annual general meeting of shareholders - presentatie resultaten … me… · okt-07 nov-07 dec-07....

TRANSCRIPT

Annual General Meeting of

11

ShareholdersMay 13, 2008

•• Registration of the quorumRegistration of the quorum

•• Composition of the ‘bureau’Composition of the ‘bureau’

22

AgendaAgenda::

1.1. Reading, deliberating and commenting of the annual report of Reading, deliberating and commenting of the annual report of the board of directors and the statutory auditor’s report on the the board of directors and the statutory auditor’s report on the annual accounts for the accounting year 2007.annual accounts for the accounting year 2007.

33

Report of the boardReport of the board

of directors for 2007of directors for 2007

44

Ger van JeverenGer van Jeveren

CEOCEO

Jan PeetersJan Peeters

CFOCFO

•• Turnover +Turnover +1010%, of which %, of which 66% organic (compared to % organic (compared to 20062006))

•• Net profit +Net profit +3434% (compared to % (compared to 20062006))

•• Very successful Initial Public Offering (‘IPO’) of Arseus, approx. Very successful Initial Public Offering (‘IPO’) of Arseus, approx. 2 2

times oversubscribedtimes oversubscribed

Key facts 2007Key facts 2007

55

times oversubscribedtimes oversubscribed

•• Acquisition of Polichimica, an Italian company which achieved a Acquisition of Polichimica, an Italian company which achieved a

turnover of turnover of €€ 10 10 million in million in 20062006

•• All commercial and logistic services located in Belgium were All commercial and logistic services located in Belgium were

centralized in Waregemcentralized in Waregem

•• Further integration of Eurotec and Besserat (both acquired in Further integration of Eurotec and Besserat (both acquired in 20062006))

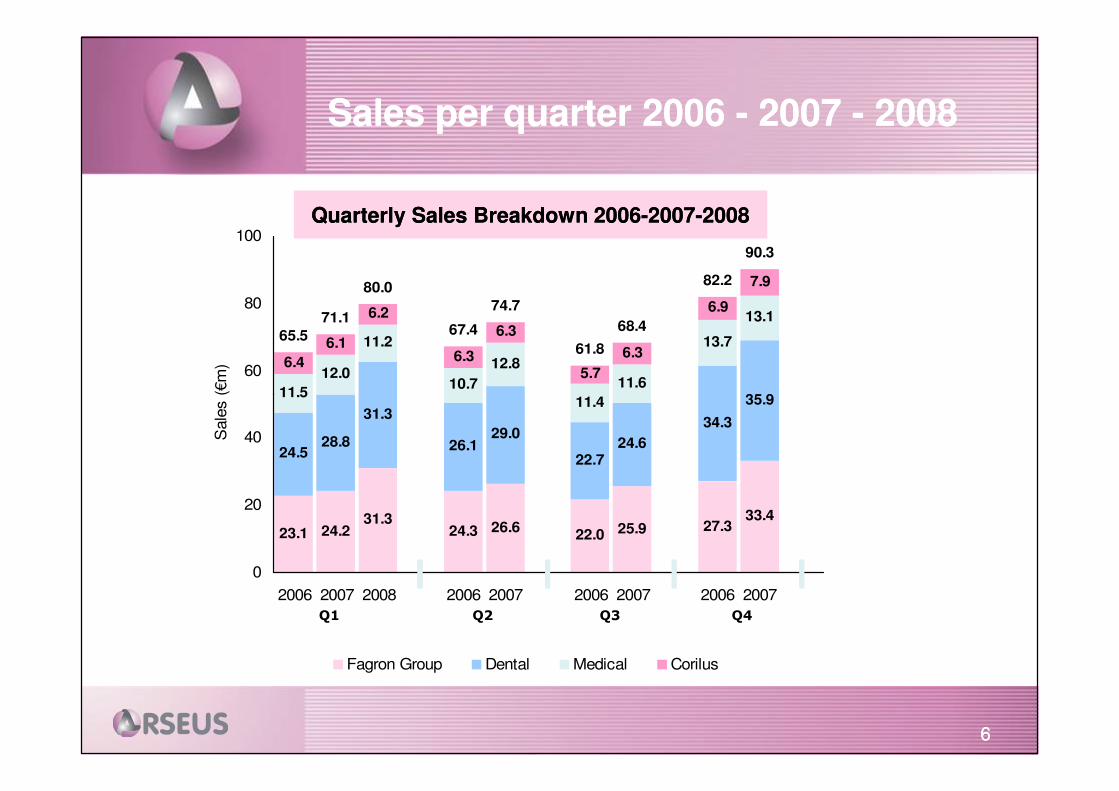

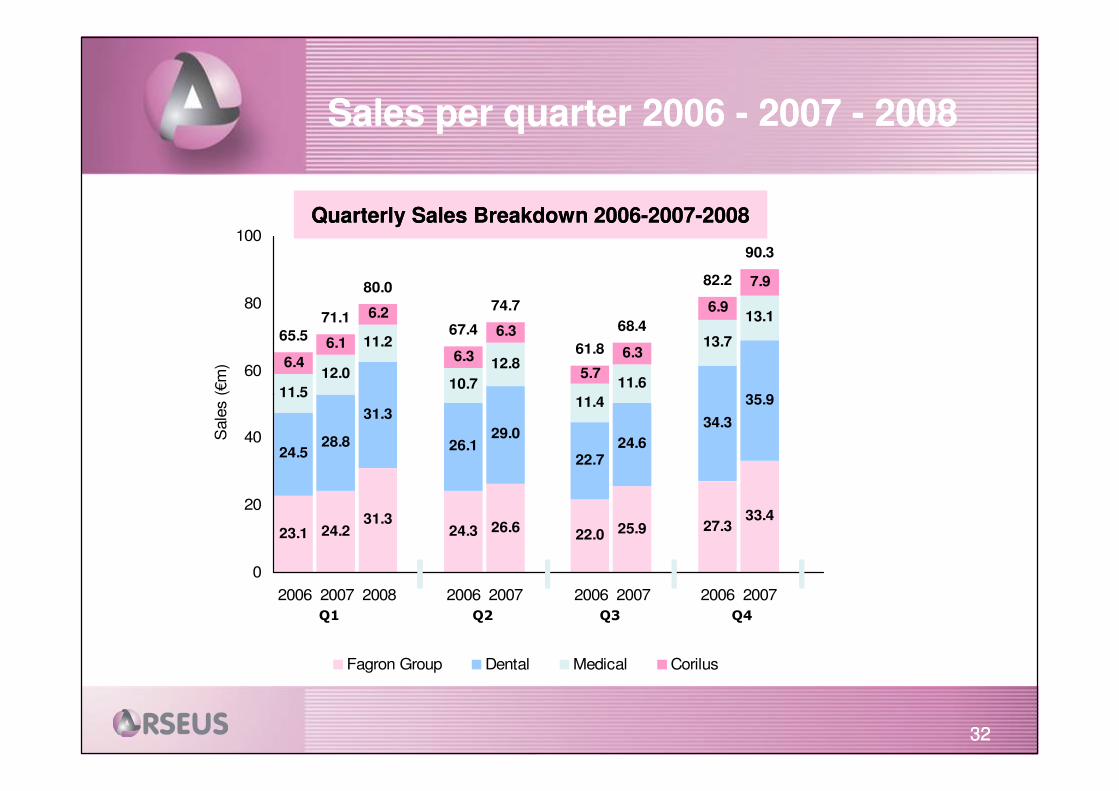

35.9

13.1

13.7

11.6

11.4

12.8

10.7

11.2

12.0

11.5

7.9

6.9

6.3

5.7

6.3

6.3

6.2

6.1

6.4

90.3

82.2

68.4

61.8

74.7

67.4

80.0

71.1

65.5

60

80

100S

ale

s (

€m

)Quarterly Sales Breakdown 2006Quarterly Sales Breakdown 2006--20072007--20082008

Sales per quarter Sales per quarter 2006 2006 -- 2007 2007 -- 20082008

66

33.427.325.922.0

26.624.331.3

24.223.1

35.9

34.3

24.622.7

29.026.1

31.3

28.824.5

11.411.5

0

20

40

2006 2007 2008 2006 2007 2006 2007 2006 2007

Sale

s (

€m

)

Fagron Group Dental Medical Corilus

Q1 Q2 Q3 Q4

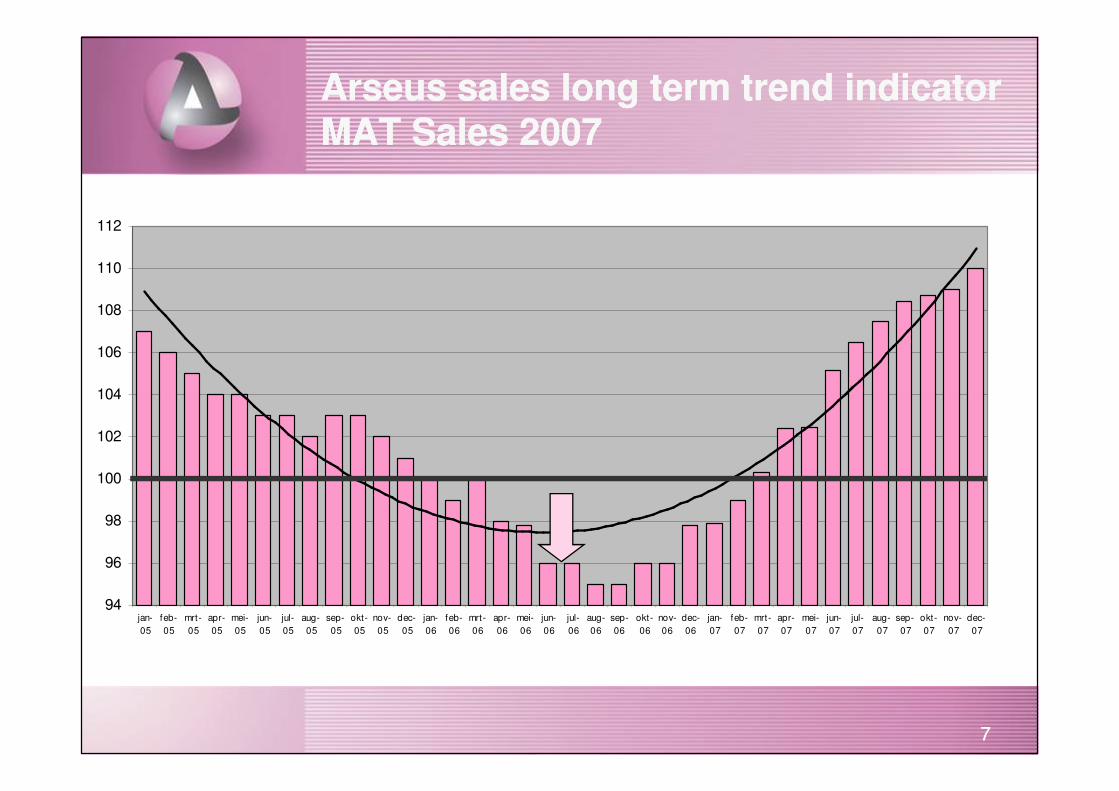

Arseus sales long term trend indicator Arseus sales long term trend indicator MAT Sales 2007MAT Sales 2007

104

106

108

110

112

77

94

96

98

100

102

104

jan-

05

feb-

05

mrt-

05

apr-

05

mei-

05

jun-

05

jul-

05

aug-

05

sep-

05

okt-

05

nov-

05

dec-

05

jan-

06

feb-

06

mrt-

06

apr-

06

mei-

06

jun-

06

jul-

06

aug-

06

sep-

06

okt-

06

nov-

06

dec-

06

jan-

07

feb-

07

mrt-

07

apr-

07

mei-

07

jun-

07

jul-

07

aug-

07

sep-

07

okt-

07

nov-

07

dec-

07

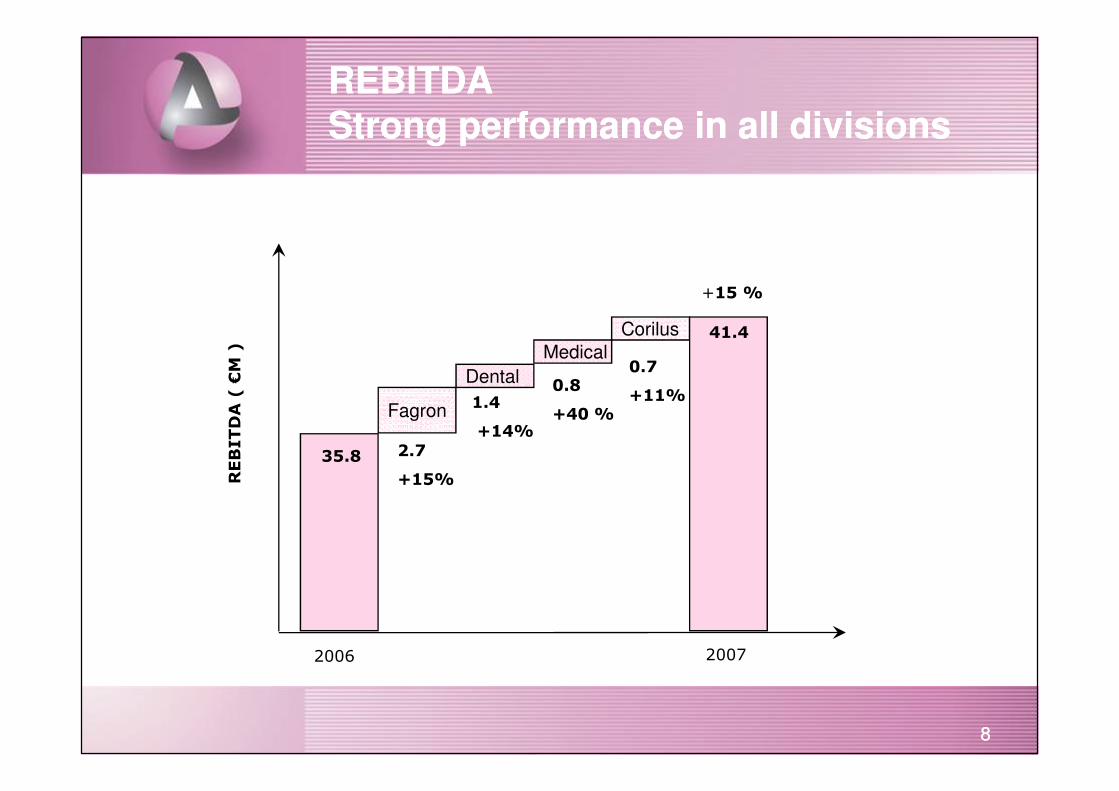

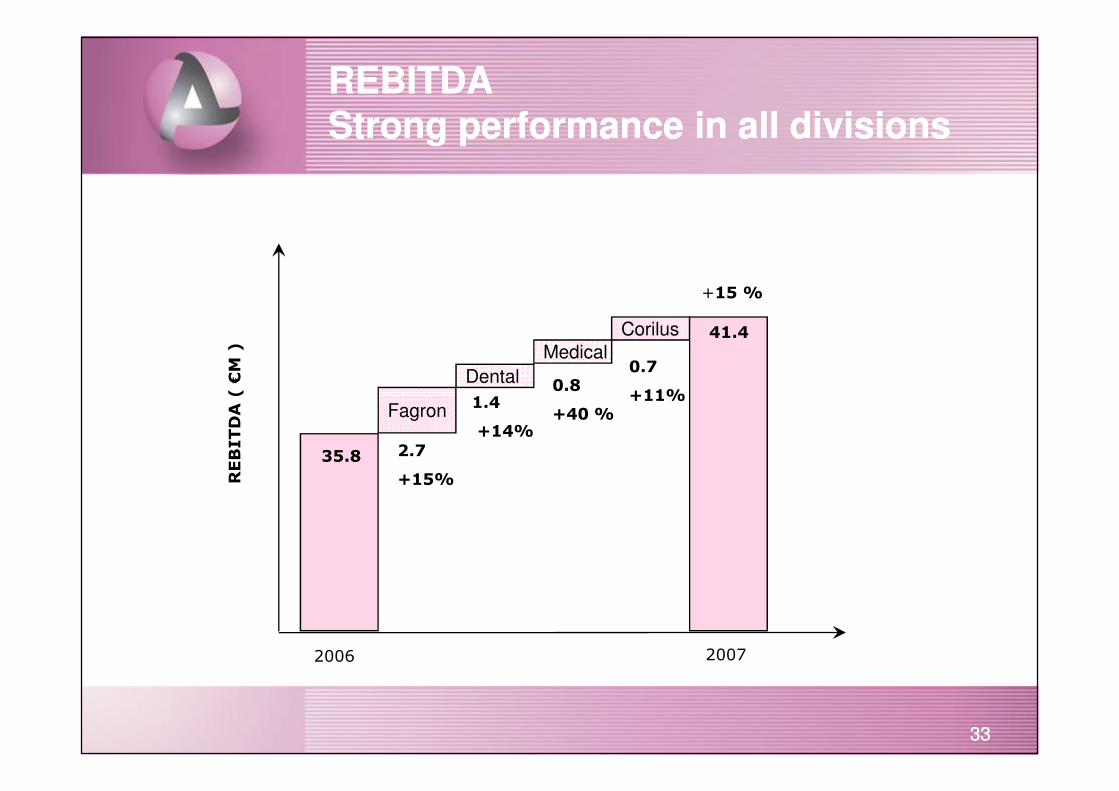

REBITDAREBITDAStrong performance in all divisionsStrong performance in all divisions

Dental

Corilus

( €M )

1.4

Medical

0.80.7

+11%

+15 %

41.4

88

Fagron

REBITDA(

2.7

+15%

1.4

+14%+40 %

+11%

35.8

2006 2007

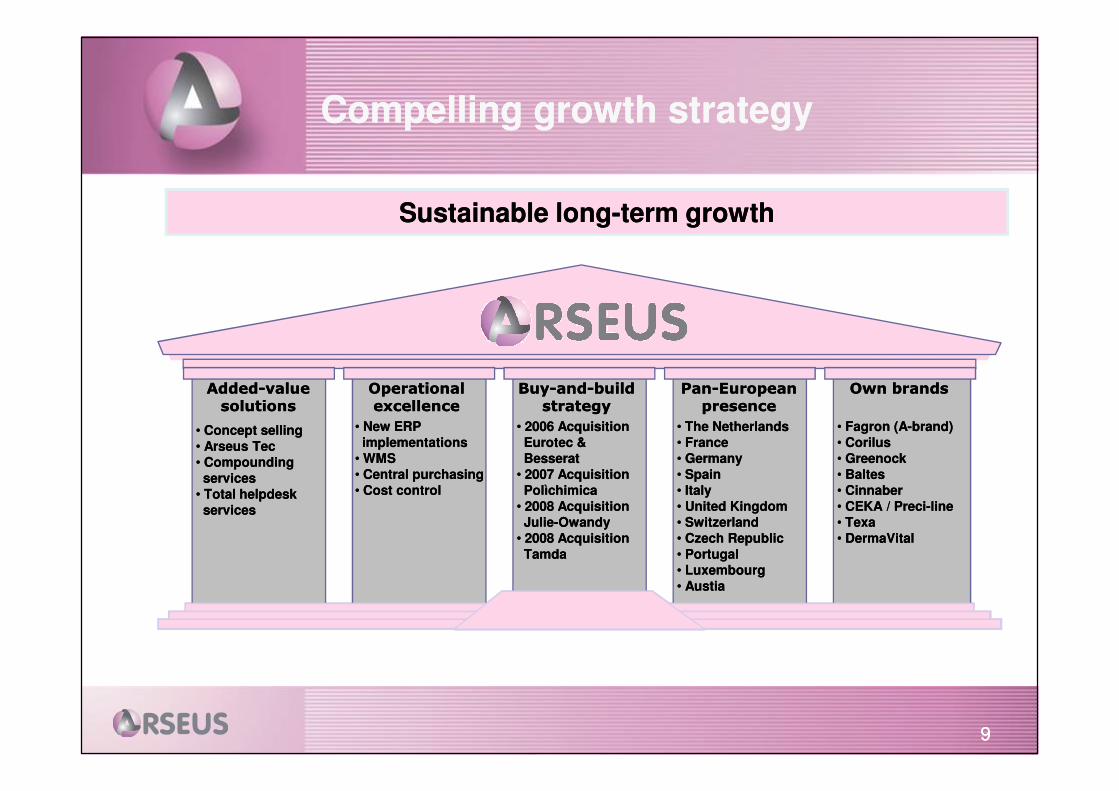

Compelling growth strategyCompelling growth strategy

Sustainable longSustainable long--term growthterm growth

Own brandsOwn brandsAddedAdded--value value BuyBuy--andand--build build PanPan--European European Operational Operational

99

Own brandsOwn brandsAddedAdded--value value solutionssolutions

BuyBuy--andand--build build strategystrategy

PanPan--European European presencepresence

Operational Operational excellenceexcellence

•• Concept sellingConcept selling•• Arseus TecArseus Tec•• Compounding Compounding servicesservices

•• Total helpdeskTotal helpdeskservicesservices

•• New ERPNew ERPimplementationsimplementations

•• WMSWMS•• Central purchasingCentral purchasing•• Cost controlCost control

•• Fagron (AFagron (A--brand)brand)•• CorilusCorilus•• GreenockGreenock•• BaltesBaltes•• CinnaberCinnaber•• CEKA / PreciCEKA / Preci--lineline•• TexaTexa•• DermaVitalDermaVital

•• 2006 Acquisition2006 AcquisitionEurotec & Eurotec & BesseratBesserat

•• 2007 Acquisition2007 AcquisitionPolìchimicaPolìchimica

•• 2008 Acquisition2008 AcquisitionJulieJulie--OwandyOwandy

•• 2008 Acquisition2008 AcquisitionTamdaTamda

•• The NetherlandsThe Netherlands•• FranceFrance•• GermanyGermany•• SpainSpain•• ItalyItaly•• United KingdomUnited Kingdom•• SwitzerlandSwitzerland•• Czech RepublicCzech Republic•• PortugalPortugal•• LuxembourgLuxembourg•• AustiaAustia

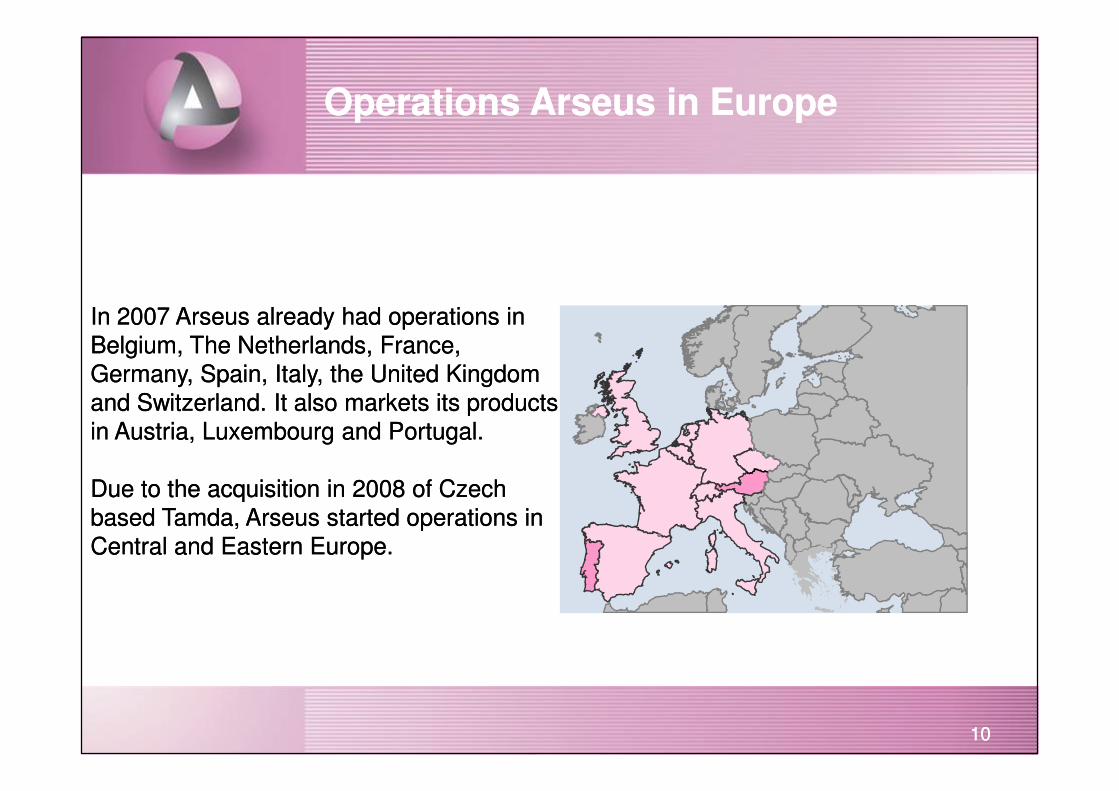

Operations Arseus in EuropeOperations Arseus in Europe

In In 2007 2007 Arseus already had operations in Arseus already had operations in

Belgium, The Netherlands, France, Belgium, The Netherlands, France,

Germany, Spain, Italy, the United Kingdom Germany, Spain, Italy, the United Kingdom

and Switzerland. It also markets its products and Switzerland. It also markets its products

1010

and Switzerland. It also markets its products and Switzerland. It also markets its products

in Austria, Luxembourg and Portugal.in Austria, Luxembourg and Portugal.

Due to the acquisition in Due to the acquisition in 2008 2008 of Czech of Czech

based Tamda, Arseus started operations in based Tamda, Arseus started operations in

Central and Eastern Europe.Central and Eastern Europe.

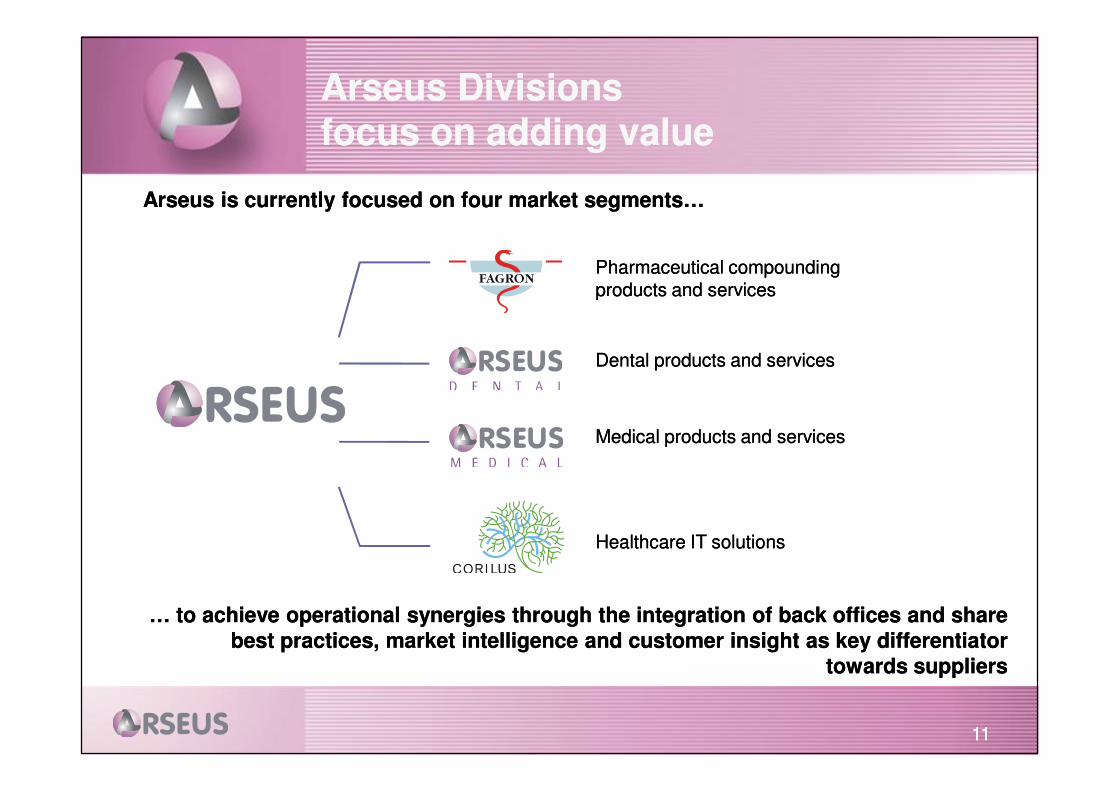

Arseus DivisionsArseus Divisionsfocus on adding valuefocus on adding value

Arseus is currently focused on four market segments…Arseus is currently focused on four market segments…

Pharmaceutical compounding Pharmaceutical compounding

products and servicesproducts and services

Dental products and servicesDental products and services

1111

…… to to achieve operational synergies through the integration of back offices and share achieve operational synergies through the integration of back offices and share best practices, market intelligence and customer insight as key differentiator best practices, market intelligence and customer insight as key differentiator

towards supplierstowards suppliers

Medical products and servicesMedical products and services

Healthcare ITHealthcare IT solutionssolutions

OneOne--stopstop--shop for shop for pharmaceutical pharmaceutical

1212

pharmaceutical pharmaceutical compoundingcompounding

36%

49%

FYFY––07 Sales07 Sales FYFY––07 EBITDA07 EBITDA

Fagron Fagron -- leading the market and well leading the market and well positioned for growthpositioned for growth

Market Position Competitive Strengths

•• Highest brand recognitionHighest brand recognition

•• Focus on total integrated Focus on total integrated solutionssolutionsOne-stop-shop

for

•• The only European The only European playerplayer

•• The only European The only European brandbrand

1313

•• Extensive product rangeExtensive product range

•• Superior qualitySuperior quality

•• Centralised purchasingCentralised purchasing

for pharmaceutical compounding

brandbrand

•• Large experienced Large experienced sales force (160 reps)sales force (160 reps)

•• Partner of choice for Partner of choice for pharmaceutical industrypharmaceutical industry

Fagron’s strategy is to expand its European presence, Fagron’s strategy is to expand its European presence,

strengthen the Fagron brand, and continue to launch strengthen the Fagron brand, and continue to launch

innovative products and servicesinnovative products and services

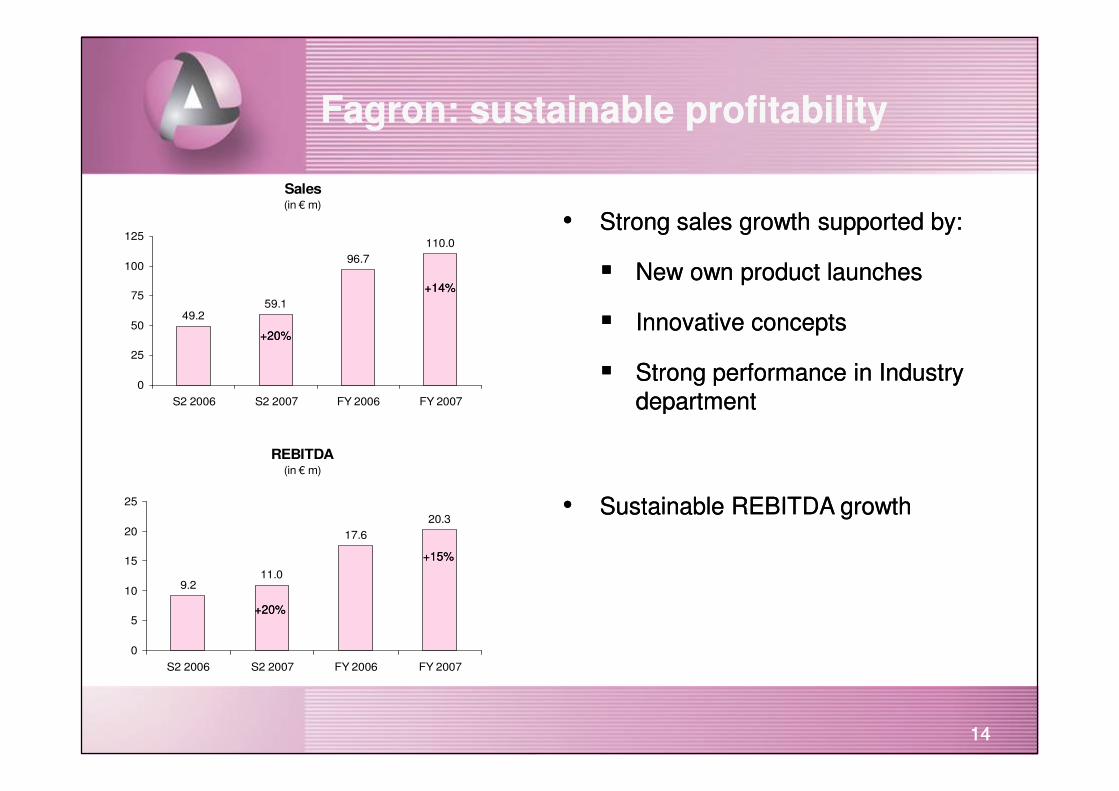

Fagron: sustainable profitabilityFagron: sustainable profitability

•• Strong sales growth supported by:Strong sales growth supported by:

�� New own product launchesNew own product launches

�� Innovative conceptsInnovative concepts

�� Strong performance in Industry Strong performance in Industry

departmentdepartment

Sales(in € m)

110.0

96.7

59.149.2

0

25

50

75

100

125

S2 2006 S2 2007 FY 2006 FY 2007

+20%+20%

+14%+14%

1414

departmentdepartmentS2 2006 S2 2007 FY 2006 FY 2007

REBITDA(in € m)

20.3

17.6

11.09.2

0

5

10

15

20

25

S2 2006 S2 2007 FY 2006 FY 2007

•• Sustainable REBITDA growthSustainable REBITDA growth

+20%+20%

+15%+15%

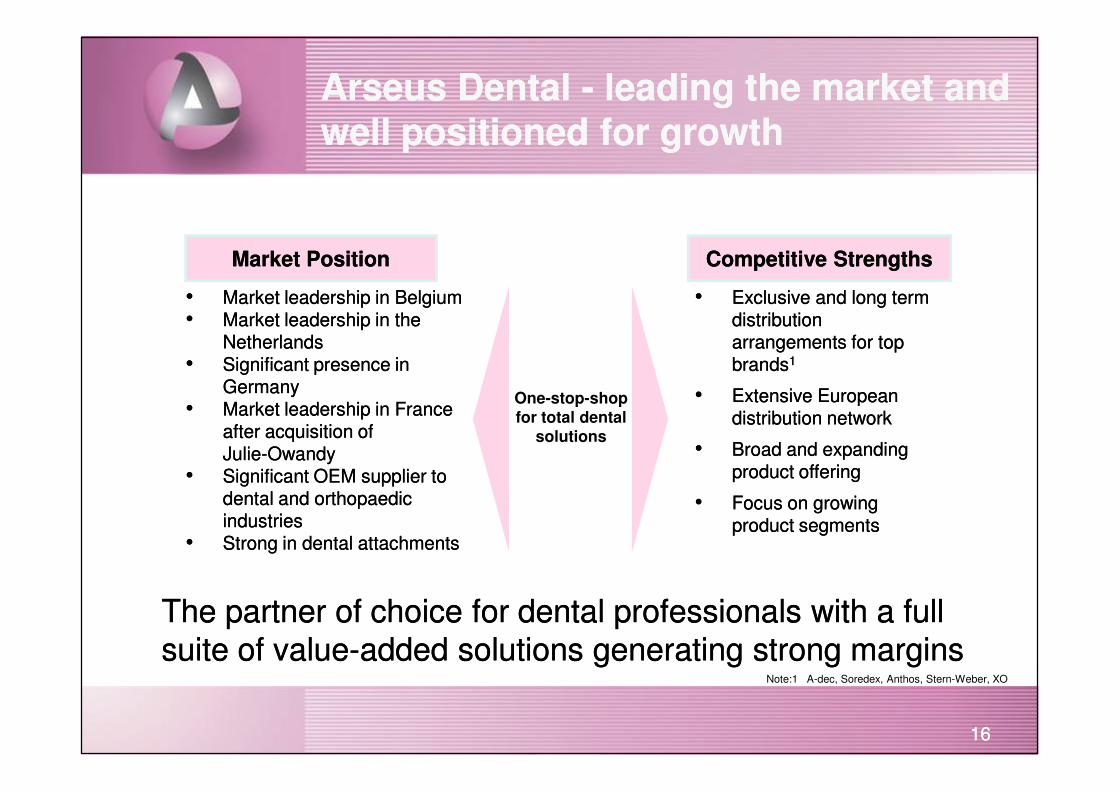

OneOne--stopstop--shop forshop fordental professionalsdental professionals

1515

39%29%

FYFY––07 Sales07 Sales FYFY––07 EBITDA07 EBITDA

Arseus Dental Arseus Dental -- leading the market and leading the market and well positioned for growthwell positioned for growth

•• Market leadership in BelgiumMarket leadership in Belgium•• Market leadership in the Market leadership in the

NetherlandsNetherlands•• Significant presence in Significant presence in

GermanyGermany••

•• Exclusive and long term Exclusive and long term distribution distribution arrangements for top arrangements for top brandsbrands11

•• Extensive European Extensive European One-stop-shop

Market PositionMarket Position Competitive StrengthsCompetitive Strengths

1616

GermanyGermany•• Market leadership in France Market leadership in France

after acquisition ofafter acquisition ofJulieJulie--OwandyOwandy

•• Significant OEM supplier to Significant OEM supplier to dental and orthopaedic dental and orthopaedic industriesindustries

•• Strong in dental attachmentsStrong in dental attachments

•• Extensive European Extensive European distribution networkdistribution network

•• Broad and expanding Broad and expanding product offeringproduct offering

•• Focus on growing Focus on growing product segmentsproduct segments

One-stop-shop for total dental

solutions

Note:1 A-dec, Soredex, Anthos, Stern-Weber, XO

The partner of choice for dental professionals with a full The partner of choice for dental professionals with a full

suite of valuesuite of value--added solutions generating strong marginsadded solutions generating strong margins

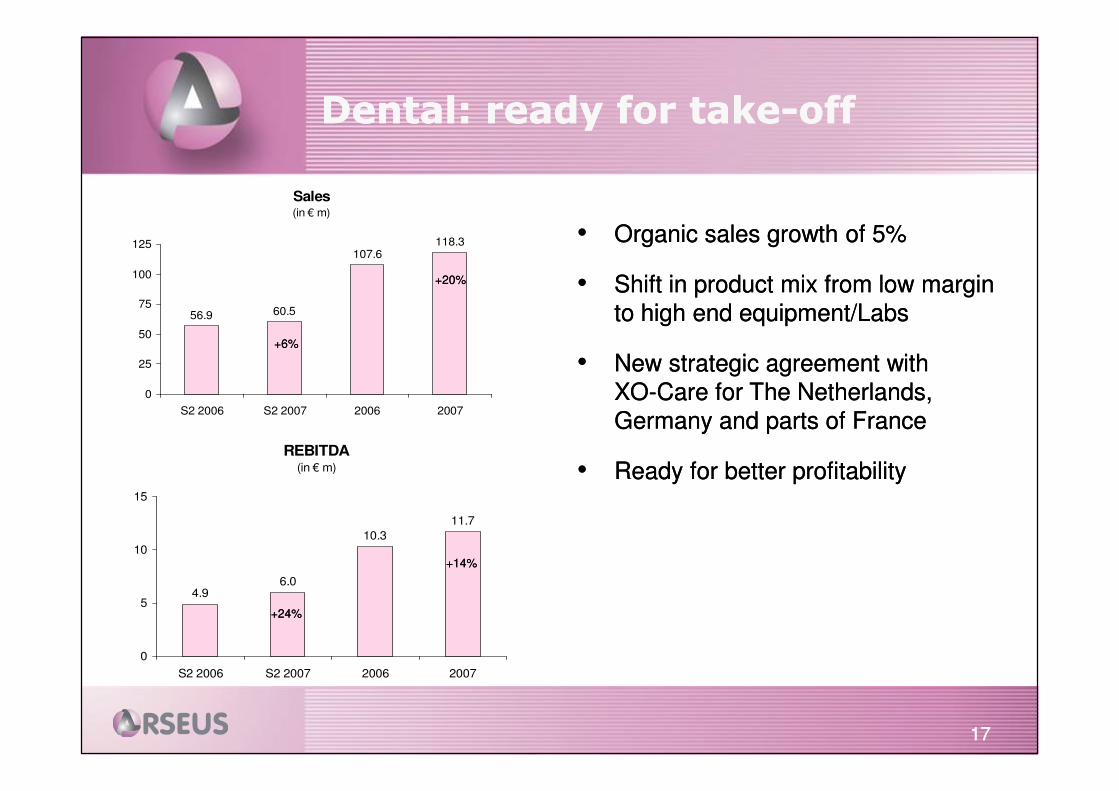

Dental: ready for takeDental: ready for take--offoff

•• Organic sales growth of 5%Organic sales growth of 5%

•• Shift in product mix from low margin Shift in product mix from low margin

to high end equipment/Labsto high end equipment/Labs

•• New strategic agreement withNew strategic agreement with

XOXO--Care for The Netherlands, Care for The Netherlands,

Sales(in € m)

118.3107.6

60.556.9

0

25

50

75

100

125

+6%+6%

+20%+20%

1717

XOXO--Care for The Netherlands, Care for The Netherlands,

Germany and parts of FranceGermany and parts of France

•• Ready for better profitabilityReady for better profitability

0

S2 2006 S2 2007 2006 2007

REBITDA(in € m)

11.7

10.3

6.04.9

0

5

10

15

S2 2006 S2 2007 2006 2007

++1414%%

+24%+24%

ValueValue--added solutions for a added solutions for a wide range of healthcare wide range of healthcare

1818

16% 7%

FYFY––07 Sales07 Sales FYFY––07 EBITDA07 EBITDA

wide range of healthcare wide range of healthcare professionalsprofessionals

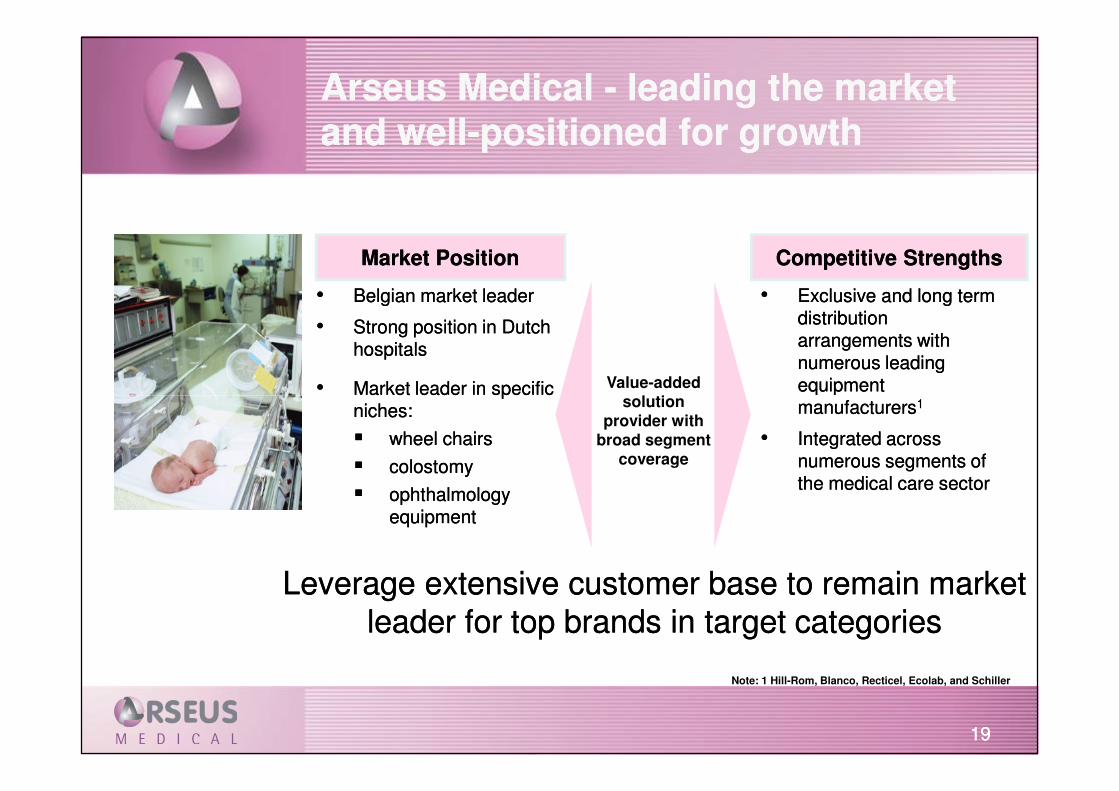

Arseus Medical Arseus Medical -- leading the market leading the market and welland well--positioned for growthpositioned for growth

Market PositionMarket Position Competitive StrengthsCompetitive Strengths

•• Exclusive and long term Exclusive and long term distribution distribution arrangements with arrangements with numerous leading numerous leading equipment equipment Value-added

solution

•• Belgian market leaderBelgian market leader

•• Strong position in Dutch Strong position in Dutch hospitalshospitals

•• Market leader in specific Market leader in specific

1919

manufacturersmanufacturers11

•• Integrated across Integrated across numerous segments of numerous segments of the medical care sectorthe medical care sector

solution provider with

broad segment coverage

•• Market leader in specific Market leader in specific niches:niches:

�� wheel chairswheel chairs

�� colostomycolostomy

�� ophthalmology ophthalmology equipmentequipment

Note: 1 Hill-Rom, Blanco, Recticel, Ecolab, and Schiller

Leverage extensive customer base to remain market Leverage extensive customer base to remain market

leader for top brands in target categoriesleader for top brands in target categories

Medical: focus on bottom lineMedical: focus on bottom line

•• S2 Sales impacted byS2 Sales impacted by

�� Low level of equipment sales in hospitalsLow level of equipment sales in hospitals

�� Effect of change in legislation Effect of change in legislation

wheelchairs wheelchairs �� 2008 impact 2008 impact €€ 2 m2 m

Sales(in € m)

49.547.3

24.725.1

10

20

30

40

50

+5%+5%

--2%2%

2020

•• S2 REBITDA impacted byS2 REBITDA impacted by

�� Lower salesLower sales

�� WheelchairsWheelchairs

•• FY REBITDA shows first signs of successful FY REBITDA shows first signs of successful

turnturn--aroundaround

•• Plan:Plan:

�� High single digit Rebitda by 2010High single digit Rebitda by 2010

�� Focus on market leadership in BeneluxFocus on market leadership in Benelux

0

S2 2006 S2 2007 2006 2007

REBITDA(in € m)

2.7

1.9

1.4

2.1

0

1

2

3

S2 2006 S2 2007 2006 2007

--31%31%

+40%+40%

Integrated IT Solutions for Integrated IT Solutions for

2121

Integrated IT Solutions for Integrated IT Solutions for Healthcare ProfessionalsHealthcare Professionals

9%16%

FYFY––07 Sales07 Sales FYFY––07 07 EBITDAEBITDA

Corilus Corilus -- well positioned for profitable well positioned for profitable growthgrowth

Market PositionMarket Position Competitive StrengthsCompetitive Strengths

•• Platform based onPlatform based oncore modulescore modules

•• Highly skilledHighly skilledsoftware developers and software developers and technical supporttechnical support

Integrated IT solutions for healthcare

•• Market leader in BelgiumMarket leader in Belgium

�� approximately 12,000 approximately 12,000 customerscustomers

•• Strong positionStrong position

2222

technical supporttechnical support

•• Ability toAbility toleverage customer leverage customer relationships of other Arseus relationships of other Arseus divisionsdivisions

•• Strong brands supported by Strong brands supported by strong intellectual propertystrong intellectual property

healthcare professionals

•• Strong positionStrong positionin the Dutchin the Dutchveterinary segmentveterinary segment

•• Significant presence in the Significant presence in the French healthFrench healthcentre segmentcentre segment

Leverage platform to provide high quality Leverage platform to provide high quality

solutions to a broad range of healthcare professionalssolutions to a broad range of healthcare professionals

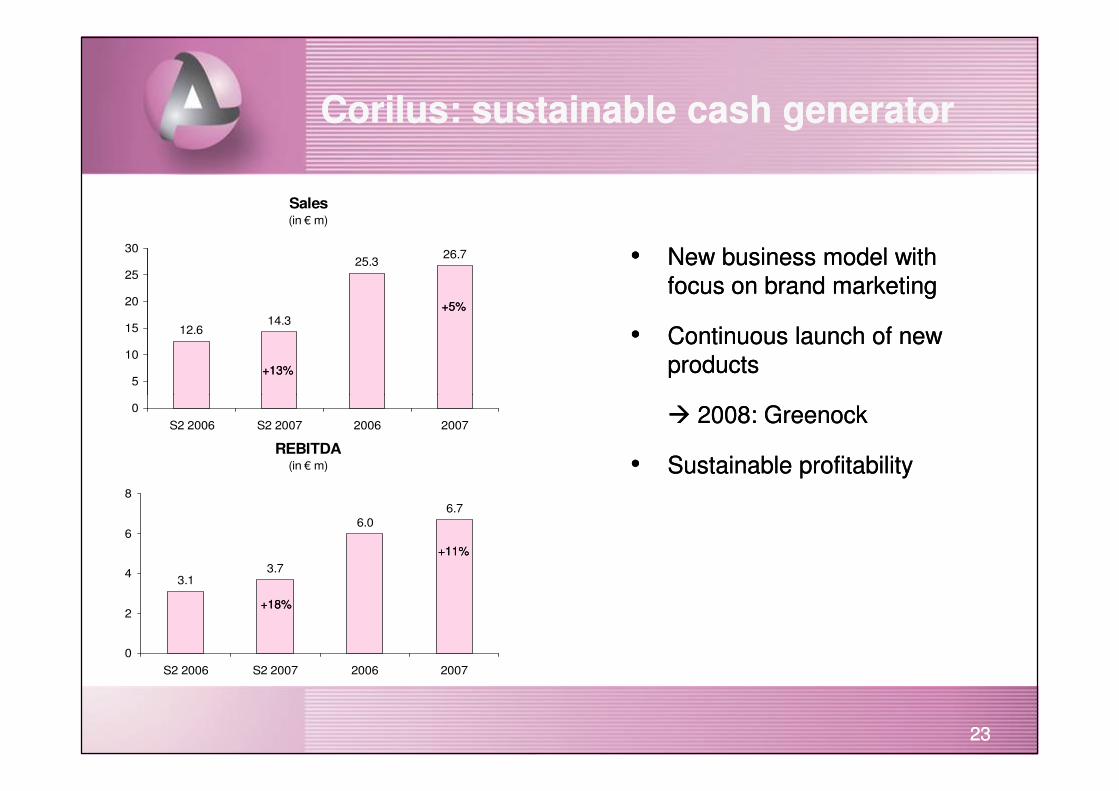

Corilus: sustainable cash generatorCorilus: sustainable cash generator

•• New business model with New business model with

focus on brand marketingfocus on brand marketing

•• Continuous launch of new Continuous launch of new

productsproducts

Sales(in € m)

26.725.3

14.312.6

5

10

15

20

25

30

+13%+13%

+5%+5%

2323

�� 2008: Greenock2008: Greenock

•• Sustainable profitabilitySustainable profitability

0

S2 2006 S2 2007 2006 2007

REBITDA(in € m)

6.7

6.0

3.73.1

0

2

4

6

8

S2 2006 S2 2007 2006 2007

++1111%%

+18% +18%

•• In January Corilus installed In January Corilus installed Greenock softwareGreenock software in the first pharmacies.in the first pharmacies.

•• In March Arseus reached an agreement to start exclusive negotiations In March Arseus reached an agreement to start exclusive negotiations to to acquire the French company Julieacquire the French company Julie--OwandyOwandy. Julie. Julie--Owandy provides Owandy provides

total solutions to dentists via the combination of software and dental total solutions to dentists via the combination of software and dental

imaging equipment and realized imaging equipment and realized turnover of approx. turnover of approx. €€ 20 m 20 m in 2007, in 2007,

withwith anan EBITDA margin of approx. 12%EBITDA margin of approx. 12%. The. The acquisition price of acquisition price of €€18.3 m 18.3 m will be paid entirely in cash and Arseus will also take over will be paid entirely in cash and Arseus will also take over €€ 2 2

After balance sheet dateAfter balance sheet date

2424

18.3 m 18.3 m will be paid entirely in cash and Arseus will also take over will be paid entirely in cash and Arseus will also take over €€ 2 2

million in debt.million in debt.

•• In April Arseus acquired a In April Arseus acquired a 70% interest in TAMDA S.A.70% interest in TAMDA S.A., the first step in , the first step in

Central & Eastern Europe. TAMDA is the Central & Eastern Europe. TAMDA is the Czech market leaderCzech market leader in the in the

sale of pharmaceutical raw materials, creams and ointments to sale of pharmaceutical raw materials, creams and ointments to

pharmacists and realized pharmacists and realized revenues ofrevenues of approx. approx. €€ 6 m6 m in 2007. The in 2007. The

acquisition fits the acquisition fits the buybuy--andand--build strategybuild strategy of Arseus, and of Arseus, and supports supports Fagron’s strategyFagron’s strategy to expand its position as market leader in magistral to expand its position as market leader in magistral

preparations in Europe.preparations in Europe.

Acquisition JulieAcquisition Julie--OwandyOwandy

2525

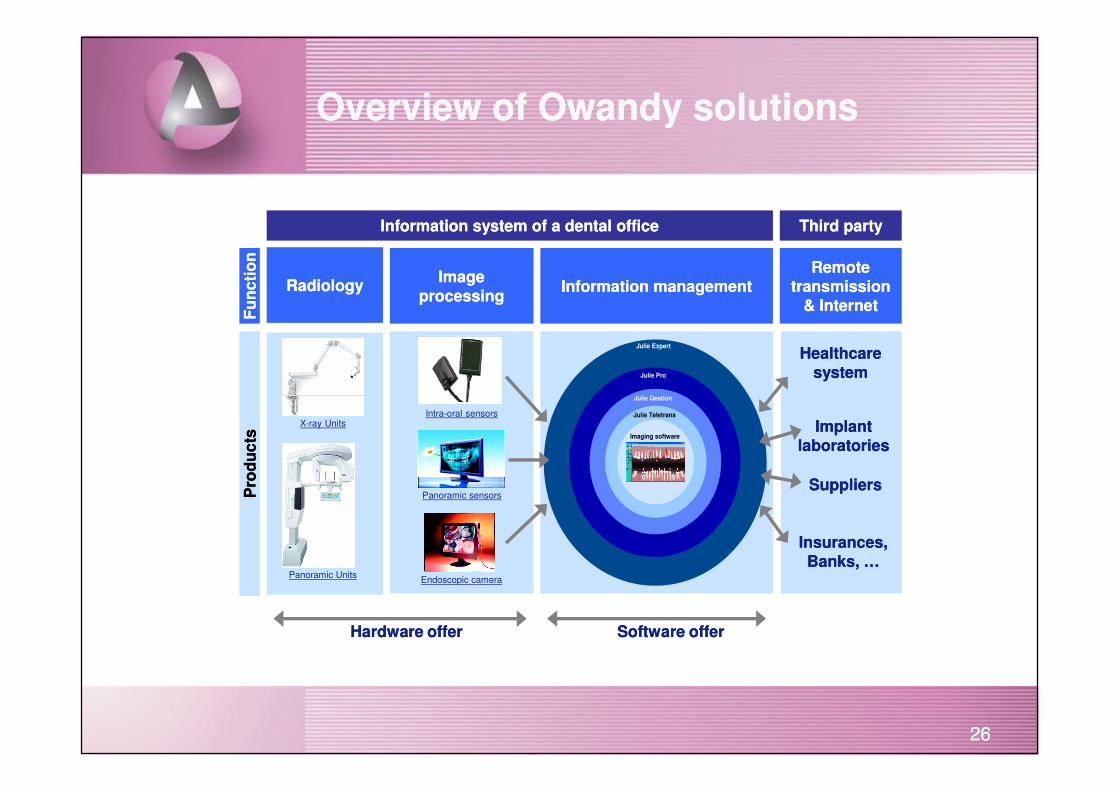

Information system of a dental officeInformation system of a dental office Third partyThird party

Fu

nc

tio

nF

un

cti

on

RadiologyRadiologyImage Image

processingprocessingInformation managementInformation management

Remote Remote transmission transmission

& Internet& Internet

Healthcare Healthcare systemsystem

Julie Gestion

Julie Pro

Julie Expert

Overview of Owandy solutionsOverview of Owandy solutions

2626

Pro

du

cts

Pro

du

cts

Hardware offerHardware offer Software offerSoftware offer

X-ray Units

Panoramic Units

Intra-oral sensors

Panoramic sensors

Endoscopic camera

Implant Implant laboratorieslaboratories

SuppliersSuppliers

Insurances, Insurances, Banks, …Banks, …

Ima

Imaging software

Julie Teletrans

Julie Gestion

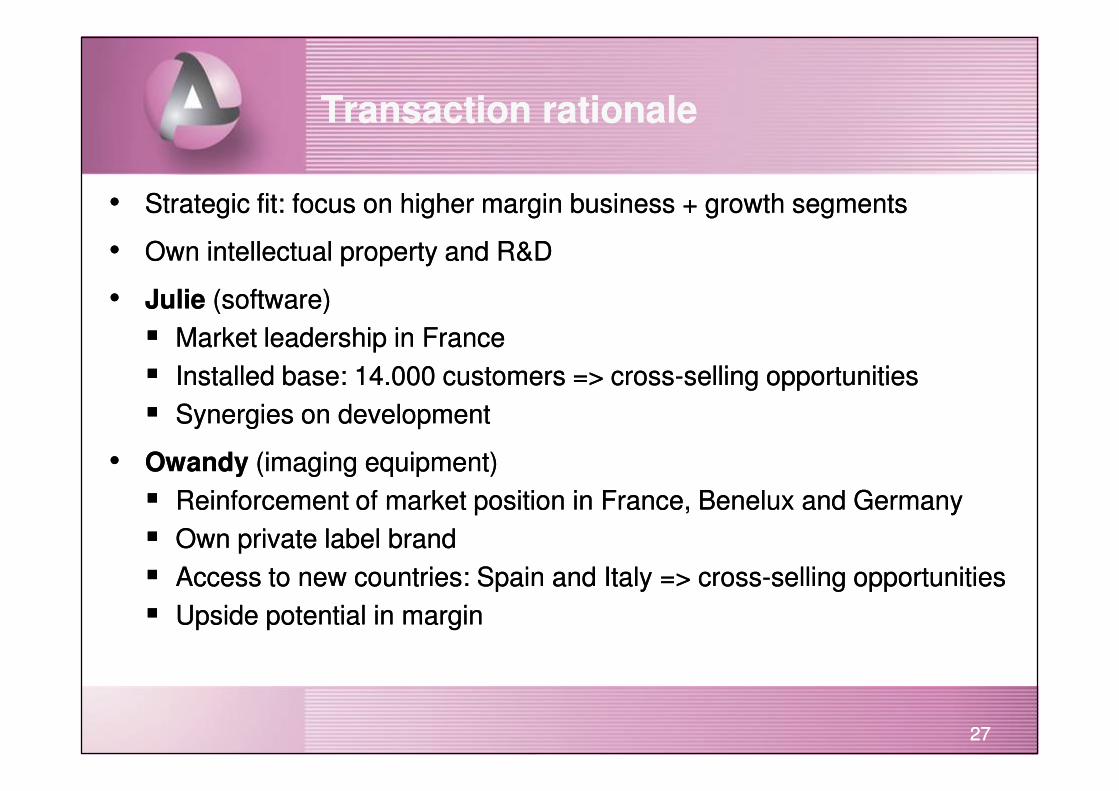

Transaction rationaleTransaction rationale

•• Strategic fit: focus on higher margin business + growth segmentsStrategic fit: focus on higher margin business + growth segments

•• Own intellectual property and R&DOwn intellectual property and R&D

•• JulieJulie (software)(software)

�� Market leadership in France Market leadership in France

�� Installed base: 14.000 customers => crossInstalled base: 14.000 customers => cross--selling opportunitiesselling opportunities

��

2727

�� Synergies on developmentSynergies on development

•• OwandyOwandy (imaging equipment)(imaging equipment)

�� Reinforcement of market position in France, Benelux and GermanyReinforcement of market position in France, Benelux and Germany

�� Own private label brandOwn private label brand

�� Access to new countries: Spain and Italy => crossAccess to new countries: Spain and Italy => cross--selling opportunitiesselling opportunities

�� Upside potential in marginUpside potential in margin

Acquisition TamdaAcquisition Tamda

2828

Transaction rationaleTransaction rationale

•• Geographical expansion of Fagron businessGeographical expansion of Fagron business

•• Access to Eastern Europe => growth marketsAccess to Eastern Europe => growth markets

•• Production capacity => possible synergies (low cost)Production capacity => possible synergies (low cost)

•• Market leader in local marketMarket leader in local market

2929

•• Cross selling possibilitiesCross selling possibilities

•• Central purchase agencyCentral purchase agency

For 2008, the management expects an For 2008, the management expects an organic growth in organic growth in turnoverturnover of approx. of approx. 7% to 8%7% to 8%. Arseus still expects . Arseus still expects to complete to complete a few acquisitionsa few acquisitions during the course of the second and third during the course of the second and third quarter.quarter.

Furthermore, Arseus aims to achieve Furthermore, Arseus aims to achieve turnover of turnover of €€ 500 million 500 million

Outlook 2008Outlook 2008

3030

Furthermore, Arseus aims to achieve Furthermore, Arseus aims to achieve turnover of turnover of €€ 500 million 500 million in 2010in 2010 and realise this by means of a and realise this by means of a combination of organic combination of organic growth and acquisitionsgrowth and acquisitions..

Financial Overview Financial Overview 20072007

3131

35.9

13.1

13.7

11.6

11.4

12.8

10.7

11.2

12.0

11.5

7.9

6.9

6.3

5.7

6.3

6.3

6.2

6.1

6.4

90.3

82.2

68.4

61.8

74.7

67.4

80.0

71.1

65.5

60

80

100S

ale

s (

€m

)Quarterly Sales Breakdown 2006Quarterly Sales Breakdown 2006--20072007--20082008

Sales per quarter Sales per quarter 2006 2006 -- 2007 2007 -- 20082008

3232

33.427.325.922.0

26.624.331.3

24.223.1

35.9

34.3

24.622.7

29.026.1

31.3

28.824.5

11.411.5

0

20

40

2006 2007 2008 2006 2007 2006 2007 2006 2007

Sale

s (

€m

)

Fagron Group Dental Medical Corilus

Q1 Q2 Q3 Q4

REBITDAREBITDAStrong performance in all divisionsStrong performance in all divisions

Dental

Corilus

( €M )

1.4

Medical

0.80.7

+11%

+15 %

41.4

3333

Fagron

REBITDA(

2.7

+15%

1.4

+14%+40 %

+11%

35.8

2006 2007

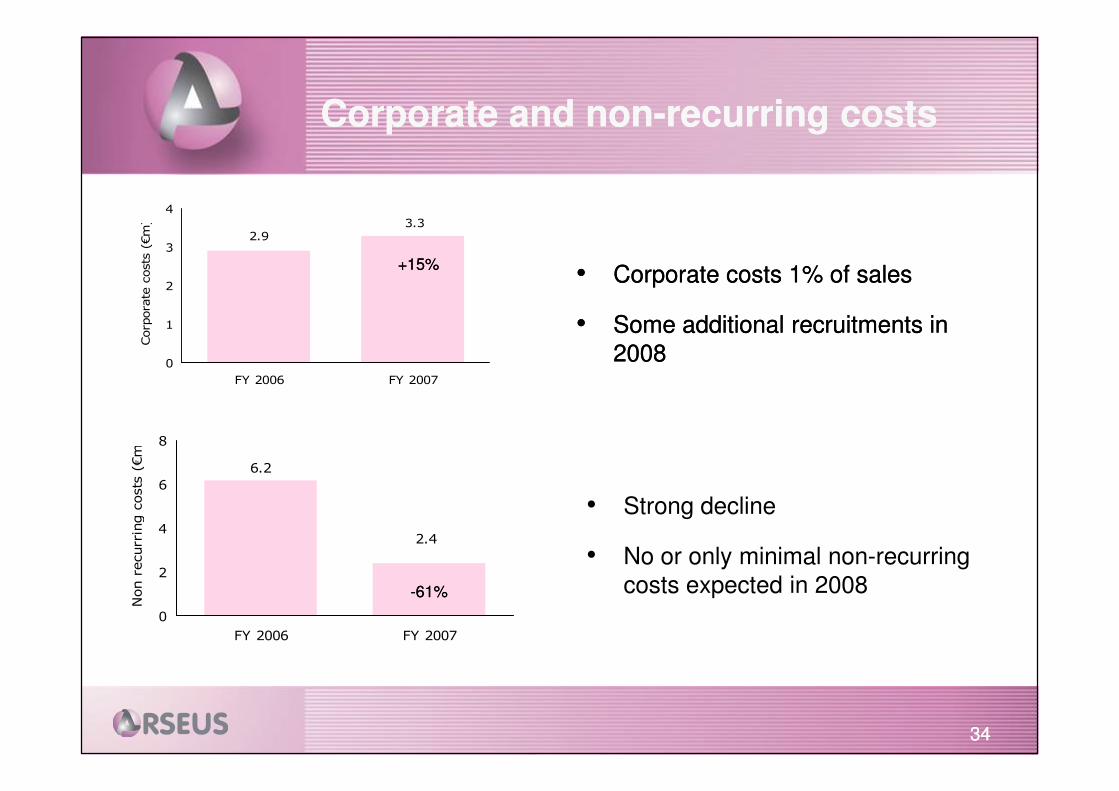

Corporate and nonCorporate and non--recurring costsrecurring costs

•• Corporate costs 1% of salesCorporate costs 1% of sales

•• Some additional recruitments in Some additional recruitments in

20082008

2.93.3

0

1

2

3

4

FY 2006 FY 2007

Corporate costs (€m)

+15%+15%

3434

6.2

2.4

0

2

4

6

8

FY 2006 FY 2007

Non recurring costs (€m)

• Strong decline

• No or only minimal non-recurring

costs expected in 2008--6161%%

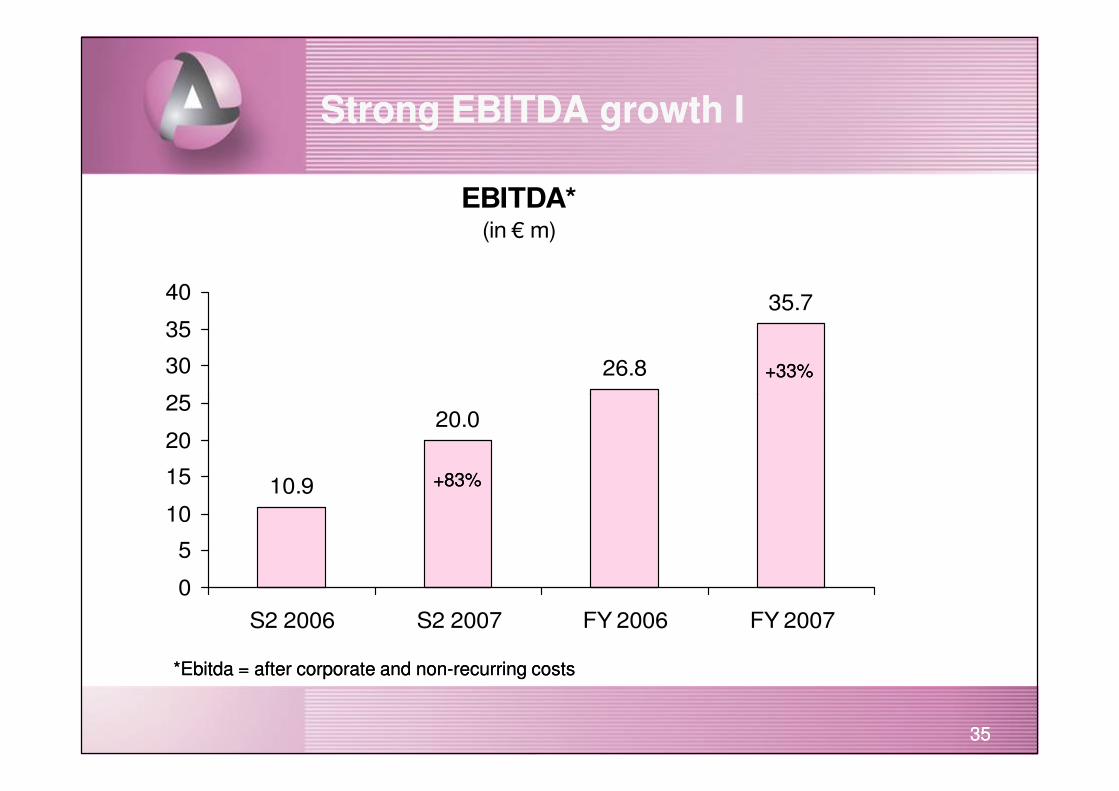

EBITDA*(in € m)

35.7

26.8

25

30

35

40

Strong EBITDA growth IStrong EBITDA growth I

+33%+33%

3535

20.0

10.9

0

5

10

15

20

25

S2 2006 S2 2007 FY 2006 FY 2007

*Ebitda = after corporate and non*Ebitda = after corporate and non--recurring costs recurring costs

+83%+83%

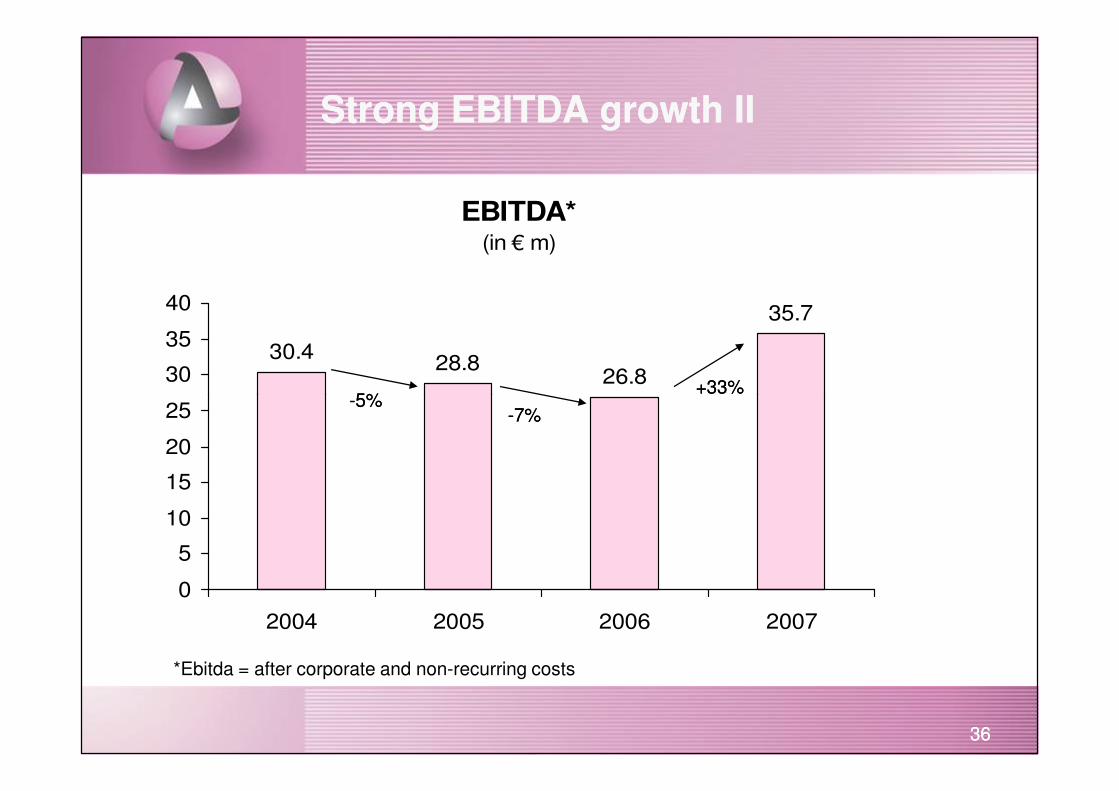

Strong EBITDA growth IIStrong EBITDA growth II

EBITDA*(in € m)

35.7

26.828.8

30.430

35

40

--5%5%++3333%%

3636

*Ebitda = after corporate and non-recurring costs

0

5

10

15

20

25

2004 2005 2006 2007

--5%5%--7%7%

++3333%%

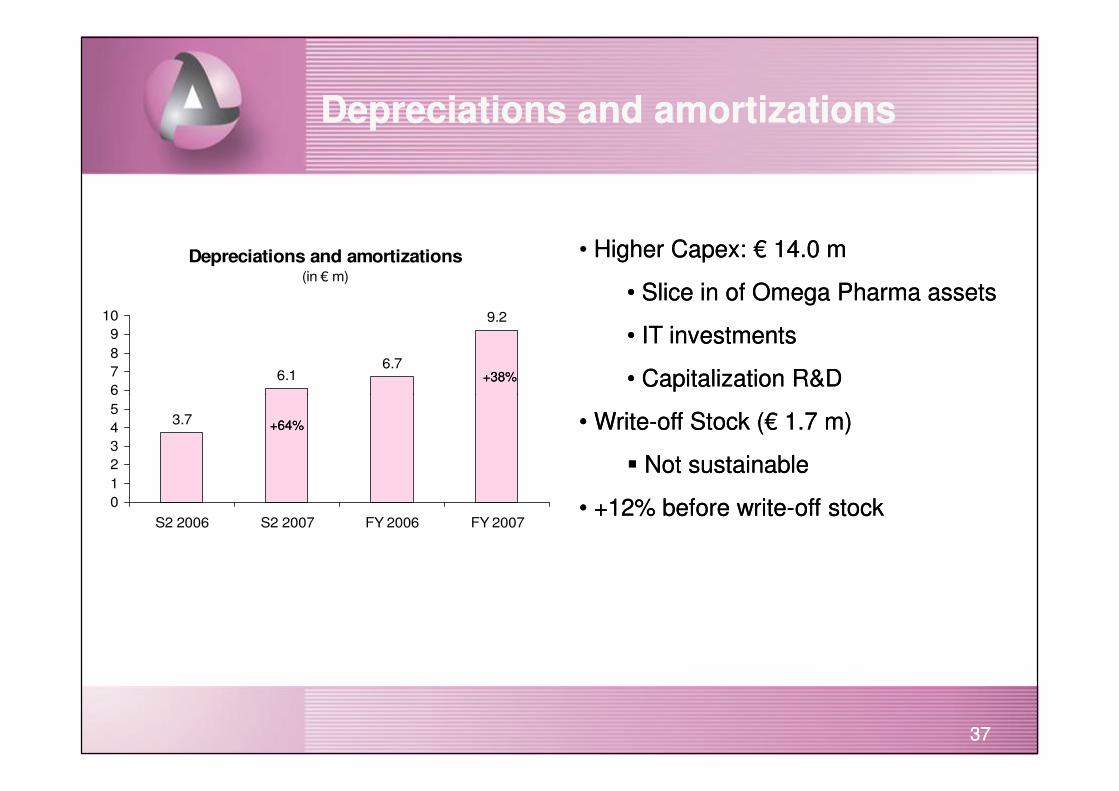

Depreciations and amortizations(in € m)

9.2

6.76.1

6

7

8

9

10

Depreciations and amortizationsDepreciations and amortizations

• Higher Capex: Higher Capex: €€ 14.0 m14.0 m

•• Slice in of Omega Pharma assetsSlice in of Omega Pharma assets

•• IT investmentsIT investments

•• Capitalization R&DCapitalization R&D+38%+38%

3737

3.7

0

1

2

3

4

5

6

S2 2006 S2 2007 FY 2006 FY 2007

•• WriteWrite--off Stock (off Stock (€€ 1.7 m)1.7 m)

�� Not sustainableNot sustainable

•• +12% before write+12% before write--off stockoff stock

+64%+64%

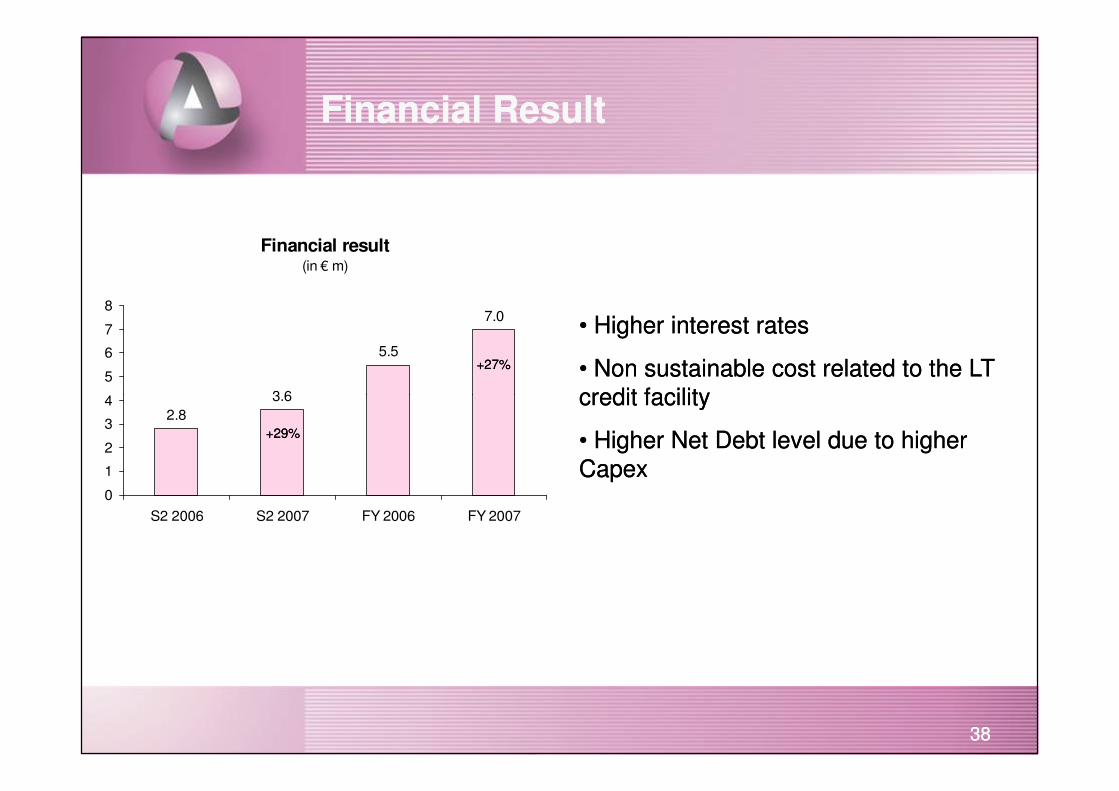

Financial result(in € m)

7.0

5.5

3.64

5

6

7

8

Financial ResultFinancial Result

•• Higher interest ratesHigher interest rates

•• Non sustainable cost related to the LT Non sustainable cost related to the LT

credit facilitycredit facility

+27%+27%

3838

3.6

2.8

0

1

2

3

4

S2 2006 S2 2007 FY 2006 FY 2007

credit facilitycredit facility

•• Higher Net Debt level due to higher Higher Net Debt level due to higher

CapexCapex

+29%+29%

Net ProfitNet Profit

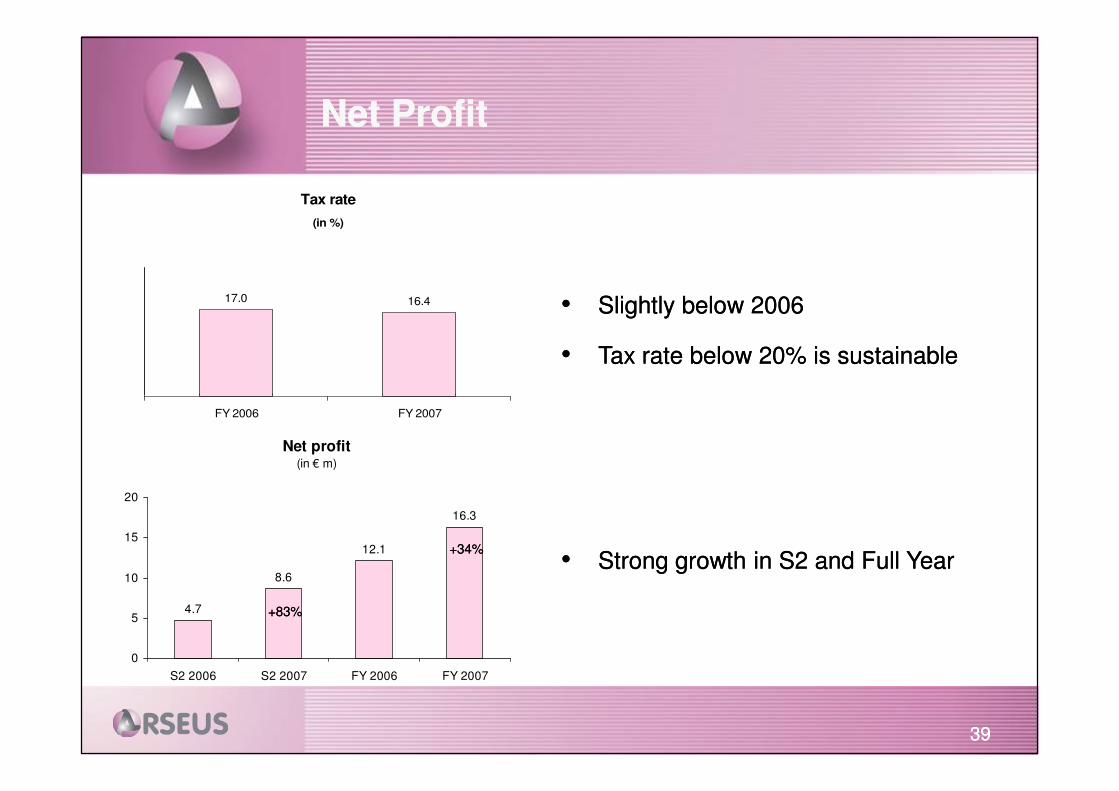

•• Slightly below 2006Slightly below 2006

•• Tax rate below 20% is sustainableTax rate below 20% is sustainable

Tax rate

(in %)

16.417.0

3939

•• Strong growth in S2 and Full YearStrong growth in S2 and Full Year

FY 2006 FY 2007

Net profit(in € m)

4.7

8.6

12.1

16.3

0

5

10

15

20

S2 2006 S2 2007 FY 2006 FY 2007

+83%+83%

++3434%%

Conclusion P&LConclusion P&L

•• Strong operational performance in all divisionsStrong operational performance in all divisions

•• Corporate costs under controlCorporate costs under control

•• Low level of nonLow level of non--recurring costsrecurring costs

•• Strong impact of inventory write off on DAStrong impact of inventory write off on DA

4040

•• Strong impact of inventory write off on DAStrong impact of inventory write off on DA

•• Financial result impacted by oneFinancial result impacted by one--offs (credit facility)offs (credit facility)

•• Sustainable tax rate < 20%Sustainable tax rate < 20%

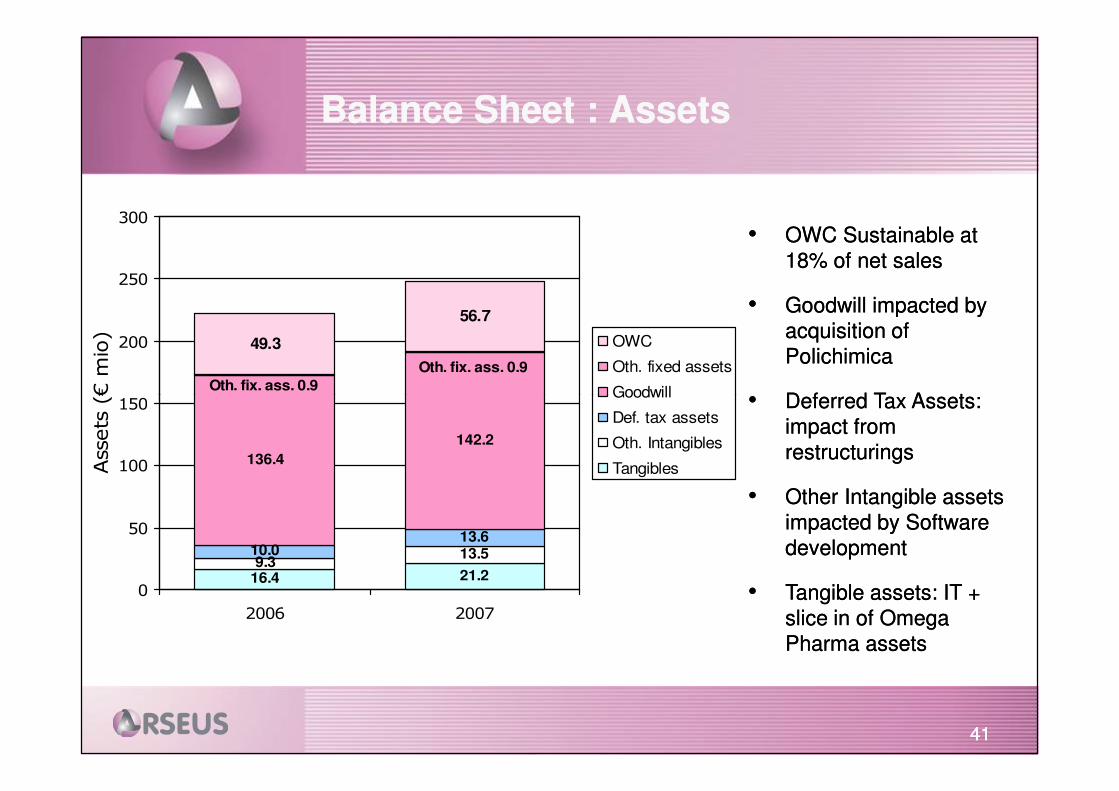

Balance Sheet : AssetsBalance Sheet : Assets

•• OWC Sustainable at OWC Sustainable at

18% of net sales18% of net sales

•• Goodwill impacted by Goodwill impacted by

acquisition of acquisition of

Polichimica Polichimica

•• Deferred Tax Assets: Deferred Tax Assets: Oth. fix. ass. 0.9

Oth. fix. ass. 0.9

56.7

49.3

150

200

250

300

Assets (€ m

io) OWC

Oth. fixed assets

Goodwill

4141

•• Deferred Tax Assets: Deferred Tax Assets:

impact from impact from

restructuringsrestructurings

•• Other Intangible assets Other Intangible assets

impacted by Software impacted by Software

developmentdevelopment

•• Tangible assets: IT + Tangible assets: IT +

slice in of Omega slice in of Omega

Pharma assetsPharma assets

21.216.4

13.59.3

13.610.0

136.4

142.2

0

50

100

150

2006 2007

Assets (€ m

io)

Goodwill

Def. tax assets

Oth. Intangibles

Tangibles

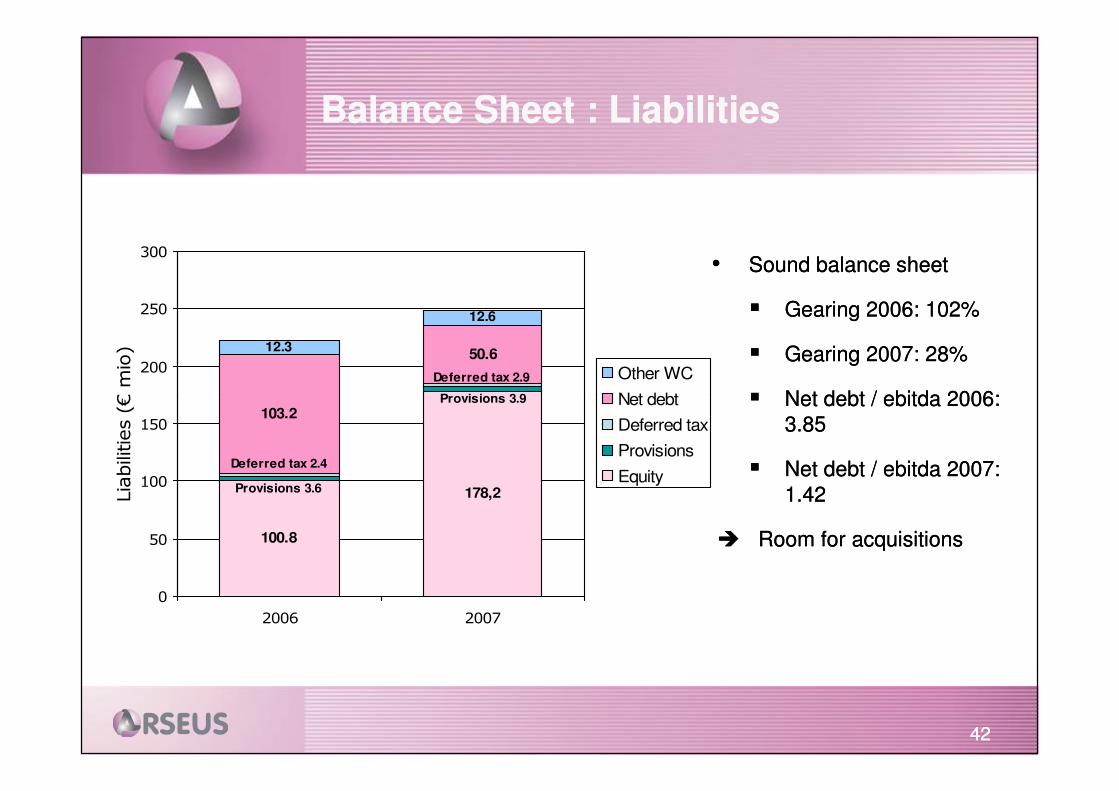

Balance Sheet : LiabilitiesBalance Sheet : Liabilities

•• Sound balance sheetSound balance sheet

�� Gearing 2006: 102%Gearing 2006: 102%

�� Gearing 2007: 28%Gearing 2007: 28%

�� Net debt / ebitda 2006: Net debt / ebitda 2006: Provisions 3.9

Deferred tax 2.9

50.612.3

12.6

200

250

300

Liabilities (€ m

io)

Other WC

Net debt

4242

�� Net debt / ebitda 2006: Net debt / ebitda 2006:

3.853.85

�� Net debt / ebitda 2007: Net debt / ebitda 2007:

1.421.42

�� Room for acquisitionsRoom for acquisitions

178,2

100.8

Provisions 3.9

Provisions 3.6

Deferred tax 2.4

103.2

0

50

100

150

2006 2007

Liabilities (€ m

io)

Net debt

Deferred tax

Provisions

Equity

AgendaAgenda::

2.2. Discussion and approval of the annual accounts closed on Discussion and approval of the annual accounts closed on December 31December 31stst 2007.2007.

Motion to voteMotion to vote::

4343

Motion to voteMotion to vote::Approval of the annual accounts closed on December 31Approval of the annual accounts closed on December 31stst 2007.2007.

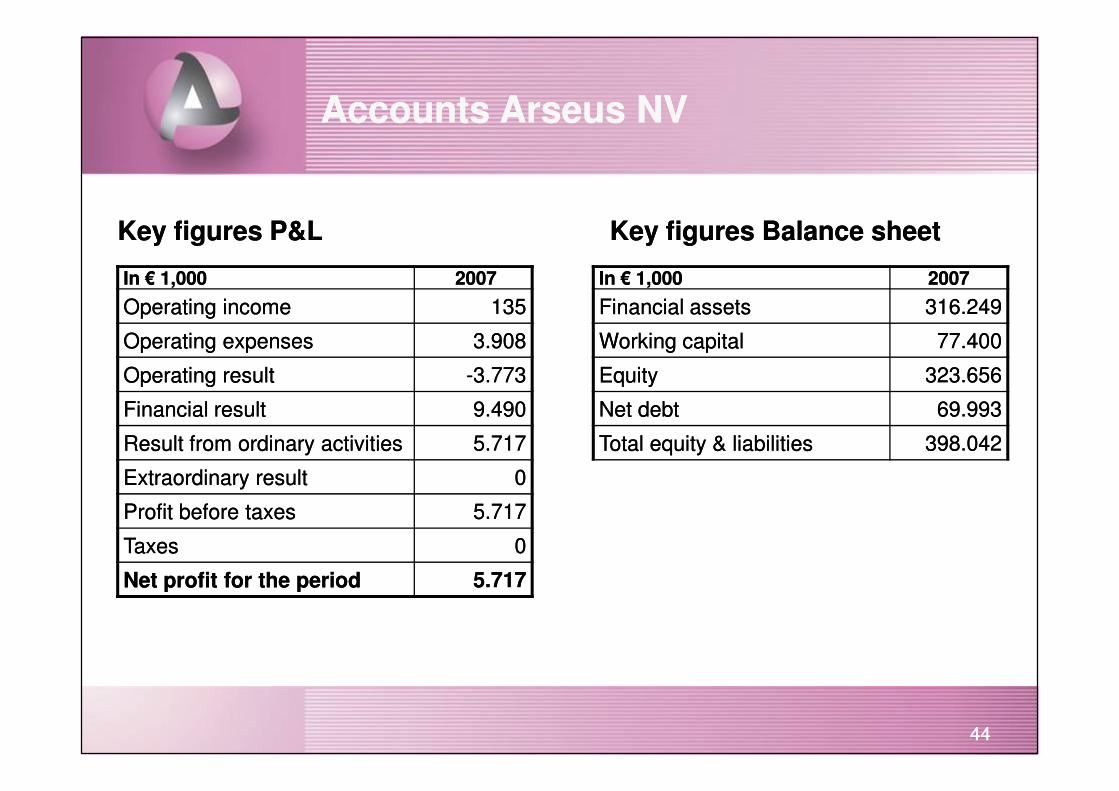

Key figures P&LKey figures P&L

In In €€ 11,,000000 20072007

Operating incomeOperating income 135135

Operating expensesOperating expenses 3.9083.908

Operating resultOperating result --3.7733.773

Key figures Balance sheet Key figures Balance sheet

In In €€ 1,0001,000 20072007

Financial assetsFinancial assets 316.249316.249

Working capitalWorking capital 77.40077.400

EquityEquity 323.656323.656

Accounts Arseus NVAccounts Arseus NV

4444

Financial resultFinancial result 9.4909.490

Result from ordinary activities Result from ordinary activities 5.7175.717

Extraordinary resultExtraordinary result 00

Profit before taxesProfit before taxes 5.7175.717

TaxesTaxes 00

Net profit for the periodNet profit for the period 5.7175.717

Net debtNet debt 69.99369.993

Total equity & liabilities Total equity & liabilities 398.042398.042

AgendaAgenda::

3.3. Appropriation of the result of the financial year closed on Appropriation of the result of the financial year closed on December 31December 31stst 2007.2007.

Motion to voteMotion to vote::

4545

Motion to voteMotion to vote::Approval of the allocation of the result as included in the annual accounts including a gross dividend of € 0.06 per share.

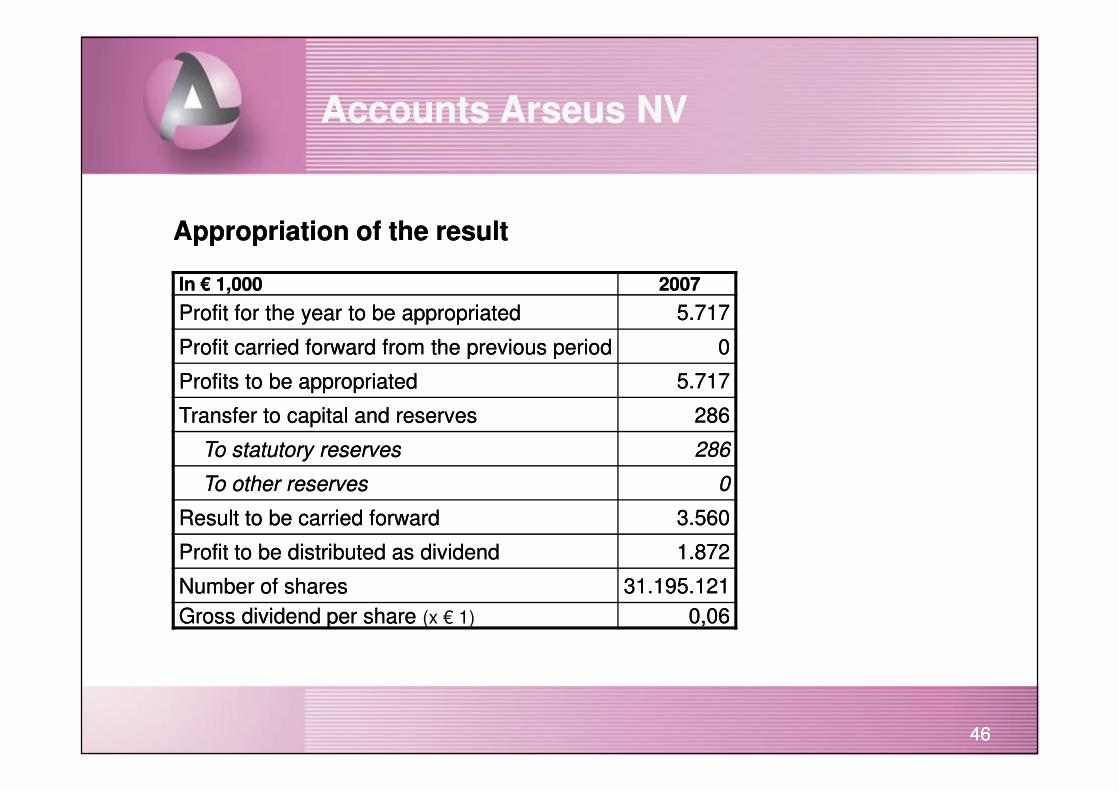

Appropriation of the resultAppropriation of the result

In In €€ 1,0001,000 20072007

Profit for the year to be appropriatedProfit for the year to be appropriated 5.7175.717

Profit carried forward from the previous periodProfit carried forward from the previous period 00

Profits to be appropriatedProfits to be appropriated 5.7175.717

Accounts Arseus NVAccounts Arseus NV

4646

Transfer to capital and reservesTransfer to capital and reserves 286286

To statutory reservesTo statutory reserves 286286

To other reservesTo other reserves 00

Result to be carried forwardResult to be carried forward 3.5603.560

Profit to be distributed as dividendProfit to be distributed as dividend 1.8721.872

Number of sharesNumber of shares 31.195.12131.195.121

Gross dividend per share Gross dividend per share (x € 1) 0,060,06

AgendaAgenda::

44.. Communication of the consolidated annual accounts and the Communication of the consolidated annual accounts and the consolidated reports.consolidated reports.

4747

AgendaAgenda::

5.5. Granting discharge to the members of the board of directors Granting discharge to the members of the board of directors and the statutory auditor.and the statutory auditor.

Motion to voteMotion to vote::

4848

Motion to voteMotion to vote::By separate vote, granting full discharge to the directors and By separate vote, granting full discharge to the directors and statutory auditor who were active during the financial year 2007 statutory auditor who were active during the financial year 2007 for the tasks executed by them during the course of the financial for the tasks executed by them during the course of the financial year.year.

Board of directorsBoard of directors::•• Robert PeekRobert Peek•• Johannes StolsJohannes Stols•• Luc VandewalleLuc Vandewalle•• Gerardus van JeverenGerardus van Jeveren•• Jan PeetersJan Peeters

4949

•• Jan PeetersJan Peeters•• Couckinvest NV (Marc Coucke)Couckinvest NV (Marc Coucke)•• Benoit GraulichBenoit Graulich

Statutory auditorStatutory auditor::•• PricewaterhouseCoopers Bedrijfsrevisoren BCVBAPricewaterhouseCoopers Bedrijfsrevisoren BCVBA

AgendaAgenda::

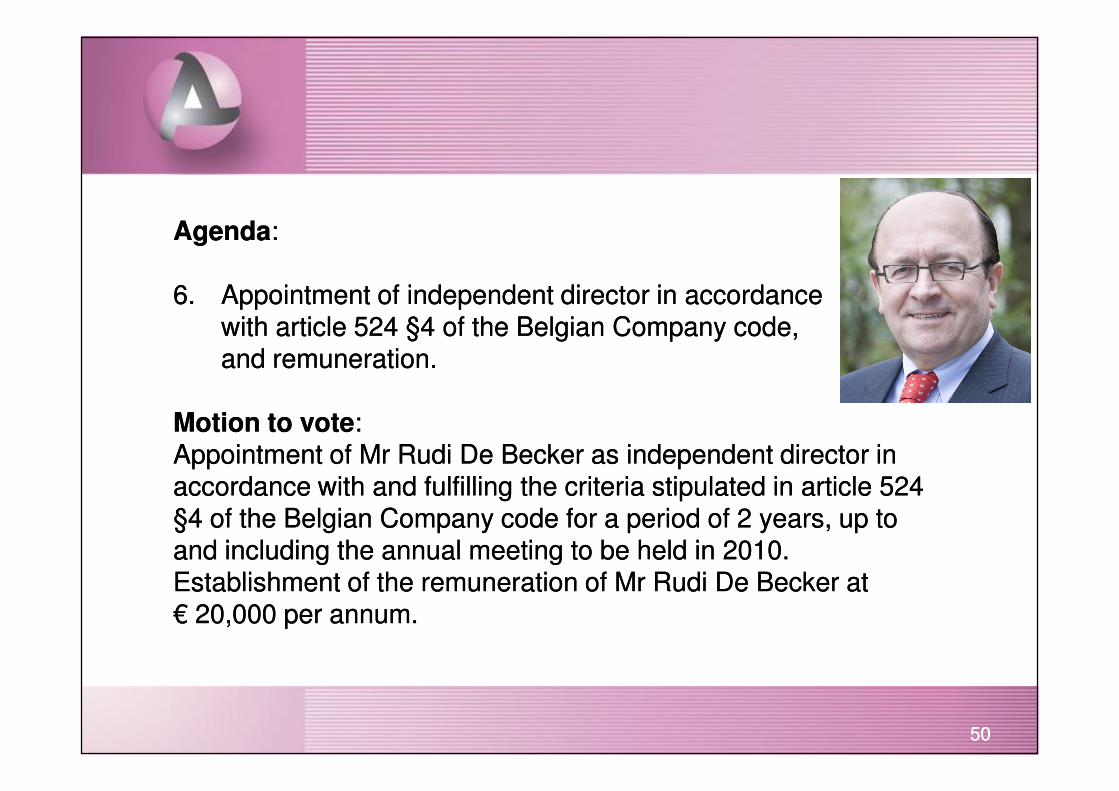

6.6. Appointment of independent director in accordance Appointment of independent director in accordance with article 524 with article 524 §§4 of the Belgian Company code, 4 of the Belgian Company code, and remuneration.and remuneration.

5050

Motion to voteMotion to vote::Appointment of Mr Rudi De Becker as independent director in Appointment of Mr Rudi De Becker as independent director in accordance with and fulfilling the criteria stipulated in article 524 accordance with and fulfilling the criteria stipulated in article 524 §§4 of the Belgian Company code for a period of 2 years, up to 4 of the Belgian Company code for a period of 2 years, up to and including the annual meeting to be held in 2010. and including the annual meeting to be held in 2010. Establishment of the remuneration of Mr Rudi De Becker at Establishment of the remuneration of Mr Rudi De Becker at €€ 20,000 per annum.20,000 per annum.

AgendaAgenda::

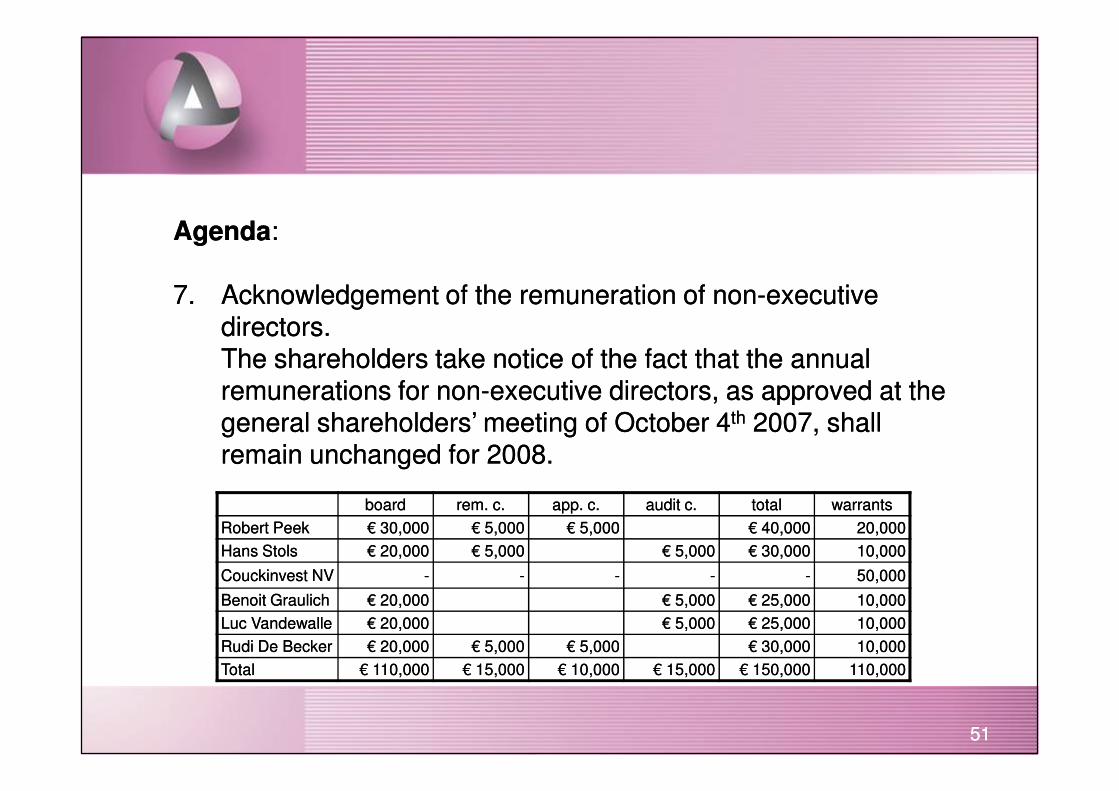

7.7. Acknowledgement of the remuneration of nonAcknowledgement of the remuneration of non--executive executive directors.directors.The shareholders take notice of the fact that the annual The shareholders take notice of the fact that the annual remunerations for nonremunerations for non--executive directors, as approved at the executive directors, as approved at the

5151

remunerations for nonremunerations for non--executive directors, as approved at the executive directors, as approved at the general shareholders’ meeting of October general shareholders’ meeting of October 44thth 20072007, shall , shall remain unchanged for remain unchanged for 20082008..

boardboard rem. c.rem. c. app. c.app. c. audit c.audit c. totaltotal warrantswarrants

Robert PeekRobert Peek €€ 30,00030,000 €€ 5,0005,000 €€ 5,0005,000 €€ 40,00040,000 20,00020,000

Hans StolsHans Stols €€ 20,00020,000 €€ 5,0005,000 €€ 5,0005,000 €€ 30,00030,000 10,00010,000

Couckinvest NVCouckinvest NV -- -- -- -- -- 50,00050,000

Benoit GraulichBenoit Graulich €€ 20,00020,000 €€ 5,0005,000 €€ 25,00025,000 10,00010,000

Luc VandewalleLuc Vandewalle €€ 20,00020,000 €€ 5,0005,000 €€ 25,00025,000 10,00010,000

Rudi De BeckerRudi De Becker €€ 20,00020,000 €€ 5,0005,000 €€ 5,0005,000 €€ 30,00030,000 10,00010,000

TotalTotal €€ 110,000110,000 €€ 15,00015,000 €€ 10,00010,000 €€ 15,00015,000 €€ 150,000150,000 110,000110,000

AgendaAgenda::

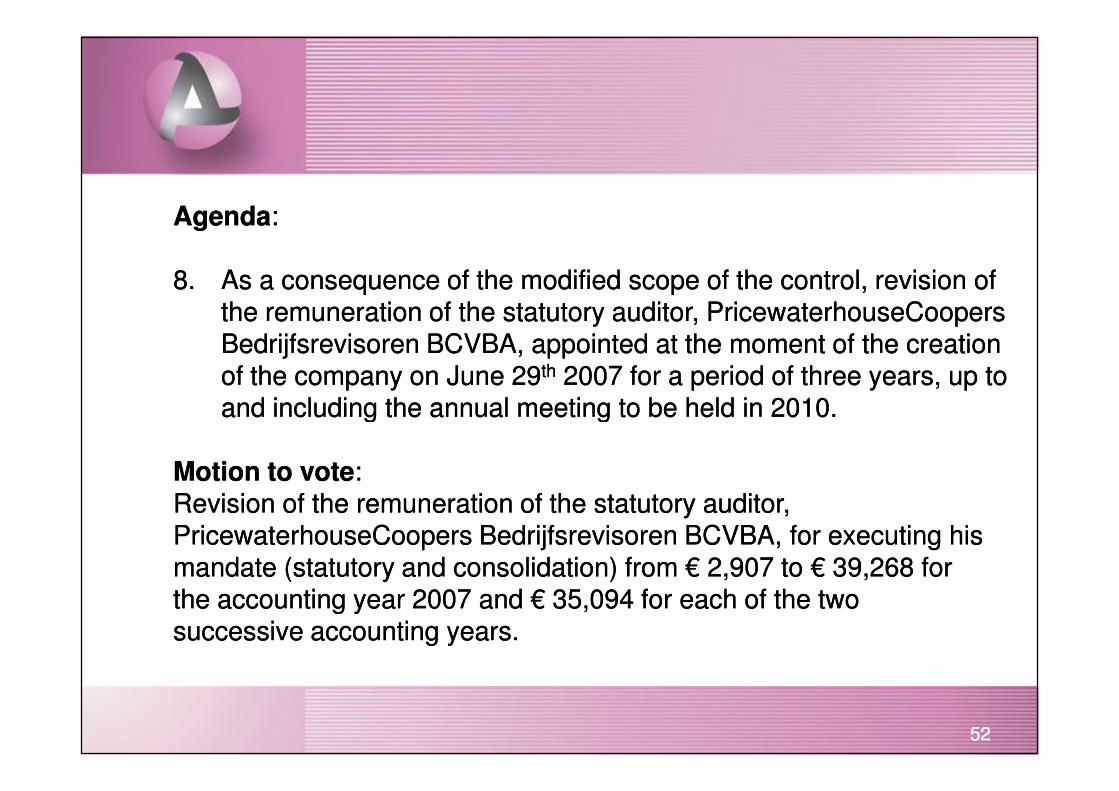

8.8. As a consequence of the modified scope of the control, revision of As a consequence of the modified scope of the control, revision of the remuneration of the statutory auditor, PricewaterhouseCoopers the remuneration of the statutory auditor, PricewaterhouseCoopers Bedrijfsrevisoren BCVBA, appointed at the moment of the creation Bedrijfsrevisoren BCVBA, appointed at the moment of the creation of the company on June 29of the company on June 29thth 2007 for a period of three years, up to 2007 for a period of three years, up to and including the annual meeting to be held in 2010.and including the annual meeting to be held in 2010.

5252

and including the annual meeting to be held in 2010.and including the annual meeting to be held in 2010.

Motion to voteMotion to vote::Revision of the remuneration of the statutory auditor, Revision of the remuneration of the statutory auditor, PricewaterhouseCoopers Bedrijfsrevisoren BCVBA, for executing his PricewaterhouseCoopers Bedrijfsrevisoren BCVBA, for executing his mandate (statutory and consolidation) from mandate (statutory and consolidation) from €€ 2,907 to 2,907 to €€ 39,268 for 39,268 for the accounting year 2007 and the accounting year 2007 and €€ 35,094 for each of the two 35,094 for each of the two successive accounting years.successive accounting years.

AgendaAgenda::

9.9. Explanation and discussion of the Corporate Governance at Explanation and discussion of the Corporate Governance at Arseus NV.Arseus NV.

•• Current composition of the board of directorsCurrent composition of the board of directors

5353

•• Current composition of the board of directorsCurrent composition of the board of directors•• Current composition of the executive committeeCurrent composition of the executive committee•• Overview of remunerationsOverview of remunerations•• Corporate Governance CharterCorporate Governance Charter

Composition of the board of directorsComposition of the board of directors

5454

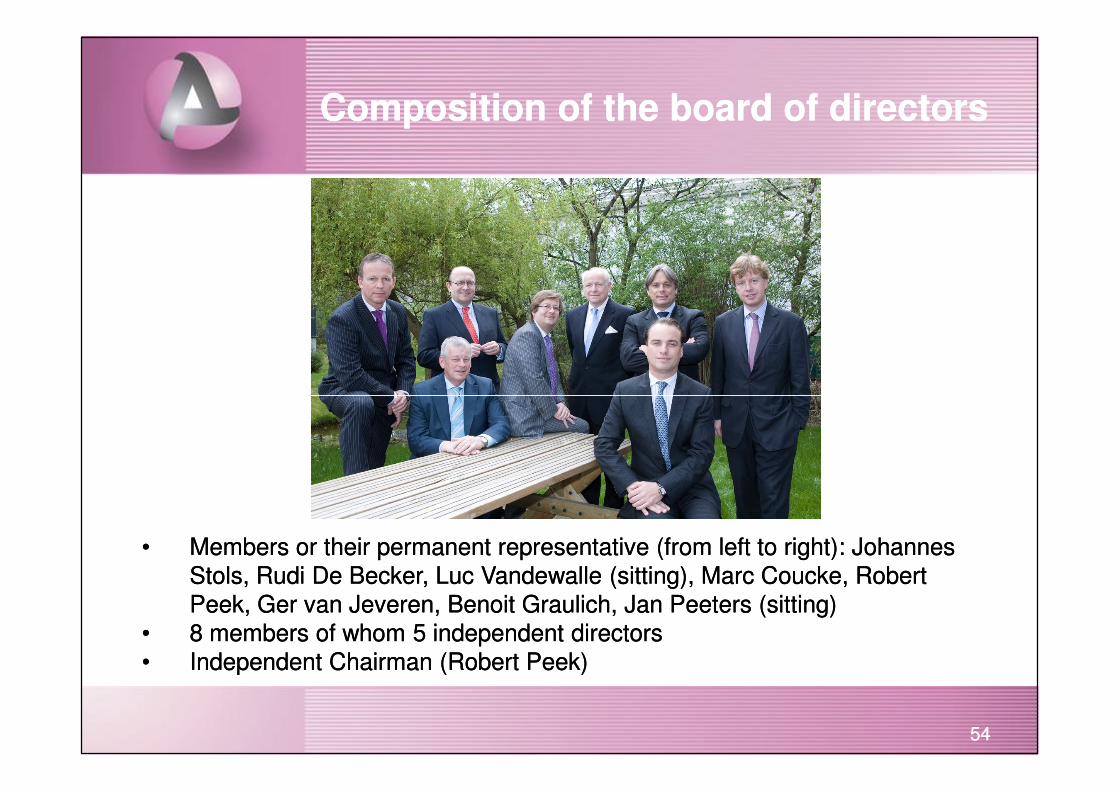

•• Members or their permanent representative (from left to right): Johannes Members or their permanent representative (from left to right): Johannes

Stols, Rudi De Becker, Luc Vandewalle (sitting), Marc Coucke, Robert Stols, Rudi De Becker, Luc Vandewalle (sitting), Marc Coucke, Robert

Peek, Ger van Jeveren, Benoit Graulich, Jan Peeters (sitting)Peek, Ger van Jeveren, Benoit Graulich, Jan Peeters (sitting)

•• 8 members of whom 5 independent directors8 members of whom 5 independent directors

•• Independent Chairman (Robert Peek)Independent Chairman (Robert Peek)

board board

of directorsof directors

remunerationremuneration

committeecommittee

auditaudit

committeecommittee

executiveexecutive

committeecommittee

appointmentappointment

committeecommittee

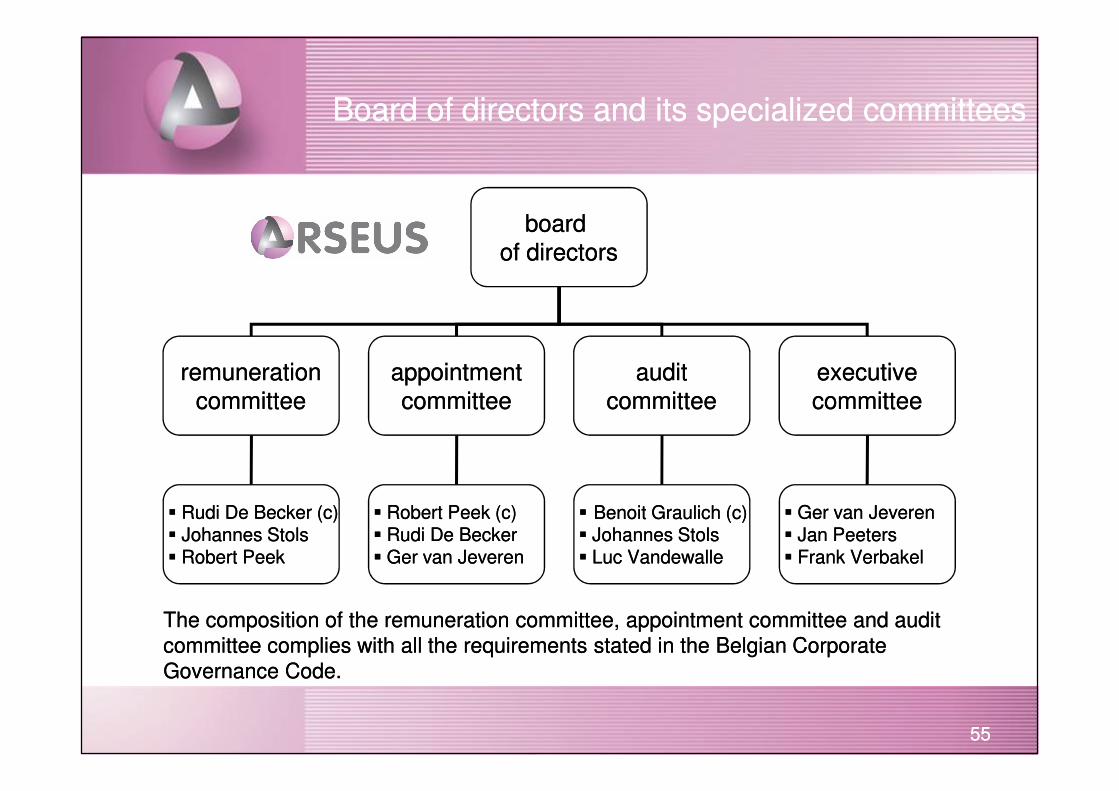

Board of directors and its specialized committeesBoard of directors and its specialized committees

5555

committeecommittee committeecommittee committeecommitteecommitteecommittee

�� Robert Peek (c)Robert Peek (c)�� Rudi De BeckerRudi De Becker�� Ger van JeverenGer van Jeveren

�� Rudi De Becker (c)Rudi De Becker (c)�� Johannes StolsJohannes Stols�� Robert PeekRobert Peek

�� Benoit Graulich (c)Benoit Graulich (c)�� Johannes StolsJohannes Stols�� Luc VandewalleLuc Vandewalle

�� Ger van Jeveren Ger van Jeveren �� Jan PeetersJan Peeters�� Frank VerbakelFrank Verbakel

The composition of the remuneration committee, appointment committee and audit The composition of the remuneration committee, appointment committee and audit

committee complies with all the requirements stated in the Belgian Corporate committee complies with all the requirements stated in the Belgian Corporate

Governance Code.Governance Code.

Composition of executive committeeComposition of executive committee

5656

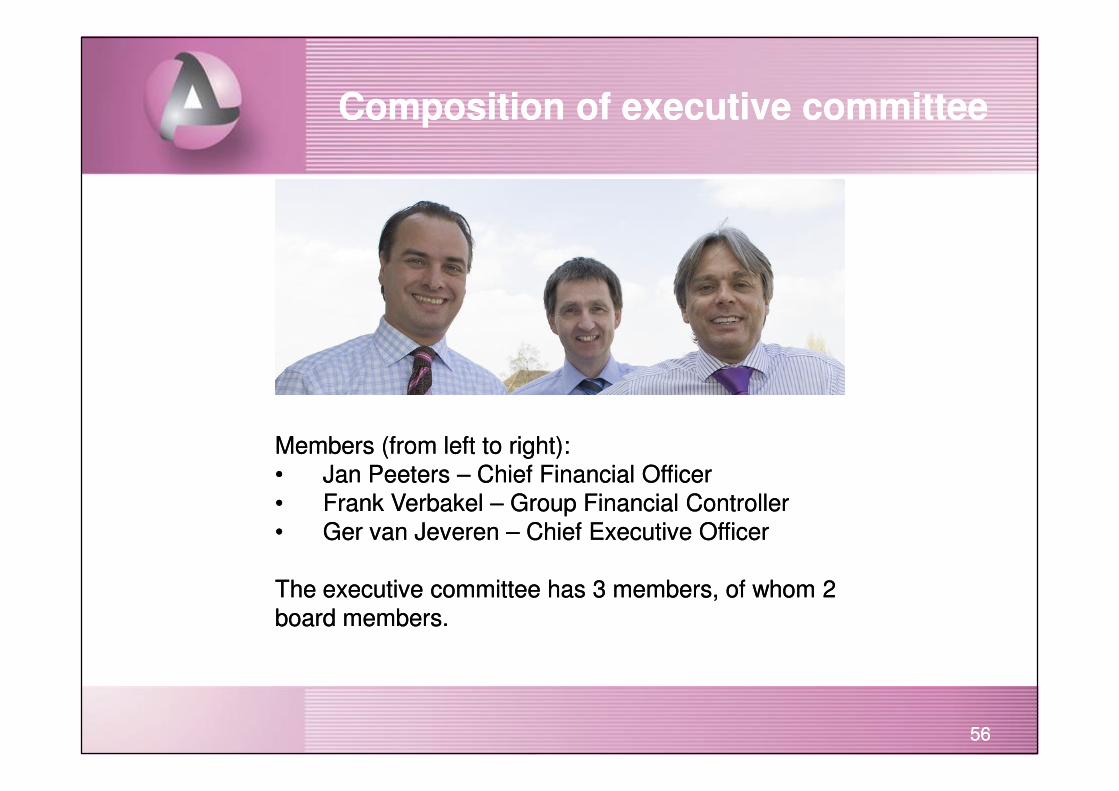

Members (from left to right):Members (from left to right):

•• Jan Peeters Jan Peeters –– Chief Financial OfficerChief Financial Officer

•• Frank Verbakel Frank Verbakel –– Group Financial ControllerGroup Financial Controller

•• Ger van Jeveren Ger van Jeveren –– Chief Executive OfficerChief Executive Officer

The executive committee has 3 members, of whom 2 The executive committee has 3 members, of whom 2

board members.board members.

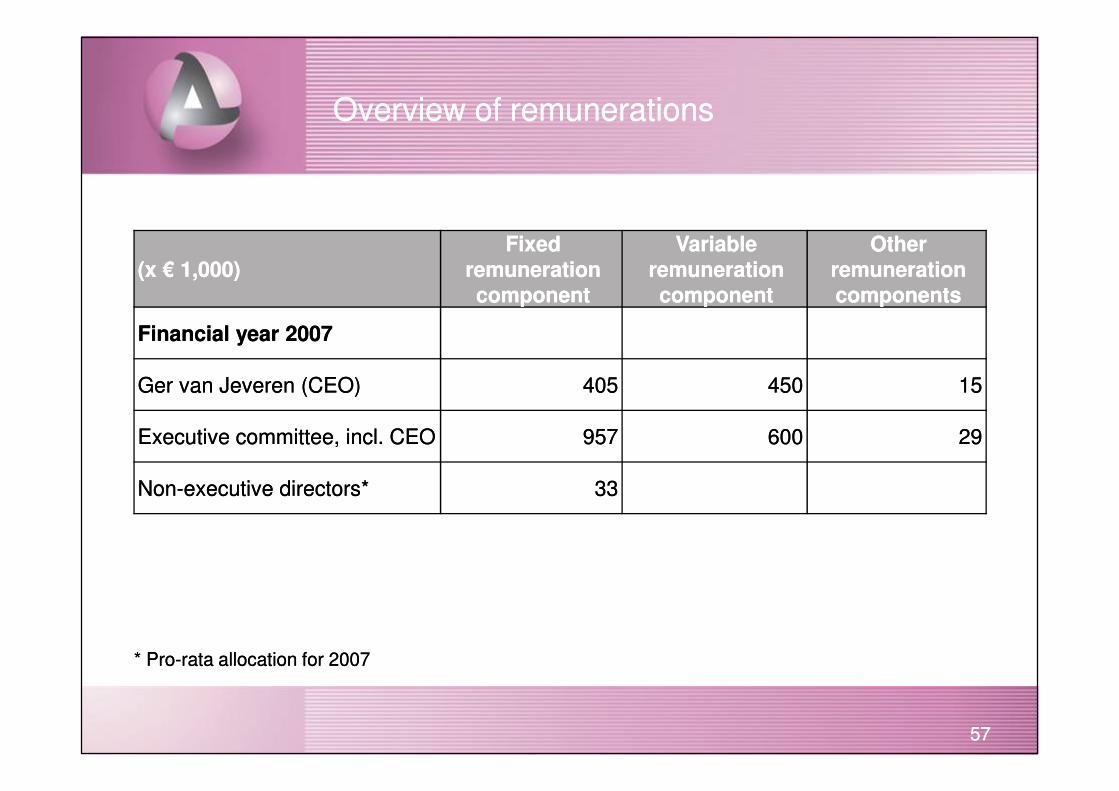

Overview of remunerationsOverview of remunerations

(x (x €€ 1,000)1,000)Fixed Fixed

remuneration remuneration componentcomponent

Variable Variable remuneration remuneration componentcomponent

Other Other remuneration remuneration componentscomponents

Financial year 2007Financial year 2007

Ger van Jeveren (CEO)Ger van Jeveren (CEO) 405405 450450 1515

5757

Ger van Jeveren (CEO)Ger van Jeveren (CEO) 405405 450450 1515

Executive committee, incl. CEOExecutive committee, incl. CEO 957957 600600 2929

NonNon--executive directors*executive directors* 3333

* Pro* Pro--rata allocation for 2007rata allocation for 2007

The board of directors of Arseus approved the first issue of the The board of directors of Arseus approved the first issue of the

Corporate Governance Charter on 4 October 2007. An updated issue Corporate Governance Charter on 4 October 2007. An updated issue

was approved on 24 April 2008.was approved on 24 April 2008.

The objective of the board of directors is to comply with the principles of The objective of the board of directors is to comply with the principles of

the Belgian Corporate Governance Code as closely as possible.the Belgian Corporate Governance Code as closely as possible.

Corporate Governance CharterCorporate Governance Charter

5858

The Company holds the opinion that it complies with all principles and The Company holds the opinion that it complies with all principles and

provisions of the Belgian Corporate Governance Code, with the exception provisions of the Belgian Corporate Governance Code, with the exception

of the possibility to allocate warrants to nonof the possibility to allocate warrants to non--executive directors and of the executive directors and of the

right for shareholders representing at least 20% of the capital to propose right for shareholders representing at least 20% of the capital to propose

subjects for the agenda of the General Meeting of Shareholders.subjects for the agenda of the General Meeting of Shareholders.

The corresponding explanations for the deviations are described in The corresponding explanations for the deviations are described in

the annual report 2007 of Arseus.the annual report 2007 of Arseus.

AgendaAgenda::

10.10. MiscellaneousMiscellaneous

5959

Contact details Financial calender

Arseus Investor RelationsArseus Investor Relations

Constantijn van RietschotenConstantijn van Rietschoten

+31 (0)88 33 11 211 (phone)+31 (0)88 33 11 211 (phone)

+31 (0)88 33 11 201 (fax)+31 (0)88 33 11 201 (fax)

15 May ‘0815 May ‘08 Dividend payableDividend payable

15 July ‘0815 July ‘08 Trading update Q2 2008Trading update Q2 2008

26 August ‘0826 August ‘08 S1 2008 resultsS1 2008 results

14 October ‘0814 October ‘08 Trading update Q3 2008Trading update Q3 2008

6060

+31 (0)88 33 11 201 (fax)+31 (0)88 33 11 201 (fax)

[email protected]@arseus.com

Disclaimer

This presentation contains forwardThis presentation contains forward--looking information which is based on current internal estimates looking information which is based on current internal estimates and expectations as well as market expectations. Forwardand expectations as well as market expectations. Forward--looking statements contain inherent risks looking statements contain inherent risks and apply exclusively on the date they are made. The actual results may differ substantially from and apply exclusively on the date they are made. The actual results may differ substantially from those included in the forward looking statement.those included in the forward looking statement.

14 October ‘0814 October ‘08 Trading update Q3 2008Trading update Q3 2008

13 January ‘0913 January ‘09 Trading update Q4 & FY 2008Trading update Q4 & FY 2008