a study on customer perception towards customer relationship management crm practices in...

TRANSCRIPT

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

34

A STUDY ON CUSTOMER PERCEPTION TOWARDS

CUSTOMER RELATIONSHIP MANAGEMENT (CRM)

PRACTICES IN NATIONALISED BANKS

*Mr. T.Partha Saradhy, **Dr. S.E.V.Subrahmanyam, ***Dr. T.Narayana Reddy

*Assistant Professor, Department of Management Studies, Sreenivasa Institute of Technology and

Management Studies, Chittoor.

**Director, Department of Management Studies, Sreenivasa Institute of Technology and

Management Studies, Chittoor.

***Assistant Professor, Department of Humanities, JNTU College of Engineering, JNTUA,

Anantapur.

ABSTRACT

The CRM practices are adopted to generate better understanding of the customers for product

development, segmentation, appropriate targeting, campaign management and maintenance of long

term profitable and mutually beneficial relationships with customers. A very small proportion of its

potential has been utilized. The paper investigates the successful implementation of CRM. An

attempt is made to clear the benefits of Customer Relationship Management. These results were

discussed and analyzed to get results about how far CRM is implemented to secure competitive

advantage. A set of recommendations will be made so as to pinpoint how CRM can be used to secure

competitiveness. The present level of MIS covers, information needed for control, performance

monitoring, decision making. The purpose of this research is to study the comparative use of CRM in

various private sector banks. Customer Relationship Management is an approach to identify the

tastes and preferences of individual, every customer is viewed with his life time value, and not only

for customer satisfaction but customer retention is also more important.

Keywords: Public Sector Banks, CRM Practices, Customers Satisfaction, Retention. 1. INTRODUCTION TO CUSTOMER RELATIONSHIP MANAGEMENT

Customer Relationship Management is the business buzzword in these days. Customer

Relationship Management promises faster customer service with lower costs, more customer

satisfaction with better customer retention and ultimately achieving customer loyalty. All this is done

in hope for more sales and profits. According to company’s goals can be best achieved through

INTERNATIONAL JOURNAL OF MANAGEMENT (IJM)

ISSN 0976-6502 (Print)

ISSN 0976-6510 (Online)

Volume 5, Issue 11, November (2014), pp. 34-47

© IAEME: http://www.iaeme.com/IJM.asp

Journal Impact Factor (2014): 7.2230 (Calculated by GISI)

www.jifactor.com

IJM

© I A E M E

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

35

identification and more satisfaction of the customers' needs and wants. CRM is a system to identify,

target, acquiring, and retaining the best outcome of customers. Customer Relationship Management

helps in understanding customer needs, and in building relationship with customers by providing the

most suitable products and services with enhanced customer service. It integrates all sub systems to

maintain a database of customer contacts, purchases, and technical support, among other things. This

database helps the company in identifying the needs of the customers to improve the quality of the

relationship.

Customer is the king. Forget the meaning of royal treatment of customers, many of the

organizations are not treating the customer with dignity. Doing a favor by answering a few questions

of the customers on the phone – after putting them on hold for an hour! Standing in line to buy

something was common and expected. The customers go to airports to buy a ticket because the

airlines kept them there.

Nowadays, many businesses such as banks, insurance companies, and other service providers

realize the importance of Customer Relationship Management (CRM) and its potential to help them

acquire new customers retain existing ones and maximize their lifetime value. At this point, close

relationship with customers will require a strong coordination between IT and marketing

departments to provide a long-term retention of selected customers.

The phenomenon of globalization has paved the way for the entry of new generation

multinational (foreign) banks in general and private sector banks in particular into the Indian banking

market. Several banking experts argue that the world class services that are offered by these new

generation banks have a tremendous bearing on the mindset and expectations of Indian banking

customers. The services that are offered by these banks are characterized on a 24 hour X 7 day a

week basis with a focus on delivering higher quality of service across the multiple channels. In this

context, phone banking and internet technologies have emerged as a major option before the Indian

banks. In addition to these modern services such as Tele-banking, Internet banking, Mobile banking,

and Automated Teller Machine (ATM) banking are also offered by Indian banks to serve customers

better. It is against this backdrop, the studies on understanding the demographics of customers’ and

their attitudes towards customer relationship management (CRM) practices are gaining importance.

Several researches studies that were conducted on the customer service aspects of Indian banking

scenario, highlighted the need for designing effective

Customer relationship management (CRM) systems for enhancing the customer satisfaction

and loyalty, Reserve Bank of India (RBI) instructed all public sector banks to focus on implementing

innovative customer relationship management (CRM) systems through multiple touch points of

CRM systems such as call centers, websites, email systems and interactive kiosks across various

service units and support processes. Research studies further revealed that customer relationship

management (CRM) is emerging as an offshoot of the modern technological landscape by

incorporating customer demographics, business intelligence, and Internet proximity and therefore

takes its place at the heart of the modern banks. These technological advancements and global

competitive pressures have reoriented the public sector commercial banks in India to pay more

attention to the changing customer needs and effective CRM interventions in the light of the changes

in the consumer demographics.

The forces of change shaping the banking and financial system worldwide are fundamental

and constant. The intense competitive pressure on the financial system has generated a variety of

products and services to meet the specialized needs of millions of customers. The impact of these

changes in the international financial system was felt in India in the early nineties when she initiated

the process of integrating her economy with the global economic order. This ushered in the phase of

financial sector reforms in our country. Reforms, which are primarily aimed at aligning the Indian

banking system to the international best practices, are having lasting effect on the entire fabric of the

Indian financial system which is presently undergoing a major phase of metamorphosis. While

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

36

reflecting on the dynamics of this change and its implications in the management of banks, one need

to emphasize the phenomenal growth profile of the Indian banking industry in retrospect and

prospect in terms of business, branch network, etc. Correspondingly, the average population served

per bank branch has come down significantly. The cultural diversity, vast geographical spread and

federal character of the country are amply represented in the complexity of the banks' operations.

There has been a perceptible change in the environmental scenario in banking and finance since the

early nineties, and, consequently, managing these institutions efficiently is a major and continuous

challenge.

Adoption of CRM Technology in Banking System Information Technology revolution had a great impact in the Indian banking sector. The use

of computers software had led to introduction of online banking system in India. The use of the

modern innovation and computerization of the banking industry in India has improved after

economic liberalization in the year 1991 as the country's banking sector has been exposed to the

world's market. The Indian banks were finding it difficult to compete with the international banking

standards in terms of customer service to provide convenience without the use of the information

technology and computer system and software.

Reserve Bank of India in the year 1984 formed Committee on Mechanism in the Banking

sector whose chairman was Dr C Rangarajan, Deputy Governor, Reserve Bank of India. The major

recommendations of the committee were implementing MICR Technology in all the banks in the

metropolis in India. It provided us standardized cheque forms and encoding and decoding system.

In the year 1994, the Reserve Bank of India set up Committee on Computerization in Banks

was headed by Dr. C.R. Rangarajan which emphasized that the settlement operation must be

computerized in the clearing houses of Reserve Bank of India in Bhubaneswar, Guwahati, Jaipur,

Patna and Thiruvananthapuram. It further stated that there should be National Clearing of inter-city

cheques at Kolkata, Mumbai, Delhi, Chennai and MICR should be made Operational. It also focused

on computerization of banking services in all branches and increasing connectivity among branches

through computers. It also suggested implementing on-line banking facilities.

The committee submitted reports in the year 1989 and computerization of all branches started

form the year 1993 with settlement between IBA and bank employees' association.

In the year 1994, Committee on Technology Issues relating to Payments System, Cheque

Clearing and Securities Settlement in the Banking sector was set up with chairman Shri.WS Saraf,

Executive Director, Reserve Bank of India. It emphasized on Electronic Funds Transfer (EFT)

system, with the internet communication network as its carrier. It also said that MICR clearing

should be set up in all banks with more than 100 branches.

Introduction to State Bank of India

The origin of the State Bank of India goes back to the first decade of the nineteenth century

with the establishment of the Bank of Calcutta in the year 1806. Three years later the bank received

its charter and was re-designed as the Bank of Bengal in the year 1809. A unique institution, it was

the first joint-stock bank of British India sponsored by the Government of Bengal. The Bank of

Bombay established in the year 1840 and the Bank of Madras in the year 1843 followed the Bank of

Bengal. These three banks remained at the apex of modern banking system in India till their

amalgamation as the Imperial Bank of India in the year 1921.

Primarily Anglo-Indian creations, the three presidency banks came into existence with a

compulsion of imperial finance or by the felt needs of local European commerce and were not

imposed from outside in an arbitrary manner to modernize Indian banking system and it helps for

developing Indian economy. Their evolution was shaped by ideas from similar developments in

International Journal of Management (IJM), ISSN 0976

Volume 5, Issue 11, November (2014), pp.

Europe and England and was influenced by changes occurring in the

urban trading environment.

Introduction to Andhra Bank

Andhra Bank is a public sector bank, with a network of

counters, 38 satellite offices and 1563

in to the states of Tripura and Himachal Pradesh. The bank now operates in 25 states and three Union

Territories.

The government of India owns 58% of its share capital and is

62.14% by infusing 2 billion in capital. The state owned

10% of the shares. The bank has done a total business of

March 2013.

Andhra Bank has ranked No.1 in terms of number of Life Insurance Policies mobilised amongst all

the agency banks dealing with the Life Insurance Corporation of India. The bank also has tie

United India Insurance Company Limited under Banc

Dr. Hhogaraju Pattabhi Sitaramayya founded Andhra Bank in 1923 in Machilipatnam,

Andhra Pradesh. The bank was registered on 20 November 1923 and commenced business

year 1923 with a paid up capital of

linguistic division of states was promulgated and Hyderabad was made the capital of

Pradesh. The registered office of the bank was subsequently shifted to Andhra Bank Buildings,

Sultan Bazar, Hyderabad, Telangana. In the second phase of

commenced in the year 1980, the bank became a wholly owned G

2. REVIEW OF LITERATURE

This study was relevant to the previous studies and researches

subject to find out and fill up if any

generally be found, number of books is

loan syndication, securitization, profitability and productivity etc. but, few studies

the role of Customer Relationship Management

Uppal R.K. (2010) Explains in his study about

banking industry during 2000-2007. The study concludes that among all

while mobile banking and it does not hold a strong position in public and old private

new private sector banks and foreign banks

average branches providing mobile

in e-banks which have positive impact on profits

all, foreign banks are in the top position followed by new private sector banks in providing

banking services and their efficiency is also much higher as compared to other groups. The

also suggests some strategies to improve m

Oghenerukeybe E. A. (2009)

influencing the effective implementation of existing

banking web browsers using the Communication

proposed by Wogalter in the year

very effective at alerting and shielding

participants do not understand the full meaning of the banking sites while the attention of some

users is not captured enough, for they ignore the warnings completely. Even with the presence

participants still go ahead to submit sensit

management of banks develop effective security strategies for the future of electronic

Nigeria.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

37

and was influenced by changes occurring in the structure of both the lo

is a public sector bank, with a network of many branches,

counters, 38 satellite offices and 1563 ATMs as on 30 Nov 2013. During 2011

states of Tripura and Himachal Pradesh. The bank now operates in 25 states and three Union

The government of India owns 58% of its share capital and is planning

62.14% by infusing 2 billion in capital. The state owned Life Insurance Corporation of India holds

10% of the shares. The bank has done a total business of 2230 billion for the fiscal year ended 31

Andhra Bank has ranked No.1 in terms of number of Life Insurance Policies mobilised amongst all

gency banks dealing with the Life Insurance Corporation of India. The bank also has tie

United India Insurance Company Limited under Banc assurance

Dr. Hhogaraju Pattabhi Sitaramayya founded Andhra Bank in 1923 in Machilipatnam,

e bank was registered on 20 November 1923 and commenced business

1923 with a paid up capital of 100000 and an authorized capital of 1million

tates was promulgated and Hyderabad was made the capital of

Pradesh. The registered office of the bank was subsequently shifted to Andhra Bank Buildings,

Sultan Bazar, Hyderabad, Telangana. In the second phase of nationalization

1980, the bank became a wholly owned Government bank.

REVIEW OF LITERATURE

This study was relevant to the previous studies and researches in the related

if any research gaps existed. Literature on

of books is available on banking related aspects as merchant

loan syndication, securitization, profitability and productivity etc. but, few studies

Customer Relationship Management in the banking services.

Explains in his study about the extent of mobile banking in Indian

2007. The study concludes that among all CRM

does not hold a strong position in public and old private

private sector banks and foreign banks in mobile banking is good enough with nearly 50 pc

obile banking services. Mobile banking customers are also the highest

which have positive impact on profits and business per employee of these banks. Among

the top position followed by new private sector banks in providing

banking services and their efficiency is also much higher as compared to other groups. The

ts some strategies to improve mobile banking services.

Oghenerukeybe E. A. (2009) he explained in his study about user’s perception

ve implementation of existing objectives and to evaluate

browsers using the Communication-Human Information Processing Model

the year 2006 in the field of warning sciences. Findings reveal that

very effective at alerting and shielding users from revealing sensitive informa

understand the full meaning of the banking sites while the attention of some

users is not captured enough, for they ignore the warnings completely. Even with the presence

participants still go ahead to submit sensitive information. These outcomes may

management of banks develop effective security strategies for the future of electronic

6502(Print), ISSN 0976 - 6510(Online),

structure of both the local and

branches, it has 15 extension

as on 30 Nov 2013. During 2011–12, the bank entered

states of Tripura and Himachal Pradesh. The bank now operates in 25 states and three Union

planning to increase it to

Life Insurance Corporation of India holds

2230 billion for the fiscal year ended 31

Andhra Bank has ranked No.1 in terms of number of Life Insurance Policies mobilised amongst all

gency banks dealing with the Life Insurance Corporation of India. The bank also has tie-up with

Dr. Hhogaraju Pattabhi Sitaramayya founded Andhra Bank in 1923 in Machilipatnam,

e bank was registered on 20 November 1923 and commenced business in the

million in the year 1956,

tates was promulgated and Hyderabad was made the capital of Andhra

Pradesh. The registered office of the bank was subsequently shifted to Andhra Bank Buildings,

nationalization of commercial banks

overnment bank.

in the related fields. The

. Literature on banking services can

available on banking related aspects as merchant banking,

loan syndication, securitization, profitability and productivity etc. but, few studies are undertaken on

the extent of mobile banking in Indian

CRM is the most effective

does not hold a strong position in public and old private sector but in

banking is good enough with nearly 50 pc

banking customers are also the highest

and business per employee of these banks. Among

the top position followed by new private sector banks in providing mobile

banking services and their efficiency is also much higher as compared to other groups. The study

user’s perception of factors

objectives and to evaluate the effectiveness of

Information Processing Model, a model

ciences. Findings reveal that is not

users from revealing sensitive information. 27 percent

understand the full meaning of the banking sites while the attention of some

users is not captured enough, for they ignore the warnings completely. Even with the presence of

ive information. These outcomes may help the

management of banks develop effective security strategies for the future of electronic banking in

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

38

Migdadi Y.K.A. (2008) he revealed in his investigation to identify the quality of internet

banking service encounter of the retail banks in Jordan, and to identify the quality aspects that should

be improved or sustained. The study evaluates the banks' web sites by using the web site quantitative

evaluation method in the year 2008 for sixteen retail banks in Jordan. The results indicate that the

banks in Jordan have significant positive quality of the internet banking system and service

encounter, further the banks' web sites are rich in their content and significant in the navigation, but

the speed of home page down load and web site accessibility should be developed in the future for

better results.

Banknet India (2006) he concluded after conducting an online survey on 316 ATM users

during the month of August-September, 2006 and survey is limited to India to get insight into users’

perceptions. It is concluded from the survey that the most use (56 pc) of ATM services is for bill

payments and pre-paid mobile recharge where 64 pc respondents feeling comfortable with depositing

of cash/cheques through ATM but they have to wait in long queues and find no money left in the

machine. Most of the respondents claimed to know about fee charged at other bank ATMs and 20 pc

demand more privacy. Overall conclusion is ATMs are preferred over branch banking by majority of

the respondents show the increasing popularity of e-banking among the public sector banks.

3. NEED FOR THE STUDY

Advanced Customer Relationship Management technology requirement increased because of

competitive pressures in banking industry, particularly in banking services. Indian banks are

functioning increasingly with competitive pressure within the banking system from non banking

institutions as well as from domestic and international capital markets.

In this era of increased competition, in order to improve standards it will be benefit able for

the banks to develop long term relationship with the customers by offering superior quality and

services. Developing long term relations with the potential customer depends on three dimensions

like service quality, product quality and relationship quality. In banking industry since the perceived

service quality acts as a foundation for developing long-term customer relationship, the present study

is mainly undertaken to present the customer perception on CRM and to study the perceived services

and its quality provided by the bank system.

4. THE PRIMARY OBJECTIVE OF THE STUDY

The primary focus of this study is on the role of customer relationship management in

banking sector, the banking employees’ relation with its customer to maximize customer satisfaction.

The study conducted to find out the customer relationship management factor influencing on

customer satisfaction as well as customer retention through analysis

To identify the important factors for select a particular bank and identified factors influencing

the bank with selected sample customers of focus pre selected banks. The identified factors which

are influencing are quality of service, and personal relation effectiveness of customer relationship

management techniques. This study is based on 250 customers of SBI and ANDHRA banks.

5. OBJECTIVES OF THE STUDY

The main objectives of the study are as follows.

1. To study the perception of SBI & ANDHRA BANK customers about Customer Relationship

Management.

2. To analyze the perceived service quality of the customers towards their bankers.

3. To study the CRM practices adopted by the banks to improve banking performance.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

39

6. SCOPE OF THE STUDY

The scope of the study is limited to the survey of customers perception of selected public

sector commercial banks namely State Bank Of India(SBI), ANDHRA Bank in chittoor district of

Andhra Pradesh.

7. RESEARCH METHODOLOGY

To achieve designed objectives of the study and to analyze the different factors with

appropriate methodology has been adopted. The present study is exploratory as well as descriptive.

The survey was conducted during August and October 2014. The present study is based on primary

and secondary data. The primary data has been collected from a sample of 250 customers of State

Bank of India and ANDHRA Bank Chittoor in district of Andhra Pradesh. The Primary data has

been collected with a well structured and pre tested questionnaire which was based on Likert five

point scale, secondary data has been collected through internet and websites of selected banks.

The customer perception of State Bank of India and ANDHRA bank on Customer

Relationship Management was judged on the variables like Routinely asking the customer to

provide feedback, Providing customized services and products, Transparent and well defined system,

Bank website is user friendly, Communication tools are very effective, Well developed privacy

policy, Increasing customer convenience, Consistent customer experience, Customer is the biggest

asset of the organization, Retaining existing customers, Conducting customer loyalty programmes,

Excellent employee response, ATMs are adequately provided.

Apart from the questionnaire being used for data collection, personal discussions were also

conducted with the respondents to get further information. The data so collected has been analyzed

with statistical techniques like percentages, averages and charts.

8. ANALYSIS AND INTERPRETATION

Table 8.1: representing customer perception on CRM in banks

S. No Variable Name SA A N D SD

1. Routinely asking the customer to provide feedback 20 25 100 55 50

2. Providing customized services and products 110 70 60 10 0

3. Transparent and well defined system 120 100 10 13 7

4. Bank website is user friendly 50 120 30 30 20

5. Communication tools are very effective 72 80 50 28 20

6. Well developed privacy policy 120 100 20 7 3

7. Increasing customer convenience 40 60 60 50 40

8. Consistent customer experience 90 120 20 15 5

9. Customer is the biggest asset of the organization 95 110 40 3 2

10. Retaining existing customers 50 150 30 10 10

11. Conducting customer loyalty programmes 50 50 100 25 25

12. Excellent employee response 30 100 100 10 10

13. ATMs are adequately provided 120 100 30 0 0

International Journal of Management (IJM), ISSN 0976

Volume 5, Issue 11, November (2014), pp.

Table 8.2: representing customer pe

Inference: 8% of customers are strongly agree

provide feedback 10% of customer

disagree the statement.

Table 8.3: representing customer perception on the statement ‘

Inference: 44% of customers are strongly agree the

and products, 28% of customer agree

the statement.

Opinion No. of

Respondents

Percentage

Strongly

Agree

20

Agree 25

Neutral 100

Disagree 55

Strongly

Disagree

50

Total 250

Opinion

No. of

Respondents

Percentage

Strongly

Agree

110

Agree 70

Neutral 60

Disagree 10

Strongly

Disagree

0

Total 250

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

40

customer perception on the statement ‘Routinely

to provide feedback’

omers are strongly agree the statement bank routinely asking customer

% of customers agree, 40% of customers are neutral and 42

customer perception on the statement ‘Providing customized

and services’

ustomers are strongly agree the statement bank providing cus

28% of customer agree, 24% of customers are neutral and 4%

Percentage

(%)

8

10

40

22

20

100

Percentage

(%)

44

28

24

4

0

100

6502(Print), ISSN 0976 - 6510(Online),

Routinely asking the customer

routinely asking customers to

of customers are neutral and 42% of customers

oviding customized products

k providing customized services

% of customers disagree

International Journal of Management (IJM), ISSN 0976

Volume 5, Issue 11, November (2014), pp.

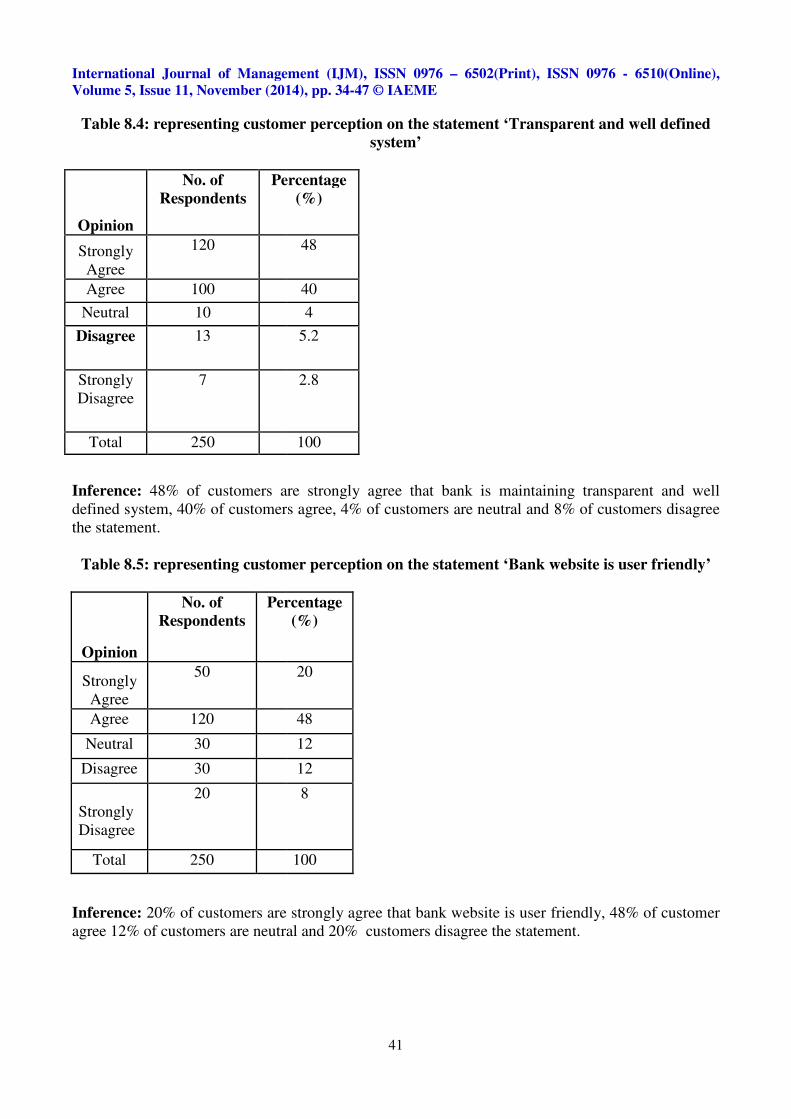

Table 8.4: representing customer perception on the statement ‘

Inference: 48% of customers are strongly agree th

defined system, 40% of customer

the statement.

Table 8.5: representing customer perception on the statement ‘

Inference: 20% of customers are strongly agree that bank website is user friendly

agree 12% of customers are neutral and 20

Opinion

No. of

Respondents

Percentage

Strongly

Agree

120

Agree 100

Neutral 10

Disagree 13

Strongly

Disagree

7

Total 250

Opinion

No. of

Respondents

Percentage

Strongly

Agree

50

Agree 120

Neutral 30

Disagree 30

Strongly

Disagree

20

Total 250

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

41

customer perception on the statement ‘Transparent and well defined

system’

ustomers are strongly agree that bank is maintaining transp

40% of customers agree, 4% of customers are neutral and 8%

customer perception on the statement ‘Bank website is user friendly

customers are strongly agree that bank website is user friendly

of customers are neutral and 20% customers disagree the statement

Percentage

(%)

48

40

4

5.2

2.8

100

Percentage

(%)

20

48

12

12

8

100

6502(Print), ISSN 0976 - 6510(Online),

Transparent and well defined

bank is maintaining transparent and well

f customers are neutral and 8% of customers disagree

Bank website is user friendly’

customers are strongly agree that bank website is user friendly, 48% of customer

s disagree the statement.

International Journal of Management (IJM), ISSN 0976

Volume 5, Issue 11, November (2014), pp.

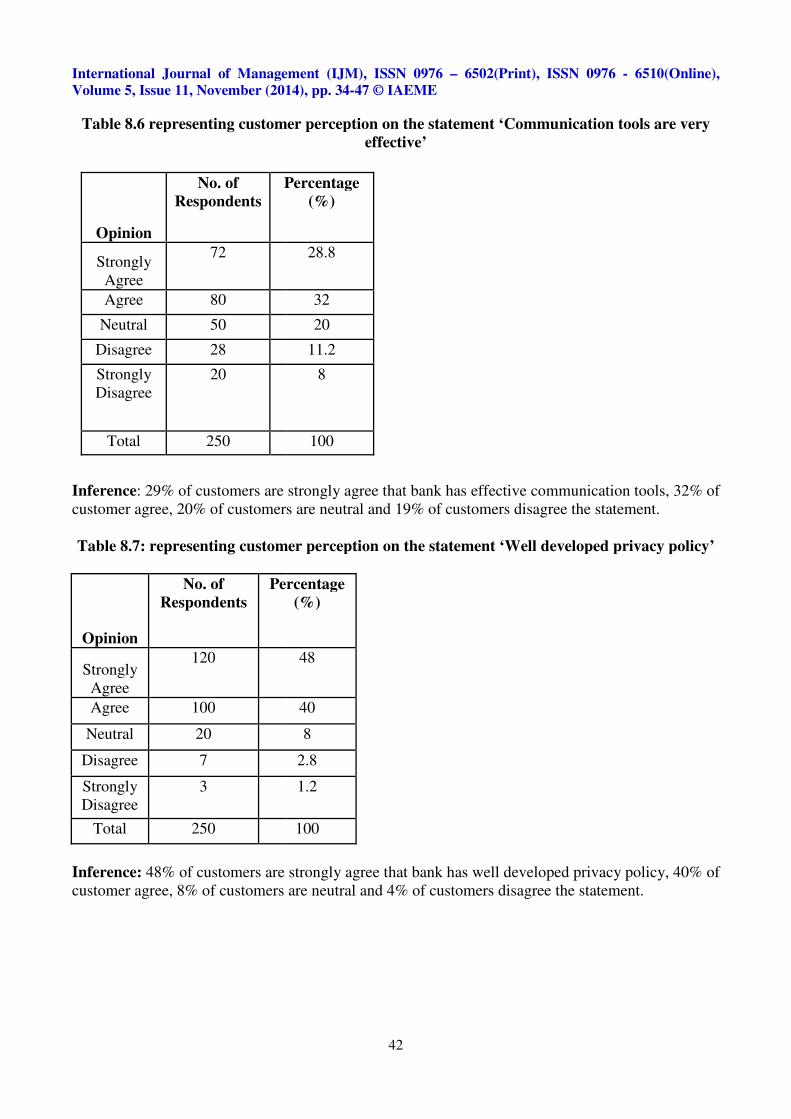

Table 8.6 representing customer perception on the statement ‘

Inference: 29% of customers are strongly agree that bank has effective communication tools

customer agree, 20% of customers are

Table 8.7: representing customer perception on the statement

Inference: 48% of customers are s

customer agree, 8% of customers are neutral and 4

Opinion

No. of

Respondents

Percentage

Strongly

Agree

72

Agree 80

Neutral 50

Disagree 28

Strongly

Disagree

20

Total 250

Opinion

No. of

Respondents

Percentage

Strongly

Agree

120

Agree 100

Neutral 20

Disagree 7

Strongly

Disagree

3

Total 250

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

42

customer perception on the statement ‘Communication tools are very

effective’

customers are strongly agree that bank has effective communication tools

20% of customers are neutral and 19% of customers disagree the statement

customer perception on the statement ‘Well developed privacy policy

customers are strongly agree that bank has well developed privacy policy

8% of customers are neutral and 4% of customers disagree the statement

Percentage

(%)

28.8

32

20

11.2

8

100

Percentage

(%)

48

40

8

2.8

1.2

100

6502(Print), ISSN 0976 - 6510(Online),

Communication tools are very

customers are strongly agree that bank has effective communication tools, 32% of

customers disagree the statement.

Well developed privacy policy’

well developed privacy policy, 40% of

customers disagree the statement.

International Journal of Management (IJM), ISSN 0976

Volume 5, Issue 11, November (2014), pp.

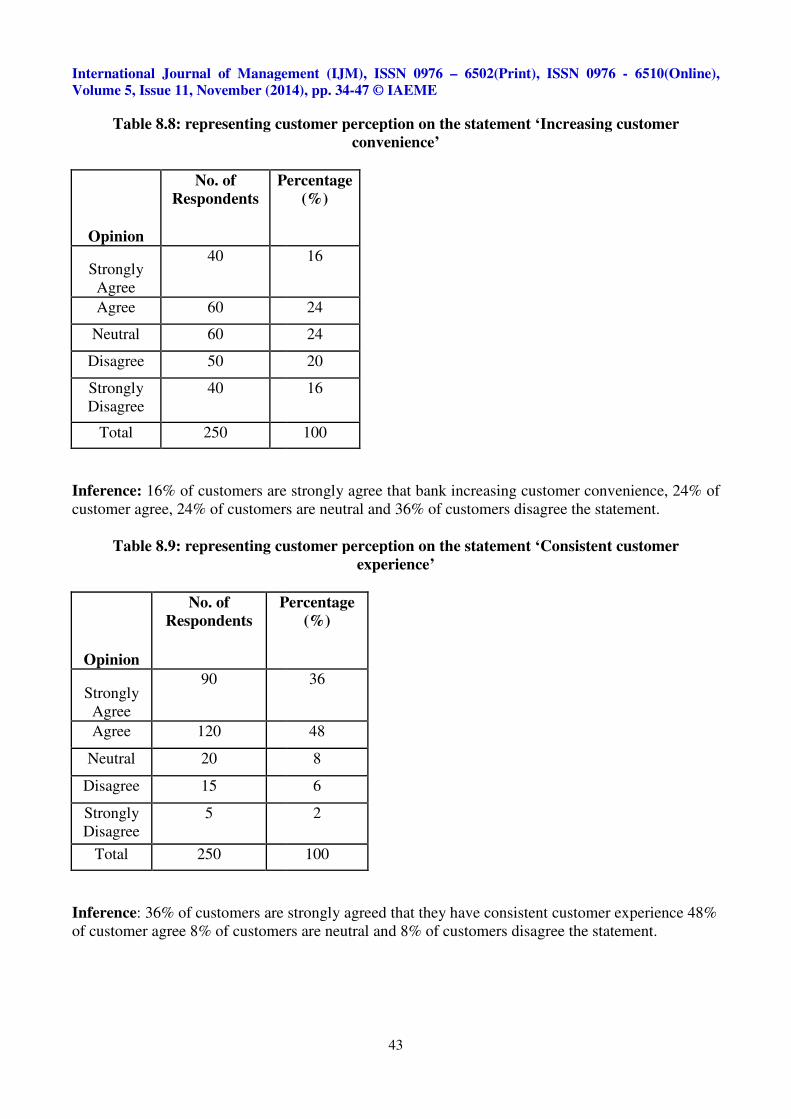

Table 8.8: representing customer perception on the statement ‘

Inference: 16% of customers are strongly agree that bank i

customer agree, 24% of customers are neutral and 36

Table 8.9: representing customer perception on the statement ‘

Inference: 36% of customers are strongly

of customer agree 8% of customers are neutral and 8

Opinion

No. of

Respondents

Percentage

Strongly

Agree

40

Agree 60

Neutral 60

Disagree 50

Strongly

Disagree

40

Total 250

Opinion

No. of

Respondents

Percentage

Strongly

Agree

90

Agree 120

Neutral 20

Disagree 15

Strongly

Disagree

5

Total 250

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

43

customer perception on the statement ‘Increasing customer

convenience’

customers are strongly agree that bank increasing customer convenience

24% of customers are neutral and 36% of customers disagree the statement

customer perception on the statement ‘Consistent customer

experience’

customers are strongly agreed that they have consistent customer experience 48%

of customer agree 8% of customers are neutral and 8% of customers disagree the statement

Percentage

(%)

16

24

24

20

16

100

Percentage

(%)

36

48

8

6

2

100

6502(Print), ISSN 0976 - 6510(Online),

Increasing customer

customer convenience, 24% of

customers disagree the statement.

Consistent customer

onsistent customer experience 48%

customers disagree the statement.

International Journal of Management (IJM), ISSN 0976

Volume 5, Issue 11, November (2014), pp.

Table 8.10 representing customer perception on the statement ‘

Inference: 38% of customers are strongly agree that customer is the biggest asset of the bank

of customers agree, 16% of customers are neutral and 2% customers disagree the statement

Table 8.11: representing customer per

Inference: 20% of customers are stron

customer agree, 12% of customers are neutral and 8

Opinion

No. of

Respondents

Strongly

Agree

95

Agree 110

Neutral 40

Disagree 3

Strongly

Disagree

2

Total 250

Opinion

No. of

Respondents

Percentage

Strongly

Agree

50

Agree 150

Neutral 30

Disagree 10

Strongly

Disagree

10

Total 250

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

44

customer perception on the statement ‘Customer is the biggest asset of

the organization’

customers are strongly agree that customer is the biggest asset of the bank

16% of customers are neutral and 2% customers disagree the statement

customer perception on the statement ‘Retaining existing customers

customers are strongly agree that bank retaining existing customers

12% of customers are neutral and 8% of customers disagree the statement

Percentage

(%)

38

44

16

1.2

0.8

100

Percentage

(%)

20

60

12

4

4

100

6502(Print), ISSN 0976 - 6510(Online),

Customer is the biggest asset of

customers are strongly agree that customer is the biggest asset of the bank, 44%

16% of customers are neutral and 2% customers disagree the statement.

Retaining existing customers’

retaining existing customers, 60% of

customers disagree the statement.

International Journal of Management (IJM), ISSN 0976

Volume 5, Issue 11, November (2014), pp.

Table 8.12: representing customer perception on the statement

Opinion

No. of

Respondents

Strongly

Agree

50

Agree 50

Neutral 100

Disagree 25

Strongly

Disagree

25

Total 250

Inference: 20% of customers are strongly agree that bank conductin

20% of customers agree, 40% of customers are neutral and 20

Table 8.13: representing

Inference: 12% of customers are strongly

customers agree, 40% of customers are neutral and

Opinion

No. of

Respondents

Strongly

Agree

30

Agree 100

Neutral 100

Disagree 10

Strongly

Disagree

10

Total 250

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

45

customer perception on the statement Conducting C

programmes

Percentage

(%)

20

20

40

10

10

100

customers are strongly agree that bank conducting customer loyalty programmes

of customers are neutral and 20% customers disagree

representing customer perception on the statement ‘

response’

customers are strongly agreed about excellent employee r

% of customers are neutral and 8% of customers disagree the statement

Percentage

(%)

12

40

40

4

4

100

6502(Print), ISSN 0976 - 6510(Online),

Conducting Customer loyalty

g customer loyalty programmes,

% customers disagree.

Excellent employee

about excellent employee response, 40% of

customers disagree the statement.

International Journal of Management (IJM), ISSN 0976

Volume 5, Issue 11, November (2014), pp.

Table 8.14: representing customer perception on the statement ‘

Inference: 48% of customers are strongly agree about adequate provision of ATMs

customers agree, 12% of customers are neutral and no

9. CONCLUSION

The findings of this research study revealed that the tenure of banking

respondents has an influence on the CRM efficiency especially in public

Nationalized banks are succeeding in

succeeding in maintaining transparent

privacy policy and ATMs provision.

comprehensive approach for develop

because Customer Relationship

close contact with end customers but have lesser value to

end customers.

The implementation of CRM yields

benefits is cost reduction. Secondly, the integrated view of the customer provides the bank an

opportunity to understand its customers well and accordingly cater to their needs with individualized

offering.

Strategic approach towards CRM implementa

benefits of the CRM investments made by banks

respondents has an influence on the consumers’ awareness of CRM. Further analysis of the data

revealed that the gender of the respondents has no

The strategic framework suggested for effective implementation of CRM

importance of understanding CRM as an organization wide strategy and need for alignment of

bank’s culture and processes to bring customer centricity at the core of operations

Opinion

No. of

Respondents

Percentage

Strongly

Agree

120

Agree 100

Neutral 30

Disagree 0

Strongly

Disagree

0

Total 250

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

46

customer perception on the statement ‘ATMs are adequately

provided’

stomers are strongly agree about adequate provision of ATMs

f customers are neutral and no customer disagree the statement

The findings of this research study revealed that the tenure of banking

respondents has an influence on the CRM efficiency especially in public

Nationalized banks are succeeding in collecting feedback regularly from the right customers and

succeeding in maintaining transparent and well defined system, customers are highly satisfied with

privacy policy and ATMs provision. Customer Relationship Management is now becoming a new

for developing business sustainability in nationalized banks

elationship Management is important for banking industry because

close contact with end customers but have lesser value to industries that are further away from the

The implementation of CRM yields more number of benefits to the bank one of the importa

benefits is cost reduction. Secondly, the integrated view of the customer provides the bank an

opportunity to understand its customers well and accordingly cater to their needs with individualized

trategic approach towards CRM implementation will enable attainment of

the CRM investments made by banks. It was also observed that the occupation of the

respondents has an influence on the consumers’ awareness of CRM. Further analysis of the data

he respondents has no influence on the CRM efficiency

The strategic framework suggested for effective implementation of CRM

understanding CRM as an organization wide strategy and need for alignment of

ses to bring customer centricity at the core of operations

Percentage

(%)

48

40

12

0

0

100

6502(Print), ISSN 0976 - 6510(Online),

ATMs are adequately

stomers are strongly agree about adequate provision of ATMs, 40% of

disagree the statement.

The findings of this research study revealed that the tenure of banking transactions of the

respondents has an influence on the CRM efficiency especially in public banking sector.

regularly from the right customers and

ustomers are highly satisfied with

is now becoming a new

in nationalized banks. This is

banking industry because that has

industries that are further away from the

number of benefits to the bank one of the important

benefits is cost reduction. Secondly, the integrated view of the customer provides the bank an

opportunity to understand its customers well and accordingly cater to their needs with individualized

will enable attainment of the desired

It was also observed that the occupation of the

respondents has an influence on the consumers’ awareness of CRM. Further analysis of the data

influence on the CRM efficiency

The strategic framework suggested for effective implementation of CRM emphasizes the

understanding CRM as an organization wide strategy and need for alignment of

ses to bring customer centricity at the core of operations

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 11, November (2014), pp. 34-47 © IAEME

47

REFERENCES

1. Kothari C R (2004), “Research Methodology”, New Delhi, New Age International Publishers

2. Ravichandran N (2003), “Indian Banking Sector: Challenges and Opportunities”, Vikalpa,

vol. 28, No. 3, pp.83-89.

3. Uppal K R and Rimpi Kaur (2008), “Customer Service in Banks: An Empirical Study”, The

Icfaian Journal of Management Research, vol. VIII, No. 4, pp. 7-20.

4. Saurbhi Chaturvedi and Dr. Rishu Roy (2008), “Impact of CRM on Organizational

Effectiveness: An Exploratory Study of Services Sector”, Management Trends, vol. 5, No. 1,

pp.12-18.

5. Kotler P, `Marketing Management’ (2009), Pearson India.

6. Ravi V, Raju N P, Sridhar S, `Big Data, Analytics, CRM: A Formidable Triumvirate for

Banking’, The Indian Banker, vol. III, No.2, Feb 2012, pp 14-23.

7. Mukherjee K, `Using CRM Effectively’, TMTC Journal of Management, Vol. 8, No. 2, Dec

2010, pp 59-65.

8. Navdeep Agarwal and Mohit Gupta (2005) “Dissemination of Customer Oriented Strategy to

Customer Contact Service Employees-Application of Hartline, Macham and Mckee(2000)

Model in Indian Settings”, South Asian Journal of Management , January- March 2005, 12,1,

p 58-78.

9. Rajnish, Jain, Sangeeta, Jain and Upinder, Dhar,(2007),"CUREL: A Scale for Measuring

Customer Relationship Management Effectiveness in Service Sector”, Journal of Services

Research, Volume 7, Number 1 (April - September 2007).

10. Divya Prabha D and Dr. Krishnaveni R (2008), “A study on Corporate Customer

Relationship Management in Banking Industry”, PSG Journal of Management Research, vol.

1, No. 2, pp.177-121.

11. Kale, Sudhir, ‘CRM Failure and the Seven Deadly Sins’, Marketing Management, Sept- Oct

2004, Vol 12, Issue 5, pp 42-46.

12. Sureshchander, G.S, Chadndrashekharan, Rajendran, Anantharaman, (2003), "Customer

Perceptions of Service Quality in the Banking Sector of a Developing Economy-A critical

Analysis", International Journal of Bank Marketing, 21/5, 2003-233-242.

13. Coltman T., ‘Can Superior CRM Capabilities Improve Performance in Banking’, Journal of

Financial Services Marketing, Vol.12,2 (2007).

14. Sandip Dhakecha, “A Study on Effectiveness of Cause Related Marketing [CRM] as a

Strategic Philanthropy in Terms of Brand Popularity & Sales”, International Journal of

Marketing & Human Resource Management (IJMHRM), Volume 4, Issue 1, 2013,

pp. 28 - 39, ISSN Print: 0976 – 6421, ISSN Online: 0976- 643X.

15. Allahyar Beigi Firoozi, Mehran Aslaniyan, Faranak Yusefvand and Mojtaba Pahlavani,

“Formulating and Prioritizing CRM Implementation Strategies in Mehr Eghtesad Bank of

Iran using Combinational Model of PIP and ANP”, International Journal of Marketing &

Human Resource Management (IJMHRM), Volume 4, Issue 2, 2013, pp. 40 - 53, ISSN Print:

0976 – 6421, ISSN Online: 0976- 643X.

16. Dr. V.Antony Joe Raja, “New Strategy in Today Banking Sector: Bank Customer

Relationship Management (CRM) & Marketing Mix in World”, International Journal of

Marketing & Human Resource Management (IJMHRM), Volume 4, Issue 3, 2013,

pp. 19 - 29, ISSN Print: 0976 – 6421, ISSN Online: 0976- 643X.

17. T.Vijayakumar and Dr. R. Velu, “Customer Relationship Management in Indian Retail

Banking Industry”, International Journal of Management (IJM), Volume 2, Issue 1, 2011,

pp. 41 - 51, ISSN Print: 0976-6502, ISSN Online: 0976-6510.