accounting systems for government contractors

TRANSCRIPT

Accounting Systems for Government Contractors

John Pace, CPA, CVASteven Lyons, CPA

Accounting Systems for Government Contractors

John Pace, CPA, CVA, CGMA, Senior Manager− More than 15 years of accounting and finance experience− Prepares and analyzes indirect rate calculations, prepares

incurred cost submission proposals, provides forward pricing and proposal support and analysis

− Provides guidance related to the proper treatment of government contractor specific accounting issues

− Develops government contractor compliant accounting systems

− FAR, CAS and other regulations related to government contractors

John Pace

2

Accounting Systems for Government Contractors

Steven Lyons, CPA, Supervisor− Over 10 years of experience− Audit assurance and accounting responsibilities− Preparation of reviews and compilations for various small

businesses government contractors and nonprofit clients− Budget development and financial planning analysis− Served as Controller and CFO on various outsourced

accounting projects

Steven Lyons, CPA

3

Accounting Systems for Government Contractors

4

Combined experience of 30+ years specializing in accounting and consulting for organizations doing business with the US Government

Broad range of experience with DCAA, government and private contractors

Active in Industry Associations:− Maryland Association of CPAs Government Contracts Committee− Montgomery County Chamber of Commerce Government Contractor

Network− Reston Chamber of Commerce Government Contractor Committee

Background

Accounting Systems for Government Contractors

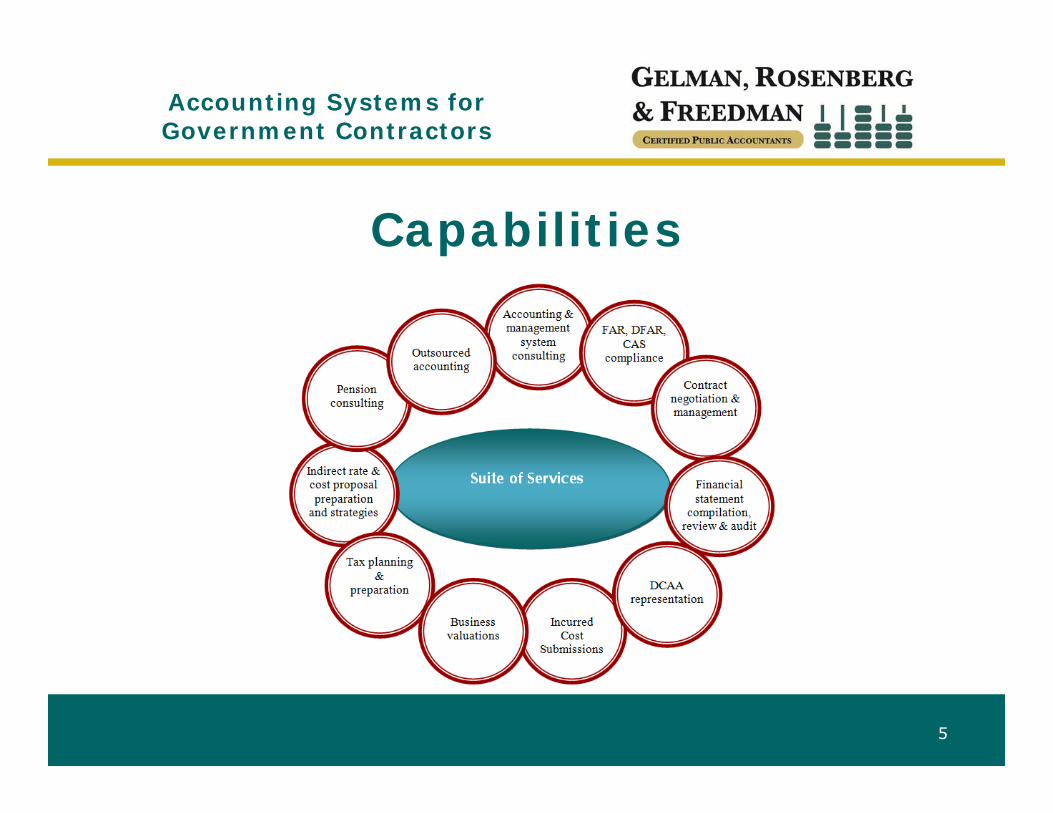

Capabilities

5

Accounting Systems for Government Contractors

I. Examples of Common Accounting Systems

II. Key Accounting System Components

III. Chart of Accounts

IV. Importance of Written Policies and Procedures

V. Internal Control Environment

6

Overview

Accounting Systems for Government Contractors

7

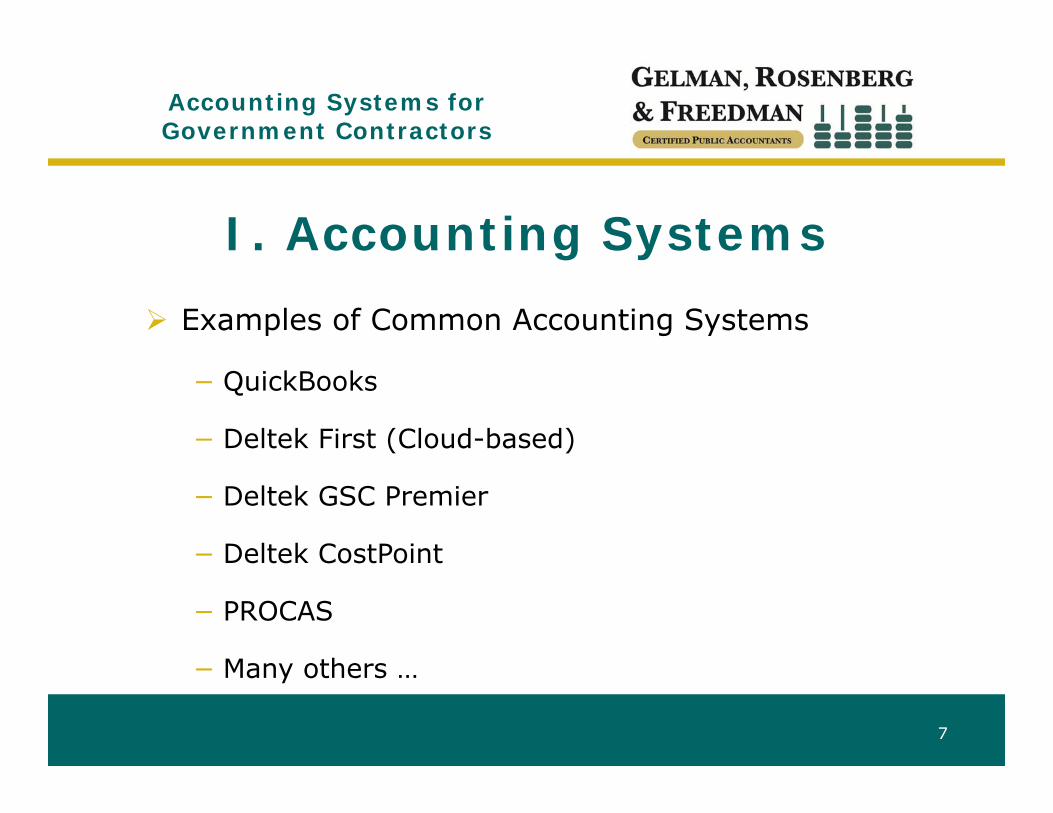

I. Accounting Systems Examples of Common Accounting Systems

− QuickBooks

− Deltek First (Cloud-based)

− Deltek GSC Premier

− Deltek CostPoint

− PROCAS

− Many others …

Accounting Systems for Government Contractors

Chart of accounts that separates direct, indirect and unallowable costs

Has a timekeeping system

Has a labor distribution system that charges direct and indirect labor to the appropriate cost objectives

8

II. Key Components of an Acceptable Accounting System

Accounting Systems for Government Contractors

Accumulates costs by contract and/or task order

Provides cost data so that indirect costs can be allocated to cost objectives based upon relative benefits received

Provides profit and loss reports by contract that can be reconciled with the general ledger

9

II. Key Components of an AcceptableAccounting System (cont.)

Accounting Systems for Government Contractors

Identifies and segregates unallowable costs (FAR Part 31)

Cost accounting records are reconciled to and controlled by the general ledger on a current basis

Maintaining and following accounting policies and procedures

10

II. Key Components of an AcceptableAccounting System (cont.)

Accounting Systems for Government Contractors

Backbone of your accounting system

Must have the ability to segregate costs types:

−Direct: 5000− Indirect: 6000-8000−Unallowable: 9000 (Direct and

indirect)

11

III. Chart of Accounts

Accounting Systems for Government Contractors

Uniform usage for all contract types (set up for most stringent reporting)

Using this format provides for much easier calculation of indirect rates and NICRA’s.

12

III. Chart of Accounts (cont)

Accounting Systems for Government Contractors

13

III. Government Contractor Chart of Accounts

Accounting Systems for Government Contractors

III. Sample Job Profit & Loss Statement

14

Accounting Systems for Government Contractors

15

IV. Importance of Written Policies and Procedures

1. Assignment of authority and areas of responsibilityAdequate segregation of duties if possible

2. General accounting system

3. Identification and exclusion of unallowable costs

Accounting Systems for Government Contractors

16

IV. Importance of Written Policies and Procedures (cont.)

4. Direct/indirect charge practices

5. Allocation of indirect costs to final cost objectives

6. Approval and documentation of journal entries

Accounting Systems for Government Contractors

17

IV. Importance of Written Policies and Procedures (cont.)

7. Establishment of account numbers

8. Approvals for establishing contract charge numbers

Accounting Systems for Government Contractors

18

1. Correct noted deficiencies promptly CPA’s management letter DCAA internal control audits

2. Maintain written policies and procedures

3. Reconcile cost accounting records back to general ledgers

4. Identify costs by contract

V. Internal Control Environment

Accounting Systems for Government Contractors

Initiate/maintain training program to reasonably assure that all employees (especially new employees) are aware of proper time charging

Write procedures and policies that:− Identify the work to be performed− Track labor charges to a final cost objective− Explain allowable or unallowable/direct or indirect− Corrections are documented− Authorizations and approvals needed

19

V. Labor System Controls

Accounting Systems for Government Contractors

Final Thoughts

Be proactive

Review your system in detail BEFORE your system audit

Make sure policies and procedures are written and followed

Follow your timekeeping procedures

Keep your books up to date

20

Accounting Systems for Government Contractors

Important References

FAR Part 31: Contract Principles and Procedures−www.acquisition.gov\far

“Information for Contractors”−www.dcaa.mil

21