and the eurozone crisis” - university of …mchinn/discussion_gourinchas_martin.pdf · “the...

TRANSCRIPT

Discussion of“The Economics of Sovereign Debt, Bailouts

and the Eurozone Crisis”by Pierre‐Olivier Gourinchas and Philippe Martin

Menzie ChinnUW Madison and NBER

West Coast WorkshopInternational Finance & Open Economy

MacroeconomicsSanta Cruz, CA, October 2, 2015

Outline

• Data• Model attributes/results• When does the model apply?• Authors’ conclusions• My questions

Are bad realizations possible?

-.30

-.25

-.20

-.15

-.10

-.05

.00

.05

.10

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

EuroArea 19

Germany

Italy

Log real GDP,2008Q1=0

Model attributes

• Calvo (1988)• Two periods, three countries (g, i, u)• Only uncertainty regards the endowment• Bonds motivated by bond‐in‐utility function; bonds yield money‐like utility services

• Contagion given by collateral cost on g, κ, implies soft budget constraint on i.

• Allowance for ex ante and ex post voluntary transfers gto i.

• Another source of uncertainty comes in π probability of transfers (π = 0 full discrection; π = 1 full commitment)

Results• Partial monetization of debt is possible both with and without a monetary union but in the first case the distortion generated by inflation is shared by all households in the monetary union

• Transfers in a monetary union cannot be ruled out ex‐post in order to avoid a costly default

• but ex‐post transfers are made “at minima”: i.e. they leave the indebted countries indifferent between a situation of default and no default.

• ex‐ante, the possibility of transfers influences debt rollover decisions (i.e. can lead to excessive debt issuance)

• allow for the possibility of reforms. But reforms are influenced by debt overhang problem.

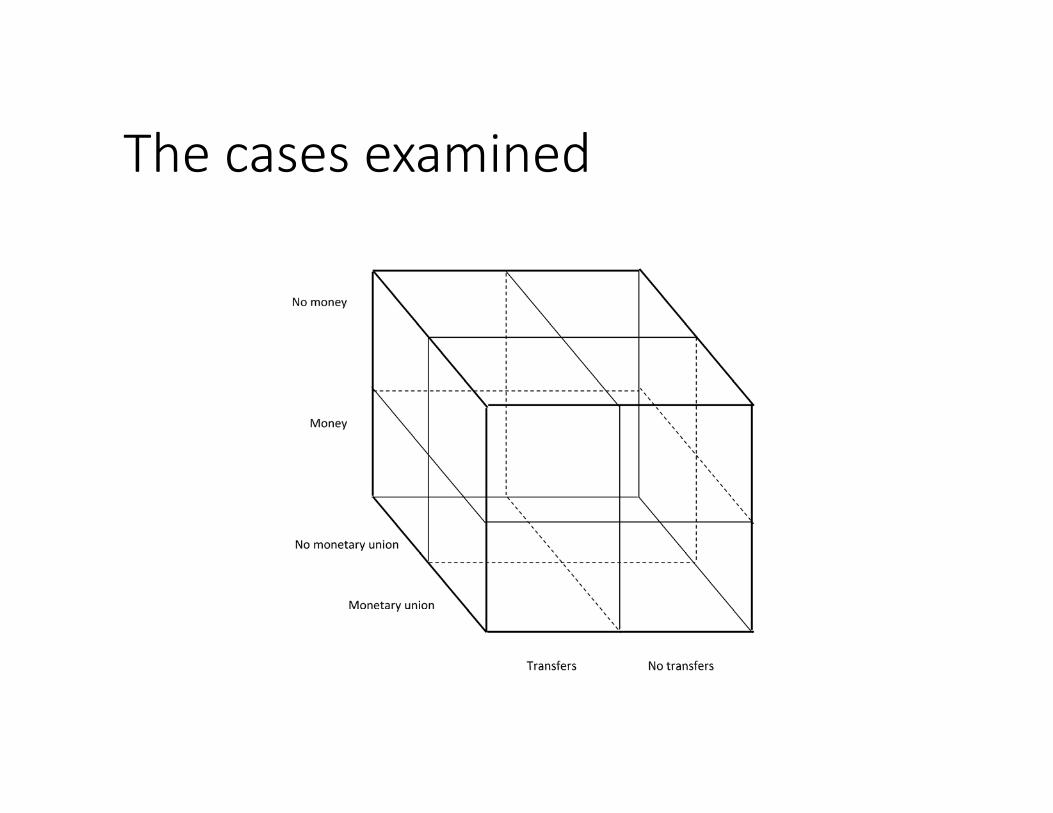

When does (each) model apply?

• The author’s examine cases distributed along several dimensions:

• No union/union• No transfers/transfers• Money/no money

The cases examined

Pre‐EMU

EMU, with price stability!

1999‐2007: price stability/no monetization likely

-.01

.00

.01

.02

.03

.04

.05

.06

96 98 00 02 04 06 08 10 12 14

Euroarea

Italy

Germany

Year-on-yearinflation

EMU, pre‐crisis

Or is this EMU, pre‐crisis?

The author’s conclusions?

• Technical conclusions already noted

• Is the German or Italian view (more) correct?

• Would it have been better to have united and dissolved than to have never united at all?

My questions (I)

• In the basic model (page 12), the authors conclude:

“It follows immediately that an ex‐ante no‐transfer commitment ‐ such as a no‐bailout clause‐ is not renegotiation proof and therefore will be difficult to enforce.”

Does this conclusion generalize to the other cases, and if so doesn’t this mean the entire EMU exercise was doomed to failure? The zero spreads are consistent with full discretion?Or is “no‐bailout” talk effective in increasing perceived π?

Sovereign yields and commitment

The disappearance of spreads

0

5

10

15

20

25

30

94 96 98 00 02 04 06 08 10 12 14

GermanyFrance

Greece

ItalySpain Portugal

Ireland

EMU Draghi

My questions (II)

• ECB monetization, page 29:

“[I]f the ECB decides to monetize the debt all the benefit is captured by g.”

If this is so, why does Germany object so vehemently?

Last thoughts

• A relatively realistic model; lots of institutional features injected

• The framework is clear, even if there are many cases to be worked out

• Some intriguing interpretations of past and current events

• I am curious to see how the authors come down on certain questions