angola: perspectives on the financial crisis ricardo gazel second afr economists retreat...

TRANSCRIPT

Angola: Perspectives on the Financial Crisis

Ricardo Gazel

Second AFR Economists RetreatJohannesburg, South Africa

December 5, 2008

Impact on Financial Sector

• Likely small as:– No stock market– No strong connection of domestic bank

system with international financial markets (except via Portuguese banks)

– Small interbaking credit market– Low loans to deposit ratios– Solid macroeconomic indicators: budget

surplus, high international reserves, low external debt.

Net International Reserves US$ Millions

5002500450065008500

1050012500145001650018500

2003

2004

2005

2006

2007

08-J

an

08-F

eb

08-M

ar

08-A

pr

08-M

ay

08-J

un

08-J

ul

08-A

ug

08-S

ep

10-O

ct-0

8

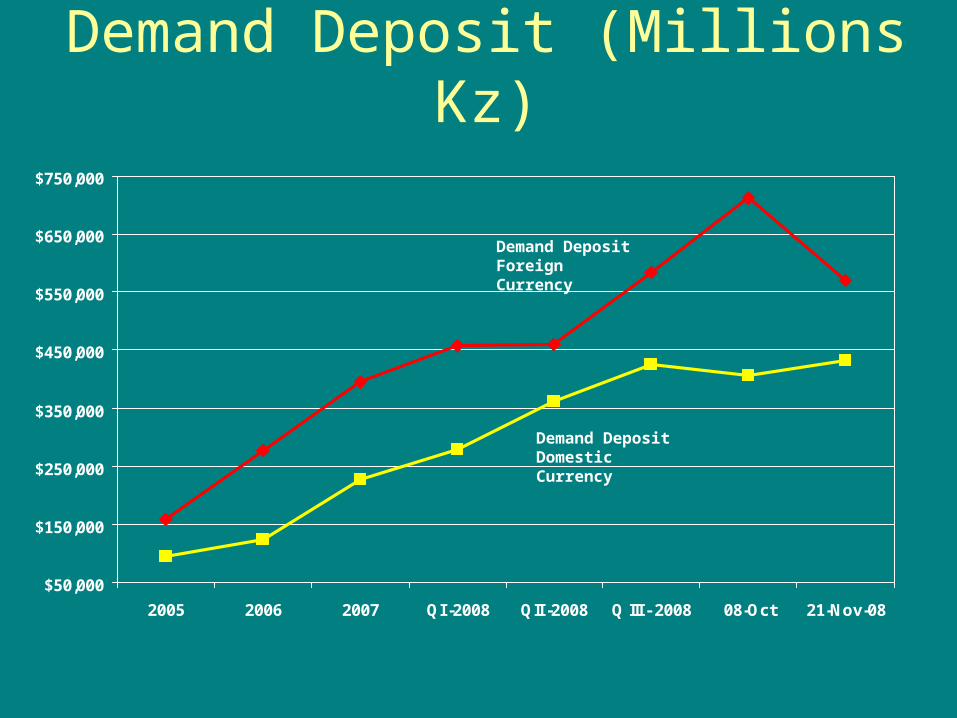

Demand Deposit (Millions Kz)

$50,000

$150,000

$250,000

$350,000

$450,000

$550,000

$650,000

$750,000

2005 2006 2007 QI -2008 QII -2008 Q III - 2008 08-Oct 21-Nov-08

Demand Deposit Foreign Currency

Demand Deposit Domestic Currency

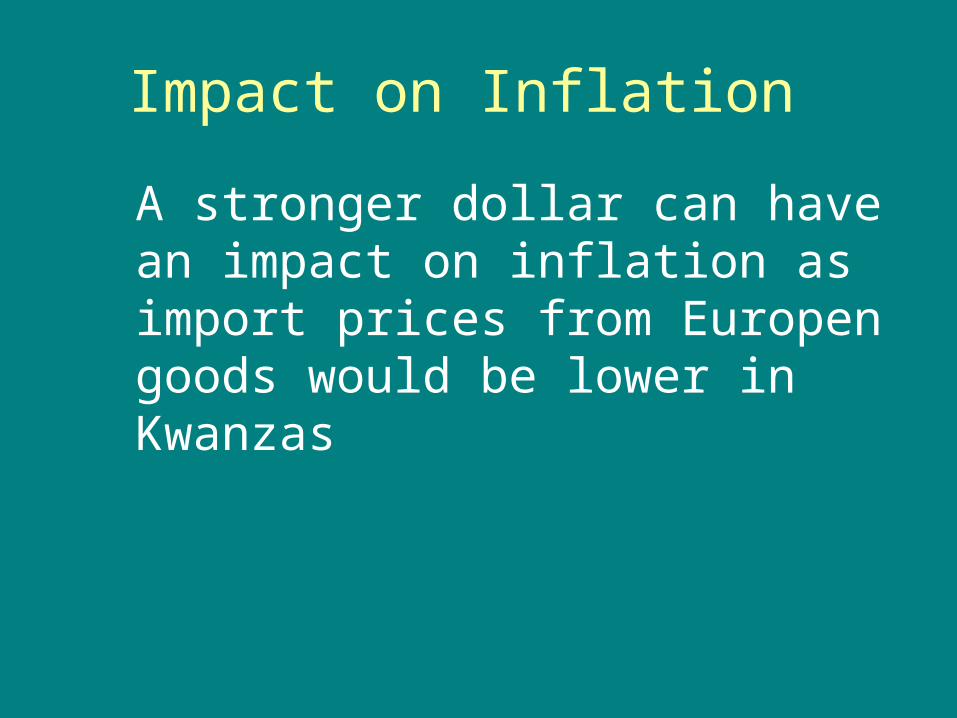

Impact on Inflation

A stronger dollar can have an impact on inflation as import prices from Europen goods would be lower in Kwanzas

Yearly Inflation

0

50

100

150

200

250

300

2000 2001 2002 2003 2004 2005 2006 2007

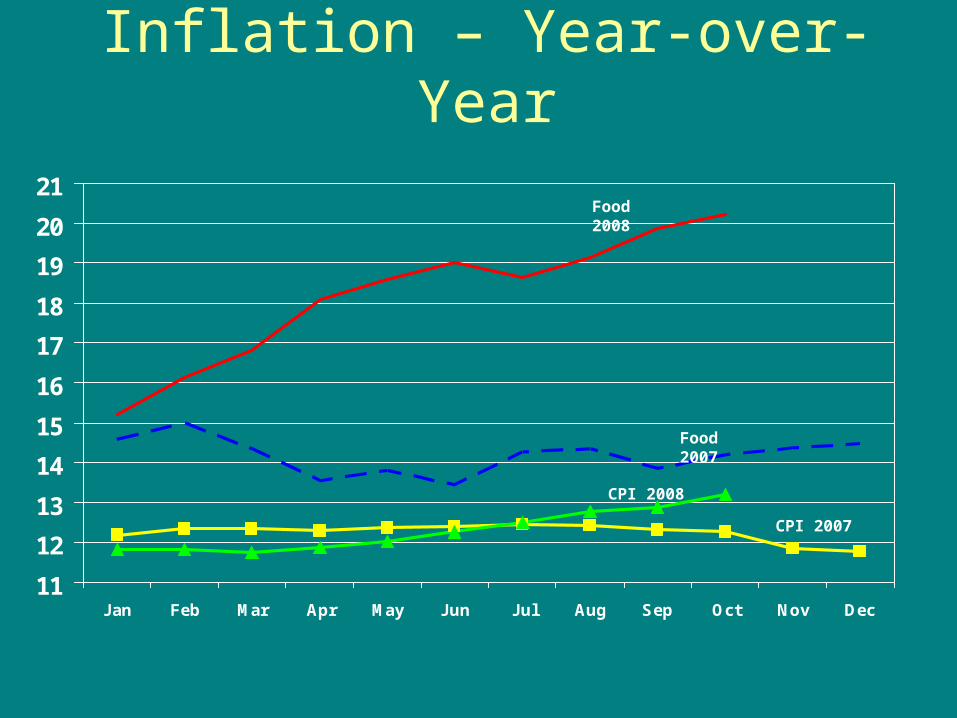

Inflation – Year-over-Year

11

12

13

14

15

16

17

18

19

20

21

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Food 2008

CPI 2008

Food 2007

CPI 2007

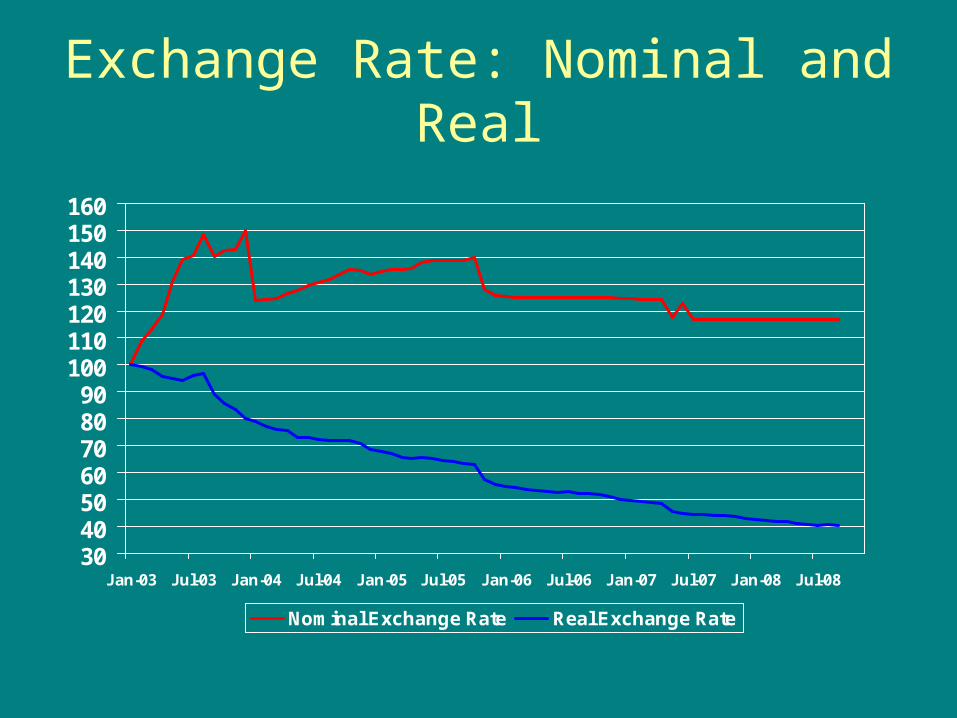

Exchange Rate: Nominal and Real

30405060708090

100110120130140150160

Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08

Nominal Exchange Rate Real Exchange Rate

Nominal Exchange Rates

60

70

80

90

100

110

120

130

Jan-07 Mar-07 May-07 Jul-07 Sep-07 Nov-07 Jan-08 Mar-08 May-08 Jul-08 Sep-08

Do

llar,

Eu

ro

8

9

10

11

12

Ra

nd

dollar Euro Rand (Right axis)

Impact on Real Economy • Real Economy:

– Lower price of oil – lower government revenues and lower national income

– Lower government demand – lower growth of non-oil sector

• Investment and Capital Flows– Less liquidity in international credit markets

can reduce investment flows as price of capital increases

– Higher Costs of Government Financing

Exports:US$ Millions

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2003 2004 2005 2006 2007

Oil Non-oil

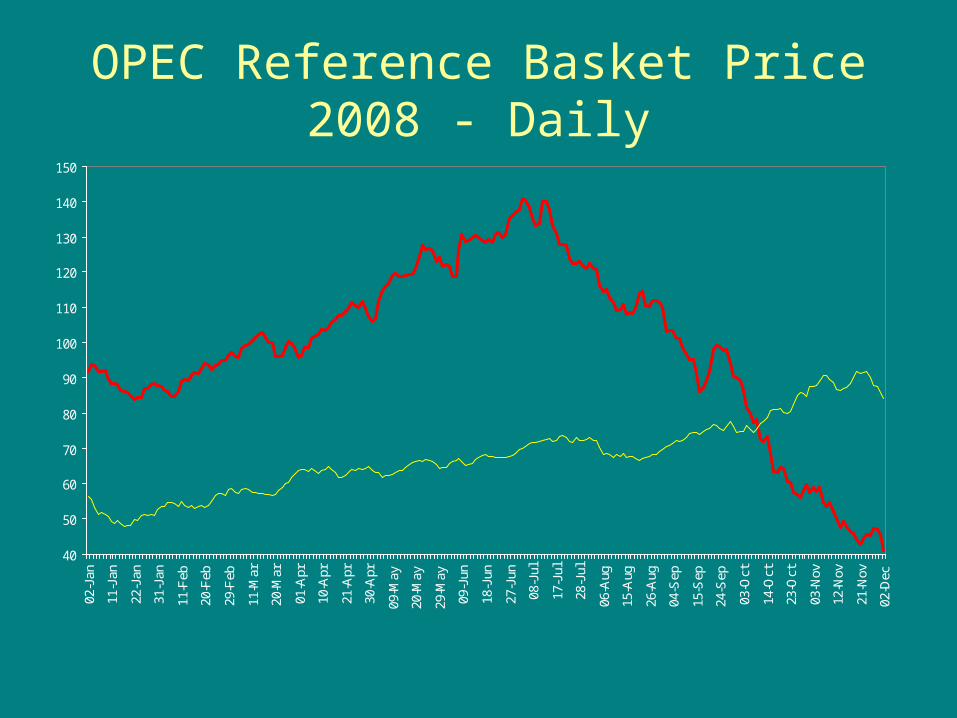

OPEC Reference Basket Price2008 - Daily

40

50

60

70

80

90

100

110

120

130

140

150

02-J

an

11-J

an

22-J

an

31-J

an

11-F

eb

20-F

eb

29-F

eb

11-M

ar

20-M

ar

01-A

pr

10-A

pr

21-A

pr

30-A

pr

09-M

ay

20-M

ay

29-M

ay

09-J

un

18-J

un

27-J

un

08-J

ul

17-J

ul

28-J

ul

06-A

ug

15-A

ug

26-A

ug

04-S

ep

15-S

ep

24-S

ep

03-O

ct

14-O

ct

23-O

ct

03-N

ov

12-N

ov

21-N

ov

02-D

ec

Oil Exports:Volume and Price

311.1 302.6

344.5

452

487.8

522

584

623

24.228.2

36.1

50

61.4

72.4

97.08

55

200

250

300

350

400

450

500

550

600

650

2002 2003 2004 2005 2006 2007 2008 2009

20

30

40

50

60

70

80

90

100

110

Volume (millions of barrels) Price (US$/barrel)

Oil Exports (US$ millions)

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

2002 2003 2004 2005 2006 2007 2008 2009

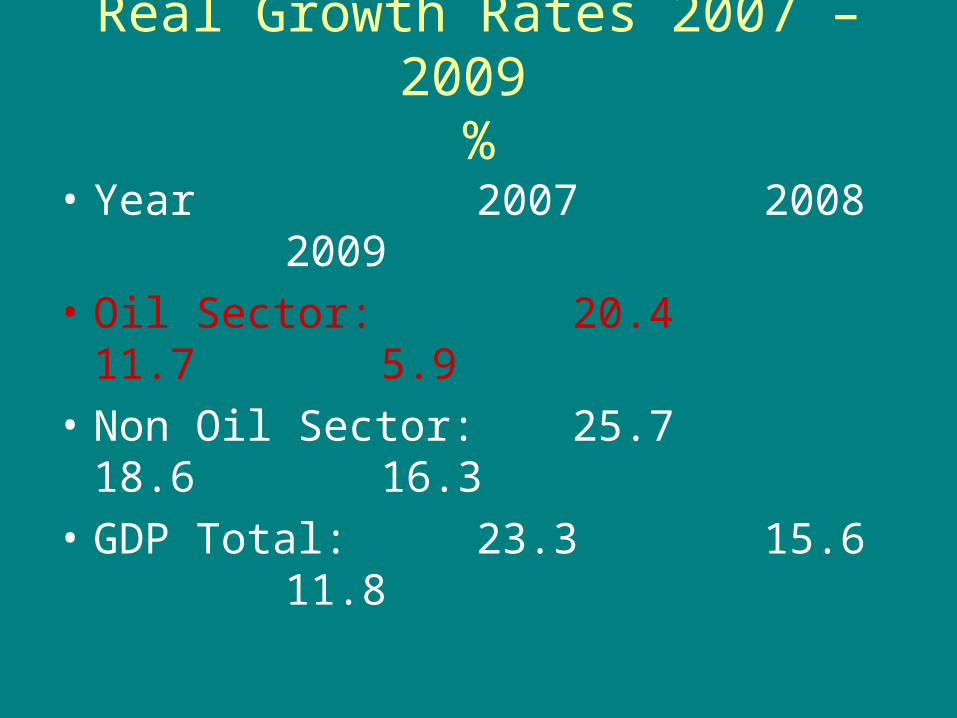

Real Growth Rates 2007 – 2009 %

• Year 2007 2008 2009

• Oil Sector: 20.4 11.7 5.9

• Non Oil Sector: 25.7 18.616.3

• GDP Total: 23.3 15.611.8

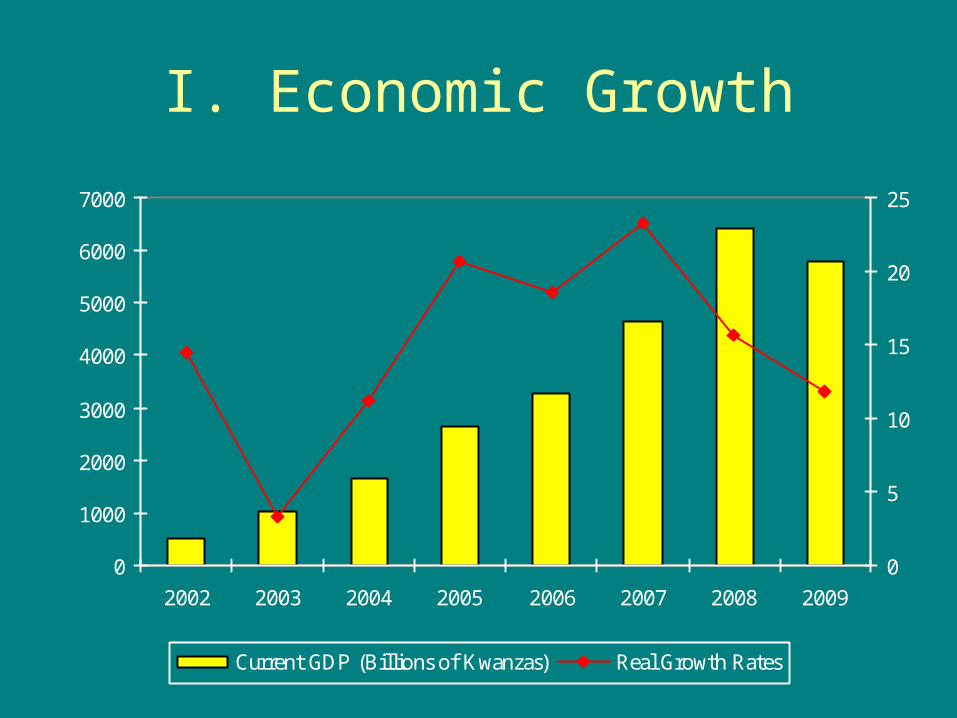

I. Economic Growth

0

1000

2000

3000

4000

5000

6000

7000

2002 2003 2004 2005 2006 2007 2008 2009

0

5

10

15

20

25

Current GDP (Billions of Kwanzas) Real Growth Rates

OIL ProductionMillion Barrels per Day

OPEC Monthly Oil Market Report

1.4

1.6

1.8

2.0

2.2

2007 2008 OPEC Quota OPEC Quotawith

ProductionCut

GovernmentForecast 2009

Real Growth Rates 2007 – 2009 %

• Year 2007 2008 2009

• Oil Sector: 20.4 11.7 5.9

• Non Oil Sector: 25.7 18.616.3

• GDP Total: 23.3 15.611.8

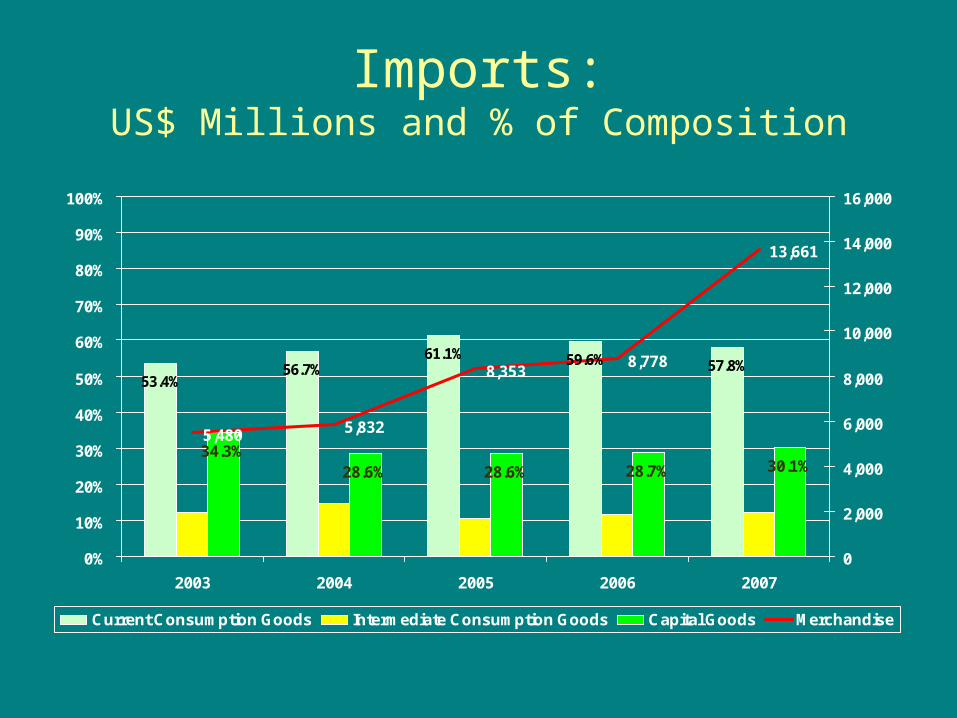

Imports:US$ Millions and % of Composition

53.4%56.7%

61.1% 59.6% 57.8%

34.3%28.6% 28.6% 28.7% 30.1%

5,480 5,832

8,3538,778

13,661

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 2004 2005 2006 2007

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Current Consumption Goods Intermediate Consumption Goods Capital Goods Merchandise

Fiscal Accounts: Revenues Billions of Kwanzas)

0

500

1000

1500

2000

2500

3000

3500

2003 2004 2005 2006 2007 2008 2009

Oil Non-oil

Fiscal Accounts: Growth Rates % over previous year

-30%

0%

30%

60%

90%

2004 2005 2006 2007 2008 2009

Total Revenues Oil Non-oil

Fiscal Accounts: Revenues and Expenditures(% do GDP)

-80%

-60%

-40%

-20%

0%

20%

40%

60%

2003 2004 2005 2006 2007 2008 2009

Non-oil GDP as % of GDP Non-Oil primary fiscal balance (as % of Non-oil GDP)

External Debt including Arrears

0%

10%

20%

30%

40%

50%

60%

70%

80%

2003 2004 2005 2006 2007 2008 2009

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

As % GDP External Debt (US$millions)