a.j. noronha - dow case study

TRANSCRIPT

Important Disclosure This presentation is for investor informational purposes only. This document does not constitute an offer to sell or a solicitation of an offer to buy. An offer may be made only by the delivery of the Fund’s Confidential Private Placement Memorandum, Partnership Agreement and related documents, and any offer is subject to the terms of such documents. Investors should refer to these documents before considering an investment. Although this presentation has been prepared from sources deemed reliable, no representations can be made as to the accuracy and completeness of this presentation. Hedge funds are highly speculative investments that involve a high degree of risk. Investors can lose all or a substantial amount of their investment. There is no established secondary market for hedge fund interests. High fees and expenses in a hedge fund may significantlyreduce net investor capital. Past performance is not indicative of future results. References to market indices are for comparison purposes only. This document is proprietary to Desai Capital Management, LLC (“Desai” or“ DCM”) and must be held in strict confidence; it is intended only for authorized recipients. This document may not be used, disclosed, copied, or reproduced in any format, in whole or in part, without the express written permission of DCM.

2

Blue-chip industry leader with multiple significant catalysts:

Market price lags intrinsic value

50% decline in input prices = immense cost savings and increased product demand

Multiple activist investors to help unlock value

Any one of these catalysts could unlock value on its own, but bringing them all together positions DOW for a large potential synergistic effect

Our Thesis:

4

Industry Leader The chemical industry has seen massive consolidation, with Dow firmly established as the #2 global company behind only Germany’s BASF 1

1: http://www.statista.com/statistics/272704/top-10-chemical-companies-worldwide-based-on-revenue/

DCM uses a fundamental-driven investment approach to determine a given company’s intrinsic value

Our approach is rooted in the value investing principles successfully used by Buffett, Graham, Klarman, and Marks among others Mr. Desai has substantial equity research & portfolio management experience, with a focus on fundamental-driven investing

Our internal analysis identified an intrinsic value range of $55-60 (next slide; we believe valuation ranges provide a margin of safety)

DOW reached a 52-week high of $54.97, but was trading near 52-week lows between $41-45 when we entered the position We identified a 25%+ upside, with limited downside due to the catalysts discussed within

We continue to hold a long position as we believe there is still appreciation potential, DOW is still trading below intrinsic value, and our catalysts have yet to fully play out

Market value lags intrinsic value

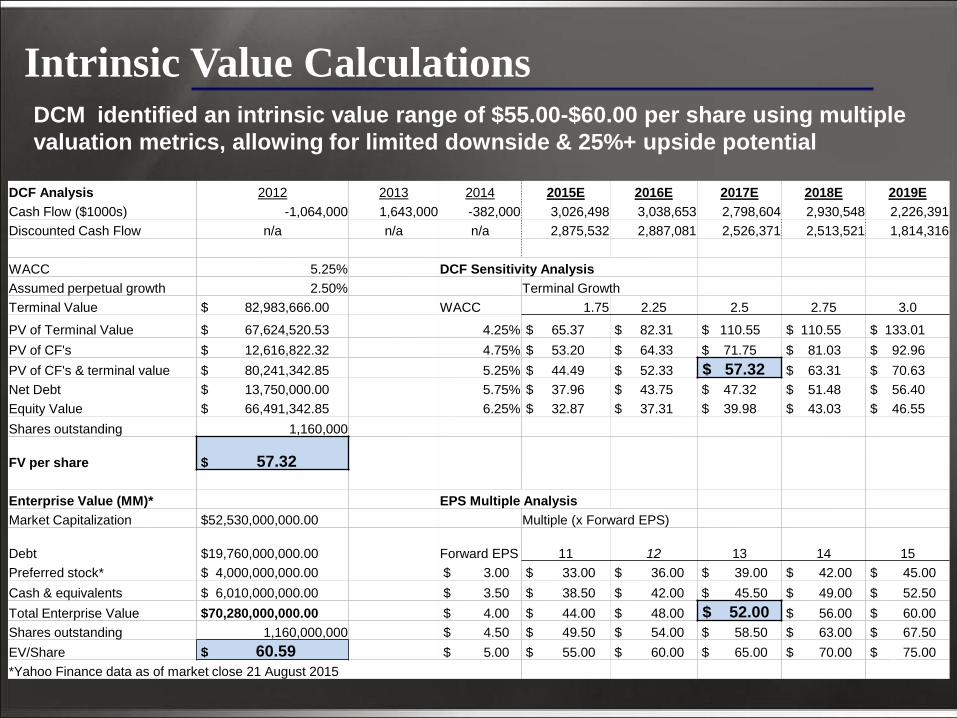

Intrinsic Value Calculations

2

DCM identified an intrinsic value range of $55.00-$60.00 per share using multiple

valuation metrics, allowing for limited downside & 25%+ upside potential

DCF Analysis 2012 2013 2014 2015E 2016E 2017E 2018E 2019E

Cash Flow ($1000s) -1,064,000 1,643,000 -382,000 3,026,498 3,038,653 2,798,604 2,930,548 2,226,391

Discounted Cash Flow n/a n/a n/a 2,875,532 2,887,081 2,526,371 2,513,521 1,814,316

WACC 5.25% DCF Sensitivity Analysis

Assumed perpetual growth 2.50% Terminal Growth

Terminal Value $ 82,983,666.00 WACC 1.75 2.25 2.5 2.75 3.0

PV of Terminal Value $ 67,624,520.53 4.25% $ 65.37 $ 82.31 $ 110.55 $ 110.55 $ 133.01

PV of CF's $ 12,616,822.32 4.75% $ 53.20 $ 64.33 $ 71.75 $ 81.03 $ 92.96

PV of CF's & terminal value $ 80,241,342.85 5.25% $ 44.49 $ 52.33 $ 57.32 $ 63.31 $ 70.63

Net Debt $ 13,750,000.00 5.75% $ 37.96 $ 43.75 $ 47.32 $ 51.48 $ 56.40

Equity Value $ 66,491,342.85 6.25% $ 32.87 $ 37.31 $ 39.98 $ 43.03 $ 46.55

Shares outstanding 1,160,000

FV per share $ 57.32

Enterprise Value (MM)* EPS Multiple Analysis

Market Capitalization $52,530,000,000.00 Multiple (x Forward EPS)

Debt $19,760,000,000.00 Forward EPS 11 12 13 14 15

Preferred stock* $ 4,000,000,000.00 $ 3.00 $ 33.00 $ 36.00 $ 39.00 $ 42.00 $ 45.00

Cash & equivalents $ 6,010,000,000.00 $ 3.50 $ 38.50 $ 42.00 $ 45.50 $ 49.00 $ 52.50

Total Enterprise Value $70,280,000,000.00 $ 4.00 $ 44.00 $ 48.00 $ 52.00 $ 56.00 $ 60.00

Shares outstanding 1,160,000,000 $ 4.50 $ 49.50 $ 54.00 $ 58.50 $ 63.00 $ 67.50

EV/Share $ 60.59 $ 5.00 $ 55.00 $ 60.00 $ 65.00 $ 70.00 $ 75.00

*Yahoo Finance data as of market close 21 August 2015

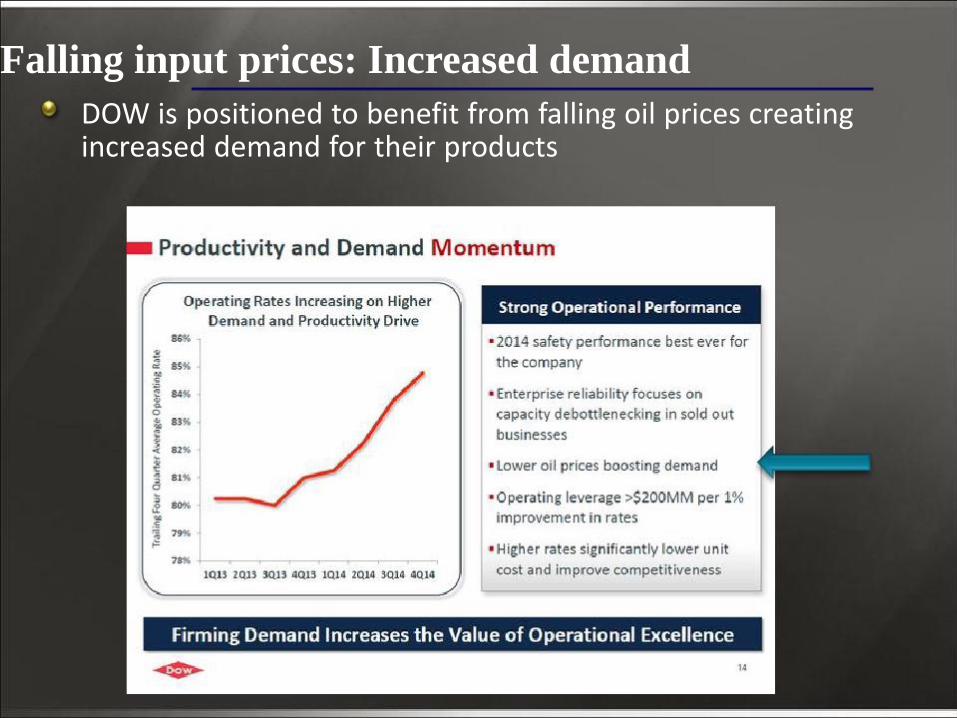

DOW is positioned to benefit from falling oil prices creating increased demand for their products

Falling input prices: Increased demand

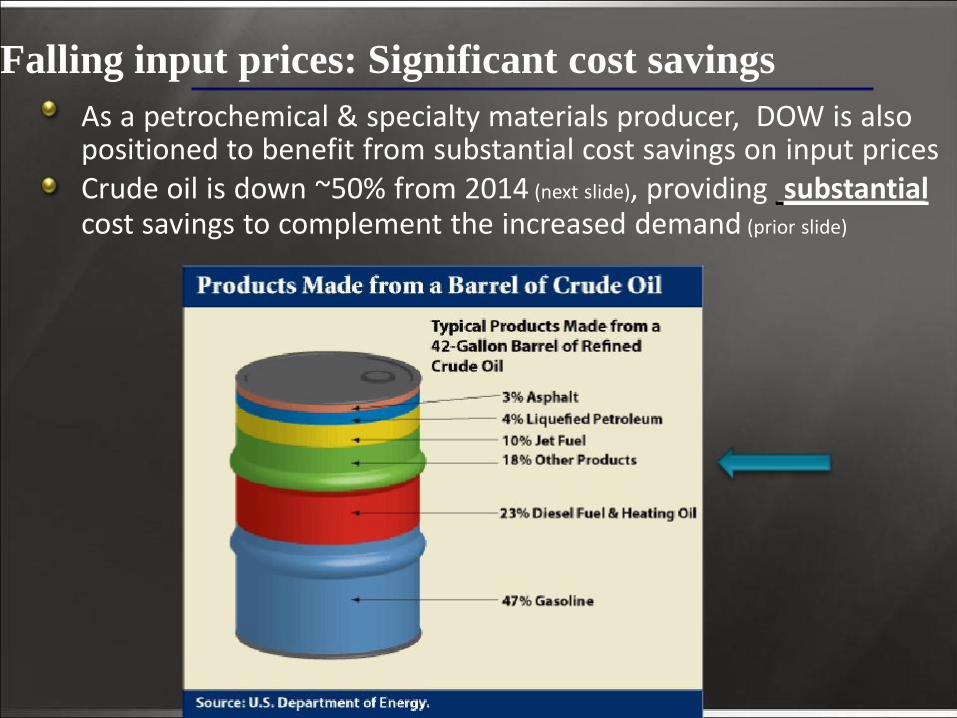

As a petrochemical & specialty materials producer, DOW is also positioned to benefit from substantial cost savings on input prices Crude oil is down ~50% from 2014 (next slide), providing substantial cost savings to complement the increased demand (prior slide)

Falling input prices: Significant cost savings

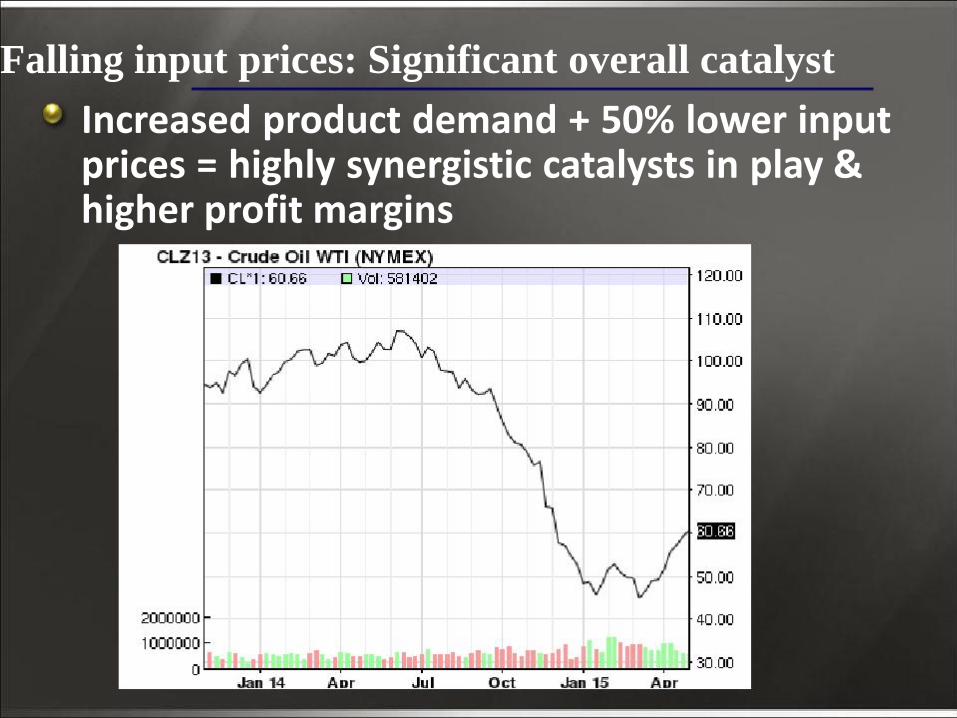

Increased product demand + 50% lower input prices = highly synergistic catalysts in play & higher profit margins

Falling input prices: Significant overall catalyst

2: http://www.economist.com/news/leaders/21642169-why-activist-investors-are-good-public- company-capitalisms-unlikely-heroes

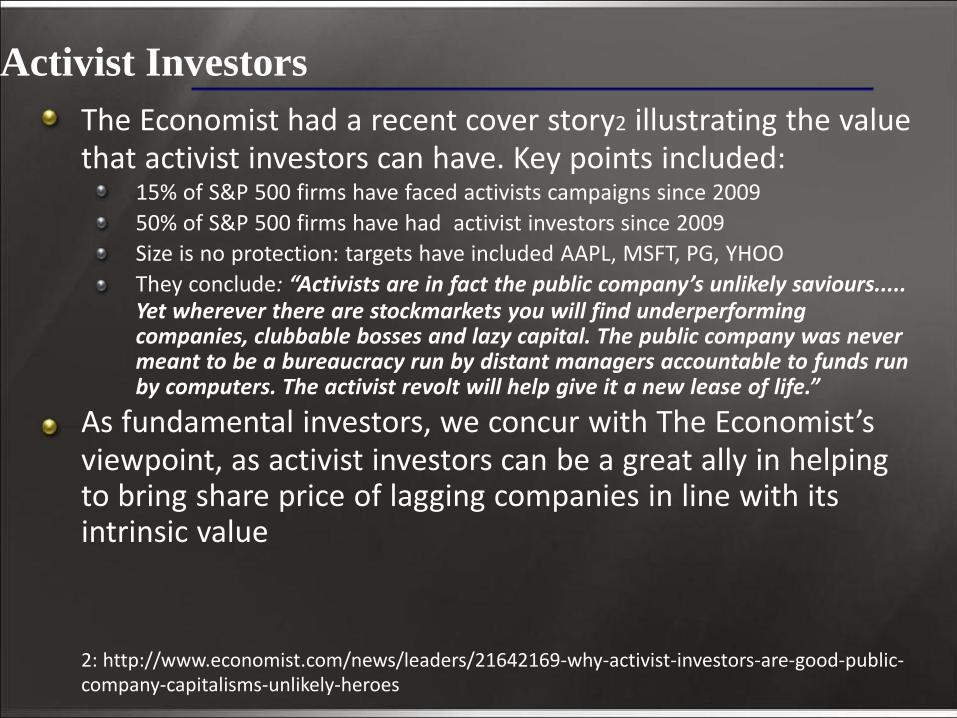

Activist Investors

The Economist had a recent cover story2 illustrating the value that activist investors can have. Key points included: 15% of S&P 500 firms have faced activists campaigns since 2009

50% of S&P 500 firms have had activist investors since 2009

Size is no protection: targets have included AAPL, MSFT, PG, YHOO

They conclude: “Activists are in fact the public company’s unlikely saviours..... Yet wherever there are stockmarkets you will find underperforming companies, clubbable bosses and lazy capital. The public company was never meant to be a bureaucracy run by distant managers accountable to funds run by computers. The activist revolt will help give it a new lease of life.”

As fundamental investors, we concur with The Economist’s viewpoint, as activist investors can be a great ally in helping to bring share price of lagging companies in line with its intrinsic value

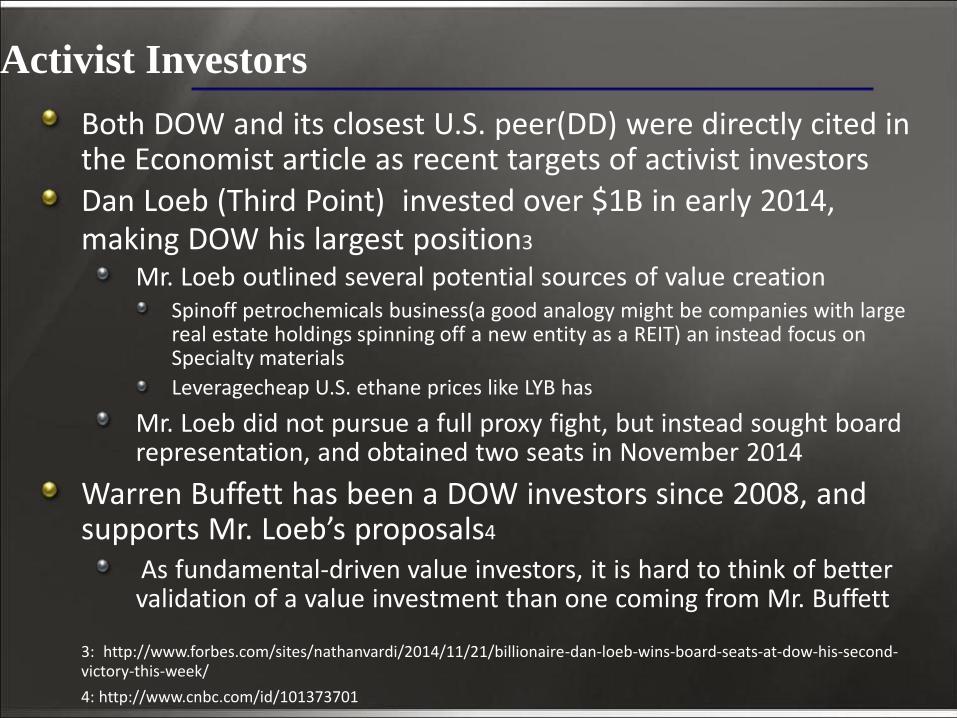

Both DOW and its closest U.S. peer(DD) were directly cited in the Economist article as recent targets of activist investors

Dan Loeb (Third Point) invested over $1B in early 2014, making DOW his largest position3

Mr. Loeb outlined several potential sources of value creation Spinoff petrochemicals business(a good analogy might be companies with large real estate holdings spinning off a new entity as a REIT) an instead focus on Specialty materials

Leveragecheap U.S. ethane prices like LYB has

Mr. Loeb did not pursue a full proxy fight, but instead sought board representation, and obtained two seats in November 2014

Warren Buffett has been a DOW investors since 2008, and supports Mr. Loeb’s proposals4

As fundamental-driven value investors, it is hard to think of better validation of a value investment than one coming from Mr. Buffett

3: http://www.forbes.com/sites/nathanvardi/2014/11/21/billionaire-dan-loeb-wins-board-seats-at-dow-his-second- victory-this-week/

4: http://www.cnbc.com/id/101373701

Activist Investors

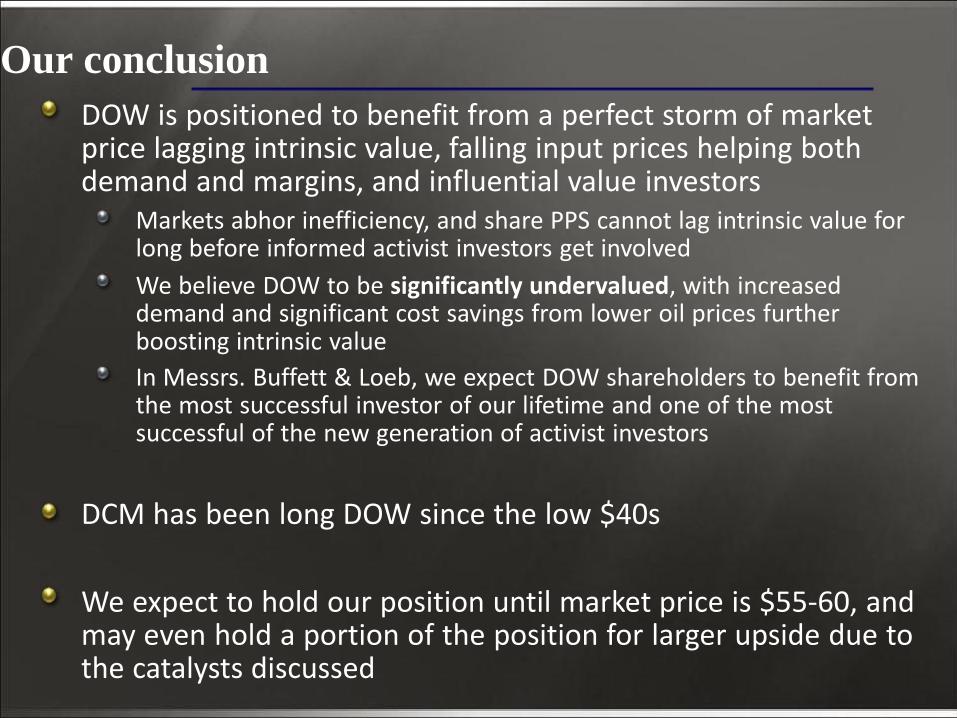

DOW is positioned to benefit from a perfect storm of market price lagging intrinsic value, falling input prices helping both demand and margins, and influential value investors

Markets abhor inefficiency, and share PPS cannot lag intrinsic value for long before informed activist investors get involved

We believe DOW to be significantly undervalued, with increased demand and significant cost savings from lower oil prices further boosting intrinsic value

In Messrs. Buffett & Loeb, we expect DOW shareholders to benefit from the most successful investor of our lifetime and one of the most successful of the new generation of activist investors

DCM has been long DOW since the low $40s

We expect to hold our position until market price is $55-60, and may even hold a portion of the position for larger upside due to the catalysts discussed

Our conclusion

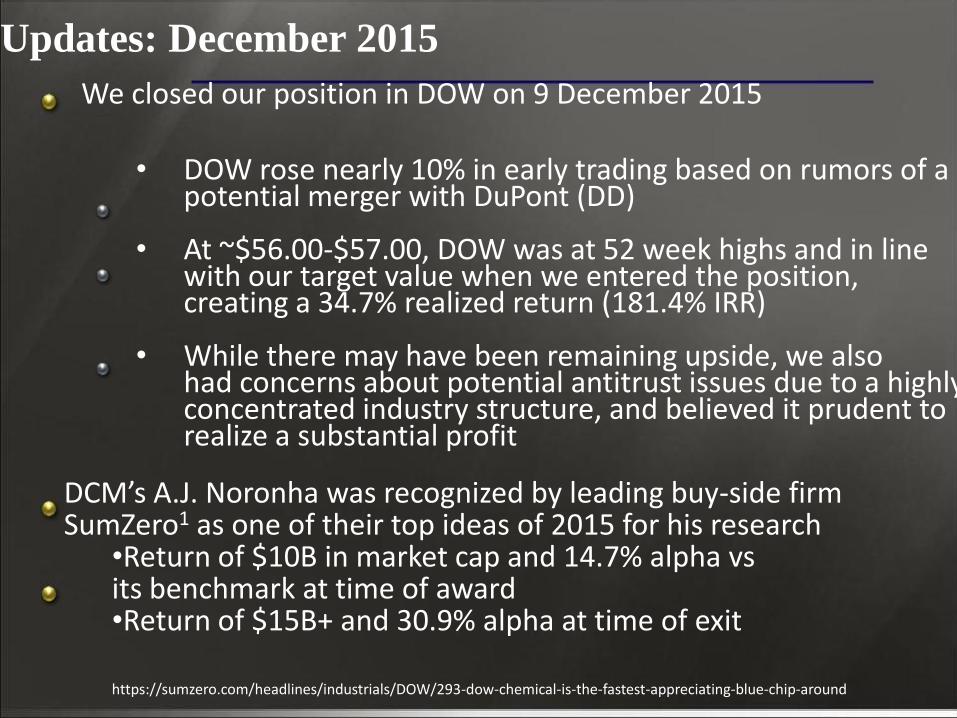

We closed our position in DOW on 9 December 2015

• DOW rose nearly 10% in early trading based on rumors of a potential merger with DuPont (DD)

• At ~$56.00-$57.00, DOW was at 52 week highs and in line with our target value when we entered the position, creating a 34.7% realized return (181.4% IRR)

• While there may have been remaining upside, we also had concerns about potential antitrust issues due to a highly concentrated industry structure, and believed it prudent to realize a substantial profit

DCM’s A.J. Noronha was recognized by leading buy-side firm SumZero1 as one of their top ideas of 2015 for his research

•Return of $10B in market cap and 14.7% alpha vs its benchmark at time of award •Return of $15B+ and 30.9% alpha at time of exit

https://sumzero.com/headlines/industrials/DOW/293-dow-chemical-is-the-fastest-appreciating-blue-chip-around

Updates: December 2015