a housing discussion a discussion, not a consultation a call for ideas and views discussion phase...

TRANSCRIPT

A Housing Discussion

• A discussion, not a consultation• A call for ideas and views• Discussion phase largely complete by end of

August, but….• …don’t wait until then to contribute• Join the discussion today, tomorrow and again

next week• Website will be regularly updated to reflect what

people are saying

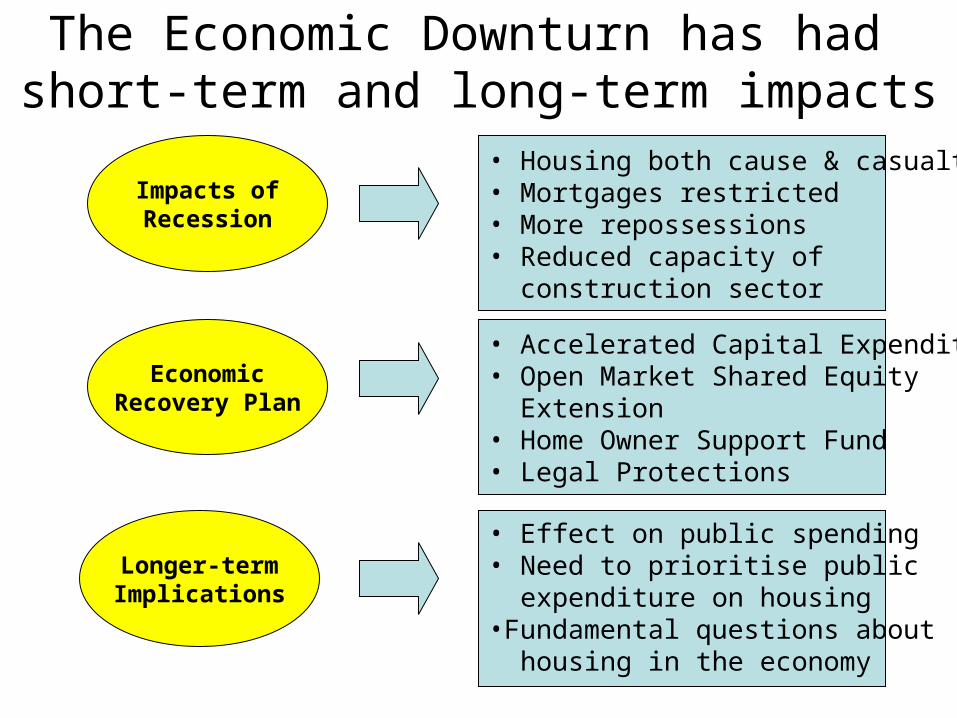

The Economic Downturn has had short-term and long-term impacts

• Housing both cause & casualty• Mortgages restricted• More repossessions• Reduced capacity of construction sector

Impacts ofRecession

EconomicRecovery Plan

• Accelerated Capital Expenditure• Open Market Shared Equity Extension• Home Owner Support Fund• Legal Protections

Longer-termImplications

• Effect on public spending• Need to prioritise public expenditure on housing•Fundamental questions about housing in the economy

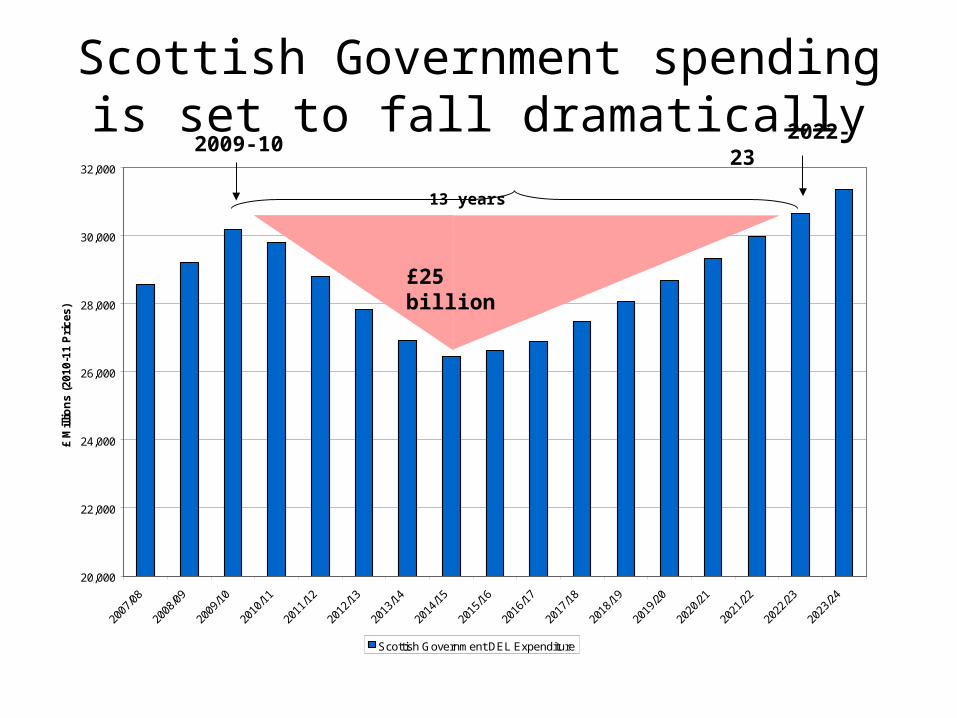

Scottish Government spending is set to fall dramatically

20,000

22,000

24,000

26,000

28,000

30,000

32,000

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12

2012

/13

2013

/14

2014

/15

2015

/16

2016

/17

2017

/18

2018

/19

2019

/20

2020

/21

2021

/22

2022

/23

2023

/24

£ M

illio

ns

(201

0-11

Pri

ces

)

Scottish Government DEL Expenditure

13 years

£25 billion

2009-10 2022-23

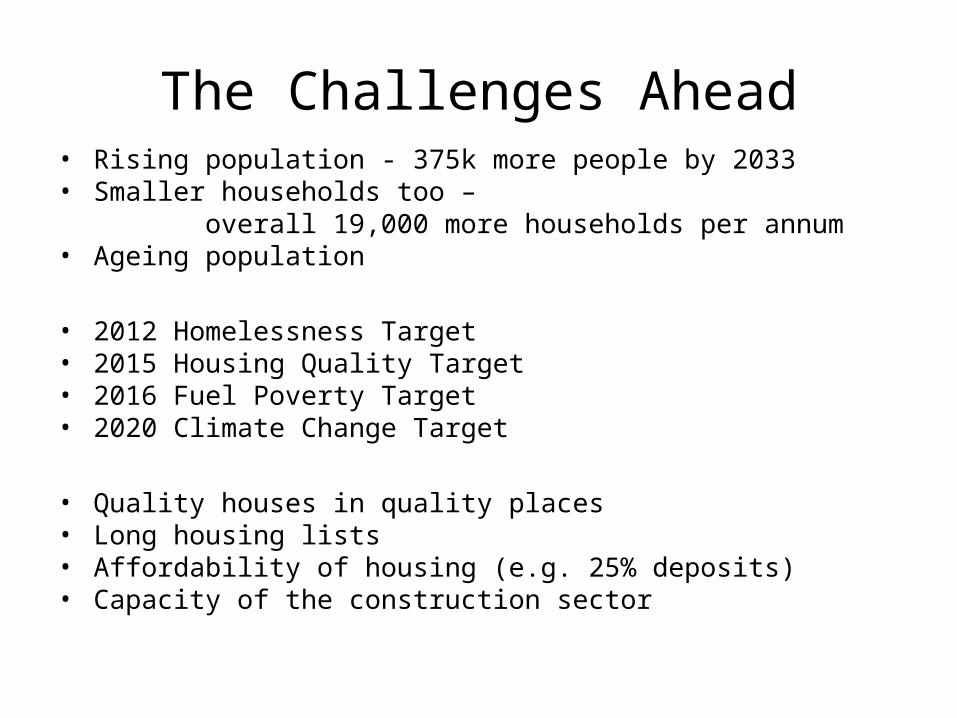

The Challenges Ahead• Rising population - 375k more people by 2033• Smaller households too –

overall 19,000 more households per annum• Ageing population

• 2012 Homelessness Target• 2015 Housing Quality Target• 2016 Fuel Poverty Target• 2020 Climate Change Target

• Quality houses in quality places• Long housing lists• Affordability of housing (e.g. 25% deposits)• Capacity of the construction sector

5 Key Themes for Discussion

Need

Affordable Supply

Housing Options

Quality and Place

Performance

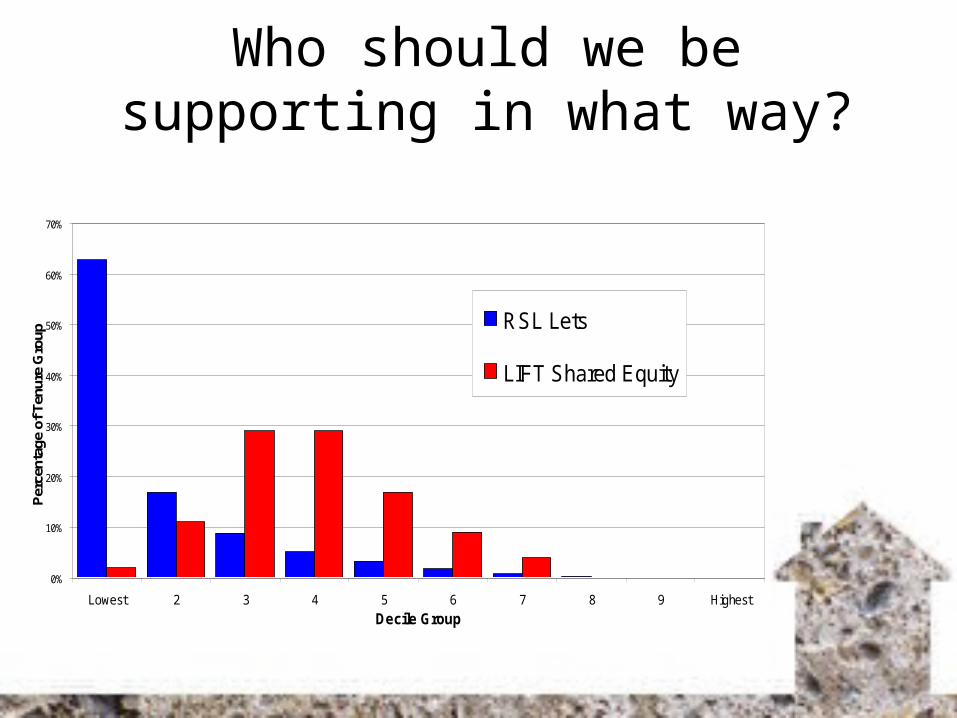

Who should we be supporting in what way?

0%

10%

20%

30%

40%

50%

60%

70%

Lowest 2 3 4 5 6 7 8 9 Highest

Decile Group

Per

cent

age

of T

enur

e G

roup

RSL Lets

LIFT Shared Equity

Where should we target our support?

A focus on regeneration, homelessness or affordability would lead to very different

regional priorities

Regeneration% of data zones in LA in SIMD

bottom 15%Homelessness

pressure to 2012 (Waugh model) AffordabilityLQ house prices to LQ income

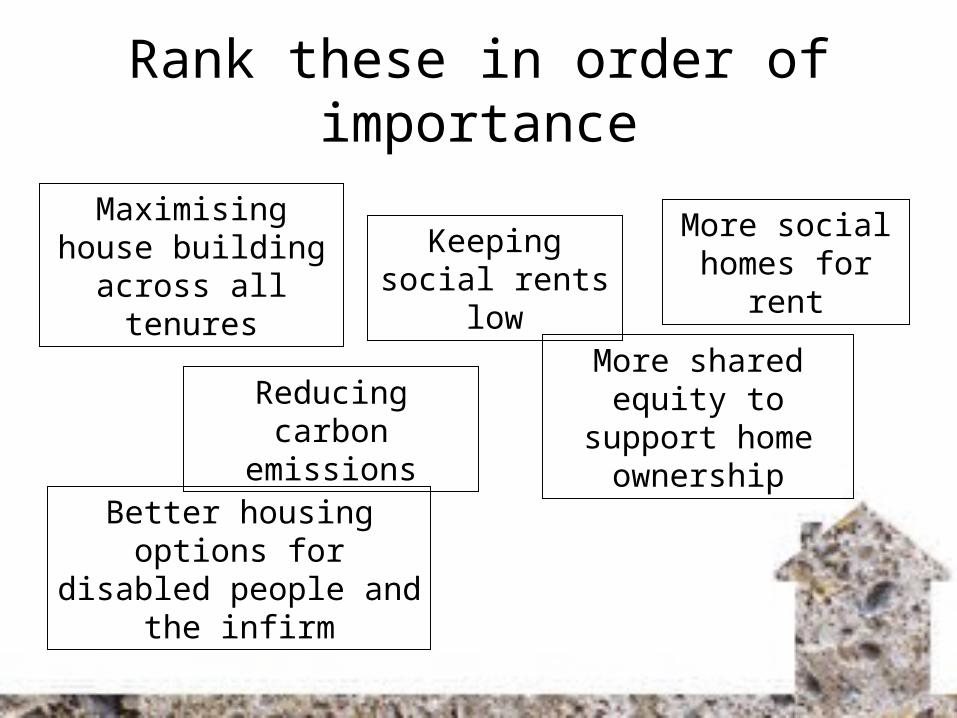

Rank these in order of importance

Maximising house building across all

tenures

More social homes for rent

More shared equity to support home

ownership

Better housing options for disabled people and the

infirm

Keeping social rents low

Reducing carbon emissions

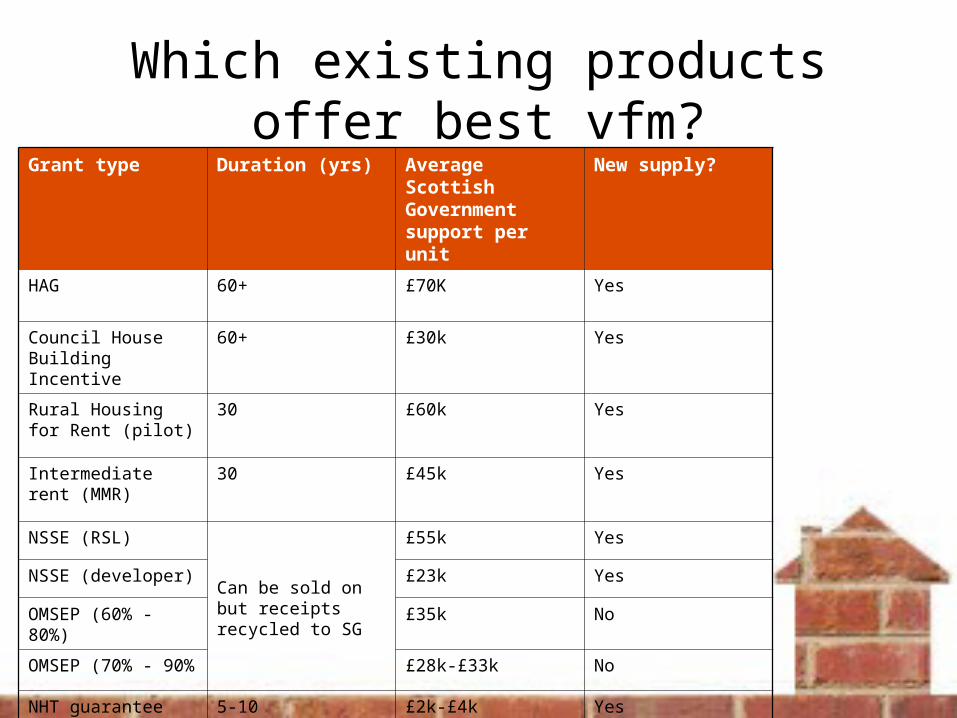

Which existing products offer best vfm?

Grant type Duration (yrs) Average Scottish Government support per unit

New supply?

HAG 60+ £70K Yes

Council House Building Incentive

60+ £30k Yes

Rural Housing for Rent (pilot)

30 £60k Yes

Intermediate rent (MMR)

30 £45k Yes

NSSE (RSL)

Can be sold on but receipts recycled to SG

£55k Yes

NSSE (developer) £23k Yes

OMSEP (60% - 80%) £35k No

OMSEP (70% - 90% £28k-£33k No

NHT guarantee 5-10 £2k-£4k Yes

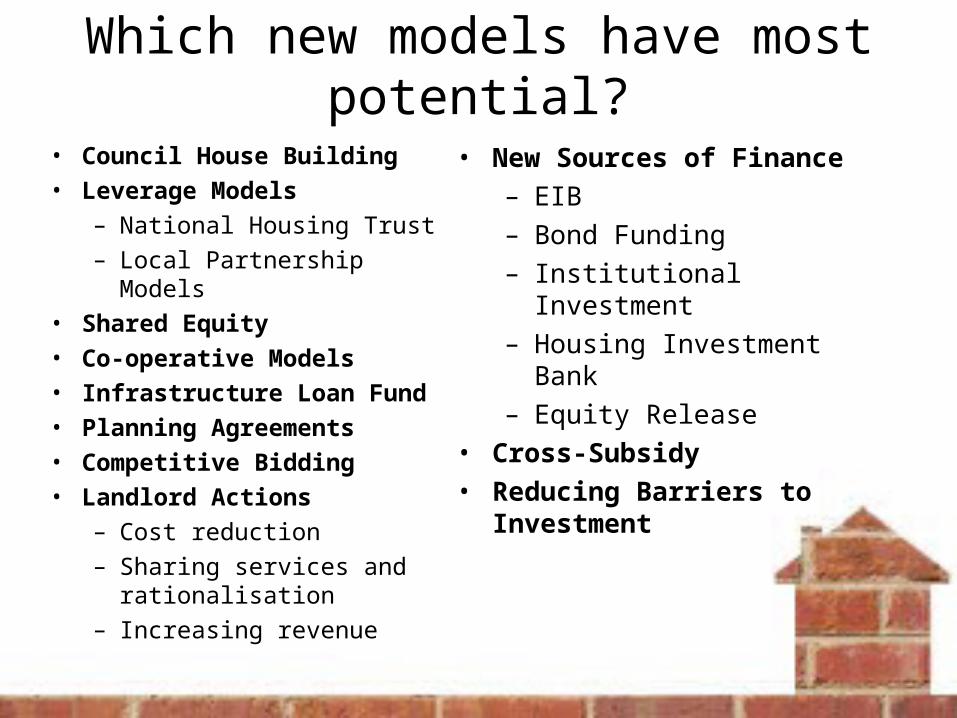

Which new models have most potential?

• Council House Building• Leverage Models

– National Housing Trust– Local Partnership Models

• Shared Equity• Co-operative Models• Infrastructure Loan Fund• Planning Agreements• Competitive Bidding• Landlord Actions

– Cost reduction– Sharing services and

rationalisation– Increasing revenue

• New Sources of Finance– EIB– Bond Funding– Institutional Investment– Housing Investment Bank– Equity Release

• Cross-Subsidy• Reducing Barriers to

Investment

Improving Choice: Housing Options

More housing products = more choice and complexity

Advisory/Options approach- Preventing homelessness (e.g. N Ayrshire)- Tackling housing lists (e.g. Perth and Kinross)- Reviewing housing circumstances

….and we need to continue to make progress on Common Housing Registers and improve the mobility/choice of social tenants……

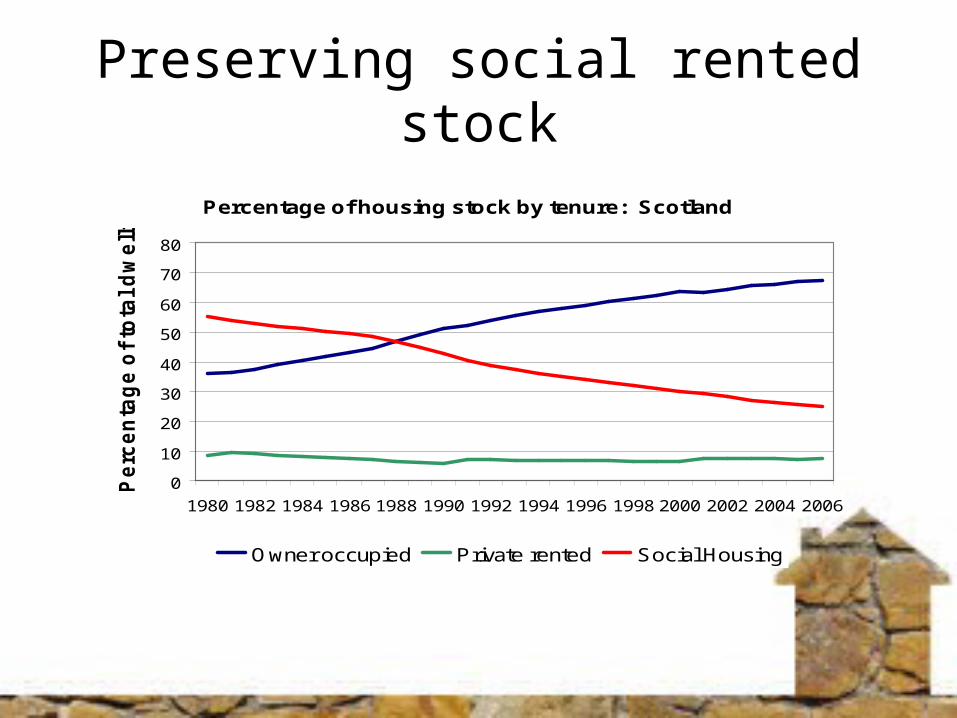

Preserving social rented stock

Percentage of housing stock by tenure: Scotland

0

10

20

30

40

50

60

70

80

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

Pe

rce

nta

ge

of

tota

l d

we

llin

gs

Owner occupied Private rented Social Housing

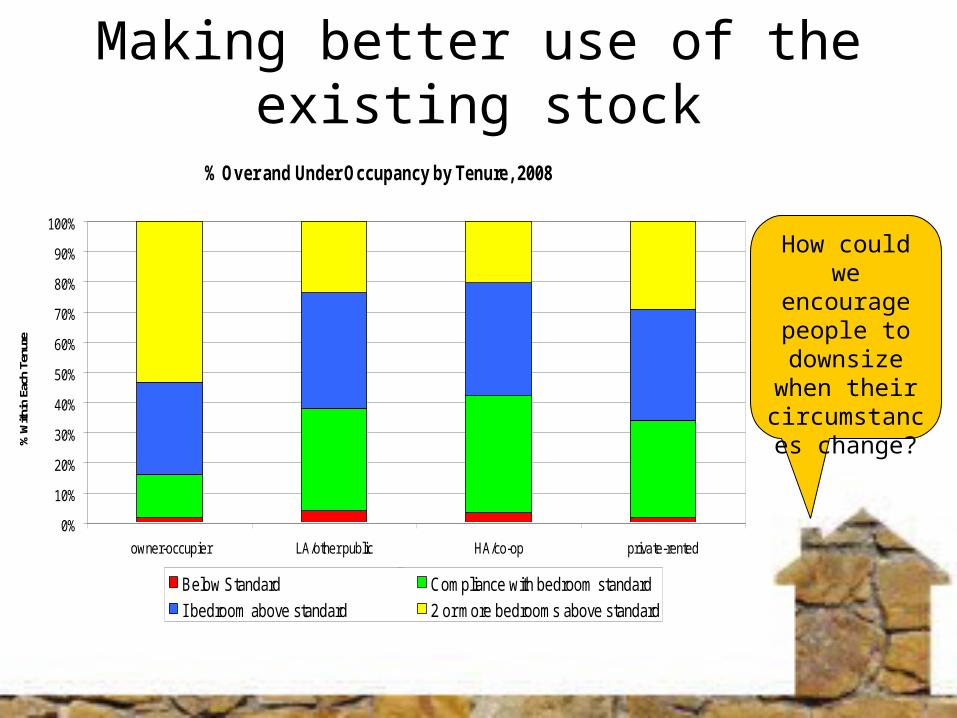

Making better use of the existing stock

How couldwe encourage

people to downsize when their

circumstances change?

% Over and Under Occupancy by Tenure, 2008

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

owner-occupier LA/other public HA/co-op private-rented

Tenure

% W

ithin

Eac

h Te

nure

Below Standard Compliance with bedroom standard

I bedroom above standard 2 or more bedrooms above standard

Housing and support for independent living

• How to plan for an 84% increase in people living beyond 75, by 2033?

• How to deliver better choice and fairer opportunities for disabled people?

• How to maintain and develop vital support, adaptations and care and repair services?

• Who pays?• What role for volunteers and social enterprises?• How to make public services work better

together?

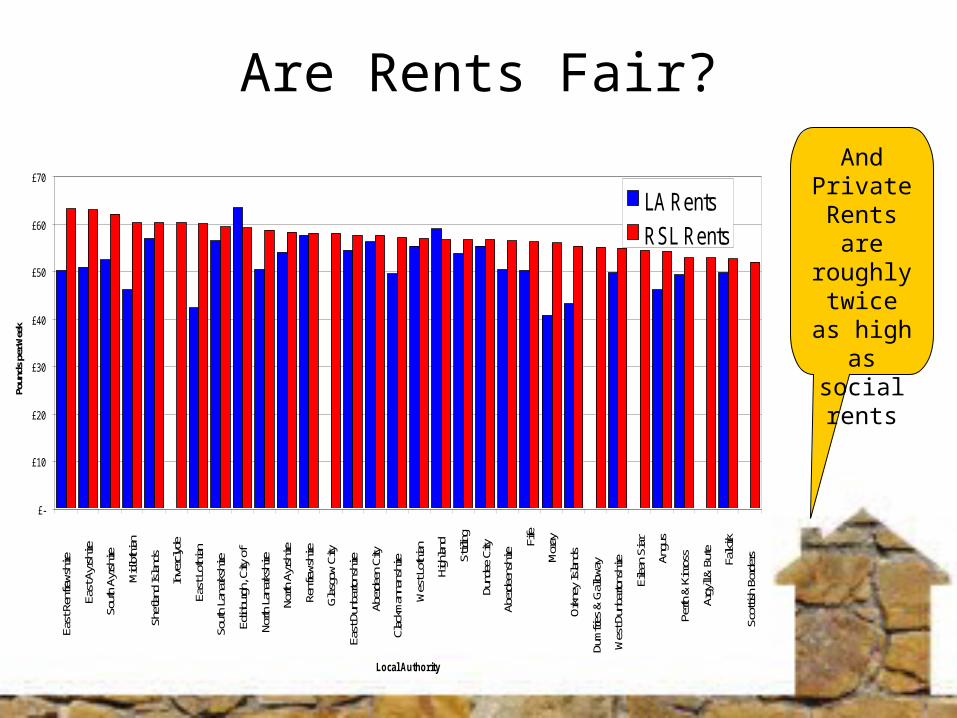

Are Rents Fair?And

Private Rents are roughly twice as high as social rents

£-

£10

£20

£30

£40

£50

£60

£70

East

Ren

frews

hire

East

Ayr

shire

Sout

h Ay

rshi

re

Midl

othia

n

Shet

land

Islan

ds

Inve

rclyd

e

East

Lot

hian

Sout

h La

nark

shire

Edin

burg

h, C

ity o

f

North

Lan

arks

hire

North

Ayr

shire

Renf

rews

hire

Gla

sgow

City

East

Dun

barto

nshi

re

Aber

deen

City

Clac

kman

nans

hire

Wes

t Lot

hian

High

land

Stirl

ing

Dund

ee C

ity

Aber

deen

shire

Fife

Mor

ay

Ork

ney

Isla

nds

Dum

fries

& G

allow

ay

Wes

t Dun

barto

nshi

re

Eilea

n Si

ar

Angu

s

Perth

& K

inros

s

Argy

ll & B

ute

Falki

rk

Scot

tish

Bord

ers

Local Authority

Poun

ds p

er W

eek

LA RentsRSL Rents

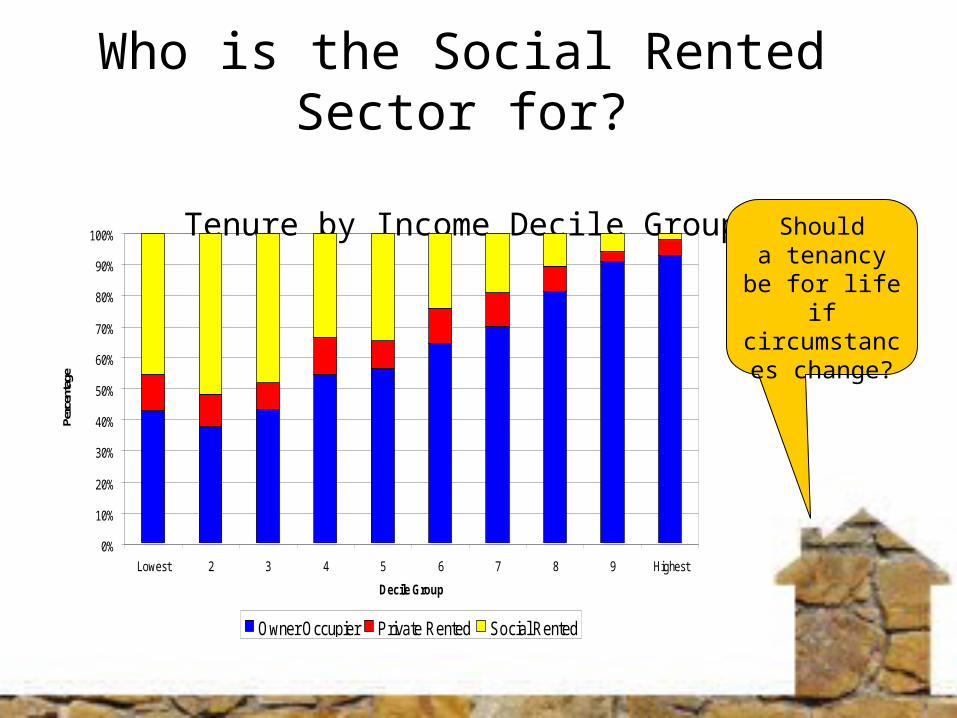

Who is the Social Rented Sector for?

Tenure by Income Decile GroupShould

a tenancybe for life if

circumstances change?

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Lowest 2 3 4 5 6 7 8 9 Highest

Decile Group

Perc

enta

ge

Owner Occupier Private Rented Social Rented

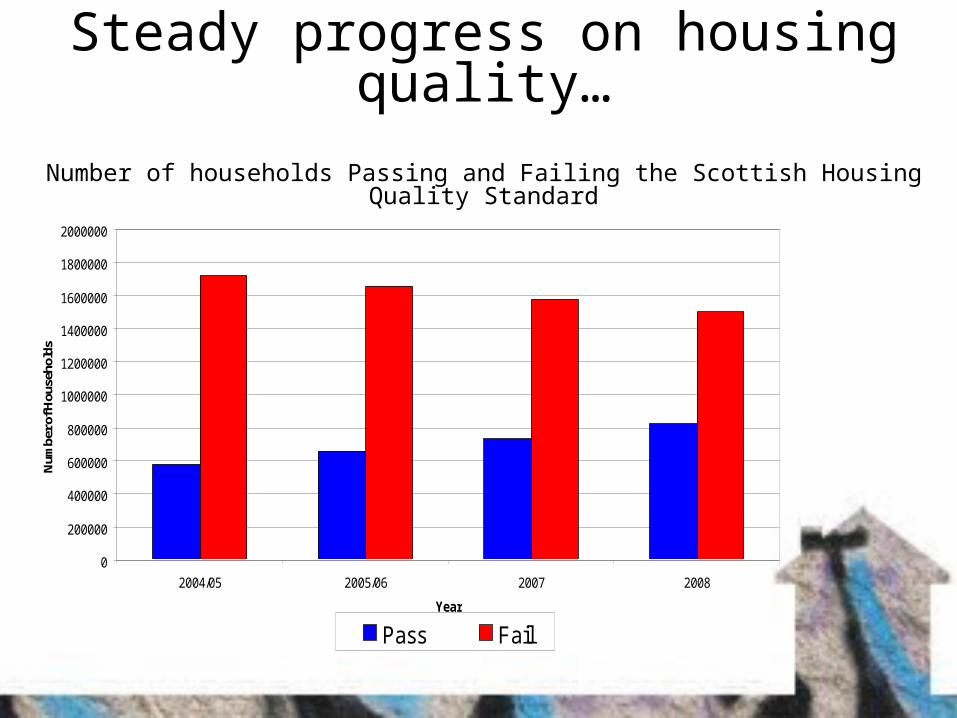

Steady progress on housing quality…

Number of households Passing and Failing the Scottish Housing Quality Standard

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2000000

2004/05 2005/06 2007 2008

Year

Num

ber o

f Hou

seho

lds

Pass Fail

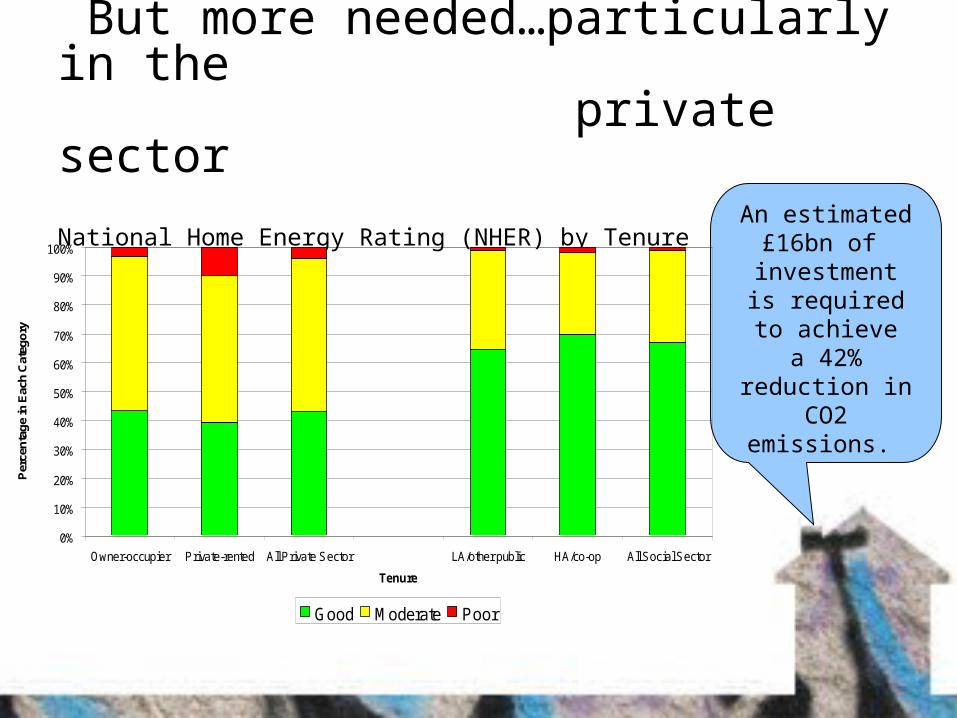

But more needed…particularly in the private sector

National Home Energy Rating (NHER) by Tenure An estimated£16bn of

investmentis requiredto achieve

a 42%reduction in

CO2 emissions.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Owner-occupier Private-rented All Private Sector LA/other public HA/co-op All Social Sector

Tenure

Per

cent

age

in E

ach

Cat

egor

y

Good Moderate Poor

Successful Places• Places for communities which will last• Good placemaking key to sustainable lifestyles

and good health• What have we learned about mixed-tenure

developments and good design?• As part of the Economic Recovery Plan, the

Government has acted to ease cashflow pressures on developers.

• How do we continue to develop and fund well-designed communities during the downturn?

Designing Streets – Polnoon ExemplarSuccessful Places: Polnoon Exemplar

What’s stopping more developments of this quality happening?

We all need to up our game and work together

• Government• Landlords (private and social)• Lenders• Institutional Investors• Developers• Households and individuals

……what would you do differently?

• Best way is on-line• You can post comments or tweet at any time• Or you can e-mail or write to us at:

Housing Policy Debate, Scottish Government,

1H Victoria Quay, Edinburgh, EH6 6QQ

How can I join in?