a theoretical perspective of financial management in sick...

TRANSCRIPT

28

CHAPTER 2

A THEORETICAL PERSPECTIVE OF FINANCIAL

MANAGEMENT IN SICK UNITS

Industrial sickness in India, as it is elsewhere in the developing

countries of the world, is of great concern for all policy makers.

Crores of bank funds and institutional resources are locked up in sick

units --large, medium, and small. These out standings are in addition

to unpaid arrears of excise duty, sales tax, provident fund, wages,

power bills, and like.The incidence of sickness, quite understandably,

has been a cause of considerable concern to the government, financial

institutions, and banks. This has been stated several times in the

Economic Surveys prepared annually by the government.As sickness

leads to acute financial embarrassment, the finance manager has a

special interest in getting a forewarning of this sickness. Moreover, he

has an onerous responsibility in steering a sick unit towards

recovery.

Definition of Sickness

There are two ways of looking at insolvency. The Stock-Based

Insolvency occurs when the firm has a negative net worth, implying

that its assets are less than its debts. The Flow Based Insolvency

occurs when the operating cash--flows of the firm are not enough to

29

meet its obligations. Some of the definitions of sickness, as used in

India, by various agencies are given below.

The Reserve Bank of India defined a sick unit as ‚One which

has incurred cash losses for one year and, in the judgment of the

financing bank, is likely to incur cash losses for the current as well as

the following year, and / or there is an imbalance in the unit’s

financial structure, that is, the current ratio is less than 1:1 and debt

/equity ratio (total outside liabilities as a ratio of net worth) is

worsening.‛

The Companies (Second Amendment) Act, 2002 defines a ‚Sick

Company‛ as one:

(a) Which has accumulated losses in any financial year equal to 50

percent or more of its average net worth during four years

immediately preceding the financial year in question, or

(b) Which has failed to repay its debts within any consecutive

quarters on demand, for repayment by its creditors

An examination of the above definitions suggests that

regulatory authorities in India have, by and large, defined sickness in

terms of well- defined financial indicators. While such an approach

may be motivated by a desire to ensure that the agencies involved in

handling sick units operate within a uniform framework, it seems

deficient because sickness cannot always be captured so neatly by

30

quantitative financial indicators. We are inclined to offer broader

definitions along the following lines:

A business firm may be regarded as sick, if

(i) it faces financial embarrassment (arising out of its inability

to honor its obligations as and when they mature), and

(ii) Its viability is seriously threatened by adverse factors.

Causes of sickness

A firm remains healthy if it (i) operates in a reasonably

favorable environment, and (ii) has a fairly efficient management.

When these conditions are not satisfied, the firm is likely to become

sick. Hence sickness may be caused by:

a) Unfavorable external Environment

b) Managerial deficiencies

Unfavorable External Environment

The firm may be affected by one or more of the following

external factors over which it may hardly have any control.

Shortage of key inputs like power and basic raw materials

Changes in governmental policies with respect to excise

duties, customs duties, export duties, reservation etc.

Emergence of large capacity, leading to intense competitions

Development of new technology

Sudden decline in orders from the government

31

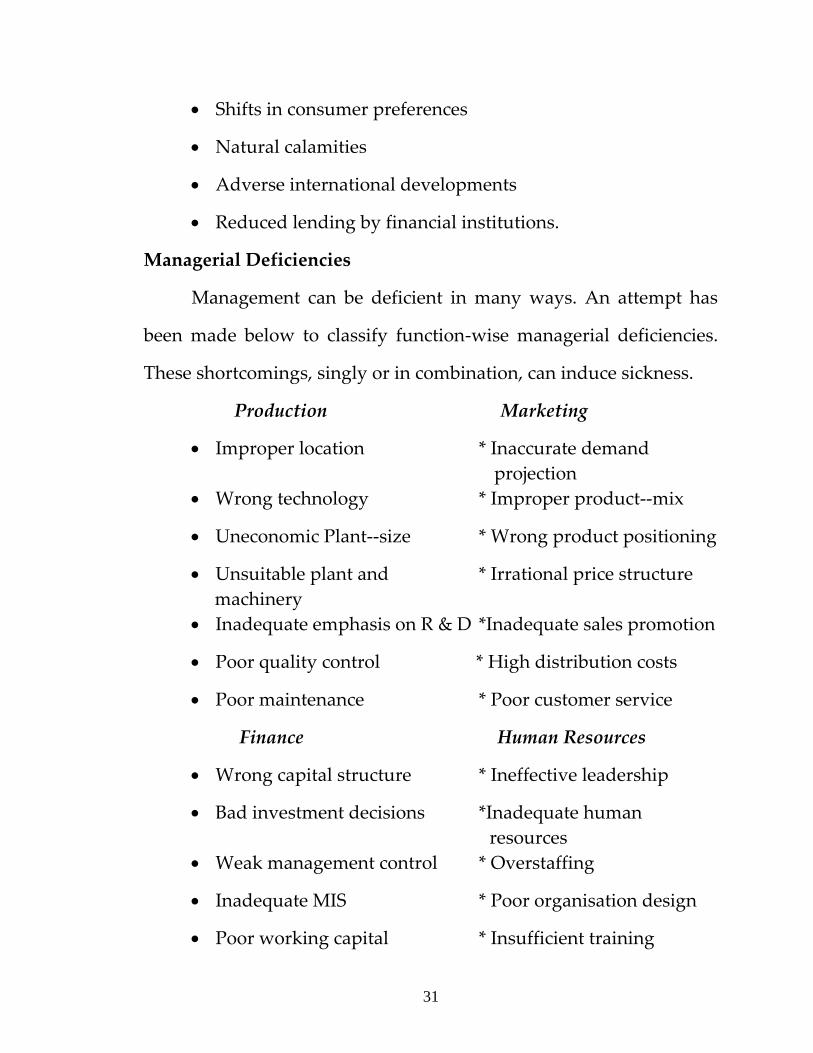

Shifts in consumer preferences

Natural calamities

Adverse international developments

Reduced lending by financial institutions.

Managerial Deficiencies

Management can be deficient in many ways. An attempt has

been made below to classify function-wise managerial deficiencies.

These shortcomings, singly or in combination, can induce sickness.

Production Marketing

Improper location * Inaccurate demand

projection

Wrong technology * Improper product--mix

Uneconomic Plant--size * Wrong product positioning

Unsuitable plant and * Irrational price structure

machinery

Inadequate emphasis on R & D *Inadequate sales promotion

Poor quality control * High distribution costs

Poor maintenance * Poor customer service

Finance Human Resources

Wrong capital structure * Ineffective leadership

Bad investment decisions *Inadequate human

resources

Weak management control * Overstaffing

Inadequate MIS * Poor organisation design

Poor working capital * Insufficient training

32

management

Strained relations with * Irrational compensation

investors

RBI Study on Causes of Sickness

A study conducted by RBI on the causes of industrial sickness,

concluded as follows. ‚A broad generalization regarding important

causes of industrial sickness emerges. It is observed that the factor

most often responsible for industrial sickness can be defined as

‘Management’.This may take the form of poor production

management, poor labour management, poor resource management,

lack of professionalism, dissensions within the management, or even

dishonest management‛.

Symptoms of sickness

Sickness does not occur overnight, but develops gradually over time.

A firm which is becoming sick shows symptoms which indicate that

trouble lies ahead of it. Some of the common symptoms are:

Delay or default in payment to suppliers

Irregularity in bank account

Delay or default in payment to banks and financial

institutions

Non-submission of information to banks and financial

institutions

33

Frequent requests to banks and financial institutions for

additional credit.

Decline in capacity utilization

Poor maintenance of plant and machinery

Low turnover of assets

Accumulation of inventories

Inability to take trade discount

Excessive turnover of personnel

Extension of accounting period

Resort to ‘creative accounting’ which seeks to present a

better financial picture than what it really is

Decline in the price of equity shares and debentures.

Revival of a sick unit

When an industrial unit is identified as sick, a viability study

should be conducted to assess whether the unit can be revived /

rehabilitated within a reasonable period. If the viability study

suggests that a unit can be rehabilitated, a suitable plan for

rehabilitation must be formulated. If the viability study indicates that

the unit is ‚better dead than alive‛, steps should be taken to liquidate

it expeditiously.

34

Viability study

A reasonably comprehensive assessment of the various aspects

of the working of a unit, a viability study, should cover the following:

Market

Operations

Finance

Human resources

Environment

The viability study may suggest one of the following:

(a) The unit can be revived by adopting one or more of the following

measures: debt restructuring, infusion of funds, correction of

functional deficiencies, granting of special reliefs and concessions

by the government, replacement of existing management because

of its incompetence and / or dishonesty.

(b) The unit is not potentially viable- This essentially implies that the

benefits expected from remedial measures are less than the cost of

such remedial measures.

Revival programmes:-The revival programme usually involves the

following:

Settlement with Creditors: - A sick unit is normally in straitened

financial circumstances and is not able to honor its commitments to

its creditors (financial institutions, debenture holders, commercial

banks, suppliers, and governmental authorities). To alleviate its

35

financial distress, a settlement scheme has to be worked out which

may involve one or more of the following: rescheduling of principal

and interest payment; waiver of interest; conversion of debt into

equity; payment of arrears in installments.

Provision of additional Capital: - Typically, a revival programme

entails provision of additional Capital. This may be required for

modernisation and repair of plant and machinery, for purchase of

balancing equipment, for sustaining a new marketing drive, and for

enhanced working capital needed to support a higher level of

operations. The additional capital has to be provided on concessional

terms, at least for the initial years, so that the financial burden on the

unit is not high.

Divestment and Disposal: - The revival programme may involve

divestment of unprofitable plants and operations and disposal of

slow moving and obsolete stocks. The thrust of these actions should

be to strengthen the liquidity of the unit and facilitate reallocation of

resources for enhancing the profitability of the unit.

Reformulation of product - Market Strategy: - Many a business

failure can be traced to an ill-conceived product -market strategy. For

reviving a sick unit, its product- market strategy may have to be

significantly reformulated to improve the prospects of its profitable

recovery. This, of course, calls for a great deal of imagination and

penetrating analysis.

36

Modernisation of Plant and Machinery: - In order to improve

manufacturing efficiency, plant and machinery may have to be

modernised, renovated, and repaired. This may be essential for

attaining certain cost standards and quality norms for competing

effectively in the market place.

Reduction in Manpower: - Generally sick firms tend to be over-

staffed. The revival programme must seek to reduce superfluous

manpower. Remember an old managerial saying: ‚The leaner the

organisation, the greater are its chances of survival.‛ Golden

Handshakes often involving paying significant retrenchment

compensation are a better proposition than carrying redundant

manpower on the payroll of the unit.

Strict Control over Costs: - A profitable organisation can afford

wastefulness and laxity in its expenditures. A tottering firm, seeking

to regain its health and vigor, has to exercise strict control over its

discretionary expenses. A zero-base review of all the discretionary

expenses may be undertaken to eliminate programmes and activities

which are a drain on the finances of the firm.

Streamlining of Operations: - Manufacturing, purchasing, and selling

operations have to be meticulously examined so that they can be

streamlined. Value engineering, standardization, simplification, cost-

benefit analysis, and other approaches should be exploited fully to

improve the efficiency of the operations.

37

Improvement in Managerial Systems: - The managerial systems in

the unit must be strengthened. In this exercise, greater attention may

have to be paid to the following:

Environmental monitoring

Organisational structure

Responsibility accounting

Management information system

Budgetary control

Workers Participation: - In general, workers participation in

management enhances employee commitment, motivation, and

morale. Further, the suggestions offered by the workers result in

improvements that lead to higher manufacturing efficiency and

productivity. A sick organization, which is being revived, can

perhaps benefit, even more from workers; participation in

management. During the revival phase, the dedication, commitment,

and support of workers is indispensable and meaningful: workers

participation and involvement goes a long way in ensuring this.

Change of Management: - A change in management may be

necessary where the present management is dishonest and / or

incompetent. It has been observed that a new chief executive, who is

competent, committed, and up righteous, can often bring about

dramatic results. A classic example of this phenomenon was the

38

dramatic turnaround of Chrysler Corporation under the stewardship

of Lee Iacocca.

Merger with a healthy company: - If a sick firm cannot pull itself by

its own bootstraps, the option of merger with a healthy firm must be

seriously explored. The healthy firm can leverage its resources to

revive the sick firm.

Debt restructuring

Mechanisms for Debt Restructuring: - Financially distressed

companies that have difficulty in servicing their debt resort to debt

restructuring aimed primarily at reducing the burdens of debt. The

mechanism for debt restructuring depends on how a financially

distressed company is classified. Financially distressed companies

may be classified into the following categories.

A. Companies that fall under the definition of a ‘ Sick Industrial

Company’ (Industrial company which is more than five

years old and which has accumulated losses equal to or

exceeding its entire net worth) as per Section 2(0) of the Sick

Industrial Companies ( Special Provisions) Act 1985 ( SICA).

B. Companies that fall under the definition of a ‘Potentially

Sick Company’ as per Section 23 of SICA.

C. Companies that do not fall under both the above categories.

39

For companies falling under A: Debt restructuring becomes a

statutory process under the jurisdiction of the Board for Industrial

and Financial Reconstruction (BIFR) set up under SICA.

Companies that fall under B: Cannot avail of the BIFR route for

debt restructuring. Such companies have to negotiate with the

existing lenders to restructure their debt in a mutually acceptable

manner. If a potentially sick company has loan accounts ( Rs. 20 crore

and above) which are under a consortium financing arrangement,

the Corporate Debt Restructuring (CDR) Guidelines issued by the

RBI are applicable. The CDR scheme facilitates a restructuring of

consortium loans through a non- judicial process by creating a legally

binding Debtor- Creditor Agreement (DCA) and an Inter- Creditor

Agreement (ICA) which have to be ratified by lenders who have

provided at least 75 percent of the loans.

If the loans are not covered by the CDR Scheme or if the CDR is

not possible because of inadequate support by concerned lenders,

debt restructuring may be done through a Negotiated Settlement

(NS) or a One Time Settlement (OTS). Under and NS the amount due

is negotiated and crystallized and becomes payable over an agreed

period, usually not more than 18 months. Under an OTS, the amount

due is negotiated and crystallized and becomes payable within a

short period of three to six months.

40

Companies that fall under C have to negotiate with their

respective lenders and follow a process which is similar to that

followed for companies that all under B.

Common Elements: - Excluding the cases of Negotiated Settlement

(NS) or a One Time Settlement (OTS), the common elements of debt

restructuring schemes are as follows:

Interest Rate Relief: - The contracted interest rate may be reduced if

the borrower is not in a position to achieve cash break-even.

Deferment of Past Interest Dues: - The areas of interest, up to the

restructuring date, are deferred and a repayment schedule spread

over a period of time that has been worked out.

Waiver of Penalties: - levied in the form of compound interest and

liquidated damages for non-payment of dues on time is generally

waived.

Reschedulement of Loan Repayment: - The loan repayment schedule

is reworked, after assessing the cash flow position.

Reduction in the Loan: - Amount In a situation where the borrower

cannot potentially service the loan, lenders may write off a portion of

the loan.

One of the ongoing debates in Kerala is about what course the

administrators would choose to keep the State's mammoth public

sector on an even keel. The issue has come to the fore even as the new

incumbents are grappling with possible ways to get around the

41

severe financial crisis that the State is facing. And the public sector,

with a fair share of loss-making enterprises, which need urgent

revival measures, including significant financial back-up, has not

made the task of the policy-makers any easier.

With a total investment of close to Rs 14,000 crore, the returns

from 100-odd public sector undertakings over the years have been

miserably low. As per the latest estimates, while 45 enterprises made

a total profit of Rs 285 crore, as many as 50 others accounted for a loss

of Rs 332 crore, leaving as net position a combined loss of Rs 47 crore.

Also, among the 50 loss-making undertakings, 46 have incurred cash

losses.

More disturbing is the fact that 60 undertakings have totted up

accumulated losses to the tune of Rs 2,616 crore and the net worth

has turned negative in the case of 37 of them. The picture may still be

incomplete considering that the audit of accounts has been in arrears,

ranging from one year to 11 years, in 66 undertakings.

It is pointed out that while the performance of the public

utilities such as the Electricity Board, Transport Corporation and the

Water Authority may reflect the compulsions of their role as the

providers of basic social infrastructure, the real test ahead for the

Government will be to tackle the chronic problems plaguing the

42

manufacturing sector, comprising 60 units and 12 cooperatives,

under the Industries Department. This assumes significance as these

public sector companies straddle the State's industrial map, leaving

little space for private capital to find even a toe-hold presence. The

Government’s resolve to rev up industrialization by attracting

private investment will thus have to necessarily be integrated to

efforts to streamline the working of the public sector units.

Apart from a few companies such as Kerala Minerals and

Metals Ltd, Travancore Titanium Products Ltd and Malabar

Cements, which have acquitted themselves well, in terms of

consistency in making profits, the records of most of the other units

leave much to be desired. And a good number of them with large

accumulated losses and negative net worth are currently in the

revival mode.

The Industries Department had brought out an elaborate White

Paper in 1998 on the status of the public sector units, and with

prescriptions to remedy the situation. According to the White Paper,

the total long-term funds with the public sector units amounted to Rs

1,300 crore as on March 31st1996. This comprised equity infusion of

Rs 610 crore, Government loans of Rs 207 crore and long-term loans

of Rs 484 crore from financial institutions.

43

Against this, the actual asset creation had been only to the extent of

Rs 721 crore, including capital work-in-progress. The balance amount

had gone towards funding accumulated losses. Even the gross block

of Rs 721 crore had depreciated by more than 50 per cent with the net

fixed assets standing at Rs 290 crore.

An immediate task in this context is technology up--gradation,

at most of the units which are 20-25 years old. It is estimated that an

investment of Rs 350 crore is required to restore the assets to the

original levels of gross block. Some of the reasons being cited for the

lackluster performance of the public sector units are lack of

professionalism in management at various levels, absence of timely

analysis of problems and reluctance on the part of the bankers to

extend need-based working capital credit to the units.

The paper has also pointed its finger to less productive, high-

cost, and excess manpower in many a unit and called for a strategy to

tackle the issue. It has also suggested mergers or amalgamations of

enterprises which are engaged in the same line of business to

produce an Approach Paper for State Level Public Enterprises, the

gist of which is that the Government would not continue to prop up

loss-making public sector entities.

44

Restructuring is the term the paper uses to describe what the

Government proposes to do in the case of such units and this

encompasses privatization. The target was to restructure 25

enterprises by June 2003. The nature of the restructuring process

would be decided on a case-by-case basis. The Enterprise Reforms

Committee (ERC) constituted by the Government would be

presenting a detailed proposal on each such case to the State

Planning Board. After scrutinizing the proposal, the Planning Board

would make suitable recommendations to the State Cabinet for final

decision. The restructuring process would be a time-bound

operation. The ERC had been invested with sufficient powers to tell

the Government what should be done with each public sector unit

(PSU).

The trade unions too had by now realized the inevitability of

addressing the problem of Kerala's public sector objectively. These

units were running up an annual loss of about Rs. 40,000 per

employee. Public spending on PSUs had to be reduced so that the

savings achieved thus could be devoted for poverty reduction and

infrastructure development

A more radical suggestion hinted at in the paper is the closure

of companies with high net worth erosion and where many past

efforts at revival had not yielded results. In the light of the findings in

45

the White Paper, the previous Government had taken a few reluctant

steps such as closing down of couple of unviable units such as Sidkel

Television and Keltron Power Devices, where employees were

relieved under Voluntary Retirement schemes. In the case of pruning

of excess manpower, the Government's initiative was limited to

sending out 625 employees of the Kerala State Electronics

Development Corporation (Keltron), a holding company, and this

was under VRS. In regard to liquidating the liabilities to banks and

financial institutions, the Government was able to persuade the

creditors of some of the companies to come around for a one-time

settlement which involved writing off accumulated interests. But the

institutions had been rather cautious in this respect and in some cases

such as that of Keltron, settlement packages have been pending for

some time, for want of agreements on key issues. On the financial

side, the previous Government had created a Kerala Industry

Revitalisation Fund (KIRF) with an initial corpus of Rs 250 crores.

The fund was constituted with budgetary support, as also with

money raised through issue of bonds worth Rs 180 crores. The funds

were designed to be allocated to units after signing Performance

Contracts. While allocations have already been made to certain units,

the financial crisis that gripped the Government in the last few

months had come in the way of further allocations, and this had

46

landed units which were in urgent need of working capital and other

funds--infusion, in grave operational problems.

One of the options being talked about to streamline the public

sector is disinvestment. In the early nineties, Government had

decided to go in for disinvestment in some of the loss-making units,

and the Public Sector Restructuring and Internal Audit Board (RIAB)

prepared a list of such units, and invited offers. However, the

response was extremely poor.

The only firm offer was for the vitamin-A plant of the Kerala

State Drugs and Pharmaceuticals Ltd (KSDP) and it came from the

National Dairy Development Board (NDDB). But the bidders made a

hasty retreat in the face of stiff political opposition to the move. As

the observers point out, it will require not just hard decisions by the

Government, but also earnest efforts on its part to bring about a

political consensus to tackle the issues confronting the public sector.

Restructuring

Restructuring is the corporate management term for the act of

partially dismantling or otherwise reorganizing a company for the

purpose of making it more profitable. Also known as Corporate

Restructuring, Debt Restructuring and Financial Restructuring.

Restructuring is often done as part of a bankruptcy or of a strategic

47

takeover by another firm, such as a leveraged buyout by a private

equity firm, or when the firm is in continuous loss.

Executives involved in restructuring often hire financial and

legal advisors to assist in the transaction details and negotiation. It

may also be done by a new CEO hired specifically to make the

difficult and controversial decisions required to save or reposition the

company. It generally involves financing debts, selling portions of the

company to investors, and reducing or reorganizing operations.

The basic nature of restructuring is a zero sum game. Strategic

restructuring reduces financial losses, simultaneously reducing

tensions between debt and equity holders to facilitate a prompt

resolution of the distressed situation.

Steps:

Ensure the company has enough liquidity to operate during

implementation of a complete restructuring

Produce accurate working capital forecasts

Provide open and clear lines of communication with creditors

who mostly control the company's ability to raise financing

Update detailed business plans and considerations

48

Characteristics

Retention of corporate management, sometimes "stay bonus"

payments, or equity grants

Sale of underutilized assets, such as patents or brands

Outsourcing of operations such as payroll and technical

support to a more efficient third party

Moving of operations such as manufacturing, to lower-cost

locations

Reorganization of functions such as sales, marketing, and

distribution

Renegotiation of labor contracts to reduce overhead

Refinancing of corporate debt to reduce interest payments

A major public relations campaign to reposition the company

with consumers

Forfeiture of all or part of the ownership share by pre--

restructuring stock holders (if the remainder represents only a

fraction of the original firm, it is termed a stub).

Results

A company that has been restructured effectively will

theoretically be leaner, more efficient, better organized, and better

focused on its core business, with a revised strategic and financial

plan. If the restructured company was a leverage acquisition, the

49

parent company will likely resell it at a profit if the restructuring has

proven successful.

Corporate Restructuring

Executives are always talking about the restructuring of their

corporations, with special reference to job-cuts, divisional closures,

and focus on core competence, geographical concentration, product

identification, and strategic business units. They do incidentally refer

to things like ‘Business Process Re-engineering’ and ‘Enterprise

Resource planning’. Reference is also made to flat, dynamic and

nimble structures with an emphasis on repositioning. Some of these

remarks are serious, some are only punches made in the air, and

some are very entertaining! Those who go through the process of

restructuring, keep on changing their definitions as the process

progresses and most of them conclude strategically, that there cannot

be one single, all –inclusive definition of restructuring.

In practice, restructuring starts with its very purpose. It begins

very often, with the redefining or re--searching of the purpose of

doing business. Some CEOs always try to restructure some of their

businesses, just because they were not happy with the quantum and

quality of the purpose achieved (may be in terms of shareholder’s

wealth maximization or corporate image and ethical management or

50

equal justice for all the stakeholders or market leadership through

market share or technological advancement)

Once the purpose is adequately redefined, scope for

restructuring surfaces. Sometimes it so happens that realization of the

scope for restructuring may bring you back to the purpose and you

start rethinking about the purpose itself. Of course, you have to make

up your mind and finally decide on the purpose, if restructuring is

not to be too late.

Business restructuring therefore may be approximately defined

as a conscious effort to restructure policies, programmes, products,

processes and people, to serve the redefined purpose on a sustainable

basis, because most of the restructuring exercises are carried out with

an impulsive reaction to the market variables, or internal problems,

without a serious attempt of looking at long term(or sustainable)

results. Some restructuring exercises prove to be very idealistic, and

hence are inappropriate and very expensive. Organizations carry out

the process of restructuring, without a time-bound programme and

without detailed planning. The management of the process of

restructuring, post –restructuring results, the overall cost –benefit

analysis of each phase and the impact of restructuring have all to be

worked out; with optimistic, moderate and pessimistic projections.

The new purpose (based on the owners-managers--vision) and the

required dose of restructuring need to be quantitatively and

51

qualitatively well-defined. The CEO and his team must raise certain

questions on restructuring, before they reach a conclusive design of

the restructuring programme-

1. Is it a result of a crisis situation or well-thought out long term,

remedial solution to problems?

2. Should it be on the softer front or harder front or both? (i.e. to

say, should it only deal with people-related issues or should it

also refer to products, technology etc.?)

3. Should it be done at any cost or at reasonable cost, so that the

benefit is attractive enough? Should it be done, even if the cost

of doing it is visible but the benefits are long-term and hence

not so tangible?

4. Should it be only sectoral, segmental or divisional? To begin

with, should it be first tried out in the most comfortable

division or department or territory, or should it be attempted

first in the Support Departments which are less important? In

case of the latter, even if it does not succeed, it may not matter

much to the whole of the organisation.

5. Who should participate in the whole process of restructuring

and management of change to be effected after the process is

over? Should the process be more participative and transparent,

so that a wider support from all the stakeholders can be

expected? Is it possible that the operational spread of the

52

restructuring exercise will be left to the key – executives, and at

the longer end of the process, the owners participate? Who

should ultimately be held responsible for the success/ failure of

the entire exercise?

6. Should outside facilitators, consultants, coordinators and /or

supervisors be involved in this process? Should restructuring

process and result benchmarks be obtained from the industry,

so that every step in the process could be properly appraised?

Or do we feel that our restructuring compulsions are entirely

unique in nature and hence the industry’s benchmarks may not

be of much use?

7. Should the whole process be carried out at a stretch or should

there be breathing cum testing gap between two phases?

8. Should it be entirely market-driven? Or should it be so

ambitious that the organisation would strength from it and

change the market? What type of market-signals and

indications of internal readiness should be considered while

deciding the scope, approach, time-frame, participation and

change –management strategies?

9. Can the core-competence be redefined and restructured to suit

a considerable change in the purpose? Can there be a core-

competence of stretching the traditional competencies and

replacing or reshaping the conventional competencies? Is this

53

change in the purpose, demanding not just restructuring, but

reincarnation?

Elaborate and unbiased answers to the above questions should

offer a very comprehensive definition of restructuring, every time the

purpose should decide this definition, because borrowed or adapted

definitions may prove to be costly to everybody.

Scope of Restructuring

If the purpose decides the scope of restructuring, it should also

decide the broad sequence of restructuring. Very often, the purpose

alone may not decide this sequence. The owner’s confidence, market

variables of urgent attention etc, do decide the sequence of

restructuring. Look at the following alternative restructuring

sequences-

Sequence 1-

Product Restructuring

Organizational Restructuring Processes Restructuring

People-related

Restructuring

Financial Restructuring

Sequence 2-

Restructuring of Core Competence and Competitive Advantages

54

Organizational Restructuring

Product Restructuring Process Restructuring

People –related Restructuring

Financial Restructuring

Sequence 3-

Organizational Restructuring Process Restructuring

Financial Restructuring

People-related Restructuring

Restructuring of Insignificant Product –related Specifics

Sequence 4-

Restructuring of the Organizational System to Response to

External Variables

Micro –level Organizational Restructuring

People –related Restructuring

Sequence 5-

Process Restructuring

Financial Restructuring

Sequence 6-

Product Restructuring

Processes Restructuring

Financial Restructuring

55

Sequence 7-

Restructuring of the Ownership

Pattern Financial Restructuring

Managerial Restructuring

Divisional Restructuring

The above explained are perhaps, the most commonly used

sequences of business restructuring. Every restructuring attempt has

a financial implication and hence, contrary to the above illustrative

examples, financial restructuring is very often parallel to or part of

operational restructuring. A very isolated example of ownership—

pattern--restructuring may not directly relate to products, processes

and people (except the entrepreneurial top executives). Hence, we

may comfortably conclude that every restructuring exercise has

immediate, short run and long run financial implications. The most

successful examples of business restructuring are also appropriate

examples of strategic cost-benefit analysis carried out, for such

restructuring attempts and their overall impact. It is very much like a

shrewd chess-player correcting his imperfect moves or

uncomfortable position, after considering the ultimate impact on

his/her end-game and trying to be the ultimate winner. Small

loopholes left in the exercise prove to be very costly, just as a small

degree of negligence in a surgical operation either deteriorates the

patient’s health further or make post-surgical maintenance very

56

expensive and complex. Therefore, a detailed cost-benefit analysis of

the entire exercise and its effects must be carried out. Exact numerical

expressions, of course are not always possible, when you try to

project the costs and benefits. With computerized simulations,

however, one can project various levels of optimism.

Symptoms for Restructuring

Are there any symptoms one can list which would help us in

deciding the need, quantum, timing and cost-benefit projections of a

restructuring exercise? The answer is yes. Although, the list may not

be all inclusive, it could certainly be very indicative, and a strategist

should be happy with such indications

Operational Symptoms

1. Continuously reducing employee productivity.

2. Delays in supply chain and distribution chain.

3. Weak market feedback on products, prices and promotional

policies.

4. Increasing confusion in divisional, individual and territorial

performance accounting, appraisal etc.

5. High employee turnover.

6. Decline in new market development efforts.

7. High asset maintenance and repairs.

8. Growing incidences of industrial relations problems,

production stoppages.

57

9. Disturbed ratio between the number of core employees and

support employees and the time and effort spent on core

performances and support performances.

10. Uncomfortable relations with external stakeholders like

contractors, vendors, government departments, consultants etc.

Strategic Symptoms

1. Slowed down desire for perpetual growth and wealth-

acceleration

2. Growing mismatch between strategy formulations by owners

and managers.

3. Declining market leadership to influence the government,

competitors, vendors, distributors and customers.

4. Imbalance of value-additions done by value-driving divisions,

individuals and other strategic inputs.

5. Heavy subsidisation of weak products and divisions, creating

increased pressure on strong products and divisions.

6. Imbalance between short-term tactics and long term strategies.

Financial Symptoms

1. Increasing operating costs and cost of finances.

2. Falling share-price in the market, without a near-future scope

for correction.

58

3. Declining earning ratios for divisions, vendors, distributors and

shareholders.

4. Increasing costs at the supply-side and demand-side of the

value chain.

5. Increasing prices of licenses, copy-right, patents etc.

6. Growing costs of corrective efforts, revision or reincarnation of

products and services.

7. Increasing costs on marketing operations and hence growing

pressure on manufacturing costs.

8. Unusual cost of wastage, inefficiencies, idle time, insurance,

maintenance, deliveries etc.

9. Increasing mismatch between indirect taxes and direct taxes.

10. Increased costs of applied research, concept sale and take-off

efforts.

11. Heavy costs connected with market development, restricting

competitor’s entry to established or new markets, up--gradation

of customer tastes etc.

12. Imbalance between core cost and support cost.

13. Serious drawbacks and problems in the implementation of

transfer price mechanism.

14. Continuous loss situation.

Market, Economy-level and Global Symptoms

59

1. Substantial change in the government’s policies towards tariffs,

subsidies, tax- Impositions, international trade etc.

2. Sustained recession, shrinking international market.

3. Cheaper funds availability from the international market.

4. Growing import-substitution.

5. Growing influence of networking and multinational

corporations.

6. Increased international culture of branding anything and

everything.

7. Domestic confusion with interest rate behavior and other bank-

related policies.

8. Hyper rate of information technology, advancement resulting

in the globe becoming one single market.

9. Increasing replacement of skill and system employees by

knowledge employees and entrepreneurial employees.

10. Opening up of certain economies, regions and the growing

scope of new businesses, government-private sector

participation, international joint-ventures etc.

11. An economy’s transition from the core sector to service sector

to information tech- sector to the advisory sector. The economy

of the US is already in the advisory sector of the transition

process.

60

The above lists are not totally comprehensive, and therefore a

strategist will have to use a fine combination of these symptoms (at

micro and macro levels) in order to decide on the application for

business restructuring.

The Restructuring Plan

If the purpose of restructuring is clearly decided, a

Restructuring Plan could then have reasonable clarity and shape.

Although each individual purpose would decide the details of the

plan distinctively, a general structure may be summarized as follows-

Step 1. Define the purpose further, with the maximum details of

possible sustainability.

Step 2. Decide the sequence of restructuring

Step 3. Chalk out all minute details of each operation (related to

the soft and hard aspects of restructuring) under each

phase of the sequence, with the use of PERT-CPM charts

and details about major hurdles and tactics to overcome

these hurdles. These tactics should be based on both

optimistic and moderate expectations.

Step 4. Have a parallel cost-benefit chart along with PERT –CPM

chart of operations. The costs and benefits should be on

both the scales--short and long.

61

Step 5. Design a lead team of key executives and owners to carry

out the whole process of restructuring, decide on the

action plan for each member of the team, and

‘homogenous progress parameters’ to monitor the

process.

Step 6. Chalk out a detailed plan with soft and hard aspects,

costs and crisis-management tactics, for the post-

restructuring management of change and result

indicators.

Financial aspects of various restructuring exercises (for various

purposes)

Financial aspects of restructuring vary in quantum and quality,

depending on the purpose. Following are the few major purposes

and hence major instances of restructuring:-

1. Employee productivity, cost and performance restructuring.

2. Business downsizing and optimal-sizing for drastic changes in

market variables and economy-level developments.

3. Restructuring of existing products and value-chains and hence, the

restructuring of supply chains and distribution chains.

4. Organizational restructuring for better performance-result

monitoring, and strategy formulations.

5. Restructuring of capacities, technology, and processes.

6. Ownership restructuring

62

7. Restructuring of control--empowerment, i.e the relationship

between owners and managers.

8. Restructuring of heavy loss-making divisions, sick units and dead

or unsuccessful units.

9. Restructuring for mega take-off, market leadership, international

markets and a quantum jump in horizontal and vertical

operations.

10. Restructuring caused by generation-gap, professional weaknesses

and cultural issues.

11. Restructuring as a result of privatization and liberalization.

12. Superior benchmarking and organizational change for a blue-chip

company, to retain its growth rate, extraordinary employees, and

transit from a company to a group of companies.

13. Ethical restructuring for setting up a new business ethos and long

term success parameters.

14. Operational and Accounting Restructuring to respond to drastic

changes in fiscal and monetary policies of the government.

15. Restructuring of basic or core competency and framing new

business agendas and rules.

Innovative Financial Engineering

‘Institution Building’ of great commercial organizations has

been mostly based on fine combination of three things:-

63

1) Brand--based on ethical business and entrepreneurial

employees

2) Technology, products and systems and

3) Innovative financial engineering. It is possible however,

to achieve great heights in institution building, with

timely innovations in financial engineering.

Financial engineering

The cementing of products, systems, people, brands and

technology has to be done with financial structuring, financial control

system, financial benchmarking and financial quantification of every

qualitative business variable. Such cementing could be called

‘Financial Engineering’. Materially the quantum and quality of

financial engineering may be the same, but it is very often interpreted

differently by different stake-holders. Look at the following example.

Now, how do you decide the ‘Group ROI’, if your group runs the

above three businesses, in different economies, with different

products and scales? You will have to think about a weighted (and

perhaps appropriately discounted) Economic Rate of Return, which

should take care of global average bench-marking and long –term

wealth appreciation process(against the threats of inflation, for ex

ratios, socio-economic uncertainties and different aspirations of local

partners or investors).

64

Financial engineering here would require a great amount of algebraic

algorithms, common sense and a strategic understanding of

benchmarking. To conclude, let us list the pre-requisites essential for

‘innovative’ financial engineering.

1. Creative (or parallel) thinking.

2. Courage to challenge the traditional (or classical) thinking.

3. Shrewdness to locate and discount individual interests of

different stakeholders.

4. High ability to use business arithmetic and economic thinking

together with each other.

5. High ability to relate strategies, notional parameters and

financial benchmarks in a holistic manner.

6. Employ a strategic approach for combining the intellectual and

the emotional quotient.

7. A very sharp entrepreneurial understanding of the financial

implications (in other words, it is the own thinking).

8. Understanding the shortcuts wherever possible, without

applying the complex and time consuming mathematical

algorithms (may be alternatively called, ‘maturity in selecting

the most reasonable solution to a given problem without

involving the so-called degree of sophistication).

65

Too many complex business variables existing in one single

situation and the heavy cost of analysis to be carried out may compel

an Indian entrepreneur to go for ‘approximations’ in his final

conclusion. Therefore, he may not be using the advanced algebraic

algorithms developed by the western academician. Still, the fact

remains that the Indian approach to creative financial engineering

perhaps has no parallel in the world.

Activity Based Costing (ABC)

‘Strategic Cost Management’ has recently been revolving

around Activity Based Costing (ABC), rightly or wrongly. ABC

predominantly refers to sensitive activities as ‘cost drivers’ for

ultimate accuracy in costing a product or service. Gigantic

automation of multi-purpose processes lead to a wide-spread

application of ABC, without an entrepreneurial emphasis on

Objective Based Costing.

An Indian ‘sandwich seller’ has been using the ABC approach

thoroughly, for cost identification and profit-maximization. He may

sell a standard product, for $1, which involves standard activities,

time, inputs and sequencing. If you ask him for a special sandwich

involving new activities, deletion of old activities, change in

sequence, change in quality of inputs, etc., he would make quick

logarithmic calculations and arrive at a new price for you. His

analysis of ‘new overhead allocation‛ is always approximate, but

66

more profitable and strategically correct’. He would use ABC to a

tolerable and manageable extent and then get into Objective Based

Costing (OBC).Of course; the revolution in information technology

has made the application of ABC easier and logical. But the

interesting fact that emerges from these two examples is that

traditional ideas presented in an innovative package, could look like

‘innovative concepts’. In fact, introducing innovations in small

approaches will offer big advantages.

Holistic approach to innovative financial engineering

A strategist should always apply innovations to financial

products and processes, keeping in mind the holistic design of an

entire business process. The connection between the two phases of

this process has to be perceived in the light of all the phase of the

process, along with the external variables. The holistic approach may

be summarized as follows:

1. Benchmarking of the earning-expectations

2. Product and process choices

3. Funding structure (variations, costs and flexibility)

4. Fund-deployment strategies

5. Monitoring and assessment systems

6. Programmes and policies to reward various stakeholders

67

7. Satisfaction of the shareholders

8. Perpetual sustenance of the financial and real growth of the

business enterprise.

68

Reference

1. W.H.Beaver, ‚Financial Ratios as Predictors of Failures‛,

Empirical Research in Accounting: Selected Studies 1966,

Supplement to vol.4, Journal of Accounting Research.

2. L.C.Gupta, Financial Ratios as Forewarning Indicators of

Sickness, Bombay: ICICI, 1979.

3. E.I.Altman, ‚Financial Ratios, Discriminant Analysis and the

Prediction of Corporate Bankruptcy‛, journal of Finance, vol.23

(Setember 1968).

4. S.S.Srivastava and R.A.Yadav, Management and Monitoring of

Industrial Sickness, New Delhi: Concept Publishing Company,

1996.

5. Baruch Lev, Financial Statement Analysis: A New Approach,

Englewood Cliffs, N.J.:Prentice-Gall, Inc, 1974.

6. C.J Johnson, ‚Ratio Analysis and the Prediction of Firm

Failure‛, the Journal of Finance (December 1970)

7. This section draws on Chapter 14 of the book Investment

Banking by Pratap Subramanyam, published by Tata McGraw-

Hill.

8. The Companies (Second Amendment) Act, 2002 amended

certain provisions of the Companies Act, 1956 and repealed the

69

Sick Industries Companies Act, 1985. The 2002 Act calls for the

establishment of the National Company law Tribunal (NCLT)

to handle all cases relating to company law matters previously

handled by the Bureau of Industrial and Financial

Reconstruction (BIFR) and the Company Law Board (CLB),

both of which have been abolished, and the High Court. Since

the NCLT has not been established on a full-fledged basis, the

BIFR and SICA continue to be functional, although at a reduced

level of activity. With the passage of the Securitisation and

Reconstruction of Financial Assets and Enforcement of Security

Interest Act, or simply the Securitisation Act, specified banks

and financial institutions can enforce any security created in

their favour by an NPA (non performing asset) defaulter

without the intervention of the court. This too has resulted in

lesser work for BIFR.

9. The reserve Bank of India notification

10. The Companies (Second Amendment) Act, 2002

11. A study conducted by RBI on the causes of industrial sickness

12. Strategic financial Management by G P Jakhotiya