advanced financial accounting: chapter 3 group reporting ii tan, lim & lee chapter 3© 20151

TRANSCRIPT

Advanced Financial Accounting: Chapter 3

Group Reporting II

Tan, Lim & Lee Chapter 3 © 2015 1

Learning Objectives

1. Understand the difference between investor’s separate financial statements and the consolidated statements;

2. Understand the differences and similarities in various mode of business combinations;

3. Appreciate the acquisition method and its implications;

4. Know how to determine the amount of consideration transferred;

5. Understand the identification of the acquirer;

6. Know how to recognize and measure identifiable net assets, liabilities and goodwill in accordance to IFRS 3; and

7. Understand the nature of goodwill.

Tan, Lim & Lee Chapter 3 2© 2015

Content

Tan, Lim & Lee Chapter 3 © 2015 3

1. Introduction

2. Overview of the consolidation process

3. Business combinations

4. Determining the amount of consideration transferred

5. Recognition and measurement of identifiable assets, liabilities

and goodwill

6. Conclusion

1. Introduction

Introduction

Tan, Lim & Lee Chapter 3 © 2015 4

Separate financial statements

(Legal entity)

Consolidated financial statements

(Economic entity)

Governing rules and regulations

In accordance with corporate regulations In accordance with IFRS 10

Possible exemptions for presentation No exemption

IFRS 10 allowed for exemptions by a parent if it’s : A wholly owned or partially

owned subsidiary; Debt or equity instruments not

traded in public; Did not file financial

statements for purpose of issuing instruments to public; and

Ultimate parent produces consolidated financial statements.

Separate Vs Consolidated Financial Statement

Tan, Lim & Lee Chapter 3 © 2015 5

Separate financial statements

(Legal entity)

Consolidated financial statements

(Economic entity)

Income recognition Dividends Share of profits

Asset recognition

Investment in a subsidiary carried at:• Cost (IAS 27) or • As a financial instrument (IFRS 9)

Investment in a subsidiary:• Investment is eliminated and subsidiary’s net assets are added to the parent (IFRS 10)

Investment in an associate carried at:• Cost (IAS 28) or• As a financial instrument (IFRS 9)

Investment in an associate:• Equity method (IAS 28)

Content

Tan, Lim & Lee Chapter 3 © 2015 6

1. Introduction

2. Overview of the consolidation process

3. Business combinations

4. Determining the amount of consideration transferred

5. Recognition and measurement of identifiable assets, liabilities

and goodwill

6. Conclusion

2. Overview of the consolidation process

Consolidation Process

• Consolidation is the process of preparing and presenting the financial statements of a group as an economic entity

• No ledgers for group entity

• Consolidation worksheets are prepared to:– Combine parent’s and subsidiaries financial statements

– Adjust or eliminate effects of intra-group transactions and balances

– Allocate profit to non-controlling interests

Tan, Lim & Lee Chapter 3 © 2015 7

Parent’s Financial

Statements+

Subsidiaries' Financial

Statements+/- Consolidation adjustments

and eliminations =Consolidated

financial statements

Legal entities Economic entity

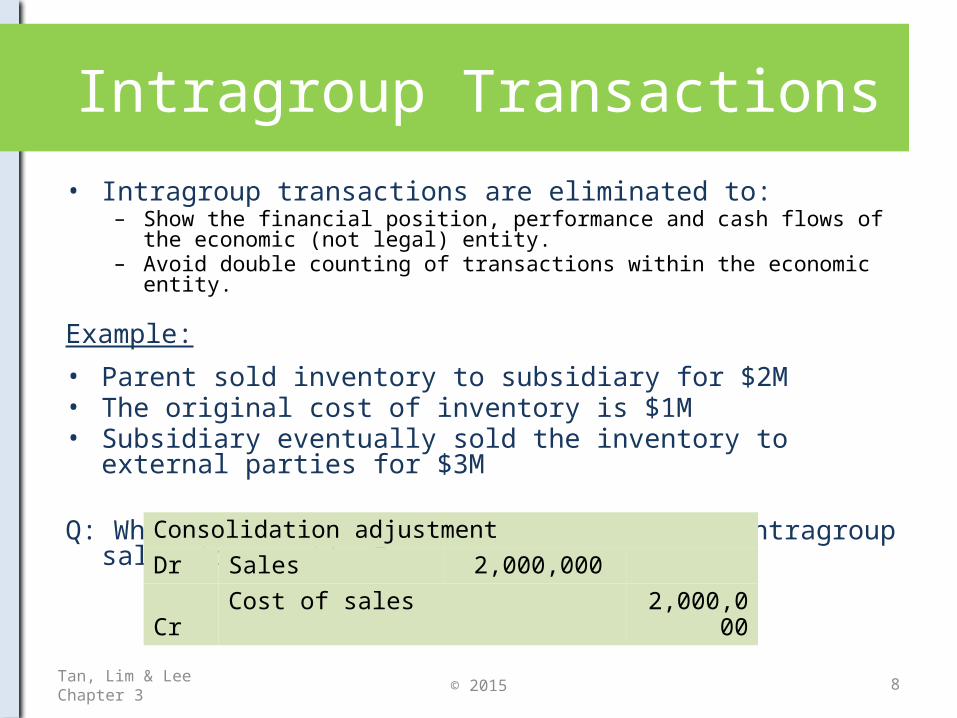

Intragroup Transactions

• Intragroup transactions are eliminated to:– Show the financial position, performance and cash flows of the economic (not

legal) entity.– Avoid double counting of transactions within the economic entity.

Example:

• Parent sold inventory to subsidiary for $2M• The original cost of inventory is $1M• Subsidiary eventually sold the inventory to external parties for $3M

Q: What is the journal entry to eliminate intragroup sales transaction?

Tan, Lim & Lee Chapter 3 © 2015 8

Consolidation adjustment

Dr Sales 2,000,000 Cr Cost of sales 2,000,000

Intragroup Transactions

Tan, Lim & Lee Chapter 3 © 2015 9

Extract of consolidated worksheet

Parent's Income

Statement

Subsidiary's Income

Statement

Consolidation elimination entries

and adjustment

Consolidated income

statementWithout

elimination Dr Cr

Sales $2,000,000 $3,000,000 2,000,000 $3,000,000 $5,000,000

Cost of sales (1,000,000) (2,000,000) 2,000,000 (1,000,000)

($3,000,000)

Gross profit $1,000,000 $1,000,000 $2,000,000 $2,000,000

Note: Without elimination the consolidated sales and cost of sales figures will be overstated by $2 M.

* The consolidation process will be discussed in greater detail in Chap 4.

Content

Tan, Lim & Lee Chapter 3 © 2015 10

1. Introduction

2. Overview of the consolidation process

3. The acquisition method

4. Determining the amount of consideration transferred

5. Recognition and measurement of identifiable assets, liabilities

and goodwill

6. Conclusion

3. Business Combinations

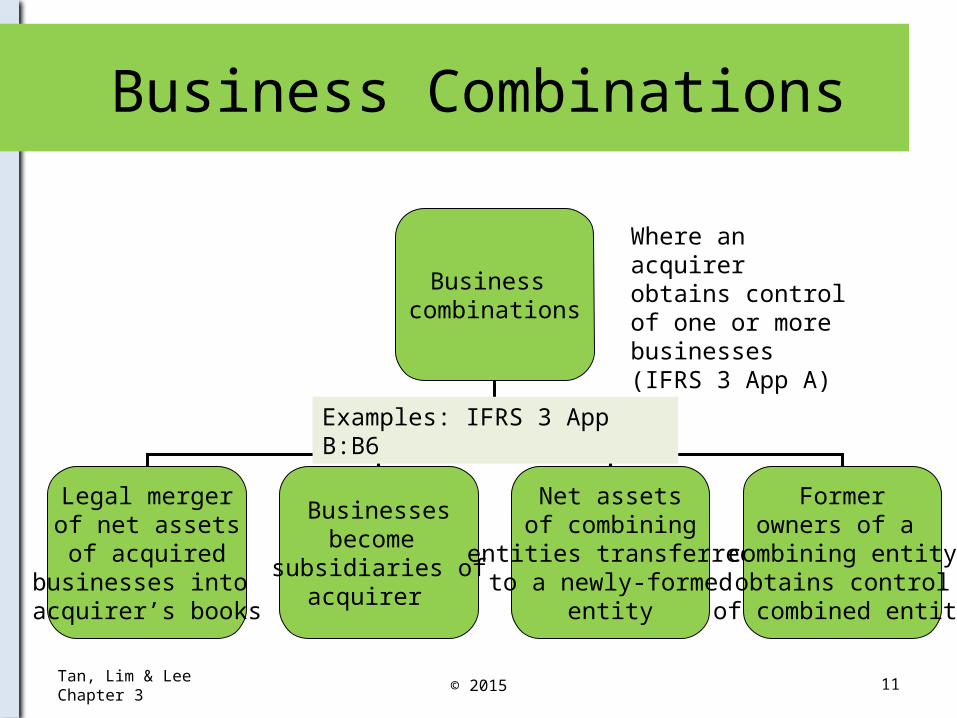

Business Combinations

Tan, Lim & Lee Chapter 3 © 2015 11

Business combinations

Legal mergerof net assetsof acquired

businesses into acquirer’s books

Businessesbecome

subsidiaries ofacquirer

Net assetsof combining

entities transferredto a newly-formed

entity

Formerowners of a

combining entityobtains control

of combined entity

Where an acquirer obtains control of one or more businesses (IFRS 3 App A)

Examples: IFRS 3 App B:B6

• Business combinations may take different forms ; however two characteristics are present:

Tan, Lim & Lee Chapter 3 © 2015 12

Business Combinations

• 3 main attributes of control• Power over acquiree• Exposure or rights to variable returns of acquiree• Ability to use power to affect acquiree’s returns.

Acquirer has control of

business acquired

• 2 vital characteristics of a business (IFRS 3)• Integrated set of activities and assets• Capable of being conducted and managed to

provide returns (i.e. dividends) to investors and other stakeholders.

Target of acquisition is a

business

Business combinations involving entities under common control is outside of scope of IFRS 3

The Acquisition Method

• IFRS 3 requires all business combinations to be accounted for using the acquisition method from the perspective of an acquirer.

• An acquirer can obtain control in an acquiree through:1. Acquisition of assets and assumption of liabilities of acquiree

Include assets and liabilities not previously recognised by acquiree: contingent liabilities, brand name, in-process R&D etc.

2. Acquisition of controlling interest in the equity of acquiree Deemed to be effective acquisition of assets and assumption of

liabilities of acquiree Control over an acquiree in substance means that acquirer has control

over net assets of acquiree Effects: (2) accounted for as if they are effects of (1)

3. Combination of (1) and (2)* Effects: Accounted for as if they are effects of (1)

Tan, Lim & Lee Chapter 3 © 2015 13

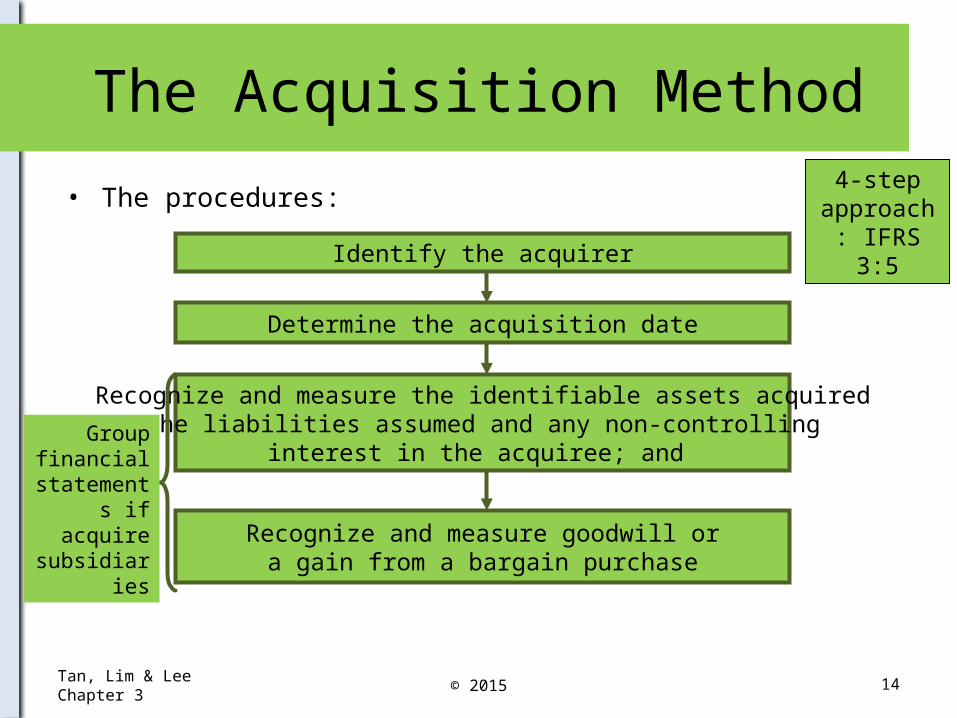

The Acquisition Method

• The procedures:

Tan, Lim & Lee Chapter 3 © 2015 14

Identify the acquirer

Determine the acquisition date

Recognize and measure the identifiable assets acquiredthe liabilities assumed and any non-controlling

interest in the acquiree; and

Recognize and measure goodwill ora gain from a bargain purchase

Group financial

statements if acquire

subsidiaries

4-step approach: IFRS 3:5

Identify the Acquirer

• IFRS 3 requires the identification of the acquirer in all circumstances

– Acquirer is the entity that obtains control of another combining entities

– Concept of control is based on IFRS 10 but the standard may not

always conclusively determine the identity of the acquirer.

– IFRS 3 Appendix B provides additional criteria to identify controlling

acquirer.

Tan, Lim & Lee Chapter 3 © 2015 15

Identify the Acquirer

Tan, Lim & Lee Chapter 3 © 2015 16

Additional control criteria under IFRS 3 Appendix B

Acquirer is the entity that:

• Transfers cash or other assets or incurs liabilities to acquire another entity

Issues shares as consideration to acquire shares of another entity

Pays a premium over the fair value of the equity interest

Acquirer is the entity:

• Whose owners hold the largest relative voting rights in a combined entity

• Whose owners hold the largest minority voting interest in the combined entity (if no other entity has significant voting interest)

• Which is larger in size

Acquirer is the entity:

• Whose owners have the ability to elect, appoint or remove a majority of directors

• Whose management is dominant in the combined entity

•Who initiates the business combination

Based on consideration transferred

Based on entity size Based on dominance

Identify the Acquirer – Reverse Acquisition

• Reverse acquisition – Legal parent is the acquiree and legal subsidiary is the acquirer– Often initiated by the legal subsidiary– Motive for entering into such an arrangement often to seek a backdoor

listing

• Exchange of shares in a reverse acquisition

Tan, Lim & Lee Chapter 3 © 2015 17

Owners of Company B (Legal subsidiary)

Company A (Legal parent)

Company B (Legal subsidiary)

1. Company A (Legal parent) takes over shares of Company B from owners

2. Company A issues own shares to owners of Company B as purchase consideration

3. Company B has the power and ability to affect the returns of the legal parent after the share exchange

Identify the Acquirer – Reverse Acquisition

Example

On 1 July 20x5, P (private), arranged to have all its shares acquired by L (public listed). The arrangement required L to issue 20 million shares to P’s shareholders in exchange for the existing 6 million shares of P. Existing shareholders of L owned 5 million of L.

After the issue of 20 million L shares, P’s shareholders now owned 80% (20 million shares out of a total of 25 million shares) of the issued shares of the combined entity. L’s shareholders owned 20% of the shares in the combined entity after the share issue. P’s shareholder act in concert to exercise control over the combined entity.

Tan, Lim & Lee Chapter 3 © 2015 18

L’s shareholders (5 million shares)

P’s shareholders (20 million shares)

L

P

20% 80%

100%

Content

Tan, Lim & Lee Chapter 3 © 2015 19

1. Introduction

2. Overview of the consolidation process

3. Business combinations

4. Determining the amount of consideration transferred

5. Recognition and measurement of identifiable assets, liabilities

and goodwill

6. Conclusion

4. Determining the amount of consideration transferred

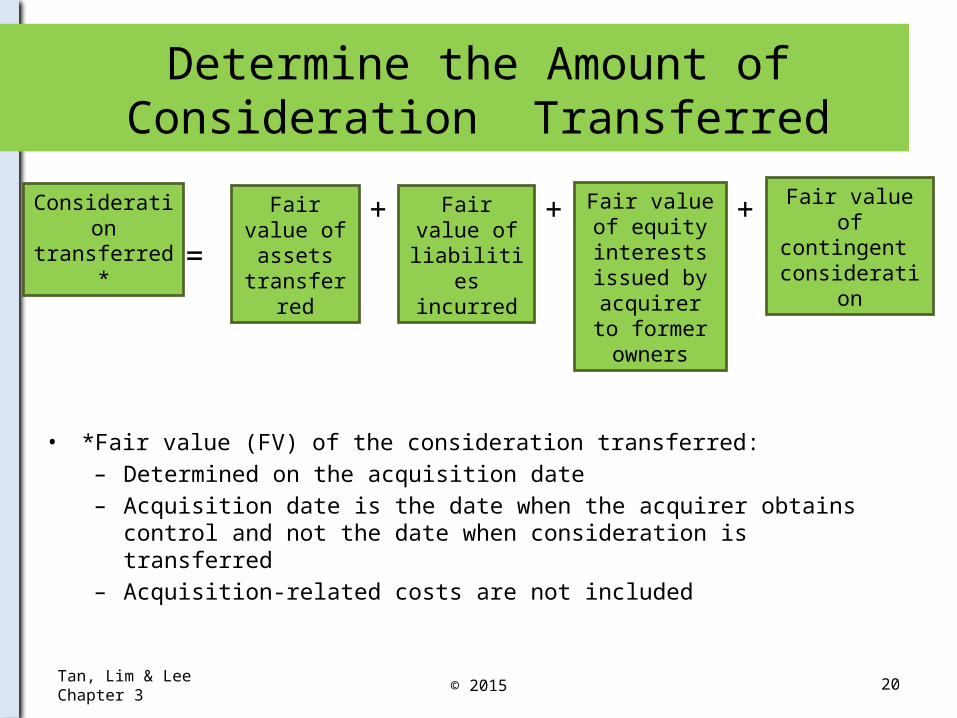

Determine the Amount of Consideration Transferred

• *Fair value (FV) of the consideration transferred:– Determined on the acquisition date – Acquisition date is the date when the acquirer obtains control and not the

date when consideration is transferred– Acquisition-related costs are not included

Tan, Lim & Lee Chapter 3 © 2015 20

Fair value of assets

transferred

+ Fair value of liabilities

incurred

+ Fair value of equity

interests issued by acquirer to

former owners

Consideration transferred* = + Fair value of

contingent consideration

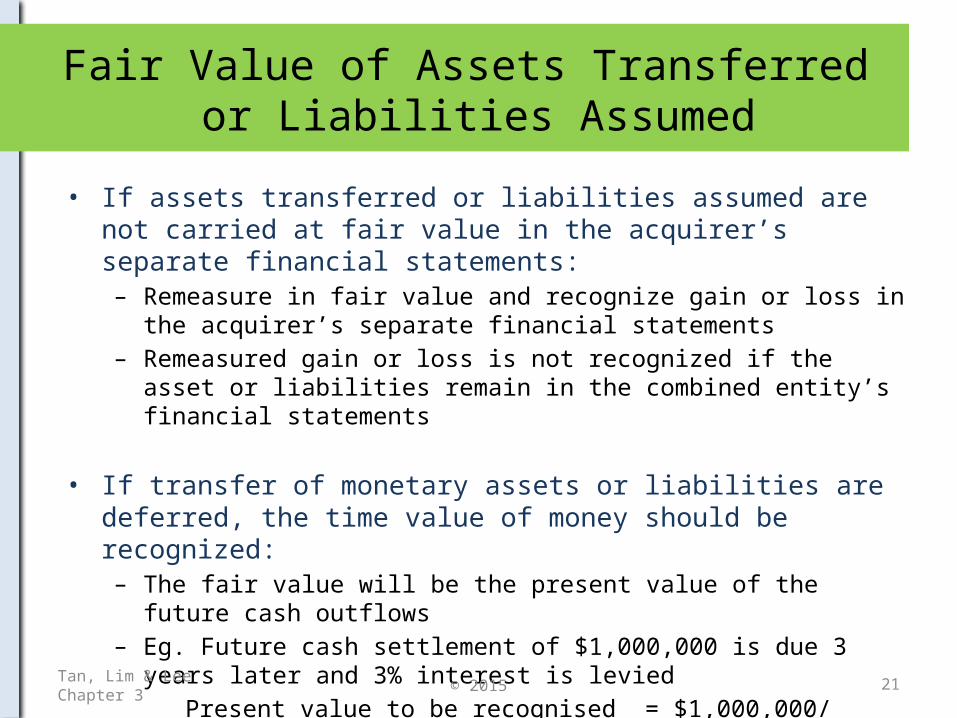

Fair Value of Assets Transferred or Liabilities Assumed

• If assets transferred or liabilities assumed are not carried at fair value in the acquirer’s separate financial statements:– Remeasure in fair value and recognize gain or loss in the acquirer’s

separate financial statements– Remeasured gain or loss is not recognized if the asset or liabilities

remain in the combined entity’s financial statements

• If transfer of monetary assets or liabilities are deferred, the time value of money should be recognized: – The fair value will be the present value of the future cash outflows– Eg. Future cash settlement of $1,000,000 is due 3 years later and 3%

interest is levied

Present value to be recognised = $1,000,000/ (1+0.03)^3

= $915,142

Tan, Lim & Lee Chapter 3 © 2015 21

Fair value of Equity Interests Issued by the Acquirer

• Fair value of equity interests issued is measured:

– (1) By market price (e.g. published quoted prices of shares)

– (2) With reference to either the acquisition date fair value of the acquirer OR

acquiree, whichever is more reliable. (For example, if market price is not

available or not reliable for the acquiree, use the fair value of the acquirer)

• Illustration of (2)

Tan, Lim & Lee Chapter 3 © 2015 22

Acquirer Owners of Acquiree

Acquiree

Issues X number of shares

Conveys A number of shares to acquirer

Gains control over acquiree

Total number of shares after issue: Y

FV of acquirer’s equity: $Z

FV of equity issued is either:• X/Y multiplied by $Z; or• A/B multiplied by $C

Illustration 1:Fair Value of Equity Issued

P Ltd acquires 100% of S Co through an issue of 5,000,000 shares

to the owners of S Co.

Tan, Lim & Lee Chapter 3 © 2015 23

P Ltd S Co

Number of existing shares 10,000,000 2,000,000

Number of new shares issued 5,000,000 -

Market price per share $2.00 -

Fair value of equity 30,000,000 9,000,000

Illustration 1:Fair Value of Equity Issued

Tan, Lim & Lee Chapter 3 © 2015 24

Situation 1: P Ltd’s market price is a reliable indicator

Consideration transferred = 5,000,000 shares x $ 2.00 = $10,000,000

Situation 2: Fair value of S Co is a better estimate

Consideration transferred = $9,000,000

Explanation: Since P Ltd is acquiring 100% of S Co, the fair value of the equity (FV of S Co. as a whole including the implicit goodwill) acquired by P is $9 million.

Fair Value of Contingent Consideration

• Contingent consideration

– Obligation (right) of the acquirer to transfer (receive) additional assets or

equity interests to (from) acquiree’s former owner if specific event occurs

• Eg. Event A: acquirer gets a refund of part of the consideration transferred if the

acquiree does not achieve the target profit

• Fair value of contingent consideration or refund will change as new information

arises

– Fair value of the contingent consideration has to be estimated (For event A)

is deducted from consideration transferred

– Fair value of contingent consideration is adjusted retrospectively as a

correction of error if events after acquisition reveal information that was

missed or misapplied during the acquisition date

Tan, Lim & Lee Chapter 3 © 2015 25

Acquisition-Related Costs

• All acquisition-related costs are expensed off• Costs of issuing debt are recognized in accordance with IAS 39

– As yield adjustment to the cost of borrowing and are amortized over the tenure of the loan

– Journal entry for the payment of debt issuance cost

• Costs of issuing equity are recognized in accordance with IAS 32– A reduction against equity– Journal entry to record the payment of cost of issuing equity

Tan, Lim & Lee Chapter 3 © 2015 26

Dr Unamortized debt issuance costsCr Cash

Dr EquityCr Cash

Content

Tan, Lim & Lee Chapter 3 © 2015 27

1. Introduction

2. Overview of the consolidation process

3. Business combinations

4. Determining the amount of consideration transferred

5. Recognition and measurement of identifiable assets, liabilities

and goodwill

6. Conclusion

5. Recognition and measurement of identifiable assets, liabilities and

goodwill

Recognition Principle

Tan, Lim & Lee Chapter 3 © 2015 28

Business Combinations are accounted under the acquisition method

Requirement: At acquisition date, the acquirer will recognizeacquiree’s net assets at fair value

Underlying assumption:

There has been an exchange transaction at arm-length pricing

There is an effective ”acquisition” of the subsidiary’s identifiable assets and liabilities

at fair value

Recognition Principle• Identifiable net assets (INA) must comply with two conditions to

qualify for recognition:– (1) INA must meet the definition of an asset or a liability – (2) INA must be priced into the consideration transferred and not a

separate stand-alone transactions

• Concept of separate transactions:– Transaction that is entered into for the benefit of acquirer rather than

acquiree– Pre-existing relationship with acquiree – for e.g. as a supplier – the

payment for the goods is separate from the consideration transferred– However, certain pre-existing relationship can be classified as

“reacquired rights” and should be recognized as an intangible asset on the basis of the remaining contractual term of the contract – for e.g. Reacquiring franchised rights granted to acquiree

Tan, Lim & Lee Chapter 3 © 2015 29

Recognition Principle

Tan, Lim & Lee Chapter 3 © 2015 30

Fair value differential

Book value of subsidiary’s

identifiable net assets

Fair value of subsidiary’s

identifiable net assets

At acquisition date:• Fair value differential will be recognized in the consolidation worksheet

In subsequent years:•

Depreciation/amortization/

cost of sale of asset will be based on the fair value recognized at the acquisition date

These entries have to be re-enacted every year until the disposal of investment

Classification of Identifiable Assets or Liabilities

• Classification of identifiable assets or liabilities is made with respect to:1. Information;

2. Conditions; and

3. Corporate policies existing as at acquisition date

Tan, Lim & Lee Chapter 3 © 2015 31

Classified as Available-for-sale securities

Reclassified as held-to-maturity according to

acquirer’s group policy

Example: Bond investment

Under acquiree’s financial statements Under consolidated financial statements

Intangible Assets

• IFRS 3 requires the acquirer to recognize the fair value of an acquiree’s unrecognized identifiable asset (e.g. intangible asset) in the consolidated financial statements– Rationale: the acquisition event justifies recognition of intangible

assets– Do not provide guidance on measurement of fair value of the

recognized intangible asset

• To qualify for recognition, the intangible asset must either:

1. Be Separable (“Separability criterion”) OR

2. Arises from contractual or other legal rights (“Contractual-legal criterion”)

Example of intangible assets: Brand names and customer relationships – When Heineken acquired APB; it acquired the iconic Tiger Beer Brand.

Tan, Lim & Lee Chapter 3 32© 2015

Intangible Assets

Tan, Lim & Lee Chapter 3 © 2015 33

Are these considered intangible assets?

Assembled workforce with specialized knowledge

× No: Firm-specific and integrated with acquiree

× (Fails separability criterion)

Potential contracts or contracts under negotiation

× No: Fails separability or contractual-legal criterion

Opportunity gains from an operating lease in favorable market conditions

Yes: Meets the contractual-legal criterion

Customer and subscriber lists of acquiree

Yes: Meets the separability criterion (show evidence of exchange transactions for similar types of lists)

Contingent Liabilities & Provisions

• Contingent liabilities are recognized by acquirer if they are:– Present obligations arising from past events and– Reliably measurable, even if outcome is not probable (IFRS 3:23)

• Example: Provisions for restructuring & termination costs are recognized if they are:

Present constructive or

legal obligations arising from past

events

Reliably measurable

Tan, Lim & Lee Chapter 3 34© 2015

Probable outflow of economic resources

Indemnification Assets

• Contractual indemnity– Provided by the former owners of the acquiree to the acquirer to make

good any subsequent loss arising from contingency or an asset or a liability

• Treatment for indemnity – The acquirer has to recognize an “indemnification asset” at the same

time the indemnified asset or liability is recognized– The indemnification asset is measured on the same basis as the

indemnified asset or liability

• Example: An acquiree is exposed to a contingent liability. Based on probabilistic estimation, the FV of the contingent liability is $100,000. The former owners provide a contractual guarantee to indemnify the acquirer of the loss. – In the consolidated balance sheet, the acquirer recognizes contingent

liabilities and an indemnification asset of $100,000 at FV

Tan, Lim & Lee Chapter 3 © 2015 35

Deferred Tax Relating to FV Differentials of Identifiable Assets and Liabilities

• The recognition of fair value differential may give rise to future tax payable or future tax deduction– tax effects need to be accounted for because the basis for taxation does

not change in a business combination– i.e. The excess of fair value over book value of identifiable net assets

will give rise to a taxable temporary difference and vice versa.

• No deferred tax liability is recognized on goodwill as goodwill is a residual

Tan, Lim & Lee Chapter 3 © 2015 36

FV > Book value of identifiable assets Deferred tax liabilities

FV < Book value of identifiable assets Deferred tax assets

FV < Book value of identifiable liabilities Deferred tax liabilities

FV > Book value of identifiable liabilities Deferred tax assets

Non-controlling interests

• Non-controlling interests (NCI) arises when acquirer obtains control of a subsidiary but does not have full ownership of voting rights.

• In a business combination, NCI are recognized by the acquirer as equity based on the following equation– Rationale: To represent outside interests’ share in the net assets of the

acquiree

Tan, Lim & Lee Chapter 3 © 2015 37

Carrying amount of acquirer’s assets +

Acq date FV of acquiree’s identifiable assets + Goodwill

Carrying amount of acquirer’s liabilities + Acq date of

FV of acquiree’s identifiable liabilities

Acquirer’s equity + NCI

share of equity of acquiree

Assets - Liabilities = Equity

Non-controlling interests

• IFRS 3 allows NCI at acquisition date to be measured at either:– Fair value; or– The present ownership instruments’ proportionate share in the

recognized amount of identifiable assets

Tan, Lim & Lee Chapter 3 © 2015 38

Fair value method Proportionate share of identifiable assets method

• Obtain a reliable measure of fair value of NCI (e.g. quoted price in active market)

• In absence of quoted price, use valuation techniques to value NCI (e.g. peer companies’ valuation or appropriate assumptions)

• Applies present ownership interests held by NCI to the recognized amounts of identifiable net assets to determine initial amount of NCI

• If NCI have potential ordinary shares, they should be measured at fair value

Goodwill

• A premium that an acquirer pays to achieve synergies from business combination– Must be recognized separately as an asset – Determined as a residual

• IFRS 3 allows 2 ways of determining goodwill:

Tan, Lim & Lee Chapter 3 © 2015 39

Fair value of consideration transferred+

Fair value of non-controlling interests+

Fair value of the acquirer’s previously held interest in the acquiree

- Acquiree’s recognized net

identifiable assets measured in

accordance with IFRS 3

Goodwill =

Fair value of non-controlling interests

Measured at fair value at acquisition date (include goodwill)

Measured as a proportion of identifiable assets as at acquisition date

Goodwill

Tan, Lim & Lee Chapter 3 © 2015 40

Integral to the entity as a whole, not individually identifiable or severable as a standalone asset

Goodwill

Depends on reliable measurement of

consideration transferred, NCI, previously held equity interests and

identifiable net assets

An expectation of

future economic benefits

arising from acquisition

Integral to the entity as a whole, not individually

identifiable or severable as a standalone asset

Goodwill

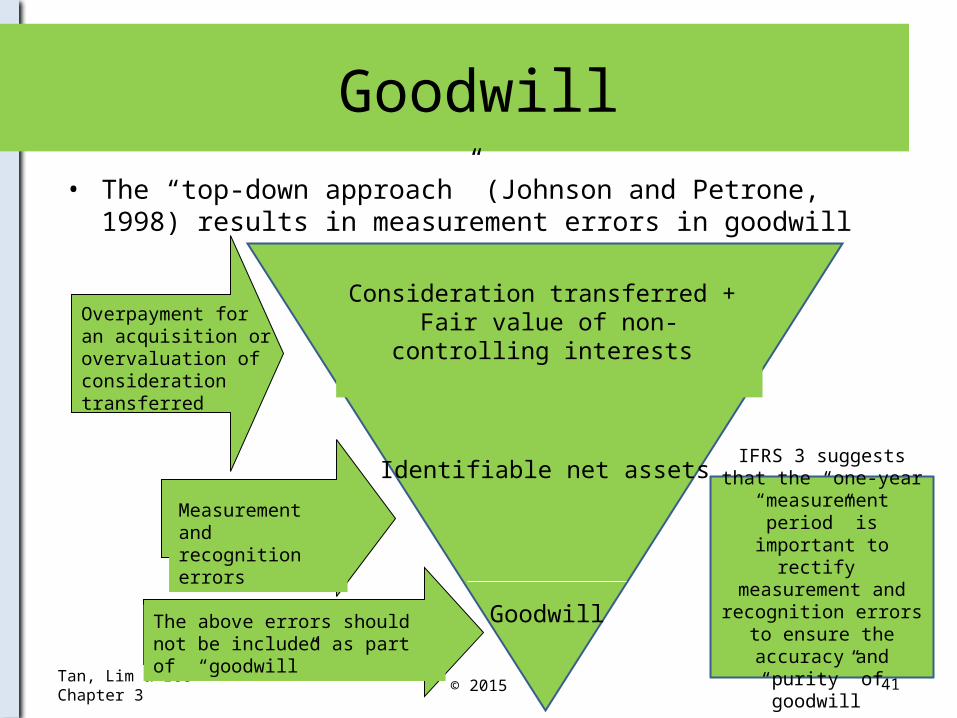

• The “top-down approach” (Johnson and Petrone, 1998) results in measurement errors in goodwill

Tan, Lim & Lee Chapter 3 41

Goodwill

Consideration transferred + Fair value of non-controlling interests

Identifiable net assets

Overpayment for an acquisition or overvaluation of consideration transferred

Measurement and recognition errors

The above errors should not be included as part of “goodwill”

© 2015

IFRS 3 suggests that the “one-year

“measurement period” is important to rectify measurement and

recognition errors to ensure the accuracy

and “purity” of goodwill

Goodwill

• In a “bottom-up” approach (Johnson and Petrone, 1998):

Tan, Lim & Lee Chapter 3 © 2015 42

Goodwill

Internally-generated Goodwill

(Core Goodwill)

Fair value of synergies (Combination goodwill)

• “Going concern element” and represent the ability of acquiree to generate higher rate of return than from its individual assets

• Generated from the unique combination of the acquirer and acquiree

• FV of the group > than sum of FV of individual entities

Illustration 1: Goodwill

Illustration 1On 1 July 20x1, P purchased 1.5 million shares from S Co’s existing owners. Total number of shares issued by S Co was 2 million. A reliable FV of S Co’s share was $10/share. P Co was obligated to pay an additional $1 million to vendors of S Co if S Co maintained existing profitability over the subsequent two years from 1 July 20x1. It was highly likely that S Co would achieve this expectation and the fair value of the contingent consideration was assessed at $1 million. FV of NCI as at 1 July 20x1 was $5 million. Assume a tax rate of 20%

Additional information of S Co.• Book value of net assets: $3,650,000• FV of net assets : $14,350,000• FV less book value (net assets): $10,700,000• Share capital: $2,000,000• Retained earnings: $1,650,000

Tan, Lim & Lee Chapter 3 © 2015 43

Illustration 1: Goodwill

Determine the acquirer's interest in the acquiree:

Percentage ownership (75%)

Consideration transferred: = ($1,500,000 x $10) + $1,000,000 [FV of contingent consideration]

= $16,000,000

Determine goodwill: Consideration transferred + FV of NCI – FV of identifiable net assets at acquisition date

Determine deferred tax liability of (20% x $10,700,000) = $2,140,000

Determine FV of identifiable net assets = $14,350,000 - $2,140,000 = $12,210,000

Goodwill = $16,000,000 + $5,000,000 - $12,210,000 = $8,790,000

Tan, Lim & Lee Chapter 3 © 2015 44

Gain From a Bargain Purchase

• A gain from bargain purchase arises when:

• In essence, a windfall gain to acquirer• The acquirer must re-assess the fair value of identifiable net assets,

consideration transferred and non-controlling interests. If there is no measurement error:– The gain will be recognized immediately in the income statement

Tan, Lim & Lee Chapter 3 © 2015 45

Fair value of consideration transferred+

Fair value of non-controlling interests+

Fair value of the acquirer’s previously held interest in the acquiree

Acquiree’s net identifiable assets

measured in accordance with

IFRS 3<

Measurement Period

• IFRS 3 allows adjustments to be made retrospectively to “provisional amounts” relating to goodwill, fair value of identifiable net assets and consideration transferred if:– New information about facts and circumstances existing at acquisition date arises,– Within 1 year of acquisition date (“Measurement period”)

• Events and circumstances arising after acquisition date does not lead to measurement period adjustments• Adjustments only allowed because of incorrect or incomplete information available

as at acquisition date but was missed or misapplied

• After measurement period (1 year), any correction of errors will be deemed as a prior - period adjustment (IAS 8)• Exception: Any change in estimate arising from information on new events and

circumstances arising after acquisition date will be recognized in the current period • Example: acquirer may fail to obtain information on all contracts of acquiree as at

acquisition date

Tan, Lim & Lee Chapter 3 © 2015 46

Measurement Period – Summary

Tan, Lim & Lee Chapter 3 © 2015 47

Acquisition date

12 months End of measurement period

Error: Discovery of info on facts and circumstances existing as of acquisition date

Retrospective change: Adjust goodwill, fair value of identifiable net assets, fair value of NCI as if the accounting was completed on acquisition date

Change in estimate: Circumstances arising after acquisition date

Prospective change: no correction of goodwill, fair value of identifiable net assets or fair value of NCI

Any correction of error after end of measurement period requires prior period item disclosures

Conclusion

Tan, Lim & Lee Chapter 3 © 2015 48

• All business combinations are characterized by three conditions:

1. Existence of acquirer

2. Acquirer has control over an acquiree

3. Acquiree is a business

• Many modes of business combinations:

– Acquirers acquires net assets of the business

(Consequence: Assets and liabilities acquired recognized in the acquirer’s legal

entity financial statements)

– Acquirer acquires control over the equity of the acquiree

(Consequence: acquirer and acquiree retain separate legal identities but

economically, these entities belong to same group)

– Regardless of form, economic substance of combination is the same and

acquisition method should be applied

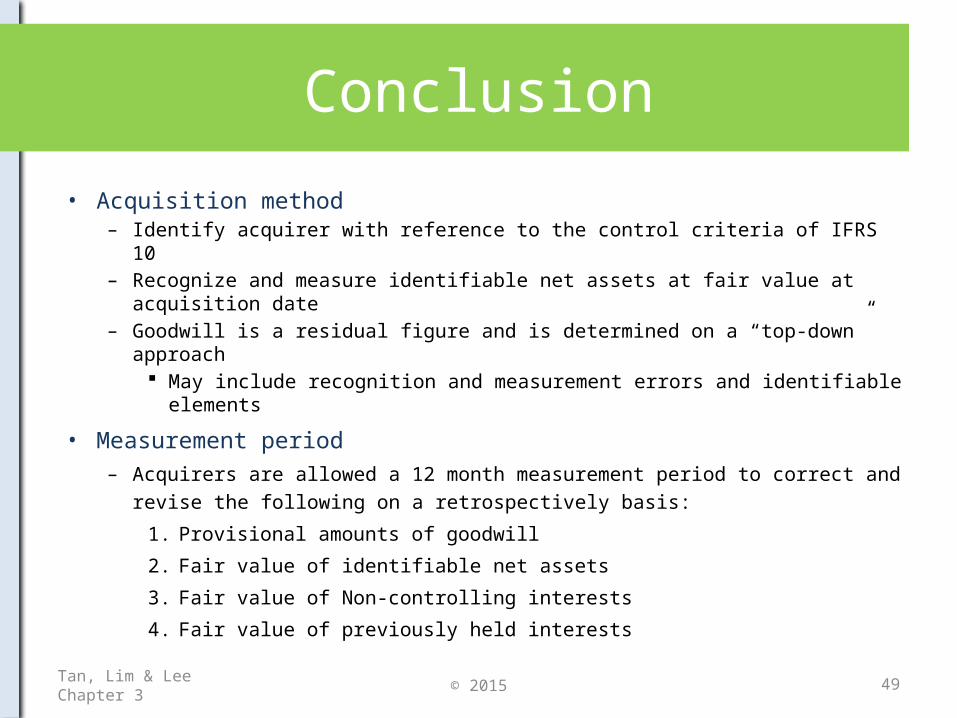

Conclusion

• Acquisition method– Identify acquirer with reference to the control criteria of IFRS 10– Recognize and measure identifiable net assets at fair value at acquisition

date– Goodwill is a residual figure and is determined on a “top-down” approach

May include recognition and measurement errors and identifiable elements

• Measurement period– Acquirers are allowed a 12 month measurement period to correct and revise

the following on a retrospectively basis:

1. Provisional amounts of goodwill

2. Fair value of identifiable net assets

3. Fair value of Non-controlling interests

4. Fair value of previously held interests

Tan, Lim & Lee Chapter 3 © 2015 49