.2 Other

10,734 10,372

INCOME FROM FINANCIAL LOANS - -

1.3 Interest earned on financial loans

- - 1.4 Financial loan fees and commissions - -

LEASING INCOME

- -

1.5 Financial leasing income

- - 1.6 Business leasing income

- -

1.7 Leasing fees and commissions - - II. FINANCIAL EXPENSES (-)

57,502 37,134

2.1 Interest on Funds Borrowed

48,378 34,148 2.2 Interest on Factoring Payables - - 2.3 Financial leasing expenses

- -

2.4 Interest on Securities Issued 6,810 - 2.5 Other Interest Expenses

- 2

2.6 Fees and commissions paid

2,314 2,984 III. GROSS P/L (I+II)

103,366 82,292

IV. OPERATING EXPENSES (-) 17 20,098 16,393 4.1 Personnel expenses

13,891 12,151

4.2 Provision for termination benefits

36 - 4.3 Research & development expenses

- -

4.4 General administrative expenses

5,909 4,044 4.5 Other

262 198

V. GROSS OPERATING P/L (III+IV)

83,268 65,899 VI. INCOME FROM OTHER OPERATING ACTIVITIES

273,795 296,472

6.1 Interest received from banks

5,556 5,053 6.2 Interest earned on reverse repurchase transactions

- -

6.3 Interest earned on marketable securities

- - 6.3.1 Interest earned on financial assets held for trading

- -

6.3.2 Financial assets designated at fair value through profit/(loss) - - 6.3.3 Income from available-for-sale financial assets

- 127,883

6.3.4 Income from investments held to maturity - - 6.4 Dividends 21 29 - 6.5 Profit from capital market transactions

- 20,253

6.5.1 Profit from derivative financial transactions

- 20,253 6.5.2 Other

- -

6.6 Foreign exchange gains

264,931 141,695 6.7 Other 19 3,279 1,588 VII. SPECIFIC PROVISIONS FOR NON-PERFORMING LOANS (-) 4 18,068 23,089 VIII. OTHER OPERATING EXPENSES (-)

284,345 178,293

8.1 Impaired marketable securities

- - 8.1.1 Impaired financial assets designated at fair value through profit/(loss)

- -

8.1.2 Loss from available-for-sale financial assets

- - 8.1.3 Loss from investments held to maturity - - 8.2 Impaired non-current assets

- -

8.2.1 Impaired non-current tangible assets

- - 8.2.2 Impaired non-current assets held for sale and discontinued operations

- -

8.2.3 Impaired goodwill

- - 8.2.4 Other impaired non-current assets - - 8.2.5 Impaired investments in affiliates, subsidiaries and joint-ventures

- -

8.3 Loss from derivative financial transactions

42,381 928 8.4 Foreign exchange loss

241,439 176,775

8.5 Other 19 525 590 IX. NET OPERATING PROFIT/LOSS (V+…+VIII)

54,650 160,989

X. SURPLUS AMOUNT RECOGNIZED AS INCOME AFTER MERGER

- - XI. NET MONETARY POSITION PROFIT/LOSS

- -

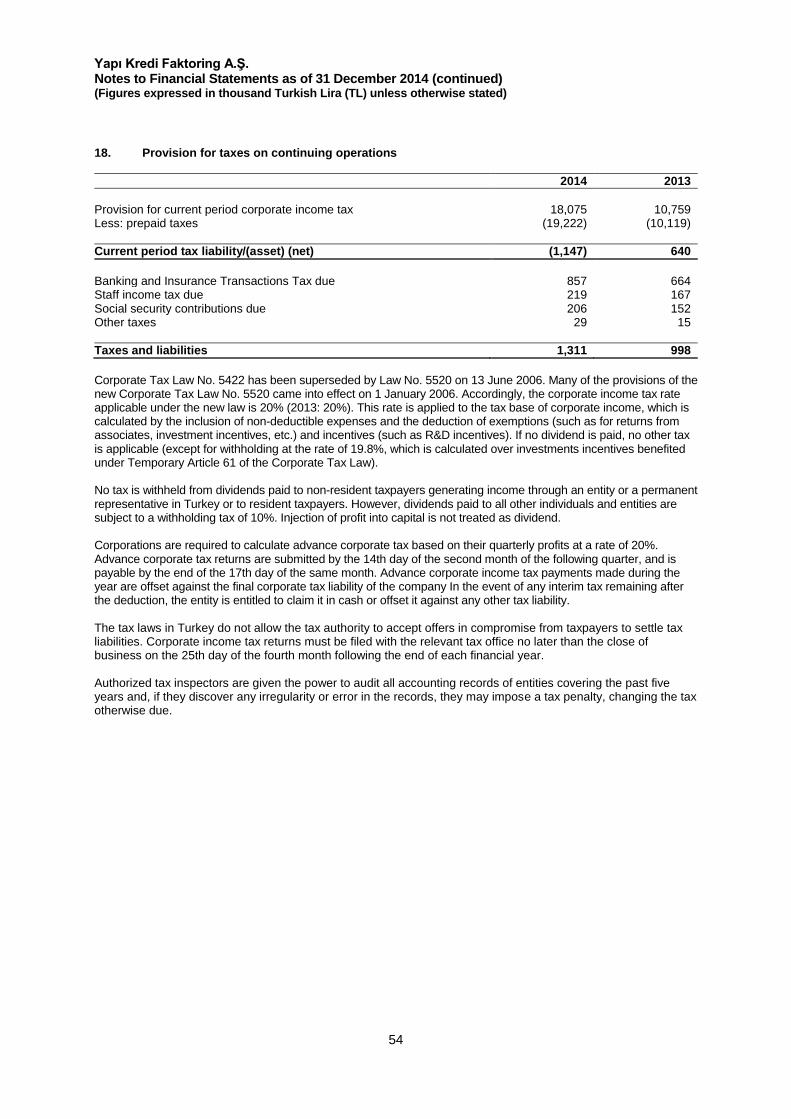

XII. BEFORE-TAX PROFIT/LOSS FROM CONTINUING OPERATIONS (IX+X+XI) 54,650 160,989 XIII. PROVISION FOR TAX ON CONTINUING OPERATIONS (±) 18 9,813 11,654 13.1 Provision for current taxes

18,075 10,759

13.2 Expense effect of deferred taxes (+)

- 895 13.3 Income effect of deferred taxes (-)

(8,262) -

XIV. NET ANNUAL PROFIT/LOSS FROM CONTINUING OPERATIONS (XII±XIII) 44,837 149,335 XV. INCOME FROM DISCONTINUED OPERATIONS - - 15.1 Income from available-for-sale financial assets - - 15.2 Profit on affiliates, subsidiaries and joint-ventures sold - - 15.3 Other income from discontinued operations

- -

XVI. LOSSES FROM DISCONTINUED OPERATIONS (-) - - 16.1 Expenses for available-for-sale financial assets - - 16.2 Loss on affiliates, subsidiaries and joint-ventures sold - - 16.3 Expenses for other discontinued operations

- -

XVII. BEFORE-TAX PROFIT/LOSS FROM DISCONTINUED OPERATIONS (XV-XVI) - - XVIII. PROVISION FOR TAX ON DISCONTINUED OPERATIONS (±) - - 18.1 Provision for current taxes

- -

18.2 Expense effect of deferred taxes (+)

- - 18.3 Income effect of deferred taxes (-)

- -

XIX. NET ANNUAL PROFIT/LOSS FROM DISCONTINUED OPERATIONS (XVII±XVIII) - - XX. NET ANNUAL PROFIT/LOSS (XIV+XIX)

44,837 149,335

EARNİNGS PER SHARE

1.40 4.68

Earnings per share from continuing operations 20 1.40 4.68

Earnings per share from discontinued operations - -

EARNINGS PER DILUTED SHARE

- -

Earnings per share from continuing operations - -

Earnings per share from discontinued operations -

Yapı Kredi Faktoring A.Ş. Statement of income and expenses recognized in shareholders’ equity for the accounting period between 1 January and 31 December 2014 (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

The following notes constitute a part of the accompanying financial statements.

25

Independently Audited

31 December

2014 31 December 2013

I. PROFIT/LOSS OF THE PERIOD 44,837 149,335 II. OTHER COMPREHENSIVE INCOME (10) 12 2.1 Not to be re-classified on Profit/Loss (10) 12 2.1.1 Tangible assets revaluation adjustments - - 2.1.2 Intangible assets revaluation adjustments - - 2.1.3 Defined Benefit Plans Reevaluation Gains / Losses (10) 12

2.1.4 Other Comprehensive Income Components that will not be Reclassified As Other Profit Or Loss - -

2.1.5 Taxes regarding other comprehensive income that will not be reclassified in profit or loss - -

2.1.5.1 Current Tax Expense / Income - - 2.1.5.2 Deferred Tax Expense / Income - - 2.2 To be reclassified on profit or loss - - 2.2.1 Foreign exchange conversion differences - -

2.2.2 Revaluation and/or reclassification income/expenses of Available-for-sale financial assets - -

2.2.3 Cash flow risk protection income/expenses - - 2.2.4 Investment risk protection income/expenses regarding foreign businesses - - 2.2.5 Other Comprehensive Income Items that would be reclassified in profit or loss - - 2.2.6 Taxes regarding other comprehensive income that will be reclassified in profit or loss - - 2.2.6.1 Current Tax Expense / Income - - 2.2.6.2 Deferred Tax Expense / Income - -

III. TOTAL COMPREHENSIVE INCOME (I+II) 44,827 149,347

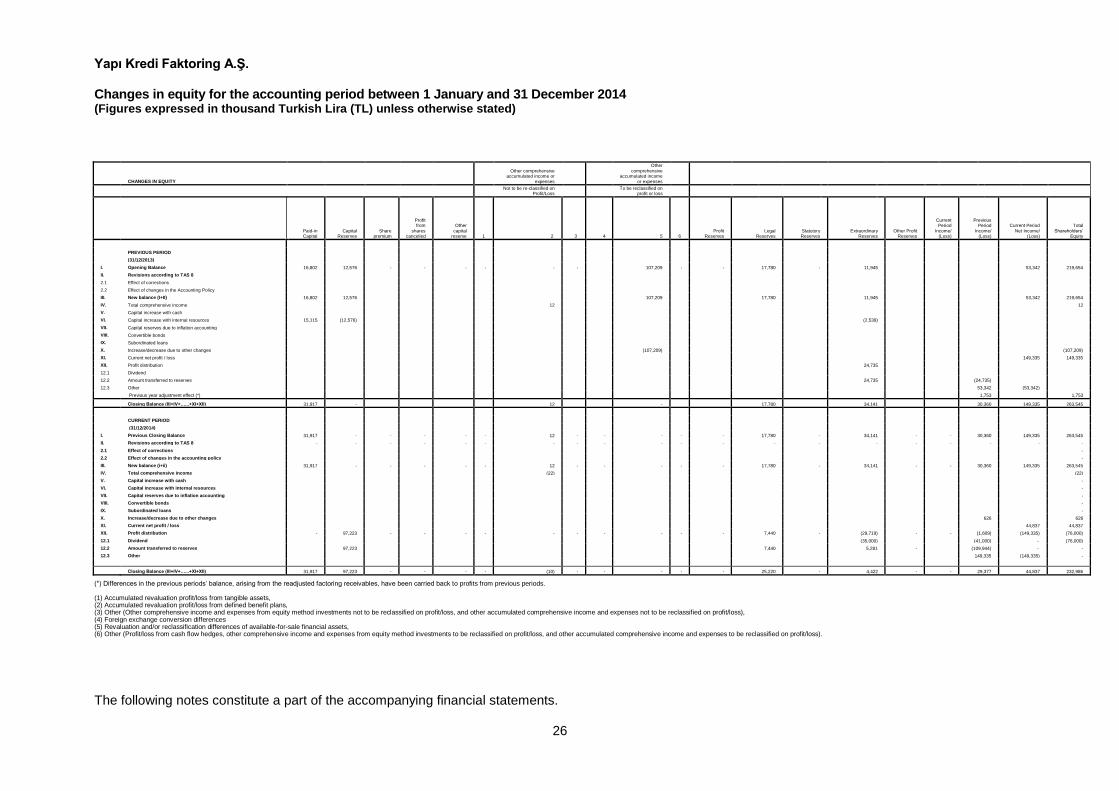

Yapı Kredi Faktoring A.Ş. Changes in equity for the accounting period between 1 January and 31 December 2014 (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

The following notes constitute a part of the accompanying financial statements.

26

CHANGES IN EQUITY

Other comprehensive accumulated income or

expenses

Other comprehensive

accumulated income

or expenses

Not to be re-classified on

Profit/Loss To be reclassified on

profit or loss

Paid-in Capital

Capital Reserves

Share premium

Profit from

shares cancelled

Other capital

reserve

1

2

3 4

5

6

Profit Reserves

Legal Reserves

Statutory Reserves

Extraordinary Reserves

Other Profit Reserves

Current Period

Income/ (Loss)

Previous Period

Income/ (Loss)

Current Period Net Income/

(Loss)

Total Shareholders’

Equity

PREVIOUS PERIOD

(31/12/2013)

I. Opening Balance 16,802 12,576 - - - - - - 107,209 - - 17,780 - 11,945 53,342 219,654

II. Revisions according to TAS 8

2.1 Effect of corrections

2.2 Effect of changes in the Accounting Policy

III. New balance (I+II) 16,802 12,576 107,209 17,780 11,945 53,342 219,654

IV. Total comprehensive income 12 12

V. Capital increase with cash

VI. Capital increase with internal resources 15,115 (12,576) (2,539)

VII. Capital reserves due to inflation accounting

VIII. Convertible bonds

IX. Subordinated loans

X. Increase/decrease due to other changes (107,209) (107,209)

XI. Current net profit / loss 149,335 149,335

XII. Profit distribution 24,735

12.1 Dividend

12.2 Amount transferred to reserves 24,735 (24,735)

12.3 Other 53,342 (53,342)

Previous year adjustment effect (*) 1,753 1,753

Closing Balance (III+IV+…...+XI+XII) 31,917 - 12 - 17,780 34,141 30,360 149,335 263,545

CURRENT PERIOD

(31/12/2014)

I. Previous Closing Balance 31,917 - - - - - 12 - - - - - 17,780 - 34,141 - - 30,360 149,335 263,545

II. Revisions according to TAS 8 - - - - - - - - - - - - - - - - - - - -

2.1 Effect of corrections -

2.2 Effect of changes in the accounting policy -

III. New balance (i+ii) 31,917 - - - - - 12 - - - - - 17,780 - 34,141 - - 30,360 149,335 263,545

IV. Total comprehensive income (22) (22)

V. Capital increase with cash -

VI. Capital increase with internal resources -

VII. Capital reserves due to inflation accounting -

VIII. Convertible bonds -

IX. Subordinated loans -

X. Increase/decrease due to other changes 626 626

XI. Current net profit / loss 44,837 44,837

XII. Profit distribution - 97,223 - - - - - - - - - - 7,440 - (29,719) - - (1,609) (149,335) (76,000)

12.1 Dividend (35,000) (41,000) - (76,000)

12.2 Amount transferred to reserves 97,223 7,440 5,281 - (109,944) - -

12.3 Other

149,335 (149,335) -

Closing Balance (III+IV+…...+XI+XII) 31,917 97,223 - - - - (10) - - - - - 25,220 - 4,422 - - 29,377 44,837 232,986

(*) Differences in the previous periods’ balance, arising from the readjusted factoring receivables, have been carried back to profits from previous periods. (1) Accumulated revaluation profit/loss from tangible assets, (2) Accumulated revaluation profit/loss from defined benefit plans, (3) Other (Other comprehensive income and expenses from equity method investments not to be reclassified on profit/loss, and other accumulated comprehensive income and expenses not to be reclassified on profit/loss), (4) Foreign exchange conversion differences (5) Revaluation and/or reclassification differences of available-for-sale financial assets, (6) Other (Profit/loss from cash flow hedges, other comprehensive income and expenses from equity method investments to be reclassified on profit/loss, and other accumulated comprehensive income and expenses to be reclassified on profit/loss).

Yapı Kredi Faktoring A.Ş. Cash Flow Statement for the accounting period between 1 January and 31 December 2014 (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

The following notes constitute a part of the accompanying financial statements.

27

Independently Independently

audited audited

Note

31 December 2014 31 December 2013

A. Cash Flow from Operating Activities 1.1 Operating Profit before Changes in Operating Assets and Liabilities 72,486 49,615

1.1.1 Received Interests/Leasing Income

150,602 110,049 1.1.2 Paid Interests/Leasing Expenses

(55,188) (34,150)

1.1.3 Leasing Expenses

- - 1.1.4 Dividends Received

29 -

1.1.5 Fees and Commissions Received 16 15,822 14,430 1.1.6 Other Income

- -

1.1.7 Collections from Written-off Non-Performing Receivables 4 1,103 1,140 1.1.8 Cash Payments to Staff and Service Providers (13,927) (12,151) 1.1.9 Taxes Paid 18 (19,222) (10,119) 1.1.10 Other

(6,733) (19,584)

1.2 Change in Operating Assets and Liabilities (291,452) (138,606)

1.2.1 Net Decrease (Increase) in Factoring Receivables

(625,544) (498,485) 1.2.1 Net Decrease (Increase) in Financial Loans

- -

1.2.1 Net Decrease (Increase) in Leasing Receivables

- - 1.2.2 Net Decrease (Increase) in Other Assets

(799) 144

1.2.3 Net Decrease (Increase) in Factoring Payables

(1,688) (3,832) 1.2.3 Net Decrease (Increase) in Leasing Payables

- -

1.2.4 Net Decrease (Increase) in Loans Received

335,604 362,721 1.2.5 Net Decrease (Increase) in Payables Due

- -

1.2.6 Net Decrease (Increase) in Other Payables

975 846

I. Net Cash Flow from Operating Activities (218,966) (88,991)

B. Cash Flow from Investing Activities

-

2.1 Acquisition of Affiliates, Subsidiaries and Joint Ventures - - 2.2 Proceeds from sale of affiliates, subsidiaries and joint-ventures - - 2.3 Purchase of tangible and intangible assets 11.12 (208) (265) 2.4 Proceeds from sale of tangible and intangible assets 11.12 - 165 2.5 Purchase of available-for-sale financial assets

- -

2.6 Proceeds from sale of available-for-sale financial assets

- 107,552 2.7 Purchase of held-to-maturity investments

- -

2.8 Proceeds from sale of held-to-maturity investments

- - 2.9 Other

- -

II. Net cash flow from investing activities (208) 107,452

C. Cash flow from financing activities

224,000 -

3.1 Cash obtained from funds borrowed and securities issued 300,000 - 3.2 Funds repaid and stocks and bonds repurchased - - 3.3 Capital market instruments issued

- -

3.4 Dividend payments

(76,000) -

3.5 Financial leasing payments

- - 3.6 Other

- -

III. Net cash flow from financing activities

224,000 -

IV. Effects of exchange rate changes on cash and cash equivalents (587) (185)

V. Net decrease (increase) in cash and cash equivalents 4,239 18,276

VI. Cash and cash equivalents at beginning of year 3 20,772 2,496

VII. Cash and cash equivalents at end of year 25,011 20,772

Yapı Kredi Faktoring A.Ş. Profit Distribution Statement for the accounting period between 1 January and 31 December 2014 (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

The following notes constitute a part of the accompanying financial statements.

28

ONE THOUSAND TL

Current period Previous period

(31/12/2014) (*) (31/12/2013)

I. Distribution of annual profit 1.1 Profit 54,650 160,989

1.2 Taxes and statutory liabilities payable (-) (9,813) (11,654) 1.2.1 Corporate income tax (income tax) (18,075) (10,759) 1.2.2 Income tax withheld - - 1.2.3 Other taxes and statutory liabilities (***) 8,262 (895)

A. Net profit (1.1 - 1.2) 44,837 149,335

1.3 Accumulated loss (-) - - 1.4 First legal reserve (-) - - 1.5 Other statutory reserves (-)(**) - (97,223)

B Distributable Net Profit of the Period [(a-(1.3+1.4+1.5)] 44,837 52,112

1.6 First dividend to shareholders (-) - - 1.6.1 To owners of ordinary shares - (1,596) 1.6.2 To owners of privileged shares - - 1.6.3 To owners of privileged shares - - 1.6.4 To profit sharing bonds - - 1.6.5 To holders of profit and loss sharing certificates - - 1.7 Dividend to employees (-) - - 1.8 Dividends to board of directors (-) - - 1.9 Second dividend to shareholders (-) - - 1.9.1 To owners of ordinary shares - (39,404) 1.9.2 To owners of privileged shares - - 1.9.3 To owners of privileged shares - - 1.9.4 To profit sharing bonds - - 1.9.5 To holders of profit and loss sharing certificates - - 1.10 Second legal reserve (-) - (3,940) 1.11 Statutory reserves (-) - - 1.12 Extraordinary reserves - 7,172 1.13 Other reserves - - 1.14 Special funds - -

- -

II. Distribution of reserves

2.1 Appropriated reserves - - 2.2 Second legal reserves (-) - (3,500) 2.3 Dividends to shareholders (-) - - 2.3.1 To owners of ordinary shares - (35,000) 2.3.2 To owners of privileged shares - - 2.3.3 To owners of privileged shares - - 2.3.4 To profit sharing bonds - - 2.3.5 To holders of profit and loss sharing certificates - - 2.4 Dividends to employees (-) - - 2.5 Dividends to board of directors (-) - -

III. Profit per Share

3.1 To owners of ordinary shares (TL) - 4.68 3.2 To owners of ordinary shares (%) - - 3.3 To owners of privileged shares (TL) - - 3.4 To owners of privileged shares (%) - -

IV. Dividend per share

4.1 To owners of ordinary shares (TL) - - 4.2 To owners of ordinary shares (%) - - 4.3 To owners of privileged shares (TL) - - 4.4 To owners of privileged shares (%)

(*) Since the profit distribution proposal had not been prepared by the Board of Directors, only the amount of profit available for distribution is recognized in 2014 profit distribution statements.

(**) As per the General Assembly resolution, the tax-exempt amount (75%) of the gains from the sale of Allianz Sigorta A.Ş. shares on 12 July 2013, amounting to TL 97,223 according the profit distribution statement for 2013, was classified under capital reserves account for 2014.

(***) The BRSA has expressed its opinion that, income generated from deferred tax assets may not be qualified as cash or internal resource, and as such, the income generated in this manner should not be classified as part of the current term income subject to dividend distribution and capital increase. As of 31 December 2014, the Company

has deferred tax income amounting to TL 8,262 (31 December 2013: None).

Yapı Kredi Faktoring A.Ş. 31 Aralık 2014 tarihi itibariyle finansal tablolara ilişkin açıklayıcı dipnotlar (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

29

1. Company Organization and the Field of Activity

Yapı Kredi Faktoring A.Ş. (“the Company”) was established in Istanbul on 25 March 1999 under the title of Koç Faktoring Hizmetleri A.Ş. The Company is a member of Koç Finansal Hizmetler A.Ş. (“KFH”), which was established on 16 March 2006. KFH signed a strategic partnership agreement with UniCredito Italiano S.p.A. (“UCI”) under a resolution adopted by the Koç Group on 12 October 2002. On 31 October 2007, KFH transferred its shares in the Company over to Yapı ve Kredi Bankası A.Ş., who became the major shareholder of the Company with 99.95% share. The Company offers factoring services in Turkey and abroad.

A member of Factors Chain International (“FCI”), the Company also operates in both domestic and international markets (exports and imports) under Law No. 6361 on Financial Leasing, Factoring and Financing Companies, enacted on 13 December 2013.

Koç Faktoring Hizmetleri A.Ş. merged with Yapı Kredi Faktoring A.Ş. on 29 December 2006 by taking over the Company’s entire assets and liabilities without liquidation, and changed its name to Yapı Kredi Faktoring A.Ş.

The Company’s main office is located at Büyükdere Caddesi Yapı Kredi Plaza A Blok Kat: 14 Levent, Istanbul - Turkey. The company employs 114 personnel as of 31 December 2014 (2013: 91). The Company is engaged primarily in factoring services in a single geographic area: Turkey. On 30 January 2015, the Board of Directors approved the disclosure of the Company’s financial statements, which may be amended by General Assembly. 2. Basis of presentation of financial statements 2.1 Basis of presentation

2.1.1 Accounting standards

The Company financial statements are prepared in thousand Turkish Lira (TL), within the framework of the "Communiqué on Uniform Chart of Accounts to be Implemented by Financial Leasing, Factoring and Financing Companies and Its Explanation as well as the Form and Scope of Financial Statements to Be Announced to Public" ("Communiqué on Financial Statements") issued by the Banking Regulation and Supervision Agency ("BRSA") and published on the Official Gazette No. 28861 of 24 December 2013, and in accordance with Turkish Accounting/Financial Reporting Standards (“TAS/TFRS”) issued by the Public Oversight Accounting and Auditing Standards Authority (“POA”). Financial statements of Financial Leasing, Factoring and Financial Companies are prepared and publicly disclosed in accordance with BRSA guidelines. The financial statements have been prepared on the historical cost basis except for derivative financial instruments presented at their fair values.

Yapı Kredi Faktoring A.Ş. Notes to Financial Statements as of 31 December 2014 (continued) (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

30

2. Basis of presentation of financial statements (continued) 2.1.2 Functional currency The accompanying financial statements are prepared in thousand TL, in accordance with the historical cost basis, reflecting the changes in general purchasing power of TL until 31 December 2004), except for financial assets and liabilities at fair value. The accompanying financial statements are presented in the functional currency circulated in the economic environment where the Company carries on business. The Company’s financial position and business results are presented in Turkish Lira, the currency designated by the Company for its financial statements. 2.1.3 Offsetting Financial assets and liabilities are offset and the net amount is reported in the balance sheet when the Company has a legally enforceable right to offset the recognized amounts and there is an intention to collect/pay related financial assets and liabilities on a net basis, or to realize the asset and settle the liability simultaneously. 2.1.4 Going concern The Company has prepared the accompanying financial statements on a going concern basis. 2.2. Changes in accounting policies 2.2.1 Changes in accounting policies Significant changes in accounting policies are applied retrospectively or prospectively, depending on the newly applied accounting standard. No significant changes occurred in the Company’s accounting policy during the fiscal year. 2.2.2 Changes and errors in accounting estimates Changes in accounting estimates that relate to only one period are applied in the current period, whereas changes that relate to future periods are applied both in the current and following periods prospectively No significant changes occurred in the Company’s accounting estimates during the fiscal year. Significant errors in accounting are corrected retrospectively and financial statements for the relevant periods are restated. 2.2.3 Comparative information and adjustments in financial statements for the previous accounting

period

The Company’s financial statements are prepared comparatively with the previous fiscal period, in order to determine the financial situation and performance trends. As the presentation or classification of the financial statement items change, financial statements for the previous year are reclassified accordingly to explain the changes and ensure comparability. 2.2.4 Amendments and interpretations Accounting policies serving as a basis for the financial statements for the fiscal year ending on 31 December 2014 are consistent with those used in the previous year, with the exception of new and amended TAS/TFRS standards and interpretations effective as of 01 January 2014, which are listed below. The effects of these standards and interpretations on the Company’s financial position and performance are discussed in their relevant sections.

Yapı Kredi Faktoring A.Ş. Notes to Financial Statements as of 31 December 2014 (continued) (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

31

2. Basis of presentation of financial statements (continued) New standards, amendments and interpretations effective as of 01 January 2014:

TAS 32 Financial Instruments: Presentation – Offsetting the Financial Assets and Liabilities (amendment)

The amendment clarifies the meaning of the connotation; “having a current legal right regarding the offsetting of the accounted amounts” and application area of TAS 32 offsetting principles regarding no concurring and gross settlement of the account systems (such as clearing offices). The standard did not have any significant impact on the Company’s financial position or performance. TFRS Interpretation 21, Levies

The interpretation clarifies that an entity recognizes a liability for a levy when the activity that triggers payment, as identified by the relevant legislation, occurs. It also clarifies that a levy liability can only be accrued progressively if the activity that triggers payment occurs over a period of time, in accordance with the relevant legislation. For a levy that is triggered upon reaching a minimum threshold, no liability is recognized before the specified minimum threshold is reached. The interpretation is not applicable for the Company and did not have any impact on its financial position or performance. TAS 36 Impairment of Assets - Recoverable amount disclosures for non-financial assets (Amended)

As a consequential amendment to TFRS 13 Fair Value Measurement, some of the disclosure requirements in TAS 36 Impairment of Assets regarding measurement of the recoverable amount of impaired assets has been modified. The amendments required additional disclosures about the measurement of impaired assets (or a group of assets) with a recoverable amount based on fair value minus their costs of disposal. The standard did not have any significant impact on the Company’s financial position or performance. TAS 39 Financial Instruments: Accounting and Measurement – Novation of derivatives and continuation of hedge accounting (Amendment)

The amendment provides an exception to the requirement for the discontinuation of hedge accounting in circumstances when a hedging instrument is required to be novated to a central counterparty as a result of laws or regulations. The standard did not have any impact on the Company’s financial position or performance. TFRS 10 Consolidated Financial Statements (amendment)

The TFRS 10 standard is amended to bring an exception regarding keeping the companies that fits into the definition of an investment company exempted from consolidation provisions. With this exception for the consolidation provisions, the investment companies are required to account their joint ventures by the fair value within the framework of TFRS 9 Financial Instruments standards. The amendment did not have any impact on the Company’s financial position or performance.

Yapı Kredi Faktoring A.Ş. Notes to Financial Statements as of 31 December 2014 (continued) (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

32

2. Basis of presentation of financial statements (continued)

ii) Standards issued but not in effect or early adopted

New standards, interpretations and amendments that have been declared as of the approval date of the financial statements, but not implemented or adopted early by the Company for the current reporting period are as follows. Unless otherwise indicated, the Company will make necessary amendments in its financial statements and disclosures after new standards and interpretations take effect. TFRS 9 Financial Instruments – Classification and Measurement

As amended in December 2012, the new standard is effective for accounting periods beginning 1 January 2015 onwards. The first phase of TFRS 9 introduces new provisions for classifying and measuring financial instruments. The amendments made to TFRS 9 will mainly affect the classification and measurement of financial assets and measurement of fair value option liabilities and requires that the change in fair value of a fair value option financial liability attributable to credit risk is presented under other comprehensive income. The Company will evaluate the impact of the standard on its financial position and performance as the other stages of the standard are approved by the POA. TAS 19 Defined Benefit Plans: Employee Contributions (Amendment)

TAS 19 mandates that an entity has to consider contributions from employees or third parties when accounting for defined benefit plans. The amendments clarifies that, if the amount of the contributions is independent of the number of years of service, contributions may be recognized as a reduction in the service cost in the period in which the related service is rendered, instead of attributing the contributions to the periods of service. The amendments will be applied retrospectively to accounting periods beginning 1 July 2014 onwards. The amendments will not have any impact on the Company’s financial position and performance. TFRS 11 – Accounting for Acquisitions of Interests in Joint Operations (Amendments)

TFRS 11 has been amended to provide guidance on the accounting for acquisitions of interests in joint operations in which the activity constitutes a business. The amendment requires that the acquirer of an interest in a joint operation in which the activity constitutes a business, as defined in TFRS 3, is required to apply all of the principles on business combinations accounting in TFRS 3 and other TFRSs with the exception of those principles that conflict with the guidance in TFRS 11. Additionally, the acquirer has to disclose information as required by TFRS 3 and other TFRSs regarding business combinations. The amendments will be applied prospectively to accounting periods beginning 1 January 2016 onwards. Early adoption is permitted. The amendments will not have any impact on the Company’s financial position and performance.

Yapı Kredi Faktoring A.Ş. Notes to Financial Statements as of 31 December 2014 (continued) (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

33

2. Basis of presentation of financial statements (continued) TAS 16 and TAS 38 - Clarification of Acceptable Methods of Depreciation and Amortisation (Amendments

to IAS 16 and IAS 38)

The amendments to TAS 16 and TAS 38 have prohibited the use of revenue-based depreciation for tangible assets, and significantly limited the use of revenue-based amortisation for intangible assets The amendments will be applied prospectively to accounting periods beginning 1 January 2016 onwards. Early adoption is permitted. The mentioned amendment will not have any impact on the Company’s financial position and performance. TAS 16 Tangible Assets and IAS 41 Agriculture: Bearer Plants (Amendments)

TAS 16 has been amended regarding the accounting of "bearer plants". The amendments provide the definition for bearer plant as a living plant that is used in the production or supply of agricultural produce after maturation, is expected to bear produce for more than one period, and is kept by the enterprise throughout its productive life. However, as mature bearer plants no longer undergo significant biological transformation and are used solely to grow produce, the amendments bring bearer plants from the scope of TAS 41 into the scope of TAS 16, and therefore enable entities to measure them at cost subsequent to initial recognition or at revaluation. The amendments also clarify that produce growing on bearer plants will be measured using the fair value less costs to sell approach prescribed by TAS 41. The amendments will be applied prospectively to accounting periods beginning 1 January 2016 onwards. Early adoption is permitted. The amendments are not applicable for the Company and will not have any impact on its financial position or performance. Annual Improvements to TAS/TFRS

In September 2014, POA issued the following amendments to the standards in relation to “Annual Improvements - 2010–2012 Period” and “Annual Improvements - 2011–2013 Period". The amendments are effective for accounting periods beginning 1 July 2014 onwards. Annual improvements - 2010–2012 Period

TFRS 2 Share-based Payment Definitions relating to vesting conditions have changed and performance condition and service condition are defined in order to clarify various issues. The change will be applied prospectively. TFRS 3 Business Combinations

Contingent consideration in a business acquisition that is not classified as equity is subsequently measured at fair value through profit or loss, regardless of whether it falls under the scope of TFRS 9 Financial Instruments or not. The change will be applied prospectively for the business mergers. TFRS 8 Operational Segments The amendments are; i) Operating segments may be combined/aggregated if they are consistent with the core principles of the standard. ii) The reconciliation of segment assets to total assets is only required to be disclosed if the reconciliation is reported to the chief operating decision maker. The amendments will be applied retrospectively.

Yapı Kredi Faktoring A.Ş. Notes to Financial Statements as of 31 December 2014 (continued) (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

34

2. Basis of presentation of financial statements (continued) TAS 16 Tangible Assets and TAS 38 Intangible Assets

The amendments to TAS 16.35(a) and TAS 38.80(a) clarify that revaluation can be performed as follows: i) Adjust the gross carrying amount of the asset to market value or ii) determine the market value of the carrying amount and adjust the gross carrying amount proportionately so that the resulting carrying amount equals the market value. The amendment will be applied retrospectively. TAS 24 Related Party Disclosures The amendment clarifies that a management entity – an entity that provides key management personnel services – is a related party subject to the related party disclosures. The amendment will be applied retrospectively. Annual Improvements - 2011-2013 Period

TFRS 3 Business Combinations The amendment clarifies that; i) Joint arrangements, as well as joint ventures, are outside the scope of TFRS 3 ii) The scope exception applies only to the accounting in the financial statements of the joint arrangement itself. The amendment will be applied prospectively. TFRS 13 Basis for Conclusions on Fair Value Measurement

The amendment clarifies that portfolio exception in TFRS 13 is applicable not only to financial assets and financial liabilities but to all other contracts under the scope of TAS 39. The amendment will be applied prospectively. TAS 40 Investment Property The amendment clarifies the interrelationship of TFRS 3 and TAS 40 when classifying property as investment property or owner-occupied property. The amendment will be applied prospectively. The amendments are not expected to have any material impact on the Company’s financial position or performance. New standards, amendments and interpretations that are issued by the International Accounting

Standards Board (IASB), but not issued by POA

The following standards, interpretations and amendments to existing IFRS standards are issued by the IASB but not yet effective up to the date of issuance of the consolidated financial statements. However, these standards, interpretations and amendments to existing IFRS standards are not yet adopted/issued by the POA, thus they do not constitute part of TFRS. The Company will make the necessary changes to its financial statements after the new standards and interpretations are issued and become effective under TFRS.

Yapı Kredi Faktoring A.Ş. Notes to Financial Statements as of 31 December 2014 (continued) (Figures expressed in thousand Turkish Lira (TL) unless otherwise stated)

35

2. Basis of presentation of financial statements (continued) Annual Improvements - 2010–2012 Cycle

TFRS 13 Fair Value Measurement As it is explained in the Justifications of the Decision, short term commercial amounts receivable and payables, that the amount of interest had not been indicated; may be denoted over its invoice amount, in situations where the discount effect is unimportant. The amendments will be applied immediately. Annual Improvements - 2011-2013 Cycle

IFRS 15 - Revenue from Contracts with Customers

In May 2014, the IASB issued IFRS 15 Revenue from Contracts with Customers. The new five-step model in the standard provides the recognition and measurement requirements of revenue. The standard applies to revenue from contracts with customers and provides a model for the sale of some non-financial assets that are not an output of the entity’s ordinary activities (e.g., the sale of tangible assets). IFRS 15 is effective for accounting periods beginning 1 January 2017 onwards. Early adoption is permitted. Entities will transition to the new standard following either a full retrospective approach or a modified retrospective approach. The modified retrospective approach would allow the standard to be applied beginning with the current period, with no restatement of the comparative periods, but additional disclosures are required. The impact of the amendment on the financial position or performance of the Company is under evaluation. IFRS 9 Financial Instruments - Final Standard (2014)

In July 2014 the IASB published the final version of IFRS 9 Financial Instruments. The final version of IFRS 9 brings together the classification and measurement, impairment and hedge accounting phases of the IASB’s project to replace IAS 39 Financial Instruments: Recognition and Measurement. IFRS 9 is built on a logical, single classification and measurement approach for financial assets that reflects the business model in which they are managed and their cash flow characteristics. Built upon this is a forward-looking expected credit loss model that will result in more timely recognition of loan losses and is a single model that is applicable to all financial instruments subject to impairment accounting. In addition, IFRS 9 addresses the so-called ‘own credit’ issue, whereby banks and others book gains through profit or loss as a result of the value of their own debt falling due to a decrease in credit worthiness when they have elected to measure that debt at fair value. The standard also includes an improved hedge accounting model to better link the economics of risk management with its accounting treatment. IFRS 9 is effective for accounting periods beginning 1 January 2018 onwards; however, early adoption is permitted. In addition, the own credit changes can be early applied in isolation without otherwise changing the accounting for financial instruments. The impact of the standard on the financial position or performance of the Company is under evaluation. IAS 27 - Equity Method in Separate Financial Statements (Amendments to IAS 27(