aluca cmg / vic · 2018-07-09 · aluca cmg / vic melbourne legal session 19th april 2018. aluca...

TRANSCRIPT

ALUCA CMG / VIC Melbourne Legal Session

19th APRIL 2018

ALUCA Life insurance Excellence Awards

• 10 categories: Leadership x 2, Claims x 2, Underwriting x 2, Rehab x 1, Education x 1, Innovation x 1 and Service x 1 .

• Prizes for winner & logo for all finalists to use.

• Nominations close April 20th

• Early bird tickets for black tie event $125+ GST@ aluca.com/events/event-calendar

turkslegal.com.au

TPD - How should you deal

with events between the date

of assessment and trial?

Darryl Pereira, Partner

Sofia Papachristos, Partner

Subsequent Events – how should they be treated?

Subsequent Deteriorations

Subsequent Injuries

Subsequent Job Applications

Subsequent Work

Summary

Overview

| 5

1

2

3

4

5

Regulatory Landscape - TPD definitions

| 6

PJC Report March 2018

▪ Committee recommended standardising TPD definitions

▪ Insurance in Superannuation Code of Practice be updated to reflect this

recommendation

APRA Deputy Chairman Helen Rowell's speech 'APRA Update:

What can you expect in 2018'

▪ Acknowledged Insurance in Superannuation Code was a significant industry-

led effort and an important step forward

▪ However, APRA consider Code should be strengthened including by

standardising definitions for disability

a) absent from work through illness or injury for six consecutive months;

and

b) in the opinion of the insurer, the life insured has become incapacitated

to such an extent as to render the life insured unlikely ever to engage

in or work for reward in any occupation or work for which [he/she] is

reasonably capable of performing by reason of education, training or

experience

▪ Whilst the words ‘Date of Assessment’ rarely appear in the definition, it is

the contractually agreed marker when the opinion on the likelihood of a

return to ETE work is to be formed.

▪ The DOA is generally accepted as being at the end of the qualifying

period – 3 or 6 months continuous absence from work.

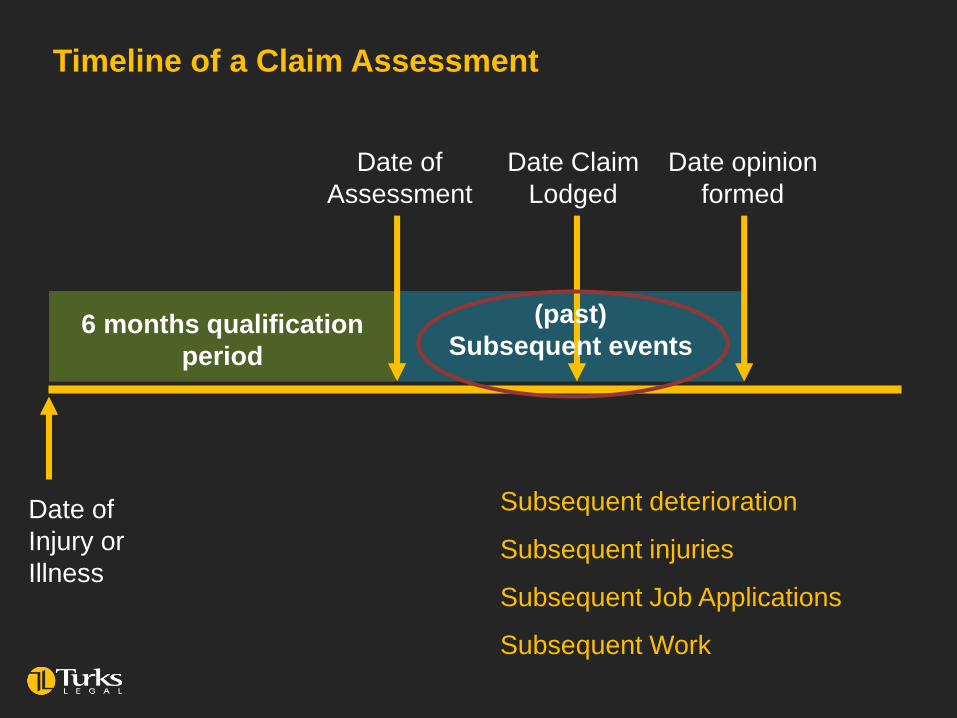

Standard TPD Definition

| 7

Date of

Injury or

Illness

6 months qualification

period

Date of

Assessment

Date Claim

Lodged

Date opinion

formed

Subsequent deterioration

Subsequent injuries

Subsequent Job Applications

Subsequent Work

Timeline of a Claim Assessment

(past)

Subsequent events

The TPD Flow Chart

| 9

H

E

A

L

T

H

Good

PoorTIME

Health

ou

tco

mes

Date of Assessment Date Opinion Formed

Return to

Work Point

Injury

▪ The DOA will invariably be a date long past by the time the insurer is ready

to form an opinion on likelihood of a return to ETE work.

▪ The misalignment of these two dates will throw up complexities for insurers:

▪ in obtaining evidence which will need to deal with historical events and the

subsequent events which occur between the two bookend dates

▪ how is the DOA prognostication impacted by events that are no longer future

possibilities but actual events occurring after the DOA – the “subsequent events”

The subsequent events complexity

| 10

Subsequent Deteriorations

Subsequent Injuries

Subsequent Job Applications

Subsequent Employment

Summary

| 11

1

2

3

4

5

Tower v Farkas

| 12

One issue the CoA raised was how it should deal with the fact that the insured was in remission at the time the insurer’s decision

was made.

Lower court found that the insured met this definition and the insurer appealed to CoA.

Definition of TI was ‘an illness or condition which is highly likely to result in death within 12 months’ .

Dispute over whether the insured was TI under a life policy (non-Hodgkins lymphoma).

1 Deteriorations

‘…the evidence in question in the present case must relate to the insured’s prognosis as at the date of diagnosis/occurrence of the relevant disease… But it is only the prognosis as at that date that governs entitlements under the Policy… evidence that the insured did or did not survive for 12 months casts no relevant light on that prognostic matter. For the Court to have regard to facts which could not be known at the contractually agreed date for assessment would effectively deny the bargain struck between the parties.’

Tower v Farkas

| 13

Mason P

1 Deteriorations

Tower v Farkas

| 14

Mason P

‘… to pay regard to later events, except those reflecting on the prognosis that was or ought to have been formed on 1 May 2002, would be to depart from the relevant bargain which was necessarily forward-looking in a prognostic sense’

1 Deteriorations

Halloran v Harwood Nominees

| 15

‘If an employee is not disabled as defined at the relevant date, a subsequent deterioration in his or her condition would not qualify him [or her] for a disablement benefit. Conversely, if he or she is disabled as defined at the relevant date, a subsequent improvement in his or her condition does not retrospectively disqualify the employee from the benefit’.

1 Deteriorations

McArthur v Mercantile Mutual

| 16

‘As the Court’s role is to determine whether the definition of total and permanent disablement has been fulfilled… there is no reason why the Court performing that task, should be confined to the evidence before the respondent on 14 October 1996.

Medical reports coming into existence after the relevant time will be admissible provided that they are pertinent to the determination of the appellant’s condition at the relevant time’

Muir J

1 Deteriorations

TAL v Shuetrim

| 17

Approved of this is comment in Finch v Telstra [2010]

Approved of the phrase ‘the court does not speculate when it can know’- used in Willis v the Commonwealth [1946]

The Court approved of the reasoning above in McArthur(para 150)

Issue arose as to how one of the insurers dealt with medical reports coming into existence after the DOA - they were given less weight

1 Deteriorations

TAL v Shuetrim

| 18

‘What matters is that that state of affairs arose while I was a Telstra Employee. It does not matter that the symptoms of that state of affairs emerged more clearly after I left Telstra’s employment.’

1 Deteriorations

Wheeler v FSS

| 19

• Former NSW Police officer

• Medically discharged due to PTSD

• chronic psychiatric illness – years for condition to stabilise/reach a

point where reliable psychiatric prognosis can be given

1 Deteriorations

Wheeler v FSS

| 20

However, the question is whether the insured person is in fact incapacitated in the relevant way, and all evidence probative of that

question that is brought into existence between the date of assessment and the date of the determination must be

taken into account.’

The required incapacity must exist as at the end of the period.

Later evidence cannot be discounted in favour of evidence contemporaneous with the date of assessment.

1 Deteriorations

Hellessey v MetLife

| 21

• Former police officer

• Witnessed numerous traumatic events during course of

employment

• Medically discharged on basis developed PTSD, Major Depressive

Disorder and Anxiety

• Insurer decline strong emphasis on preferring evidence closer in

proximity to DOA

1 Deteriorations

Hellessey v MetLife

| 22

‘The question is whether the claimant’s incapacity satisfies the clause at the assessment date, not whether the prognosis as at the assessment date suggested that the ETE clause is satisfied’.

‘Consequently, where time elapses after the assessment date before the insurer decides whether it is satisfied that the TPD definition has been established, the insurer must have due regard to all medical and other evidence concerning the likely consequences of the claimant’s incapacity as at the assessment date that becomes available.’

1 Deteriorations

Hellessey v MetLife

| 23

• In the case of psychological injuries such as PTSD, some

members will recover and others’ psychological injuries

will become chronic, and they will not recover

• The evidence available as at the assessment date may

be an unsound basis for determining whether the TPD

clause has been satisfied

• The consequences of later and particularly longitudinal

evidence may be a more reliable guide to the true nature

of the claimant’s incapacity as at the assessment date

1 Deteriorations

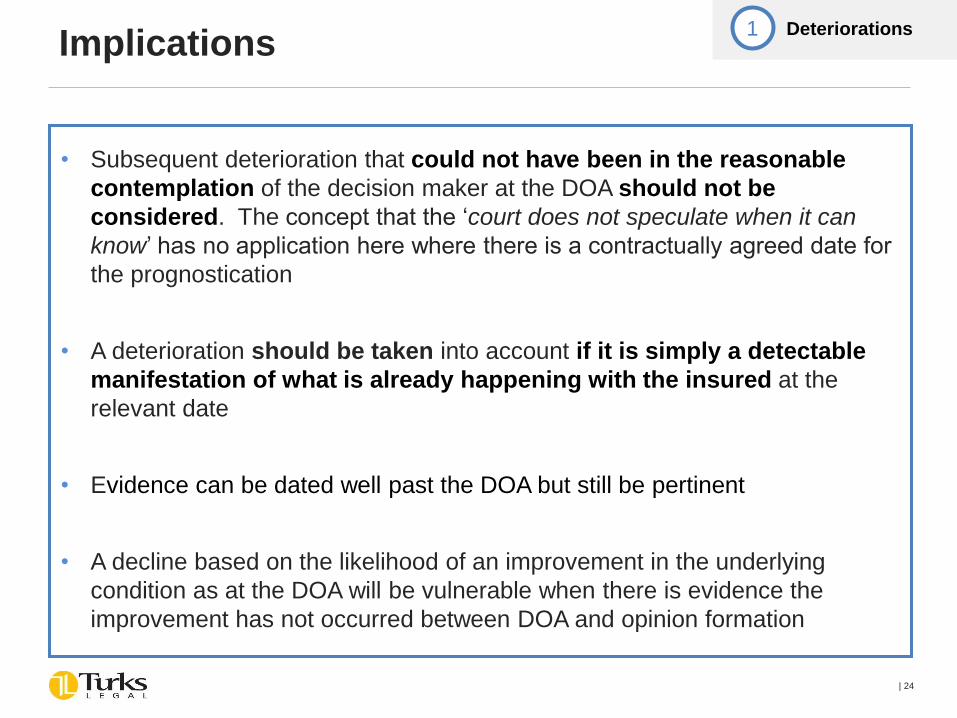

• Subsequent deterioration that could not have been in the reasonable

contemplation of the decision maker at the DOA should not be

considered. The concept that the ‘court does not speculate when it can

know’ has no application here where there is a contractually agreed date for

the prognostication

• A deterioration should be taken into account if it is simply a detectable

manifestation of what is already happening with the insured at the

relevant date

• Evidence can be dated well past the DOA but still be pertinent

• A decline based on the likelihood of an improvement in the underlying

condition as at the DOA will be vulnerable when there is evidence the

improvement has not occurred between DOA and opinion formation

Implications

| 24

1 Deteriorations

Subsequent Deteriorations

Subsequent Injuries

Subsequent Job Applications

Subsequent Work

Summary

| 25

1

2

3

4

5

Fresh Injury

| 26

Fresh injury (unrelated to existing condition)

Deterioration

(in existing condition)

Date of Assessment

Date of Assessment

Date Opinion Formed

Date Opinion Formed

Fresh injury not

considered ✔

Should the Deterioration be

taken into account?

2 Subsequent Injury

▪ Events need not be taken into account if not indicative of true state of affairs

at DOA

▪ e.g. the occurrence of a wholly unrelated frank injury does not need to be

taken into account for the TPD question because it cannot be relevant to

true state of affairs as at the DOA

▪ However, will be trickier where it is possible to link the new injury to the

existing condition at DOA

Implications

| 27

2 Subsequent Injury

Subsequent Deteriorations

Subsequent Injuries

Subsequent Job Applications

Subsequent Work

Summary

| 28

1

2

3

4

5

• Insured’s submitting failed job applications (often occurring

years after DOA) as evidence TPD

• How should they be treated in context of the likelihood of the

insured returning to a suitable occupation as at the DOA?

Job Applications

| 29

3 Job Applications

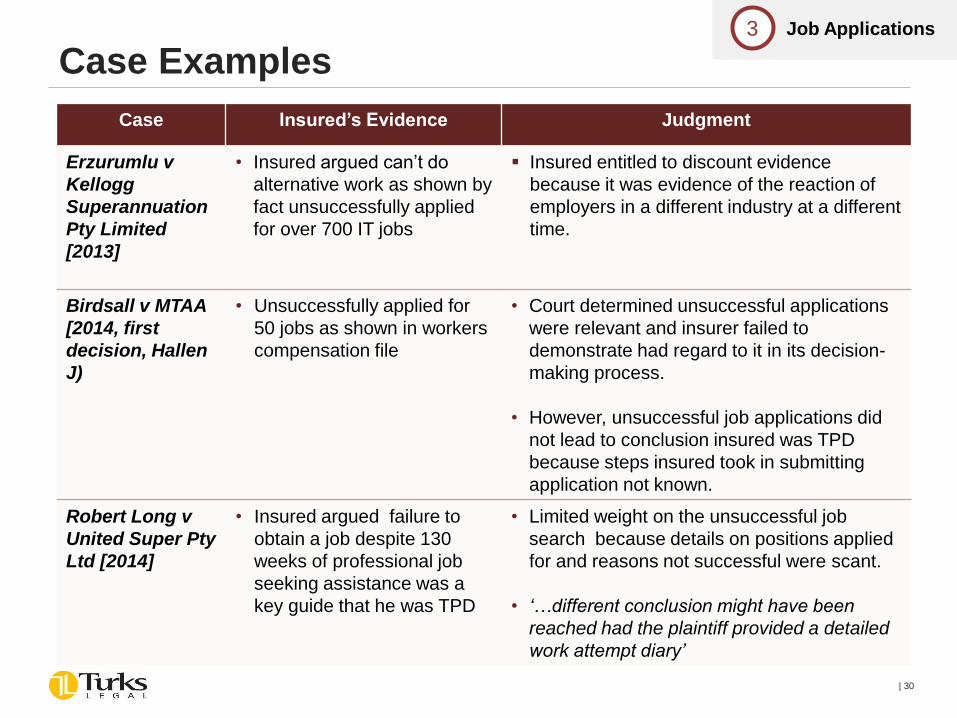

Case Examples

| 30

3 Job Applications

Case Insured’s Evidence Judgment

Erzurumlu v

Kellogg

Superannuation

Pty Limited

[2013]

• Insured argued can’t do

alternative work as shown by

fact unsuccessfully applied

for over 700 IT jobs

▪ Insured entitled to discount evidence

because it was evidence of the reaction of

employers in a different industry at a different

time.

Birdsall v MTAA

[2014, first

decision, Hallen

J)

• Unsuccessfully applied for

50 jobs as shown in workers

compensation file

• Court determined unsuccessful applications

were relevant and insurer failed to

demonstrate had regard to it in its decision-

making process.

• However, unsuccessful job applications did

not lead to conclusion insured was TPD

because steps insured took in submitting

application not known.

Robert Long v

United Super Pty

Ltd [2014]

• Insured argued failure to

obtain a job despite 130

weeks of professional job

seeking assistance was a

key guide that he was TPD

• Limited weight on the unsuccessful job

search because details on positions applied

for and reasons not successful were scant.

• ‘…different conclusion might have been

reached had the plaintiff provided a detailed

work attempt diary’

• Unsuccessful job applications should be treated as a factor relevant to

whether insured TPD as at DOA

• Court’s reasoning appears to be that failed job applications cast light on the

insured’s employability as at (and since) the DOA

• However, the extent of its relevance will depend on what is known about the

failed job applications weighed against the medical evidence

• Failed job applications that are well past the DOA should not be a significant

factor absent compelling evidence

Implications

| 31

3 Job Applications

Subsequent Deteriorations

Subsequent Injuries

Subsequent Job Applications

Subsequent Work

Summary

| 32

1

2

3

4

5

• Focus on returns to ETE work after DOA but before opinion

formed

• How far is such subsequent employment relevant?

Returns to Work

| 33

4 Subsequent Work

Case Examples

| 34

4 Subsequent Work

Case Facts Judgment

Halloran v

Harwood

Nominees Pty

Ltd [2007

NSWSC]

• Insured ceased working as

a greaser in May 1996 due

to back problems

• Requalified and returned to

work outside of DOA ETE 3

years later

• ‘If Mr Halloran had returned to

work as a greaser or had

returned to heavy labour that

would prove that he could

not have been permanently

disabled for work for which he

was suited as at the relevant

date for assessment’

Panos v FSS

Trustee

Corporation

[2015

NSWSC]

• DOA November 2011

• September 2012 - Insured

completed a return to work

trial nursing home

• October 2012 - offered

casual position in that role

• Judge found insured was not

TPD given the subsequent work

performed:

o was within ETE at DOA;

o proved the insured was

capable of doing that work

at the DOA

SCT Example

| 35

4 Subsequent Work

Case Facts Determination

SCT

Determination

– D14-15\165

• Insured returned after DOA

to employment within ETE

• Insurer denied claim based

primarily on return to work

• Insurer’s decision fair and

reasonable

• ‘May take account of actual

events arising after the qualifying

period, providing those events

follow a probable course of

events arising from the

complainant’s condition at the

end of the qualifying period’

Williams v Mercer Super (QDC, Dec 2017)

| 36

4 Subsequent Work

Facts Judgment

Plaintiff ceased work with a

merchant bank in October

2009

Claimed TPD due to health

problems including

fibromyalgia

Subsequently worked an hour

or so per week for husband’s

business

Commenced a law degree in

2012, received credits and

distinctions whilst claim being

considered

2015: completed her law

degree

• More significant emphasis on the study

undertaken than the work performed

• ‘Because the plaintiff demonstrated

tenacious resilience for three years in

spite of those symptoms, it is likely that

she can summons the same tenacious

resilience if called upon to do part-time

administrative work. That causes me to

doubt the pessimism of the plaintiff, her

husband and Dr Stringer. The plaintiff’s

academic achievements make more

credible the opinions of doctors…who

each accept the plaintiff has an ability

to handle part-time work, at least’

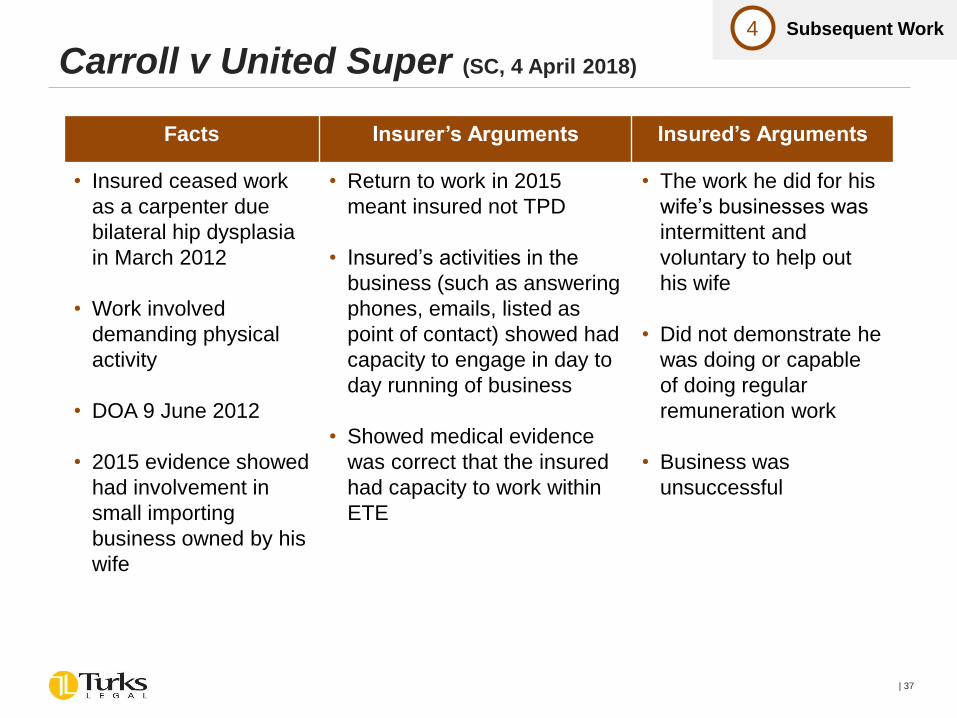

Carroll v United Super (SC, 4 April 2018)

| 37

4 Subsequent Work

Facts Insurer’s Arguments Insured’s Arguments

• Insured ceased work

as a carpenter due

bilateral hip dysplasia

in March 2012

• Work involved

demanding physical

activity

• DOA 9 June 2012

• 2015 evidence showed

had involvement in

small importing

business owned by his

wife

• Return to work in 2015

meant insured not TPD

• Insured’s activities in the

business (such as answering

phones, emails, listed as

point of contact) showed had

capacity to engage in day to

day running of business

• Showed medical evidence

was correct that the insured

had capacity to work within

ETE

• The work he did for his

wife’s businesses was

intermittent and

voluntary to help out

his wife

• Did not demonstrate he

was doing or capable

of doing regular

remuneration work

• Business was

unsuccessful

Judgment

| 38

Judgment

• The work performed by insured was relevant to TPD question

• Held the work performing in the business was unprofitable and of an intermittent

nature did not qualify as regular remunerative work

• Evidence only showed had capacity to undertake some tasks in an undemanding

situation

• Determined insured was TPD

4 Subsequent Work

Judgment

| 39

‘…And the Court concludes that he underplayed his involvement in the business. But the cross-examination did not establish that this business…was capable of providing regular remunerative work for Mr Carroll. Nor did it establish that Mr Carroll was sufficiently regularly involved in the administration of the business that his activity could be used as a signpost of his capacity to perform regular remunerative work’

4 Subsequent Work

• Returns to ETE work clearly relevant and may be decisive

• Critical issue is whether the return to ETE work demonstrates one can

continue that work on a sustained basis

• Returns to work in a family business will be more closely scrutinised as to

whether such work truly reflects ability to cope with day to day stresses of

work or attend work on a sustained basis

• Returns to work outside of ETE may still be relevant to showing capacity as

at DOA

Implications

| 40

4 Subsequent Work

Subsequent Deteriorations

Subsequent Injuries

Subsequent Job Applications

Subsequent Work

Summary

| 41

1

2

3

4

5

▪ Qualification for DSP includes a requirement that the person has a continual

inability to work as defined under the Social Security Act 1991

▪ Authorities accept that issue must be considered based on the applicants

situation as it was at the time of the application for the DSP

▪ How have DSP cases treated subsequent events which occur after the DSP

date of assessment ?

| 42

Disability Support Pension5 Summary

Leading Principles:

• Subsequent events relevant if “referable to the Applicant’s condition during the

qualification period.”

• Evolution of a medical condition relevant to weight place on competing opinions:

• ‘Any subsequent evolution of a particular condition might be relevant to any

weight the Tribunal places on competing prognostications…is not open in law for

this Tribunal to use any evidence of such progression [of a medical condition] to

directly award a DSP because of those changed circumstances’.

[Bobera and the Secretary, Department of Families, Housing, Community Services and Indigenous Affairs [2012]

• Shouldn’t use hindsight!

• ‘While hindsight may suggest that treatment did not result in improvement within

two years, that is not the question for the Tribunal to determine…For that reason,

evidence of treatment, and the efficacy of that treatment, after the qualification

period is not directly relevant to the Tribunal’s decision.’

[Fanning and Secretary, Department of Social Services 2014]

DSP approach to subsequent events

| 43

5 Summary

Key Takeaways – Deteriorations

| 44

✓ A deterioration should be taken into account if it illuminates an existing

state of affairs. Courts will strain to classify subsequent events in this

longitudinal way

✓ The key is whether subsequent evidence is “pertinent to the determination

of the appellant’s condition at the relevant time”

✓ Avoid discounting evidence well past the DOA in favour of evidence closer

to the DOA just because of the temporal difference

✓ Use language which demonstrates subsequent changes were considered

to determine the true state of affairs at the DOA

5 Summary

✓The occurrence of a wholly unrelated frank injury or illness is not required to

be taken into account because cannot be indicative of the true state of

affairs as at the DOA

✓If this applies, ensure documentation reflects new conditions are not relevant

to the state of affairs at the DOA

Key Takeaways – Subsequent Injury

| 45

4 Returns to Work5 Summary

Key Takeaways – Job Applications

| 46

✓Ensure assessment documentation reflects took into account

unsuccessful job applications as relevant to TPD question

✓In terms of weight to give to such unsuccessful applications

consider:

✓Types of roles applied for – were they realistically within

insured’s ETE?

✓Evidence regarding depth and breadth of job seeking effort

✓Unsuccessful applications are of limited importance absent

compelling evidence regarding roles applied for, efforts to obtain

those roles and reasons for rejection

5 Summary

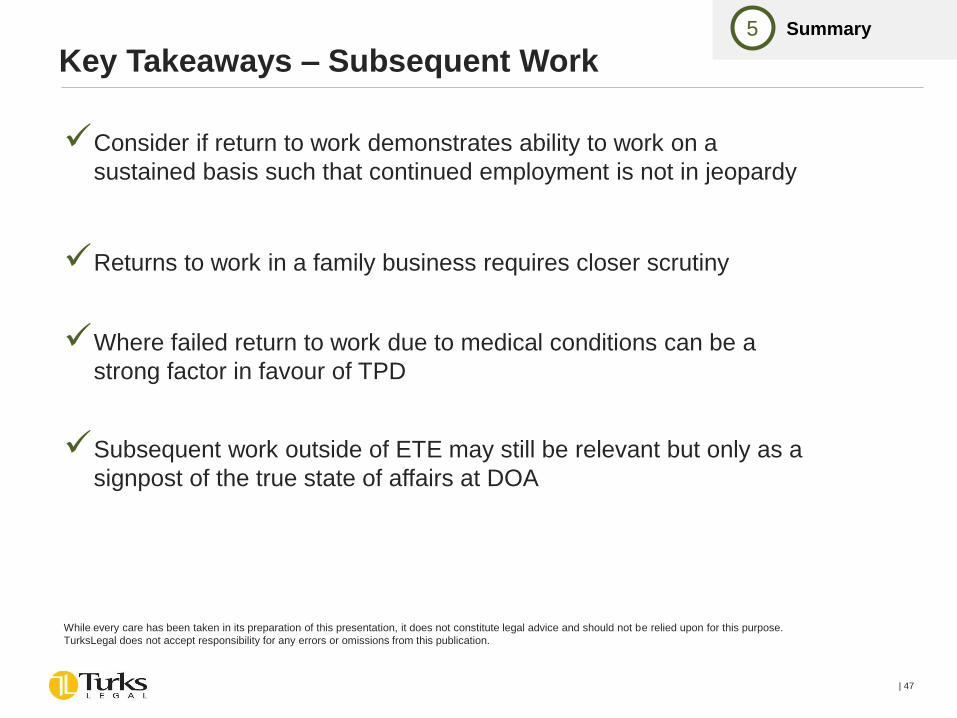

Key Takeaways – Subsequent Work

| 47

✓Consider if return to work demonstrates ability to work on a

sustained basis such that continued employment is not in jeopardy

✓Returns to work in a family business requires closer scrutiny

✓Where failed return to work due to medical conditions can be a

strong factor in favour of TPD

✓Subsequent work outside of ETE may still be relevant but only as a

signpost of the true state of affairs at DOA

While every care has been taken in its preparation of this presentation, it does not constitute legal advice and should not be relied upon for this purpose.

TurksLegal does not accept responsibility for any errors or omissions from this publication.

5 Summary

For more information,

please contact:

turkslegal.com.au

Darryl Pereira

Partner

02 8257 5718

Sydney 02 8257 5700 Melbourne 03 8600 5000 Brisbane 07 3212 6700 Newcastle 02 8257 5700

Sofia Papachristos

Partner

03 8600 5049

TPD Claims – The Next FrontierCMG ALUCA Presentation

Presented by Nicholas Matkovich and Diren Fernando

19 April 2018

Overview

What’s next? Unresolved issues in TPD assessments

• The duty of utmost good faith – what are its implications?

• Determining the Date for Assessment

• Issues re ETE

• The trustee’s duty

• Making use of Section 29(6) ICA

51

Court’s reviewing Insurer’s (-and Trustee’s) Decisions

• Stage One Enquiry

– Whether the decisions to decline a claim can be set aside because the decisions have been made in breach of the duties owed by the trustee and the insurer.

52

Court’s reviewing Insurer’s (-and Trustee’s) Decisions

• Stage Two Enquiry– Assuming the decisions to decline a claim can be set

aside, the Court will then reserve to itself the assessment of whether the claimant is entitled to the TPD benefit on the basis of the whole of the evidence including events which have occurred after the insurer’s decision to decline the claim.

Hannover Life v Sayseng [2005] NSWCA 214

Birdsall v MTAA Superannuation Fund Pty Ltd [2015] NSWCA 104

53

Separate Determination

• The Court can determine the First and Second Stage enquiries separately.

• In fact, Courts in NSW have been prepared to order separate determinations of the First and Second Stage issues. In reviewing the First Stage, the Court will usually limit its review to the material which was before the insurer.

Note: Wild v FSS [2017] NSWSC 237

Annan v FSS [2017] NSWSC 1453

54

Duties of Decision Makers

• Trustee– The trustee is required to act in good faith, on a real

and genuine consideration of the material before it, for the purpose for which it was conferred, for sound reasons where reasons are disclosed, although the trustee is not obliged to give reasons for its decision.

Hannover Life v Sayseng [2005] NSWCA 214

55

Insurer

• Duty of Utmost Good Faith / Good Faith

– Imposes an obligation on the insurer to exercise its rights and discharge its obligations under the insurance contract with utmost good faith.

Ziogos v FSS [2015] NSWSC 1385

56

Insurer

• Duty to Form an Opinion– Subjective TPD Definition

• The insurer is obliged to act reasonably in considering and determining the issue. Test of reasonableness is whether the opinion formed by the insurer was not open to an insurer acting reasonably and fairly in consideration of the claim.

• The assessment of reasonableness is based on the material before the insurer at the time. The assessment of reasonableness does not require the Court to undertake a review of the merits of the insurer’s decision.

Edwards v The Hunter Valley Co-op Dairy Co Ltd (1992) 7 ANZ Ins Cas 61-113

Hannover Life v Jones [2017] NSWCA 233

57

Insurer

• Duty to Give Reasons

– Insurer should give reasons for its decisions

Ziogos v FSS [2015] NSWSC 1385

58

Issues around duty of good faith

• The claims handling process

• “Investigating” the Claim

• The evidence presented in support of a Claim Decline

• What standard is expected in a Decline Letter?

59

Focus on the Trustee’s duty

Superannuation Industry (Supervision) Act 1993 (Cth)

(7) The covenants referred to in subsection (1) include the following covenants by each trustee of the entity:

(d) to do everything that is reasonable to pursue an insurance claim for the benefit of a beneficiary, if the

claim has a reasonable prospect of success.

What does this mean?

60

Interpretation of ETE Clause

• ETE Clause– ‘Reasonably fitted by education, training or

experience’, expresses notion of a link or connection between future work and the insured’s past education, training or experience.

Hannover Life v Jones [2017] NSWCA 233

61

Interpretation of ETE Clause

• ‘Unlikely Ever’

– No real chance of employment, as distinct from a remote or speculative possibility of employment.

TAL Life Ltd v Shuetrim (2016) 91 NSWLR 439

62

Interpretation of ETE Clause

• ‘Regular Remuneration Work’– Capacity to perform ‘regular remunerative work’ is

different from the capacity to perform a particular work task.

– The physical capacity to perform one or more work tasks does not mean a person has the ability to engage in remunerative work.

Hannover Life v Colella (2014) VSCA 205

Jones v United Super [2016] NSWSC 1551

63

Interpretation of ETE Clause

• ‘Regular Remuneration Work’

– A person can be reasonably fitted for ‘Regular Remuneration Work’ by reason of education ortraining or experience, or a combination of them.

Hannover Life v Dargan [2013] NSWCA 57

64

Interpretation of ETE Clause

• ‘Regular Remuneration Work’– Part-Time Work– Regular Casual Work

– BUT NOT Irregular and occasional casual/intermittent work

Hannover Life v Dargan [2013] NSWCA 57

Manglicmot v CBOSC Pty Ltd [2011] NSWCA 204

65

Unanswered Questions re ETE

• Need for the insurer to adduce evidence of the local labour market

• What to do with pre-career occupations

66

Date for Assessment of TPD Status

• The date for assessment to determine TPD Status is the expiration of the applicable qualifying period as the relevant date.

Halloran v Harwood Nominees [2007] NSWSC 913

67

Difficulties in determining the Date for Assessment

• How to address repeated cessations of work?

ADD TIMELINE GRAPHIC

68

Use of Subsequent Medical and Other Evidence

• Later expert opinions may be relevant to and may be taken into account when the Court is considering the probability of claimant being able to engage in suggested occupations at the date for assessment.

TAL Life Ltd v Shuetrim (2016) 91 NSWLR 439

69

Difficulties in interpreting later medical evidence

• How to deal with retrospective ‘prognoses’

• How to think about ‘likelihood’

70

Remedies for Misrepresentation and Non-Disclosure

Section 29

(6) If the insurer has not avoided the contract or has not varied the contract under subsection (4), the insurer may, by notice in writing given to the insured, vary the contract in such a way as to place the insurer in the position (subject to subsection (7)) in which the insurer would have been if the duty of disclosure had been

complied with or the misrepresentation had not been made. ...(7) The position of the insurer under a contract (the relevant contract ) that is varied under subsection (6) must not be inconsistent with the position in which other reasonable and prudent insurers would have been if:

(a) they had entered into similar contracts of life insurance to the relevant contract; and

(b) there had been no failure to comply with the duty of disclosure, and no misrepresentation, by the insureds under the similar contracts before they

were entered into.

71

Use of Section 29(6)

• What evidence needs to be marshalled to use the remedy?

• What consideration needs to be given to section 29(7) at an early stage?

72

QUESTIONS?

73

Team Contacts

Nicholas Matkovich

Partner

P +61 2 9334 8531

Diren Fernando

Special Counsel

P +61 2 9334 8641

74

Adelaide | Brisbane | Canberra | Darwin | Hobart | Melbourne | Norwest | Perth | Sydney