agriculture and agrifood: choosing the future › userfiles › file › caaaq_angl.pdf · an...

TRANSCRIPT

Agriculture andAgrifood: Choosing the FutureConsultation document

An invitation to participate 3

1 The food requirementsof the population 6

2 Agricultural production 9

3 Food processing 15

4 Distribution of food produce 18

5 Foreign trade in agricultural andagri-food products 22

6 Human resource development 25

7 Agriculture, agri-foodand the environment 29

8 Health and consumer concerns 33

9 Rural life and regional development 37

10 Governance 40

How to participate 43

References 46

Table of Contents

2

Commission sur l'avenir de l'agriculture et de l'agroalimentaire québécois

Jean Pronovost, chairmanMario Dumais, commissionerPascale Tremblay, commissioner

Suzanne Dion, secretary general

RESEARCH AND TEXTDenis Cormier, research directorJean Dionne, communications directorJean-François Aubin, analystJacques Bélanger, analystMichel Carignan, analystBertrand Venne, analyst

ASSISTANCEEco Ressources Consultants

PRODUCTION COORDINATIONGino Desrosiers, communications advisor

TECHNICAL SUPPORTOdette Côté, administrative assistantSylvie Jolicoeur, administrative assistantFrance Pelletier, communications advisor

LINGUISTIC REVISIONPierre Senéchal

ENGLISH TRANSLATIONBenjamin WaterhouseChristine Gardner

LAYOUTFolio et Garetti

PHOTOGRAPHS Guy Tessier

Ce document est également disponible en français

© Commission sur l'avenir de l'agriculture et de l'agroalimentaire québécoisLegal deposit: Bibliothèque nationale du Québec, January 2007

ISBN 978-2-550-48761-6 (print version)ISBN 978-2-550-48762-3 (PDF)

3

The primary mission of Quebec’sagriculture and agri-food sector is to contribute toward feeding people,in Quebec and around the world. Whilemeeting our vital need for food, thesector also produces non-comestiblegoods such as fibre, horticulturalproducts and bio-energy. As a result,it is at the heart of a number ofsocietal issues that concern everybody.

Production, processing anddistribution, including activities in the hotel, restaurant and institutional(HRI) sector, are economic activitiesthat generate wealth, jobs andexports. Currently, the agri-foodsector in Quebec employs some452,000 people.

For those who make their living fromagriculture, it is a lifestyle as well as a source of great personal and familysatisfaction. A number of specificskills are required to be successful.Training, advisory services, researchand innovation are therefore ofstrategic importance.

In 2001, Quebec hadapproximately 47,390 farmproducers working on 30,539farming operations.

An invitationto participate

Graph 1 – BREAKDOWN OF JOBS INQUEBEC’S AGRI-FOOD SECTOR

Distribution and HRI: 71 %

Processing: 16 %

Production: 13 %

Agriculture is the territorial foundationof Quebec’s rural fabric. By definition,it is the primary and most stablefactor in the dynamic occupation ofthe land. It plays a significant role inshaping Quebec’s landscape as wellas its economic development.

Because agriculture occupies such a large percentage of Quebec’sinhabited land mass, it has a majorimpact on our environment. Farmproduction methods that arerespectful of water, soil and air qualitytherefore benefit the entire population.

Agriculture and the agri-food sectorare core elements in any strategydesigned to protect and promotehealth. Long before medical carebecomes necessary, healthy livinghabits, including eating a variety of healthy foods, are key factors in determining our individual andcollective health.

Every one of these issues comes withits own set of problems and upheavals.Some have gone so far as to use theterm crisis. Yvon Vallières, Minister,Ministère de l’Agriculture, des Pêcherieset de l’Alimentation du Québec, hadthis to say when introducing theCommission members:

“Our business environment isbecoming increasingly constrainedas a result of elements such as thefarm income crisis, chronically lowcereal prices, problems in the porksector, the mad cow crisis, threatsto supply management and thestrength of the Canadian dollar.There are also a number ofparadoxes, such as rising landprices, soaring quota costs and continued increases in the volumeof farm gate sales. At the sametime, short-term crises have tendedto disguise some major long-termtrends, namely the leveling-off of farm prices, rising costs andincreasingly strong competition.”

Over the years, society’s expectationsof the men and women whose job it is to feed the population haveincreased and become more complex.The precarious financial situation ofQuebec’s farms, along with high debtand stress levels and the problem ofinter-generational farm transfers, arethe most common difficulties currentlyfaced by the sector.

The farming profession is demandingin terms of time and training, as wellas personal and financial investment.Farmers are expected to producemore efficiently, in terms of quantityand quality, to satisfy the increasinglydiverse tastes of consumers, and atthe same time they are asked to helpimprove Quebec’s exports—all withina context of worldwide competitionwhere food product prices are tendingto stagnate or decline and productioncosts are rising steadily.

In the rural community, agriculture is no longer the only, nor even themajority, stakeholder. City dwellers are moving out to the country, andalong with the peri-urban populationand other rural inhabitants, they arebeginning to express new values.They are also making new demandsconcerning the impact of farming on the quality of the environment.

Today, Quebec’s farmingpopulation accounts for just6.4% of the total ruralpopulation.

4

Farm size is increasing, while farmnumbers are declining steadily. Thishas clearly had an impact on thedynamics in rural communities.

Growing public concerns about healthand food quality also have an impacton agriculture and the food industry.At the same time, the trust betweenconsumers and the food production,processing and distribution chain hasbeen eroded.

Some people believe technologicalinnovations, such as the introductionof GMOs, pose a threat to humanhealth, livestock health, biologicaldiversity and the environment.

Processing companies, for their part,feel trapped between producers,distributors and the demands ofinternational competition.

Some observers believe it is now time to re-examine the system usedto govern the sector’s institutions. The question is this: should therelationships between the players in the sector be adjusted and theirroles updated to meet the challengesof the future?

In light of the situation outlined above,the Quebec government has instructedthe Commission

• to review the issues and challengesnow facing the agriculture and agri-food sector in Quebec;

• to examine the effectiveness ofcurrent government actions;

• to make an assessment;

• to make recommendations thatreflect the challenges ofcompetition, farm incomes, societalexpectations and the developmentof potential in the regions.

To do this, the Commission willorganize public hearings throughoutQuebec so that everyone who wishesto do so will have an opportunity toexpress their opinion. At the sametime, the Commission will make adeliberate effort to examine everyaspect of the problems addressed,and will systematically seek outdifferent viewpoints. The Commissionwill encourage dialogue, compareopinions, seek balanced solutionsand, as far as possible, articulate aviable consensus on the questionsraised.

This consultation document has been prepared as part of this process.It is divided into ten chapters onspecific topics, including production,processing, environment, and others.Issues such as health, innovation,profitability and the farm transferprocess are woven into severaldifferent topics and are mentioned in different places. Each chaptercontains some generally accepted or frequently repeated observations,data on various trends and a certainnumber of questions. The data areoften based on average values thatdo not always reflect every aspect of the sector, or every feature ofproduction, the regional situation,farm size or other elements underconsideration.

The document is by no meansexhaustive, and is not intended toshape the eventual conclusions of the consultation process or therecommendations to be made. Itssole purpose is to provide a summaryprofile that will trigger and fueldiscussions. This profile has beendesigned to help participants identifya vision and some main themes, andto propose different options.

The Quebec government hasasked the Commission to workwith the population to definethe main elements in a renewedvision of agriculture and theagri-food sector. The membersof the Commission firmly believethat the best way to achievethis is through an open,transparent and disciplineddebate.

It is with this in mind that theCommission puts forward thefollowing observations and questions,and cordially invites you to take partin the Commission’s work.

5

The population must not only be fed,it must also be well fed. The growingprevalence of obesity, along with therelated problems of diabetes andcardiovascular disease, has led to the emergence of a number of publichealth issues that are of concern tothe agriculture and agri-food sector.One of these issues is the need tocreate an environment that willencourage as many people as possibleto adopt healthy eating habits.

THE QUEBEC MARKET

A number of social and demographiccharacteristics influence our foodrequirements. Since populationgrowth and consumption are relativelystable, the volume of food consumedin Quebec is expected to level out inthe future.

The portion of total income spent on food in Quebec and Canada isshrinking. Between 1997 and 2004, it fell from 13.2% to 12.5% in Quebec,and from 11.5% to 10.9% in Canada.1

Rising life expectancy and averageage, the shrinking size of households,higher education levels, changingvalue systems and cultural diversitywill all have an impact on the demandfor food.

The population is ageing, in bothQuebec and Canada. The Institut de la statistique du Québec (ISQ)forecasts that the portion of thepopulation aged 50 and over will risefrom 31% in 2001 to 44% in 2036.2

The first members of the Baby Boomgeneration turned 60 in 2006, and are now beginning to retire. In the last 20 years, the number of peoplein Quebec aged 65 and over has

increased, while the number aged 15 and under has declined.

According to ISQ forecasts, by 2010 the over-65 age groupwill have overtaken the under-15group in terms of size.

Based on the reference scenario usedby the ISQ to forecast demographictrends, the Quebec population shouldstop growing in 2031, at which point it will stand at nearly 8.1 millionpeople.3 The demographic curve isthen expected to descend, slowly atfirst, but picking up pace over time.

Because of its ageing population,Quebec’s consumer food sector will probably offer some interestingprospects for the development ofproducts that address concernsrelating to health and old age.

Quebec’s agriculture and agri-food sector ensures a secure supply of food for people both at home and abroad. In an increasingly

inter-related world, it is part of aneconomic network that spans markets in Quebec, Canada and the world,creating a flow of exports and imports to meet the population’s foodrequirements.

1The foodrequirements of thepopulation

Consumers are increasingly sensitiveto the composition and nutritive valueof the food they eat, and are seekinga better dietary balance. Consumersare also increasingly concerned withfood quality and safety. Faced with apopulation that wants to remain activeand healthy for as long as possible,the agriculture and agri-food sectorwill probably have to concentrateeven more on the quality aspect of itsproducts.

Obesity and its complications, alongwith many cardiovascular disorders,have food-related causes thatscientists and the general public nowunderstand fairly well. In the future,Quebec’s food sector will probablyoffer many opportunities for thedevelopment of products that addressthe health concerns of the population.

Families are busier than ever before,and their time is at a premium. Inmany families, both spouses workand have less time to spend onpreparing meals. These trends havebeen clear for some time, and there isevery indication that they will continuein the future. Consumers are thereforeseeking healthy foods that can beprepared quickly and easily.

The number of people per householdis falling, and the trend now is towardshouseholds composed of one or twopeople (63% of all households in2001).4 The number of childlesscouples and the growing numbers ofyoung adults (20 to 29 years of age)who live with their parents also havean impact on consumer habits.

The impact of the cultural communitieson society is significant. They havetheir own dietary preferences thatinfluence, at least to some extent, the variety of foods stocked in localmarkets, thus contributing to changesin consumer habits.

In the 1990s, consumers graduallybegan to incorporate ethical, politicaland environmental considerations intotheir food and consumption choices.This ongoing trend has led to theemergence of new requirements forcompliance with certain valuesapplicable to production, processingand distribution activities.Considerations such as animalwelfare, local or regional production,environmental certification, fair trade,ecological products and organicfarming now have an influence onconsumer choices.

The media have played, and willcontinue to play, a leading role inshaping eating trends. Famous chefshave become household names. The quality and nutritional value offood products, along with questionsof taste, are discussed in newspaperand magazine articles and on radioand television, helping to changeconsumer perceptions and choices.

The Commission invitesparticipants to think about theprincipal changes influencing thedemand for food products:

• Is Quebec’s agriculture and agri-food sector fully prepared to respond to present and futureconsumer needs?

• What do you think of publichealth issues, in particular thecreation of settings moreconducive to healthy eatinghabits?

7

8

WORLD DEMAND FOR FOODPRODUCTS

According to studies published by the Food and Agriculture Organization(FAO),5 the world population isincreasing by more than 70 millionpeople per year, and will level off atroughly 9.3 billion in 2050. Most ofthis growth will take place in Asia,Africa and Latin America. Forty-fivepercent of the world’s population lived in cities in 1995, a figure that is expected to rise to 60% by 2015.Clearly, this will have a significantimpact on farming.

Demographic growth, rising incomelevels, changing diets and rising per-capita consumption all influencethe demand for food. The averagedaily per-capita food consumption will rise in developing countries; in the developed world, it is already atpeak levels.

According to FAO forecasts for the period 2000 to 2030,the demand for farm productswill increase by 60%, and willhave doubled by 2050.

Diets will also change. The Organisationfor Economic Co-operation andDevelopment (OECD) and the FAO6

estimate that most of the increase inper-capita food consumption will befor animal protein. This is due to theincrease in per-capita income in manyparts of the world. As incomes rise,people choose to consume meat,eggs and dairy products morefrequently, instead of eating onlycereals such as rice, corn and millet.

The combined effect of changingdiets and demographic growthcaused world consumption of meat to almost quadruple in the period1950 to 1997. The FAO forecasts an additional increase of 23% for the period 2006 to 2015.

The FAO also forecasts that worldfood production should normally besufficient to meet this demand in thecoming decade. Production will beincreased among other things throughnew production technologies, largercultivated areas, more intensecultivation, better yields, the use ofbiotechnologies and more suitablevarieties, better public informationand research.

On the other hand, the problem of the gap in food availability, due mainlyto access and distribution difficulties,will continue to exist, especially indeveloping countries where, eventoday, some 776 million people do not have enough to eat.

The Commission would likeparticipants to reflect on andpropose solutions to the followingquestions:

• How should Quebec respond tothe dynamics of world trade inagricultural and agri-foodproducts?

• Should the anticipated increase in world demand for animalprotein be seen as an opportunityfor Quebec’s agri-food sector?

POVERTY, ABUNDANCE ANDWASTAGE

Significant quantities of farm produceand food stuffs are lost at every levelof the food chain. American researchestimates that between 40% and50% of all the food produced,processed and distributed neverreaches consumers due to cumulativelosses along the way.

The average American familywastes 130 kg of food peryear.7 Although precise figuresare not available for Quebecand Canada, it is reasonable to assume that consumerbehaviour is more or less the same.

Food banks do their best to use safefood resources that would otherwisebe discarded, directing them towardsunderprivileged segments of societyincluding many children. Socialgroups regularly criticize the paradoxof a society of abundance and wastein which Quebecers of all agesregularly miss meals because theysimply cannot afford them. Consumergroups also point out the weaknessesof the distribution network in poorneighbourhoods, especially withregard to fruits and vegetables.

The Commission would like toreceive comments andrecommendations on this subject.

• How can the agriculture and agri-food sector help combatunder nourishment andmalnutrition?

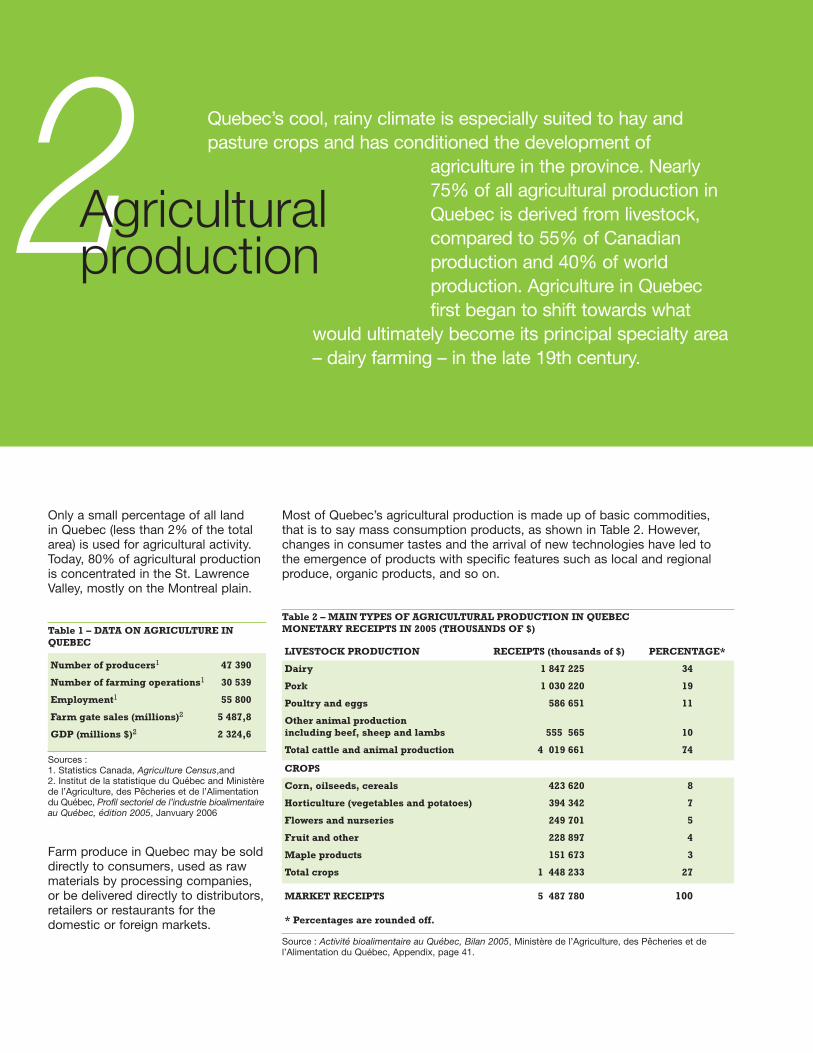

Only a small percentage of all land in Quebec (less than 2% of the totalarea) is used for agricultural activity.Today, 80% of agricultural productionis concentrated in the St. LawrenceValley, mostly on the Montreal plain.

Table 1 – DATA ON AGRICULTURE INQUEBEC

Number of producers1 47 390

Number of farming operations1 30 539

Employment1 55 800

Farm gate sales (millions)2 5 487,8

GDP (millions $)2 2 324,6

Sources : 1. Statistics Canada, Agriculture Census,and 2. Institut de la statistique du Québec and Ministèrede l’Agriculture, des Pêcheries et de l’Alimentationdu Québec, Profil sectoriel de l’industrie bioalimentaireau Québec, édition 2005, Janvuary 2006

Farm produce in Quebec may be solddirectly to consumers, used as rawmaterials by processing companies,or be delivered directly to distributors,retailers or restaurants for thedomestic or foreign markets.

Quebec’s cool, rainy climate is especially suited to hay andpasture crops and has conditioned the development of

agriculture in the province. Nearly75% of all agricultural production inQuebec is derived from livestock,compared to 55% of Canadianproduction and 40% of worldproduction. Agriculture in Quebecfirst began to shift towards what

would ultimately become its principal specialty area– dairy farming – in the late 19th century.

2Agriculturalproduction

Table 2 – MAIN TYPES OF AGRICULTURAL PRODUCTION IN QUEBEC MONETARY RECEIPTS IN 2005 (THOUSANDS OF $)

LIVESTOCK PRODUCTION RECEIPTS (thousands of $) PERCENTAGE*

Dairy 1 847 225 34

Pork 1 030 220 19

Poultry and eggs 586 651 11

Other animal productionincluding beef, sheep and lambs 555 565 10

Total cattle and animal production 4 019 661 74

CROPS

Corn, oilseeds, cereals 423 620 8

Horticulture (vegetables and potatoes) 394 342 7

Flowers and nurseries 249 701 5

Fruit and other 228 897 4

Maple products 151 673 3

Total crops 1 448 233 27

MARKET RECEIPTS 5 487 780 100

* Percentages are rounded off.

Source : Activité bioalimentaire au Québec, Bilan 2005, Ministère de l’Agriculture, des Pêcheries et del’Alimentation du Québec, Appendix, page 41.

Most of Quebec’s agricultural production is made up of basic commodities,that is to say mass consumption products, as shown in Table 2. However,changes in consumer tastes and the arrival of new technologies have led to the emergence of products with specific features such as local and regionalproduce, organic products, and so on.

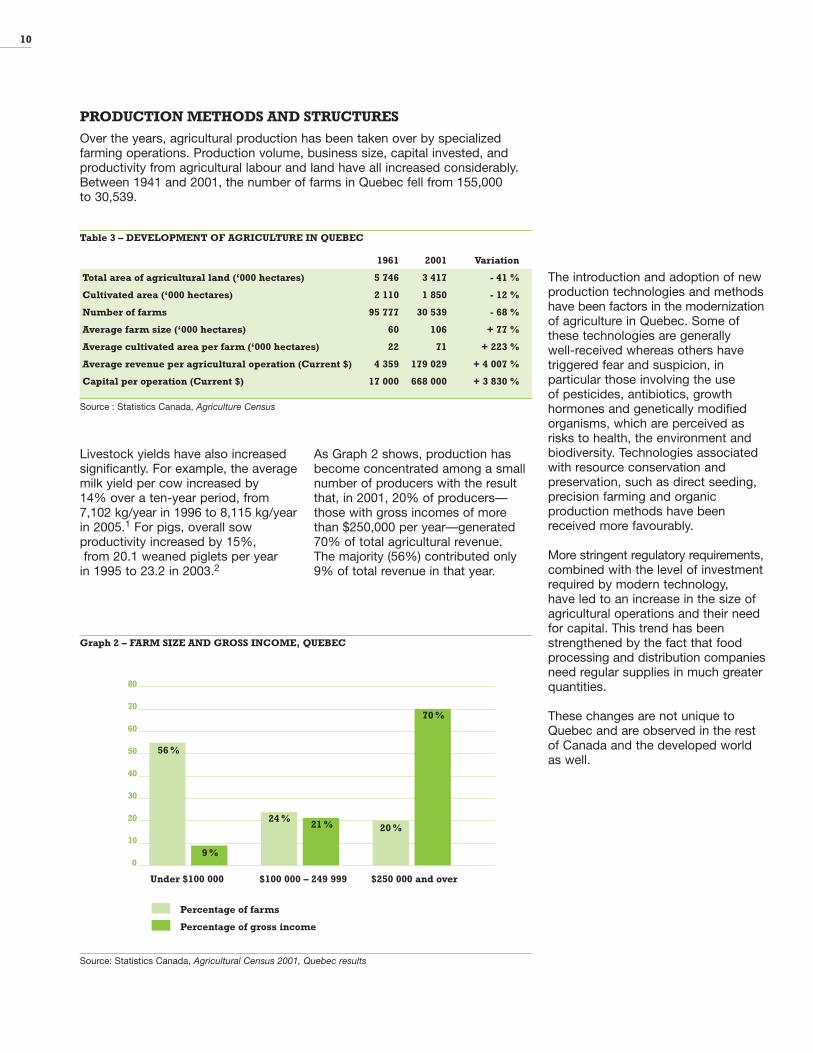

Livestock yields have also increasedsignificantly. For example, the averagemilk yield per cow increased by 14% over a ten-year period, from7,102 kg/year in 1996 to 8,115 kg/yearin 2005.1 For pigs, overall sowproductivity increased by 15%,from 20.1 weaned piglets per year

in 1995 to 23.2 in 2003.2

As Graph 2 shows, production hasbecome concentrated among a smallnumber of producers with the resultthat, in 2001, 20% of producers—those with gross incomes of morethan $250,000 per year—generated70% of total agricultural revenue. The majority (56%) contributed only9% of total revenue in that year.

The introduction and adoption of newproduction technologies and methodshave been factors in the modernizationof agriculture in Quebec. Some ofthese technologies are generally well-received whereas others havetriggered fear and suspicion, inparticular those involving the use of pesticides, antibiotics, growthhormones and genetically modifiedorganisms, which are perceived asrisks to health, the environment andbiodiversity. Technologies associatedwith resource conservation andpreservation, such as direct seeding,precision farming and organicproduction methods have beenreceived more favourably.

More stringent regulatory requirements,combined with the level of investmentrequired by modern technology, have led to an increase in the size ofagricultural operations and their needfor capital. This trend has beenstrengthened by the fact that foodprocessing and distribution companiesneed regular supplies in much greaterquantities.

These changes are not unique toQuebec and are observed in the restof Canada and the developed worldas well.

10

PRODUCTION METHODS AND STRUCTURES

Over the years, agricultural production has been taken over by specializedfarming operations. Production volume, business size, capital invested, andproductivity from agricultural labour and land have all increased considerably.Between 1941 and 2001, the number of farms in Quebec fell from 155,000 to 30,539.

Table 3 – DEVELOPMENT OF AGRICULTURE IN QUEBEC

1961 2001 Variation

Total area of agricultural land (‘000 hectares) 5 746 3 417 - 41 %

Cultivated area (‘000 hectares) 2 110 1 850 - 12 %

Number of farms 95 777 30 539 - 68 %

Average farm size (‘000 hectares) 60 106 + 77 %

Average cultivated area per farm (‘000 hectares) 22 71 + 223 %

Average revenue per agricultural operation (Current $) 4 359 179 029 + 4 007 %

Capital per operation (Current $) 17 000 668 000 + 3 830 %

Source : Statistics Canada, Agriculture Census

Graph 2 – FARM SIZE AND GROSS INCOME, QUEBEC

Source: Statistics Canada, Agricultural Census 2001, Quebec results

Under $100 000 $100 000 – 249 999 $250 000 and over

Percentage of farms

Percentage of gross income

50

60

70

80

40

30

20

10

0

56 %

9 %

24 %21 % 20 %

70 %

CONCERN ABOUT THEINCOME OF FARMS ANDFARMING FAMILIES

The income of farmers and farmingfamilies is a constant and majorconcern. Farm families have similarneeds to their city-dwellingcounterparts. On the other hand,rising investments have caused themto accumulate increasingly significantfinancial liabilities. Farm incomes canalso vary from year to year as a resultof price fluctuations, bad weather,natural disasters and otheruncontrollable phenomena.

Agriculture is a capital-intensiveactivity. In other words, the amount of capital required per unit of productsold is generally higher than in othersectors. In Canada’s economy as awhole, a company needs approximately$2 in assets for every $1 in sales,whereas in the agricultural sector, the ratio is between $4 and $6 in assets for every $1 in sales.3

Net farm income, including paymentsfrom government programs, is morestable and slightly higher in Quebecthan elsewhere in Canada.4 However,without subsidies from governmentprograms, net farm income wouldhave been negative in recent years.Low farm incomes are not confined toQuebec since this is a characteristicof most developed economies.

The debt ratio (total debt/total assets)of farms in Quebec has risen steadilysince 1994 and is now even higherthan that of other provinces.5,increasing from 21% in 1994 to 28%in 2004 (compared with 14% to 19%for Canada as a whole.) Although thedebt ratio in Quebec appears to be anindicator of the sector’s fragility, it islower than Canada’s general economy(74%) and therefore does not seem tobe as elevated in comparison.6

The incomes of farming families in many developed countries arecomparable to if not higher than thoseof non-farming families, as studies by the Organisation for Economic Co-operation and Development(OECD) have shown.7 In Quebec, in 2000, farming families had anaverage income of $59,696,compared to $59,297 for Quebecfamilies in general.8 In Canada, in the same year, farming familiesreported average incomes of $66,270compared with $66,160 for non-farming families. This is explained by the fact that, in 2000, Quebec’sfarming families earned 57.6% of theirincome outside the farm. In Canada,the figure was 73.5%. This trend hascontinued; in 2003, off-farm revenuesaccounted for 62.2% of the incomesof farming families in Quebec,compared with 78.8% for farmingfamilies in Canada as a whole. Incomparison, in the United States, off-farm revenue as a percentage ofthe total revenue of farming familiesrose from 53% in 1960 to 95% in 2000.9

Although farm owners in Quebec havehigher debt levels than their Canadiancounterparts, the value of their assetshas also increased; the average netvalue of a farm in Quebec (assetsminus liabilities) was $170,000 in 1981,but had risen to $725,000 in 2004(including production quotas).10

All the above data are averages, andthe situation of individual farms maydiffer significantly.

Accordingly, the Commission wouldlike to hear participants’ reactionsto the following questions:

• What do these trends mean for the future of small, medium-sizedand large farms in Quebec?

• What strategies are required to manage the consequences of these trends?

• What role should be played by the State?

AGRICULTURAL POLICIES

Agricultural policies cover manydifferent aspects of agriculture. The best-known include food safety,plant and animal health, soil andenvironmental protection, incomeimprovement and stabilization,financing, training and labour, researchand development, outreach andtechnology transfers, farm support,and property tax reimbursements.Some of these areas fall under theauthority of both levels of government.

11

In 2003-2004, Quebec rankedsecond among Canada’sprovinces for governmentspending in the agriculturalsector, with $704 million, theequivalent of 12.9% ofagricultural revenue generatedby farms. Alberta ranked firstwith $886 million and 13.4% of farm revenue, while Ontariowas fourth, with $455 million or 5.6% of farm revenue.11

Quebec’s agricultural policies, likethose of most industrialized countries,are aimed mainly at improving andstabilizing farmers’ income andproviding citizens with a regularsupply of food at a price they canafford to pay.

Quebec and Canadian agriculturalpolicies are directed towards threemain areas of focus, namely collectivemarketing, farm income improvementand stabilization, and farm financing.

COLLECTIVE MARKETING

Traditionally, farmers sold their ownproduce to a fairly small set ofintermediaries, who set the conditionsof sale. In the 1950s, the Quebecgovernment created the Comitéd’enquête pour la protection desagriculteurs et des consommateurs(commonly known as the HéonCommission), which tabled its reportin 1955. Its main recommendationwas to establish mechanisms thatwould allow farmers to market theirproducts collectively. The reportstipulated that its recommendationswere designed to trigger a significantincrease in the agricultural sector’s realnet revenue and purchasing power.

Collective marketing, by strength of numbers and centralized salesoperations, helps improve thenegotiating power of farmers. It canbe put into practice in a variety ofways, but there are three approachesin particular that appear to be mostpopular. The first is the voluntaryapproach through a marketing groupor cooperative, with no mandatorymembership. The second involvessetting up a single, mandatory salesorganization for a given product,known as a joint plan. Once accepted,the joint plan must be used by allunits of production supplying thecommodity in question. The thirdapproach is also based on the jointplan, with the addition of productionquotas, which are allocated amongproducers.

In 1956, the government followed up on the Héon Commission’srecommendations by adopting the Act respecting the marketing ofagricultural, food and fish productswhich allowed for the creation of jointmarketing plans for agriculturalproducts. Since then, producers havedeveloped joint plans for dairy,poultry, turkeys, table eggs, hatchingeggs, pork, maple, beef, blueberries,cash crops (grains), rabbits, cannerycrops (vegetables), apples, potatoes,goat and lamb. To implement the jointplans, marketing boards have beenset up at the producers’ request. They are generally controlled byfederations of producers.

The federal government added aquota-based supply managementsystem to the joint plan formulathroughout Canada. Supplies for milk,table eggs, hatching eggs, chickenand turkey are all managed in thisway. The system serves to controland limit production in Canada as awhole and by province, based on therequirements of the domestic market.Supply is set based on estimateddemand in order to obtain a pricecalculated on the cost of production.

When a system like this is introducedfor a given product, the Canadianquota is divided among the producingprovinces based on historicalproduction figures. The provincialmarketing boards administer thequotas and allocate them toproducers based on individualproduction histories, and then takecare of marketing.

The power to set quotas for productionis associated with the ability to controlimports. The Canadian governmentprotects its domestic market by settinghigh customs tariffs for imports:192.3% for table eggs, 280.4% forwhole chickens, 289% for cheddarcheese, and 351.4% for butter.Despite these tariffs, significantquantities of all these products are imported into Canada. This isespecially true of eggs from theUnited States.

Generally speaking, quotas aretransacted individually betweenproducers, or when farms are sold.Their total value in all supply managedsectors in Quebec was estimated atapproximately $9.2 billion in 2005.11

12

Milk is an exception to this generalrule. Quotas are sold through theFédération des producteurs de lait du Québec which has created acentralized quota exchange system.Quota values have risen steadily. InOctober 2006, the quota for the yieldof roughly one dairy cow was sellingat a historical high of over $33,000.The rise in quota prices has becomeof increasing concern to theproducers’ federations, especially inthe dairy sector in Quebec and otherCanadian provinces. The high cost ofa quota now constitutes a barrier toanyone wishing to purchase a farm. It is also one of the main causes ofindebtedness for dairy farmers.

The emergence on the market ofproducts not covered by the sametariff requirements has, in some cases,become a way of circumventing thecustoms barriers protecting sectorswith quotas.

Some new products that were notforeseen when the barriers wereerected can now be found on theCanadian and Quebec markets,including concentrated milk proteinswhich cost less and are used mainlyas substitutes in the production ofcheese and yoghourt, as well asbutter oil-sugar combinations that areused to manufacture ice cream.

Supply management and collectivemarketing methods are not popular inevery quarter. One of the criticismsoften directed at this type ofmechanism is the fact that it does notadjust quickly to changes in demand.It has been claimed that productprices would decline and consumerdemand would increase if quotaswere eliminated, allowing processingcompanies to become morecompetitive. In contrast, there areclaims that deregulation experimentsin other countries have caused adecline in the price paid to producerswith no obvious benefit to consumers.There are also those who would likeother stakeholders, includingprocessing companies, distributorsand consumers, to be involved in themanagement of Quebec’s marketingboards.

INCOME IMPROVEMENTAND STABILIZATIONPROGRAMS

The two levels of government haveintroduced a set of interventionmeasures aimed at reducing theimpact of the inherent risks ofagricultural production and improvingproducers’ revenues. Quebec, forexample, has crop insuranceprograms and farm incomestabilization insurance programs.

The first level of intervention withregard to income improvement andstabilization is the CanadianAgricultural Income StabilizationProgram (CAIS), created in 2003. Its purpose is to stabilize overall farmincome on the basis of historical netincome regardless of actual productionvolume. This type of program isdescribed as “decoupled” because it is not based on production leveland does not offer guaranteed prices for products. Accordingly, it is considered to be in compliancewith the standards negotiated ininternational agreements.

In Quebec, the Program isadministered by La Financièreagricole.13 It is funded by the federal(60%) and Quebec provincial (40%)governments. Financial participationby farmers varies from year to year,depending on differences in insuredincome. In 2004, the Program paid atotal of $181 million to agriculturalproducers. It is currently under review,as part of a new Canadian frameworkstrategy for agriculture, expected tocome into force in 2008.

13

The Commission therefore poses the following questions:

• Do the current collective marketing mechanisms in force for agriculturalproducts allow the agri-food industries to respond quickly and adequatelyto market needs in Quebec, Canada and abroad?

• Do they leave sufficient room for new products and niche production?

• Do marketing strategies based on supply management have a place in thepresent context of market liberalization? If so, what are their advantagesand disadvantages, and how could they be improved?

• Which measures should receive priority for helping supply-managedproduction sectors to deal with international competitors who succeed in circumventing Canada’s high tariff barriers?

• Should the structure of the marketing boards, currently under the authorityof agricultural producers, be expanded to allow for the involvement of other interests, such as those of consumers and processors?

• Should agricultural policies leave more room for the goals of healthy eating and public health?

Farm Income Stabilization Insurance(known by its French acronym ASRA)is a Quebec program that waslaunched in the late 1970s. It isadministered by La Financièreagricole and supplements the federalprogram for 20 commodities.* Itspurpose is to protect producers frommarket risks. Producers themselvesprovide one-third of the funding, andthe government provides the othertwo-thirds. The program recorded adeficit of $373 million in 2005-2006.

ASRA has paid outcompensation every year on 12 of the 20 products itcovers. There is no ceiling per farm on the amount ofcompensation payable.

Because ASRA applies to specificproducts and is based on the pricesreceived by producers for theproducts covered, it is more open tochallenge under international traderules. Although product supportprograms reduce income variability,the OECD feels they also distortmarket rules and allow production tobe maintained independently ofmarket needs. In other words, they donot encourage producers to questiontheir production choices. This form of income support is includedamongst those that are susceptible to being reduced by virtue of theagreements reached within theframework of the WTO negotiations.

The FAO,14 for its part, believes farmsupport should foster environmentalprotection and social aspects ratherthan production objectives.

Other measures also exist to helpmanage the inherent risks of farming,including crop insurance, whichprotects against natural disasters. The crop insurance program coversonly 16 types of production andcertain types of risks. It paid outnearly $56 million in coverage in 2005.

The programs managed by LaFinancière agricole du Québec (FADQ)are funded in part by the Ministère de l’Agriculture, des Pêcheries et de l’Alimentation du Québec. Thedepartment provided the FADQ, in2005-2006, with $305 million whichrepresents about half of its $637.4million budget. In addition, $93.5million was disbursed to producers in the same year by the department to cover the reimbursement of aportion of their property taxes.

The property tax reimbursementprogram takes into account the highlevel of capital investment in thefarming sector compared to othereconomic sectors, and the return oncapital which is lower than in othersectors. The program ensures that thefarming sector is not undulypenalized.

The Commission proposesreflection in the following areas:

• To what extent should the Stateintervene to support or increasethe income of agriculturaloperations?

• What form should Stateinterventions take, in terms of type of agriculture, type offarm and type of production?

• What should the State’s prioritygoals be?

• What type of assistance shouldthe State offer to producers?

• Should financial assistancedepend on the nature and volumeof the farm produce, theoperation’s total income, size or development stage, or othercriteria?

• Should the State continue tosupport types of production thathave been in deficit for 10, 12 and even 20 years?

• What could farmers do to maketheir farms less vulnerable andincrease their flexibility?

14

* Finished hogs, cow-calf, finished beef, grain-fed veal, milk-fed veal, lambs, milk lambs,heavy lambs, grain corn, soya, barley, oats, wheat silage, wheat for human consumption, feedwheat, barley, potatoes (fresh and stored), apples.

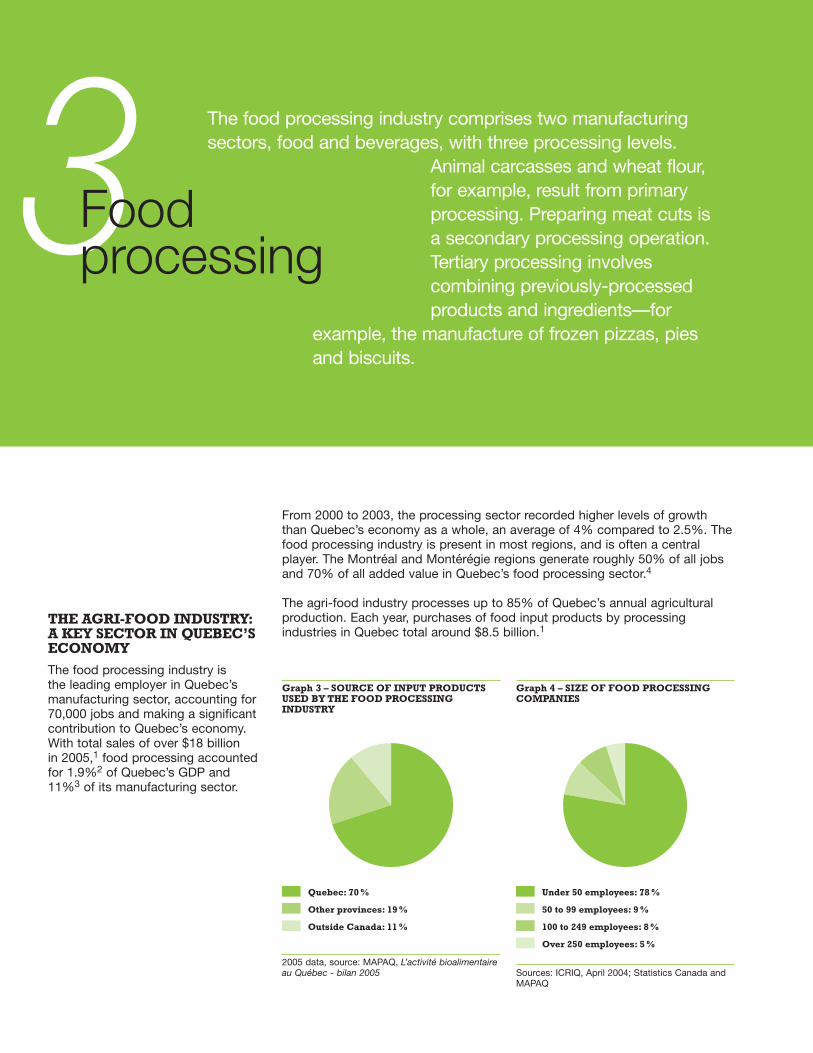

THE AGRI-FOOD INDUSTRY:A KEY SECTOR IN QUEBEC’SECONOMY

The food processing industry is the leading employer in Quebec’smanufacturing sector, accounting for70,000 jobs and making a significantcontribution to Quebec’s economy.With total sales of over $18 billion in 2005,1 food processing accountedfor 1.9%2 of Quebec’s GDP and 11%3 of its manufacturing sector.

Graph 3 – SOURCE OF INPUT PRODUCTSUSED BY THE FOOD PROCESSINGINDUSTRY

2005 data, source: MAPAQ, L’activité bioalimentaireau Québec - bilan 2005

Graph 4 – SIZE OF FOOD PROCESSINGCOMPANIES

Sources: ICRIQ, April 2004; Statistics Canada andMAPAQ

The food processing industry comprises two manufacturingsectors, food and beverages, with three processing levels.

Animal carcasses and wheat flour, for example, result from primaryprocessing. Preparing meat cuts is a secondary processing operation.Tertiary processing involvescombining previously-processedproducts and ingredients—for

example, the manufacture of frozen pizzas, pies and biscuits.

3Foodprocessing

Quebec: 70 %

Other provinces: 19 %

Outside Canada: 11 %

Under 50 employees: 78 %

50 to 99 employees: 9 %

100 to 249 employees: 8 %

Over 250 employees: 5 %

From 2000 to 2003, the processing sector recorded higher levels of growththan Quebec’s economy as a whole, an average of 4% compared to 2.5%. Thefood processing industry is present in most regions, and is often a centralplayer. The Montréal and Montérégie regions generate roughly 50% of all jobsand 70% of all added value in Quebec’s food processing sector.4

The agri-food industry processes up to 85% of Quebec’s annual agriculturalproduction. Each year, purchases of food input products by processingindustries in Quebec total around $8.5 billion.1

Twenty-two percent of operations withless than 50 employees have fewerthan five employees, 38% have five to 19 employees, and 18% have 20 to49 employees. Together, they provide19.5% of all jobs in the sector.

Graph 5 – PURCHASERS OF PRODUCTSPROCESSED IN QUEBEC

The cooperative sector occupies a key position in Quebec’s foodprocessing industry, accounting forroughly 25% of processed shipments.Cooperatives process around 85% ofthe poultry and over half of the milkand pork produced in Quebec.4

The processing industry is located atthe junction of two highly structuredsystems, downstream from agriculturalproduction and upstream from fooddistribution, both of which are keylinks in the agri-food chain.

PROCESSING ANDAGRICULTURAL PRODUCTION

It is generally recognized that Quebecprocessors can rely on a secure, well-structured supply of raw agriculturalmaterials. A feature of Quebec’sprocessing industry is its strong ties toproduction, especially in the sectorsdirectly connected to livestockproduction (milk, meat, eggs andpoultry) which account for 53% of thevalue of processed shipments; thesesectors spend 70% of their revenueon the purchase of raw agriculturalmaterials.1

A high percentage of Quebec’sagricultural production is marketedcollectively. This gives farmers adegree of leverage in their transactionswith Quebec processors. The foodprocessing industry in Ontario is morediversified and less dependent on thecost of the raw material supply. Someobservers have pointed out thatQuebec and Canada’s joint marketingmechanisms may, in some cases,place upward pressure on supplycosts making processors less cost-effective than their foreigncompetitors. Others consider that thejoint marketing systems are not suitedto the needs of processors producingniche products.

PROCESSING AND FOODDISTRIBUTION

Over the last two decades, in bothQuebec and Canada, there has beena trend towards concentration andconsolidation in the distributionsector. Market access has becomemore difficult, in particular for smalland medium-sized processing firmsthat cannot always supply thevolumes required by the majordistribution networks. Concentrationin the distribution sector has reducedcompetition. In addition, manystrategic decisions in the distributionsector are now made outside Quebec.

Agri-food companies must face thetwin challenge of competitiveness andproductivity. Processing firms inQuebec are less productive than theircounterparts in Ontario. StatisticsCanada reports that the combinedproductivity of the agriculturalproduction/processing chain inOntario is higher than in Quebec.GDP per employment is also regardedas a strong indicator of productivity. In food processing, this figure is 27%lower in Quebec than in Ontario. It hasbeen suggested that this productivitygap can be explained, at least in part,by the fact that there are fewer largecompanies (500 employees and over)in Quebec (2.8% of the total) than inOntario (5%) and elsewhere inCanada (4.2 %).5

Technology is also an importantvector for productivity. In this regard,Quebec’s smaller domestic markethinders access to cutting-edgetechnology, creates fewer opportunitiesfor economies of scale, and reducespurchasing power.

16

Retail sector and HRI, Quebec: 39 %

Retail sector and HRI, other provinces: 26 %

International: 18 %

Production and processing, Quebec: 17 %

The gross margin for Quebec’sfood processing industriesaveraged 23% between 2000and 2003, compared to 27% in Ontario and 20% for all otherCanadian provinces. Otheranalyses show that theprofitability of Canadianprocessing companies is 50%below that of firms in theUnited States.

Quebec firms are also vulnerable to tariff and non-tariff trade barriers,especially in the United States andJapan, which are Quebec’s two mainexport markets.

Worker availability is another importantfactor in productivity. Like severalother manufacturing sectors, the foodprocessing sector is finding it difficultto hire workers.

For both overseas and domesticmarkets, the strength of the Canadiandollar has increased foreigncompetition, particularly from theUnited States.5

Quebec food processing firms can,however, rely on a network ofinstitutional resources to meet theirtraining and research and developmentneeds. The scope and quality ofQuebec’s effective, well-structuredsocial programs, designed to meetthe needs of their employees, areanother significant advantage.Quebec offers some of the mostadvantageous production factors inthe world, including a reliable,abundant and competitively-pricedenergy supply, as well as access to aplentiful supply of high-quality water.

The Commission’s questionsconcern the measures that shouldbe taken to improve the productivityand competitiveness of Quebec’sfood processing industry:

• How can Quebec’s foodprocessing companies put theiradvantages to better use andimprove their competitivecapacity in domestic and foreignmarkets?

• Is the cost of raw agriculturalmaterials a problem? If so, how is it a problem and what are theconsequences?

• How can specialized processorsbe given better access todistribution networks?

• How can companies be assured of the manpower they need?

NEW MARKETDEVELOPMENT

Several stakeholders have mentionedthat few Quebec companies own orcontrol brands that are recognizedthroughout the Canadian market. Onthe other hand, the Quebec market isopen to products sold under brandscontrolled by Canadian corporationsoutside Quebec, or internationalcorporations.

Distributor brands are graduallyincreasing their market share, and the most productive firms are givenpreference when sub-contracts areawarded. As a result, recognition fornational brands controlled by Quebecfirms is a strategic issue.

In several sectors of activity, includingmass-market products, it is hard forQuebec firms to compete with largeCanadian or foreign corporations,especially in export markets. Theneed to supply large volumes on aregular basis prevents many smallfirms from gaining access to thesemarkets.

It has been suggested that theprocessing industry in Quebec can be developed by focusing on nichemarkets with higher added value,such as luxury products, includingfoie gras, ice cider and fine cheeses,health products such as preparedvegetarian dishes, organically-certifiedproducts and health-enhancing foods,and products of high practical valuesuch as pre-cut apples, preparedmeats and dishes, etc.

To capture a market niche,businesses must exhibit creativity, ahighly-developed sense of innovation,and a strong ability to adjust quicklyto a particular context. Many firmshave in fact been successful in nichemarkets showing that versatility,creativity and the ability to innovatecan allow an enterprise to seize newbusiness opportunities.

The Commission would likeparticipants to respond thefollowing questions:

• What are the most promisingmarket sectors?

• What conditions must bedeveloped in order to seizebusiness opportunities?

• What measures can be introduced to ensure thatorganizations at different levelsin the agri-food chain read themarket signals and work jointlyto prepare a response?

• What role should the State play?

• How can processors beencouraged to develop productswith positive impacts on health?

17

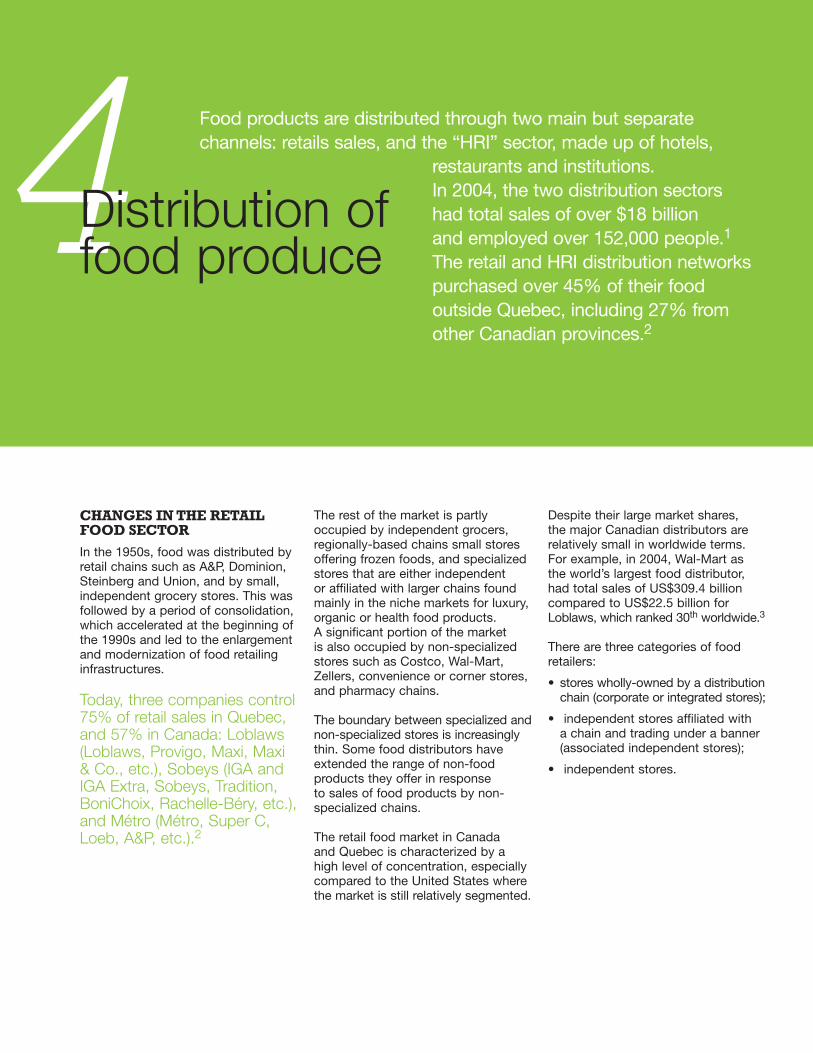

CHANGES IN THE RETAILFOOD SECTOR

In the 1950s, food was distributed byretail chains such as A&P, Dominion,Steinberg and Union, and by small,independent grocery stores. This wasfollowed by a period of consolidation,which accelerated at the beginning ofthe 1990s and led to the enlargementand modernization of food retailinginfrastructures.

Today, three companies control75% of retail sales in Quebec,and 57% in Canada: Loblaws(Loblaws, Provigo, Maxi, Maxi& Co., etc.), Sobeys (IGA andIGA Extra, Sobeys, Tradition,BoniChoix, Rachelle-Béry, etc.),and Métro (Métro, Super C,Loeb, A&P, etc.).2

The rest of the market is partlyoccupied by independent grocers,regionally-based chains small storesoffering frozen foods, and specializedstores that are either independent or affiliated with larger chains foundmainly in the niche markets for luxury,organic or health food products. A significant portion of the market is also occupied by non-specializedstores such as Costco, Wal-Mart,Zellers, convenience or corner stores,and pharmacy chains.

The boundary between specialized andnon-specialized stores is increasinglythin. Some food distributors haveextended the range of non-foodproducts they offer in response to sales of food products by non-specialized chains.

The retail food market in Canada and Quebec is characterized by ahigh level of concentration, especiallycompared to the United States wherethe market is still relatively segmented.

Despite their large market shares, the major Canadian distributors arerelatively small in worldwide terms.For example, in 2004, Wal-Mart as the world’s largest food distributor,had total sales of US$309.4 billioncompared to US$22.5 billion forLoblaws, which ranked 30th worldwide.3

There are three categories of foodretailers:

• stores wholly-owned by a distributionchain (corporate or integrated stores);

• independent stores affiliated with a chain and trading under a banner(associated independent stores);

• independent stores.

Food products are distributed through two main but separatechannels: retails sales, and the “HRI” sector, made up of hotels,

restaurants and institutions. In 2004, the two distribution sectors had total sales of over $18 billion and employed over 152,000 people.1

The retail and HRI distribution networkspurchased over 45% of their foodoutside Quebec, including 27% fromother Canadian provinces.2

4Distribution of food produce

The type of connectionbetween a store and its chaininfluences its purchasingdecisions. In particular, it determines the freedom the store has to choose itssuppliers and its ability topurchase products from localproducers or processors.

According to the magazine CanadianGrocer, integrated or corporatestores control a larger market share in Canada (60.7%) than in Quebec(36.7%). However, the combined salesof stores integrated or associated withthe major chains account for a similarmarket share, 95% in Canada and95.9% in Quebec.3 Over the last 20 years, the number of non-associatedindependent stores has decreasedsignificantly. In both Quebec andCanada, they now represent around5% of the market.2

Processing industry representativeshave voiced their concern aboutcommercial practices that increasethe difficulty of placing products insupermarkets. The major chainscharge access fees, called “slotting”fees, and demand large volumes,regular deliveries at fixed times todistribution centres, productstandardization and negotiationthrough a purchasing department. For companies located in outlyingregions, the distance to the decision-making centre compounds thesedifficulties.

A WIDER RANGE OF FOODPRODUCTS

The supply of food products hasnever been so extensive and varied.In 2005, 30,000 products could befound on the shelves of a typicalsupermarket, compared to 6,000 in1953. This is due to the willingness of distributors to respond to theneeds of consumers from a range of cultural backgrounds, and to agrowing diversity of consumer habits.Consumers are also better informedand more receptive to new products.This market shift partly explains thetrend towards the modernization andenlargement of supermarkets inQuebec. It offers business opportunitiesfor producers, processors anddistributors that are able to anticipatetrends and offer innovative, competitiveproducts.

Although these trends create businessopportunities for manufacturers, theyalso increase the marketing challenges.Quebec processors must now advertisetheir products and brands andpersuade consumers, who are shortof time and surrounded by numerousother products, to buy them.

Traditionally, major processors haveinvested heavily to acquire high-volumeproduction equipment and try tomaintain stable, high-volume productionfor as long as possible. However,product life cycles are tending tobecome shorter. Businesses that areslow to adapt lose market share tomore flexible businesses that are ableto adjust quickly to new trends. Thisis the case for the highest-performingsmall and medium-sized businesses,which have become market leadersand have quickly scored impressivebusiness successes with majordistributors.

PRIVATE-LABEL BRANDS

The strong competition betweenCanadian distributors, combined witha fear of US competition, hasgenerated a range of strategies todevelop consumer loyalty. Onestrategy involves promoting productsunder the distributor’s own brandname; the products in question areobviously not available in competingstores. In designing their own-brandstrategies, major distributors can usefirst-hand information on theexpectations and behaviour of theirconsumers, and can adapt swiftly tonew trends. As a result, private-labelbrands such as President’s Choice,Our Compliments and SélectionMérite can compete with nationalbrands owned by processors. Amongother things, these strategies havecreated business opportunities forQuebec companies that do notcontrol dominant national brands.

According to Deloitte & Touche(Benchmarking for Success 2000),private-labels processed foods andbeverages held 27% and 28% of theCanadian market respectively in 1998.It is important to note that privatebrands are stronger in Canada than in the United States. According to AC Nielsen,5 Canada ranks ninthworldwide for the market penetrationof private-label products at 19%compared to 16% in the UnitedStates. Switzerland ranks first at 45%.

19

The gradual opening up of internationaltrade in agricultural and food productsoffers additional business opportunitiesfor major distributors as they takeadvantage of lower-cost supplies,especially for their private-labelproducts. A strong Canadian dollarhas reinforced this trend. Competitionfrom US distributors obtaining suppliesfrom the international market hasencouraged other distributors tofollow the same path.

The competitive capacity of theproduction-processing chain is amajor issue for Quebec’s agri-foodsector.The Commission would liketo hear participants’ thoughts on the following question:

• What steps or measures could be implemented to ensure thatQuebec businesses of all sizes(small, medium and large), and suppliers of niche or localproducts, are able to increasetheir presence within the currentfood distribution system?

FOOD PRODUCT LABELING

The labeling of food products fallsunder the responsibility of theCanadian Food Inspection Agency(CFIA). It has requirements relating tonutritional information, and nutritionaland health claims. In Canada, labelsmust give nutritional information formost food products. This represents a considerable burden for someproducers, who see it as a relativelycostly extra expense. However, thenew requirements may open the wayto new business opportunities byhighlighting the nutritional quality ofcertain products.

Increasingly, consumers want to know what their food contains, andsome go even further and demandinformation on the origin, productionand processing of the food stuffs theyeat. This has been a factor in theproblems caused by the introductionof genetically-modified organisms(GMOs) in the food system, and adebate about the compulsory, asopposed to voluntary, labeling ofGMOs is now under way.

The Commission would like toreceive opinions and comments on the following elements:

• What is the role of labeling? How far should it be taken?

• What information is essential for consumers, and whatinformation should labelscontain?

• Should voluntary GMO labelingbe made compulsory?

• How can the labeling burdenimposed on processing anddistribution companies be takeninto account?

HOTELS, RESTAURANTS ANDINSTITUTIONS (HRI SECTOR)

Hotel, restaurant and institutional food services have grown considerablyin Quebec and represent a keysegment of the market. The percentageof HRI food spending by the Quebecpopulation is increasing although it remains below the level in theUnited States.

In 2004, for the first time in the US, the percentage of HRIspending by consumersexceeded the percentage forgrocery stores. That same year,Quebec’s restaurant sector hadsales of around $7 billion eachyear, a 4.5% increase over2003. Food services in hotelsand institutions accounted foranother $2 billion. The HRIsector employs approximately161,000 people.6

20

The purchasing policies of hotels andrestaurants differ from those of theretail sector. Traditionally, they involvelocating specific products and a moredirect business relationship. There is a clear trend towards consolidation of the HRI distribution sector, in bothQuebec and Canada, and also of themanagement of the major institutionalaccounts and cafeteria services oflarge corporations. Consolidationincreases the purchasing power of the distributors and tends to distancemanufacturers from the decision-makingcentres. One of the effects of the shiftis to add entry barriers for smallproducers and processors who areunable to supply large volumes oftheir products.

Independent restaurants and smallregional chains are often still servicedby local or regional distributors.Quebec reports the highest percentageof firms that are independent and notaffiliated with a chain.

The Commission would like toreceive opinions and comments on the following questions:

• How can Quebec’s agricultureand agri-food sector develop atrue partnership with the HRIsector to take better advantage of the opportunities it offers?

• Should the call for bids issued by public institutions place moreemphasis on Quebec products?

• How can distributors beencouraged to pay more attentionto Quebec products?

STRATEGIC IMPORTANCEOF THE HRI SECTOR

The positioning of processingcompanies with HRI distributors hasoften proved to be a strategic choice.Consumers who are introduced toMexican food, sushi or gastronomy by their experience in a restaurant orthrough the media will often seek outsimilar products on store shelves.

A number of institutions, including the Institut de tourisme et d’hôtelleriedu Québec (ITHQ) and the media,play a key role in guiding consumertrends and raising the visibility of localproducts. The ITHQ has made asignificant contribution to thedevelopment of know-how in therestaurant sector, and has helpedraise Quebec’s profile in this area.

Some stakeholders are still concernedthat the HRI market is neglected byprocessors despite the fact that, inaddition to being strategic, thismarket is generally considered to beless costly and less of a risk. Inaddition, Quebec’s hotel andrestaurant sector is dynamic andcreative, and contributes to theevolution of consumer trends.

21

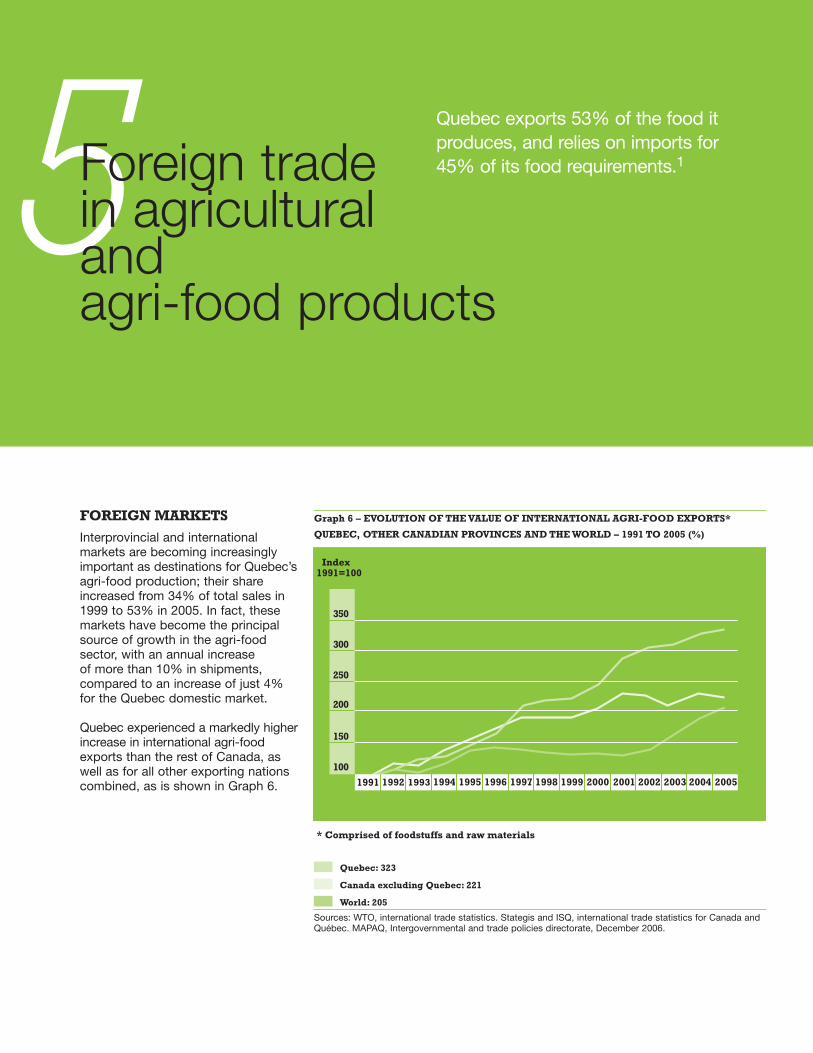

FOREIGN MARKETS

Interprovincial and internationalmarkets are becoming increasinglyimportant as destinations for Quebec’sagri-food production; their shareincreased from 34% of total sales in1999 to 53% in 2005. In fact, thesemarkets have become the principalsource of growth in the agri-foodsector, with an annual increase of more than 10% in shipments,compared to an increase of just 4%for the Quebec domestic market.

Quebec experienced a markedly higherincrease in international agri-foodexports than the rest of Canada, aswell as for all other exporting nationscombined, as is shown in Graph 6.

Quebec exports 53% of the food itproduces, and relies on imports for 45% of its food requirements.15Foreign trade

in agricultural andagri-food products

1991 1992 1993 1994 1995 1996 1997 1999 2000 2001 2002 2003 2004 2005

350

300

250

200

150

100

1998

Graph 6 – EVOLUTION OF THE VALUE OF INTERNATIONAL AGRI-FOOD EXPORTS*

QUEBEC, OTHER CANADIAN PROVINCES AND THE WORLD – 1991 TO 2005 (%)

Index1991=100

* Comprised of foodstuffs and raw materials

Sources: WTO, international trade statistics. Stategis and ISQ, international trade statistics for Canada andQuébec. MAPAQ, Intergovernmental and trade policies directorate, December 2006.

Quebec: 323

Canada excluding Quebec: 221

World: 205

Graph 7 – DESTINATION OF QUEBEC’SFOOD PRODUCTION (2005)

Quebec’s overall international balancefor agri-food trade has been positivesince 1997 mainly as a result of itsexports to the United States. Thebalance of trade with all other countriescontinues to be in deficit; in otherwords, Quebec imports more productsfrom those countries than it exports to them.

Graph 8 – DESTINATION OF QUEBEC’SFOOD EXPORTS (2005)

Quebec’s international exportsincreased by 16% between 2002 and2005. Quebec contributes more than12% of Canada’s total internationalexports, ranking behind Ontario (28%)and Alberta (16%).

International exports rose by morethan 14% in the period 2001 to 2005,and imports by 19%.2 Export growthwas achieved despite a slowdown in2003 that was due, among otherthings, to mad cow disease (bovinespongiform encephalopathy) and thestrength of the Canadian dollar.However, export growth was only 1% in 2004-2005. Data for the firstquarter of 2006 indicates a drop in thevalue of exports. Quebec’s agricultureand agri-food exports accounted formore than 6 % of its total exports in 2003.

A NEW INTERNATIONALMARKET DYNAMIC

Countries such as Mexico, Chile,Brazil, India and China4 are playing a much more important role, offeringproducts at lower prices. Thesecountries enjoy certain advantages,including a labour force and a climatethat allows them to produce rawmaterials and processed products atlittle cost. Their growing presence onthe international stage has emphasizedthe existing downward pressure onprices and will probably alter manyaspects of international trade. However,the increased supply of products hasoccurred in a context where worldwidedemand is also growing. In addition,the cost advantage enjoyed by thesecountries may be counterbalanced bydisadvantages in other areas such asquality, safety, traceability andreliability of shipments.

Competition on international markets islikely to intensify. As a result, Quebec’sfarms and processing companies willneed to be efficient, innovative andflexible to adjust to these changingconditions if they are to maintain orimprove their market position. Inaddition, the probable erosion of tariff protection due to internationalpressure, especially in the tradenegotiations undertaken by the World Trade Organization (WTO), will fragment the domestic marketscurrently under supply management.

Most of the products that areexported are processed products,which in 2005 accounted for nearly85% of Quebec’s exports, comparedwith 76% for Ontario and 60% forCanada as a whole. The principalagri-food exports from Quebec arecomposed of the following notableproducts of animal origin: fresh orfrozen pork, poultry meat, eggs,animal by-products, dairy products,and livestock. The principal exportsfrom plant origin are: cocoa products,miscellaneous food products, fruits andvegetables, honey, maple products andsugar, cereal grains, beverages.

In 2005, Quebec exportedanimal products for a value of$1.6 billion, including $1 billionin fresh or frozen pork.4

23

Quebec: 47 %

Other provinces: 30 %

Exports: 23 %

United States: 63 %

Japan: 14 %

European Union: 6 %

Other: 17 %

Animal products accounted for 43% of total agriculture and agri-foodexports, and pork alone accounted for33%. The vast majority of theseexports went to the American market.Pork exports to the United Statesrose by 58% between 2000 and 2005.Exports of crop products were valuedat $2.2 billion in 2005. The mostimportant individual products werecocoa, with exports valued at $340million or 18% of total food exports,followed by miscellaneous foodstuffsand food products, fruits andvegetables, cereal products, beveragesand maple products.1

It is worth noting that this exportgrowth occurred even as the Canadiandollar soared in value. In the period2002 to 2005, the Canadian dollarrose by 38% against the Americandollar, by 32% against the Yen and by 11% against the Euro.6

The pork industry is Quebec’s primaryexport sector. It is currentlyexperiencing some difficulties and is also facing new internationalcompetitors, including Brazil.1 Meatexports, made up mostly of pork,have declined 20% between 2003and 2005.5

Exports of cocoa derivatives, althoughless at risk for the time being,nevertheless depend on Americansugar policy and the cost of otherproduction factors.

The Commission would like toreceive comments on the followingelements:

• What importance shouldQuebec’s agriculture and agri-food sector ascribe toexports and foreign markets?

• Should our strategies emphasizethe importance of processedproducts?

• In view of worldwide competition,what should Quebec do tomaintain or strengthen itsposition on world markets?

• What can be done to ensure that processing companies arefamiliar with foreign markettrends?

• What kind of balance can bestruck between supplymanagement and exports?

IMPORTS

Quebec’s food product imports fromother provinces and other countriestotaled $3.5 billion in 2005, andincreased by 17% in the period 2002to 2005.7 Imports now satisfy 45% of our food needs and represent 16% of the total value of all Canadianimports. Ontario receives 57% ofCanada’s imports ($12.5 billion).1

Quebec mainly imports processedproducts (more than 70%). The mostimportant imports are beverages (23%),fruits and nuts (19%), cocoa, coffeeand tea (12%), honey and sugar (11%),products containing dairy ingredients(7%) and vegetables (6%).8

The strong Canadian dollar has meantthat imports are more competitive onthe Canadian market. The higher thevalue of the dollar, the more it erodestariff protection measures, especiallyin a context where domestic pricesare rising and world prices are falling.9

This could lead to an increase inimports of certain products, eventhose that are supply-managed andare protected by high tariff barriers.

Clearly, then, Quebec’s economy isfairly dependent on foreign markets,for both consumption and its ownfood production.

Participants are invited to submittheir views on the following points:

• How important is a secure foodsupply in your vision of theagriculture and agri-food sectorin Quebec?

• Do you think the importance ofimports in Quebec is a threat toits own production and to asecure food supply?

• How should the agriculture andagri-food sector deal with theworld trend towards lower tariffbarriers and falling prices?

24

BASIC TRAINING ANDCONTINUING EDUCATION

A broad range of easily-accessibletraining programs at the high school,college and university level areavailable in Quebec. The province’shigh schools dispense more than 20 basic training programs, and 15 of its colleges offer nine additionalprograms.1

The Institut de technologie agroali-mentaire (ITA) has three campuses (La Pocatière, Saint-Hyacinthe andSainte-Anne-de-Bellevue), and is thesector’s largest college-levelinstitution. It has a team of 300 peopleworking on skills development and a well-established reputation that has resulted in a placement rate forits graduates close to 100%. TheInstitution also plays a significant rolein continuing education. In 2004-2005,more than 300 continuing educationsessions were dispensed to nearly4,000 people.2

Université Laval and McGill Universityoffer university-level training inagricultural sciences. Other universitiesand institutes also offer a range ofrelated programs in the fields of biology,the environment and veterinarymedicine.

In the hotel, restaurant and institutionalsector, a number of high schools andcolleges, in addition to the Institut detourisme et d’hôtellerie du Québec(ITHQ), offer educational and trainingprograms. At the ITHQ alone, theapplications for hotel and restaurantmanagement courses remain veryhigh, representing 140% of theavailable places. At the universitylevel, registration in recent years hasgrown by almost 20% each year.3

Human resources in the agriculture and agri-food sector needtraining, advice and expertise if they are to develop their skills

and make the right choices in anincreasingly competitive environment.Research, development, newtechniques and knowledge transferwill all help determine the sector’sfuture. The task of recruiting asufficient number of qualified

employees is also a concern, and workforcedevelopment is yet another challenge for agri-foodenterprises wishing to improve their productivityand innovate.

6Humanresourcedevelopment

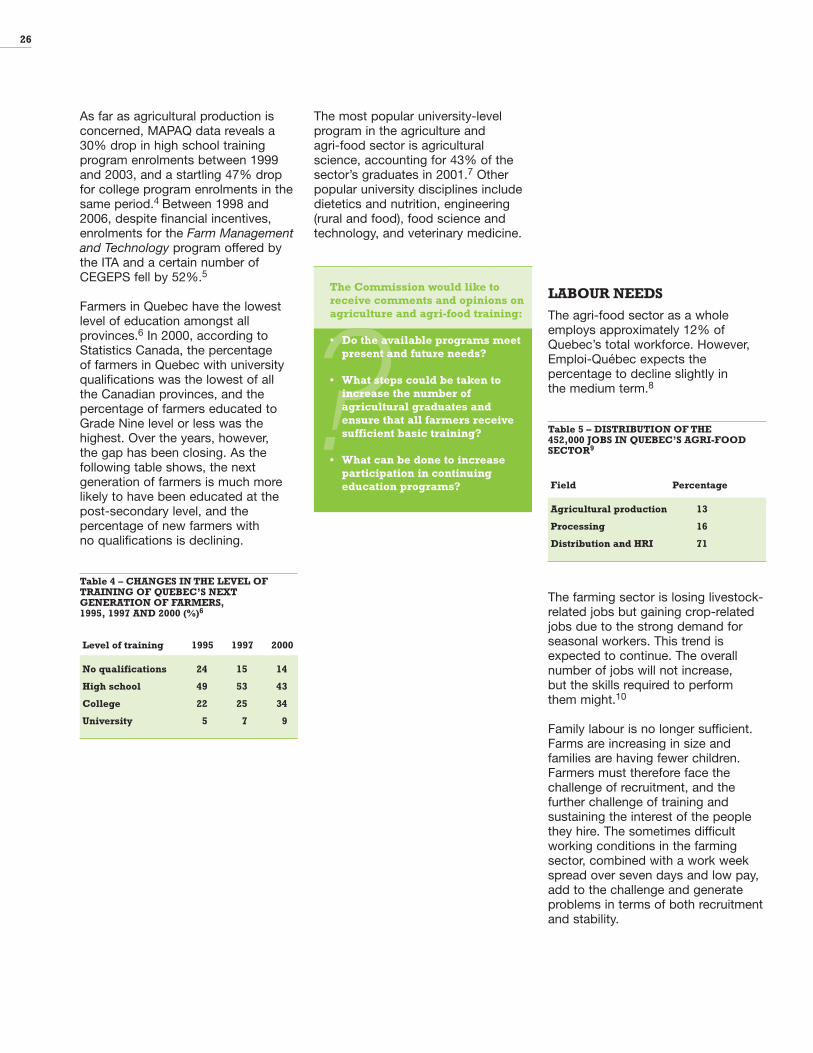

As far as agricultural production isconcerned, MAPAQ data reveals a30% drop in high school trainingprogram enrolments between 1999and 2003, and a startling 47% dropfor college program enrolments in thesame period.4 Between 1998 and2006, despite financial incentives,enrolments for the Farm Managementand Technology program offered bythe ITA and a certain number ofCEGEPS fell by 52%.5

Farmers in Quebec have the lowestlevel of education amongst allprovinces.6 In 2000, according toStatistics Canada, the percentage of farmers in Quebec with universityqualifications was the lowest of all the Canadian provinces, and thepercentage of farmers educated toGrade Nine level or less was thehighest. Over the years, however, the gap has been closing. As thefollowing table shows, the nextgeneration of farmers is much morelikely to have been educated at thepost-secondary level, and thepercentage of new farmers with no qualifications is declining.

Table 4 – CHANGES IN THE LEVEL OFTRAINING OF QUEBEC’S NEXTGENERATION OF FARMERS, 1995, 1997 AND 2000 (%)6

Level of training 1995 1997 2000

No qualifications 24 15 14

High school 49 53 43

College 22 25 34

University 5 7 9

The most popular university-levelprogram in the agriculture and agri-food sector is agriculturalscience, accounting for 43% of thesector’s graduates in 2001.7 Otherpopular university disciplines includedietetics and nutrition, engineering(rural and food), food science andtechnology, and veterinary medicine.

The Commission would like toreceive comments and opinions onagriculture and agri-food training:

• Do the available programs meetpresent and future needs?

• What steps could be taken toincrease the number ofagricultural graduates andensure that all farmers receivesufficient basic training?

• What can be done to increaseparticipation in continuingeducation programs?

LABOUR NEEDS

The agri-food sector as a wholeemploys approximately 12% ofQuebec’s total workforce. However,Emploi-Québec expects thepercentage to decline slightly in the medium term.8

Table 5 – DISTRIBUTION OF THE 452,000 JOBS IN QUEBEC’S AGRI-FOODSECTOR9

Field Percentage

Agricultural production 13

Processing 16

Distribution and HRI 71

The farming sector is losing livestock-related jobs but gaining crop-relatedjobs due to the strong demand forseasonal workers. This trend isexpected to continue. The overallnumber of jobs will not increase, but the skills required to perform them might.10

Family labour is no longer sufficient.Farms are increasing in size andfamilies are having fewer children.Farmers must therefore face thechallenge of recruitment, and thefurther challenge of training andsustaining the interest of the peoplethey hire. The sometimes difficultworking conditions in the farmingsector, combined with a work weekspread over seven days and low pay,add to the challenge and generateproblems in terms of both recruitmentand stability.

26

In the food processing industries andfood-related services sectors, theproblem of recruiting and sustainingthe interest of workers is common.Difficulties arise from the fact thatmany of the jobs are demanding andthe food industry must compete withother types of firms seeking to attractpeople from the same labour pool.

Agriculture and agri-food enterprisesneed a larger workforce that is bothstable and competent if they are tocontinue to develop.

The Commission would like toreceive comments and opinions onthe strategies required to attractand retain human resources in theagriculture and agri-food sector.

• What strategies should be used to provide agriculture and agri-food enterprises with thequalified workers they need?

• What role should governmentsplay?

• How can a new pool of workers,such as immigrants, be attractedto the agriculture and agri-foodsector?

INNOVATION

In the present, highly competitivecontext, everyone agrees on theimportance of innovation. Research,technology watch activities andknowledge transfers are a source of profit and productivity, productdiversification, adapted solutions and new processes.

In 2002, a total of around $178 millionwas invested in agriculture and agri-food research in Quebec, half bythe industry itself, 36% by the federalgovernment and 14% by the provincialgovernment. R&D spending in thesector increased significantly between1995 and 2002, from $43 million to$89 million.6 This situation reflects, in part, the decision by MAPAQ tosupport the development ofpublic/private corporations. R&Dactivities have also been implementedwith input from the industry, and thistransfer of resources has created newleverage.

In 2002, R&D spending byfood processing companiesaccounted for 0.24% ofshipments, compared with0.15% for Canada as a wholeand 0.16% for Ontario6

In fiscal year 2004-2005, MAPAQdirectly invested a sum of $22.5million in technological innovation in the form of support for centres ofexpertise, research corporations andjoint initiatives.10

Knowledge is transferred via extensionactivities. As an example, every yearthe Centre de reference en agricultureet agroalimentaire du Québec(CRAAQ) reaches approximately20,000 clients through its conferences,publications and web-baseddatabank.11 The federations of theUnion des producteurs agricoles(UPA), cooperatives, MAPAQ officesand many other associations alsoorganize a host of extension activities.A number of specialist publicationsand web sites also disseminateinformation.

Based on your own vision of theagriculture and agri-food sector,what strategies are needed tosupport research, technology watch and new knowledge transferactivities:

• Is sufficient money beinginvested in research, technologywatch and new knowledgetransfer activities, and is themoney being properly targeted?

• Do the investments target themarket niches with the bestfuture potential?

• How can exchanges between thevarious knowledge producers beimproved?

• What can be done to maximizethe impact of investments inresearch and development?

• What can local and regionalauthorities do to supportinnovative activities within theirterritories?

• What role should the State play?

27

SPECIALIZED ADVISORYSERVICES

Advisory services are vital to thetransmission of new knowledge. To play their role properly, consultantsmust be aware of recent findings,especially from applied research. Theymust forge and maintain trust-basedcontacts with their customers.

Farm advisory services used to bealmost exclusively the responsibility of MAPAQ. Twenty years ago, MAPAQchanged its strategy, cutting back ondirect interventions and reducing itsworkforce, and providing financialsupport for group advisory structuresinstead.

The collective formula, developed firstby the farm management clubs,allows groups of farmers working on avoluntary basis to develop a servicethat they themselves manage andpartly fund. Using this model,advisory services were subsequentlydeveloped in the areas of production,agro-environmental techniques andfarm transfers.

Regional advisory networks were also created. The aim was to makeadvisory services more accessibleand to tailor them more to the needsof individual regions.15 Subsidizedadvisory services are used by onlyone-third of Quebec’s agriculturaloperations.12

A number of farm suppliers, financialinstitutions, feed companies andcooperatives have recruitedagronomists and technicians anddeveloped their own advisoryservices. These services are usedextensively and are also valued byproducers, although they areperceived in some quarters as beingless neutral.

The need to coordinate these serviceswhile maintaining their accessibility and increasing the number of users hasreceived a great deal of attention inrecent years. The federal government’sstrategic framework, by leaving moreroom for individual choice by farmmanagers, has also helped to changethe dynamics of the situation, especiallywith regard to the group formula.

Processing and distribution companieshave access to the services of firms of all types offered throughEmploi-Québec, the Ministère duDéveloppement économique, del’Innovation et de l’Exportation andother federal and provincial governmentdepartments and agencies.

Lastly, a number of private companiesjoin with professional, sector-basedassociations in order to obtain theexpertise they need through workshops,conferences, events, and so on.

The Commission proposes thefollowing subjects for reflection,among others:

• How can access to advisoryservices be developed?

• What can be done to guaranteethe quality of all these services?

• What can be done to ensure thatexisting resources work together?

• Does training for advisors andconsultants meet current needs?

28

Our living environment is fragile andwe must take care of it—this is themessage we have received fromcitizens of all backgrounds. Agriculturemust preserve the resources on whichit depends if it is to remain viable.Water and soil quality are essential to its ongoing survival.

The practices best suited to preservingthe environment require work andinvestment by government, farmers,processors and other stakeholders.Although efforts in Quebec comparefavourably to those elsewhere inCanada and around the world, researchtends to show that the results obtainedare not completely satisfactory, andthat we have not yet attained thebalance needed to ensure sustainabledevelopment.2

MAIN OBSERVATIONS

WATER