analysis of sources of finances for indian railways and futureroadmap

TRANSCRIPT

Analysis of Source of Finances for the Indian

Railways [Document subtitle]

ABSTRACTThisbriefpaperbudgetsthetotalfundsthatIRFChasallocatedtotheIndianRailways,analysesitherecentadventofroleofPublicPrivatePartnership,suggestsmechanismstobuildregulatoryoversightandtransparencyinfunding.SudikshaJoshi-Intern,IndianRailwaysFinanceCorporation(IRFC)

Analysis of Source of Finances for the Indian Railways

A Glimpse of the Indian Railways Finance Corporation

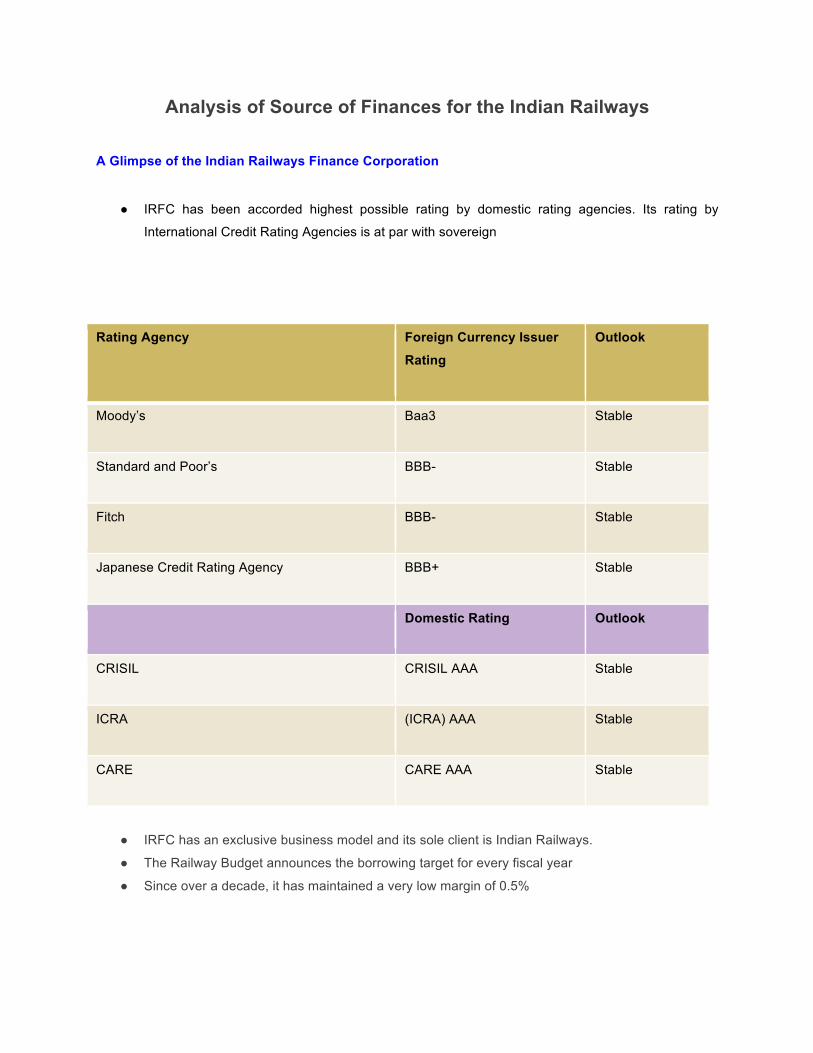

● IRFC has been accorded highest possible rating by domestic rating agencies. Its rating by

International Credit Rating Agencies is at par with sovereign

Rating Agency Foreign Currency Issuer Rating

Outlook

Moody’s Baa3 Stable

Standard and Poor’s BBB- Stable

Fitch BBB- Stable

Japanese Credit Rating Agency BBB+ Stable

Domestic Rating Outlook

CRISIL CRISIL AAA Stable

ICRA (ICRA) AAA Stable

CARE CARE AAA Stable

● IRFC has an exclusive business model and its sole client is Indian Railways.

● The Railway Budget announces the borrowing target for every fiscal year

● Since over a decade, it has maintained a very low margin of 0.5%

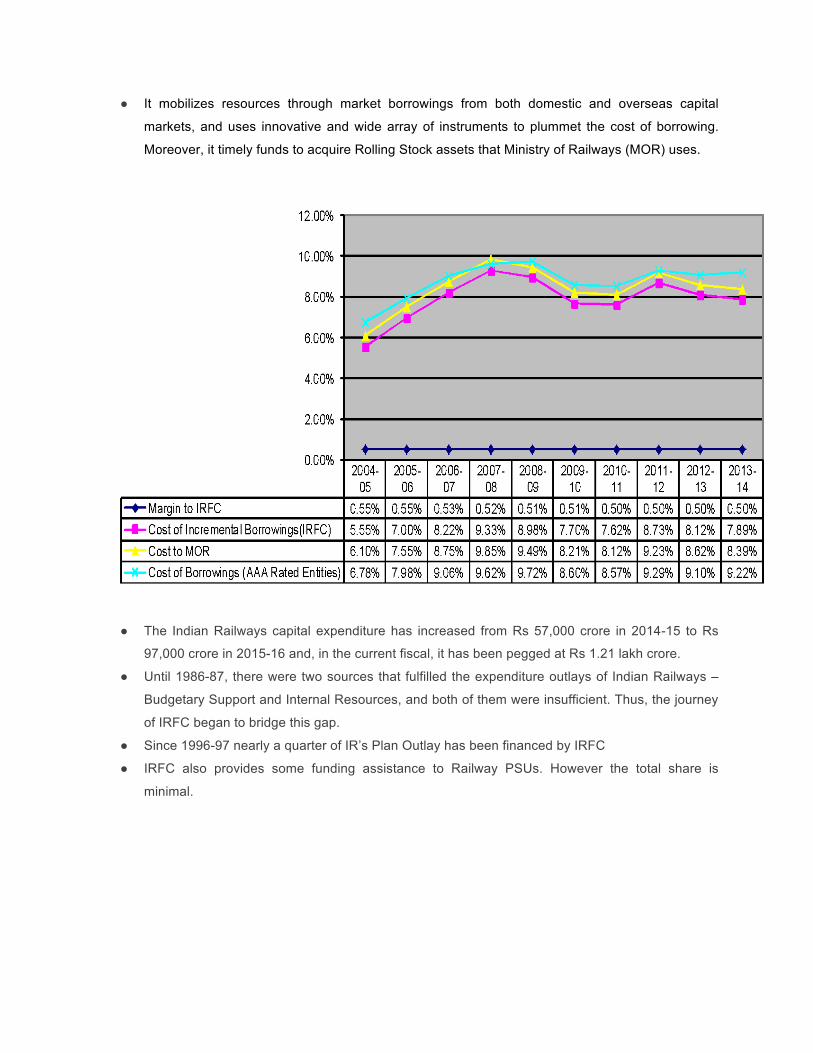

● It mobilizes resources through market borrowings from both domestic and overseas capital

markets, and uses innovative and wide array of instruments to plummet the cost of borrowing.

Moreover, it timely funds to acquire Rolling Stock assets that Ministry of Railways (MOR) uses.

● The Indian Railways capital expenditure has increased from Rs 57,000 crore in 2014-15 to Rs

97,000 crore in 2015-16 and, in the current fiscal, it has been pegged at Rs 1.21 lakh crore.

● Until 1986-87, there were two sources that fulfilled the expenditure outlays of Indian Railways –

Budgetary Support and Internal Resources, and both of them were insufficient. Thus, the journey

of IRFC began to bridge this gap.

● Since 1996-97 nearly a quarter of IR’s Plan Outlay has been financed by IRFC

● IRFC also provides some funding assistance to Railway PSUs. However the total share is

minimal.

Railway’s allocation of funds from: Outlay of the 12th Plan of Indian Railways

• In the 11th Plan period (2007-’08 to 2011-’12) Ministry of Railways had allocated Rs. 190,610 crore,

which was 2.7 times greater in nominal terms. Furthermore, MoR has pegged the Gross Budgetary

Support at a higher figure than that mentioned in the 11th Plan Outlay.

Railway’s Allocation of Funds to: Investment Plan (2015-2019)

Item Amount (Rs. Billion)

Network Decongestion 1993.20

Network Expansion 1930.00

National Projects (N.E. & Kashmir connectivity projects) 390.00

Safety 1270.00

Information Technology / Research 50.00

Rolling Stock 1020.00

Passenger Amenities 125.00

High Speed Rail & Elevated corridor 650.00

Station redevelopment and logistic parks 1000.00

Others 132.00

Total 8560.20

Total Plan Outlay of IR during the year 1996-97 to 2014-15 : Rs. 5,00,959 crore

Funding by IRFC during the period 1996-97 to 2013-14 : Rs. 1,20,179 crore

Share of IRFC in Total Plan Outlay : 24% The graph above shows the total outlay of the plan of Indian Railways and IRFC’s shares.

Public Private Partnership in Railways

The Indian Railways are in the forefront of encouraging Public-Private Partnership to enhance and

modernize the infrastructure. These are long term projects which are contracted between the

Government or statutory entity on one side and a private sector company on the other side, to deliver

efficient infrastructural services in compensation of payment. For this, a private sector consortium forms a

special company called a special purpose vehicle (SPV) to build and maintain the asset.

Core functions of PPP: ● CONTRACT SIGNING: The consortium is usually made up of a building contractor, a

maintenance company and a bank lender. The SPV signs the contract with the government and

with subcontractors to build the facility and then maintain it.

● RISK SHARING: Both the government and private agencies have to bear risks.The PPPs

incorporate a risk mitigation framework that apportions risk in terms of capacity to bear. The risk

mitigation framework is addressed through a bankable concession agreement that clearly

delineates project risks and responsibilities.

Types of PPP

There are numerous PPP Models that can be adopted. Few of these are Maintenance Management

Contract, Turnkey, Operate and management, ROT and BOT. BOT is the most preferred model for PPP

in IR. Below are 8 PPP Models which Indian Railways uses:

PPP MODELS USES

Lease/ Service Agreement Catering, Yatri Niwas Parcel, upgradation of

toilets, retiring rooms, advertising

SPV/ JV Port links suburbans

BOT Annuity, and BOT Capacity Augmentation Projects, Doubling, Gauge

Conversion, Railway Electrification etc

BOLT Annuity, and BOLT New Railway Network Freight Corridor

License Tourist trains

BOOT/BOO Multi model logistics, Budget hotels. Food plazas

Current PPP Projects under Implementation Phase

● The Indian Railways have undertaken more than 20 projects worth Rs 14,000 crore during the

12th Five year Plan, including those for laying new lines, doubling the existing ones, enhancing

port connectivity and electrifying its network under PPP model.

● While seven PPP projects worth Rs 5693 crore are under implementation as part of joint venture

model, as many others involving an expenditure of Rs 2236 crore are being implemented under

customer funded model.

● Three PPP projects worth Rs 3016 crore are being executed through the annuity route and in-

principle approval has been accorded to six others worth Rs 3078 crore.

● Indian Railway has proposed Rs 8.56 lakh crore investment plan for the next five years and the

national transporter expects to execute a sizable chunk of projects through Public-Private

Partnership and in collaboration with states.

● There are about 16 state governments which have given their in-principle approval for formation

of special purpose vehicles (SPVs) to implement rail projects in their respective states

Participative Models: Rail Connectivity and Capacity Augmentation Projects

The new policy of participative Models addresses the concerns of private investors, which included

ownership of the railway line and repayment of investment. This policy has renewed the interest of the

investors in the rail sector, which is compatible with Government’s 12th FYP, wherein, it intends to raise

investments worth USD14.8 billion through PPP route.

The targeted areas for influx of private investment are- elevated rail corridor in Mumbai, some parts of

dedicated freight corridor, freight terminals, redevelopment of stations and power generation/energy

saving projects.

Under the PPP route, approval has been granted for seven ports amounting to USD0.7 billion.

Development of the major stations to equip them with international level of amenities and services is also

being implemented through PPP. In addition, the MoR proposed to set up five wagon factories under the

JV/PPP model. For FY14, the Rail budget proposes to mobilize USD1.1 billion through the PPP route.

Investment Environment

The High Level Committee on Infrastructure Financing projects an investment of Rs. 3.4 lakhs crores,

including 13% share of the private sector. MoR has also proposed development of 50 world-class stations

in PPP mode to improve and enhance rail infrastructure in the country.

The Indian Railways has attracted increasing foreign investments through strategic alliances with various

countries over the last few years. Subsidiaries of foreign companies are being set up to cater to the huge

demand offered by IR. Since FY08, the cumulative FDI inflows into the sector has increased five-fold.

From April 2000 to November 2014, FDI in Railways related components stood at USD 634.1 million.

Some of the other areas where PPPs have participated: ● Operation of container trains and Construction of Private sidings, ICDs and railside warehouses

● Construction of Dedicated Freight Corridor (Delhi-Mumbai and Delhi Howrah) with a large

component of PPP

● High Speed Corridors

● World Class Railway Stations, Passenger amenities and Commercial utilization of land

● Pipavav Railway Corporation Limited

● K-RIDE

● The Wagon Investment Scheme

● Setting up of SPV for manufacturing of locomotives/coaches/wagons

● Parcel Services

Scope of Enforcement

Nodal Directorates and the Zonal Railways have to identify and execute the projects. They are inform the

PPP Cell and seek their advice to develop the projects coherently and synergistically. Then the PPP cell

ensures that the Nodal Directorates effectively shape the outline of the projects.

Infrastructure Debt Fund (IDF)

The Infrastructure Debt Funds (IDFs) are funds given to accelerate and enhance the flow of long term

debt in infrastructure projects. To attract offshore funds into IDFs, taxes are withheld on interest payments

on the IDF’s borrowings, from 20% to 5%. Income of the IDFs has also been exempt from income tax.

Structure and Processes involved in setting up of IDF

● IDFs are assembled as a Trust or as a Company. Typically, mutual funds (MF) regulated by SEBI

would categorise as a trust, while NBFC, regulated by RBI, would categorise as a company.

● Banks and NBFCs sponsor IDF-MFs. Alternatively, only banks and Infrastructure Finance

companies can sponsor IDF-NBFCs. “Sponsorship” implies that the equity participation by the

NBFC between 30 to 49% of the IDF.

● To sponsor IDFs, NBFCs and NBFC-IFCs have to previously get consent from the RBI

● IDF-NBFCs can accumulate resources by either issuing Dollar and Rupee denominated bonds of

at least five years maturity, or by issuing mutual funds.

Capitalization of IDF

The funds from IDF will be used for: ● high-speed rail connectivity

● station redevelopment and

● capacity augmentation across the country.

Railways is drawing concrete plans for investment of about Rs 8.5 lakh crore in the coming four years for

modernisation of rail infrastructure. MoR has bilateral agreements with 13 countries to cooperate in the

rail sector. Railways. For example, it has already signed a Rs 97,636 crore deal with Japan for the

Mumbai-Ahmedabad high-speed rail project. Besides that, Indian Railway is planning to link all metros

with high-speed trains as part of its Diamond Quadrilateral project which requires huge private funding.

Mobilizing additional funds from the overseas markets:

● LOW COST FUNDS: Railways can mobilize low cost long term funds from the overseas markets

by issuing bonds to the Sovereign Wealth Funds, Pension Funds and Insurance Companies. This

is a viable funding option that meets massive fund requirements of the Indian Railways.

● SET UP A SEPARATE FINANCIAL DEPARTMENT: To meet the other extensive financial

requirements of Railways, the IRFC can establish a small financial department within its umbrella

organisation. Its parameters are:

1. This new department could be called as Rail Infrastructure Finance Company.

2. The overarching responsibility would be to adequately safeguard risks and provide equity support

to mitigate the problems of financial gearing.

3. It can use the same business model that IRFC had used for its maiden project funding in FY

2011-12.

4. Alternatively, it can use the Sale and Leaseback Model to mitigate the risks of the projects fully

while being competitive in borrowing terms in the market. This would mitigate the project risks

completely and keep intact the borrowing competitiveness of IRFC.

● IRFC will issue bonds in the offshore or foreign capital market (issue of Samurai Bonds in

Japanese Capital Market or Yankee Bonds in the US Capital market) to fund the sale and

leaseback transaction. The bonds may be targeted at Sovereign Wealth Funds, Pension Funds

and Issuance Funds which provide low cost funding for longer tenors suitable for high gestation

Railway Projects.

● IRFC will raise All-in-Dollar Cost funds, and the MoR’s funds will be no more than 50 bps,

supposing that IRFC and Indian Railways have absolutely mitigated the exchange rate risk The

funding to MOR may be kept at 50 bps over the All-in-Dollar Cost of funds raised by IRFC

● CORPUS WITH IRFC: MoR will transfer a fixed proportion (for instance 1%) of the total loan

amount that IRFC will deposit in approved banks or invest in safely securitized instruments.

1. This corpus will be used to cover the excess outgo on account of exchange rate variation at the

time of repayment of the bonds.

2. In case of excess accretion to the funds, the same would be transferred back to MoR when

resources are scarce.

3. MoR will also intervene in the off-the-market dollar swaps that RBI does with domestic banks with

currency depreciates at the peak, as it occurred in the fiscal year 2013-’14.

4. RBI would purchase funds mobilized by IRFC at their reference rate on the date of drawdown

and will sell dollars to IRFC at 1% interest rate p.a. over the drawdown rate. Thus, MoR will

deliver the 1% additional cost of premium for hedging.

Proposed Additional Funding from World Bank

The World Bank (WB) and the Indian Railways would work together to create a Railways of India

Development Fund. Its features and coal initiatives are as following: ● Finance the $142-billion investment plans for the core infrastructure sector t

● Awaiting approval, the initial target size of the Railways of India Development Fund (RIDF) is $5

billion, which will be operational in 2017.

● World Bank would finance $500 million to redevelop 400 railway stations across the nation in

collaboration with Public Private Partnership. Thus, IFC could help Railways monetize its

immense assets.

● The development fund will also be accessible for the entire rail sector including private firms such

as concessionaires, container and siding operators, among others.

● It will attract commercial finance for financially viable railway infrastructure projects in India.

● It will provide capital lease financing for assets that are operationally integrated within the Indian

Railways and will invest in debt and equity of PPPs (public-private-partnerships) and SPVs

(special purpose vehicles) in the rail sector.

The World Bank is also working on an individual project with the Indian Railways wherein it is investing

$650 million to finance the Eastern Dedicated Freight Corridor as a direct loan. The Indian railways plans

to invest Rs. 8.5 trillion in the next five years with a total capital for infrastructure for current financial year

set at Rs.1.21 trillion.

Future Roadmap: What lies ahead?

● Robust models emerge from PPP negotiations: Railways can excavate the evolution,

expediency and efficiency of tasks equipped by PPP models in India.

● Headstrong political mandate glimmers superior infrastructure: An increased allocation to

infrastructure (mainly roads), measures to reduce risk for the private sector and ease funding

challenges, reflect strong intent.

● Spotlight is speed: The focus on speed rather than the historical solution of throwing more

rolling stock on the burdened tracks is a game-changer.

● Explore ingenious funding options: Indian Railways is seeking diverse array of funds such as-

$25bn of funding from LIC (Life Insurance Corporation of India), land monetization and bond

issuance on the cards. These curtail the complications posed by the constrained Indian banking

sector.