a revised management cost recovery (levy) framework for ... · a revised management cost recovery...

TRANSCRIPT

A revised management cost recovery (levy) framework

for the Commonwealth South Eastern Scalefish and

Shark Fishery (SESSF)

Project report for the Australian Fisheries Management Authority (AFMA)

July 2012

Note: This report is not for further distribution unless

authorised by AFMA’s Executive Manager Fisheries.

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page | 2

Contents

Project Overview ............................................................................................................... 3

Deliverables ....................................................................................................................... 3

Regulatory Basis for AFMA’s Levy Collection ................................................................ 3

Current SESSF Levy Framework – Problem Analysis ...................................................... 4

Revised SESSF Levy Framework - Design Principles .................................................... 11

Revised Levy - Options ................................................................................................... 11

Additional Issues for Consideration................................................................................. 21

Appendix 1 - SESSF quota species management cost matrix ......................................... 24

Appendix 2 - Example of revised SESSF levy model and explanatory notes ................. 26

Appendix 3 - Summary of Project Consultation .............................................................. 28

Acknowledgements

AFMA staff, and SEMAC and its Levy Working Group members have provided valuable

background information, detailed fishery specific knowledge, and valuable critique of various

options explored during the project.

In particular, an AFMA “focus group” comprising John Garvey, Trent Timiss, Andrew

Powell, Malcolm Southwell, and Brad Milic have all been generous with their time, and

helpful in the development, analysis, and critique of various options.

The project has taken place during a very busy period for all AFMA staff in the lead-up to

their next budget, significant staffing changes in the Fisheries Branch, and the ongoing need

to address various high priority fisheries management issues.

There are also very challenging business circumstances confronting some SESSF fishing

businesses, including recent surrenders of SESSF concessions due to financial hardship. To

their credit, fishing industry members of SEMAC and the Levy Working Group have

remained helpful and constructively engaged with the process to revise the SESSF levy

framework.

For questions about this report please contact either:

Andy Bodsworth,

Director, Cobalt MRM Pty Ltd

Ph: 0439602769

www.cobaltmrm.com.au

Or AFMA’s Senior Manager for the SESSF via 02 62255555.

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page | 3

Project Overview

AFMA contracted Cobalt Marine Resource Management Pty Ltd (Andy Bodsworth) to

continue work by AFMA, industry, and the SEMAC levy working group to refine the current

SESSF levy framework. A copy of the contract, including details of conditions, services,

deliverables, and fees and allowances is available on AFMA File F2012-0441.

AFMA and SESSF concession holders have recognised that the existing SESSF levy

framework is no longer the most accurate and equitable approach to collecting recoverable

fisheries management costs for these fisheries. This has been further emphasised by

stakeholder correspondence questioning the accuracy and equity of the previous approach;

and a recent Senate disallowance motion for the Levy Regulations (subsequently overturned).

The revised SESSF levy approach must be consistent with AFMA’s 2010 cost recovery

impact statement (CRIS), and relevant legislation and policy. It must accurately attribute

recoverable costs to beneficiaries (i.e. those generating the work/cost), and recover those

costs from those beneficiaries (the User Pays principle).

The new levy approach should also be transparent, and cost effective and efficient to apply.

Where appropriate it will be complemented by a fee for service approach for specified

AFMA services1.

Deliverables

Master excel spreadsheets developed as the basis for calculating levy under the proposed

framework have been provided separately to AFMA. These include the management cost

matrix, and a workbook to calculate the ITQ and Boat SFR components of the SESSF levy.

This report provides a record of the process and key issues considered in developing the

proposed model. It also describes how the model works, and the data inputs.

Electronic files generated during the project, including a large amount of background

material used for analysis, and development of the proposed model, are available on AFMA’s

Fisheries Branch Drive at H:\Southern Fisheries Section\Finance\Levies_ALL Southern

fisheries\2011-12 Levies\Andy Bods\.

Regulatory Basis for AFMA’s Levy Collection

The 1991 Fisheries Administration Act (FAA) requires recovery of AFMA’s fisheries

management costs in accordance with government targets. These targets and broader policy

guidelines are detailed in the Australian Government Department of Finance and

Deregulation (DoF) cost recovery guidelines.

AFMA’s Cost Recovery Impact Statement (CRIS) was revised in 2010 to reflect the most

recent DoF cost recovery policy requirements; and changes to AFMA’s operating

environment and functions since the previous (2004) CRIS.

Principally this includes the 2005 Ministerial Direction to AFMA, refinements to the ESD

objective, and definition of economic efficiency in the Fisheries Management Act 1991

(FMA); and changes to AFMA’s operating structure and processes following the 2007-08

Business Efficiency Review & Cost Reduction Working Group processes.

AFMA’s fisheries management levies are collected on the basis of Fishing Levy Regulations

made each year under the Fishing levy Act 1991 and the FMA. The Levy Regulations

describe the fisheries for which levy is payable, amounts payable for each fishing concession

type, due dates for payment, and relevant supporting information.

1 AFMA’s proposed Fee for Service Policy is currently being finalised.

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page | 4

Current SESSF Levy Framework – Problem Analysis

The fisheries management and regulatory challenges inherent in developing an accurate and

cost effective levy framework for a relatively complex multi species multi method fishery

like the SESSF are compounded by the current operating environment for AFMA and

commonwealth fisheries. As cost management becomes increasingly critical for fishing

businesses and governments, regulatory activities, like levy collection, are under increasing

scrutiny. Key issues identified during the review of AFMA’s existing levy approach, and in

considering options for a revised approach, are illustrated below (Figure 1).

In addition there are ongoing changes to fishing businesses, including the gear used and its

impact on the broader marine environment; and the composition of target, byproduct, and

bycatch species across fishing businesses within a fishing sector (e.g. Trawl Fisheries); and

across sectors (e.g. GHAT sub-sectors such as Gillnet, Autoline and Dropline).

Under AFMA’s user pays approach, the recoverable costs generated by AFMA’s fishery

management activities must be accurately attributed to the entitlements (e.g. Boat and Quota

SFRs, permits) that use or benefit from those services. Ideally this requires accurate

estimates (or records) of time/activities against the various budget line items (account codes)

that make up the recoverable costs for a fishery. Some of these activity areas (including

various classes of AFMA overheads) will be attributable to several fisheries across a fishery

group (e.g. some or all of the SESSF sectors).

There is potential for this process to be complex, time consuming, and expensive to

administer. The administrative costs of collecting and using such management cost data for

the levy process must also be considered alongside the benefits these data generate.

Applied accurately, consistently, and promptly, the user pays approach can make the

economic and environmental cost and benefits of fishing activity more transparent. This

price signal can be used to improve ESD and industry business efficiency outcomes by:

generating incentives to reduce fishing impacts and costs through improved fishing

practices; and promoting efficient R&D to mitigate fishing impacts/costs;

focusing AFMA and industry on the issues generating most cost, and encouraging

cost benefit appraisal against AFMA’s legislative and policy objectives; and

industry’s business objectives;

providing a clear incentive to maintain stocks at ecologically sustainable and

economically efficient levels (where management costs should also remain more

stable, and at appropriate levels). This is similar to the cost/risk trade-off approach

embedded in the Commonwealth Harvest Strategy Policy.

Detailed awareness of the cost structure of any business, and subsequent cost management is

also a key driver of business profitability. Accurate and reliable cost and activity data can

help AFMA and industry review exactly where time is being spent and costs incurred; and if

activities are delivering on organisational priorities.

This can underpin development of more efficient work processes, encourage collaboration

with industry on cost reduction opportunities, and improve accountability and fiscal

management through improved budgeting (forward estimates), and management of budgets

throughout the year.

At AFMA’s request the review did not further develop options to use a more detailed activity

based costing (ABC) approach to estimate/record management costs against specific projects

and/or beneficiaries. Noting that the level of detail in cost data available to accurately

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page | 5

estimate and attribute costs is variable across SESSF fisheries, and the relationship between

management activities, costs, and beneficiaries is complicated and dynamic; ABC may prove

to be the most robust and cost effective approach for more complex and higher cost/risk

management activities.

Contemporary time tracking and project management software to enable an ABC approach is

widely available and increasingly user friendly and cost effective. Selective, or agency wide,

adoption of this sort of approach warrants further consideration. Opportunities to use ABC to

inform AFMA’s cost recovery and levy processes have been identified throughout the project

and are noted in this report.

Project Assumptions and Constraints

The project has focused on understanding AFMA’s recoverable fisheries management

costs for SESSF sectors in the context of how these can be more accurately estimated

and aligned with beneficiaries via the ITQ and Boat SFR components of the levy. The

review has not attempted to analyse AFMA’s work processes, or the outcomes of

those in detail2.

The proposed SESSF levy framework is based on costs attributable to industry under

CRIS 2010. If CRIS 2010 changes, the new SESSF levy framework may need to be

updated.

The need to estimate a common management cost per SESSF quota species3 in line

with the transferability of SESSF quota across various fishing methods, the nature of

AFMA’s quota management and licencing systems (e.g. ITQs are not linked to fishing

methods within the SESSF), and the desire to collect a substantial proportion (e.g. 60-

80%) of recoverable management costs via that ITQ levy component, substantially

constrain options for the revised levy framework.

2 Recognising that corporate processes to ensure ‘the right work is being done efficiently” are critically

important to ensuring cost effective and efficient fisheries management that is then cost recovered via the levy

process. 3 This contrasts with the reality that there are substantially different “management costs per species” across

some SESSF fishing methods due to the different ecological footprint of these gears at different effort levels.

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Figure 1: Key issues for consideration in the development of a revised SESSF levy framework

Objective:

Accurate cost estimation &

recovery under user-

pays

Financial management

(estimates & budget

management) Accurately estimating

activities/time against

fisheries/users

Relatively high management

costs for some fisheries

Surrender of Concessions

increasing costs for remaining

fishers

% of costs to ITQs Vs Boat

SFR component (policy, price

signal?) Some

permits/sectors & species are

not levied despite their

costs

All Stakeholders should have

input into the model to be

used

Promote Levy stability across

years

Transparent model needed, consistent levy

design principles

across AFMA

Should GVP be used to

determine levy payable per

species?

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 7

The issues outlined in figure 1 are discussed below.

SESSF Levy Issue Relevance

1. Accurate Cost

Estimates for levy

purposes

Efficiently recovering the costs of AFMA’s fisheries management

services from the beneficiaries of those services is a legislative

requirement. Policy guidance is provided in AFMA’s CRIS 2010.

2. Accurate Cost

Attribution

As above. Current budget (cost centre) structures such as the different

fishing methods within the GHAT cost centre complicate this process

(in part because these methods generate different management costs per

species). Availability and accuracy of data to support cost attribution

varies across budgets and fisheries.

3. High Management

Costs in some

Fisheries

Some SESSF fisheries - particularly some GHAT sectors - currently

have relatively high management costs. Industry remains concerned

that these costs are not reducing commensurate with reductions in fleet

sizes, and/or AFMA’s cost management is not responsive enough to

adapt promptly to changing business circumstances.

4. Proportion

recovered via ITQ

Vs Boat SFR

The SEMAC Levy Working Group has recommended a greater

proportion of the recoverable costs be accrued to the ITQ component of

levy. This recognises that quota owners are relatively greater

beneficiaries of fisheries management services and should pay costs

commensurate with their holdings.

5. Levy Stability Levy stability from year to year is important for industry business

planning and management. It is also a sign of an accurate and

equitable cost recovery mechanism (given minor variations in budgets

from year to year). Unexplained significant variations in levy for a

fishery from year to year also reduce AFMA’s efficiency and

effectiveness, and reduce stakeholder confidence in AFMA’s

regulatory performance.

6. Budgets – Forward

Estimates

Recoverable management costs are driven by fishery budgets and

application of AFMA’s CRIS. Accurately forecasting work programs

and resourcing, and AFMA and industry commitment to these priorities

will increase management efficiency and levy stability across years.4

7. Budgets – Fiscal

Management

Strong fiscal management within a financial cycle will improve

AFMA’s efficiency, effectiveness, and standing with stakeholders.

This will also work to improve levy stability across years.

8. Should GVP be

used to calculate

per species costs

AFMA’s previous SESSF levy model used each species’ proportion of

GVP relative to total SESSF trawl GVP to determine the proportion of

total recoverable Tier 2 costs attributable to that species. Whilst

relatively simple and cost effective to apply, this process did not

accurately attribute actual management costs for those species to

beneficiaries. This also meant that an increase in GVP that resulted

from improved product quality, market demand etc translated into

4 Recognising that unforseen management issues will arise, and subsequent management options should be critically

evaluated and accurately costed before implementation.

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 8

increased levy even though actual management costs for that species

may not have changed - in this sense it acted more as a tax than an

accurate management cost recovery mechanism.

9. Transparency Recovery of fisheries management costs using a common per species

cost across multiple species and fishing methods, each with differential

environmental impacts and management costs, is complex. For

administrative fairness, and to promote stakeholder engagement and

support, the process to develop the revised levy model and the rationale

for the chosen approach must be clear to stakeholders.

As well as consultation and guidance from SEMAC and the LWG;

broader consultation with all SESSF concession holders for their input

and to facilitate their engagement and understanding is appropriate.

10. Knowledge

Management

A clear understanding of principles underlying the revised levy model,

how the model is structured and key input variables will assist in

implementation and ongoing refinement of the model as the operating

environment for AFMA and Industry evolves. This report is intended

to capture relevant project knowledge, and make it readily accessible to

AFMA staff.

11. Surrender of

Concessions

As fisheries become more efficient and/or business circumstances

become more challenging, surrender of fishing concessions is likely to

continue. Remaining concessions pay relatively more management

costs. This emphasises the need for economically efficient fisheries

management, including strong cost management.

12. Transition from old

to new levy

framework

Whilst the total amount recoverable via the SESSF levy process will

not change under the revised framework (this amount is a function of

the budget and application of the CRIS), there will be some SESSF

concessions paying more, and some paying less under a more accurate

cost attribution model.

Importantly, some concession holders appear to have recently

surrendered concessions due to significant levy variations and for

affordability reasons. Where the new SESSF levy framework results in

substantial changes (without commensurate changes in recoverable

costs), particularly coming after some significant levy increases in

recent years; a process to ensure administrative fairness is

recommended.

Other specific issues and concerns about the existing levy framework have been raised in industry

correspondence to AFMA and SEMAC. Key issues include:

Concerns about the apparent disproportionate levy cost of GHAT Scalefish Hook Boat

SFRs used for small scale manual baiting versus costs for a GHAT auto longline permit;

Concerns about how additional management costs in some GHAT sectors (e.g. Gillnet)

appear to have flowed in to increase levy payable by other GHAT sectors. For example,

why are Scalefish Boat SFRs for fishers targeting relatively small amounts of blue eye via

dropline costing as much as Boat SFRs /permits authorising significantly higher levels of

fishing effort (e.g. auto longline) that are likely to drive higher management costs;

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 9

Will South Australian gillnet fishers provided with temporary (12-18months) concessions

to fish via hook methods, as a management response to TEP interactions, be required to

pay a similar levy to other SESSF hook entitlements?

A more strategic context for the SESSF levy review, including how a revised levy approach can

best contribute to AFMA’s Ecosystem Based Fisheries Management (EBFM) objectives in the

medium term, is illustrated below (Figure 2).

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 10

Current State 2012:

Target and Byproduct increasingly well

managed under strong policy framework

(i.e. Commonwealth HSP)

Efficiency of management being

addressed/improving & profitability

generally improving (excepting some

externalities)

Bycatch/TEP management and WoG TEP

policy is less developed and is

undermining efficiency

AFMA Levy processes improving (tighter

budgets, more accurate cost estimation &

attribution)

More Efficient State 2015+:

Purer ITQ system (no boat SFR’s??)

Fishing is More Profitable &

Sustainable

Bycatch/TEP management improved

(in part from preceding strong price

signal & strong WoG policy in place)

Improving AFMA & Industry

efficiency/business productivity (e.g. e-

monitoring, fee for service, co-

management)

More Activity Based Costing (tight cost

management, budgeting, more business

intelligence informing productivity

gains)

Functional importance of price signal

reducing over time as best practice

policies in place and AFMA/industry

capability improves

Clear price signal (via Boat SFR levy

component for method based issues) drives

better environmental performance &

improving management efficiency.

Better cost data informs understanding of

costs and potential regulatory and business

efficiencies for AFMA & Industry

Refining the SESSF Levy – Strategic Outlook

User Pays, Price Signals, and the path to more efficient and

effective Ecosystem Based Fisheries Management

Figure 2: schematic of the strategic role of a revised SESSF levy framework

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 11

Revised SESSF Levy Framework - Design Principles

Design principles for the new levy model centre on government’s cost recovery requirements

as reflected in AFMA’s CRIS 2010. The User Pays principle is central, and the new levy

model needs a clear link between those AFMA services generating recoverable management

costs and the beneficiaries of those services. It should also encourage strong cost

management.

Further guiding principles for the new SESSF levy model have been developed in

consultation with SEMAC and its levy working group, and AFMA staff:

Recoverable management costs should be attributed to the groups that generate them,

and (where appropriate) should include sectors which currently do not pay levies;

The model should deliver a stable levy rate for an individual concession when all

other factors remain relatively constant (e.g. if management costs are unchanged, then

levy on an individual concession must not change either);

The model should be clear and logical, and cost effective to administer;

Cost increases in one fishery should not flow into other fisheries unless those costs are

also attributable to the other fishery;

The levy approach that informs the model should encourage good budget

management and accountability for both AFMA and Industry;

The basis for management costs and their attribution to fisheries/individuals must be

clear;

A fee for service approach should be used where appropriate.

User pays principle – fee for service

AFMA is also adopting a fee for service approach where services are clearly attributable to a

client, agency, or entitlement holder/fishery. For example data management costs associated

with a report on catch history for a specific entitlement/permit to support the commercial sale

of that entitlement might be recovered on a fee for service basis.

Fee for service can also encourage critical evaluation of a service i.e. is there a net benefit

from the activity; and mitigates the risk of cost shifting to non beneficiaries. It also offers a

clear and timely price signal. This can promote accountability, innovation and collaboration

between AFMA/industry, and underpin productivity increases.

Revised Levy - Options

Under the current SESSF levy framework, total recoverable fisheries management costs are

made up of two components, the ITQ (or Tier 2) component, and the Boat SFR (Tier 1)

component. The ITQ component is intended to capture the majority of recoverable fisheries

management costs (see Figure 4) that are generated under the SESSF fisheries management

system. This recognises that a concession holder with greater quota holdings is a relatively

greater beneficiary of AFMA’s fisheries management services.

Estimating recoverable fisheries management costs is relatively straightforward where there

are a small number of target species and/or fishing methods that are broadly equivalent in

their management costs. Recoverable costs can be aligned relatively easily to these species’

for the ITQ component of a levy, and to the Boat SFRs or permits in use for that fishery.

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 12

Developing an accurate levy model for multiple SESSF quota species caught by a range of

fishing methods, all of which have different ecological risk profiles, is more complex. If the

various SESSF sectors (methods) across which quota species are caught were broadly

equivalent in their management costs then a common SESSF “management cost per quota

species” (cents/kg) could be calculated from the combined recoverable costs of all SESSF

cost centres. This would be relatively straightforward, and would generally reflect the user-

pays principle.

In practice, some species are inherently more complex or costly to manage; and various

SESSF sub-sectors (fishing methods) also generate different management costs depending on

the “efficiency” of that fishing method, and of the fishery more broadly (including costs

arising from differential environmental impacts, cross jurisdictional management complexity,

efficiency of research processes, economies of scale for the fishery etc). The definition of

these cost data is also variable across fisheries. This makes it more difficult to analyse real

management costs per species, or costs for a fishery method within a sector such as the

GHAT.

If these extra “method specific” costs are spread across several fisheries, or accrue to the ITQ

component of the levy according to number of SFRs of a species held, irrespective of the

method used to take these species, then there will be some cross subsidisation across those

various SESSF sectors.

Such cost spreading also dilutes the “price signal” that an accurate user pays system

generates. It makes it more difficult for fishers to understand the detailed management costs

for their fisheries, and develop efficiencies to reduce those costs. It also reduces incentives to

reduce costs because these costs are partly subsidised by other sectors.

For example, costs that make up the Commonwealth Trawl Sector (CTS) budget are

relatively clear and linked to only one fishing method; whilst total Gillnet, Hook, and Trap

(GHAT) Fishery costs (expressed as one cost centre/budget) are made up of various costs

incurred in managing those separate fishing methods (e.g. gillnet, dropline, auto longline,

shark trotline etc). Limited activity/cost data for each of these discrete methods makes it

more difficult to separate the total GHAT budget and accurately attribute costs to

beneficiaries in line with user-pays.

It is relatively straightforward to estimate/calculate a “management cost per quota species”

value for species taken in the CTS, or by trawl generally, and then levy CTS operators based

on the quota they own. This is a reasonably accurate and fair method to attribute

management costs to beneficiaries using a common fisheries management “currency” such as

species specific ITQs.

For the various GHAT sectors this management cost attribution is more complicated. These

various fishing methods have differential management costs, and a broader range of

beneficiaries. If the total costs across GHAT sub-sectors are simply lumped together, and

divided and recovered without acknowledging the differential costs between methods, levy

paid in the more efficient GHAT fisheries (or those with less environmental impacts/costs

etc) will be greater than true management costs. These fisheries would be partly subsidising

less efficient fisheries or methods.

Such cross subsidisation will also reduce the incentive for less efficient fisheries to

find/develop management practices that reduce their costs (e.g. mitigation strategies that

reduce bycatch impacts/costs; or via research efficiencies such as moving to stock

assessments every 2 or 3 years where appropriate).

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 13

The revised SESSF levy approach must also work with AFMA’s recently upgraded licencing

and quota management systems. In brief, these systems encourage efficient trading of quota

across SESSF sectors. There is no such thing as a method specific SESSF quota SFR/unit, so

there is no practical and cost effective way of accurately linking a species specific quota SFR

(say gummy shark) to a method, such as gillnet or hook.

Therefore it is not feasible to estimate method specific management costs for each of the

SESSF quota species – and then recover those method and species specific management costs

via an ITQ component of the levy.

For example a Gummy Shark quota owner might have a portion of their quota that is

nominated to a gillnet boat, another portion nominated to a trawl boat, and some remaining

“unfished” as a static investment. Amounts of quota nominated to each of these various uses

change over time as quota owners/fishers trade via AFMA’s Gofish quota trading system to

suit their business circumstances.

The alternative to this “method specific management cost per quota species” approach is to

collect a baseline management cost per species that can apply across the multi species, multi

method nature of SESSF fisheries.

To minimise the risk of cross subsidisation (e.g. to ensure that levy payable on Gummy Shark

Quota used by a CTS operator does not also include the additional TEP related costs of the

Gillnet sector) this baseline management cost per species must, as much as possible, reflect

the inherent management complexity/costs for each SESSF quota species.

A matrix to estimate these inherent management costs per SESSF quota species, using

weighted “management cost categories”, has been developed (see management cost matrix at

Appendix 1.).

Where there is a substantial management cost differential between methods, and one sector

catches the majority of the TAC for a species (e.g. GHAT fisheries and Gummy Shark), it is

possible to increase the management cost per SFR to more accurately reflect the method

specific management cost for that species5.

This can be done without having a substantial impact on the levy cost of the ITQs for that

species held in other “non-target” fisheries (e.g. when a small amount of Gummy Shark quota

is held across these other fisheries to cover incidental and small amounts of bycatch).

Where this baseline management cost per species does not recover (via the levy process) the

true costs of a particular fishery/method, the Boat SFR component of the levy must be used to

collect those additional management costs. These extra costs are generally driven by the

broader environmental impacts of a particular fishing method.

Preferred Option:

To minimise the risk of cross subsidisation6, and thus enable a robust baseline “management

cost per quota species,” for all SESSF quota species taken irrespective of method, the

management costs for quota species taken in the CTS can be used. The CTS is a large and

reasonably efficient fishery, and there is reasonable cost data largely quarantined to that

fishery/method.

5 For example, increasing the management cost multiplier for Gummy Shark above the “inherent management

cost” derived from the per species management cost matrix (Appendix 1) can enable a higher proportion of

gummy shark related management costs to be recovered via ITQ holdings rather than Boat SFR levy fees. 6Including the risk that the ITQ based levy for a quota species may include the embedded management costs of

fishing methods that have a higher ecological impact (and management cost) due to fishing for that species.

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 14

This CTS derived “management cost per quota species” will not reflect the true management

costs for those various species if they are taken by other fishing methods. This “management

cost differential” will thus need to be recovered via the Boat SFR component. For methods

where the cost differential is high (e.g. Gillnet sector currently) a significant proportion of the

total levy cost could fall on Boat SFRs7.

The process to calculate both the ITQ and Boat SFR/Permit components under the revised

SESSF levy approach is described in table 1 below.

Final Levy Amount Payable

Once AFMA’s budget for each fishery has been developed for the coming financial year, any

over or under collection of levy from the previous year is added or subtracted to make up the

final budget. The ITQ and Boat SFR components of the new levy are then determined (Table

1 below), and the Fisheries Research and Development Corporation (FRDC) GVP based

research levy is added to the per species management levy. This total, and the amount

payable for each Boat SFR or Permit, are added to make up the final levy amount payable per

concession or package of concessions.

7 This will depend on the amount collected for key GHAT target species as described in footnote 6 above.

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 15

Table 1: proposed approach to calculate the ITQ and Boat SFR components of the SESSF Levy

SESSF sector Boat SFR component ITQ component

Trawl (CTS)

CVIT, ECDWT

The CTS Boat SFR component is calculated directly

from the CTS budget using costs attributed to the Tier 1

(Boat SFR) component of the CTS budget using generic

Tier 1 & 2 splits (see Table 2).

These total recoverable Tier 1 costs are then divided by

the number of CTS Boat SFRs to get the levy payable

per Boat SFR.

It is likely to be more cost effective and efficient to

aggregate management costs for these minor trawl

sectors into an overall SESSF Trawl Sector Budget

(excluding GAB Trawl).

The trawl manager can then use the best available

cost/activity data to estimate the Boat SFR component

of costs attributable to CVIT and ECDW respectively.

Alternative (if these cost centres are retained) – calculate

Boat SFR levy directly for these separate budgets using

the Tier 1 and 2 splits as for CTS above.

For levy purposes, a baseline or inherent management cost for

each SESSF quota species is estimated from a matrix of

weighted “management cost attributes”. This management cost

score for each quota species is used as the species specific

“management cost multiplier (see Appendix 1).

A “weighted catch value” is then calculated by multiplying the

trawl catch of each species in kg by the management cost

multiplier for each of those species (see Appendix 2.).

Each species’ weighted catch value is then divided by the sum of

all species’ weighted catch value and multiplied by the total

recoverable Tier 2 cost8 for the combined SESSF trawl fisheries

(ECDWT, CVIT, CTS). This gives an amount ($) to be

recovered - representing the species specific proportion of tier 2

costs for each quota species.

This is then divided by the total number of SFRs allocated for

each species to give the levy cost per SFR (cents per SFR) for

each SESSF quota species.

The cents per SFR value is multiplied by the amount of quota

owned of each SESSF quota species to derive the Tier 2 – or

ITQ component – of levy payable per species for SESSF quota

owners.

Summing the total Tier 2 levy amount payable from all SESSF

quota owners provides the total amount recovered across all of

the SESSF fisheries via the ITQ component of the levy.

8 The total recoverable Tier 2 costs for the trawl sectors used in the formula are derived by apportioning SESSF trawl budgets according to the Tier 1 and Tier 2 cost proportions

(see Table 2).

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 16

For the trawl sectors, on which this baseline per species

management cost is based, the Tier 2 amount recovered will be

around 85% of the combined trawl budget (see Figure 4.).

GHAT Gillnet Once all of the costs attributed to Tier 2 (ITQ

component) for the GHAT sectors have been calculated

(based on GHAT catches of SESSF quota species for the

previous year), this amount is subtracted from the total

recoverable costs for the GHAT budget to provide the

balance of GHAT costs that must be recovered.

This residual GHAT amount (or balance) will be the

Boat SFR component to be collected across all of the

GHAT sectors (as defined by Boat SFR types or permit

types).

The GHAT manager/s then estimate (based on the best

time/cost data available) the relative proportion of this

total cost that should be attributed to each GHAT

subsector.

This subsector total is then divided by the number of

Boat SFR’s/permits in that subsector to give the Tier 1

component payable for each concession type.

For GHAT fisheries the amount collected via the baseline ITQ

component of the levy (described above) will not be enough to

collect a significant proportion (e.g. 85%) of the recoverable

management costs for these fishing methods. This is because

the estimated management cost per SFR based on the trawl

fishery cost equation under-represents the true management cost

for most of the species taken in GHAT sectors.

This under-collection issue can be addressed by either:

a. Estimating a species specific management cost for the 3

primary GHAT target species (Blue Eye Trevalla,

Gummy Shark and School Shark) using the GHAT

fishery costs and catches of these species9, or

b. Making up the balance of GHAT ITQ levy under-

collection by recovering these residual “method specific”

GHAT management costs via the Boat SFR component -

of the levy - as described at left.

Auto LL

Manual baiting

trotline

Manual baiting

dropline

Trap

SA and Tas Coastal

Waters Permits

(combinations of

Gillnet, Hook, both)

Calculate Boat SFR component as for GHAT methods above. Where these permits are currently linked to a

Commonwealth Boat SFR they do not pay levy, although these linked permits do have a management cost. A decision

whether to “delink” these permits and levy them separately requires further consideration and discussion, including the

fisheries management implications of delinking, and any prior agreements relating to payment of levy for these permits.

9 This is the preferred approach as it enables a significant proportion of GHAT management costs for these species to be collected via the ITQ component of the levy consistent

with user-pays, and as requested by SEMAC and the Levy Working Group.

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 17

Number of SFRs owned for

each species multiplied by

the cents/SFR cost for that

species determines a

fishers’ ITQ levy

component

A baseline management cost

(cents per SFR) is calculated for

each quota species based on total

ITQ component of levy payable

for the CTS

Each SESSF quota species

receives a management cost

ranking using weighted

criteria as proxies for species

specific management costs

Total recoverable management

cost for each SESSF fishery (note GHAT sectors are

currently one cost centre)

This ITQ component (cents/SFR per

species) is consistent across SESSF

sectors & represents a baseline

management cost per species

Costs generated by Boat SFR

administration, and an agreed %

of bycatch/TEP & environment

related management costs are

attributed to Boat SFR component

for each sub-sector (method) of

the SESSF

Comprises approximately

86% of total levy

(CTS FY 11-12 example) Comprises approximately 14%

of total Levy for the CTS (using

Budget for FY11-12). For high

impact GHAT sectors it may be

more depending on how much is

collected via the ITQ component

ITQ Component (Tier 2)

Boat SFR Component (Tier 1)

Figure 3: overview of proposed SESSF levy framework

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 18

Boat SFR component

is 14% ($390,458)

Cost Inputs to SESSF

Levy

ITQ component is

86% ($2,413,099)

Total recoverable

management cost is

$2,788,987.

30% Fisheries Management

Services (FMS)

70% $763,535 (incl overheads)

30% SEMAC running costs 70% $79,247

0 Logbook Program costs 100% $156,714

30% Data management costs 70% $105,917

0 Licencing and quota

management costs

100% $103,193

0 PISCES and Gofish

amortisation

100% $68,950

20% Observer program costs 80% $325,340

0 Research (RAG,

Administration)

100% $227,665

0 Research projects 100% $871,058

30% Compliance Data

Collection

70% $87,368

Figure 4: Schematic of revised SESSF Levy Framework using CTS FY 2011-12 Budget

Costs attributed to ITQs

owned for each species (cents

per kg per species remains

constant across SESSF sectors

Costs attributed to Boat SFRs

for each AFMA cost

centre/fishery (high impact

methods will pay relatively more

via their Boat SFRs

Total costs recoverable from

SESSF industry sectors

(using FY2011-12 Commonwealth

Trawl Sector Budget)

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 19

Table 2: New SESSF Levy Framework - attribution of costs to Tier 1 and Tier 2 of the levy.

Proposed SESSF Levy model – attributions to Boat SFR and ITQ components of the levy for major cost activities

Cost Component Previous Model –

proportions used to

calculate ITQ and Boat

SFR components

Proposed - Boat

SFR component

Proposed

ITQ

component

Rationale

Fisheries Management

Services (FMS)

50:50 30% 70% Majority of work (cost) is core fisheries management with a

proportion (30%) attributable to method specific bycatch

issues (i.e. not spread across ITQ component)

SEMAC running costs 0:100 30% 70% As above assuming MAC work is closely related to time/cost

incurred for fisheries management services

Logbook Program costs 50:50 0 100% Majority of these costs are based on core fisheries management

(i.e. primarily quota species management)

Data management costs 50:50 30% 70% Proposed split assumes data support activities are closely

related to proportion of fisheries management services (e.g.

some time for Bycatch/TEP issues, spatial management

development)

Licencing and quota

management costs

30:70 0 100% Costs are almost all attributable to core fisheries management

(i.e. primarily SESSF quota species management)

PISCES and Gofish

amortisation

30:70 0 100% As above

Observer program costs 0:100 20% 80% Majority of work (cost) relates to core fisheries management.

A proportion (20%) relates to bycatch/TEP management.

Specific Bycatch related observer programs may be fee for

service.

Research (RAG,

Administration)

0:100 ( 65% trawl, 25%

GHAT, 10% GAB)

0 100% Research costs are one of the 6 weighted categories used to

estimate the inherent management cost per species that is then

used as the basis for the SESSF ITQ component of the levy.

Research is a high cost activity (e.g. approx 30% of the

recoverable costs for the CTS) and therefore carries the highest

weighting of the 6 activity categories (see Appendix 1.).

Research projects 0:100 (as for research) 0 100% As above (most cost is in stock assessment projects). Guidance

about research beneficiaries is available from an FRDC

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 20

projects’ flow of benefits section.

Compliance Data

Collection

20:80 30% (use FMS as

proxy?) also VMS

is based on # of

boats (i.e. boat

SFR)

70% 70% recognises that most VMS work is for quota

management/fisheries management with a proportion

attributable to Bycatch issues. VMS costs to a fishery are split

according to the number of nominated boats.

Average attribution Boat

SFR: ITQ component

Average across all

management cost splits

for current method

approx 25% to Boat SFR

and 75% to ITQ

component

Average under new model approx

14% to Boat SFR and 86% to ITQ

component

Relative split Boat SFR to ITQ component can vary according

to method and relative importance/cost of bycatch related

issues.

This proportion could be set each year based on MAC

discussion, or set for several years in a more stable

management environment to promote transparency and levy

stability (also subject to budget stability).

Overheads – Type A (CEO, GM CG, Exec Sec,

Legal – net of policy

support, senior economist,

comms)

Type A’s proportional to

fisheries direct cost

budgets

30% 70% Could be allocated to a fishery cost centre based on FTEs as

proxy for workload; and then split to T1 and T2 using the FMS

Vs Bycatch split as proxy for AFMA Executive’ work on that

fishery

Overheads – Type B

(Finance, HR, IT,

Corporate Risk)

Based on FTE’s Based on FTE’s 100% No change to broad approach but these costs then attributed

100% to ITQ component of SESSF levy

Overheads – Type C

(office services, facilities)

Based on Canberra

FTE’s

Canberra FTE’s 100% No change to broad approach but these costs then attributed

100% to ITQ component of SESSF levy

Overheads – Type D

(Commission, EM

Fisheries, GM Ops – all

net of policy support)

Type D’s split across

fisheries and operations

cost centres as for Type

A O’heads

30% 70% As suggested for Type A’s – i.e. could be allocated to a fishery

cost centre based on FTEs as proxy for workload; and then

split to T1 and T2 using the FMS Vs Bycatch split as proxy for

Commission and Executive’ work on those issues in that

fishery

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 21

Additional Issues for Consideration

Estimating and Recovering Research Costs

Under the existing levy framework, SESSF fisheries research costs (RAGs, stock

assessment research, research administration) are attributed to Tier 2 (ITQ

component). Costs are summed and then apportioned to each sector according to a

previously agreed attribution formula (65% to trawl, 25% to GHAT, 10% to GAB).

More recently there has been a more defined approach for some research costs where

there is a flow of benefits contrary to this default option (e.g. recent Gulper Shark

research costs attributed primarily to SETF and GHAT Auto LL).

The default approach outlined above also makes it more difficult for AFMA to ensure

that any cost savings obtained from research efficiencies are passed to the

beneficiaries of those efficiencies and not diluted across the entire SESSF. For

example, the GABTF has moved to multiyear assessments for some species to reduce

their research costs whilst maintaining an acceptable level of confidence in

assessments. Under the existing framework these efficiencies are not clearly passed

on to the GABTF levy base. This can reduce the incentive for industry to work with

AFMA to identify productivity improvements.

There may also be other areas where fisheries like the GABTF are benefitting from

assessment work on shared species and not paying the appropriate share of those

costs. Western Gemfish assessment costs have been mentioned as an example.

AFMA has also identified an increasing requirement for RAGs to incorporate bycatch

and TEP related research, and work associated with broader EBFM related research

into their work programs. Some of this may be attributable to industry and some to

government in line with CRIS 2010. More detailed policy guidance about how to

apply the CRIS under these circumstances may be appropriate to ensure that costs are

attributed appropriately.

Accurate estimation and attribution of research costs back to species that are then

levied under the ITQ component is complicated by the lack of detailed cost

information per species. This may be addressed by RAGs compiling more accurate

estimates of time spent against SESSF species, and/or stock assessment projects

providing a more detailed breakdown of time/costs per species to assist accurate cost

attribution.

Research costs are a major part (25-30%) of recoverable costs in SESSF fisheries, and

are also a key area for consideration to develop cost efficiencies. They are a cost area

where a more detailed activity based costing approach may be beneficial. If more

accurate data about research costs per species was available, this could be included

directly into the Tier 2 levy-base calculation rather than estimated via the species cost

matrix using HSP tier levels.

Management costs for uncaught species, or those with very low catches

The proposed SESSF levy model uses catch of a quota species to derive the

management cost per SFR for recovery via the Tier 2 component of levy. Some

species, such as Orange Roughy, generate significant recoverable management costs

even though they are not actively fished, or are caught in very small quantities.

These species’ may be attributed with an amount of “catch” sufficient to recover an

appropriate management cost levy via the Tier 2 process - or alternatively have their

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 22

catch to SFR conversion rate adjusted such that each SFR collects an amount (when

summed across all SFRs for that species) that recovers an appropriate amount of Tier

2 levy.

Levy stability from year to year

AFMA’s licencing section is currently considering options to reduce variability in

levy payable per fishery/concession from year to year and outcomes from that process

may be suitable for adoption in the SESSF levy process. Unplanned variability

reduces the efficiency of AFMA’s licencing and levy processes, and increases time

spent handling related issues and concerns from industry.

Industry have also expressed concern that AFMA is not well positioned to adapt

promptly to a changing fishing business environment. For example, as fisheries

downsize, catches decline, or additional regulatory restrictions are introduced (e.g.

marine parks), AFMA’s costs may not reduce accordingly. Other concerns centre on

whether projected cost savings from new technology and systems at AFMA (e.g. e-

monitoring) were being realised. Some of these productivity initiatives are relatively

recent and will take time to accrue. AFMA has undertaken to provide evidence of

such savings as soon as it can.

Industry are also concerned that if permit/concession surrenders continue to occur at a

high rate this can dramatically increase levy payable by remaining concession holders.

A revised levy model with a clear and direct relationship to costs and attribution of

those can help however will not directly address this issue. Efforts to reduce

management costs commensurate with reductions in fleets and or catch and effort are

fundamentally important - noting that there will always be a baseline of recoverable

“fixed costs” associated with managing a Commonwealth fishery.

Given accurate cost estimation and attribution, and assuming that “the right work is

being done efficiently”, an emphasis on improved budget forecasting, and fiscal

management within a financial year should significantly reduce unplanned or

unexplained levy variation from year to year. If unplanned and high priority

additional work is generated, and the need to do the work is accepted (i.e. benefits of

doing the work exceed costs), then the work to be done and approximate costs should

be discussed and agreed via MAC consultation, and then carefully managed to

minimise levy impacts.

In light of challenging business circumstances, and concerns about AFMA’s cost

management, industry are opposed to paying an additional amount for budget

contingencies, or to contribute to a levy fund that can help to smooth out levy

variation from year to year. This approach is used in some other industry sectors,

such as AQIS import regulation cost recovery, however the scale of operations is

generally significantly larger than for most fishing businesses.

Linked permits and Boat SFRs

Currently several SESSF permits are linked to other concessions for fisheries

management and levy payment purposes. Accurately determining the historic basis

for these linked permits is outside the scope of this review. Nonetheless it is an

important issue and may require some additional research where the reasons for

linkages are not recorded and readily available within AFMA.

For the new levy model, permits and Boat SFRs should be levied according to the

recoverable costs they generate. Under the proposed model this is largely determined

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA

Page 23

by the amount of recoverable costs attributed to the Tier 1 or Boat SFR part of the

levy, and then an estimate of management time divided by the number of permits in a

sector. Where there are sound fisheries management or other regulatory reasons for

maintaining linked permits, such that they only pay one levy per concession

“package”, maintaining some linked permits may be appropriate.

This decision requires further consideration, including any prior agreements between

AFMA and other jurisdictions about whether or not to levy permits that are part of a

linked package. This should include consideration of GHAT coastal waters permits

for Tasmania and South Australia.

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA Appendix 1

Page 24

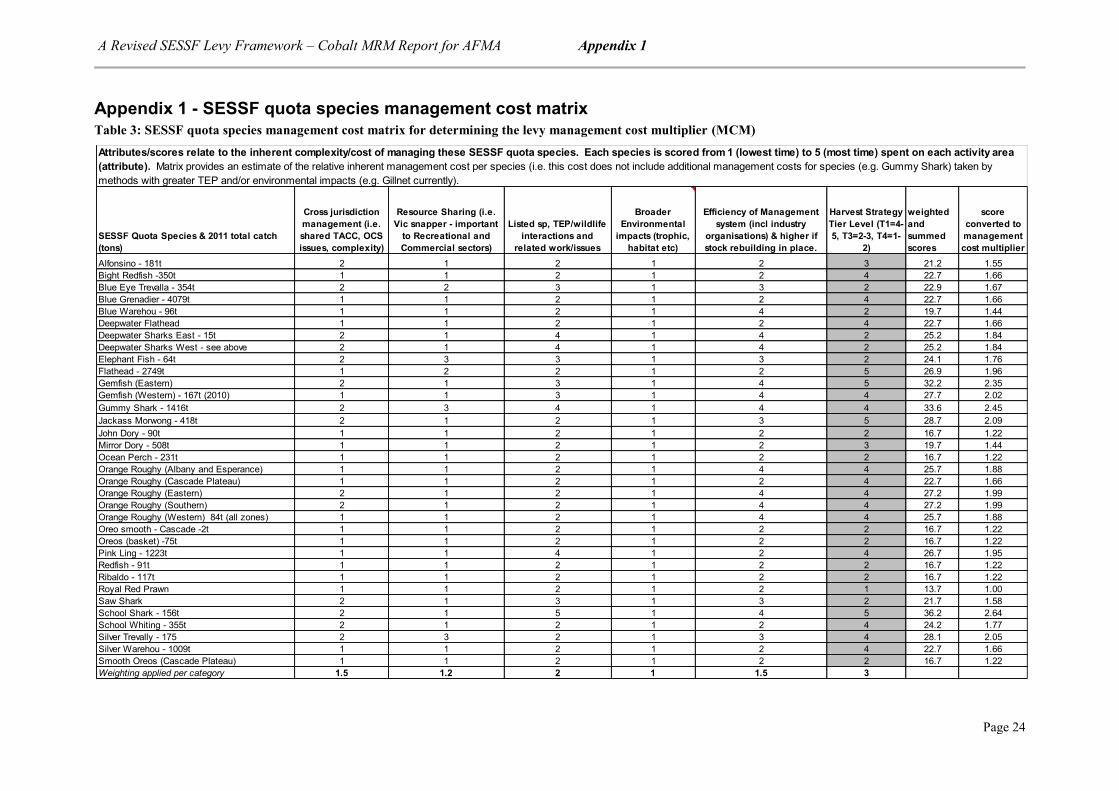

Appendix 1 - SESSF quota species management cost matrix Table 3: SESSF quota species management cost matrix for determining the levy management cost multiplier (MCM)

SESSF Quota Species & 2011 total catch

(tons)

Cross jurisdiction

management (i.e.

shared TACC, OCS

issues, complexity)

Resource Sharing (i.e.

Vic snapper - important

to Recreational and

Commercial sectors)

Listed sp, TEP/wildlife

interactions and

related work/issues

Broader

Environmental

impacts (trophic,

habitat etc)

Efficiency of Management

system (incl industry

organisations) & higher if

stock rebuilding in place.

Harvest Strategy

Tier Level (T1=4-

5, T3=2-3, T4=1-

2)

weighted

and

summed

scores

score

converted to

management

cost multiplier

Alfonsino - 181t 2 1 2 1 2 3 21.2 1.55

Bight Redfish -350t 1 1 2 1 2 4 22.7 1.66

Blue Eye Trevalla - 354t 2 2 3 1 3 2 22.9 1.67

Blue Grenadier - 4079t 1 1 2 1 2 4 22.7 1.66

Blue Warehou - 96t 1 1 2 1 4 2 19.7 1.44

Deepwater Flathead 1 1 2 1 2 4 22.7 1.66

Deepwater Sharks East - 15t 2 1 4 1 4 2 25.2 1.84

Deepwater Sharks West - see above 2 1 4 1 4 2 25.2 1.84

Elephant Fish - 64t 2 3 3 1 3 2 24.1 1.76

Flathead - 2749t 1 2 2 1 2 5 26.9 1.96

Gemfish (Eastern) 2 1 3 1 4 5 32.2 2.35

Gemfish (Western) - 167t (2010) 1 1 3 1 4 4 27.7 2.02

Gummy Shark - 1416t 2 3 4 1 4 4 33.6 2.45

Jackass Morwong - 418t 2 1 2 1 3 5 28.7 2.09

John Dory - 90t 1 1 2 1 2 2 16.7 1.22

Mirror Dory - 508t 1 1 2 1 2 3 19.7 1.44

Ocean Perch - 231t 1 1 2 1 2 2 16.7 1.22

Orange Roughy (Albany and Esperance) 1 1 2 1 4 4 25.7 1.88

Orange Roughy (Cascade Plateau) 1 1 2 1 2 4 22.7 1.66

Orange Roughy (Eastern) 2 1 2 1 4 4 27.2 1.99

Orange Roughy (Southern) 2 1 2 1 4 4 27.2 1.99

Orange Roughy (Western) 84t (all zones) 1 1 2 1 4 4 25.7 1.88

Oreo smooth - Cascade -2t 1 1 2 1 2 2 16.7 1.22

Oreos (basket) -75t 1 1 2 1 2 2 16.7 1.22

Pink Ling - 1223t 1 1 4 1 2 4 26.7 1.95

Redfish - 91t 1 1 2 1 2 2 16.7 1.22

Ribaldo - 117t 1 1 2 1 2 2 16.7 1.22

Royal Red Prawn 1 1 2 1 2 1 13.7 1.00

Saw Shark 2 1 3 1 3 2 21.7 1.58

School Shark - 156t 2 1 5 1 4 5 36.2 2.64

School Whiting - 355t 2 1 2 1 2 4 24.2 1.77

Silver Trevally - 175 2 3 2 1 3 4 28.1 2.05

Silver Warehou - 1009t 1 1 2 1 2 4 22.7 1.66

Smooth Oreos (Cascade Plateau) 1 1 2 1 2 2 16.7 1.22

Weighting applied per category 1.5 1.2 2 1 1.5 3

Attributes/scores relate to the inherent complexity/cost of managing these SESSF quota species. Each species is scored from 1 (lowest time) to 5 (most time) spent on each activity area

(attribute). Matrix provides an estimate of the relative inherent management cost per species (i.e. this cost does not include additional management costs for species (e.g. Gummy Shark) taken by

methods with greater TEP and/or environmental impacts (e.g. Gillnet currently).

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA Appendix 1

Page 25

Description of the Management Cost Matrix10

Cost Driver Relevance & Comments

1. Cross jurisdiction

management (i.e. shared

TACC, OCS issues,

complexity)

Category picks up time/cost generated by issues like shared TAC

discussions/negotiations, and OCS related discussions that

complicate management of a species and add cost. Includes

international/regional straddling stocks. Scoring should recognise

the relative impact of this driver on range of SESSF quota species

on which Tier 2 levy is payable. Scores are weighted by 1.5

(moderate)

2. Resource sharing Category picks up time/costs associated with management issues

related to resource sharing between commercial/recreational and/or

indigenous sectors. This is a relatively minor issue for SESSF

fisheries currently (excepting recent Vic/C’wealth Snapper issues)

and this category could be combined into 1. above if required.

Scores are weighted by 1.2 (low).

3. Listed Species and/or

TEP interactions &

related work/issues

Category picks up work/cost associated with TEP interactions

driven by fishing for the species in question. This can be a very

significant driver of management cost across a range of

management activities (i.e. data management costs as a result of

development of GIS based maps for spatial management of TEP

interactions). Scores are weighted by 2 (moderate-high).

4. Broader environmental

impacts (i.e. trophic

importance, habitat

impacts etc)

Category picks up work/cost associated with a species’ trophic

importance and perceptions/facts about how the ecosystem is

impacted by fishing, including broader habitat impacts and how

that fishing should be managed to meet AFMA’s EBFM

objectives. An example (non SESSF but related) could be the

substantial work initiated by stakeholder concerns about ecological

impacts of a large factory vessel trawling for small pelagic species

off Tasmania. Scores are weighted by 1 (low).

5. Harvest Strategy Tier Category picks up research costs (stock assessment projects,

research administration, and broader research projects). This is a

significant cost driver (25-30% of recoverable costs) and is

complicated by lack of detailed cost data per species. The matrix

is an attempt to cost effectively estimate and attribute these costs

based on data that is currently available (HSP tier levels) as a

proxy for true costs. Scores are weighted by 3 (high).

10

Categories and scores have been reviewed by SESSF staff for initial model development. They are a key driver for

Tier 2 levy attribution and should be critically reviewed prior to each new levy cycle.

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA Appendix 2

Page 26

Appendix 2 - Example of revised SESSF levy model and explanatory notes Table 4: copy of base model to determine Tier 2 levies for SESSF quota species

Quota species

2011 trawl

catch in kg

Management

cost multiplier

weighted

catch kg

$ per species

total

New $ per

SFR

$ SFR for

old model

2011

conversion

factor for

SFRs

% of total

trawl

catch kg

2011 attributed

trawl SFRs based

on CTS/GHAT

catch splits

2011 attributed

GHAT SFRs based

on CTS/GHAT

catch splits

2011 GHAT

catch SFRs

Total

allocated

SFRs

Trawl T2 $

collected

T2 $ collected

from "GHAT"

catch

Total $

collected

Alfonsino 179,881 1.55 278,356 $ 34,227.18 $ 0.05 $ - 0.996 2% 745,550 7,427 1,799 752,977 33,889.58$ 337.59$ 34,227.18$

Blue eye trevalla - 1.67 - $ - $ - $ 0.12 0.4131 0% 53,854 734,800 799,675 788,654 -$ -$ -$

Blue grenadier 4,047,809 1.66 6,706,954 $ 824,699.60 $ 0.17 $ 0.11 0.9081 36% 4,945,271 5,567 5,046 4,950,838 823,772.18$ 927.42$ 824,699.60$

Blue warehou 91,445 1.44 131,494 $ 16,168.74 $ 0.01 $ 0.03 0.0557 1% 2,279,774 105,081 76,333 2,384,855 15,456.31$ 712.42$ 16,168.74$

Deepwater shark basket east 69,783 1.84 128,360 $ 15,783.38 $ 0.07 $ - 0.3685 1% 207,512 9,569 8,732 217,081 15,087.63$ 695.75$ 15,783.38$

Deepwater shark basket west - 1.84 - $ - $ - $ - 0.5312 0% 259,750 - 259,750 -$ -$ -$

Elephant fish 28,010 1.76 49,273 $ 6,058.71 $ 0.07 $ 0.09 0.9634 0% 40,073 52,303 38,043 92,376 2,628.27$ 3,430.44$ 6,058.71$

Flathead 2,744,314 1.96 5,388,471 $ 662,576.45 $ 0.23 $ 0.17 0.9298 24% 2,939,432 791 794 2,940,223 662,398.24$ 178.21$ 662,576.45$

Gemfish east 127,577 2.35 299,853 $ 36,870.43 $ 0.19 $ 0.07 0.5028 1% 178,395 20,460 29,096 198,855 33,076.85$ 3,793.58$ 36,870.43$

Gemfish west (SET) - 2.02 - $ - $ - $ 0.05 0.3291 0% 285,607 - 285,607 -$ -$ -$

Gummy shark 2.45 - $ - $ - $ 0.27 0.7675 0% 246,202 1,990,241 1,642,332 2,236,443 -$ -$ -$

Jackass morwong 382,927 2.09 802,190 $ 98,638.80 $ 0.07 $ 0.05 0.3243 3% 1,359,743 6,017 5,673 1,365,760 98,204.25$ 434.55$ 98,638.80$

John dory 87,905 1.22 107,154 $ 13,175.89 $ 0.06 $ 0.17 1.075 1% 204,844 51 21 204,895 13,172.61$ 3.28$ 13,175.89$

Mirror dory 507,482 1.44 729,737 $ 89,729.82 $ 0.13 $ 0.08 1.0623 5% 673,190 20 14 673,210 89,727.19$ 2.63$ 89,729.82$

Ocean perch 192,365 1.22 234,489 $ 28,833.17 $ 0.10 $ 0.08 0.9969 2% 258,006 40,908 31,723 298,914 24,887.19$ 3,945.98$ 28,833.17$

Orange roughy cascade zone 84,557 1.66 140,105 $ 17,227.62 $ 0.01 $ 0.02 0.3318 1% 1,506,641 - 1,506,641 17,227.62$ -$ 17,227.62$

Orange roughy eastern zone - 1.99 - $ - $ - $ 0.00 0.0034 0% 725,451 - 7,254,511 -$ -$ -$

Orange roughy southern zone - 1.99 - $ - $ - $ 0.00 0.0047 0% 735,633 - 7,356,328 -$ -$ -$

Orange roughy western zone - 1.88 - $ - $ - $ 0.00 0.0413 0% 145,090 - 1,450,898 -$ -$ -$

Oreo basket, other 74,398 1.16 86,635 $ 10,652.74 $ 0.02 $ - 0.1993 1% 564,422 - 564,422 10,652.74$ -$ 10,652.74$

Oreo smooth cascade - 1.22 - $ - $ - $ - 0.4796 0% 312,758 - 312,758 -$ -$ -$

Oreo smooth other 1,631 1.22 1,988 $ 244.47 $ 0.00 $ - 0.3264 0% 137,834 - 137,834 244.47$ -$ 244.47$

Pink ling 749,650 1.95 1,460,997 $ 179,646.90 $ 0.20 $ 0.22 1.333 7% 554,152 340,688 349,212 894,840 111,250.76$ 68,396.14$ 179,646.90$

Redfish 91,582 1.22 111,636 $ 13,727.03 $ 0.03 $ 0.00 0.5676 1% 472,589 1,309 447 473,898 13,689.10$ 37.93$ 13,727.03$

Ribaldo 48,696 1.22 59,359 $ 7,298.94 $ 0.03 $ - 0.6481 0% 115,041 143,852 100,445 258,893 3,243.34$ 4,055.59$ 7,298.94$

Royal red prawn 128,247 1.00 128,247 $ 15,769.49 $ 0.04 $ 0.03 0.7929 1% 382,098 - 382,098 15,769.49$ -$ 15,769.49$

Sawshark 88,564 1.58 140,280 $ 17,249.12 $ 0.05 $ 0.15 0.6515 1% 182,725 164,154 143,109 346,879 9,086.32$ 8,162.80$ 17,249.12$

School shark 2.64 - $ - $ - $ 0.12 0.3791 0% 52,133 412,009 365,565 464,142 -$ -$ -$

School whiting 355,688 1.77 628,296 $ 77,256.40 $ 0.04 $ 0.02 0.3159 3% 2,024,991 - 2,024,991 77,256.40$ -$ 77,256.40$

Silver trevally 165,701 2.05 339,868 $ 41,790.87 $ 0.09 $ 0.04 1.162 1% 463,550 278 90 463,828 41,765.83$ 25.04$ 41,790.87$

Spotted (silver) warehou 1,008,508 1.66 1,671,032 $ 205,473.17 $ 0.21 $ 0.16 2.605 9% 981,671 132 52 981,803 205,445.58$ 27.58$ 205,473.17$

Total 11,256,720 19,624,773 2,413,098.90$ 100% 2,317,931.97$ 95,166.93$ 2,413,098.90$

Combined Trawl (excl GAB)

Tier 2 recoverable costs 2,413,098.90$

Notes: previous years trawl catch in kg is entered. This is multiplied by the per species management cost multiplier (from management cost matrix - sheet 1) to give a weighted

catch amount. The weighted catch for each species as a proportion of the sum of weighted catch for all species provides the share of total recoverable Tier 2 management costs

attributable to that species (this gives the total $ amount per species to be collected - Col E). This amount is then divided by the total number of SFRs allocated for the species

to provide the cents/SFR amount that is the basis for the T2 levy per species. The catch shares for trawl and GHAT respectively (sheet 4) are then used to determine the

amount of T2 levy per species collected for each budget (GHAT or Trawl). The balance of recoverable costs (those not collected via the tier 2 process) are then collected via the

Boat SFR or Permit levies applicable to each fishery/method (sheet 6).

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA Appendix 2

Page 27

Description of key components of the proposed SESSF Levy Model

Component Relevance & Comments

1. Trawl catch in

Kilograms

Derived from the best available catch data for the most recent

fishing season. These data are used to determine the management

cost per species, acknowledging that active catch in the fishery is

more relevant to determining management cost per species than

total number of SFRs allocated for a fishery (many of which may

be uncaught and have significantly less influence on management

costs than actual catch).

2. Management Cost

Multiplier (MCM)

Derived from the management cost matrix at Appendix 1. An

estimate of the inherent management cost of each species for levy

purposes.

3. Weighted catch in kg Derived from the catch in kg of a species multiplied by the MCM

estimated for that species.

4. $ per species total Derived by dividing the weighted catch in kg for a species by the

sum of all species’ weighted catch values; and then multiplying

this by the total recoverable Tier 2 cost for the combined SESSF

trawl fisheries (ECDWT, CVIT, CTS). This gives an amount ($)

to be recovered - representing the species specific proportion of

tier 2 costs for each quota species.

5. New $ per SFR Each SESSF quota species proportion of total recoverable T2 costs

is then divided by the total number of SFRs allocated for that

species to derive the cents per SFR value which is the basis of the

T2 levy payable for quota owners.

6. 2011 Conversion Factor

for SFRs

The conversion factor is the ratio of kg of catch to the number of

SFRs for that species. Derived from TAC and the number of SFRs

allocated for that species.

7. 2011 attributed

trawl/GHAT SFRs

based on catch splits

The most recent catches for all SESSF quota species are

proportioned to Trawl and GHAT fisheries respectively. This

catch proportion is then used to divide the total number of SFRs

into an assumed Trawl catch and GHAT catch to estimate the

amount of T2 levy collected against each of these fishery budgets.

8. T2 $ collected from

Trawl or GHAT catch

This is the $ amount assumed to be collected by attributing catch

to a sector to cover all of the SFRs on which levy must be

collected - as described above.

A Revised SESSF Levy Framework – Cobalt MRM Report for AFMA Appendix 3

Page 28

Appendix 3 - Summary of Project Consultation

Consultation to assist development of the revised SESSF levy model

Consultation type Description

Internal AFMA

consultation

This was used to scope and plan the project approach; prompt consideration

of key design principles for the revised levy model; and assist with

development and critique of options. An internal consultation document was

prepared and distributed to relevant sections within AFMA (primarily

Fisheries Branch and Service One/Licencing). Internal consultation also

served to raise AFMA awareness of the issues and risks associated with the

current approach, and staff understanding of key levy issues and cost

recovery principles.

SEMAC consultation A discussion paper canvassing issues, principles and options for the revised

levy model was prepared and circulated at the SEMAC meeting on 25 May

2012. A presentation and discussion session was also undertaken. SEMAC

expressed its general support for the principles, design criteria and

preliminary options covered at this meeting (several members were absent).

A record of the discussion is available from the SEMAC Chair’s Summary

for that meeting.

SEMAC Levy

Working Group

(LWG) consultation

The AFMA/Industry LWG was previously set up by AFMA to assist with

revision of the levy model. Membership was expanded slightly to

accommodate sectoral representatives that had shown strong interest and

made valuable contributions. In addition to one on one telephone

conversations with LWG members throughout the project, the contractor

facilitated a detailed discussion of the proposed approach at the LWG

meeting at Melbourne Airport on 11 July 2012 (Chaired by AFMA). Gerry

Geen - Seafish Tasmania, and Dale Sumner - LEFCOL gave their apologies.

Mike Rowley - Fortuna Fishing was unable to be contacted. Participants at

the Melbourne meeting were:

Brad Milic AFMA - A/g SESSF Senior Manager - Chair

Andrew Powell - AFMA Licencing Manager

Andy Bodsworth - Cobalt MRM - contractor

Simon Boag - SETFIA

Leigh Chambers - SA GHAT Fisher - Ex Scalefish Hook SFR Owner

Brian Bailey - Shark Fishing Industry Association

Robyn Gerrity - Tasmanian Scalefish Hook sector representative

Anthony Cicconte - quota owner and concession holder for various

GHAT concessions - primarily Gummy Shark

Les Scott - Petuna Sealord, quota owner and owner of various GHAT

and CTS concessions, including blue grenadier trawl and auto longline.

SESSF Concession

Holders

Broader consultation with SESSF concession holders that will be impacted

by the revised levy approach is recommended. This could be facilitated by

sending concession holders an abridged and updated version of the

discussion paper used for the 11 July LWG meeting.