about arabiaarabiainsurance.com/css/pdf/location1441784992.pdftable of contents 2 4 5 6 9 11 about...

TRANSCRIPT

Preserving your lifestyle... Simply.

Arabia Insurance Company s.a.l. - Paid up capital L.L. 51,000,000,000 –Commercial Court Register 1889Insurance Register 2, dated 11/9/1956 – Subject to Decree 9812 of 4/5/1968 - MOF #4976

Lebanon | Kuwait | Bahrain | Qatar | UAE | OmanKSA | Syria | JordanAnnual Report 2014

Table of conTenTs

2

456911

abouT aRabIa

branch officesArabia’s Vision, Mission & Goalssubsidiaries and affiliated companiesboard of Directors as of 31/12/2014executive General Management (Head office)

63consolIDaTeD fInancIal sTaTeMenT anD auDIToR’s RepoRT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . .

I. execuTIVe suMMaRy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

II. InsuRance secToR oVeRVIew . . . . . . . . . . . . . . . . . . . . .

1. Insurance IndustryIII. aRabIa opeRaTIons oVeRVIew. . . . . . . . . . . . . . . . . .

1. Insurance operations1.1 non-life Global overview1.2 life insurance operations

2. Investment operations2.1 world economy and financial market 2.2 Investment operations - General

Departments2.3 Investment operations - life

3. financial Highlights3.1 non-life3.2 life

4. other Issues4.1 Human capital update4.2 other operational Highlights

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1. corporate Governance2. Group Risk & capital Management

2.1 capital Management 2.2 Risk Management

152021242525273232

3334

353741434345

4849515155

RepoRT of THe boaRD of DIRecToRs on THe 70TH fInancIal yeaR of THe coMpany’s opeRaTIons

abouT aRabIa

annual Report 2014Report of the Board of Directors and Statements of Accounts for the Financial year ending on 31/12/2014 submitted to the 70th Annual General Assembly of Shareholders.

Head office:Arabia House - Phoenicia street - Beirut - LebanonTel. 961 - 1 - 363610 /363611 & 961 - 3 - 314350 / 314351Telefax 961 - 1 - 365139 /363659

P.O.Box 11 - 2172 Beirut - LebanonE-mail [email protected] www.arabiainsurance.com

4

branch offices

Country Branch Local Sponsor Management

Lebanon

United Arab Emirates

Sultanate of Oman

BahrainKuwaitQatar Doha

ain el MreissehTripoliZalkasaidachtauraManamaKuwait

Muscat

salalahDubaiSharjahAbu DhabiAl-Ain

M/s. Moosa abdul Rahman Hassan & co.

Mr. Mohammad Jalal

ali bin ali establishmentMr. Mohammad abdul Rahman al bahar

Tony choueiryIsmail el Rifielias sawayaToufic DerianRoger Dawalibi

shaikh butti Maktoum Juma almaktoumsheikh Khaled al KassimiMr. ahmed bin GhanoumMr. saeed sultan salmeen bin Harmal al-Dhahiri

francis Karam Tareq fakhoury / antoine sfeirJihad salaminMohammad Kaddoura

alain Georr

Mohammad othmanclaude Jabbour

fadi said chammas – country ManagerMaurice shaheenRaed Daghmash

VisionTo be the leading “customer centric” Arab Insurer.

MissionTo provide accessible, simple, effective, and client friendly products and services that respond to the evolving needs of our customers.

Arabia’s Vision, Mission & Goals

5

Sustain a culture of leadership, trust, open communication, transparency, efficiency, effectiveness and innovation, thus adding further value to our stakeholders.

Develop, invest in, empower our human capital to take on the challenges of a fast changing and growing industry, capitalizing on teamwork spirit and a “customer centric” culture.

Enhance our corporate brand by using an advanced and holistic marketing approach.

Play a positive role in the countries of our operations through local CSR activities.

Use state of the art technology.

Goals

Enhance Shareholder value.

Emphasize excellence in our relations with our stakeholders, while exercising good corporate governance, enhancing our internal controls, simplifying processes, and upholding professional ethics, integrity and social responsibility.

Respond to our customers’ needs by offering them transparent quality products, good investment opportunities, outstanding personalized services, dedicated personnel, and an elaborate, easily accessible, distribution & claims’ handling networks.

Achieve a fair return on equity, benchmarked with local markets’ yields.

6

subsidiaries & affiliated companies

ARABIA s.a.l. HOLDInG COmPAnyHead Office Arabia House Building, Phoenicia St.Tel. 961 - 1 - 363610/1 & 961 - 3 - 314350/1Fax 961 - 1 - 362975P.O.Box 11 - 2172 Beirut - LebanonE-mail [email protected]

ARABIA InTERnATIOnAL COmPAny B.S.C. ClosedHead Office Bahrain Tower - Al Khalifa AvenueTelefax +973 - 17 - 214110P.O.Box 11432 Diplomatic Area manama – Bahrain

ARABIA InSURAnCE BROKERS s.a.r.l.Head Office Arabia House Building - Phoenicia St.Tel. 961 - 1 - 363610/1Fax 961 - 1 - 363659 / 365139P.O.Box 11 - 2172 Beirut – Lebanon

7

subsidiaries & affiliated companies

ARABIA InSURAnCE COOPERATIVE COmPAnyHead Office Bin Tami Center, King Abdel Aziz RoadTel. 966-11-2153360Fax 966-11-2153197P.O.Box 286555 - 11323 Riyadh - KSAURL www.aicc.com.sa

ARABIA InSURAnCE COmPAny - SyRIA S.A.Head Office Abu Remaneh, Al Sebki Park, Hugo Chavez StreetTel. 963 - 11 - 6627745Fax 963 - 11 - 6627750P.O.Box 34801 Damascus - SyriaURL www.arabiasyria.com

Branches in the Kingdom of Saudi Arabia:Riyadh - Head OfficeJeddah Branch 1Jeddah Branch 2mekkahTaefKhamis musheitRiyadh Branch 1Riyadh Branch 2DammamKhobarHoufouf

Branches in Syria:Damascus Head Office

[email protected] Branch

8

subsidiaries & affiliated companies

ARABIA InSURAnCE COmPAny - JORDAn LtdHead Office Arabia Insurance Building - Al Shmesani

Abed El Hameed Sharaf Street- Building 3Tel. 962 - 6 - 5630530Fax 962 - 6 - 5622303P.O.Box 20031 Amman (11118) JordanE-mail [email protected] www.gaic.jo

UPI (SERVICES) LImITEDHead Office 3, Chrysanthou - mylona StreetTelefax 5340734P.O.Box 6253 - 3305 Lemesos-Cyprus

AL mASHRIQ FInAnCIAL InVESTmEnT CO. s.a.l.Head Office Arabia House Building - 131 Phoenicia St.Tel. 961 - 1 - 363610/1Fax 961 - 1 - 362975P.O.Box 4069 Beirut – Lebanon

9

board of Directors as of 31/12/2014

board of Directors

mr. Wahbe Abdallah Tamari (Chairman)mr. Hani Atallah Freij (Vice - Chairman)Arab Bank PLC (Represented by mr. Riyad Kamal)mr. nadim BaroodyDr. Karma Fahoum EI-Hassanmr. Basim Farismr. Emad AI Baharmr. Tarek AI-Suleimanms. Randa Tannousmr. muneer mouashermr. nadim Ghantous

board committees

Investment committeemr. Wahbe Tamari / Committee Chairpersonmr. Hani Freijmr. nadim Ghantous

shares Transfer committeemr. Wahbe Tamari / Committee Chairpersonmr. Hani Freijmr. nadim Baroody

nomination & Remuneration committeemr. Wahbe Tamari / Committee Chairpersonmr. Hani Freijmr. nadim Baroodymr. Basim Faris

audit committeeDr. Karma Fahoum El-Hassan / Committee Chairpersonms. Randa Tannousmr. nadim Baroody

Risk committeemr. Riad Kamal / Committee Chairpersonmr. nadim Ghantousmr. Tarek Al-Suleiman

10

Management committee

executive & administrative committeemr. muneer mouasher / Chief Executive Officermr. Hisham Barraj / Chief Insurance Officermr. nabih Baaklini / Chief Operations Officermr. Carlos Saba / Chief Human Resources Officermr. naji Fayad / Chief Financial Officer

board of Directors as of 31/12/2014

11

executive General Management (Head office)

chief executive officermr. muneer mouasher

chief officersmr. Hisham Barraj. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. nabih Baaklini. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. Carlos Saba. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. naji Fayad. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Managersmr. Abdul Hameed Habboub. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

ms. Amal mikdash. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. Antoine Haddad. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. Bassam Saadeh. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

ms. Danielle Zakher Salloum. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. Elias malek. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. Fadi Sawaya. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. Fouad Oleiwan. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. GaroSajian. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. Georges Bekhazi. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. Jamal Arnaout. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. Joseph yammouni. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. marwan Berjaoui. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. median Fares. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Chief Insurance OfficerChief Operations OfficerChief Human Resources OfficerChief Financial Officer

ClaimsPropertymarketingLoss PreventionmedicalTreasury & InvestmentActuaryAdministrationInformation TechnologyRisk management General Accident Individual LifeReinsuranceBudgeting & Financial Reporting

12

executive General Management (Head office)

Managersmr. mohammad EI-Hassan. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

ms. noura Tabbara. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

ms. Rana Chammas. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

ms. Sabine Salloum. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. Sadek Khoukas. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

mr. Samir Karnabi. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

ms. Sana Saoud malti. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Internal audit & compliancemr. Wael El Bsat. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

auditorsDeloitte & Touche

OperationsInsurance SupportHuman CapitalGroup LifeLife Sales marineAccounts

manager

life agenciesCedars Agency/ Verdun - Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Elite Agency/Ashrafieh - Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Kite Agency/Jdeideh- Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Unirisk Agency/Beirut - Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Dynamix Agency/Sharjah - UAE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Falcons Agency/Abu Dhabi, Al Ain & Dubai - UAE. . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Pharaohs Agency/Sharjah - UAE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

The A Team Agency/Dubai - UAE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

managed by mr. Riad Shoukairmanaged by mr. Antoine Zakhiamanaged by mr. Georges Saadmanaged by mr. Ghaleb Damajmanaged by mr. Ashraf Hamdymanaged by mr. Hassan Al Khatibmanaged by mr. mohamad nabil El Kasedmanaged by mr. Assaad Abou Seif

13

executive General Management (Head office)

non-life agenciesAntelias Agency/Antelias-Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Ashrafieh Agency / Ashrafieh-Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Baalbeck Agency/ Baalbeck-Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Badaro Agency/Badaro-Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Hadath Agency/Hadath-Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Jdeideh Agency/Jdeideh-Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Jib Jennine Agency/Jib Jennine-Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Koura Agency/Koura-Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Rabieh Agency/Rabieh-Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Saida Agency/Saida -Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Verdun Agency/ Verdun-Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Zahle Agency/Zahle-Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Zgharta Agency/Zgharta-Lebanon. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Al Buraimi Agency/Al Buraimi-Sultanate of Oman. . . . . . . . . . . . . . . . . . . . . . . . . . .

Al Jabal Al Akhdar mound Trade Agency/Al Ghubra -Sultanate of Oman Al mazar Agency/Al Khud- Sultanate of Oman. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Amani Al Faisal Agency/Al Hail - Sultanate of Oman. . . . . . . . . . . . . . . . . . . . . .

Future Safe Agency/Khoweir-Sultanate of Oman. . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Sohar Agency/Sohar-Sultanate of Oman. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gateway International Assurance L.L.C/ Dubai-UAE. . . . . . . . . . . . . . . . . . . . . . . .

managed by mrs. Vera Atallah Aramounimanaged by mr. Antoine Zakhiamanaged by mrs. Oumayma Haidar younessmanaged by mr. Samer Khalilmanaged by mr. matta Sakrmanaged by mr. Georges Saadmanaged by mr. Joseph Abi Faresmanaged by mr. nizam najjarmanaged by mrs. nivine Chediakmanaged by mr. Sami Awadmanaged by mr. Bassem Abou Dahermanaged by mrs. Lina Haroukmanaged by mr. Pascal masrimanaged by mr. Rached Al Jaberimanaged by mr. Khaled Al Ismailimanaged by mr. Shahul Hamedmanaged by mr. Faisal Al Farsimanaged by mr. nabih Drazmanaged by mr. Abdul Rahman Abdallah Al Farsimanaged by mr. Georges Ashkar

RepoRT of THe boaRD of DIRecToRs on THe 70TH fInancIal yeaR of THe

coMpany’s opeRaTIons

I. execuTIVe suMMaRy

RepoRT of THe boaRD of DIRecToRs

16

Dear Shareholders,

We welcome you at your company, and are glad, on behalf of the Board of Directors of Arabia Insurance Group, to present to you the Annual Report and the consolidated financial statements for the year ending December 31st

2014, along with the necessary illustrations and explanatory analysis.

As we have moved with great confidence into the year 2015, we can safely look back at the year 2014 as the year of exceptional recovery of our technical results, from an unusually bad underwriting year with losses from General Insurance departments of around LBP 0.3 B equivalent to USD 0.2 m in 2013, to a net income from General Insurance departments of around LBP 6.2 B equivalent to USD 4.1 m in 2014.

The main factor behind this transformation was a return to Technical Profitability of the motor lines from a Loss of LBP 3.5 B equivalent to USD 2.3 m in 2013 to a Profit of LBP 2.1 B equivalent to USD 1.4 m in 2014. The Property and General Accident departments also delivered an increase in their net Incomes from LBP 1.7 B equivalent to USD 1.1 m and LBP 1.1 B equivalent to USD 0.7 m respectively in 2013 to LBP 2.6 B equivalent to USD 1.7 m and LBP 3.4 B equivalent to USD 2.2 m respectively in 2014. The medical line continued to underperform, but mainly as a result of claims still flowing from non-renewed loss-producing groups. Accordingly, the Technical Loss of this line amounting to LBP 4.4 B equivalent to USD 2.9 m is expected to improve starting 2015 and onward. Total non-Life Production decreased from LBP 237 B in 2013 equivalent to USD 158 m to LBP 224 B equivalent to USD 149 m in 2014, as a result of the ongoing conservative selectivity of insured risks and more stringent underwriting, which remains a major pillar of our strategy, side by side with our strive to grow our book of business in a profitable way.

On the investments side, the company achieved in 2014 an investment income of LBP 9.8 B equivalent to USD 6.53 m, while the invested assets reached LBP 333 B equivalent to USD 222 m.

I. execuTIVe suMMaRy

RepoRT of THe boaRD of DIRecToRs

17

As mentioned last year, management was fully mobilized to tackle the sources of the previous year 2013 losses and, as promised, the drastic remedial measures it had started to implement reflected positively on the current year 2014, and will hopefully sustain an upward momentum in the subsequent years with the right strategy, the effective and efficient employment of our resources, and synergy among the various business units.

The reinsurance treaty renewals were relatively smooth this year, and reflected a true partnership between Arabia and its reinsurers in light of the large blows that those reinsurers absorbed in the past years from a number of jumbo losses that Arabia had sustained. We continued to subscribe to a Group treaty led by a first class European reinsurer, and covering the eight countries of our operations through the 3 sister companies; AIC-Lebanon, AICJ (Jordan) and AICS (Syria).

In April 2015, A.M. Best has re-affirmed the financial strength rating of B++ (Good) and the issuer credit rating of “bbb+” of Arabia Insurance Company s.a.l. (AIC) (Lebanon). The outlook for both ratings remains stable.

The ratings of AIC reflect its sound risk-adjusted capitalization and well-diversified business profile. A major factor also supportive of this rating was the remedial program which management implemented in 2014 to improve underwriting performance, which included non-renewal of loss-making contracts and the introduction of data-driven pricing tools.

I. execuTIVe suMMaRy

RepoRT of THe boaRD of DIRecToRs

18

The results of our sister companies and their respective insurance markets situation are as follows:

- Arabia Insurance Company - Jordan (AICJ) showed good results, whereby net profits before taxes increased from JD 581 K equivalent to USD 819 K in 2013 to JD 918 K equivalent to USD 1,294 K in 2014. AICJ premiums increased from JD 16 m equivalent to USD 22.6 m in 2013 to JD 17 m equivalent to USD 24.1 in 2014. Ongoing regional disruptions are still expected to impact and slow the growth of the Jordanian insurance industry over the coming few years.

- Arabia Insurance Company - Syria (AICS) continued to stand the test of the ongoing conflict in Syria, and the resultant economic and political situation. Total premiums increased from SyP 471.5 m equivalent to USD 3.3 m in 2013 to SyP 606.2 m equivalent to USD 3.4 m in 2014. Technical profitability decreased from SyP 113.6 m equivalent to USD 802 K in 2013 to SyP 106.7 m equivalent to USD 593 K in 2014.

- Arabia Insurance Cooperative Company-KSA (AICC): A major challenge faced by all insurance companies in the KSA, including AICC, is the highly competitive state of the insurance market, with 37 licensed insurance and reinsurance companies and 76 brokers and 76 insurance agencies. Despite that, the year 2014 was a positive year for AICC witnessing a major shift in its results, recovering from a loss of about SR 102 m equivalent to USD 27 m in 2013 to a profit of about SR 2 m equivalent to USD 533 K in 2014. A new Board of Directors and a new business strategy contributed to this transformation. Total premiums increased by around 10% from SR 586 m equivalent to USD 156 m in 2013 to SR 644 m equivalent to USD 172 m in 2014. It is very important to highlight that the motor and medical lines which were the main sources of underwriting losses in 2013 at deficits of SR 61 m equivalent to USD 16.3 m and SR 9.9 m equivalent to USD 2.6 m respectively, recorded handsome profits this year of SR 12.5 m equivalent to USD 3.3 m and SR 34.3 m equivalent to USD 9.1 m respectively. All the other lines also delivered good technical profits.

I. execuTIVe suMMaRy

RepoRT of THe boaRD of DIRecToRs

19

future outlook

We shall channel our efforts in 2015 and beyond towards consolidating our market position and increasing our bottom-line by continuing to identify and remove the threats to profitability in all lines of business. Fierce competition between insurance players will continue in the middle East insurance market as m&A activities become very likely. The turmoil in Syria and political instability in the region continue to remain a major concern in the short term. Despite these challenging conditions, we shall strive to capture all the opportunities in the areas of our operation, in order to achieve healthy growth and, eventually, attain a return on equity that truly reflects our history and real potential.

A key element in our insurance sales strategy is to break the vicious circle of tightening margins due to the soft market cycle, by targeting more of the personal lines of insurance and small to medium sized enterprises.

We will continue enhancing our online business solutions, and developing our human resources at all levels, always stimulating the culture of “customer centricity” across Arabia.

We are grateful to our CUSTOmERS for their continued support and loyalty, to Arabia Shareholders for their trust in Arabia, and to the board of directors, management and employees for their dedication, hard work and loyalty. Together we shall continue to plan our way forward.

yours sincerely,

Wahbe Abdallah TamariChairman of the Board of Directors

I. execuTIVe suMMaRy

RepoRT of THe boaRD of DIRecToRs

II. InsuRance secToR oVeRVIew

RepoRT of THe boaRD of DIRecToRs

21

1. Insurance Industry

In 2014, the global insurance industry finally emerged from the financial turmoil and economic uncertainty that has been challenging the life and non-life insurers for the last several years. This recovery in the economic activity has and will yield a mild improvement in non-life premium growth, as real (after inflation) premium growth is projected to be 1.4% in the advanced economies and around 8% in the emerging markets. As expected last year, the return on equity level (RoE) for the main non-life insurance markets was around 7% in the financial year 2014, down from 8.4% in the financial year 2013. This was mainly caused by the low investment returns that are continuously affecting profitability, whereby most insurers are still relying on decreased catastrophe losses and reserve releases to keep their profit margins at sustainable levels. However, it goes without saying that this cannot be relied upon forever, whereby an improvement in the underwriting standards is and will be strictly inevitable for a healthy and properly developed non-life insurance industry.

Life real premium growth in the developed markets has reached 4% in 2014, up from 1.5% in 2013, and is expected to be about 3% in 2015. In the emerging markets, life premium growth increased from 4.5% in 2013 to 9% in 2014, and is expected to score 10% in 2015. However, the low investment returns environment poses a greater challenge to the life insurance industry than the non-life, obviously because of the higher dependence of life insurers on investment yields for their profits. This is why life insurers are focusing and have to focus more on new products, increased market penetration, better distribution channels and cost-cutting. This has already started to pay off in new life business growth in major markets, mainly through the increased sales of savings policies, thus improving profitability with the RoE reaching 12%.

II. InsuRance secToR oVeRVIew

RepoRT of THe boaRD of DIRecToRs

22

In the emerging Asian markets, both non-life and life premium growth remained high at more than 12% in 2014, and is expected to grow by 13% in 2015 and 2016. In the emerging Central and Eastern Europe markets, however, premium growth will be low as a result of the slow economic recovery.

In the middle Eastern market, real growth in non-life premiums reached 1.8% in 2014, and is expected to reach 6% in 2015. Life premium growth reached around 9% in 2014, and is expected to reach 10% in 2015. Still, the irrational price competition, soft insurance terms and political instability in the region will remain a major obstacle to the healthy development of the insurance sector in this market.

2014 was a better year than 2013 in terms of natural catastrophic events, where significant insured losses totaled around USD 33 billion, down from USD 45 billion in 2013. Those insured losses were below the ten-year and five-year moving averages of around USD 59 billion and USD 56 billion, respectively. notable natural catastrophe insured losses included the February snowstorms in Japan, winter storms affecting Europe, flooding in the United Kingdom and a cold, stormy weather in the eastern half of north America. The East-Pacific witnessed Hurricane Odile and the West-Pacific was subject to Typhoon Rammasun that affected China, Vietnam and the Philippines. Cyclone Hudhud affected India in October. December witnessed a severe weather outbreak in Brisbane, Australia and severe floods in malaysia and Thailand.

1. Insurance Industry

II. InsuRance secToR oVeRVIew

RepoRT of THe boaRD of DIRecToRs

II. InsuRance secToR oVeRVIew

23

On the other hand, the year 2014 did not fare so well in terms of man-made events. These included the disappearance of malaysian Airlines Flight 370 in march, the loss of malaysian Airlines Flight 17, which was shot down over Ukraine in July, the AirAsia flight that crashed into the sea near Indonesia in December. Added to these were a refinery explosion and fire in Krasnoyarsk territory of Russia, and a militant attack on the Tripoli International Airport in Lybia.

In conclusion, and given the slim profit margins in the global insurance market in general in 2014 and last several previous years, insurers must continue to explore and identify opportunities for top line and bottom line growth, by basically developing a customer-centric culture focused on the distinctive needs and expectations of their clients, be ready to give up loss producing segments and allocate their capital to the more promising lines and markets, and investing in technologies that will enable them have a stronger digital presence, enhance their customer services, and develop a comprehensive enterprise- wide data analytics strategy aiming at appropriate business targeting, better product design, and more effective and efficient management control.

RepoRT of THe boaRD of DIRecToRs

1. Insurance Industry

RepoRT of THe boaRD of DIRecToRs

III. aRabIa opeRaTIons oVeRVIew

Consolidated Operations of Insurance Co. s.a.l, Arabia Insurance Co.-Syria and Arabia Insurance Co. – Jordan (hereinafter referred to as Arabia).

This year, we are pleased to report that Arabia recovered from an underwriting loss in its non-life operations of LBP 292 million in 2013, to an underwriting profitability of LBP 6.2 billion in 2014. This was mainly a result of the return to technical profitability recorded this year in the motor department and amounting to LBP 2.1 billion, up from a loss of LBP 3.5 billion in 2013. This was achieved through the drastic remedial measures taken to restore the positive results of this important line of business to their sustainable levels. The other good news was the increase in the net income of the Property and General Accidents departments as follows: Property from LBP 1.7 billion in 2013 to LBP 2.6 billion in 2014; General Accidents from LBP 1.1 billion in 2013 to LBP 3.4 billion in 2014. The marine department’s profitability declined from LBP 3.6 billion in 2013 to LBP 3.1 billion in 2014, mainly due to the decrease in the marine insurance rates as a result of the unreasonable competition, which naturally led to an organic shrinkage in our marine premiums. medical and Workmen’s Compensation continued to underperform, with losses of LBP 4.4 billion and LBP 0.4 million respectively. However, things will get back on track in respect of those two lines of business starting this year 2015.

25

1. Insurance operations

1.1 non-life Global overview

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

26

As mentioned last year, we have swiftly embarked on a comprehensive plan involving all of the key aspects of our business operations. We are relentlessly following a roadmap which aim is threefold: cleaning our portfolio from loss-producing risks, increasing our underwriting bottom-line, and raising our market share in insurance segments and markets where extra profitability is possible and achievable. We shall always concentrate on deriving our net income from our core business which is insurance, whereby net income from investments will naturally always constitute a plus. At the end of the day, our ultimate raison-d’être is to arrive at a respectable Return on Equity, while serving our customer base in the most optimum level. The insurance operations of Arabia remain protected by a Group Reinsurance treaty with preferential terms and underwriting capacities, supported by first class reinsurance securities.

The continuation of the extremely soft market conditions, whether in terms of cut-throat low premium rates, wide uncontrollable terms, or inflow of opportunistic capacity in the countries where Arabia operates, will remain an ever-growing challenge. We are confident that we can overcome those challenges by capitalizing on our long history, distinguished resources and the will to succeed.

1. Insurance operations

1.1 non-life Global overview

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

27

year after year, the Life Total Gross Written Premiums sustained their growth and reached in 2014 the amount of LBP 33.59 billion (USD 22.28 million), with a growth of 20.22% over 2013 figures.

The Life production is mainly originated from our Life Sales Consultants who are spread among Units, Agencies and Branches.

Consistently with the previous years, the “Arabia Lifestyle” product, which offers an optimum combination of Protection and Investment, scored the highest share in our production figure, reaching USD 6.10 million (First year Written Premiums), with an increase of 39% over last year figures.

During 2014, the First year Written Premiums of Individual Term Insurance soared by 57% (reaching USD 1.34 million) and the First year Written Premiums of Group Life Insurance increased by 14% (reaching USD 3.80 million).

life Division main goals for 2015:- Enhance the recruitment standards of new producers with increased focus on quality.

- Intensify the training for producers (old and new) in order to increase their level of professionalism, and therefore their production in quantity as well as in quality.

- Onboarding new members to the administration and technical team to optimize its productivity, enabling it to timely process the continuously increasing Life production.

1. Insurance operations

1.2 life Insurance operations

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

- Vigorous follow-up on the collection of the renewal premiums, hence conserve our policies, resulting in a direct and positive impact on the company’s bottom line.

- Face Lift our products in terms of type and features, in addition to the re-drafting of the products existing Terms and Conditions in order to simplify their vocabulary, rendering them easily understood by the policyholders, in line with the principle of accurately and transparently dealing with them.

28

1. Insurance operations

1.2 life Insurance operations

Unit-Linked Premiums in Millions of US$

$12.00

$10.00

$8.00

$6.00

$4.00

$2.00

$0.00

$3.58

$4.38

$6.10

$7.75

$8.84

$10.23

2010 2011 2012 2013 2014

First Year Unit-Linked Renewal Unit-Linked

$4.44 $3.77

$8.66

$9.33

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

29

1. Insurance operations

1.2 life Insurance operations

Geographical Distribution of Life Written Premiums in 2014

20141st Year Premiums

2014Renewal Premiums

2014Total Premiums

2013Total Premiums

LBP’000 LBP’000 LBP’000 LBP’000% % % %lebanonuaeomanbahrainKuwaitotherTotal

1,645,64611,980,5832,057,955123,229161,524499,625

16,468,562

2,692,37511,176,144

600,12542,935

486,9601,330,856

16,329,395

4,454,77923,722,8932,675,428166,164700,008

1,873,13933,592,411

4,630,61619,005,8411,654,255182,980733,794

1,493,84227,701,328

10%73%12%1%1%3%

100%

16%68%4%0%3%8%

100%

13%71%8%0%2%6%

100%

17%69%6%1%3%5%

100%

Geographical Distribution of Total Written Premiums in 2014

Lebanon

UAE

Oman

Bahrain

Kuwait

Other

71%

8%

13%0%2%6%

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

30

1. Insurance operations

1.2 life Insurance operations

Life Production Historical Chart (Total Written Premiums)

2014

2012

2010

2008

2006

2004

2002

2000

0 5 10 15 20 25 30 35 40

3.44

3.86

4.19

5.09

6.16

7.92

9.59

12.06

17.39

18.06

23.68

26.07

26.74

27.94

33.59

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

31

1. Insurance operations

1.2 life Insurance operations

Group & Open Policies

32%

Regular Premiums

63%

Additional Premiums

5%

First Year Written Premiums Distribution in 2014

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

2. Investment operations

2.1 world economy and financial Market

2014 was a year of challenges for the Treasury & Investment Department, as the interest rates remained at historically low levels, volatility in the equity markets where high, and the regulation of the insurance industry in the Gulf area continued to strengthen, particularly in connection with regulatory reserve requirements.

The global economy saw the leading Asian economies growing strongly and recovery in the U.S. economy accelerating, contrasted with weak growth in the Eurozone.

The US and European stock markets reached new record levels during 2014 after the ECB’s meeting in early June, at which it cut its key lending rate to a record low level of 0.15% and imposed a negative interest rate for deposits with the central bank, but the overall stock markets full-year gains were not as high as in 2013, as fears of a fresh economic setback mounted in December where the markets in Europe in particular were disquieted from Greek problems.

The capital markets were unsettled in July by the crisis in Ukraine and the ensuing EU sanctions against Russia in addition to the flare-up of conflict in the middle East.

As for the currency markets, the divergence in monetary policies between the US and the other major economies caused the dollar to appreciate against all the main currencies – and especially the euro.

32

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

2. Investment operations

2.2 Investment operations - General Departments

The value of Arabia invested assets in general insurance departments (excluding Property & Equipment) decreased by LBP 12.5 billion (-4.7%), from LBP 268.0 billion in 2013 to LBP 255.5 billion in 2014. This decrease was due to the drop in market price of our participation in Arabia Insurance Cooperative Company (yoy drop LBP 15.6 billion) and Saudi Enaya (yoy drop LBP 7.1 billion).

meanwhile, the net investment income of the general departments was at LBP 7.65 billion in 2014 versus LBP 9.52 billion in 2013; this decline was mainly due to the shift from term deposits in Lebanon to low yielding term deposits in the Gulf to meet the new regulatory reserve requirements, in addition to the maturity of several high coupon bonds.

33

2014all amounts in LBP’000 2013

cash and banksDue to banksfinancial assets at fair value through profit or lossfinancial assets at fair value through other comprehensive incomefinancial assets at amortized costTotal Invested AssetsInterests on bank depositsInterests and dividend income from investment securitiesnet gain on investment securities at fVTplnet gain/(loss) on disposal of investment securitiesnet foreign exchange lossesTotal Investment Income

159,056,574 (4,813,848)16,001,389 74,464,206 10,797,293

255,505,614 3,964,152 2,623,293 1,422,928 307,235

(670,618)7,646,990

146,386,111 (4,550,036)13,676,662

100,268,178 12,245,311

268,026,226 5,077,918 2,620,491 2,745,382 (58,338)

(861,826)9,523,627

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

2. Investment operations

2.3 Investment operations - life

Arabia invested assets of the Life division (excluding Property & Equipment) increased by LBP 10 billion (+14.7%), from LBP 67.6 billion in 2013 to LBP 77.6 billion in 2014. This increase was mainly due to the additions on the unit linked fund assets.

The net investment income of the Life division was at LBP 2.2 billion in 2014 versus LBP 7.4 billion in 2013; this decrease was mainly due to:

- Lower term deposits after the maturity of the 3 years Security & Growth unit linked investment product for the amount of LBP 24 billion in December 2013.

- The outstanding performance of the unit linked funds in 2013 was not repeated in 2014.

34

2014all amounts in LBP’000 2013

cash and banksDue to banksfinancial assets at fair value through profit or lossfinancial assets at fair value through other comprehensive incomefinancial assets at amortized costTotal Invested AssetsInterests on bank depositsInterests and dividend income from investment securitiesnet gain on investment securities at fVTplnet foreign exchange lossesTotal Investment Income

26,991,323 (1,507,500)39,301,614 2,361,224

10,433,905 77,580,566

464,242 1,361,930 437,903

(106,047)2,158,028

21,846,968 (1,507,500)33,867,193 2,893,565

10,534,390 67,634,616 2,022,446 1,321,641 4,041,664

37,850 7,423,601

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

35

3. financial Highlights

- FVTOCI investments decreased by around USD 15 million, mainly due to drop in the Group’s investment in AICC and Enaya.

- Reinsurance assets decreased by around USD 11 million, mainly resulting from the drop in general accidents and property reinsurance share of outstanding claims.

- net change in fair value of investments decreased by around USD 14 million, mainly resulting from the Group’s investment in AICC and Enaya.

- 2014 income from general insurance departments went up by around USD 7 million compared to 2013 from a loss of USD 6.7 million to a profit of USD 0.5 million, mainly resulting from better performance of the motor line of business, and drop in the operating expenses.

Total Assets

Total Equity

Net Profit

(usD Million)20142013

354,459380,889

Percentage -7% ↓

(usD Million)

2013 122,5832014 106,724

Percentage -13% ↓

(usD Million)

(6,660)20132014 488

Percentage 107% ↑

- medical & motor production went down by 12% & 4% respectively from 2013 to 2014, mainly due to non-renewing of some accounts in Kuwait and Lebanon.

Gross Written Premiums

(usD Million)

2013 184,0172014 178,778

Percentage -3% ↓

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

36

3. financial Highlights

- 2014 net written premiums remained almost the same compared to 2013.

Net Written Premiums(usD Million)

2013 132,8072014 132,318

Percentage 0%

- Solvency ratio decreased from 92% in 2013 to 81% in 2014, as a result of drop in total equity.

- Retention ratio increased in 2014 compared to 2013, mainly in medical and life lines of business.

Underwriting Exposure

92%

72%

2013 2014

81%

74%

Solv

ency

Solv

ency

Rete

ntio

n

Rete

ntio

n - Earnings per share (EPS) went up from USD -0.35 in 2013 to USD 0.03 in 2014.

- Return on average equity (ROE) went up from -4.9% in 2013 to 0.4% in 2014.

Profitability Metrics

20132014

EPS

($0.35)$0.03

ROE

-4.9%0.4%

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

37

3. financial Highlights

3.1 non-life

Net Loss ratioGross Loss ratio

Loss Ratio - Non-Life

80.0%

70.0%

60.0%

50.0%

40.0%

30.0%

20.0%

10.0%

0.0%

72.7%

62.3%68.9%

54.0%

2013 2014

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

Gross Loss Ratio = Change in Outstanding Claims (gross of reinsurance) + Paid Claims (gross of reinsurance) – Recoveries (gross of reinsurance) / Gross Earned Premiums (gross of reinsurance)

net Loss Ratio = Change in Outstanding Claims (net of reinsurance) + Paid Claims (net of reinsurance)– Recoveries (net of reinsurance) / net Earned Premiums (net of reinsurance)

38

40.0%

35.0%

30.0%

25.0%

20.0%

15.0%

10.0%

5.0%

0.0%

12.8% 12.8%

22.8%21.6%

35.6% 34.4%

20142013

Acquisition ratio G&A ratio

Expense Ratio - Non-Life

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

3. financial Highlights

3.1 non-life

Acquisition Ratio = Incurred Commission Expense – Earned Reinsurance Commissions + Other Expenses – Other Income / net Earned Premiums (net of reinsurance)

G&A Ratio = General & Administrative Expenses / net Written Premiums (net of reinsurance)

Expense Ratio = Acquisition Ratio + G&A Ratio

39

Combined Ratio - Non-Life

2014

120.0%

100.0%

80.0%

60.0%

40.0%

20.0%

0.0%

108.3%

34.4%

68.9%

103.3%

Net Loss ratio Expense ratio

2013

35.6%

72.7%

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

3. financial Highlights

3.1 non-life

Combined Ratio = net Loss Ratio + Expense Ratio

40

Performance KPI’s - Non-Life120.0%

100.0%

80.0%

60.0%

40.0%

20.0%

0.0%

72.7%

108.3%102.6%

35.6%

68.9%

103.3%98.6%

34.4%

Expense ratio Combined ratio Operating ratioNet Loss ratio

2013 2014

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

3. financial Highlights

3.1 non-life

Operating Ratio = Combined Ratio – (Investment Income / net Written Premiums)

41

3. financial Highlights

3.2 life

Acquisition Ratio = Commission Expense – Reinsurance Commissions / net Written Premiums

G&A Ratio = General & Administrative Expenses / net Written Premiums

Expense Ratio = Acquisition Ratio + G&A Ratio

20142013

70.0%

60.0%

50.0%

40.0%

30.0%

20.0%

10.0%

0.0%

59.1% 55.3%

44.7% 40.3%

14.4% 15.0%

Acquisition ratio G&A ratio

Expense Ratio - Life

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

42

3. financial Highlights

Benefits Paid & Return on Premiums - Life

60.0%

50.0%

40.0%

30.0%

20.0%

10.0%

0.0%

48.6%

8.6%

13.5%

3.0%

Benefits paid to net insurance premiums

Return on net insurance premiums

Benefits Paid to net Insurance Premiums Ratio = Claims Paid (net of reinsurance) + Change in Insurance Contract Liabilities (net of reinsurance) + Distribution of Profits to Policyholders / net Written Premiums – Premiums Allocated to Insurance Contract Liabilities

Return on net insurance premiums Ratio = net Income / net Written Premiums – Premiums Allocated to Insurance Contract Liabilities

2013 2014

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

43

The Human Resources Division strives to provide the highest level of service, and reflects this commitment through focusing on our mission to support Arabia’s vision of being the leading “customer centric” Arab insurer, through professional HR practices.

Our goals (supporting that mission) continue to include:-Working collaboratively with other divisions, departments and branches.

-Recruiting and retaining staff that are best qualified for Arabia’s position.

-Reviewing current and developing new, human resource-related policies and procedures.

-Conducting training for all employees to ensure all staff possess the necessary tools to perform the job.

- Providing excellent service by treating each employee with respect, and recognizing that each concern or question deserves attention.

- Providing excellent HR support that aims at managing the compensation, benefits and logistics in order to meet the demands for an efficient and performing staff.

The Workforce profile as at 31/12/2014:-630 employees (including Life Sales)

-446 employees without Life Sales

4. other Issues

4.1 Human capital update

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

44

-184 Life Sales agents

-74% of the employees have a University level education

Recruitment in 2014:-798 CVs were received through Arabia website

-91% was the acceptance rate of Job Offers at the Head Office

-9 internal recruitments

-63 external recruitments

Training in 2014:-28% of employees went through training

-2% of the training was performed abroad

-63% of the training was performed In-house

-36% of the training was local

-4,617 total training hours

4. other Issues

4.1 Human capital update

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

45

On the operations side, emphasis was placed on further enhancing Arabia’s sales strategy which calls for promoting a company wide sales driven culture for everyone working with Arabia. This approach involves training the staff on how to be skillful in approaching clients through a disciplined approach.

In preparation for this well-disciplined sales strategy, an elaborate products manual was prepared as a quick guideline to assist all branches in acquiring and growing profitable business.

The manual was comprised of 4P’s (price, place, production, product) approach to reach the needed study and included products by line, by country, place, distribution, commission structure, promotion when needed and price which will pave the way towards the strategy we want.

We revisited the role and functions of Accounts Executives in line with our strategy to become a customer centric company which is responsive to the needs of our customers.

The recruited accounts executives so far for our Lebanon operations are under the direct supervision and guidance of the Sales manager and their main functions is to grow business, retain direct and corporate accounts, be involved in cross selling and up selling of Arabia products to increase sales and revenues, grow business and always ensure client satisfaction, which will be the main target.

4. other Issues

4.2 other operational Highlights

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

46

The Operations Division further enhanced the monthly follow up on accounts receivable and collections by preparing a receivable analysis report which provides a comparative summary of accounts receivable key performance indicators detailing the aging of accounts and listing all delinquent accounts which age more than 90 days and which are not in compliance with the credit policy.

The Credit Control Supervisor’s roles are being enhanced and monitored. This would help in identifying deteriorating and non moving accounts in order to take the needed corrective action in a timely manner. We are considering outsourcing independent and specialized firms to expedite the process of collections and delivery of policies.

In line with the new “Agile and Responsive” positioning of the company, Arabia’s corporate image underwent a face lift, and established a new motto: Preserving your lifestyle... Simply.

The outsourced Call Center activities have been improved to secure a superior service to our customers. Clients’ support included follow up on motor Claims in particular, and road assistance, and responding to general queries, as well as completing personal member’s data when possible.

4. other Issues

4.2 other operational Highlights

III. aRabIa opeRaTIons oVeRVIew

RepoRT of THe boaRD of DIRecToRs

III. aRabIa opeRaTIons oVeRVIew

47

year 2014 witnessed the finalization of phase one of Arabia’s e-Commerce portal, (e-Branch), the integrated virtual experience to sell and support insurance over the web interface. e-Arabia is now ready to operate from a client perspective, allowing prospects to simulate, buy and pay online their insurance policies. In the coming phase, the portal will be developed to operate from brokers and agents perspective, including a complete workflow automating claims, renewals, and collections processes.

In Lebanon, Arabia’s Customer Relationship management (CRm) department acted as a hub amongst the different touch points, putting the customer in the center of its operations. CRm has a major role in supporting the Call Center activities securing a swift follow up on client’s requirements. As far as e-Arabia is concerned CRm has a front office role in the portal’s operations.

We are currently improving the Front & Back office experience to increase the clients’ satisfaction when visiting a branch.

4. other Issues

4.2 other operational Highlights

RepoRT of THe boaRD of DIRecToRs

RepoRT of THe boaRD of DIRecToRs

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

49

“Through its well established and advanced corporate governance structure and effective role of its governing committees and entities, Arabia is committed to keep protecting and increasing the value of the shareholders’ investments, and consolidating its reputation as an insurance company that can be always trusted by clients, employees, governments and other stakeholders.”

board of Directors

The composition, elections, meetings, duties and responsibilities of the Board of Directors are described in the Company’s Corporate Governance Charter and in accordance with the Lebanese law.

The Board of Directors delegated part of its duties to specialized committees. These committees are conducting these duties based on authorities and specific responsibilities defined in each related charter.

The main functions of these specialized committees are:

shares Transfer committeeConsiders and approves the shares transfers, and/or the subscription of the company’s shares.

Investment committeeSets the Company’s investment guidelines, approves the investment policy and supervises its investment in accordance with its risk tolerance and against agreed benchmarks.

audit & compliance committeeEncourages and safeguards the highest standards of professional integrity, financial reporting, corporate governance, compliance to all applicable laws/regulations, conformity to business ethics, and internal control.

1. corporate Governance

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

50

Risk committeeAssists the Board in fulfilling its oversight responsibilities of the Enterprise Risk management activities. Assesses the adequacy of the management of key internal and external risks, and monitors the Company’s risk profile.

executive & administrative committeeRuns and monitors the whole operations of the Company and ensures internal controls are in place.

asset-liability committeeSets the Company’s asset-liability management policy and supervises the resulting activity involving liquidity management, cash budget and forecasting.

IT steering committeemonitors and reviews IT projects, as well as provides oversight of the deliverable rollout.

business continuity Management committeeReviews the existing BCP and recommends improvements to address elements of continuity planning and restoration of the Company’s essential functions.

anti-fraud committeeAssists the Executive management in continuously developing and monitoring the Company’s Anti-Fraud Program across all functions.

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

1. corporate Governance

51

“Arabia is expected to maintain a good level of risk-adjusted capitalization in 2015. The ratings reflect the sound risk-adjusted capitalization and well-diversified business profile”. (Excerpt from AM Best Report).

2.1 capital Management

The Group continues to manage its capital on a consolidated basis. Each company within the group has its own rating and capital requirements.

The overall strategy is to meet these requirements and ensure the Group’s ability to continue as a going concern, while maximizing the return through the optimal use of our capital.

processes for Managing capital

The Group’s capital monitoring activity is driven by the strategic objectives and the Board risk appetite statements. Revisions are made in light of changes in the economical and market conditions, and the risk characteristics of operations and underlying assets. The Group’s overall strategy remains unchanged from prior year.

The Group’s capital position to certain risks is being regularly monitored through ALm, stress testing and actuarial assessments. In addition, financial risks are being overseen by the Investment Committee and mitigated by abiding to risk limits defined and stated in the Group Investment policy.

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

2. Group Risk & capital Management

52

capital adequacy assessment

The Group keeps improving the existing risk models, preparing for the upcoming solvency II capital adequacy and economic capital requirements.

At present, the Group assesses its capital position using a newly developed risk-based capital model. The assessment is made at both the group/entity level, as well as by line of business and by geographical location.

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

2. Group Risk & capital Management

2.1 capital Management

2014 2013 2012

Gearing RatioSolvency RatioCapital Adequacy Ratio

1.5981%

192%

1.4592%

170%

1.15115%174%

net Liabilities / Total Equity (see note FS34)Total Equity / net Written Premiums*net Required Capital / Total Adjusted Equity**

*net Written Premiums = Technical Premiums + Other Technical Income - Reinsurance share of Technical Premiums + fees.

** net Required Capital (nRC) is computed to support the Group risks associated with the exposure of assets, business, and underwriting to adverse economic and market conditions.

The Group monitors its capital risk position based on widely-used capital ratios:

53

aM best Rating

Rating Results

In April 2015, Am. Best Europe published the rating results of Arabia (AIC) and affirmed the financial strength rating of B++ (Good) and the issuer credit rating of bbb+ (Secure). The outlook of both ratings is stable.

2014 2013 2012

Financial StrengthCredit RatingOutlook for Both Ratings

b++ (Good)bbb+ (secure)

stable

b++ (Good)bbb+ (secure)

stable

b++ (Good)bbb+ (secure)

stable

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

2. Group Risk & capital Management

2.1 capital Management

2014 aM best opinion (Excerpts from AM. Best Report)

Rating Rationale

“The ratings reflect the sound risk-adjusted capitalisation and well-diversified business profile of Arabia Insurance Company”.

“Although AIC’s location exposes it to significant economic, financial system and political risk, country risk factors are partially mitigated by the company’s level of diversification and business continuity plans”.

54

business profile

“AIC’s good level of geographical diversification offset the risk of business interruption caused by prevailing political unrest in the region. Along with the diversification of revenue, the company’s numerous branches and subsidiaries together with robust contingency plans will help the company to function in spite of adversity”.

Risk Management

“AIC has been developing its risk management framework over recent years, in line with international best practice. A corporate governance framework is well established and is relatively well advanced when compared to many of the company’s regional peers”.

“At present AIC assesses its capital position using a risk-based capital model. The assessment is made at both the group level, as well as by business line division and geographic location”.

capitalization

“AIC is expected to maintain a good level of risk-adjusted capitalisation in 2015. The company’s capital requirements are divided equally between underwriting risks and investment risks”.

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

2. Group Risk & capital Management

2.1 capital Management

55

liquidity

“AIC’s overall liquidity is adequate, given the significant holdings of cash and deposits. The company’s current liquidity ratio (total investments/[total liabilities - capital and surplus]) is expected to remain within the range of 85% and 90% over the coming two years”.

2.2 Risk Management

Risk Management strategy

The Group recognizes and understands that risk is inherent in seeking business opportunities, in developing and implementing new and original business strategies, and in dealing with local and global enterprises and communities.

While pursuing growth and achieving stakeholder’s needs and expectations, the Group is exposed to a variety of risks including credit, market, liquidity, underwriting, operational, compliance and other risks that require maintaining appropriate risk and control structure and ongoing oversight.

Through a robust enterprise risk management framework and effective Risk Committee role, these risks are identified, assessed, and managed in accordance with the risk appetite of the Group. Our Risk Strategy is embedded in our risk appetite framework defined and approved by the Board of Directors. Risk limits are being closely monitored by the Risk management Department and overseen by the Risk Committee and Chief Executive Officer.

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

2. Group Risk & capital Management

2.1 capital Management

56

Risk Management Responsibilities

The Board of Directors, as a governing body, oversees the activities of the Group and sets the tone and culture towards effective enterprise risk management.

The Risk Committee (RC), appointed by the Board of Directors, assists in fulfilling the Board’s risk oversight responsibilities and advises the Board on matters related to risk governance, risk policies and risk appetite setting.

The RC monitors the risk profile of the Group as well as oversees the structure and operation of the risk management and control systems.

It also ensures proper adherence to the company’s risk management policies, approves risk limits and assesses the adequacy of internal controls designed to respond and mitigate the risks to an acceptable level.

The Executive & Administrative Committee (EAC), headed by the Chief Executive Officer (CEO), is responsible for implementing sound and transparent risk management activities throughout the Group. The EAC maintains a risk culture where people are accountable by effectively managing risk, sponsors the ERm framework and provides necessary commitment and support to the Risk management Department.

The EAC also ensures that the business owners implement risk management policies in the areas for which they operate.

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

2. Group Risk & capital Management

2.2 Risk Management

57

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

The Risk management Department integrates the corporate risk culture, as well as promotes the risk and internal control awareness among all entities and functions within the Group. It maintains and updates the ERm framework, develops risk methodologies as well as advises the Risk Committee on the risk tolerance and risk profile.

Through the application of the Group ERm Framework and Risk metrics, the Risk management Department identifies, measures and reports all types of risks within the Group. The Risk Committee is continuously informed on material risks along with assessment of internal controls and risk management action plans.

2. Group Risk & capital Management

2.2 Risk Management

58

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

UNDERWRITING RISK

non-life / non-Medical Medical

premium Risk

Reserve Risk

catastrophic Risk

life

OPERATIONAL RISK

people Risk business process Risk

Information Technology Risk

IT system failures Risk

IT system Data security breaches

external events

natural Disaster

Man-Made Disaster

STRATEGIC RISK

business Risk

Governance Risk

Reputational Risk

external environmental Risk

economic Risk

societal Risk

Geopolitical Risk

FINANCIAL RISK

credit Risk

counterparty Default Risk

concentration Risk

Market Risk

equity Risk

Interest Rate Risk

spread Risk

others

asset-liability Management Risk

liquidity Risk

Insolvency Risk

COMPLIANCE RISK

legal Risk

Insurance laws & Regulations

Risk categories

The Group categorizes its risks to distinguish between the different types of risk exposures. The main five risk categories and related sub-categories are:

2. Group Risk & capital Management

2.2 Risk Management

59

Mitigation of Key Risks

underwriting Risk

The underwriting strategy attempts to ensure that the underwritten risks are well diversified in terms of type and amount of risk, industry and geography.

The Group mitigates this risk through underwriting guidelines and authority limits for issuing insurance contracts, as well as through diversification across lines of business and proper reinsurance arrangements.

Pricing benchmarks and formulas by line of business/type/category are set in the respective underwriting manuals, to serve as a guideline for risk commensurate premium quoting. A newly acquired software is used to continuously revise and enhance the pricing strategy.

claims settlement Risk

Clear documented claims settlement guidelines and limits by class of business are communicated to the claims functions.

Periodical reviews are carried out by the Head Office to ensure proper adherence to these guidelines and adequate internal control system.

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

2. Group Risk & capital Management

2.2 Risk Management

60

Reserving Risk

The reserves are calculated based on substantiated assumptions, methods and assessments. Periodical reviews by internal and external parties are being made to ensure that the reported reserves are reasonable and sufficient.

Reinsurance credit Risk

The Group minimizes its financial exposure arising from large claims by entering into reinsurance agreements that are suitable and adequate for the corresponding business. Reinsurance placements are done with international reinsurers and in alignment with the risk appetite of the Board.

concentration Risk

This is the risk that the total coverage sum insured is aggregated at the level of a single policy, contract, or client and a large loss would be generated in the case that this single contract is hit by a covered event. The Group mitigates this risk and protects its equity through the transfer of catastrophe risks and proper reinsurance arrangements.

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

2. Group Risk & capital Management

2.2 Risk Management

61

collection credit Risk

The financial loss that the Group could incur as a result of a change in the financial position of a counterparty is being managed through the Group’s credit policy and monitored through periodical analytical reports that highlight any breaches for the credit limits specified in the policy.

Market Risk

The Group closely monitors external market and regulatory developments through the supervision of the Board Investment Committee and Asset-Liability Committee.

The Board Investment Committee sets the guidelines and supervises the investment activities in accordance with the risk tolerance and limits described in the investment policy. The Committee receives periodically risk analysis reports (VaR simulation and risk scoring) and performance updates from our Treasury & Investment Department and seeks to reduce market risks by ensuring a high level of diversification both in its investment portfolio and direct investments.

The Asset-Liability Committee monitors the funding and cash budget and manages the liquidity risk in accordance with the Board risk appetite.

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

2. Group Risk & capital Management

2.2 Risk Management

62

operational Risk

business continuity Risk

The Group enhanced its understanding of natural hazards, man-made hazards, political risk exposures and other emergency events (system breakdown) that could severely affect the continuity of the operations if they occur.

Through the proper implementation of Arabia’s Business Continuity Plan, and the effective role of the BCm Committee, the Group is insuring that the business in the countries of operations can continue in the event of any unexpected incident.

IV. coRpoRaTe GoVeRnance, RIsK & capITal ManaGeMenT

RepoRT of THe boaRD of DIRecToRs

2. Group Risk & capital Management

2.2 Risk Management

consolIDaTeD fInancIal sTaTeMenT anD auDIToR’s RepoRT

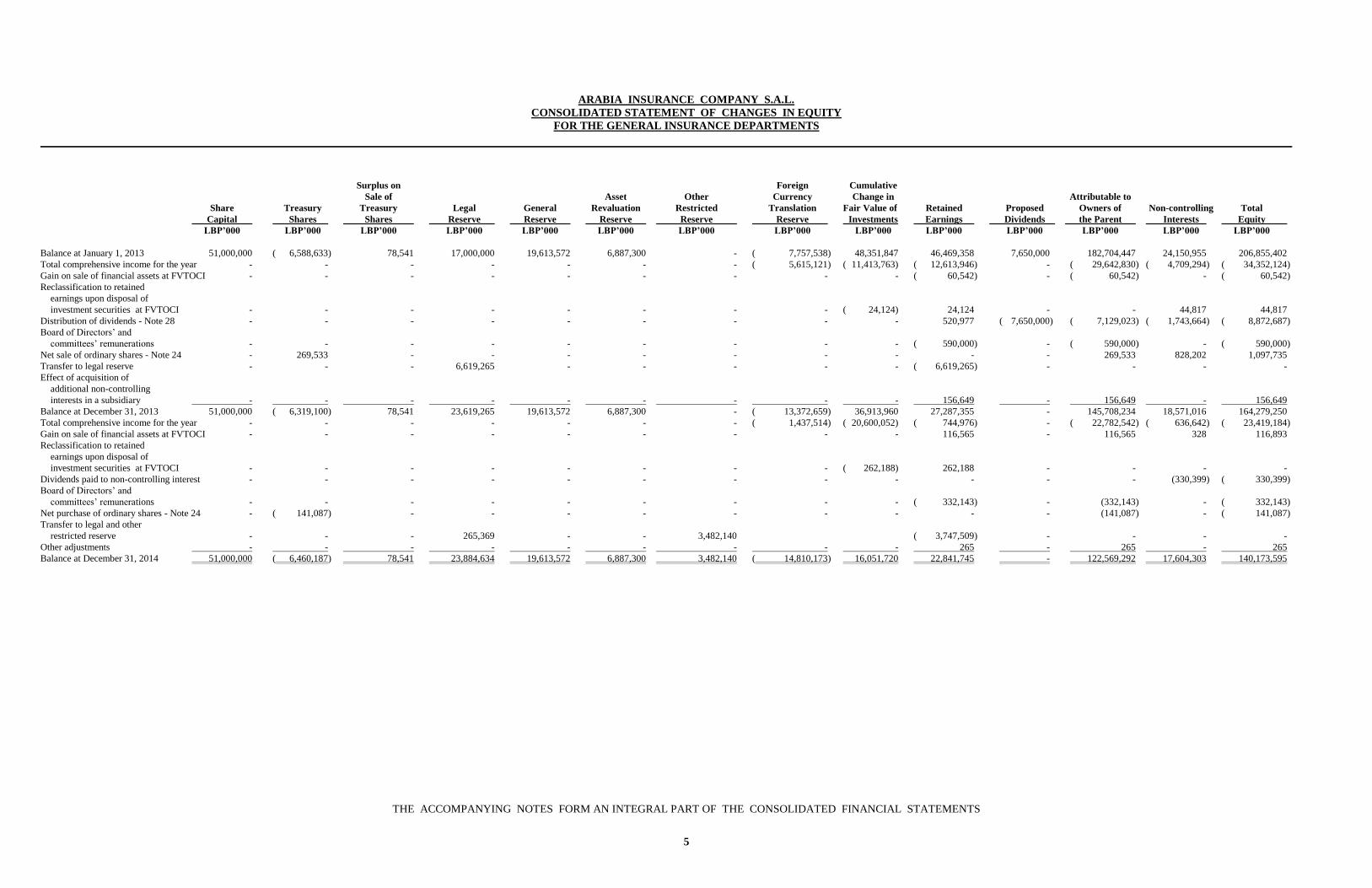

ARABIA INSURANCE COMPANY S.A.L.

CONSOLIDATED FINANCIAL STATEMENTS

AND INDEPENDENT AUDITOR'S REPORT

YEAR ENDED DECEMBER 31, 2014

ARABIA INSURANCE COMPANY S.A.L.

CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR'S REPORT

YEAR ENDED DECEMBER 31, 2014

TABLE OF CONTENTS

Page

Independent Auditor's Report 1-2

Consolidated Financial Statements:

Consolidated Statement of Financial Position 3-4

Consolidated Statement of Profit or Loss 5

Consolidated Statement of Profit or Loss and Other Comprehensive Income 6

Consolidated Statement of Changes in Equity 7

Consolidated Statement of Cash Flows 8

Life Division, Consolidated Statement of Assets and Liabilities -- Appendix I 9

Life Division, Consolidated Statement of Profit or Loss and Other

Comprehensive Income -- Appendix II 10

Life Division, Consolidated Statement of Cash Flows -- Appendix III 11

Notes to the Consolidated Financial Statements 12-79

ARABIA INSURANCE COMPANY S.A.L.

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

FOR THE GENERAL INSURANCE DEPARTMENTS

December 31,

ASSETS Notes 2014 2013

LBP’000 LBP’000

Cash and banks 5 159,056,574 146,386,111

Financial assets at fair value through profit or loss

(“FVTPL”) 6 16,001,389 13,676,662

Insurance receivables, net 7 57,116,711 70,809,425

Due from reinsurers 8 24,168,170 25,975,774

Due from related party company 23 448,900 325,146

Financial assets at fair value through

other comprehensive income (“FVTOCI”) 9 74,464,206 100,268,178

Financial assets at amortized cost 10 10,797,293 12,245,311

Reinsurance assets 20 47,045,462 62,953,057

Deferred acquisition costs 11 13,016,522 15,242,181

Other assets 12 4,534,690 3,533,321

Property and equipment 13 20,118,727 22,957,873

Intangible assets 14 761,293 472,218

Investment property 15 5,098,759 5,203,846

Total Assets 432,628,696 480,049,103

Assets of the Life Division -- Appendix I 99,060,396 91,284,524

Combined Assets of General Insurance

Departments and Life Division 531,689,092 571,333,627

THE ACCOMPANYING NOTES FORM AN INTEGRAL PART OF THE CONSOLIDATED

FINANCIAL STATEMENTS

2

ARABIA INSURANCE COMPANY S.A.L.

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

FOR THE GENERAL INSURANCE DEPARTMENTS

(Continued)

December 31,

LIABILITIES Notes 2014 2013

LBP’000 LBP’000

Due to banks 17 4,813,848 4,550,036

Insurance payables 18 26,313,563 28,688,649

Payables to insurance and reinsurance companies 13,621,431 11,675,848

Income tax payable 19 2,276,034 2,857,186

Due to life division 16 9,907,237 9,588,991

Accrued expenses and other liabilities 19 8,631,175 10,237,662

Provision for outstanding claims 20 118,695,136 133,982,610

Provision for unearned premiums 20 95,839,280 101,528,749

Unearned commission from reinsurers 2,636,576 2,582,120

Provision for employees' end-of-service indemnity 22 6,035,110 5,820,305

Provision for contingencies 22 2,968,992 3,821,724

Deferred tax liability 19 716,719 435,973

Total Liabilities 292,455,101 315,769,853

EQUITY

Share capital 24 51,000,000 51,000,000

Treasury shares 24 ( 6,460,187) ( 6,319,100)

Surplus on sale of treasury shares 24 78,541 78,541

Legal reserve 25 23,884,634 23,619,265

General reserve 19,613,572 19,613,572

Asset revaluation reserve 26 6,887,300 6,887,300

Other restricted reserve 37 3,482,140 -

Foreign currency translation reserve ( 14,810,173) ( 13,372,659)

Cumulative change in fair value of financial assets at FVTOCI 27 16,051,720 36,913,960

Retained earnings 22,841,745 27,287,355

Equity attributable to owners of the parent company 122,569,292 145,708,234

Non-controlling interests 29 17,604,303 18,571,016

Total Equity 140,173,595 164,279,250

Total Liabilities and Equity 432,628,696 480,049,103

Liabilities of the Life Division – Appendix 1 79,148,661 71,689,421

Net Assets of the Life Division – Appendix 1 19,911,735 19,595,103

Total Liabilities and Net Assets of the Life Division - Appendix I 99,060,396 91,284,524

Combined Liabilities and Equity of General Insurance

Departments and Life Division 531,689,092 571,333,627

THE ACCOMPANYING NOTES FORM AN INTEGRAL PART OF THE CONSOLIDATED

FINANCIAL STATEMENTS

3

ARABIA INSURANCE COMPANY S.A.L.

CONSOLIDATED STATEMENT OF PROFIT OR LOSS FOR THE

GENERAL INSURANCE DEPARTMENTS

Year Ended

December 31,

Notes 2014 2013

LBP’000 LBP’000

Net income/(loss) of General Insurance Departments:

Marine 3,100,002 3,574,347

Motor 2,070,457 ( 3,481,451)

Property 2,567,172 1,674,880

General accidents 3,367,572 1,124,851

Workmen's compensation ( 421,138) ( 401,552)

Medical ( 4,437,263) ( 2,394,452)

Reinsurance inwards ( 51,294) ( 388,229)

Net income/(loss) of general insurance departments

(net of allocated general and administrative expenses) 30 6,195,508 ( 291,606)

Provision for credit losses, net 7,8 ( 621,409) ( 4,188,184)

Net income/(loss) of insurance departments

(after provision for credit losses and allocated

general and administrative expenses) 5,574,099 ( 4,479,790)

Income/(loss) from Investments:

Interest on bank deposits 3,964,152 5,077,918

Interest and dividend income from investment securities at FVTOCI 1,376,872 1,230,443

Interest and dividend income from investment securities at amortized cost 781,527 840,434

Interest and dividend income from investment securities at FVTPL 464,894 549,614

Realized gain on investment securities at FVTPL 1,335,030 1,919,035

Unrealized gain on investment securities at FVTPL 6 87,898 826,347

Net gain/(loss) on disposal of investment securities 307,235 ( 58,338)

Net foreign exchange losses ( 670,618) ( 861,826)

Other income 311,198 472,115

Net loss from building ( 39,528) ( 62,254)

Net income from investments 7,918,660 9,933,488

Total income from general insurance departments and investments 13,492,759 5,453,698

General and administrative expenses unallocated to

General Insurance Departments 31 ( 10,890,958) ( 13,740,954)

Provision for contingencies 22 - ( 1,220,089)

Profit/(loss) before tax 2,601,801 ( 9,507,345)

Income tax expense 19 ( 2,509,276) ( 1,955,983)

Profit/(loss) for the year 92,525 ( 11,463,328)

Attributable to:

Owners of the parent company ( 744,976) ( 12,613,946)

Non-controlling interests 29 837,501 1,150,618

92,525 ( 11,463,328)

THE ACCOMPANYING NOTES FORM AN INTEGRAL PART OF THE CONSOLIDATED FINANCIAL

STATEMENTS

4

ARABIA INSURANCE COMPANY S.A.L.

CONSOLIDATED STATEMENT OF PROFIT OR LOSS

AND OTHER COMPREHENSIVE INCOME

FOR THE GENERAL INSURANCE DEPARTMENTS

Year Ended

December 31,

2014 2013

LBP’000 LBP’000

Profit/(loss) for the year 92,525 ( 11,463,328)

Other comprehensive income (“OCI”):

Items that will not be reclassified subsequently to profit or loss:

Net change in fair value of financial assets at FVTOCI – Note 27 ( 20,640,299) ( 11,672,214)

Items that may be reclassified subsequently to profit or loss: