accelerating growth - kinh do corporation · 44 corporate strategy. audited report 83 general...

TRANSCRIPT

ACCELERATING

GROWTH

ANNUALREPORT 2014

Establishing foundation

Introduction

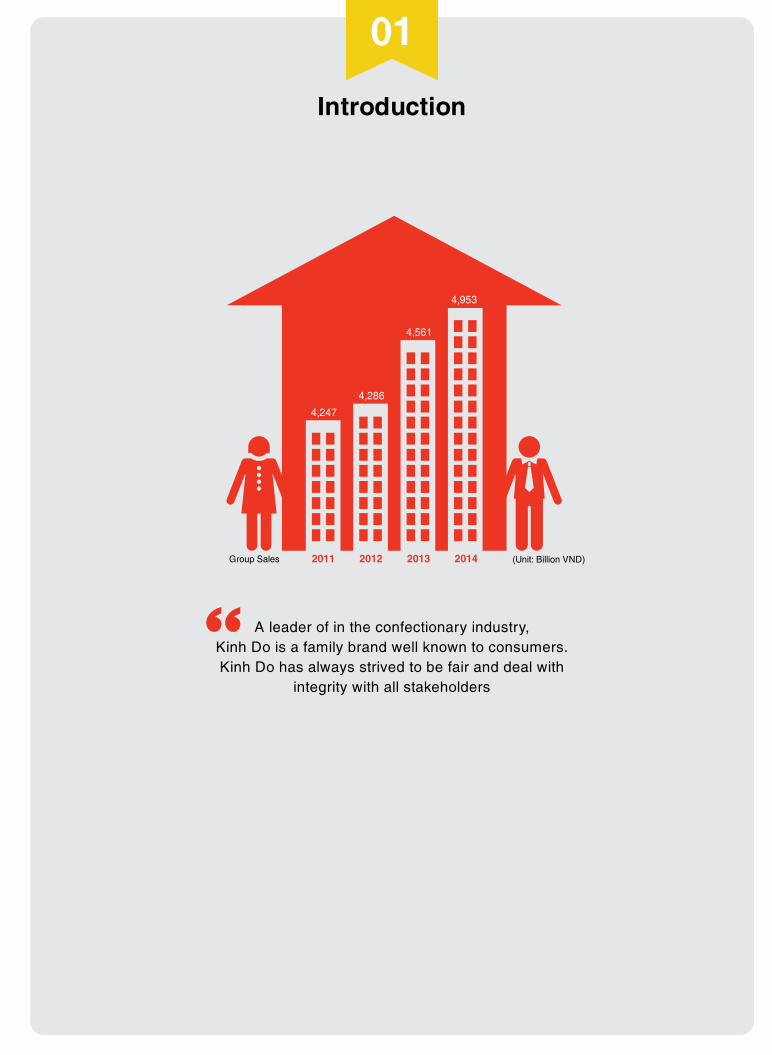

A leader of in the confectionary industry, Kinh Do is a family brand well known to consumers. Kinh Do has always strived to be fair and deal with

integrity with all stakeholders

01

2011 2012 2013 2014

4,247

4,953

4,561

4,286

Group Sales (Unit: Billion VND)

Strategy

In 2014, Kinh Do refocused its commitment to expand it’s addressable market to 50 million consumers

through diversification of our product portfolio.

02

7:30 AM 10:30 AM

7:00 PM9:00 PM

Innovative transition

50 millioncustomers

04-25Contents

26-51

IntroductIon

06 2014 In Brief08 Performance Highlights06 Vision - Mission 12 Our Leadership Board of Directors 17 Executive Management Committee 20 Supervisory Board 22 Related Transactions24 List of Subsidiaries and Related Parties

Strategy

28 Chairman’s Message 32 CEO’s Message 36 Key Performance Indicators 38 Business Model 40 Strategic Orientation 44 Corporate Strategy

audIted report

83 General Information 85 Report of Management 86 Independent Auditors’ Report 88 Consolidated Balance Sheet 90 Consolidated Income Statement 91 Consolidated Cash flow Statement 93 Notes to The Consolidated Financial Statements

governance

64 Corporate Governance Structure 74 Key Risk Factors 76 Corporate Social Responsibility

Leveraging the strength of our distribution network, Kinh Do has targeted the entry into

new categories including instant noodles, cooking oils, condiments, ice cream and milk.

The goal is to meet daily needs of the Vietnamese consumers.

21 years

LEADING POSITION in confectionery industry

Business Review

03

Diversify categories Creating brands

Governance

Kinh Do is a company with a long history and development. To sustain the future growth and expansion, we have targeted to operate with a

clear corporate governance structure that facilitates transparency and accountability.

04

WIN M&A

80 %

Expanding reach

Audited Report

05

Kinh Do's export markets

35 countries

Increasing our target markets through partnerships and alliances with the goal

of having our products reach the world.

52-61 62-79 80-133

BuSIneSS revIew

54 Financial Highlights 56 Market Overview 58 Group Results 60 KDC Share Price & Statistics

Establishing foundation

Introduction

A leader of in the confectionary industry, Kinh Do is a family brand well known to consumers. Kinh Do has always strived to be fair and deal with

integrity with all stakeholders

01

2011 2012 2013 2014

4,247

4,953

4,561

4,286

Group Sales (Unit: Billion VND)

Establishing foundation

Introduction

A leader of in the confectionary industry, Kinh Do is a family brand well known to consumers. Kinh Do has always strived to be fair and deal with

integrity with all stakeholders

01

2011 2012 2013 2014

4,247

4,953

4,561

4,286

Group Sales (Unit: Billion VND)

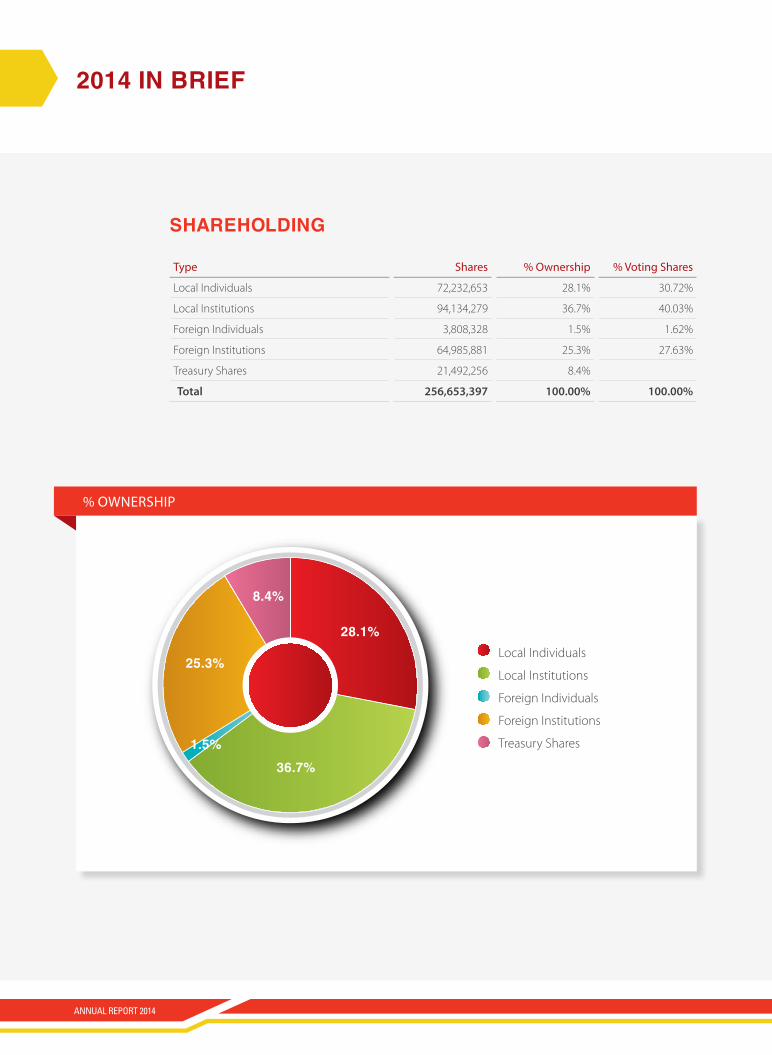

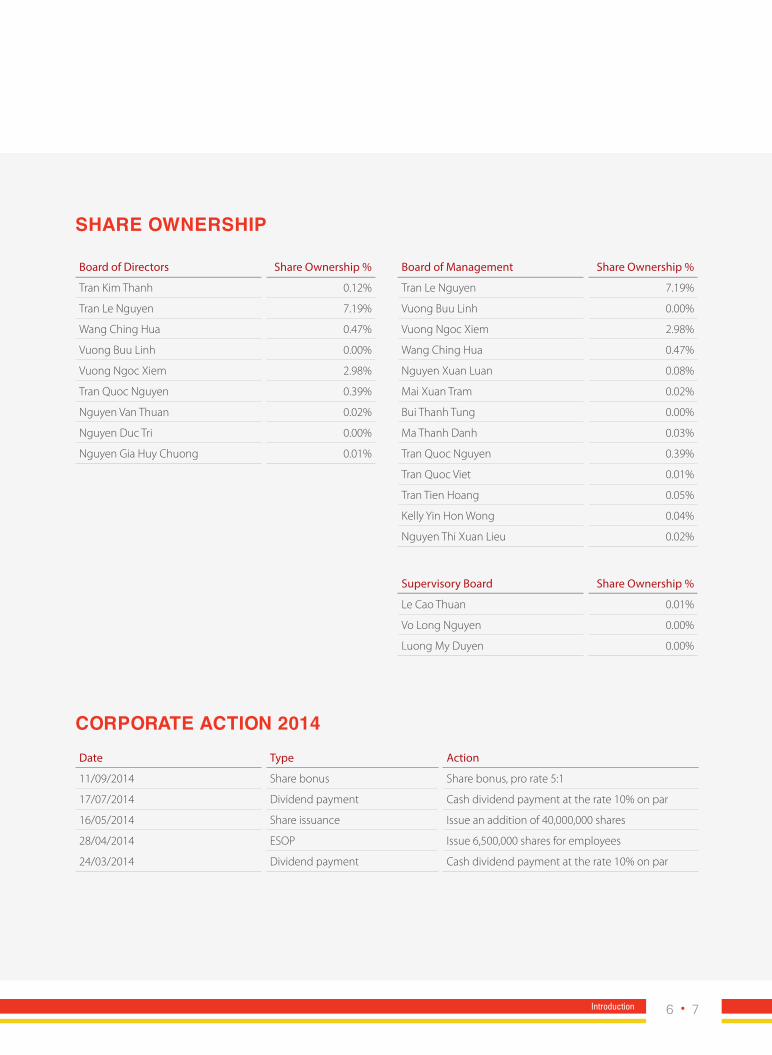

2014 In BrIef

Type Shares % Ownership % Voting Shares

Local Individuals 72,232,653 28.1% 30.72%

Local Institutions 94,134,279 36.7% 40.03%

Foreign Individuals 3,808,328 1.5% 1.62%

Foreign Institutions 64,985,881 25.3% 27.63%

Treasury Shares 21,492,256 8.4%

Total 256,653,397 100.00% 100.00%

ShareholdIng

28.1%

36.7%1.5%

25.3%Local Individuals

Local Institutions

Foreign Individuals

Foreign Institutions

Treasury Shares

% OwnerShip

8.4%

ANNUAL REPORT 2014

Board of Directors Share Ownership %

Tran Kim Thanh 0.12%

Tran Le Nguyen 7.19%

Wang Ching Hua 0.47%

Vuong Buu Linh 0.00%

Vuong Ngoc Xiem 2.98%

Tran Quoc Nguyen 0.39%

Nguyen Van Thuan 0.02%

Nguyen Duc Tri 0.00%

Nguyen Gia Huy Chuong 0.01%

Board of Management Share Ownership %

Tran Le Nguyen 7.19%

Vuong Buu Linh 0.00%

Vuong Ngoc Xiem 2.98%

Wang Ching Hua 0.47%

Nguyen Xuan Luan 0.08%

Mai Xuan Tram 0.02%

Bui Thanh Tung 0.00%

Ma Thanh Danh 0.03%

Tran Quoc Nguyen 0.39%

Tran Quoc Viet 0.01%

Tran Tien Hoang 0.05%

Kelly Yin Hon Wong 0.04%

Nguyen Thi Xuan Lieu 0.02%

Supervisory Board Share Ownership %

Le Cao Thuan 0.01%

Vo Long Nguyen 0.00%

Luong My Duyen 0.00%

corporate actIon 2014

Share ownerShIp

Date Type Action

11/09/2014 Share bonus Share bonus, pro rate 5:1

17/07/2014 Dividend payment Cash dividend payment at the rate 10% on par

16/05/2014 Share issuance Issue an addition of 40,000,000 shares

28/04/2014 ESOP Issue 6,500,000 shares for employees

24/03/2014 Dividend payment Cash dividend payment at the rate 10% on par

6 7Introduction

performance hIghlIghtS

group SaleS (VND billion)

return on equIty (%)

groSS profIt (VND billion)

return on aSSetS (%)

profIt Before taX (VND billion)

groSS profIt margIn (%)

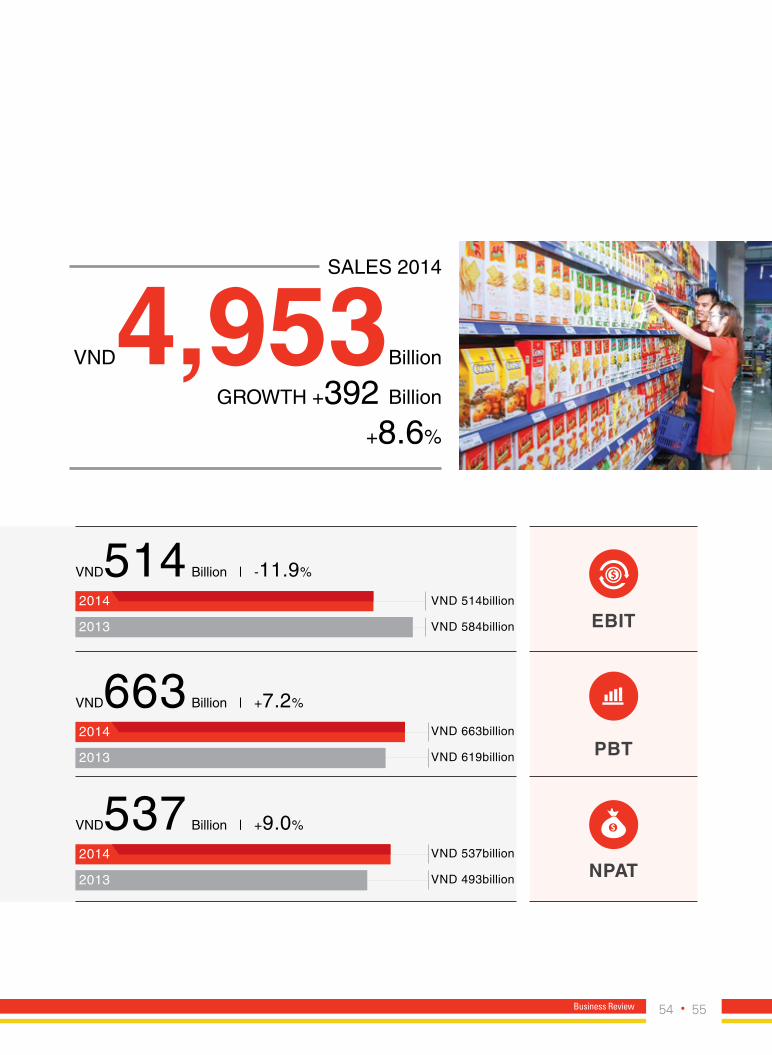

4,953VND4,953billion

group SaleS In 2014

2014

2014

2014

2014

2014

2014

4,953

8.54

2,146

6.82

663

43.33

4,561

10.09

1,976

7.73

619

43.33

2013

2013

2013

2013

2013

2013

+8.60%

-155 basis points

-91 basis points

+8.59% +7.17%

ANNUAL REPORT 2014

2,146dIvIdendS (VND billion)

deBt equIty ratIo (x)

earnIngS per Share (VND)

current ratIo (x)

free caSh flowS (VND billion)

net caSh (VND billion)

VND2,146billion

groSS profIt In 2014

2014

2014

2014

2014

379

0.25

2,296

2.82

318

0.31

2,542

2.54

2013

2013

2013

2013

+19.2% -9.67%

2014

2,4671,958

2013

+26%

2014

5091,129

2013

-54.89%

8 9Introduction

vISIon - mISSIon

vISIon

flavor your lIfe Kinh Do creates life’s flavor through wholesome,healthy, nutritious and convenient foods.

8:00 am

10:30 am

1:30 pm6:30 pm

8:30 pm

ANNUAL REPORT 2014

mISSIon

our conSumer mISSIonIs to identify and produce affordable staple and packaged foods, snacks, bakery products, beverages and juices, confectioneries and condiments, instant foods, processed meats and health supplements that are appealing. Our products are pioneering market-leading, hygienic, healthy, satisfying and conveniently available to all consumers.

our Shareholder mISSIonIs to maximize investment returns over the long-term and to manage risks in order to give certainty and confidence that investments in our business can achieve our shareholder’s goals.

our partner mISSIonIs to create sustainable value for supply chain partners through the creation of innovative food products, which address consumer demand trends and satisfy or exceed consumer expectations; and provide equitable returns for all.

our people mISSIonIs to nurture and develop the skills and abilities of our people to meet the professional demands of their work and satisfy their personal needs. The aim is to create a dynamic, creative, innovative and dependable community within the company.

our communIty mISSIonIs to contribute to the communities in which we operate through sponsorship programs.

10 11Introduction

ANNUAL REPORT 2014

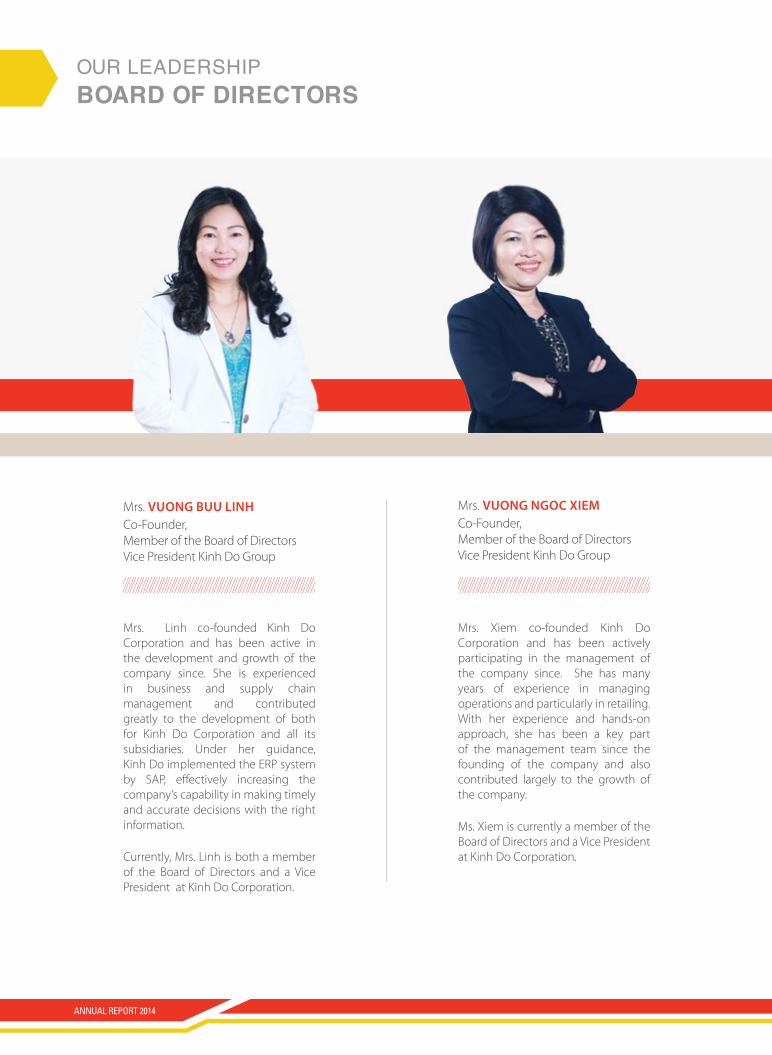

Our LeaDership Board of dIrectorS

Founder, Chairman of the Board of Directors of Kinh Do Group

Co-Founder, Vice Chairman of the Board of Directors, CEO of Kinh Do Group

A veteran entrepreneur with a lifetime of experience in management and business, he is the right combination of boldness in driving the company and caution in managing risk. Under his leadership, Kinh Do has grown from a small family business to become Vietnam’s number one confectionary company. His acute business sense led to the successful turnaround of Wall’s ice-cream business to become the country’s number one single serve ice cream company. Mr. Thanh’s leadership strategy for Kinh Do Corporation is to create the best company, consisting of the best people built around the best processes. Mr. Thanh is currently the Chairman of the Board for Kinh Do Corporation and sits on various boards of other large Vietnamese corporations; helping to contribute to the growth and development of the country. He is a Member of the Central Committee of the Vietnam Homeland Front. He has received several awards and accolades from both the central and local Government of Vietnam for his significant contributions to the socio-economic developments of the country. Mr. Thanh is the founder of Kinh Do Corporation.

An experienced entrepreneur with a track record of building large and profitable businesses over the last few decades, Mr. Nguyen has been instrumental in the development of Kinh Do Corporation. Under his management, Kinh Do has emerged as one of the most well-known brands in Vietnam in addition to a broad portfolio of market dominating products that are the best in their categories. Mr. Nguyen successfully initiated and engineered the acquisition of the Wall’s ice cream factory and who spear-headed the development of the market for ice cream and built the business as it is today. Mr. Nguyen serves concurrently as both the Vice-Chairman of the Board and the CEO of Kinh Do Corporation. He is an active member of the board of directors for the Vietnam Chamber Commerce and Industry (VCCI) and participates on the board of several prominent companies in Vietnam. Mr. Nguyen is a co-founder of Kinh Do Corporation.

Mr. Tran Kim Thanh Mr. Tran Le nguyen

12 13Introduction

Mrs. Xiem co-founded Kinh Do Corporation and has been actively participating in the management of the company since. She has many years of experience in managing operations and particularly in retailing. With her experience and hands-on approach, she has been a key part of the management team since the founding of the company and also contributed largely to the growth of the company.

Ms. Xiem is currently a member of the Board of Directors and a Vice President at Kinh Do Corporation.

Co-Founder, Member of the Board of Directors Vice President Kinh Do Group

Mrs. Vuong ngoc Xiem

Mrs. Linh co-founded Kinh Do Corporation and has been active in the development and growth of the company since. She is experienced in business and supply chain management and contributed greatly to the development of both for Kinh Do Corporation and all its subsidiaries. Under her guidance, Kinh Do implemented the ERP system by SAP, effectively increasing the company’s capability in making timely and accurate decisions with the right information.

Currently, Mrs. Linh is both a member of the Board of Directors and a Vice President at Kinh Do Corporation.

Co-Founder, Member of the Board of Directors Vice President Kinh Do Group

Mrs. Vuong Buu Linh

Our LeaDership Board of dIrectorS

ANNUAL REPORT 2014

Mr. Wang has over 21 years of experience in the food manufacturing and processing industry, and was one of the original founders that helped to set up Kinh Do Corporation’s manufacturing operations.

He has since been instrumental in helping to develop and scale Kinh Do Corporation’s manufacturing foot print in Vietnam. He is a member of the Board of Directors and a Vice President at Kinh Do Corporation.

Co-Founder, Member of the Board of Directors Vice President Kinh Do Group

Member of the Board of Directors of Kinh Do Group, General Director of KI DO Corporation

Mr. Wang ching hua

Mr. Nguyen has over 18 years of experience managing various member companies within Kinh Do Corporation. He has held several key senior management positions including General Manager, Board Member and Vice President at both the group and subsidiary level.

He is currently a member of the Board of Directors at Kinh Do, Vice President of Kinh Do Corporation and the General Manager of the Kido Ice Cream Company.

Mr. Tran Quoc nguyen

14 15Introduction

Member of the Board of Directors of Kinh Do Group

Mr Tri was voted into the Board of Directors of Kinh Do since 2013. He holds a Phd in Business Management at Nanyang Technological University – Singapore.

He has been working for a sugar company under Agricultural Ministry and teach at Trident University (California, US), Faculty of Economics – Risho University (Tokyo, Japan), Ho Chi Minh Economic University, and other joint programs in Vietnam.

Mr. nguyen Duc TriMember of the Board of Directorsof Kinh Do Group

Member of the Board of Directors of Kinh Do Group

Mr. Thuan is a Member of the Board of Directors of Kinh Do Corporation. He has a Doctorate in economics, and is currently the Dean of Finance – Banking Department at Ho Chi Minh City Open University. He has over 30 years’ of experience as a lecturer in the field of banking and finance.

Besides his academic works at Ho Chi Minh Open University, he is also a financial consultant and advisor for many companies and foreign organizations operating in Vietnam.

Mr. nguyen Van Thuan

Mr. Chuong was voted into the Board of Directors of Kinh Do since 2013. He holds a Master of Law at Law University of Bristol (UK), specialized in International Commercial Law.

He is currently the consultant lawyer at Luat Viet lawyer office and a General Director/Managing Lawyer of Phuoc & Co. Office.

Mr. nguyen gia huy chuong

Our LeaDership Board of dIrectorS

ANNUAL REPORT 2014

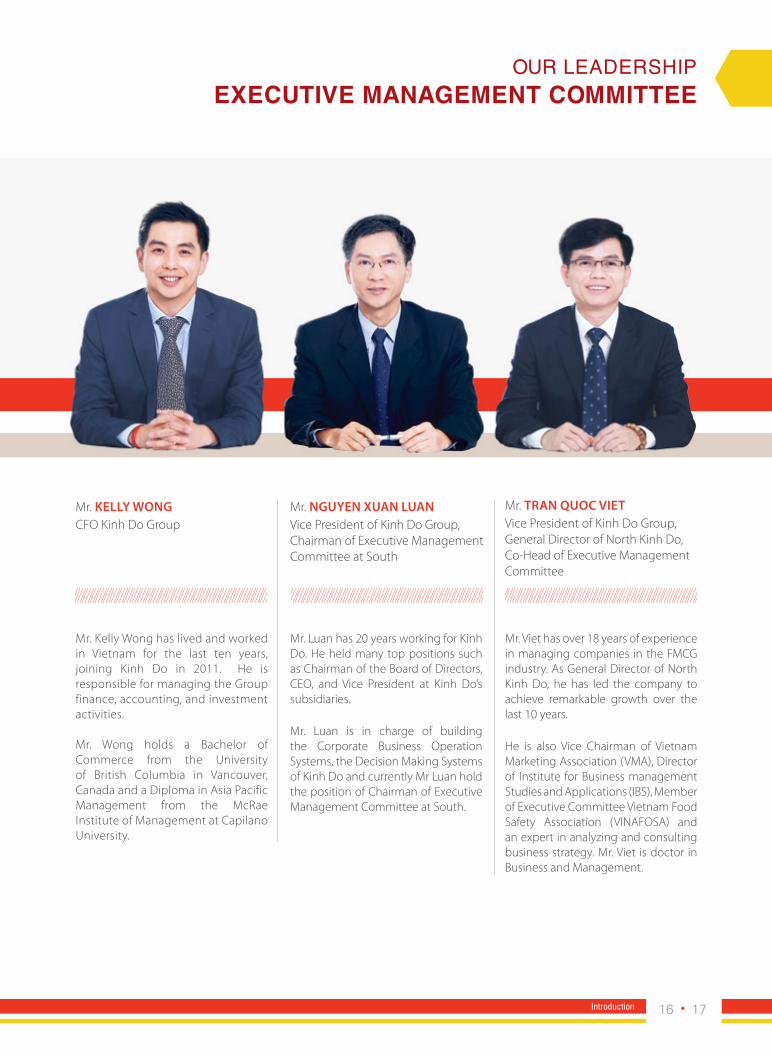

Our LeaDership eXecutIve management commIttee

Mr. Viet has over 18 years of experience in managing companies in the FMCG industry. As General Director of North Kinh Do, he has led the company to achieve remarkable growth over the last 10 years.

He is also Vice Chairman of Vietnam Marketing Association (VMA), Director of Institute for Business management Studies and Applications (IBS), Member of Executive Committee Vietnam Food Safety Association (VINAFOSA) and an expert in analyzing and consulting business strategy. Mr. Viet is doctor in Business and Management.

Vice President of Kinh Do Group, General Director of North Kinh Do, Co-Head of Executive Management Committee

Mr. Tran Quoc VieT

Mr. Kelly Wong has lived and worked in Vietnam for the last ten years, joining Kinh Do in 2011. He is responsible for managing the Group finance, accounting, and investment activities.

Mr. Wong holds a Bachelor of Commerce from the University of British Columbia in Vancouver, Canada and a Diploma in Asia Pacific Management from the McRae Institute of Management at Capilano University.

CFO Kinh Do GroupMr. KeLLy Wong

Mr. Luan has 20 years working for Kinh Do. He held many top positions such as Chairman of the Board of Directors, CEO, and Vice President at Kinh Do’s subsidiaries.

Mr. Luan is in charge of building the Corporate Business Operation Systems, the Decision Making Systems of Kinh Do and currently Mr Luan hold the position of Chairman of Executive Management Committee at South.

Vice President of Kinh Do Group, Chairman of Executive ManagementCommittee at South

Mr. nguyen Xuan Luan

16 17Introduction

Our LeaDership eXecutIve management commIttee

Mr. Hoang has over 18 years of experience in procurement management in the FMCG industry. He was appointed to Director of Supply Chain at Kinh Do Corporation in 2011. He currently leads the company’s COST TEAM and plays a significant role in developing the order management strategy for the entire group.

He holds a Bachelor of Economics from the University of Economics and Higher Leadership Skill Certificate from UCLA Anderson (Los Angeles, USA).

Director of Kinh Do GroupMr. Tran Tien hoang

Mr. Tung has over 17 years experience in manufacturing management and with in-depth knowledge on the SBU operating model. He is currently a SBU Director and Head of the Labor Union for Kinh Do Corporation.

He holds a degree from the University of Economics with a specialization in Business Administration.

Director of Kinh Do GroupMr. Bui Thanh Tung

Mr. Tram was among the first of the management team to help lay the foundation of the current group distribution system. He has been with Kinh Do since the early days and has developed a deep understanding of the company, its competitive environment and the Vietnamese market.

He holds an MBA from California Miramar University in the US.

Director of Kinh Do GroupMr. mai Xuan Tram

ANNUAL REPORT 2014

Mrs. Nguyen Thi Xuan Lieu graduated with Honors from the Ho Chi Minh City University of Economics in 1981. She has over 30 years of working experiences in the finance and banking sector, with almost 20 years holding key position in credit management, banking, and finance in one of the most prestigious banks of Vietnam - Vietnam Bank for Industry and Trade.

She has successfully completed the PhD thesis at Ho Chi Minh City University of Economics and was honored with the Certificate of Merit from the Prime Minister in 2010, 3rd rank Labour Medal of Merit in 2012 and many others. She will focus on post-investment integration and value creation of KDC’s strategic investments.

Director of Kinh Do GroupMrs. nguyen Thi Xuan Lieu

Mr. Danh holds a Bachelor’s of Science (B.Sc) in electrical engineering, Degree in Business Administration from the University of Economics and a Masters of Business Administration with a focus in International Business Strategy and Brand Management from Belgium.

He has over ten years of experience in financial management, business strategy and brand management consultancy and advisory in mergers and acquisitions. He is now in charge of the Internal Control department of the whole Group.

Director of Kinh Do GroupMr. ma Thanh Danh

18 19Introduction

Ms. Duyen has been working for Kinh Do since 1993 and has held several key positions, including Accountant, Deputy Manager of the Accounting Department at Kinh Do and Chief Accountant Kinh Do. Since 2006 Mrs. Duyen has been the Chief Accountant at Kinh Do Real Estate Joint Stock Company.

She holds a degree in Finance and Accounting and has spent her career at Kind Do Corporation.

Member of the Supervisory BoardMrs. Luong my Duyen

Mr. Nguyen holds a Bachelor of Economics with a specialization in Business Administration. He is a certified Fund Manager with a certificate issued by the State Securities Commission of Vietnam.

He was one of first brokers of the OTC market Vietnam and has over 11 years of investment experience.

Member of the Supervisory BoardMr. Vo Long nguyen

Mr. Thuan was one of the first pioneers who helped to successfully establish North Kinh Do Company and played an important role in building the company to what it is today.

Mr. Thuan graduated with an MBA and as the valedictorian at Benedictine University - USA, he also holds a Bachelor of Accounting and Audit from the University of Economics and a Bachelor of Computer and Mathematics Applications from Polytechnic University. Currently, he is the Finance Director of North Kinh Do and Head of the Supervisory Board at Kinh Do Corporation.

Head of the Supervisory Board Mr. Le cao Thuan

Our LeaDership SupervISory Board

ANNUAL REPORT 2014

20 21Introduction

tranSactIon of InSIderS

related tranSactIonS

no. name relationshipShares Owned at

BeginningShares Owned at

ending ActionAmount % Amount %

1 Ezaki Glico Strategic Shareholder 16.800.000 10.1% 8.400.000 5.1%Structure investment portfolio

2 Viet Nam Investment Property Holding LTD

Major Shareholder 7.625.921 4.6% 5,378,226 2.1%Structure investment portfolio

3 Windstar Resouces Limited Major Shareholder 238,410 0.1% - 0.0%Structure investment portfolio

4 Tran Kim Thanh Internal Shareholder 130,000 0.1% 276,000 0.1% Buy + share bonus

5 Vuong Buu Linh Major Shareholder 80,000 0.0% 168,000 0.1% Buy + share bonus

6 Tran Le Nguyen Major Shareholder 13,888,748 6.7% 16,906,497 7.19% Buy + share bonus

7 Vuong Ngoc Xiem Major Shareholder 5,777,003 2.8% 7,004,403 2.7% Buy + share bonus

8 Tran Quoc Nguyen Major Shareholder 565,366 0.3% 913,207 0.4% Buy + share bonus

9 Wang Ching Hua Major Shareholder 862,611 0.4% 1,107,133 0.4% Buy + share bonus

10 Nguyen Gia Huy Chuong Major Shareholder - 0.0% 10,000 0.0% Buy + share bonus

11 Nguyen Duc Tri Major Shareholder - 0.0% 10,000 0.0% Buy + share bonus

12 Nguyen Van Thuan Major Shareholder 20,683 0.0% 35,683 0.0% Buy + share bonus

13 Nguyen Xuan Luan Major Shareholder 135,000 0.1% 192,000 0.1%Buy +Sell + Share Bonus

14 Bui Thanh Tung Major Shareholder 73,000 0.0% 45,000 0.0%Buy +Sell + Share Bonus

15 Mai Xuan Tram Major Shareholder 72,506 0.0% 45,007 0.0%Buy +Sell + Share Bonus

16 Tran Quoc Viet Major Shareholder 50,273 0.0% 80,327 0.0%Buy +Sell + Share Bonus

17 Tran Tien Hoang Major Shareholder 150,000 0.1% 114,000 0.0% Buy + share bonus

18 Ma Thanh Danh Major Shareholder 8,159 0.0% 63,790 0.0% Buy + share bonus

19 Kelly Yin Hon Wong Major Shareholder 30,000 0.0% 87,480 0.0%Buy +Sell + Share Bonus

20 Le Cao Thuan Major Shareholder 3,505 0.0% 28,206 0.0% Buy + share bonus

21 Luong My Duyen Major Shareholder 6,009 0.0% 12,010 0.0%Buy +Sell + Share Bonus

22 Vo Long Nguyen Major Shareholder 7,750 0.0% 21,300 0.0% Buy + share bonus

23 Nguyen Thi Oanh Major Shareholder 50,000 0.0% 84,000 0.0% Buy + share bonus

ANNUAL REPORT 2014

tranSactIon of related partIeS

no. name relationshipShares Owned at

BeginningShares Owned at

ending ActionAmount % Amount %

1 Tran Vinh Nguyen Tran Kim Thanh 458,941 0.2% 604,729 0.2% Buy + share bonus

2 Vuong Quoc Tru Vuong Buu Linh 3,643,572 1.7% 4,456,286 1.7% Buy + share bonus

3 Vuong Buu Ngoc Vuong Buu Linh 309,557 0.1% 383,468 0.2% Buy + share bonus

4 Vuong Ngan Hao Vuong Ngoc Xiem 6,000 0.0% 12,000 0.0% Buy + share bonus

5 Mai Thi Kim Phuong Mai Xuan Tram 549 - 9 0.0% Sell

6 Vuong Thu Binh Vuong Ngoc Xiem 12,500 0.0% 24,000 0.0% Buy +Sell + Share Bonus

7 Vuong Thu Le Vuong Ngoc Xiem 12,007 0.0% 11,008 0.0% Buy +Sell + Share Bonus

8 Vuong Buu Dinh Ma Thanh Danh 205,936 0.1% 271,123 0.1% Buy +Sell + Share Bonus

9 Ngo Phan Anh Dao Tran Tien Hoang 69,334 0.0% 19,204 0.0% Buy +Sell + Share Bonus

10 Nguyen Thi Hong Hanh Le Cao Thuan 3,501 0.0% 30,601 0.0% Buy + share bonus

11 Le Cao Tu Le Cao Thuan - 0.0% 1,800 0.0% Buy + share bonus

22 23Introduction

List Of SuBSIdIarIeS and related partIeS

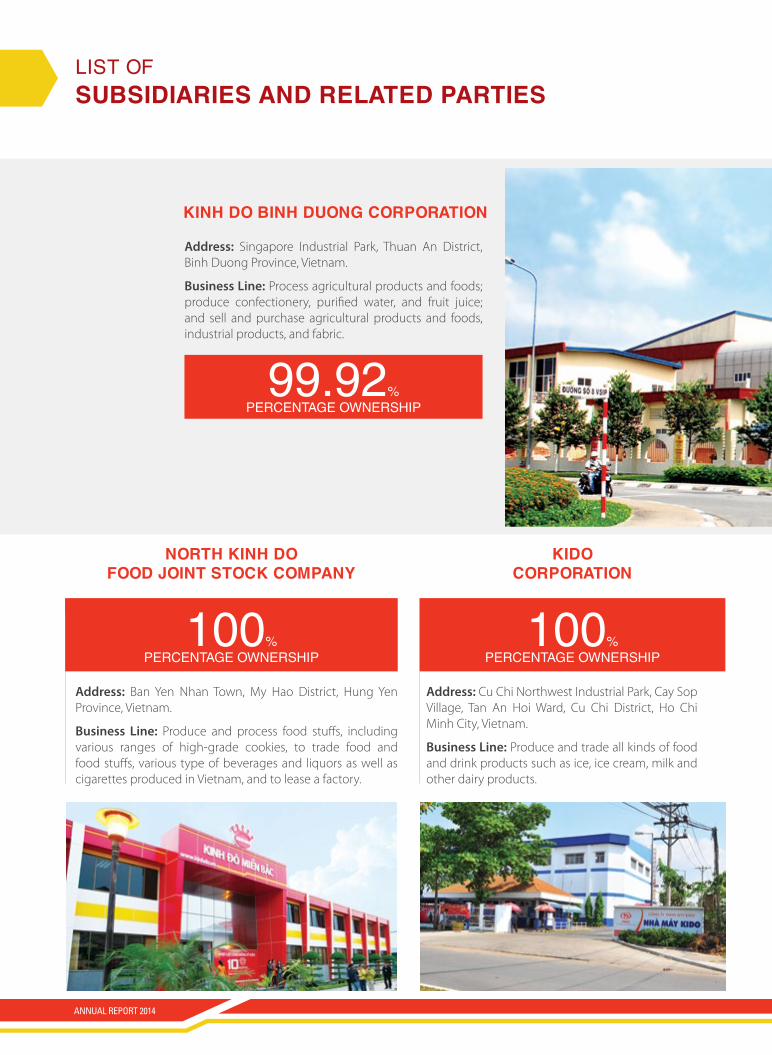

KInh do BInh duong corporatIon

north KInh do food JoInt StocK company

KIdo corporatIon

address: Singapore Industrial Park, Thuan An District, Binh Duong Province, Vietnam.

Business Line: Process agricultural products and foods; produce confectionery, purified water, and fruit juice; and sell and purchase agricultural products and foods, industrial products, and fabric.

address: Ban Yen Nhan Town, My Hao District, Hung Yen Province, Vietnam.

Business Line: Produce and process food stuffs, including various ranges of high-grade cookies, to trade food and food stuffs, various type of beverages and liquors as well as cigarettes produced in Vietnam, and to lease a factory.

address: Cu Chi Northwest Industrial Park, Cay Sop Village, Tan An Hoi Ward, Cu Chi District, Ho Chi Minh City, Vietnam.

Business Line: Produce and trade all kinds of food and drink products such as ice, ice cream, milk and other dairy products.

100% Percentage ownershiP

100% Percentage ownershiP

99.92% Percentage ownershiP

ANNUAL REPORT 2014

vInaBIco confectIonery JoInt StocK company

tan an phuoc company lImIted

lavenue InveStment corporatIon

address: 436 No Trang Long Street, Ward 13, Binh Thanh District, Ho Chi Minh City, Vietnam.

Business Line: Produce and sell confectionery and purified water.

address: 6/134 National Road No. 13, Hiep Binh Phuoc Ward, Thu Duc District, Ho Chi Minh City, Vietnam.

Business Line: Operate in real estate industry.

address: 3rd floor, May Flower Tower, 12 Le Thanh Ton Street, District 1, Ho Chi Minh City, Vietnam.

Business Line: Operate in real estate industry.

100% Percentage ownershiP

80% Percentage ownershiP

50% Percentage ownershiP

24 25Introduction

Strategy

In 2014, Kinh Do refocused its commitment to expand it’s addressable market to 50 million consumers

through diversification of our product portfolio.

02

7:30 AM 10:30 AM

7:00 PM9:00 PM

Innovative transition

50 millioncustomers

Strategy

In 2014, Kinh Do refocused its commitment to expand it’s addressable market to 50 million consumers

through diversification of our product portfolio.

02

7:30 AM 10:30 AM

7:00 PM9:00 PM

Innovative transition

50 millioncustomers

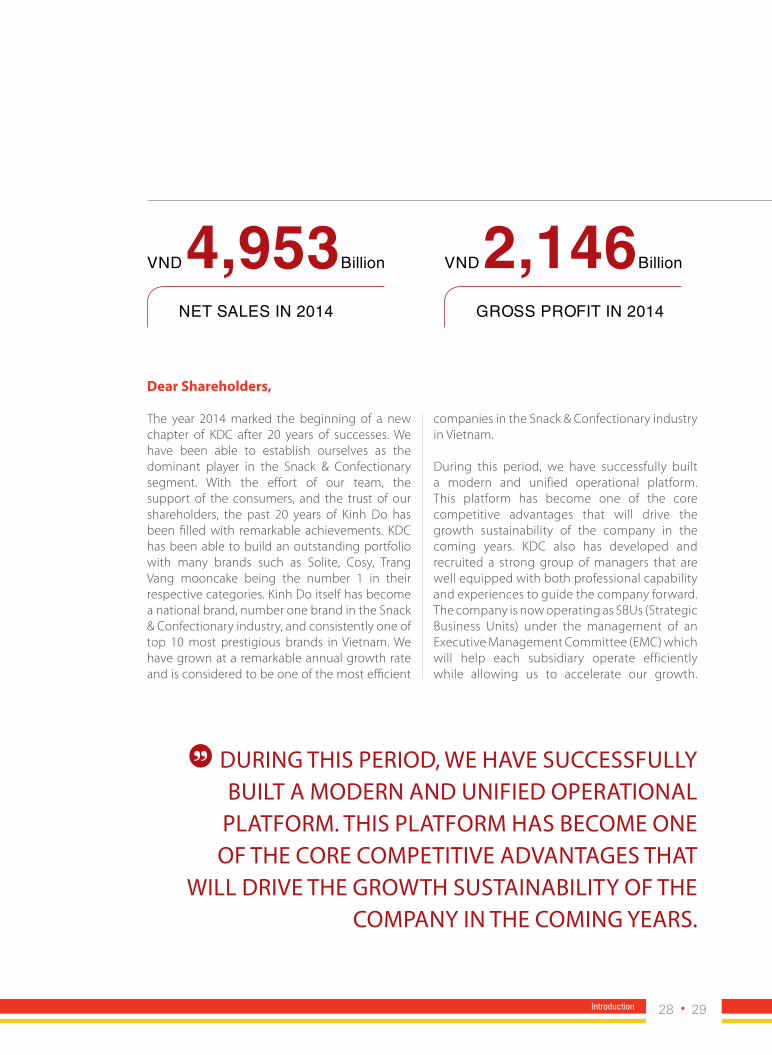

chaIrman’S meSSage

ANNUAL REPORT 2014

Dear Shareholders,

The year 2014 marked the beginning of a new chapter of KDC after 20 years of successes. We have been able to establish ourselves as the dominant player in the Snack & Confectionary segment. With the effort of our team, the support of the consumers, and the trust of our shareholders, the past 20 years of Kinh Do has been filled with remarkable achievements. KDC has been able to build an outstanding portfolio with many brands such as Solite, Cosy, Trang Vang mooncake being the number 1 in their respective categories. Kinh Do itself has become a national brand, number one brand in the Snack & Confectionary industry, and consistently one of top 10 most prestigious brands in Vietnam. We have grown at a remarkable annual growth rate and is considered to be one of the most efficient

companies in the Snack & Confectionary industry in Vietnam.

During this period, we have successfully built a modern and unified operational platform. This platform has become one of the core competitive advantages that will drive the growth sustainability of the company in the coming years. KDC also has developed and recruited a strong group of managers that are well equipped with both professional capability and experiences to guide the company forward. The company is now operating as SBUs (Strategic Business Units) under the management of an Executive Management Committee (EMC) which will help each subsidiary operate efficiently while allowing us to accelerate our growth.

During ThiS periOD, we hAVe SucceSSfully BuilT A MODern AnD unifieD OperATiOnAl

plATfOrM. ThiS plATfOrM hAS BecOMe One Of The cOre cOMpeTiTiVe ADVAnTAgeS ThAT

will DriVe The grOwTh SuSTAinABiliTy Of The cOMpAny in The cOMing yeArS.

VND 4,953Billion

Net saLes iN 2014

VND 2,146Billion

GrOss prOfit iN 2014

28 29Introduction

chaIrman’S meSSage

These factors together will help establish a firm foundation for the next growth phase of KDC.

As Vietnam is participating further into the globalization process, the country is being integrated further into the ASEAN economic group and by the end of this year it will also start to join the free trade pact with the EU. Within this context, KDC needs a breakthrough strategy in order to continue its success. KDC has been in the Snack & Confectionary industry for the past two decades and been considered as one of the pioneers in Vietnam. During this period, KDC has successfully built its reputation as the most renowned name in this industry. However, continued success required KDC to seek growth beyond just the confectionary space. There was a growing need for the company to find a new direction and a new area with a much larger playing field. Hence, a strategy was derived to extract the potentials from the Value Creation process and to re-direct the focus and resources into more larger segments. Make no mistake, KDC will continue to pursue the Food & Flavor strategy but looking at much larger categories and a much bigger space.. We will bring forward a new product portfolio that aims to increase (1) the number of potential consumers, (2) the consumption frequency of each consumer, and (3) reach towards overseas markets.

In order for us to concentrate and redirect our scarce resources to enter into a larger Food and Flavor space, in 2014, KDC made a landmark transaction to transfer a portion of the Snack & Confectionary business to a strategic partner, Mondelēz International. This cooperation will help to accelerate the development of Snack &

Confectionary segment in the future by placing it in the hands of the world’s number one confectionary company and allows us to focus on developing our presence in the much larger Food and Flavor space.

With the strategic orientation of moving toward being a food conglomerate, KDC has undergone a prolonged Transformative Change with our focus being shifted from Value Conversion to Value Creation. This means the consumer is placed at the heart of our entire operational focus. For the next phase, KDC will focus on two strategic goals: (1) developing KDC to become a leading food conglomerate with specialized distribution channels; (2) develop and upgrading our Value Creation process. As the economy continues to develop, the Vietnamese consumers have increasingly more access to a variety of options, and information about products. Hence, in order to succeed, company needs to understand its consumer behavior, it’s changing dynamics and bring appropriate products to meet the specific needs of individual consumer. Recognizing the growing importance of consumer’s behavior in the growth of our company, KDC has set our goals to align our entire operations to ensure that we are able to meet the needs of individual consumers. For the next chapter of growth, our strategy will be centered on 4C’s (Consumer, Category, Country, Channel). The 4C’s is the new corporate strategy, which will help guide us for the coming years. It’s also designed to help us focus on the delivery of product to consumers and dictates the way in which we interact with them. This as we mentioned already is the core element of KDC’s focus during the next phase of development.

ANNUAL REPORT 2014

In addition to the new strategic orientation for the Group, I am pleased to announce that our business has continued to achieve outstanding results. Our business has grown steadily with improved profitability despite a difficult external environment and moderate consumer demand. In addition, KDC has successfully launched the instant noodle product under the “Dai Gia Dinh” brand, marking our first entry into the daily essential space. In the upcoming months, our portfolio will further expand to include cooking oil and condiments. They will serve as the basis to develop and execute the new strategy.

KDC has undergone 21 years of development with tremendous successes. Now, we are once again at the beginning of a new chapter of growth, backed by years of preparation and experience. I truly believe that KDC will continue its success. Looking back at our journey, we would like to thank the commitment, support and cooperation of our shareholders, investors, employees, partners, suppliers, and distributors. We truly could not have enjoyed these successes without all of you. I would like to wish you all great health and success in the upcoming year.

TRAN KIM THANHChairmanKinh Do Group

KDc hAS unDergOne 21 yeArS Of DeVelOpMenT wiTh TreMenDOuS SucceSSeS. nOw, we Are Once AgAin AT

The Beginning Of A new chApTer Of grOwTh, BAcKeD By yeArS Of prepArATiOn AnD experience. i Truly

BelieVe ThAT KDc will cOnTinue iTS SucceSS.

30 31Introduction

ceo’S meSSage

OVerAll, efficiency in Our OperATiOn prOViDeD uS A STrOng MOMenTuM DeSpiTe

unfAVOrABle MAcrO enVirOnMenT AnD MODerATe MArKeT DeMAnD.

ANNUAL REPORT 2014

Dear Shareholders,

Last year, though we have seen economic recovery signals and a more stable GDP growth rate, the overall market was still hindered by moderate demand. However, KDC still achieved an impressive growth rate by concentrating on core business, shifting our operation toward the market, and improving our services to satisfy complex market demand. The year of 2014 also marked a turning point in the execution of our strategic plan.

The year of 2014 was the year KDC continues to dedicate its efforts to Stage 4 of the Transformative Change: Profitable Growth which aimed at achieving profit from sustainable resources. I am glad to announce that KDC has reached the revenue of VND4,953 bn, equivalent to the growth of 8.6% YoY, net profit before tax of VND663bn, increasing by 7.1%YoY. Though operating profit margin remained stable compared to 2013, profit before tax still grew by 7.2% YoY. Net profit after tax also increased by 9.00%, reaching VND537 bn. Return on Equity this year decreased to 8.5% lower than last year level of 10.09%. However, if excluding the equity increased of VND 1,404 bn due to the private share issuance, this year ROE reached 11.0% in line with our commitment to the shareholders. Overall, efficiency in our operation provided us a strong momentum despite unfavorable macro environment and moderate market demand.

To accomplish such outstanding result, I would like to express my gratitude to the commitment, support, and discipline of the entire KDC’s team. I also would like to thank our shareholders, investors, and partners including our suppliers, distributors for your support, and finally and dearly the consumer for the trust and belief in our company and our products.

Last year, the management structure under: Functions working directly with each Strategic Business Units under the monitor and guidance of the Executive Management Committee continues to show its effectiveness in managing an increasingly complex company. Timely management decisions made by EMC in the past year have helped the firm to maximize opportunities while control risks at acceptable level. In addition, KDC’s distribution platform was further strengthened becoming the foundation for our company to enter the daily essential space in the coming period. With over 200 distributors, 160.000 POS and 30.000 cold chains across the country, KDC has become one the best distribution platform in the domestic market. Aside from its scale, the highlight of the platform is the successful implementation of the Distribution Management System (DMS). This system allow us to monitor sales at retail level through mobile devices and set up automatic orders for the distributor. This, in turn, has accelerate our business cycle, the selling and delivery speed while improve the level of our customer services.

Besides, understanding the importance of building and developing brand, we continuously launched a variety of campaigns that aims to increase brand recognition, consumer loyalty, and customer satisfaction. In the year 2014, KDC launched and re-launched a variety of core brands, for instance, Kinh Do Fresh Bun, AFC, Cosy Wafer, Snack, Cookies, Ice-cream and Yoghurt to satisfy the increasingly complex consumers’ demand. Trade marketing activities for core products, especially seasonal product lines like Mid-Autumn and Tet….. were also enhanced. Remarkably, in additional to our premium offering, we recently launched many new product lines that dedicated to the health of consumers while remained affordable.

DiViDeNDs iN 2014

VND 663Billion +7.3%

VND 379Billion +19.2%

prOfit BefOre tax iN 2014

32 33Strategy

fOr The upcOMing chApTer, we wiSh ThAT The ShArehOlDerS, inVeSTOrS, AnD pArTnerS incluDing Our SupplierS, DiSTriBuTOrS will cOnTinue TO cOMMiT AnD SuppOrT uS.

The year 2014 also earmarked our expansion toward Food & Flavor space. This includes products that are consumed daily including meal compliments and meal replacements and can be used multiple times throughout the day. Due to its nature, this space has high coverage and much higher penetration that promises a great potential for revenue and profit growth.

2015 economic outlook remains fairly moderate which will pose challenges to our business. However, there are signs of recovery from the real estate market while CPI index is forecasted to be quite stable. As such, following the 2015 strategic goals of our Chairman, KDC has outlined an execution plan in detail to pursue the strategy, accelerate our company growth rate and create more value to the Shareholders.

ceo’S meSSage

ANNUAL REPORT 2014

In the upcoming years, one of the key success factors for us is the development and efficiency improvements of our distribution channels. The success of the entire organization will depend on our ability to drive the efficiency of individual channel as well as cross channel synergy. Moving forwards, KDC will reorganized into a Food Conglomerate with each subsidiary specializing on one of the following channels: packaged, frozen, retail and export. Currently, KDC has already possessed a strong distribution platform, experienced sales force and high market coverage across the country. Post the transformation, KDC will look to enhance the synergy cross channels to increase overall efficiency. In the longer term, KDC will seek additional opportunities to enter into the regional and global market. In additional to leveraging our low cost base to enter global playground, we will look for opportunities to leverage regional resources to improve our Value Creation process.

Furthermore, the entire category strategy of KDC will be consumer centric. Previously, serving opportunity of our product portfolio was limited within breakfast, afternoon tea, and dessert while missing two important periods: lunch and dinner. In addition, our consumer target age group was limited within 20 to 45 years old. Hence, in the future, we aim to diversify our product portfolio to serve the entire consumer base from urban to rural areas in different age group covering the entire consumer’s daily live. To be specific, after the launch of instant noodles at the end of 2014, we will look to launch premium instant noodles, cooking oil, condiments, and other products in Food & Flavour space.

We have also build a system and process to collect and analyze consumer feedbacks. As such, KDC could understand what products that its customers need, where they want to buy, at which time to use and in turn driving the entire operation base on such information. Hence, we look to develop the Dai Gia Dinh brand to become a brand that is well connected

with Vietnamese families. Endorsed by this brand, more products will be launched to satisfy the needs of different type of consumers in different age group throughout the day.

Even though Food & Flavour is an attractive space, it is also a field with large and experienced players. Thus, in order to prepare our entry, KDC needs a strong foundation that can sustain over the long term. As a result, KDC has restructured its Snack & Confectionary business by entering into a strategic partnership with Mondelēz International. This agreement will accelerate the development of Snack & Confectionary in the future and allow us to focus our resources to enter into Food & Flavour.

Together with establishing a strategic plan and a details execution plan, we have also set up a proactive risk management process. The process will carefully monitor and actively manage potential external and internal risks to assure the execution of business targets each year. To be specific, risks may come from the industry, suppliers, customers, business partner, entrance into new market and consumers’ demand.

For the upcoming chapter, we wish that the shareholders, investors, and partners including our suppliers, distributors will continue to commit and support us. Your trust will become our strength and motivation throughout our journey to accomplish our strategic goals and operating targets. Finally, I would like to wish you all great health and success in the upcoming year.

TRAN LE NGUYENChief Excutive OfficerKinh Do Group

34 35Strategy

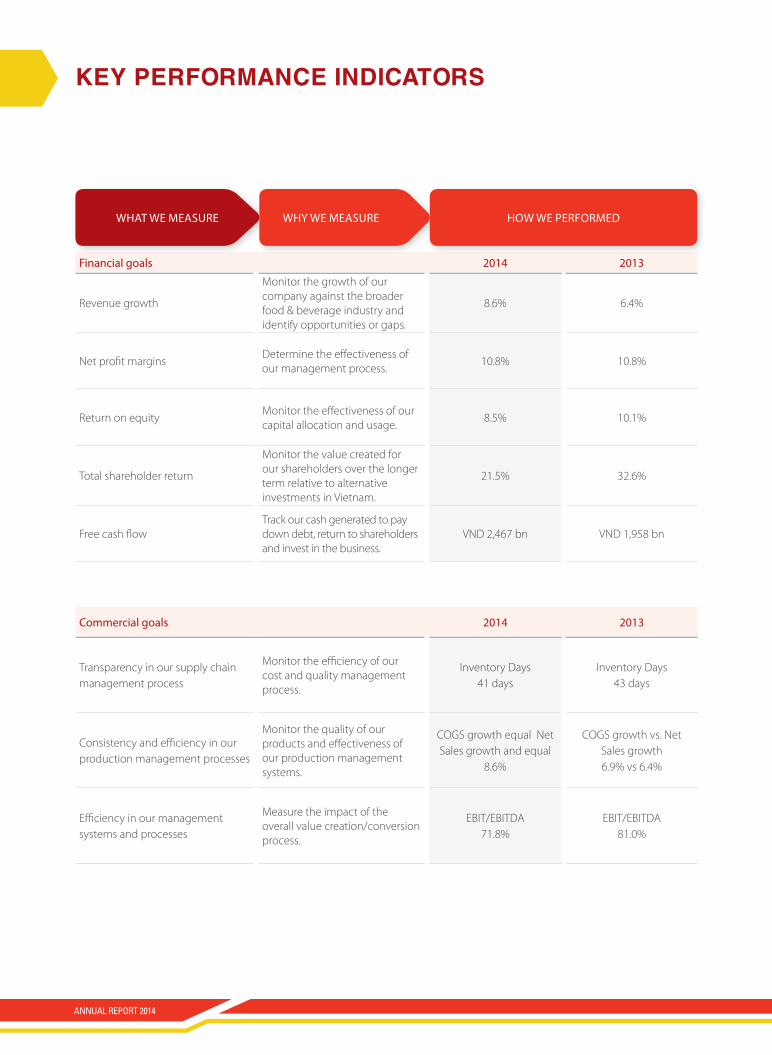

Key performance IndIcatorS

financial goals 2014 2013

Revenue growth

Monitor the growth of our company against the broader food & beverage industry and identify opportunities or gaps.

8.6% 6.4%

Net profit marginsDetermine the effectiveness of our management process.

10.8% 10.8%

Return on equityMonitor the effectiveness of our capital allocation and usage.

8.5% 10.1%

Total shareholder return

Monitor the value created for our shareholders over the longer term relative to alternative investments in Vietnam.

21.5% 32.6%

Free cash flowTrack our cash generated to pay down debt, return to shareholders and invest in the business.

VND 2,467 bn VND 1,958 bn

commercial goals 2014 2013

Transparency in our supply chain management process

Monitor the efficiency of our cost and quality management process.

Inventory Days 41 days

Inventory Days 43 days

Consistency and efficiency in our production management processes

Monitor the quality of our products and effectiveness of our production management systems.

COGS growth equal Net Sales growth and equal

8.6%

COGS growth vs. Net Sales growth6.9% vs 6.4%

Efficiency in our management systems and processes

Measure the impact of the overall value creation/conversion process.

EBIT/EBITDA71.8%

EBIT/EBITDA81.0%

whAT we MeASure why we MeASure hOw we perfOrMeD

ANNUAL REPORT 2014

36 37Strategy

MArKeTing

SAleS fOrcecOnSuMerS

reTAilerS DiSTriBuTOr

MAnufAcTuring

SupplierS

VAlu

e

cOn

VerS

iOn

VAlu

e

creA

TiO

n

Suppliers - Kinh Do is working with over 200 suppliers world-wide to ensure that the best quality materials are sourced for the best price with the objective of having a consistent balance between quality and profitability.

Employees - Kinh Do is working with over 8,000 employees including 4.800 in manufacturing, 1.650 in the distribution system and 1.550 in the growth platform to convert raw materials to product and create value through delivery of products that leverage our marketing and sales knowledge.

Distributors - Reaching through 3 channels to access 161,000 point of sales to deliver products. Connected through our Distributor Management System which allows us to access on a daily basis the inventory and sales volume throughout our channels.

Retailers - Serving over 161,000 point of sales and connected to our platform through our mobility platform to manage the sales execution process at a retailer level.

Consumers - Targeting over 50 million consumers with our range of products through 3 channels in Vietnam.

BuSIneSS model

impaCtiNG

the DaiLy LiVes Of

50 miLLiON CONsumers

ANNUAL REPORT 2014

Our business process is separated into two primary areas, including “Value Conversion” and “Value Creation”. The two distinct parts reflects the primary construct of KDC’s current business and the evolution of our business model over the last 21 years. The traditional process of Value Conversion which KDC was founded upon, relied heavily on pricing power and scale. Competitive advantages were defined by the ability to negotiate large discounts for volume and manufacturing in large enough scale to create price competitiveness. The types of products were not highly differentiated and growth required adding new categories or extension of existing products to expand. The market context was that consumers were not overly concerned with variety and choice but relied heavily on the availability of products to satisfy their needs.

KDC extended business model to include Value Creation fairly early on, which is defined by investing in the process of branding, marketing, selling and distribution. This Value Creation process is much less tangible than Value Conversion (plant and equipment) and has taken a much larger investment in time and money to build. The Value Creation process includes investment in knowledge capital (system and processes), human capital (highly skilled professional managers) and intellectual capital (product brands and reputation). It is also a much more fluid investment which requires a different type of approach in management and is heavily reliant on knowledge capital to keep everything organized. While more complex, Value Creation can be leveraged to create much better returns and accelerate growth; as a result large improvements in our profitability profile.

As the country develops, Vietnamese consumers have also evolved with increasing demands in term of product quality and complexity. This resulting change in consumer behavior has changed KDC’s

AS The cOunTry DeVelOpS, VieTnAMeSe

cOnSuMerS hAVe AlSO eVOlVeD wiTh increASing

DeMAnDS in TerM Of prODucT quAliTy

AnD cOMplexiTy. ThiS reSulTing chAnge in

cOnSuMer BehAViOr hAS chAngeD KDc’S BuSineSS MODel frOM A puSh TO A pull MODel cOnnecTing

uS clOSer TO The cOnSuMer.

business model from a push to a pull model connecting us closer to the consumer. This means that the flow of products and information has essentially formed a feedback loop that puts consumers at a critical juncture by giving them the ability to tell us what they want (pulling product). The consumers provide us insight into not only what type of products they like but also, where they would buy it, why they like it, when they eat it and who it’s meant for. This is in contrast to the traditional model where KDC dictated what products were available (push) and consumers readily accepted it since they were much less discerning given fewer choices. Thus, our ability to collect and analyze consumer insight is critical for future success and improves our capability to adapt and evolve as an organization to meet the changes of the consumer base.

38 39Strategy

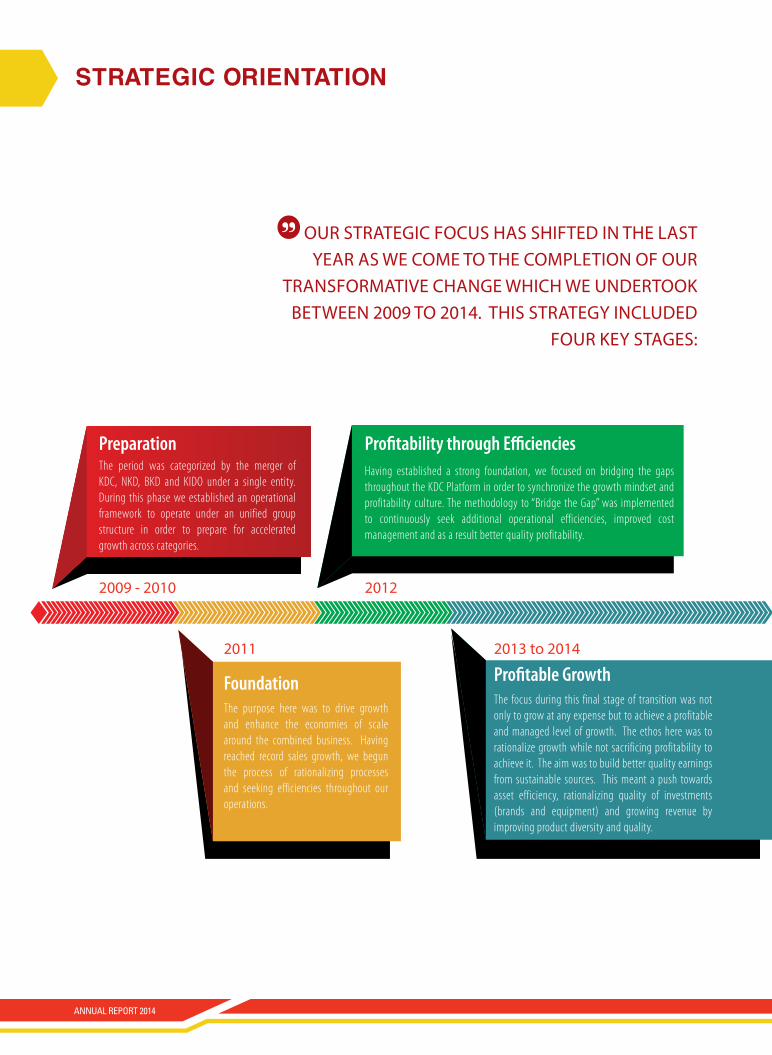

StrategIc orIentatIon

Our STrATegic fOcuS hAS ShifTeD in The lAST yeAr AS we cOMe TO The cOMpleTiOn Of Our

TrAnSfOrMATiVe chAnge which we unDerTOOK BeTween 2009 TO 2014. ThiS STrATegy incluDeD

fOur Key STAgeS:

Preparation Profitability through Efficiencies

Foundation Profitable Growth

2009 - 2010 2012

2011 2013 to 2014

The period was categorized by the merger of KDC, NKD, BKD and KIDO under a single entity. During this phase we established an operational framework to operate under an unified group structure in order to prepare for accelerated growth across categories.

Having established a strong foundation, we focused on bridging the gaps throughout the KDC Platform in order to synchronize the growth mindset and profitability culture. The methodology to “Bridge the Gap” was implemented to continuously seek additional operational efficiencies, improved cost management and as a result better quality profitability.

The purpose here was to drive growth and enhance the economies of scale around the combined business. Having reached record sales growth, we begun the process of rationalizing processes and seeking efficiencies throughout our operations.

The focus during this final stage of transition was not only to grow at any expense but to achieve a profitable and managed level of growth. The ethos here was to rationalize growth while not sacrificing profitability to achieve it. The aim was to build better quality earnings from sustainable sources. This meant a push towards asset efficiency, rationalizing quality of investments (brands and equipment) and growing revenue by improving product diversity and quality.

ANNUAL REPORT 2014

AMOng The 3p’S fOcuS, The MOST ADApTiVe eleMenT iS The prODucT STrATegy.

In order to complete the Transformational Change, we needed to maintain our focus in order to achieve our strategic goals. As such, we narrowed down our strategic focus by featuring 3P’s that we believe were pivotal in our success:

Among the 3P’s focus, the most adaptive element is the product strategy. We have previously identified our product strategy to be based on the Snack &

Confectionary category with an extension into Food & Flavor based on the same platform to leverage further efficiencies and growth.

PlatForm

PEoPlEThe organization and operational platform to execute the strategy of rapid growth and profitability.

The development of products that are adaptive to consumer tastes and demand. The “Value Creation” process leading to better customer loyalty and as a result stronger brands.

strengthening the combined resources across the group

to optimize value for the organization.

Product

40 41Strategy

StrategIc orIentatIon

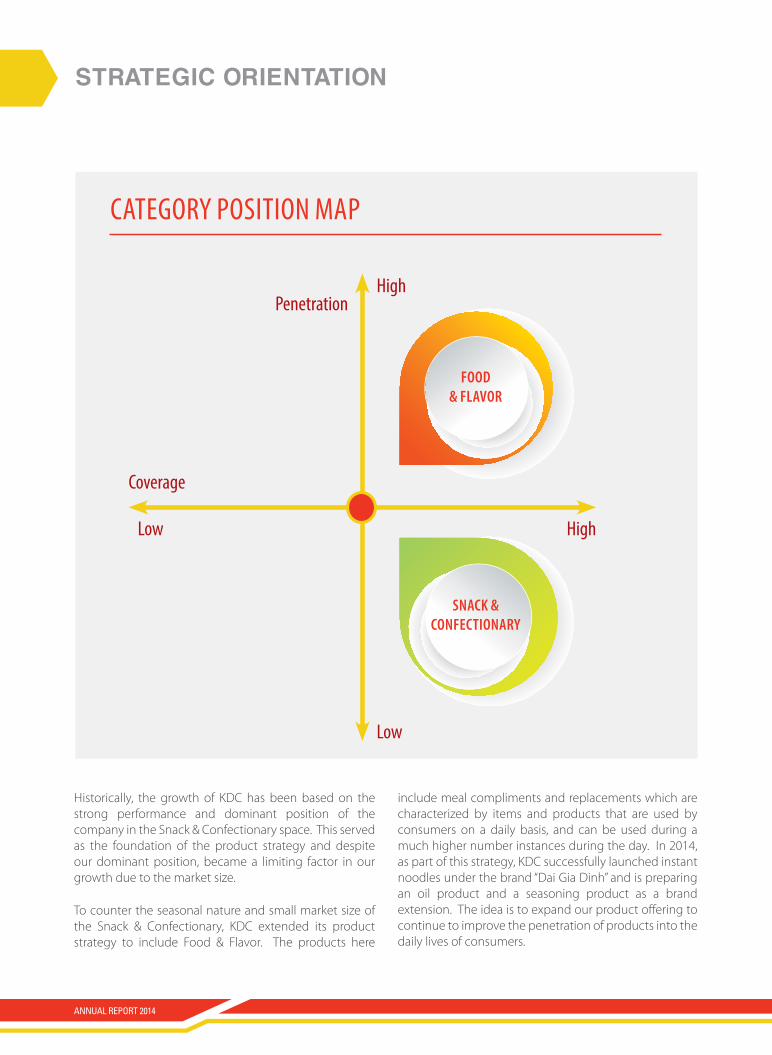

Historically, the growth of KDC has been based on the strong performance and dominant position of the company in the Snack & Confectionary space. This served as the foundation of the product strategy and despite our dominant position, became a limiting factor in our growth due to the market size.

To counter the seasonal nature and small market size of the Snack & Confectionary, KDC extended its product strategy to include Food & Flavor. The products here

Category PoSItIon MaP

HighPenetration

Coverage

High

Low

Low

Food & Flavor

Snack & conFEctionary

include meal compliments and replacements which are characterized by items and products that are used by consumers on a daily basis, and can be used during a much higher number instances during the day. In 2014, as part of this strategy, KDC successfully launched instant noodles under the brand “Dai Gia Dinh” and is preparing an oil product and a seasoning product as a brand extension. The idea is to expand our product offering to continue to improve the penetration of products into the daily lives of consumers.

ANNUAL REPORT 2014

CONSUMERS

Breakfast8AM - 10AM

Lunch12PM - 2PM

Tea4PM - 6PM

Dinner8PM - 10PMSnack Dessert

DAIRY

ICE - CREAM

BEVERAGE

SAUCES

NOODLES

COFFEE

COOKING OIL

CONFECTIONERY

As we began to review the completion of the Transformative Change, the Board of Directors began a strategic review into the future of the KDC business. They looked at the construct of the existing business model, which is defined by a combination of Value Conversion and Value Creation in order to determine where we can derive the most future value for shareholders.

A strategic decision was made to explore the potential to unlock some of the value in KDC that resided in the Value Conversion part of the business and to refocus the company against higher growth areas with broader potential. This naturally led us to review and rationalize the Value Conversion part of our business under Snack & Confectionary. The resulting decision, thus, was to seek a compatible partner in the Snack & Confectionary space to provide the leverage to accelerate our entry into the Food & Flavor category which was deemed to be a much larger and robust market.

This resulted in the signing of an agreement with Mondelēz International to bring forward the future value of the Snack & Confectionary business and to effectively hand over the Value Creation process for the Snack & Confectionary business to them.

While it would seem like a large transition due to the reduction of our stake in that part of the business, it is necessary to note that KDC’s core business is the Food & Beverage business. The Snack & Confectionary business is a small portion of that which we believe has much lower growth potential than the overall Food & Flavor space. The proposed deal also created a unique opportunity from a Value Creation process perspective since it allows KDC to focus purely on the Value Creation process rather than juggling between the labor intensive aspect of Value Conversion and Value Creation.

A STrATegic DeciSiOn wAS MADe TO

explOre The pOTenTiAl TO unlOcK SOMe Of

The VAlue in KDc ThAT reSiDeD in The VAlue cOnVerSiOn pArT Of The BuSineSS AnD TO

refOcuS The cOMpAny AgAinST higher

grOwTh AreAS wiTh BrOADer pOTenTiAl.

42 43Strategy

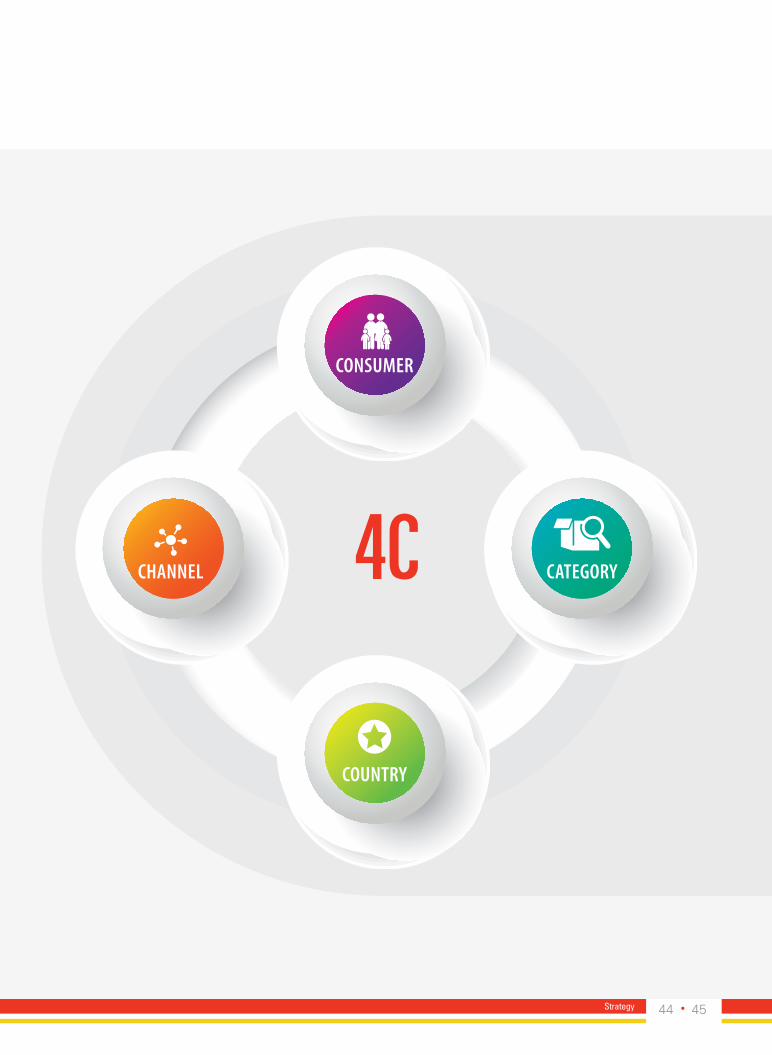

corporate Strategy

The VAlue creATiOn prOceSS iS DriVen By A reViSeD cOrpOrATe STrATegy which will replAce The TrAnSfOrMATiVe chAnge STrATegy.

Our reViSeD cOrpOrATe STrATegy will Be DiViDeD inTO A fOur pArT execuTiOn plAn which incluDeS

1) ConSumer 2) Category 3) Country 4) Channel. TheSe 4c’S (cOnSuMer, cATegOry, cOunTry, chAnnel) will Define Our execuTiOn plAn fOr The nexT few yeArS AnD iS inTenDeD TO SerVe AS A MAp upOn which KDc cAn exTenD iTS VAlue creATiOn prOceSS in An

AccelerATeD fAShiOn AnD AS A reSulT DeliVer higher ShArehOlDer reTurnS AnD prOfiTS.

ANNUAL REPORT 2014

conSumEr

channEl 4C

country

catEGory

44 45Strategy

corporate Strategy

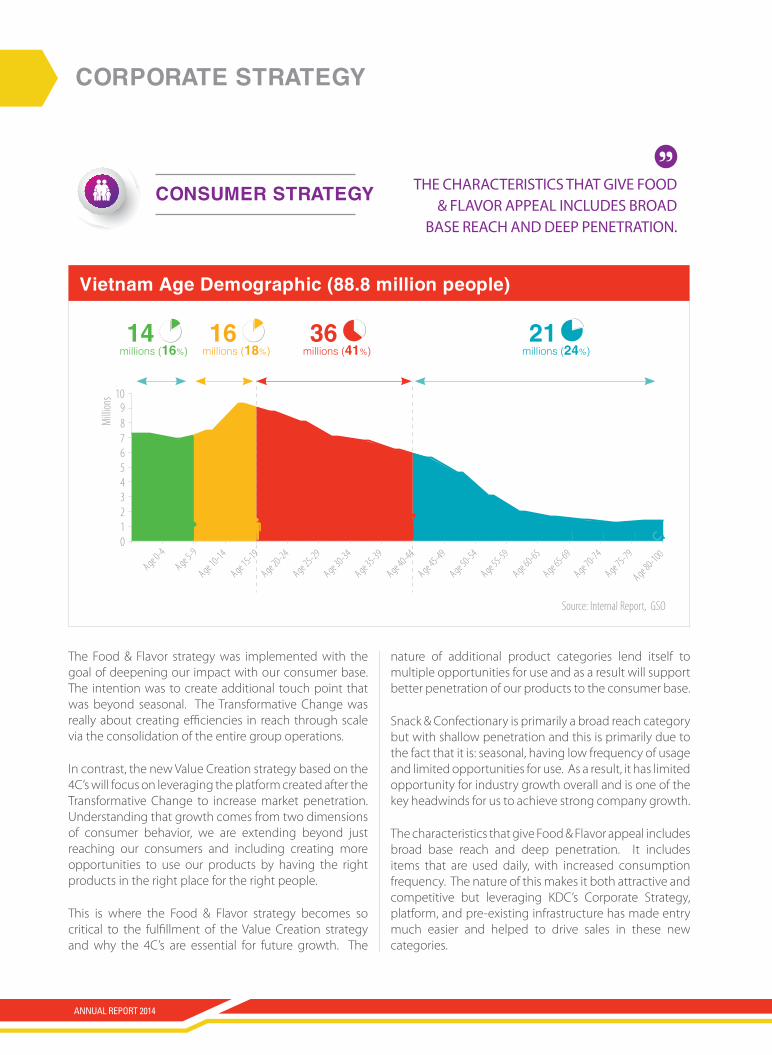

Vietnam Age Demographic (88.8 million people)

10

Millio

ns

Age 0-4

Age 5-9

Age 10-14

Age 15-19

Age 20-24

Age 25-29

Age 30-34

Age 35-39

Age 40-44

Age 45-49

Age 50-54

Age 55-59

Age 60-65

Age 65-69

Age 70-74

Age 75-79

Age 80-100

9876543210

21millions (24%)

36 millions (41%)

16millions (18%)

14millions (16%)

Source: Internal Report, GSO

conSumer Strategy

The Food & Flavor strategy was implemented with the goal of deepening our impact with our consumer base. The intention was to create additional touch point that was beyond seasonal. The Transformative Change was really about creating efficiencies in reach through scale via the consolidation of the entire group operations.

In contrast, the new Value Creation strategy based on the 4C’s will focus on leveraging the platform created after the Transformative Change to increase market penetration. Understanding that growth comes from two dimensions of consumer behavior, we are extending beyond just reaching our consumers and including creating more opportunities to use our products by having the right products in the right place for the right people.

This is where the Food & Flavor strategy becomes so critical to the fulfillment of the Value Creation strategy and why the 4C’s are essential for future growth. The

nature of additional product categories lend itself to multiple opportunities for use and as a result will support better penetration of our products to the consumer base.

Snack & Confectionary is primarily a broad reach category but with shallow penetration and this is primarily due to the fact that it is: seasonal, having low frequency of usage and limited opportunities for use. As a result, it has limited opportunity for industry growth overall and is one of the key headwinds for us to achieve strong company growth.

The characteristics that give Food & Flavor appeal includes broad base reach and deep penetration. It includes items that are used daily, with increased consumption frequency. The nature of this makes it both attractive and competitive but leveraging KDC’s Corporate Strategy, platform, and pre-existing infrastructure has made entry much easier and helped to drive sales in these new categories.

The chArAcTeriSTicS ThAT giVe fOOD

& flAVOr AppeAl incluDeS BrOAD BASe reAch AnD Deep peneTrATiOn.

ANNUAL REPORT 2014

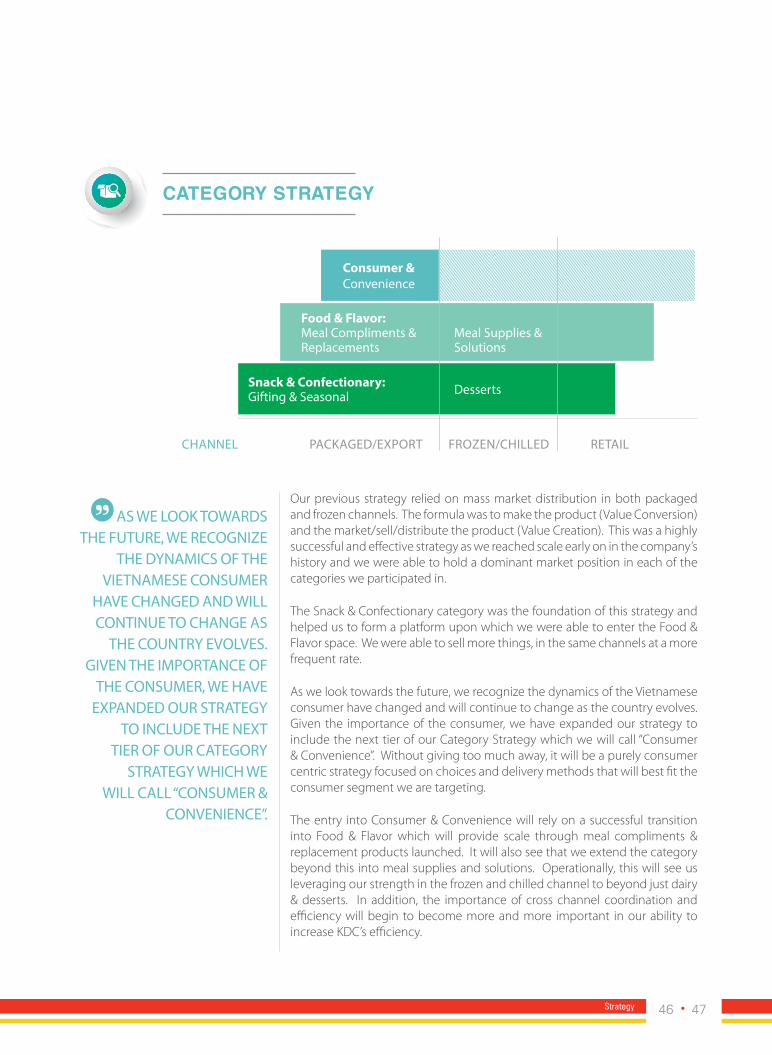

category Strategy

Our previous strategy relied on mass market distribution in both packaged and frozen channels. The formula was to make the product (Value Conversion) and the market/sell/distribute the product (Value Creation). This was a highly successful and effective strategy as we reached scale early on in the company’s history and we were able to hold a dominant market position in each of the categories we participated in.

The Snack & Confectionary category was the foundation of this strategy and helped us to form a platform upon which we were able to enter the Food & Flavor space. We were able to sell more things, in the same channels at a more frequent rate.

As we look towards the future, we recognize the dynamics of the Vietnamese consumer have changed and will continue to change as the country evolves. Given the importance of the consumer, we have expanded our strategy to include the next tier of our Category Strategy which we will call “Consumer & Convenience”. Without giving too much away, it will be a purely consumer centric strategy focused on choices and delivery methods that will best fit the consumer segment we are targeting.

The entry into Consumer & Convenience will rely on a successful transition into Food & Flavor which will provide scale through meal compliments & replacement products launched. It will also see that we extend the category beyond this into meal supplies and solutions. Operationally, this will see us leveraging our strength in the frozen and chilled channel to beyond just dairy & desserts. In addition, the importance of cross channel coordination and efficiency will begin to become more and more important in our ability to increase KDC’s efficiency.

Consumer & convenience

Food & Flavor:Meal compliments & replacements

Snack & Confectionary:gifting & Seasonal Desserts

Meal Supplies &Solutions

chAnnel pAcKAgeD/expOrT frOzen/chilleD reTAil

AS we lOOK TOwArDS The fuTure, we recOgnize

The DynAMicS Of The VieTnAMeSe cOnSuMer

hAVe chAngeD AnD will cOnTinue TO chAnge AS

The cOunTry eVOlVeS. giVen The iMpOrTAnce Of

The cOnSuMer, we hAVe expAnDeD Our STrATegy

TO incluDe The nexT Tier Of Our cATegOry

STrATegy which we will cAll “cOnSuMer &

cOnVenience”.

46 47Strategy

corporate Strategy

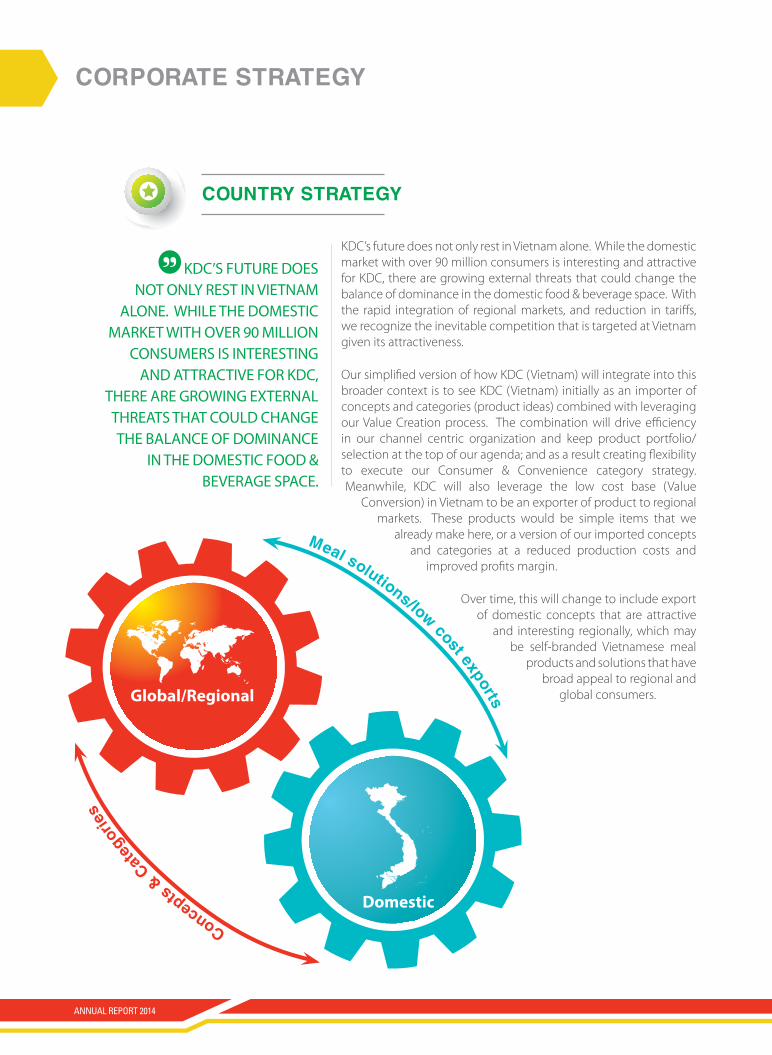

country Strategy

KDC’s future does not only rest in Vietnam alone. While the domestic market with over 90 million consumers is interesting and attractive for KDC, there are growing external threats that could change the balance of dominance in the domestic food & beverage space. With the rapid integration of regional markets, and reduction in tariffs, we recognize the inevitable competition that is targeted at Vietnam given its attractiveness.

Our simplified version of how KDC (Vietnam) will integrate into this broader context is to see KDC (Vietnam) initially as an importer of concepts and categories (product ideas) combined with leveraging our Value Creation process. The combination will drive efficiency in our channel centric organization and keep product portfolio/selection at the top of our agenda; and as a result creating flexibility to execute our Consumer & Convenience category strategy. Meanwhile, KDC will also leverage the low cost base (Value

Conversion) in Vietnam to be an exporter of product to regional markets. These products would be simple items that we

already make here, or a version of our imported concepts and categories at a reduced production costs and

improved profits margin.

Over time, this will change to include export of domestic concepts that are attractive

and interesting regionally, which may be self-branded Vietnamese meal

products and solutions that have broad appeal to regional and

global consumers.

KDc’S fuTure DOeS nOT Only reST in VieTnAM

AlOne. while The DOMeSTic MArKeT wiTh OVer 90 MilliOn

cOnSuMerS iS inTereSTing AnD ATTrAcTiVe fOr KDc,

There Are grOwing exTernAl ThreATS ThAT cOulD chAnge The BAlAnce Of DOMinAnce

in The DOMeSTic fOOD & BeVerAge SpAce.

Domestic

global/regional

concepts & c

atego

ries

meal solutions/low cost exports

ANNUAL REPORT 2014

channel StrategyKD

CDI

StrI

buto

rSre

taILe

rSCo

nSuM

erS

infrASTrucTure/plATfOrM

SAleS/MArKeTing

MArKeT

pAcKAgeD gOODS frOzen reTAil expOrT

The KDC platform will continue to be built upon and dictate our ability to distribute products. While the business model is consumer centric, our platform is about delivery and execution. The entire platform still centered around Strategic Business Units (SBU) which define the categories we compete in but broader than that, we are prioritizing our resources around our channels. These include four different primary distribution channels that are responsible for handling packaged foods, frozen/chilled products, retail and export. These channels currently cover all of Vietnam, and further than that will target to gain a larger foothold regionally and also globally in order to expand our market size and reach.

The KDc plATfOrM will cOnTinue TO Be BuilT upOn AnD DicTATe Our ABiliTy TO DiSTriBuTe prODucTS.

48 49Strategy

corporate Strategy

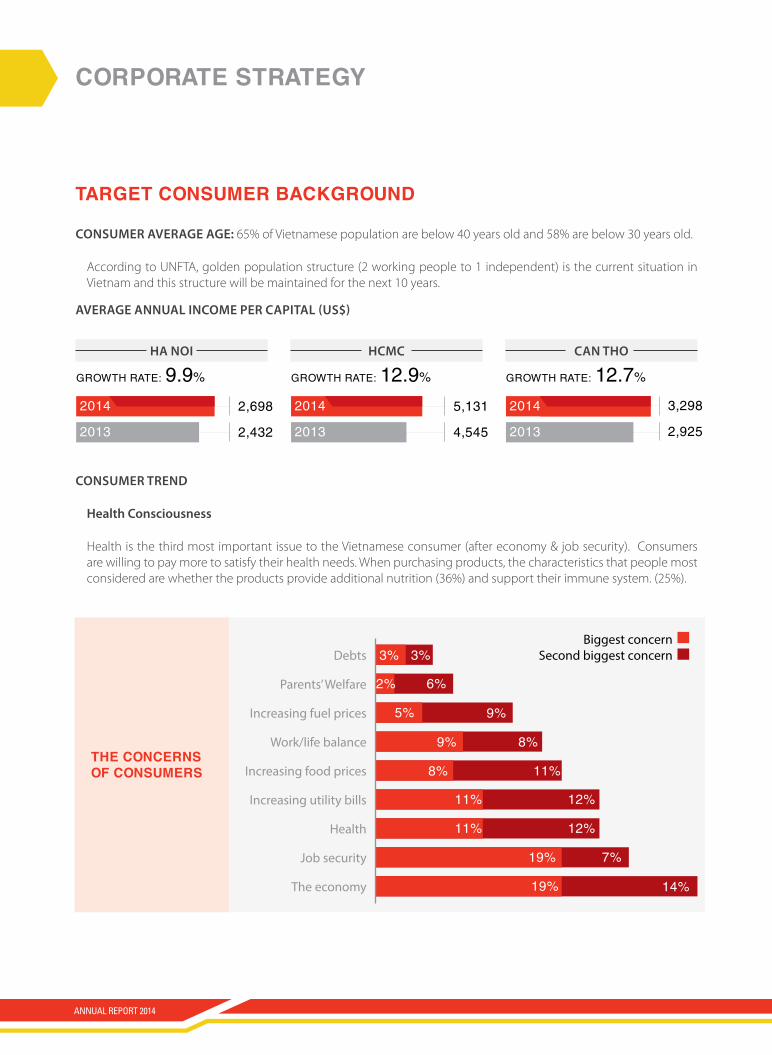

target conSumer BacKground

consumer aVerage age: 65% of Vietnamese population are below 40 years old and 58% are below 30 years old.

According to UNFTA, golden population structure (2 working people to 1 independent) is the current situation in Vietnam and this structure will be maintained for the next 10 years.

aVerage annuaL income Per caPiTaL (us$)

consumer TrenD

health consciousness

Health is the third most important issue to the Vietnamese consumer (after economy & job security). Consumers are willing to pay more to satisfy their health needs. When purchasing products, the characteristics that people most considered are whether the products provide additional nutrition (36%) and support their immune system. (25%).

ha noi hcmc can Tho

20142,698 5,131

2,432 4,5452013 2013 2013

GrOwth rate: 9.9% GrOwth rate: 12.9% GrOwth rate: 12.7%

3,298

2,925

Debts

parents’ welfare

increasing fuel prices

work/life balance

increasing food prices

increasing utility bills

health

Job security

The economy

3%

2%

5%

9%

8%

11%

11%

19%

19%

3%

6%

9%

8%

11%

12%

12%

7%

14%

the concernS of conSumerS

Biggest concern Second biggest concern

2014 2014

ANNUAL REPORT 2014

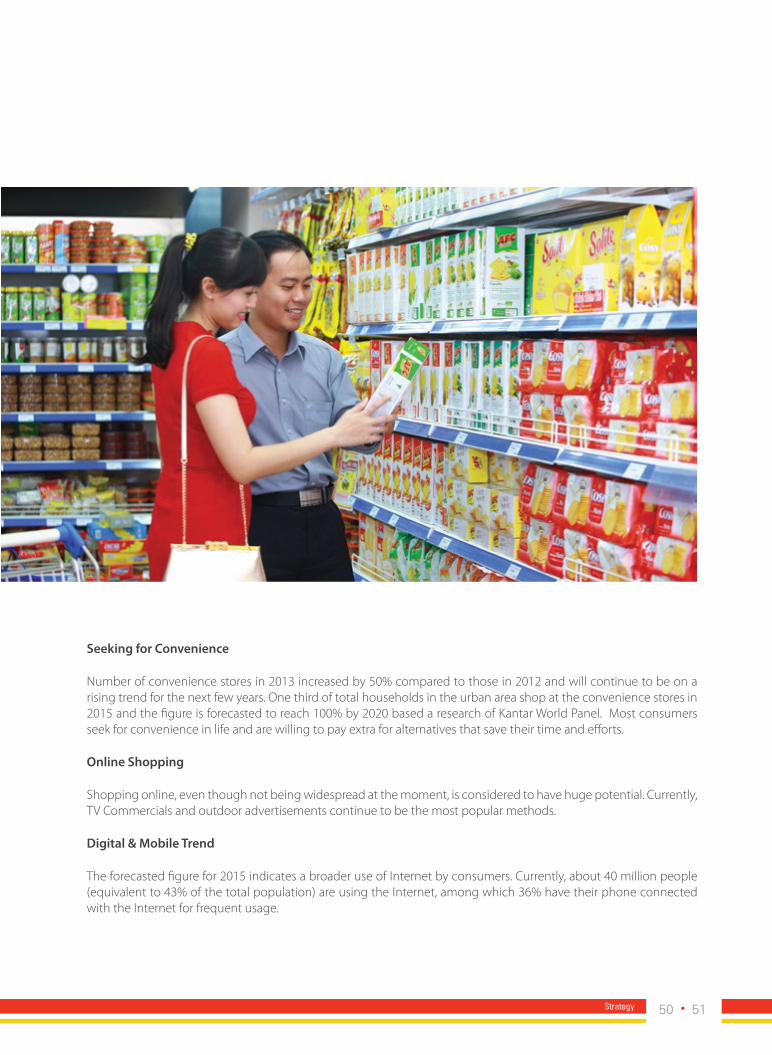

seeking for convenience

Number of convenience stores in 2013 increased by 50% compared to those in 2012 and will continue to be on a rising trend for the next few years. One third of total households in the urban area shop at the convenience stores in 2015 and the figure is forecasted to reach 100% by 2020 based a research of Kantar World Panel. Most consumers seek for convenience in life and are willing to pay extra for alternatives that save their time and efforts.

online shopping

Shopping online, even though not being widespread at the moment, is considered to have huge potential. Currently, TV Commercials and outdoor advertisements continue to be the most popular methods.

Digital & mobile Trend

The forecasted figure for 2015 indicates a broader use of Internet by consumers. Currently, about 40 million people (equivalent to 43% of the total population) are using the Internet, among which 36% have their phone connected with the Internet for frequent usage.

50 51Strategy

Leveraging the strength of our distribution network, Kinh Do has targeted the entry into

new categories including instant noodles, cooking oils, condiments, ice cream and milk.

The goal is to meet daily needs of the Vietnamese consumers.

21 years

LEADING POSITION in confectionery industry

Business Review

03

Diversify categories

Leveraging the strength of our distribution network, Kinh Do has targeted the entry into

new categories including instant noodles, cooking oils, condiments, ice cream and milk.

The goal is to meet daily needs of the Vietnamese consumers.

21 years

LEADING POSITION in confectionery industry

Business Review

03

Diversify categories

fInancIal hIghlIghtS

(VnD’bil) 2013 2014 change % change

Sales 4,561 4,953 +392 +8.6%

Gross Profit 1,976 2,146 +169 +8.6%

Operating Expenses 1,393 1,632 +239 +17.2%

EBIT 584 514 -70 -11.9%

PBT 619 663 +44 +7.2%

NPAT 493 537 +44 +9.0%

Effective Tax Rate 20.3% 19.0% -1.3% -136 basis points

VND 2,146billion

VND 1,976billion

groSS profIt

VND 1,632billion

VND 1,393billion

operatIng eXpenSeS

2014

2013

VnD2,146 Billion | +8.6%

2014

2013

VnD1,632 Billion | +17.2%

ANNUAL REPORT 2014

VnD4,953Billion

growth +392 Billion

+8.6%

saLes 2014

VND 514billion

VND 584billion eBIt

VND 663billion

VND 537billion

VND 619billion

VND 493billion

pBt

npat

2014

2013

VnD514 Billion | -11.9%

2014

2013

2014

2013

VnD663 Billion | +7.2%

VnD537 Billion | +9.0%

54 55Business Review

marKet overvIew

macro environment

Against a backdrop of relatively benign growth and low inflation, the overall economy has undergone a well managed recovery from 2011 till today. The prevailing stable conditions in 2014 have been an extension of the policies from 2013 and continues to be resilient against both major external and internal macro economic shocks. The stability created a unique environment which includes the lowest CPI in over a decade caused by falling food prices and fuel prices and a more stable GDP growth. However, even at these depressed pricing levels, consumer demand is muted with confidence levels at an all time low. Hence, the slow expansion can be largely attributed to low demand and ample supply.

To understand last year’s market dynamics, we need to look at different factors affecting supply and demand. On the supply side, we saw overall credit growth decelerate sharply since 2011, averaging well under 20% for the last 3 years, which reinforces the fact of underinvestment and low GDP growth. Despite such a decrease, money supply continued to expand and therefore created strong liquidity in the domestic market. With low credit growth, strong liquidity, and low CPI, the only asset class that was able to absorb that amount of excess funds was government bonds.

Looking more into the liquidity situation, created a low interest rate environment yet the markets continued to be risk adverse. Low interest rates are a result of falling yields caused by strong liquidity chasing government bonds. The government issued significant amount of bonds to absorb this liquidity resulting in the strong expansion of the public sector balance sheet. The continued expansion of the public sector balance sheet had been aimed at financing the structural reform of the banking sector rather than other productive areas (i.e. investment or growth). Therefore, we had a unique situation of risk adversity with strong liquidity, coupled with low inflation, low interest rates and low GDP growth.

Against this macroeconomic backdrop, our industry has continued to see favorable and accommodative policies on the supply side for production, including both inputs and financing costs. In contrast, we saw very little catalyst on the demand side to drive growth and expansion. This has been characterized by low disposable incomes, low wealth creation and also a lack of real growth, which has affected the overall consumer sentiment. The contradicting situation primarily related to the fact that the flow of funds in accommodative supply policies had been ultimately used to clean up the banking sector NPL’s. This left the larger economy underinvested and without a clear catalyst or fuel for growth. Specifically, the consumers and our target markets have been left nominally the same as when we started the crisis, indicating no sign of growth while sentiment continues to be poor, and outlook negative...

Our inDuSTry hAS cOnTinueD TO

See fAVOrABle AnD AccOMMODATiVe

pOlicieS On The Supply SiDe fOr prODucTiOn,

incluDing BOTh inpuTS AnD finAncing

cOSTS. in cOnTrAST, we SAw Very liTTle

cATAlyST On The DeMAnD SiDe TO

DriVe grOwTh AnD expAnSiOn.

Npat

537 VND BiLLiON

ANNUAL REPORT 2014

group reSultS

Performance

The fiscal year 2014 was an extension of the previous year strategy where we continued to focus our efforts on Stage 4 of our Transformative Change Strategy: Profitable Growth. The strategy proved to be resilient against the benign economic conditions and poor consumer sentiment. To be specific, the favorable supply conditions allowed us to continue monitizing on the restructuring of our value chain which we have divided into value conversion and value creation. This delineation has supported to focus and target our efforts to extract value and efficiency. Moreover, internal initiatives prevailed over implementing external ones such as advertising and promotions as poor consumer demand limited the effectiveness of external investments in the market.

Despite the lack of strong interest and demand and supply imbalances, we were able to increase net sales by 8.6% reaching VND4,953bn. Gross profit margins were on target at 43.0% with input prices remaining relatively stable across the board. Global commodity prices continued to be stable throughout 2014, which allowed for a significant decline in raw material price risk versus 2013. The primary cost increases were domestically driven, including labor, electricity and manufacturing overhead, which combined accounted for less than 15% of our total cost of goods sold;

limiting the impact of its increase. The sharp decline in oil prices in the last part of 2014 have yet to impact our raw material input costs, however this should positively impact our profitability by the 2nd or 3rd quarter of 2015 as the flow through from oil price declines begin to reach our suppliers of key commodities. Selling and general administrative costs were in line with revenue growth but it’s important to note that the construct of these costs have altered slightly.

During the course of 2014, we continued to rationalize and realign our process to create better quality earnings. Overall operating costs compared to 2013 has actually declined, and the actual increase of 17.2% was based on infrastructure investment that was designed for future capacity and capability, including the relocation of our corporate offices, building of additional warehouse capacity in the north, and investing in additional cold chain capacity. Sales and marketing costs increased by 21.8% year on year. The breakdown between variable and fixed costs are now approximately 48% vs. 52%. Variable costs consisting of advertising and promotion expenses, and fixed costs consisting of infrastructure costs. Advertising and promotional spending was well managed and reduced by VND70bn. Trade marketing activities increased by VND59bn and has been targeted at our core products to drive sales volume growth.

56 57Business Review

Overall, 2014 spending was well managed with variables directly in line with our growth and fixed at a managed rate that balanced the immediate impact and future growth. Sales infrastructure costs increased by 46.6%, within which the primarily is due to the regulated rise in salaries and wages as set out by the government in the early part of 2014. The additional increase was the result of sales incentives, which were paid out for successful achievement of volume targets.

Net operating profit was flat against 2013 and the difference primarily being a proactive approach to investing in infrastructure for future growth. This was balanced with an overall increase in profits before tax of VND 663bn, which was 7.2% better year-on-year. The savings from financing costs and reductions in debt were used to finance last year structural investment which helped to bring profits growth back in line with overall growth. Profit after taxes were 9.0% better reaching VND537bn, which was a direct result of active management over tax strategies, which helped to save approximately VND12bn in taxes paid against a higher pre-tax profit.

Overall, while there continued to be a lack of a strong catalyst to drive growth combined with strong headwinds in our industry, we maintained our performance with a defensive strategy. In a meantime, some of these challenges while manageable are believed to be structural across the entire confectionary industry. Therefore, a strategic review was undertaken to address longer term growth issues, resulting in strong shift in strategy that will see us expanding beyond snack & confectionary.

assets

Financial liquidity positions continued to be strong, with cash positions increasing from 2013 through a private placement in 2014, which was earmarked for several M&A projects. We are now becoming more aggressive in deployment as we believe that the current economic cycle is prime for investment entry as the market continues to be liquid but risk adverse. Since our first investment in Vinabico, we have continued this process with a strategic investment of 24% in Vocarimex, Vietnam’s largest edible oil company. Regarding this

marKet overvIew

free Cash fLOw

509 VND BiLLiON

ANNUAL REPORT 2014

investment, we have earmarked an addition VND700bn to increase our stake beyond 51%, which should be concluded by the end of 2015. Other investments relating to PP&E were kept minimal in 2014 as we continued to digest the CAPEX made during 2013.

liabilities

Our debt ratios remain fairly consistent with 2013’s debt-equity ratio of 0.25 times and an external gearing of 0.09 times. Taking advantage of the domestic liquidity and also as part of the cost reduction strategy, we fully repaid the more expensive long-term loans taken out in early 2014 with lower cost financing. This helped us to reduce average borrowing costs from 6.5% in 2013 to 4.1% in 2014. Even though we do not believe that our cost of borrowing can be reduced further, we continue to be bullish on the domestic liquidity and the current rate levels. Therefore, we continue to maintain shorter duration debt and do not foresee the need to swap funding further. We continue to actively monitor potential funding issues which could negatively impact these funding positions.

Working Capital

We continue to find efficiencies in our working capital management with a further reduction in our business cycle from 32.96 days to 31.93 days. The reduction was contributed primarily by reduction in inventory, which continued to be well managed and significantly improved by our Distributor Management System, which supported us to manage inventory levels throughout our supply chain.

return on equity & total Shareholder return

Return on equity was 8.6% vs. last year’s 10.09% but against a net increase of equity of approximately VND1,404bn due to the private placement. Excluding such impact, Return on Equity would have been 11.0%, which is close to where our commitment to shareholders has been. Regarding the positive financial highlights, it has been proven that we continued to be strongly committed to growth, profitability and returns and believed in maintain a relatively strong payout to shareholders.

GrOss prOfit

2,146 VND BiLLiON

58 59Business Review

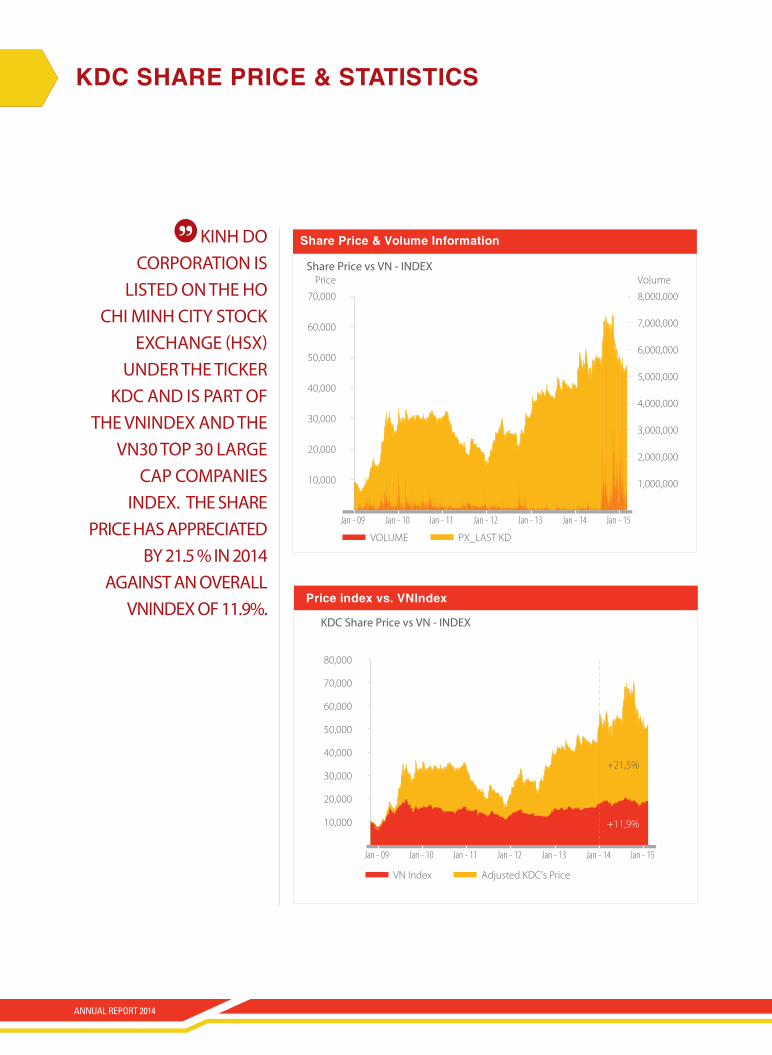

Kdc Share prIce & StatIStIcS

Kinh DO cOrpOrATiOn iS

liSTeD On The hO chi Minh ciTy STOcK

exchAnge (hSx) unDer The TicKer

KDc AnD iS pArT Of The VninDex AnD The

Vn30 TOp 30 lArge cAp cOMpAnieS

inDex. The ShAre price hAS AppreciATeD

By 21.5 % in 2014 AgAinST An OVerAll

VninDex Of 11.9%.

Share Price vs VN - INDEX

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Price Volume

Jan - 09 Jan - 10 Jan - 11 Jan - 12 Jan - 13 Jan - 14 Jan - 15

VOLUME PX_LAST KD

Share Price & Volume Information

Price index vs. VNIndex

KDC Share Price vs VN - INDEX

10,000

20,000

30,000

40,000

50,000

60,000

70,000

+21,5%

+11,9%

80,000

VN Index Adjusted KDC’s Price

Jan - 09 Jan - 10 Jan - 11 Jan - 12 Jan - 13 Jan - 14 Jan - 15

ANNUAL REPORT 2014

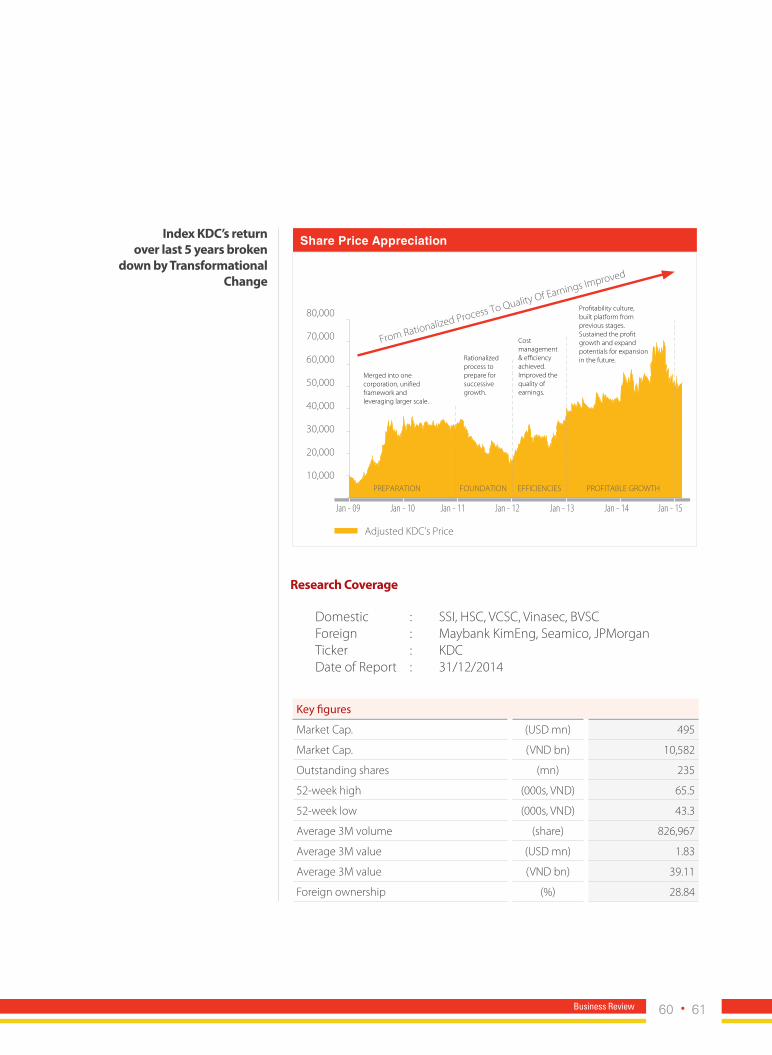

Domestic : SSI, HSC, VCSC, Vinasec, BVSCForeign : Maybank KimEng, Seamico, JPMorgan Ticker : KDCDate of Report : 31/12/2014

Index KDC’s return over last 5 years broken

down by transformational Change

Share Price Appreciation

Adjusted KDC’s Price

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Jan - 09 Jan - 10 Jan - 11 Jan - 12 Jan - 13 Jan - 14 Jan - 15

From Rationalized Process To Quality Of Earnings Improved

Merged into one corporation, uni�ed framework and leveraging larger scale.

Rationalized process to prepare for successivegrowth.

Cost management & e�ciency achieved.Improved the quality of earnings.

Pro�tability culture, built platform fromprevious stages.Sustained the pro�tgrowth and expand potentials for expansion in the future.

PREPARATION FOUNDATION EFFICIENCIES PROFITABLE GROWTH

Key figures

Market Cap. (USD mn) 495

Market Cap. (VND bn) 10,582

Outstanding shares (mn) 235

52-week high (000s, VND) 65.5

52-week low (000s, VND) 43.3

Average 3M volume (share) 826,967

Average 3M value (USD mn) 1.83

Average 3M value (VND bn) 39.11

Foreign ownership (%) 28.84

research Coverage

60 61Business Review

Creating brands

Governance

Kinh Do is a company with a long history and development. To sustain the future growth and expansion, we have targeted to operate with a

clear corporate governance structure that facilitates transparency and accountability.

04WIN M&A

80 %

Creating brands

Governance

Kinh Do is a company with a long history and development. To sustain the future growth and expansion, we have targeted to operate with a

clear corporate governance structure that facilitates transparency and accountability.

04

WIN M&A

80 %

COrpOrate governance Structure

general meetIng oF ShareholDerS

InD

ePen

Den

t a

uD

Ito

r