ab variable products series fund, inc. · global thematic growth portfolio beginning on may 1,...

TRANSCRIPT

PROSPECTUS | MAY 1, 2020

AB Variable Products Series Fund, Inc.Class A Prospectus

AB VPSGlobal Thematic Growth Portfolio

Beginning on May 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, you may not be receivingpaper copies of the Portfolio’s shareholder reports from the insurance company that offers your contract unless you specifically requestpaper copies from the insurance company or from your financial intermediary. Instead of delivering paper copies of the reports, theinsurance company may choose to make the reports available on a website, and will notify you by mail each time a report is posted andprovide you with a website link to access the report. Instructions for requesting paper copies will be provided by your insurance company.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take anyaction. You may elect to receive shareholder reports and other communications from the insurance company or your financialintermediary electronically by following the instructions provided by the insurance company or by contacting your financial intermediary.

You may elect to receive all future reports in paper free of charge from the insurance company. You can inform the insurance company oryour financial intermediary that you wish to continue receiving paper copies of your shareholder reports by following the instructionsprovided by the insurance company or by contacting your financial intermediary. Your election to receive reports in paper will apply to allportfolio companies available under your contract with the insurance company.

This Prospectus describes the Portfolio that is available as an underlying investment through your variable contract. For information aboutyour variable contract, including information about insurance-related expenses, see the prospectus for your variable contract whichaccompanies this Prospectus.

The Securities and Exchange Commission has not approved or disapproved these securities or passed upon the adequacy of thisProspectus. Any representation to the contrary is a criminal offense.

Investment Products Offered

� Are Not FDIC Insured� May Lose Value� Are Not Bank Guaranteed

TABLE OF CONTENTS

Page

SUMMARY INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

ADDITIONAL INFORMATION ABOUT THE PORTFOLIO’S RISKS AND INVESTMENTS . . . . . . . . . . . . . . . . . . . . . . . . . 8

INVESTING IN THE PORTFOLIO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

MANAGEMENT OF THE PORTFOLIO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

DIVIDENDS, DISTRIBUTIONS AND TAXES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

GLOSSARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

FINANCIAL HIGHLIGHTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

APPENDIX A—HYPOTHETICAL INVESTMENT AND EXPENSE INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .A-1

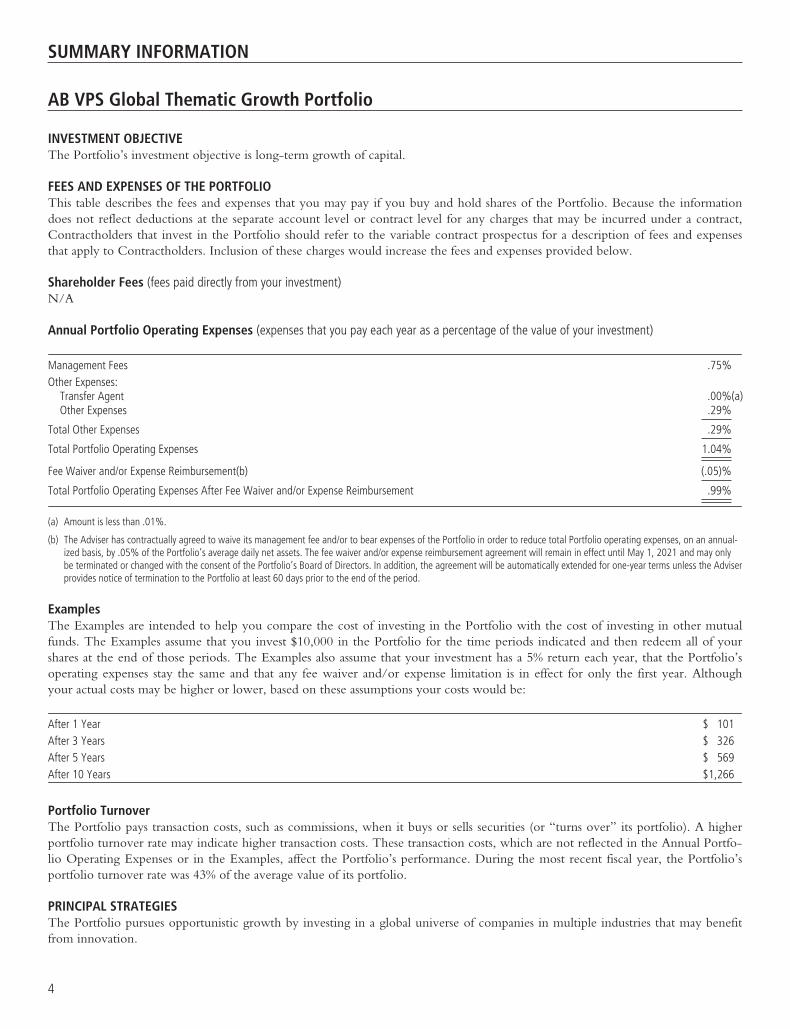

SUMMARY INFORMATION

AB VPS Global Thematic Growth Portfolio

INVESTMENT OBJECTIVEThe Portfolio’s investment objective is long-term growth of capital.

FEES AND EXPENSES OF THE PORTFOLIOThis table describes the fees and expenses that you may pay if you buy and hold shares of the Portfolio. Because the informationdoes not reflect deductions at the separate account level or contract level for any charges that may be incurred under a contract,Contractholders that invest in the Portfolio should refer to the variable contract prospectus for a description of fees and expensesthat apply to Contractholders. Inclusion of these charges would increase the fees and expenses provided below.

Shareholder Fees (fees paid directly from your investment)N/A

Annual Portfolio Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

Management Fees .75%Other Expenses:

Transfer Agent .00%(a)Other Expenses .29%

Total Other Expenses .29%

Total Portfolio Operating Expenses 1.04%

Fee Waiver and/or Expense Reimbursement(b) (.05)%

Total Portfolio Operating Expenses After Fee Waiver and/or Expense Reimbursement .99%

(a) Amount is less than .01%.

(b) The Adviser has contractually agreed to waive its management fee and/or to bear expenses of the Portfolio in order to reduce total Portfolio operating expenses, on an annual-ized basis, by .05% of the Portfolio’s average daily net assets. The fee waiver and/or expense reimbursement agreement will remain in effect until May 1, 2021 and may onlybe terminated or changed with the consent of the Portfolio’s Board of Directors. In addition, the agreement will be automatically extended for one-year terms unless the Adviserprovides notice of termination to the Portfolio at least 60 days prior to the end of the period.

ExamplesThe Examples are intended to help you compare the cost of investing in the Portfolio with the cost of investing in other mutualfunds. The Examples assume that you invest $10,000 in the Portfolio for the time periods indicated and then redeem all of yourshares at the end of those periods. The Examples also assume that your investment has a 5% return each year, that the Portfolio’soperating expenses stay the same and that any fee waiver and/or expense limitation is in effect for only the first year. Althoughyour actual costs may be higher or lower, based on these assumptions your costs would be:

After 1 Year $ 101After 3 Years $ 326After 5 Years $ 569After 10 Years $1,266

Portfolio TurnoverThe Portfolio pays transaction costs, such as commissions, when it buys or sells securities (or “turns over” its portfolio). A higherportfolio turnover rate may indicate higher transaction costs. These transaction costs, which are not reflected in the Annual Portfo-lio Operating Expenses or in the Examples, affect the Portfolio’s performance. During the most recent fiscal year, the Portfolio’sportfolio turnover rate was 43% of the average value of its portfolio.

PRINCIPAL STRATEGIESThe Portfolio pursues opportunistic growth by investing in a global universe of companies in multiple industries that may benefitfrom innovation.

4

The Adviser employs a combination of “top-down” and “bottom-up” investment processes with the goal of identifying the mostattractive securities worldwide, fitting into broader themes, which are developments that have broad effects across industries andcompanies. Drawing on the global fundamental research capabilities, the Adviser seeks to identify long-term secular growth trendsthat will affect multiple industries. The Adviser will assess the effects of these trends, on entire industries and on individual compa-nies. Through this process, the Adviser intends to identify key investment themes, which will be the focus of the Portfolio’sinvestments and which are expected to change over time based on the Adviser’s research.

In addition to this “top-down” thematic approach, the Adviser will also use a “bottom-up” analysis of individual companies thatfocuses on prospective earnings growth, valuation and quality of company management. The Adviser normally considers a largeuniverse of mid- to large-capitalization companies worldwide for investment.

The Portfolio invests in securities issued by U.S. and non-U.S. companies from multiple industry sectors in an attempt to maximizeopportunity, which should also tend to reduce risk. The Portfolio invests in both developed and emerging market countries. Undernormal market conditions, the Portfolio invests significantly (at least 40%—unless market conditions are not deemed favorable bythe Adviser) in securities of non-U.S. companies. In addition, the Portfolio invests, under normal circumstances, in the equitysecurities of companies located in at least three countries. The percentage of the Portfolio’s assets invested in securities of compa-nies in a particular country or denominated in a particular currency varies in accordance with the Adviser’s assessment of theappreciation potential of such securities.

The Portfolio may invest in any company and industry and in any type of equity security, listed and unlisted, with potential for capitalappreciation. It invests in well-known, established companies as well as new, smaller or less-seasoned companies. Investments in new,smaller or less-seasoned companies may offer more reward but may also entail more risk than is generally true of larger, establishedcompanies. The Portfolio may also invest in synthetic foreign equity securities, which are various types of warrants used internationallythat entitle a holder to buy or sell underlying securities, real estate investment trusts and zero-coupon bonds.

The Portfolio may, at times, invest in shares of exchange-traded funds, or ETFs, in lieu of making direct investments in equity secu-rities. ETFs may provide more efficient and economical exposure to the type of companies and geographic locations in which thePortfolio seeks to invest than direct investments.

Currencies can have a dramatic impact on equity returns, significantly adding to returns in some years and greatly diminishing themin others. Currency and equity positions are evaluated separately. The Adviser may seek to hedge the currency exposure resultingfrom securities positions when it finds the currency exposure unattractive. To hedge all or a portion of its currency risk, the Portfo-lio may, from time to time, invest in currency-related derivatives, including forward currency exchange contracts, futures contracts,options on futures contracts, swaps and options. The Adviser may also seek investment opportunities by taking long or short posi-tions in currencies through the use of currency-related derivatives.

The Portfolio may enter into other derivatives transactions, such as options, futures contracts, forwards and swaps. The Portfoliomay use options strategies involving the purchase and/or writing of various combinations of call and/or put options, including onindividual securities and stock indices, futures contracts (including futures contracts on individual securities and stock indices) orshares of ETFs. These transactions may be used, for example, to earn extra income, to adjust exposure to individual securities ormarkets, or to protect all or a portion of the Portfolio’s portfolio from a decline in value, sometimes within certain ranges.

PRINCIPAL RISKS• Market Risk: The value of the Portfolio’s assets will fluctuate as the stock or bond market fluctuates. The value of its invest-

ments may decline, sometimes rapidly and unpredictably, simply because of economic changes or other events, including publichealth crises (including the occurrence of a contagious disease or illness), that affect large portions of the market. It includes therisk that a particular style of investing, such as the Portfolio’s growth approach, may underperform the market generally.

• Foreign (Non-U.S.) Risk: Investments in securities of non-U.S. issuers may involve more risk than those of U.S. issuers.These securities may fluctuate more widely in price and may be more difficult to trade due to adverse market, economic, politi-cal, regulatory or other factors.

• Emerging Market Risk: Investments in emerging market countries may have more risk because the markets are less developedand less liquid, and because these investments may be subject to increased economic, political, regulatory or other uncertainties.

• Currency Risk: Fluctuations in currency exchange rates may negatively affect the value of the Portfolio’s investments or reduceits returns.

• Capitalization Risk: Investments in mid-capitalization companies may be more volatile than investments in large-capitalizationcompanies. Investments in mid-capitalization companies may have additional risks because these companies may have limitedproduct lines, markets or financial resources.

5

• Derivatives Risk: Derivatives may be difficult to price or unwind and leveraged so that small changes may produce dispropor-tionate losses for the Portfolio. Derivatives, especially over-the-counter derivatives, are also subject to counterparty risk.

• Focused Portfolio Risk: Investments in a limited number of companies may have more risk because changes in the value of asingle security may have a more significant effect, either negative or positive, on the Portfolio’s net asset value, or NAV.

• Management Risk: The Portfolio is subject to management risk because it is an actively-managed investment fund. The Ad-viser will apply its investment techniques and risk analyses in making investment decisions for the Portfolio, but there is no guar-antee that its techniques will produce the intended results. Some of these techniques may incorporate, or rely upon, quantitativemodels, but there is no guarantee that these models will generate accurate forecasts, reduce risk or otherwise perform asexpected.

As with all investments, you may lose money by investing in the Portfolio.

BAR CHART AND PERFORMANCE INFORMATIONThe bar chart and performance information provide an indication of the historical risk of an investment in the Portfolio byshowing:

• how the Portfolio’s performance changed from year to year over ten years; and

• how the Portfolio’s average annual returns for one, five and ten years compare to those of a broad-based securities market index.

The performance information does not take into account separate account charges. If separate account charges were included, an invest-or’s return would be lower. The Portfolio’s past performance, of course, does not necessarily indicate how it will perform in the future.

Bar Chart

Calendar Year End (%)

10

11

12 13 14 15 17 19

18

16

18.93

-23.23

13.52

23.26

5.06 2.89

36.6630.16

-9.79-0.62

During the period shown in the bar chart, the Portfolio’s:

Best Quarter was up 16.88%, 3rd quarter, 2010; and Worst Quarter was down -24.92%, 3rd quarter, 2011.

Performance TableAverage Annual Total Returns(For the periods ended December 31, 2019)

1 Year 5 Years 10 Years

Portfolio 30.16% 10.41% 8.21%

MSCI AC World Index (Net)(reflects no deduction for fees, expenses, or taxes except the reinvestment of dividends net ofnon-U.S. withholding taxes) 26.60% 8.41% 8.79%

INVESTMENT ADVISERAllianceBernstein L.P. is the investment adviser for the Portfolio.

PORTFOLIO MANAGERThe following table lists the person responsible for day-to-day management of the Portfolio’s portfolio:

Employee Length of Service Title

Daniel C. Roarty Since 2013 Senior Vice President of the Adviser

6

PURCHASE AND SALE OF PORTFOLIO SHARESThe Portfolio offers its shares through the separate accounts of participating life insurance companies (“Insurers”). You may onlypurchase and sell shares through these separate accounts. See the prospectus of the separate account of the Insurer for informationon the purchase and sale of the Portfolio’s shares.

TAX INFORMATIONThe Portfolio may pay income dividends or make capital gains distributions. The income and capital gains distributions are expectedto be made in shares of the Portfolio. See the prospectus of the separate account of the Insurer for federal income tax information.

PAYMENTS TO INSURERS AND OTHER FINANCIAL INTERMEDIARIESIf you purchase shares of the Portfolio through an Insurer or other financial intermediary, the Portfolio and its related companiesmay pay the intermediary for the sale of Portfolio shares and related services. These payments may create a conflict of interest byinfluencing the Insurer or other financial intermediary and your salesperson to recommend the Portfolio over another investment.Ask your salesperson or visit your financial intermediary’s website for more information.

7

ADDITIONAL INFORMATION ABOUT THE PORTFOLIO’S RISKS AND INVESTMENTS

This section of the Prospectus provides additional informationabout the Portfolio’s investment practices and risks, includingprincipal and non-principal strategies and risks. This Prospectusdoes not describe all of the Portfolio’s investment practices;additional descriptions of the Portfolio’s strategies, investments,and risks can be found in the Portfolio’s Statement of Addi-tional Information (“SAI”).

MARKET RISKThe market value of a security may move up or down, some-times rapidly and unpredictably. These fluctuations may cause asecurity to be worth less than the price originally paid for it, orless than it was worth at an earlier time. Market risk may affecta single issuer, industry, sector of the economy or the market asa whole. Global economies and financial markets are increas-ingly interconnected, which increases the probabilities thatconditions in one country or region might adversely impactissuers in a different country or region. Conditions affectingthe general economy, including political, social, or economicinstability at the local, regional, or global level may also affectthe market value of a security. Health crises, such as pandemicand epidemic diseases, as well as other incidents that interruptthe expected course of events, such as natural disasters, war orcivil disturbance, acts of terrorism, power outages and otherunforeseeable and external events, and the public response toor fear of such diseases or events, have and may in the futurehave an adverse effect on the Portfolio’s investments and netasset value and can lead to increased market volatility. Forexample, any preventative or protective actions that govern-ments may take in respect of such diseases or events may resultin periods of business disruption, inability to obtain rawmaterials, supplies and component parts, and reduced or dis-rupted operations for the Portfolio’s portfolio companies. Theoccurrence and pendency of such diseases or events could ad-versely affect the economies and financial markets either inspecific countries or worldwide.

DERIVATIVESThe Portfolio may, but is not required to, use derivatives forhedging or other risk management purposes or as part of itsinvestment strategies. Derivatives are financial contracts whosevalue depends on, or is derived from, the value of an under-lying asset, reference rate or index. The Portfolio may use de-rivatives to earn income and enhance returns, to hedge oradjust the risk profile of its investments, to replace more tradi-tional direct investments and to obtain exposure to otherwiseinaccessible markets.

There are four principal types of derivatives—options, futurescontracts, forwards and swaps—each of which is described be-low. Derivatives include listed and cleared transactions that areprivately negotiated and where the Portfolio’s derivative tradecounterparty is an exchange or clearinghouse and non-clearedbilateral “over-the-counter” transactions where, the Portfolio’sderivative trade counterparty is a financial institution.Exchange-traded or cleared derivatives transactions tend to be

subject to less counterparty credit risk than those that are pri-vately negotiated.

The Portfolio’s use of derivatives may involve risks that are dif-ferent from, or possibly greater than, the risks associated withinvesting directly in securities or other more traditionalinstruments. These risks include the risk that the value of a de-rivative instrument may not correlate perfectly, or at all, withthe value of the assets, reference rates, or indices that they aredesigned to track. Other risks include: the possible absence of aliquid secondary market for a particular instrument and possibleexchange-imposed price fluctuation limits, either of which maymake it difficult or impossible to close out a position when de-sired; and the risk that the counterparty will not perform itsobligations. Certain derivatives may have a leverage compo-nent and involve leverage risk. Adverse changes in the value orlevel of the underlying asset, note or index can result in a losssubstantially greater than the Portfolio’s investment (in somecases, the potential loss is unlimited).

The Portfolio’s investments in derivatives may include, but arenot limited to, the following:

• Forward Contracts. A forward contract is an agreementthat obligates one party to buy, and the other party to sell, aspecific quantity of an underlying commodity or othertangible asset for an agreed-upon price at a future date. Aforward contract generally is settled by physical delivery ofthe commodity or tangible asset to an agreed-upon location(rather than settled by cash) or is rolled forward into a newforward contract. The Portfolio’s investments in forwardcontracts may include the following:

– Forward Currency Exchange Contracts. The Portfoliomay purchase or sell forward currency exchange contractsfor hedging purposes to minimize the risk from adversechanges in the relationship between the U.S. Dollar andother currencies or for non-hedging purposes as a meansof making direct investments in foreign currencies, as de-scribed below under “Other Derivatives and Strategies—Currency Transactions”. The Portfolio, for example, mayenter into a forward contract as a transaction hedge (to“lock in” the U.S. Dollar price of a non-U.S. Dollarsecurity), as a position hedge (to protect the value of secu-rities the Portfolio owns that are denominated in a foreigncurrency against substantial changes in the value of theforeign currency) or as a cross-hedge (to protect the valueof securities the Portfolio owns that are denominated in aforeign currency against substantial changes in the value ofthat foreign currency by entering into a forward contractfor a different foreign currency that is expected to changein the same direction as the currency in which the secu-rities are denominated).

• Futures Contracts and Options on Futures Contracts.A futures contract is a standardized, exchange-traded agree-ment that obligates the buyer to buy and the seller to sell aspecified quantity of an underlying asset (or settle for cashthe value of a contract based on an underlying asset, rate or

8

index) at a specific price on the contract maturity date. Op-tions on futures contracts are options that call for the deliv-ery of futures contracts upon exercise. The Portfolio maypurchase or sell futures contracts and options thereon tohedge against changes in interest rates, securities (throughindex futures or options) or currencies. The Portfolio mayalso purchase or sell futures contracts for foreign currenciesor options thereon for non-hedging purposes as a means ofmaking direct investments in foreign currencies, as describedbelow under “Other Derivatives and Strategies—CurrencyTransactions”.

• Options. An option is an agreement that, for a premiumpayment or fee, gives the option holder (the buyer) the rightbut not the obligation to buy (a “call option”) or sell (a “putoption”) the underlying asset (or settle for cash an amountbased on an underlying asset, rate or index) at a specifiedprice (the exercise price) during a period of time or on aspecified date. Investments in options are considered spec-ulative. The Portfolio may lose the premium paid for themif the price of the underlying security or other asset de-creased or remained the same (in the case of a call option) orincreased or remained the same (in the case of a put option).If a put or call option purchased by the Portfolio were per-mitted to expire without being sold or exercised, its pre-mium would represent a loss to the Portfolio. ThePortfolio’s investments in options include the following:

– Options on Foreign Currencies. The Portfolio may investin options on foreign currencies that are privately nego-tiated or traded on U.S. or foreign exchanges for hedgingpurposes to protect against declines in the U.S. Dollar valueof foreign currency denominated securities held by thePortfolio and against increases in the U.S. Dollar cost ofsecurities to be acquired. The purchase of an option on aforeign currency may constitute an effective hedge againstfluctuations in exchange rates, although if rates move ad-versely, the Portfolio may forfeit the entire amount of thepremium plus related transaction costs. The Portfolio mayalso invest in options on foreign currencies for non-hedgingpurposes as a means of making direct investments in foreigncurrencies, as described below under “Other Derivativesand Strategies—Currency Transactions”.

– Options on Securities. The Portfolio may purchase orwrite a put or call option on securities. The Portfolio maywrite covered options, which means writing an option forsecurities the Portfolio owns, and uncovered options.

– Options on Securities Indices. An option on a securitiesindex is similar to an option on a security except that,rather than taking or making delivery of a security at aspecified price, an option on a securities index gives theholder the right to receive, upon exercise of the option,an amount of cash if the closing level of the chosen indexis greater than (in the case of a call) or less than (in thecase of a put) the exercise price of the option.

– Other Option Strategies. In an effort to earn extra in-come, to adjust exposure to individual securities or mar-kets, or to protect all or a portion of its portfolio from adecline in value, sometimes within certain ranges, the

Portfolio may use option strategies such as the concurrentpurchase of a call or put option, including on individualsecurities, stock indices, futures contracts (including onindividual securities and stock indices) or shares ofexchange-traded funds, or ETFs, at one strike price andthe writing of a call or put option on the same individualsecurity, stock index, futures contract or ETF at a higherstrike price in the case of a call option or at a lower strikeprice in the case of a put option. The maximum profitfrom this strategy would result for the call options from anincrease in the value of the individual security, stock in-dex, futures contract or ETF above the higher strike priceor, for the put options, from the decline in the value ofthe individual security, stock index, futures contract orETF below the lower strike price. If the price of the in-dividual security, stock index, futures contract or ETFdeclines, in the case of the call option, or increases, in thecase of the put option, the Portfolio has the risk of losingthe entire amount paid for the call or put options.

• Swap Transactions. A swap is an agreement that obligatestwo parties to exchange a series of cash flows at specifiedintervals (payment dates) based upon, or calculated by, refer-ence to changes in specified prices or rates (e.g., interest ratesin the case of interest rate swaps, currency exchange rates inthe case of currency swaps) for a specified amount of anunderlying asset (the “notional” principal amount). Generally,the notional principal amount is used solely to calculate thepayment stream, but is not exchanged. Most swaps are enteredinto on a net basis (i.e., the two payment streams are nettedout, with the Portfolio receiving or paying, as the case maybe, only the net amount of the two payments). Certain stand-ardized swaps, including certain interest rate swaps and creditdefault swaps, are subject to mandatory central clearing andare required to be executed through a regulated swap ex-ecution facility. Cleared swaps are transacted through futurescommission merchants (“FCMs”) that are members of centralclearinghouses with the clearinghouse serving as central coun-terparty, similar to transactions in futures contracts. Portfoliospost initial and variation margin to support their obligationsunder cleared swaps by making payments to their clearingmember FCMs. Central clearing is intended to reduce coun-terparty credit risks and increase liquidity, but central clearingdoes not make swap transactions risk free. The Securities andExchange Commission (“Commission”) may adopt similarclearing and execution requirements in respect of certainsecurity-based swaps under its jurisdiction. Privately nego-tiated swap agreements are two-party contracts entered intoprimarily by institutional investors and are not cleared througha third party, nor are these required to be executed on a regu-lated swap execution facility. The Portfolio’s investments inswap transactions include the following:

– Interest Rate Swaps, Swaptions, Caps and Floors. Interestrate swaps involve the exchange by the Portfolio withanother party of their respective commitments to pay orreceive interest (e.g., an exchange of floating-rate pay-ments for fixed-rate payments). Unless there is a counter-party default, the risk of loss to the Portfolio from interestrate swap transactions is limited to the net amount of

9

interest payments that the Portfolio is contractually obli-gated to make. If the counterparty to an interest ratetransaction defaults, the Portfolio’s risk of loss consists ofthe net amount of interest payments that the Portfoliocontractually is entitled to receive.

An option on a swap agreement, also called a “swaption”,is an option that gives the buyer the right, but not theobligation, to enter into a swap on a future date in ex-change for paying a market-based “premium”. A receiverswaption gives the owner the right to receive the totalreturn of a specified asset, reference rate, or index. Apayer swaption gives the owner the right to pay the totalreturn of a specified asset, reference rate, or index. Swap-tions also include options that allow an existing swap tobe terminated or extended by one of the counterparties.

The purchase of an interest rate cap entitles the purchaser,to the extent that a specified index exceeds a pre-determined interest rate, to receive payments of intereston a contractually-based principal amount from the partyselling the interest rate cap. The purchase of an interestrate floor entitles the purchaser, to the extent that a speci-fied index falls below a predetermined interest rate, toreceive payments of interest on an agreed principalamount from the party selling the interest rate floor. Itmay be more difficult for the Portfolio to trade or closeout interest rate caps and floors in comparison to othertypes of swaps.

Interest rate swap, swaption, cap and floor transactions, forexample, may be used in an effort to preserve a return orspread on a particular investment or a portion of the Port-folio’s portfolio or to protect against an increase in theprice of securities the Portfolio anticipates purchasing at alater date. The Portfolio may enter into interest rateswaps, caps and floors on either an asset-based or liability-based basis, depending upon whether it is hedging its as-sets or liabilities.

– Currency Swaps. The Portfolio may invest in currencyswaps for hedging purposes to protect against adversechanges in exchange rates between the U.S. Dollar andother currencies or for non-hedging purposes as a meansof making direct investments in foreign currencies, as de-scribed below under “Other Derivatives and Strategies—Currency Transactions”. Currency swaps involve the ex-change by the Portfolio with another party of a series ofpayments in specified currencies. Currency swaps may bebilateral and privately negotiated with the Portfolioexpecting to achieve an acceptable degree of correlationbetween its portfolio investments and its currency swapsposition. Currency swaps may involve the exchange ofactual principal amounts of currencies by the counter-parties at the initiation, and again upon the termination,of the transaction.

• Other Derivatives and Strategies

– Currency Transactions. The Portfolio may invest innon-U.S. Dollar-denominated securities on a currencyhedged or unhedged basis. The Adviser may actively man-age the Portfolio’s currency exposures and may seek

investment opportunities by taking long or short positionsin currencies through the use of currency-related de-rivatives, including forward currency exchange contracts,futures contracts and options on futures contracts, swapsand options. The Adviser may enter into transactions forinvestment opportunities when it anticipates that a foreigncurrency will appreciate or depreciate in value but securitiesdenominated in that currency are not held by the Portfolioand do not present attractive investment opportunities.Such transactions may also be used when the Adviser be-lieves that it may be more efficient than a direct investmentin a foreign currency-denominated security. The Portfoliomay also conduct currency exchange contracts on a spotbasis (i.e., for cash at the spot rate prevailing in the currencyexchange market for buying or selling currencies).

– Synthetic Foreign Equity Securities. The Portfolio mayinvest in different types of derivatives generally referred toas synthetic foreign equity securities. These securities mayinclude international warrants, or local access products.International warrants are financial instruments issued bybanks or other financial institutions, which may or maynot be traded on a foreign exchange. International war-rants are a form of derivative security that may give hold-ers the right to buy or sell an underlying security or abasket of securities representing an index from or to theissuer of the warrant for a particular price or may entitleholders to receive a cash payment relating to the value ofthe underlying security or index, in each case upon ex-ercise by the Portfolio. Local access products are similar tooptions in that they are exercisable by the holder for anunderlying security or a cash payment based upon thevalue of that security, but are generally exercisable over alonger term than typical options. These types of instru-ments may be American style, which means that they canbe exercised at any time on or before the expiration dateof the international warrant, or European style, whichmeans that they may be exercised only on the expirationdate.

Other types of synthetic foreign equity securities in whichthe Portfolio may invest include covered warrants, andlow exercise price warrants. Covered warrants entitle theholder to purchase from the issuer typically a financial in-stitution, upon exercise, common stock of an interna-tional company or receive a cash payment (generally inU.S. Dollars). The issuer of the covered warrants usuallyowns the underlying security or has a mechanism, such asowning equity warrants on the underlying securities,through which it can obtain the underlying securities.The cash payment is calculated according to a pre-determined formula, which is generally based on thedifference between the value of the underlying securityon the date of exercise and the strike price. Low exerciseprice warrants are warrants with an exercise price that isvery low relative to the market price of the underlyinginstrument at the time of issue (e.g., one cent or less). Thebuyer of a low exercise price warrant effectively pays thefull value of the underlying common stock at the outset.In the case of any exercise of warrants, there may be atime delay between the time a holder of warrants givesinstructions to exercise and the time the price of the

10

common stock relating to exercise or the settlement dateis determined, during which time the price of the under-lying security could change significantly. In addition, theexercise or settlement date of the warrants may be affectedby certain market disruption events, such as difficultiesrelating to the exchange of a local currency into U.S.Dollars, the imposition of capital controls by a local juris-diction or changes in the laws relating to foreign invest-ments. These events could lead to a change in the exercisedate or settlement currency of the warrants, or postpone-ment of the settlement date. In some cases, if the marketdisruption events continue for a certain period of time,the warrants may become worthless, resulting in a totalloss of the purchase price of the warrants.

The Portfolio will only acquire synthetic foreign equitysecurities covered warrants issued by entities deemed tobe creditworthy by the Adviser, which will monitor thecreditworthiness of the issuers on an ongoing basis.Investments in these instruments involve the risk that theissuer of the instrument may default on its obligation todeliver the underlying security or cash in lieu thereof.These instruments may also be subject to illiquid invest-ments risk because there may be a limited secondary mar-ket for trading the warrants. They are also subject, likeother investments in foreign securities, to foreign (non-U.S.) risk and currency risk.

– Eurodollar Instruments. Eurodollar instruments are essen-tially U.S. Dollar-denominated futures contracts or op-tions that are linked to the London Interbank OfferedRate (LIBOR). Eurodollar futures contracts enable pur-chasers to obtain a fixed rate for the lending of funds andsellers to obtain a fixed rate for borrowings. In July 2017,the United Kingdom Financial Conduct Authority, whichregulates LIBOR, announced a desire to phase out the useof LIBOR by the end of 2021. See “LIBOR Transitionand Associated Risk” below for additional information.

CONVERTIBLE SECURITIESPrior to conversion, convertible securities have the same gen-eral characteristics as non-convertible debt securities, whichgenerally provide a stable stream of income with generallyhigher yields than those of equity securities of the same or sim-ilar issuers. The price of a convertible security will normallyvary with changes in the price of the underlying equity secu-rity, although the higher yield tends to make the convertiblesecurity less volatile than the underlying equity security. Aswith debt securities, the market value of convertible securitiestends to decrease as interest rates rise and increase as interestrates decline. While convertible securities generally offer lowerinterest or dividend yields than non-convertible debt securitiesof similar quality, they offer investors the potential to benefitfrom increases in the market prices of the underlying commonstock. Convertible debt securities that are rated Baa3 or lowerby Moody’s Investors Service, Inc. or BBB- or lower by S&PGlobal Ratings or Fitch Ratings and comparable unrated secu-rities may share some or all of the risks of debt securities withthose ratings.

DEPOSITARY RECEIPTS AND SECURITIES OFSUPRANATIONAL ENTITIESThe Portfolio may invest in depositary receipts. AmericanDepositary Receipts, or ADRs, are depositary receipts typicallyissued by a U.S. bank or trust company that evidence owner-ship of underlying securities issued by a foreign corporation.Global Depositary Receipts, or GDRs, European DepositaryReceipts, or EDRs, and other types of depositary receipts aretypically issued by non-U.S. banks or trust companies and evi-dence ownership of underlying securities issued by either aU.S. or a non-U.S. company. Depositary receipts may notnecessarily be denominated in the same currency as the under-lying securities into which they may be converted. In addition,the issuers of the stock underlying unsponsored depositary re-ceipts are not obligated to disclose material information in theUnited States. Generally, depositary receipts in registered formare designed for use in the U.S. securities markets, and deposi-tary receipts in bearer form are designed for use in securitiesmarkets outside of the United States. For purposes ofdetermining the country of issuance, investments in depositaryreceipts of either type are deemed to be investments in theunderlying securities.

A supranational entity is an entity designated or supported bythe national government of one or more countries to promoteeconomic reconstruction or development. Examples ofsupranational entities include the World Bank (InternationalBank for Reconstruction and Development) and the EuropeanInvestment Bank. “Semi-governmental securities” are securitiesissued by entities owned by either a national, state or equiv-alent government or are obligations of one of such governmentjurisdictions that are not backed by its full faith and credit andgeneral taxing powers.

FORWARD COMMITMENTSForward commitments for the purchase or sale of securitiesmay include purchases on a when-issued basis or purchases orsales on a delayed delivery basis. In some cases, a forwardcommitment may be conditioned upon the occurrence of asubsequent event, such as approval and consummation of amerger, corporate reorganization or debt restructuring orapproval of a proposed financing by appropriate authorities(i.e., a “when, as and if issued” trade).

When forward commitments with respect to fixed-incomesecurities are negotiated, the price, which is generally expressedin yield terms, is fixed at the time the commitment is made,but payment for and delivery of the securities take place at alater date. Securities purchased or sold under a forwardcommitment are subject to market fluctuation and no interestor dividends accrue to the purchaser prior to the settlementdate. There is the risk of loss if the value of either a purchasedsecurity declines before the settlement date or the security soldincreases before the settlement date. The use of forward com-mitments helps the Portfolio to protect against anticipatedchanges in interest rates and prices.

11

ILLIQUID SECURITIESThe Portfolio limits its investments in illiquid securities to 15%of its net assets. Under Rule 22e-4 under the InvestmentCompany Act of 1940 (the “1940 Act”), the term “illiquidsecurities” means any security or investment that the Portfolioreasonably expects cannot be sold or disposed of in currentmarket conditions in seven calendar days or less without thesale or disposition significantly changing the market value ofthe investment.

The Portfolio may not be able to sell such securities and may notbe able to realize their full value upon sale. Restricted securities(securities subject to legal or contractual restrictions on resale)may be illiquid. Some restricted securities (such as securities is-sued pursuant to Rule 144A under the Securities Act of 1933(“Rule 144A Securities”) or certain commercial paper) may bemore difficult to trade than other types of securities.

INVESTMENT IN EXCHANGE-TRADED FUNDS AND OTHERINVESTMENT COMPANIESThe Portfolio may invest in shares of ETFs, subject to the re-strictions and limitations of the 1940 Act, or any applicablerules, exemptive orders or regulatory guidance thereunder.ETFs are pooled investment vehicles that seek to track the per-formance of a specific index or implement actively-managedinvestment strategies. Index ETFs will not track their under-lying indices precisely since the ETFs have expenses and mayneed to hold a portion of their assets in cash, unlike the under-lying indices, and the ETFs may not invest in all of the secu-rities in the underlying indices in the same proportion as theindices for varying reasons. The Portfolio will incur transactioncosts when buying and selling ETF shares, and indirectly bearthe expenses of the ETFs. In addition, the market value of anETF’s shares, which is based on supply and demand in themarket for the ETF’s shares, may differ from its NAV. Accord-ingly, there may be times when an ETF’s shares trade at a dis-count to its NAV.

The Portfolio may also invest in investment companies otherthan ETFs, as permitted by the 1940 Act, and the rules andregulations or exemptive orders thereunder. As with ETF in-vestments, if the Portfolio acquires shares in other investmentcompanies, Contractholders would bear, indirectly, the ex-penses of such investment companies (which may includemanagement and advisory fees), which to the extent notwaived or reimbursed, would be in addition to the Portfolio’sexpenses. The Portfolio intends to invest uninvested cashbalances in an affiliated money market fund as permitted byRule 12d1-1 under the 1940 Act. The Portfolio’s investmentin other investment companies, including ETFs, subjects thePortfolio indirectly to the underlying risks of those investmentcompanies.

LIBOR TRANSITION AND ASSOCIATED RISKThe Portfolio may invest in certain debt securities, derivatives orother financial instruments that utilize the London InterbankOffered Rate, or “LIBOR,” as a “benchmark” or “referencerate” for various interest rate calculations. In July 2017, theUnited Kingdom Financial Conduct Authority, which regulates

LIBOR, announced a desire to phase out the use of LIBOR bythe end of 2021. Although financial regulators and industryworking groups have suggested alternative reference rates, suchas European Interbank Offer Rate, Sterling Overnight InterbankAverage Rate and Secured Overnight Financing Rate, globalconsensus on alternative rates is lacking and the process foramending existing contracts or instruments to transition awayfrom LIBOR remains unclear. The elimination of LIBOR orchanges to other reference rates or any other changes or reformsto the determination or supervision of reference rates could havean adverse impact on the market for, or value of, any securitiesor payments linked to those reference rates, which may adverselyaffect the Portfolio’s performance and/or net asset value. Un-certainty and risk also remain regarding the willingness and abil-ity of issuers and lenders to include revised provisions in newand existing contracts or instruments. Consequently, the tran-sition away from LIBOR to other reference rates may lead toincreased volatility and illiquidity in markets that are tied toLIBOR, fluctuations in values of LIBOR-related investments orinvestments in issuers that utilize LIBOR, increased difficulty inborrowing or refinancing and diminished effectiveness of hedg-ing strategies, adversely affecting the Portfolio’s performance.Furthermore, the risks associated with the expected discontinua-tion of LIBOR and transition may be exacerbated if the worknecessary to effect an orderly transition to an alternative refer-ence rate is not completed in a timely manner. Because the use-fulness of LIBOR as a benchmark could deteriorate during thetransition period, these effects could occur prior to the end of2021.

LOANS OF PORTFOLIO SECURITIESFor the purpose of achieving income, the Portfolio may makesecured loans of portfolio securities to brokers, dealers andfinancial institutions (“borrowers”) to the extent permitted underthe 1940 Act or the rules and regulations thereunder (as suchstatute, rules or regulations may be amended from time to time)or by guidance regarding, interpretations of or exemptive ordersunder the 1940 Act. Under the Portfolio’s securities lendingprogram, all securities loans will be secured continuously by cashcollateral and/or non-cash collateral. Non-cash collateral willinclude only securities issued or guaranteed by the U.S.Government or its agencies or instrumentalities. The loans willbe made only to borrowers deemed by the Adviser to be cred-itworthy, and when, in the judgment of the Adviser, theconsideration that can be earned at that time from securitiesloans justifies the attendant risk. If a loan is collateralized by cash,the Portfolio will be compensated for the loan from a portion ofthe net return from the interest earned on the collateral after arebate paid to the borrower (in some cases this rebate may be a“negative rebate”, or fee paid by the borrower to the Portfolioin connection with the loan). If the Portfolio receives non-cashcollateral, the Portfolio will receive a fee from the borrowergenerally equal to a negotiated percentage of the market value ofthe loaned securities. For its services, the securities lending agentreceives a fee from the Portfolio.

The Portfolio will have the right to call a loan and obtain thesecurities loaned at any time on notice to the borrower within

12

the normal and customary settlement time for the securities.While the securities are on loan, the borrower is obligated topay the Portfolio amounts equal to any income or other dis-tributions from the securities. The Portfolio will not have theright to vote any securities during the existence of a loan, butwill have the right to regain ownership of loaned securities inorder to exercise voting or other ownership rights. When thePortfolio lends securities, its investment performance willcontinue to reflect changes in the value of the securities loaned.

The Portfolio will invest cash collateral in a money marketfund approved by the Portfolio’s Board of Directors (the“Board”) and expected to be managed by the Adviser. Anysuch investment will be at the Portfolio’s risk. The Portfoliomay pay reasonable finders’, administrative, and custodial feesin connection with a loan.

A principal risk of lending portfolio securities is that the bor-rower will fail to return the loaned securities upon terminationof the loan and that the value of the collateral will not be suffi-cient to replace the loaned securities.

PREFERRED STOCKThe Portfolio may invest in preferred stock. Preferred stock is aclass of capital stock that typically pays dividends at a specifiedrate. Preferred stock is generally senior to common stock, but issubordinated to any debt the issuer has outstanding. Accordingly,preferred stock dividends are not paid until all debt obligationsare first met. Preferred stock may be subject to more fluctuationsin market value, due to changes in market participants’ percep-tions of the issuer’s ability to continue to pay dividends, thandebt of the same issuer. These investments include convertiblepreferred stock, which includes an option for the holder to con-vert the preferred stock into the issuer’s common stock undercertain conditions, among which may be the specification of afuture date when the conversion may begin, a certain number ofcommon shares per preferred share, or a certain price per sharefor the common stock. Convertible preferred stock tends to bemore volatile than non-convertible preferred stock, because itsvalue is related to the price of the issuer’s common stock as wellas the dividends payable on the preferred stock.

REAL ESTATE INVESTMENT TRUSTS (REITS)REITs are pooled investment vehicles that invest primarily inincome-producing real estate or real estate related loans or in-terests. REITs are generally classified as equity REITs, mort-gage REITs or a combination of equity and mortgage REITs.Equity REITs invest the majority of their assets directly in realproperty and derive income primarily from the collection ofrents. Equity REITs can also realize capital gains by sellingproperties that have appreciated in value. Mortgage REITsinvest the majority of their assets in real estate mortgages andderive income from the collection of interest payments andprincipal. Similar to investment companies such as the Portfo-lio, REITs are not taxed on income distributed to shareholdersprovided they comply with several requirements of the InternalRevenue Code of 1986. The Portfolio will indirectly bear itsproportionate share of expenses incurred by REITs in whichthe Portfolio invests in addition to the expenses incurred di-rectly by the Portfolio.

REPURCHASE AGREEMENTS AND BUY/SELL BACKTRANSACTIONSThe Portfolio may enter into repurchase agreements. In a re-purchase agreement transaction, the Portfolio buys a security andsimultaneously agrees to sell it back to the counterparty at aspecified price in the future. However, a repurchase agreement iseconomically similar to a secured loan, in that the Portfolio lendscash to a counterparty for a specific term, normally a day or afew days, and is given acceptable collateral (the purchased secu-rities) to hold in case the counterparty does not repay the loan.The difference between the purchase price and the repurchaseprice of the securities reflects an agreed-upon “interest rate”.Given that the price at which the Portfolio will sell the collateralback is specified in advance, the Portfolio is not exposed to pricemovements on the collateral unless the counterparty defaults. Ifthe counterparty defaults on its obligation to buy back the secu-rities at the maturity date and the liquidation value of thecollateral is less than the outstanding loan amount, the Portfoliowould suffer a loss. In order to further mitigate any potentialcredit exposure to the counterparty, if the value of the securitiesfalls below a specified level that is linked to the loan amountduring the life of the agreement, the counterparty must provideadditional collateral to support the loan.

The Portfolio may enter into buy/sell back transactions, whichare similar to repurchase agreements. In this type of transaction,the Portfolio enters a trade to buy securities at one price andsimultaneously enters a trade to sell the same securities atanother price on a specified date. Similar to a repurchaseagreement, the repurchase price is higher than the sale priceand reflects current interest rates. Unlike a repurchase agree-ment, however, the buy/sell back transaction is considered twoseparate transactions.

RIGHTS AND WARRANTSRights and warrants are option securities permitting their hold-ers to subscribe for other securities. Rights are similar to war-rants except that they have a substantially shorter duration.Rights and warrants do not carry with them dividend or votingrights with respect to the underlying securities, or any rights inthe assets of the issuer. As a result, an investment in rights andwarrants may be considered more speculative than certainother types of investments. In addition, the value of a right or awarrant does not necessarily change with the value of the un-derlying securities, and a right or a warrant ceases to have valueif it is not exercised prior to its expiration date.

SHORT SALESThe Portfolio may make short sales as a part of overall portfoliomanagement or to offset a potential decline in the value of a secu-rity. A short sale involves the sale of a security that the Portfoliodoes not own, or if the Portfolio owns the security, is not to bedelivered upon consummation of the sale. When the Portfoliomakes a short sale of a security that it does not own, it must bor-row from a broker-dealer the security sold short and deliver thesecurity to the broker-dealer upon conclusion of the short sale.

If the price of the security sold short increases between the timeof the short sale and the time the Portfolio replaces the borrowedsecurity, the Portfolio will incur a loss; conversely, if the pricedeclines, the Portfolio will realize a short-term capital gain. Al-though the Portfolio’s gain is limited to the price at which it sold

13

the security short, its potential loss is theoretically unlimited be-cause there is a theoretically unlimited potential for the price of asecurity sold short to increase.

STANDBY COMMITMENT AGREEMENTSStandby commitment agreements are similar to put optionsthat commit the Portfolio, for a stated period of time, topurchase a stated amount of a security that may be issuedand sold to the Portfolio at the option of the issuer. Theprice and coupon of the security are fixed at the time ofthe commitment. At the time of entering into the agree-ment, the Portfolio is paid a commitment fee, regardless ofwhether the security ultimately is issued. The Portfolio willenter into such agreements only for the purpose of inves-ting in the security underlying the commitment at a yieldand price considered advantageous to the Portfolio andunavailable on a firm commitment basis.

There is no guarantee that a security subject to a standby commit-ment will be issued. In addition, the value of the security, if issued,on the delivery date may be more or less than its purchase price.Since the issuance of the security is at the option of the issuer, thePortfolio will bear the risk of capital loss in the event the value ofthe security declines and may not benefit from an appreciation inthe value of the security during the commitment period if the is-suer decides not to issue and sell the security to the Portfolio.

STRUCTURED PRODUCTSThe Portfolio may invest in certain hybrid derivatives-type in-struments that combine features of a traditional stock or bondwith those of, for example, a futures contract or an option.These instruments include structured notes and indexed secu-rities, commodity-linked notes and commodity index-linkednotes and credit-linked securities. The performance of thestructured product, which is generally a fixed-income security,is tied (positively or negatively) to the price or prices of anunrelated reference indicator such as a security or basket ofsecurities, currencies, commodities, a securities or commoditiesindex or a credit default swap or other kinds of swaps. Thestructured product may not pay interest or protect the principalinvested. The structured product or its interest rate may be amultiple of the reference indicator and, as a result, may beleveraged and move (up or down) more rapidly than the refer-ence indicator. Investments in structured products may providea more efficient and less expensive means of obtaining ex-posure to underlying securities, commodities or other de-rivatives, but may potentially be more volatile and carry greatertrading and market risk than investments in traditional secu-rities. The purchase of a structured product also exposes thePortfolio to the credit risk of the structured product.

Structured notes are derivative debt instruments. The interestrate or principal of these notes is determined by reference to anunrelated indicator (for example, a currency, security, or indicesthereof) unlike a typical note where the borrower agrees tomake fixed or floating interest payments and to pay a fixed sumat maturity. Indexed securities may include structured notes aswell as securities other than debt securities, the interest orprincipal of which is determined by an unrelated indicator.

Commodity-linked notes and commodity index-linked notesprovide exposure to the commodities markets. These are de-rivative securities with one or more commodity-linked compo-nents that have payment features similar to commodity futures

contracts, commodity options, commodity indices or similar in-struments. Commodity-linked products may be either equity ordebt securities, leveraged or unleveraged, and have both securityand commodity-like characteristics. A portion of the value ofthese instruments may be derived from the value of a commod-ity, futures contract, index or other economic variable.

ZERO-COUPON AND PAYMENT-IN-KIND BONDSZero-coupon bonds are issued at a significant discountfrom their principal amount in lieu of paying interest peri-odically. Payment-in-kind bonds allow the issuer to makecurrent interest payments on the bonds in additional bonds.Because zero-coupon bonds and payment-in-kind bonds donot pay current interest in cash, their value is generallysubject to greater fluctuation in response to changes inmarket interest rates than bonds that pay interest in cashcurrently. Both zero-coupon and payment-in-kind bondsallow an issuer to avoid the need to generate cash tomeet current interest payments. These bonds may involvegreater credit risks than bonds paying interest currently.Although these bonds do not pay current interest in cash,the Portfolio is nonetheless required to accrue interest in-come on such investments and to distribute such amountsat least annually to shareholders. Thus, the Portfolio couldbe required at times to liquidate other investments in or-der to satisfy its dividend requirements.

ADDITIONAL RISK AND OTHER CONSIDERATIONSInvestments in the Portfolio involve the risk considerationsdescribed below.

FOREIGN (NON-U.S.) SECURITIESInvesting in securities of foreign issuers involves special risksand considerations not typically associated with investing inU.S. securities. The securities markets of many foreign coun-tries are relatively small, with the majority of market capital-ization and trading volume concentrated in a limited numberof companies representing a small number of industries. ThePortfolio’s investments in securities of foreign issuers mayexperience greater price volatility and significantly lowerliquidity than a portfolio invested solely in securities of U.S.companies. These markets may be subject to greater influenceby adverse events generally affecting the market, and by largeinvestors trading significant blocks of securities, than is usual inthe United States. In addition, the securities markets of someforeign countries may be closed on certain days (e.g., localholidays) when the Portfolio is open for business. Under thesecircumstances, the Portfolio will be unable to add to or exit itspositions in certain foreign securities even though it mayotherwise be attractive to do so.

Securities registration, custody, and settlement may in someinstances be subject to delays and legal and administrative un-certainties. Foreign investment in the securities markets of cer-tain foreign countries is restricted or controlled to varyingdegrees. These restrictions or controls may at times limit orpreclude investment in certain securities and may increase thecosts and expenses of the Portfolio. In addition, the repatriationof investment income, capital or the proceeds of sales of secu-rities from certain countries is controlled under regulations,including in some cases the need for certain advance govern-ment notification or authority, and if a deterioration occurs ina country’s balance of payments, the country could impose

14

temporary restrictions on foreign capital remittances. Incomefrom certain investments held by the Portfolio could be re-duced by foreign income taxes, including withholding taxes.

The Portfolio also could be adversely affected by delays in, or arefusal to grant, any required governmental approval for repa-triation, as well as by the application to it of other restrictionson investment. Investing in local markets may require thePortfolio to adopt special procedures or seek local gov-ernmental approvals or other actions, any of which may in-volve additional costs to the Portfolio. These factors may affectthe liquidity of the Portfolio’s investments in any country andthe Adviser will monitor the effect of any such factor or factorson the Portfolio’s investments. Transaction costs, includingbrokerage commissions for transactions both on and off thesecurities exchanges, in many foreign countries are generallyhigher than in the United States.

Issuers of securities in foreign jurisdictions are generally notsubject to the same degree of regulation as are U.S. issuers withrespect to such matters as insider trading rules, restrictions onmarket manipulation, shareholder proxy requirements, andtimely disclosure of information. The reporting, accounting,and auditing standards of foreign countries may differ, in somecases significantly, from U.S. standards in important respects,and less information may be available to investors in securitiesof foreign issuers than to investors in U.S. securities. Sub-stantially less information is publicly available about certainnon-U.S. issuers than is available about most U.S. issuers.

The economies of individual foreign countries may differ favor-ably or unfavorably from the U.S. economy in such respects asgrowth of gross domestic product or gross national product, rate ofinflation, capital reinvestment, resource self-sufficiency, and bal-ance of payments position. Nationalization, expropriation or con-fiscatory taxation, currency blockage, political changes,government regulation, political or social instability, public healthcrises (including the occurrence of a contagious disease or illness),revolutions, wars or diplomatic developments could affect ad-versely the economy of a foreign country. In the event ofnationalization, expropriation, or other confiscation, the Portfoliocould lose its entire investment in securities in the country in-volved. In addition, laws in foreign countries governing businessorganizations, bankruptcy and insolvency may provide less pro-tection to security holders such as the Portfolio than that providedby U.S. laws.

The United Kingdom (the “U.K.”) formally withdrew from theEuropean Union (the “EU”) on January 31, 2020, and is now in atransition period through December 31, 2020, during which theU.K. and the EU will seek to agree on the terms of their futurerelationship. Although the U.K. will remain in the EU singlemarket and customs union during the transition period, the long-term nature of the U.K.’s relationship with the EU is unclear, andthere is considerable uncertainty as to when any agreement will bereached and implemented. The uncertainty surrounding the im-plementation and effect of the U.K. ceasing to be a member of theEU, the uncertainty in relation to the legal and regulatory frame-work that may apply to the U.K. and its relationship with theremaining members of the EU (including, in relation to trade) hascaused and is likely to cause increased economic volatility andmarket uncertainty globally. During the transition period and be-yond, the impact on the U.K. and European economies and thebroader global economy could be significant, resulting in increasedvolatility and illiquidity, currency fluctuations, impacts on

arrangements for trading and on other existing cross-border coop-eration arrangements (whether economic, tax, fiscal, legal, regu-latory or otherwise), and in potentially lower growth forcompanies in the U.K., Europe and globally, which could have anadverse effect on the value of the Portfolio’s investments.

Investments in securities of companies in emerging mar-kets involve special risks. There are approximately 100countries identified by the World Bank as Low Income,Lower Middle Income and Upper Middle Income coun-tries that are generally regarded as emerging markets.Emerging market countries that the Adviser currently con-siders for investment include:

ArgentinaBangladeshBelarusBelizeBrazilBulgariaChileChinaColombiaCroatiaCzech RepublicDominican RepublicEcuadorEgyptEl SalvadorGabonGeorgiaGhanaGreece

HungaryIndiaIndonesiaIraqIvory CoastJamaicaJordanKazakhstanKenyaLebanonLithuaniaMalaysiaMexicoMongoliaNigeriaPakistanPanamaPeruPhilippines

PolandQatarRussiaSaudi ArabiaSenegalSerbiaSouth AfricaSouth KoreaSri LankaTaiwanThailandTurkeyUkraineUnited Arab EmiratesUruguayVenezuelaVietnam

Countries may be added to or removed from this list at anytime.

Investing in emerging market securities imposes risks differentfrom, or greater than, risks of investing in domestic securitiesor in the securities of companies in foreign, developed coun-tries. These risks include: smaller market capitalization of secu-rities markets, which may suffer periods of relative illiquidity;significant price volatility; restrictions on foreign investment;and possible repatriation of investment income and capital. Inaddition, foreign investors may be required to register the pro-ceeds of sales and future economic or political crises could leadto price controls, forced mergers, expropriation or confiscatorytaxation, seizure, nationalization, or creation of governmentmonopolies. The currencies of emerging market countries mayexperience significant declines against the U.S. Dollar, anddevaluation may occur subsequent to investments in these cur-rencies by the Portfolio. Inflation and rapid fluctuations in in-flation rates have had, and may continue to have, negativeeffects on the economies and securities markets of certainemerging market countries.

Additional risks of emerging market securities may include:greater social, economic and political uncertainty and instability;more substantial governmental involvement in the economy; lessgovernmental supervision and regulation; unavailability of cur-rency hedging techniques; companies that are newly organizedand small; differences in auditing and financial reporting stan-dards, which may result in unavailability of material informationabout issuers; and less developed legal systems. In addition,

15

emerging securities markets may have different clearance and set-tlement procedures, which may be unable to keep pace with thevolume of securities transactions or otherwise make it difficult toengage in such transactions. Settlement problems may cause thePortfolio to miss attractive investment opportunities, hold a por-tion of its assets in cash pending investment, or be delayed indisposing of a portfolio security. Such a delay could result inpossible liability to a purchaser of the security.

FOREIGN (NON-U.S.) CURRENCIESThe Portfolio invests some portion of its assets in securitiesdenominated in, and receives revenues in, foreign currenciesand will be adversely affected by reductions in the value ofthose currencies relative to the U.S. Dollar. Foreign currencyexchange rates may fluctuate significantly. They are determinedby supply and demand in the foreign exchange markets, therelative merits of investments in different countries, actual orperceived changes in interest rates, and other complex factors.Currency exchange rates also can be affected unpredictably byintervention (or the failure to intervene) by U.S. or non-U.S.Governments or central banks or by currency controls orpolitical developments. In light of these risks, the Portfolio mayengage in certain currency hedging transactions, as describedabove, which involve certain special risks. The Portfolio mayalso invest directly in foreign currencies for non-hedging pur-poses directly on a spot basis (i.e., cash) or through derivativestransactions, such as forward currency exchange contracts, fu-tures contracts and options thereon, swaps and options as de-scribed above. These investments will be subject to the samerisks. In addition, currency exchange rates may fluctuate sig-nificantly over short periods of time, causing the Portfolio’sNAV to fluctuate.

MANAGEMENT RISK – QUANTITATIVE TOOLSThe Adviser may use investment techniques that incorporate, orrely upon, quantitative models. These models may not work asintended and may not enable the Portfolio to achieve itsinvestment objective. In addition, certain models may be con-structed using data from external providers, and these inputs maybe incorrect or incomplete, thus potentially limiting theeffectiveness of the models. Finally, the Adviser may change,enhance and update its models and its usage of existing models atits discretion.

INVESTMENT IN SMALLER, LESS-SEASONED COMPANIESInvestment in smaller, less-seasoned companies involves greaterrisks than are customarily associated with securities of moreestablished companies. Companies in the earlier stages of theirdevelopment often have products and management personnelthat have not been thoroughly tested by time or the market-place; their financial resources may not be as substantial as those

of more established companies. The securities of smaller, less-seasoned companies may have relatively limited marketabilityand may be subject to more abrupt or erratic market movementsthan securities of larger, more established companies or broadmarket indices. The revenue flow of such companies may beerratic and their results of operation may fluctuate widely andmay also contribute to stock price volatility.

FUTURE DEVELOPMENTSThe Portfolio may take advantage of other investment practicesthat are not currently contemplated for use by the Portfolio, orare not available but may yet be developed, to the extent suchinvestment practices are consistent with the Portfolio’s invest-ment objective and legally permissible for the Portfolio. Suchinvestment practices, if they arise, may involve risks that aredifferent from or exceed those involved in the practices de-scribed above.

CHANGES IN INVESTMENT OBJECTIVE AND POLICIESThe AB Variable Products Series (VPS) Fund’s (the “Fund”)Board may change the Portfolio’s investment objective withoutshareholder approval. The Portfolio will provide shareholders with60 days’ prior written notice of any change to the Portfolio’sinvestment objective. Unless otherwise noted, all other investmentpolicies of the Portfolio may be changed without shareholderapproval.

TEMPORARY DEFENSIVE POSITIONFor temporary defensive purposes to attempt to respond toadverse market, economic, political or other conditions, thePortfolio may invest in certain types of short-term, liquid, in-vestment grade or high-quality debt securities. While the Port-folio is investing for temporary defensive purposes, it may notmeet its investment objective.

PORTFOLIO HOLDINGSThe Portfolio’s SAI includes a description of the policies andprocedures that apply to disclosure of the Portfolio’s portfolioholdings.

CYBER SECURITY RISKMutual funds, including the Portfolio, are susceptible to cybersecurity risk. Cyber security breaches may allow an unauthorizedparty to gain access to Portfolio assets, Contractholder data, orproprietary information, or cause the Portfolio and/or its serviceproviders to suffer data corruption or lose operational function-ality. In addition, cyber security breaches in companies in whichthe Portfolio invests may affect the value of your investment inthe Portfolio.

16

INVESTING IN THE PORTFOLIO

HOW TO BUY AND SELL SHARESThe Portfolio offers its shares through the separate accounts ofthe Insurers. You may only purchase and sell shares throughthese separate accounts. See the prospectus of the separate ac-count of the Insurer for information on how to purchase and sellthe Portfolio’s shares. AllianceBernstein Investments, Inc.(“ABI”) may, from time to time, receive payments from Insurersin connection with the sale of the Portfolio’s shares through theInsurers’ separate accounts.

The Portfolio’s NAV is available by calling (800) 221-5672.

The Insurers maintain omnibus account arrangements with theFund in respect of the Portfolio and place aggregate purchase,redemption and exchange orders for shares of the Portfoliocorresponding to orders placed by the Insurers’ customers, orContractholders, who have purchased contracts from the In-surers, in each case, in accordance with the terms and con-ditions of the relevant contract. Omnibus accountarrangements maintained by the Insurers are discussed belowunder “Policy Regarding Short-Term Trading”.

The purchase or sale of the Portfolio’s shares is priced at thenext-determined NAV after the order is received in properform.

ABI may refuse any order to purchase shares. The Portfolioreserves the right to suspend the sale of its shares to the publicin response to conditions in the securities markets or for otherreasons.

The Portfolio expects that it will typically take up to three busi-ness days following the receipt of a redemption request inproper form to pay out redemption proceeds. However, whilenot expected, payment of redemption proceeds may take up toseven days from the day a request is received in proper form bythe Portfolio by the close of regular trading on any day theNew York Stock Exchange (the “Exchange”) is open(ordinarily, 4:00 p.m., Eastern time, but sometimes earlier, asin the case of scheduled half-day trading or unscheduledsuspensions of trading).

The Portfolio expects, under normal circumstances, to use cashor cash equivalents held by the Portfolio to satisfy redemptionrequests. The Portfolio may also determine to sell portfolio as-sets to meet such requests. Under certain circumstances,including stressed market conditions, the Portfolio may de-termine to pay a redemption request by accessing a bank lineof credit or by distributing wholly or partly in kind securitiesfrom its portfolio, instead of cash.

PAYMENTS TO FINANCIAL INTERMEDIARIESFinancial intermediaries, such as the Insurers, market and sellshares of the Portfolio and typically receive compensation forselling shares of the Portfolio. This compensation is paid fromvarious sources.

Insurers or your financial intermediary receivescompensation from ABI and/or the Adviser in severalways from various sources, which include some or all ofthe following:

- defrayal of costs for educational seminars and training;- additional distribution support; and- payments related to providing Contractholder

recordkeeping and/or administrative services.

ABI and/or the Adviser may pay Insurers or other financialintermediaries to perform recordkeeping and administrativeservices in connection with the Portfolio. Such payments willgenerally not exceed 0.35% of the average daily net assets ofthe Portfolio attributable to the Insurer.

Other Payments for Educational Support and DistributionAssistanceIn addition to the fees described above, ABI, at its expense,currently provides additional payments to the Insurers that sellshares of the Portfolio. These sums include payments to re-imburse directly or indirectly the costs incurred by the Insurersand their employees in connection with educational seminarsand training efforts about the Portfolio for the Insurers’employees and/or their clients and potential clients and mayinclude payments for distribution analytical data regardingPortfolio sales by the Insurer. The costs and expenses associatedwith these efforts may include travel, lodging, entertainmentand meals.

For 2020, ABI’s additional payments to these firms for educa-tional support and distribution assistance related to the Fund’sPortfolios are expected to be approximately $350,000. In 2019,ABI paid additional payments of approximately $370,000 forthe Fund’s Portfolios.

If one mutual fund sponsor that offers shares toseparate accounts of an Insurer makes greater dis-tribution assistance payments than another, theInsurer may have an incentive to recommend oroffer the shares of funds of one fund sponsor overanother.

Please speak with your financial intermediary tolearn more about the total amounts paid to yourfinancial intermediary by the Adviser, ABI and byother mutual fund sponsors that offer shares to In-surers that may be recommended to you. Youshould also consult disclosures made by your finan-cial intermediary at the time of purchase.

As of the date of this Prospectus, ABI anticipates that the In-surers or their affiliates that will receive additional payments foreducational support include:

AIGAXA Equitable

17

Brighthouse Life Insurance CompanyLincoln Financial DistributorsPacific Life Insurance CompanyPrudential FinancialRiversource Life Insurance CompanyTransamerica CapitalVariable Annuity Life Insurance Company

Although the Portfolio may use brokers and dealers that sellshares of the Portfolio to effect portfolio transactions, the Port-folio does not consider the sale of AB Mutual Fund shares as afactor when selecting brokers or dealers to effect portfoliotransactions.