agriculture and food industry in india 2011 - food processing sector

TRANSCRIPT

Agriculture and Food Industry – India (Part VI)

January 2011

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

2AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

Food Processing Sector in India

•Executive Summary

•Market Overview

•Product Segments

•Drivers and Challenges

•Competition

•Corporate Actions and Investments

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

3AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

Executive Summary

Market Overview

• The food processing industry is valued at INR 3.4 trillion (USD 70 bn) and is expected to witness a CAGR of 14% (2009-2012)

• States like Andhra Pradesh, Uttar Pradesh and Madhya Pradesh are highly attractive for food processing industry

Product Segments

AGRICULTURE AND FOOD INDUSTRY IN INDIA FOOD PROCESSING SECTOR - EXECUTIVE SUMMARY

Drivers & Challenges

Competition

• Indian food processing sector is highly competitive with many foreign players in the market

• More players are planning to tap the mass market in segments like fruits & vegetables, meat & poultry and fisheries

Conclusion

• Increasing retailing and higher consumer spend is expected to increase the penetration of processing food in India

• Low penetration in the sector offers immense opportunities for growth hence large PE investments is seen from 2007 to 2010

Drivers:

• Increasing consumer spend on processed foods

• India’s competitive edge

• Growing food retailing in India

• Government support

• Growth in food processing exports

• Growth in terminal markets

• Low level of penetration in domestic market

Challenges:

• Lack of integrated supply chain and scale of operations

• Limited use of technology in food processing

• High taxes on branded agricultural products

• Diary products and fruits & vegetables are the most attractive segments for investments

• Packaged foods, beverages and staples are characterized by high volumes and low margins

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

4AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

Food processing industry in India has huge untapped

potential and offers scope for large investments

• The industry is valued at INR 3.4 trillion (USD 70 bn) and is

expected to witness a CAGR of 14% in the period 2009-

2012E

• India is one of the top producers of milk, pulses,

sugarcane and tea in the world

• Government has taken major initiatives towards ensuring

multi-fold growth in this sector that has an investment

opportunity of about INR 1.1 trillion (USD 24 bn) by 2015

• Mega Food Parks are coming up in India to integrate the

supply chain and promote food processing

• Foreign direct investments was ~INR 6.3 bn (USD 143

mn) in 2007-08

• States like Andhra Pradesh, Uttar Pradesh and Madhya

Pradesh are highly attractive for food processing industry

Source: Source: Ministry of Food Processing Industries, IBEF articles & KPMG Research

Packaged Foods 3%

Fisheries 12%

Meat & Poultry 10%6%

Fruits & Vegetables 10%

Diary Sector 37%

Scope: Food processing includes Diary Sector, Fruits & Vegetables,

Meat & Poultry, Fisheries, Packaged Foods, Beverages and Staples

Range 6 – 10%

Food processing sector is expected to grow at a CAGR of 12%

from 2009 to 2012 …

… with dairy sector having the highest penetration in the

market

Food Processing Sector Overview

Market Overview1

2

4,7844,186

3,6803,430

0

1,000

2,000

3,000

4,000

5,000

INR bn +12%

2012e2011e2010e2009

AGRICULTURE AND FOOD INDUSTRY IN INDIA FOOD PROCESSING SECTOR – MARKET OVERVIEW

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

5AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

Diary products, fruits and vegetables are the most attractive

segments for investments

Source: Press articles; Ministry of Food Processing website; IBEF & KPMG research report “Food Processing- market & opportunities”, Apr 2008

• India is the leading producer of milk in the world, and produced about 108 MT in 2007

� ~37% of the produced milk is processed and ~676 diary plants are registered with the

government

• The major growing segment include- branded butter, cheese and ice cream and the total

market is valued at ~INR 20.3 bn (USD 442 mn) and expected to grow at an average rate

of ~13%

• Ultra Heated Treatment and flavored milk are other high growth market

Meat and Poultry

• India has the largest livestock population (470 mn) globally

• About 5 mn tonnes of meat is produced per year in India

• Per head consumption of fresh and processed meat is as low as 1.5 kg in India against

world average of 35.5 kg

• Majority of animals in India are not bred for meat, the processing percentage for meat

is as follows

-Buffaloes (11%), Cattle (6%), Sheep (33%), Goat (38%)

• The annual poultry production in India is 450 mn broilers and 33 bn eggs growing at

20% and 16%

Fruits and

Vegetables

• Globally, India is second and third largest producer of vegetables (100 MT) and fruits (50

MT) respectively

� India accounts for 8.4% of the world’s F&V production

• Less than 2% of total vegetables produced are processed commercially in India

• Share of organized sector in fruits processing is ~48% and ~20% of processed F&V are

exported

� Mango and its other products alone constitute 50% of the total F&V exports

Dairy ProductsGrowth

Rate

+15%

Growth

Rate

+20%

Growth

Rate

+10%

Major product segments in food processing sector (1 of 2)

MT – Million Tonnes

AGRICULTURE AND FOOD INDUSTRY IN INDIA FOOD PROCESSING SECTOR – PRODUCT OVERVIEW

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

6AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

Packaged foods, beverages and staples are restricted to

urban areas, characterized by high volumes and low margins

• India ranks third in fish production in the world

• Frozen shrimp contributes to 34.62% of exports in terms of volume and 63.5% in value

• India has about 369 freezing units with daily processing capacity of 10,226 tonnes and

499 frozen storage units with a capacity of 134,767 tonnes

Beverages

• India is the largest tea producer in the world accounting for 28% of global production

and 5th largest coffee producer accounting for 4% of total production in the world

• There are 100 plants across India under aerated soft drinks segment

• Exports in soft drinks are valued at INR 7.2 bn (USD 156 mn) per annum

• Attracted FDI of more than INR USD 1 bn

Packaged foods

• India has around 60,000 bakeries; 20,000 traditional food units

• The growing segments in packaged foods include

� Soups market is at a nascent stage and is valued at INR 644 mn (USD 14 mn)

� Confectionaries market pegged at INR 22.3 bn (USD 484.3 mn) growing at 5.7%

� Biscuit market is estimated to be INR 17.2 bn (USD 373.4 mn) and is growing at 7.5%

� Culinary products; tomato ketchups and jams at 18-20% annually

Fisheries

Staples

• India is the second largest wheat producer globally with an output of 70 MT valued at

INR 9 bn (USD 195 mn)

• There are 10,000 pulse mills with 14 MT milling capacity per annum

Source: Press articles; Ministry of Food Processing website; IBEF & KPMG research report “Food Processing- market & opportunities”, Apr 2008

Growth

Rate

+20%

Growth

Rate

+8%

Growth

Rate

+27%

Growth

Rate

+85%

Major product segments in food processing sector (2 of 2)

Note: Fisheries sector include marine, in-land and aquaculture; Packaged foods primarily include ready-to-eat snacks, chips, namkeen, bakery

products etc.; Beverages primarily comprises non-alcoholic beverages like aerated soft drinks, fruit juices and hot beverages

Conversion of USD to INR – average of that year from oanda.com

AGRICULTURE AND FOOD INDUSTRY IN INDIA FOOD PROCESSING SECTOR – PRODUCT OVERVIEW

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

7AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

Drivers

Increasing consumer spend on

processed foods

India’s competitive edge

Growing food retailing in India

Government support

Growth in food processing exports

Growth in terminal markets

Low level of penetration in domestic

market

Challenges

Lack of integrated supply chain and

scale of operations

Limited use of technology in food

processing

High taxes on branded agricultural

products

Drivers & Challenges – Summary ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

8AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

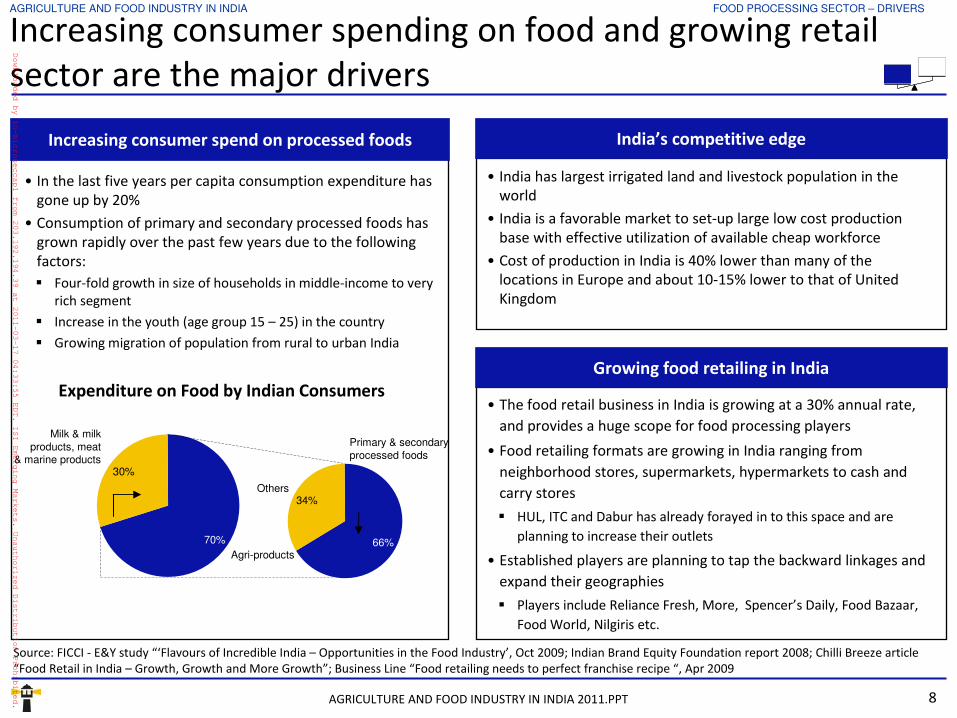

Increasing consumer spending on food and growing retail

sector are the major drivers

• India has largest irrigated land and livestock population in the

world

• India is a favorable market to set-up large low cost production

base with effective utilization of available cheap workforce

• Cost of production in India is 40% lower than many of the

locations in Europe and about 10-15% lower to that of United

Kingdom

• The food retail business in India is growing at a 30% annual rate,

and provides a huge scope for food processing players

• Food retailing formats are growing in India ranging from

neighborhood stores, supermarkets, hypermarkets to cash and

carry stores

� HUL, ITC and Dabur has already forayed in to this space and are

planning to increase their outlets

• Established players are planning to tap the backward linkages and

expand their geographies

� Players include Reliance Fresh, More, Spencer’s Daily, Food Bazaar,

Food World, Nilgiris etc.

Source: FICCI - E&Y study “‘Flavours of Incredible India – Opportunities in the Food Industry’, Oct 2009; Indian Brand Equity Foundation report 2008; Chilli Breeze article

“Food Retail in India – Growth, Growth and More Growth”; Business Line “Food retailing needs to perfect franchise recipe “, Apr 2009

• In the last five years per capita consumption expenditure has

gone up by 20%

• Consumption of primary and secondary processed foods has

grown rapidly over the past few years due to the following

factors:

� Four-fold growth in size of households in middle-income to very

rich segment

� Increase in the youth (age group 15 – 25) in the country

� Growing migration of population from rural to urban India

30%

70%

Agri-products

Milk & milk

products, meat & marine products

34%Others

66%

Primary & secondary

processed foods

Expenditure on Food by Indian Consumers

Increasing consumer spend on processed foods India’s competitive edge

Growing food retailing in India

AGRICULTURE AND FOOD INDUSTRY IN INDIA FOOD PROCESSING SECTOR – DRIVERS

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

9AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

Government initiatives to achieve the target size of USD 210

bn by 2015 to boost the industry

Source: Ministry of Food Processing India; ET Interview with Food-processing minister “Food processing can create more jobs”, Jul 2009; The Financial Express “Food

processing min plans Rs 1,200-crore VC fund” Sep 2009 Note: Conversion of USD to INR – average of that year from oanda.com

Foreign investment

and VC funding

Mega food parks

Tax rebates

Skill development

plans

• 100% FDI as well as technology transfer is allowed in this sector and grants are given by the

government for setting up common facilities in Agro Food Park

• Plans to set up a dedicated venture capital fund to support the investment requirements

� The venture capital fund would be set up with a corpus of about INR 11.5 bn (USD 250 mn) by 2010

� Fund could be either a government initiative or under public-private-partnership model

• Government plans on establishing 30 mega food parks in all states enabling integration of the fruit

and vegetable sector from farm gate to the retail outlet

� Operations towards developing 10 parks has begun

� All parks are expected to be established by 2015

• Government to provide financial support by means of capital investment in Food Parks, subject to a

maximum of INR 506 bn (USD 11 bn)

• Government is planning to declare a tax holiday for all food processing units

• It also plans to extend 100% depreciation benefit for infrastructure projects in the sector from first

year onwards

• Income tax rebate is allowed for 100% of profits for first 5 years and 25% for next 5 years

• Reduced custom and excise duties on various products

• Government plans to design a curriculum for skill development programmes in consultation with

HRD ministry, Labour ministry and institutions

• Plans to collaborate with aid agencies like World Bank and Asian Development Bank to raise funds

for running large-scale skill development programs

• Prepare a blueprint for Skill Development Mission and collaborate with Industrial Training Institutes

(ITI) to focus on training the workers at various levels of food processing

Government Support

AGRICULTURE AND FOOD INDUSTRY IN INDIA FOOD PROCESSING SECTOR – DRIVERS

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

10AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

Development of terminal markets creating linkages with

aggregators and logistics providers is driving growth

Source: Maharashtra State Agricultural Marketing Board “Projects: Terminal Markets”, IBEF and other press articles; Economic Times “Food processing can create more

jobs”, Jul 2009; igovernment article “India to set up 30 food parks”, May 2008; Yahoo news “High taxes hitting food processing sector: Assocham” Nov 2009

• The growth in terminal markets will lead to

stronger integration between food producers and

processors

• In order to integrate the domestic produce with

retail chains the government of India is promoting

terminal markets � It plans to set-up 8 terminal markets with an investment

of USD 131 mn

� Cities under consideration are Mumbai, Nashik, Nagpur,

Chandigarh, Rai, Patna, Bhopal and Kolkata

� 21 more terminal markets are proposed for future

• The penetration levels in the domestic market are

low in India because majority of processing units are

export oriented

• India has large untapped domestic potential

0

20

40

60

8080%

Brazil

70%

Malaysia

40%

Philippines

5%

78%

China

30%

Thailand India

%

Processing % of Food Produced Across Countries

Growth in terminal markets

Low level of penetration in domestic market

AGRICULTURE AND FOOD INDUSTRY IN INDIA FOOD PROCESSING SECTOR – DRIVERS

Terminal

Markets

Project Cost

(INR bn)

Handling

Capacity

(Metric

Tonnes)

Area

Required

(Acres)

Mumbai 1.9-2.5 3000 125

Nashik 0.6 1000 100

Nagpur 0.6 750 100

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

11AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

Lack of integrated supply chain, limited use of technology

and higher taxes on branded food are major challenges

Source: Economic Times “Food processing can create more jobs”, Jul 2009; igovernment article “India to set up 30 food parks”, May 2008; Yahoo news “High taxes

hitting food processing sector: Assocham” Nov 2009; IBEF report 2008; igovernment article “India to set up 30 food parks”, May 2008

Lack of integrated supply chain

Limited use of technology in food processing

High taxes on branded agricultural products

• Lack of proper value chain and

technology for food processing in India:

� Produce worth INR 460 bn (USD 10 bn)

is wasted every year in India

� Nearly 20-25% of the fruits &

vegetables production in India is lost in

spoilage at various stages of harvesting

• Lack of technology, poor quality of

seeds and planting material is one of

the reasons for this, scale of operations

is also a key factor

• About 90% of the units are small scale

and hence does not reap the benefits of

economies of scale

• Food processing in India is majorly a

manual process

• Technology plays an important role for

storing fruits & vegetables for a long

period in order to enable further

processing

• There are about 3600 licensed

slaughter-houses in India but due to

lack of technology, meat processing is

low in India

• Besides 12.5% of value-added tax, branded processed products are subject

to a 2% central sale tax and also attract local entry tax and octroi up to 4%

• On the other hand, unbranded products are in many cases exempted from

tax or often taxed at a 4% concessional rate, which adversely affects the

competitiveness of the sector

Challenges

AGRICULTURE AND FOOD INDUSTRY IN INDIA FOOD PROCESSING SECTOR – CHALLENGES

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

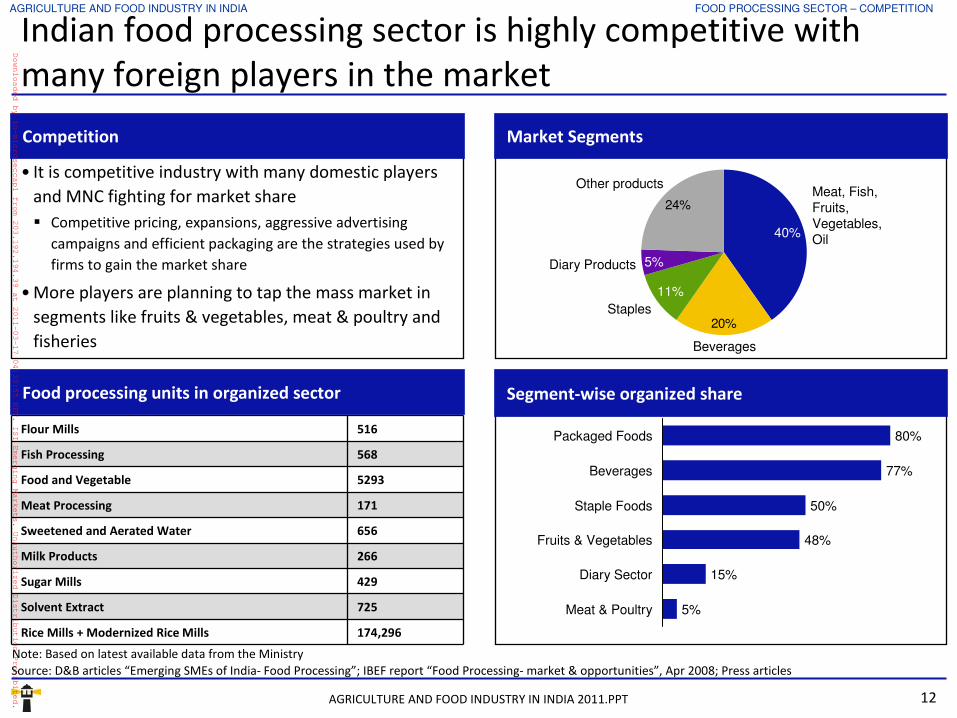

Indian food processing sector is highly competitive with

many foreign players in the market

• It is competitive industry with many domestic players

and MNC fighting for market share

� Competitive pricing, expansions, aggressive advertising

campaigns and efficient packaging are the strategies used by

firms to gain the market share

• More players are planning to tap the mass market in

segments like fruits & vegetables, meat & poultry and

fisheries

Source: D&B articles “Emerging SMEs of India- Food Processing”; IBEF report “Food Processing- market & opportunities”, Apr 2008; Press articles

80%Packaged Foods

77%Beverages

50%Staple Foods

48%Fruits & Vegetables

15%Diary Sector

5%Meat & Poultry

24%

20%

Meat, Fish,

Fruits,

Vegetables,

Oil40%

Beverages

Staples

11%

Diary Products 5%

Other products

Flour Mills 516

Fish Processing 568

Food and Vegetable 5293

Meat Processing 171

Sweetened and Aerated Water 656

Milk Products 266

Sugar Mills 429

Solvent Extract 725

Rice Mills + Modernized Rice Mills 174,296

Competition Market Segments

Food processing units in organized sector Segment-wise organized share

AGRICULTURE AND FOOD INDUSTRY IN INDIA FOOD PROCESSING SECTOR – COMPETITION

Note: Based on latest available data from the Ministry

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

13AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

Source: PE India, VC Circle, Company Website, Press Articles

Low penetration in the sector offers immense opportunities

for growth hence large PE investments seen from 2007-10

Mergers and Acquisitions

Date Acquired Company AcquirerAmount (INR mn)

Stake(%)

Dec 2009 Vigo Biotech Aniol Group 220-250/ 90%

Jul 2008 Cream Bell Devyani Food Industries 26%

Sep 2007 Field Fresh Foods Pvt Ltd. Del Monte Pacific Ltd 4500-5500 /100%

May 2007 Karen’s Gourmet Kitchen (KGK) Temptation Foods 26%

Private Equity Investment

Date Investee Company Investor Amount / Stake (%)

Mar 2010 Global Green Company India Agri Business Fund 480 / 22%

Jan 2009 Tirumala Milk Products Carlyle Group 1100

Oct 2009 LT Foods and Subsidiary Daawat

Foods Ltd.

Rabo Equity Advisors 487/14.7% and 26.2%

Feb 2008 Vallabhdas Kanji Limited (VKL) Argonaut Private Equity NA

Jun 2008 Parag Milk Foods Pvt. Ltd (“Parag/

Gowardhan”)

Motilal Oswal Venture Capital Advisors

Private Limited

600

Jun 2007 Karuturi Networks Bennett, Coleman and Co Ltd (BCCL) NA

AGRICULTURE AND FOOD INDUSTRY IN INDIA FOOD PROCESSING SECTOR – CORPORATE ACTIONS AND INVESTMENTS

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

14AGRICULTURE AND FOOD INDUSTRY IN INDIA 2011.PPT

Thank you for the attention

About Netscribes

Netscribes is a knowledge-consulting and solutions firm with clientele across the globe. The company’s expertise spans areas of investment &

business research, business & corporate intelligence, content-management services, and knowledge-software services. At its core lies a true

value proposition that draws upon a vast knowledge base. Netscribes is a one-stop shop designed to fulfil clients’ profitability and growth

objectives.

The Agriculture and Food Industry - India report is a part of Agriculture Industry Series.

For more detailed information or customized research requirements please contact:

Disclaimer: This report is published for general information only. Although high standards have been used the preparation, Research on India,

Netscribes (India) Pvt. Ltd. or “Netscribes” is not responsible for any loss or damage arising from use of this document. This document is the

sole property of Netscribes (India) Pvt. Ltd. and prior permission is required for guidelines on reproduction.

Research on India is a product of Netscribes (India) Pvt. Ltd. Research on India is dedicated to disseminating information and providing quick

insights on “hot” industries in India and other emerging markets. Track our new releases and major updates in these industries on

Gagan UppalPhone: +91 22 4098 7530

E-Mail: [email protected]

Gaurav KumarPhone: +91 33 4064 6214

E-Mail: [email protected]

ISIEmergingMarketsPDF in-microseccap1 from 203.192.194.39 on 2011-03-17 04:33:55 EDT. DownloadPDF.

Downloaded by in-microseccap1 from 203.192.194.39 at 2011-03-17 04:33:55 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.