animal genetics and breeding thesis and dissertations

TRANSCRIPT

DSpace Institution

DSpace Repository http://dspace.org

Animal Genetics and Breeding Thesis and Dissertations

2021-06-17

ON-FARM PHENOTYPIC

CHARACTERIZATION OF SEKOTA

SHEEP TYPE AND BREEDING

PRACTICES OF FARMERS IN

SELECTED DISTRICTS OF

WAGHIMRA ZONE, AMHARA

REGION, ETHIOPI

Afework Tafach

http://ir.bdu.edu.et/handle/123456789/12117

Downloaded from DSpace Repository, DSpace Institution's institutional repository

| P a g e

BAHIRDARUNIVERSITY

SCHOOL OF GRADUATE STUDIES

FACTORS INFLUENCING LOAN REPAYMENT OF WOMENS’ IN RURAL

MULTIPURPOSE COOPERATIVES; THE CASE OF GUBALAFTO WOREDA,

NORTH WOLLO ZONE, AMHARA REGION

M.Sc. Thesis Research

By

Mesfin Tesfay

E-mail- [email protected]

MAJOR ADVISOR; Zemen Ayalew (PhD)

CO ADVISOR; Almaz Giziew (PhD)

Bahir Dar, Ethiopia.

November, 2020

0

| P a g e

BAHIRDAR UNIVERSITY

SCHOOL OF GRADUATE STUDIES

FACTORS INFLUENCING LOAN REPAYMENT OF WOMENS’ IN RURAL

MULTIPURPOSE COOPERATIVES; THE CASE OF GUBALAFTO WOREDA,

NORTH WOLLO ZONE, AMHARA REGION

M.Sc. Thesis Research

By

Mesfin Tesfay

E-mail- [email protected]

MAJOR ADVISOR; Zemen Ayalew (PhD)

CO ADVISOR; Almaz Giziew (PhD)

Bahir Dar, Ethiopia.

November, 2020

0

I | P a g e

THESIS APPROVAL SHEET

As member of the Board of Examiners of the Master of Sciences (M.Sc.) thesis open defense

examination, we have read and evaluated this thesis prepared by Mr. Mesfin Tesfay “Factors

Influencing Loan Repayment of Women’s’ Multipurpose Cooperatives, the Case of Gubalaffto

Woreda North Wollo Zone, Amahar Region” We hereby certify that, the thesis is accepted for

fulfilling the requirements for the award of the degree of Master of Sciences (M.Sc.) in Rural

Development Management.

Board of Examiners

Degsew Melak (PhD) ________

Name of External Examiner Signature Date

Azanaw Abebe__________ _ ___

Name of Internal Examiner Signature Date

II | P a g e

DECLARATION

This is to certify that this thesis entitled “Factors Influencing Loan Repayment of Women’s’

Multipurpose Cooperatives, the Case of Gubalaffto Woreda North Wollo Zone, Amahar Region”

submitted in partial fulfillment of the requirements of the degree of Master of Science in Rural

Development Management to the Graduate Program of College of Agriculture and Environmental

Sciences, Bahir Dar University by Mr. Mesfin Tesfay. (ID. No. BDU07021134PS) is an authentic

work carried out by him under our guidance. The matter embodied in this project work has not

been submitted earlier for award of any degree or diploma to the best of our knowledge and belief.

Name of the Student

Mr. Mesfin Tesfay, ,

Signature Date

Name of the Supervisors

1) Zemen Ayalew (PhD) -------------------------- ,-----------------------------

Major supervisor Signature Date

2) Almaz Giziew (PhD) ---------------------------------, ----------------------------------------

Co-Advisor Signature Date

III | P a g e

ACKNOWLEDGEMENT

I am deeply grateful and indebted to Dr. ZEMEN AYALEW, major advisor, for his

encouragement, suggestions, guidance and overall assistance. Successful accomplishment of this

research would have been very difficult without his generous time devotion from the early design

of the questionnaire to the final write-up of the thesis by adding valuable, constructive and ever

teaching comments and thus I am indebted to him for his kind and tireless efforts that enabled me

to finalize the study.

I also owe my deepest gratitude to Dr. ALMAZ GIZIEW, co-advisor, for her useful and valuable

comments which became important points of consideration in the manuscript. She has spent her

valuable time from shaping the questionnaire of the survey through the production of the draught

of the thesis.

Moreover, the 115 sample respondent’s cooperative, extension workers, cooperative Office, and

other cooperated individuals deserve special thanks for their unforgettable duty during data

collection.

Finally, I would like to express my sincere appreciation and gratitude to my wife, Workiy Kassa

for her special strength. My father, Tesfay Engda, which financial support made the study a

success.

IV | P a g e

DEDICATION

I dedicate this thesis manuscript to my wife, W/ro Workiy Kassa, together with our kids Emanda

Mesfin, for all their continuous contribution throughout my life.

V | P a g e

ACRONYMS AND ABBREVIATION

ACCI Americans for Community Cooperation in Other Nations

ADB Asian Development Bank

AEMFI Association of Ethiopian micro finance institution

ARFEOB Amahar Regional Finance & Economic Offices

CFI Cooperative Financial Institutions

COOPs Cooperatives

CSA Central Statistics Authority CUs Credit Unions

EPRDFE Ethiopian People’s Revolutionary Democratic Force

FAO Food and Agricultural Organization

FCA Federal Cooperative Agency

FSAs Financial Services Associations

GDP Gross Domestic Product

GWAARUDO Gubalaffeto Woreda Agriculture and rural Development Office

GWCOPO Gubalaffeto Woreda Cooperative Promotion Office

ICA International Cooperative Alliance

ILO International Labor Organization

M.a.s.l Meters above Sea Level

MFIs Microfinance Institutions

MOA Ministry of Agriculture

VI | P a g e

NGOs Non- Governmental Organization

NWZCOP North wollo zone cooperatives promotion office

SACCO Saving and Credit Cooperative

TLU Tropical Live Stock Unit

UN United Nations

UNCDF United Nations Capital Development Fund

UNDP United Nations Development Program

UNICEF United Nations Children's Fund

I | P a g e

Contents DECLARATION ............................................................................................................................ II

ACKNOWLEDGEMENT ............................................................................................................ III

DEDICATION .............................................................................................................................. IV

ABSTRACT ....................................................................................................................................V

CHAPTER ONE ............................................................................................................................. 1

1. INTRODUCTION ...................................................................................................................... 1

1.1 Background of the Study ....................................................................................................... 1

1.2 Statement of the Problem ...................................................................................................... 3

1.4 Objectives of the Study ......................................................................................................... 4

1.5 Scope and Limitations ........................................................................................................... 4

1.6 Significance of the Study ...................................................................................................... 5

1.7. Organization of the Thesis ................................................................................................... 5

CHAPTER TWO ............................................................................................................................ 5

2. LITERATURE REVIEW ........................................................................................................... 5

2.1 Definitions and Concepts ...................................................................................................... 5

2.2. Loan Repayment Performance of borrowers ....................................................................... 8

2.3 SACCOs ................................................................................................................................ 9

2.4. History of Savings and Credit Cooperatives in Ethiopia ................................................... 10

2.4.1 RUSACCOs in the Amhara Region ......................................................................... 11

2.5. Organization and Management of SACCOs ...................................................................... 11

2.6. Empirical Studies on Loan Repayment Performance ........................................................ 12

2.6.1. Empirical studies in Ethiopia ...................................................................................... 12

CHAPTER THREE ....................................................................................................................... 15

3. RESEARCH METHDOLOGY ................................................................................................. 15

II | P a g e

3.1 Description of the study area .............................................................................................. 15

3.1.2Farming system ............................................................................................................. 15

3.1.3 Farmer’s cooperatives .................................................................................................. 16

3.2 Sample size determination .................................................................................................. 17

3.3 Sampling technique ............................................................................................................. 17

3.4 Methods of data collection .................................................................................................. 18

3.6 Descriptive statistics ........................................................................................................... 19

3.7 Econometric model ............................................................................................................. 19

3.7.1 Specification of the Logit Model ................................................................................. 20

3.8 Hypothesis and Definition of Variables .............................................................................. 21

CHAPTER FOUR ......................................................................................................................... 27

4. RESULTS AND DISCUSSION ............................................................................................... 27

4.1. Demographic and Socio-economic Characteristics ........................................................... 27

4.1.1 Age of the borrowers .................................................................................................... 27

4.1.2 Family structure ........................................................................................................... 28

4.1.3 Educational status ........................................................................................................ 28

4.1.4 Celebrate on social holidays ........................................................................................ 29

4.1.1.5 Participation on saving & Loan amount ................................................................... 31

4.1.6 Agro ecologic differentials ........................................................................................... 31

4.1.7 Loan diversion .............................................................................................................. 33

4.1.8 Timeliness of credit. ..................................................................................................... 34

4.1.9. Livestock ownership of sample households ................................................................ 35

4.2.2 Results of Econometric Analysis ................................................................................. 37

4.2.3 Focus Groups Discussion ............................................................................................. 42

4.2.4 Key Informants Interview ............................................................................................ 42

III | P a g e

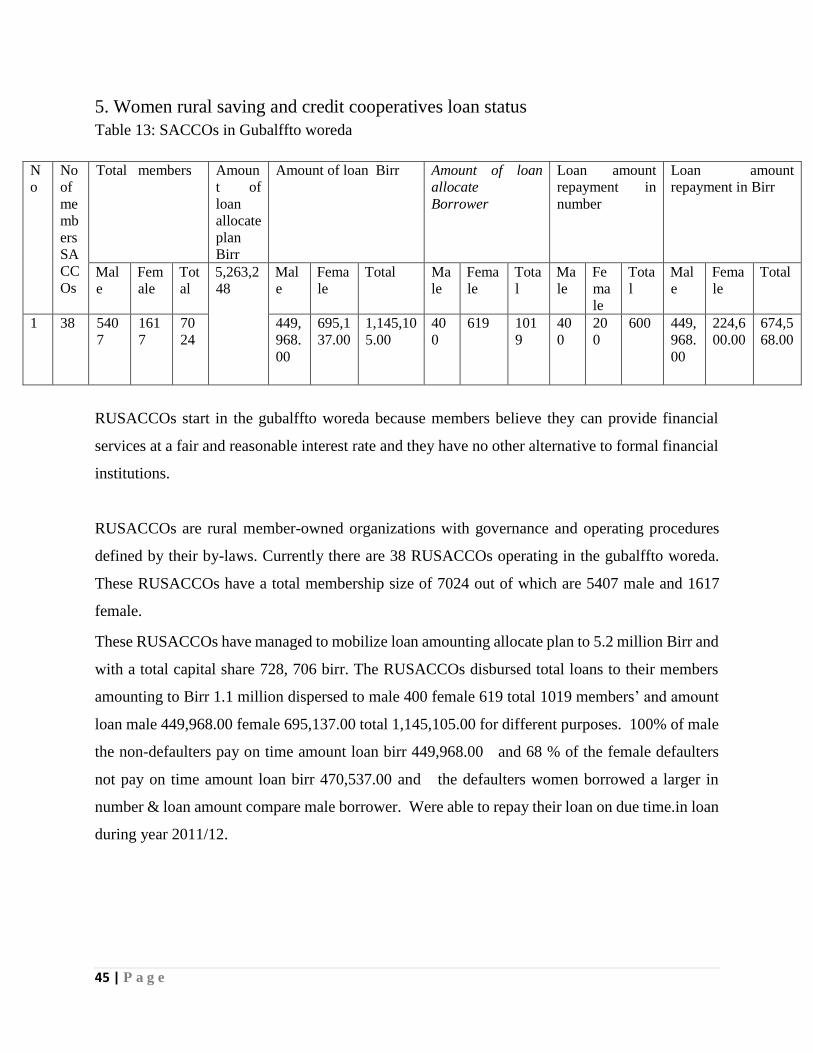

5. Women rural saving and credit cooperatives loan status .......................................................... 45

CHPTER FIVE ............................................................................................................................. 46

5. CONCLUSION AND RECOMMENDATION ........................................................................ 46

5.1. Conclusion ......................................................................................................................... 46

5.2. Recommendation .......................................................................................................... 47

6. REFERNCES .......................................................................................................................... 48

7. Appendixes ................................................................................................................................ 53

IV | P a g e

LIST OF TABLES

Table x Summary for independent variables, measurement scales and the hypothesized

Relationships ................................................................................................................................. 25

Table 1 Age structure of the borrowers by saving and credit cooperative.................................... 27

Table 2 Family size of the respondents by borrower group .......................................................... 28

Table 3 Education level of respondents by borrower ---------------------------------------------------29

Table 4: Amount of money spent to celebrate holidays ................................................................ 30

Table 5 Participation on saving & Loan amount --------------------------------------------------------31

Table 6: Borrowers’ responses on of agro ecologic differentials problems ................................. 32

Table 7 Loan diversion & others ................................................................................................... 33

Table 8: Borrowers’ responses on Timeliness of credit ................................................................ 35

Table 9 Average size of livestock (TLU/household) for sample respondents .............................. 36

Table 11: Contingency coefficient for discrete variables ............................................................. 38

Table 12 the logit model ............................................................................................................. 39

V | P a g e

ABSTRACT Saving & credit cooperative have vital contribution to the economic development and creation of

asset opportunity in developing countries with large number of rural area. The objective of his

study was to examine the main factors influencing loan repayment among rural women based on

multipurpose cooperatives’ members in Guba-Lafto Woreda. In the course of this study primary

data were collected from 115 respondents. 38 Saving & credit cooperative have Guba-Lafto

Woreda 3 multipurpose cooperative was selected stratified. In addition, secondary data were

collected from relevant organizations and relatable documents. Descriptive and Econometric

analytical techniques that was used in this study. Descriptive statistics including mean, standard

deviations, frequency, percentages, etc. econometric analysis binary logistic regression was used

in this study. Location of borrowers, Level of education of the household, Age of the household,

family size of the household, celebration of social ceremonies, amount of credit borrowed by the

household and loan amount were highly important in influencing loan repayment performance as

evidenced by the model result. Therefore, consideration of factors affecting loan repayment

performance because it provides information that would enable to undertake effective measures

with the goal of improving loan repayment performance and hence help achieve success in rural

women. It would also enable lenders such and policy makers to have knowledge as to where and

how to channel efforts in order to minimize loan defaults.

Key words: multipurpose, loan repayment, binary logit

1 | P a g e

CHAPTER ONE

1. INTRODUCTION 1.1 Background of the Study

Women represent 50% of the world population, and play a vital role in food production and food

security. The world’s experiences show that food security encompassed a broad range of issues.

All these issues are central to women. Agricultural development is a complex process and a

challenging one as well (Trinh T. and Ha T., 2009). Women account for 70% of agricultural

workers, 80% of food producers, and 100% of those who process basic foodstuffs and they

undertake from 60% to 90% of the marketing (Fresco, 1998). It is often stated that women are

responsible for more than half the world’s food production. They are said to be “feeding the world”.

The role women play in agriculture and the rural society is fundamental to agricultural and rural

development in sub-Saharan Africa.

In Ethiopia agriculture is the mainstay of the economy accounts for about 40 percent of national

GDP, 90 percent of exports, 85 percent of employment, and 90 percent of the poor (David J., 2008).

Women are the backbone of the agricultural sector and the food production system (MOPED and

UNICEF, 1994). The agricultural sector contributes to overall economic growth as well as

providing the poor with opportunities for socio-economic development activities. Agriculture

activities heavily relied on family labour and women played a key important role in farming and

improving the quality of life in rural areas (World Bank, 2004 cited in Berhan, 2010). Out of the

total subsistence agricultural production, they are responsible for about 50%. As some reports

indicate women contribute around 65% of the labour-force in agriculture (TGE and UNICEF,

1993).

Agricultural Cooperatives contribute to poverty reduction by providing economic opportunities

for their members; employment, livelihoods, wide variety of services, empower the disadvantaged

to defend their interests; provide security to the poor by allowing them to convert individual risks

into collective risks; and mediate member access to assets to earn a living (ATA, 2012).

2 | P a g e

Agricultural cooperatives in particular help farmers access the inputs required to cultivate crops

and keep livestock. In addition to making accessible agricultural inputs, they help process of

agricultural products, transport and market their produce. These services help pull members of

cooperatives out of poverty.

According to USAID (2005), in Ethiopia farm production is almost totally in the hands of small

farmers; private commercial farms are of negligible importance. The origin of cooperatives dates

from Hailesilassies‟ regime, but they became the dominant form of organizing farmers under state

control during the Derg regime. Proclamation No. 138/78 made membership in cooperatives

obligatory; cooperatives were used as a means of state control over the rural population and to

extract food and other farm products from farmers and channel them to urban consumers and the

elite at subsidized prices..

Projection population size unpublished document Amahar regional finance and economy biro

(2016), in Guballfto Woreda is estimated to be total population 154,323 male 79,490 /51.51%/

female 74,833/48.49%/lives rural areas. Mass of the rural women is involved in mixed farming.

Cereals are the predominant agriculture produce accounting for 36.59% of the total cultivated land

and 18% of the grain production (Gwrdao, 2016).

According to 2016 Gubalfftto Woreda cooperative promotion office’s loan upturn report, mainly

Gubalfftto Woreda cooperative promotion office, saving and credit cooperatives have been

engaged both directly and indirectly in providing loan to the farmers. For the last decade, a total

of 5,263,248birr has been disbursed for farmers but only 10% of it is collected back. Obviously,

the data shows as the loan repayment performance is so poor, this implies investigative repayment

is very vital agenda.

Thus, for securing high loan repayment rate it is vital to thoroughly investigate various aspects of

credit defaults and factors influencing loan repayment so that it can help financial institutions,

policy makers and other stake holders to have information on the issue and help them as a basis

for intervention moves. Therefore, this study will be undertaken to investigate how loan repayment

is going on among members of rural women based on saving and credit cooperatives in the rural

parts of Gubalffto Woreda cooperative office and evaluate its factors

3 | P a g e

1.2 Statement of the Problem

The agricultural cooperatives in Ethiopia are considered to be the most important organizations

that pay attention and try to support the rural development in general and the agricultural

development in special through the activities and services achieved for the sake of farmers.

Agricultural cooperatives in Ethiopia play a great role for the development of agricultural sector in

the country. However, agricultural cooperatives in Ethiopia have faced several challenges. Among

these problems, women repayment loan on time is the most challenging one.

In Guba-Lafto Woreda, there are multipurpose agricultural cooperatives. These cooperatives give

various functions for the members and the society as a whole. The cooperative provide agricultural

inputs such as fertilizer, seeds and chemicals, and distributes these inputs at reasonable price. In

addition to this, the cooperatives provide consumer goods with a reasonable price and also the

cooperatives purchase different agricultural products from the farmers at a competitive price and

the farmer’s gate profit from the cooperatives based on the amount of their supply.

Multi-purpose agricultural cooperatives provide different agricultural inputs through loan to its

members and others. However, cooperatives have faced serious problems of loan recovery. The

cooperatives get loan through unions and the union‟s access loan from Commercial Bank of

Ethiopia through the guarantee of the regional government.

Multi-purpose Agricultural cooperatives expected to support the agricultural sector for the

achievement of growth and transformations desired form this sector. But to contribute its part and

to give better service for the members and for the society as a whole, the cooperatives are expected

to improve their loan recovery performances.

The North Wollo Zone, the Regional Government and non-governmental organizations extend

loan facilities to narrow the gap between the required and the owned capital which help to use

improved agricultural technologies that would increase production and productivity.

However, there is a series loan repayment problem in the rural parts of Guba-Lafto Woreda. For

instance, according to North Wollo cooperative promotion accountable office official fourth

4 | P a g e

quarter report (2019) about 24 million birr loan was not repaid. Moreover, out of the total loan

finance distributed by different organizations for the last decade, almost 90% of has not been

returned. The review of literature has shown that there are theoretical and empirical gaps. The

direct link between the causes of poor loan repayment and the level of loan repayment performance

has not been shown. Therefore there is a need to close the gap and this is exactly what this study

aims at.

1.3 Research Questions

1. What are the status financial performances of multipurpose agricultural cooperative?

2. What are the main demographic socio-economic and institutional factors influencing loan

repayment of rural women in the study area?

3. What are strengths & weakness of multipurpose agricultural cooperatives compare to other

financial institutions?

1.4 Objectives of the Study

The general objective of his study was to examine the main factors influencing loan repayment

among rural women based on cooperatives’ multipurpose agricultural cooperatives members in

Guba-Lafto Woreda.

1.4.1 The specific objectives

To assess the financial performances of multipurpose agricultural cooperatives with

respect to loan provision and repayment

To identify the demographic, socio-economic and institutional factors influencing loan

repayment of rural women;

To examine the strength & weakness of rural multipurpose agricultural cooperatives with

respect to credit provision.

1.5 Scope and Limitations

The study is delimited to rural parts of Guba-Lafto woreda. It focused on performance of rural

women in loan repayment from saving and credit cooperatives’ and concentrated on evaluating the

socio-economic and institutional factors that were associated with loan repayment. The restrictions

5 | P a g e

of this study were mainly attributed to time, money, cross sectional data and trustworthiness of

interviewees’ data on their personal.

1.6 Significance of the Study

This study attempted to assess the factors affecting loan repayment among rural women in the

Guba-Lafto woreda. The result of this study will provides information that will enable effective

measures to be undertaken to increase loan repayment and for rural women credit packages to be

effective. It will also enable lenders such as non-governmental organizations and policy makers to

have information as to where and how to channel efforts in order to minimize loan defaults. The

study is also expected to contribute towards better credit management with possible pay-off in

improved loan repayment.

1.7. Organization of the Thesis

The remaining parts of the thesis are organized as follows. Chapter two presents review of literature

that includes definitions of concepts, the need for credit, overview of the financial system in

Ethiopia and empirical studies on loan repayment performance. Chapter three presents the research

methodologies employed in the study. Results obtained are presented and discussed in detail in

chapter four. Finally, chapter five presents’ policy implications of the research.

CHAPTER TWO

2. LITERATURE REVIEW 2.1 Definitions and Concepts

2.1.1The Definition of Savings and credit Cooperative

Savings and credit cooperative societies (SACCOs), sometimes referred to as financial

cooperatives, are an autonomous association of persons united voluntarily to meet their common

economic, social and cultural needs and aspirations through a jointly owned, democratically

6 | P a g e

controlled enterprise (International Cooperative Alliance, 1995; International Labour

Organization, 2002; Cheruiyot et al., 2012). Financial cooperatives are member-owned

cooperatives with the mandate to mobilizes savings and provide access to affordable credit to

members as a way to assist their socioeconomic well-being. In financial cooperatives, the members

are simultaneously owners and clients (ICA, 2013; USAID, 2005), and the cooperatives are formed

on common bonds, either community bonds or occupational/association bonds. The common

bonds are used as security because they ensure that members have a sense of identity, mutual

concern, cooperation, loyalty and trust

The theorist Lysander Spooner was stated that the historical initiation of Micro financing service

was traced back in the middle of 1800‟s. Consequently he wrote the impact of the credit schemes

on the target entrepreneurs and farmers while targeting the poor peoples to get out of the poverty.

Meanwhile, the modern industry of microfinance service has been initiated since 1970 by Grameen

Bank of Bangladish and pioneer Mohammed Yunus. Shore bank was the first microfinance and

community development bank founded 1974 in Chicago. According to Prof. Mohammed Yunus

and Grameen Banks phrases, an improvement in the economy and social welfare could partly

realized through delivering micro-credits to the poor people (Microfinance and Micro-credit,

2016).

The first credit and saving cooperatives were established in the mid - 19th century, mainly in

Germany. Two men are considered as the founding fathers of the credit cooperative movement:

Herman Schultz- Delitsche, who formation credit cooperative for minor artisans and the urban

middle classes, and Freidrich Reifeisen, the founder of the rural credit cooperative. In Italy, Luigi

Luzzatti established credit cooperatives which combined the principles well-known by his two

German predecessors. After the consumer cooperative, the credit cooperative is the most common

type of cooperative to be found in the modern world, including the Third World. This form of

cooperative has been established in both rural and urban areas by labor unions and other

organizations, including government bodies. Because of its very abundance, it provides an answer

to the most pressing need of large groups of people: the necessity of obtaining monetary credit for

various purposes (Gallo Z, 1989).

7 | P a g e

Hor Kimsay (2011) reported that microfinance institutions were established originally as a nonfor-

profit making financial schemes that had particularly serves the poor (low-income groups of the

society) at rural areas. As it was reported on this module, through time it was believed by some

peoples in Cambodia that serving those poor peoples as non-profit making institute has its own

impact on the financial sustainability of these MFIs to realize that the services would address a

wide range of poor peoples in the country. As a result MFIs in the Cambodia has reviewed their

credit scheme and tried to marginalize the services by commercializing their credit schemes at

lower interest rates than commercial banks. The reason for transforming the MFIs service into

commercial is to bring the transparency of the financial services, increasing the confidence of

donors and investors and to ensure that MFIs are financially sustainable to serve wide range of

poor societies which demands financial services.

Moreover, the author stated that the average loan sizes of MFIs were steadily increased from time

to time based on the repayment experience of borrowers. However through periods an increase in

number of clients served and average loan sizes experiences some defaulted loans over couple of

few years that leads the microfinance practitioners to review their implementation mechanisms

and needs of new credit assessment methodologies that emphasizes on the micro and small scale

Enterprises (MSE). The assessment was focused on the cash flow assessment of borrowers rather

than the collateral requirements which may fulfill the needs of MSE‟s. An increase in the average

loan size and change of loan approach to MSEs was the result of the increased capacity of lending

larger loan size by MFIs (Hor Kimsay, 2011).

Microfinance institutions in developing countries have a great contribution in reducing poverty. It

has been proved that microfinance service can be viewed as a developmental strategy implementer

that intended to empower poor women entrepreneurs, to initiate their businesses and providing

them awareness on how to manage their assets and its related risks (Abdulfettah,

8 | P a g e

2013). Furthermore, the availability of these micro-credits schemes and other financial schemes

increases the number of enabled young poor groups which have been organized in the form of

micro & small scale enterprises. This in turn will creates a great employment opportunities for the

poor young societies which have been lacked with financial sources at national level (Abdul Fattah,

2013).

A cooperative society is defined by the Cooperative Societies Act, (Birchall, J.2003) as an

association of persons who have voluntarily joined together for the purpose of achieving a common

need through the formation of a democratically controlled organization and who make equitable

contributions to the capital required for the formation of such an organization, and who accept the

risks and the benefits of the undertaking in which they actively participate.

In contrast, all microfinance institutions are intended to provide financial services in the absence

of any collateral values unlike the formal commercial banks by delivering various microfinance

schemes such as; micro credits, saving mobilization and provision of insurance schemes to the

poor. The major objectives of these microfinance services are to strengthening the economic bases

of the low-income generating activities of the poor peoples who are living in the rural and urban

areas of the country (Fikirte, 2011).

Repayment performance of borrowers can be affected due to various factors. An economic theory

suggests that a flexible repayment schedule set by the lending institutes can benefits borrowers and

potentially enhances their capacity of repaying their debts. On the contrary, MFIs practitioners

believed that high repayment recovery rate can be realized through maintaining the regular

repayment time schedules (Abdulfettah, 2013)

2.2. Loan Repayment Performance of borrowers

According to various researchers, microfinance institutions loan repayment performances can be

influenced by a number of factors identified as borrower’s characteristics and lender’s lending

characteristics. The lending approaches of microfinances can be classified as group-based

approach and individual-based approach. A common characteristic of group lending approach is

that the group obtains the loan under joint liability, where each member in a group is responsible

9 | P a g e

for repayment of loans of his or her peers. Screening of the viable loan applicants, monitoring the

individual borrower’s efforts and enforcing repayment of their peers‟ loan among the members

are listed as the major characteristics of group-based lending approaches (Zeller, 1996 as cited in

Abafita, 2003)

Individuals are supposed to select those whom they trust to form a group with; that is they are more

interested to form group with those whom can make regular repayments and have a good concern

about the possible loss they face in case of non-repayments (Abafita, 2003). In most of the cases,

in group-lending approaches the functions of screening, monitoring and enforcement of

repayments are mainly endorsed to the group members than the lending institutes (Abafita, 2003).

Furthermore, in addition to the above benefits from group-based lending approach, commitment

of the borrower to feel indebtedness to the obligation they entered into is an exemplified character

of borrowers for on-time loan repayment performances (Florence & Daniel, 2014).

2.3 SACCOs

SACCOs is an acronym for Savings and Credit Cooperative Societies. It is a cooperative which

encourages its members to save money and enables them the obtain loans they may need for

various purposes from their collected savings. This definition provides an indication of the two

main tasks of the cooperative.

The first task is to enable members to save their money on a regular basis, or according to their

needs. The member saves his/her money within the context of the cooperative. Knowing that

he/she will receive a suitable return for his effort, in the form of interest on his savings.

Accordingly, in order to encourage savings, it is wanted to pay members interest at a higher rate

than that obtainable at any other type of financial institution. The member will then realize that it

is choice to save with his/her own cooperative. Cooperatives in many countries make the mistake

of paying interest on their members' savings at a lower rate than that accessible elsewhere (Aredo,

D. 2013).

The second task of the cooperative is to grant loans to its members. Loans are arranged from the

members' accumulated savings. Obviously, not all the members can take out loans, or obtain them

10 | P a g e

immediately or simultaneously. Members are granted loans in accordance with their seniority

within the cooperative and the amount of their savings. Generally speaking, the size of loans

granted from the cooperative's fund is governed by the liquidity regulations of the country in which

it is located. Clearly therefore, the size of loans granted to members does not exceed the total of

their savings. But there are some exceptional cases where the cooperative serves as an intermediary

for obtaining additional credit for a member. This subject will be discussed more extensively later.

The member pays the (cooperative) fund interest on the credit his/her receives. The rate of interest

will be lower than that at other, commercial financial institutions, for this is part of the service the

cooperative provides to its members.

2.4. History of Savings and Credit Cooperatives in Ethiopia

Cooperation is the way of life of Ethiopians and has a long year of experience as a tradition. This

Cooperation may be facilitated by cultural or religious organizations that make the population

bring together. For example, Iddir /focuses on funeral celebration/, Ikuib /which helps for saving

money and self-help to the members/, and Debo / which is focused on the cooperation on labor

peak times like in the time of harvest, wedding , etc./.

Modern cooperative in Ethiopia was started at the time of Emperor Haile-selasie first in 1961 by

Decree number 44/1961 and later on a proclamation were enacted on 1966. With all shortcomings,

this legal ground gave inputs for co-operative development in the country. During the Dergeue

regime, tremendous efforts were exerted to organize different types of co-operatives in line with

proclamation No.138/1983. During this time, co-operatives were mainly organized to transform

rural economy to the socialist style rather than benefiting their members. In this process,

internationally accepted co-operative principles were violated which consequently led to the

dissolution of co-operatives and devastation of their properties during the transition period.

(Dagnew Gessesse, 2004)

However, the recent enactment of co-operative society proclamation No.85/94 and

No.147/98Created fertile ground for restructuring the previous co-operatives and organizing new

ones, in line with the new market oriented economic policy of the government, EPRDF .

Savings and credit cooperatives in Ethiopia have no very long origin. The first savings and credit

cooperative in Ethiopia was established in 1964 by employees of Ethiopian Airlines and the

initiative of interested individual Ethiopians who have foreign countries exposure and peace-core

11 | P a g e

workers of foreign citizens. During the same period, savings and credit cooperatives were

established by employees of Ethiopian Road Authority and the Telecommunication Agency

(Dejene, 1993).

Until the year 2001, there was no a saving and credit cooperative society in rural Ethiopia. The

first rural savings and credit cooperative society in Ethiopia is Hidu primary savings and credit

cooperative society. It is found in Oromiya Regional State, East Shewa Zone, and ‘Errer’ Woreda

at ‘Hidu’ farmers association (Kebele).

2.4.1 RUSACCOs in the Amhara Region

RUSACCOs are rural member-owned organizations with governance and operating procedures

defined by their by-laws. Currently there are 3,050 RUSACCOs operating in the region. These

RUSACCOs have a membership size of 598,454 out of which are 388,861 male and female.

209,593.

The general assembly, the management and board of directors are in charge of day-to-day

activities. Some RUSACCOs have employed staff and are managed by a management committee.

Other committees are the control committee, loan, saving, education and dispute committees. Low

skills and weak incentives for committee members limit sound management and growth.

2.5. Organization and Management of SACCOs

The organizational structure of a typical primary saving and credit cooperative society in Ethiopia

is shown in Figure 1. The organization and management of SACCOs essentially follow the

cooperatives principles.

The ‘democratic member control’ principle of cooperatives allows for all management functions

to be delegated to an elected management committees and to hired nature; (ii) regional cooperative

societies found in two or more regions; and (iii) the union cooperative Societies organized by the

union of different cooperative societies (Proclamation No. 274/2002).

Management while the source of power remains with the members of the cooperative. SACCOs’

day-to-day management rests with different committees. These are: Management Committee,

12 | P a g e

Control Committee, Loan Committee, Saving Committee Training and Education Committee

Arbitration or dispute resolution committee.

2.6. Empirical Studies on Loan Repayment Performance

Loan repayment show is affected by a number of socio-economic and institutional factors. While

some of the factors positively influence the loan repayment, the other factors are negatively

affecting the repayment rate. Regarding to the loan repayment performance of borrowers several

Studies have been conducted in many countries by different authors. Some of the studies are

summarized below.

2.6.1. Empirical studies in Ethiopia

A recent study by Fikirte (2011), Samuel (2011) indicated that age, education, income, loan

supervision, suitability of repayment period, availability of other credit sources and livestock

holding are important and significant factors that enhance the loan repayment performance of

borrowers, while loan diversion, celebration of social ceremonies, household size and loan size are

found to significantly increase loan default. The study also revealed that being female and business

experiences of the borrower were found to be significant in enhancing loan repayment performance

of borrowers.

A study conducted by Diribsa (2010) on determinants of members’ loan repayment in Ambo

Farmers ‘Cooperative union revealed that educational level, livestock ownership , interest rate,

distance of market ,experience with credit use, sources of income, land ownership and sex of

member were important factors influencing loan repayment in cooperatives.

Abebe (2011) examined determinants of credit repayment and fertilizer use by members of

cooperatives in Ada district, Oromia Region, Ethiopia. Tobit model was employed to identify

factors influencing loan repayment performance of the households. The result of the model showed

that family size, livestock ownership, on-farm income, non-farm income and saving habit were the

statistically significant factors influencing timely loan repayment performance positively

Brehanu and Fufa (2008) employed probit and logit regression to study the determinants of loan

repayment rates for agricultural loans among small-scale farmers in Ethiopia. In the study, they

13 | P a g e

found that borrowers with larger farms, higher numbers of livestock and farms located in a rainfall

area had a higher capacity to repay loans, since all those factors increased the farmers’ productivity

and income. The study also found that borrowers who had extra business income and were

experienced in using agricultural technology had a good repayment performance.

Million et al. (2012) studied factors affecting loan repayment performance of smallholder farmers

in east Hararghe zone, Oromia, Ethiopia using a tobit model. The result of the model showed that

agro- ecological zone, off-farm activity, production loss, informal credit, celebration of social

ceremonies, number of contact days of the farm household head with extension agents and loan

income ratio, determined repayment performance.

Brehanu and Fufa (2008) employed probit and logit regression to study the determinants of loan

repayment rates for agricultural loans among small-scale farmers in Ethiopia. In the study, they

found that borrowers with larger farms, higher numbers of livestock and farms located in a rainfall

area had a higher capacity to repay loans, since all those factors increased the farmers’ productivity

and income. The study also found that borrowers who had extra business income and were

experienced in using agricultural technology had a good repayment performance.

Bekeleet al. (2005) studied the socio-economic factors influencing repayment of agricultural input

loan in Ethiopia using a logit model. The result of the model showed that total livestock holding,

the amount of loan taken by households, off farm income by member of the household, yield loss,

grain production and timeliness of input supply, were became significant variables

As study founded by (Degu Addis, 2007) indicated that socio economic variables such as age,

family size, resource ownership and expenditure pattern affects the decision of household savings

significantly.

Studies done so far as mentioned earlier concentrated more on a rural women Savings and Credit

Cooperative loan repayment. This study therefore tries to narrow the research gap paying particular

attention to factors influencing loan repayment rural women saving and credit cooperatives loan

that lead members to be defaulters.

14 | P a g e

2.7 Conceptual Framework

The conceptual framework in diagram 1 shows the relationships between the independent and

dependent variables. The researcher conceptualizes the given independent variables that influence

loan repayment of the rural women in saving and credit cooperatives in diagram 1 as below.

Diagram1: Conceptual framework of factors affecting loan repayment rural women

Economic factors

Livestock

price

Returns from

actions

financed by

the loan

Returns

from other

sources

Participation

on voluntary

Loan

amount

Dependent variable

Loan repayment

SACCOs

Institutional

factors

Loan control

Appropriaten

ess of

repayment

Demographic & cultural

factors

Age

Marital status

Education level

Celebrate on social holidays

Family size

15 | P a g e

CHAPTER THREE

3. RESEARCH METHDOLOGY 3.1 Description of the study area

3.1.1 Location and Area Description

The studies were undertaken in Gubalaffto worda which is one of the 14 woreda’s of North Wollo

administrative zone in Amhara National Regional State (ANRS). The woreda covers a total area

of 931.0km2and located at the distance of 120 km from Dessie and 2km from the capital city

Woldiya.

According to 2016 projection population of Amahra region finance and economic office, the

population of the Woreda is estimated to 154,323 are living in rural kebels & the remaining 9,114

are urban dwellers. Among the rural dwellers, 79,490(51.51%) are males and74, 833 (48.49%)

females. The altitude of the Woreda ranges from 1325 to 882masl. The Woreda is divided in to

three agro ecological zones namely, Kolla (lowland) accounting about 17%, WoynaDega

(midland) accounting for 46% and the remaining 37% is Dega (highland) (Gubalafeto Agriculture

and Rural Development office 2016report).

Topographic conditions vary between flat (20%), rugged (35%), valley (15%) and hilly (3%)

conditions. The Woreda receives a bi-modal type of rainfall that occurs in the periods from

February to May (known as ‘belg’ or short rainy season) & from July to end of November (known

as ‘Meher’ or the main/ long rainy season).The average rainfall of the woreda (20062008) ranges

from 650-1000mm (HWAO 2010). Consequently, out of the 38 rural kebeles 12kebeles both meher

and belg producing areas whereas the remaining 26are meher producingkebeles. Both seasons are,

characterized by a variability of rainfall in amount and distribution, which in turn critically affect

the planting and production of most agronomic crops.

3.1.2Farming system

Farming system in the study area is mixed largely depends on rain fed subsistence agriculture,

mainly on cultivation of field crops, of which cereals mainly take the dominant ratio. The major

crops cultivated are teff and sorghum, but crops such as barley, maize, peas, and wheat are also

grown. Furthermore, farmers having irrigable lands also cultivate horticultural crops such as onion,

cabbage, tomatoes & coffee as well as sugarcane and orange. (Nwgwrdao, 2016)

16 | P a g e

Field crops are primarily produced for home consumption, while horticultural crops are cultivated

as cash crops. In addition to crop production, farmers are also involved in livestock production

consisting of mainly cattle and small ruminants. Cattle production is not as wide spread as small

ruminant production because of inadequate grazing lands. Apart from crop and livestock, wage

labor, firewood and charcoal sale are the source of incomes for the rural women. Migratory labor

opportunities are also available mainly out of the woreda and extended to other main towns and

Arab countries. Engagement in various types of trading activities is an important supplementary

occupation for many households of the study area which include marketing different kinds of

agricultural (grain and animals) and consumer goods; handicrafts of several types (Nwgwrdao,

2016)

3.1.3 Farmer’s cooperatives

North Wollo zone administration’s cooperative promotion accountable office 2008 annual report,

there are 18 kinds of cooperatives, members of farmers’ and 127,291,571.91 capital cooperatives

in rural and urban cooperatives. Gubalaffeto cooperative promotion accountable office 2016.There

are 5kindsof cooperatives, members of farmers’ and capital cooperatives. Those cooperatives

are engaged in different kinds of streams Table 1. Kinds and numbers of cooperatives Gubalaffeto

woreda

No.

kind of the cooperative

Number number of its members Capital

male Female Total

1 Saving and credit cooperative 38 5407

1617

7024

728,706.61

Source, Nwzgwcop, 2019 annual report

The sampling design According to the data obtained from Gubalaffto Woreda cooperative promotion bureau there are

38 registered primary saving and credit cooperatives .From those38 primary saving and credit

cooperative are in rural. This study is about rural saving and credit cooperatives.

17 | P a g e

3.2 Sample size determination

A simple random sampling procedure was adopted for the selection of the sample households who

are the member of RUSACCOs in the woreda. The sample size for the study is determined by a

simplified formula suggested by Yemane (1967).Sampling of error 0.09 Because of time, resources

and accessibility limitation to address all cooperatives.

The Yamane formula for determining the sample size is given by:

n = N / (1 + Ne^2)

Where

n= corrected sample size,

N = population size, and

e = sampling of error 0.09.

Accordingly, the sample size or number of respondent needed for the study is calculated as follow,

n = N / (1 + Ne^2)

n=1617/ (1 + 1617(0.09)2

n= 114.699560

n= 115

3.3 Sampling technique

In the 2019 fiscal year report there were 38 saving and credit cooperatives in the Gubalaffto woreda

from 38 RUSACCOs found in the Gubalaffto woreda from the total RUSACCOs found in the

district, 3 were selected randomly. Out of 1, 617 total member’s households of RUSACCOS 115

sample members of households were selected randomly using probability proportional to size

sampling technique. Concurrently, 25 committee members, from the sampled RUSACCOs, were

18 | P a g e

selected for focus group discussion (FGD) and 5 professionals from Woreda cooperative office

were selected as key informants (KI).

Table: 1 Sample primary cooperatives of sampling members: Woreda Cooperative Promotion

Office

No RUSACCOS Total Members of

RUSACCOS Sample size

1 Saknqa 650 47

2 Beqalo maneqia 402 29

3 Doro geber 565 39

Total 1617 115

3.4 Methods of data collection

For this study both primary and secondary data sources were used. Primary data were collected

from the sample SACCO women members using questionnaire. Personal observations focus group

discussion and key informant interview were the primary data collection methods. Secondary data

were gathered from SACCO reports and records of DAs, woreda cooperatives report, audit report

RUSACCO. To collect the data in the proper manner enumerators who are responsible and familiar

to the culture of the area will be assigned for each Sacco and training will be given. The training

will focus on how to approach and ask the respondents and how to collect data using the

questionnaire. The researcher was visit each enumerator every day and crosschecking has been

made when there is mistrust of any error.

3.5 Methods of Data Analysis

In the literature review part, several descriptive and econometric models that have been used to

analyze factors influencing of loan repayment. This section presents descriptive and Econometric

analytical techniques that were used in this study.

19 | P a g e

3.6 Descriptive statistics

A descriptive analysis was employed to examine socio economic and institutional characteristics’

of the respondents. Under this method of data analysis, descriptive statistics including mean,

standard deviations, frequency, percentages, etc. were used to summarize and describe the socio-

economic characteristics of the respondents .These are inferential t-test and chi-square tests were

used to compare the defaulters and does not defaulters in terms of different explanatory variables.

3.7 Econometric model

Loan repayment is a dependent variable, while different socio-economic and lender related factors

are considered as independent variables. In this study, the dependent variable assumes

Values 0 and 1, which is 1 if the debtor is a defaulter and 0 if the debtors does not defaulter.

Therefore, loan repayment is treated as dichotomous dependent variable. Loan repayment is,

therefore, a non-continuous dependent variable that does not satisfy the key assumptions in the

linear regression analysis.

To examine the factors affecting the loan repayment, discrete choice model should be used. Thus,

the most widely used and appropriate qualitative response models are the logit and probit models

(Verbeek, 2008).

According to Gujarati (1995), the logit model follows the maximum likelihood estimation

technique, and assumes that the random variable follows the normal cumulative density function.

It means that the likelihood of an event to occur happens when the utility exceeds certain critical

thresh hold level.

Logit and probit models are used for binary response variables. These models have some

advantages over the linear probability model: fitted probabilities are between zero and one and the

partial effects diminish (Wooldridge, 2000).

Linear Probability Model (LPM) is plagued by several problems such as non-normality and

heteroscedasticity of the error term, possibility of the dependent variable lying outside the 01range

most importantly it assumes that the mean value of the dependent variable is linearly related with

the explanatory variable, that is the marginal effect of the explanatory variable is remaining

constant throughout, which seems patently unrealistic (Gujarati, 1995).

20 | P a g e

3.7.1 Specification of the Logit Model

According to Maddala (2001), the usual logit model can be used without any change even with

unequal sampling rates. Logit is the natural logarithm. By taking the aforementioned justifications,

logistic model is selected for this study. Econometrically the Cumulative logistic probability is

here by shortly specified.

The specification of the Logit model is;

Pi = F (Zi) =F (α+Σ β iXi) = 1/ 1+ e-zi……………………………1

Where, Pi is the probability that an individual will make a certain choice (default or does not

Default) given Xi e denotes the base of natural logarithms, which is approximately equal to

2.0718;

Xi represents the ith explanatory variables; and α

and βi are parameters to be estimated

Hosmer and Lemeshew (1989) pointed out that the logistic model could be written in terms of

the odds and log of odds, which enables one to understand the interpretation of the coefficients.

The odds ratio implies the ratio of the probability (Pi) that an individual would choose an

alternative to the probability (1-Pi) that he/she would not choose it.

(1-Pi) = 1 / 1+ezi ……………………………………………………….. (2)

Therefore,

(Pi) = 1+e-zi = e zi …………………………………………………….. (3)

(1-Pi) 1+ezi

Or,

(Pi) = (1+e-zi) = e (α+Σ β iXi) ………………………………..………… (4)

21 | P a g e

(1-Pi) (1+ezi)

Taking the natural logarithm of the equation (4)

Zi= Ln (Pi) = α+β1X1+ β2X2+…+ β

MXm…………………………………………………….. (5)

If the disturbance term (Ui) is taking into account, the logit model becomes

Zi= α +Σm β iXi +ui…………………………….…………………………………….. (6)

3.8 Hypothesis and Definition of Variables

Explanatory variables for this study are selected and hypothesis of this study is recognized based

on the literature reviewed, discussion held with stakeholders, and the researcher’s Knowledge on

the study area. Definition and brief explanation of the explanatory variable selected for this study

and their Likely factors influences on loan repayment are presented below.

The dependent variable of the logit model: The dependent variable of the model is loan

repayment. It is a dummy variable which has a value of 0 if the debtor repays all amount of loan

it took from the specific saving and credit cooperative on the loan pay on time and 1 if failed to

do so.

The independent variables of the model: The independent variables of the model are those which

are hypothesized to have an association with loan repayment show? The potential explanatory

variables which will hypothesize to factors influencing loan repayment show of rural women are

explained below.

Age /AGhh/: It is a continuous variable measured by total number of years from the respondent’s

birth until the examination conducted. The household’s age is hypothesized to have positive

association with farmers’ loan repayment show. As the age progress, farmers ‘experience,

knowledge, stability and honesty which in go might assistance them to collect wealth over time

which would enable debtors to repay their debt in time than young borrowers. Fikirte (2011) noted

that with increase in age, it is usually expected that borrowers get more stability and experience on

their business.

22 | P a g e

Family size (FA-SIZ): Refers to the number of people under the similar roof. The larger the

household members, the more the labor force available for production determination. Therefore,

there is a possibility to have more alternative sources of income to overcome credit risk. Based on

this, families with adequate labor-force would be expected to low probability of defaulting. On the

other hand, large family size may imply self-insufficiency in terms of food consumption because

large family consumes more than do small households. This is usually true if the dependency ratio

of the household is large. Therefore, the effect of family size, on formal loan repayment capacity

may be unknown a prior. Besides, because large family size implies more consumption

expenditure that will be not on time for loan repayment. In this case, we expect a negative sign for

the variable (Abraham, 2006; Samuel, 2011).

Marital status /MATS/: It is represented by 0 if the respondent is married while she took her last

loan and 1 if she is single. It is assumed that married households are more established and

responsible for social values than the rest of the groups. In addition married persons believe that

the value of their occupational show is highly consequential as far as making a good family is

concerned. As study (Marziehet al., 2013) stated that married households are more economically

developed than single households. Therefore, married cooperative members expected to have a

positive effect on the magnitude of savings.

Education level /EDULE/: This is a categorical than example Uneducated, below high school ,

Certificate, and College variable measured by level of formal education accomplishment. It is

assumed that educated debtors may acquire better awareness in choosing a money-making

business, could have better market information, and exposure to technologies. Thus, it is

predictable that it will have a positive influence on loan repayment. A more educated client is

expected to use the loan effectively as compared to a less educated one. In line with this, educated

borrowers may develop the entrepreneurial skill and they may engage in a new business (Pasha

and Tolosa, 2014).

Celebrate on social holiday’s /CSCOH/: This is a continuous variable measured by the total

amount of money spent (in Birr) for celebrating different types of social holidays like wedding.

This variable is hypothesized to have a negative influence on loan repayment as it is nonproductive

23 | P a g e

expense. . Performance. Besides, because more consumption expenditure hence may erode the

fund that will be available for loan repayment. In this case, we expect a negative sign for the

variable (Abraham, 2006; Samuel, 2011).

Participation on voluntary saving /PVSA/: A type of saving produces applied by saving and

credit cooperatives in which members are invited to save money voluntarily, and allowed to

withdraw it freely upon their request. It is a dummy variable which is represented by 1 if the

respondent has voluntary saving and 0 otherwise. Those members who are involved in such

activities can easily pay their loan back from what they saved. Therefore, it is hypothesized that

this variable positively influences loan repayment.

Loan amount /LOANT/: This is because the borrowers have enough funds to finance their

business that makes them get more profit and increase their business profile (Nawai and Shariff,

2012; Pasha and Tolosa, 2014).It is a continuous variable measured by the total amount of money

(in Birr) accessed as a loan from the cooperative. An efficient amount of loan which equals with

the arranged business plan can create favorable situation for the debtor to use it appropriately and

repay it back. But, if the disbursed loan size is below or above the required, it will lead to diversion

of the resource to other activities or mishandling respectively. Thus, this variable may have

positive and negative indication.

Agro ecologic differentials /AGEO/:The area is divided into two which are dega and Woynadega

areas, which are represented by 0 and 1 respectively. As the life of farmers is highly connected to

nature and most of the farmers are engaged in agriculture correlated activities the amount of rainfall

will meaningfully influence their activities. Thus, those debtors from areas with relatively better

rainfall are expected to have a better loan repayment show. Amare (2005) found that being a

residence of adequate rainfall area will increase the probability of not becoming a non-defaulter.

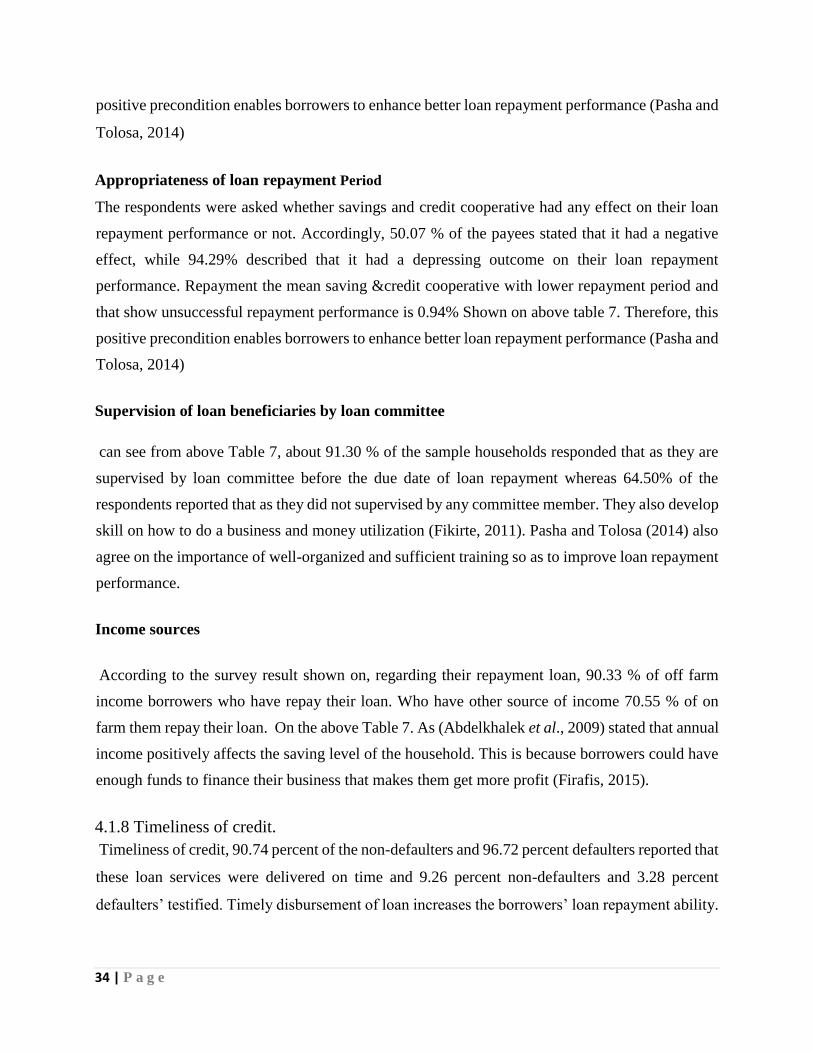

Appropriateness of repayment time/ APPRTI/: It is a dummy variable which takes 1 if the loan

repayment dated is appropriate and 0 if not. It is expected that suitable repayment dated could help

debtors benefit from the loan investment properly, gain income and pay the loan back on time.

This variable is hypothesized to have a positive influence on loan repayment. Timely disbursement

of loan increases the borrowers’ loan repayment ability. Therefore, this positive precondition

enables borrowers to enhance better loan repayment performance (Pasha and Tolosa, 2014)

24 | P a g e

Loan supervision/LOSU/If there is a continuous follow up and supervision visit to evaluate the

loan utilization and repayment, this makes borrowers to observe their obligation and improve the

proper use of the loan thereby improving repayment performance. Therefore, we expect a positive

relationship. If the lender provides training facilities, the clients will be able to understand the rule

and regulations easily. They also develop skill on how to do a business and money utilization

(Fikirte, 2011). Pasha and Tolosa (2014) also agree on the importance of well-organized and

sufficient training so as to improve loan repayment performance.

Income from on farming activities /INCONFAA/: In addition, if the business plan of the creditor

is profitable, it will contribute to timely repayment of the loan. Hence, this variable is expected to

have a positive sign. Total annual income earned from sale of agricultural products, petty trade,

off-farm activities, and livestock products by improving its productivity to secure the members’

basic needs and gradually to change the household members’ life style. As (Abdelkhalek et al.,

2009) stated that annual income positively affects the saving level of the household.

Income from off farming activities /INCOFFRAA/: It includes any income gained from

activities or sources other than the provided loan. Such sources of income are hypothesized to have

positive impact on loan repayment show. It is a dummy variable which is represented by 0 if the

respondent has other sources of income and 1 otherwise. It is believed that respondents’ additional

source of income could influence loan repayment performance of clients. This is because

borrowers could have enough funds to finance their business that makes them get more profit

(Firafis, 2015).

Timeliness of loan issue /TMILOIS/: Timely disbursement of loan increases the borrowers’ loan

repayment ability. Therefore, this positive precondition enables borrowers to enhance better loan

repayment performance (Pasha and Tolosa, 2014).It is a dummy variable which takes 0 if the loan

is distributed on the right time which is demand by the debtor and 1 if not. It is predictable that

those loans which are distributed on the right time will make the creditors gain revenue from their

business which in turn leads them to pay their credit on time.

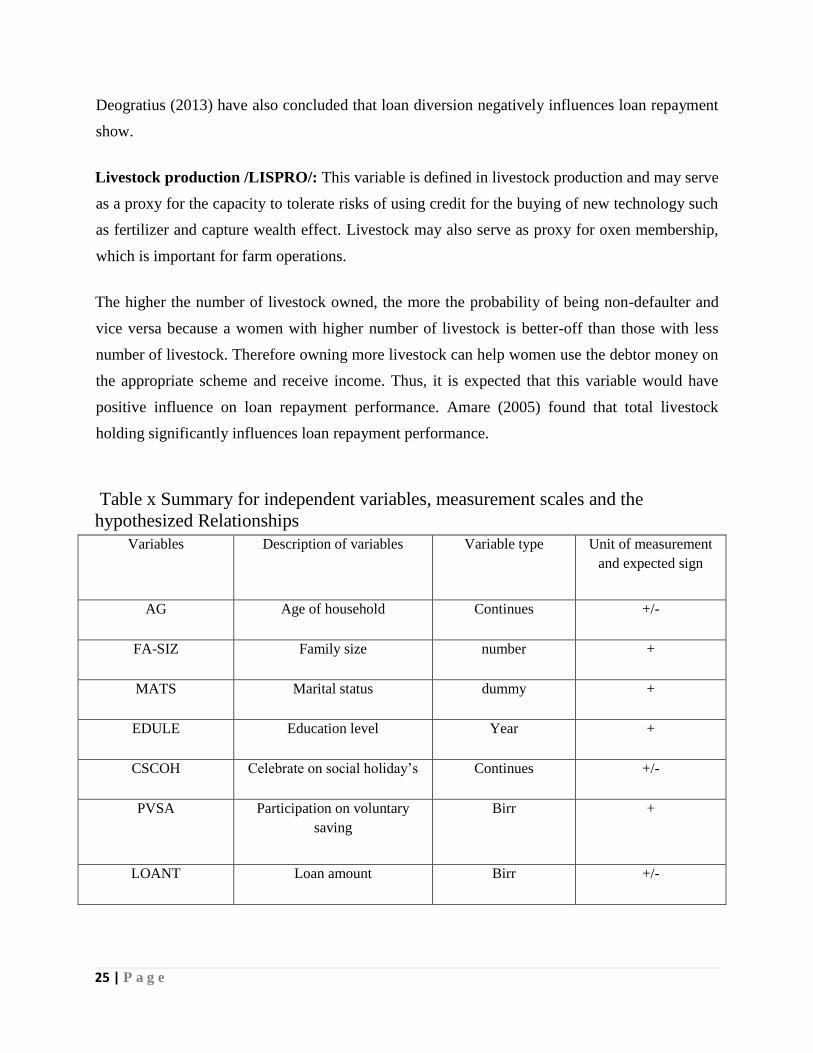

Loan diversion /LONDIV/: Sometimes debtors may distract the loan from the proposed business

and use it for consumption. This type of act may lead debtors to be defaulters. It takes the value of

0 if the loan is not distracted to consumption purpose and 1otherwise.In addition, Gerald and

25 | P a g e

Deogratius (2013) have also concluded that loan diversion negatively influences loan repayment

show.

Livestock production /LISPRO/: This variable is defined in livestock production and may serve

as a proxy for the capacity to tolerate risks of using credit for the buying of new technology such

as fertilizer and capture wealth effect. Livestock may also serve as proxy for oxen membership,

which is important for farm operations.

The higher the number of livestock owned, the more the probability of being non-defaulter and

vice versa because a women with higher number of livestock is better-off than those with less

number of livestock. Therefore owning more livestock can help women use the debtor money on

the appropriate scheme and receive income. Thus, it is expected that this variable would have

positive influence on loan repayment performance. Amare (2005) found that total livestock

holding significantly influences loan repayment performance.

Table x Summary for independent variables, measurement scales and the

hypothesized Relationships

Variables Description of variables Variable type Unit of measurement

and expected sign

AG Age of household Continues +/-

FA-SIZ Family size number +

MATS Marital status dummy +

EDULE Education level Year +

CSCOH Celebrate on social holiday’s Continues +/-

PVSA Participation on voluntary

saving

Birr +

LOANT Loan amount Birr +/-

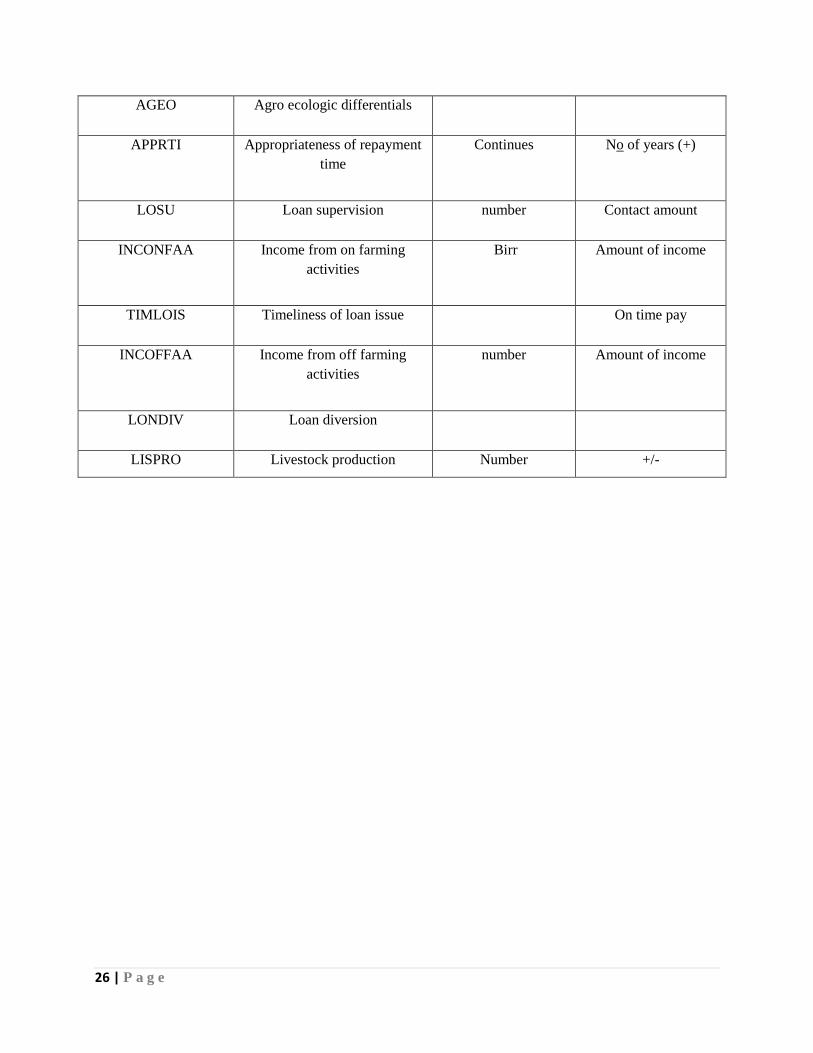

26 | P a g e

AGEO Agro ecologic differentials

APPRTI Appropriateness of repayment

time

Continues No of years (+)

LOSU Loan supervision number Contact amount

INCONFAA Income from on farming

activities

Birr Amount of income

TIMLOIS Timeliness of loan issue On time pay

INCOFFAA Income from off farming

activities

number Amount of income

LONDIV Loan diversion

LISPRO Livestock production Number +/-

27 | P a g e

CHAPTER FOUR

4. RESULTS AND DISCUSSION This chapter presents the outcomes from the descriptive and econometric analyses. The descriptive

analysis made use of tools such as mean, percentage, standard deviation and frequency distribution.

In addition were working to compare defaulters and non-defaulters group with respect to some

explanatory variables. Econometric analysis was carried out to identify the most important factors

that affect the loan repayment show and to measure the relative importance of significant

explanatory variables on loan repayment.

4.1. Demographic and Socio-economic Characteristics

4.1.1 Age of the borrowers

Table 1 Age structure of the borrowers by saving and credit cooperative

Age

Non-defaulter Defaulter Total

No % No % No %

18-35 29 53.70 39 63.93 68 59.13

36-45 12 22.22 12 19.67 24 20.87

>45 13 24.08 10 16.40 23 20.00

Source: Survey results 2020

**Significant at 0.05 per cent significance level

In the above table 1, interviewed households 39 (63.93%) were defaulters, and 29(53.70%) were

non-defaulters was found to be statistically significant, according to Fikirte (2011) noted that with

increase in age, it is usually expected that borrowers get more stability and experience on their

business.

28 | P a g e

4.1.2 Family structure

The family size of the non-defaulters &defaulters was 40.74% and 45.90%respectively, with that

was found to be statistically significant (Table 2). The average family size of non-defaulters was

5.96, while that of defaulters was 6.33with significant difference between means.

Table 2 Family size of the respondents by borrower group

Family size Non-defaulters Defaulters Total

1- 5 19 35.19 23 37.70 44 38.26

6 - 8 22 40.74 8 13.10 27 23.48

7 - 8 7 12.96 28 45.90 35 30.43

> 8 7 12.96 2 3.30 9 7.83

Total 54 61

115

Mean 5.95 6.33 6.1

Source: Survey results 2020

4.1.3 Educational status

Respondents in terms of literacy level has shown that 53. 04% were illiterate, 36.52% could read

and write, 10.43% had attended formal education. This study it was found that there exists

significant difference between defaulter & non-defaulter in relation to education level, at 0.05%

level of significance. A more educated client is expected to use the loan effectively as compared

to a less educated one. In line with this, educated borrowers may develop the entrepreneurial skill

and they may engage in a new business (Pasha and Tolosa, 2014).

N % N % N %

29 | P a g e

Table 3 Education level of respondents by borrower

Illiterate 28 51.85 33 54.10 61 53. 04

Read and write 22 40.74 20 32.79 42 36.52

Above high school 4 7.41 8 13.11 12 10.43

College 0 0 0 0 0 0

Mean 0.81 1.12 1.00

Source: Computed from survey data 2020

**, significant at 5 per cent significance level, respectively

4.1.4 Celebrate on social holidays

Social ceremonies such as different holidays, wedding, Religion day and funeral of family

members remained celebrated in the study area. According the study outcome, 81 respondents

(70.43percent) have informed that they was celebrated one or more of these irregular ceremonies

and 34 respondents (29.53 per cent) stated that they had not celebrated any ceremonies. These

social ceremonies have their own negative impact on the loan repayment performance of

Borrowers and force the household to use the borrowed money for consumption. However, there

is statistically significant difference between non-defaulter and Defaulter regarding the number of

members celebrate social ceremony. Besides, because more consumption expenditure hence may

erode the fund that will be available for loan repayment. In this case, we expect a negative sign for

the variable (Abraham, 2006; Samuel, 2011).

Educational level N % N % N %

Non - Defaulter Defaulter Total sample

30 | P a g e

Table 4: Amount of money spent to celebrate holidays

Description Non-defaulter Defaulter Total

No % No % No %

Not celebrated 19 35.19 15 24.59 34 29.57

Yes celebrated 35 64.81 46 75.41 81 70.43

Mean of Expenditure 425.75 930.27 481.03

Maximum 4000 8691 8691

Minimum 0 0 0

Standard deviation 604.85 1536.56 1190.38

Source: Computed from survey data 2020

31 | P a g e

4.1.1.5 Participation on saving & Loan amount

Table 5 Participation on saving & Loan amount

Variable Number % of borrowers Loan repayment

Mean Stan.Dev

Participation on saving

voluntary saving 34

64.67 .6466667 .4803845

Otherwise 81 80.04 .800411 .3145386

Loan amount

Adequate

34 50.14 .5014286 .5039526

Inadequate 81 90.06 .9005556 .2559923

Source: Survey results 2020

The Participation on saving had any effect on their loan repayment saving or otherwise.

Accordingly, 64.67% of the voluntary saving that it had a positive effect, while 80.04% reported

that it had a depressing effect on their loan repayment act. Representative differences between the

two was not statistically significant (Table 5)

The survey results disclose that 50.14% of the borrowers stated that the loan was adequate while

90.06 % described that the Inadequate. More specifically, defaulters informed that the loan they

established Inadequate (Table 5) .Timely disbursement of loan increases the borrowers’ loan

repayment ability. Therefore, this positive precondition enables borrowers to enhance better loan

repayment performance (Pasha and Tolosa, 2014)

4.1.6 Agro ecologic differentials

Natural disasters such as drought, pest and diseases infestation of crops and animals reduce farm

income of the household by affecting the productivity crops as well as animals. Hence natural

calamities have a negative impact on loan repayment of farmers. According the survey result out

32 | P a g e

of the total 115 respondent’s only 40.87, 35.65% &23.48% kola, Dega and woyena Dega

respectively told as they had faced with different natural disaster especially with flood problem

and loss of animals due to disease infestation respectively. But 40.87 % kola respondents reported

as they didn’t face any natural calamity. The Chi-square value, revealing differences between the

three groups agro ecology, was no significant at0.005% significant level (Table 6). Amare (2005)

found that being a residence of adequate rainfall area will increase the probability of not becoming

a non-defaulter.

Table 6: Borrowers’ responses on of agro ecologic differentials problems

Problem of natural

disaster

Non-defaulters Defaulters Total

Number Percent Number Percent

Number Percent

Dega 21 38.18 20 33.33 41 35.65

kola 24 43.64 23 38.33 47 40.87

WoynaDega 10 18.18 17 28.33 27 23.48

Total 55 100 61 100 115 100

Source: Survey results 2020

.* Significant at less than 0.005 per cent level of significance

33 | P a g e

4.1.7 Loan diversion