agenda - teska associates, inc. | building community ... · agenda • introductions ... •...

TRANSCRIPT

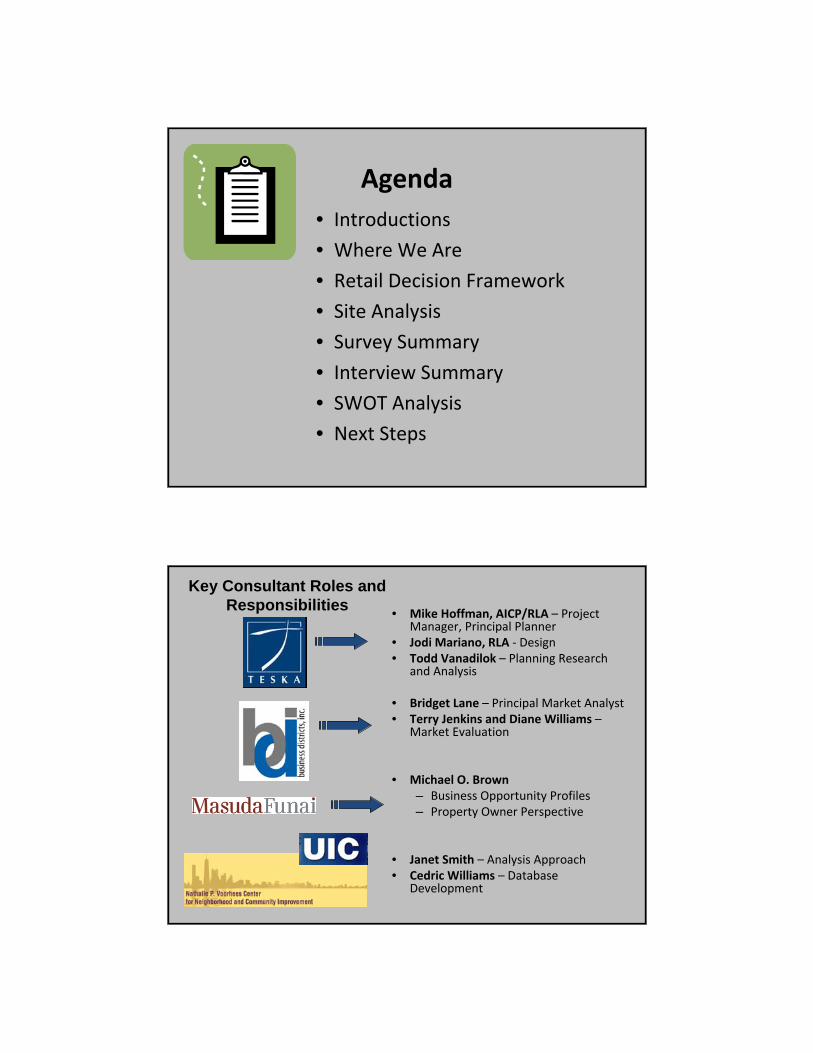

Agenda• Introductions

• Where We Are

• Retail Decision Framework

• Site Analysis

• Survey Summary

• Interview Summary

• SWOT Analysis

• Next Steps

Key Consultant Roles and Responsibilities • Mike Hoffman, AICP/RLA – Project

Manager, Principal Planner• Jodi Mariano, RLA ‐ Design• Todd Vanadilok – Planning Research

and Analysis

• Bridget Lane – Principal Market Analyst• Terry Jenkins and Diane Williams –

Market Evaluation

• Michael O. Brown– Business Opportunity Profiles– Property Owner Perspective

• Janet Smith – Analysis Approach• Cedric Williams – Database

Development

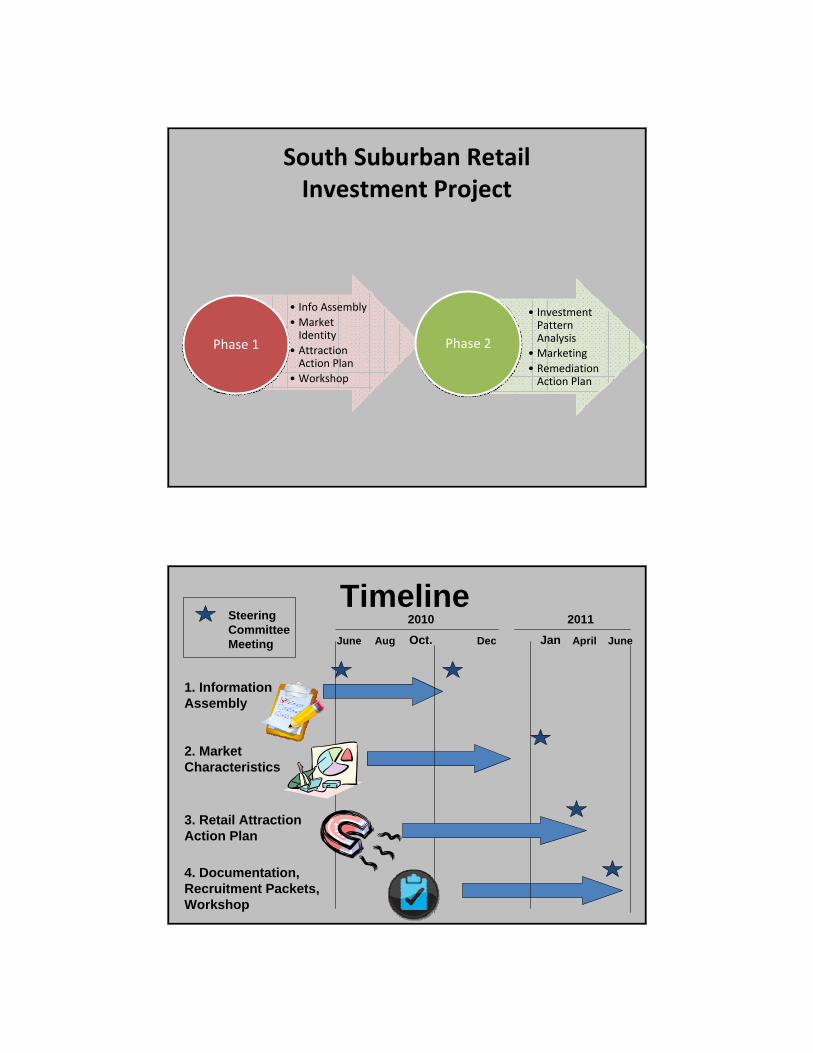

South Suburban RetailInvestment Project

• Info Assembly• Market Identity

• Attraction Action Plan

• Workshop

Phase 1Phase 1

• Investment Pattern Analysis

• Marketing• Remediation Action Plan

Phase 2Phase 2

June Aug Oct. Dec Jan April June

1. Information Assembly

2. Market Characteristics

3. Retail Attraction Action Plan

4. Documentation, Recruitment Packets, Workshop

Timeline2010 2011Steering

Committee Meeting

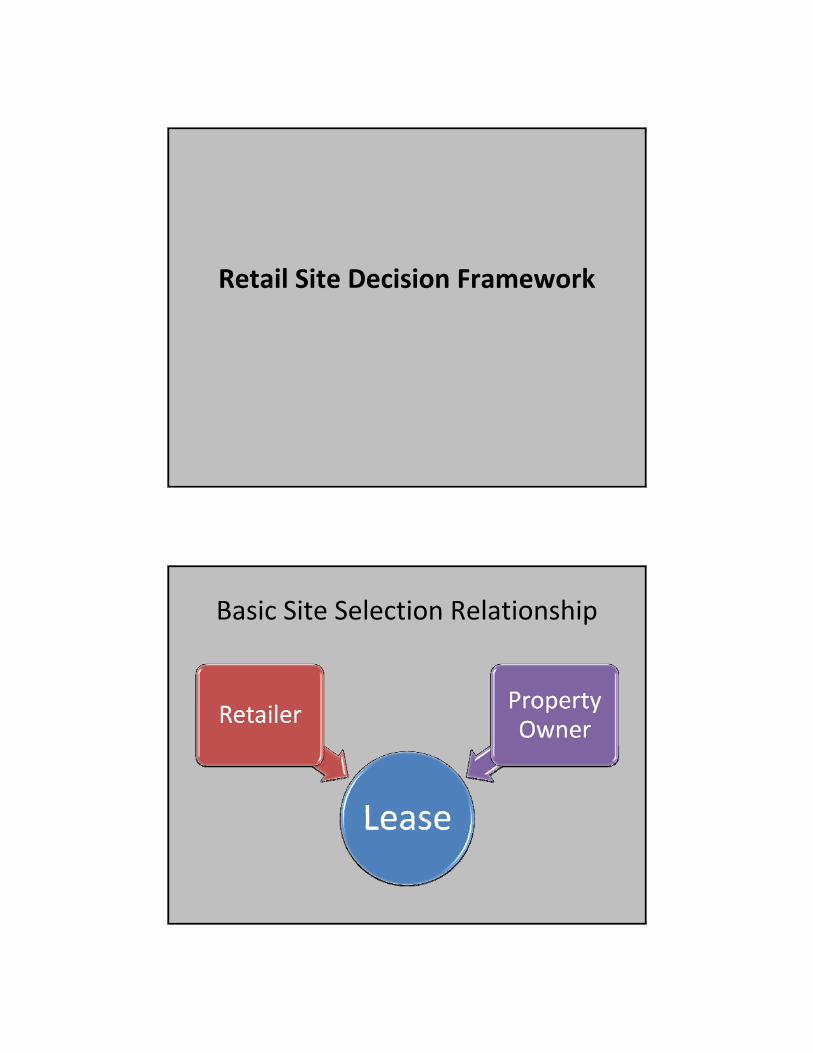

Retail Site Decision Framework

Basic Site Selection Relationship

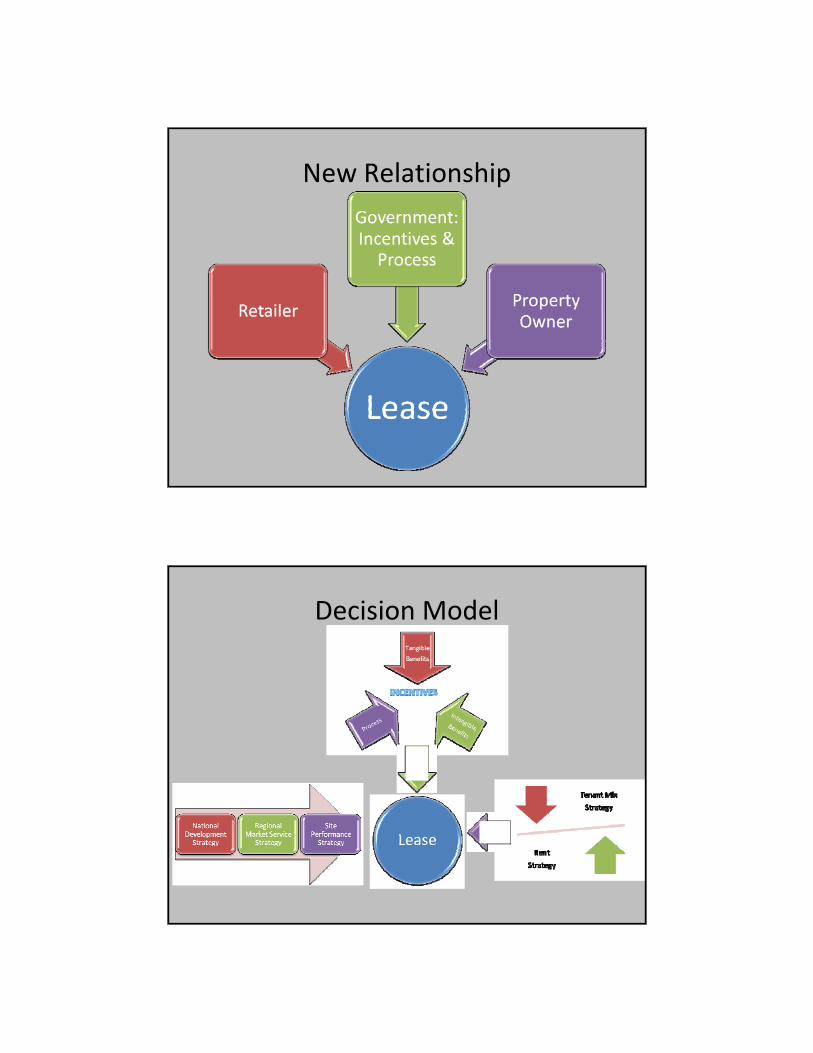

New Relationship

Decision Model

Motivation

• Retailer– Sales – Expenses = Profit– Intangibles: image + gut feel

• Property Owner– Rents – Expenses‐ debt service = Profit– Intangible: image

• Government– Tangible Benefits = Taxes & Jobs– Intangible Benefits = satisfied residents + image– Process completion

Interviews• 12 of 24 property owners completed

• Summary– Difficult economy

– Taxes, taxes, taxes

– Vacancies are causing “hyper”competition

– Retailer interest exists

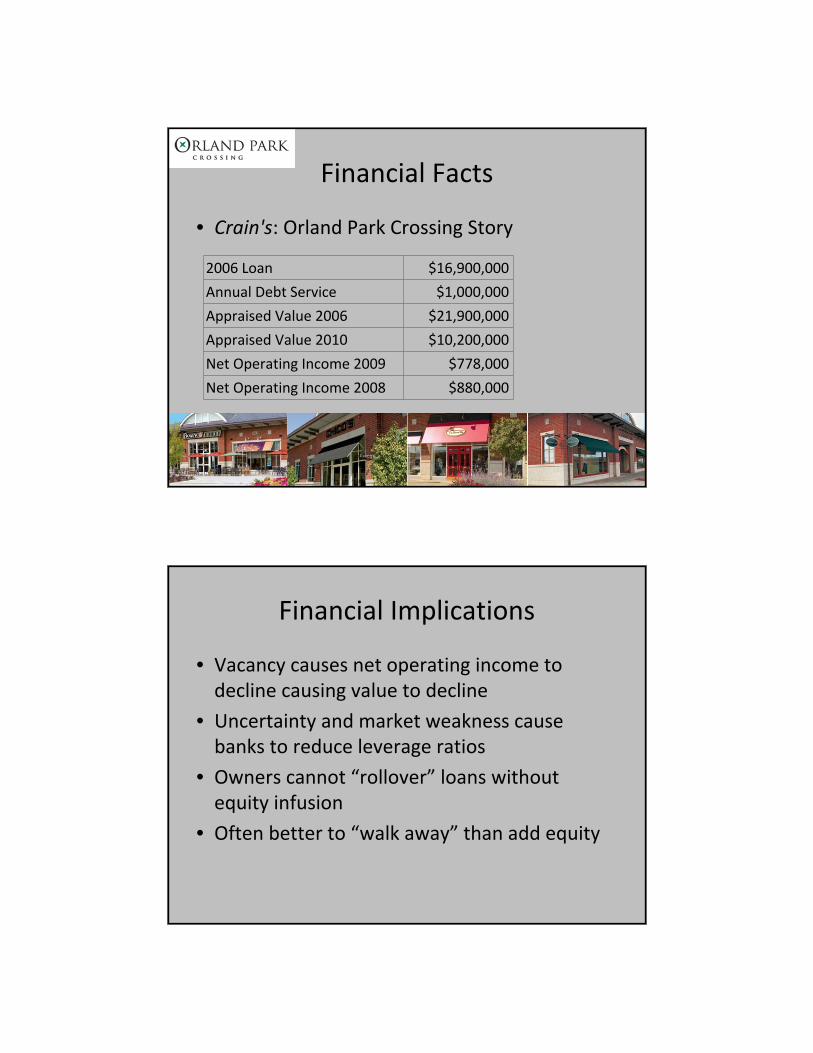

Financial Facts

• Crain's: Orland Park Crossing Story

2006 Loan $16,900,000

Annual Debt Service $1,000,000

Appraised Value 2006 $21,900,000

Appraised Value 2010 $10,200,000

Net Operating Income 2009 $778,000

Net Operating Income 2008 $880,000

Financial Implications

• Vacancy causes net operating income to decline causing value to decline

• Uncertainty and market weakness cause banks to reduce leverage ratios

• Owners cannot “rollover” loans without equity infusion

• Often better to “walk away” than add equity

Property Tax Facts – McDonald’s Tax Comparison

Address Community2009 Taxes

Land SQFT

Taxes/ Land SQFT

2707 Sauk Trail Sauk Village $36,276 38,263 $0.95

1032 N Northwest Hwy Park Ridge $60,913 48,542 $1.25

100 Sauk Trail Rd South Chicago Heights $45,609 30,000 $1.52

9110 W. 159th St Orland Park $67,647 43,244 $1.56

4830 Dempster Skokie $68,921 35,643 $1.93

100 West Rand Road Mount Prospect $65,702 33,850 $1.94

5441 West 159th Street Oak Forest $75,956 38,401 $1.98

2400 W Lincoln Hwy Olympia Fields $78,872 35,915 $2.20

3132 West 183rd Street Homewood $101,669 44,640 $2.28

4855 W Sauk Trail Richton Park $87,744 35,972 $2.44

15920 S. Harlem Tinley Park $119,745 44,113 $2.71

4010 W. 211th St Matteson $132,677 46,625 $2.85

Source: Cookcountytreasurer.com ; Cookcountyassessor.com

Property Tax Impacts

• Assumptions:– Mc Donald's cost the same to build & operate anywhere – Owners seek the same return everywhere

• Matteson Property Tax Example– Average annual property taxes per land square foot of 20 unit sample: $1.99

– Matteson annual per square foot property taxes: $2.85– Annual property tax due to variance from average: $38,835

• Profit Equalization Strategy– 109 more transactions per day that contribute $1– Pay $500,000 less for property

Property Tax Impacts

• What if the landlord absorbs the tax differential?– Gross rent capped at $20– Taxes “float” around $10– CAM and insurance are $5– Triple net is $5– At 8% cap rate the value is $62.50– It cost about $218 to build new brick, concrete block back‐up, steel frame store

– Significant remodeling might cost $50 – Interest if 75% financed at 8% is $3.75

• This model undermines reinvestment

Vacancy

Subarea Gross SFVacancy Rate Vacant SF

N.W. Suburbs 15,874,756 13.6% 2,158,967

North Suburbs 9,908,367 8.9% 881,845

West Suburbs 7,945,280 8.9% 707,130

City North 8,131,681 6.5% 528,559

City South 6,157,829 10.8% 665,046

S.W. Suburbs 9,490,094 9.4% 892,069

South Suburbs 7,011,322 21.5% 1,507,434

TOTAL 128,578,383 11.9% 15,300,828

Source: CBRE, Chicago Retail Market View 3rd Quarter 2010

Preliminary data estimates study area vacancy rate at 20.2%.

Vacancy

15‐Minute Drive Time Population

Non‐Mall Shopping Center

SF

Non‐Mall Shopping Center

SF/Capita

Total Shopping Center

SF/capita

Woodfield 337,677 3,252,454 9.6 16.2

Oakbrook 424,613 5,805,794 13.7 18.6

Chicago Ridge 317,009 5,164,923 16.3 18.9

Orland Park 224,633 2,732,090 12.2 17.6

River Oaks 295,850 2,039,569 6.9 10.9

Spring Hill 216,642 1,937,000 8.9 15.3

Stratford Square 236,079 948,543 4.0 9.6

Randhurst 324,612 2,900,405 8.9 13.0

Lincoln Mall 271,200 3,047,248 11.2 14.9Source: 2010 Directory of Major Malls, Inc. (Malls over 200,000 square feet)

Site Analysis

• Goals– Modern configuration

– Excellent access

– Attractive appearance

– Strong co‐tenancies

– “A” quality stores

• Best

• Standards

Example 1

Example 2 - Naperville

Example 2

Example 3 - Frankfort

Database Design

Goal:Produce data that is of use to the communities ANDthat can assess likelihood of retail redlining

Approach:1. Develop baseline conditions database containing two

necessary types of data: primary (survey, focus groups, interviews) and secondary (e.g., Experian, sales data, IDOT traffic counts, etc)

2. Triangulate data to get rich analysis of each community3. Eliminate potential explanations for investment patterns

that are NOT evidence of redlining

Hypotheses to test for Redlining

• H1: Retail patterns in the study area are attributed to supply and demand mismatch (leakages, gaps, surplus).

• H2: Retail patterns in the study area are attributed to investment barriers/challenges (local, regional, national).

For both, we will:• stratify the analysis across the retail categories targeted in the consumer survey.

• assume that similar patterns will be found in comparison communities.

If not, then we can assume there are other factors contributing to the patterns found in the study area.

Analyzing Local Retail Patterns

Property Owners Retailers

Consumers

BASIC patterns

How does your community look in general? How does it compare to…?

e.g., consumer leakage: sit-down family restaurants

Property Owners Retailers

ConsumersSecondary dataSecondary data

SPECIFIC patterns

What do consumers want? Why aren’t retailers here?

e.g., consumer leakage: 23% of families surveyed drive 5 miles to Panera Bread; there are 3 locations where PB could locate in our community; all three have lease restrictions that PB will not sign.

Primary dataPrimary data

Assessing Patterns

Use similar approach as with housing redlining:

Eliminate possible “non-redlining” behavior as explanation

Supply/demand gaps

Investment barriers/challenges

Likely redlining behavior ??

Comm 1 Comm 2

Profile of respondentsMatteson Olympia

FieldsParkForest

Richton Park

Combined

Households 5,479 1,772 8,665 4,728 20,644

15% response goal 822 266 1,300 709 3,097

Final 11‐1‐10 281 195 208 85 769

% of households 5.1% 11.0% 2.4% 1.8% 3.7%

• 165 responses from outside the four target communities.

• Total responses = 939 (includes 5 from unspecified location).

• Heard from long-term residents (61%), and both young families (26%) and older empty nesters (27%).

• Respondents are higher income (54% above $75,000) and own their homes (96%).

• Race/ethnicity of respondents suggests slight over-representation of African Americans and under-representation of Hispanics.

Key Supply and Demand “Big Picture”Findings

• Most travel longer distances to shop (74% drive more than 5 minutes).

• Most buy groceries at Dominick’s (Matteson) and Jewel (Olympia Corners)

• Comparing features (cleanliness, parking, safety, signage, customer service) of Lincoln Mall to Orland Park: OP is better than LM across all conditions asked about. Comments provide additional insights.

• Still, people shop in Lincoln Mall, and more often than at Orland Park, particularly at JC Penney’s and Carson Pirie Scott.

• Unmet demand: People want things not in their community now, particularly higher end & family dining options, shoes, health food stores and home furnishings.

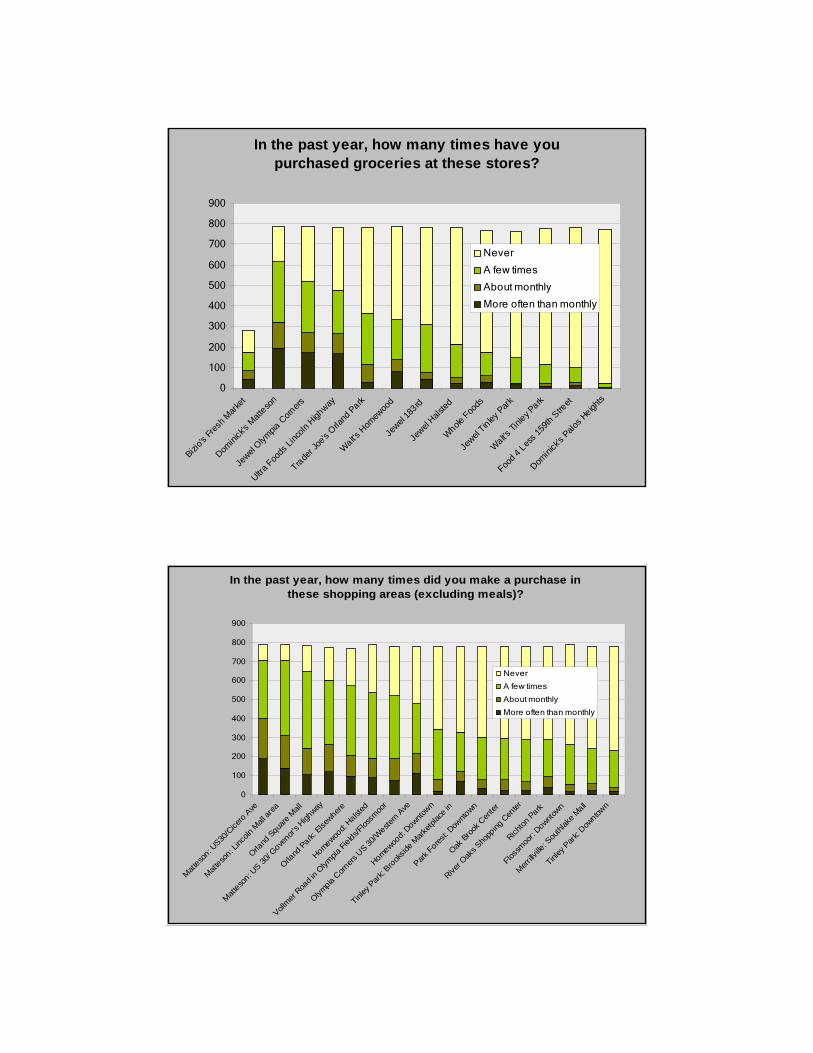

In the past year, how many times have you purchased groceries at these stores?

0

100

200

300

400

500

600

700

800

900

Bizio's

Fres

h Mark

et

Domini

ck's

Matteso

n

Jewel

Olympia

Corn

ers

Ultra Foo

ds Li

ncoln

High

way

Trader J

oe's

Orland

Park

Walt's H

omew

ood

Jewel

183rd

Jewel

Halsted

Whole Foo

ds

Jewel

Tinley Park

Walt's Ti

nley P

ark

Food 4

Less 1

59th

Street

Domini

ck's

Palos H

eights

Never

A few times

About monthly

More often than monthly

In the past year, how many times did you make a purchase in these shopping areas (excluding meals)?

0

100

200

300

400

500

600

700

800

900

Matteso

n: US30

/Cice

ro A

ve

Matteso

n: Linc

oln M

all ar

ea

Orland

Squa

re M

all

Matteso

n: US 30

/ Gove

nor's H

ighway

Orland

Park: Else

where

Homewood:

Halsted

Vollmer

Road i

n Olym

pia Fi

elds/Flos

smoo

r

Olympia C

orners

US 30

/Weste

rn Ave

Homewood:

Downtown

Tinley

Park:

Brook

side M

arketp

lace in

Park Fores

t: Dow

ntown

Oak B

rook

Cen

ter

River O

aks S

hopp

ing C

enter

Richton

Park

Flossm

oor:

Downtown

Merrillv

ille: S

outhl

ake M

all

Tinley

Par

k: Dow

ntown

Never

A few times

About monthly

More often than monthly

In the past year, how many times have you purchased merchandise at these department stores?

0

100

200

300

400

500

600

700

800

900

Carson

Pirie Sco

tt Linco

ln Ma

JC Penney's L

incoln M

a

Macy's

Orla

nd Pa rk

Carson Pirie

Scott O

rland

Squa

Kohl's Tinley P

a rk

Kohl's

Homew

ood

JC Penney

's Orla

nd Squar

Nordstro

m

Macy's

River Oaks

Koh l's in Frankfo

rtSaks

Kohl's

in Crete

Von M

aur

JC Penney

's Moke

na

Never

A few times

About monthly

More often than monthly

Group Exercise

• Strengths and weaknesses

Next Steps

• Market Characteristics Phase– SWOT Analysis Summary

– Model Developments

– Business Opportunities Profiles for Each Center

– Market Share (“leakage”)

• Next Steering Committee – January 6th?