a profile of the south african citrus market value chain...

TRANSCRIPT

A PROFILE OF THE SOUTH AFRICAN CITRUS MARKET VALUE CHAIN

2014

Directorate Marketing Private Bag X 15

ARCADIA 0007

Tel: 012 319 8455/6 Fax: 012 319 8131

Email: [email protected] www.daff.gov.za

2

TABLE OF CONTENTS

1. DESCRIPTION OF THE INDUSTRY ......................................................................................................... 4 1.1 Production areas .................................................................................................................... 5

1.2 Citrus cultivars .................................................................................................................... 13 1.3 Production ........................................................................................................................... 17 1.4 Employment ........................................................................................................................ 18

2. MARKET STRUCTURE .......................................................................................................................... 19 2.1 Orange crop distribution ..................................................................................................... 19

2.2 Orange prices ...................................................................................................................... 20 2.3 Soft citrus crop distribution ................................................................................................ 21

2.4 Soft citrus prices ................................................................................................................. 21 2.5 Grapefruit crop distribution ................................................................................................ 22 2.6 Grapefruit prices ................................................................................................................. 23 2.7 Lemons and limes crop distribution .................................................................................... 24

2.8 Lemon and lime prices ........................................................................................................ 24 2.9 Exports ................................................................................................................................ 25

2.9.1 Oranges ........................................................................................................................ 26

2.9.2 Lemons and limes ........................................................................................................ 31 2.9.3 Grapefruits ................................................................................................................... 36

2.9.4 Soft citrus ..................................................................................................................... 40

2.10 Provincial and district export values of South African citrus ........................................... 43

2.11 Share analysis.................................................................................................................... 50 2.12 Imports .............................................................................................................................. 54

2.12.1 Orange ........................................................................................................................ 54 2.12.2 Grapefruit ................................................................................................................... 54 2.12.3 Lemons and limes ...................................................................................................... 54

2.12.4 Soft citrus ................................................................................................................... 54 2.13 Processing ......................................................................................................................... 54

2.13.1 Orange ........................................................................................................................ 55 2.13.2 Lemon ........................................................................................................................ 56 2.13.3 Lime ........................................................................................................................... 56

2.13.4 Grapefruit ................................................................................................................... 56

3. MARKET INTELIGENCE ........................................................................................................................ 57 3.1 Competitiveness of South African citrus products ............................................................. 57

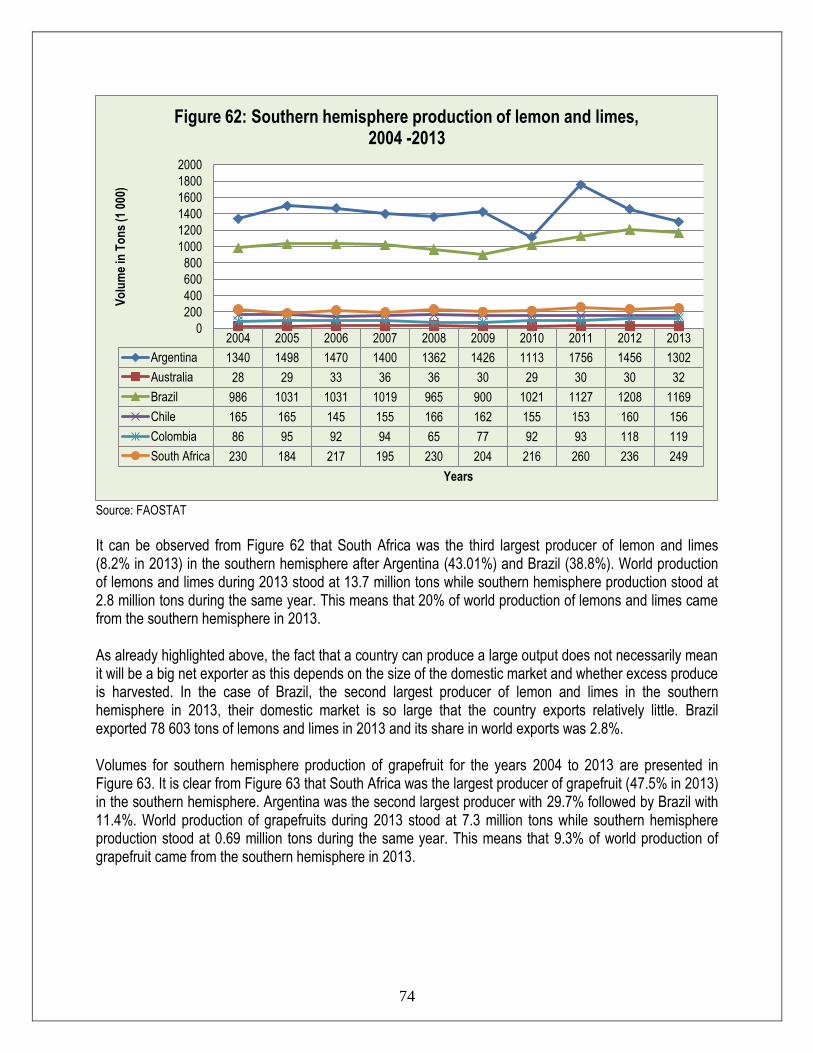

3.2 South Africa vs. southern hemisphere production .............................................................. 73

4. MARKET ACCESS ................................................................................................................................. 76 4.1 Tariff, quotas and the price entry system ............................................................................ 76 4.2 Non tariff barriers ............................................................................................................... 84

4.2.1 Quality standards ......................................................................................................... 84

4.2.2 Biosecurity ................................................................................................................... 85 4.2.3 Plant Protection Product (PPP) database ..................................................................... 85

4.3 European Union (EU) ......................................................................................................... 85

4.4 Consumer health and safety requirements .......................................................................... 85 4.5 Japan ................................................................................................................................... 87 4.6 United States of America .................................................................................................... 87

3

5. DISTRIBUTION CHANNELS .................................................................................................................. 88 6. LOGISTICS ............................................................................................................................................. 88

6.1 Mode of transport ................................................................................................................ 88 6.2 Cold chain management ...................................................................................................... 88

6.3 Packaging ............................................................................................................................ 89

7. MARKET VALUE CHAIN ........................................................................................................................ 89 7.1 Domestic and export markets.............................................................................................. 90 7.2 Processing industry ............................................................................................................. 91 7.3 Global retail chains ............................................................................................................. 91

7.4 Final consumer .................................................................................................................... 91

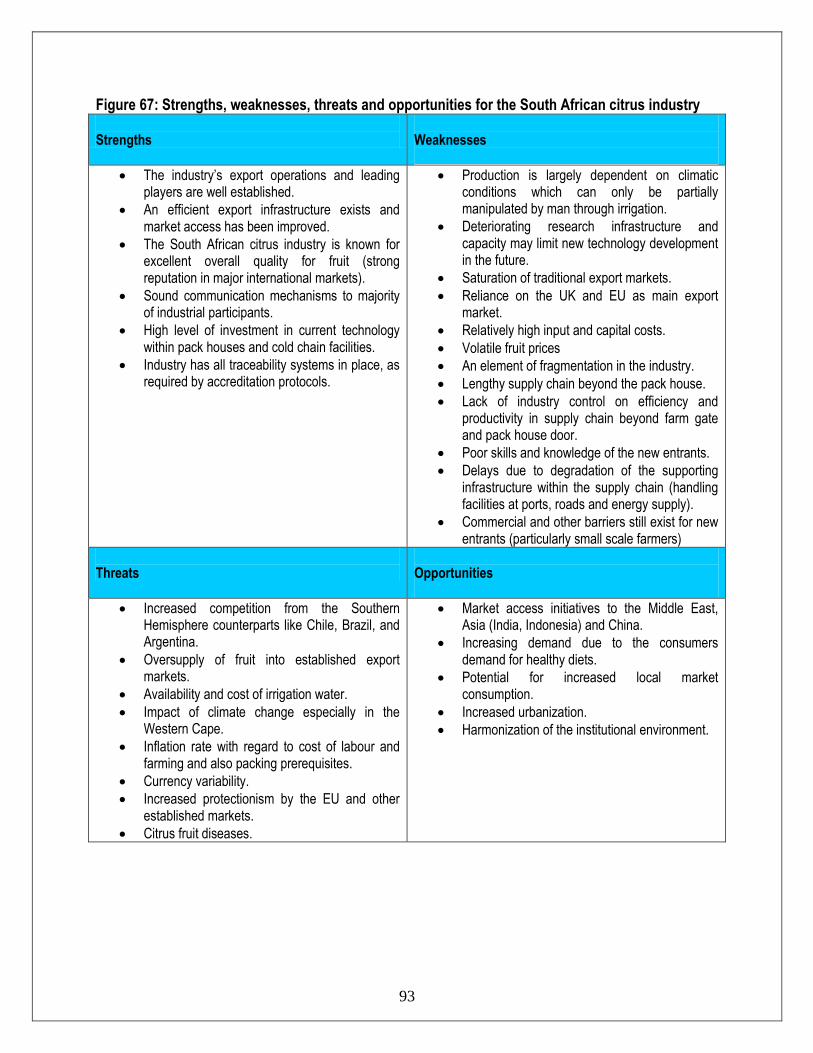

8. ORGANIZATIONAL ANALYSIS ............................................................................................................. 92 8.1 Producer and associated organizations ............................................................................... 92 8.2 Strengths, Weaknesses, Opportunities and Threat analysis ................................................ 92

9. EMPOWERMENT ISSUES AND TRANSFORMATION OF THE AGRICULTURE SECTOR ................. 94 9.1 Youth in citrus..................................................................................................................... 94

9.2 Mentorship .......................................................................................................................... 94 9.3 Extension............................................................................................................................. 94

10. BUSINESS OPPORTUNITIES AND CHALLENGES ............................................................................ 94 10.1 Business opportunities ...................................................................................................... 94 10.2 Challenges ......................................................................................................................... 95

11. ACKNOWLEDGEDMENTS ................................................................................................................... 95

4

1. DESCRIPTION OF THE INDUSTRY In terms of gross value, the citrus industry is the third largest horticultural industry after decidouos fruits and vegetables. During the 2012/13 production season the industry contributed R8.3 billion to total gross value of South African agricultural production. This represented 18% of the total gross value (R46.4 billion) of horticulture during the same period. The industry is also an important foreign exchange earner and comprises of four broad categories, namely oranges, easy peelers (soft citrus), grapefruit, and lemons and limes. Gross value of citrus production for the past decade is shown in Figure 1.

Source: Citrus Growers’ Association (CGA), 2013 and DAFF, 2013

As depicted on Figure 1 on average, the gross value of production (GVP) for citrus has been increasing over the past ten years. The industry experienced three successive good years starting from 2011 to 2013 . The increase was mainly due to amongst others increased exports and the weakening of the Rand against the major currencies of South Africa’s trading partners. However, there were exceptions in 2005 and 2009 seasons where there were decreases of 33% and 21% respectively. The primary cause of the decreases may have been due to less quantity of citrus exported, owing to floods, which affected the quality and the size of the crop. The total gross value of all citrus products increased by 6% between 2010 and 2011, 156% between 2002 and 2011 and by 19% between 2012 and 2013. The biggest contributor to total citrus gross value is oranges, which accounted for 70% in 2013. The other three categories of citrus products except naartjie accounted for more than R1 billion each during the same period. The total gross value is driven by among other things the volume of production, volume of exports, the exchange rate, international prices, etc.

1 000 000

2 000 000

3 000 000

4 000 000

5 000 000

6 000 000

7 000 000

8 000 000

2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14

Figure 1: Gross value of production for citrus products, 2004/05 - 2013/14

Orange Lemon and lime Grapefruit Naartjies Total gross value

5

1.1 Production areas Citrus represents one of South Africa’s most important fruit group by value and volume. Production occurs mainly in the Limpopo, Western Cape, Mpumalanga, Eastern Cape, KwaZulu-Natal and Northern Cape provinces (see Figure 2 and Map 1). Within the Southern African Development Community (SADC) region Zimbabwe, Swaziland and Mozambique also produce citrus, although in much smaller volumes. Swaziland had 1 142 ha of land under citrus cultivation in 2013. A total area of 64 202 ha was under citrus production in South Africa during 2013. There are important differences between production regions in South Africa based mainly on climate. The Western Cape and Eastern Cape are considered ‘cooler’ citrus growing areas and production is focused on Navel oranges and lemons. The cooler climate allows farmers to respond to consumer demand for easy peelers like clementines and satsumas, and most of the country’s easy peelers are produced in these two regions. Farm sizes are also smaller and most citrus in the Western and Eastern Cape is packed by privatized cooperatives in huge facilities that are amongst the largest in the world. In Mpumalanga, Limpopo and KwaZulu-Natal, the climate is warmer and better suited to the cultivation of grapefruit and Valencia oranges. Farm sizes in these regions are larger and many farmers pack in smaller privately owned facilities. The size in hectares and percentage contributions of the various citrus production regions to total citrus production during 2013 are depicted in Figure 2.

Source: Citrus Growers Association (CGA), 2013

Limpopo 37%

Eastern Cape 23%

Mpumalanga 15%

Western Cape 14%

KwaZulu-Natal 5%

Northern Cape 2%

Swaziland 2%

Other 2%

Figure 2: Citrus production areas in hectares, 2013

6

It is evident from Figure 2 that most citrus production takes place in the Limpopo province at 37% (23 970 ha). Limpopo is followed by the Eastern Cape and Mpumalanga at 23% (14 770 ha) and 15% (9 375 ha) respectively. The fourth largest producer of citrus products in terms of size in 2013 was the Western Cape province at 14% (9 232 ha). Kwazulu Natal contributed 5% (3 192 ha) during the same period while the Northern Cape accounted to 2% (1 451 ha). The major citrus production areas in Kwazulu Natal are Pongola, Nkwalini and Kwazulu Natal Midlands (see Map 1). In the Eastern Cape, the major citrus production areas are the Eastern Cape Midlands, Sundays River Valley and Patensie. The Boland region and Ceres region are the main citrus production areas in the Western Cape. Onderberg, Nelspruit and Senwes are the main citrus production areas in Mpumalanga while the major areas in Limpopo are Hoedspruit, Letsitele and Vhembe.

7

Map 1: Citrus producing regions of South Africa

Source: Citrus Growers Association (CGA), 2012

8

The area planted per citrus variety or group during 2013 is shown in Figure 3. It can be observed from Figure 3 that the most planted citrus variety in 2013 was Valencia at 41% (26 362 ha). Limpopo province contributed 56 percent of all Valencia oranges in planted in 2013. Another citrus variety planted the most in 2013 was Navel oranges (24% or 15 624 ha). The Eastern Cape province contributed 37 percent of all Navel oranges planted in 2013. The third largest planted citrus category was grapefruit at 15% (9 336 ha) of total area planted to citrus products in 2013. Soft citrus accounted for 10% (6 401 ha) while lemons and limes accounted for 9% (5 904 ha) during the same period.

Source: Citrus Growers Association (CGA), 2012

The production areas for Valencia oranges are shown in Figure 4. In 2013 most Valencia oranges were planted in the Limpopo province (56%) (14 398 ha). Limpopo was followed by the Eastern Cape province at 15 percent (3 797 ha) and Mpumalanga province at 14 percent (3 659 ha). Another important grower of Valencia oranges during 2013 was the Western Cape province which accounted for 8% of total area planted to Valencia oranges during the same year. The total hectares planted to Valencia oranges in 2013 was 26 362 ha. The 2013 figure was 4% higher than that of 2011.

Valencia 41%

Navel 24%

Grapefruit 15%

Soft Citrus 10%

Lemon 9%

Midseason 1%

Pummelo 0%

Figure 3: Area planted per variety (group) in hectares, 2014

9

Source: Citrus Growers Association (CGA), 2013

Figure 5 presents production areas for navel oranges during 2013. The Eastern Cape province is the leading grower of navel oranges at 37 percent (5 791 ha). Second is Western Cape province at 25 percent (3 848 ha), followed by the Limpopo at 20 percent (3 110 ha) and Mpumalanga at 12 percent (1 817 ha). The total hectares planted to navel oranges in 2013 was 15 624 ha. The total area planted to navel oranges during 2013 was 5% lower than the area planted in 2011.

Limpopo 56%

Eastern Cape 15%

Mpumalanga 14%

Western Cape 8%

KwaZulu-Natal 3%

Swaziland 2%

Northern Cape 2%

Figure 4: Production areas of valencias in hectares, 2014

10

Source: Citrus Growers Association (CGA), 2013

Figure 6 presents production areas for soft citrus in 2013. The Western Cape province is the leading grower of soft citrus at 39 percent (2 560 ha). It is followed by the Eastern Cape province at 34 percent (2 176 ha) and Limpopo province at 12 percent (768 ha). The total hectares planted to soft citrus in 2013 was 6 465 ha. This was 24 percent higher than the area planted in 2011.

Eastern Cape 37%

Western Cape 25%

Limpopo 20%

Mpumalanga 12%

KwaZulu-Natal 3%

Northern Cape 3%

Other 84 0%

Figure 5: Production areas of navels in hectares, 2014

11

Source: Citrus Growers Association (CGA), 2013

Figure 7 presents production areas for grapefruit in 2013.

Eastern Cape 34%

Western Cape 39%

Limpopo 12%

Mpumalanga 10%

Northern Cape 3%

Other 2%

Grand Total 0%

Figure 6: Production areas of soft citrus in hectares, 2014

12

Source: Citrus Growers Association (CGA), 2013

The Limpopo province is the leading grower of grapefruit at 44 percent (4 127 ha). It is followed by the Mpumalanga province at 27 percent (2 531ha) and Kwazulu-Natal province at 15 percent (1 451 ha) and Swaziland at percent (540 ha). The total hectares planted to grapefruit in 2013 was 9 336 ha. This was 1 percent less than the total area planted to grapefruit in 2011. Production areas for lemons and limes during 2013 are presented in Figure 8. The Eastern Cape province is the leading grower of lemons and limes at 46 percent (2 726 ha). It is followed by the Limpopo and Western Cape at 24% (1 397ha) and 11%(636 ha) respectively. The Mpumalanga province is also a significant producer of lemons and limes, accounting for 10% (572 ha) during 2013. The total hectares planted to lemons and limes in South Africa during 2013 was 5 904 ha and this was 51 percent higher than the area planted in 2013.

Limpopo 44%

Mpumalanga 27%

KwaZulu-Natal 15%

Swaziland 6%

Northern Cape 4%

Eastern Cape 3%

Other 63 1%

Figure 7: Production areas of grapefruit in hectares, 2014

13

Source: Citrus Growers Association (CGA), 2013

1.2 Citrus cultivars A number of cultivars or varieties of oranges, soft citrus, grapefruit, and lemons and limes are grown in South Africa. The varieties of Valencia oranges planted in South Africa during 2013 are presented in Figure 9. The cultivars planted mostly in South Africa are Delta (27% or 7 013 ha), Midnight (25% or 6 549 ha), Valencia (11% or 2 972 ha), and Turkey (Juvalle) (10% or 2 617 ha). Together, the four cultivars accounted for 73% of total Valencia oranges planted during 2013. The total area planted to Valencia oranges in South Africa during 2013 was 26 362 ha. The area planted was 4 percent higher than that planted in 2013.

Eastern Cape 2 726 46%

Limpopo 1 397 24%

Western Cape 636 11%

Mpumalanga 572 10%

KwaZulu-Natal 377 6%

Northern Cape 120 2%

Other 76 1%

Figure 8: Production areas of lemon and lime in hectares, 2014

14

Source: Citrus Growers Association (CGA), 2013

The cultivars of navel oranges cultivated in South Africa during 2013 are illustrated in Figure 10.

Source: Citrus Growers Association (CGA), 2012

Delta 7 013 27%

Midknight 6 549 25%

Valencia* 2 972 11%

Turkey (Juvalle) 2 617 10%

Oukloon (Olinda, Late) 1 844 7%

Du Roi 1 686 6%

Benny 1 576 6% Other 2

105 8%

Figure 9: Valencia(Oranges) cultivars planted in 2014(ha)

Palmer 4 144 26%

Bahianinha 2 195 14%

Navel* 1 950 12%

Washington 1 685 11%

Robyn 1 020 7%

Other 1 231 30%

Figure 10: Navel (oranges) cultivars planted in 2014 (ha)

15

The major cultivar of navel oranges planted in South Africa is Palmer, with 4 144 ha of land planted to it in 2013. This represented 26% of total area planted to navel oranges in 2013. Palmer is followed by Bahianinha at 14% (2 195 ha), Navel at 12% (1 950 ha) and Washington at 11% (1 685 ha). Other cultivars accounted for 30% (4 630 ha) of total area planted to navel oranges in 2013. The total area planted to Navel oranges during 2013 was 15 624 ha. Figure 11 presents cultivars of soft citrus planted in South Africa during 2013. The major soft citrus cultivar planted in South Africa during 2013 was Mandarin, representing 55% (3 519 ha) of total soft citrus cultivars planted in 2013. It was followed by Clementine at 29% (1 850 ha) and Satsuma at 16% (1 032 ha). A total area of 6 401 ha was planted to soft citrus in 2013.

Source: Citrus Growers Association (CGA), 2013

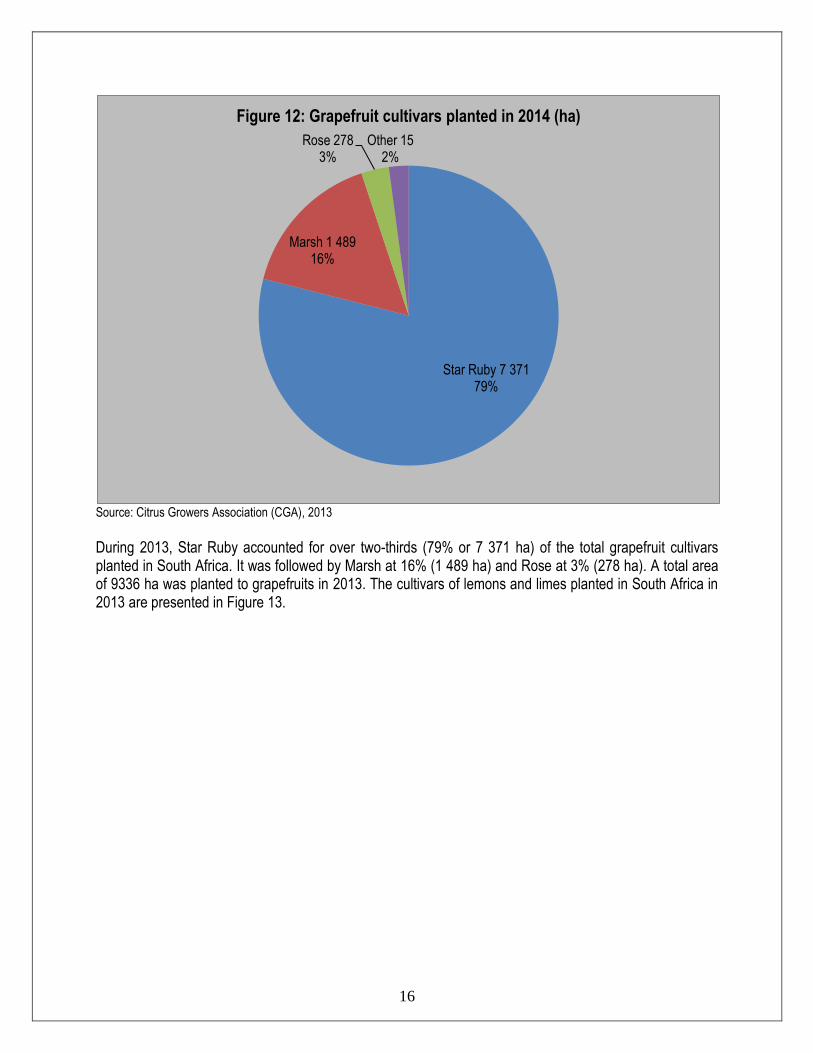

The cultivars of grapefruits cultivated in South Africa during 2013 are presented in Figure 12.

Clementine 29%

Mandarin 55%

Satsuma 16%

Figure 11: Soft citrus cultivars planted in 2014 (ha)

16

Source: Citrus Growers Association (CGA), 2013

During 2013, Star Ruby accounted for over two-thirds (79% or 7 371 ha) of the total grapefruit cultivars planted in South Africa. It was followed by Marsh at 16% (1 489 ha) and Rose at 3% (278 ha). A total area of 9336 ha was planted to grapefruits in 2013. The cultivars of lemons and limes planted in South Africa in 2013 are presented in Figure 13.

Star Ruby 7 371 79%

Marsh 1 489 16%

Rose 278 3%

Other 15 2%

Figure 12: Grapefruit cultivars planted in 2014 (ha)

17

Source: Citrus Growers Association (CGA), 2013

The most important cultivar of lemons and limes planted in South Africa is Eureka. Figure 13 indicates that Eureka was planted on a total area of 3 810 hectares, representing 65% of the total area planted to lemons and limes in 2013. Eureka was followed by Lemon at15% (904 ha) and Eureka SL at 7% (409 ha). A total area of 5904ha was planted to lemons and limes in 2013. 1.3 Production Citrus production has over the past ten years has been fairly stable (see Figure 14). In 2013 oranges contributed 72 percent of total citrus production. It was followed by grapefruit at %, lemons and limes at 9% and soft citrus at 1%.

Eureka 3 810 65%

Lemon 904 15%

Eureka SL 409

7%

Lisbon 309 5%

Limoneira 209 4%

Genoa 197 3%

Other 66 1%

Figure 13: Lemon and Lime cultivars planted in 2014 (ha)

18

Source: Statistics and Economic Analysis, DAFF

According to Figure 14, orange production has been on the increase since the 2005 production season. The increase has been mainly due to good climatic conditions in leading production areas. Production of oranges however experienced a 10% decline in 2009 when compared with 2008 and increased again to just over 1.4 million tons in 2010. Orange production declined again by 2% when compared to the previous production season (2010) but remained above the 1.4 million tons mark. The volume of lemons and limes increased by 19% in 2011 when compared to 2010 while production of grapefruits also increased by 18%. The production of soft citrus declined by 4% during the same period. 1.4 Employment The citrus industry is labour intensive and it is estimated that it employs more than 100 000 people, with large numbers of workers in the orchards and packing houses. An unspecified number of people are employed throughout the supply chain services such as transport, port handing and allied services. It is estimated that more than a million households depend on the South African citrus industry for their livelihood. The prescribed minimum wage is used as a baseline for determining basic wages in accordance with the legislation governing conditions of service. Minimum wages for farm workers for the period 1 March 2014 to 1 February 2017 are presented in Table 1. The consumer price index (CPI) is used in the calculation of annual wage adjustments. The sectoral determination stipulates that the wage increase will be determined by utilizing the previous year’s minimum wage plus CPI + 1.5%. Table 1: Minimum wages for farm workers in the Republic of South Africa, 2014 - 17 Minimum rate for the period Minimum rate for the period Minimum rate for the period

-

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 400 000

1 600 000

1 800 000

2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14

Vo

lum

e in

To

ns

Years

Figure 14: Total production of citrus products, 2004 - 2013

Orange Lemon and lime Grapefruit Naartjies

19

1 March 2014 to 28 February 2015 1 March 2015 to 28 February 2016

1 March 2016 to 28 February 2017

Monthly Weekly Daily Hourly Monthly Weekly Hourly Monthly Weekly Hourly

R2420.41 R525.00 111.691 R12.41 Previous year’s minimum wage + CPI2 + 1.5%

Previous year’s minimum wage + CPI + 1.5%

Source: Department of Labour 2. MARKET STRUCTURE Citrus production in South Africa is mainly aimed at the export market. Locally, citrus produce is sold though different marketing channels such as National Fresh Produce Markets (NFPMs), informal markets (street hawkers and bakkie traders), and directly to processors for juice making and dried fruit production. The fruits are also sold directly to wholesalers and retailers through direct supply contracts. The annual crop distribution and prices of the different citrus products are presented below. 2.1 Orange crop distribution The annual distribution of oranges to the different markets is presented in Figure 15. In 2013, 68% ( 1 109 709 tons) of all oranges produced ( 1 632 917 tons) was exported. This indicates the importance of export markets to South Africa’s production of oranges. The second most important market for South African oranges is the processing sector. The sector absorbed 20% ( 322 664 tons) of total orange production in 2013 while the remaining 12% ( 127 674 tons) was sold through the local markets. The total volume of oranges that were exported and processed during 2013 were both 7% higher than that processed and exported in 2012 while the volumes sold through the local markets and those sent to the processing sector increased by 0.74% during the same period.

1 For an employee who works 9 hours per day

2 The CPI to be utilised is the available CPI for the lowest quintile as released by Statistics South Africa six weeks prior to the increment date.

20

Source: Citrus Growers Association (CGA), 2013

2.2 Orange prices Figure 16 presents historical price trends of oranges during the past decade.

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Vo

lum

e in

To

ns

Years

Figure 15: Orange crop distribution, 2013

Local sales (ton) Exports (ton) Processed (ton)

0

1 000

2 000

3 000

4 000

5 000

6 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Ave

rag

e p

rice

s (R

and

/To

n

Years

Figure 16: Historical price trends for oranges, 2004 -2013

Local sales (ton) Exports (ton) Processed (ton)

21

Source: Citrus Growers Association (CGA), 2012

As can be seen in Figure 16 oranges fetch higher returns in the export markets. The average price per ton in the export markets during 2013 was R4 952.00. This was 792% higher than the average export price during the previous year. The average prices of oranges deopped drastically between 2012 and 2013 due to sanctions of South African citrus production to European Markets. Oranges sold in the local markets in 2013 fetched an average price of R2 077.00 per ton while those absorbed by the processing sector fetched the lowest price at R589.00 per ton. 2.3 Soft citrus crop distribution The annual soft citrus crop distribution for the past ten years is presented in Figure 17. The majority of the South African annual soft citrus crop is absorbed by the export market. A total volume of 126 633 tons of soft citrus was exported in 2013. This represented 87% of the total production ( 146270 tons) of soft citrus in 2013. The local market is the second most important market for soft citrus in South Africa, absorbing approximately 7% ( 10 135 tons) of the total crop in 2013.

Source: Citrus Growers Association (CGA), 2013

2.4 Soft citrus prices Historical price trends for soft citrus for the past ten years are presented in Figure 18.

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Vo

lum

e in

To

ns

Years

Figure 17: Soft citrus crop dustribution, 2004 - 2013

Local sales (ton) Exports (ton) Processed (ton)

22

Source: Citrus Growers Association (CGA), 2013

As in the case of oranges, soft citrus fetch the highest returns in the export markets. The average price received by a South African exporter in the export markets in 2013 was R 8 531.00 per ton. Soft citrus also fetch higher prices in the local markets. The average price received in the local markets during 2013 was R 4 366.00 per ton. It is important to note that prices of soft citrus in both the exports and processing markets recorded no significant growth between 2012 and 2013. 2.5 Grapefruit crop distribution Figure 19 presents the annual distribution of grapefruit in South Africa during the period 2004 to 2013. The leading market for South Africa’s grapefruits is the export market. Approximately 58% ( 252 930 tons) of the total grapefruits produced in South Africa during 2013 ( 434 070 tons) was exported. Another important market for grapefruits in South Africa is the processing sector. The sector absorbed 40% ( 175 221 tons) of the total crop in 2013. A very minimal amount of grapefruit is sold through the locally markets annually.

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Ave

rag

e p

rice

(R

/T)

Years

Figure 18: Historical price trends for soft citrus

Local sales (ton) Exports (ton) Processed (ton)

23

Source: Citrus Growers Association (CGA), 2013

2.6 Grapefruit prices Figure 20 illustrates historical price trends for grapefruits during the past ten years.

Source: Citrus Growers Association (CGA), 2013

0

50 000

100 000

150 000

200 000

250 000

300 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Vo

lum

e in

To

ns

Years

Figure 19: Grapefruit crop distribution, 2004 - 2014

Local sales (ton) Exports (ton) Processed (ton)

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Ave

rag

e p

rice

s (R

/T)

Years

Figure 20: Historical price trends for grapefruit, 2004 - 2013

Local sales (ton) Exports (ton) Processed (ton)

24

The net realisation in the export market has been highly volatile during the past decade, reaching a high of R3 723.00 per ton in 2011 and a low of R925.00 per ton in 2005. The average price realised in the export market during 2013 was R 3 405.00 per ton while those in the local and processing markets were R2 352/ton and R374.00/ton respectively. In 2005, it was more profitable to sell grapefruits in the local markets than in the export market as prices realised in the local markets were higher than those realised in the export markets. Between 2012 and 2013, prices realised in the local and export markets increased while those realised in the processing market declined. 2.7 Lemons and limes crop distribution The annual distribution of lemons and limes for the period 2004 to 2013 is presented in Figure 21.

Source: Citrus Growers Association (CGA), 2013

Over 159 thousand tons of lemons and limes were exported in 2013. This represented 77% of the total production of lemons and limes in 2013. The second most important market for South African lemons and limes is the processing industry. 16% ( 31 911 tons) of the total annual crop was sent to the processing industry in 2013 while the remaining 7% was sold in the local markets. The quantities of lemons and limes sent to the export markets have been increasing throughout the last decade while volumes sent to the processing and local markets have been stagnant. 2.8 Lemon and lime prices Historical prices of lemons and limes for the past decade are presented in Figure 22. Prices realised in the export markets fluctuated strongly during the last ten years and the biggest fluctuation was experienced

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

160 000

180 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Vo

lum

e in

To

ns

Years

Figure 21: Lemon and Lime crop distribution, 2004 - 2013

Local sales (ton) Exports (ton) Processed (ton)

25

between 2009 and 2010 when prices moved from just over R2 000.00 per ton in 2009 to over R5 000.00 per ton in 2010. The average price realised in the export markets during 2013 was R 6 994.00 per ton. Prices realised in the local markets increased steadily during the past decade, reaching a high of R 5 668.00 per ton in 2013. Prices realised in the processing sector also decreased from R982.00/ton in 2009 to R596.00/ton in 2013. Prices realised in both the export and local markets increased between 2012 and 2013 while those realised in the processing markets decreased during the same period.

Source: Citrus Growers Association (CGA), 2013

2.9 Exports As already indicated in the preceding subsections, citrus production in South Africa is mainly aimed at the export market. South Africa exported a total combined volume of 1 700 297 tons of citrus products in 2013. The volume exported was 9% higher than the volume exported in the previous year (2012). Annual citrus produce exported by South Africa to the world from 2004 to 2013 are depicted in Figure 23.

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Ave

rag

e p

rice

s (R

/T)

Years

Figure 22: Historical price trends for lemon and lime, 2004 -2013

Local sales (ton) Exports (ton) Processed (ton)

26

Source: Quantec Easydata

As can be seen in Figure 23, the biggest contributor to the total volume of South African citrus exports is oranges that contributed 68% ( 1 150 496 tons) to total citrus products exports in2013. Oranges were followed by grapefruit at 14% ( 241 797tons) and lemons and limes and soft citrus at 10% and 8% respectively during the same year. Volumes of citrus products sold to export, local and processing markets between 2004 and 2013 increased during the same period. 2.9.1 Oranges Exports of South African oranges to the various regions of the world over the past decade are presented in Figure 24. Oranges totalling 1150496 tons and worth R6.4 billion were exported by South Africa in 2013. During the last decade most of South Africa’s exports of oranges went to the European and Asian markets. In 2013 exports to Europe accounted for 53% of total South African orange exports while those to Asia accounted for 36%. South African exports of oranges to Europe have been relatively stable over the past decade, remaining over 400 thousand tons annually. Exports to Asia overtook those to Europe in 2005 (693 770 tons to Asia compared with 530 568 tons to Europe) and 2006 (532 031 tons to Asia compared with 511 396 tons to Europe) before retreating again in 2007. Exports to Europe increased again in 2013 after a decline in 2012. The Americas and Africa also constitute important markets for South African exports of oranges.

0

200000

400000

600000

800000

1000000

1200000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Vo

lum

e in

To

ns

Years

Figure 23: Volumes of citrus product exports, 2002 - 2011

Orange Lemon and Lime Grapefruit Soft citrus

27

Source: Quantec Easydata

Due to their relative importance to exports of South African oranges, the European and Asian markets are further analysed below. Volumes of South African orange exports to the various regions of Europe from 2004 to 2013 are presented in Figure 25. In Europe, the bulk of South African exports of oranges go to the European Union. 76% of all South African exports of oranges to Europe in 2013 were absorbed by the European Union. The EU was followed by Eastern Europe at 23% while the remaining 1% went to Northern, Southern and Western Europe. Exports to Europe peaked at 606 403 tons in 2007. The exports of South African oranges to the European Union and Eastern Europe increased by 9% and 5% respectively between 2012 and 2013. Exports to Europe as a whole also increased by 8% between 2012 and 2013.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

World 717459 1376514 1171068 1015242 1077205 1033960 1109127 1113268 1088802 1150496

Africa 57530 8224 47846 63541 60108 49841 66523 30735 47818 51589

Americas 51941 143753 79355 53596 64319 73395 61901 69699 72733 75876

Asia 167750 693770 532031 288300 368809 393219 382714 367317 405470 413921

Europe 440162 530568 511396 606403 583723 516792 597622 508482 562306 609052

Oceania 59 24 274 189 50 434 168 25 465 6

Not allocated 16 176 166 3212 196 279 199 9 10 52

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

Vo

lum

e in

To

ns

Years

Figure 24: Volumes of orange exports exported to various regions in the world, 2004 - 2013

28

Source: Quantec Easydata

Due to its significance to South African exports of oranges the European Union market is further disaggregated in Figure 26. It is important to note that only those countries whose orange imports from South Africa were at least 10 000 tons in at least one year during the period under review are shown in Figure 26. The major importers of South African oranges in the European Union are the Netherlands, the United Kingdom and Italy. In 2013, the three countries accounted for 74% of all South African orange exports to the European Union ( 464 429 tons), with the Netherlands accounting for 48% and the United Kingdom and Italy contributing 18% and 8% respectively. Between 2012 and 2013, exports to the Netherlands increased by 11% while those to Italy and the United Kingdom also went down by 15% and 23% respectively.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Europe 440162 530568 511396 606403 583723 516792 597622 508918 562920 610030

Eastern Europe 89422 72064 112438 147350 114949 110623 154967 137811 132764 138913

Northern Europe 746 2085 963 813 1048 5272 2366 2246 1990 2174

Southern Europe 918 0 43 142 398 646 2226 315 2227 2278

Western Europe 1499 5932 708 655 214 2971 463 621 277 2237

European Union 347578 450487 397244 457443 467115 397281 437600 367925 425662 464429

0

100000

200000

300000

400000

500000

600000

700000

Vo

lum

e in

To

ns

Years

Figure 25: Volumes of oranges exported to different regions of Europe, 2004 - 2013

29

Source: Quantec Easydata

Volumes of South African exports of oranges to the different regions of Asia are presented in Figure 27. The most important Asian region in terms of South African exports of oranges is Western Asia. In 2013, exports to Western Asia accounted for 66% of total South African exports of oranges to Asia. Total South African exports of oranges to Asia peaked at 693 770 tons in 2005 and have declined sharply during 2006 and 2007 before picking up again in 2008. There was a 2% increase in total exports to Asia between 2012 and 2013.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

European Union 347578 450487 397244 457443 467115 397281 437600 367925 425662 464429

Belgium 31914 34658 26407 50746 32167 33626 5481 4786 3860 2660

Germany 9521 10037 5364 7849 10988 11167 12826 10022 10745 9046

Spain 60651 62151 45915 71103 57931 32412 19482 15773 23019 18604

France 11530 13840 10731 7699 7533 8875 25479 16144 23163 25832

United Kingdom 62444 85082 70459 78696 82856 71441 69711 66869 65964 81512

Greece 13417 3170 6052 16867 8678 4687 4091 2591 1775 1856

Italy 29894 62547 45577 35887 35501 60911 41856 29510 31960 36784

Netherlands 121443 165874 161345 155569 189823 151982 197813 175039 201186 223588

Portugal 842 978 2801 6581 10072 5602 40252 29566 42821 41269

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

Vo

lum

es i

n T

on

s

Years

Figure 26: Volumes of oranges exported to various European Union member states, 2004 -2013

30

Source: Quantec Easydata

Volumes of South African orange exports to the different countries in Western Asia during the last decade are presented in Figure 28.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Asia 167750 693770 532031 288300 368809 393219 382714 367436 405839 414093

Eastern Asia 58392 158594 167236 67261 55516 60799 60407 72343 66871 55068

South-central Asia 1116 360221 42468 17938 17272 72930 39373 44998 43326 39901

South-eastern Asia 18403 36345 41394 38980 27532 35538 33483 32176 43320 45888

Western Asia 89840 138610 280933 164120 268489 223952 249451 217918 252322 273236

0

100000

200000

300000

400000

500000

600000

700000

800000

Vo

lum

e in

To

ns

Years

Figure 27: Volumes of oranges exported to various regions in Asia, 2004 - 2013

31

Source: Quantec Easydata

Note that only those countries whose orange imports from South Africa were at least 100 tons in at least one year during the period under review are shown in Figure 28. The major importers of South African oranges in Western Asia are the United Arab Emirates and Saudi Arabia. In 2013 the United Arab Emirates imported 106 782 tons of oranges from South Africa while Saudi Arabia imported 92 882 tons from South Africa. Between 2012 and 2013, South African exports of oranges to Saudi Arabia declined by 8% while those to the United Arab Emirates increased by 13%. 2.9.2 Lemons and limes Exports of South African lemons and limes to the various regions of the world over the past decade are presented in Figure 29. Lemons and limes totalling 175 085 tons were exported by South Africa in 2013. Between 2009 and 2010 the total volume of lemons and limes exported by South Africa increased by 62%. The total volume of exports however recorded an increase of 5% between 2012 and 2013. During the last decade most of South Africa’s exports of lemons and limes went mainly to the European and Asian markets. In 2013 exports to Asia accounted for 52% of total South African lemons and limes exports while those to Europe accounted for 42%. It can be observed in Figure 29 that total South African exports of lemons and limes are predominantly determined by quantities absorbed by the Asian market. Total South African exports of lemons and limes to the world peaked in 2009 at 396 945 tons while those to Asia

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Western Asia 89840 138610 280933 164120 268489 223952 249451 217918 252322 273236

United Arab Emirates 30194 70336 85123 69868 79849 100743 104064 78659 93912 106782

Bahrain 1778 7160 13028 2829 5193 3722 3543 3884 5888 5211

Israel 107 0 0 293 1247 0 0 0 0 27

Jordan 146 13 726 24 579 619 193 442 50 0

Kuwait 2874 2402 43112 7388 26292 23541 35366 30323 32969 50628

Oman 6665 2881 7708 7811 11973 19238 13936 9126 12402 11158

Qatar 1131 10445 1374 2764 4000 3753 2771 4686 5101 5715

Saudi Arabia 46305 45374 129718 72482 138308 72204 88746 89456 101267 92882

0

50000

100000

150000

200000

250000

300000

Vo

lum

e in

To

ns

Years

Figure 28: Volumes of oranges exports to different countries in Western Asia, 2004 -2013

32

peaked at 287 644 tons during the same year. Africa and the Americas also constitute important markets for South African lemons and limes.

Source: Quantec Easydata

Figure 30 presents volumes of lemons and limes exported to various regions of Europe during the last ten years. Europe absorbed a total volume of 73 701 tons of lemons and limes from South Africa in 2013. The volume was 3% up from the 71 418 tons imported from South Africa during 2012. Within Europe, the major markets for South African lemons and limes are the European Union and Eastern Europe. The European Union absorbed 51% of total South African exports of lemons and limes to the European continent in 2013.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

World 115301 339195 143870 121999 165657 396945 150606 165217 165827 175085

Africa 2489 2043 1990 2129 1883 13979 2451 2695 3597 3526

Americas 601 671 629 2138 2216 637 1697 2809 2623 6682

Asia 58007 257843 81059 78951 75789 287644 70248 77671 88183 91170

Europe 54096 78572 57555 38575 85711 94520 76051 82038 71418 73701

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

Vo

lum

e in

To

ns

Years

Figure 29: Volumes of lemons and lime exported to the various regions of the world, 2004 - 2013

33

Source: Quantec Easydata

Due to its significance to exports of South African lemons and limes, the European Union market is further disaggregated in Figure 31. Within the European Union, the major importers of South African lemons and limes are the Netherlands and the United Kingdom. Together the two countries accounted for 70% of total European Union imports of lemons and limes from South Africa in 2013, with the Netherlands accounting for 42% and the United Kingdom accounting for 27%.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Europe 54096 78572 57555 38575 85711 94520 76051 82038 71418 73701

Eastern Europe 7582 6337 6539 4292 10195 29303 24879 30814 22067 33467

Northern Europe 23 46 40 0 26 75 162 185 176 170

Southern Europe 148 0 58 1956 1587 3777 412 403 1566 2201

Western Europe 336 165 219 9 215 148 167 549 92 0

European Union 46007 72023 50699 32319 73689 61218 50430 50087 47517 37863

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

Vo

lum

e in

To

ns

Years

Figure 30: Volumes of lemon and lime exported to various European regions

34

Source: Quantec Easydata

Volumes of lemons and limes exported by South Africa to the various regions of Asia are presented in Figure 32. It is evident that the majority of South African exports of lemons and limes that went to Asia during the last decade were destined for Western Asia. Approximately 79% of all South African exports of lemons and limes to Asia in 2013 were absorbed by Western Asia. The remainder went to Eastern Asia (11%), South-Central Asia (10%) and South-Eastern Asia (9%).

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

European Union 46007 72023 50699 32319 73689 61218 50430 50087 47517 37863

Belgium 5361 5234 5090 2006 6209 4060 94 214 189 83

Germany 3859 2838 1511 911 2152 1755 1961 1349 1383 5376

Spain 1125 4241 2243 961 1774 169 135 389 51 247

France 643 1009 612 359 461 3157 981 1197 753 496

United Kingdom 10986 24596 18016 14152 23601 15889 17103 14316 16222 10493

Greece 2124 1297 2146 1106 1297 2410 616 1172 777 153

Italy 8423 7833 7113 3273 5318 16380 4479 7837 4241 2566

Netherlands 10027 21239 8265 6507 27073 13855 21186 19193 19675 16036

Slovenia 1527 2019 755 49 150 24 168 0 0 0

0 10000 20000 30000 40000 50000 60000 70000 80000

Vo

lum

e in

To

ns

Years

Figure 31: Volumes of lemon and lime exported to various European Union member states, 2004 - 2013

35

Source: Quantec Easydata

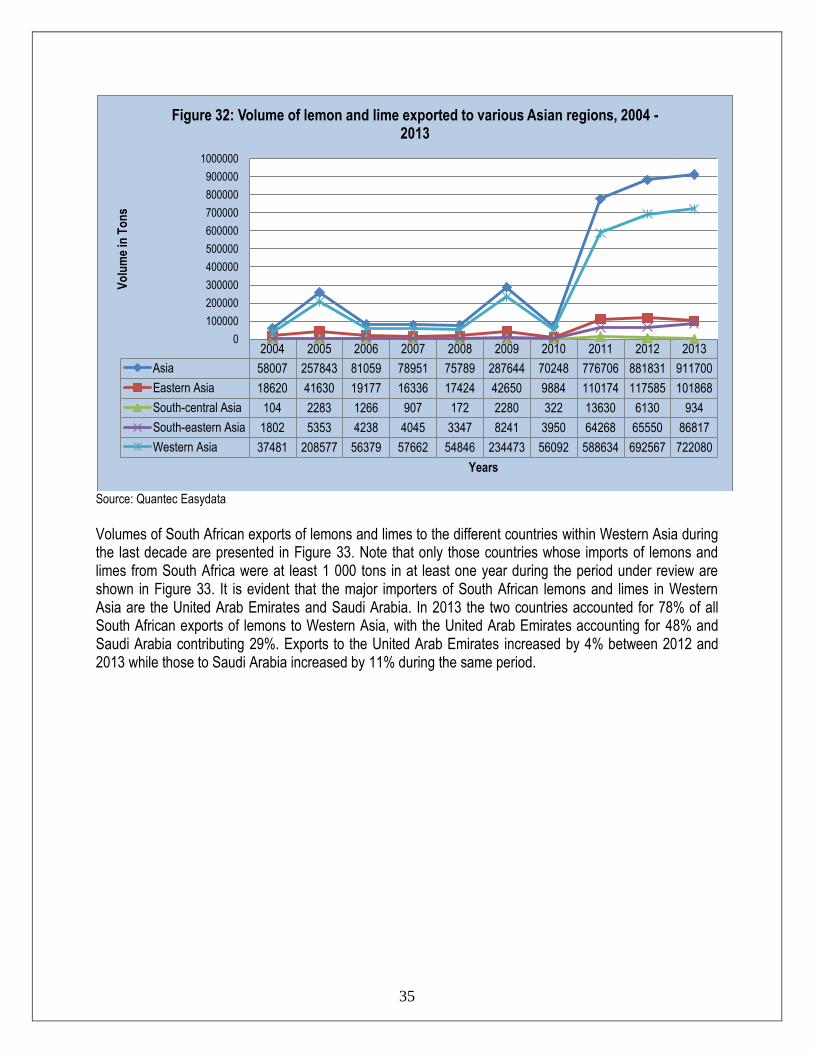

Volumes of South African exports of lemons and limes to the different countries within Western Asia during the last decade are presented in Figure 33. Note that only those countries whose imports of lemons and limes from South Africa were at least 1 000 tons in at least one year during the period under review are shown in Figure 33. It is evident that the major importers of South African lemons and limes in Western Asia are the United Arab Emirates and Saudi Arabia. In 2013 the two countries accounted for 78% of all South African exports of lemons to Western Asia, with the United Arab Emirates accounting for 48% and Saudi Arabia contributing 29%. Exports to the United Arab Emirates increased by 4% between 2012 and 2013 while those to Saudi Arabia increased by 11% during the same period.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Asia 58007 257843 81059 78951 75789 287644 70248 776706 881831 911700

Eastern Asia 18620 41630 19177 16336 17424 42650 9884 110174 117585 101868

South-central Asia 104 2283 1266 907 172 2280 322 13630 6130 934

South-eastern Asia 1802 5353 4238 4045 3347 8241 3950 64268 65550 86817

Western Asia 37481 208577 56379 57662 54846 234473 56092 588634 692567 722080

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

Vo

lum

e in

To

ns

Years

Figure 32: Volume of lemon and lime exported to various Asian regions, 2004 -2013

36

Source: Quantec Easydata

2.9.3 Grapefruits Quantities of South African exports of grapefruits to the various regions of the world during the last decade are shown in Figure 34. Grapefruits totalling 241 797 tons and worth R1.1 billion were exported by South African in 2013. Most of South Africa’s exports of grapefruits are destined for the European and Asian markets. In 2013, Europe accounted for 58% ( 140 347 tons) of total South African exports (241 797 tons) of grapefruits while those to Asia accounted for 35% (83 902 tons). There was a 196% increase in South African grapefruit exports in 2005. The increase was mainly the result of a huge increase in the demand for South African grapefruits in Asia during the same period. Exports to all regions increased by 35% between 2012 and 2013. Exports to Africa and the Americas remained below 30 000 tons during the period under review. The European and Asian markets will be disaggregated further below.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Western Asia 37481 208577 56379 57662 54846 234473 56092 58863 69257 72208

United Arab Emirates 14062 88640 25639 29337 27294 131196 28370 25009 33826 35191

Bahrain 2220 11016 1203 1990 1500 2112 1794 2609 2525 2421

Kuwait 1145 72167 2903 3057 4536 30616 4493 7501 8586 8522

Oman 423 2980 572 884 1224 4466 806 820 1914 1554

Qatar 714 234 403 658 542 842 705 1476 2095 1621

Saudi Arabia 18536 33356 25079 21103 18559 64324 19056 20652 18828 20987

0

50000

100000

150000

200000

250000

Vo

lum

e in

To

ns

Years

Figure 33: Volumes of lemon and lime exported to various countries of the Western Asia, 2004 -2013

37

Source: Quantec Easydata

Volumes of South African exports of grapefruits to the various regions of Europe from 2004 to 2013 are presented in Figure 35.

Source: Quantec Easydata

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

World 217136 642544 255815 261456 195764 370699 179610 217205 178229 241797

Africa 24721 1209 21146 28461 10532 13778 13465 12316 10281 9220

Americas 2999 22987 6689 4409 3517 22973 4876 6607 5224 8367

Asia 78487 461724 125937 87336 68571 124620 56292 73098 67586 83902

Europe 110928 156610 102025 141226 113099 208308 104940 125181 95074 140347

0

100000

200000

300000

400000

500000

600000

700000

Vo

lum

e in

To

ns

Years

Figure 34: Volumes of grapefruit exported to various regions in the world, 2004 - 2013

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Europe 110928 156610 102025 141226 113099 208308 104940 125181 95074 140347

Eastern Europe 6187 7482 14299 19065 14955 20471 18703 25028 14710 27946

Northern Europe 0 6 20 203 83 2019 165 100 109 162

Southern Europe 1 0 0 58 36 2008 25 142 56 229

Western Europe 202 227 101 117 61 169 39 417 33 432

European Union 104537 148894 87604 121784 97964 183641 86008 99495 80167 111578

0

50000

100000

150000

200000

250000

Vo

lum

e in

To

ns

Years

Figure 35: Volumes of grapefruit exported to various regions of Europe, 2004 - 2013

38

It is evident from Figure 35 that during the last decade the bulk of South African grapefruit exports that went to Europe were destined for the European Union. In 2013, 79% of all South African exports of grapefruits to Europe were absorbed by the European Union, with smaller quantities going to Eastern, Northern and Southern Europe. Total South African exports of grapefruits to Europe peaked in 2009 at 208 308 tons. It is interesting to note that volumes of South African exports of grapefruits to Europe more than doubled between 2004 and 2009. South African grapefruit exports to Europe increased by 47% between 2012 and 2013. Another growing market for South African grapefruits is Eastern Europe. Grapefruit exports to Eastern Europe increased from 6 187 tons in 2004 to 27 946 tons in 2013, an increase of 351% in ten years. Due to its significance to South African grapefruit exports the European Union market is further disaggregated in Figure 36.

Source: Quantec Easydata

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

European Union 104537 148894 87604 121784 97964 183641 86008 99495 80167 111578

Belgium 10904 15203 7823 31892 7511 10745 1265 1319 239 528

Bulgaria 195 40 2782 1386 217 147 271 274 223 300

Germany 3651 3622 2373 1738 2610 6820 4130 3275 3082 2887

Spain 5994 14964 4172 6416 4402 8203 2743 2989 1150 2089

France 5282 6896 5013 5161 3362 21686 3423 4714 2652 5267

United Kingdom 20389 25872 17526 15298 18776 14104 11218 10880 10097 12161

Greece 1130 943 404 1458 80 900 870 1497 1365 1932

Italy 10955 14471 12297 11742 9326 43621 7979 10141 9252 12508

Netherlands 45847 64892 29616 40214 47791 72932 50098 59795 46708 65031

Portugal 0 267 42 1418 412 276 1411 1332 2203 3464

Sweden 123 281 3047 1488 584 392 460 640 756 1244

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

Vo

lum

e in

To

ns

Years

Figure 36: Volumes of grapefruit exported to different European Union member states, 2004 - 2013

39

It is important to note that only those countries whose grapefruit imports from South Africa were at least 1 000 tons in at least one year during the period under review are shown in Figure 36. The major importers of South African grapefruits in the European Union are the Netherlands and the United Kingdom. In 2011 the Netherlands accounted for 58% of all South African grapefruit exports to the European Union while the United Kingdom accounted for 11% during the same year. Other important players in 2013 included Italy (11%) and France (5%). Grapefruit exports to the European Union as a whole increased by 39% between 2012 and 2013. Figure 37 presents volumes of South African exports of grapefruits to the different regions of Asia. The major Asian region in terms of South African grapefruit exports is Eastern Asia. The region absorbed 87% of the total South African exports of grapefruits to Asia in 2013. The total South African grapefruit exports to Asia peaked at 461 724 tons in 2005. South African exports of grapefruits to Asia increased by 7% between 2004 and 2013 while those to Eastern Asia decreased by 4% during the same period. South African exports of grapefruits declined from 124 620 tons in 2009 to 56 292 tons in 2010, representing a decline of 55% and increased again by 6% in 2013.

Source: Quantec Easydata

Volumes of South African grapefruit exports to the different countries in Eastern Asia during the last decade are presented in Figure 38. Note that only those countries whose grapefruit imports from South Africa were at least 1 000 tons in at least one year during the period under review are shown in Figure 38. The major importer of South African grapefruit in Eastern Asia is Japan. In 2013, Japan absorbed 66% of the total South African exports of grapefruits to Eastern Asia. South African exports of grapefruits to Japan

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Asia 78487 461724 125937 87336 68571 124620 56292 73098 67586 83902

Eastern Asia 76449 452309 120767 74291 63257 104331 51353 65704 60851 72996

South-central Asia 0 64 2 0 9 218 405 277 110 103

South-eastern Asia 660 1299 827 1579 823 1036 1072 1463 1612 2270

Western Asia 1378 8051 4341 11466 4482 19035 3462 5654 5014 8533

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

Vo

lum

e in

To

ns

Years

Figure 37: Volumes of grapefruit exported to various regions of Asia, 2004 - 2013

40

increased by 4% between 2012 and 2013. Other importers of South African grapefruit in Eastern Asia are China, Hong Kong and Taiwan.

Source: Quantec Easydata

2.9.4 Soft citrus Figure 39 presents volumes of South African exports of soft citrus to the different regions of the world during the last decade.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Eastern Asia 76449 452309 120767 74291 63257 104331 51353 68605 65376 78765

China 19 169 90 126 100 295 331 1458 1484 9593

Hong Kong 739 9023 6234 3702 2212 8883 3476 5594 5006 4680

Japan 73896 416297 105008 66324 59580 91834 45553 55631 49837 51967

Taiwan 1796 26821 9021 4114 1366 3319 1993 3020 4573 5769

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

Vo

lum

e in

To

ns

Years

Figure 38: Volumes of grapefruit exported to various countries of the Eastern Asia, 2004 - 2013

41

Source: Quantec Easydata

Most of South Africa’s exports of soft citrus during the past ten years went to Europe. The continent absorbed 75% of the total South African exports of soft citrus in 2013. South African exports of soft citrus to the world increased by 8% between 2012 and 2013. The second most important continent for South African exports of soft citrus in 2013 was Asia, which absorbed 19 567 tons during the same year. Exports to Africa and the Americas have been stable over the last decade, remaining below the 20 000 tons mark. Export volumes for South African soft citrus to the various regions of Europe for the period 2004 to 2013 are presented in Figure 40. It is evident that during the last decade the European Union absorbed the bulk of South African exports of soft citrus that went to Europe. The European Union accounted for 87% of the total South African exports of soft citrus in 2013. The remaining 13% went to Eastern and Southern Europe. Exports to Europe went up by 11% between 2012 and 2013. It is interesting to note that while exports to the European Union declined between 2010 and 2011, exports to Eastern Europe have been increasing during the ten years under review.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

World 77595 85674 86797 106781 112249 127115 115878 107945 122053 132920

Africa 1260 1511 1527 1498 1664 3481 2238 2634 3417 2991

Americas 11791 14789 23799 11464 9408 15402 13148 9557 13582 10510

Asia 5947 6311 8435 10653 12890 18000 17465 19046 15870 19567

Europe 58596 63038 53014 82970 88261 90156 83015 76708 89183 99851

0

20000

40000

60000

80000

100000

120000

140000

Vo

lum

e in

To

ns

Years

Figure 39: Volumes of soft citrus exports various regions of the world, 2004 - 2013

42

Source: Quantec Easydata

Due to its relative importance to exports of South African soft citrus the European Union market is further disaggregated below. Volumes of South African exports of soft citrus to the different European Union member states during the last decade are presented in Figure 41. Only those countries whose imports of soft citrus from South Africa were at least 1 000 tons in at least one year during the period under review are shown in Figure 41. The major importers of soft citrus from South Africa are the United Kingdom and the Netherlands. In 2013, the two countries accounted for 92% of the total South African exports of soft citrus to the European Union, with the United Kingdom accounting for 57% and the Netherlands contributing 35%. Between 2012 and 2013, exports to the United Kingdom went up by 4% while those to the Netherlands also increased by 25%.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Europe 58596 63038 53014 82970 88261 90156 83015 76708 89183 99851

Eastern Europe 6778 4699 5575 5944 13368 8538 13013 12782 12324 12736

Southern Europe 44 0 0 43 10 2204 242 132 64 20

European Union 51774 58277 47398 76874 74705 79207 69747 63747 76751 87094

0

20000

40000

60000

80000

100000

120000

Vo

lum

e in

To

ns

Years

Figure 40: Volumes of soft citrus exported to various regions Europe, 2004 - 2013

43

Source: Quantec Easydata

2.10 Provincial and district export values of South African citrus Figure 40 below depicts the value of citrus exports from each province of South Africa during the last ten years. The figure presents an interesting but somewhat misleading view of the source of citrus products destined for the export markets. Firstly, the fact that approximately 71% of the citrus export value was derived from the Western Cape in 2013 does not mean that the province was the main producer of citrus. It only implies that the majority of registered exporters are based in the Western Cape. Secondly, the province (Western Cape) serves as exit point for citrus exports through the Cape Town harbour. Citrus products worth R9.3 billion were exports by South Africa in 2013. Following the Western Cape in terms of the value of citrus exports in 2013 were the Eastern Cape, Limpopo and Gauteng at 13%, 10% and 3% respectively.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

European Union 51774 58277 47398 76874 74705 79207 69747 63747 76751 87094

Belgium 2425 2380 1495 3287 3282 2736 834 315 45 172

Germany 847 164 0 280 41 160 398 26 428 1219

Spain 409 621 259 1967 759 670 181 465 618 232

France 94 62 264 243 385 769 605 621 773 1576

United Kingdom 34876 43564 36794 53204 48207 55585 45266 40802 48181 50271

Ireland 26 51 653 2089 3523 3251 1808 1782 1901 1946

Italy 220 148 101 264 72 238 271 1211 110 93

Netherlands 12432 10742 7342 14958 17719 14798 18932 17879 24003 30198

0 10000 20000 30000 40000 50000 60000 70000 80000 90000

100000

Vo

lum

e in

To

ns

Years

Figure 41: Volumes of soft citrus exported to various European Union member states, 2004 - 2013

44

Source: Quantec Easydata

The following figures (Figures 43 - 51) show the value of citrus exports from the various districts in the nine provinces of South Africa. Figure 43 illustrates values of citrus exports by the Eastern Cape province. It is clear from Figure 43 that citrus exports from the Eastern Cape are mainly from the Nelson Mandela, Cacadu, Chris Hani and Amatole municipalities. High export values for the leading municipalities were recorded in 2013 (for Amatole, Nelson Mandela, Chris Hani and Cacadu). The use of the Port Elizabeth harbour as an exit point may have played a major role in both Nelson Mandela and Cacadu municipalities being leaders in the export of citrus from the Eastern Cape. A total of R1.1 billion worth of citrus products exports was recorded by the Eastern Cape in 2013. This was 48% higher than the value exported in 2012.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

RSA 2972 3177 3525 4317 5643 5294 6574 7067 7388 9335

Western Cape 2218 2233 2411 3377 4356 3966 5013 5164 5366 6585

Eastern Cape 82 70 193 281 390 429 463 747 792 1178

Northern Cape 8 11 16 11 35 34 28 36 32 48

Free State 0 0 1 2 1 1 0 0 1 13

Kwazulu-Natal 18 47 53 60 53 37 16 19 25 28

North West 0 2 2 0 4 0 1 10 0 0

Gauteng 388 437 444 107 112 104 164 182 204 239

Mpumalanga 149 173 119 176 227 232 368 279 351 336

Limpopo 109 203 285 303 466 490 521 629 617 908

0 1000 2000 3000 4000 5000 6000 7000 8000 9000

10000

Ran

ds

(R10

00 0

00)

Years

Figure 42: Value of citrus exports by province, 2004 - 2013

45

Source: Quantec Easydata

Values of citrus exports by the Limpopo province are shown in Figure 44.

Source: Quantec Easydata

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Eastern Cape 82 70 193 281 390 429 463 747 792 1178

Cacadu 11 14 77 81 129 143 111 186 211 245

Amatole 0 0 0 3 2 13 18 46 48 67

Chris Hani 0 0 0 0 0 0 0 31 82 141

O. R. Tambo 33 0 0 0 0 0 0 0 0 0

Nelson Mandela 38 56 116 197 258 273 335 484 451 724

0

200

400

600

800

1000

1200

1400

Ran

ds(

R10

00 0

00)

Years

Figure 43: Value of citrus exports by the Eastern Cape province, 2004 - 2013

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Limpopo 109 203 285 303 466 490 521 629 617 908

Mopani 82 142 226 149 312 283 330 482 447 718

Vhembe 0 0 0 8 22 66 42 73 72 62

Capricorn 1 11 25 80 9 9 1 3 7 0

Waterberg 1 1 6 4 6 1 0 0 0 0

Sekhukhune 26 50 28 62 116 130 147 72 92 127

0

100

200

300

400

500

600

700

800

900

1000

Ran

ds

(R10

00 0

00)

Years

Figure 44: Value of citrus exports by Limpopo province, 2004 - 2013

46

The major citrus exporting region in the Limpopo province is Mopani. The region recorded R908 million worth of citrus product exports in 2013. Other important exporting regions are the Greater Sekhukhune and Vhembe municipalities. High export values of the leading municipalities were recorded in 2013 (for Mopani) and 2010 (for Greater Sekhukhune). The total export value for citrus product exports from Limpopo increased from R617 million in 2012 to R908 million in 2013. Values of citrus exports from the Mpumalanga province are depicted in Figure 45.

Source: Quantec Easydata

Citrus exports from Mpumalanga are mainly from Ehlanzeni and to a lesser extend Nkangala and Gert Sibande municipalities. High export values for the leading municipalities were recorded in 2012 (for Ehlanzeni) and 2010 (for Nkangala). A total value of R336 million worth of citrus products exports was recorded by Mpumalanga in 2013. This was down from R351 million recorded in 2012. Values of citrus exports from the Western Cape are illustrated in Figure 46. The major citrus exporting region in the Western Cape is the City of Cape Town. The city recorded citrus exports worth R5 billion in 2013. Other leading municipalities are the Cape Winelands and West Coast which recorded citrus exports worth R934 million and R445 million respectively during 2013. The use of the Cape Town harbour as an exit point plays a major role in the City of Cape Town being a leader in the export of citrus from the Western Cape.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Mpumalanga 149 173 119 176 227 232 368 279 351 336

Gert Sibande 4 10 18 14 13 11 14 16 28 0

Nkangala 9 3 5 10 15 26 64 25 17 33

Ehlanzeni 136 160 96 152 200 196 290 238 306 303

0

50

100

150

200

250

300

350

400

Ran

ds

(R10

00 0

00)

Years

Figure 45: Value of citrus exports by Mpumalanga province, 2004 - 2013

47

Source: Quantec Easydata

Citrus export values from the Gauteng province are presented in Figure 47.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Western Cape 2218 2233 2411 3377 4356 3966 5013 5164 5366 6585

City of Cape Town 1672 1645 1724 2619 3134 2854 3801 3892 3868 5011

West Coast 145 138 208 231 391 363 366 364 417 445

Cape Winelands 370 439 465 518 819 733 825 888 1013 934

Overberg 28 6 10 7 10 13 17 15 13 107

Eden 3 5 4 1 2 3 4 4 56 88

0

1000

2000

3000

4000

5000

6000

7000

Ran

ds

(R10

00 0

00)

Years

Figure 46: Value of citrus exports by Western Cape province, 2004 - 2013

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Gauteng 388 437 444 107 112 104 164 182 204 239

Sedibeng 0 0 1 0 1 0 0 0 0 3

Metsweding 17 22 5 1 0 0 0 0 21 80

West Rand 0 7 3 5 5 3 4 4 5 32

Ekurhuleni 3 2 2 45 2 25 14 14 13 10

City of Johannesburg 91 96 68 48 80 58 103 110 79 103

City of Tshwane 276 311 365 8 24 19 43 54 86 12

0 50

100 150 200 250 300 350 400 450 500

Ran

ds

(R10

00 0

00)

Years

Figure 47: Value of citrus exports by Gauteng province, 2004 - 2013

48

Source: Quantec Easydata

The total value of citrus products exports from Gauteng declined from R388 million in 2004 to R239 million in 2013, a decline of 38% in ten years. The major citrus products exporting regions in Gauteng are the Cities of Tshwane and Johannesburg. The City of Tshwane (as well as Gauteng province) has gradually lost its share from the high values in 2004. The primary reason for that decline may be the consolidation by the Western Cape and the City of Johannesburg as the main exporters of citrus in South Africa. The Ekurhuleni municipality has also established itself as a major exporter of citrus products in Gauteng over the past ten years. Values of citrus exports from Kwazulu Natal are presented in Figure 48. The major exporter of citrus products in Kwazulu Natal is eThekwini municipality. The municipality recorded exports of citrus products worth R28 million in 2013. This was up from the R25 million recorded in 2012. Other important contributors towards the total value of citrus products exports in Kwazulu Natal during the past ten years are Uthungulu and Umgungundlovu. Generally, there were some fluctuations on the citrus export values for eThekwini municipality over the past decade. The use of the Durban harbour as an exit point plays a major role in eThekwini municipality being a leader in the export of citrus from Kwazulu Natal.

Source: Quantec Easydata

Values of citrus exports from the Free State province are shown in Figure 49. It is clear from Figure 48 that citrus exports from the Free State are mainly from Xhariep and Lejweleputswa municipality. High export value for the leading municipality was recorded in 2013 when the Xhariep municipality exported citrus products worth R12.5 billion. Citrus products worth R12.9 billion all from Xhariep municipality were exported by the Free State province in 2013.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Kwazulu-Natal 18 47 53 60 53 37 16 19 25 28

Ugu 0 0 0 0 0 0 0 1 0 0

Umgungundlovu 0 0 12 16 17 0 0 0 0 0

Uthungulu 3 20 8 1 7 12 2 0 0 0

eThekwini 15 27 33 43 28 25 13 19 25 22

0

10

20

30

40

50

60

70

Ran

ds(

R10

00 0

00)

Years

Figure 48: Value of citrus exports by the Kwazulu Natal, 2004 - 2013

49

Source: Quantec Easydata

Values of citrus exports from the North West province are shown in Figure 50.

Source: Quantec Easydata

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Free State 298 387 547 1544 1300 1260 306 162 1120 12984

Xhariep 0 0 0 0 0 0 0 0 966 12535

Motheo 0 0 0 1160 0 0 0 0 0 0

Lejweleputswa 298 387 547 384 1300 1260 306 162 154 449

0

2000

4000

6000

8000

10000

12000

14000

Ran

ds

(R10

00)

Years

Figure 49: Value of citrus exports by the Free state province, 2004 - 2013

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

North West 0 2 2 0 4 0 1 10 0 0

Bojanala 0 2 2 0 4 0 0 0 0 0

Bophirima 0 0 0 0 0 0 1 10 0 0

Southern 0 0 0 0 0 0 0 6 21 138

0

20

40

60

80

100

120

140

160

Ran

ds

(R10

00 0

00)

Years

Figure 50: Value of citrus exports by the North West province, 2004 - 2013

50

The major exporters of citrus products in the North West province are Bojanala and Bophirima districts. All export recorded during past two marketing season were from Southern district. Values of citrus exports from the Northern Cape province are shown in Figure 51.

Source: Quantec Easydata

It is clear from Figure 51 that citrus exports from the Northern Cape are mainly from Siyanda municipality and the Francis Baard (to a lesser extent). High export values for the Siyanda district were recorded in 2013. Citrus products exports worth R48 million were recorded in the Northern Cape in 2013. The value was up from the R32 million recorded in 2012. 2.11 Share analysis Table 2 is an illustration of provincial shares towards national citrus exports. It shows that Western Cape together with Gauteng province (to a lesser extend) have commanded the greatest share of citrus exports for the past ten years. The two provinces accounted for 75.7% of the total value of citrus products exports in 2011. This is in spite of the fact that Limpopo, Eastern Cape and Mpumalanga provinces are the leading producers of citrus products. Limpopo and Mpumalanga provinces accounted for 8.9% and 3.9% respectively while Kwazulu Natal accounted for 0.3% in 2011. The Eastern Cape province accounted for 10.6% of the total citrus products export value in 2011. As explained earlier, this means that the leading export provinces (Western Cape and Gauteng) derive their advantage from the fact that the registered exporters are based in their provinces and they also have exit points for citrus exports.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Northern Cape 8 11 16 11 35 34 28 36 32 48

Siyanda 8 11 16 11 32 31 25 34 31 44

Frances Baard 0 0 0 0 3 2 3 2 1 4

0

10

20

30

40

50

60

Ran

ds

(R10

00 0

00)

Rands

Figure 51: Value of citrus exports by Northern Cape province, 2004 - 2013

51

Table 2: Share of Provincial citrus exports to the total RSA citrus exports (%), 2004 – 2013 Years District

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

RSA 100 100 100 100 100 100 100 100 100 100

Western Cape 75 70 68 78 77 75 76 73 73 71

Eastern Cape 3 2 5 7 7 8 7 11 11 13

Northern Cape 0 0 0 0 1 1 0 1 0 1

Free State 0 0 0 0 0 0 0 0 0 0

Kwazulu-Natal 1 1 1 1 1 1 0 0 0 0

North West 0 0 0 0 0 0 0 0 0 0

Gauteng 13 14 13 2 2 2 2 3 3 3

Mpumalanga 5 5 3 4 4 4 6 4 5 4

Limpopo 4 6 8 7 8 9 8 9 8 10 Source: Calculated from Quantec Easydata

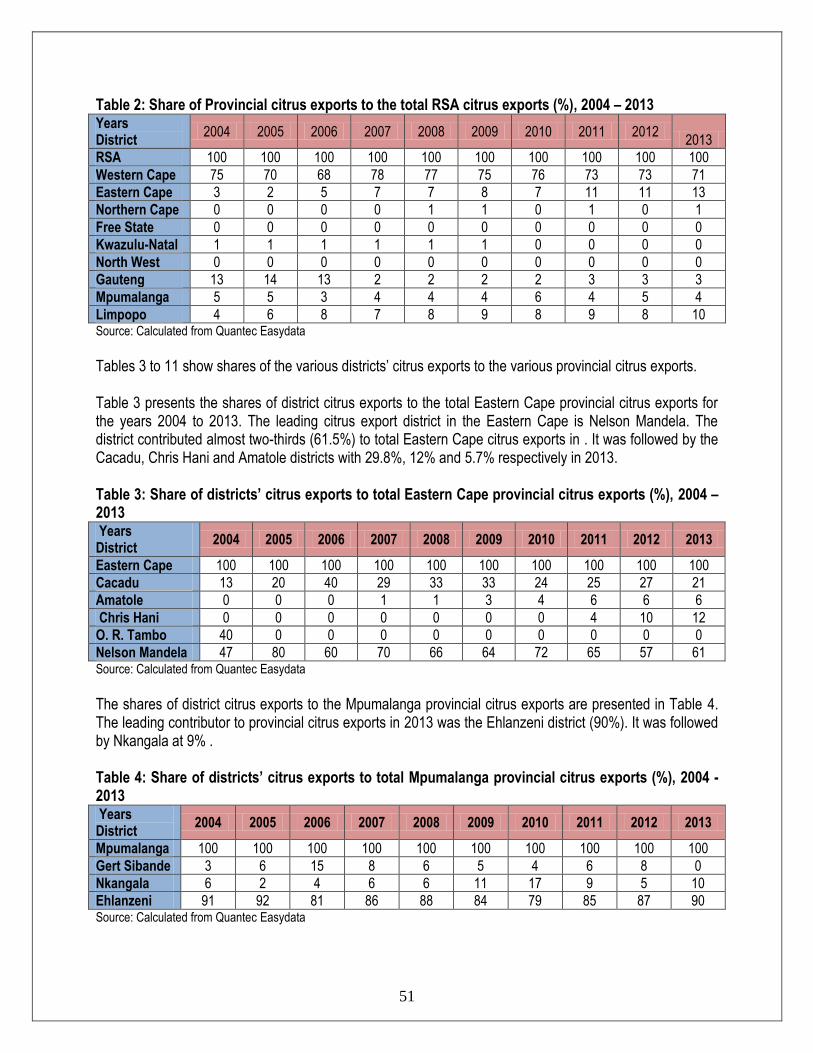

Tables 3 to 11 show shares of the various districts’ citrus exports to the various provincial citrus exports. Table 3 presents the shares of district citrus exports to the total Eastern Cape provincial citrus exports for the years 2004 to 2013. The leading citrus export district in the Eastern Cape is Nelson Mandela. The district contributed almost two-thirds (61.5%) to total Eastern Cape citrus exports in . It was followed by the Cacadu, Chris Hani and Amatole districts with 29.8%, 12% and 5.7% respectively in 2013. Table 3: Share of districts’ citrus exports to total Eastern Cape provincial citrus exports (%), 2004 – 2013 Years District

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Eastern Cape 100 100 100 100 100 100 100 100 100 100

Cacadu 13 20 40 29 33 33 24 25 27 21

Amatole 0 0 0 1 1 3 4 6 6 6

Chris Hani 0 0 0 0 0 0 0 4 10 12

O. R. Tambo 40 0 0 0 0 0 0 0 0 0

Nelson Mandela 47 80 60 70 66 64 72 65 57 61 Source: Calculated from Quantec Easydata

The shares of district citrus exports to the Mpumalanga provincial citrus exports are presented in Table 4. The leading contributor to provincial citrus exports in 2013 was the Ehlanzeni district (90%). It was followed by Nkangala at 9% . Table 4: Share of districts’ citrus exports to total Mpumalanga provincial citrus exports (%), 2004 - 2013 Years District

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Mpumalanga 100 100 100 100 100 100 100 100 100 100

Gert Sibande 3 6 15 8 6 5 4 6 8 0

Nkangala 6 2 4 6 6 11 17 9 5 10

Ehlanzeni 91 92 81 86 88 84 79 85 87 90 Source: Calculated from Quantec Easydata

52