a strong and vibrant financial sector for sustainable growth – the role … · 2013-09-25 · a...

TRANSCRIPT

The Investors Conference 2005- in conjunction with the 30th Annual MeetingIslamic Development Bank22nd June 2005

A Strong and Vibrant Financial Sector for Sustainable Growth – the role of Capital Markets

Dato’ Zarinah AnwarDeputy Chief ExecutiveSecurities Commission

Malaysia

2

AGENDA

1. Role of the capital market in economic growth

2. Strategies for the development of Malaysia’s capital market

3. Islamic capital market – Development and challenges

3

The capital market as a key driver of private sector growth

0

10

20

30

40

50

60

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 20040

50

100

150

200

250

300

350

400

450

500

New public debt securities issues New private debt securities issuesNew equity issues Nominal GDP (LHS)

Funds raised in the capital market

Source: BNM

New

issu

es (R

M b

il)

Nom

inal

GD

P (R

M b

il)

4

And the equity market performance is largely co-related with long-term income trends

Inde

x po

ints

US

Dol

lars

per

cap

ita

0

200

400

600

800

1000

1200

1400

1600

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

0

1000

2000

3000

4000

5000

KLCI index Per capita income (LHS)

1993: Securities Commission established

1991 New Development Policy introduced,

Privatisation Masterplanimplemented

2004: Demutualisation.

Exchange is listed in 2005

1997: East Asian Financial Crisis

1998: Ringgit peg and capital controls imposed. National Economic Recovery Plan

introduced2001: Launch of

Capital Market and Financial Sector

Masterplans

Source: Thomson Financial Datastream, BNM, SC

5

Relative size of the capital market to the banking sector

Size of the equity market, bond market and banking sector (1990-2004)

0

200

400

600

800

1000

1200

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

RM

bill

ion

Debt securities outstanding

Equity market capitalisation

Banking sector assets

6

The capital market plays a key role in financing diverse needs

• K-economy

– Equity funding through venture capital & MESDAQ Market

• Small-Medium Enterprises

– Equity funding through Second Board & MESDAQ Market

• Privatisation & Infrastructure Projects

– Bonds through issue of Private Debt Securities

– Equity financing through Bursa Malaysia

• Islamic Capital Market (ICM)

– Availability of Syariah-compliant debt & equity securities, warrants &

call warrants

– Availability of Islamic investment products such as unit trusts, Islamic

Indices and Crude Palm Oil futures

7

The Islamic capital market component is a significant part of Malaysia’s capital market

Equity market

• 826 companies out of the 984 companies (84%) on Bursa are Syariah compliant –representing 64% of total market capitalisation (2004)

Private debt securities

• Islamic bonds valued at RM 9.1bn raised during 2004, accounting for 25% of gross issuance of PDS

Market capitalisation-2004 New PDS issued-2004

Islamic25%

Conventional75%

Islamic64%

Conventional36%

8

The capital market also plays an important role in mobilising savings through the investment management industry

0

20

40

60

80

100

1996 1997 1998 1999 2000 2001 2002 2003 2004

RM

bill

ion

20

26

32

38

44

No

of M

anag

emen

t com

pani

es

Unit trust NAV (LHS) No of Management Cos (RHS)

Growth of unit trust and fund management industry

Source: Securities Commission

9

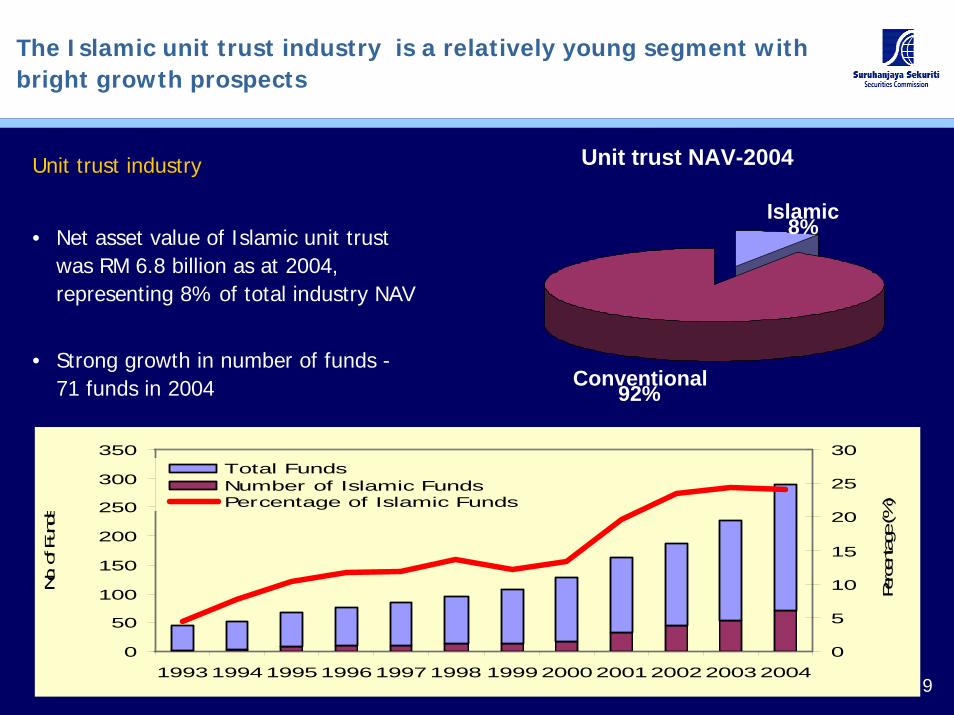

The Islamic unit trust industry is a relatively young segment with bright growth prospects

Islamic8%

Conventional92%

Unit trust industry

• Net asset value of Islamic unit trust was RM 6.8 billion as at 2004, representing 8% of total industry NAV

• Strong growth in number of funds -71 funds in 2004

0

50

100

150

200

250

300

350

199319941995199619971998 199920002001200220032004

No. of F

unds

0

5

10

15

20

25

30

Percen

tage

(%)

Total FundsNumber of Islamic FundsPercentage of Islamic Funds

Unit trust NAV-2004

10

AGENDA

1. Role of the capital market in economic growth

2. Strategies for the development of Malaysia’s capital market

3. Islamic capital market – Development and challenges

11

The Capital Market Masterplan (CMP) provides a strategic roadmap for the development of the capital market

• Equity market• Bond market• Derivatives market• Stockbroking industry• Market institutions

• Investment management• Regulatory framework • Corporate governance• Islamic capital market• Technology & e-commerce• Training & education

With 152 recommendations covering 11 areas:

Vision • To be internationally

competitive,

• To provide an efficient conduit for the mobilisation and allocation of funds, and

• And supported by a facilitative and strong regulatory framework

Vision Vision • To be internationally

competitive,

• To provide an efficient conduit for the mobilisation and allocation of funds, and

• And supported by a facilitative and strong regulatory framework

12

Phased approach to implementation

20062006 2010201020012001 2003 20042004 20052003 2005

PHASE 3PHASE 3PHASE 2PHASE 2PHASE 1PHASE 1•• Strengthen key sectors Strengthen key sectors

and gradually liberalise and gradually liberalise market accessmarket access

•• Enhance market processes and Enhance market processes and infrastructure and international infrastructure and international positioning in areas of comparative positioning in areas of comparative and competitive advantageand competitive advantage

•• Strengthen domestic Strengthen domestic capacity and develop capacity and develop strategic and nascent strategic and nascent sectorssectors

13

Key thrusts: Broaden sources of financing

• Introduced shelf registration scheme to expedite issuance

• 3,5 and 10-year MGS futures contracts to enhance liquidity

and price discovery process in secondary markets

• Facilitative framework for issuance of asset-backed securities

Developed the corporate

bond market

Financed high growth

companies though

venture capital

• Widened the product range

• Introduced a facilitative regulatory and tax framework

• Established strategic alliances with other Islamic capital markets

Accelerated the

development of the

Islamic capital market

• Enhanced participation of local institutional investors

• Introduced a facilitative tax framework

Enhanced efficiency of

fund raising • Reduced processing time for corporate proposals

• Shift to disclosure based regime

14

Key thrusts: Creating a conducive environment for investors

• SCANS, SCORE and SC levy reduced

• Stamp duty capped

Developed a vibrant

investment

management industry

Enhanced investor

protection

Lowered execution cost

for investors

• Greater international portfolio diversification allowed

• Tax incentives to encourage collective investment schemes

• Facilitated the development of financial planning

• Developed the trust and custodial services

• Strengthened corporate governance framework

• Enhanced disclosure & transparency

• Enhanced surveillance and enforcement

• Extensive education programs for directors

15

Key thrusts: Developing strong and competitive intermediaries

Restructured market

institutions

• Consolidation and demutualisation of the exchange

• Enhanced trading, clearing and settlement infrastructure

• Deregulation of fixed fee structures

• Widened scope and range of services

• Deregulated branching restrictions

Fostered constructive

competition

• CLSA, CSFB, JP Morgan, Macquarie & UBS given approval in

principle to establish operations in Malaysia.

• SC to issue up to five new licenses to enable leading global

fund managers to establish operations in Malaysia.

• Allowed 100% ownership of futures brokers and venture

capital companies.

Liberalisation of foreign

participation

16

Key thrusts: Strengthening Malaysia’s capital market position

• Focus on good governance, sound management, building

shareholder valueEnhancing quality of

public listed companies

• Benchmarking; building brand and expanding their franchise

• Professionals and advisors must further enhance their

reputation for integrity and reliability.

Enhancing quality of

capital market

intermediation services

• Review market structure to ensure appropriate access to capital

• Emphasis on enhancing market liquidity.Enhancing quality of

market framework

• Strengthen the gate-keeping function, shift to risk-based

surveillance and expand the range of actions

• Build cross-border surveillance and enforcement capabilities.

Enhancing surveillance and

enforcement

17

AGENDA

1. Role of the capital market in economic growth

2. Strategies for the development of Malaysia’s capital market

3. Islamic capital market – Development and challenges

18

The CMP identified the Islamic Capital Market (ICM) as a key component of Malaysia’s capital market

To establish Malaysia as an international Islamic capital market centre

• Facilitating expansion of products and services in

Islamic capital market

• More effective mobilisation of Islamic funds

• Strengthening tax, accounting and regulatory

framework for ICM

• Enhancing international value recognition of ICM

Key components of the Islamic financial services sector create acomprehensive enabling environment …

Islamic Banking

Islamic capital market

Takaful

• To effectively play its role as an efficient conduit

• Contribute to the overall stability of Islamic

financial services sector:

• Islamic banking to mobilise deposits and

provide financing

• Takaful to provide mutual protection/

institutional investor role

• Islamic capital market to provide long term fund

raising and investment

3

The development of a vibrant ICM is reliant on sound fundamentals ofthe overall capital market

• Sound economic and market fundamentals are important for

instilling greater confidence among investors

• Funds invest in markets that comply with principles of securities

regulation

corporate governance

practices

accounting & tax framework

regulatory framework

country sovereign rating

20

It requires planning and a sound regulatory infrastructure

• Capital Market Masterplan

• Facilitative regulatory framework

• Shariah Advisory Council

have enabled and facilitated the development of

Islamic Capital Market

• Shariah stocks - 84% of total listed shares (April 2005)

• Mutual funds - 71 funds with NAV of USD 1.8 bil & market share of 7.7% (2004)

• Bonds – 25% of total PDS issued (2004)

21

Diverse products and intermediaries and emphasis on education

Tools & ProductsTools & ProductsAvailability of Availability of ShariahShariah--compliant instruments, compliant instruments,

investment and indicesinvestment and indices

IntermediariesIntermediariesAvailability of Islamic banking and Availability of Islamic banking and stockbrokingstockbroking, ,

TakafulTakaful and asset management servicesand asset management services

EducationEducationGeneral awareness & understanding of General awareness & understanding of

Islamic finance conceptsIslamic finance concepts

22

23

Strong support from the government

Budget 2003Budget 2003

Budget 2004Budget 2004

Budget 2005Budget 2005

• Tax deduction for expenses incurred on issuance of Islamic private debt securities that adopt mudharabah, musyarakahand ijarah principles for 5 years commencing 2003

• Deductions given on expenses incurred in the issuance of Islamic securities based on the principle of Istisna for 5 years where property under construction can also be used to back such bonds

• Tax exemption on interest income derived by non-resident companies from ringgit-denominated Islamic securities and debentures

• Tax neutrality between Islamic and conventional products by exempting additional tax or duty provided the products are approved by the Syariah Advisory Council

24

Developing internationally-compatible Islamic accounting standards

Most jurisdictions apply IAS/GAAPs for their financial institutionsMost jurisdictions apply IAS/GAAPs for their financial institutions

• Most jurisdictions apply IAS for Islamic financial institutions

• 4 jurisdictions (i.e. Jordan, Sudan, Bahrain and Qatar) apply AAOIFI accounting standards

• These jurisdictions apply IAS for areas not covered by AAOIFI accounting standards

IAS AAOIFI stds. / IAS National Islamic accounting standards / IAS

• Malaysia applies national Islamic accounting standards for Islamic financial institutions

• IAS are used for areas not covered by national Islamic accounting standards

In addition, for Islamic financial institutions, the following is applied

In addition, for Islamic financial institutions, the following is applied

Ensuring international compatibility with global securities regulation

IOSCO appointed an ICM Task Force to assess the state of development & regulation of Islamic capital markets globally

Memberships:

Malaysia, Bahrain, Indonesia, Jordan, Nigeria & Turkey

Australia, Italy, South Africa, Thailand, UK & US

Key issues and findings of ICM Task Force report :

Shariah convergence

Shariah compliance and regulation

Product innovation & market competitiveness

Accounting & tax framework

Skills development

International cooperation

Information database

25

Malaysia has broad experience in promoting international cooperation and cross-border investments in ICM

• Participation in international efforts such as IFSB and IOSCO ICM Task Force

• Facilitates cross border issues

• Issuance of Malaysian global Islamic bonds

• Promotion / offering of foreign Islamic bonds in Malaysia

• Fund raising exercise by multilateral banks and MNCs

• Participation in overseas Islamic private equity investment

• Knowledge sharing and mutual assistance programmes

26

27

Thank youThank you