agent power-point-

TRANSCRIPT

Judge Learned Hand 1872-1961 U.S. Federal Courts of Appeals

In America there are two tax systems One for the Informed (lower taxes)

And one for the Under-Informed (higher taxes)

Qualified Plans (401k’s, IRA’s 403b’s) are for the Under-Informed

It’s time to become informed

Personal

You Have Two Basic Choices

CorporatePension

PlansxQualified Non-Qualified

Primary Risks of Qualified Plans

1. Market Losses

2. High Management Fees

3. Future Tax Rate Increases

4. Longevity Risk

There Is A Better Plan

How Many More Market Crashes In Your Lifetime?

Primary Risks of Qualified Plans

1. Market Losses

2. High Management Fees

3. Future Tax Rate Increases

4. Longevity Risk

There Is A Better Plan

The Real Cost of Owning a Mutual Fund:

Disclosed and/or hidden fees can easily eat up 30% or more

. com

Non taxable account0.90% Expense Ratio1.44% Transaction Costs0.83% Cash Drag1.00% Tax Cost4.17% Average Costs

Ty A. Bernicke - 04.04.11

How Much Do You Pay?

thus facilitating “apples-to apples "comparisons among their plan’s investment options; and a new level of fee and expense transparency

FACT SHEET

February 2012

Final Rule to Improve Transparency of Fees and Expenses to Workers in 401(k)-Type Retirement Plans

…thus facilitating “apples-to-apples” comparison of fees and expense transparency

Primary Risks of Qualified Plans

1. Market Losses

2. High Management Fees

3. Future Tax Rate Increases

4. Longevity Risk

There Is A Better Plan

Which Way Do You Think Taxes Will Go?

Did You Just Say Taxes Will Probably Go Up?

Your Current Tax Rate

Your Future Tax Rate

Tax Deferral Isn’t Good For You. But it’s GREAT for Uncle Sam

How will the Government make up for the

shortage?

Raise Taxes

Change Tax Brackets or

Eliminate Tax Deductions

Primary Risk of Qualified Plans

1. Market Losses

2. High Management Fees

3. Future Tax Rate Increases

4. Will I Outlive My Money

And the Safer Alternative

Primary Risk of Qualified Plans

AARP Quote… (61 percent) said they

fear depleting their assets more

than they fear dying.

And the Safer Alternative

There Is a Better Way!

According to the Federal Reserve

22% of this investment is owned by the wealthiest 1% of U.S.

55% of this asset is owned by the wealthiest 10%.

Source: http://online.wsj.com/news/articles/SB10001424052748703435104575421411449555240

What do advisors to the wealthiest 10% know

that your CPA doesn’t?Wall Street Journal October 2010

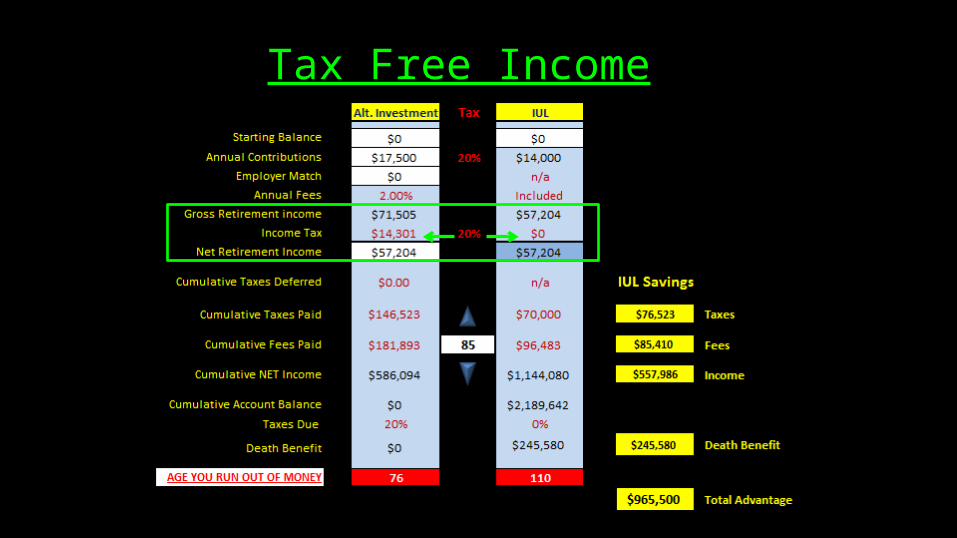

Tax Free Retirement Savings & A Tax Free Death Benefit

Rolled Into One Plan

Tax Free Income For Now or Retirement

& A Tax Free Death Benefit To Protect Your Family

Created by 3 Congressional Acts

TEFRA - DEFRA - TAMRA

Tax Free UnderInternal Revenue Codes

7702 & 72(e)

Superior Attributes of a Tax Free Plan

1. No Market Losses

2. 30% - 50% Lower Management Fees

3. Tax Free Income for LIFE

4. Income for Life

The Safer Alternative

Losses Are Controlled ByA Cap & A Floor

What is a Cap & Floor?

No Market Loss - The Cap & Floor

You Give Up Some of the Gain

22%10%To 15%

8.5% .8.5%

.

-25%

0%

Cap

Floor

You Give UpSome of the Gain

To Guarantee Zero Loss

S&P With Loss

IUL with Cap & Floor

Year

S&P Returns

Account Value

IUL

ReturnsAccount

Value

2000

-10.14% $89,860

0.00% $100,000

2001

-13.04% $78,142

0.00% $100,000

2002

-23.37% $59,880

0.00% $100,000

2003

26.38% $75,677

13.00% $113,000

2004

8.99% $82,480

8.99% $123,159

2005

3.00% $84,955

3.00% $126,853

2006

13.62% $96,526

13.00% $143,344

2007

3.50% $99,933

3.50% $148,404

2008

-38.49% $61,469

0.00% $148,404

2009

23.45% $75,883

13.00% $167697

2010

12.78% $85,581

12.78% $189,129

2011

0.00% $85,581

0.00% $189129

2012

13.29% $96,955

13% $213,715

2013

29.60% $125,653

13.00% $241,498

16 Yrs.

3.54%Taxable $125,653

7.92%

Tax Free $241,498

Guarantee: Zero Market Loss$241,498 7.92% Tax Free

$125,653 3.54% Taxable

Cap

Floor

$100k Initial InvestmentApples to Apples Comparison

Actual S&P Performance

2 Year “Average Return” According to Wall Street

Year

#1 $100,000 + 100% = $200,000

#2 $200,000 - 50% = $100,000

100% +

-50%

+50% divided by 2 years = "Average Gain of 25%” ???

Benefits of a Tax Free Plan

1. No Market Losses

2. 30% - 50% Lower Management Fees

3. Tax Free Income

4. Life Time Income

5. Flexible Contributions

The Safer Alternative

Far Less Fees

53% Less

Benefits of a Tax Free Plan

1. No Market Losses

2. 30% - 50% Lower Management Fees

3. Tax Free Income

4. Life Time Income

5. Flexible Contributions

The Safer Alternative

Tax Free Income

Benefits of a Tax Free Plan

1. No Market Losses

2. 30% - 50% Lower Management Fees

3. Tax Free Income

4. Life Time Income

5. Flexible Contributions

The Safer Alternative

Income For Life

Benefits of a Tax Free Plan

1. No Market Losses

2. 30% - 50% Lower Management Fees

3. Tax Free Income

4. Life Time Income

5. Flexible Contributions

The Safer Alternative

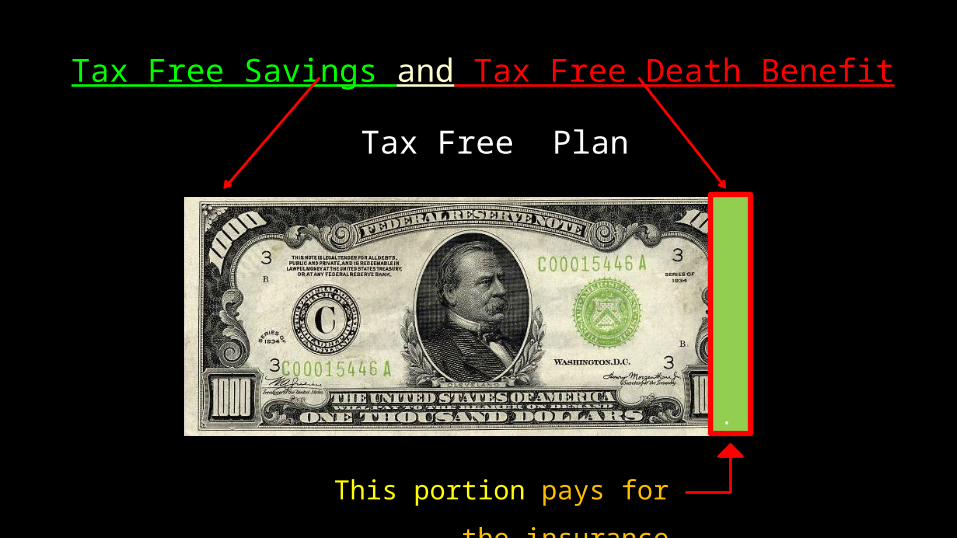

This portion pays for the insurance

Tax Free Savings and Tax Free Death Benefit

.

Tax Free Plan

Borrow$$$

Cash Value / Savings Continues to Grow

How Is That Possible?

Borrow$$$ Borrow

$$$Age 65 100

Even As You Take Home Retirement Income

The Cash Value / Savings

COLLATERALAgainst Any Loans You Take

The Cash Value continues to grow even when you borrow money

$200,000 Value

House has No

mortgage

Borrow$100k from home

Plus Interest

Why a Loan Does Not Lower The Cash Value

$200,000

$200,000

X 10% $220,000

Cash ValueSavings

SubtractRetirement Income

Loan & Interest

Balance IsA Tax Free Death Benefit to Heirs

_=

The Income You BorrowIs Not Repaid Until After You Pass On.

Guaranteed 100% at risk of loss

Guaranteed you’ll pay

Guaranteed not locked in

Guaranteed taxable

Not fully disclosed

Guaranteed 0% risk of market loss

Guaranteed Tax Free

Guaranteed locked-in

Guaranteed tax free

Fully disclosed

Risk

Taxes

Gains

Death Benefit

Fees

Taxable 401k/Qualified Tax Free Plan

Compare the Guarantees