analyst working sessionanalyst working session · goldstrike precious metals remaining royalty...

TRANSCRIPT

Analyst Working SessionAnalyst Working Session

May 13, 2010

1

Cautionary StatementF d L ki St t tForward-Looking StatementsThis Presentation contains "forward-looking statements", which may include but are not limited to, statements with respect to future events orfuture performance, management's expectations regarding Franco-Nevada’s growth, results of operations, estimated future revenues, costs andtiming of acquiring new royalties, equity and other resource related interests, requirements for additional capital, mineral reserve and resourcesestimates, production costs and revenue, future demand for and prices of commodities, expected mining sequences, business prospects andopportunities. All statements, other than statements of historical fact, are forward-looking statements. In addition, the words "expects",”expected”, “estimated” and similar expressions identify forward-looking statements. The forward-looking statements contained in thisPresentation are based upon assumptions management believes to be reasonable, including, without limitation, the ongoing operation of theproperties by the owners or operators of such properties in a manner consistent with past practice, the accuracy of public statements anddisclosures made by the owners or operators of such underlying properties, no material adverse change in the market price of the commodities,and any other factors that cause actions, events or results to differ from those anticipated, estimated or intended. However, there can be noassurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from thoseg p , yanticipated in such statements. Franco-Nevada cannot assure investors that actual results will be consistent with these forward-lookingstatements and readers are cautioned that forward-looking statements are not guarantees of future performance. Accordingly, readers shouldnot place undue reliance on forward-looking statements due to the inherent uncertainty therein. These risks, uncertainties and other factorsinclude, but are not limited to: general business and economic conditions; fluctuations in the prices of the primary commodities that drive theCompany’s royalty revenue (gold, platinum group metals, copper, nickel, oil and gas); fluctuations in the value of the Canadian and Australiandollar and any other currency in which the Company generates revenue relative to the U S dollar; changes in national and local governmentdollar, and any other currency in which the Company generates revenue, relative to the U.S. dollar; changes in national and local governmentlegislation, including taxation policies; regulations and political or economic developments in any of the countries where the company holdsinterests in mineral or oil and gas properties; influence of macroeconomic developments; business opportunities that become available to, or arepursued by us; access to debt and equity capital; litigation; title disputes related to our interests or any of the underlying properties; operating ortechnical difficulties; risks and hazards associated with the business of development and mining, including, but not limited to unusual orunexpected operating difficulties, financial stress and other natural disasters or civil unrest. For additional information with respect to risks,uncertainties and assumptions please also refer to the “Risk Factors” section of our most recent Annual Information Form filed with theuncertainties and assumptions, please also refer to the Risk Factors section of our most recent Annual Information Form filed with theCanadian securities regulatory authorities on www.sedar.com, as well as our Annual and interim MD&A. The forward-looking statements hereinare made as of the date of this Presentation only and Franco-Nevada does not assume any obligation to update or revise them to reflect newinformation, estimates or opinions, future events or results or otherwise, except as required by applicable law.

Non-GAAP Measures

2

Royalty Revenue, Free Cash Flow, EBITDA and Adjusted Net Income are intended to provide additional information only and do not have anystandardized meaning prescribed by GAAP and should not be considered in isolation or as a substitute for measures of performance preparedin accordance with GAAP. These measures are not necessarily indicative of operating profit or cash flow from operations as determined underGAAP. Other companies may calculate these measures differently.

Agenda

Financial Update (20 Minutes) Sandip Rana• Q1 2010 Financial Results• Revenue & Commodity Contribution• Revenue Sensitivity & Leverage

Operating Mineral Assets Highlights (20 Minutes) Steve Aaker• Goldstrike • RobinsonGo ds e• Palmarejo• Stillwater• Gold Quarry

ob so• Marigold• Bald Mountain

Oil & Gas Assets Highlights (5 Minutes) Geoff Waterman• Oil & Gas Reserves & Production

Advanced Mineral Assets Highlights (15 Minutes) Paul BrinkT i t Oth Ad d A t• Tasiast

• Detour• Subika (Ahafo)

• Other Advanced Assets• Growth Profile

Prosperity Acquisition (20 Minutes) Paul Brink

3

Q&A

Management

Title Canada David Harquail President & CEO

Sandip Rana Chief Financial Officer p

Sharon Dowdall VP, Special Projects

Jacqueline Jones Chief Legal Officer & Corporate Secretary

H. Geoff Waterman Chief Operating Officer

Paul Brink S.V.P. Business Development

Petra Decher VP, Finance & Assistant Secretary

Jason O’Connell Manager, IR & Business Development

Debbie McEnaney Controller

Lena Miller Senior Accountant

Cindy Smith Land Analyst

Donna Andrejek Office Manager - Toronto

U.S. Stephen Alfers Chief of U.S. Operations Steve Aaker S.V.P. Acquisitions

Jeff Jenkins Director of Finance - U.S. Operations

Edward Jackson Director of Mineral Lands

Katie Griffith Land Administrator

Robert Eckles Office Manager - Denver

4

Australia Kevin McElligott Managing Director, Australian Operations

Q1 2010 Results and Financial Highlights

Sandip Rana – CFO

5

Company Continues to Deliver Strong Financial Results

Continued growth in Royalty Revenue• 43% year-over-year increase

Continued growth in Gold Royalty Revenue• 43% year-over-year increase

Strong Earnings & Free Cash Flow

Working Capital Strong – Approximately $600M

Diversification of Revenue

6

Q1 2010 Highlights

(US$ millions except per share and %) Q1 ’10 Q1 ’09 Q1 ’08Royalty Revenue(1) $41.8 $29.2 $27.5Royalty Revenue $41.8 $29.2 $27.5

Gold Royalty Revenue 27.4 19.1 12.2

Total revenue(2) 37.9 33.1 27.5

Net income 7.8 3.8 5.2

Earnings per share $0.07 $0.04 $0.06

Free Cash Flow(3) 37.1 24.9 23.4

Free Cash Flow(3) per share 0.33 0.25 0.26

Margin(4) 89% 85% 85%

Adjusted Net Income(5) 8.6 0.5 4.4

Adjusted Net Income per share $0.08 $0.01 $0.05

(At March 31, 2010) (At March 31, 2009) (At March 31, 2008)

Working capital $598.1 $185.2 $290.9

Total shareholders’ equity $2,010.6 $1,423.1 $1,528.8

7

(1) Royalty Revenue is defined by the Company as cash received or receivable from operating royalty assets earned during the period.(2) Includes fair value changes on derivative assets. (3) Free Cash Flow is defined by the Company as operating income plus depletion and depreciation, non-cash charges, and any impairment of investments and royalty interests.(4) Margin is defined as Free Cash Flow (3) as a % of Royalty Revenue(1).

(5) Adjusted Net Income is defined by the Company as net income excluding impairment charges related to royalties and working interests and investments, fair value changes for royalties accounted for as derivative assets, foreign currency gains/losses; gains/losses on sale of investments; and the impact of taxes on all these items.

Growth in Royalty Revenue(1) from Precious Metal Assets

45

50

30

35

40

ns)

Oil & Gas

15

20

25

($ m

illio

n Oil & GasBase Metals & OtherPGMGold

0

5

10

75% of Royalty Revenue in Q1’10 derived from precious metals

0Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010

8

75% of Royalty Revenue in Q1 10 derived from precious metals

(1) Royalty Revenue is defined by the Company as cash received or receivable from operating royalty assets earned during the period.

Royalty Revenue(1) & Free Cash Flow (“FCF”)(2)

3Royalty Revenue(1)

.5 $3

9.0

$37.

1

2.9 $3

6.4

$44.

3

$41.

8

Free Cash Flow (2)

Royalty Revenue(1)

89%

89%88%

85%$2

4.9 $27.

9 $32 .

$29.

2 $32 $

FCF/Revenue % 85%85%

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010

9

(1) Royalty Revenue is defined by the Company as cash received or receivable from operating royalty assets earned during the period. Note revenue figures are in millions. (2) Free Cash Flow is defined by the Company as operating income plus depletion and depreciation, non-cash charges, and any impairment of investments and royalty interests

Royalty Revenue(1) by Commodity

Three months endedYear Ended

Oil and

Three months ended March 31, 2010

Oil & G

Year Ended December 31, 2009

Gold65%PGM

10%

Other Minerals

2%

O a dGas23%

Gold70%

PGM8%

Other Minerals

2%

Oil & Gas20%

10%

10

(1) Royalty Revenue is defined by the Company as cash received or receivable from operating royalty assets earned during the period.

Quality Assets in Quality Jurisdictions

Royalty Revenue(1) by CountryThree Months Ended March 31, 2010

Australia

Royalty Revenue(1) Components Three Months Ended March 31, 2010

Palmarejo22%

B M t l

Edson8%

Midale2%

O&G Other

7%

Mexico

Other3%

Australia3%

Gold Quarry4%

Goldstrike - NSR9%Stillwater

8%

Pandora2%

Base Metals & Other

2%

Weyburn6% US

45%

Mexico22%

Goldstrike - NPI11%

Marigold8%

Gold Other11%

Canada27%

Diversified portfolio generating 89% Margin(2)

11

(1) Royalty Revenue is defined by the Company as cash received or receivable from operating royalty assets earned during the period.(2) Margin is defined as Free Cash Flow as a percentage of Royalty Revenue.

Growing Gold – Less Dependent on Goldstrike

100%

Royalty Revenue(1) Contribution

70%

80%

90%

100%

40%

50%

60%

70%

10%

20%

30%

40%

0%

10%

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010

Goldstrike Precious Metals Remaining Royalty Revenue

12

(1) Royalty Revenue is defined by the Company as cash received or receivable from operating royalty assets earned during the period.

Royalty Revenue(1) Q1 2009 to Q1 2010

8,996

4,1741,905 1,631

1,236

2,220 1,578 1 209

41,805

29,217

8,996 1,578 1,209 347

13(1) Royalty Revenue is defined by the Company as cash received or receivable from operating royalty assets earned during the period. Note, revenue is in thousands of dollars.

Net Income Q1 2009 to Q1 2010

8 414

4,1742,780 459

16,557

8,414

3 797

16,138

7,714

4 548

7,781

3,797 4,548

14Note, net income is in thousands of dollars.

Franco-Nevada’s Capacity for New Projects

Capital Resources @ March 31, 2010 US$ Millions

Working Capital $598

Marketable Investments (Primarily NEM) $52

Available Credit Facility $175

Total Available Capital $825

No debt, hedges or material capital obligations

Plus additional capacity from growing free cash flows

15

Sources of Gold Leverage

Higher leverage from royalty structure:– profit based royalties (Goldstrike, Hemlo …)

l d lti

Working interests

7%

Three months ended March 31, 2010

– scaled royalties (Holloway, Holt …)

– gold streams (Palmarejo)

10% gold price move ≈Revenue-

Based royalties

Profit

Other22%

7%

10% gold price move 13% change in gold revenue*

Higher gold prices add further leverage from:

56%Profit-based

royalties15%

Higher gold prices add further leverage from: – resource to reserve conversion– increased risk capital to advance projects on Franco lands

Royalties provide:- more leverage and yield than an ETF

16* Management estimate based on $1100/oz gold price

- less project, capital and cost risk than an operator

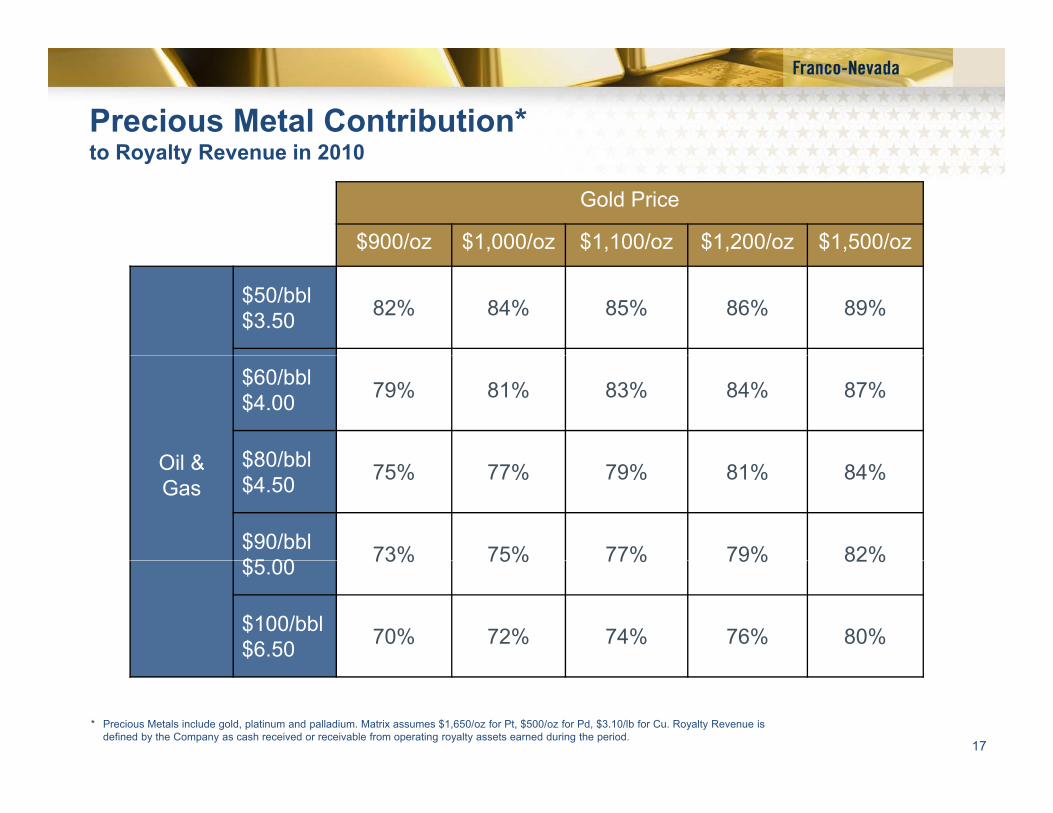

Precious Metal Contribution*to Royalty Revenue in 2010to Royalty Revenue in 2010

Gold Price

$900/oz $1,000/oz $1,100/oz $1,200/oz $1,500/oz

$50/bbl$3.50 82% 84% 85% 86% 89%

Oil &

$60/bbl$4.00 79% 81% 83% 84% 87%

$80/bblOil & Gas

$80/bbl$4.50 75% 77% 79% 81% 84%

$90/bbl$5 00 73% 75% 77% 79% 82%$5.00 73% 75% 77% 79% 82%

$100/bbl$6.50 70% 72% 74% 76% 80%

17

* Precious Metals include gold, platinum and palladium. Matrix assumes $1,650/oz for Pt, $500/oz for Pd, $3.10/lb for Cu. Royalty Revenue is defined by the Company as cash received or receivable from operating royalty assets earned during the period.

Additional Financial Details in Appendices

Accounting Definitions for FCF & Adjusted Net Income

Derivative Accounting for PalmarejoDerivative Accounting for Palmarejo

Book Values

Income TaxesIncome Taxes

– Tax Depletion and Tax Balances

– Applicable Statutory Tax Ratespp y

Costs and Expenses & Interest Expense

Capital Structure

Liquidity & Capital Resources

Security of Investments

18

Operating Mineral Assets

Steve Aaker – Senior VP AcquisitionsSte e a e Se o cqu s t o s

19

Franco- Nevada Royalty Operators include:

Core Operators:

Goldstrike - NevadaBald Mountain - Nevada

Up and Comers:

Palmarejo – Mexico*Bald Mountain - NevadaHemlo - Ontario

Gold Quarry – Nevada*Ah f S th Gh *

Mesquite – CaliforniaCerro San Pedro – Mexico

Holloway - OntarioAhafo South – Ghana*

Marigold - NevadaMusselwhite – Ontario

Hislop - OntarioHolt - Ontario

Tasiast - Mauritania

Stillwater – MontanaEast Boulder - Montana

Detour Lake - Ontario

PalmarejoGoldstrike

Palmarejo

20* post IPO acquisitions

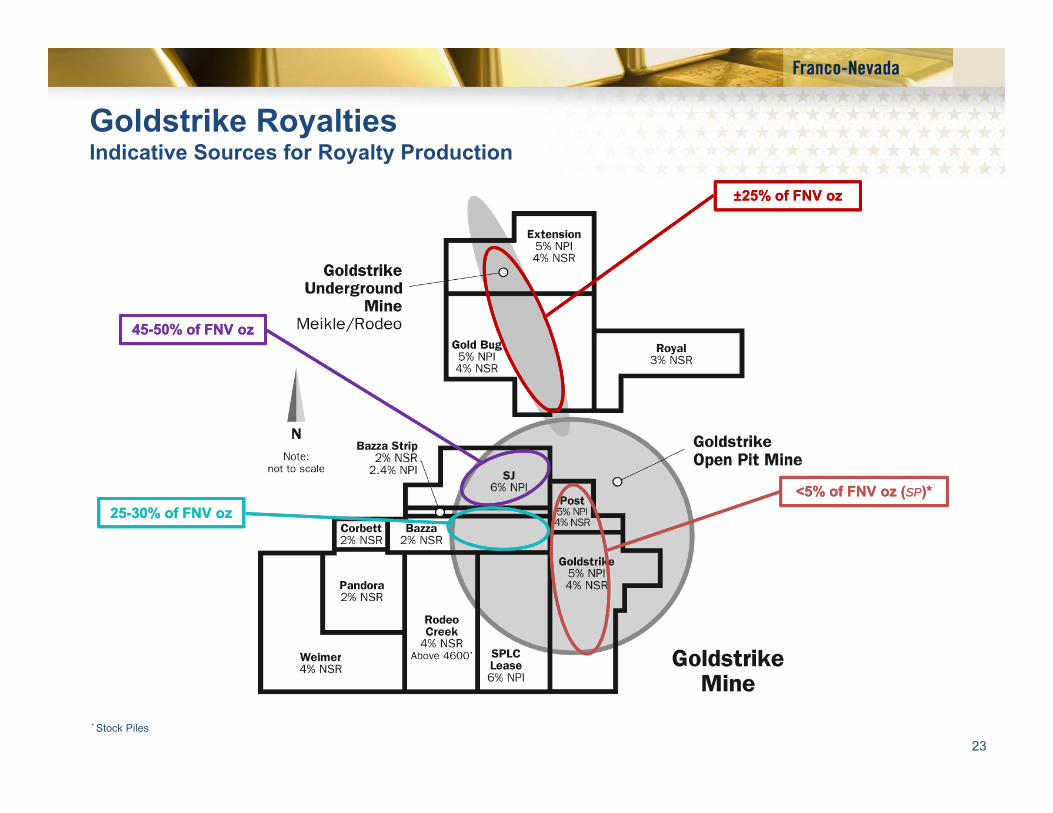

Goldstrike RoyaltiesView looking West

D id S h h h t

Goldstrike Royalties:

• Located in Nevada & Operated by Barrick

• 4% NSR and 5% NPI on the Post and Goldstrike claims

David Schumacher photo

• 4% NSR and 5% NPI on the Post and Goldstrike claims

• 4% NSR and 5% NPI on the Extension and Gold Bug claims

• 2% NSR over the Bazza claims and a 2% NSR and 2.4% NPI over the Bazza Strip area

21

• 6% NPI on the SJ claims and SPLC lease area

• 2% - 4% NSR royalties on other peripheral claim and fee lands.

Goldstrike Royalties

2009 results - Barrick reported:

• Goldstrike produced 1,355 K oz at cash costs of $464/oz

– A major waste removal phase began in 2H-09 with the processing of lower grade ores in theA major waste removal phase began in 2H-09, with the processing of lower grade ores in theBetze-Post pit.

2010 guidance - Barrick expects:

• Goldstrike production to decline to 1,150 to 1,200 K oz at total cash costs of $495 to $515/oz

2008 2009 2010

– grades and recoveries in the first half of the year are expected to be lower due to minesequencing and waste stripping.

Actual Actual Forecast

NSR Revenue ($m) (2) $18.7 $21.5NPI Revenue ($m) (2) $30.9 $20.5Production (K oz)(1) 1,706 1,355 ±1,200P&P Reserves (K o ) (1) 12 839 12 156P&P Reserves (K oz) (1) 12,839 12,156M&I Resources (K oz) (1) 2,312 2,353Inferred Resources (K oz) (1) 1,390 1,046% Oz Prod. (FNV royalty) (2) 86% 100% 85-100%

David Schumacher photo

22

(1) Production and Reserves - Resources are reported on a 100% basis & include ounces not subject to FNV’s royalty. Production forecast based on Barrick guidance. (2) Revenue and % Oz Prod. are for FNV’s pro-rata share of produced ounces and royalty revenues therefrom based on historical results.

Meikle-Rodeo

p

Goldstrike Royalties Indicative Sources for Royalty ProductionIndicative Sources for Royalty Production

±25% of FNV oz±25% of FNV oz

45-50% of FNV oz45-50% of FNV oz

<5% of FNV oz (SP)*<5% of FNV oz (SP)*25-30% of FNV oz25-30% of FNV oz

23* Stock Piles

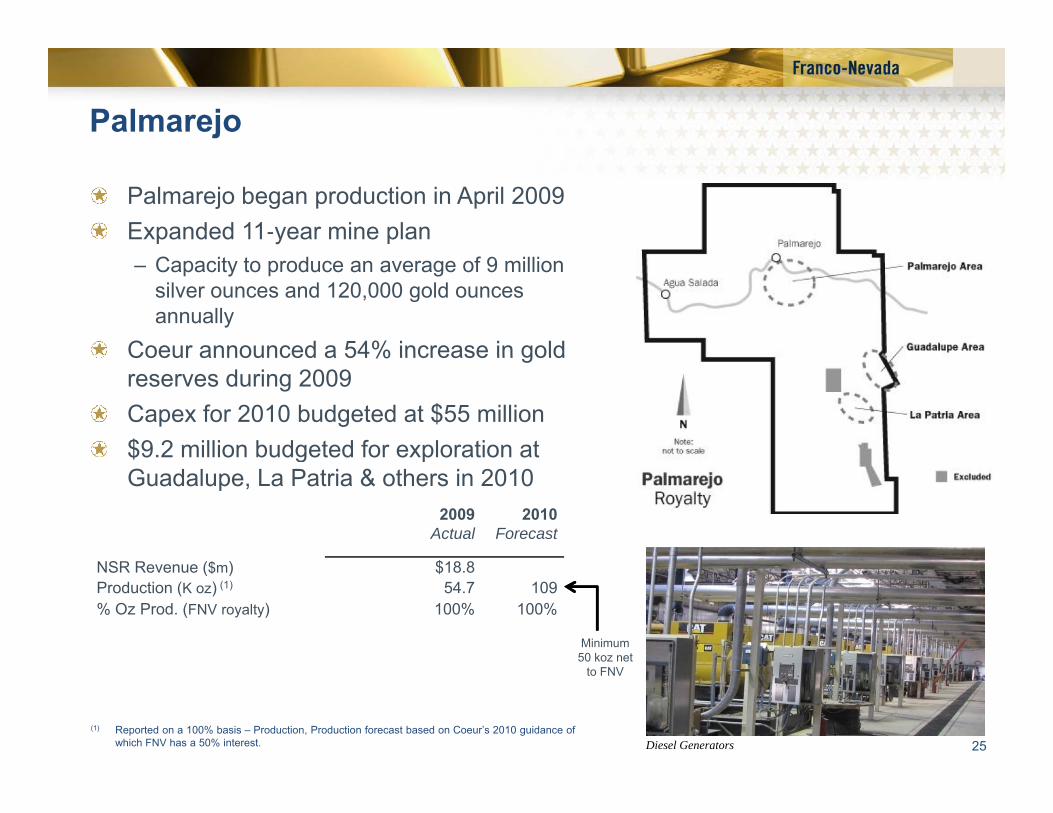

Palmarejo

Gold Royalty Stream on Coeur’s Ag-Au project in Mexico • $75 million acquisition in January 2009• 50% of gold produced from the 29 000 acre Palmarejo Property (uncapped)50% of gold produced from the 29,000 acre Palmarejo Property (uncapped)• less $400 per oz (increasing by 1% per annum after four years)• Minimum of 50,000 ozs per annum beginning July 1, 2009 until 400,000 ozs have been paid• Additional 316,436 shares of FNV ($5 million at closing) if certain milestones are achieved( g)

24

Palmarejo

Palmarejo began production in April 2009Expanded 11‐year mine plan– Capacity to produce an average of 9 million

silver ounces and 120,000 gold ounces annually

Coeur announced a 54% increase in goldCoeur announced a 54% increase in gold reserves during 2009Capex for 2010 budgeted at $55 million$9.2 million budgeted for exploration at $ g pGuadalupe, La Patria & others in 2010

2009 Actual

2010Forecast

$NSR Revenue ($m) $18.8Production (K oz) (1) 54.7 109% Oz Prod. (FNV royalty) 100% 100%

Minimum 50 koz net

25Diesel Generators(1) Reported on a 100% basis – Production, Production forecast based on Coeur’s 2010 guidance of

which FNV has a 50% interest.

to FNV

Stillwater Royalty

Stillwater Royalty

• 5% NSR o Payable on

production from 813production from 813 of the 995 claims

o Royalty claims cover the majority of the Stillwater mine and all

f th E t B ldof the East Boulder mine

26View looking south View looking south

Stillwater

PGM metal price declines led to a restructuring of operations at the Stillwater complex in 2009, resulting in:g

• reduced production from East Boulder• reduced total company workforce, including

contractors, by 27%.• performance to date under the restructured

mine plan and increased metal prices point to a favorable 2010 operating year

2008 actual

2009 actual

2010 forecast

Revenue ($000) (1) $13,553 $10,135Production (PGM K oz) (2) 499 530 515Production (PGM SW/EB) (2) 384/115 407/123 370/125Production (PGM SW/EB) ( ) 384/115 407/123 370/125P&P Reserve (PGM K oz) (2) 20,461 20,614% Oz Prod. (FNV royalty) (3) 88% 88% 85-90%

27

(1) Revenue is based on FNV’s pro-rata share of production(2) Production and Reserves are reported on a 100% basis & include ounces not subject to FNV’s royalty.

2010 forecast based on Stillwater 2010 guidance.(3) Management estimate

Gold Quarry Royalty

Gold Quarry Royalty is based on:

• 7 29% NSR of “Property” production or7.29% NSR of Property production, or• Minimum Annual Royalties (“MAR”) tied to

unpaid “Property:”1. Reserves2 Stockpiles2. Stockpiles

David Schumacher photo

2009 Totals

2010Forecast

NSR Revenue ($m) $13.8($ ) $Royalty Oz Net to FNV (K oz) (1) 14,431 16,500

28(1) Royalty ounces are 100% net to FNV.

Gold Quarry – West Wall Layback

Newmont’s GQ West Wall Layback

In Feb-2010 NEM announced a 2 9 Moz ProvenIn Feb 2010, NEM announced a 2.9 Moz Proven and Probable reserve increase at Gold Quarry

• Increase resulted from conversion of West Wall Layback resources announced last year

• New P&P ounces will extend mine life of Gold Quarry

• The P&P ounces on the Property will NeNe p y

positively impact the life of Franco’s MAR/reserves

• In 2010 Q-1 conference call, Newmont reports continued exploration success at

ew

P&P?

ew

P&P?

reports continued exploration success at Gold Quarry

29Exact portion of deposit subject to royalty is uncertain

Gold Quarry RoyaltyNewmont’s GQ geotechnical failure

In Feb-2010, NEM announced a geotechnical failure occurred at GQ, resulting in the deferral of 150,000 oz/year in production for both 2010 and 2011. NEM

ti i t i i th d f d i 2012 danticipates mining the deferred ounces in 2012 and 2013.

• Franco understands the event occurred in the SE portion of the pit, for the most part off the “P t ”“Property”

• The deferral of GQ production will impact Franco’s royalty payments only if the new mine plan results in unexpected changes to Property

Revised Outlook

Stockpiles and/or Reserves and the associated MAR calculation based thereon.

Revised OutlookAt acquisition, guidance for the GQ Royalty was “on average, greater than

11,200 gold royalty ounces per annum”. In 2009, the MAR-Stockpile payment increased to 14,431 ozs. For 2010, initial guidance, based on the MAR-

Stockpile is expected to be 16 500 oz

30

Stockpile, is expected to be 16,500 oz

FNV accrues for minimum royalty provision in Q4 only

Robinson Cu-Au Royalties

Robinson Royaltiesy• 0.225% NSR royalty

• 10% price participation royalty on 51% of the gold produced above 60,000 oz

Unpatented Claims

Patented Claims

above 60,000 oz

• A price participation royalty on 51% of each pound of copper produced in excess of 130 million pounds multiplied by a

Kimbley Wedge

5¢/lb minimum plus 40% of the difference between the average spot price less a threshold price of $1.00 per pound adjusted for inflation (CPI 1990 basis)

31

(CPI -1990 basis).

Robinson Cu-Au Royalties

2008Actual

2009 Actual

2010 Forecast

Au Revenue ($000) $2,868 $1,946Cu Revenue ($000) $10 534 $512Cu Revenue ($000) $10,534 $512Production (K oz Au) (1) 137.6 99.0 80P&P Reserves (K oz Au) 905 704M&I Resources (K oz Au) (2) 1,901 1,993

Production (Mlbs Cu) 159.7 122.5 135( )P&P Reserves (K t Cu) 728 546M&I Resources (K t Cu) (2) 2,082 1,974% Oz Prod. (FNV royalty) 100% 100% 100%

(1) 2010 production forecast based on Quadra guidance.(2) Resources & reserves from Quadra website. M&I are inclusive of P&P but do not include

stockpiles. M&I are at a 0.3% Cu Cutoff.

32

David Schumacher photo

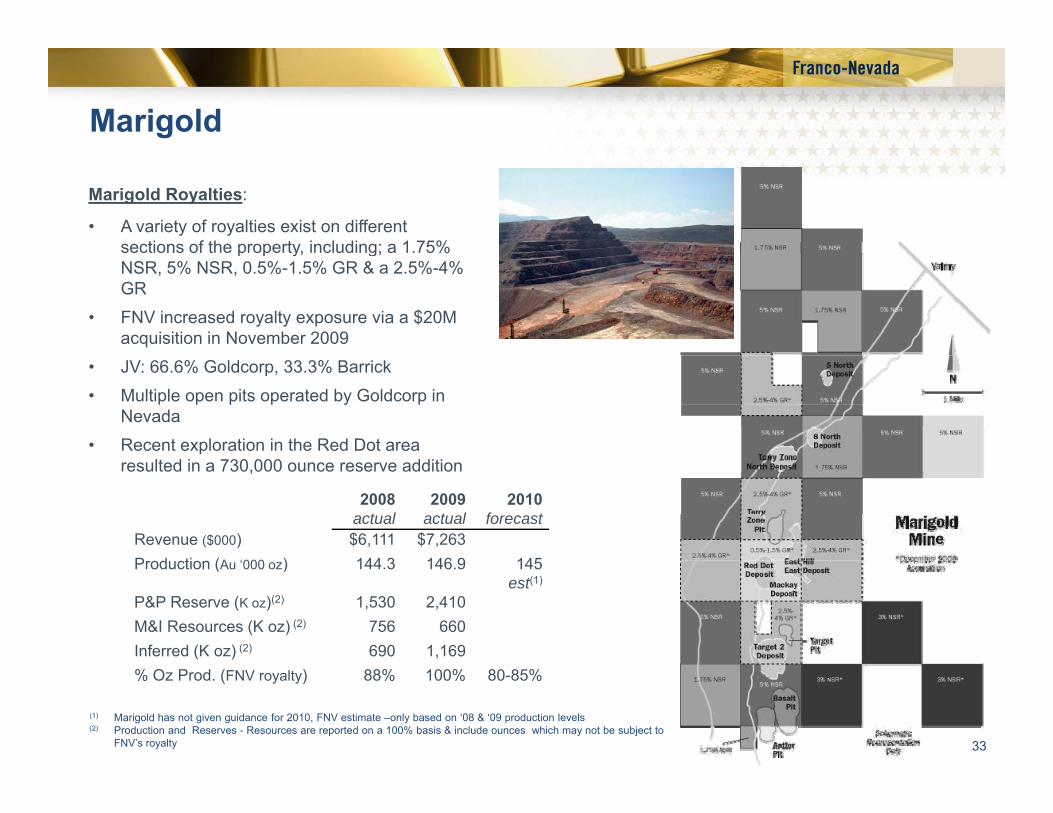

Marigold

Marigold Royalties:

• A variety of royalties exist on different sections of the property, including; a 1.75% sect o s o t e p ope ty, c ud g; a 5%NSR, 5% NSR, 0.5%-1.5% GR & a 2.5%-4% GR

• FNV increased royalty exposure via a $20M acquisition in November 2009

• JV: 66.6% Goldcorp, 33.3% Barrick • Multiple open pits operated by Goldcorp in

Nevada• Recent exploration in the Red Dot area

resulted in a 730,000 ounce reserve addition

2008 actual

2009 actual

2010 forecast

Revenue ($000) $6,111 $7,263P d ti (A ‘000 ) 144 3 146 9 145Production (Au ‘000 oz) 144.3 146.9 145

est(1)

P&P Reserve (K oz)(2) 1,530 2,410M&I Resources (K oz) (2) 756 660Inferred (K oz) (2) 690 1,169

33

(1) Marigold has not given guidance for 2010, FNV estimate –only based on ‘08 & ‘09 production levels(2) Production and Reserves - Resources are reported on a 100% basis & include ounces which may not be subject to

FNV’s royalty

% Oz Prod. (FNV royalty) 88% 100% 80-85%

Bald MountainBald Mountain Royalties:

• Located in Nevada & operated by Barrick

• Royalties cover only a portion ofRoyalties cover only a portion of the eastern side of the Bald Mountain mine

• 4% NSR on most of the resources & 2.418% NSR on an area f l k Littl B ld Mtformerly known as Little Bald Mtn

• Exploration success resulted in a P&P reserve increase of 57% in 2009

2008 2009 2010 actual actual forecast

Revenue ($000) $2,546 $2,056

Production (Au ‘000 oz) 105 75 75-100 est(1)

P&P Reserve (K oz) (2) 2,846 4,489M&I Resources (K oz) (2) 1,718 1,178Inferred (K oz) (2) 1,525 468% Oz Prod. (FNV royalty) (3) 70% 73% ≈45%

(1) Barrick has not provided guidance for 2010 – FNV forecast is estimate-only based on

34

p g yproduction from 2008-9

(2) Production and Reserves - Resources are reported on a 100% basis & include ounces not subject to FNV’s royalty

(3) Historic % production from FNV lands are back calculated based on average gold price in 2008-2009, 2010 forecast is based on 2003-2007 average % of production off FNV lands

Royalty Lands Only

Other Operating Assets

Asset Operator/ LocationReserves(1)

(‘000 oz)

2009 Production

(‘000 oz)

2009 Royalty

Revenue(‘000 $US)

Estimated 2010Prod. Subject to FNV Royalty (%)

2010 Operator Forecast(2)

(‘000 oz)

Hollister(3)

(3-5% NSR)Great Basin/ Nevada 1,122 44.7 $1,555 100% 135

Holloway/Hislop (4)

(6% & 4% NSR)

St Andrew/ Ontario 119/142 18.8 $1,068 100% 85

(6% & 4% NSR)

Mesquite(0.5-2% NSR)

New Gold/ California 3,137 150 $2,832 100% 145-155

Cerro San Pedro(3)

New Gold/ Mexico 1,408 95.5 $2,245 100% 95-100(Au) 1,400-1,600(Ag)Pedro

(1.95% GR)1,400 1,600(Ag)

Mt Muro7% NSR of 90% (>$410/oz)

Straits Resources/ Indonesia

210 37.4 (Au)208,000 (Ag)

$2,201 60-70% 48

North Lanut5% NSR on 80% of production

Avocet/ Indonesia

216 46.9 $1,760 100% 48

Mt. Keith (0.25% NPI &

BHP/Australia

$720 100% 35-40 Kt Ni

35

(0.375% GR)

(1) Reserves reported by operator for 100% of property & may include ounces not subject to FNV’s royalty(2) 2010 guidance disclosed by operator for 100% of production from the property – Note: Mt Muro production forecast based on June 2010 year end & North Lanut forecast

based on company guidance of 4,000 ounces of production per month, annualized(3) Hollister assumes AuEq ounces, Cerro San Pedro includes gold only ounces except where noted(4) 2010 forecast includes some production from Hislop

Oil and Gas

Geoff Waterman – Chief Operating OfficerGeoff Waterman Chief Operating Officer

36

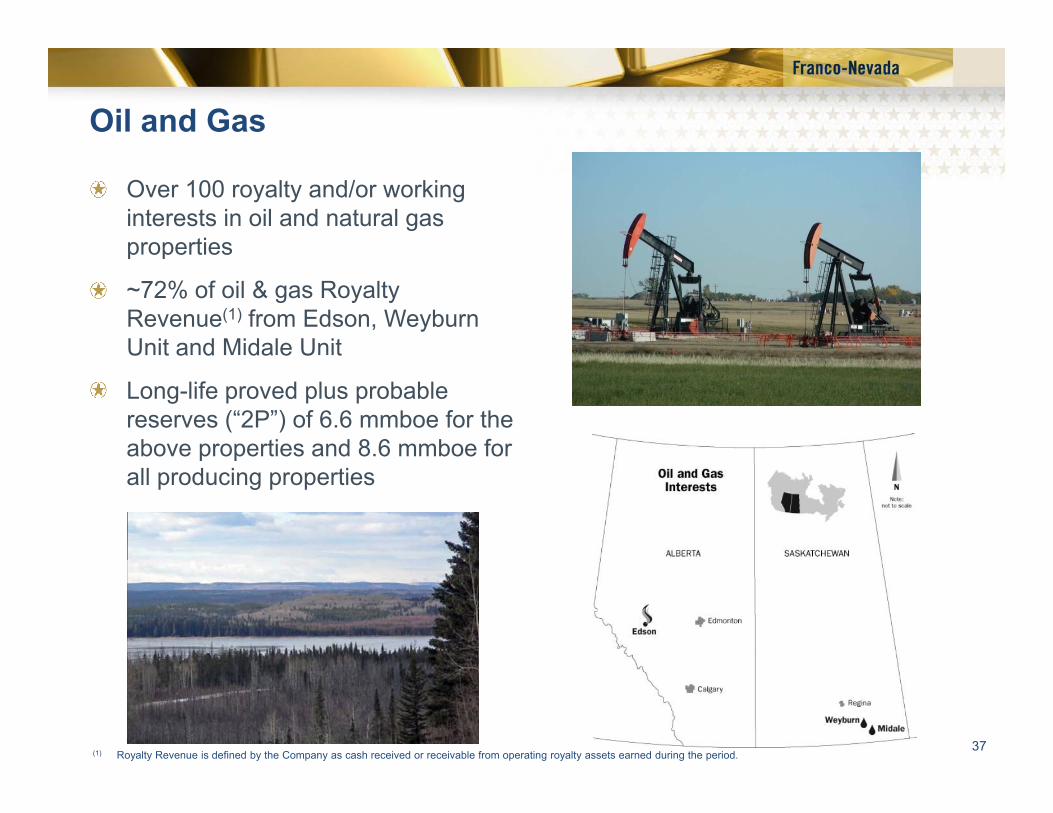

Oil and Gas

Over 100 royalty and/or working interests in oil and natural gas propertiesproperties

~72% of oil & gas Royalty Revenue(1) from Edson, WeyburnUnit and Midale UnitU t a d da e U t

Long-life proved plus probable reserves (“2P”) of 6.6 mmboe for the above properties and 8.6 mmboe for p pall producing properties

37(1) Royalty Revenue is defined by the Company as cash received or receivable from operating royalty assets earned during the period.

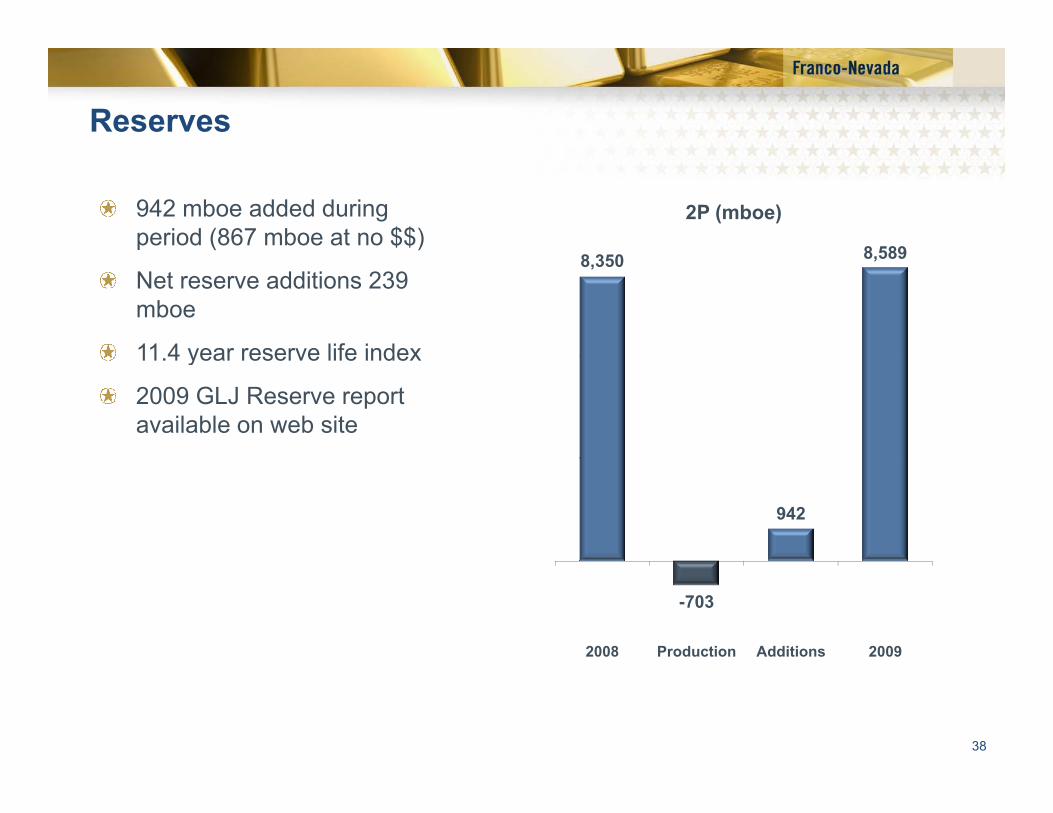

Reserves

8 589

2P (mboe)942 mboe added during period (867 mboe at no $$)

8,350 8,589Net reserve additions 239 mboe

11 4 year reserve life index11.4 year reserve life index

2009 GLJ Reserve report available on web site

942

-703

2008 Production Additions 2009

38

2P Oil and Gas Reserves and RLI (years)

12.0

9 000

10,000

8.0

10.0

6 000

7,000

8,000

9,000

ex in

yea

rs)

4 0

6.0

4,000

5,000

6,000

erve

Life

Inde

(mbo

e)

2.0

4.0

1,000

2,000

3,000

RLI

(Res

e

--12/31/2007 12/31/2008 12/31/2009

Oil (mboe) Gas (mboe) RLI

39

Reserve replacement without exploration costs

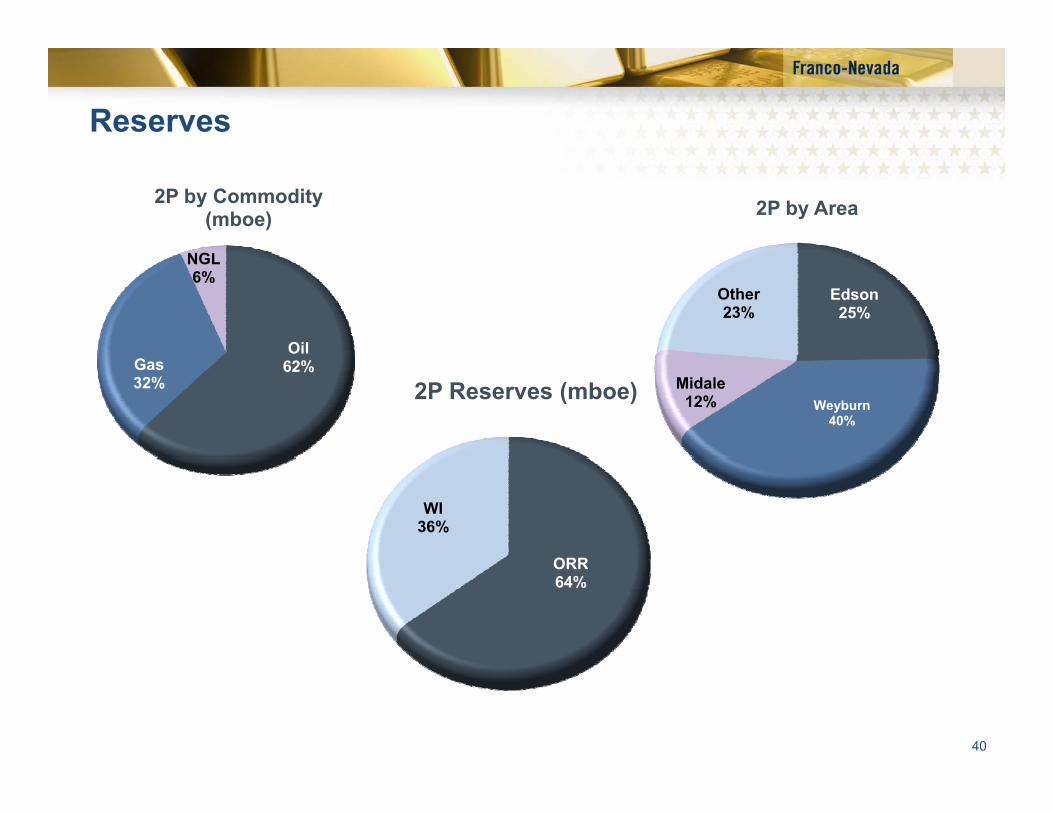

Reserves

2P by Area

NG

2P by Commodity (mboe)

Edson25%

Other23%

Oil

NGL6%

Weyburn40%

Midale12%

62%Gas32% 2P Reserves (mboe)

ORR

WI36%

ORR64%

40

Production History (mboe)(Actual & Forecast)(Actual & Forecast)

900Actual & GLJ Forecast

808

703 750

663 700

800

900

591

500

600 tio

n

reca

st

orec

ast

reca

st

tion

200

300

400

Act

ual

Prod

uct

2009

Fo

2009

Fo

2009

Fo

Act

ual

Prod

uct

-

100

200

41

2008 2009 2010E 2011E 2012E

Ad d Mi l A tAdvanced Mineral Assets

Paul Brink – S.V.P. Business Developmentp

42

SubikaSubika Royalty:

• 2% NSR on a portion of Ahafo South• Beginning after 1.2Moz are produced

f th lt t (887 000 ffrom the royalty property (887,000 oz of production to the end of 2009)

• Covers ~78 km2 and all or portions of 3 of the 4 pits at Ahafo South

• Announced in late 2009 for $58 million• Announced in late 2009 for $58 million• Operated by Newmont in Ghana

Recent Developments:

Project Details

• Newmont exploring Subika Expansion project through deepening of pit and possible new UG mine

• Potential to develop 7-9 million oz, i l di t t S bik

Expected Royalty Start-up(1) 2012Production Subject to Royalty(2) ~50%P&P Reserves (K oz) (3) 9,380M&I Resources (K oz)(3) 7,600A l P d ti ( ) (3) 500 550 k

including current reserves, at Subika(most if not all on FNV ground)

• $40-$60 million in exploration budget for 2010

• In 2010 Q 1 conference call Newmont

43

Annual Production (K oz) (3) 500-550 koz • In 2010 Q-1 conference call, Newmont reports continued drill success at Subika

(1) Start-up based on management estimate of 1.2Moz threshold having been reached.(2) Historically ~ 50% or production has come from royalty ground.(3) Production and Reserves - Resources are reported on a 100% basis & include ounces not subject

to FNV’s royalty

TasiastTasiast Royalty:

• 2% NSR

• Beginning after 600,000 oz are produced from the property (313 502 oz of production to the end of 2009)(313,502 oz of production to the end of 2009)

• Operated by Red Back in Mauritania

Recent Developments:

• Red Back has forecasted production of 245koz – 265koz in 2010

• March 2010 announced reserve increase of 64% to 5.03 M oz

• According to company, both resources and reserves have the potential for significant expansion with new reserves expected in Q3/2010 and an expansion feasibility study in 2011

Cd $600 illi i l i h Ki i M f

Project Details

• Cdn$600 million private placement with Kinross in May for an anticipated processing and mining expansion at Tasiast.

Expected Royalty Start-up(1) 2011Production Subject to Royalty 100%P&P Reserves (K oz) (2) 5,030M&I Resources (K oz) (2) 6,510Inferred Resources (K oz) (2) 1 300

44

Inferred Resources (K oz) 1,300Annual Production (K oz) (2) >250

(1) Start-up based on management estimate of 600 koz threshold having been reached.(2) Production and Reserves - Resources are reported on a 100% basis – M&I resources include

reserves.

DetourDetour Royalty:

• 2% NSR• Full feasibility stage project owned by Detour Gold in

Recent Developments:

• Detour completed a C$275 million financing in November, 2009 toward development of the projectOntario

Project DetailsExpected Royalty Start-up(1) End of 2012Production Subject to Royalty 100%P&P Reserves (K oz) (2) 8,813

development of the project• Pre-feasibility study in September, 2009

outlined 560koz annual production at $404/oz

• Detour now expects to exceed 10 millionM&I Resources (K oz)(2) 17,263Inferred Resources (K oz) (2) 5,189Annual Production (K oz) (2) 600Expected Mine Life 14.5 yrs

Detour now expects to exceed 10 million ounces in reserves and achieve production of over 600,000 ounces of gold per year

• Permitting is underway and feasibility study is expected in mid-2010

(1) St t b d t ’ ti li & l d ti b d D t id(1) Start-up based on operator’s timeline & annual production based on Detour guidance.(2) Production and Reserves - Resources are reported on a 100% basis – M&I resources include

reserves.

45

Recent Development Project News

Property Royalty Update

Hollister 3-5% NSR Great Basin recently signed an agreement with Newmont to process 30 000 t 50 000 t f t k il d t b h d b NEM t30,000 to 50,000 tons of stockpiled to be purchased by NEM at $1,000/oz. Currently 51,000 tons are stockpiled containing 49,000 AuEq oz. Hollister also had its first gold pour at its Esmeralda Mill on April 14 and has guided 2010 production of 135,000 oz (including stockpiles).p )

Hemlo 3% NSR &50% NPI

FNV began receiving some initial revenue-based royalties in 2009 and the current operating plan projects the production of 200koz from the property between 2010-2015.

Perama Hill 2% NSR Eldorado is in the process of permitting the project and could begin construction in early 2011 if permits are received as planned. Production is expected to be 110koz per year.

$Rosemont 1.5% NSR Augusta has been focused on permitting and financing the $900 million Rosemont project and recently closed a $43 million off-take financing with Red Kite, an equity financing, and the sale of a precious metals stream to Silver Wheaton for $230 million.

Other Various Dee/Arturo Duketon Kirkland Lake Pinson Ity Falcondo

46

Other Various Dee/Arturo, Duketon, Kirkland Lake, Pinson, Ity, Falcondo

Outlook for Longer Term Gold GrowthGold only royalty revenues excluding other revenues (1)Gold only royalty revenues excluding other revenues (1)

H l $5 15

$100 5m

Palmarejo $16-19mHolloway-Hislop 4-5m

Tasiast $10-11mHolt 3-4mMarigold 1-4mDuketon 2-3m

Hemlo $5-15mDetour 12-13mAhafo 6-11mRosemont 1-2mGoldfields 1-2mPerama Hill 2-3m

$70.7m

$100.5m y pHollister 3-5mOther 1-2m

Ity 1m

Fully paid assets no further investment in $ or mgm’t timeFully paid assets – no further investment in $ or mgm’t time

2008A 2009A 2010/11E 2011/12E 2012/14E

~$100m in potential new gold Royalty Revenues(1) by 2014

47

$100m in potential new gold Royalty Revenues by 2014

(1) Royalty Revenue is defined by the Company as cash received or receivable from operating royalty assets earned during the period. *Appendix provides detail to pro-forma estimates assuming $1100 gold.

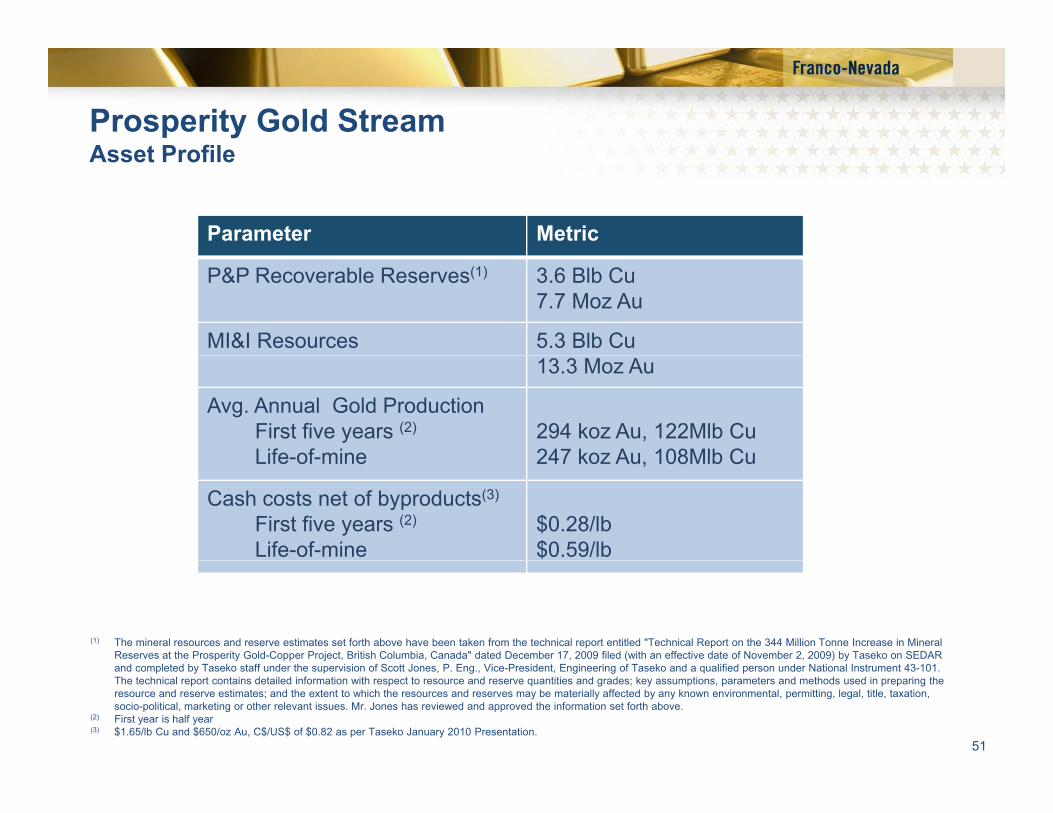

Prosperity Gold Stream

Paul Brink – S.V.P Business Developmentau S us ess e e op e t

48

Prosperity Gold Stream Overview

Gold stream on LOM gold production from Prosperity

Overview

production from Prosperity

Long life project in Canada

Focus asset for Taseko MinesFocus asset for Taseko Mines Ltd.

Proven operator in the region p

Open pit copper/gold porphyry

Asset value is approx. 50% copper and 50% gold(1)

p

copper and 50% gold

49

(1) Revenue calculated at $1,100/oz Au and $2.50/lb Cu.

Prosperity Gold StreamTermsTerms

$350 million deposit funded pro-rata during construction with other financing for the project and 2 million FNV 2017 share warrantsg p j

Right to purchase gold equal to 22% of LOM gold in concentrate for $400/oz (inflation adjusted)

Funding contingent on:Funding contingent on:

– permitting,

– project being fully financed, and

– 75% of concentrate contracted for 5 years

Deposit funded pro-rata with other sources of capital

Completion test at 90% level

Minimum gold delivery after 27 months from first draw at 80% of plan until completion

50

Secured by a lien on the Prosperity property

Prosperity Gold StreamAsset ProfileAsset Profile

Parameter Metric

P&P Recoverable Reserves(1) 3.6 Blb Cu7.7 Moz Au

MI&I Resources 5.3 Blb Cu13.3 Moz Au

Avg. Annual Gold Production First five years (2)

Life-of-mine294 koz Au, 122Mlb Cu247 koz Au 108Mlb CuLife-of-mine 247 koz Au, 108Mlb Cu

Cash costs net of byproducts(3)

First five years (2)

Life-of-mine$0.28/lb$0.59/lb

(1) The mineral resources and reserve estimates set forth above have been taken from the technical report entitled "Technical Report on the 344 Million Tonne Increase in Mineral Reserves at the Prosperity Gold-Copper Project, British Columbia, Canada" dated December 17, 2009 filed (with an effective date of November 2, 2009) by Taseko on SEDAR

51

and completed by Taseko staff under the supervision of Scott Jones, P. Eng., Vice-President, Engineering of Taseko and a qualified person under National Instrument 43-101. The technical report contains detailed information with respect to resource and reserve quantities and grades; key assumptions, parameters and methods used in preparing the resource and reserve estimates; and the extent to which the resources and reserves may be materially affected by any known environmental, permitting, legal, title, taxation, socio-political, marketing or other relevant issues. Mr. Jones has reviewed and approved the information set forth above.

(2) First year is half year(3) $1.65/lb Cu and $650/oz Au, C$/US$ of $0.82 as per Taseko January 2010 Presentation.

Prosperity Gold StreamDevelopment StatusDevelopment Status

BC environmental assessment certificate issued January 2010

Federal environmental assessment process expected to be complete – Q3 2010*

Following permitting, expect two and a half years of construction and commissioning

52

commissioning

* Taseko May 12th, 2010 Press Release

Prosperity Gold StreamProduction ProfileProduction Profile

180200350

120140160180

200

250

300

C

406080100

50

100

150

old

(Koz

)C

opper (Mlb)

020

0

50

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33

Go

Long mine life

Au in Conc. Production Profile (Koz) FNV Gold Stream (Koz) Cu in Conc. Production Profile (Mlb)

53

Long mine lifeSource: Based on Mine Production Profile in Taseko Technical Report dated November 2, 2009. Current environmental approval applications are for a mine plan with a 20 year mine life.

Prosperity Gold StreamA t Q litAsset Quality

1st 5 Yrs$0 28/lb

LOM$0.59/lb

$0.28/lb

Low total operating costs net of byproducts

54

(1) First year of the five years is a half year(2) By-product cost calculated assuming $1.65/lb Cu and $650/oz Au, C$/US$ of $0.82(3) Costs are shown before impact of gold stream. Stream at 22% adds ~ $0.24/lb at $650/oz Au for the first five years.

Source: Taseko Technical Report dated November 2, 2009, Taseko January 2010 Presentation

Prosperity Gold StreamContribution Analysis

95%

100%

Contribution Analysis

11.1%15.8% 17.6%

14.1%

85%

90%

95%

utio

n (%

)

88.9%84 2% 85.9%

75%

80%

ativ

e C

ontr

ibu

ProsperityFNV

84.2% 82.4%85.9%

60%

65%

70%Rel

a

60%EV 2014 Revenue 2014 CF NAV

Prosperity contribution is highly accretive

55

Note: Revenue and CF for estimates for FNV for 2014 are assumed to be the same as the BMO research revenue and CF estimate for 2013 at $925/oz Au. Revenue and CF for Prosperity are based on $925/oz for 2014 (first full year of payments). EV is based on May 6, 2010 closing price for FNV. NPV estimate for FNV and Prosperity is based on analyst consensus estimates. The long term average consensus price used for gold is $860/oz.

Prosperity Gold StreamPotential UpsidePotential Upside

Gold resource of 13.3Moz* is approx 20% larger thanapprox. 20% larger than current reserve

Change in mill configuration may increase throughput currently planned >70,000 tpd

Exploration potential on the p p85km2 concession

56

* See Taseko Technical Report dated November 2, 2009 for Assumptions

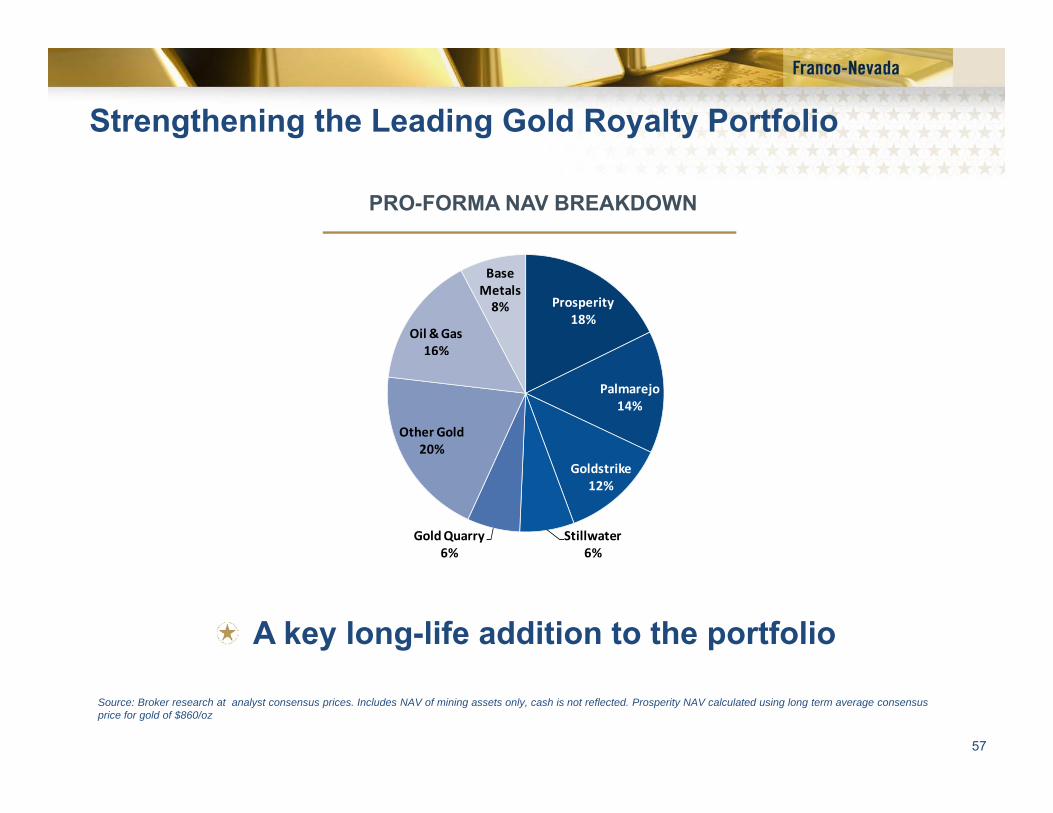

Strengthening the Leading Gold Royalty Portfolio

PRO-FORMA NAV BREAKDOWN

Prosperity18%

Oil & Gas16%

Base Metals8%

Palmarejo14%

Other Gold20%

Goldstrike12%

Stillwater6%

Gold Quarry6%

A key long-life addition to the portfolio

57

Source: Broker research at analyst consensus prices. Includes NAV of mining assets only, cash is not reflected. Prosperity NAV calculated using long term average consensus price for gold of $860/oz

Increasing Precious Metals Exposure

2010E Revenue 2014E Revenue

Oil & Gas

Base Metal5% Oil &

Gas

Base Metal2%

Oil & Gas18% 10%

Precious Metal80%

Precious Metal85%

Pro-forma revenue 85% precious metals

58

Estimates using current prices of $1,100/oz Au, $78/bbl oil, $4.00/mcf gas, $1,650/oz Pt & $500/oz Pd . 2014 revenue estimate includes Prosperity.

Geopolitical Stability

2010E Revenue 2014E Revenue

Australia3%

Other4% Australia

3% Other10%

Canada21%

Mexico21%

Canada38%Mexico

15%

10%

US US

Prosperity increases revenue from Canada

51% 34%

59

Franco-Nevada estimates using current prices of $1,100/oz Au, $78/bbl oil, $4.00/mcf gas, $1,650/oz Pt & $500/oz Pd. 2014 revenue estimate includes Prosperity.

y

Substantial Long Term Gold GrowthGold only royalty revenues excluding other revenues (1)Gold only royalty revenues excluding other revenues (1)

Prosperity $44-48m

Hemlo $5-15mD t 12 13

$100.5m Palmarejo $16-19mHolloway-Hislop 4-5mHollister 3-5mOther 1 2m

Tasiast $10-11mHolt 3-4mMarigold 1-4mDuketon 2-3mIty 1m

Detour 12-13mAhafo 6-11mRosemont 1-2mGoldfields 1-2mPerama Hill 2-3m

$70.7m Other 1-2m

2008A 2009A 2010/11E 2011/12E 2012/14E

$ (1)

60

~$150m in potential new gold Royalty Revenues(1) by 2014(1) Royalty Revenue is defined by the Company as cash received or receivable from operating royalty assets earned during the period. Appendix provides detail to pro-forma

estimates assuming $1,100/oz gold.

Increased Gold Price Leverage

Existing gold leverage: 1.3:1

– NPI's (Goldstrike NPI, Interlake NPI)NPI s (Goldstrike NPI, Interlake NPI)

– Scaled Royalties (Holloway, Holt)

– Gold Streams (Palmarejo)

Prosperity stream gold leverage: 1.6:1

Gold Price RevenueProsperity Revenue @ 1,100/oz $45.4MProsperity Revenue @ 1,210/oz $52.5MPercentage Change 10.0% +15.7%

Additional gold price optionality:

Resources convert to reserves

* Revenue estimate based on first full year of production in 2014 per Taseko mine plan.

61

– Resources convert to reserves

– Developers raise capital to advance properties with existing royalties

Current Capital Resources Untouched

Franco-Nevada expects to generate sufficient funds from operations to fund its commitment without using current capital resourcesto fund its commitment without using current capital resources

Capital Resources @ March 31, 2010 US$ Millions

Working Capital $598

Marketable Investments (Primarily NEM) $52

A ailable Credit Facilit $175Available Credit Facility $175

Total Available Capital $825

>$800 million remains available for other transactionsPortfolio continues to generate strong free cash flow

62

Summary

Accretive acquisition on all metrics

Long life asset in Canada with proven operator and exploration upside

fFNV funds only as project is de-risked

22% of 13.3 million ounces* of gold

63

* See Taseko Technical Report dated November 2, 2009 for Assumptions

Summary

David Harquail – CEOa d a qua C O

64

Franco-Nevada’s two year performance

Dec. 2007 IPO of new Franco-Nevada for $1.26B (C$15.20/sh.)

In two years Franco-Nevada has delivered:In two years, Franco-Nevada has delivered:

– $250M of Free Cash Flow(1)

– 80% share price increase – $50M in dividends– 300 royalty interests– $600M in liquidity FNV vs S&P/TSX since IPO FNV S&P

– $3B in market cap

150%

200%

250%FNV vs S&P/TSX since IPO FNV S&P

50%

100%

65

0%

(1) Free Cash Flow is defined by the Company as operating income plus depletion and depreciation, non-cash charges, and any impairment of investments and royalty interests.

Dividends paid to date

C$/sh US$ millions

June 2008 $0.12$21.8m

Dec 2008 $0 12Dec. 2008 $0.12

June 2009 $0.14$28 2m$28.2m

Dec. 2009 $0.14

$50 million in dividends paid to date

66

Indicated Dividends for 2010**

Final semi-annual dividend to be paid in June followed by start of monthly dividends in Julymonthly dividends in July

C$/share US$

June 2010 $0.150$July $0.025

August $0.025September $0.025October $0.025November $0.025December $0 025December $0.025

$0.30 $34 million*

Three years of growing annual dividends

67

** September to December dividends subject to board declaration* Based on C$=$US and 114m shares outstanding.

Three years of growing annual dividends

Franco-Nevada’s Advantages

Royalty Business Model

rike

Established Diversified Portfolio

89% Cash Flow Margins

Gol

dstr

% g

Most Available Capital

No Debt or Hedges ldQ

uarr

y

No Debt or Hedges

Strong Organic Growth Profile

$30M f A l I di t d Di id d oG

o

>$30M of Annual Indicated Dividends

Track Record of Value Accretion Palm

arej

o

68

Thank You

Bald Mountain ‐ BarrickGoldstrike ‐ Barrick East Boulder ‐ StillwaterWeyburn ‐ Cenovus

Cerro San Pedro ‐ New Gold Mesquite – New GoldPalmarejo ‐ Coeur

Marigold ‐ Goldcorp

Robinson ‐ Quadra Tasiast ‐ Red BackMarigold ‐ Goldcorp

69

Appendices

70

Appendix - Table of Contents

Accounting Definitions for FCF & Adjusted Net Income

Derivative Accounting for PalmarejoDerivative Accounting for Palmarejo

Book Values

Income Taxes

– Tax Depletion and Tax Balances

– Applicable Statutory Tax Rates

C t d E & I t t ECosts and Expenses & Interest Expense

Capital Structure

Liquidity & Capital Resourcesq y p

Security of Investments

Gold Growth Profile - Asset Details

71

Oil & Gas Assets

Appendix - Free Cash Flow

Free Cash Flow is defined by the Company as operating income plus depletion and depreciation non cash chargesincome plus depletion and depreciation, non-cash charges, and any impairment of investments and royalty interests.

Q1 2010 Q1 2009

(millions) (millions)

Operating income $11 7 $4 7Operating income $11.7 $4.7

Depletion and depreciation 20.2 23.0

Stock-based compensation expense 1.1 0.9Loss/gain in fair value of royalties accounted for as derivative assets 4.1 (3.7)

Free Cash Flow $37.1 $24.9

72

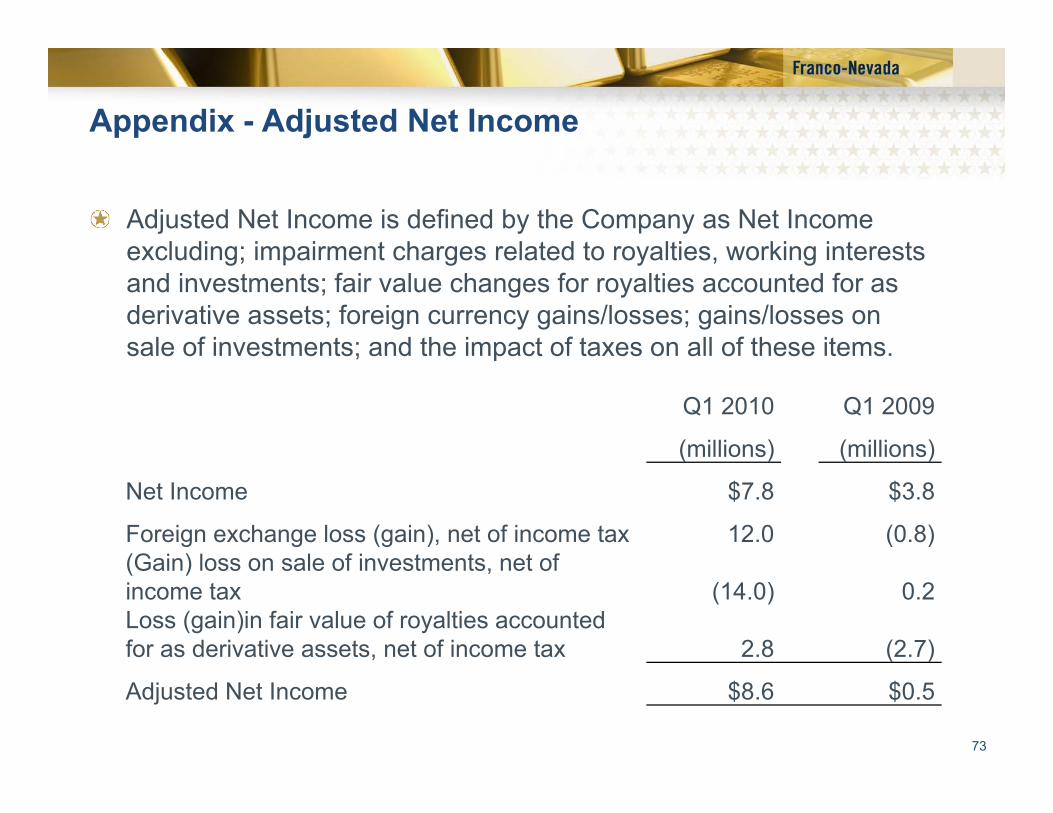

Appendix - Adjusted Net Income

Adjusted Net Income is defined by the Company as Net Income excluding; impairment charges related to royalties working interestsexcluding; impairment charges related to royalties, working interests and investments; fair value changes for royalties accounted for as derivative assets; foreign currency gains/losses; gains/losses on sale of investments; and the impact of taxes on all of these items.sale of investments; and the impact of taxes on all of these items.

Q1 2010 Q1 2009

(millions) (millions)( ) ( )

Net Income $7.8 $3.8

Foreign exchange loss (gain), net of income tax 12.0 (0.8)(Gain) loss on sale of investments net of(Gain) loss on sale of investments, net of income tax (14.0) 0.2Loss (gain)in fair value of royalties accounted for as derivative assets, net of income tax 2.8 (2.7)

73

Adjusted Net Income $8.6 $0.5

Appendix - Palmarejo Gold Stream Accounting

Accounting Treatment

– Minimum Royalty (“MR”)• Fair value accounting required to be used;• MR will be marked to fair value at each balance sheet date;;• Adjustments in fair value recognized in income as a separate

income statement caption;• Separate depletion charge not recorded as inherent in fair value

calculation.

– Non-MR Portion • Standard royalty accounting appliesStandard royalty accounting applies

Contingent consideration– Special warrants exercisable, for no additional consideration, into

74

316,436 FNV shares when project meets certain time-based completion tests

Appendix - Palmarejo Gold Stream Accounting

Fair Value of Palmarejo MR is sensitive to changes in key assumptions (discount rate, gold prices, project parameters);

Generates significant non-cash variations to total revenue and earnings, which will be recognized quarter by quarter.

$30

$40

$50

)

Palmarejo Royalty Revenue Versus Total Revenue

$0

$10

$20

$30

Millions (SU$

Royalty Revenue

Fair Value

Total Revenue

-$10

$0

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010

75

Further reinforces our belief that Royalty Revenue & Free Cash Flow are the most effective metrics to measure our business

Appendix - Net Book ValuesAt December 31 2009At December 31, 2009

ProducingExploration

& DevelopmentGold

Barrick Goldstrike 183$ $ - Barrick Goldstrike 183$ $Bald Mountain 17 - Gold Quarry 94 - Palmarejo 135 - Marigold 24 - Other 78 125Other 78 125

531$ 125$ PGMsStillwater $ 210 $ - Pandora 19

$ 229 $ $ 229 $ - Other MineralsRobinson $ 9 - Falcondo 29 - Other 6 29

$ 44 $ 29 $ 44 $ 29 Oil and GasEdson $ 125 $ - Weyburn 58 - Midale 17 -

76

Other 68 123 $ 268 $ 123

TOTAL $ 1,072 $ 277 $ 1,349

Note, figures are in millions of dollars.

Appendix - Income TaxesTax Depletion and Balances at December 31 2009Tax Depletion and Balances at December 31, 2009

Canada– Canadian oil & gas: 10% declining balance - C$155mCanadian oil & gas: 10% declining balance C$155m– Canadian mining: 30% declining balance - C$10m– Foreign assets: lesser of income or 30% declining balance - C$54m

US– Generally uses cost depletion on a units-of-production basis - US$620m

Australia– May use financial statement depletion – units-of-production basis - US$29m

Mexico– Can be claimed at up to 15% straight line - US$75m

77

Appendix - Income TaxesApplicable Statutory Tax Rates (At March 31 2010)Applicable Statutory Tax Rates (At March 31, 2010)

Canadian combined(1) income tax rates declining

– 2010 – 28.34%

– 2011 – 26.29%

2012 24 %– 2012 – 24.57%

– 2013 – 24.24%

US combined(1) income tax rate is 37 12%(2)US combined( ) income tax rate is 37.12%( )

Australian income tax rate is 30%

Mexican income tax rate in 2010 is 30%Mexican income tax rate in 2010 is 30%

78

(1) Combined is federal plus provincial or state tax. (2) Effective rate after deduction for state tax in federal tax calculation

Appendix - Costs and Expenses

Total $6.6 million (For the year ended December 31, 2009)

Nevada Net Proceeds Taxes 52%Oil & Gas Production Taxes 22%Oil & Gas Operating Costs on WI 17%

Expense components

Oil & Gas Operating Costs on WI 17%Montana Net Proceeds Taxes 9%

pe se co po e ts

– Standby fee for Credit Facility ~ $250,000 per quarter @ current leverage ratio

– Amortization of credit facility expenses – Total cost of $2.1 million being amortized over 3 years on a straight-line basis

– Capital tax eliminated in July 2010 (2009 - $1.1 million)

79

p y ( )

Appendix - Liquidity & Capital Resources

Full Credit facility of $175 million available Total Liquidity of $621.5 million at March 31, 2010

Current cost of advances

– – BMO Prime Rate plus 0.125%

,

– – BMO Base Rate plus 0.125%

Subject to 0.5625% standby fee on

Short-term investments

28%

Cash and cashj y

undrawn balances ($985k/year) Available-for-sale

securities8%

cash equivalents

64%

80

Appendix - Organic Gold Growth Potential

Project Operator Royalty

Annual Incremental Royalty Potential

@ $1100 gold

Palmarejo Coeur d’Alene 50% stream $16-19m

2010

a a ejo Coeu d e e 50% st ea $ 6 9Holloway–Hislop St Andrew Gold 4-6% NSR 4-5m Hollister Great Basin Gold 3-5% NSR 3-5m Hemlo NSR Barrick Gold 3% NSR 1-2m $24-31m

2011

Tasiast Red Back Mining 2% NSR $10-11m Holt St Andrew Gold 10% NSR 3-4m Marigold Goldcorp 1.4-4% NSR 1-4m Duketon Regis Resources 2% NSR 2-3m Ity La Mancha 1-1.5% NSR 1mIty La Mancha 1 1.5% NSR 1m $17-23m

Hemlo NPI Barrick Gold 50% NPI $5-15m Detour Detour Gold 2% NSR 12-13m Ahafo Newmont 2% NSR 6-11m

2012+ Rosemont Augusta Resources 1.5% NSR 1-2m Goldfields Linear Gold 2% NSR 1-2m Perama Hill Eldorado Gold 2% NSR 2-3m $27-46m

Management ‘s projection of start of royalty

81

Management s projection of start of royalty. Applicable royalty rate at $1,100 gold for sliding scale royalties.Reflects operators’ public guidance as of December 2009.Reflects management’s projections based on available data for production and costs (where applicable).2009 was a half year of production. 2010 is increment for full year.Gold only. With copper & silver, royalty potential is $7-9m.

Appendix - Edson (Alberta)

Liquids-rich gas play 209 km. west of Edmontonof Edmonton

15% ORR over 25,920 gross acres

AECO-C spot prices less GCA i tprocessing cost

Wells drilled at no cost to Franco-Nevada

RLI: 7 years

Operator:

82

Appendix - Weyburn/Midale Units (Saskatchewan)

MidaleWeyburnUnitUnit

83

Appendix - Weyburn Unit (Saskatchewan)

Unitized oil play 129 km. southeast of Regina

Medium sour crude (28 to 31 degree API, 2% sulphur)

1.11% non-operated working interest, 0.44% royalty

C$10 t C$15/bbl diff ti l t Ed t Li ht iC$10 to C$15/bbl differential to Edmonton Light price

CO2 miscible flood started in 2000 (>15 million tonnes sequestered to date)

CO2 flood rolled out to ~60% of unit

CO2 flood and infill drilling has increased production 65%

RLI: 22 years

Operator: Cenovus Energy Inc.

84

Appendix - Midale Unit (Saskatchewan)

Unitized oil play 40 km southeast of Weyburn

( % )Medium sour crude (28 to 31 degree API, 2% sulphur)

1.59% non-operated working interest, 1.18% royalty

C$10 to C$15/bbl differential to Edmonton Light priceC$10 to C$15/bbl differential to Edmonton Light price

CO2 injection began in 2005, over 10 patterns operating, 41 patterns by 2010

CO2 injection over next 20 years to assist in recovery of an additional 45-60 mmbbl (1.2-1.5 mmbbl net to FN)

Potential to sequester ~ 8.75 million tonnes of CO2

RLI: 16 years

Operator:

85

Appendix - Exploration

Non-producing land– 12,000 net acres of unproved non

producing land under lease

– Interests in 184 non producing agreements which include ~100,000 gross acres of undeveloped mineral title,gross acres of undeveloped mineral title, available for farm out

Arctic Gas– Discovered by Panarctic Oils between

1969 and 1986

– > 130 wells drilled at cost of ~C$254 millionWI between 3% and 15%– WI between 3% and 15%

– Contingent recoverable resource of 428 bcf (net)

– Economic models based on production

86

of 1 bcf/d over 20 years

Franco-Nevada CorporationCapital Structure(2)

Shares Outstanding 114.02m

Warrants @ C$32/sh March 2012 5.75m

Analyst Coverage

BMO Capital Markets David Haughton

BOA/Merrill Lynch Mike Jalonen

Warrants @ C$75/sh June 2017 5.75m

Options (Avg C$16.00/sh) 2.43m

Other 0.43m

128 38m

CIBC Capital Markets Cosmos Chiu

GMP Securities Craig West

National Bank Financial Tanya Jakusconek128.38m

Share Price Range(1) C$32.12-C$23.10

Market Capitalization(2) $3.3B

Working Capital + Marketable (3) $650 3m

Paradigm Capital Don MacLean

RBC Capital Markets Stephen Walker

UBS Securities Brian MacArthur

Wellington West Paolo LostrittoInvestments(3) $650.3m

Available Credit Facilities $175m

Debt or Hedges Nil

2010 Dividends (Indicative) (4) $34.21m

Wellington West Paolo Lostritto

Major ShareholdersFidelity US

I T i k C d2010 Dividends (Indicative) $34.21m (C$0.30/share)

Management Ownership (3) 5.0%(6.3% diluted)

Invesco Trimark Canada

T. Rowe Price US

Blackrock Europe

Oppenheimer US

87

(1) Previous 52 weeks(2) As at April 30, 2010(3) As at March 31, 2010 (4) @ $CAN/$US = 1.00