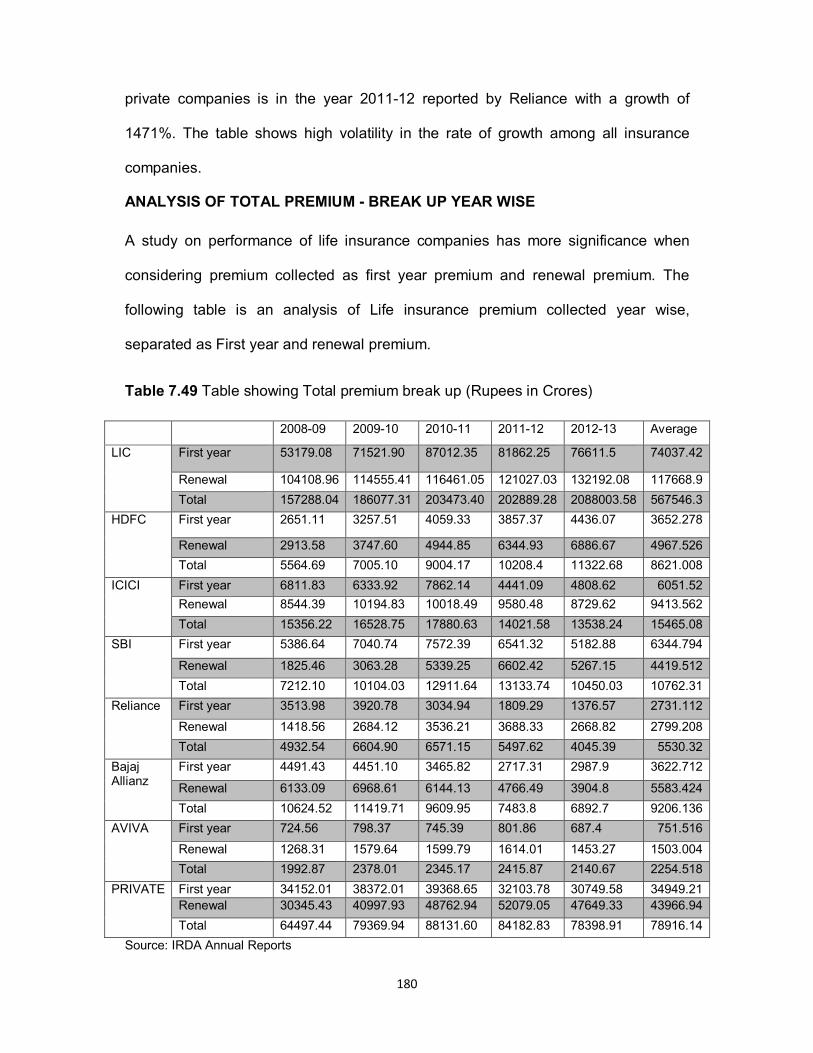

an analysis of performance of private sector life...

TRANSCRIPT

133

AN ANALYSIS OF PERFORMANCE OF PRIVATE SECTOR LIFE INSURANCE

COMPANIES VIS A VIS PUBLIC SECTOR LIFE INSURANCE COMPANIES

An in depth analysis of the various parameters of performance for a Life Insurance

Company were identified and the data was subjected to analysis with the help of

ratios, correlation technique and percentage analysis. The various findings have

been as follows.

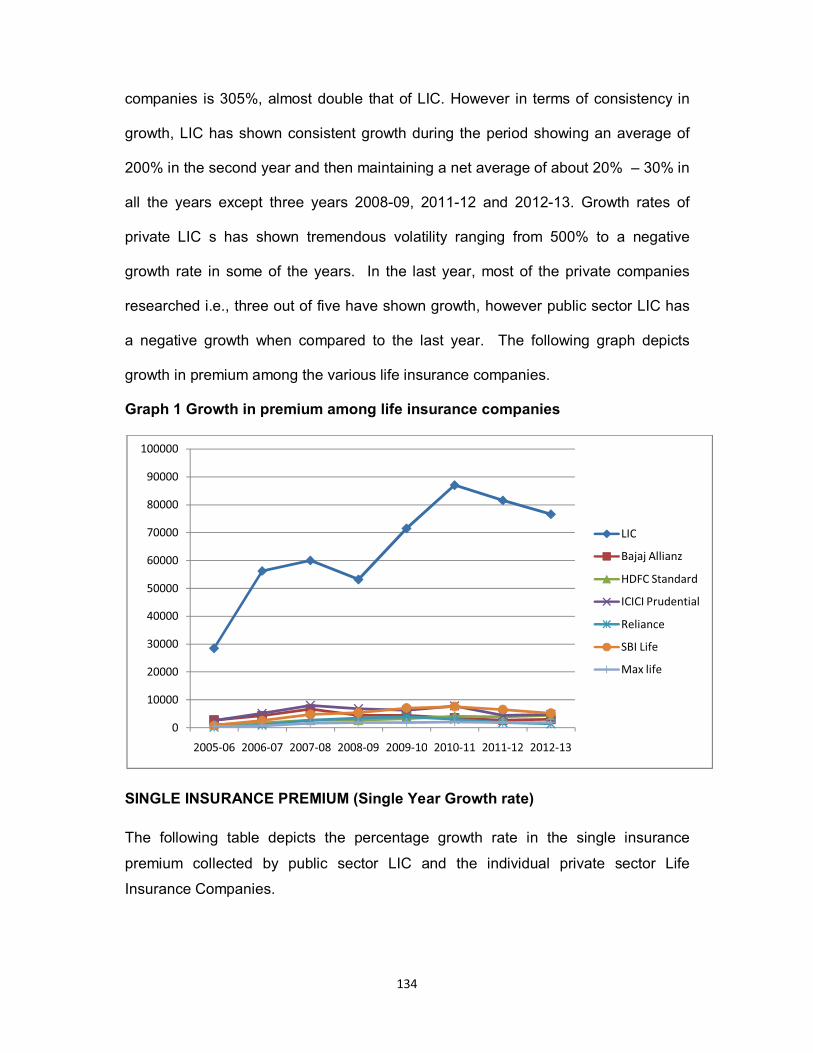

SINGLE INSURANCE PREMIUM: Premium collected by Life insurance companies

on individual lives is the single most important factor that determines the success

and performance of a life insurance company. Insurance is a product that is not

bought but is sold. The following table depicts the amount of premium collected in

Crores of rupees by the various life insurance companies, public and private.

Table 7.1Table showing amount of premium in Crores of rupees

INSURER 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

LIC 28515.87

56222.56 59996.57 53179.08 71521.90 87021.13 81562.13 76611.50

Bajaj Allianz

2716.77

4301.27 6674.48

4451.10 4451.1 3465.82 2717.31 2987.9

HDFC Standard

1042.65

1648.85 2685.37 2651.11 3257.51 4059.33 3857.47 4436.37

ICICI Prudential

2602.5

5162.13 8034.75 6811.83 6333.92 7862.14 4441.09 4808.02

Reliance 193.56

932.11 2751.05 3513.98 3920.78 3034.94 1809.29 1376.57

SBI Life 827.82

2563.84 4782.94 5386.64 7040.74 7589.58 6531.32 5182.8

Max life 471.36

712.11 1597.83 1842.91 1849.09 2061.39 1901.72 1899.34

Source: Company Annual Reports

The table above clearly shows that the overall growth rate of LIC from the year 2005

up to 2012 has increased by 168%. However the growth rate of HDFC during the

same period is 325%. ICICI Prudential has shown a growth rate of 84%, SBI Life

has shown a phenomenal growth rate of 500%. Reliance has increased by 611%

Bajaj Allianz has shown a growth of 146% within two years, however the growth

subsequently fell to 10% only by 2012-13. Max Life has shown a growth of 300%

during the same period. The average growth of the 6 private life insurance

134

companies is 305%, almost double that of LIC. However in terms of consistency in

growth, LIC has shown consistent growth during the period showing an average of

200% in the second year and then maintaining a net average of about 20% – 30% in

all the years except three years 2008-09, 2011-12 and 2012-13. Growth rates of

private LIC s has shown tremendous volatility ranging from 500% to a negative

growth rate in some of the years. In the last year, most of the private companies

researched i.e., three out of five have shown growth, however public sector LIC has

a negative growth when compared to the last year. The following graph depicts

growth in premium among the various life insurance companies.

Graph 1 Growth in premium among life insurance companies

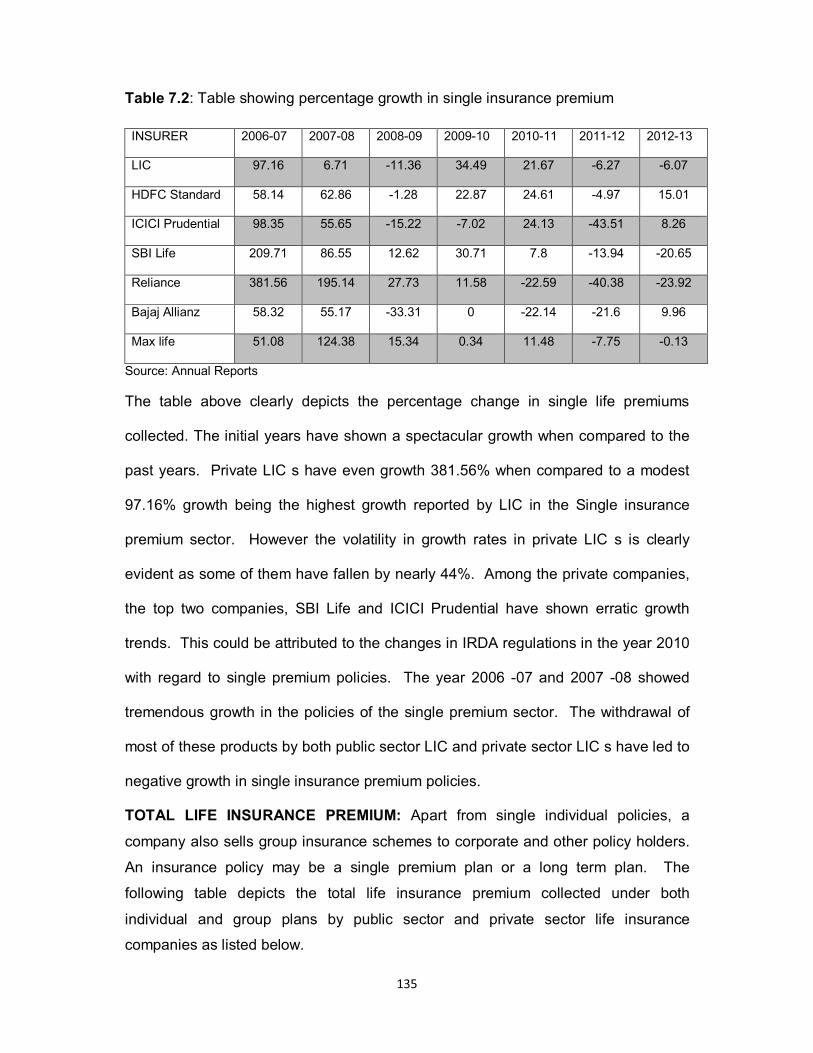

SINGLE INSURANCE PREMIUM (Single Year Growth rate)

The following table depicts the percentage growth rate in the single insurance

premium collected by public sector LIC and the individual private sector Life

Insurance Companies.

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

LIC

Bajaj Allianz

HDFC Standard

ICICI Prudential

Reliance

SBI Life

Max life

135

Table 7.2: Table showing percentage growth in single insurance premium

INSURER 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

LIC 97.16

6.71 -11.36 34.49 21.67 -6.27 -6.07

HDFC Standard 58.14

62.86 -1.28 22.87 24.61 -4.97 15.01

ICICI Prudential 98.35

55.65 -15.22 -7.02 24.13 -43.51 8.26

SBI Life 209.71

86.55 12.62 30.71 7.8 -13.94 -20.65

Reliance 381.56

195.14 27.73 11.58 -22.59 -40.38 -23.92

Bajaj Allianz 58.32

55.17 -33.31 0 -22.14 -21.6 9.96

Max life 51.08

124.38 15.34 0.34 11.48 -7.75 -0.13

Source: Annual Reports

The table above clearly depicts the percentage change in single life premiums

collected. The initial years have shown a spectacular growth when compared to the

past years. Private LIC s have even growth 381.56% when compared to a modest

97.16% growth being the highest growth reported by LIC in the Single insurance

premium sector. However the volatility in growth rates in private LIC s is clearly

evident as some of them have fallen by nearly 44%. Among the private companies,

the top two companies, SBI Life and ICICI Prudential have shown erratic growth

trends. This could be attributed to the changes in IRDA regulations in the year 2010

with regard to single premium policies. The year 2006 -07 and 2007 -08 showed

tremendous growth in the policies of the single premium sector. The withdrawal of

most of these products by both public sector LIC and private sector LIC s have led to

negative growth in single insurance premium policies.

TOTAL LIFE INSURANCE PREMIUM: Apart from single individual policies, a

company also sells group insurance schemes to corporate and other policy holders.

An insurance policy may be a single premium plan or a long term plan. The

following table depicts the total life insurance premium collected under both

individual and group plans by public sector and private sector life insurance

companies as listed below.

136

Table 7.3 Total Life Insurance premium collected (Rs. In Crores)

Source: IRDA Annual Reports

INSURER 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

LIC 90792.22

127822.84 149789.99 157288.04 186077.31 203473.31 202889.28 208830.58

HDFC Standard

1569.91

2855.87 4858.58 5564.69 7005.10 9004.17 10202.40 11322.68

ICICI Prudential

4261.05

7912.99 13561.08 15385.22 16528.75 17880.63 14021.58 13538.24

SBI Life 1075.32

2928.49 5622.14 7212.10 10104.03 12945.29 13133.74 10450.03

Reliance 224.21

1004.66 3225.44 4932.54 6604.90 6571.15 5497.62 4057.39

Bajaj Allianz

3133.58

5345.24 9725.31 10624.52 11419.71 9609.95 1483.8 6892.7

Max life 788.13

1500.28 2714.60 3857.26 4860.54 6812.63 6390.53 6638.70

The table above clearly shows that the overall growth rate of LIC from the year 2005

up to 2012 has increased by 130%. However the growth rate of HDFC during the

same period is 621.23%. ICICI Prudential has shown a growth rate of 200%, SBI

Life has shown a phenomenal growth rate of 800%. Reliance has increased by a

whopping 1709%, Bajaj Allianz has shown a modest growth of 119% by 2012-13.

Max Life has shown a growth of 700% during the same period. The average growth

of the 6 private life insurance companies is 690%, five times that of LIC.

However in terms of consistency in growth, LIC has shown consistent growth during

the period showing an average of 200% in the second year and then maintaining a

net average of about 20% – 30% in all the years except three years 2008-09, 2011-

12 and 2012-13.Growth rates of private LIC s has shown tremendous volatility

ranging from 1709% to a negative growth rate in some of the years. In the last year,

most of the private companies researched i.e, three out of five have shown negative

growth, however public sector LIC has a positive growth when compared to the last

year.

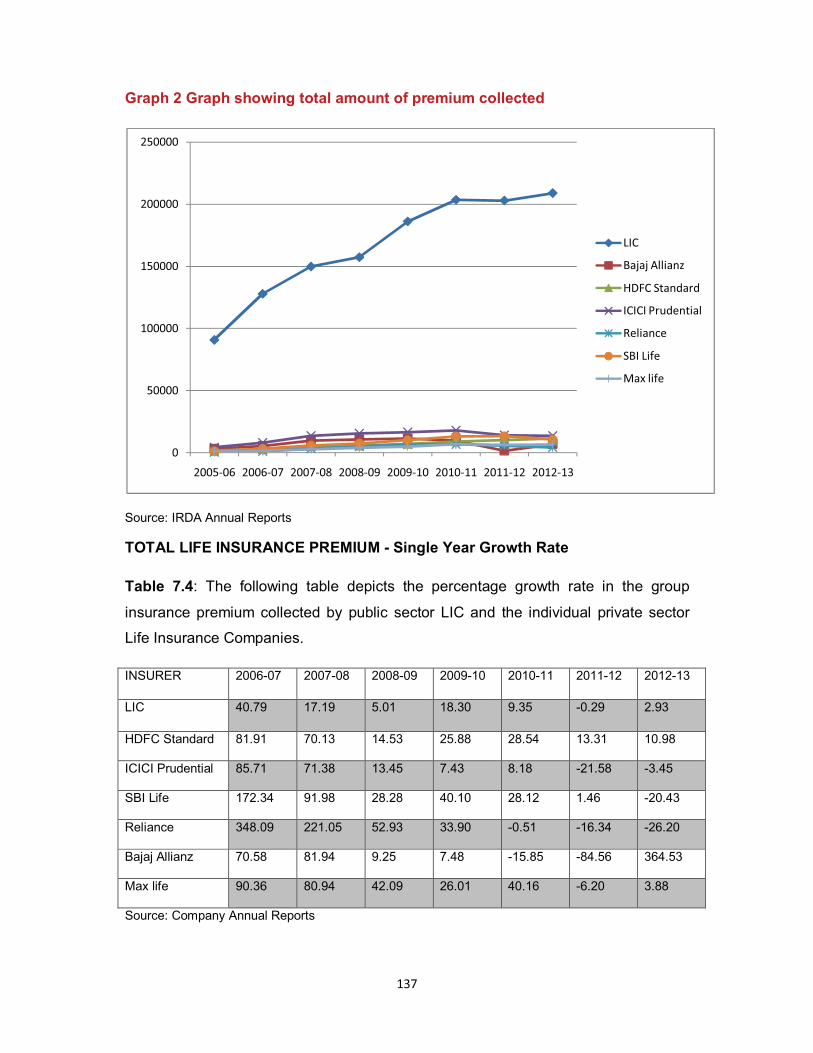

The following graph shows the total amount of premium in crores of rupees

137

Graph 2 Graph showing total amount of premium collected

Source: IRDA Annual Reports

TOTAL LIFE INSURANCE PREMIUM - Single Year Growth Rate

Table 7.4: The following table depicts the percentage growth rate in the group

insurance premium collected by public sector LIC and the individual private sector

Life Insurance Companies.

INSURER 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

LIC 40.79

17.19 5.01 18.30 9.35 -0.29 2.93

HDFC Standard 81.91

70.13 14.53 25.88 28.54 13.31 10.98

ICICI Prudential 85.71

71.38 13.45 7.43 8.18 -21.58 -3.45

SBI Life 172.34

91.98 28.28 40.10 28.12 1.46 -20.43

Reliance 348.09

221.05 52.93 33.90 -0.51 -16.34 -26.20

Bajaj Allianz 70.58

81.94 9.25 7.48 -15.85 -84.56 364.53

Max life 90.36

80.94 42.09 26.01 40.16 -6.20 3.88

Source: Company Annual Reports

0

50000

100000

150000

200000

250000

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

LIC

Bajaj Allianz

HDFC Standard

ICICI Prudential

Reliance

SBI Life

Max life

138

The table above clearly depicts the percentage change in total life premiums

collected. The initial years have shown a spectacular growth when compared to the

past years. Private LIC s have even growth 348.09% when compared to a modest

40.79% growth being the highest growth reported by LIC in the Single insurance

premium sector. However the volatility in growth rates in private LIC s is clearly

evident as some of them have fallen by nearly 84%. Among the private companies,

the top two companies, SBI Life and ICICI Prudential have shown erratic growth

trends. This could be attributed to the changes in IRDA regulations in the year 2010

with regard to unit linked policies. The year 2006 -07 and 2007 -08 showed

tremendous growth in the policies. The withdrawal of most of the unit linked

products by both public sector LIC and private sector LIC s have led to negative

growth in total life insurance premium.

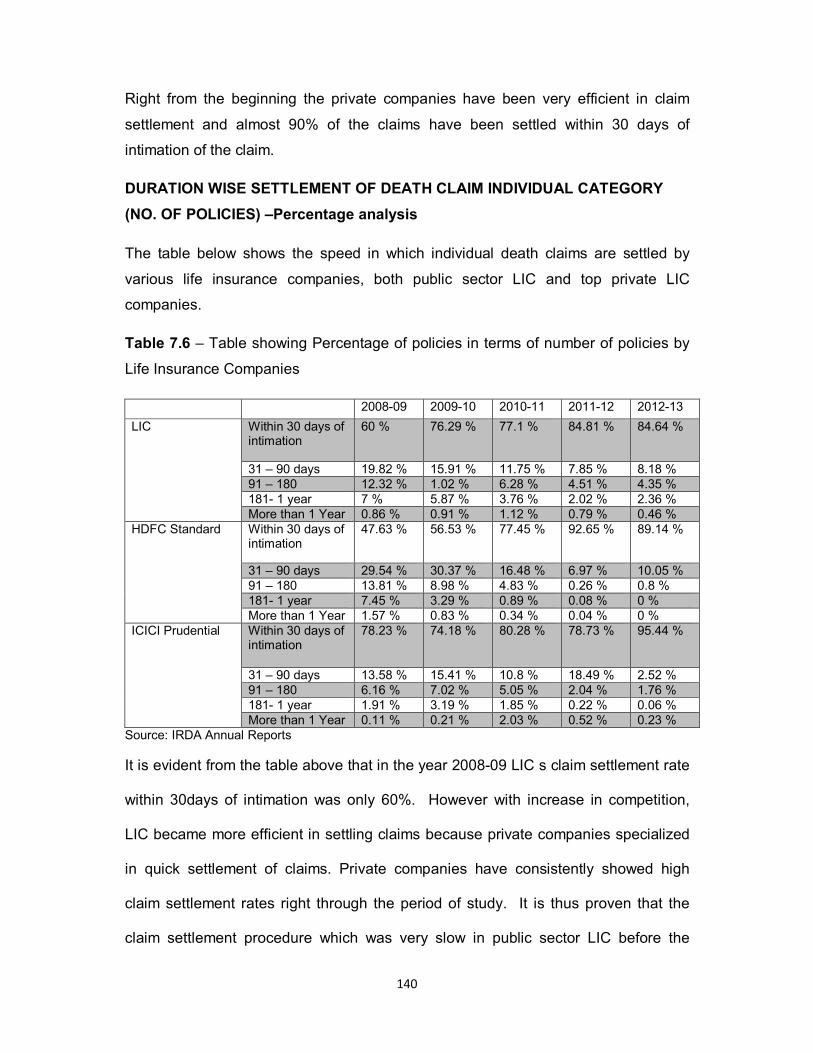

SETTLEMENT OF DEATH CLAIM: The time taken for settlement of death claims is

also an important determinant of the client relationship strategies and settlement of

maturity and death claims go a long way in building up the image of the company.

The average time taken by an insurance company is about six months. However the

earlier the claim is settled and fewer the claims repudiated increases customer

retention and loyalty for the insurance company.

The following table depicts the number of individual claims settled and an analysis of

the time taken to settle death claims in different Companies

Table 7.5 Duration wise settlement of Death Claim Individual Category in terms of

Number of policies

2008-09 2009-10 2010-11 2011-12 2012-13

LIC Within 30 days of intimation

338629 457655 553197 604303 620881

31 – 90 days 111874 95463 84312 55957 60040 91 – 180 69544 6148 45041 32160 31873 181- 1 year 39502 35203 26944 14417 17345 More than 1 4840 5440 8025 5664 3406

139

Year Bajaj Allianz Within 30 days

of intimation 5550 7567 15469 17656 17635

31 – 90 days 3863 9524 6717 6083 5175 91 – 180 889 2964 1388 840 1376 181- 1 year 127 215 345 43 6 More than 1 Year

55 46 61 36 -

HDFC Standard Within 30 days of intimation

1214 1977 3384 4588 5338

31 – 90 days 753 1062 720 345 602 91 – 180 352 314 211 13 48 181- 1 year 190 115 39 4 - More than 1 Year

40 29 15 2 -

ICICI Prudential Within 30 days of intimation

7274 10740 12170 11270 13736

31 – 90 days 1263 2231 1637 2646 362 91 – 180 573 1016 765 292 253 181- 1 year 178 462 280 32 9 More than 1 Year

10 30 308 74 33

Reliance Within 30 days of intimation

3073 6779 10326 10574 13221

31 – 90 days 73 681 2685 6387 4731 91 – 180 30 72 229 387 540 181- 1 year 13 58 5 10 14 More than 1 Year

15 17 9 9 5

SBI Life Within 30 days of intimation

1765 4205 6572 10450 11217

31 – 90 days 965 1443 1528 839 1379 91 – 180 404 294 139 20 71 181- 1 year 108 45 8 10 7 More than 1 Year

20 35 2 9 2

Aviva Within 30 days of intimation

681 1474 1614 1669 1825

31 – 90 days 185 115 219 235 283

91 – 180 102 23 32 33 23

181- 1 year 41 13 16 13 -

More than 1 Year

23 10 25 56 3

Private total Within 30 days of intimation

23308 43368 70246 81949 90182

31 – 90 days 11679 20234 19753 23144 18595

91 – 180 4107 7130 4715 3564 4076

181- 1 year 1290 1254 1117 644 360

More than 1 Year

355 214 572 464 171

Source: IRDA Annual Reports

In the study period of five years LIC s individual claims have increased to 200% and

those of private companies have increased almost five times in all the companies.

140

Right from the beginning the private companies have been very efficient in claim

settlement and almost 90% of the claims have been settled within 30 days of

intimation of the claim.

DURATION WISE SETTLEMENT OF DEATH CLAIM INDIVIDUAL CATEGORY

(NO. OF POLICIES) –Percentage analysis

The table below shows the speed in which individual death claims are settled by

various life insurance companies, both public sector LIC and top private LIC

companies.

Table 7.6 – Table showing Percentage of policies in terms of number of policies by

Life Insurance Companies

2008-09 2009-10 2010-11 2011-12 2012-13

LIC Within 30 days of intimation

60 % 76.29 % 77.1 % 84.81 % 84.64 %

31 – 90 days 19.82 % 15.91 % 11.75 % 7.85 % 8.18 % 91 – 180 12.32 % 1.02 % 6.28 % 4.51 % 4.35 % 181- 1 year 7 % 5.87 % 3.76 % 2.02 % 2.36 % More than 1 Year 0.86 % 0.91 % 1.12 % 0.79 % 0.46 %

HDFC Standard Within 30 days of intimation

47.63 % 56.53 % 77.45 % 92.65 % 89.14 %

31 – 90 days 29.54 % 30.37 % 16.48 % 6.97 % 10.05 % 91 – 180 13.81 % 8.98 % 4.83 % 0.26 % 0.8 % 181- 1 year 7.45 % 3.29 % 0.89 % 0.08 % 0 % More than 1 Year 1.57 % 0.83 % 0.34 % 0.04 % 0 %

ICICI Prudential Within 30 days of intimation

78.23 % 74.18 % 80.28 % 78.73 % 95.44 %

31 – 90 days 13.58 % 15.41 % 10.8 % 18.49 % 2.52 % 91 – 180 6.16 % 7.02 % 5.05 % 2.04 % 1.76 % 181- 1 year 1.91 % 3.19 % 1.85 % 0.22 % 0.06 % More than 1 Year 0.11 % 0.21 % 2.03 % 0.52 % 0.23 %

Source: IRDA Annual Reports

It is evident from the table above that in the year 2008-09 LIC s claim settlement rate

within 30days of intimation was only 60%. However with increase in competition,

LIC became more efficient in settling claims because private companies specialized

in quick settlement of claims. Private companies have consistently showed high

claim settlement rates right through the period of study. It is thus proven that the

claim settlement procedure which was very slow in public sector LIC before the

141

advent of private life insurance companies has now improved due to loss of

monopoly position of LIC. The table below is the continuation of the analysis of the

other private insurance companies’ duration of settlement of claims from the date of

intimation.

Table 7.7 Table showing Percentage of policies in terms of number of policies by

Life Insurance Companies

2008-09 2009-10 2010-11 2011-12 2012-13

SBI Life Within 30 days of intimation

54.11 % 69.83 % 79.67 % 92.25 % 88.49 %

31 – 90 days 29.58 % 23.96 % 18.52 % 7.41 % 10.88 %

91 – 180 12.39 % 4.88 % 1.69 % 0.18 % 0.56 %

181- 1 year 3.31 % 0.75 % 0.1 % 0.09 % 0.06 %

More than 1 Year 0.61 % 0.58 % 0.02 % 0.08 % 0.02 %

Reliance Within 30 days of intimation

95.91 % 89.12 % 77.91 % 60.89 % 71.42 %

31 – 90 days 2.28 % 8.95 % 20.26 % 36.78 % 25.56 %

91 – 180 0.94 % 0.95 % 1.73 % 2.23 % 2.92 %

181- 1 year 0.41 % 0.76 % 0.04 % 0.06 % 0.08 %

More than 1 Year 0.47 % 0.22 % 0.07 % 0.05 % 0.03 %

Bajaj Allianz Within 30 days of intimation

52.94 % 37.25 % 64.51 % 71.6 % 72.9 %

31 – 90 days 36.85 % 46.88 % 28.01 % 24.67 % 21.39 %

91 – 180 8.48 % 14.59 % 5.79 % 3.41 % 5.69 %

181- 1 year 1.21 % 1.06 % 1.44 % 0.17 % 0.02 %

More than 1 Year 0.52 % 0.23 % 0.25 % 0.15 % 0 %

Aviva Within 30 days of intimation

65.99 % 90.15 % 84.68 % 83.2 % 85.52 %

31 – 90 days 17.93 % 7.03 % 11.49 % 11.71 % 13.26 %

91 – 180 9.88 % 1.41 % 1.68 % 1.65 % 1.08 %

181- 1 year 3.97 % 0.8 % 0.84 % 0.65 % 0 %

More than 1 Year 2.23 % 0.61 % 1.31 % 2.79 % 0.14 %

Private total Within 30 days of intimation

57.21 % 60.07 % 72.87 % 74.66 % 79.54 %

31 – 90 days 28.67 % 28.02 % 20.49 % 21.09 % 16.4 %

91 – 180 10.08 % 9.88 % 4.89 % 3.25 % 3.59 %

181- 1 year 3.17 % 1.74 % 1.16 % 0.59 % 0.32 %

More than 1 Year 0.87 % 0.3 % 0.59 % 0.42 % 0.15 %

Source: IRDA Annual Reports

It is evident from the table above that the overall efficiency of settlement of claims

has consistently increased over the past five years among the private companies.

Companies with faster claim settlement rates have a competitive edge over the other

companies and are thus building goodwill by keeping clients’ interest their top most

142

priority. Quick claim settlement is one of the major determinants in customer

satisfaction and determines the length of client’s association with the Life Insurance

companies and reduces the possibility of termination due to lapse of policy.

SETTLEMENT OF DEATH CLAIM – INDIVIDUAL CATEGORY BENEFIT AMOUNT

PAID (Rs. In Crores)

The following table depicts the benefit amount paid and the duration wise settlement

of death claim. Claims of LIC have increased almost twenty five times in terms of

amount in the past five years. Claims on private sector LIC s have also increased

tremendously over the past five years, ranging from five times in case of ICICI and

Reliance and to ten times in case of the other private life insurance companies over

the past five years.

Table 7.8 Table showing Duration wise settlement of Death claim under Individual

category and the benefit amount paid in Crores of rupees

2008-09 2009-10 2010-11 2011-12 2012-13

LIC Within 30 days of intimation

249.02 3340.12 4708.08 5369.01 5634.86

31 – 90 days 828.03 707.6 709.46 606.99 1102.53 91 – 180 504.84 445.83 378.43 360.50 306.56 181- 1 year 291.49 260.93 228.67 150.69 140.21 More than 1 Year 41.72 40.07 68.5 72.32 38.74

HDFC Standard Within 30 days of intimation

8.88 26.95 48.92 81.10 105.65

31 – 90 days 14.53 20.59 20.38 14.88 34.05 91 – 180 8.15 14.43 8.17 0.77 4.23 181- 1 year 5.1 2.38 1.16 0.10 - More than 1 Year 1.17 1.33 1.95 0.12 -

ICICI Prudential Within 30 days of intimation

63.3 165.25 117.85 159.05 262.87

31 – 90 days 22.3 28.01 31.96 42.75 13.95 91 – 180 12.79 15.56 23.81 8.58 14.70 181- 1 year 3.1 8.34 19.63 0.84 0.19 More than 1 Year 0.20 0.87 8.43 1.63 0.79

SBI Life Within 30 days of intimation

21 54.45 94.9 150.83 166.98

31 – 90 days 16.04 28.51 38.8 24.94 45.25 91 – 180 7.61 7.05 4.58 0.69 4.87 181- 1 year 2.03 1.41 0.27 0.21 0.36 More than 1 Year 0.31 1.02 0.29 0.27 0.07

Reliance Within 30 days of intimation

32.24 62.68 78.90 80.18 119.40

31 – 90 days 1.74 12.85 33.97 84.27 73.15 91 – 180 0.59 2.37 6.15 15 14.78 181- 1 year 0.28 1.56 0.24 34 0.33

143

More than 1 Year 0.21 0.15 0.2 0.27 0.21 Bajaj Allianz Within 30 days of

intimation 80.61 93.22 188.009 228.09 226.75

31 – 90 days 73.86 143.85 103.56 100.90 85.28 91 – 180 17.07 50.87 26.52 24.72 37.17 181- 1 year 2.14 5.88 7.65 1019 0.05 More than 1 Year 0.76 1.10 1.02 0.77 -

Aviva Within 30 days of intimation

14.09 21.83 28.25 32.07 49.79

31 – 90 days 4.43 2.5 5.76 17.22 24.95 91 – 180 2.54 0.43 0.95 2.26 5.16 181- 1 year 0.99 0.24 0.25 0.40 - More than 1 Year 0.33 0.37 0.87 1.46 0.07

Private total Within 30 days of intimation

288.94 599.04 927.48 1223.03 1492.11

31 – 90 days 231.33 372.52 391.6 483.38 487.23 91 – 180 83.69 152.31 126.32 114.98 147.62 181- 1 year 23.81 29.14 40.40 16.40 13 More than 1 Year 5.35 5.57 16.30 55.44 7.36

Source: IRDA Annual Reports

On an average claims of private companies have increased five times the amount

paid in five years. The table given below shows the percentage of amount of death

claims and the duration of their settlement in the category of individual claims.

SETTLEMENT OF DEATH CLAIM – INDIVIDUAL CATEGORY BENEFIT AMOUNT

PAID – Percentage Analysis

The following table depicts the benefit amount paid and the duration wise settlement

of death claim in terms of percentage.

Table 7.9 Table showing Duration wise settlement of Death claim in Individual

category in terms of Benefit paid in percentages

2008-09 2009-10 2010-11 2011-12 2012-13 LIC Within 30 days of

intimation 13 % 69.66 % 77.27 % 81.85 % 78.01 %

31 – 90 days 43.24 % 14.76 % 11.64 % 9.25 % 15.26 % 91 – 180 26.36 % 9.3 % 6.21 % 5.5 % 4.24 % 181- 1 year 15.22 % 5.44 % 3.75 % 2.3 % 1.94 % More than 1 Year 2.18 % 0.84 % 1.12 % 1.1 % 0.54 %

HDFC Standard Within 30 days of intimation

23.47 % 41.03 % 60.71 % 83.63 % 73.4 %

31 – 90 days 38.41 % 31.35 % 25.29 % 15.34 % 23.66 % 91 – 180 21.54 % 21.97 % 10.14 % 0.79 % 2.94 % 181- 1 year 13.48 % 3.62 % 1.44 % 0.1 % 0 % More than 1 Year 3.09 % 2.02 % 2.42 % 0.12 % 0 %

ICICI Prudential Within 30 days of 62.25 % 75.79 % 58.43 % 74.72 % 89.87 %

144

intimation

31 – 90 days 21.93 % 12.85 % 15.85 % 20.08 % 4.77 % 91 – 180 12.58 % 7.14 % 11.81 % 4.03 % 5.03 % 181- 1 year 3.05 % 3.83 % 9.73 % 0.39 % 0.06 % More than 1 Year 0.2 % 0.4 % 4.18 % 0.77 % 0.27 %

SBI Life Within 30 days of intimation

44.69 % 58.9 % 68.35 % 85.24 % 76.76 %

31 – 90 days 34.13 % 30.84 % 27.95 % 14.1 % 20.8 % 91 – 180 16.19 % 7.63 % 3.3 % 0.39 % 2.24 % 181- 1 year 4.32 % 1.53 % 0.19 % 0.12 % 0.17 % More than 1 Year 0.66 % 1.1 % 0.21 % 0.15 % 0.03 %

Reliance Within 30 days of intimation

91.96 % 78.73 % 66.05 % 37.52 % 57.44 %

31 – 90 days 4.96 % 16.14 % 28.44 % 39.43 % 35.19 % 91 – 180 1.68 % 2.98 % 5.15 % 7.02 % 7.11 % 181- 1 year 0.8 % 1.96 % 0.2 % 15.91 % 0.16 % More than 1 Year 0.6 % 0.19 % 0.17 % 0.13 % 0.1 %

Bajaj Allianz Within 30 days of intimation

46.21 % 31.61 % 57.54 % 16.61 % 64.92 %

31 – 90 days 42.34 % 48.78 % 31.69 % 7.35 % 24.42 % 91 – 180 9.79 % 17.25 % 8.12 % 1.8 % 10.64 % 181- 1 year 1.23 % 1.99 % 2.34 % 74.19 % 0.01 % More than 1 Year 0.44 % 0.37 % 0.31 % 0.06 % 0 %

Aviva Within 30 days of intimation

62.96 % 86.05 % 78.3 % 60.04 % 62.26 %

31 – 90 days 19.79 % 9.85 % 15.96 % 32.24 % 31.2 % 91 – 180 11.35 % 1.69 % 2.63 % 4.23 % 6.45 % 181- 1 year 4.42 % 0.95 % 0.69 % 0.75 % 0 % More than 1 Year

1.47 % 1.46 % 2.41 % 2.73 % 0.09 %

Private total Within 30 days of intimation

45.64 % 51.7 % 61.75 % 64.6 % 69.49 %

31 – 90 days 36.54 % 32.15 % 26.07 % 25.53 % 22.69 % 91 – 180 13.22 % 13.15 % 8.41 % 6.07 % 6.87 % 181- 1 year 3.76 % 2.52 % 2.69 % 0.87 % 0.61 % More than 1 Year

0.85 % 0.48 % 1.09 % 2.93 % 0.34 %

Source: IRDA Annual Reports

In the case of LIC, it is evident from the table that five years ago only 13% of the

amount paid out as claims happened within the first thirty days of claim intimation.

However on an average during the same period, nearly fifty percent of the claims of

private life insurance companies were settled within thirty days of intimation. This

percentage gradually and consistently increased to nearly seventy per cent in the

year 2012-2013. LIC shows erratic growth in claim settlement percentages.

145

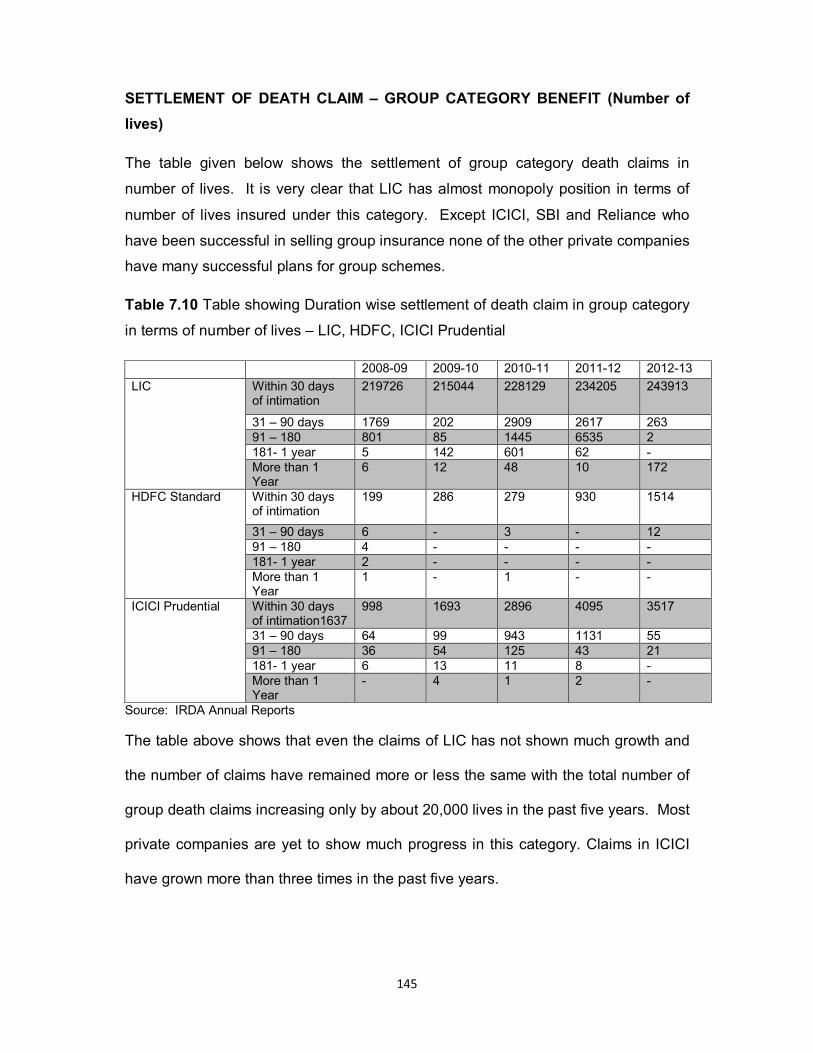

SETTLEMENT OF DEATH CLAIM – GROUP CATEGORY BENEFIT (Number of

lives)

The table given below shows the settlement of group category death claims in

number of lives. It is very clear that LIC has almost monopoly position in terms of

number of lives insured under this category. Except ICICI, SBI and Reliance who

have been successful in selling group insurance none of the other private companies

have many successful plans for group schemes.

Table 7.10 Table showing Duration wise settlement of death claim in group category

in terms of number of lives – LIC, HDFC, ICICI Prudential

2008-09 2009-10 2010-11 2011-12 2012-13

LIC Within 30 days of intimation

219726 215044 228129 234205 243913

31 – 90 days 1769 202 2909 2617 263 91 – 180 801 85 1445 6535 2 181- 1 year 5 142 601 62 - More than 1 Year

6 12 48 10 172

HDFC Standard Within 30 days of intimation

199 286 279 930 1514

31 – 90 days 6 - 3 - 12 91 – 180 4 - - - - 181- 1 year 2 - - - - More than 1 Year

1 - 1 - -

ICICI Prudential Within 30 days of intimation1637

998 1693 2896 4095 3517

31 – 90 days 64 99 943 1131 55 91 – 180 36 54 125 43 21 181- 1 year 6 13 11 8 - More than 1 Year

- 4 1 2 -

Source: IRDA Annual Reports

The table above shows that even the claims of LIC has not shown much growth and

the number of claims have remained more or less the same with the total number of

group death claims increasing only by about 20,000 lives in the past five years. Most

private companies are yet to show much progress in this category. Claims in ICICI

have grown more than three times in the past five years.

146

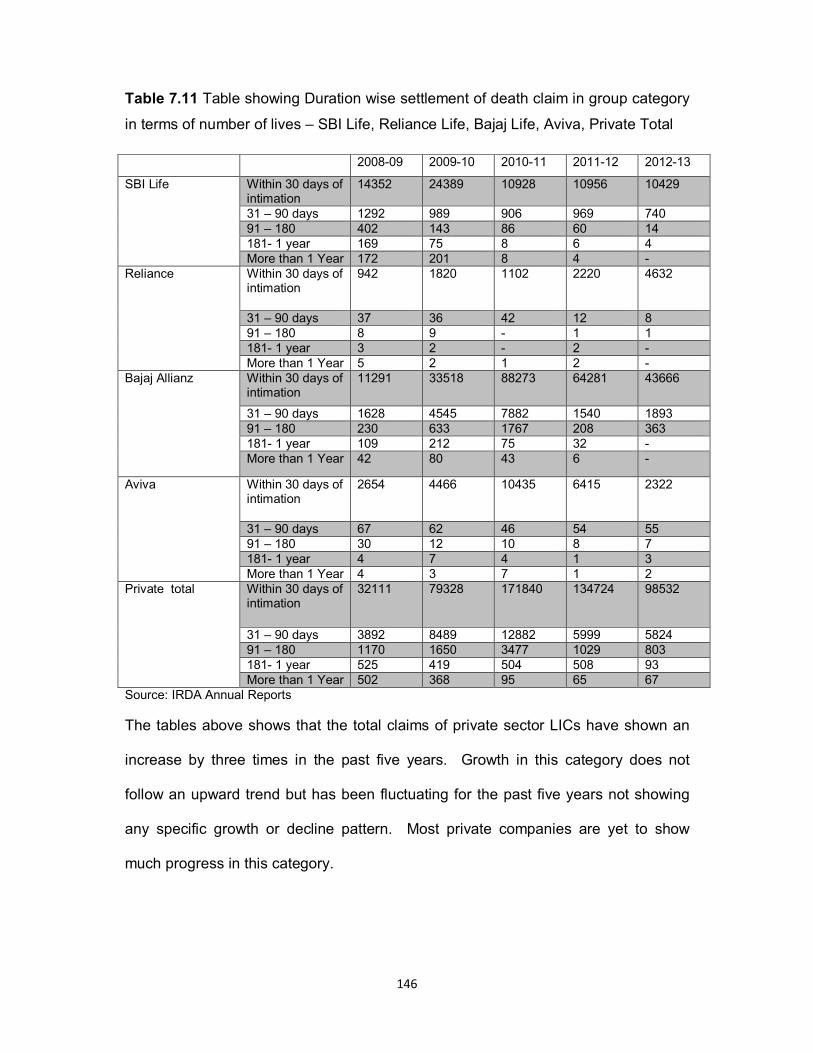

Table 7.11 Table showing Duration wise settlement of death claim in group category

in terms of number of lives – SBI Life, Reliance Life, Bajaj Life, Aviva, Private Total

2008-09 2009-10 2010-11 2011-12 2012-13

SBI Life Within 30 days of intimation

14352 24389 10928 10956 10429

31 – 90 days 1292 989 906 969 740 91 – 180 402 143 86 60 14 181- 1 year 169 75 8 6 4 More than 1 Year 172 201 8 4 -

Reliance Within 30 days of intimation

942 1820 1102 2220 4632

31 – 90 days 37 36 42 12 8 91 – 180 8 9 - 1 1 181- 1 year 3 2 - 2 - More than 1 Year 5 2 1 2 -

Bajaj Allianz Within 30 days of intimation

11291 33518 88273 64281 43666

31 – 90 days 1628 4545 7882 1540 1893 91 – 180 230 633 1767 208 363 181- 1 year 109 212 75 32 - More than 1 Year 42 80 43 6 -

Aviva Within 30 days of intimation

2654 4466 10435 6415 2322

31 – 90 days 67 62 46 54 55 91 – 180 30 12 10 8 7 181- 1 year 4 7 4 1 3 More than 1 Year 4 3 7 1 2

Private total Within 30 days of intimation

32111 79328 171840 134724 98532

31 – 90 days 3892 8489 12882 5999 5824 91 – 180 1170 1650 3477 1029 803 181- 1 year 525 419 504 508 93 More than 1 Year 502 368 95 65 67

Source: IRDA Annual Reports

The tables above shows that the total claims of private sector LICs have shown an

increase by three times in the past five years. Growth in this category does not

follow an upward trend but has been fluctuating for the past five years not showing

any specific growth or decline pattern. Most private companies are yet to show

much progress in this category.

147

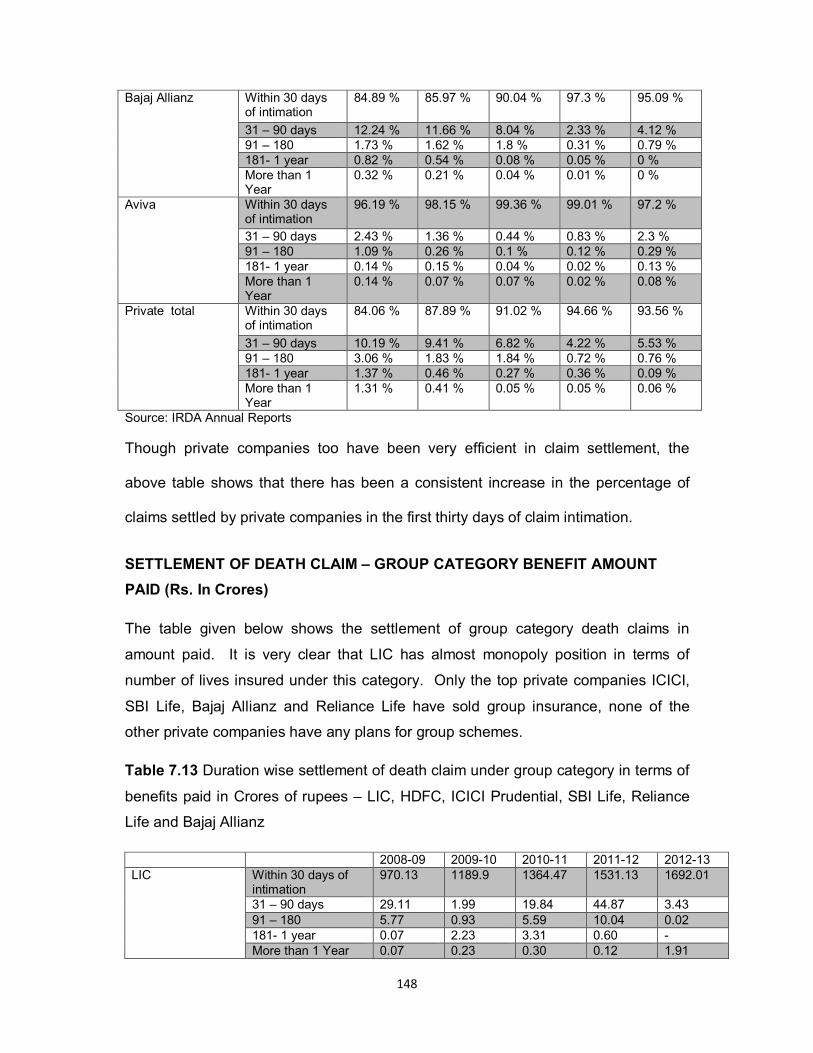

SETTLEMENT OF DEATH CLAIM – GROUP CATEGORY BENEFIT AMOUNT

(number of lives) –Percentage analysis

The table given below the percentage of death claims benefits paid under group

category is clearly depicted. Public sector LIC shows tremendous efficiency in

settlement of group category death claims with nearly hundred percent of the claims

being settled in the first thirty days of intimation. Claim settlement efficiency has

remained constantly good in the case of LIC.

Table 7.12 Duration wise settlement of Death claim under group category on the

basis of number of lives on percentage basis

2008-09 2009-10 2010-11 2011-12 2012-13 LIC Within 30 days

of intimation 98.84 % 99.8 % 97.85 % 96.21 % 99.82 %

31 – 90 days 0.8 % 0.09 % 1.25 % 1.08 % 0.11 % 91 – 180 0.36 % 0.04 % 0.62 % 2.68 % 0 % 181- 1 year 0 % 0.07 % 0.26 % 0.03 % 0 % More than 1 Year

0 % 0.01 % 0.02 % 0 % 0.07 %

HDFC Standard Within 30 days of intimation

93.87 % 100 % 98.59 % 100 % 99.21 %

31 – 90 days 2.83 % 0 % 1.06 % 0 % 0.79 % 91 – 180 1.89 % 0 % 0 % 0 % 0 % 181- 1 year 0.94 % 0 % 0 % 0 % 0 % More than 1 Year

0.47 % 0 % 0.35 % 0 % 0 %

ICICI Prudential Within 30 days of intimation1637

90.4 % 90.87 % 72.84 % 77.57 % 97.88 %

31 – 90 days 5.8 % 5.31 % 23.72 % 21.42 % 1.53 % 91 – 180 3.26 % 2.9 % 3.14 % 0.81 % 0.58 % 181- 1 year 0.54 % 0.7 % 0.28 % 0.15 % 0 % More than 1 Year

0 % 0.21 % 0.03 % 0.04 % 0 %

SBI Life Within 30 days of intimation

87.58 % 94.54 % 91.55 % 91.34 % 93.22 %

31 – 90 days 7.88 % 3.83 % 7.59 % 8.08 % 6.61 % 91 – 180 2.45 % 0.55 % 0.72 % 0.5 % 0.13 % 181- 1 year 1.03 % 0.29 % 0.07 % 0.05 % 0.04 % More than 1 Year

1.05 % 0.78 % 0.07 % 0.03 % 0 %

Reliance Within 30 days of intimation

94.67 % 97.38 % 96.24 % 99.24 % 99.81 %

31 – 90 days 3.72 % 1.93 % 3.67 % 0.54 % 0.17 % 91 – 180 0.8 % 0.48 % 0 % 0.04 % 0.02 % 181- 1 year 0.3 % 0.11 % 0 % 0.09 % 0 % More than 1 Year

0.5 % 0.11 % 0.09 % 0.09 % 0 %

148

Bajaj Allianz Within 30 days of intimation

84.89 % 85.97 % 90.04 % 97.3 % 95.09 %

31 – 90 days 12.24 % 11.66 % 8.04 % 2.33 % 4.12 % 91 – 180 1.73 % 1.62 % 1.8 % 0.31 % 0.79 % 181- 1 year 0.82 % 0.54 % 0.08 % 0.05 % 0 % More than 1 Year

0.32 % 0.21 % 0.04 % 0.01 % 0 %

Aviva Within 30 days of intimation

96.19 % 98.15 % 99.36 % 99.01 % 97.2 %

31 – 90 days 2.43 % 1.36 % 0.44 % 0.83 % 2.3 % 91 – 180 1.09 % 0.26 % 0.1 % 0.12 % 0.29 % 181- 1 year 0.14 % 0.15 % 0.04 % 0.02 % 0.13 % More than 1 Year

0.14 % 0.07 % 0.07 % 0.02 % 0.08 %

Private total Within 30 days of intimation

84.06 % 87.89 % 91.02 % 94.66 % 93.56 %

31 – 90 days 10.19 % 9.41 % 6.82 % 4.22 % 5.53 % 91 – 180 3.06 % 1.83 % 1.84 % 0.72 % 0.76 % 181- 1 year 1.37 % 0.46 % 0.27 % 0.36 % 0.09 % More than 1 Year

1.31 % 0.41 % 0.05 % 0.05 % 0.06 %

Source: IRDA Annual Reports

Though private companies too have been very efficient in claim settlement, the

above table shows that there has been a consistent increase in the percentage of

claims settled by private companies in the first thirty days of claim intimation.

SETTLEMENT OF DEATH CLAIM – GROUP CATEGORY BENEFIT AMOUNT

PAID (Rs. In Crores)

The table given below shows the settlement of group category death claims in

amount paid. It is very clear that LIC has almost monopoly position in terms of

number of lives insured under this category. Only the top private companies ICICI,

SBI Life, Bajaj Allianz and Reliance Life have sold group insurance, none of the

other private companies have any plans for group schemes.

Table 7.13 Duration wise settlement of death claim under group category in terms of

benefits paid in Crores of rupees – LIC, HDFC, ICICI Prudential, SBI Life, Reliance

Life and Bajaj Allianz

2008-09 2009-10 2010-11 2011-12 2012-13 LIC Within 30 days of

intimation 970.13 1189.9 1364.47 1531.13 1692.01

31 – 90 days 29.11 1.99 19.84 44.87 3.43 91 – 180 5.77 0.93 5.59 10.04 0.02 181- 1 year 0.07 2.23 3.31 0.60 - More than 1 Year 0.07 0.23 0.30 0.12 1.91

149

HDFC Standard Within 30 days of intimation

2.22 2.36 2.77 6.44 16.35

31 – 90 days 0.2 - 0.02 - 4.14 91 – 180 0.13 - - - - 181- 1 year 0.12 - - - - More than 1 Year 0.04 - - - -

ICICI Prudential Within 30 days of intimation

17.72 26.51 30.34 42.50 55.33

31 – 90 days 2.91 3.58 11.90 16.40 5.61 91 – 180 1.37 2.4 1.88 0.89 2.05 181- 1 year 0.34 0.55 0.95 0.08 - More than 1 Year - 0.3 - 0.09 -

SBI Life Within 30 days of intimation

111.62 135.74 148.65 171.48 192.02

31 – 90 days 26.26 23.52 24.49 28.43 28.93 91 – 180 6.31 3.72 3.53 3.23 0.93 181- 1 year 3.6 1.35 0.46 0.31 0.30 More than 1 Year 3.87 5.98 1.41 0.91 -

Reliance Within 30 days of intimation

19.59 23.76 24.65 24.63 27.69

31 – 90 days 0.56 1.61 1.71 0.45 0.28 91 – 180 0.27 0.18 0 0.03 0.11 181- 1 year 0.16 0.01 0 0.51 - More than 1 Year 0.1 0.01 0.01 0.01 -

Bajaj Allianz Within 30 days of intimation

37.29 51.65 132.71 138.54 165.02

31 – 90 days 4.67 11.47 14.66 17.10 27.31 91 – 180 1 2.02 2.75 2.50 4.99 181- 1 year 0.5 0.71 0.45 0.13 - More than 1 Year 0.18 0.21 0.16 0.02 -

Source: IRDA Annual Reports

The table above shows that the claims of LIC have shown growth of about 100% in

the last five years. Most private companies are have group claims growth of about

five times in the past five years in terms of amount. Claims in ICICI have grown

more than three times in the past five years.

Table 7.14 Duration wise settlement of death claim under group category in terms of

benefits paid in Crores of rupees – Aviva and Private Total

Aviva Within30 days of intimation

5.7 11.10 25.64 19.52 16.38

31 – 90 days 0.69 0.37 0.1 0.66 1.40 91 – 180 0.06 0.02 0.02 0.44 0.15 181- 1 year 0.02 0.03 0.01 - 0.01 More than 1 Year

0.02 0.01 0.02 0.05 0.05

Private total Within30 days of intimation

227.59 341.29 571.04 668.22 812.12

31 – 90 days 57.86 63.92 74.94 101.58 114.44

150

91 – 180 20.22 18.72 15.30 20.53 21.08 181- 1 year 9.23 5.52 3.30 3.29 1.67 More than 1 Year

7.43 9.63 1.74 1.38 0.37

Source: IRDA Annual Reports

The above table depicts the growth in total claims settled by private companies over

the past five years, the overall amount of claim settled within thirty days having

increased nearly four times in the year 2012-13 when compared to 2008-09

SETTLEMENT OF DEATH CLAIM – GROUP CATEGORY BENEFIT AMOUNT

PAID –Percentage analysis

Table 7.15 Duration wise settlement of death claim under group category in terms of

benefits paid in percentages – LIC, HDFC, ICICI Prudential and SBI Life.

2008-09 2009-10 2010-11 2011-12 2012-13 LIC Within 30 days of

intimation 96.52 % 99.55 % 97.92 % 96.49 % 99.68 %

31 – 90 days 2.9 % 0.17 % 1.42 % 2.83 % 0.2 % 91 – 180 0.57 % 0.08 % 0.4 % 0.63 % 0 %

181- 1 year 0.01 % 0.19 % 0.24 % 0.04 % 0 % More than 1 Year 0.01 % 0.02 % 0.02 % 0.01 % 0.11 %

HDFC Standard Within 30 days of intimation

81.92 % 100 % 99.28 % 100 % 79.8 %

31 – 90 days 7.38 % 0 % 0.72 % 0 % 20.2 % 91 – 180 4.8 % 0 % 0 % 0 % 0 % 181- 1 year 4.43 % 0 % 0 % 0 % 0 % More than 1 Year 1.48 % 0 % 0 % 0 % 0 %

ICICI Prudential Within 30 days of intimation

79.32 % 79.51 % 67.32 % 70.88 % 87.84 %

31 – 90 days 13.03 % 10.74 % 26.4 % 27.35 % 8.91 % 91 – 180 6.13 % 7.2 % 4.17 % 1.48 % 3.25 % 181- 1 year 1.52 % 1.65 % 2.11 % 0.13 % 0 % More than 1 Year 0 % 0.9 % 0 % 0.15 % 0 %

SBI Life Within 30 days of intimation

73.6 % 79.7 % 83.26 % 83.91 % 86.43 %

31 – 90 days 17.32 % 13.81 % 13.72 % 13.91 % 13.02 % 91 – 180 4.16 % 2.18 % 1.98 % 1.58 % 0.42 % 181- 1 year 2.37 % 0.79 % 0.26 % 0.15 % 0.14 % More than 1 Year 2.55 % 3.51 % 0.79 % 0.45 % 0 %

Source: IRDA Annual Reports

The table above shows that LIC has been excellent in quick settlement of claims in

this category with most of the claims being settled within the first thirty days of

intimation. Private companies which are slowly picking up business in this line have

also showed a consistent increase in efficiency with most of the claims being settled

151

within a maximum period of thirty days and the remaining within ninety days. Very

few cases have gone beyond the time duration of six months.

The table below shows that almost all private companies have consistently increased

the efficiency in claim settlement and the private companies total also shows that

there is a 15% increase in the percentage of claims settled within the first thirty days,

with almost all of them being settled within six months.

Table 7.16 Duration wise settlement of death claim under group category in terms of benefits paid in percentages – Reliance, Bajaj Allianz & Aviva Reliance Within 30 days

of intimation 94.73 % 92.92 % 93.48 % 96.1 % 98.61 %

31 – 90 days 2.71 % 6.3 % 6.48 % 1.76 % 1 % 91 – 180 1.31 % 0.7 % 0 % 0.12 % 0.39 % 181- 1 year 0.77 % 0.04 % 0 % 1.99 % 0 % More than 1 Year

0.48 % 0.04 % 0.04 % 0.04 % 0 %

Bajaj Allianz Within 30 days of intimation

85.45 % 78.19 % 88.04 % 87.52 % 83.63 %

31 – 90 days 10.7 % 17.36 % 9.73 % 10.8 % 13.84 % 91 – 180 2.29 % 3.06 % 1.82 % 1.58 % 2.53 % 181- 1 year 1.15 % 1.07 % 0.3 % 0.08 % 0 % More than 1 Year

0.41 % 0.32 % 0.11 % 0.01 % 0 %

Aviva Within 30 days of intimation

87.83 % 96.27 % 99.42 % 94.44 % 91.05 %

31 – 90 days 10.63 % 3.21 % 0.39 % 3.19 % 7.78 % 91 – 180 0.92 % 0.17 % 0.08 % 2.13 % 0.83 % 181- 1 year 0.31 % 0.26 % 0.04 % 0 % 0.06 % More than 1 Year

0.31 % 0.09 % 0.08 % 0.24 % 0.28 %

Private total Within 30 days of intimation

70.61 % 77.73 % 85.7 % 84.05 % 85.52 %

31 – 90 days 17.95 % 14.56 % 11.25 % 12.78 % 12.05 % 91 – 180 6.27 % 4.26 % 2.3 % 2.58 % 2.22 % 181- 1 year 2.86 % 1.26 % 0.5 % 0.41 % 0.18 % More than 1 Year

2.31 % 2.19 % 0.26 % 0.17 % 0.04 %

Source: IRDA Annual Reports

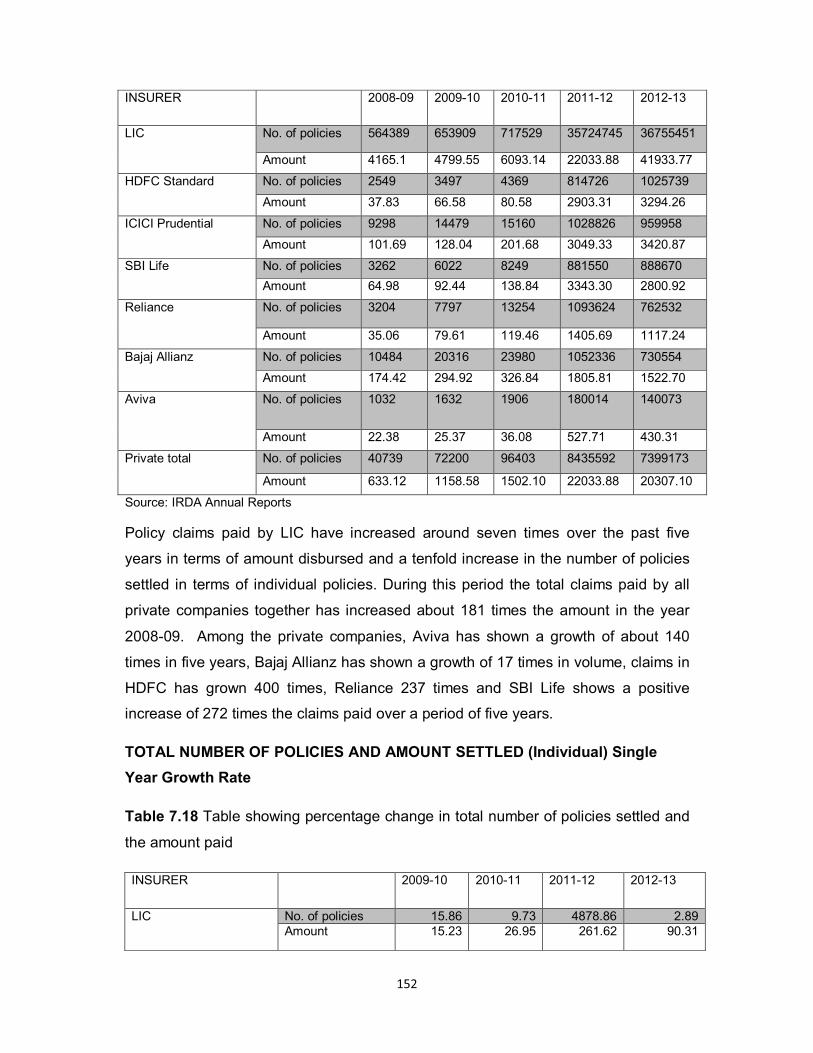

TOTAL NUMBER OF POLICIES AND AMOUNT SETTLED (Individual)

Table 7.17 The table shown below depicts a comparative analysis of policy claims

settled in terms of total number of policies and the total amount paid as claims on

individual policies

152

INSURER 2008-09 2009-10 2010-11 2011-12 2012-13

LIC No. of policies 564389 653909 717529 35724745 36755451

Amount 4165.1 4799.55 6093.14 22033.88 41933.77

HDFC Standard No. of policies 2549 3497 4369 814726 1025739

Amount 37.83 66.58 80.58 2903.31 3294.26

ICICI Prudential No. of policies 9298 14479 15160 1028826 959958

Amount 101.69 128.04 201.68 3049.33 3420.87

SBI Life No. of policies 3262 6022 8249 881550 888670

Amount 64.98 92.44 138.84 3343.30 2800.92

Reliance No. of policies 3204 7797 13254 1093624 762532

Amount 35.06 79.61 119.46 1405.69 1117.24

Bajaj Allianz No. of policies 10484 20316 23980 1052336 730554

Amount 174.42 294.92 326.84 1805.81 1522.70

Aviva No. of policies 1032 1632 1906 180014 140073

Amount 22.38 25.37 36.08 527.71 430.31

Private total No. of policies 40739 72200 96403 8435592 7399173

Amount 633.12 1158.58 1502.10 22033.88 20307.10

Source: IRDA Annual Reports

Policy claims paid by LIC have increased around seven times over the past five

years in terms of amount disbursed and a tenfold increase in the number of policies

settled in terms of individual policies. During this period the total claims paid by all

private companies together has increased about 181 times the amount in the year

2008-09. Among the private companies, Aviva has shown a growth of about 140

times in five years, Bajaj Allianz has shown a growth of 17 times in volume, claims in

HDFC has grown 400 times, Reliance 237 times and SBI Life shows a positive

increase of 272 times the claims paid over a period of five years.

TOTAL NUMBER OF POLICIES AND AMOUNT SETTLED (Individual) Single

Year Growth Rate

Table 7.18 Table showing percentage change in total number of policies settled and

the amount paid

INSURER 2009-10 2010-11 2011-12 2012-13

LIC No. of policies 15.86 9.73 4878.86 2.89 Amount 15.23 26.95 261.62 90.31

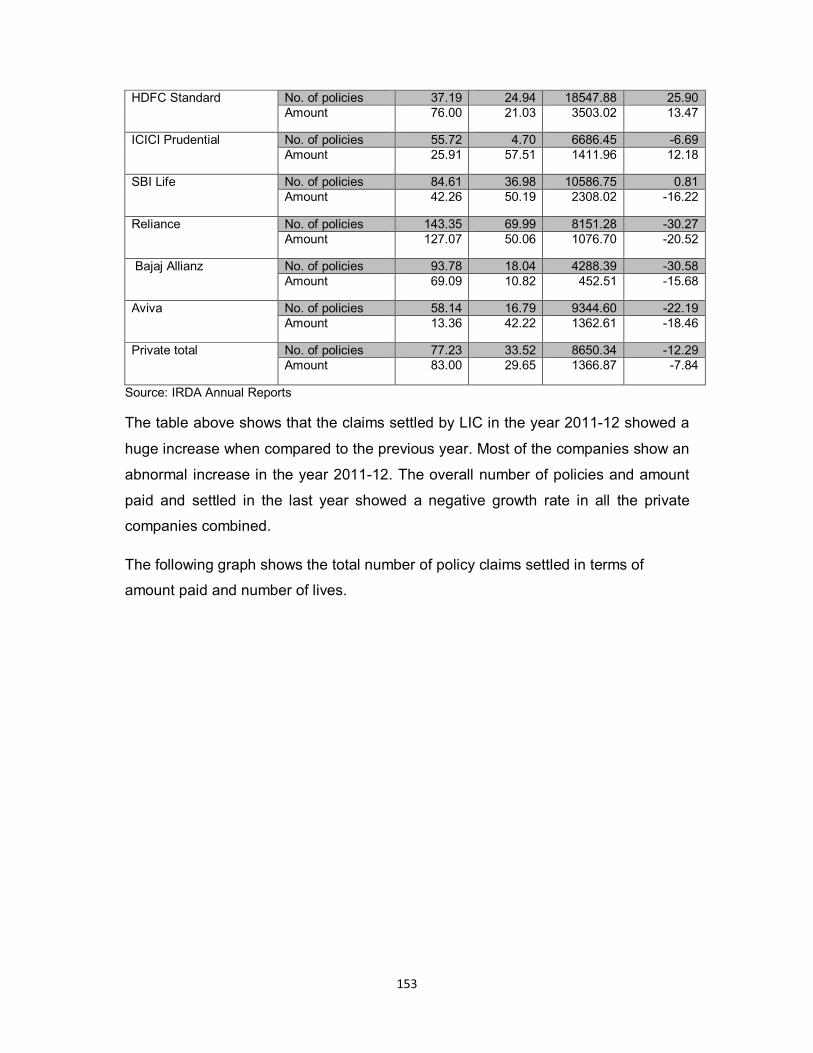

153

HDFC Standard No. of policies 37.19 24.94 18547.88 25.90 Amount 76.00 21.03 3503.02 13.47

ICICI Prudential No. of policies 55.72 4.70 6686.45 -6.69 Amount 25.91 57.51 1411.96 12.18

SBI Life No. of policies 84.61 36.98 10586.75 0.81 Amount 42.26 50.19 2308.02 -16.22

Reliance No. of policies 143.35 69.99 8151.28 -30.27 Amount 127.07 50.06 1076.70 -20.52

Bajaj Allianz No. of policies 93.78 18.04 4288.39 -30.58 Amount 69.09 10.82 452.51 -15.68

Aviva No. of policies 58.14 16.79 9344.60 -22.19 Amount 13.36 42.22 1362.61 -18.46

Private total No. of policies 77.23 33.52 8650.34 -12.29 Amount 83.00 29.65 1366.87 -7.84

Source: IRDA Annual Reports

The table above shows that the claims settled by LIC in the year 2011-12 showed a

huge increase when compared to the previous year. Most of the companies show an

abnormal increase in the year 2011-12. The overall number of policies and amount

paid and settled in the last year showed a negative growth rate in all the private

companies combined.

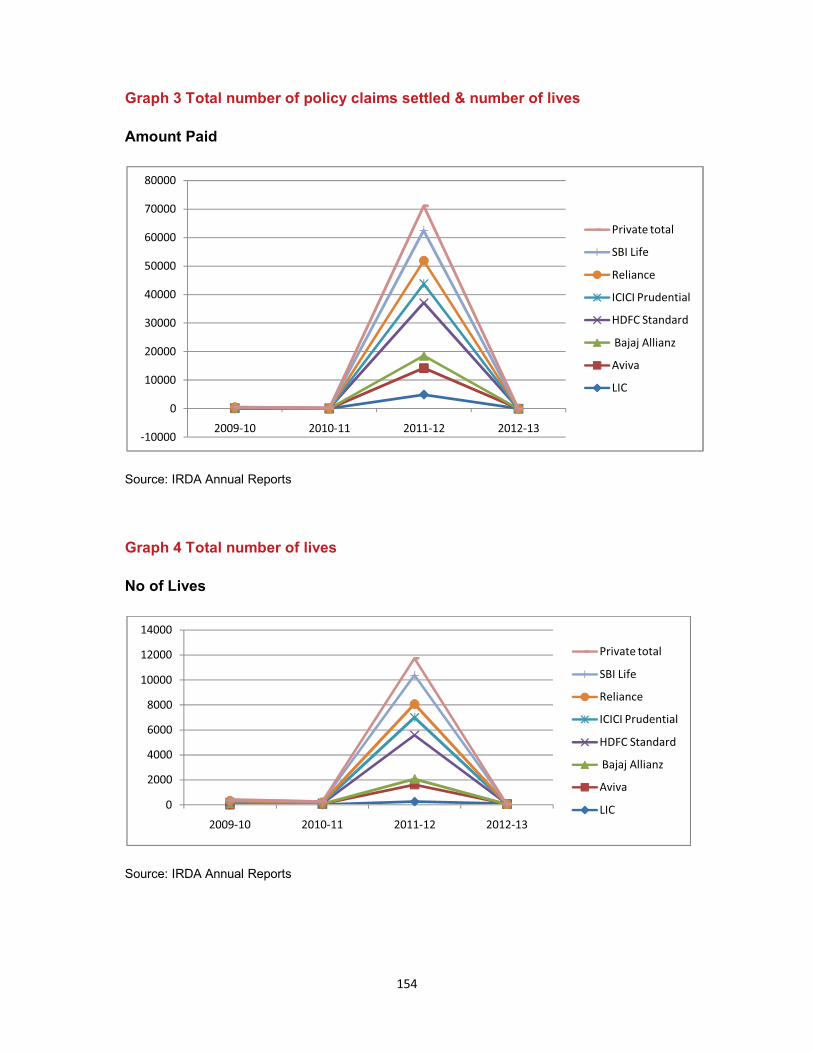

The following graph shows the total number of policy claims settled in terms of

amount paid and number of lives.

154

Graph 3 Total number of policy claims settled & number of lives

Amount Paid

Source: IRDA Annual Reports

Graph 4 Total number of lives

No of Lives

Source: IRDA Annual Reports

-10000

0

10000

20000

30000

40000

50000

60000

70000

80000

2009-10 2010-11 2011-12 2012-13

Private total

SBI Life

Reliance

ICICI Prudential

HDFC Standard

Bajaj Allianz

Aviva

LIC

0

2000

4000

6000

8000

10000

12000

14000

2009-10 2010-11 2011-12 2012-13

Private total

SBI Life

Reliance

ICICI Prudential

HDFC Standard

Bajaj Allianz

Aviva

LIC

155

Table 7.19 TOTAL NUMBER OF POLICIES AND AMOUNT SETTLED (GROUP)

(Rupees in Crores)

INSURER 2008-09 2009-10 2010-11 2011-12 2012-13

LIC No. of policies 222307 215485 233132 243429 245467

Amount 1005.15 1195.28 1393.51 1586.75 1709.08

HDFC Standard No. of policies 212 286 283 930 1526

Amount 2.71 2.36 2.78 6.44 20.49

ICICI Prudential No. of policies 1104 1863 3976 5279 3593

Amount 22.34 33.34 45.06 59.96 63.19

SBI Life No. of policies 16387 15817 11936 11995 11499

Amount 151.63 170.32 178.54 204.66 233.90

Reliance No. of policies 995 1869 1145 2237 4641

Amount 20.61 25.59 26.36 25.62 28.07

Bajaj Allianz No. of policies 13300 38988 28040 66067 45922

Amount 43.64 66.05 150.73 158.29 197.32

Aviva No. of policies 2759 4550 10502 6479 2329

Amount 6.49 11.53 25.79 20.67 17.99

Private total No. of policies 38200 9254 188798 142325 119970

Amount 322.33 439.08 666.31 794.99 1040.34

Source: IRDA Annual Reports

In the group category, there is almost consistent growth in claims paid and settled

amounts in the five year period given above. The overall private sector has shown

an abnormal variation in the number of policies paid and amount claimed in the

period of five years.

Analysis of Operating efficiency – The second determinant of performance of life

insurance companies is an analysis of profit and operating expenses of both private

and public sector Life Insurance Companies. An indepth analysis was made of all

the factors that determine the profitability of an insurance company and the various

factors are presented in the following charts and tables.

PROFIT BEFORE TAXATION AS PER SHAREHOLDERS’ ACCOUNT (IN LAKHS)

The following table is a representation of profits of various insurance companies over

a period of eight years through profit analysis and expense

156

Table 7.20 Table showing profit before taxation in lakhs

INSURER 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

LIC 63158

77362 84463 95735 106072 117180 131334 148992

HDFC Standard

-12875

-12556 -24351 -50296 -27518 -9900 27102 45572

ICICI Prudential

-2333

-69167 -154314 -88070 28053 83250 141372 156961

SBI Life 203

384 3475 -2664 27749 37045 55582 62217

Reliance -9840 -31511 76807 108491 28397 12929 3757 38042

Bajaj Allianz -9854

-7170 -21388 -7067 55699 108166 134958 134357

Aviva -14387

-13175 -20249 -49550 -34472 2875 7357 3200

Source: IRDA Annual Reports

The LIC of India due to the its head start and advantageous position of being the first

and only life insurance company since 1956 has been consistently making profits

and in the past eight years its profit has increased more than 200%. There is an

average increase of about 10,000 lakhs every year in premiums collected by LIC.

Among the private companies in the year 2005-06 all private companies surveyed

except SBI Life showed losses. Maximum loss reported was by AVIVA which was

the latest entry to the insurance segment. This is attributed to the fact that almost all

private companies which were still in the initial years of their existence had not yet

reached breakeven point. In the year 2006-07 too all private companies except SBI

Life recorded losses with ICICI Prudential reporting the highest loss which more than

doubled in the year 2007-08. However, Reliance and SBI Life showed profits in the

year 2007-08 and all other companies continued their loss making spree. The year

2008-09 too was not good for the private companies and losses were reported by all

companies except Reliance. SBI Life reported a loss for the first time after four years

however made up with a huge profit in the next year and the dramatic increase

continued up to 2012-13. Almost all the companies had a break even in the year

157

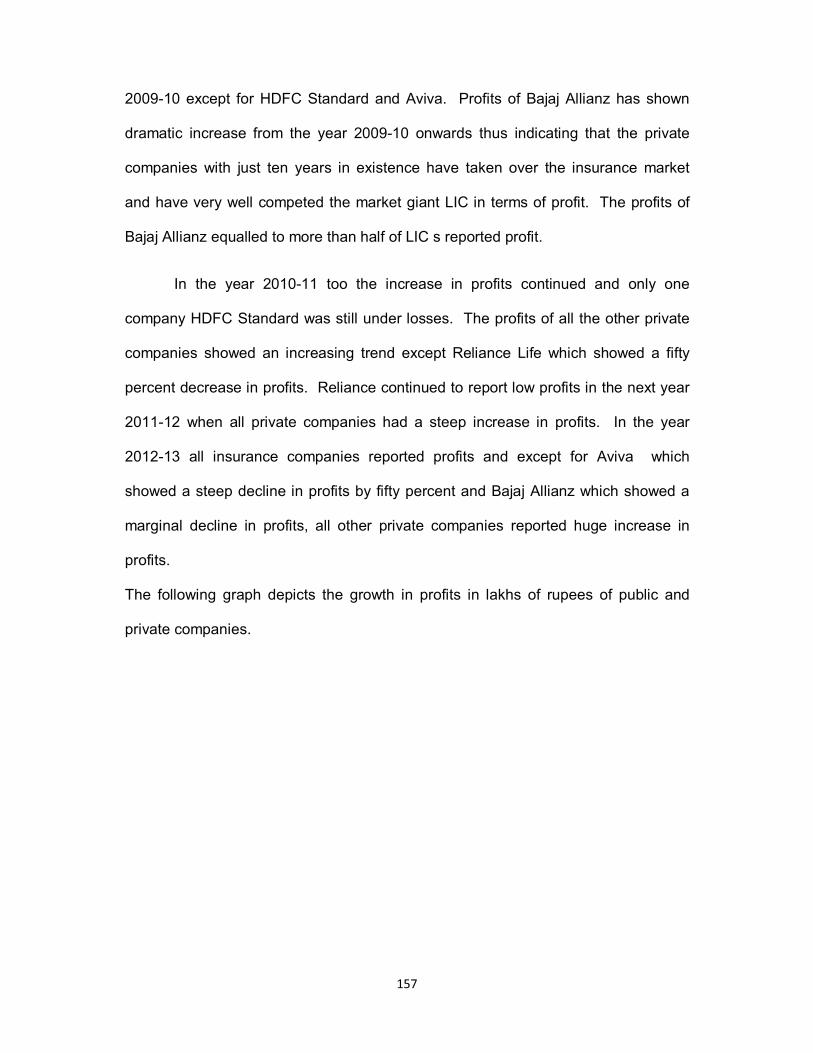

2009-10 except for HDFC Standard and Aviva. Profits of Bajaj Allianz has shown

dramatic increase from the year 2009-10 onwards thus indicating that the private

companies with just ten years in existence have taken over the insurance market

and have very well competed the market giant LIC in terms of profit. The profits of

Bajaj Allianz equalled to more than half of LIC s reported profit.

In the year 2010-11 too the increase in profits continued and only one

company HDFC Standard was still under losses. The profits of all the other private

companies showed an increasing trend except Reliance Life which showed a fifty

percent decrease in profits. Reliance continued to report low profits in the next year

2011-12 when all private companies had a steep increase in profits. In the year

2012-13 all insurance companies reported profits and except for Aviva which

showed a steep decline in profits by fifty percent and Bajaj Allianz which showed a

marginal decline in profits, all other private companies reported huge increase in

profits.

The following graph depicts the growth in profits in lakhs of rupees of public and

private companies.

158

Graph 5 Growth in profits of insurance companies

Source: IRDA Annual Reports

PROFIT BEFORE TAXATION SINGLE YEAR GROWTH RATE

The following table shows the growth rate of profit as per shareholder’s account for

the period of seven years showing rate of increase in profits of both LIC and private

sector life insurance companies

Table 7.21 Table showing profit before taxation – percentage of growth over

previous year

INSURER 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

LIC 22.49 9.18 13.35 10.80 10.47 12.08 13.45

HDFC

Standard

-2.48 93.94 106.55 -45.29 -64.02 -373.76 68.15

ICICI

Prudential

2864.72 123.10 -42.93 -131.85 196.76 69.82 11.03

SBI Life 89.16 804.95 -176.66 -1141.63 33.50 50.04 11.94

Reliance 220.23 -343.75 41.25 -73.83 -54.47 -70.94 912.56

Bajaj Allianz -27.24 198.30 -66.96 -888.16 94.20 24.77 -0.45

Aviva -8.42 53.69 144.70 -30.43 -108.34 155.90 -56.50

Source: IRDA Annual Reports

-200000

-100000

0

100000

200000

300000

400000

500000

600000

700000

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

SBI Life

Reliance

ICICI Prudential

HDFC Standard

Bajaj Allianz

Aviva

LIC

159

Table 7.22 Table showing Net profit net profit earned by insurance companies after

tax

INSURER

3/31/2005

3/31/2006 3/31/2007

3/31/2008 3/31/2009 3/31/2010 3/31/2011 3/31/2012 3/31/2013

LIC 70,836.50

63,158.01 77,362.03

84,462.59 95,734.88 106,071.68 117,180.37

131,334.29

148,992.49

HDFC -12,875.72

-12,556.11

-24,350.94

-50,296.31

-27,518.44

-9,900.21

27,101.54

45,147.91

ICICI -18,787.89

-64,890.72

-139,506.27

-77,969.96

25,796.85

80,762.28

138,417.37

149,593.92

SBI 203.16

383.99

3,475.43

3,475.43

27,749.14

37,045.22

55,582.14

62,217.09

Reliance

-76,806.78

-108,491.01

-28,378.84

-12,929.10

37,257.13

38,041.72

BAJAJ (9854) (7170) (21389) (7068) 54229 105704 131120 128564

AVIVA (14387) (13175) (20249) (49505) (34472) 2875 7357 3200

Source: IRDA Annual Reports

POLICY HOLDER’S ACCOUNT SURPLUS

It is mandatory for every life insurance company to transfer 95% of its profits as

bonus to policy holders’ accounts. Policy holders may opt to receive the bonus in

cash or accumulate the bonus for encashment at the time of maturity of policy. The

following table shows the amount of surplus in policy holders’ account.

Table 7.23 Table showing surplus in policy holders accounts in lakhs of rupees

INSURER 2005-

06

2006-

07

2007-

08

2008-

09

2009-

10

2010-

11

2011-

12

2012-

13

LIC 62177 75781 82959 92910 103092 113760 128123 143638

HDFC

Standard

255 339 7038 16664 19094 6698 37292 64211

ICICI

Prudential

1006 13601 32512 21293 129770 60760 133196 144968

SBI Life 0 1 8156 10845 19426 35112 58545 73151

Reliance 0 0 0 1587 8677 9621 37845 44428

Bajaj Allianz 6182 13788 19803 11550 40961 84095 100530 86247

Aviva 46864 75738 133337 111296 320967 208574 20659 26694

Source: IRDA Annual Reports

The table above indicates that policy holders account surplus in LIC has shown a

steady increase over the past seven years. LIC has shown a growth of more than

160

200% in terms of increase in policy holders’ account in the past seven years. The

surplus in policy holders accounts among its private counter parts varied

tremendously among the companies and within the company itself. ICICI has shown

a growth of about 144 times in the past seven years. Aviva shows abnormal surplus

which is dramatically increased by eight times in the year 2009-10 and shown to be

gradually depleting with a drastic fall in the years 2011-12 and 2012-13. Other

private companies have shown a gradual increase in policy holders’ surplus with

marginal decrease in the middle of the seven year period.

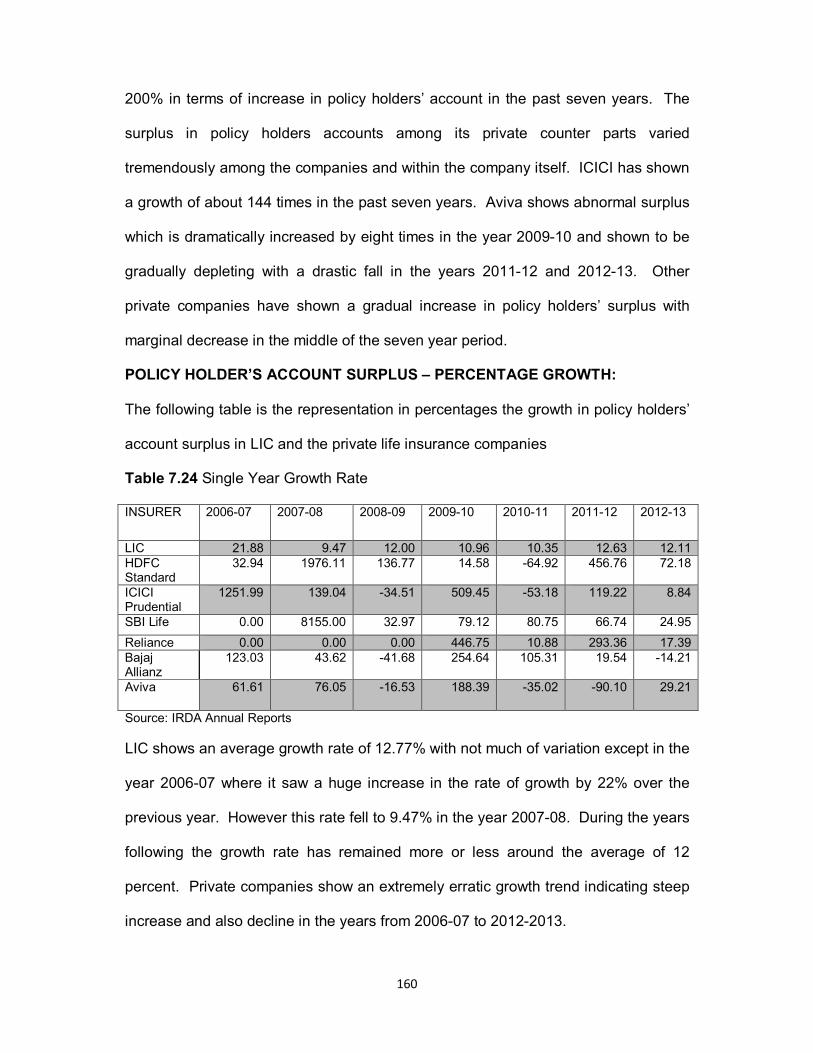

POLICY HOLDER’S ACCOUNT SURPLUS – PERCENTAGE GROWTH:

The following table is the representation in percentages the growth in policy holders’

account surplus in LIC and the private life insurance companies

Table 7.24 Single Year Growth Rate

INSURER 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

LIC 21.88 9.47 12.00 10.96 10.35 12.63 12.11 HDFC Standard

32.94 1976.11 136.77 14.58 -64.92 456.76 72.18

ICICI Prudential

1251.99 139.04 -34.51 509.45 -53.18 119.22 8.84

SBI Life 0.00 8155.00 32.97 79.12 80.75 66.74 24.95

Reliance 0.00 0.00 0.00 446.75 10.88 293.36 17.39 Bajaj Allianz

123.03 43.62 -41.68 254.64 105.31 19.54 -14.21

Aviva 61.61 76.05 -16.53 188.39 -35.02 -90.10 29.21

Source: IRDA Annual Reports

LIC shows an average growth rate of 12.77% with not much of variation except in the

year 2006-07 where it saw a huge increase in the rate of growth by 22% over the

previous year. However this rate fell to 9.47% in the year 2007-08. During the years

following the growth rate has remained more or less around the average of 12

percent. Private companies show an extremely erratic growth trend indicating steep

increase and also decline in the years from 2006-07 to 2012-2013.

161

PERFORMANCE EVALUATION OF AGENCY MODEL OF INSURANCE

The agency model has always been the most popular mode of selling insurance.

The agency concept involves the recruitment of retired persons, housewives, self-

employed individuals or even students. The life insurance company provides

professional training and gets them to target their acquaintances, friends and

relatives and sell life insurance products. This strategy has always been used by life

insurance companies because of the fact that in India, life insurance is still sold and

not bought. The functioning of the agency model is always the biggest challenge to

an insurance company since this group of people leaves the company without

hesitation. Agents have by far been the most disloyal to the company especially in

the case of private companies. In the recent past Bankassurance has gained a lot of

popularity where in a person is forced to buy an insurance policy when he

approaches the bank for a loan. However the success of a life insurance company is

directly dependent on the training and development and maintaining of its agents.

Insurance companies now have both individual and corporate agents selling policies

on their behalf. The following table indicates the number of individual agents of

various life insurance companies

Table 7.25 Table showing number of individual agents of life insurers

INSURER 2005-06 2006-07

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 Average

LIC 1052993

1103047

1193744 1344856 1402807 1337064 1278234 1172983 1235716

HDFC Standard

34887 79109 144714 207626 198879 136009 106244 77503 140710

ICICI Prudential

72383 234460 306354 299879 241830 190407 138883 147547

233106

SBI Life 8128 25356 40643 68993 65532 29628 86989 94138 59915

Reliance 19965 95620 184194 149613 195565 189433 150590 124038 158431

Bajaj Allianz

109141 216191 250239 204941 167741 18967 173146 148000 184052

Aviva 10974 29052 35307 30838 32728 23219 19126 17470 27531

Private 370846 890152 1326748 1592579 1575476 1302328 1080651 949774 1298365

Source: IRDA Annual Reports

162

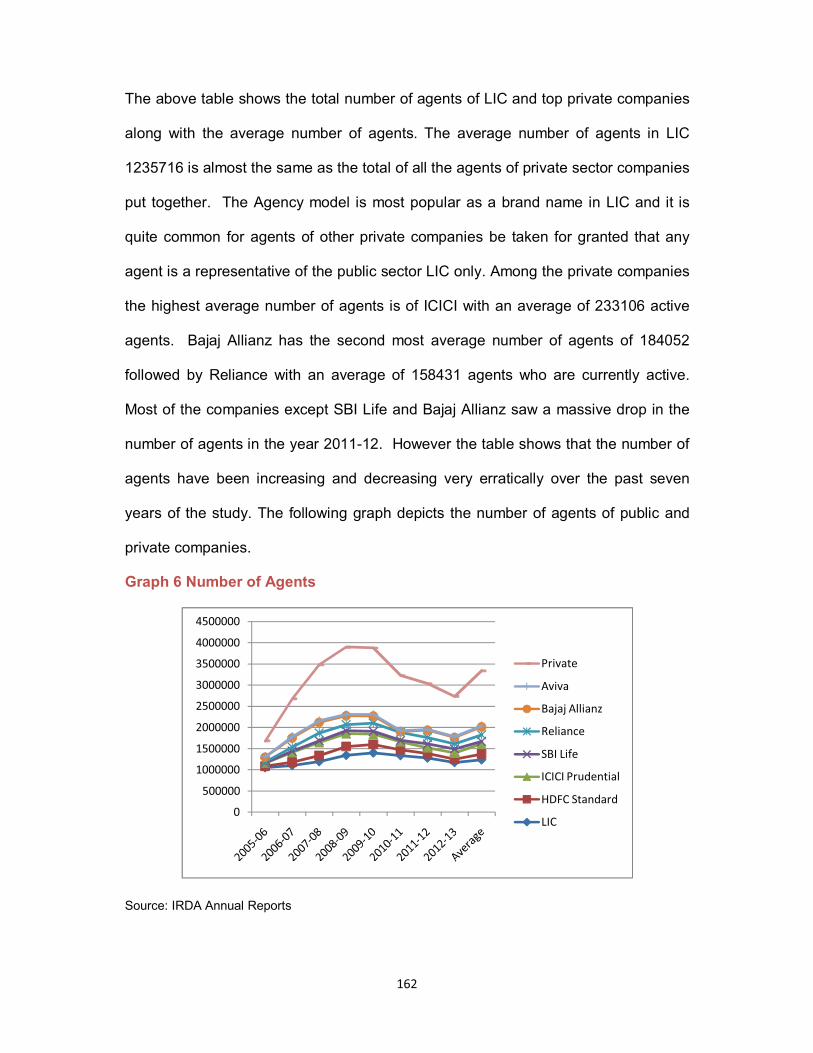

The above table shows the total number of agents of LIC and top private companies

along with the average number of agents. The average number of agents in LIC

1235716 is almost the same as the total of all the agents of private sector companies

put together. The Agency model is most popular as a brand name in LIC and it is

quite common for agents of other private companies be taken for granted that any

agent is a representative of the public sector LIC only. Among the private companies

the highest average number of agents is of ICICI with an average of 233106 active

agents. Bajaj Allianz has the second most average number of agents of 184052

followed by Reliance with an average of 158431 agents who are currently active.

Most of the companies except SBI Life and Bajaj Allianz saw a massive drop in the

number of agents in the year 2011-12. However the table shows that the number of

agents have been increasing and decreasing very erratically over the past seven

years of the study. The following graph depicts the number of agents of public and

private companies.

Graph 6 Number of Agents

Source: IRDA Annual Reports

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

Private

Aviva

Bajaj Allianz

Reliance

SBI Life

ICICI Prudential

HDFC Standard

LIC

163

CORPORATE AGENTS

Apart of individual agents, Life insurance companies employ corporate agencies and

banks to sell policies. The policies sold by corporate agents have however not been

as many as those sold by individual agents. However this model is gaining more

popularity in the recent days. The following table states the number of corporate

agents of various life insurance companies.

Table 7.26 Table showing number of corporate agents of life insurance companies

INSURER 2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

Average

LIC 74 226 345 415 510 295 240 207 330.28

HDFC 15 33 848 371 374 8 8 9 238

ICICI 7 17 46 47 22 15 14 11 25.57

SBI 8 27 23 94 127 100 73 83 76.42

Reliance 4 12 39 126 225 67 45 14 76

Bajaj 26 87 520 682 864 289 26 87 368.71

Aviva 3 5 21 17 15 11 246 210 75.42

Source: IRDA Annual Reports

The table reveals that in spite of the fact that LIC was in existence nearly 58 years,

the concept of corporate agents was one of recent origin. Hence in this segment,

the private companies too are very close in their average number of corporate

agents. Among all life insurance companies, Bajaj Allianz has the highest average

number of corporate agents with 369 followed by LIC with an average of 330 agents.

ICICI has the least number of corporate agents with an average of only 26.

The following table depicts the growth in terms of percentage in the number of

corporate agents of various life insurance companies.

164

Table 7.27 Table showing growth in Number of corporate agents in percentages

INSURER 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 Average

LIC 205.4054 52.65487 20.28986 22.89157 -42.1569 -18.6441 -13.75 32.38 HDFC 120 2469.697 -56.25 0.808625 -97.861 0 12.5 349.84

ICICI 142.8571 170.5882 2.173913 -53.1915 -31.8182 -6.66667 -21.4286 25.30 SBI 237.5 -14.8148 308.6957 35.10638 -21.2598 -27 13.69863 75.98

Reliance 200 225 223.0769 78.57143 -70.2222 -32.8358 -68.8889 79.24

Bajaj 234.6154 497.7011 31.15385 26.68622 -66.5509 -91.0035 234.6154 123.88

Aviva 66.66667 320 -19.0476 -11.7647 -26.6667 2136.364 -14.6341 350.18

Source: IRDA Annual Reports

The table above shows that the highest average growth rate 350% is that of AVIVA

however, it is seen that the pattern of growth of corporate agents in AVIVA is

abnormal and therefore not a correct representation. HDFC also reports average

growth rate of 350% but is highly erratic and cannot be considered as a true and

genuine representation of growth of corporate agents. LIC, ICICI, SBI and Bajaj

report a more realistic growth rate and it is seen that the growth of corporate agents

is much higher in private companies than in LIC. This is indicative of a future trend

among life insurance companies where in they will work towards forming more

corporate partnerships and tie ups for the sale of insurance products.

POLICIES SOLD UNDER THE AGENCY MODEL

The following table shows the average number of policies sold by the agents of LIC

and various private companies.

Table 7.28 Table showing the average number of policies sold by individual

and Corporate Agents

INSURER 2008-09 2009-10 2010-11 2011-12 2012-13

LIC Individual 28 28 26 27 29

Corporate agents 2190 1606 1708 2194 2569

HDFC Standard Individual 4 3 3 3 4

Corporate agents 428 704 1751 47211 56628

ICICI Prudential Individual 4 3 3 2 2

Corporate agents 7723 7413 13195 16328 28843

SBI Life Individual 11 13 8 6 6

Corporate agents 5659 4405 3118 3820 4610

165

Reliance Individual 4 5 4 4 3

Corporate agents 7448 5840 6412 6072 6608

Bajaj Allianz Individual 6 5 4 3 3

Corporate agents 1824 1286 1247 1717 1042

Aviva Individual 7 3 3 3 3

Corporate agents 1211 1667 3870 7067 5870

Private total Individual 6 4 4 3 3

Corporate agents 1857 2289 1976 2533 5064

Source: IRDA Annual Reports

The table depicts that the individual agents of LIC have been most successful in

selling an average of 29 policies which is by far the highest among all insurance

companies. Among the private companies, agents of SBI Life have been the most

successful selling upto an average of 13 policies per agent. In the Corporate agent

sector HDFC far out beats the other companies with a total of 56628 policies sold in

the year 2012-13. The growth in this segment has been only in the last two financial

years in the case of HDFC and also in the case of ICICI Prudential which is next in

line in terms of policies sold by Corporate Agents.

The following graph depicts the number of policies sold by individual and corporate

agents of private and public sector life insurance companies.

Graph 7 Number of policies sold by individual

Source: IRDA Annual Reports

0

10

20

30

40

50

60

70

80

2008-09 2009-10 2010-11 2011-12 2012-13

Private total

SBI Life

Reliance

ICICI Prudential

HDFC Standard

Bajaj Allianz

Aviva

LIC

166

Graph 8 Number of policies sold by Corporate Agents

Source: IRDA Annual Reports

The following table shows the percentage of policies sold by public and private

sector life insurance agents individually and through Corporate agents

Table 7.29 Table showing Average Number of Policies by Individual and Corporate

Agents and percentage growth in the respective segments

INSURER 2009-10 2010-11 2011-12 2012-13 Average

LIC Individual 0 -7.14286 3.846154 7.407407 27.6

Corporate agents -26.6667 6.351183 28.45433 17.09207 2053.4

HDFC Standard Individual -25 0 0 33.33333 3.4

Corporate agents 64.48598 148.7216 2596.231 19.94662 21344.4

ICICI Prudential Individual -25 0 -33.3333 0 2.8

Corporate agents -4.01398 77.99811 23.74384 76.64748 14700.4

SBI Life Individual 18.18182 -38.4615 -25 0 8.8

Corporate agents -22.1594 -29.2168 22.51443 20.68063 4322.4

Reliance Individual 25 -20 0 -25 4

Corporate agents -21.5897 9.794521 -5.30256 8.827404 6476

Bajaj Allianz Individual -16.6667 -20 -25 0 4.2

Corporate agents -29.4956 -3.03266 37.69046 -39.3128 1423.2

0

20000

40000

60000

80000

100000

120000

2008-09 2009-10 2010-11 2011-12 2012-13

Private total

SBI Life

Reliance

ICICI Prudential

HDFC Standard

Bajaj Allianz

Aviva

LIC

167

Aviva Individual -57.1429 0 0 0 3.8

Corporate agents 37.65483 132.1536 82.60982 -16.9379 3937

Private total Individual -33.3333 0 -25 0 4

Corporate agents 23.26333 -13.6741 28.18826 99.92104 2743.8

Source: IRDA Annual Reports

The average of LIC is 28% and in case of private sector the percentage in case of

individual policies is a meagre 4%. However in case of Corporate agents, the private

sector companies far out beat LIC.

Performance of Agents

The following table depicts the policies written by agents of various life insurance

companies

7.30 Table showing number of policies in thousands

INSURER 2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

LIC 179564 189419 192428 210154 226058 240381 255845 270251 HDFC Standard

590 752 996 1244 1497 1598 1762 1938

ICICI Prudential

173 734 1037 1313 972 1090 1293 1502

SBI Life 352 411 420 489 579 789 1204 1724 Reliance 77 189 220 234 600 1939 2154 2327 Bajaj Allianz

395 511 540 721 941 1820 2283 2507

Aviva 34 51 48 62 62 152 254 317 Private 3545 4746 5740 7533 9007 12839 15430 17605

Source: IRDA Annual Reports

The agents of LIC have consistently been the highest sellers of policies right through

the period. It was found that due to severe competition from the private sector life

insurance companies, LIC reinvented itself, improved training and development of its

employees and agents and also designed new products that were customer centric

to affirm its position as highest policy seller in the industry. Over the period of eight

years, the total growth in the number of policies in LIC was more than 9 crores. The

average growth over the years has been about 1 crore policies.

168

Private companies are far behind in the number of policies sold with the total policies

being only 2% of the policies sold by LIC alone in the year 2005-06. Growth in the

whole private sector has been a little over 1,40,00,00,000 in terms of number of

policies sold with the major growth being shown in Bajaj Allianz.

The following graph depicts the number of policies sold in thousands by insurance

companies.

Graph 9 Number of policies sold

The following table depicts the percentage of growth in policies sold by LIC and other

private companies. The table shows that the rate of growth in LIC has been more or

less consistent with an average growth of about 6% throughout the period of eight

years. However in the overall private sector, there has been an average growth rate

of 26%. The average growth rate of HDFC is 19%, ICICI Prudential has an average

growth rate of a phenomenal 59% over the seven year period. SBI Life has average

growth rate of 27%, Reliance of 81%, being the company with the highest growth

rate, Bajaj Allianz has grown at 32% and Aviva has an average growth rate of 44%.

0

50000

100000

150000

200000

250000

300000

350000

Private

Aviva

Bajaj Allianz

Reliance

SBI Life

ICICI Prudential

HDFC Standard

LIC

169

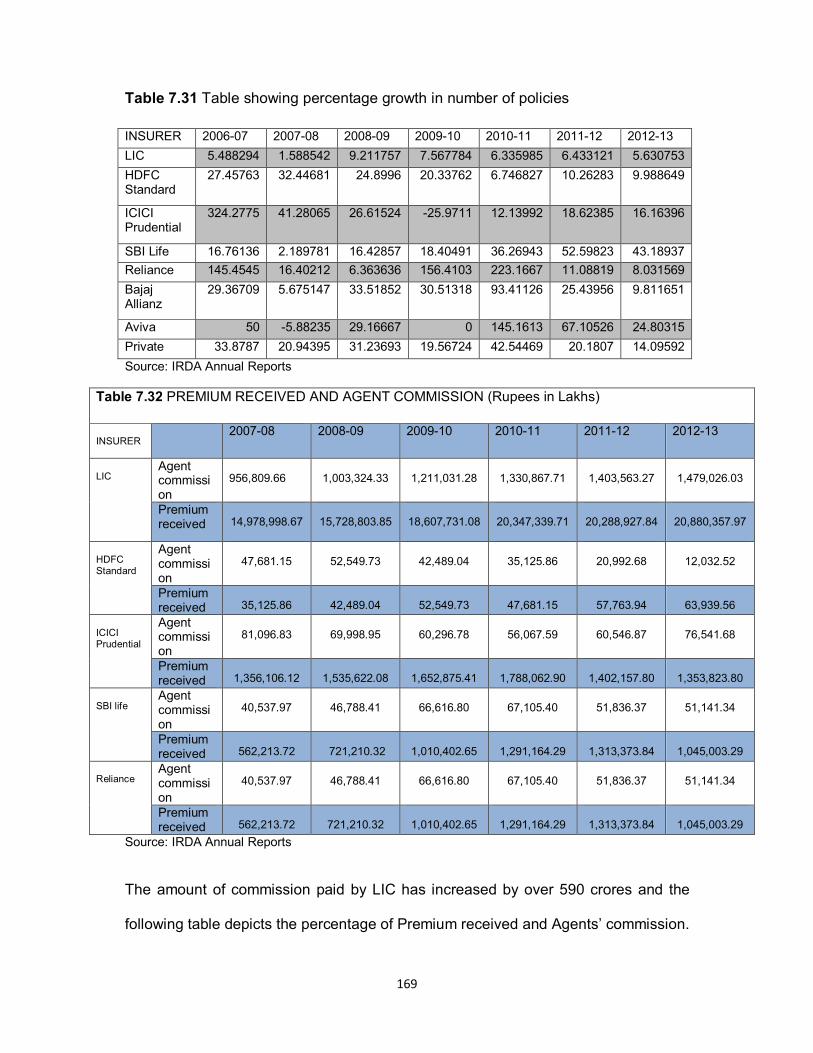

Table 7.31 Table showing percentage growth in number of policies

INSURER 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

LIC 5.488294 1.588542 9.211757 7.567784 6.335985 6.433121 5.630753

HDFC Standard

27.45763 32.44681 24.8996 20.33762 6.746827 10.26283 9.988649

ICICI Prudential

324.2775 41.28065 26.61524 -25.9711 12.13992 18.62385 16.16396

SBI Life 16.76136 2.189781 16.42857 18.40491 36.26943 52.59823 43.18937

Reliance 145.4545 16.40212 6.363636 156.4103 223.1667 11.08819 8.031569

Bajaj Allianz

29.36709 5.675147 33.51852 30.51318 93.41126 25.43956 9.811651

Aviva 50 -5.88235 29.16667 0 145.1613 67.10526 24.80315

Private 33.8787 20.94395 31.23693 19.56724 42.54469 20.1807 14.09592

Source: IRDA Annual Reports

Table 7.32 PREMIUM RECEIVED AND AGENT COMMISSION (Rupees in Lakhs)

INSURER

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

LIC

Agent commission

956,809.66

1,003,324.33

1,211,031.28

1,330,867.71

1,403,563.27

1,479,026.03

Premium received

14,978,998.67

15,728,803.85

18,607,731.08

20,347,339.71

20,288,927.84

20,880,357.97

HDFC Standard

Agent commission

47,681.15

52,549.73

42,489.04

35,125.86

20,992.68

12,032.52

Premium received

35,125.86

42,489.04

52,549.73

47,681.15

57,763.94

63,939.56

ICICI Prudential

Agent commission

81,096.83

69,998.95

60,296.78

56,067.59

60,546.87

76,541.68

Premium received

1,356,106.12

1,535,622.08

1,652,875.41

1,788,062.90

1,402,157.80

1,353,823.80

SBI life

Agent commission

40,537.97

46,788.41

66,616.80

67,105.40

51,836.37

51,141.34

Premium received

562,213.72

721,210.32

1,010,402.65

1,291,164.29

1,313,373.84

1,045,003.29

Reliance

Agent commission

40,537.97

46,788.41

66,616.80

67,105.40

51,836.37

51,141.34

Premium received

562,213.72

721,210.32

1,010,402.65

1,291,164.29

1,313,373.84

1,045,003.29

Source: IRDA Annual Reports

The amount of commission paid by LIC has increased by over 590 crores and the

following table depicts the percentage of Premium received and Agents’ commission.

170

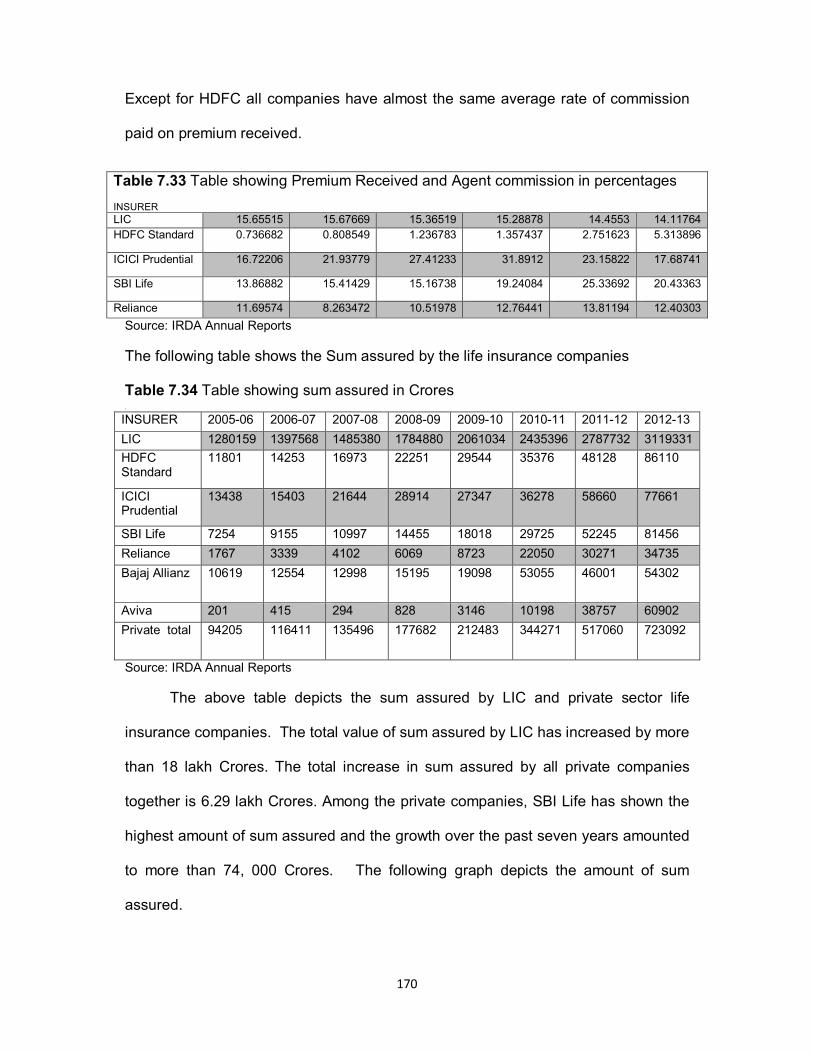

Except for HDFC all companies have almost the same average rate of commission

paid on premium received.

Table 7.33 Table showing Premium Received and Agent commission in percentages

INSURER LIC 15.65515 15.67669 15.36519 15.28878 14.4553 14.11764

HDFC Standard 0.736682 0.808549 1.236783 1.357437 2.751623 5.313896

ICICI Prudential 16.72206 21.93779 27.41233 31.8912 23.15822 17.68741

SBI Life 13.86882 15.41429 15.16738 19.24084 25.33692 20.43363

Reliance 11.69574 8.263472 10.51978 12.76441 13.81194 12.40303

Source: IRDA Annual Reports

The following table shows the Sum assured by the life insurance companies

Table 7.34 Table showing sum assured in Crores [

INSURER 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

LIC 1280159 1397568 1485380 1784880 2061034 2435396 2787732 3119331

HDFC Standard

11801 14253 16973 22251 29544 35376 48128 86110

ICICI Prudential

13438 15403 21644 28914 27347 36278 58660 77661

SBI Life 7254 9155 10997 14455 18018 29725 52245 81456

Reliance 1767 3339 4102 6069 8723 22050 30271 34735

Bajaj Allianz 10619 12554 12998 15195 19098 53055 46001 54302

Aviva 201 415 294 828 3146 10198 38757 60902

Private total 94205 116411 135496 177682 212483 344271 517060 723092

Source: IRDA Annual Reports

The above table depicts the sum assured by LIC and private sector life

insurance companies. The total value of sum assured by LIC has increased by more

than 18 lakh Crores. The total increase in sum assured by all private companies

together is 6.29 lakh Crores. Among the private companies, SBI Life has shown the

highest amount of sum assured and the growth over the past seven years amounted

to more than 74, 000 Crores. The following graph depicts the amount of sum

assured.

171

Graph 10 Amount of sum assured

Source: IRDA Annual Reports

The following table shows the percentage of growth in sum assured by all the life

insurance companies

Table 7.35 Table showing Sum Assured in Crores – Percentage growth

INSURER 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 Average LIC 9.171439 6.283201 20.16319 15.47185 18.1638 14.4673 11.89494 14

HDFC Standard

20.7779 19.0837 31.09645 32.77606 19.74005 36.04704 78.91872 34

ICICI Prudential

14.62271 40.51808 33.58899 -5.41952 32.65806 61.69579 32.39175 30

SBI Life 26.20623 20.12015 31.44494 24.64891 64.97391 75.76114 55.91157 43

Reliance 88.96435 22.85115 47.95222 43.73043 152.78 37.28345 14.74679 58

Bajaj Allianz

18.22205 3.536721 16.9026 25.68608 177.804 -13.2956 18.04526 35

Aviva 106.4677 -29.1566 181.6327 279.9517 224.1577 280.0451 57.13807 157

Private total

23.572 16.3945 31.1345 19.58611 62.02284 50.18982 39.84683 35

Source: IRDA Annual Reports

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

Private total

Aviva

Bajaj Allianz

Reliance

SBI Life

ICICI Prudential

HDFC Standard

LIC

172

In the above table LIC shows an increase steadily at an average rate of 14% in the

total sum assured. The private companies in total on the other hand have increased

at an average rate of 35% in sum assured

MARKETING OF INSURANCE PRODUCTS

The role of marketing in insurance cannot be overemphasized. Given that the nature

of the product is such that this is a product that is not bought but sold, insurance

companies take pain staking efforts in the P s of marketing, Product, pricing,

promotion, publicity. An insurance product is designed keeping in mind the various

needs of the customer, company’s goal and financial objectives and the general

condition of the economy and financial market and money market conditions. Every

product designed by an insurance company should be mandatorily be approved by

the IRDA. Marketing costs have been an imperative expenditure on the revenues of

the company the companies having to allocate huge amounts to gain new customers

and retain old clients. Client retention in insurance is a big challenge and hence

companies have expended a huge amount on marketing of products. The following

table depicts the amount spent on marketing by the public sector and private sector

life insurance companies.

Table 7.36 Table showing marketing expenses of life insurance companies ( Rs. In Crores) INSURER 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 Average

LIC 20,253.65

24,389.96

30,496.26

32,459.35

34,921.35

26,460.10

28,163.45

HDFC Standard

11,081.42

40,347.80

27,659.82

33,595.09

3,117.82

2,835.96

19,772.99

ICICI Prudential

3,357.43

11170.44 2,932.21

8,697.92

11,410.92

13,052.43

8,436.89

SBI Life 3,893.69

3684.62 3,000.24

3,622.85

3,927.14

4,686.20

3,802.46

Reliance 19,585.66

25,440.62

49528.78 43647.95 21,657.71

22,897.59

30,459.72

Source: IRDA Annual Reports

In spite of continuous marketing efforts, the average amount spent on marketing by

LIC is second in the industry to Reliance Company spending an average of more

173

than 30,000 Crores on marketing. The change in amount spent on marketing by LIC

has varied only slightly. Where as in private companies, there is a steep incline in

the marketing costs of HDFC in the year 2008-09, however due to severe cost

cutting, the expenditure drastically reduced in 2011-12. SBI Life has consistently

spent a nominal amount on marketing. Though marketing plays an important role,

the study did not reveal any direct correlation between amount spent on marketing

and premiums collected. The following table shows the percentage change in

marketing expenses incurred by life insurance companies.

Table 7.37 Table showing percentage change in marketing expenses

INSURER 2008-09 2009-10 2010-11 2011-12 2012-13

LIC 20.42254 25.03612 6.43715 7.584872 -24.2294

HDFC Standard 264.1032 -31.4465 21.45809 -90.7194 -9.04029

ICICI Prudential 232.7081 -73.7503 196.6336 31.19137 14.38543

SBI Life -5.36946 -18.574 20.75201 8.399188 19.32857

Reliance 29.89412 94.68386 -11.8736 -50.3809 5.72489

Source: IRDA Annual Reports

The above table reveals that there has been a sudden decrease in marketing

expenses incurred by LIC in the year 2012-13. Reliance Company has shown a

wide variation and so has the expenditure incurred by HDFC Standard which shows

a 264% increase in the second year followed by a negative growth in the third year

and fifth year. The following table shows the relationship between the Premium

received as against Marketing expenses of the companies.

Table 7.38 Table showing Premium Received / Marketing Expenses

INSURER 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 LIC 739.5703 644.8885 610.1644 626.856 580.9892 789.1262

HDFC Standard

3.169798 1.05307 1.899858 1.419289 18.52703 22.546

ICICI Prudential

403.912 137.4719 563.6961 205.5736 122.8786 103.722

SBI Life 144.391 195.7353 336.7739 356.3946 334.4352 222.9959 Reliance 16.46837 19.38844 13.33547 15.05488 25.38412 17.66733 Source: IRDA Annual Reports

174

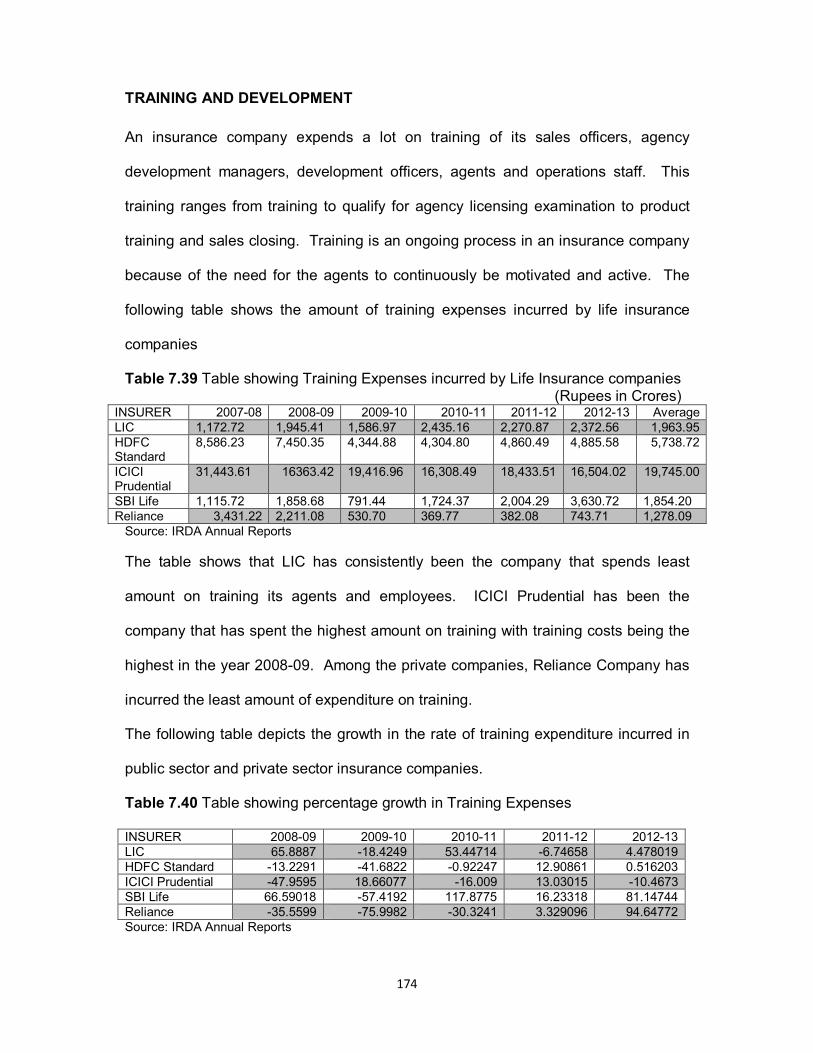

TRAINING AND DEVELOPMENT

An insurance company expends a lot on training of its sales officers, agency

development managers, development officers, agents and operations staff. This

training ranges from training to qualify for agency licensing examination to product

training and sales closing. Training is an ongoing process in an insurance company

because of the need for the agents to continuously be motivated and active. The

following table shows the amount of training expenses incurred by life insurance

companies

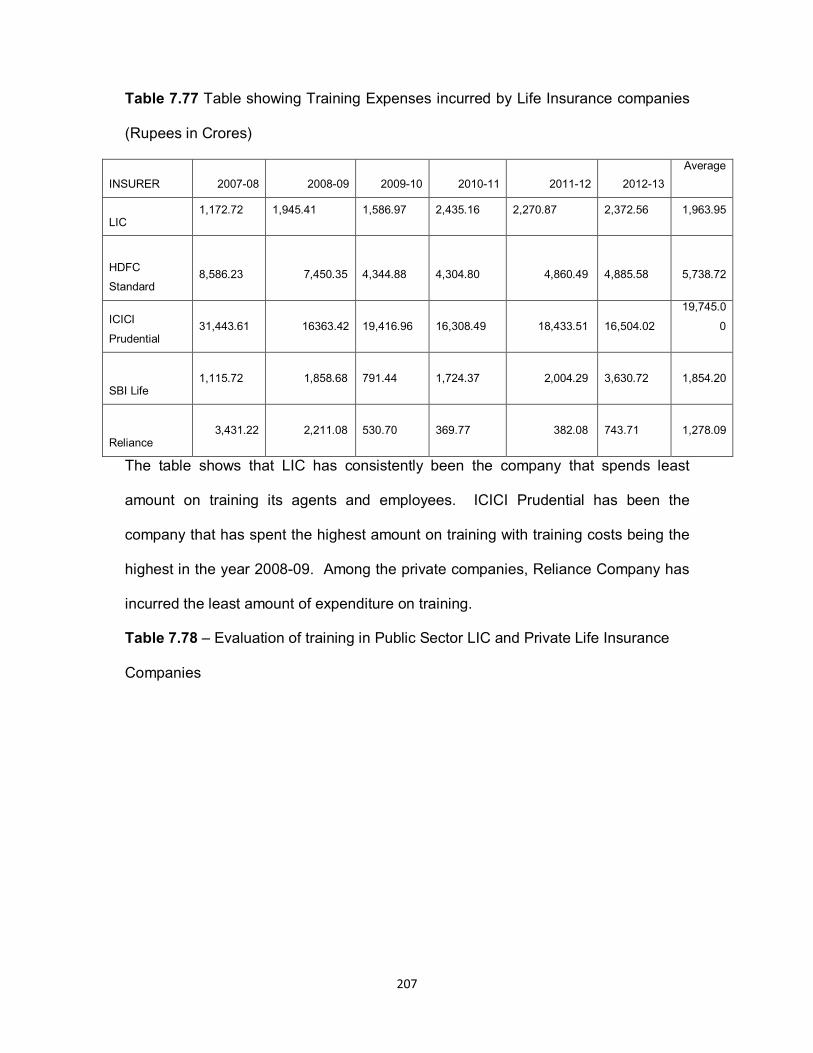

Table 7.39 Table showing Training Expenses incurred by Life Insurance companies (Rupees in Crores)

INSURER 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 Average LIC 1,172.72 1,945.41 1,586.97 2,435.16 2,270.87 2,372.56 1,963.95 HDFC Standard

8,586.23 7,450.35 4,344.88 4,304.80 4,860.49 4,885.58 5,738.72

ICICI Prudential

31,443.61 16363.42 19,416.96 16,308.49 18,433.51 16,504.02 19,745.00

SBI Life 1,115.72 1,858.68 791.44 1,724.37 2,004.29 3,630.72 1,854.20 Reliance 3,431.22 2,211.08 530.70 369.77 382.08 743.71 1,278.09

Source: IRDA Annual Reports

The table shows that LIC has consistently been the company that spends least

amount on training its agents and employees. ICICI Prudential has been the

company that has spent the highest amount on training with training costs being the

highest in the year 2008-09. Among the private companies, Reliance Company has

incurred the least amount of expenditure on training.

The following table depicts the growth in the rate of training expenditure incurred in

public sector and private sector insurance companies.

Table 7.40 Table showing percentage growth in Training Expenses

INSURER 2008-09 2009-10 2010-11 2011-12 2012-13 LIC 65.8887 -18.4249 53.44714 -6.74658 4.478019 HDFC Standard -13.2291 -41.6822 -0.92247 12.90861 0.516203 ICICI Prudential -47.9595 18.66077 -16.009 13.03015 -10.4673 SBI Life 66.59018 -57.4192 117.8775 16.23318 81.14744 Reliance -35.5599 -75.9982 -30.3241 3.329096 94.64772 Source: IRDA Annual Reports

175

Apart from the first year increase in training expenditure in the year 2008-09, LIC has