annual report 1998 - skf

TRANSCRIPT

Annual Report

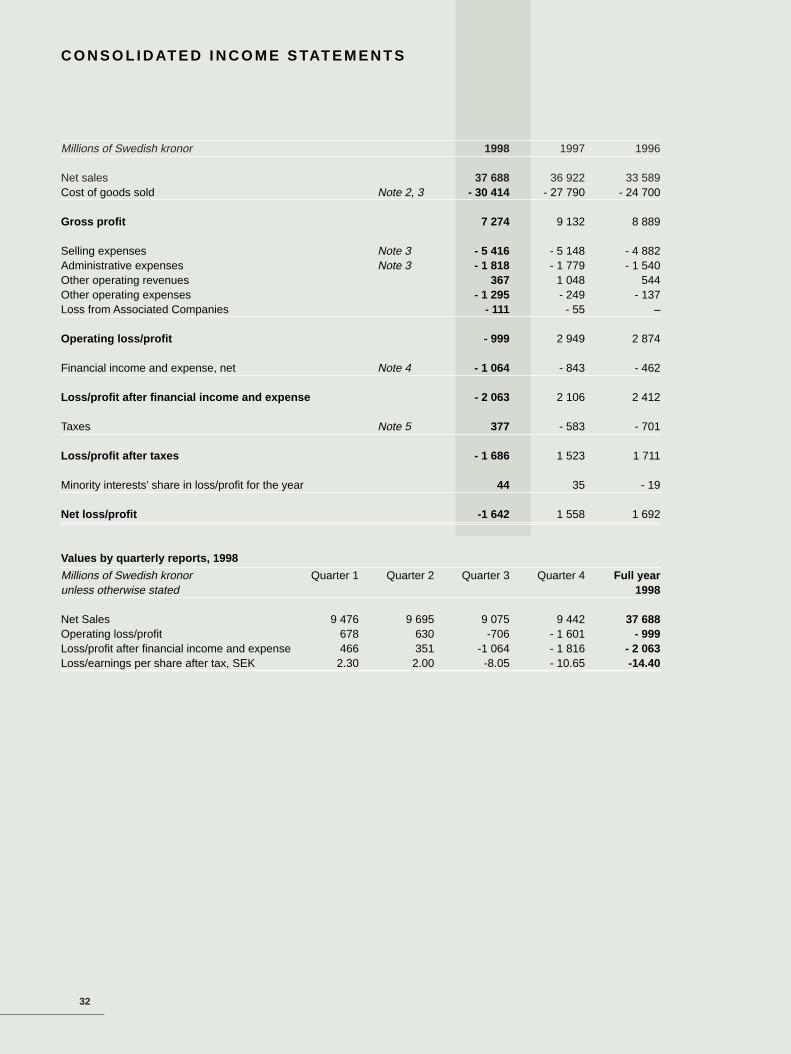

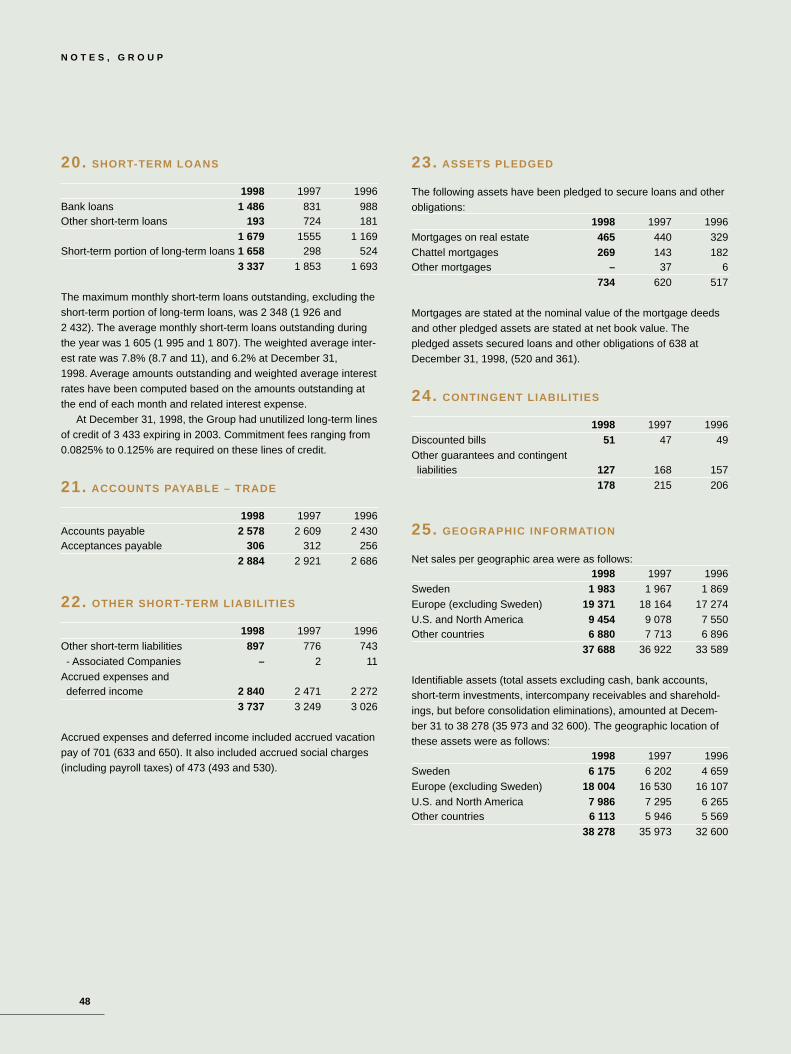

KEY FIGURES 1998 1997 1996

Net sales, MSEK 37 688 36 922 33 589

Operating loss/profit, MSEK - 999 2 949 2 874

Loss/profit after financial income

and expense, MSEK - 2 063 2 106 2 412

Additions to tangible assets, MSEK 2 148 2 664 2 710

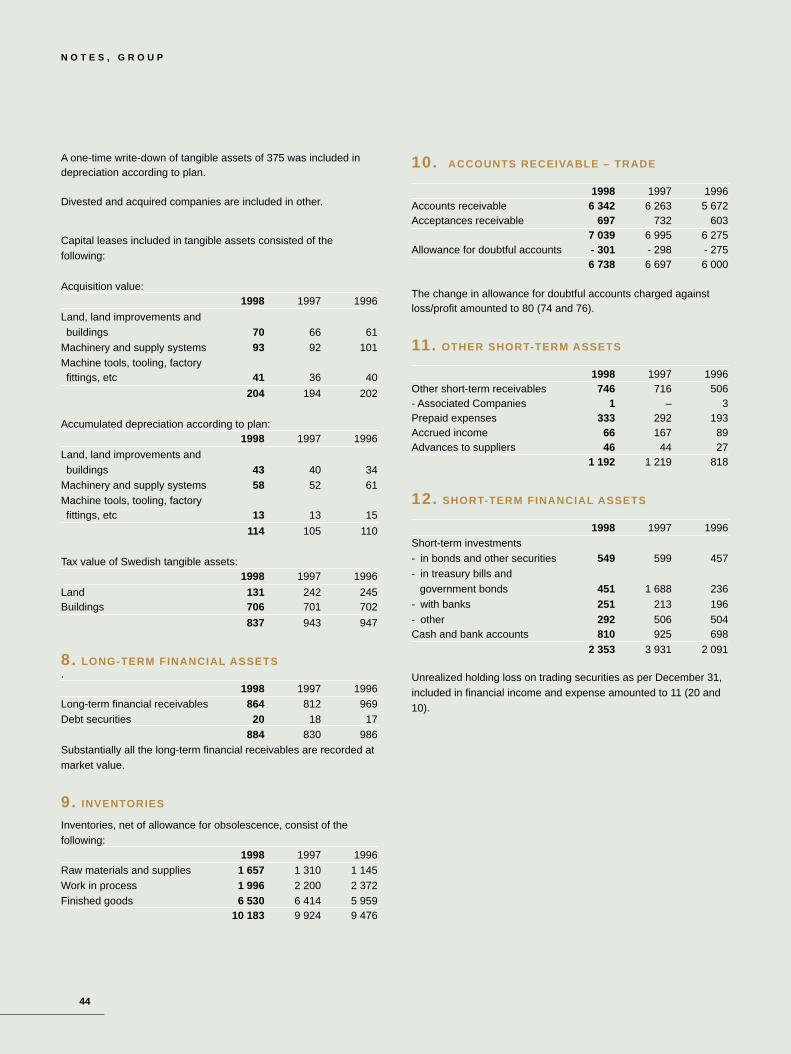

Loss/earnings per share after tax, SEK - 14.40 13.70 14.90

Dividend per share, SEK 2.00* 5.25 5.25

Return on capital employed, % - 2.8 13.0 14.7

Solvency, % 29.0 33.5 34.3

Number of employees registered 45 436 43 241 43 123

* Dividend according to the Board’s proposed distribution of surplus

PHOTO: Bertil Strandell, Håkan Ludwigsson, Lars Möller and many others

PRODUCTION: Malmer & Partners AB, 1999

’

Aftermarket Those customers, such asdistributors, who buy bearings for resaleas spare parts.

Angular contact ball bearing Bearing inwhich the raceways of the inner and outerring are displaced with respect to eachother in the direction of the bearing axis.This means that the bearing is particularlysuitable for the accommodation of simul-taneously acting radial and axial loads.

Axial load Load acting in the directionalong the shaft/axis.

Ball bearing Bearing with balls as rollingelements. May contain one or more rowsof balls.

Bearing Machine element for reducingthe friction between moving machineparts. Most bearings nowadays are rollingbearings, consisting of inner ring, outerring, a number of rolling elements (balls orrollers) and a cage. Most bearings aremade from steel.

Bearing housing Product in which arolling bearing is mounted for protectionand support. Made of cast metal or plasticand used in many different applications,such as fans, paper-making machines, etc.

Bearing unit Product in which the bear-ing has been integrated with other compo-nents in a single unit. The bearing isgreased for its entire lifetime.

Cage Bearing component which keepsthe balls or rollers separated from eachother when the bearing is rotating. Nor-mally made of steel, but sometimes ofbrass or plastic.

CARB™ Toroidal bearing – new bearingtype which can accomodate misalignmentand axial displacement of the shaft, andalso is compact. It has not been possibleto combine these properties in one bear-ing before.

Cylindrical roller bearing (CRB) Rollerbearing with cylindrical rollers.

Deep groove ball bearing (DGBB) Ballbearing where the balls run in grooves inthe inner and outer ring. The bearing is aradial bearing but can also take a certainaxial load. Used in such applications aselectric motors.

Elastomer Synthetic rubber.

Electromechanical fl ight control sys -tem System using electromechanicalactuators for moving the control surface ofthe aircraft.

Fly-by-wire System in which the surfacecontrols of the aircraft are powered byelectrically signaled actuators associatedto position transducers and flight controlcomputers.

Hub Unit /THBU Easy-to-mount, com-pact bearing unit for passenger car andtruck wheels.

Kits Kits where the bearing is suppliedtogether with the other components thatthe customer requires in order to performa given repair.

Lead time Time from the ordering of rawmaterial to delivery of the finished bear-ing.

Light trucks A designation used in theUS to cover everything from jeeps andvans to lightweight trucks.

Linear motor Electric motor which givesdirect linear movement and force withoutthe use of mechanical transformations.

Linear products Precision manufacturedcomponents, units and systems for linearmovement.

Needle roller bearing (NRB) Bearingwith long, thin cylindrical rollers. Used inapplications where space is limited, e gin gearboxes.

OEM customers Original EquipmentManufacturers – those customers whobuy bearings to use them in their ownproducts, e g manufacturers of cars,household appliances, machines, etc.

Positioning table Unit with linear guidescombined with linear drive element. Couldbe equipped with electric motor, measure-ment system and electronics for positioncontrol.

Precision bearing Bearing for machinetools with very high rotating speed. Usedin such applications as spindle units.

Radial bearing Ball or roller bearing forradial loads.

Radial load Load acting in a directionperpendicular to the shaft/axis, i e alongthe radius.

Radial seal A type of oil seal.

Roller bearing Bearing with rollers asrolling elements. May contain one or morerows of rollers.

Rolling bearing steel Very clean specialsteel for rolling bearing production.

Rolling bearings Common name for balland roller bearings.

Rolling elements Common name for theballs and rollers in a bearing.

Rolling/milling Method of processing steelto produce the desired products (bar, wire,sheet and tube).

Seal Steel or rubber component which ismounted between the outer and the innerring in a bearing, or around the shaft outsidethe bearing, to prevent dirt and moisturefrom entering the bearing and the lubricantfrom leaking out. Bearings which do nothave seals are often mounted in sealedbearing housings, for example. Seals arealso used in many other applications (egValve stem seal, Shock absorber seal).

Sensor Electric transmitter which registersrevolutions, speed, temperature, etc. Inte-grated in wheel bearing units and certaindeep groove ball bearings.

Shock absorber seal Sealing ring, spe-cially designed for short, shock-loaded axialmovements.

SKF Engineering & Research Centre B.V .(ERC) SKF’s research center in theNetherlands.

Spherical bearing Ball bearing (SABB) orroller bearing (SRB) where the inside sur-face of the outer ring is part of a sphere,which means that the bearing can adaptitself to misalignment of the shaft. SKF wasfounded on Sven Wingquist’s revolutionaryinvention of the double row spherical ballbearing.

Spindle unit Complete bearing unit withprecision bearings for machine tools.

Taper roller bearing (TRB) Roller bearingwith tapered rollers.

Thrust bearing Ball or roller bearing foraxial loads.

TQM Total Quality Management – qualityconcept within SKF comprising production,products, employees, service and attitudes.

Trouble-Free Operation (TFO) A concept,developed by SKF, which aims at giving thecustomer as trouble-free an operation aspossible. The concept is often tailor-madeand includes products and service, mainte-nance products, training, monitoring andother equipment.

Valve stem seal Seal for control and meter-ing of oil lubrication for inlet and outletvalves of combustion engines.

Accounting Principles Principles forhow specific transactions should beaccounted for.

Associated company A company inwhich the SKF Group has an interestrepresenting between 20 and 50% of thevoting rights, and where the SKF Grouphas a significant influence.

Break-even The sales volume whereincome and costs are equal, i e a zeroresult is achieved.

Capital employed The value of acompany's total assets, minus non-interest bearing liabilities.

Cash management Control strategiesover the company’s cash flows, in addi-tion to investment strategies on excessfunds.

Cash Flow A company's cashsurplus/deficit from the ongoing opera-tions.

Convertible Bonds An option to converta loan for a predetermined number ofcommon shares.

Cost effi ciency Within SKF there is anongoing effort to eliminate non-valueadded activities and to standardizeremaining activities to achieve highprofitability and efficiency.

Credit risk Risk that the borrower doesnot fulfil his obligations towards thelender.

Deferred tax Differences betweenaccounted and fiscal valuations ofassets and debts creates deferred taxliabilities and deferred tax assets, repre-senting future tax payment.

FIFO (First In First Out) The methodused by SKF to calculate which productsare still in stock, compared with LIFO(Last In First Out).

Financial derivatives An instrumentwhich is derived from, for example, anunderlying currency or interest rate.(See also Forward exchange contracts.)

Financial Year A financial year is theperiod in which the result of the opera-tions is measured. In SKF the financialyear is the same as the calendar year.

Forward exchange contracts A deriva-tive instrument where the companyagrees to buy or sell a certain currencyat a predetermined rate and date. Theagreement is obligatory for the company.

Hedge A financial contract made inorder to secure the value of an asset orliability or a future cash flow.

Interest-rate risk Risk for a loss in a fixinterest rate security due to changes inthe interest rate.

Issue A group of stocks or bonds thatare offered or sold at the same time.

Joint-venture company A company,formed by two or more companies, inwhich the risk is shared in relation to forexample capital input.

Operating Income Result generatedfrom a company's operations, i e incomeminus cost of goods sold minus salesand administrative expenses.

Price and mix Volume shifts betweenvarious customer segments withdifferent price levels.

Rating Official judgement of acompany's financial strength made by afinancial institute on behalf of potentiallenders.

Return Yield, in the form of dividends orinterest payments, on invested capital.

Risk-bearing capital The investedcapital in a company, usually stock andequity as opposed to bonds and loans.

Risk limits The maximum acceptablerisk of loss according to the pre-determined risk policy.

Sale/lease back A transaction where anasset is sold, and then leased back bythe original owner.

SFAS Accounting recommendationsissued by the U.S. Financial AccountingStandards Board.

Solvency The part of the company'stotal financing that is not financed withloans or other liabilities, i e share-holders’ equity's part of total assets.

Volatility A statistical function thatmeasures the speed of change of theprice of a commodity.

U.S. GAAP Generally AcceptedAccounting Principles in the U.S.

Financial information and reportingAB SKF will publish the following financial reports in 1999Report on 1998 operations . . . . . . . . . . . . . . . . .January 28Annual Report 1998 . . . . . . . . . . . . . . . . . . . . . . . .March 18Interim report January-March 1999 . . . . . . . . . . . . .April 22Interim report January-June 1999 . . . . . . . . . . . . . . .July 15Interim report January-September 1999 . . . . . . .October 21

The reports are available in Swedish and English. They aresent automatically to those shareholders who haveinformed the Company that they wish to receive them. Theycan also be ordered fromSKF Group CommunicationSE-415 50 GöteborgSwedentel +46-31-337 19 88, fax +46-31-337 17 22

The financial reports are also published on SKF’s home-page on the Internet www.skf.com

An annual report, Form 20-F, is produced for the Securitiesand Exchange Commission in the US.

Annual General MeetingThe Annual General Meeting will be held at SKFKristinedal, Byfogdegatan 4, Göteborg, Sweden, at 3.30p.m. on Thursday, April 22, 1999.

In order to participate in the meeting, shareholders must be recorded in the shareholders’ register maintained

by the Securities Register Centre (VPC AB) by Mon-day, April 12, 1999.

must notify the Company before noon on Monday, April 19,1999, of their intention to attend (AB SKF, Group Legal,SE-415 50 Göteborg, Sweden, tel +46-31-337 24 36,fax +46-31-337 16 91), giving details of name, address,telephone and shareholding.

Shareholders whose shares are registered in the name of atrustee through the Trust Department of a bank must havetheir shares temporarily re-registered in their own names.Sharesholders must notify their trustees of their wish to re-register their shares in plenty of time before April 12.

Payment of dividendsApril 27, 1999, is proposed as the record date for share-holders entitled to receive dividends for 1998. If this date isaccepted by the Annual General Meeting, it is expected thatthe Securities Register Centre will send out notices of pay-ment on May 4, 1999.

SKF Environmental Report 1998The Environmental Report, which is distributed togetherwith the Annual Report, is a comprehensive description ofthe SKF Group’s environmental activities during the year.

Aktiebolaget SKF, SE-415 50 Göteborg, Sweden

Telephone +46-31-337 10 00, fax +46-31-337 28 32, www.skf.com

S K F ’ s V I S I O N

is to be recognized as the world leader in

bearings, seals and related products.

We will achieve this by being the best

company in the industry in:

• providing customer value

• developing our employees

• creating shareholder value

T H I S I S S K F

SKF was founded in 1907 and since then

has always occupied a position in the front

line of technical innovation. Since its start,

SKF has been responsible for most of the

pioneering inventions within rolling bearing

technology. Thanks to having adopted an

aggressive focus from the start, SKF is

today the world’s leading producer of rolling

bearings and also holds a leading position

within special steels and elastomeric seals.

With some 80 production sites in 23 coun-

tries and sales through the Group’s own

sales companies and/or via authorized dis-

tributors in virtually all of the world’s coun-

tries, SKF is always close to the customer.

Zinc mine in Canada

page 6

Filter bed in Austria

page 10

SKF in Formula 1

page 14

Assembly of snowmobile in Finland

page 8

Industrial distributor in Singapore

page 17

Truck customer in the U.S.

page 20

Bearing simulation program

page 30

C O N T E N T S

SKF Group 2

The Chairman’s Review 4

Letter from the President 5

Board of Directors’ Report 7

The Board of Directors and its work procedures 9

Environment 10

Bearings 11

Seals 19

Steel 23

Financial objectives and dividend policy 26

Financial risk management 26

EMU 27

Year 2000 28

Technical development 30

F I N A N C I A L I N F O R M AT I O N

Consolidated income statements 32

Consolidated balance sheets 34

Consolidated statements of cash flow 36

Notes to the consolidated financial statements 38

U.S. GAAP 51

Parent Company income statements 58

Parent Company statements of cash flow 58

Parent Company balance sheets 59

Notes to the financial statements for the Parent Company 60

Proposed distribution of surplus 65

Auditors’ report 65

Shares and shareholders 66

Board of Directors 68

Management 70

Seven-year review of the SKF Group 72

Words in SKF’s world 73

Financial glossary 74

In January 1999 the SKF Group received a worldwide ISO

14001 certification, the international standard for environ-

mental management. Considering the global spread of SKF

manufacturing sites and customers, consistency is probably

the most important feature resulting from our endeavours to

achieve such a worldwide certification.

One of our ambitions is to select suppliers and raw mate-

rials that are least harmful to the environment. With respect to

the printing process, it is therefore important to us that our

suppliers use only processes and materials which are environ-

mentally approved. That is why we have chosen to print this

publication at the Falkenbergs Tryckeri AB, Sweden and on

Arctic stock from Håfreströms AB, Sweden, both environmen-

tally approved.

2

S T E E L

B E A R I N G S

This is SKF SKF's strength factors

S E A L S

The function of a rolling bearing is to min-imize the friction between a fixed and amoving surface, and to carry a load. SKFis the world’s leading rolling-bearing com-pany, with more than 50 bearing produc-tion facilities in 21 countries. A globalsales organization, consisting of whollyowned sales companies and 7 000 distribu-tors and dealers, annually supplies aroundone million customers in more than 130countries with bearings from a range ofmore than 20 000 varieties.

SKF’s determined focus on research anddevelopment has given the company aposition as the bearing-technology leader,with a large number of pioneering innova-tions that have established standards forthe entire industry. These range from SvenWingquist’s self-aligning ball bearing,through the Hub Unit to CARB™. Aworldwide sales and distribution networkassures that SKF remains close to its cus-tomers, wherever they are located, while ahighly qualified corps of application engi-neers is always available to resolve techni-cal problems.

The function of a seal is to separate amachine element from the outside world,either to prevent dirt and moisture comingin, or to avoid lubricants leaking out.Through its subsidiary Chicago Rawhide,SKF is the leading manufacturer of radialseals in the US. Chicago Rawhide is, with6 plants in the US, the largest company inthe Seals Division, which also includesRFT in Italy, Europe’s leading bearing-sealscompany, CR Elastomere in Germany,wholly owned production companies inIndia and Mexico, and three joint-venturecompanies: in Japan, China and Korea.

Chicago Rawhide has a very strong posi-tion in the US automotive aftermarketwhere the trademark CR is well estab-lished. Sales of SKF bearings to the USautomotive aftermarket are also made viaChicago Rawhide, which further enhancesthe service level to this important market.In Europe, the division’s position is beingstrengthened by CR Elastomere’s productrange. Here, the division takes advantageof SKF’s efficient distribution system forrolling bearings.

The steel from which rolling bearings areproduced is vital to the quality of the bear-ings. Ovako Steel is Europe’s leadingrolling bearing-steel company and sellsslightly less than half its production toSKF’s bearing manufacturing plants. Anincreasing share is sold to other bearingmanufacturers and certain highly demand-ing applications primarily within WesternEurope’s machinery and automotive sectors. The steel is manufactured inHofors (Sweden). Ovako Steel also hasmanufacturing facilities in France, theU.K. and the US.

Analysis precision and freedom frominclusions are factors that are critical to thebearing’s operational lifetime. Ovako Steelproduces the cleanest steel in the world.The long association with SKF and theintegration achieved between the two com-panies, has provided Ovako Steel with aunique competence and competitiveness.The extensive restructuring in recent years,the shift in focus to rolling bearing steeland the divestment of parts of the salesorganization have further strengthened thecompany.

3

S K F G R O U P

SKF’s customers Performance in 1998 What lies ahead?

Trucks 7%

Cars 16%

Industrialdistribution 27%

Specializedindustries 9%

Generalmachinery 14%

Aerospace 5%

Customizedengineering 9%

Vehiclereplacement 7%

Electricalindustry 6%

Cars 32%

Industrialdistribution

11%

Vehiclereplacement37%

Aerospace3%

Trucks 4%

Electricalindustry 1%

Generalmachinery

12%

Cars 10%

Industrialdistribution 15%

Customizedengineering 7%

Trucks 4%

General machinery

50%

Electricalindustry 2%

Specializedindustries 12%

Increased sales to car and truck customersin both Western Europe and the US com-pensated for the downturn within heavyindustry caused by the economic crisis inAsia. Deliveries increased but the changein customer mix and the severe competi-tion led to depressed prices and lowerearnings. Extensive measures were initi-ated to change the structure of the Group’sbearing operations. Loss-making and lessprofitable operations were discontinuedand resources redirected towards profitableparts of the business. A new division, withresponsibility for the industrial aftermar-ket, was established.

The focus on developing the Group’s prof-itable bearing operations will be strength-ened. The aftermarket will be assignedgreater prominence. Service centers will bebuilt up to cultivate the service market. Theefficiency enhancement programs will elimi-nate loss-making operations and improveearnings. Further reductions will be made tothe product range and inventories. Invest-ments will focus on plant rationalization andmodernization programs. Flexibility withinthe plants will increase by reducing resettingtimes and raising production frequency. Thedevelopment of new products with higheradded value is continuing and new productswill be launched in the market.

Chicago Rawhide continued to strengthenits international presence in order to meetits customers’ increasing globalization.Manufacturing units were established inKorea and Mexico. Production operationswill be started in India during the first quar-ter of 1999. Restructuring in the distributorsegment in the US led to the establishmentof new customer groups and inventoryreductions, which resulted in declined prof-itability. In Europe operations developedfavorably as a result of deliveries to theautomotive sector in Western Europe andmore widespread use of sealed bearings.

The division will develop and strengthen itspresence in the newer markets where ChicagoRawhide has its own production operations.Dependence on the North American marketwill therefore decrease to some extent. Inorder to restore profitability, the divisionwill also increase its focus on more prof-itable areas of operation. The focus onindustrial customers and the aftermarket inWestern Europe will continue, with the aimof increasing market share. Product devel-opment and the production of new productsis continuing, as is the division’s focus onthe aviation sector, which is expected togenerate good results during 1999.

After a good start to the year, demand grad-ually declined due to production decreasesin the Group’s bearing plants and lowerdemand from external customers. Steelproduction totalled approximately 423 000tons. An important milestone for OvakoSteel during the year was the start-up of thenew tube mill in Hofors, Sweden. Usingadvanced technology, the new tube millwill lead to improved productivity withinsteel operations and more cost-effectivebearing production. The decision was madeto sell or discontinue forging operations inArvika, which have operated at a loss forseveral years.

Efforts to increase the amount of steel soldoutside the SKF Group, which are alreadybeginning to show material results, willcontinue. Deliveries of seamless hot-rolledtubes from the new tube mill in Hofors,Sweden, will gradually increase when themill is fully run-in during the first quarterof 1999. Demand for tubes is alreadygood. The first six months of 1999 will becharacterized by the introduction of a com-pletely new and totally integrated adminis-trative system.

increased focus on operations in which theGroup holds strong, leading positions, willlead to a positive earnings trend for SKF.

In conclusion, I would like to take thisopportunity on behalf of the Board to thankthe Group’s employees for their good workin an extremely tough competitive climate.The ongoing restructuring of the companyhas also placed extra demands on theefforts of all employees.

Göteborg, January 28, 1999

Chairman of the Board

4

’

To a large extent, global economicdevelopments during 1998 wereshaped by the financial crisis that

started in Southeast Asia in summer 1997.

The effects spread like rings on water, fol-lowing the first devaluation. What started asa financial problem in a few countriesdeveloped into economic crises in manyAsian countries and resulted in serious dis-ruptions to the world economy. The weak-ening demand and virtually a total morato-rium on investments in Asian infrastructureled to reduced demand for the products ofEuropean and US suppliers. As a result,production activity in heavy industriesdeclined, which compounded the escalatinguncertainty regarding economic develop-ments in the rest of the world.

The sharp currency devaluations in manyAsian countries improved the internationalcompetitiveness of local companies. Thistrend is increasing the need for continuedstructural changes among Western com-panies, to enable them to assert themselvesin the face of the growing competition.

As the year progressed, a more generaldecline became increasingly evident in theeconomy. In its six-month report, SKFalready drew attention to the decrease indemand that had become noticeable withinheavy industries in both Western Europeand North America. This was a disturbing

factor, particularly in view of the fact thatthe Group’s profitability had weakenedsteadily during the preceding three years,despite favorable demand and growing vol-umes. At the same time, the intense compe-tition remained unchanged. Although various packages of measures had been ini-tiated in an effort to reverse the negativeprofit trend, their expected effects did notmaterialize.

A management change occurred on September 1, 1998, when Sune Carlssontook up the position as President and Chief Executive Officer. Accordingly, Peter Augustsson left the Group.

Additional action programs were initiatedduring the autumn. These entailed the ter-mination and restructuring of certain loss-making operations and a clearly statedfocus on improving the Group’s profitabil-ity. To enable the necessary changes in theGroup structure, the Board decided to postprovisions totalling SEK 3.1 billion, whichwere charged against profit for 1998. As aresult, SKF was forced to report a large lossfor the fiscal year.

In view of the loss incurred for 1998, theBoard proposes that a dividend of SEK 2.00be paid per share.

I am convinced, as is the Board as a whole,that the ongoing programs, with an

I n 1998, the demand trend for SKFproducts turned downwards in mostmarkets and customer segments.

Competition increased and low inflationsharpened the price pressure in the market.The rate of capacity utilization within theGroup’s production units was unsatisfac-tory, particularly towards the end of theyear, when a necessary reduction of inven-tories was made. In total, the SKF Groupreported a substantial loss after provisionsof MSEK 3 135 for the 1998 fiscal year.

In order to build the foundation for afavorable profit trend at SKF, an extensiveprogram of efficiency enhancement andrestructuring measures was decided duringthe year. These measures are currently beingimplemented with high speed. More long-term work was initiated to strengthen SKF’smarketing activities and develop the Group’sstronger businesses. It should be noted thata considerable proportion of SKF’s approxi-mately 400 profit centers are showinghealthy profitability and that many of themalso posted improved profits in 1998.

The aim of the ongoing efficiency pro-gram is to cut costs by reducing the numberof employees by 4 000 prior to the end of1999. To alleviate the social consequencesof the personnel cutbacks, early retirementsolutions have been applied extensively.Approximately half of the planned programof measures had been implemented byDecember 31, 1998.

During the autumn, a review was madeof a number of operations that had givenrise to substantial losses, in many casesover a considerable period of time. Amongother consequences, this resulted in deci-sions to exit the textile machinery compo-nents area, to terminate the production oftaper roller bearings in the US and to closea seals plant in the US. In addition, a deci-sion was taken to exit the forging businessin Arvika. Production capacity in Brazil isbeing reduced sharply due to weak demand.These restructuring measures will result ina further reduction of the workforce involv-ing approximately 2 000 employees.

Due to the difficult market situation,SKF’s strategy for expansion in Asia wasfocused on improving the earnings ofrecently acquired companies. Towards theend of the year, there was a certain stabi-lization of demand in the region. The fun-damental assessment that Asia is an impor-tant market for SKF’s long-term expansionstands firm.

SKF’s organization was streamlinedduring 1998. Bearing operations are noworganized in four global divisions, eachwith a distinct market focus: Automotive,Electrical, Industrial and Service. TheComponents, Emerging & Specialty andAsia Pacific divisions were integratedwithin these divisions. The Seals and Steeldivisions remain essentially unchanged.

The Group will review its customerfocus with the aim of developing value

added business strategies to strengthen ourcompetetive advantages. In an effort toimprove profitability, considerable attentionwill be assigned to marketing, logistics,pricing and customer segmentation matters.The industrial aftermarket still has substan-tial potential and will thus continue to be atarget area for SKF.

Another area that will be assigned prior-ity is the SKF Group’s structure and level ofintegration. The aim is to reduce the highamount of tied-up capital and to improvecash flow.

The business during 1998 was marked byan increasingly difficult market climate andby extensive changes within SKF aimed atimproving profitability. Demand is expectedto continue to decline this year. Earningsfor the next few quarters are likely toremain weak until the efficiency improve-ment programs start to improve the profit.

Göteborg, January 28, 1999

President

5

6

SKF distributor Fred E. Shillington, Canadian Bearings Ltd., shown here withDenis J. Babin, Noranda Inc., Brunswick Mine, during a visit to the Bathurstzinc mine in eastern Canada. This is a good example of a successful tripartiterelationship between SKF, the distributor and the customer. The customer,Brunswick Mine, has access to all information from SKF with regard to techni-cal support, delivery capacity, prices and other key data. In return, SKFreceives all necessary information about the mining company’s requirementsvia the distributor.

7

’

2000 by which time all of the activities willhave been implemented.

These structural changes also mean thatthe number of employees in the Group willbe decreased by a further approximately2 000 persons, in addition to the 4 000announced earlier.

The total cost of the programs approvedduring 1998 was MSEK 3 135 and wascharged against Group earnings in anamount of MSEK 1 216 during the thirdquarter and MSEK 1 919 during the fourthquarter.

During the year, focus was increased onthe profitable industrial aftermarket forrolling bearings through the establishmentof the Service Division, with global respon-sibility for this segment. An important partof the new division’s operations is thedevelopment of new products and servicesto support its network of industrial distribu-tors and MRO (Maintenance & RepairOperations) customers. In this field SKFcan draw upon its unique competence andextensive and in-depth know-how of bear-ing technology, supplemented by a largeand experienced team of field engineers.

The Group’s financial net was MSEK -1 064 (-843). The deterioration was mainlyattributable to increased net borrowingsduring the year, currency losses in joint-venture companies in Asia and a MSEK110 write-down of SKF’s shareholding inthe Chinese bearing company WafangdianBearing Company Limited.

Group inventories expressed as a per-centage of annual sales amounted to 27%(27) at the end of the year. In terms ofvalue, inventories totalled MSEK 10 183 asof December 31, 1998 (9 924).

There was a build-up of inventories atthe beginning of 1998 to meet expected

There has been a growing overcapacityin the bearing industry in recent years. Thishas led to a battle for market share, whichhas had an adverse effect on sales price lev-els. Despite a favorable productivity trendin the SKF factories, the improvementswere insufficient to offset the negative con-sequences of the price trend.

To reverse the negative trend affectingSKF in recent years, the Group’s strategywas changed to prioritize profitability ratherthan volume expansion and discontinueunprofitable operations.

The cost-reduction measures announcedin autumn 1997 and June 1998 will result incost decreases amounting to approximatelyMSEK 1 500. The restructuring programdecided in autumn 1998 is intended toimprove earnings by about MSEK 600. Thefull impact will not be felt until fiscal year

In 1998, SKF reported a loss, afterfinancial income and expense, ofMSEK 2 063, compared with profitof MSEK 2 106 in 1997. Excluding

provisions, the profit would have beenMSEK 1 072, down by 49% comparedwith 1997.

Group net sales increased 2% to MSEK37 688, compared with MSEK 36 922 in1997. Additional volumes accounted for3.5% of the increase, compared with 7% in1997. Currency changes led to net salesincreasing by 1.0% when translated intoSEK.

The price and product mix trend had anegative impact of 2.0% on Group sales,compared with 1997. The increased vol-umes were mainly sold to customers whopurchase large volumes, but who provideSKF with lower margins.

Group operating earnings declined in the 1998 fiscal year to a loss of MSEK 999,compared with profit of

MSEK 2 949 in 1997. Operating earnings were charged with provisions amounting to MSEK 3025.

Excluding these provisions,the operating profit would have been MSEK 2026,down by 31% compared

with 1997.

A snowmobile is tested following final assembly at the Lynx-Bombardien plant in Rovaniemi, Finland.

8

higher demand that never materialized. Theinventory levels were reduced during thesecond half of the year. This had an adverseeffect on manufacturing costs.

The loss per share amounted to SEK14.40, compared with earnings per share ofSEK 13.70 in 1997.

The Group’s solvency deteriorated from33.5% at year-end 1997 to 29.0% at the endof 1998 as a result of the provisions madefor the efficiency enhancement program.

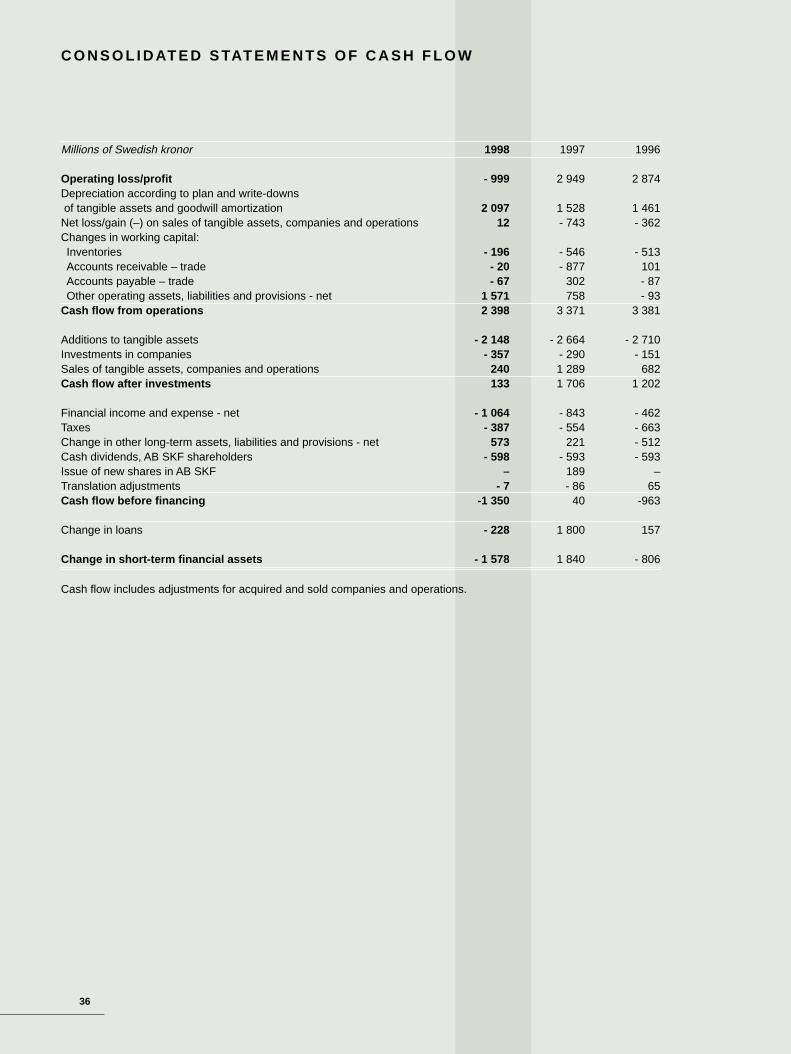

Interest-bearing loans at year-end 1998totalled MSEK 8 179 (8 391), while pen-sion liabilities amounted to MSEK 7 139(6 171). As of the same date, the Group hadfinancial assets of MSEK 3 237 (4 761),including short-term financial assets ofMSEK 2 353 (3 931).

SKF’s capital expenditure in tangibleassets amounted to MSEK 2 148 (2 664).Depreciation according to plan was MSEK 1 722 (1 528).

Approximately MSEK 149 (120) of theGroup’s total capital expenditure is attribut-able to environmental investments, the aimof which is to improve SKF’s internal andexternal environment.

Capital expenditure during the next fewyears is expected to be slightly lower thanannual Group depreciations.

Investments in research and developmentamounted to MSEK 702 (757), correspond-ing to 1.9% (2.1) of annual sales. Thisamount includes only investments in prod-uct and process development.

SKF is aiming at a high rate of innova-tion. During 1998, SKF submitted 145 firsttime patent applications. This can be com-pared with the 146 submitted in 1997 and130 in 1996.

SKF increased its focus on training of itsemployees during 1998. The Learning Cen-tre (TLC) was established at SKF’s corpo-rate head office. During the year, trainingprograms were conducted in such areas asleadership, project management and finan-cial and international management. TLCand the SKF College, which focuses onproviding technical training, arrangedcourses for about 700 SKF employees dur-ing the year.

An international training program formanagers, the Global Leadership Pro-gramme, was introduced in 1998. Eachparticipant is assigned and carries out a personal development project during a 12-month period under the supervision of theimmediate superior and a selected mentor.

Group work in the quality area continuesat a high rate. The TQM (Total Quality

Management) process has resulted in agrowing number of production channelsreporting “Zero Defects,” meaning that nocustomer complaints have been receivedduring a 12-month period. In general, thenumber of customer complaints has beenhalved during the past four years.

Final stages on the snowmobile assembly line at the Lynx-Bombardien plant on the Arctic Circle in Rovaniemi, northern Finland. Lynx-Bombardien is Europe’s sole producer of snowmobiles, which are used extensively throughout the Arctic area. Since it is common forfamilies in the region to have one or more snowmobiles, a strong aftermarket is being opened up for various SKF products.

Steel tubes from Ovako Steel are sold to cus-tomers in Italy via the distributor Sandvik Italia.

9

B O A R D O F D I R E C T O R S ’ R E P O R T

Geographic distibution of net sales, average number of employees and

tangible assets (percent)

25

1419

5358

65

39

3

6 5 4

10 129North America

Western EuropeCentral and

Eastern Europe

3 20

Middle Eastand Africa

Asia

Latin America

Net sales

Average number of employees

Tangible assets

The Board of Directors and itswork procedures

The Annual General Meeting of AB SKF,held in the spring of 1998, elected tenBoard members. In addition hereto twomembers and two deputy members havebeen appointed by the employees. Peter

Augustsson left as President of the Com-pany and as member of the Board of Direc-tors as of August 31, 1998.

During 1998 the Board held nine meet-ings. The Board has adopted written rulesof procedure for its internal work. Theserules confirm already existing practice andcontain i a rules regarding

Trucks 6%

Cars 18%

Generalmachinery 15%

Specializedindustries 8%

Customizedengineering 8%

Industrialdistribution 27%

Aerospace 4%

Electricalindustry 5%

Vehicle replacement 9%

• number of Board meetings and timingfor Board meetings

• items normally included in the Boardagenda

• presentation to the Board of reports fromthe external auditors

The Board has also issued writteninstructions regarding

• when and how information required forthe Board’s assessment of the Company’sand the Group’s financial position shall becollected and reported to the Board;

• allocation of the tasks between the Boardand the President; and

• the order in which the deputy Presidentsshall act in the President’s absence.

Also these written instructions confirmalready existing practice within the Com-pany.

Net sales by customer segment 1998

10

The year 1998 was a special yearfor SKF and the environment, asthe Group received worldwidecertification to ISO 14001: the

international standard for environmentalmanagement. The global certificate coversSKF’s manufacturing units in 17 countriesspread over five continents, and reflects thecompany’s standing as the worldwide leaderin its business.

Coping with cultural differences

The project for global approval to ISO14001 included SKF’s factories in India,South Africa and Poland, where environ-mental awareness has traditionally beenmuch lower than in our factories in WesternEurope and the US. The Group’s employeesin these countries worked extremely hard toachieve the very high standards required forISO certification, concentrating especiallyon awareness training and culture change.The SKF factory at Poznan in Poland thusbecome one of the first organizations in thatcountry to be approved to ISO 14001.

Cost-effective strategy developed

SKF applied to a leading certification bodyfor a single ISO 14001 certificate coveringall manufacturing units in the Group, ratherthan individual certificates for each unit. Bydeveloping a single environmental manage-ment system (EMS) which could be usedby all its factories worldwide, SKF could beassessed by the auditors as one companyrather than as numerous individual units.This strategy substantially reduces the costsfor certification and subsequent surveil-lance audits.

Widespread benefi ts ofcertifi cation

SKF’s ISO 14001 approval will benefit cus-tomers, employees, shareholders and theenvironment. The certification providesassurance to customers, to shareholders andto other interested parties that SKF takes itsenvironmental responsibility seriously; thushelping customers meet their own obliga-tions.

The certification has also helpedemployee development. Extensive trainingwas necessary to ensure that the Group’semployees had sufficient environmentalawareness to operate the management sys-tem, and this training has allowed employ-ees to take on greater responsibility andauthority. More than 20 000 employeeshave passed different types of environmen-tal training.

ISO 14001 should also increase share-holder value, by helping to improve thelong-term stability of the company. Envi-ronmental accidents can be very expensiveto rectify, and may lead to damaging pub-licity and loss of reputation for any com-pany. An effective environmental manage-ment system should minimize the potentialfor accidents and emergencies. This notonly safeguards the environment, but alsoprotects the company and the share value.

Of course, the environment is the mostimportant beneficiary of the Group’sapproval to ISO 14001, as the standardfocuses on continual improvement of envi-ronmental care. Examples of such improve-ments around the Group can be found in theSKF Environmental Report 1998.

Accidents and injuries reducedagain

1998 provided further evidence of thedownward trend in the number of work-related accidents and injuries in the Group.SKF Pune in India showed a 23% reductionin the number of injuries in 1998, but thebest result was achieved by the plant atAltoona, PA, in the United States. They hadno lost time due to injuries during the entireyear.

SKF Environmental Report 1998

The Environmental Report, which is dis-tributed with the Annual Report, is a com-prehensive description of the SKF Group’senvironmental activities during the year.

Filter beds at SKF Österreich in Steyr separate grinding waste from coolant liquid so that both can berecycled.

The bearing business reported a substan-

tial loss for 1998 due to comprehensive

provisions for restructuring. Operating

earnings amounted to a loss of MSEK

1 177 compared with a profit of MSEK

2 294 in 1997. Operating earnings were

charged with provisions of MSEK 2 882.

Excluding these restructuring provisions

operating earnings would have been

MSEK 1 705.

Sales of bearings increased during

1998 to MSEK 32 453 (31 991).

0

7 000

14 000

21 000

28 000

35 000

96 97 98

29 2

04

31 9

91

32 4

53

- 1 500

0

1 500

3 000

96 97 98

2 48

2

2 29

4

- 1

177

0

5 00

1 000

1 500

2 000

2 500

96 97 98

2 24

9

2 08

7

1 64

1

0

10 000

20 000

30 000

40 000

96 97 98

36 7

01

36 6

42

37 9

16

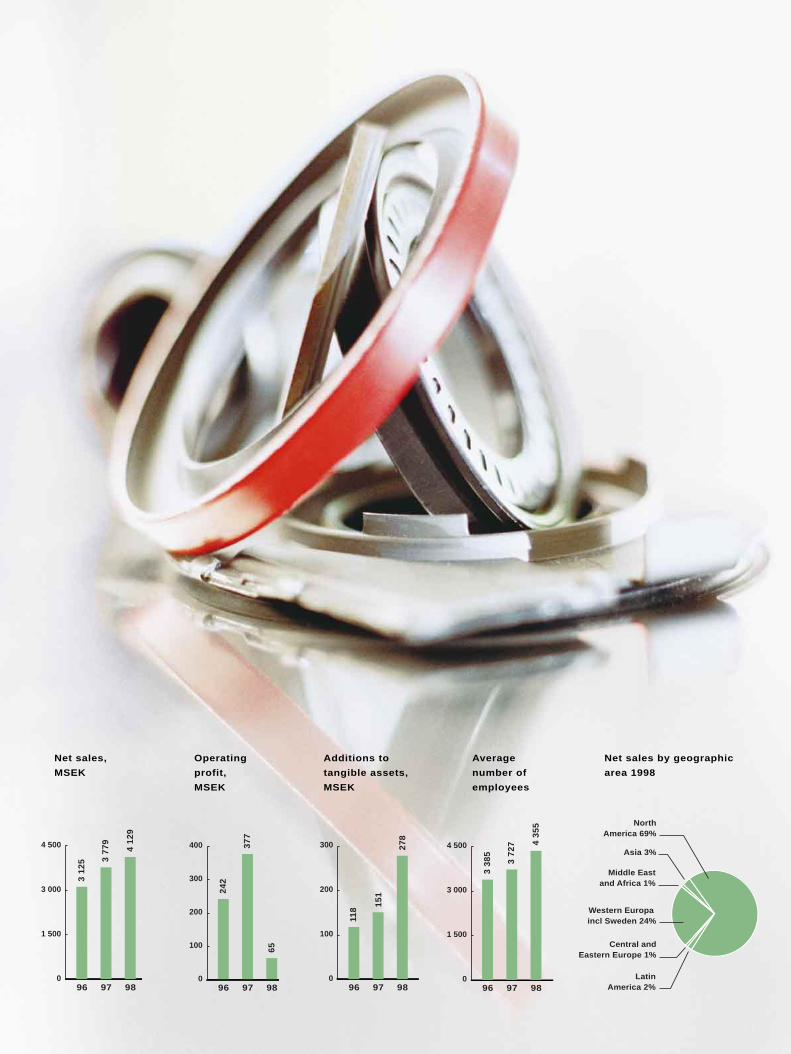

Asia 11%

NorthAmerica 21%

Latin America 7%

Middle Eastand Africa 3%

Central andEastern Europe 3%

Sweden 4%

Western Europa excl Sweden 51%

Operating

loss/profit,

MSEK

Additions to

tangible assets,

MSEK

Average

number of

employees

Net sales by geographic

area 1998

Net sales,

MSEK

12

This giant grinding mill at Noranda Inc., Brunswick Mine, in eastern Canada, isequipped with spherical roller bearings from SKF. The crushed zinc ore isdelivered directly from the mine and is ground into smaller particles in the millbefore going to the flotation process.

13

B E A R I N G S

The Industrial Division comprisesthree business areas – GeneralMachinery, Specialized Indus-tries and Customized Engineer-

ing – and focuses on industrial OEM cus-tomers. Manufacturing includes a largenumber of different types of industrial bear-ings, predominantly spherical, cylindricaland angular contact bearings.

Sales increased by 9.1% to MSEK 8 189(7 506). Before provisions, the division’s

operating margin declined slightly duringthe year as a result of unsatisfactory capac-ity utilization and lower prices.

During the year, the Industrial Divisiondeveloped new business activities with afocus on customers with more demandingapplications. New solutions were developedwith more functions integrated into thebearing application in order to improve theperformance and lifecycle.

During 1998, telephone sales generatedgood results in Europe and the US. Accord-ing to customers, this has improved thequality of their relations with SKF, sincecontacts have become more frequent andefficient for both parties.

Investments during the year amounted toMSEK 504 and focused mainly on increas-

ing the efficiency of existing plants. A pro-gram has been initiated to reduce resettingtimes in production and thus enhance ser-vice levels and reduce inventories. At thesame time, the product range is beingreduced in cooperation with customers.

The Industrial Division also comprisesthe manufacturing and sales of linearmotion products, which are found in therapidly expanding market for ergonomicand mobility aiding equipment. Positioning

systems is another product with significantgrowth in this area. These systems includespecialized sub-assemblies, designed and

built in close co-operation with the cus-tomers, as well as high speed, high preci-sion positioning tables incorporating linearmotors.

The sales development is positive in thisbusiness area, as is the profitability.

An area that the division is also focusingon is spindles for machine tools based onhigh-precision bearings. The acquisition of Russel T Gilman Inc., a leading US manu-facturer of such spindles, increased SKF’s

sales in this segment to MSEK 150 during1998. Machine tool spindles are also pro-duced in Germany and Sweden.

0

2 000

4 000

6 000

8 000

10 000

9897960

200

400

600

800

9897960

3 000

6 000

9 000

12 000

15 000

989796

6 83

0

7 50

6

8 18

9

483

662

504 10

633

11 5

78

11 6

29

External sales, Additions to RegisteredMSEK tangible number of

assets, MSEK employees

Giant loader at Brunswick Mine, Noranda Inc.,Canada.

Assembly line for snowmobile production at theLynx-Bombardien plant in Finland.

The baking ovens at the Göteborgs Kex biscuitplant in Sweden are equipped with SKF’s HighTemperature Bearings.

14

B E A R I N G S

Clevedon, UKRod endsSpherical plain bearingsSuspension and engine

Cassino, ItalyDeep groove ball bearingsEngine

Fontenay , FranceDeep groove ball bearingsEngine

Mühlheim, GermanySpecial needle cage

Differential

Thomery , FranceThin section bearingsEngine and gearbox

Jamestown, USPrecision angular

contact ball bearingsWheels

Schweinfurt, GermanySpecial cylindrical roller bearingsSpecial four-point contact ball bearingsGearbox and differential

Steyr , AustriaFour-point contact ball bearings

Gearbox

Villar Perosa, ItalyPrecision angular contact ball bearings

Wheels

Race cars live a punishing life. Designed, engineeredand maintained for one, single purpose: to win races.

The very popular NASCAR Winston Cup races arean excellent way to promote the SKF brand in the US.SKF has a sponsor agreement with Roush Racing andalso delivers seals, bearings and technical support tothis Ford Taurus and others in the Roush Racing stable.

SKF has been Ferrari’s technical partner and bear-ing supplier since 1947. The longest unbroken techni-cal partnership between a team and a supplier inGrand Prix history. The number of bearings in a mod-ern race car is staggering. This season’s F399 isequipped with nearly 150 SKF bearings, manufacturedat nine different locations.

15

B E A R I N G S

The Automotive Division is respon-sible for all sales to manufactur-ers of cars, trucks, buses andrelated aftermarkets. The divi-

sion is also responsible for the manufactureof taper roller bearings, wheel hub units,special products for vehicle manufacturers,and kits for the vehicle aftermarket.

Sales increased by 9.0% to MSEK 8 650(7 934). Although the division’s operatingmargin, before provisions, remained unsat-isfactory, it improved significantly duringthe year due to the restructuring programand efficiency improvements, which werestarted in the first half of the year, and tofavorable volumes.

Global production of cars and lighttrucks declined by 3% during 1998, primar-ily as a result of significantly lower volumesin Asia. The production of cars rose by over6% in Western Europe but decreased by 2%in the US.

The manufacture of heavy vehiclesincreased by 19% in Western Europe, by12% in the US and by 13% in South Amer-ica. Production in both India and Japanshowed a decline of more than one third.

In the vehicle aftermarket, SKF contin-ued to grow strongly in Europe andincreased its market share. This was mainlyattributable to sales of kits, which havebeen marketed heavily for the past fewyears and are now gaining increased marketacceptance. During the year, SKF receivedan award from CLEPA, the componentsparts association in Europe, for its EDI linkto vehicle component distributors.

In North America, SKF increased itsshares of the markets for cars and lighttrucks. Group sales rose by 20%, due tohighly favorable sales of the models towhich SKF provides bearings and due tonew business.

In Brazil, the sharp weakening of theautomotive market also affected SKF. Salesof locally produced kits for the automotiveaftermarket commenced during 1998. In the

truck segment, SKF decided to terminatedeliveries to Brazilian trailer manufacturersdue to unprofitable price levels.

Due to the structural changes in theKorean bearing market, SKF acquired theremaining shares in the joint venture com-pany for wheel hub units.

The SKF Group has had a joint venture

company in Italy with INA for water pumpspindles for cars. SKF has decided to leavethis business and has agreed to sell itsminority shareholding to INA.

0

2 000

4 000

6 000

8 000

10 000

9897960

200

400

600

800

1 000

9897960

3 000

6 000

9 000

12 000

989796

7 12

0

7 93

4

8 65

0

799

560 67

7

7 78

9

7 86

8

10 8

36

External sales, Additions to RegisteredMSEK tangible number of

assets, MSEK employees

Trailer axle equipped with discbrake and SKF truck hub unitmanufactured at the Group’splant in Lüchow, Germany.

B E A R I N G S

16

The Electrical Division is respon-sible for the sales to manufactur-ers of electric motors, householdappliances, electric components

for cars, and two-wheelers. The division isalso responsible for the production of alldeep groove ball bearings within SKF. Themajor part of these products is sold via theother bearing divisions.

Sales increased by 4.5% to MSEK 1 621

In India, production of two-wheelersimproved during the year, leading toincreased deliveries from SKF. At the sametime, the Group encountered problems atthe newly acquired plant in Indonesia dueto a dramatic decline in demand for motor-cycles. This led to prolonged productionstoppages among SKF customers and thusalso at the Group’s own plant.

With the aim of strengthening its marketposition, SKF continued to assign priorityto new products with higher added value.These included deep groove ball bearingswith sensors. Bearings equipped with opti-cal sensors are used for controlling highspeed motors.

SKF also launched an environmentallyfriendly, lead-free lubricant during the year.

The investments made during 1998focused on technical upgrades of variousplants and environmental improvements.

(1 551). The division’s operating margin,before provisions, is unsatisfactory and alsodeclined in 1998 as a result of sharplyincreased competition.

The sales increase was mainly attribut-able to customers in the white goods manu-facturing segment in Europe and the US. InEurope, the strong demand from subsuppli-ers to the automotive industry also con-tributed to increased deliveries.

0

500

1 000

1 500

2 000

9897960

200

400

600

800

9897960

2 000

4 000

6 000

8 000

989796

1 34

0

1 55

1

1 62

1

665

440

395

5 87

1

6 41

4

6 09

1

External sales, Additions to RegisteredMSEK tangible number of

assets, MSEK employees

Two-wheelers, motor-cycles and scooters, are amajor market segment forthe Electrical Division, particularly in Asia, wherethis picture was taken.

17

The Service Division was estab-lished in mid-1998. The divisioncomprises sales in the industrialaftermarket of all SKF-produced

bearings and of externally purchased prod-ucts. The division has sales units in morethan 50 countries and a network of approxi-mately 7 000 distributors and dealers, sub-stantially more than any competitor.

Sales decreased by 5.3% to MSEK11 669 (12 324). The division’s operatingmargin before provisions declined slightly

due to negative volume development in theUS and Southeast Asia.

In Western Europe, the largest market forthe division, sales increased although therewas considerable price pressure.

In the United States, the second largestmarket, sales to distributors were seriouslyaffected by structural changes, which led tosubstantial re-balancing of inventories.

As expected, sales to the Asia Pacificregion were lower than in 1997. However,this negative trend has probably bottomedout and price levels are firming up.

Whilst growth in Eastern Europe contin-ued, severe slowdowns occurred in bothMiddle East, Africa and Latin Americasales regions.

Most of the division’s sales are madethrough the authorised distributor networkand these channels have entered a period ofconsolidation and rationalization which isexpected to continue.

SKF has developed a comprehensiveoffering of products and services. This isbeing enhanced by new, higher technologyofferings, such that IMS or Integrated

SLS, SKF’s authorized distributor in Singapore and with facilities in Malaysia and Indonesia, is represented here byTan Hwee Khim, daughter of the founder, Tan Tiong Seng. SLS supplies its customers with all manner of SKF products, including rolling bearings, seals, maintenance and VSM products. The strength factor underlying SLS’ssuccess is the company’s close cooperation with customers and the extremely high levels of service it offers.

18

B E A R I N G S

The bearing market worldwide

SKF is the world’s largest bearing supplier,followed by the two Japanese companiesNSK and NTN, then FAG of Germany,Timken of the US and Koyo of Japan.

SKF is the largest supplier to the WestEuropean market. SKF is also the largestsupplier to Latin America, Africa and theMiddle East. In the US, Timken is the lead-

ing supplier, followed by SKF and Torring-ton of America.

NSK is the largest supplier in Japan.SKF, which is the largest non-Japanesebearing company in this market, has a mar-ket share of around 2%.

Markets in Central and Eastern Europe,as well as China, are mainly supplied by

The SKF Group’s operations in the aviationsector comprises MRC and SKF AVIO,which manufacture aeroengine bearings,and SARMA and AMPEP, manufacturers ofairframe bearings, electromechanical flightcontrol systems and electromechanicalequipment for fly-by-wire systems. Boththese operations developed very favorablyduring 1998. The strong growth for largecommercial aircraft, regional jet planes andhelicopters in the US and Europe led toincreased sales and improved margins.

0

3 000

6 000

9 000

12 000

15 000

9897960

20

40

60

80

9897960

1 000

2 000

3 000

4 000

989796

11 0

71

12 3

24

11 6

69

1

46

67

3 05

3

3 24

0

3 06

5

External sales, Additions to RegisteredMSEK tangible number of

assets, MSEK employees

local companies, although Western, as SKF,and Japanese producers have started toestablish positions as manufacturers inthese countries.

The global bearing market is estimatedto be worth approximately SEK 160 billion,of which the US and Western Europejointly account for about 60%

Maintenance Solution packages can be sup-plied to enduser customers. This conceptaims to combine the excellent logistics ser-vice from our distributors with advanced

high impact mechanical and electronictechnology from SKF. The goal is that cus-tomers can increase productivity and theoperational lifetime of their mechanical

rotating machinery, and at the same timeimprove the efficiency and cost of theirmaintenance programs. This should resultin improved uptime for the customers.

ISC, or Industrial Service Centres, arebeing established in key markets, and theywill offer bearing repairs, assembly ser-vices, training, condition monitoring ser-vices and fault diagnosis.

The CFM56 jet aircraft engine isthe best selling jet engine in theworld today. SKF is the leadingbearing supplier on the engine,featuring parts provided by SKFAVIO in Italy and MRC Bearingsin the US.

0

1 500

3 000

4 500

96 97 98

3 12

5 3 77

9

4 12

9

0

100

200

300

400

96 97 98

242

377

65

0

100

200

300

96 97 98

118

151

278

0

1 500

3 000

4 500

96 97 98

3 38

5

3 72

7 4 35

5

Asia 3%

NorthAmerica 69%

LatinAmerica 2%

Middle Eastand Africa 1%

Central andEastern Europe 1%

Western Europa incl Sweden 24%

Operating

profit,

MSEK

Additions to

tangible assets,

MSEK

Average

number of

employees

Net sales by geographic

area 1998

Net sales,

MSEK

20

With a large fleet of 230 trucks and more than 1 000 trailers, Jeff Kelly fromG&D Transportation, Loves Park, Illinois in the United States, is an importantcustomer for Chicago Rawhide. The company hauls various types of mixedfreight throughout the North American continent. G&D Transportation receivesits service and deliveries of CR seals and SKF bearings through TransAmTruck & Trailer Parts Inc. in Rockford, Illinois. TransAm is a well-equipped supplier of spare parts for heavy trucks and is a selected distributor of CRproducts. The company supplies not only individual truck owners but alsodelivers to the larger trucking companies, as shown here.

In order to restore profitability withinChicago Rawhide, the largest company inthe Seals Division, a comprehensiverestructuring program was initiated. At thesame time a number of new products, suchas a bonded piston seal for automatic gear-boxes and valve stem seals, was launched.

Seals operations in Western Europe con-sist of CR Elastomere in Germany, whichproduces seals for the European automotiveindustry and RFT in Italy, which produces a

range of seals for rolling bearings andshock absorbers.

Sales of seals to customers in WesternEurope developed positively during theyear. The Seals Division also benefitedfrom the favorable growth in the Europeanautomotive industry. Sales of new productssuch as valve stem seals with integratedsprings and new solutions for truck axlesalso contributed to the division’s growth inEurope.

North America accounts for 69%of the division’s sales. Theimprovement in earnings in thedivision’s European operations

could not offset the major decline in theUS. The important North American auto-motive aftermarket was exposed to exten-sive restructuring in the distributor area.This had an adverse effect on the division’searnings, since it resulted in increased costsfor business development at new customers.

The Seals Division’s sales rose by 9.3% in 1998 to MSEK 4129. The division’s operating profit declined

to MSEK 65 in 1998 from MSEK 377 in 1997,primarily as a result of the unsatisfactory market trend in

North America. Excluding provisions the division posted an operating profit of MSEK 164.

21

The new sign common to all distributors of Chicago Rawhide andSKF automotive aftermarket products.

A typical truck unit for the US heavy vehicles market, a key customer segment for Chicago Rawhide.

22

S E A L S

The building of a production base inAsia, which started a couple of years agothrough the majority acquisition of a Chi-nese seals company, continued during 1998.SKF acquired 50% of the Korean sealscompany, KFOS, which has now beenrenamed CR Korea.

In India, Chicago Rawhide established awholly owned subsidiary in Bangalore dur-ing autumn 1997. Following preparatorywork, production is expected to commenceduring the first quarter of 1999.

During the year, CR Mexicana alsobecame a wholly owned subsidiary throughChicago Rawhide’s acquisition of the Mexi-can partner’s 60% shareholding.

Global seals market

The total market for elastomeric products,which is how the Seals Division has chosento define its market, is approximately SEK80 billion.

The leading companies within the elas-tomeric products area are Freudenberg/NOK (a German/Japanese alliance),Chicago Rawhide, America’s FederalMogul and Dana, and the TI Group inEurope. During the year, a number of struc-tural changes occurred among the Ameri-can competitors, but not within the segmentin which Chicago Rawhide has its corebusiness.

Chicago Rawhide is the leading supplierof radial seals in the North American market.

Repair of machine parts in the engine bay of aheavy truck at Rockford Truck Sales and Service.

Miele, a German customer of the SKF Group is equipping its washingmachines with SKF deep groove ball bearings and CR seals. Thedynamic seal, see cut-out picture, has a special labyrinth feature towardsthe water side of the washing machine drum, in order to prevent washingpowder residuals from influencing the sealability of the unit.

Asia 3%

NorthAmerica 23%

Central andEastern Europe 1%

Middle Eastand Africa 1%

Western Europe excl Sweden 50%

Sweden 22%

0

1 000

2 000

3 000

4 000

96 97 98

3 27

1

3 39

1

3 22

9

0

50

100

150

200

250

96 97 98

153

242

1

0

150

300

450

96 97 98

334

419

221

0

1 000

2 000

3 000

96 97 98

2 96

2

2 79

2

2 68

6

Operating

profit,

MSEK

Additions to

tangible assets,

MSEK

Average

number of

employees

Net sales by geographic

area 1998

Net sales,

MSEK

24

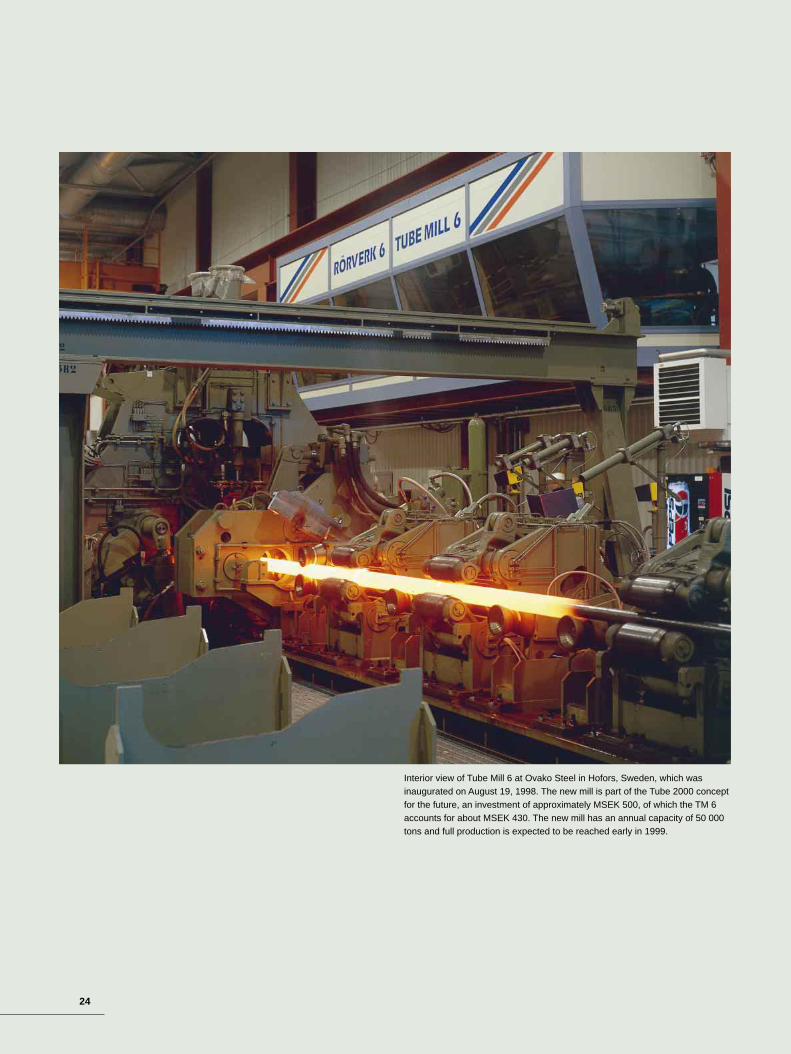

Interior view of Tube Mill 6 at Ovako Steel in Hofors, Sweden, which was inaugurated on August 19, 1998. The new mill is part of the Tube 2000 conceptfor the future, an investment of approximately MSEK 500, of which the TM 6accounts for about MSEK 430. The new mill has an annual capacity of 50 000tons and full production is expected to be reached early in 1999.

25

The Western European market forspecial steels was marked bystrong demand and increasingvolumes during the first half of

the year. The second half was characterizedby rapidly declining demand. Measures toadapt both production and manning to thenew conditions became necessary.

In North America, which accounts forone fourth of the sales, demand alsodeclined significantly during the secondhalf of the year, due, among other reasons,to a sharp decline in the oil industry.

The weaker market conditions during thesecond half led to a deterioration in bothsales and earnings. Profit was alsoadversely affected by the running-in costsrelated to the new tube mill in Hofors.

The new tube mill, an investment ofabout MSEK 500, was inaugurated inAugust and contributes capacity of 50 000

tons. The addition of this new mill strength-ened Ovako Steel’s position as a leadingsupplier of seamless hot-rolled tubes.

During 1998, preparatory work was initi-ated for a new and totally integrated systemthat will cover all of the administrative rou-tines in the company. In January 1999, thefirst step in the process was taken, when thesystem was introduced within the account-ing, purchasing and maintenance areas. Theremaining administrative departments willadopt the new system in April 1999.

On the marketing side, continued effortsare being made to increase sales to customersoutside the SKF Group. The proportion ofoutside sales increased during the year.

Global steel market

Ovako Steel is Europe’s leading supplier ofrolling-bearing steel. The company is alsothe world’s largest producer of through-hardening steel for rolling bearings. OvakoSteel holds a unique position by being theonly company to produce a combination ofbars, tubes and rolled rings.

Certain European competitors are cur-rently phasing out their production of barproducts in order to focus on flat steel prod-ucts. As a result, Germany’s Thyssen hasdisposed of Nedstaal and the French com-pany, Usinor, has announced that it intendsto withdraw from Asco, an Ovako Steelcompetitor.

America’s Timken, which like SKF hasits own steel production operations, hastaken over the UK’s Desford, which pro-duces tubes for bearing production.

Sales of steel,which declined gradually during the fiscal year, totalled MSEK 3229,down slightly

compared with sales of MSEK 3 391 in 1997. The operating profit amounted to MSEK 1 for 1998,

compared with a profit of MSEK 242 in 1997. Excluding provisions,the operating profit amounted

to MSEK45.

Special steel tube being cut to length for Italian customers at a distribution plant in Milan, where Sandvik Italia distributes Ovako Steel’s products.

Financial risks

SKF’s operations are exposed to currencyrisks, interest-rate risks and credit risks.

The Group’s financial policy clearlydefines currency, interest-rate and creditrisks and establishes responsibility andauthority for the management of financialrisks. This policy states that the objective isto eliminate or minimize risk and to con-tribute to a better return on Group assetsthrough an active management of risks.

The management of these risks, andresponsibility for all treasury operations, islargely centralized in SKF Treasury Centre,the Group’s internal bank.

Currency risks

The currency risks to which the Group isexposed consist of changes in exchangerates in future flows of payments, transac-tion exposure, as well as the revaluation ofresults, assets and liabilities in foreign cur-

26

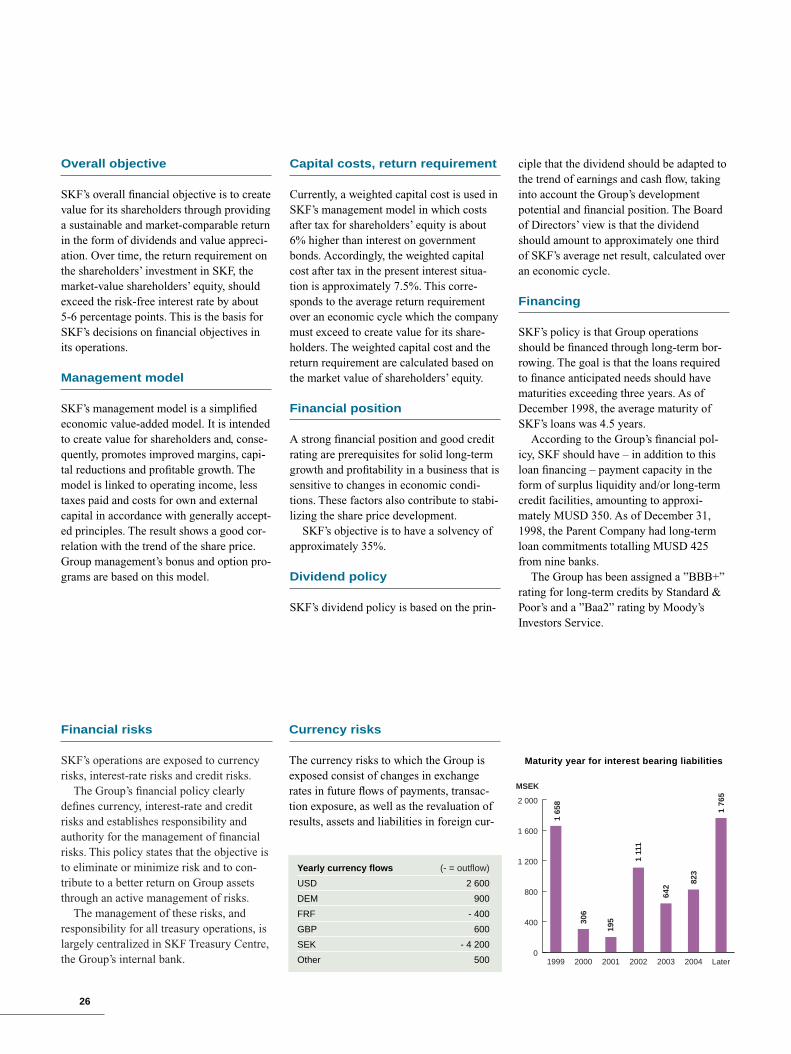

Overall objective

SKF’s overall financial objective is to createvalue for its shareholders through providinga sustainable and market-comparable returnin the form of dividends and value appreci-ation. Over time, the return requirement onthe shareholders’ investment in SKF, themarket-value shareholders’ equity, shouldexceed the risk-free interest rate by about5-6 percentage points. This is the basis forSKF’s decisions on financial objectives inits operations.

Management model

SKF’s management model is a simplifiedeconomic value-added model. It is intendedto create value for shareholders and, conse-quently, promotes improved margins, capi-tal reductions and profitable growth. Themodel is linked to operating income, lesstaxes paid and costs for own and externalcapital in accordance with generally accept-ed principles. The result shows a good cor-relation with the trend of the share price.Group management’s bonus and option pro-grams are based on this model.

Capital costs, return requirement

Currently, a weighted capital cost is used inSKF’s management model in which costsafter tax for shareholders’ equity is about6% higher than interest on governmentbonds. Accordingly, the weighted capitalcost after tax in the present interest situa-tion is approximately 7.5%. This corre-sponds to the average return requirementover an economic cycle which the companymust exceed to create value for its share-holders. The weighted capital cost and thereturn requirement are calculated based onthe market value of shareholders’ equity.

Financial position

A strong financial position and good creditrating are prerequisites for solid long-termgrowth and profitability in a business that issensitive to changes in economic condi-tions. These factors also contribute to stabi-lizing the share price development.

SKF’s objective is to have a solvency ofapproximately 35%.

Dividend policy

SKF’s dividend policy is based on the prin-

ciple that the dividend should be adapted tothe trend of earnings and cash flow, takinginto account the Group’s developmentpotential and financial position. The Boardof Directors’ view is that the dividendshould amount to approximately one thirdof SKF’s average net result, calculated overan economic cycle.

Financing

SKF’s policy is that Group operationsshould be financed through long-term bor-rowing. The goal is that the loans requiredto finance anticipated needs should havematurities exceeding three years. As ofDecember 1998, the average maturity ofSKF’s loans was 4.5 years.

According to the Group’s financial pol-icy, SKF should have – in addition to thisloan financing – payment capacity in theform of surplus liquidity and/or long-termcredit facilities, amounting to approxi-mately MUSD 350. As of December 31,1998, the Parent Company had long-termloan commitments totalling MUSD 425from nine banks.

The Group has been assigned a ”BBB+”rating for long-term credits by Standard &Poor’s and a ”Baa2” rating by Moody’sInvestors Service.

Yearly currency flows (- = outflow)

USD 2 600

DEM 900

FRF - 400

GBP 600

SEK - 4 200

Other 5000

400

800

1 200

1 600

2 000

Later200420032002200120001999

1 65

8

306

195

1 11

1

642

823

1 76

5

MSEK

Maturity year for interest bearing liabilities

27

E M U

rencies when these currencies are translatedto Swedish kronor, translation exposure.

Transaction exposureThe Group’s principal commercial flows offoreign currencies pertain to exports fromEurope to North America and Asia, and toflows of currencies within Europe. Theintroduction of the euro will reduce the cur-rency risks for SKF’s European operations.Over the long term, SKF is seeking toestablish a balance between production andsales within the European, American andAsian zones, respectively.

SKF has flows in some 20 currencies.The total flow of goods exceeds MSEK31 000. After offsetting flows in the samecurrency, the net flow amounts to approxi-mately MSEK 7 500. The flows that – dueto their size – could have a major impact onSKF’s income are inflows in USD, DEMand GBP that are converted into SEK, FRFand ITL. Fluctuations of approximately10% in foreign exchange rates in these cur-rencies can affect Group result by a coupleof hundred million kronor.

SKF’s policy is to hedge currency flowsfor three to six months on average. This isthe length of time deemed to be required toadjust to new conditions. Within the frame-work of established risk limits, it is possiblefor SKF Treasury Center to make deviationsfrom this average period. Risks are managed

based on a risk-evaluation system that takesinto account the volatility of currencies aswell as their mutual relationship. As of year-end, the lengths of the actual forward con-tracts conformed with the basic policy.

Translation exposureGroup result is also affected by the effect oftranslating the results of foreign subsidiariesto Swedish kronor. When there is a changeof approximately 10% in the value of thekrona, this effect can also amount to a couple of hundred million kronor, depend-ing on the country in which the result aroseand the respective currency movement inrelation to the Swedish krona.

The Group is also affected by the transla-tion to Swedish kronor of net assets heldoutside Sweden. At year-end 1998, SKF’snet foreign assets amounted to MSEK10 000. For the time being these currenciesare not hedged. Translation effects in for-eign net assets do not have any impact onGroup result but are transferred directly toshareholders equity.

Economic exposureSKF’s principal competitors have thegreater part of their production capacity inGermany, the US or Japan. Currencychanges affecting those countries’ cost situ-ation primarily in relation to Sweden, Italyand France, where SKF, in addition to Ger-

many and the US, has substantial manufac-turing operations, affect SKF’s competitive-ness in relation to these competitors.

Interest-rate risks

The risk associated with interest rates is thatchanges in interest rates will have a nega-tive impact on Group result. SKF’s basicpolicy for establishing fixed-interest-rateperiods is that the average duration shouldbe six months. This applies to borrowing aswell as investment of funds and alsoincludes the use of derivatives.

The composition of the Group’s interest-rate portfolio is diversified. Normal changesin interest rates are not considered to haveany significant impact on SKF’s result.

Credit risks

Credit risks pertain to the creditworthinessof counterparties. Credit risks that arise as aresult of trading in financial instruments andin connection with the investment of liquidfunds are carefully defined in the financialpolicy. Transactions are carried out onlywithin established limits, and with counter-parties who have good credit ratings.

On January 1, 1999, the common currencyknown as the euro was introduced in the 11member nations of the European MonetaryUnion (EMU).

SKF conducts extensive business opera-tions in EMU, with strong concentration inGermany, France and Italy. In 1998, EMUcountries accounted for approximately 45%of Group net sales and more than 50% ofGroup production.

The new euro currency, accordingly, willhave far-reaching effects on SKF’s opera-

tions, despite Sweden remaining outsideEMU for the time being.

SKF’s euro policy

SKF developed a euro policy during 1998to introduce the new currency in theGroup’s operational activities, whereby:• SKF companies in EU countries concludetheir sales and purchasing transactionsbased on the euro effective January 1, 1999.• SKF has been distributing price lists

quoted in euro to EU countries since January 1, 1999.• SKF has been equipped to send andreceive invoices and payments in both euroand the local currencies of EU countriessince January 1, 1999. • During the transitional period from 1999through 2001, SKF’s customers have theoption to select either the euro or their localcurrency as their invoicing currency.

28

The Year 2000 issue refers to the risk thatsystems, products and equipment havingdate-sensitive components will not recog-nize the year 2000. Throughout this dis-closure SKF uses the generic phrase ”year2000 compliant” to mean that a system,product or equipment will perform itsintended functions on or after January 1,2000 the same as it did before January 1,2000.

1. The SKF Year 2000 Project

SKF has been actively addressing Year 2000issues since 1996. In 1997 SKF decided tocoordinate all Year 2000 activities centrally.The progress and status of the Year 2000Project is reported to SKF Group Manage-ment every second month by the ProjectLeader.

Each Group Division, staff unit and ser-

vice unit has a Year 2000 Project Leader.Each Project Leader has his/her own ProjectTeam. In total approximately 350 people areinvolved in SKF’s Year 2000 Project on afull or part time basis.

SKF’s Year 2000 Project includes identi-fying the potential risk areas, increasingrisk awareness and introducing action plansfor managing Year 2000 issues.

2. State of Readiness

IT Applications and IT PlatformsMapping and risk assessment of IT Applica-tions (computer programs and databases) andIT Platforms (hardware, networks, operatingsystems, etc) including supplier complianceevaluations have been completed and most

Since 1985 SKF is quoted on the NASDAQ stock exchange. As a consequence, SKF

each year submits to the Securities and Exchange Commission (SEC) certain financial

and other information. For 1998 SEC has requested specific information related to the

handling of the year 2000 issue. The below is the information that SKF intends to sub-

mit to SEC regarding SKF's handling of the year 2000 issue.

SKF’s EMU project

In November 1996, SKF appointed a work-ing group to evaluate the effects of an even-tual introduction of a common currency inEurope.

The preparations have encompassedstrategic, financial, legal and infrastructuralaspects of information technology, financialaccounting and reporting.

Strategic aspectsSKF operates in an international industry,and the introduction of a common currencyin Europe is not expected to create any sig-nificant changes in the Group’s strategicdirection. SKF has treated Europe as a single market for the past several years.

A change in the Group’s overall directionof operations, or geographical localization,as a direct consequence of the new cur-rency’s introduction should not be expected,based on information available today.

Financial aspectsBecause of the broad geographical spreadof Group operations, SKF is exposed to a

complex situation regarding currency risks.Introduction of the euro will simplify theGroup’s risk situation, since the number ofcurrencies handled will be smaller. Further-more, the euro will provide increasedopportunities for more effective manage-ment of the Group’s liquid assets.

Infrastructural aspectsInformation technology will require thelargest work input to prepare for conversionto euro as the Group’s accounting andreporting currency.