a possible effect of the eurozone debt crisis commentary no5... · the spotlight throughout the...

TRANSCRIPT

A TORRENT OF MORTGAGE DEFAULTS: A POSSIBLE EFFECT OF THE EUROZONE DEBT CRISIS | 1

A torrent of mortgage defaults A possible effect of the eurozone debt crisis

Angelo Fiorante*

ECRI Commentary No. 5 (May 2011)

Introduction

The credit markets in Europe have witnessed fast-paced development, where the credit extended to households has increased considerably during the last decade. After seeing a range of property bubbles and overvalued real estate markets across Europe, a legitimate question is whether the amount of mortgage credit outstanding has reached its limit for certain countries? The various episodes of the ongoing eurozone debt crisis have received a lot of attention, but they have to some extent overshadowed the debate on how the loan repayment ability of households will be affected after the resolution of the crisis. Will the more indebted European households manage to keep their heads above water as new and more stringent economic conditions take hold across some of the eurozone countries? This commentary takes a closer look at the mortgage credit developments of households in the eurozone peripheral countries of Portugal, Ireland, Greece, Italy and Spain, nations that have been in the spotlight throughout the European sovereign debt crisis (from 2010 to the present). They have gone under the unpleasant acronym of the PIIGS nations, a term that has been frequently used by the international economic press to describe the boom–bust odyssey that some of these markets have exhibited.

1. The size of the mortgage markets in Europe

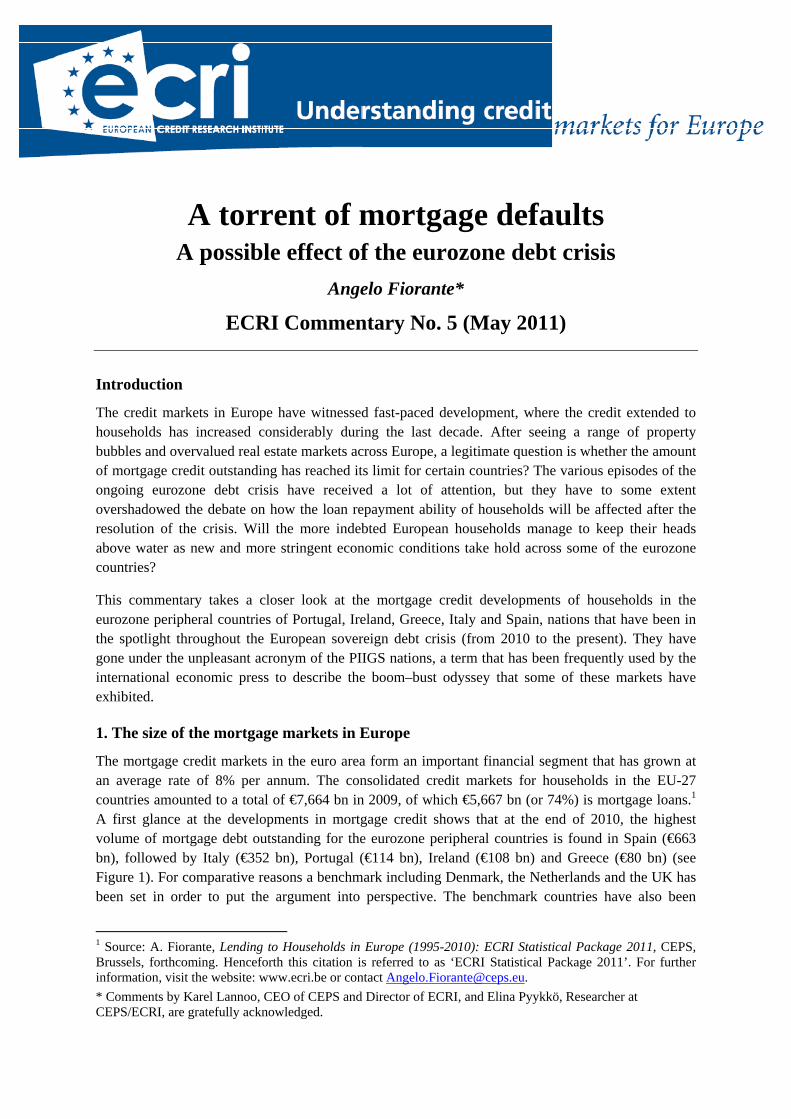

The mortgage credit markets in the euro area form an important financial segment that has grown at an average rate of 8% per annum. The consolidated credit markets for households in the EU-27 countries amounted to a total of €7,664 bn in 2009, of which €5,667 bn (or 74%) is mortgage loans.1 A first glance at the developments in mortgage credit shows that at the end of 2010, the highest volume of mortgage debt outstanding for the eurozone peripheral countries is found in Spain (€663 bn), followed by Italy (€352 bn), Portugal (€114 bn), Ireland (€108 bn) and Greece (€80 bn) (see Figure 1). For comparative reasons a benchmark including Denmark, the Netherlands and the UK has been set in order to put the argument into perspective. The benchmark countries have also been

1 Source: A. Fiorante, Lending to Households in Europe (1995-2010): ECRI Statistical Package 2011, CEPS, Brussels, forthcoming. Henceforth this citation is referred to as ‘ECRI Statistical Package 2011’. For further information, visit the website: www.ecri.be or contact [email protected]. * Comments by Karel Lannoo, CEO of CEPS and Director of ECRI, and Elina Pyykkö, Researcher at CEPS/ECRI, are gratefully acknowledged.

2 | ANGELO FIORANTE

chosen because of their large, but more mature and persistent credit markets. Denmark and the Netherlands are small economies that are comparable with Portugal, Ireland and Greece, and the UK’s economy is comparable with those of Italy and Spain.

Figure 1. Mortgage credit volume

Note: End of year exchange rates derived from Eurostat. Source: ECRI Statistical Package 2011.

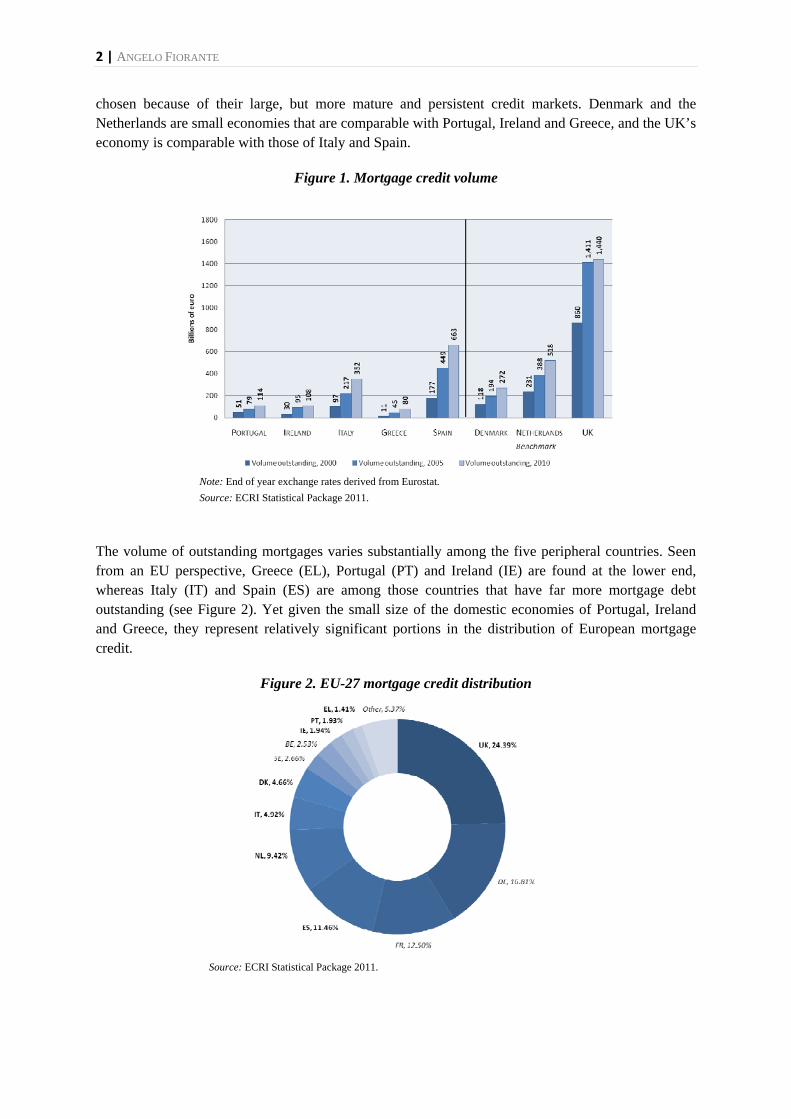

The volume of outstanding mortgages varies substantially among the five peripheral countries. Seen from an EU perspective, Greece (EL), Portugal (PT) and Ireland (IE) are found at the lower end, whereas Italy (IT) and Spain (ES) are among those countries that have far more mortgage debt outstanding (see Figure 2). Yet given the small size of the domestic economies of Portugal, Ireland and Greece, they represent relatively significant portions in the distribution of European mortgage credit.

Figure 2. EU-27 mortgage credit distribution

Source: ECRI Statistical Package 2011.

A TORRENT OF MORTGAGE DEFAULTS: A POSSIBLE EFFECT OF THE EUROZONE DEBT CRISIS | 3

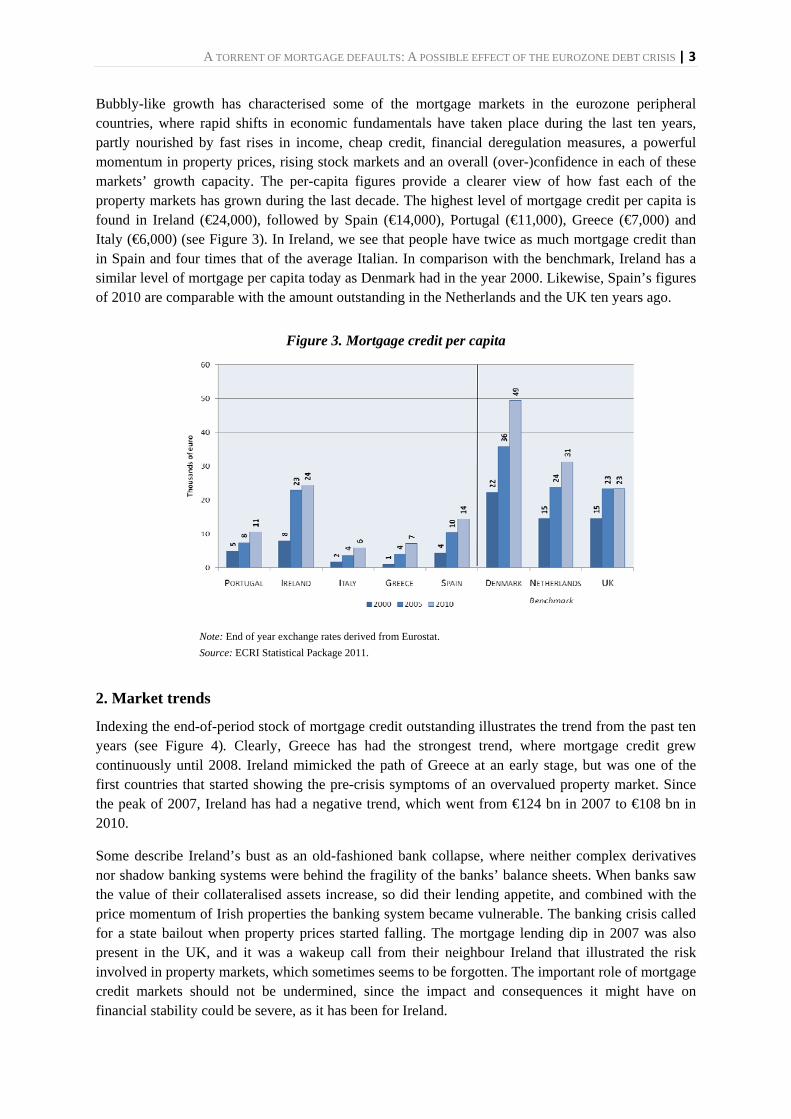

Bubbly-like growth has characterised some of the mortgage markets in the eurozone peripheral countries, where rapid shifts in economic fundamentals have taken place during the last ten years, partly nourished by fast rises in income, cheap credit, financial deregulation measures, a powerful momentum in property prices, rising stock markets and an overall (over-)confidence in each of these markets’ growth capacity. The per-capita figures provide a clearer view of how fast each of the property markets has grown during the last decade. The highest level of mortgage credit per capita is found in Ireland (€24,000), followed by Spain (€14,000), Portugal (€11,000), Greece (€7,000) and Italy (€6,000) (see Figure 3). In Ireland, we see that people have twice as much mortgage credit than in Spain and four times that of the average Italian. In comparison with the benchmark, Ireland has a similar level of mortgage per capita today as Denmark had in the year 2000. Likewise, Spain’s figures of 2010 are comparable with the amount outstanding in the Netherlands and the UK ten years ago.

Figure 3. Mortgage credit per capita

Note: End of year exchange rates derived from Eurostat. Source: ECRI Statistical Package 2011.

2. Market trends

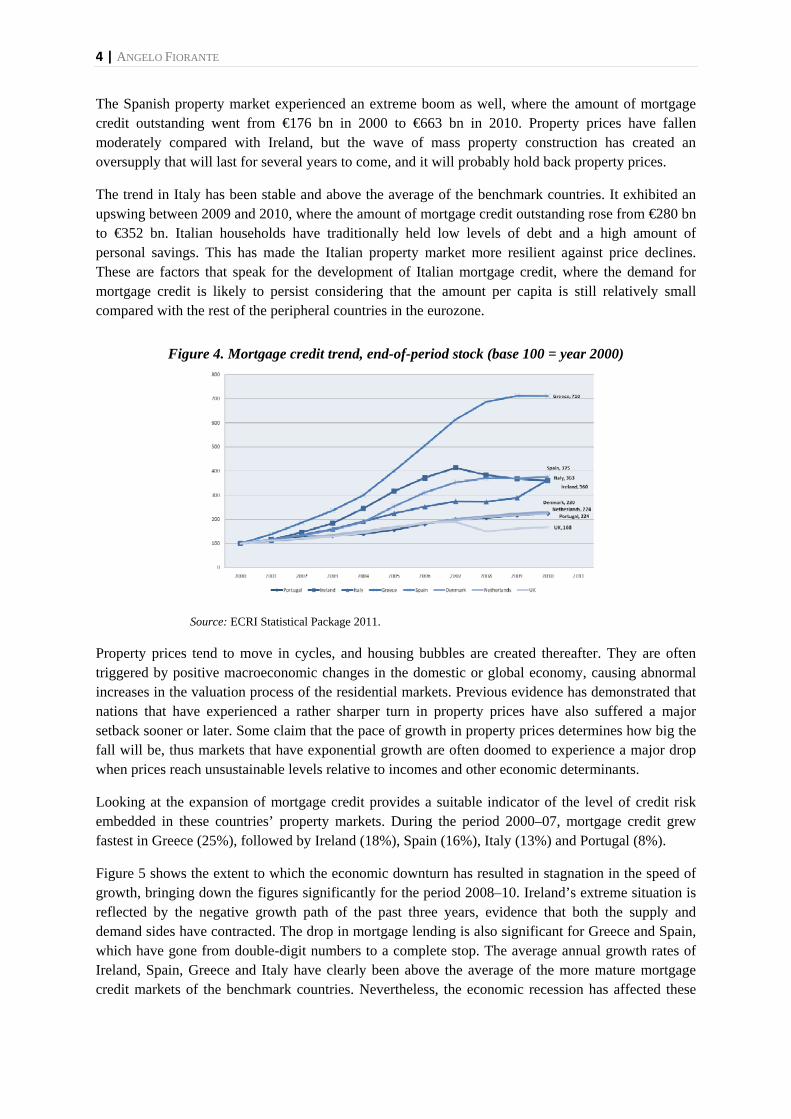

Indexing the end-of-period stock of mortgage credit outstanding illustrates the trend from the past ten years (see Figure 4). Clearly, Greece has had the strongest trend, where mortgage credit grew continuously until 2008. Ireland mimicked the path of Greece at an early stage, but was one of the first countries that started showing the pre-crisis symptoms of an overvalued property market. Since the peak of 2007, Ireland has had a negative trend, which went from €124 bn in 2007 to €108 bn in 2010.

Some describe Ireland’s bust as an old-fashioned bank collapse, where neither complex derivatives nor shadow banking systems were behind the fragility of the banks’ balance sheets. When banks saw the value of their collateralised assets increase, so did their lending appetite, and combined with the price momentum of Irish properties the banking system became vulnerable. The banking crisis called for a state bailout when property prices started falling. The mortgage lending dip in 2007 was also present in the UK, and it was a wakeup call from their neighbour Ireland that illustrated the risk involved in property markets, which sometimes seems to be forgotten. The important role of mortgage credit markets should not be undermined, since the impact and consequences it might have on financial stability could be severe, as it has been for Ireland.

4 | ANGELO FIORANTE

The Spanish property market experienced an extreme boom as well, where the amount of mortgage credit outstanding went from €176 bn in 2000 to €663 bn in 2010. Property prices have fallen moderately compared with Ireland, but the wave of mass property construction has created an oversupply that will last for several years to come, and it will probably hold back property prices.

The trend in Italy has been stable and above the average of the benchmark countries. It exhibited an upswing between 2009 and 2010, where the amount of mortgage credit outstanding rose from €280 bn to €352 bn. Italian households have traditionally held low levels of debt and a high amount of personal savings. This has made the Italian property market more resilient against price declines. These are factors that speak for the development of Italian mortgage credit, where the demand for mortgage credit is likely to persist considering that the amount per capita is still relatively small compared with the rest of the peripheral countries in the eurozone.

Figure 4. Mortgage credit trend, end-of-period stock (base 100 = year 2000)

Source: ECRI Statistical Package 2011.

Property prices tend to move in cycles, and housing bubbles are created thereafter. They are often triggered by positive macroeconomic changes in the domestic or global economy, causing abnormal increases in the valuation process of the residential markets. Previous evidence has demonstrated that nations that have experienced a rather sharper turn in property prices have also suffered a major setback sooner or later. Some claim that the pace of growth in property prices determines how big the fall will be, thus markets that have exponential growth are often doomed to experience a major drop when prices reach unsustainable levels relative to incomes and other economic determinants.

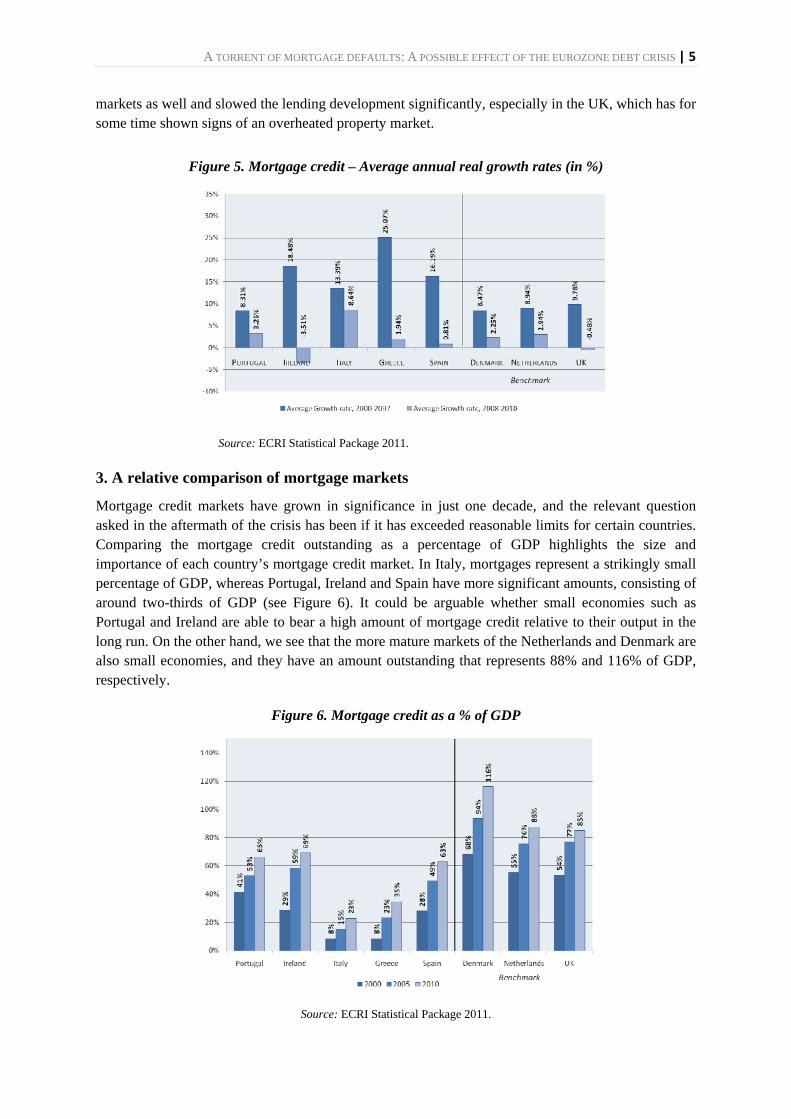

Looking at the expansion of mortgage credit provides a suitable indicator of the level of credit risk embedded in these countries’ property markets. During the period 2000–07, mortgage credit grew fastest in Greece (25%), followed by Ireland (18%), Spain (16%), Italy (13%) and Portugal (8%).

Figure 5 shows the extent to which the economic downturn has resulted in stagnation in the speed of growth, bringing down the figures significantly for the period 2008–10. Ireland’s extreme situation is reflected by the negative growth path of the past three years, evidence that both the supply and demand sides have contracted. The drop in mortgage lending is also significant for Greece and Spain, which have gone from double-digit numbers to a complete stop. The average annual growth rates of Ireland, Spain, Greece and Italy have clearly been above the average of the more mature mortgage credit markets of the benchmark countries. Nevertheless, the economic recession has affected these

A TORRENT OF MORTGAGE DEFAULTS: A POSSIBLE EFFECT OF THE EUROZONE DEBT CRISIS | 5

markets as well and slowed the lending development significantly, especially in the UK, which has for some time shown signs of an overheated property market.

Figure 5. Mortgage credit – Average annual real growth rates (in %)

Source: ECRI Statistical Package 2011.

3. A relative comparison of mortgage markets

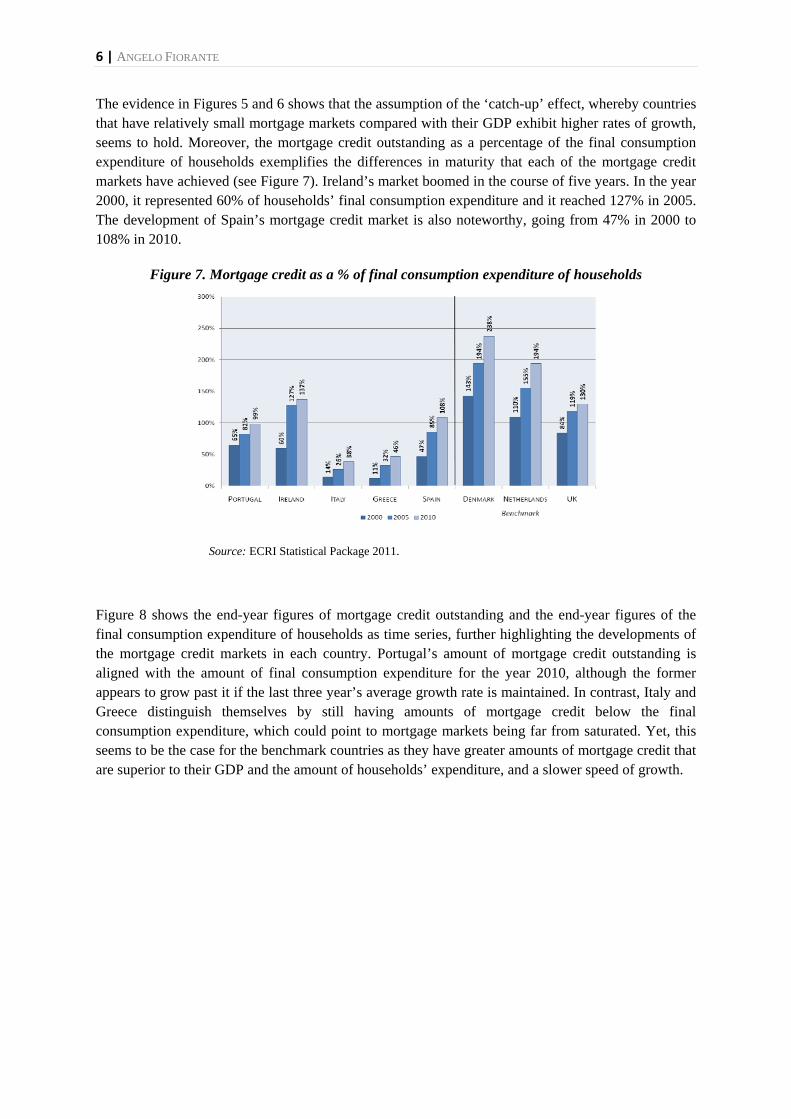

Mortgage credit markets have grown in significance in just one decade, and the relevant question asked in the aftermath of the crisis has been if it has exceeded reasonable limits for certain countries. Comparing the mortgage credit outstanding as a percentage of GDP highlights the size and importance of each country’s mortgage credit market. In Italy, mortgages represent a strikingly small percentage of GDP, whereas Portugal, Ireland and Spain have more significant amounts, consisting of around two-thirds of GDP (see Figure 6). It could be arguable whether small economies such as Portugal and Ireland are able to bear a high amount of mortgage credit relative to their output in the long run. On the other hand, we see that the more mature markets of the Netherlands and Denmark are also small economies, and they have an amount outstanding that represents 88% and 116% of GDP, respectively.

Figure 6. Mortgage credit as a % of GDP

Source: ECRI Statistical Package 2011.

6 | ANGELO FIORANTE

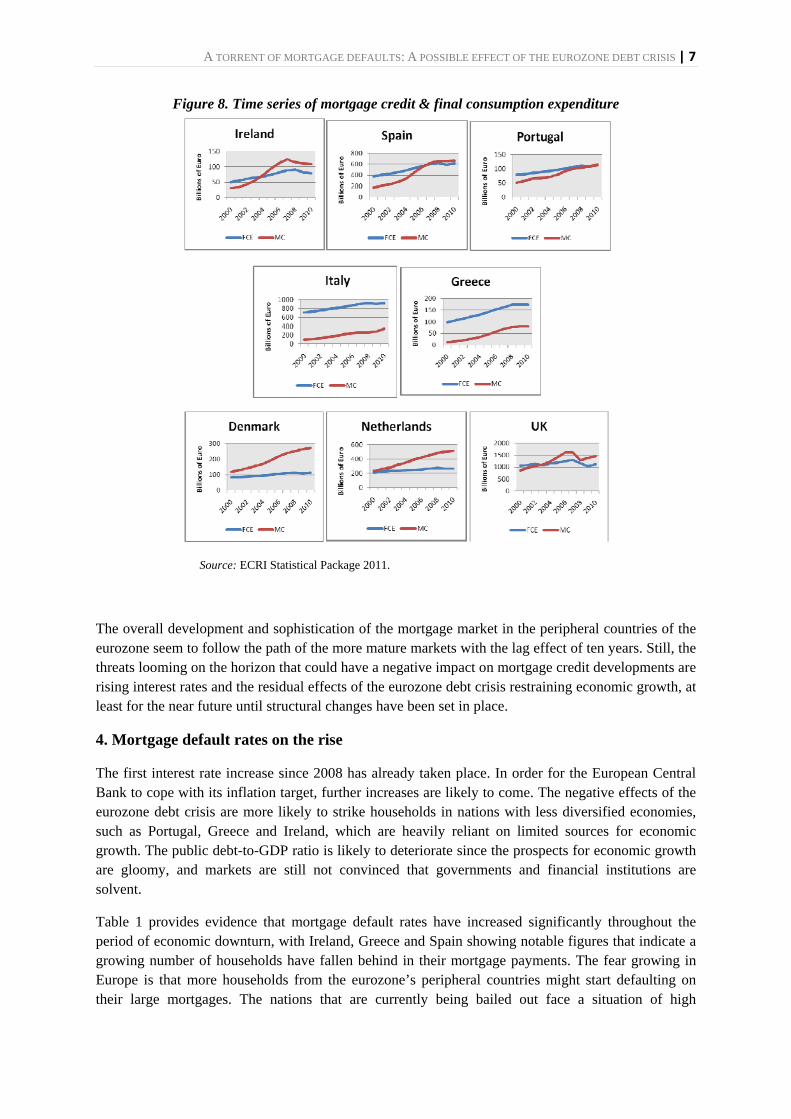

The evidence in Figures 5 and 6 shows that the assumption of the ‘catch-up’ effect, whereby countries that have relatively small mortgage markets compared with their GDP exhibit higher rates of growth, seems to hold. Moreover, the mortgage credit outstanding as a percentage of the final consumption expenditure of households exemplifies the differences in maturity that each of the mortgage credit markets have achieved (see Figure 7). Ireland’s market boomed in the course of five years. In the year 2000, it represented 60% of households’ final consumption expenditure and it reached 127% in 2005. The development of Spain’s mortgage credit market is also noteworthy, going from 47% in 2000 to 108% in 2010.

Figure 7. Mortgage credit as a % of final consumption expenditure of households

Source: ECRI Statistical Package 2011.

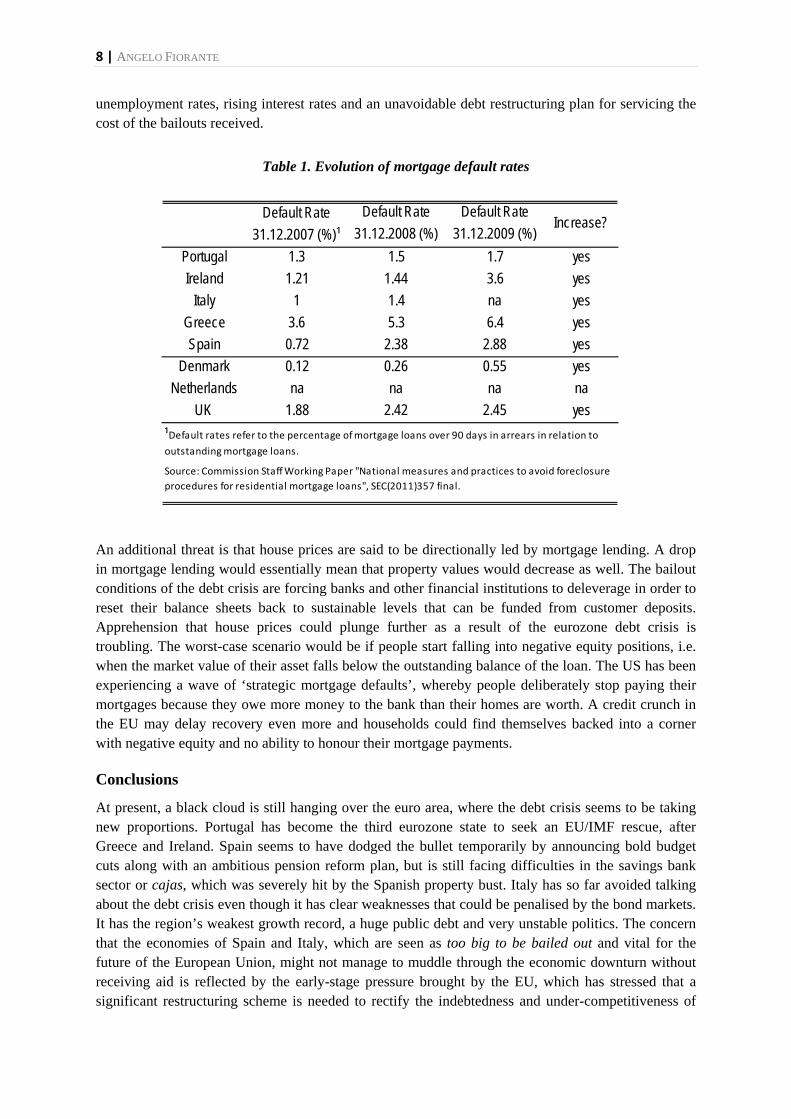

Figure 8 shows the end-year figures of mortgage credit outstanding and the end-year figures of the final consumption expenditure of households as time series, further highlighting the developments of the mortgage credit markets in each country. Portugal’s amount of mortgage credit outstanding is aligned with the amount of final consumption expenditure for the year 2010, although the former appears to grow past it if the last three year’s average growth rate is maintained. In contrast, Italy and Greece distinguish themselves by still having amounts of mortgage credit below the final consumption expenditure, which could point to mortgage markets being far from saturated. Yet, this seems to be the case for the benchmark countries as they have greater amounts of mortgage credit that are superior to their GDP and the amount of households’ expenditure, and a slower speed of growth.

A TORRENT OF MORTGAGE DEFAULTS: A POSSIBLE EFFECT OF THE EUROZONE DEBT CRISIS | 7

Figure 8. Time series of mortgage credit & final consumption expenditure

Source: ECRI Statistical Package 2011.

The overall development and sophistication of the mortgage market in the peripheral countries of the eurozone seem to follow the path of the more mature markets with the lag effect of ten years. Still, the threats looming on the horizon that could have a negative impact on mortgage credit developments are rising interest rates and the residual effects of the eurozone debt crisis restraining economic growth, at least for the near future until structural changes have been set in place.

4. Mortgage default rates on the rise

The first interest rate increase since 2008 has already taken place. In order for the European Central Bank to cope with its inflation target, further increases are likely to come. The negative effects of the eurozone debt crisis are more likely to strike households in nations with less diversified economies, such as Portugal, Greece and Ireland, which are heavily reliant on limited sources for economic growth. The public debt-to-GDP ratio is likely to deteriorate since the prospects for economic growth are gloomy, and markets are still not convinced that governments and financial institutions are solvent.

Table 1 provides evidence that mortgage default rates have increased significantly throughout the period of economic downturn, with Ireland, Greece and Spain showing notable figures that indicate a growing number of households have fallen behind in their mortgage payments. The fear growing in Europe is that more households from the eurozone’s peripheral countries might start defaulting on their large mortgages. The nations that are currently being bailed out face a situation of high

8 | ANGELO FIORANTE

unemployment rates, rising interest rates and an unavoidable debt restructuring plan for servicing the cost of the bailouts received.

Table 1. Evolution of mortgage default rates

An additional threat is that house prices are said to be directionally led by mortgage lending. A drop in mortgage lending would essentially mean that property values would decrease as well. The bailout conditions of the debt crisis are forcing banks and other financial institutions to deleverage in order to reset their balance sheets back to sustainable levels that can be funded from customer deposits. Apprehension that house prices could plunge further as a result of the eurozone debt crisis is troubling. The worst-case scenario would be if people start falling into negative equity positions, i.e. when the market value of their asset falls below the outstanding balance of the loan. The US has been experiencing a wave of ‘strategic mortgage defaults’, whereby people deliberately stop paying their mortgages because they owe more money to the bank than their homes are worth. A credit crunch in the EU may delay recovery even more and households could find themselves backed into a corner with negative equity and no ability to honour their mortgage payments.

Conclusions

At present, a black cloud is still hanging over the euro area, where the debt crisis seems to be taking new proportions. Portugal has become the third eurozone state to seek an EU/IMF rescue, after Greece and Ireland. Spain seems to have dodged the bullet temporarily by announcing bold budget cuts along with an ambitious pension reform plan, but is still facing difficulties in the savings bank sector or cajas, which was severely hit by the Spanish property bust. Italy has so far avoided talking about the debt crisis even though it has clear weaknesses that could be penalised by the bond markets. It has the region’s weakest growth record, a huge public debt and very unstable politics. The concern that the economies of Spain and Italy, which are seen as too big to be bailed out and vital for the future of the European Union, might not manage to muddle through the economic downturn without receiving aid is reflected by the early-stage pressure brought by the EU, which has stressed that a significant restructuring scheme is needed to rectify the indebtedness and under-competitiveness of

Portugal 1.3 1.5 1.7 yesIreland 1.21 1.44 3.6 yes

Italy 1 1.4 na yesGreece 3.6 5.3 6.4 yesSpain 0.72 2.38 2.88 yes

Denmark 0.12 0.26 0.55 yesNetherlands na na na na

UK 1.88 2.42 2.45 yes

Default Rate 31.12.2007 (%)¹

Default Rate 31.12.2008 (%)

Default Rate 31.12.2009 (%)

Increase?

¹Default rates refer to the percentage of mortgage loans over 90 days in arrears in relation to

outstanding mortgage loans.

Source: Commission Staff Working Paper "National measures and practices to avoid foreclosure procedures for residential mortgage loans", SEC(2011)357 final.

A TORRENT OF MORTGAGE DEFAULTS: A POSSIBLE EFFECT OF THE EUROZONE DEBT CRISIS | 9

their economies. Meanwhile, households from the already bailed-out countries could find themselves in a similar situation as their governments and their financial institutions – insolvent – if appropriate measures are not taken to both resolve the sovereign debt crisis and protect borrowers’ ability to repay their loans.

One of the major challenges ahead for the credit industry is to abolish the unorthodox lending and borrowing practices that took place before the crisis, reinforce the underwriting standards for granting credit and establish a plan for a hypothetical worst-case scenario on how potentially bad loans should be treated without losing financial credibility. Action has already been taken by the European Commission, whose proposed directive on credit agreements relating to residential property (COM(2011) 142 final)2 aims at regulating the European mortgage credit industry through robust rules concerning advertising, pre-contractual information, advice, assessment of creditworthiness and early repayment rights.

Still, the probability that the European sovereign debt crisis could escalate into a mortgage debt crisis should not be entirely neglected, since the ability of households to repay loans has been aggravated by the crisis. It has pushed back living standards significantly for some of these nations’ households, and as their indebtedness reaches levels that might not be supported by the new and more stringent economic conditions that are taking shape, one might predict that defaults and foreclosures are going to continue rising.

2 European Commission, Proposal for a Directive of the European Parliament and of the Council on credit agreements relating to residential property, COM(2011) 142 final, Brussels, 31.3.2011 (http://ec.europa.eu/internal_market/finservices-retail/credit/mortgage_en.htm).

10 | ANGELO FIORANTE

European Credit Research Institute The EUROPEAN CREDIT RESEARCH INSTITUTE (ECRI) is an independent research institution devoted to the study of banking and credit. It focuses on institutional, economic and political aspects related to retail finance and credit reporting in Europe but also in non-European countries. ECRI provides expert analysis and academic research for a better understanding of the economic and social impact of credit. We monitor markets and regulatory changes as well as their impact on the national and international level. ECRI was founded in 1999 by the CENTRE FOR EUROPEAN POLICY STUDIES (CEPS) together with a consortium of European credit institutions. The institute is a legal entity of CEPS and receives funds from different sources. For further information, visit the website: www.ecri.eu.

ECRI Commentary Series ECRI Commentaries provide short analyses of ongoing developments with regard to credit markets in Europe. ECRI researchers as well as external experts contribute to the series. External experts are invited to suggest topics of interest for ECRI Commentaries.

ECRI Statistical Package Since 2003, ECRI has published a highly authoritative, widely cited and complete set of statistics on consumer credit in Europe. This valuable research tool allows users to make meaningful comparisons among all 27 EU member states and with a number of selected non-EU countries, including the US and Canada. For further information, visit the website: www.ecri.eu or contact [email protected].

The Author Angelo Fiorante is Research Assistant at the European Credit Research Institute of CEPS in Brussels. He holds an M.Sc. in Finance and a B.Sc. in Business Administration & Economics, both from the Stockholm University School of Business. At ECRI he follows the credit developments in Europe and is also in charge of collecting the statistics for ECRI’s flagship publication, the Statistical Package on consumer credit and lending to households.

European Credit Research Institute (ECRI)

Place du Congrés 1 B-1000 Brussels, Belgium

Tel.: +32-2-2293911 Fax: +32-2-2194151 Email: [email protected] Web: www.ecri.eu

Disclaimer: The European Credit Research Institute is a sub-institute of the Centre for European Policy Studies (CEPS). The views expressed in this commentary do not necessarily reflect those of ECRI or CEPS’ members.