agriminco- mda (cedar) 29 august 2014 mda (cedar) 29 august 2014.pdf · agriminco corp. management...

TRANSCRIPT

AgriMinco Corp.

Management’s Discussion and Analysis For the three and nine months ended June 30, 2014

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

2

Introduction

Unless the context suggests otherwise, references to “AgriMinco”, “the Company”, “Issuer”, “ANO” or similar terms refer to AgriMinco Corp.

This Management’s Discussion and Analysis (“MD&A”) is a discussion and review of operations, current financial position and outlook for AgriMinco and should be read in conjunction with the unaudited condensed interim consolidated financial statements of the Company for the three and nine months ended June 30, 2014 and the audited consolidated financial statements and related notes for the year ended September 30, 2013.

All amounts included in the MD&A are reported in Canadian dollars, unless otherwise specified.

The MD&A is based upon the financial statements prepared in accordance with International Financial Reporting Standards (“IFRS”). This MD&A is dated as of August 29, 2014 and includes activities through to this date unless otherwise indicated.

Forward Looking Information

Except for statements of historical fact, the discussion and analysis of financial performance and position including, without limitation, statements regarding projections, future plans, and objectives of AgriMinco are forward-looking statements that are subject to various risks and uncertainties. Forward-looking statements are based on management experience, historical results, current expectations and analyses, trends, government policies, and current business and economic conditions, including AgriMinco’s analysis of its projects. There can be no assurance that such statements will prove to be accurate; actual results and future events could differ materially from those anticipated in such statements.

Overview of the Company

AgriMinco was incorporated under the Canada Business Corporations Act on July 12, 2010, and has continued as a company under the Business Corporations Act of Ontario. AgriMinco is principally engaged in the acquisition, exploration and development of agricultural mineral projects across Africa. On March 9, 2011, Ethiopian Potash Corp (‘EPC’) completed a reverse takeover (“RTO”) with Panorama Resources Ltd. During 2013, EPC amended its articles to change its name to AgriMinco. The shares trade on the Toronto Venture Exchange (“TSX-V”) under the symbol ANO. The address of the Company’s corporate office is 200 Bay Street, Suite 3800, Toronto, Ontario, Canada. Company Restructuring

On May 13, 2014, Premier African Minerals Limited (“Premier”) exercised its option to acquire the Company’s 30% interest in the Danakil Holdings Limited (“Danakil”) joint venture, as set out in the MD&A dated March 31, 2014. In exercising the option agreement, Premier paid the following consideration to AgriMinco:

• The cancellation of 120,821,176 shares representing approximately 42% of the issued share capital of AgriMinco.

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

3

• The settlement of certain debt obligations owed by the Company to third parties up to an aggregate maximum of $1,500,000.

• The issuance of new Premier ordinary shares with a value equal to $1,000,000 based on the volume weighted average price per Premier ordinary share for the five trading days immediately in favour of AgriMinco.

Following the completion of the option agreement and the restructuring of AgriMinco, the current corporate structure comprises of an AIM listed security representing approximately 11.44% of the issued share capital of Premier and the wholly owned subsidiaries of G&B African Resources Mali SARL (“G&B Mali”) and G&B African Resources SARL (“G&B”).

Following the restructuring, the current corporate structure is illustrated below:

Material Properties

(a) Togo

Togo is an elongate country, some 56,785km2 in extent, located in West Africa and bounded by Ghana, Burkina Faso, Benin, and the Gulf of Guinea. Togo is 579km long and 160km wide at the broadest point. Infrastructure and accessibility in Togo is unsophisticated but operational. The country has 7,500km of roads, approximately a third of which are paved. Togo acts as the main transit trucking route from the coast through the region of Bassar to its northern inland neighbours. Some 568km of railway is available and there are nine airports throughout the country, two of which have paved runways. The telecommunications network is based on microwave radio relay stations and is supplemented by a mobile cellular system. Two operational ports are located at Lomé and Kpeme.

Historically, a colony of Germany and France, Togo became a democracy in 1960. Togo is a small pro-Western, market-oriented country heavily dependent on both commercial and subsistence agriculture. Togo does not have a well-developed mineral industry and mining production is limited to the mining of phosphates and limestone. Togo, supported by the World Bank and the International Monetary Fund

100% Togo Mali 100%

AGRIMINCO CORPORATION (TSX-V: ANO)

G&B AFRICAN RESOURCES SARL

G&B African Resources Mali

SARL

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

4

(“IMF”), has attempted to implement economic reform measures, encourage foreign investment, and balance revenues with expenditures.

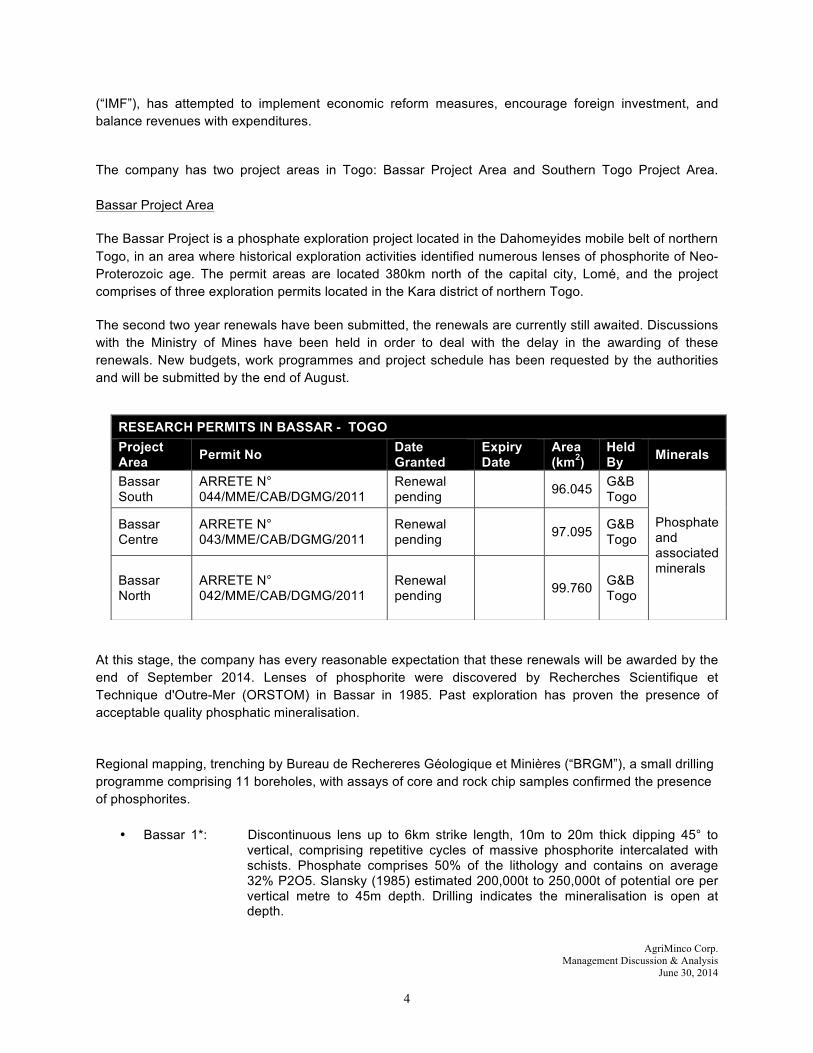

The company has two project areas in Togo: Bassar Project Area and Southern Togo Project Area. Bassar Project Area

The Bassar Project is a phosphate exploration project located in the Dahomeyides mobile belt of northern Togo, in an area where historical exploration activities identified numerous lenses of phosphorite of Neo-Proterozoic age. The permit areas are located 380km north of the capital city, Lomé, and the project comprises of three exploration permits located in the Kara district of northern Togo.

The second two year renewals have been submitted, the renewals are currently still awaited. Discussions with the Ministry of Mines have been held in order to deal with the delay in the awarding of these renewals. New budgets, work programmes and project schedule has been requested by the authorities and will be submitted by the end of August.

At this stage, the company has every reasonable expectation that these renewals will be awarded by the end of September 2014. Lenses of phosphorite were discovered by Recherches Scientifique et Technique d'Outre-Mer (ORSTOM) in Bassar in 1985. Past exploration has proven the presence of acceptable quality phosphatic mineralisation.

Regional mapping, trenching by Bureau de Rechereres Géologique et Minières (“BRGM”), a small drilling programme comprising 11 boreholes, with assays of core and rock chip samples confirmed the presence of phosphorites.

• Bassar 1*: Discontinuous lens up to 6km strike length, 10m to 20m thick dipping 45° to vertical, comprising repetitive cycles of massive phosphorite intercalated with schists. Phosphate comprises 50% of the lithology and contains on average 32% P2O5. Slansky (1985) estimated 200,000t to 250,000t of potential ore per vertical metre to 45m depth. Drilling indicates the mineralisation is open at depth.

RESEARCH PERMITS IN BASSAR - TOGO Project Area Permit No Date

Granted Expiry Date

Area (km2)

Held By Minerals

Bassar South

ARRETE N° 044/MME/CAB/DGMG/2011

Renewal pending 96.045 G&B

Togo

Phosphate and associated minerals

Bassar Centre

ARRETE N° 043/MME/CAB/DGMG/2011

Renewal pending 97.095 G&B

Togo

Bassar North

ARRETE N° 042/MME/CAB/DGMG/2011

Renewal pending 99.760 G&B

Togo

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

5

• Bassar 2*: Pascal (1989) suggested an in-situ resource of 5 Mt ore at 20% to 23% P2O5; 35-40% SiO2.

• Bassar 1* and 3*: 5 Mt ore at 32.5% to 34% P2O5; 7-11% SiO2 (Pascal 1989).

• Bassar 4*: 6km long lens with massive phosphate horizons (>36% P2O5) intercalated with barren units. Pascal estimated <5 Mt ore at 36% P2O5; 6% SiO2. *Note - the resource estimates quoted are non-compliant with any international mineral reporting codes, are in-situ estimates and have not been verified. Magnetic separation test work on the ore by BRGM produced a concentrate containing 37.18% P2O5 with no deleterious elements. The phosphoric acid obtained during test work is suitable for the production of mono-ammonium phosphate/di-ammonium phosphate fertiliser (“MAP/DAP”) as well as superphosphates. The heavy liquid separation testwork indicated that the P2O5 content of all the samples can be upgraded in the sinks fraction. Furthermore, the Fe2O3 and SiO2 content of the samples were downgraded in the sinks of all the samples. An effective method of increasing the P2O5 grade of the samples would be to separate the particles in the sample according to density using a dense media separation technique. The sinks fraction would be upgraded in terms of P2O5 and high recoveries would be achievable. The historical exploration has shown the potential of the Bassar area to contain phosphate ore of good quality and provided an excellent framework for ANO to develop a much larger Resource. An ANO in-house non-compliant estimate from the historical results shows that 20-22Mt at 28-30% P2O5 to a depth of 100m could be developed. Therefore the Company has set an initial Exploration Target of 50-55Mt at 28-30% P2O5 to 300m depth as its first objective and from this establish a fully code compliant Mineral Resource with 18 months of the renewal of the licences. Southern Togo Project ANO holds three rights in the southern coastal region of Maritime Province. The Southern Togo Project area comprises a block of contiguous rectangular exploration permits which contain separate occurrences of potentially economic phosphates and clays. The clay deposit is called the Dagbati-Watchidome attaplugite-smectite deposit. The licences abut onto the SNPT phosphate mining lease (Kpogame/Dagbati deposit) in the west and extend eastwards towards the Mono River, the border between Togo and Benin. A number of bitumen roads allow access to the project area and a well-developed network of tarred roads, secondary dirt roads and tracks service numerous towns and villages within the licence block. The WACEM-Lomé railway line passes within 2km of the project area which lies within 20km of the coast. Topographically, the relief is generally flat and low lying. No historical mining activities are known to have taken place within the permits; however the SNPT open pit phosphate mine abuts onto the project area to the west and to the northeast of the project the WACEM cement/clinker works occurs.

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

6

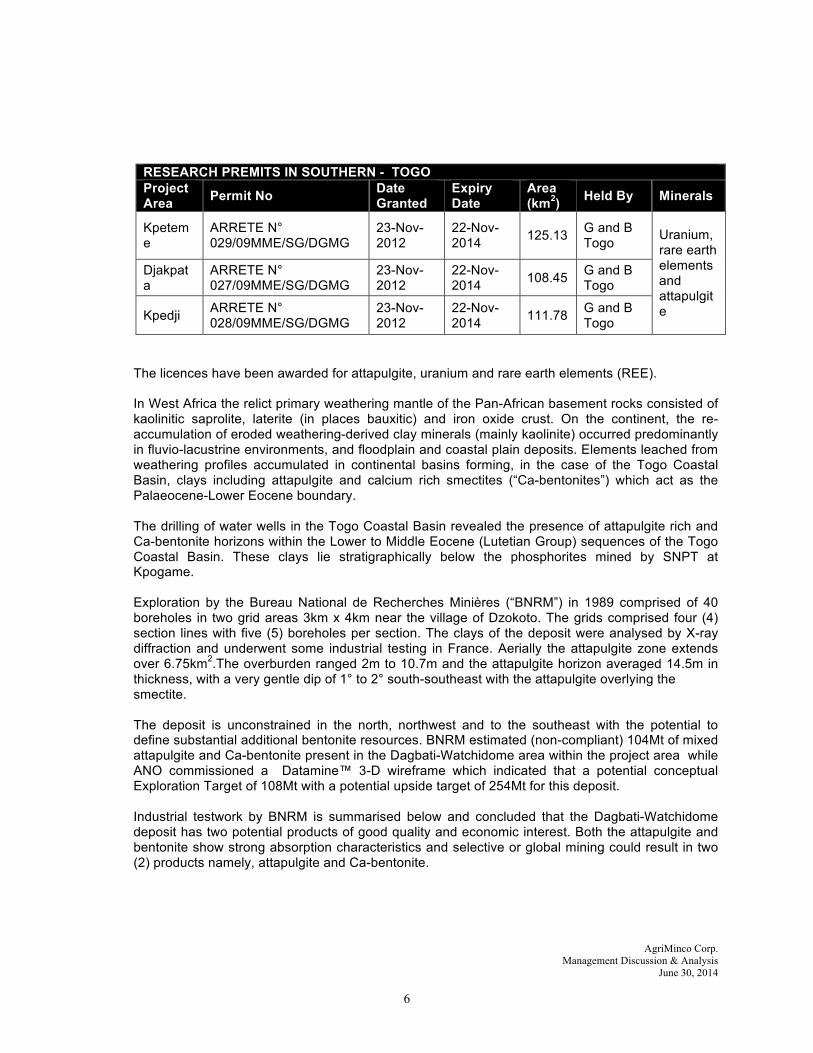

RESEARCH PREMITS IN SOUTHERN - TOGO Project Area Permit No Date

Granted Expiry Date

Area (km2) Held By Minerals

Kpeteme

ARRETE N° 029/09MME/SG/DGMG

23-Nov-2012

22-Nov-2014 125.13 G and B

Togo Uranium, rare earth elements and attapulgite

Djakpata

ARRETE N° 027/09MME/SG/DGMG

23-Nov-2012

22-Nov-2014 108.45 G and B

Togo

Kpedji ARRETE N° 028/09MME/SG/DGMG

23-Nov-2012

22-Nov-2014 111.78 G and B

Togo

The licences have been awarded for attapulgite, uranium and rare earth elements (REE). In West Africa the relict primary weathering mantle of the Pan-African basement rocks consisted of kaolinitic saprolite, laterite (in places bauxitic) and iron oxide crust. On the continent, the re-accumulation of eroded weathering-derived clay minerals (mainly kaolinite) occurred predominantly in fluvio-lacustrine environments, and floodplain and coastal plain deposits. Elements leached from weathering profiles accumulated in continental basins forming, in the case of the Togo Coastal Basin, clays including attapulgite and calcium rich smectites (“Ca-bentonites”) which act as the Palaeocene-Lower Eocene boundary.

The drilling of water wells in the Togo Coastal Basin revealed the presence of attapulgite rich and Ca-bentonite horizons within the Lower to Middle Eocene (Lutetian Group) sequences of the Togo Coastal Basin. These clays lie stratigraphically below the phosphorites mined by SNPT at Kpogame. Exploration by the Bureau National de Recherches Minières (“BNRM”) in 1989 comprised of 40 boreholes in two grid areas 3km x 4km near the village of Dzokoto. The grids comprised four (4) section lines with five (5) boreholes per section. The clays of the deposit were analysed by X-ray diffraction and underwent some industrial testing in France. Aerially the attapulgite zone extends over 6.75km2.The overburden ranged 2m to 10.7m and the attapulgite horizon averaged 14.5m in thickness, with a very gentle dip of 1° to 2° south-southeast with the attapulgite overlying the smectite. The deposit is unconstrained in the north, northwest and to the southeast with the potential to define substantial additional bentonite resources. BNRM estimated (non-compliant) 104Mt of mixed attapulgite and Ca-bentonite present in the Dagbati-Watchidome area within the project area while ANO commissioned a Datamine™ 3-D wireframe which indicated that a potential conceptual Exploration Target of 108Mt with a potential upside target of 254Mt for this deposit. Industrial testwork by BNRM is summarised below and concluded that the Dagbati-Watchidome deposit has two potential products of good quality and economic interest. Both the attapulgite and bentonite show strong absorption characteristics and selective or global mining could result in two (2) products namely, attapulgite and Ca-bentonite.

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

7

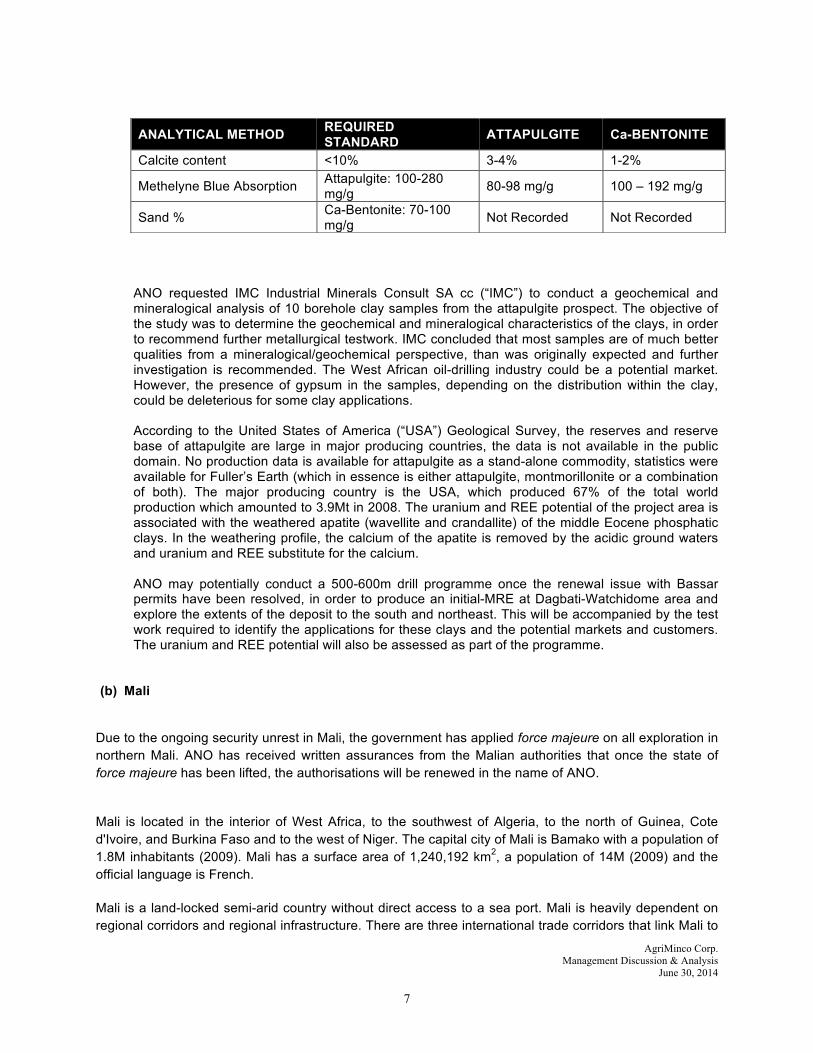

ANO requested IMC Industrial Minerals Consult SA cc (“IMC”) to conduct a geochemical and mineralogical analysis of 10 borehole clay samples from the attapulgite prospect. The objective of the study was to determine the geochemical and mineralogical characteristics of the clays, in order to recommend further metallurgical testwork. IMC concluded that most samples are of much better qualities from a mineralogical/geochemical perspective, than was originally expected and further investigation is recommended. The West African oil-drilling industry could be a potential market. However, the presence of gypsum in the samples, depending on the distribution within the clay, could be deleterious for some clay applications. According to the United States of America (“USA”) Geological Survey, the reserves and reserve base of attapulgite are large in major producing countries, the data is not available in the public domain. No production data is available for attapulgite as a stand-alone commodity, statistics were available for Fuller’s Earth (which in essence is either attapulgite, montmorillonite or a combination of both). The major producing country is the USA, which produced 67% of the total world production which amounted to 3.9Mt in 2008. The uranium and REE potential of the project area is associated with the weathered apatite (wavellite and crandallite) of the middle Eocene phosphatic clays. In the weathering profile, the calcium of the apatite is removed by the acidic ground waters and uranium and REE substitute for the calcium. ANO may potentially conduct a 500-600m drill programme once the renewal issue with Bassar permits have been resolved, in order to produce an initial-MRE at Dagbati-Watchidome area and explore the extents of the deposit to the south and northeast. This will be accompanied by the test work required to identify the applications for these clays and the potential markets and customers. The uranium and REE potential will also be assessed as part of the programme.

(b) Mali

Due to the ongoing security unrest in Mali, the government has applied force majeure on all exploration in northern Mali. ANO has received written assurances from the Malian authorities that once the state of force majeure has been lifted, the authorisations will be renewed in the name of ANO.

Mali is located in the interior of West Africa, to the southwest of Algeria, to the north of Guinea, Cote d'Ivoire, and Burkina Faso and to the west of Niger. The capital city of Mali is Bamako with a population of 1.8M inhabitants (2009). Mali has a surface area of 1,240,192 km2, a population of 14M (2009) and the official language is French.

Mali is a land-locked semi-arid country without direct access to a sea port. Mali is heavily dependent on regional corridors and regional infrastructure. There are three international trade corridors that link Mali to

ANALYTICAL METHOD REQUIRED STANDARD ATTAPULGITE Ca-BENTONITE

Calcite content <10% 3-4% 1-2%

Methelyne Blue Absorption Attapulgite: 100-280 mg/g 80-98 mg/g 100 – 192 mg/g

Sand % Ca-Bentonite: 70-100 mg/g Not Recorded Not Recorded

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

8

the sea: Tema–Ouagadougou–Bamako; Dakar–Bamako; and Abidjan–Ferkesessedougou–Bamako.

Mali is characterised by a marked difference between the northern and southern regions. The northern region is arid and sparsely populated, whereas the southern region is host to most of the country’s largest cities, a relatively higher population density, a concentration of natural resources (mostly precious metals), and economic activity (agricultural production). There is a significant land mass that has high agricultural potential and value that has yet to be utilised. Economic activity is largely confined to the riverine area irrigated by the Niger River and about 65% of its land area is desert or semi-desert

The project comprises of two geographically separate areas or prospects, within the remote northern region of Mali, equidistant between Algeria and Mauritania. The project comprises two separate Exploration Authorisations. The prospects are greenfields in nature and cover Sebkhas (salt pans) within the Taoudenni Basin known to contain potassium and related evaporitic minerals. The geological analogy to the ANO Sebkha targets are closed-basin brine deposits as found in South and North America and China, which produce potassium along with a number bi-products.

The evaporate deposits of the Taoudenni–Agorgott Sebkha, mainly consist of sediments with a high glauberite (sodium sulphate) content. The remainder of the deposits consist of salt beds with a gypsum (CaSO4.2H2O), mirabilite (Na2SO4.10H2O), bloedite (Na2Mg(SO4)2•4H2O), thenardite (Na2SO4) or halite (NaCl) composition.

• 35 Mt of gypsum; • 53.1 Mt of salt (NaCl); • 198.7 Mt of mirabilite; and • 336.7 Mt of glauberite

The presence of sylvite (KCl) up to 2% was noted in exploratory work conducted by the Malian authorities in the mi-1960s. In the literature a small sylvite (KCl) deposit has been reported from the salt depression of Taoudenni in the far north of Mali (Johnson 1995). Unconfirmed reports of Ivanov (1969) speak of potash salts reaching 180 million short tons from an unspecified location 'between Timbuktu and Taoudenni', this has not yet been verified.

Corporate Activities

AgriMinco announced the resignation of Michael Galloro as a director of the Company and from all other positions and functions effective from July 29, 2014. Simultaneously, Bruce Cumming relinquished the acting positions he had held as President and CEO and CFO. Johan Slabber accepted an appointment to the board and the positions of Director and CEO, and Jacqueline Popplestone was appointed as Chief Financial Officer. Bruce Cumming remains on our board as an Executive Director.

AgriMinco Refocus

Whilst AgriMinco maintains certain exploration activities, the Company has recognised the imperative need to reposition itself to a point where it is able to generate revenue and sustainable cash flow to fund ongoing operations. As a result, management has embarked on an aggressive search for potential acquisitions or other business associations in the African agriculture and energy sector. Whilst certain negotiations are underway, there is no definitive agreement with any other party at this time.

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

9

Results of Operations

The following table sets out selected quarterly financial information, presented in Canadian dollars. The information is prepared in accordance with IFRS as indicated in the table below:

June 30 March 31 December 31

September 30

2014 2014 2013 2013

Net income (loss) $2,399,949 $(2,407,001) $(221,318) $ 1,088,258

Earnings (loss) per share 0.009 (0.008) (0.001) 0.007

Working capital (deficiency) 388,110 (3,279,254) (2,874,775) (2,656,963) Total assets 904,065 1,380,267 3,435,472 3,552,154 Total liabilities 515,955 3,313,569 2,961,773 2,857,137

Cash flow from financing activities 477,330 66,143 44,471 1,602,223

June 30 March 31 December 31

September 30

2013 2013 2012

2012

Net income (loss) $1,171,297 $(653,295) $(478,758) $(43,282,130) Earnings (loss) per share 0.010 (0.009) (0.004) (0.360)

Working capital (deficiency) (1,841,712) (4,879,254) (4,231,765) (3,753,007) Total assets 4,704,119 79,167 57,679 83,744 Total liabilities 2,798,497 4,958,421 4,289,444 3,836,751

Cash flow from financing activities 1,602,223

24,913 - 95,706

Three months ended June 30, 2014

During the three months ended June 30, 2014, the Company incurred a net income of $2,399,949 (June 30, 2013 - $1,171,297).

Contributors to net income include:

• Gain on sale of interest in joint venture of $1,154,047 (June 30, 2013 - $nil), which is a non-recurring transaction.

• Gain on settlement of debt, including debentures and accounts payable, of $1,459,894, which is a non-recurring transaction.

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

10

• Professional fees of $15,000 (June 30, 2013 - $870,447), which account for 8% of the total operating expenses.

• Management fees of $33,000 (June 30, 2013 - $30,000), which account for 17% of the total operating expenses.

• Office and general expenses of $145,294 (June 30, 2013 – $55,349), which account for 75% of the total operating expenses (June 30, 2013 - 7%). Most of the total office and general expenses was incurred by the Company’s subsidiaries, Mali and Togo.

The Company did not incur any exploration costs on its properties during the period.

Liquidity and Capital Resources

Going Concern

These financial statements have been prepared based upon accounting principles applicable to a going concern, which assume that the AgriMinco will continue in operation for the foreseeable future and will be able to realize its assets and discharge its liabilities in the normal course of business.

In assessing whether the going concern assumption is appropriate, management takes into account all available information about the future, which is at least, but is not limited to, twelve months from the end of the reporting period. Management is aware in making its assessment, of material uncertainties related to events or conditions, such as those described herein, that may cast significant doubt upon the Company’s ability to continue as a going concern.

AgriMinco earns no operating revenues and has incurred accumulated losses of $53,517,728 (September 30, 2013 – $55,788,136). At June 30, 2014, the Company had a working capital surplus of $388,110 (September 30, 2013 – deficit of $2,656,963). AgriMinco may potentially incur further losses in the development and expansion of its business, all of which casts doubt upon the Company’s ability to continue as a going concern.

The sale of the Company’s remaining interest in the Danakil joint venture to Premier listed on AIM exchange allowed the Company to settle most outstanding debt and provided short-term operating cash. The sale, in part or in whole, of the Premier shares acquired in the transaction will provide the Company with an additional source of funding for on-going operating expenses. The realization of cash is however dependent on the future share price and liquidity of the Premier shares. Despite these circumstances, the Company maintains the position that the application of the going concern assumption is still appropriate. Accordingly, these consolidated financial statements do not reflect the adjustments to the carrying values of assets and liabilities, the reported expenses and the statement of financial position classifications used that would be necessary should the Company be unable to continue as a going concern.

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

11

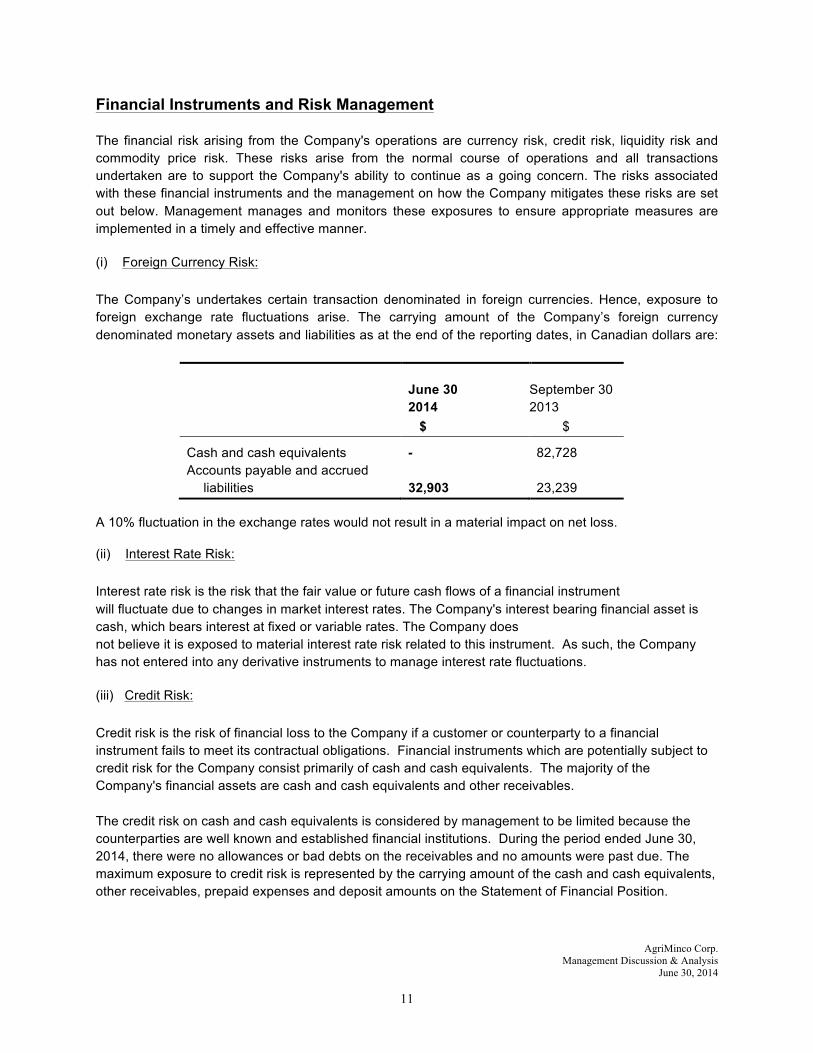

Financial Instruments and Risk Management

The financial risk arising from the Company's operations are currency risk, credit risk, liquidity risk and commodity price risk. These risks arise from the normal course of operations and all transactions undertaken are to support the Company's ability to continue as a going concern. The risks associated with these financial instruments and the management on how the Company mitigates these risks are set out below. Management manages and monitors these exposures to ensure appropriate measures are implemented in a timely and effective manner.

(i) Foreign Currency Risk:

The Company’s undertakes certain transaction denominated in foreign currencies. Hence, exposure to foreign exchange rate fluctuations arise. The carrying amount of the Company’s foreign currency denominated monetary assets and liabilities as at the end of the reporting dates, in Canadian dollars are:

June 30 2014

September 30 2013

$ $

Cash and cash equivalents - 82,728

Accounts payable and accrued liabilities 32,903 23,239

A 10% fluctuation in the exchange rates would not result in a material impact on net loss.

(ii) Interest Rate Risk:

Interest rate risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate due to changes in market interest rates. The Company's interest bearing financial asset is cash, which bears interest at fixed or variable rates. The Company does not believe it is exposed to material interest rate risk related to this instrument. As such, the Company has not entered into any derivative instruments to manage interest rate fluctuations.

(iii) Credit Risk:

Credit risk is the risk of financial loss to the Company if a customer or counterparty to a financial instrument fails to meet its contractual obligations. Financial instruments which are potentially subject to credit risk for the Company consist primarily of cash and cash equivalents. The majority of the Company's financial assets are cash and cash equivalents and other receivables. The credit risk on cash and cash equivalents is considered by management to be limited because the counterparties are well known and established financial institutions. During the period ended June 30, 2014, there were no allowances or bad debts on the receivables and no amounts were past due. The maximum exposure to credit risk is represented by the carrying amount of the cash and cash equivalents, other receivables, prepaid expenses and deposit amounts on the Statement of Financial Position.

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

12

(iv) Liquidity Risk:

Liquidity risk is the risk that the Company will not be able to meet its financial obligations as they become due. The Company’s policy is to ensure that it will always have sufficient cash to allow it to meet its liabilities when they become due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Company’s reputation. The key to success in managing liquidity is the degree of certainty in the cash flow projections. If future cash flows are fairly uncertain, the liquidity risk increases.

Typically, the Company ensures that it has sufficient cash to meet expected operational expenses. To achieve this objective, the Company prepares annual expenditure budgets, which are regularly monitored and updated as considered necessary.

The Company monitors its risk of shortage of funds by monitoring the maturity dates of existing trade and other accounts payable. Accounts payable and accrued liabilities at June 30, 2014 have contractual maturities of less than 90 days and are subject to normal trade terms for the industry and location.

The Company has no source of revenue and has cash requirements to meet its administrative overheads, maintain its mineral investments and to settle amounts payable to its creditors. Through its disposal of its interest in the Danakil joint venture (note 7 Investment in Joint Venture in the condensed interim consolidated financial statements) the Company has settled most outstanding debt and payables and has available its Premier shares to liquidate to raise additional cash. The management of the Company intends to actively seek revenue generating opportunities to generate cash or can raise cash through the issuance of equity.

Fair Value:

The fair value of a financial instrument is the amount of consideration that would be agreed upon in an arm’s length transaction between willing parties.

Determination of Fair Value:

Fair values have been determined for measurement and/or disclosure purposes based on the following methods. When applicable, further information about the assumptions made in determining fair values is disclosed in the notes specific to that asset or liability.

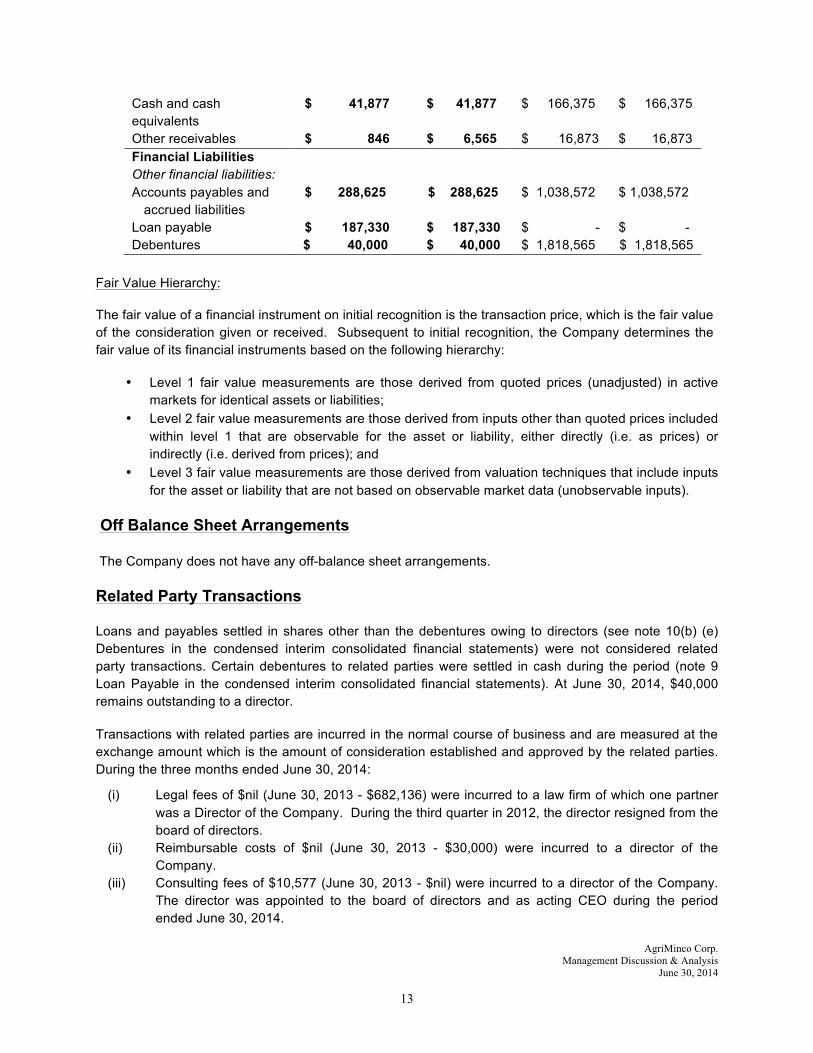

The Statement of Financial Position carrying amounts for cash and cash equivalents, other receivables, trade and other payables, loans payable and debentures approximate fair value due to their short-term nature.

June 30 2014 June 30 2014 September 30 2013

September 30 2013

Carrying value

Fair value Carrying value

Fair value

Financial Assets Loans and receivables:

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

13

Cash and cash equivalents

$ 41,877 $ 41,877 $ 166,375 $ 166,375

Other receivables $ 846 $ 6,565 $ 16,873 $ 16,873 Financial Liabilities Other financial liabilities: Accounts payables and

accrued liabilities $ 288,625 $ 288,625 $ 1,038,572 $ 1,038,572

Loan payable $ 187,330 $ 187,330 $ - $ - Debentures $ 40,000 $ 40,000 $ 1,818,565 $ 1,818,565

Fair Value Hierarchy:

The fair value of a financial instrument on initial recognition is the transaction price, which is the fair value of the consideration given or received. Subsequent to initial recognition, the Company determines the fair value of its financial instruments based on the following hierarchy:

• Level 1 fair value measurements are those derived from quoted prices (unadjusted) in active markets for identical assets or liabilities;

• Level 2 fair value measurements are those derived from inputs other than quoted prices included within level 1 that are observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices); and

• Level 3 fair value measurements are those derived from valuation techniques that include inputs for the asset or liability that are not based on observable market data (unobservable inputs).

Off Balance Sheet Arrangements

The Company does not have any off-balance sheet arrangements.

Related Party Transactions

Loans and payables settled in shares other than the debentures owing to directors (see note 10(b) (e) Debentures in the condensed interim consolidated financial statements) were not considered related party transactions. Certain debentures to related parties were settled in cash during the period (note 9 Loan Payable in the condensed interim consolidated financial statements). At June 30, 2014, $40,000 remains outstanding to a director.

Transactions with related parties are incurred in the normal course of business and are measured at the exchange amount which is the amount of consideration established and approved by the related parties. During the three months ended June 30, 2014:

(i) Legal fees of $nil (June 30, 2013 - $682,136) were incurred to a law firm of which one partner was a Director of the Company. During the third quarter in 2012, the director resigned from the board of directors.

(ii) Reimbursable costs of $nil (June 30, 2013 - $30,000) were incurred to a director of the Company.

(iii) Consulting fees of $10,577 (June 30, 2013 - $nil) were incurred to a director of the Company. The director was appointed to the board of directors and as acting CEO during the period ended June 30, 2014.

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

14

$nil (June 30, 2013 - $279,314) remains in accounts payable and accrued liabilities at June 30, 2014 relating to the above expenses.

The transactions entered into with Premier during the period ended June 30, 2014 are considered related party transactions as ZRH Nominees Ltd. is a principal shareholder, and two directors of the Company are also directors. As of June 30, 2014, the Company had a loan payable outstanding to Premier of $187,330 (note 9 Loan Payable in the condensed interim consolidated financial statements).

Compensation of Directors

During July 2013, the Board of Directors agreed to suspend the payment and accrual of Directors fees until such time as the Company’s cash flow position improved. As of June 30, 2014, the Company had $nil (September 30, 2013- $55,000) in accrued fees payable to Directors.

Commitments & Contingency

Royalty Agreement

Pursuant to a royalty agreement dated September 1, 2010, subject to and in accordance with the provisions of the agreement, the Company has granted to such parties a 3% royalty on the actual gross amount of payment received by the Company from any purchaser of potash ores or other ores or products produced from operations under one or more mining leases from the Danakil properties in Ethiopia.

All parties other than Averil S.A. quitclaimed any and all interest they may have in the royalty agreement. On March 29, 2014 Averil S.A. delivered a notice to the Company and Circum Minerals (the current owner of the Danakil properties) asserting the royalty agreement was valid. While the Company disagreed with the assertion made by Averil S.A. with respect to the validity of the royalty agreement, the Company determined that based on the risks and costs of litigation and the potential claims that Circum Minerals could have against the Company it was in the best interest of the Company to settle with Averil S.A. to, among other things, cancel the royalty and terminate any interest Averil S.A. may have in the Royalty.

On August 28, 2014 the Company entered into a settlement agreement, pursuant to which, among other things, all of Averil’s claimed interest in the royalty and the royalty agreement was extinguished in consideration for the payment of $275,000 to Averil S.A. The Company is currently in negotiations with a third party to obtain financing to pay this amount. If the financing is not successful the Company will pay this amount from existing sources available to it.

Outstanding Share Data

The following securities were outstanding as at August 29, 2014:

Common shares 164,990,751 Stock options – vested 10,762,162

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

15

Dividend Policy

No dividends have been paid to date on the shares. The Company anticipates that for the foreseeable future it will retain any future earnings and other cash resources for the operation and development of its business. Payment of any future dividends will be at the discretion of the Company’s Board of Directors after taking into account many factors, including its operating results, financial condition and current and anticipated cash needs.

Risks and Uncertainties

Exploration and development activities of a mineral resource company are by their nature highly speculative and its operations involve a number of risks, some of which are beyond the Company’s control. Financial, operational and non-financial risks could materially affect the Company’s future operating results and could cause actual events to differ materially from those described in the forward-looking information of the Company.

The following is a description of significant risk factors and uncertainties:

• Cash flows and additional funding requirements

A significant amount of funding is required to support the capital and operating expenditures in connection with the exploration and evaluation of the mineral properties. Without adequate financing, the exploration and evaluation of the mineral properties will be delayed or postponed or terminated entirely.

Notwithstanding the due diligence undertaken prior to acquiring the properties, the legal system in Africa is not yet as developed as legal systems in Canada, which leads to a higher level of uncertainty in the application and determination of African legal issues than would be expected in Canada. This can lead to regulatory delays, ill motivated use of courts or regulatory bodies and inconsistency in interpretation and enforcement of applicable African laws. Such risks are part of over-all risks of doing business in Africa and should be taken into account by any investor in African mineral projects.

• Licenses, permits, laws and regulations

The Company’s exploration and development activities require permits and approvals from various government authorities and are subject to far-reaching laws and regulations. These laws and regulations are subject to change, can become more stringent and compliance can therefore become more costly. As well, the Company may be required to compensate those suffering loss or damage by reason of its activities. There can be no guarantee the Company is able to maintain or obtain all necessary licenses, permits and approvals that may be required to explore and develop its properties, commence construction or operation of mining facilities.

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

16

• Current global financial conditions

Financial markets globally have been subject to increased volatility and numerous financial institutions have either gone into bankruptcy or have had to be rescued by governmental authorities. Access to financing has been negatively impacted by liquidity crises throughout the world. These factors may impact the ability of the Company to obtain financing, whether by equity or loans and other credit facilities, in the future and, if obtained, on terms favourable to the Company. If these increased levels of volatility and market turmoil continue, the Company may not be able to secure appropriate debt or equity financing, any of which could affect the trading price of the Company’s securities in an adverse manner.

• Nature of mining and mineral exploration and development

The mining industry involves a high degree of risk. The Company’s operations are subject to hazards and risks normally encountered in the industry. These risks include, but are not limited to, finding and developing the reserve economically, uncertainties, delays, interruptions in development and production and/or conducting operations in a cost effective manner. The Company is diligent in monitoring and responding to changes in the risk factors that affect the nature of mining and mineral exploration and evaluation.

• Resource and Reserve estimates

Uncertainties are inherent in estimating mineral resources and reserves. There are many factors that are beyond the control of the Company, such as the subjective nature of the estimates, accuracy in the quantity and quality available, the assumptions made and judgements used by the engineers and geologists. These factors can have a material effect on the financial position and future results from operations.

• Revenue

The Company is currently in an exploration and evaluation stage and has not commenced commercial production or development of the Property. The exploration and evaluation of the Property will require substantial capital commitments and there are no assurances that the Company will generate any revenues and be profitable in the future.

• Mineral commodity prices

The Company is exposed to commodity price risks. The Company closely monitors potash commodity prices, equity movements and the market to determine the appropriate course of action. These prices have fluctuated significantly in recent years. There is no assurance that commercial qualities may be produced in the future or that a profitable market will exist for the mineral. A decrease in the market price may have an adverse effect on the Company’s financial condition and results of operations.

• Foreign operations

At present, all of the operations of the Company are in Africa, as a result, the operations of the Company are exposed to various levels of political, economic and other risks and uncertainties

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

17

associated with operating in foreign jurisdictions. These risks and uncertainties include, but are not limited to, currency exchange rates; high rates of inflation; labour unrest, war, terrorism, crime, famine, drought, illegal mining, corruption uncertainty of the rule of law; renegotiation or nullification of existing concessions, licenses, permits and contracts; changes in taxation policies; restrictions on foreign exchange; changing political conditions; currency controls; and governmental regulations or require the awarding of contracts to local contractors or require foreign contractors to employ citizens of, or purchase supplies from, a particular jurisdiction. Changes, if any, in mining or investment policies or shifts in political attitudes in Africa may adversely affect the operations or profitability of the Company.

Operations may be affected in varying degrees by government regulations with respect to, but not limited to, restrictions on production, price controls, import or export controls, currency remittance, income taxes, foreign investment, maintenance of claims, environmental legislation, land use, land claims of local people, water use and mine safety. Failure to comply strictly with applicable laws, regulations and local practices relating to mineral right applications and tenure, could result in loss, reduction or expropriation of entitlements. The occurrence of these various factors and uncertainties cannot be accurately predicted and could have an adverse effect on the operations and profitability of the Company.

The legal system in Africa is not yet as developed as legal systems in Canada, which leads to a higher level of uncertainty in the application and determination of African legal issues than would be expected in Canada, which can lead to regulatory delays, ill motivated use of courts or regulatory bodies and inconsistency in interpretation and enforcement of applicable African laws. Such risks are part of over-all risks of doing business in Africa and should be taken into account by any investor in African mineral projects.

• Share price fluctuations

The market price of securities of many companies, particularly exploration stage companies, experience wide fluctuations in price that are not necessarily related to the operating performance, underlying asset values or prospects of such companies. There can be no assurance that fluctuations in the Company’s share price will not occur, in particular that other factors beyond the control of the Company could cause a significant decline in the market price of the shares.

• Environmental risks and hazards

The Company’s activities are subject to the laws and regulations from all levels of government. These laws govern environmental protection and employee health and safety. The costs of complying with these laws and regulations may reduce future profits from operations. As well, a failure to fully comply with laws and regulations may have a significant effect on the development and future operations of the Company. This would include the suspension or ceasing of operations.

• Availability and dependence on management and outside advisors

The Company has relied and intends to rely on management and outside advisors for development, construction and operating expertise. If the work of the aforementioned parties

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

18

is deficient or negligent or is not completed in a timely manner, it could have a material adverse effect on the Company.

• Competition risk

Numerous competitors in the industry may result in the Company being unable to acquire desired property, recruit or retain qualified employees or acquire the capital necessary to develop its property. The inability to compete with other mining companies for these resources would have a material adverse effect on the Company’s results of operation and business.

• Uninsured risks

The Company maintains insurance to cover normal business risks. In the course of exploration and development of mineral properties, certain risks, and in particular, unexpected or unusual geological operating conditions including explosions, rock bursts, cave in, fire and earthquakes may occur. It is not always possible to fully insure against such risks as a result of high premiums or other reasons. Should such liabilities arise, they could result in significant liabilities to the Company and increase costs of projects.

• Conflicts of interest

Certain Officers and Directors serve or may agree to serve as directors or officers of other companies and, to the extent that such other companies may participate in ventures in which the Company may participate, these Officers and Directors may have a conflict of interest in negotiating and concluding terms respecting such participation.

• Qualified personnel

Recruiting and retaining qualified personnel in the future is critical to the Company’s success. As the Company explores its mineral properties, the need for skilled labour will increase. The number of persons skilled in the exploration and development of mining properties is limited and competition for this workforce is intense. Properties in Mali and Togo may be significantly delayed or otherwise adversely affected if the Company cannot recruit and retain qualified personnel as and when required.

Sources of Estimation Uncertainty

Preparation of the Company’s consolidated financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Estimates and assumptions are based on management’s experience and expectations of future events are continually evaluated. Management believes such estimates and assumptions are reasonable under the circumstances. Actual results could

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

19

differ from estimated amounts by a material amount.

Matters that require management to make estimates and assumptions include, but are not limited to, the following:

(i) Exploration and Evaluation Costs

The application of the Company’s accounting policy for exploration and evaluation costs requires judgement in determining whether it is likely that future economic benefits will flow to the Company, which may be based on assumptions about future events or circumstances. Estimates and assumptions made may change if new information becomes available. If, after expenditure is capitalized, information becomes available suggesting that the recovery of expenditure is unlikely, the amount capitalized is written off in the profit or loss in the year the new information becomes available.

(ii) Impairment of Long-Lived Assets

The carrying value of investment in exploration and evaluation costs are reviewed for impairment when facts and circumstances suggest that the carrying amount exceeds the recoverable amount. If the property is assessed to be impaired, it is written down to its estimated recoverable amount. Significant judgments and estimates are made when estimating this net recoverable value. Therefore the recorded value of investment in exploration and evaluation costs could materially change from period to period due to changes in estimates.

(iii) Share-Based Payments

The Company measures the cost of equity-settled transactions with consultants, officers and directors by reference to the fair value of the equity instruments at the date at which they are granted. Estimating fair value for share-based payment transactions requires determining the most appropriate valuation model, which is dependent on the terms and conditions of the grant. This estimate also requires determining the most appropriate inputs to the valuation model including the expected life of the stock option, volatility and dividend yield and making assumptions about them. The assumptions and models used for estimating fair value for share-based payment transactions are disclosed in note 10 to the financial statements.

Significant Accounting Policies

This MD&A should be read in conjunction with the unaudited condensed interim consolidated financial statements of the Company for the nine months ended June 30, 2014 and the audited consolidated financial statements and related notes for the year ended September 30, 2013.

International Financial Reporting Standards

Future Standards, Amendments and Interpretations

(i) IFRS 9 Financial Instruments, effective for annual periods beginning on or after January 1, 2015, with early adoption permitted, introduces new requirements for the classification and measurement of financial instruments.

AgriMinco Corp. Management Discussion & Analysis

June 30, 2014

20

(ii) IFRS 10 Consolidated Financial Statements effective for annual periods beginning on or after January 1, 2013, with early adoption permitted, establishes principles for the presentation and preparation of consolidated financial statements when an entity controls one or more other entities.

(iii) IFRS 11 Joint Arrangements, effective for annual periods beginning on or after January 1, 2013, with early adoption permitted, addresses inconsistencies in the reporting of joint arrangements by requiring a single method to account for interests in jointly controlled entities.

(iv) IFRS 12 Disclosure of Interests in Other Entities, effective for annual periods beginning on or after January 1, 2013, with early adoption permitted, is a new and comprehensive standard on disclosure requirements for all forms of interests in other entities, including joint arrangement, associates, structured entities and other off-balance sheet vehicles.

(v) IFRS 13 Fair Value Measurement was issued by the IASB in May 2011. IFRS 13 establishes new guidance on fair value measurement and disclosure requirements for IFRSs and US generally accepted accounting principles (GAAP). The guidance, set out in IFRS 13 and an update to Topic 820 in the FASB’s Accounting Standards Codification (formerly referred to as SFAS 157), completes a major project of the boards’ joint work to improve IFRSs and US GAAP and to bring about their convergence. The standard is effective for annual periods beginning on or after January 1, 2013.

The Company is currently assessing the effects of these new standards, and intends to adopt them once they become effective. Certain other standards have been issued but are not expected to have a material impact on the Company’s consolidated financial statements.

Other Information

Additional information relating to the Company is available under the Company’s profile on SEDAR at www.sedar.com and on the Company’s website www.agriminco.com.

On behalf of the Board of Directors

Johan Slabber

Chief Executor Officer