addendum - ipti – international property tax institute · nevada ... information contained in...

TRANSCRIPT

ADDENDUMGENERAL INFORMATION1

TABLE OF CONTENTSAddendum – General Information ......................... A-1United States ......................................................... A-2Alabama ................................................................. A-2Alaska ..................................................................... A-2Arizona ................................................................... A-3Arkansas ................................................................. A-5California ................................................................ A-6Colorado ................................................................. A-8Connecticut ............................................................ A-9Delaware .............................................................. A-10District of Columbia .............................................. A-12Florida .................................................................. A-12Georgia ................................................................. A-13Hawaii ................................................................... A-14Idaho .................................................................... A-16Illinois ................................................................... A-17Indiana .................................................................. A-18Iowa ...................................................................... A-20Kansas ................................................................... A-21Kentucky ............................................................... A-22Louisiana .............................................................. A-23Maine ................................................................... A-25Maryland .............................................................. A-26Massachusetts ...................................................... A-27Michigan ............................................................... A-28Minnesota ............................................................ A-29Mississippi ............................................................ A-30Missouri ................................................................ A-31Montana ............................................................... A-31Nebraska ............................................................... A-32Nevada ................................................................. A-34New Hampshire .................................................... A-35New Jersey ........................................................... A-36New Mexico .......................................................... A-36New York .............................................................. A-37North Carolina ...................................................... A-38North Dakota ........................................................ A-39Ohio ...................................................................... A-41Oklahoma ............................................................. A-41Oregon .................................................................. A-42

Pennsylvania ......................................................... A-43Puerto Rico ........................................................... A-44Rhode Island ......................................................... A-45South Carolina ...................................................... A-45South Dakota ........................................................ A-46Tennessee ............................................................. A-47Texas ..................................................................... A-47Utah ...................................................................... A-48Vermont................................................................ A-49Virginia ................................................................. A-50Washington .......................................................... A-51West Virginia ........................................................ A-51Wisconsin ............................................................. A-52Wyoming .............................................................. A-53Australia ............................................................... A-55Australian Capital Territory (ACT) ......................... A-55New South Wales ................................................. A-55Queensland .......................................................... A-56South Australia ..................................................... A-61Tasmania............................................................... A-62Victoria ................................................................. A-64Western Australia ................................................. A-65Canada ................................................................. A-67Alberta .................................................................. A-67British Columbia (BC) ............................................ A-67New Brunswick ..................................................... A-70Newfoundland ...................................................... A-71Nova Scotia ........................................................... A-71Ontario ................................................................. A-72Quebec ................................................................. A-73Saskatchewan ....................................................... A-74Hong Kong ............................................................ A-75Ireland .................................................................. A-77New Zealand ........................................................ A-81South Africa ......................................................... A-82United Kingdom ................................................... A-85England ................................................................. A-85Northern Ireland................................................... A-87Scotland ................................................................ A-90Wales .................................................................... A-91

1. Information contained in this Addendum is based on details supplied during 2013; there may have been some factual changes in a number of jurisdictions since then which are not reflected in the current version of the Addendum.

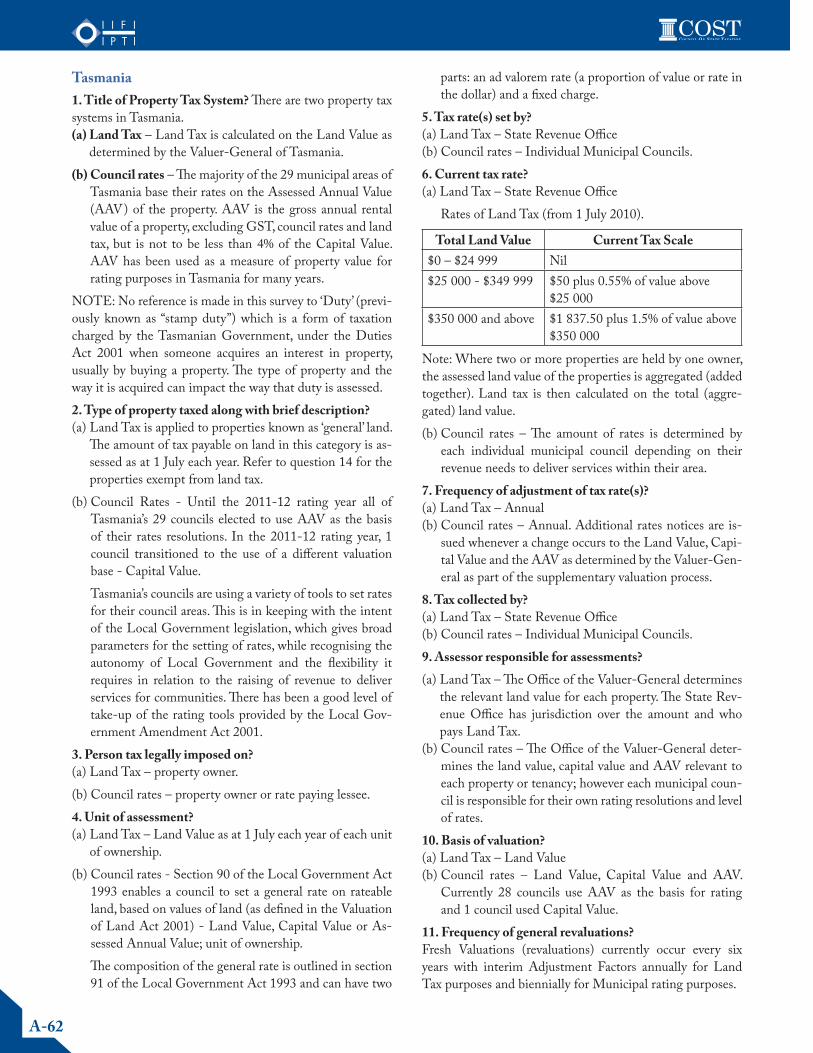

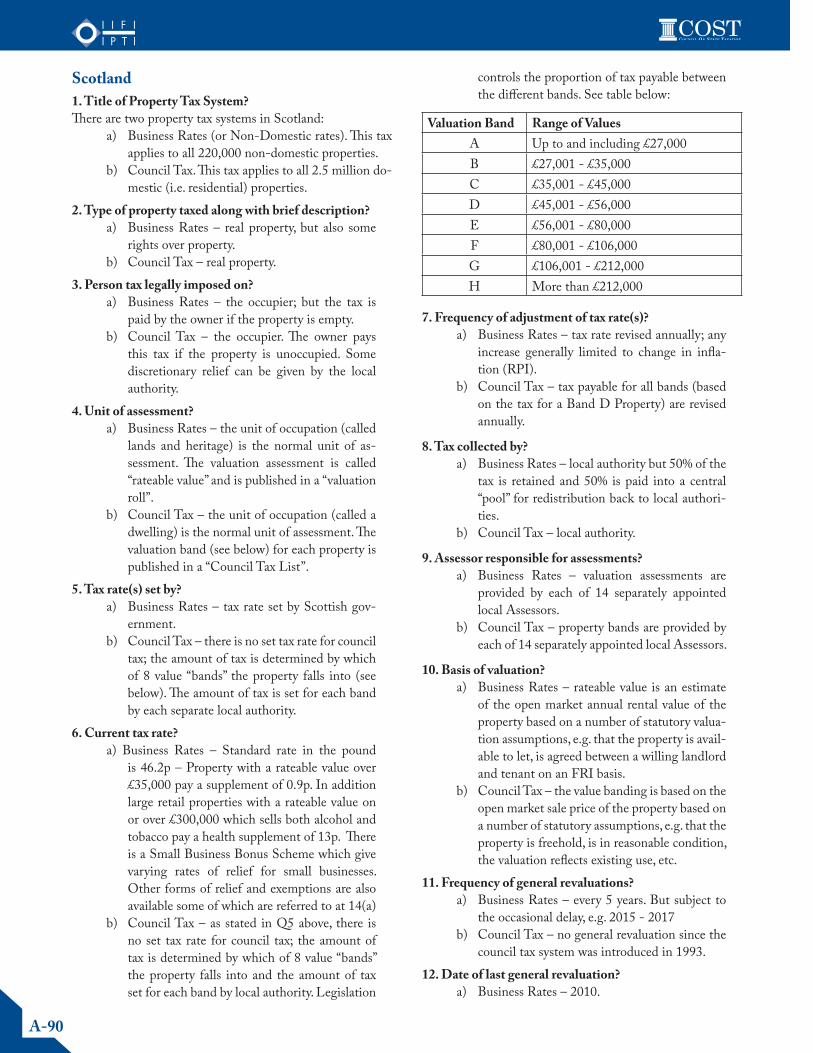

A-2

UNITED STATES

Alabama1. Title of Property Tax System? Property Tax.2. Type of property taxed along with brief description?Real property and business personal property. Intangible property is generally taxable, unless specifically exempted. Ala. Code § 40-11-1(b).3. Person tax legally imposed on? Owner. Ala. Code § 40-7-14. Unit of assessment? Piece, parcel, tract, or lot. Ala. Code § 40-11-1(b).5. Tax rate(s) set by? State and local government.6. Current tax rate? The state’s tax rate is 0.65%. City and county tax rates range from 0-4.93%, but the average rate state-wide (including the state’s rate) is 4.2%. There are four classes of property with different assessment ratios:Class I (Utility) – 30% of market valueClass II (catch all) – 20% of market valueClass III (Agricultural/Residential/Forest/Historic) – 10% of market valueClass IV (Privately owned autos and trucks) – 15% of market value. Ala. Code § 40-8-1(a).7. Frequency of adjustment of tax rate(s)? Annually.8. Tax collected by? State Department of Revenue and county tax offices, depending on the specific property tax.9. Assessor responsible for assessments? All taxable real and personal property, with the exception of public utility property, is assessed on the local level by the county assess-ing official. Utility property, freight line and equipment com-panies are centrally assessed by the Department of Revenue (DOR).10. Basis of valuation? Fair and reasonable market value. Ala. Code § 40-7-62. 11. Frequency of general revaluations? Property is ap-praised annually.12. Date of last general revaluation? Varies by assessing ju-risdiction13. Valuation date used for current assessment period? Oc-tober 1st. Ala. Code § 40-1-314. Main exemptions/reliefs? Agricultural land; charities; government; religious organizations; homesteads; schools15. Initial appeal process? A taxpayer may object to property values published by a county tax assessor by filing a written protest with the county board of equalization within 30 days of the date of final pub-lication of the property values in the local newspaper or by posting in three public places. Ala. Code § 40-3-20; Four Seasons, Inc. v. State, 450 So. 2d 110 (Ala. 1984). A taxpayer

may appeal a “final decision” of a board of equalization to the circuit court of the county where the property is located. Ala. Code § 40-3-25. The taxpayer must file notice of appeal with the secretary of the board of equalization and with the clerk of the circuit court within 30 days from the date of the final decision. Ala. Code § 40-3-25. 16. Independent body to determine unresolved appeals?Appeals of decisions by the board of equalization may be appealed to the circuit court of the county in which the prop-erty at issue is located. Ala. Code §§ 40-3-24, -25.17. Property tax revenue vs. other revenue? Alabama collected approximately $2.57 billion in state and local property taxes in 2010. This represented 19.37% of the $13.28 billion in state and local taxes collected.Property taxes accounted for approximately 44% of taxes col-lected at the local government level.At the state level, property taxes represented only about 4% of total taxes collected.18. Any significant recent changes and important issues?Classification of Property as Residential or Homestead (Amend-ing Ala. Code §§ 40-8-1 and 40-9-19; Effective Date: Sept. 1, 2011) - Provides that the classification of property as resi-dential property or a homestead would not be affected under certain conditions when the property is damaged by a natural disaster. Act 2011-710 (SB 506).

Alaska1. Title of Property Tax System? Property Tax.2. Type of property taxed along with brief description?All real and tangible personal property used primarily to ex-plore for, produce, or transport unrefined oil or gas by pipe-line is subject to a state-wide property tax. Alaska Stat. §§ 43.56.010, 29.45.080. Real and personal property is locally assessed and taxed by municipalities. Alaska Stat. § 29.45.010. 3. Person tax legally imposed on?Every person having ownership or control of an interest in taxable property. Alaska Stat. § 43.56.070, 29.45.120.4. Unit of assessment? Parcel.5. Tax rate(s) set by? Governing body (city council, or the borough assembly).6. Current tax rate? Fourteen of the eighteen organized boroughs levy a property tax. Only eleven cities outside of boroughs levy a property tax. Tax rates for locally assessed real and personal property are not published. The oil and gas property tax rate is 2% of assessed value. A credit of up to 2% against the state-wide tax imposed on oil and gas property by local jurisdictions is allowed. The smallest mill rate recorded for 2012 was $1.26 per thousand, while the largest was $32.916. http://www.commerce.state.ak.us/dca/osa/pub/12AKTax_tab5.pdf (pp. 29-32).

A-3

7. Frequency of adjustment of tax rate(s)? Annually. Alaska Stat. § 29.45.240(b)

8. Tax collected by? Municipal/Local government. Alaska Stat. § 29.45.240

9. Assessor responsible for assessments? Local Assessor is responsible for locally assessed real and personal property. Alaska Stat. § 29.45.240. The DOR is re-sponsible for assessing oil and gas production and pipeline property.

10. Basis of valuation?Property in Alaska is required to be assessed (valued for tax purposes) at fair market value. An assessment should be about the same amount as what the owner believes the prop-erty would sell for in the open real estate market. Alaska Stat. § 29.45.110. There are some variations on what “full and true value” is, in limited cases. These are found in Alaska Stat. §§ 29.45.060 -.065, 29.45.110, and 29.45.230, and cover certain uses that restrict or limit the ability to recover full and true value upon sale, such as farm use, conservation easement, or property affected by a natural disaster.

11. Frequency of general revaluations?Both state and municipal taxable property is valued annually. Alaska Stat. §§ 29.45.160, 43.56.090.

12. Date of last general revaluation?At the state level, the Department of Revenue must annually prepare an assessment roll. Alaska Stat. § 43.56.090. At the local level, the county assessor must also prepare an assess-ment roll annually. Alaska Stat. § 29.45.160.

Assessors assess property as of its full cash value on Janu-ary 1st. Assessors then mail preliminary tax statements to property owners, with tax bills following once levy rates are determined.

Alaska law does not specify a deadline for completion of the assessment roll. But tax rates have to be established by June 15th of each year, with tax statements sent out no later than July 1st.

13. Valuation date used for current assessment period? January 1st. Alaska Stat. §§ 29.45.110, 43.56.060.14. Main exemptions/reliefs?Homesteads; federal property; municipal property; intangi-ble property; nonprofit, religious, charitable, and educational organizations; state property and property of the University of Alaska; timber (unharvested); etc.Alaska exempts from property taxes, the first $150,000 of as-sessed value for all senior citizens (65 years of age and over) and disabled veterans (50% or more service connected disabil-ity). http://www.commerce.state.ak.us/dca/osa/taxfacts.htm15. Initial appeal process?Assessments of centrally assessed oil and gas property must be filed in writing with the Alaska Department of Revenue

(DOR) within 20 days of the effective date of the notice. Alaska Stat. § 43.56.110. For locally assessed property, tax-payers have 30 days from the notice of assessment to submit a written appeal to the assessor. Alaska Stat. § 29.45.190.16. Independent body to determine unresolved appeals?Centrally Assessed property : Objections to centrally assessed property (i.e., oil and gas property) must be filed with the DOR within 20 days of the effective date of the notice. Alaska Stat. § 43.56.110. After a ruling by the Department a party may further appeal to the local Board of Equalization within 50 days from the effective date of the notice of the assessment. Alaska Stat. § 43.56.120. An owner or munici-pality may appeal to the superior court for trial de novo of the board of equalization’s action. Alaska Stat. § 43.56.130(i).Locally Assessed property : For locally assessed property, tax-payers have 30 days from the notice of assessment to submit a written appeal to the assessor. If unsatisfied with the as-sessor’s ruling the taxpayer may appeal to the local Board of Equalization. Alaska Stat. § 29.45.190. Board decisions may be appealed to the superior court. Alaska Stat. § 29.45.210.17. Property tax revenue vs. other revenue?Alaska collected approximately $1.52 billion in state and lo-cal property taxes in 2011. This compares to $7.4 billion in total state taxes collected.Property taxes accounted for approximately 80% of taxes col-lected at the local government level.18. Any significant recent changes and important issues?Residential Exemptions: An initiative measure to increase residential property tax exemptions has passed in the August 28, 2012 primary election ballot. Initiative 09RPEA would allow local governments to subtract up to $50,000 from a home’s assessed value before calculating property taxes. State law currently limits the exemption to $20,000. The initiative will further adjust the exemption amount for inflation.

Arizona1. Title of Property Tax System? Property Tax.2. Type of property taxed along with brief description?Real and personal property - Locally assessed: general busi-ness + Centrally assessed: mining, oil and gas, utilities, pipe-lines, airlines, railroads, telecommunications3. Person tax legally imposed on?The real property tax is imposed on the property itself and there is no personal liability on the Owner. For personal property, the owner is personally liable for the tax.4. Unit of assessment? Separate Parcel.5. Tax rate(s) set by? County.6. Current tax rate? Tax rates vary by districts within each of the 15 counties. Nine different classes of property are taxed at different per-

A-4

centages of their value: Ariz. Rev. Stat. § 42-11001. http://www.azdor.gov/Portals/0/AnnualReports/FY12_Annual_Report_Web.pdf (pp.76-77).Class 1: most business property, including mining, utilities, commercial, and telecommunications - rate being reduced over time on the following scale: 20% for tax year 201219.5% for tax year 201319% for tax year 201418.5% for tax year 201518% for tax year 2016 and beyondAriz. Rev. Stat. § 42-15001Class 2: agricultural profit and non-profit – 16% through tax year 2015, 15% thereafter. Ariz. Rev. Stat. §§ 42-12002, 42-15002.Class 3: residential property - 10%. Ariz. Rev. Stat. §§ 12003, 42-15003.Class 4: rented residential property - 10%. Ariz. Rev. Stat. §§ 42-12004, 42-15004.Class 5: railroad and flight property, Ariz. Rev. Stat. § 42-12005 - 15%Class 6: special purposes property - 5%. Ariz. Rev. Stat. §§ 42-12006, 42-15006.Class 7: commercial historic property - same as Class 1 property, except modifications to restore and rehabilitate his-toric property is assessed at 1% for up to ten years. Ariz. Rev. Stat. §§ 42-12007, 42-15007.Class 8: historic/residential property - same as Class 4 prop-erty (10%), except modifications to restore and rehabilitate historic property is assessed at 1% for up to ten years. Ariz. Rev. Stat. §§ 42-12008, 42-15008.Class 9: possessory interests on government property used for specific purposes - 1%. Ariz. Rev. Stat. §§ 42-1200, 42-15009.

7. Frequency of adjustment of tax rate(s)? Annually.

8. Tax collected by? County.

9. Assessor responsible for assessments? Local county assessor, except centrally assessed property (railroads, mines, utilities, pipelines, oil, gas and geothermal properties, airlines, private car companies, telecommunica-tions companies, airport fuel delivery companies) are valued by the Arizona Department of Revenue.10. Basis of valuation?Full cash value , which is defined as the value as determined by statute and if no statutory method is prescribed, full cash value is synonymous with market value which means the es-timate of value that is derived annually by using standard ap-praisal methods and techniques. Ariz. Rev. Stat. § 42-1100111. Frequency of general revaluations? Annually.

12. Date of last general revaluation? Property is valued ev-ery year.13. Valuation date used for current assessment period?January 1st of the year before the tax year. I.e., January 1, 2014 will be the valuation date for the 2015 property tax year.14. Main exemptions/reliefs?Agricultural property (up to $50,000); business personal property (first $50,000, the business personal property and agricultural property exemptions are increased annually for inflation – the 2013 exemption amount is approximately $133,868); government and public property; non profit hos-pitals, health care facilities for the elderly or disable, and community health care centers; intangible property; non-profit, religious, charitable, and educational organizations15. Initial appeal process?Locally Assessed Property: Appeal to county assessor, then to the county board of equalization. If the county has no board of equalization, then the assessment is appealed to the state board of equalization.Centrally Assessed Property: Department of RevenueAlternately, a direct appeal to the Arizona tax court or the superior court in the county where the property is located, by-passing the administrative appeal steps, may be main-tained. Ariz. Rev. Stat. § § 42-16201 and 16204.16. Independent body to determine unresolved appeals?Yes. Taxpayers may appeal to court decisions of the county boards of equalization, Ariz. Rev. Stat. § 42-16202, the state board of equalization, Ariz. Rev. Stat. § 42-16203, and the DOR, Ariz. Rev. Stat. § 42-16204. Alternatively, taxpayers may appeal directly to the court prior to exhausting all of their administrative remedies. Ariz. Rev. Stat. § 42-16201 17. Property tax revenue vs. other revenue?Arizona collected approximately $7.32 billion in state and local property taxes in 2010. This represented 37.26% of the $19.63 billion in state and local taxes collected.Property taxes accounted for approximately 69.25% of taxes collected at the local government level.At the state level, property taxes represented only 7.6% of total taxes collected.18. Any significant recent changes and important issues?Proposition 117 - Two value system collapsed beginning in tax year 2015. In November 2012, Arizona voters approved Proposition 117, a constitutional amendment, which col-lapses Arizona’s two value system for tax year 2015 (valua-tion year 2014) and thereafter. Under Proposition 117, “[f ]or purposes of taxes levied beginning in tax year 2015, the value of real property and improvements . . . used for all ad valorem taxes shall be the lesser of the full cash value of the property or an amount 5% greater than the value of property determined pursuant to this subsection for the prior year.” In short, annual increases in property value will be capped at 5% over the previous year’s limited value, with the total limited

A-5

value not exceeding full cash value. This new limited value will be used for purposes of calculating both primary and secondary property taxes.

Arkansas1. Title of Property Tax System? Property Tax.2. Type of property taxed along with brief description? Real and personal property.3. Person tax legally imposed on?Owner. Ark. Code Ann. § 26-3-201. Unless a lease for a term of 10 years and the property belongs to the state or any religious, scientific, or benevolent society or institution, whether incorporated or not, and school, semi-nary, saline, or other lands, then it shall be assessed to the lease holder. Ark. Code Ann. § 26-26-905.4. Unit of assessment? Separate Parcel.5. Tax rate(s) set by? County.6. Current tax rate? Though only one class of property, there are varying millage rates for counties, cities, and school districts. Combining the county, city, and school district rates, the highest tax rate for 2012 was 5.2%, the lowest was 3.72%, and the average was 4.6%. http://www.arkansas.gov/acd/pdfs/2012_Millage_Re-port.pdf. All property is assessed at 20% of true, actual, or market value.7. Frequency of adjustment of tax rate(s)? Annually.8. Tax collected by?Real property and personal property taxes are collected by the county government. Taxes from centrally assessed prop-erty are collected by the Department of Finance and Ad-ministration.9. Assessor responsible for assessments? County assessors appraise and assess all property in the counties. The Tax Division of the Public Services Commis-sion assesses and equalizes the property of public utilities and carriers and private car companies.10. Basis of valuation?20% of true and full market or actual value. Ark. Code Ann. § 26-26-303 Under sections 1 and 2 of Amendment 79 of the Arkansas Constitution, the following limits on increases in assessed value apply:If the parcel is not a taxpayer’s homestead used as the tax-payer’s principal place of residence, then for the first assess-ment following reappraisal, any increase in the taxable as-sessed value of the parcel shall be limited to not more than ten percent (10%) of the taxable assessed value of the parcel for the previous year. In each year thereafter the taxable as-sessed value shall increase by an additional ten percent (10%) of the taxable assessed value of the parcel for the year prior to the first assessment that resulted from reappraisal but shall

not exceed the full assessed value determined by the most recent reappraisal.Except as provided in paragraph g), if the parcel is a tax-payer’s homestead used as the taxpayer’s principal place of residence then for the first assessment following reappraisal, any increase in the taxable assessed value of the parcel shall be limited to not more than five percent (5%) of the taxable assessed value of the parcel for the previous year. In each year thereafter the taxable assessed value shall increase by an ad-ditional five percent (5%) of the taxable assessed value of the parcel for the year prior to the first assessment that resulted from reappraisal but shall not exceed the full assessed value as determined by the most recent reappraisal.If a homestead owner’s taxable assessed value was frozen prior to the current assessment year, it will only change in the follow-ing circumstances: the current or a subsequent reassessment establishes that the taxable assessed value of his/her property has decreased; the current or future owner no longer qualifies under Amendment 79 for the freeze: the full assessed value of any substantial improvement, as defined in ACD Rule 4.08.2, will be added to the taxable assessed value of the property.

11. Frequency of general revaluations? Varies by assessing jurisdiction.

12. Date of last general revaluation? January 1st.

13. Valuation date used for current assessment period?Public property used exclusively for public purposes 14. Main exemptions/reliefs?Churches used as such Cemeteries used exclusively as such School buildings and apparatus Libraries and grounds used exclusively for school purposes Buildings and grounds and material used exclusively for charity, Ark. Constitution Art. 16 Sec. 5All capital invested in a textile mill for the manufacture of cotton and fiber goods in any manner is exempt for seven years from the date of the location of said mill, Ar. Const. amend. 12Intangible personal property may be designated as one or more classes of personal property and such class or classes may be exempted by the legislature, Ark. Constitution Amd. 57. All intangible personal property has been exempted by the legislature, Ark. Code Ann. § 26-3-302Household furniture and furnishings, clothing, appliances, and other personal property within the home, if not held for sale, rental, or other commercial or professional use, are ex-empt. Ark. Constitution Amd. 7115. Initial appeal process?Locally Assessed - If dissatisfied with the county assessor’s as-sessment of his or her property a property owner may peti-tion or apply by letter before the third Monday in August

A-6

to the county board of equalization for an adjustment. Ark. Code Ann. §§ 26-26-910, 26-27-317. [The board is required to begin hearing appeals no later than the second Monday in August, and must decide the merits of an adjustment and notify the property owner of its decision in writing no later than 10 working days after the hearing].Centrally Assessed - Public utilities and carriers and private car companies dissatisfied with the assessment by the Tax Division of the Public Service Commission (PSC) may file a written petition for review with the PSC or Transporta-tion Safety Agency (TSA) respectively within 10 days from receiving notice of the assessment. Ark. Code Ann. §§ 26-26-1610, 26-26-1705. [Taxpayers are entitled to have interest waived if, for reasons outside the taxpayer’s control, a hearing cannot be held within 180 days of the taxpayer filing a pro-test. Ark. Code Ann. § 26-18-405(d)(1)(C)].16. Independent body to determine unresolved appeals?Locally Assessed – A property owner dissatisfied with the deci-sion of the county equalization board may appeal to the county court by the second Monday in October. Ark. Code Ann. § 26-27-318. [The appeal has preference over all other matters in the court and is heard and decided on or before November 15th of the same year]. Taxpayers are required to first exhaust their rem-edy before the board of equalization in order to appeal to the county court, unless they did not have an opportunity to appear before the board. Ark. Code Ann. § 26-27-318.Centrally Assessed – Public utilities, carriers, and private car companies may appeal the order or finding of the PSC or TSA to the Pulaski County Circuit Court and then to the Arkansas Supreme Court by filing written notice with the PSC within 30 days from the date of the action or order ap-pealed. Ark. Code Ann. § 26-24-123 .17. Property tax revenue vs. other revenue?Arkansas collected approximately $1.74 billion in state and lo-cal property taxes in 2010, representing 18.32% of the $9.49 billion in state and local taxes collected. At the state level, property taxes represented only 12.28% of total taxes collected.Property taxes accounted for approximately 41.89% of taxes collected at the local government level.18. Any significant recent changes and important issues?Hearing on Appeal - Under Act 585 (S.B. 332), taxpayers are entitled to have interest waived if, for reasons outside the taxpayer’s control, a hearing cannot be held within 180 days of the taxpayer filing a protest of a proposed assessment by the director.

California1. Title of Property Tax System? Property Tax.2. Type of property taxed along with brief description?Real and personal property – Public utilities and railroads and intercounty pipelines are centrally assessed. Other prop-erty is locally assessed.

3. Person tax legally imposed on?Owner for locally assessed property; owner or user for cen-trally assessed property.

4. Unit of assessment?Separate parcel for locally assessed property; the operating unit for centrally assessed property.

5. Tax rate(s) set by?County, with the exception of the timber yield tax rate which is set by the state. Can also be set by municipalities to cover local costs not covered by county.

6. Current tax rate? The maximum general rate of tax on assessed value is 1%. Additional increments may be added to repay voter approved bonded indebtedness. The Timber Yield tax rate is 2.9%.

7. Frequency of adjustment of tax rate(s)? Annually.

8. Tax collected by?Taxes under the state-administered “Private Railroad Car Pro-gram” [discussed infra] and the Timber Yield Tax are collected by the State Board of Equalization (BOE). Tax revenue collected from the “State-Assessed Properties Program” or the “Timber Yield Tax Program” is collected at the county level. Tax revenue from locally assessed property is collected at the county level.

9. Assessor responsible for assessments? The BOE assesses (1) railroad cars (that are not owned by railroad companies, but are operated on railway lines within the state) under its Private Railroad Car Program; (2) pub-lic utilities and railroads under its State-Assessed Properties Program; and, (3) the harvest value of timber under its Tim-ber Yield Tax program. All other property is assessed at the county level by local assessors.

10. Basis of valuation?The assessed value of most locally assessed real property is equal to its most recent purchase price adjusted each year by the lesser of 2% or the rate of inflation. Personal property and state-assessed property are annually assessed at current fair market value.

11. Frequency of general revaluations?Most locally assessed Real Property –Real property is re-valued to market value upon the date that a change of own-ership occurs or the new construction is completed. When real estate values decline or property damage occurs causing a property’s market value to fall below its assessed value, a property owner may obtain a “decline in value adjustment.”Locally Assessed Personal Property – Annually at market value on the January 1st lien dateUtilities – Annually at market valueon the January 1st lien date12. Date of last general revaluation? Lien date 201313. Valuation date used for current assessment period?Generally, January 1st with special rules for “change of own-ership” and “new construction”

A-7

14. Main exemptions/reliefs?• Government properties• Properties used for non-commercial purposes, includ-

ing hospitals, religious properties, charities, and non-profit schools and colleges

• Homestead Exemption - $7,000 of full market value, or if qualified, Disabled Veterans’ Exemption (for 2013: $122,128 basic or $183,193 low income (changes annually based upon inflation factor))

• Personal property held for sale or lease in the ordinary course of business

• Standing Timber• Application Software

15. Initial appeal process?Locally-assessed property - Property owners can appeal by filing an application for changed assessment with a county board of supervisors (sitting as a local board of equalization) or assessment appeals board between July 2nd and September 15th (depending on the county’s specific deadline). However, if notice of assessment was not provided to the taxpayer prior to August 1st, the assessment appeal deadline is extended to November 30th. / Assessments made outside the regular as-sessment period (supplemental assessments and escape as-sessments) must be appealed within 60 days from the date the notice of change in assessment is mailed. State-assessed property – A utility may file a petition for re-assessment with the BOE to appeal the assessed value of a utility’s unitary and nonunitary property. The petition must be filed by July 20. A public hearing may be held in response to the petition if requested by the assesse..

16. Independent body to determine unresolved appeals?Locally-assessed property - If the county board denies the appeal, the taxpayer may file an action in superior court, but only under certain circumstances. Taxpayers must exhaust their administrative remedies before seeking relief in court. This includes filing an application for changed assessment with the appeals board and a claim for refund of taxes with the appropriate county official(s). An action against a county must be filed in superior court within six months after the county denies the claim for refund. However, if the county fails to act on the claim for refund for more than six months, the taxpayer may consider the claim rejected and file legal action without waiting for the county to act.State-assessed property – Special requirements apply for judicial review of state-assessed property, under Cal. Rev. & Tax. § 5148.

17. Property tax revenue vs. other revenue?California collected approximately $53.51 billion in state and local property taxes in Fiscal Year 2010-2011, represent-ing 28.9% of the $185.22 billion in state and local taxes col-lected.At the state level, property taxes represented only 2.7% of total taxes collected.

Property taxes accounted for approximately 73.40% of taxes collected at the local government level.18. Any significant recent changes and important issues?Standardized procedures are not always followed by the as-sessors. Assessors proactively reduced values when current market value fell below the factored base during the recent economic downturn.In late November 2012, Sen. Mark Leno, D-San Francisco, announced a constitutional amendment to lower voter ap-proval on school district parcel taxes – a specialized form of property tax – from two-thirds to 55 percent. Other legisla-tive leaders, such as Senate President Pro Tem Darrell Stein-berg, have already endorsed such a change. In late November 2012, the Legislature’s budget analysts re-leased a report on the state’s property tax system, suggesting that the way $55 billion a year in local property taxes are distributed, adopted 30-plus years ago, may be outdated.On August 5, 2013, the California Supreme Court issued its ruling on the subject case involving the validity of Property Tax Rule 474, Petroleum Refining Properties, which provides that refinery property consisting of land, improvements and fixtures is rebuttably presumed to be a single appraisal unit in determining Proposition 8 declines in value below the Proposition 13 adjusted base year value for property tax valu-ation purposes. The Supreme Court held that Rule 474 is substantively valid but procedurally defective under the Administrative Proce-dure Act (APA). Specifically, the Supreme Court held that the adoption of Rule 474 did not exceed the Board’s rule-making authority because the rule is consistent with appli-cable constitutional and statutory provisions as well as the long-standing valuation principle that the proper appraisal unit is the collection of assets that people in the marketplace normally buy and sell as a single unit. Property Taxes staff released a letter on October 21, 2013, to County Assessors, County Counsels, County Boards of Su-pervisors, and other interested parties soliciting information relative to an economic impact report that staff will prepare in conjunction with the proposed re-adoption of Property Tax Rule 474, Petroleum Refining Properties.On August 12, 2013, the California Supreme Court issued its decision in Elk Hills Power, LLC v. State Board of Equal-ization (2013) 57 Cal.4th 593 (Elk Hills). This case addressed the question of how to properly value for property tax pur-poses a power plant, whose construction and operation had required the owner to acquire and apply certain Emission Reduction Credits (ERCs). It was undisputed that the ap-plied ERCs were intangible assets which provided legal rights that were necessary for the beneficial and productive use of the power plant. (Id. at p. 619.) The issue presented to the Court was whether the applied ERCs were properly considered by the Board in determining unitary value.

A-8

The Supreme Court concluded that, with respect to the RCLD, “the Board directly and improperly taxed the power company’s ERCs when it added their replacement cost to the power plant’s taxable value.” (Elk Hills, supra, 57 Cal.4th at p. 602.)

Colorado1. Title of Property Tax System? Property Tax.2. Type of property taxed along with brief description?Real and personal property (with the exception of personal property of a registered insurance company or financial insti-tution) – General business property is locally assessed. Oper-ating property of public utilities is centrally assessed.3. Person tax legally imposed on? Owner.4. Unit of assessment? Separate Parcel.5. Tax rate(s) set by? County Treasurer.6. Current tax rate? Current Tax Rate – Each political subdivision calculates a tax rate based on the revenue needed from property tax and the to-tal assessed value of real and personal property located within the political subdivision’s boundaries. All of the tax rates of the various taxing entities providing services in a tax area are added together to form the total tax rate. The total tax rate is a combination of the taxpayer’s county tax rate, city tax rate, school district tax rate, and the water and sanitation tax rate. In 2011, Denver’s combined general millage or Mill Rate in-cluding Denver Public Schools and Urban Drainage District was 71.307 mills or a tax rate of $0.071307 for every $1 of assessed value.Assessment Ratio – Residential real property is determined in accordance with Colo. Rev. Stat. § 39-1-104.2, which set forth an assessment ratio of 7.96% for 2011 and 2012. For 2013 and after the assessment ratio is to be set annually by the state legislature. The assessment rate for most other types of property, including personal property, is 29% of actual value. Colo. Rev. Stat. § 39-1-104.7. Frequency of adjustment of tax rate(s)? Annually.8. Tax collected by? Local government. No tax is collected at the state level.9. Assessor responsible for assessments? Local assessors (in the sixty-four counties)10. Basis of valuation?Residential property is valued using only the market ap-proach to value. Most non-residential property, including personal property, is valued by considering the market ap-proach, the cost approach, and the income approach to value.

11. Frequency of general revaluations?Real property is re-valued every two years. Personal property is re-valued annually.

12. Date of last general revaluation?2013. Real property is valued in the odd-number year.

13. Valuation date used for current assessment period? January 1st.

14. Main exemptions/reliefs?• Government and public property• Intangible property• Nonprofit religious, charitable, and educational orga-

nizations

Homestead Exemptions – for seniors and disabled veterans: 50% of the first $200,000 of actual value of the primary resi-dence of a qualifying homeowner (aged 65 or older, disabled veteran, or the homeowner’s surviving spouse). Colo. Rev. Stat. § 39-3-203.

See the link below to access the Assessors’ Reference Library, Volume 2, Chapter 10 – Exemptions for specifics.

http://www.colorado.gov/cs/Satel l i te?blobcol=ur l data&blobheadername1=Content-Disposition&blobheader name2=Content-Type&blobheadervalue1=inline%3B+file name%3D%22ARL+Volume+2-October+2013.pdf%22& blobheadervalue2=application%2Fpdf&blobkey=id&blob table=MungoBlobs&blobwhere=1251898776227&ssbinary=true

Also, Addendum 10-A, page 10.29 in the Assessors’ Refer-ence Library, Volume 2 provides a reference list of categories of exempt property and corresponding statutory references.

15. Initial appeal process?Oral or written protests for real property must be postmarked or delivered to the assessor on or before June 1st. Colo. Rev. Stat. § 29-5-121. Personal property protests must be post-marked or delivered to the assessor by June 30th. Colo. Rev. Stat. § 39-5-122(2)

The assessor must make a decision on the protest and mail a Notice of Determination by the last regular working day in June for real property and by July 10th for personal property. Any county may elect to extend the Notice of Determination mailing date from the last regular working day in June to the last regular working day in August.

Centrally assessed property must be appealed to the Board of Assessment Appeals (BAA) or Denver district court.

16. Independent body to determine unresolved appeals?If dissatisfied with the assessor’s decision, a taxpayer may ap-peal to the county board of equalization by July 15th for real property and by July 20th for personal property. Colo. Rev. Stat. § 39-8-106.

If still dissatisfied after the county board’s decision, a tax-payer may appeal to an arbitrator, district court, or the BAA within 30 days of the date the decision was mailed.

17. Property tax revenue vs. other revenue?Colorado collected approximately $8 billion in state and lo-cal property taxes in 2010, representing 39% of the $20.5 billion in total state and local taxes collected.

A-9

At the state level, property taxes represented 0% of total taxes collected.Property taxes accounted for approximately 67.33% of taxes collected at the local government level.18. Any significant recent changes and important issues?Negotiated Personal Property Tax Incentives - A taxpayer who establishes a new business facility can negotiate with a county for an annual incentive payment or credit. Previously, the maximum amount of the negotiated incentive payment or credit was limited to 50% of the amount of county taxes due on the taxable personal property located at or within the operation of the new business facility for the current prop-erty tax year. Now that ceiling has been increased to the full amount of county personal property taxes. H.B. 12-1029, signed into law on March 24, 2012.Refunds: Personal property refunds may be given if the state’s revenues exceed the limit on revenue in state Con-stitution.

Connecticut1. Title of Property Tax System? Property Tax.2. Type of property taxed along with brief description?Real and personal property (including personal property of non-residents if property is in the state for 3 months of the year) – All property is locally assessed. The state administers a special personal property tax for certain telecommunication providers. 3. Person tax legally imposed on? Owner.4. Unit of assessment? Separate Parcel.5. Tax rate(s) set by?Municipal/Local government, including counties, cities, and special taxing districts6. Current tax rate? Current Tax Rate - Local property tax mill rates for fiscal year 2012-2013 are based upon the 2011 grand list and are available in a document at http://www.ct.gov/opm/cwp/view.asp?a=2987&q=385976. These are the most current mill rates and are reflected in each municipality’s July 2012 tax bills. – The lowest combined millage rate of 11.001 is in Greenwich. The highest mill rate of 74.29 is in Hartford. The average millage rate (of those available) is approximately19.54.After the board of assessment appeals finalizes determina-tions for hearings held in March or April, a taxing jurisdic-tion determines the amount of property tax revenue that it will need for the upcoming fiscal year and sets a mill rate. Multiplying the mill rate (the basis for which is a thousandth of a dollar) by a property’s net assessment results in the prop-erty tax. The net assessment of a property is the assessment minus all exemptions for which a taxpayer qualifies.Assessment Ratio – With the exception of certain classified land, all property (regardless of class) is assessed at 70% of

true and actual (fair market) value. However, assessor may add a 25% assessment penalty if a taxpayer files a late Per-sonal Property Declaration, or an audit reveals that the tax-payer omitted personal property from the declaration.

7. Frequency of adjustment of tax rate(s)? Annually.

8. Tax collected by?Municipal/Local government, including counties, cities, and special taxing districts

9. Assessor responsible for assessments? Local assessor.

10. Basis of valuation? True and actual (fair market) value

11. Frequency of general revaluations?Real property must be re-valued at least every 10 years Conn. Gen. Stat. § 12-62(b).

12. Date of last general revaluation?Generally, October 1, 2009 for real property, Conn. Gen. Stat. § 12-62(b)(3), but localities may have initiated revaluations since then. For instance, the Town of Middlebury’s last revaluation was October 1, 2011. The City of Norwalk has commenced its Octo-ber 1, 2013 revaluation. The Town of Monroe’s next revaluation is scheduled for October 1, 2014. Each town is able to schedule it’s revaluation independent of other jurisdictions or the state as long as they get them in approximately every 5 years. Some have deferred more than once so that the cycle is 6 or 7 years.

13. Valuation date used for current assessment period? Oc-tober 1st for both real and personal property

14. Main exemptions/reliefs?Low income abatement program (if tax exceeds 8% of tax-payer’s income), Conn. Gen. Stat. § 12-124a(a)Family personal propertyGovernment or public propertyUtility propertyNon-profit and religious organizations15. Initial appeal process?A taxpayer who disagrees with an assessor’s determination regarding an assessment has the right to submit a written request for a hearing to a local board of assessment appeals. Conn. Gen. Stat. § 12-111. The date for submitting a hearing request is either February 20th or March 20th, depending on when the grand list is completed. Hearings occur in March or April. Boards of assessment appeals also meet at least once during the month of September to hear appeals related to motor vehicle assessments. Conn. Gen. Stat. § 12-112. A tax-payer must appear at a hearing before the board of assess-ment appeals, or must ensure that someone appears on the taxpayer’s behalf. Conn. Gen. Stat. § 12-113.Protest is mandatory to file a Superior Court tax appeal.16. Independent body to determine unresolved appeals?If a taxpayer disagrees with a determination of a board of assessment appeals, the taxpayer may file an appeal with the

A-10

superior court for the judicial district in which the property is located. Conn. Gen. Stat. § 12-117a.

17. Property tax revenue vs. other revenue?Connecticut collected approximately $9 billion in state and local property taxes in 2010, representing 42% of the $21.41 billion in state and local taxes collected.No taxes are collected at the state level.Property taxes accounted for approximately 98.6% of taxes collected at the local government level.

18. Any significant recent changes and important issues?Exemptions – Beginning with the October 1, 2011 assess-ment year, manufacturing machinery and equipment, in-cluding machinery and equipment used in connection with biotechnology, is exempt from Connecticut property taxes regardless of when acquired. The requirement that the ma-chinery and equipment be new has also been eliminated. Act 61 (H.B. 6652), Laws 2011

Tax Bills – Effective October 1, 2011, and applicable to as-sessment years starting on or after that date, local Connecticut property tax collectors may send tax bills and statements to tax-payers electronically so long as the taxpayer consents to elec-tronic receipt. The community must also post its email address on its website and establish procedures to ensure that taxpayers receiving electronic bills and statements also receive the com-munity’s return email address. Act 185 (H.B. 5256), Laws 2011

Partially Completed Structures – A new law explicitly al-lows towns to levy property taxes on partially completed buildings and structures. Public Act 12-157, (effective October 1, 2012 and applicable to assessment years starting on or after that date)

Jeopardy Tax Collection – Changes the process by which local tax collectors take action to collect taxes that are as-sessed but not yet due (jeopardy tax collection). Prior law required tax collectors to take immediate action to collect a tax that was assessed but not yet due when they believed that payment might be jeopardized by delay. / The act instead re-quires that they take such action only if they determine, after exercising due diligence, the payment will be delayed. The act also requires local tax collectors to notify the (1) taxpayer and (2) municipality’s chief elected official or chief executive officer when beginning a jeopardy tax collection proceeding. Public Act 12-26, (effective October 1, 2012 and applicable to assessment years starting on or after that date)

Personal Property Tax Audit Penalty – By law, a local tax assessor can compel a taxpayer to testify or produce certain books and records as part of a personal property tax audit. Under prior law, taxpayers who failed to appear at the audit, refused to answer any pertinent question, or failed to pro-duce the records were subject to a fine of up to $100, up to 30 days in prison, or both. A new law classifies this crime as a class D misdemeanour, which increases the maximum fine

from $100 to $250 and maintains the maximum prison term of up to 30 days. Public Act 12-80 (effective October 1, 2012)Filing Deadline Waivers – A new law allows certain tax-payers to receive property tax exemptions even though they missed the statutory filing deadlines for them. The exemp-tions are for manufacturing machinery and equipment, com-mercial trucks, and non-profit organization property. It also allows a taxpayer to receive a refund of the penalty assessed for failing to file a personal property declaration even though the taxpayer missed the deadline for filing the declaration. Public Act 12-2, JSS §§ 3-12 (effective upon passage)Revaluation Phase-In for Decreases in Property Values - Allows municipalities to phase in post-revaluation decreases in property values using methods that are comparable to those the law allows for phasing in increases in property val-ues. Public Act 12-2, JSS §§ 168-170 (effective July 1, 2012 and applicable to assessment years starting October 1, 2012)

Delaware1. Title of Property Tax System? Property Tax.2. Type of property taxed along with brief description?Real property. [Personal property exempt]. – All real prop-erty is locally assessed.3. Person tax legally imposed on?Generally, tax is imposed on the owner. However, for leased property, tenant is responsible for property tax (must pay it to person entitled to rent, unless other agreement exists). Tenant can deduct same amount out of rent. No set valuation date.4. Unit of assessment? Separate Parcel.5. Tax rate(s) set by? Counties, cities, and special taxing districts 6. Current tax rate? Kent County – Generally, property is assessed at 60% of its true value. For the 2012-2013 fiscal year the highest combined tax rate was $3.1352 per $100, while the lowest was $1.6271 per $100 http://dedo.delaware.gov/dedo_pdf/NewsEvents_pdf/publications/2012-2013_Property_Tax_Report.pdf. All property classified as Commercial C-2 had a tax rate of $1.59 per $100 of taxable value. However, some cities and towns had differing assessment ratios and/or rates:• The City of Camden charges $0.96 per $100 of tax-

able value for senior citizens.• The City of Dover taxes property at 100% of its 2010

assessment.• The Town of Kenton taxes property at 100% of its

1992 assessment.• The Town of Little Creek taxes senior citizens at $0.30

per $100 of assessment.• The rate for Houston was the 2010-2011 rate.• The City of Milford taxes property at 100% of its 2002

assessment.

A-11

• The Town of Smyrna taxes property at 100% of its 2006 assessment.

• Each property is charged an additional $276 base tax year per year for waste removal.

New Castle County – Generally, property is assessed at 100% of true value. For the 2012-2013 fiscal year the the highest combined tax rate was $4.2691 per $100, while the lowest was $1.8670 per $100 http://dedo.delaware.gov/dedo_pdf/NewsEvents_pdf/publications/2012-2013_Property_Tax_Report.pdf. . • Residents of the “Ardens” do not own their property,

but hold 99-year leases. Taxes are assessed on square feet of land, not value of house.

• The Town of Elsmere charges an additional $275 for each residential and commercial unit.

• Delaware City has a City Park Tax of 0.0500 which was added to the city rate.

Sussex County – Generally, property is assessed at 50% of true value. For the 2012-2013 fiscal year the highest com-bined tax rate was $6.5311 per $100, while the lowest was $3.5079 per $100 http://dedo.delaware.gov/dedo_pdf/New-sEvents_pdf/publications/2012-2013_Property_Tax_Re-port.pdf.. There was also a county capitalization tax of $3.00. However, some cities and towns had differing assessment ratios and/or rates:• The Town of Bethany Beach taxes property at 100% of

its 2002 assessment.• The Town of Blades taxes property at 50% of its 1989

assessment.• The Town of Dagsboro taxes property at 100% of its

1994 assessment.• The Town of Delmar taxes property at 100% of its

2008 assessment.• The Town of Dewey Beach taxes property at 100% of

the 1974 county assessment. (used only for beach re-plenishment)

• The Town of Laurel taxes property at 100% of its 1974 assessment.

• The Town of Lewes taxes property at 50% of its 2000 assessment.

• The City of Milford taxes property at 100% of its 2002 assessment.

• The Town of Millsboro taxes property at 100% of its 1992 assessment.

• The Town of Millville taxes property at 100% of its 1974 assessment.

• The town of Milton taxes property at 100% of its 2009 assessment

• The Town of Ocean View taxes property at 100% of its 2007 assessment.

• The Town of Rehoboth Beach taxes property at 50% of its 1968 assessment.

• The City of Seaford taxes property at 50% of its 2008 assessment.

• The Town of Slaughter Beach taxes property at 100% of its 1974 assessment.

7. Frequency of adjustment of tax rate(s)? Annually. Del. Code Ann. tit. 9, § 8101.

8. Tax collected by? County government

9. Assessor responsible for assessments? County assessor

10. Basis of valuation?All real property subject to assessment is assessed at its true value in money. Del. Code Ann. tit. 9, § 8306

11. Frequency of general revaluations?No provision for periodic review. 12. Date of last general revaluation?The date of last reassessment varies by county: Kent county, 1987; New Castle county, 1983; Sussex county, 1974.13. Valuation date used for current assessment period?No specific state-wide date. While assessed annually, the val-uation date varies by county and municipality: Kent county, 1987; New Castle county, 1983; Sussex county, 1974.14. Main exemptions/reliefs?Government propertyProperty used for educational, religious, or charitable purposesExemption for seniors ($5,000 of assessed value for those with incomes of $3,000 or less who have owned and occu-pied property in the state for at least 3 years)No homestead exemption15. Initial appeal process? Appeals are initially made to the county’s Board of Assess-ment Review. In Kent County appeals are made between April 1st and April 15th of each year; in Sussex County, be-tween February 15th and March 1st of each year; in New Cas-tle County, between March 15th and April 1st of each year. Del. Code Ann. tit. 9, § 8311.16. Independent body to determine unresolved appeals?Appeals from decisions of any Board of Assessment Review to the superior court of the county in which the person re-sides must be made within 30 days of the postmark date after receiving notice of the decision. Del. Code Ann. tit. 9, § 8312.17. Property tax revenue vs. other revenue?Delaware collected approximately $664 million in state and local property taxes in 2010, representing 18.57% of the $3.58 billion in state and local taxes collected.No taxes are collected at the state level.Property taxes accounted for approximately 82% of taxes col-lected at the local government level.18. Any significant recent changes and important issues?Exemptions – Effective July 25, 2011, religious, educational, charitable, or other specified organizations that own property in New Castle County are not automatically exempt from

A-12

county property tax and must apply for such exemption. The application for property tax exemption must be submitted to the county assessment division by March 1st of the preceding fiscal year. If the property is acquired after March 1st, the ap-plication must be submitted within 30 days of the property acquisition. Ch. 11 (H.B. 31), Laws 2011

District of Columbia1. Title of Property Tax System? Property Tax.2. Type of property taxed along with brief description?Real property and tangible personal property.3. Person tax legally imposed on? Owner.4. Unit of assessment? Separate Parcel.5. Tax rate(s) set by? Council of the District of Columbia. D.C. Code § 47-501.6. Current tax rate? Varies amongst classes of property from .85% to 10%. http://otr.cfo.dc.gov/otr/cwp/view,a,1330,q,594394.asp7. Frequency of adjustment of tax rate(s)?Annually for real property, but varies for personal property. D.C. Code § 47-501.8. Tax collected by?Office of Tax and Revenue/DC Treasurer9. Assessor responsible for assessments? Assessors are appointed by the mayor10. Basis of valuation?Open market value. D.C. Mun. Regs. § 306.11. Frequency of general revaluations?Real property is updated annually12. Date of last general revaluation? 2012.13. Valuation date used for current assessment period?January 1st for real property and July 1st for personal property. D.C. Mun. Regs. § 306; D.C. Code § 47-1523.14. Main exemptions/reliefs?Religious and charitable properties are fully exemptedHomestead exemption reduces the primary residence prop-erty value by $69,100.Tax relief is also available to seniors 65 and older with ad-justed gross income of $125000or less, as well as permanently and totally disabled taxpayers with adjusted gross income of $ 125000 or less.15. Initial appeal process?Initial appeals are made to the local assessor16. Independent body to determine unresolved appeals?Unresolved appeals go to the Real Property Tax Appeals Commission17. Property tax revenue vs. other revenue?Washington, D.C. collected approximately $1.86 billion in state and local property taxes in 2010, representing 36.96% of the $5.03 billion in state and local taxes collected.

At the state level, property taxes represented 0% of total taxes collected.Property taxes accounted for approximately 36.96% of taxes collected at the local government level.18. Any significant recent changes and important issues?

Florida1. Title of Property Tax System? Property Tax.2. Type of property taxed along with brief description?Real property, personal property, and intangibles – General business property is locally assessed. Railroad and private carline operating property are the only property types that are centrally assessed. Fla. Admin. Code Ann. r. 12D-2.002.3. Person tax legally imposed on? Owner.4. Unit of assessment? Separate Parcel.5. Tax rate(s) set by?Local governments, including cities, counties, school boards, and special districts. Each year, usually in August and Sep-tember, locally elected officials in each jurisdiction set a mill-age or tax rate for the upcoming fiscal year which usually begins on October 1st.6. Current tax rate? For 2012, the highest county combined millage rate was 23.442, the lowest was 9.7536, and the average was 17.3241 http://dor.myflorida.com/dor/property/resources/data.html.Several types of local governments can levy property taxes to support the services they provide to people in a county, city, or other specific area. They are called taxing authorities and include counties, municipalities, school districts, and special districts such as water management, fire protection, mos-quito protection or other special districts. Before adopting a budget and setting a millage (tax) rate, taxing authorities must hold public hearings and follow the statewide truth in millage (TRIM) requirements. Millage rates for each juris-diction are uniform across all property types.7. Frequency of adjustment of tax rate(s)? Annually.8. Tax collected by? County Tax Collector.9. Assessor responsible for assessments? County property appraiser10. Basis of valuation? Market value.11. Frequency of general revaluations?Annually, with physical inspection every 5 years. Fla. Stat. Ann. § 193.023(2)12. Date of last general revaluation? January 1, 2013

13. Valuation date used for current assessment period? January 1st. Fla. Stat. Ann. § 192.042

14. Main exemptions/reliefs?Educational institutionsHomestead exemption - $50,000 limit

A-13

Assessment increases limited to 3% annually for owners of homestead property and 10% annually for owners of other propertyLocal option additional homestead exemption for low in-come seniors of up to $50,000 or value of property if just value is less than $250,000.Personal property (first $25,000)Property used for charitable, religious, scientific, or literary purposesTangible personal property owned solely for personal use as household goods by the owner is wholly exemptGovernment property immune from taxation.

15. Initial appeal process?Any taxpayer who objects to the assessment may request an informal conference with the property appraiser or a mem-ber of the appraiser’s staff, although such a conference is not a prerequisite to formal administrative or judicial review. A taxpayer who objects to the assessment may file a petition requesting review by the local value adjustment board. Fla. Stat. §§ 194.011, 194.015.The petition must be filed within 25 days from the mailing of the notice of assessment. Fla. Stat. § 194.011.A taxpayer who objects to the assessment may file a petition requesting review by the local value adjustment board. Fla. Stat. §§ 194.011, 194.015

16. Independent body to determine unresolved appeals? Circuit court. Fla. Stat. § 194.036

17. Property tax revenue vs. other revenue?The ad valorem tax is an annual tax levied by local govern-ments based on the value of real and tangible personal prop-erty as of January 1 of each year. Florida’s constitution pro-hibits the state government from levying an ad valorem tax.

In 2012, Florida levied approximately $24.175 billion in local property taxes. State-wide, local ad valorem taxes ac-counted for 75.6% of all taxes collected at the county level. In 2012, local school districts received 35.54% of their financial support from state sources, 46.32% from local sources, and 18.14% from federal sources.

18. Any significant recent changes and important issues?Appeals – Applicable to petitions filed with value adjust-ment boards on or after July 1, 2011, Florida requires a peti-tioner to pay a specified amount of property tax before April 1. The value adjustment board will deny the petition by writ-ten decision by April 20th if the petitioner fails to make the required payment. Ch. 181 (H.B. 281), Laws 2010

Educational Property Exemption – Provides an exemption from ad valorem taxation for certain property used for edu-cational purposes. Sections 25 and 33, 2012-193, L.O.F. (CS/HB 7097 3rd Eng.)

Periodic Review – Allows the Department of Revenue dis-cretion in determining whether to review the assessments

of certain businesses. Section 16, 2012-193, L.O.F. (CS/HB 7097 3rd Eng.)Taxpayer Rights: Value Adjustment Board Hearing – Pro-vides that a taxpayer has a right to have a hearing before the Value Adjustment Board rescheduled if the hearing is not commenced within a reasonable time, not to exceed two hours after the scheduled time. Section 2, 2012-193, L.O.F. (CS/HB 7097 3rd Eng.)Rules and Regulations: The Florida Department of Rev enue continues to clarify the rules and regulations for value adjust-ment boards. Value adjustment boards cannot refuse to accept a petition or require written authorizations from licensed tax representatives or agents who file a petition with the board.

Georgia1. Title of Property Tax System? Property Tax.2. Type of property taxed along with brief description?Real and personal property – General business property is locally assessed. Airlines, railroad equipment companies, spe-cial franchises, and public utilities are centrally assessed.Intangible property is not taxed, and hasn’t been since 1995, although constitutional authority exists to do so.3. Person tax legally imposed on? Owner.4. Unit of assessment? Separate Parcel.5. Tax rate(s) set by?State, county, cities, schools and towns6. Current tax rate? In 2012, the average county and municipal millage rate is 30 mills. Additionally, the state millage rate in each county is 0.25 mills. The attached document “2012 Georgia County Ad Valorem Tax Digest Millage Rates” contains millage rates for each county, which includes the school rate, county in-corporated rate, city rates, and unincorporated county rates https://etax.dor.ga.gov/ptd/cds/csheets/LGS_Georgia_County_Ad_Valorem_Tax_Digest_Millage_Rates_by_Tax-ing_Jurisdiction_PTSR006OD_2012.pdfThe state portion of the property tax is scheduled to be phased out at the rate of 0.05 mills per year beginning in 2011, when the state tax rate was 0.25 mills and ending in 2016, when the millage rate will be zero. Ga. Code Ann. § 48-5-8.Taxable tangible property is assessed at 40% of its fair market value. Ga. Code Ann. § 48-5-7.7. Frequency of adjustment of tax rate(s)? Annually.8. Tax collected by?The county tax commissioner is responsible for collecting property taxes for the county, school and State. And in some counties the tax commissioner may collect property taxes for the city.9. Assessor responsible for assessments? County.10. Basis of valuation? Fair market value.

A-14

11. Frequency of general revaluations?The real property valuation cycle is every 3 years. The county appraisal staff must prepare annual assessments of real prop-erty. Ga. Comp. R. & Regs. 560-11-2-.28. However, there are no provisions requiring reappraisal or physical inspection of property for appraisal purposes at specified intervals.

12. Date of last general revaluation? Varies by assessing ju-risdiction.

13. Valuation date used for current assessment period? January 1st.

14. Main exemptions/reliefs?Governmental and public property; Homesteads; Additional homesteads for seniors; Inventory; Nonprofit, charitable, sci-entific, religious, and educational organizations

15. Initial appeal process?Appeal to county board of equalization, hearing officer, or to a binding arbitrator; must be filed with 45 days from mailing of assessment. Ga. Code Ann. § 48-5-311. The taxpayer’s ap-peal may be based on taxability, value, uniformity, and/or the denial of an exemption. The written appeal is filed with the County Board of Tax Assessors.

16. Independent body to determine unresolved appeals?The taxpayer must select one of the three options below when filing an appeal:

Appeal to the County Board of Equalization: The appeal based on value, uniformity, taxability or denial of exemption is filed by the property owner and reviewed by the board of assessors. The board of assessors may change the assessment and send a new notice. The property owner may appeal the assessment in the amended notice within 30 days. This sec-ond appeal made the property owner or any initial appeal which is not amended by the board of assessors is automati-cally forwarded to the Board of Equalization. A hearing is scheduled and conducted and the Board of Equalization renders its decision at the conclusion of the hearing. If the taxpayer is still dissatisfied, an appeal to Superior Court may be made.

Appeal to a Hearing Officer: The taxpayer may appeal to a Hearing Officer, who is a state certified general real property or state certified residential real property appraiser and is ap-proved as a hearing officer by the Georgia Real Estate Com-mission and the Georgia Real Estate Appraiser Board, when the issue of the appeal is the value or uniformity of value of non-homestead real property, but only when the value is equal to or greater than $1,000,000. If the taxpayer is still dissatisfied with the decision of the hearing officer, an appeal to Superior Court may be made.

Appeal to an Arbitrator: An appeal of value may be filed to Arbitration by filing your appeal specifying Arbitration with the board of assessors within 45 days of the date of the notice. The Board of Assessors must notify the taxpayer of

the receipt of the arbitration appeal within 10 days. The tax-payer must submit a certified appraisal of the subject prop-erty within 45 days of the filing of the notice of appeal which the board of assessors may accept or reject. If the taxpayer’s appraisal is rejected the board of assessors must certify the appeal to the county clerk of superior court for arbitration. The arbitration is authorized by the judge and a hearing is scheduled within 30 days. The arbitration will issue a deci-sion at the conclusion of the hearing, which is a final and which may not be appealed further. If the taxpayer’s value is determined by the arbitrator to be the value, the county is responsible for the clerk of the superior court’s fees, if any, and the fees and costs the arbitrator. If the board of assessors’ value is determined by the arbitrator to be the value, the tax-payer is responsible for the clerk of the superior court’s fees, if any, and the fees and costs the arbitrator.

17. Property tax revenue vs. other revenue?Georgia collected approximately $10.59 billion in state and local property taxes in 2010, representing 35.18% of the $30 billion in state and local taxes collected. At the state level, property taxes represented less than 1% of total taxes col-lected.Property taxes accounted for approximately 68.54% of taxes collected at the local government level.

18. Any significant recent changes and important issues?HB 48 (O.C.G.A § 48-5-48.2) - This bill adds a second level to the existing “Freeport exemption” for ad valorem taxation. The Level 2 Freeport exemption covers goods, wares, and merchandise of every character and kind constituting the inventory of a business which would not otherwise qualify for a Level 1 Freeport exemption. The Level 2 exemption is structured in a similar manner as the Level 1 exemption in that the local governing authority has discretion to grant or deny the exemption for the applicable tangible personal property and can determine the percentage of relief (if any) to be granted from ad valorem taxation. With respect to the Level 1 Freeport exemption the bill also provides that cer-tain foreign merchandise in transit may be exempted from ad valorem taxation.

Hawaii1. Title of Property Tax System? Property Tax.

2. Type of property taxed along with brief description?Real property. [Personal property exempt]. – All property is locally assessed within the four counties.

3. Person tax legally imposed on?Owners. See, e.g., ROH 8-2.1; MCC 3.48.130; HCC 19-27; KCC 5A-7.1 (in Kauai, assessed to lessee for leaseholds of 15 years or more) . [ note that Hawaii law gives the counties the authority to administer the property taxes in their jurisdic-tion, thus we are deleting references to the HRS where it is no longer applicable

A-15

The Real Property Tax laws are found here:Revised Ordinances of Honolulu (“ROH”)Kauai County Code (“KCC”)Maui County Code (“MCC”)Hawaii County Code (“HCC”)4. Unit of assessment? Separate Parcel.5. Tax rate(s) set by? Counties.6. Current tax rate? Rates are determined at the county level and depend on property type ranging anywhere from $0 per $1,000 for public service property in Honolulu County to $15.50 per $1,000 for time share property in Maui County For Honolulu County: http://www.realpropertyhonolulu.com/content/rpadcms/documents/2012/12_rates.pdf.For Kauai County: http://www.kauai.gov/Government/Departments/Finance/RealProperty/TaxRates/tabid/102/Default.aspxFor Maui County: http://www.mauicounty.gov/index.aspx?NID=755For Hawaii County: http://www.hawaiipropertytax.com/Forms/HtmlFrame.aspx?mode=Content/TAXRATES.htm7. Frequency of adjustment of tax rate(s)?Annually – The fiscal year runs from July 1st through June 30th 8. Tax collected by? County.9. Assessor responsible for assessments? County.10. Basis of valuation?Fair market value. See, e.g., ROH 8-7.1(a); KCC 5A-8.1; HCC 19-5311. Frequency of general revaluations?Property is valued and assessed annually. See, e.g., ROH 8-7.1(a); KCC 5A-8.1; HCC 19-53.12. Date of last general revaluation?Varies by assessing jurisdiction13. Valuation date used for current assessment period?October 1 in Honolulu county (ROH 8-6.2) October 1 for Kauai county (KCC 5A-6.2)January 1 in Maui county - http://www.mauicounty.gov/in-dex.aspx?NID=1111January 1 for Hawaii county (HCC 19-47)14. Main exemptions/reliefs?Governmental and public property; Homesteads; Special homesteads for senior citizens; Nonprofit, religious, chari-table, and educational organizations; and Disabled persons15. Initial appeal process?An informal appeal may be directed to the assessor/appraiser assigned to the parcel. A formal appeal may be lodged with the county board of review or an appeal may be filed with the State Tax Appeal Court. However, Maui and Hawaii coun-ties require an appeal be first lodged with the local county board of review. See #16 below.

16. Independent body to determine unresolved appeals?Generally, a taxpayer or a county may appeal directly to the Hawaii Tax Appeal Court (TAC) without appealing to an administrative body established by county ordinance. Haw. Rev. Stat. § 232-16. A decision of a board of review may also be appealed to the TAC. Haw. Rev. Stat. § 232-17. An ap-peal to the TAC must be submitted in writing no later than 30 days after the decision of a board of review or county administrative body is filed and must be accompanied by the cost of the appeal, not to exceed $100. Haw. Rev. Stat. §§ 232-17, 232-22. A notice of appeal must be served on the director of taxation and, in the case of an appeal from a decision involving the county as a party, the real property assessment division of the county involved. Haw. Rev. Stat. § 232-16.

A decision of the TAC may be appealed to the Hawaii Inter-mediate Appellate Court by filing a written notice of appeal and depositing the costs of appeal with the TAC within 30 days after the decision of the TAC is filed. Haw. Rev. Stat. § 232-19.Small claims appeals: A small claims procedure is available in the tax appeal court for claims in which the total tax liabil-ity, not including penalties and interest, is less than $1,000. Haw. Rev. Stat. § 232-5.However, for Maui and Hawaii counties, an appeal must first be filed with the Real Property Tax Division Board of Re-view (Maui Ord. 3900 (2011)) for Maui and the Tax Board of Review for Hawaii county. http://www.hawaiipropertytax.com/Forms/HtmlFrame.aspx?mode=Content/Forms_Ap-peals.htm&LMparent=23717. Property tax revenue vs. other revenue?Hawaii collected approximately $1.4 billion in state and lo-cal property taxes in 2010, representing 21.11% of the $6.6 billion in state and local taxes collected. At the state level, property taxes represented 0% of total taxes collected.Property taxes accounted for approximately 79.09% of taxes collected at the local government level.18. Any significant recent changes and important issues?Appeals : Hawaii taxpayers appealing real property tax assess-ments must first obtain a decision from a local administrative body established by county ordinance before appealing to the tax appeal court, if required by the county. In such circum-stances, the notice of appeal to the tax appeal court must be accompanied by a copy of the decision from the administra-tive body. Act 106(Haw. Leg. 2011) ; effective June 14, 2011Small Claims Appeals: Hawaii has enacted legislation to pro-vide that pre-trial discovery is prohibited in small claims tax appeals without prior written approval of the court and that costs and fees awarded to the prevailing party are limited to fees paid directly to the court in the course of conducting the appeal at issue. Where an appeal from a decision involves a county as a party, notice of the appeal and a copy of the state-

A-16

ment is to be served on the real property assessment division of the county involved. Act 167 (Haw. Leg. 2011)Agricultural Land (Honolulu): Applicable to tax years begin-ning on and after July 1, 2013, a Honolulu ordinance revises the availability of real property tax incentives provided by the city for dedication of agricultural land to agricultural use. Land may only be approved for agricultural use dedica-tion for five-year or 10-year periods, where formerly a one-year approval period was allowed. Further, if dedicated land is unable to be maintained as agricultural land throughout the entire dedication period, the owner may file a land use change cancellation. Definitions and clarifying language per-taining to agricultural land use dedication are added. ROH 8-7.3 amended by Ordinance 11-26, Honolulu City Council (2011)Act 326 (Haw. Leg. 2012): Requires each county to provide the department of taxation with information necessary and for department to provide the counties with information necessary for the enforcement of county real property tax laws.