accounting english lu_xiufen e-mail: [email protected] [email protected]

TRANSCRIPT

Accounting EnglishLu_Xiufen E-mail: [email protected] 13707884146

Lesson oneLesson one

Lesson EightLesson Eight

Adjusting Adjusting ProceduresProcedures

Lesson EightLesson Eight

Adjusting Adjusting ProceduresProcedures

Accounting English

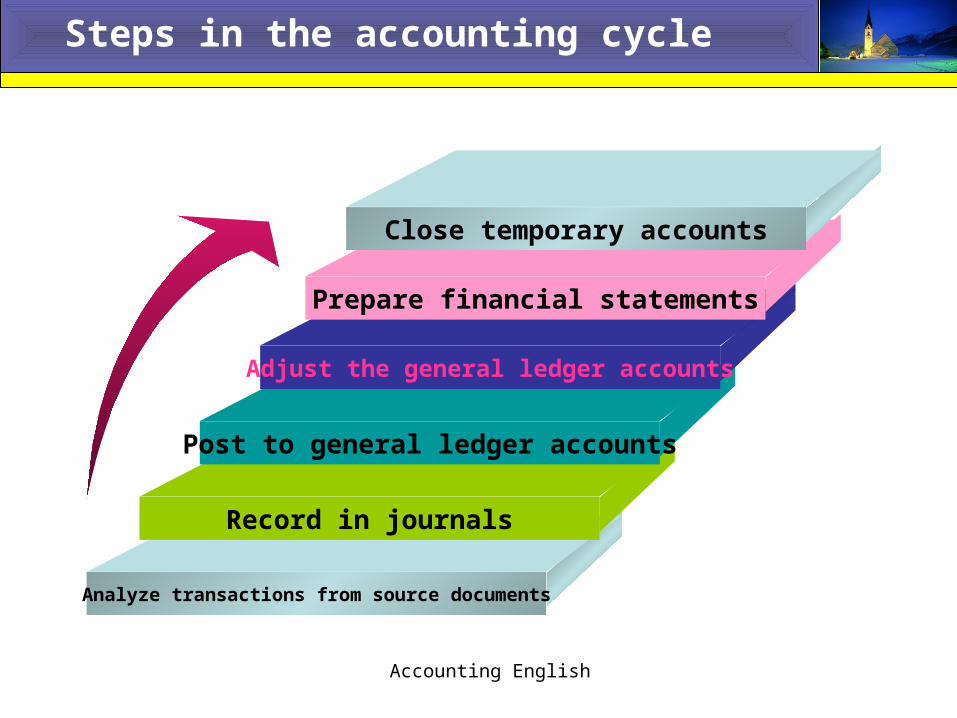

Steps in the accounting cycle

Analyze transactions from source documents

Record in journals

Post to general ledger accounts

Adjust the general ledger accounts

Prepare financial statements

Close temporary accounts

Accounting English

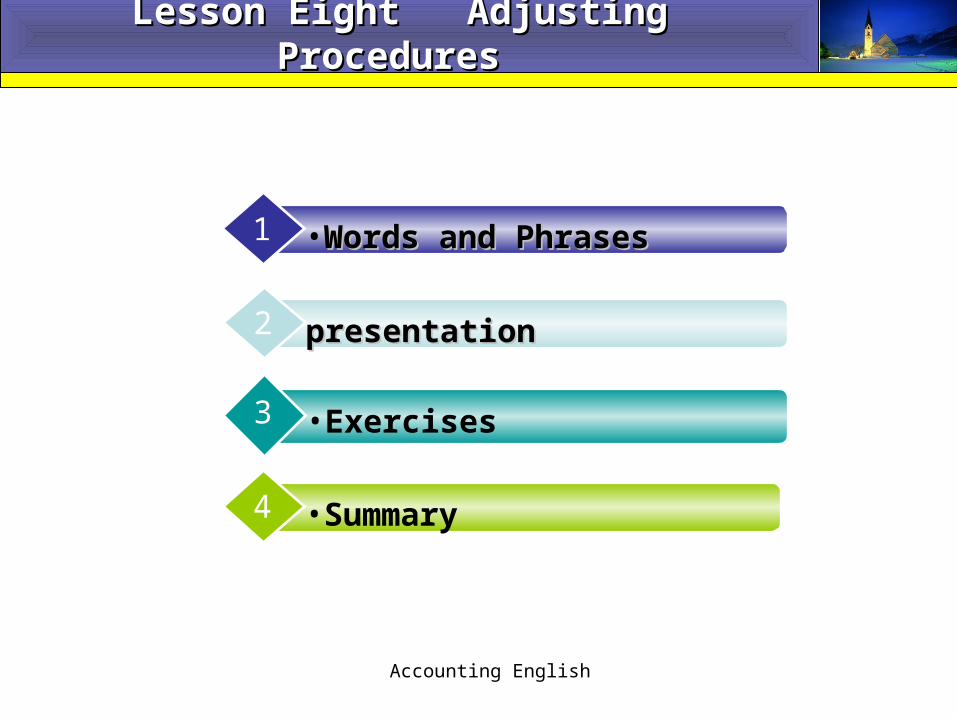

Lesson Eight Adjusting Procedures Lesson Eight Adjusting Procedures

•Words and PhrasesWords and Phrases1

presentation presentation 2

•Exercises3

•Summary4

Accounting English

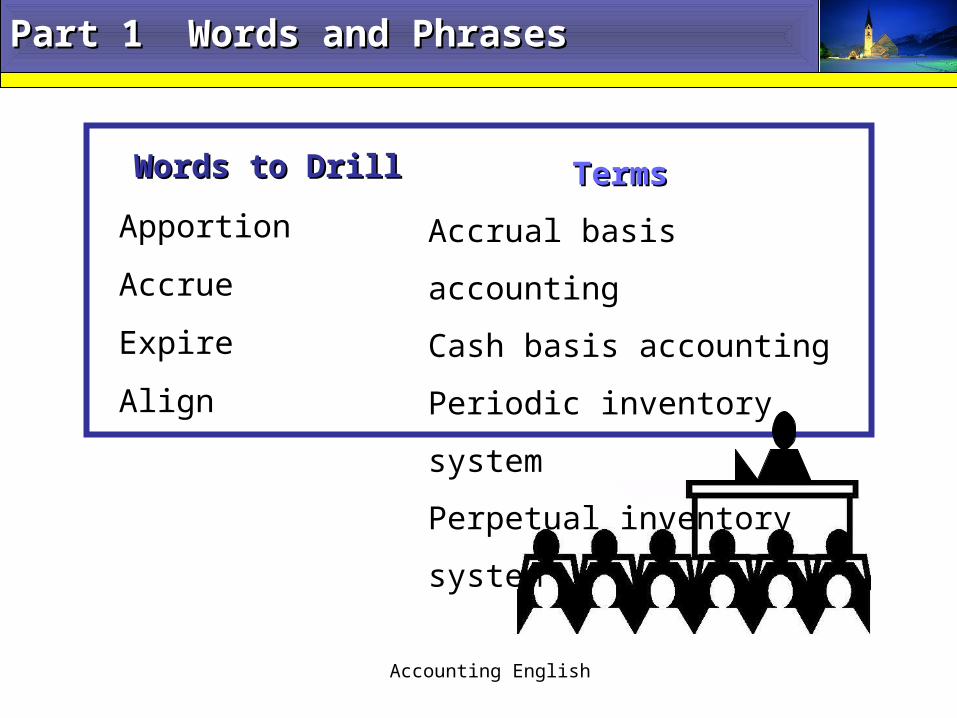

Part 1 Words and PhrasesPart 1 Words and Phrases

Words to DrillWords to Drill

Apportion

Accrue

Expire

Align

Terms Terms

Accrual basis accounting

Cash basis accounting

Periodic inventory system

Perpetual inventory system

Accounting English

Part 1 Words and PhrasesPart 1 Words and Phrases

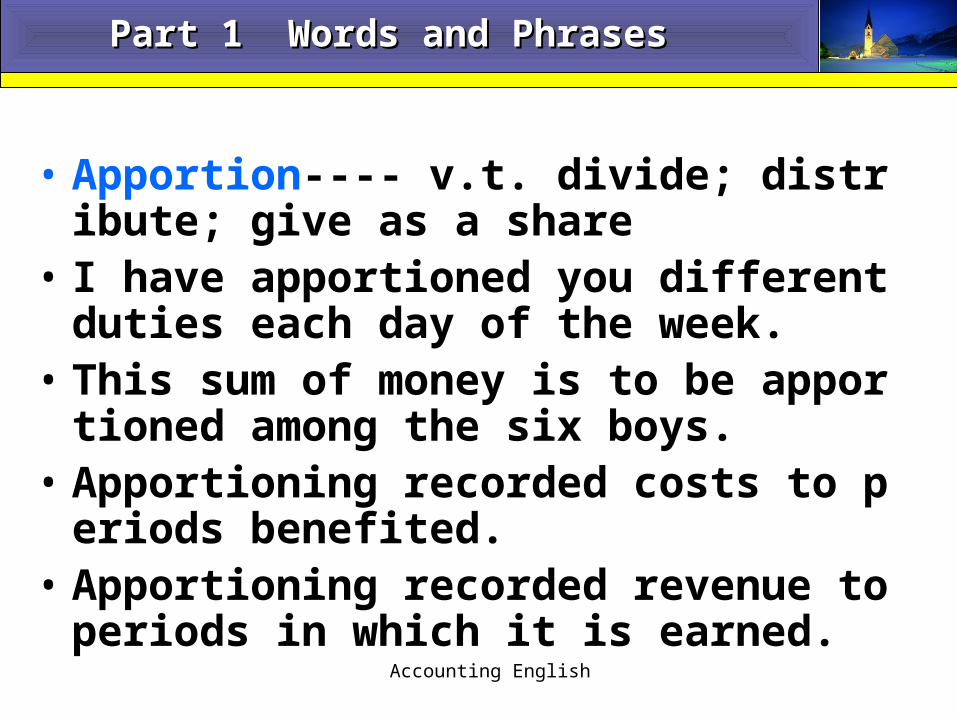

• Apportion---- v.t. divide; distribute; give as a share

• I have apportioned you different duties each day of the week.

• This sum of money is to be apportioned among the six boys.

• Apportioning recorded costs to periods benefited.

• Apportioning recorded revenue to periods in which it is earned.

Accounting English

Part 1 Words and PhrasesPart 1 Words and Phrases

• Accrue v.t., v.i. come as a natural growth or development.

• If you keep your money in the Savings Bank, interest accrued.

• Accrued interest is interest due, but not yet paid or received.

• Accruing unrecorded expenses

• Accruing unrecorded revenue

Accounting English

Part 1 Words and PhrasesPart 1 Words and Phrases

• Expire v.i. (of a period of time )come to an end

• When does your driving license expire?• At the end of each accounting period, the

estimated portion of the outlay that has expired during the period or that has benefited the period must be transferred from an asset account to an expense account.

Accounting English

Part 1 Words and PhrasesPart 1 Words and Phrases

• Align v.t. bring, come, into agreement, close cooperation etc (with)

• Adjusting entries made to align revenue and expense with the appropriate periods consist of four types:

(1) Apportioning recorded costs . (2) Apportioning recorded revenue. (3) Accruing unrecorded expenses. (4) Accruing unrecorded revenue.

Accounting English

Terms --Accounting Basis

1

accrual basis

accounting

2

cash basis

accounting

Accounting English

Terms --Accounting Basis

Text

Accounting Accounting system system

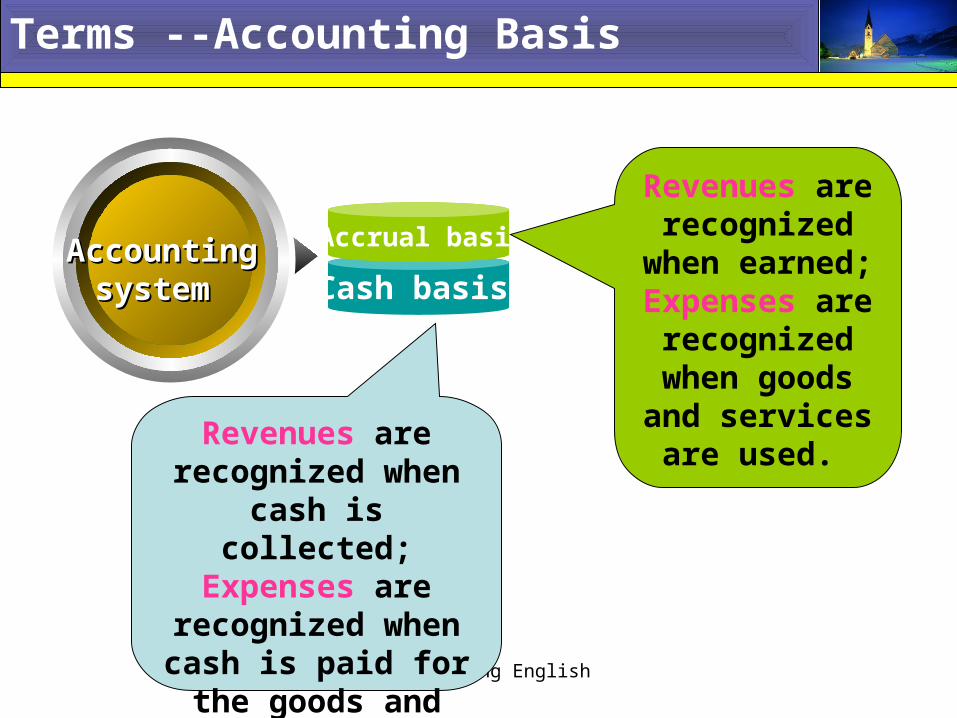

Accrual basis

Cash basis

TextRevenues are recognized when cash is collected;

Expenses are recognized when

cash is paid for the goods and services.

Revenues are recognized

when earned;Expenses are

recognized when goods and services

are used.

Accounting English

Terms –Inventory System

1

Periodic inventory system

2

Perpetual inventory system

Accounting English

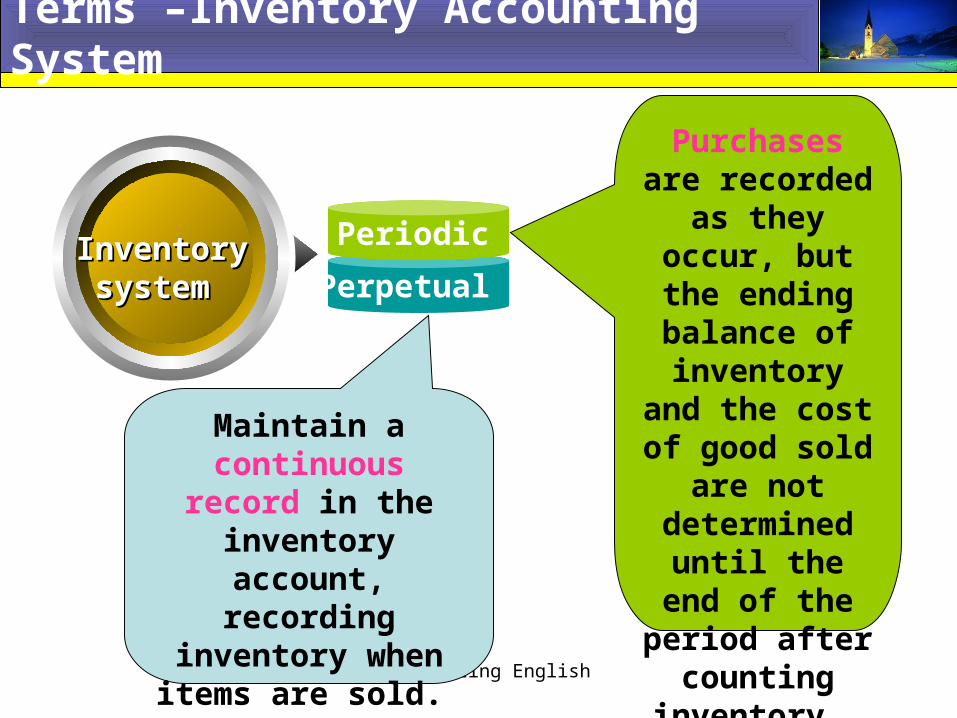

Terms –Inventory Accounting System

Text

Inventory Inventory system system

Periodic

Perpetual

TextMaintain a

continuous record in the inventory

account, recording inventory when items are sold.

Purchases are recorded as

they occur, but the ending balance of

inventory and the cost of

good sold are not determined until the end of the period after

counting inventory.

Accounting English

Part 2 PresentationPart 2 Presentation

a. Why is the adjusting step of the

accounting cycle necessary?

b. When does the adjusting step occur?

c. How to journalize the adjusting

entries?

Accounting English

Based upon accrual accounting Based upon accrual accounting

Why is the adjusting step of the

accounting cycle necessary?

Accounting English

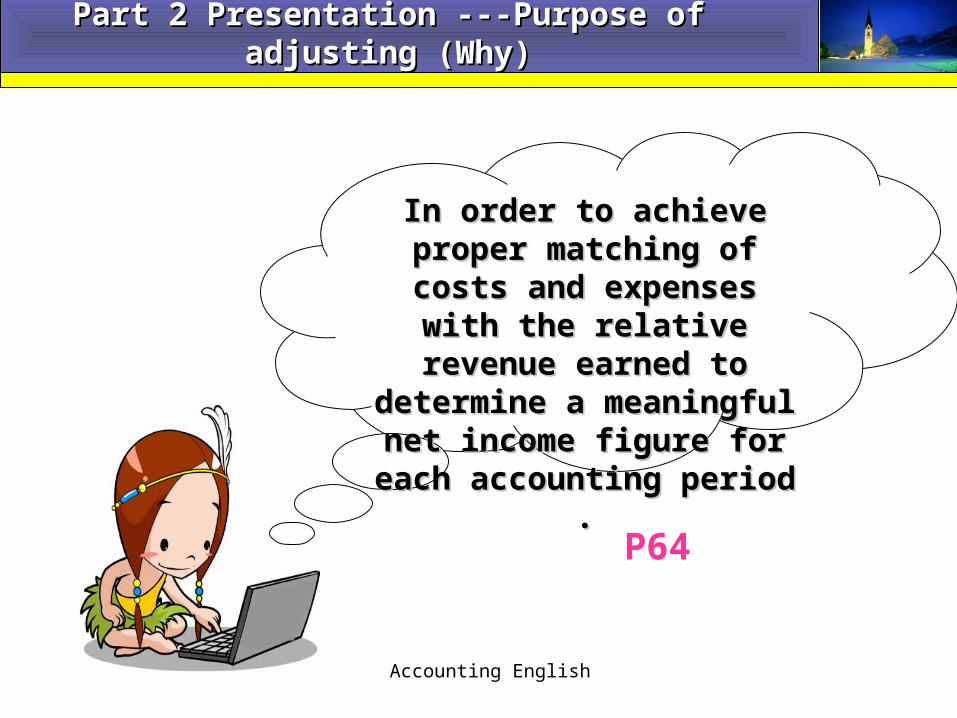

Part 2 Presentation ---Purpose of adjusting Part 2 Presentation ---Purpose of adjusting (Why)(Why)

In order to achieve proper In order to achieve proper matching of costs and matching of costs and

expenses with the relative expenses with the relative revenue earned to determine revenue earned to determine

a meaningful net income a meaningful net income figure for each accounting figure for each accounting

period .period .

P64

Accounting English

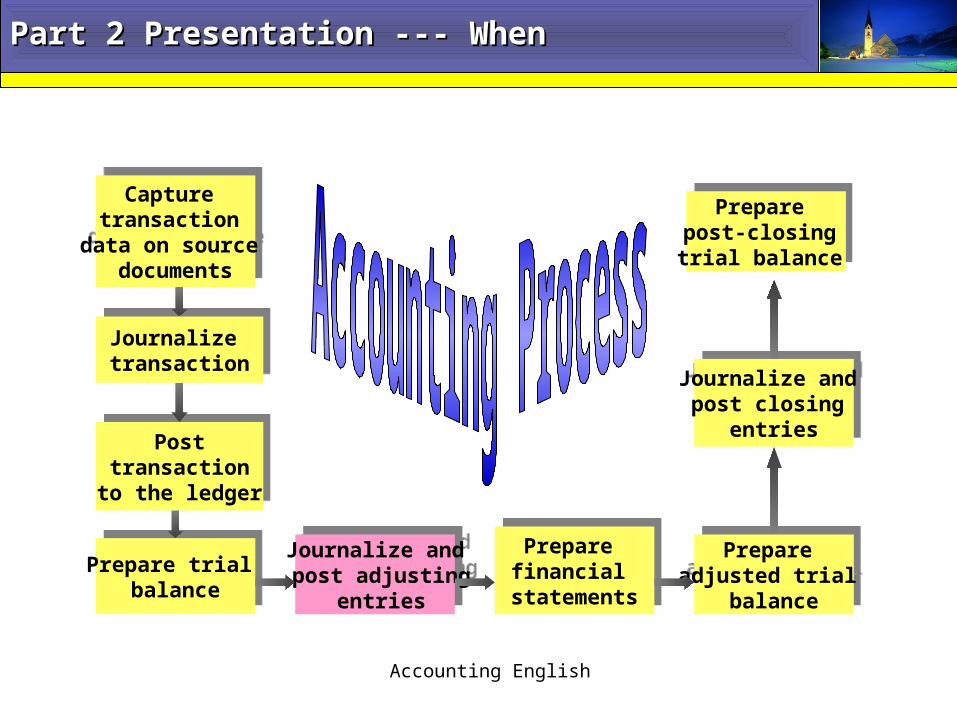

Capture transaction

data on source documents

Capture transaction

data on source documents

Journalize transaction

Journalize transaction

Posttransaction

to the ledger

Posttransaction

to the ledger

Prepare trial balance

Prepare trial balance

Journalize and post adjusting

entries

Journalize and post adjusting

entries

Prepare financial

statements

Prepare financial

statements

Prepare adjusted trial

balance

Prepare adjusted trial

balance

Journalize and post closing

entries

Journalize and post closing

entries

Prepare post-closing trial balance

Prepare post-closing trial balance

Part 2 Presentation --- When Part 2 Presentation --- When

Accounting English

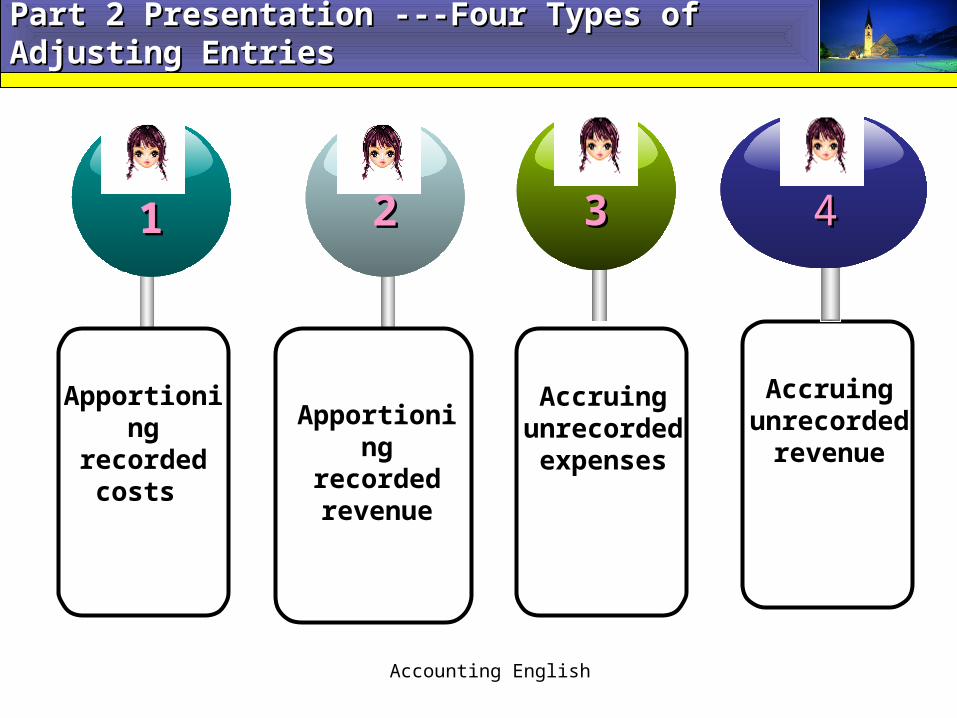

Part 2 Presentation ---Four Types of Adjusting EntriesPart 2 Presentation ---Four Types of Adjusting Entries

11 22

Apportioning recorded

costs

Apportioning recorded revenue

Accruing unrecorded expenses

Accruing unrecorded

revenue

33 44

Accounting English

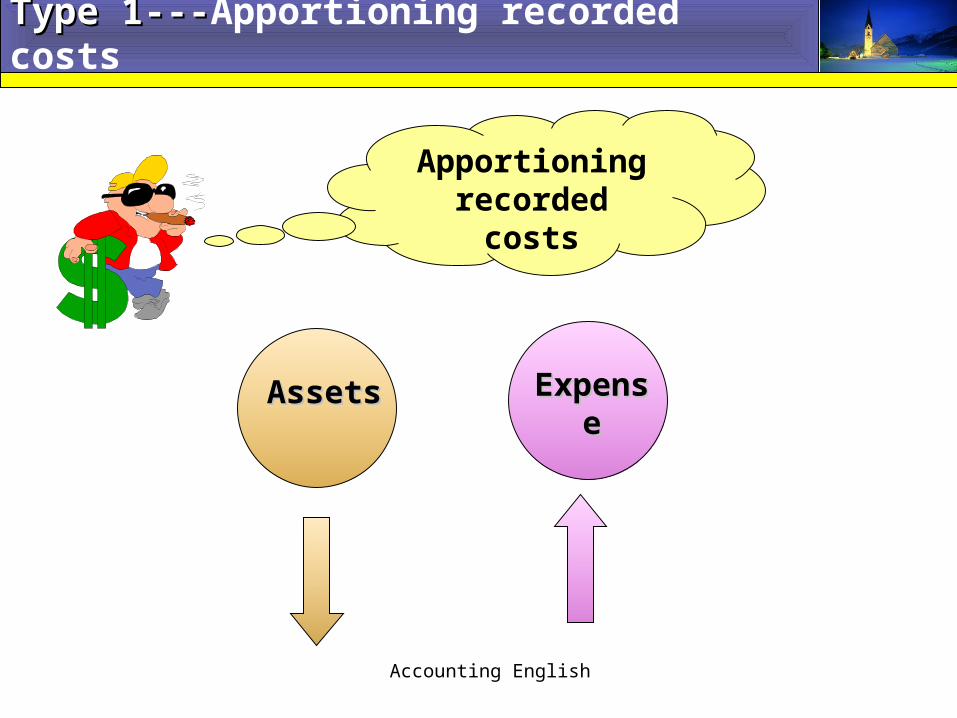

Type 1---Type 1---Apportioning recorded costs

Apportioning recorded costs

ExpenseExpenseAssets Assets

Accounting English

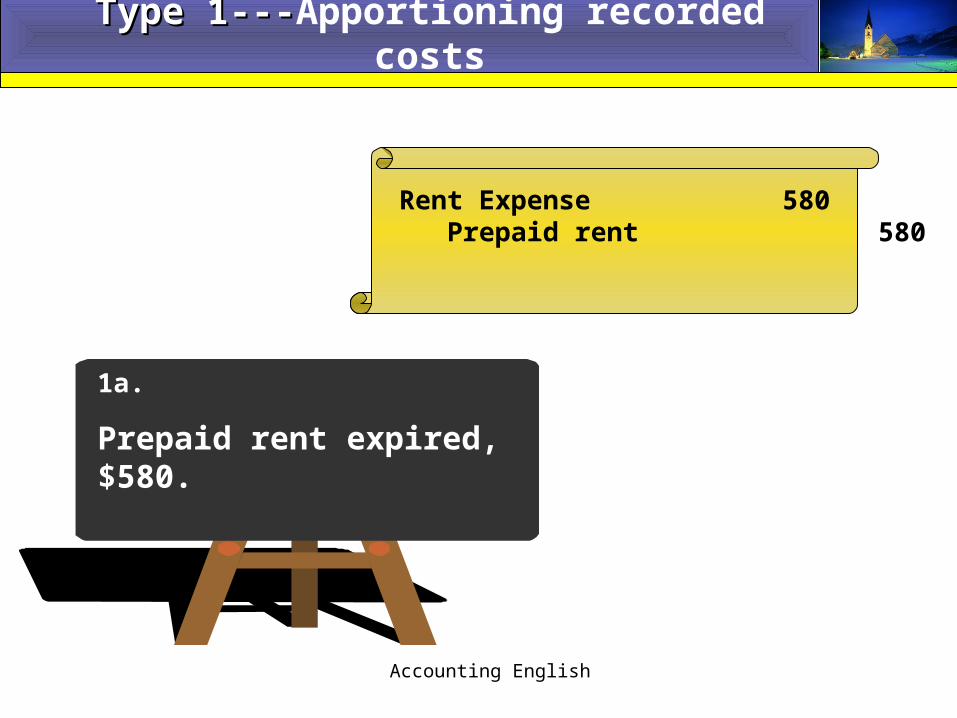

Type 1---Type 1---Apportioning recorded costs

1a.

Prepaid rent expired, $580.

Rent Expense 580 Prepaid rent 580

Accounting English

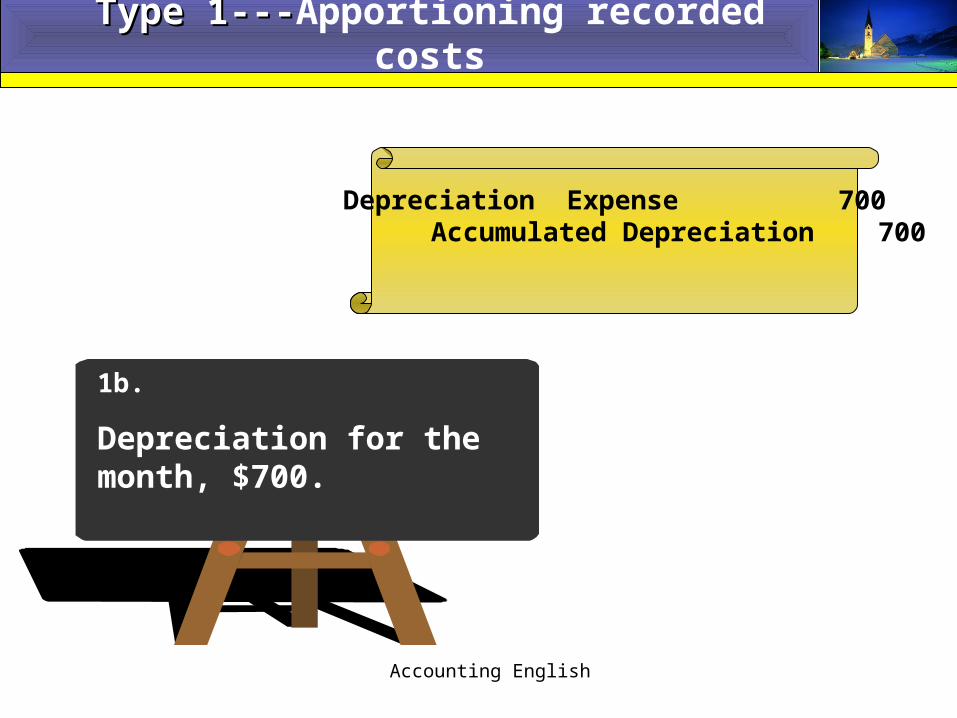

Type 1---Type 1---Apportioning recorded costs

1b.

Depreciation for the month, $700.

Depreciation Expense 700 Accumulated Depreciation 700

Accounting English

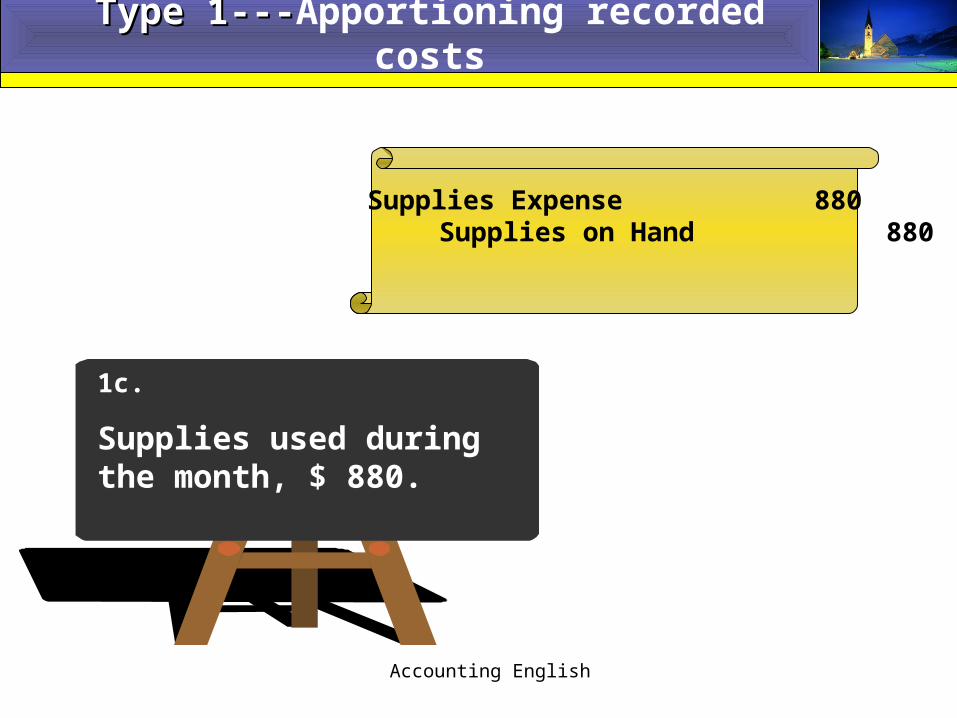

Type 1---Type 1---Apportioning recorded costs

1c.

Supplies used during the month, $ 880.

Supplies Expense 880 Supplies on Hand 880

Accounting English

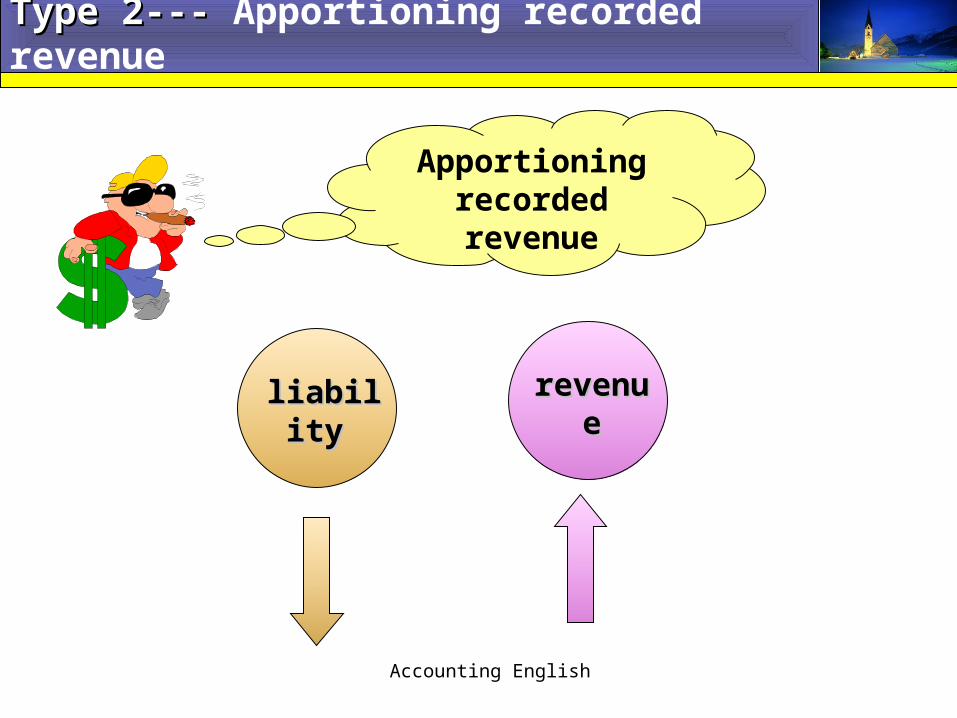

Type 2--- Type 2--- Apportioning recorded revenue

Apportioning recorded revenue

revenuerevenueliability liability

Accounting English

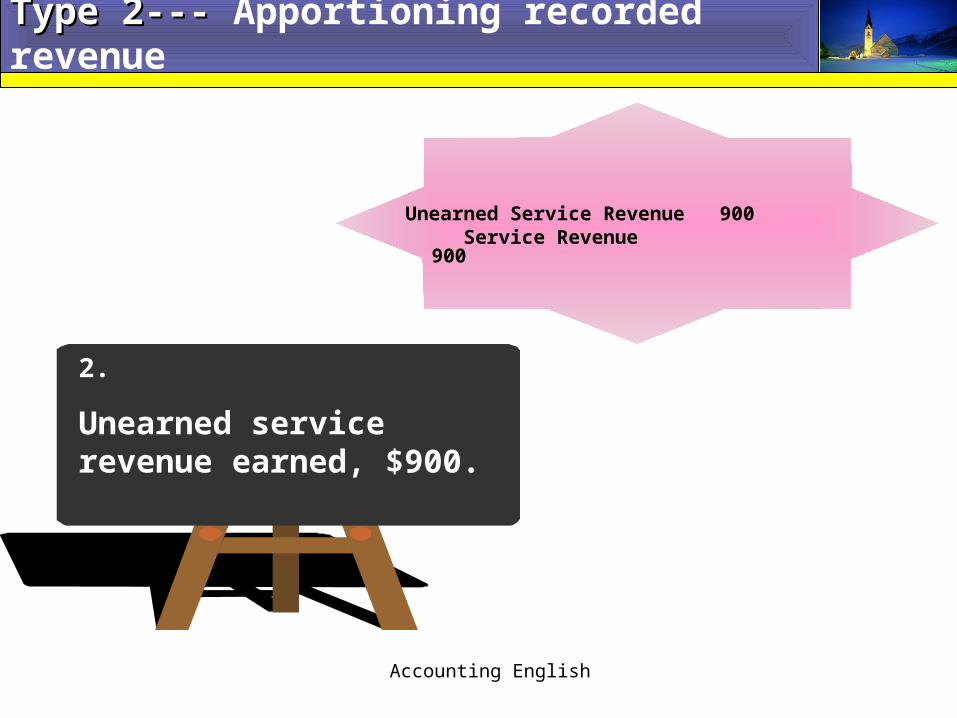

2.

Unearned service revenue earned, $900.

Unearned Service Revenue 900 Service Revenue 900

Type 2--- Type 2--- Apportioning recorded revenue

Accounting English

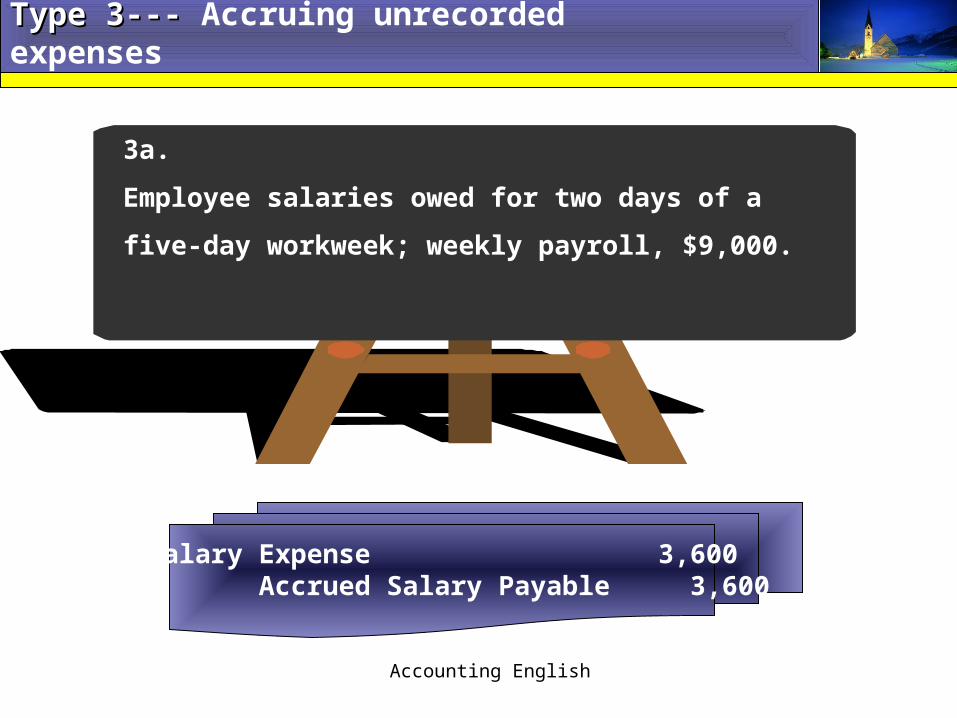

3a.

Employee salaries owed for two days of a five-day

workweek; weekly payroll, $9,000.

Salary Expense 3,600 Accrued Salary Payable 3,600

Type 3--- Type 3--- Accruing unrecorded expenses

Accounting English

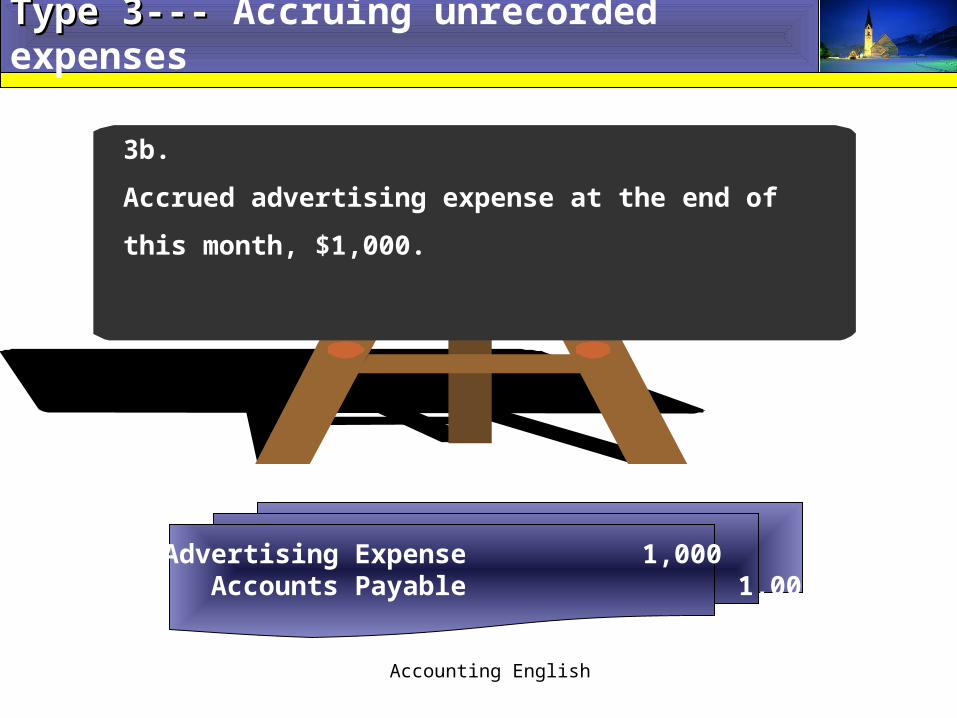

3b.

Accrued advertising expense at the end of this month,

$1,000.

Advertising Expense 1,000 Accounts Payable 1,000

Type 3--- Type 3--- Accruing unrecorded expenses

Accounting English

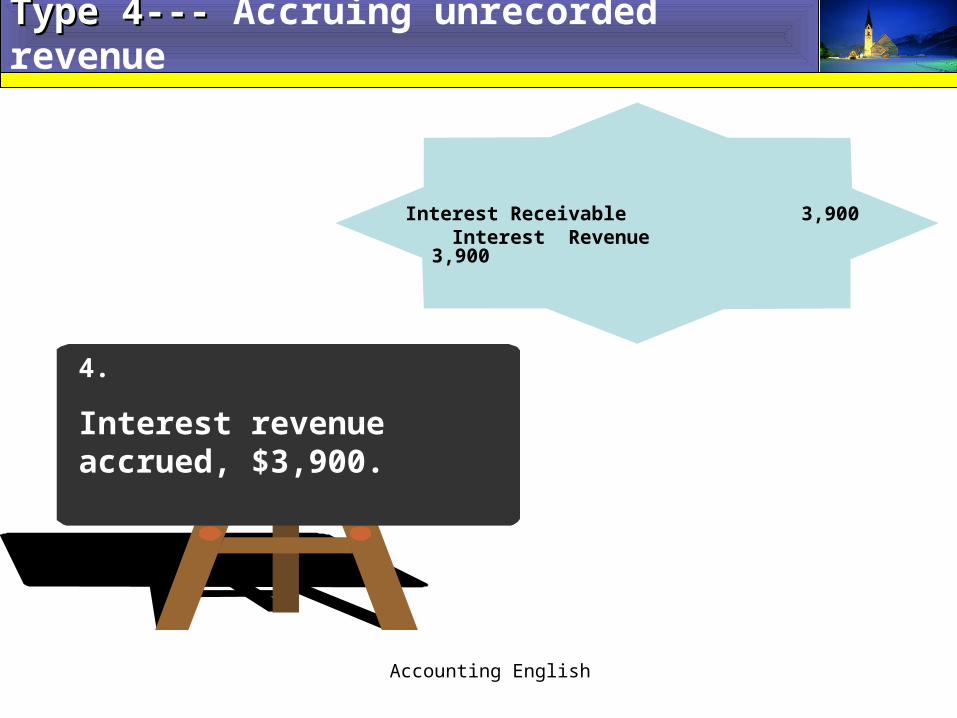

4.

Interest revenue accrued, $3,900.

Interest Receivable 3,900 Interest Revenue 3,900

Type 4--- Type 4--- Accruing unrecorded revenue

Accounting English

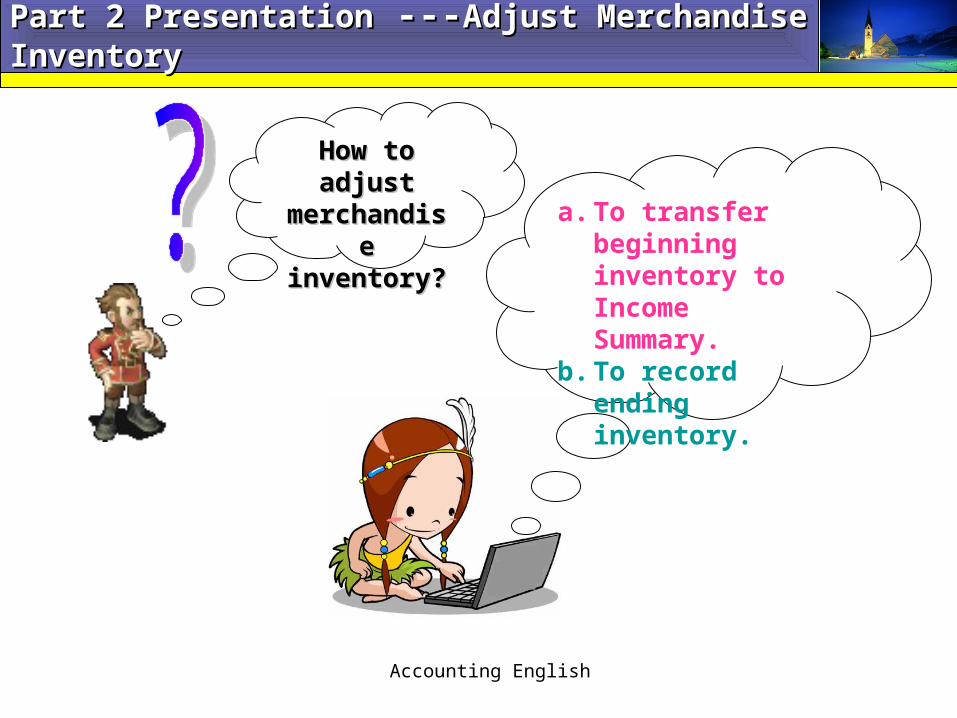

Part 2 PresentationPart 2 Presentation --- ---Adjust Merchandise InventoryAdjust Merchandise Inventory

How to How to adjust adjust

merchandise merchandise inventory?inventory?

a. To transfer beginning inventory to Income Summary.

b. To record ending inventory.

Accounting English

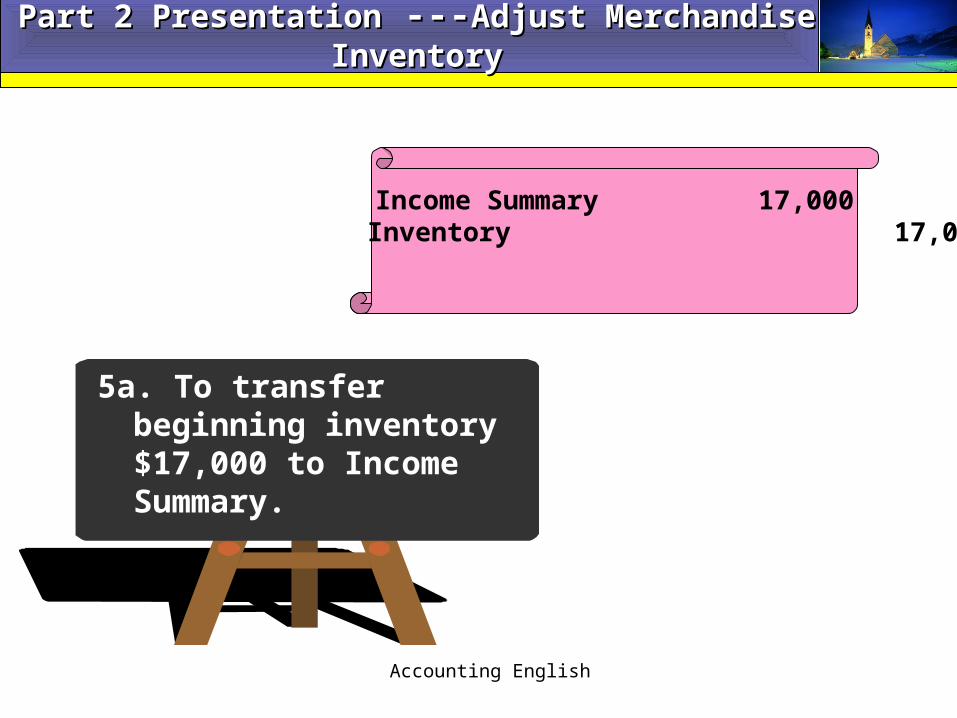

Part 2 PresentationPart 2 Presentation --- ---Adjust Merchandise InventoryAdjust Merchandise Inventory

5a. To transfer beginning inventory $17,000 to Income Summary.

Income Summary 17,000 Inventory 17,000

Accounting English

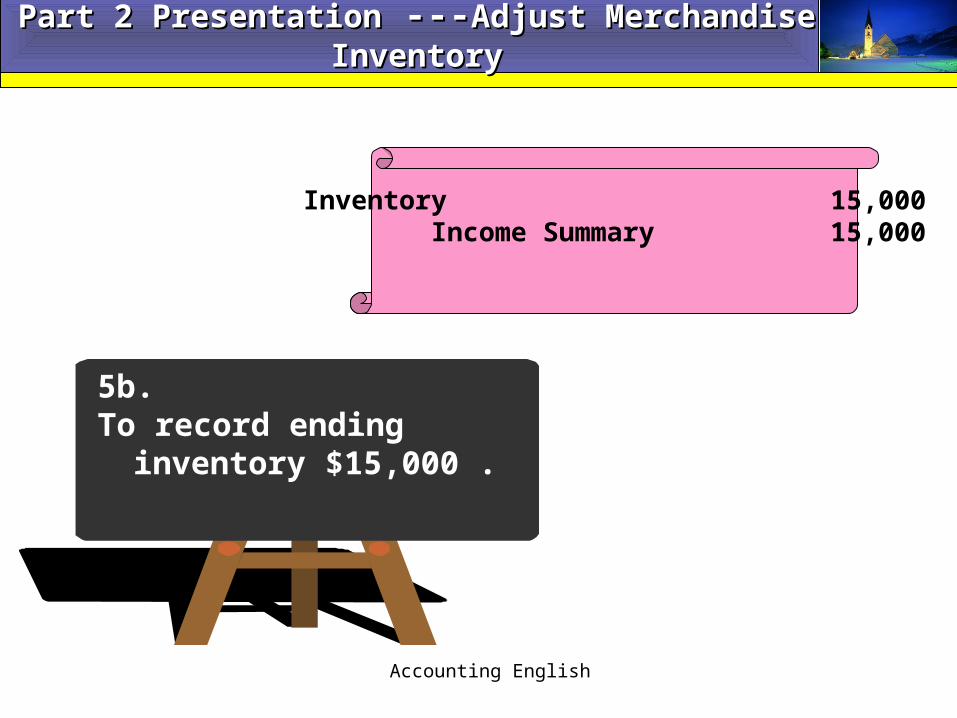

Part 2 PresentationPart 2 Presentation --- ---Adjust Merchandise InventoryAdjust Merchandise Inventory

5b. To record ending inventory

$15,000 .

Inventory 15,000 Income Summary 15,000

Accounting English

Many of business transaction affect the net income of more than one period, therefore, it is often necessary to adjust some account balances at the end of each accounting period in order to achieve proper matching of costs and n order to achieve proper matching of costs and expenses with the relative revenue earned to determine a expenses with the relative revenue earned to determine a meaningful net income figure fore each accounting period. meaningful net income figure fore each accounting period.

Part 3 ExercisesPart 3 Exercises

a. Why is the adjusting step of the accounting cycle necessary ?

Accounting English

It occurs after the journals have been posted It occurs after the journals have been posted and a trial balance of ledger accounts has and a trial balance of ledger accounts has been taken, but before financial statements been taken, but before financial statements are prepared.are prepared.

Part 3 ExercisesPart 3 Exercises

b. When does the adjusting step occur?

Accounting English

• Under accrual basis: revenues are recognized when earned; expenses are recognized when goods and services are used.

• Under cash basis: revenues are recognized when cash is collected; expenses are recognized when cash is paid for the goods and services.

Part 3 ExercisesPart 3 Exercises

c. How do the accrual basis and cash basis of accounting differ?

Accounting English

The four types of adjustments are:

(1) Apportioning recorded costs to periods benefited.

(2) Apportioning recorded revenue to periods in which it is earned.

(3) Accruing unrecorded expenses

(4) Accruing unrecorded revenue

Part 3 ExercisesPart 3 Exercises

d. What four different types of adjustments are frequently

needed at the end of an accounting period?

Accounting English

• (1) To transfer beginning inventory to Income Summary account.

• (2) To record ending inventory.

Part 3 ExercisesPart 3 Exercises

e. How to describe the adjusting procedure for merchandise inventory records under a

periodic inventory system?

Accounting English

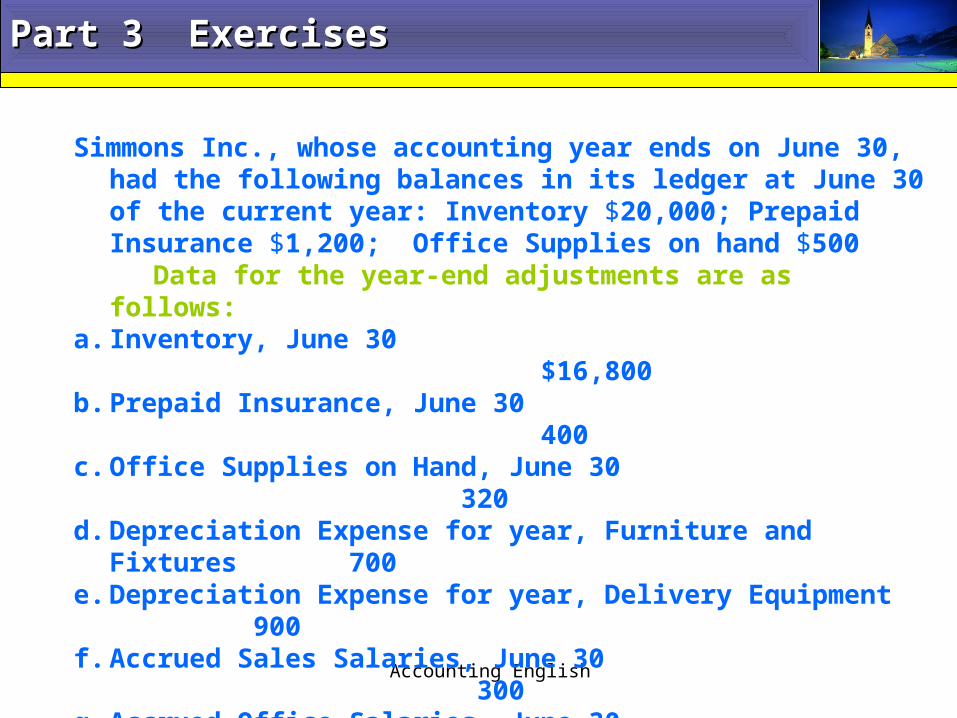

Simmons Inc., whose accounting year ends on June 30, had the following balances in its ledger at June 30 of the current year: Inventory $20,000; Prepaid Insurance $1,200; Office Supplies on hand $500

Data for the year-end adjustments are as follows:a. Inventory, June 30 $16,800b. Prepaid Insurance, June 30 400 c. Office Supplies on Hand, June 30 320d. Depreciation Expense for year, Furniture and Fixtures 700e. Depreciation Expense for year, Delivery Equipment 900f. Accrued Sales Salaries, June 30 300g. Accrued Office Salaries, June 30 200 Require :Make the necessary adjusting entries in the general journal.

Part 3 ExercisesPart 3 Exercises

Accounting English

Part 4 SummaryPart 4 Summary

a. It is necessary to adjust some accounts balances in order to achieve proper matching in order to achieve proper matching of costs and expenses with the relative of costs and expenses with the relative revenue earned to determine a meaningful net revenue earned to determine a meaningful net income figure for each accounting period .income figure for each accounting period .b. The adjusting step occurs after the journals occurs after the journals have been posted and a trial balance of ledger have been posted and a trial balance of ledger accounts has been taken, but before financial accounts has been taken, but before financial statements are prepared.statements are prepared.

Accounting English

Part 4 SummaryPart 4 Summary

c. The four different types of adjustments frequently needed at the end of an accounting period are:

1.Apportioning recorded costs to periods benefited. 2.Apportioning recorded revenue to periods in which it

is earned. 3.Accruing unrecorded expenses 4.Accruing unrecorded revenued.d. The adjusting procedure for merchandise inventory

records under a periodic inventory system are: 1.To transfer beginning inventory to Income Summary

account. 2.To record ending inventory.

Accounting English

HomeworkHomework

P69. 6