a brief overview of current research on dividends gretchen a. fix department of statistics rice...

TRANSCRIPT

A Brief Overview of Current Research on Dividends

Gretchen A. Fix

Department of Statistics

Rice University

8 October 2003

Why Study Dividends?

Dividends are the primary determinant of equity value Equity value: funds contributed by stockholders + retained earnings

A firm can do two things with its earnings: Pay them out to equity holders Reinvest in positive NPV projects

As a firm matures, growth opportunities will become limited, and it will not have the second option

The price of a stock is strong signal of expected future dividend payments

Overview

Four papers of interest “New Lists: Fundamentals and Survival Rates”

Fama and French (working paper)

“Disappearing Dividends: Changing Firm Characteristics or Lower Propensity to Pay?”

Fama and French (JFE)

“Dividends, Share Repurchases, and the Substitution Hypothesis” Grullon and Michaely (JoF)

“Are Dividends Disappearing? Dividend Concentration and the Consolidation of Earnings”

DeAngelo, DeAngelo, and Skinner (forthcoming JFE)

Overview

My (proposed) contributions What is survival analysis?

Why apply survival analysis to this question?

My hypothesis and plan of attack

“New Lists: Fundamentals and Survival Rates”Fama and FrenchCRSP Working Paper

1979 marks a jump in the rate at which new firms list on US exchanges pre 1979 160 per year post 1979 550 per year

Characteristics of new lists change Dist’n of profitability becomes more left skewed

Profitability measured as ratio of earnings (before interest) to assets, Et / At

Dist’n of growth becomes more right skewed Growth measured as scaled change in assets, (At – At-1) / At-1

“New Lists: Fundamentals and Survival Rates”Fama and FrenchCRSP Working Paper

Changing firm characteristics negatively impact new list survival 1973 firms

P(new list survives its first 10 yrs) = 61.0 % 1991 firms

P(new list survives its first 10 yrs) = 37.0%

“New Lists: Fundamentals and Survival Rates”Fama and FrenchCRSP Working Paper

Further analysis attributes decline in survival rates not to mergers, but to delistings caused by poor performance “more than two in five of the new lists of 1981-

1991 are delisted within ten years for poor performance”

“Disappearing Dividends: Changing Firm Characteristics or Lower Propensity to Pay?”Fama and FrenchJournal of Financial Economics, 60, 3 – 43

Dividends currently taxed at a higher rate than capital gains

Firms that pay dividends effectively have a higher cost of equity than those that don’t

“Disappearing Dividends: Changing Firm Characteristics or Lower Propensity to Pay?”Fama and FrenchJournal of Financial Economics, 60, 3 – 43

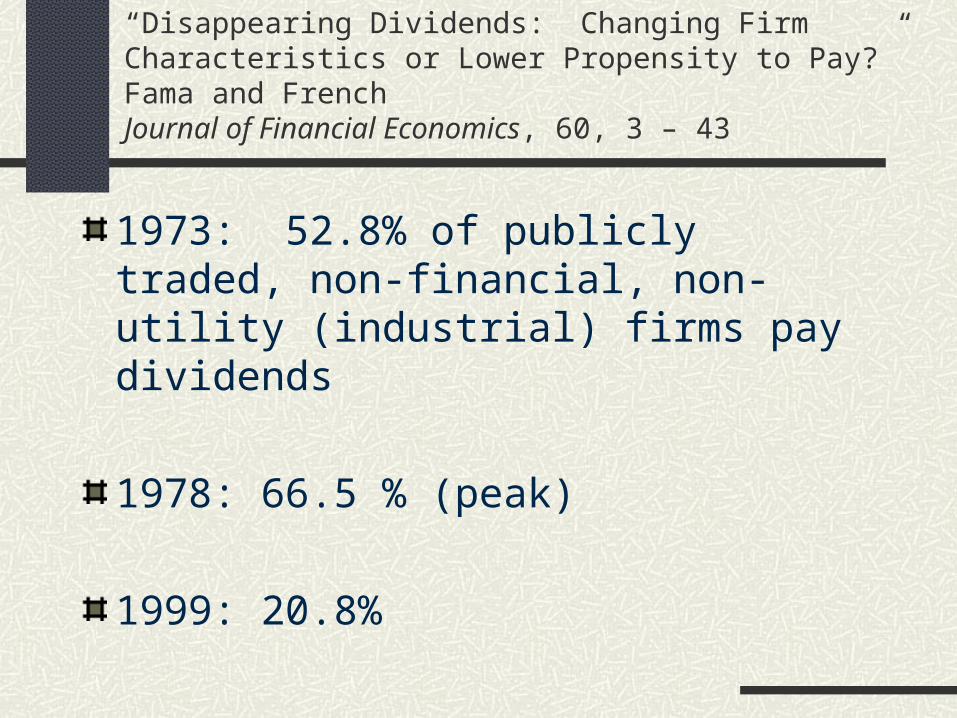

1973: 52.8% of publicly traded, non-financial, non-utility (industrial) firms pay dividends

1978: 66.5 % (peak)

1999: 20.8%

“Disappearing Dividends: Changing Firm Characteristics or Lower Propensity to Pay?”Fama and FrenchJournal of Financial Economics, 60, 3 – 43

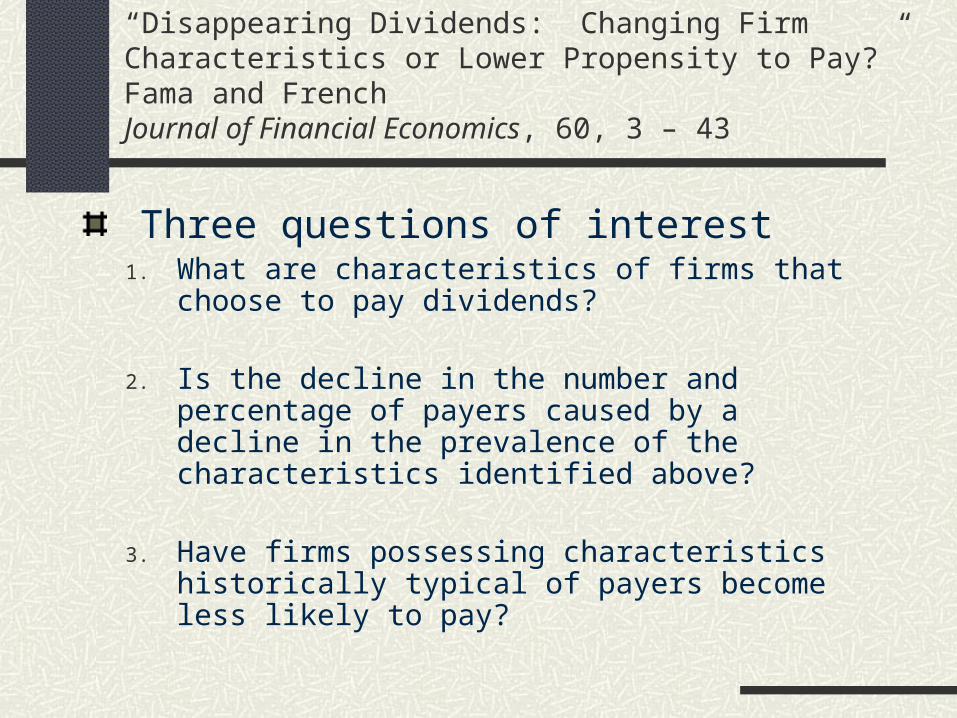

Three questions of interest1. What are characteristics of firms that choose to pay

dividends?

2. Is the decline in the number and percentage of payers caused by a decline in the prevalence of the characteristics identified above?

3. Have firms possessing characteristics historically typical of payers become less likely to pay?

“Disappearing Dividends: Changing Firm Characteristics or Lower Propensity to Pay?”Fama and FrenchJournal of Financial Economics, 60, 3 – 43

Answers1. Relevant characteristics: profitability,

investment (growth) opportunities, size Former payers: distressed Never payers: more profitable than former payers,

abundant investment opportunities Payers: more profitable than never payers, fewer

investment opportunities, large size

“Disappearing Dividends: Changing Firm Characteristics or Lower Propensity to Pay?”Fama and FrenchJournal of Financial Economics, 60, 3 – 43

Answers (cont’d)2. Surge of new lists (1979) floods market with

firms possessing characteristics of never payers Low profitability, strong growth, small size

“Disappearing Dividends: Changing Firm Characteristics or Lower Propensity to Pay?”Fama and FrenchJournal of Financial Economics, 60, 3 – 43

Answers (cont’d)3. Regardless of their characteristics, firms have

become less likely to pay dividends “Lower propensity to pay” Techniques used to establish lower propensity to

pay Logistic regression Portfolio approach

“Disappearing Dividends: Changing Firm Characteristics or Lower Propensity to Pay?”Fama and FrenchJournal of Financial Economics, 60, 3 – 43

Logistic regression approach 1963-1977 base period

Response variable equals 1 if firm pays dividends, 0 otherwise

Fit logistic regression model to base period data using size, profitability, and investment opportunities as independent variables

“Disappearing Dividends: Changing Firm Characteristics or Lower Propensity to Pay?”Fama and FrenchJournal of Financial Economics, 60, 3 – 43

Logistic regression approach (cont’d) Take ß vector from base period model and size, profitability,

and investment data from each year post 1977

For each year, estimate expected % of dividend payers

Variation in expected % of payers reflects changing characteristics of population of firms

Difference between expected % of payers and actual % of payers reflects “lower propensity to pay”

“Disappearing Dividends: Changing Firm Characteristics or Lower Propensity to Pay?”Fama and FrenchJournal of Financial Economics, 60, 3 – 43

Share repurchases Some claim that firms are now tending to

substitute share repurchases for dividends; thus, share repurchase activity could be the reason fewer firms are paying out dividends

Fama and French dismiss this--maintain that share repurchases are largely the domain of dividend paying firms

“Dividends, Share Repurchases, and the Substitution Hypothesis”Grullon and MichaelyJournal of Finance, 57 (4), 1649-1684

Despite the relative tax advantage of capital gains over ordinary income, US firms seemed to favor dividends over share repurchases when undertaking cash payouts

However, share repurchase activity has been on the rise over the past 20 years

1980-2000 share repurchase expenditures up 26.1%;dividends up 6.8% over same period

“Dividends, Share Repurchases, and the Substitution Hypothesis”Grullon and MichaelyJournal of Finance, 57 (4), 1649-1684

Three questions of interest1. Has there been a change in payout policy?

2. Are firms funding share repurchases with money they otherwise would have used for dividends?

3. If firms are substituting, why didn’t they start earlier?

“Dividends, Share Repurchases, and the Substitution Hypothesis”Grullon and MichaelyJournal of Finance, 57 (4), 1649-1684

Answers1. Since 1980s, more firms have opted to initiate

share repurchase activity than begin to pay dividends Percentage of firms that pay only dividends (of total

number of firms distributing cash to equity holders)

1972: 69% 2000: 20%

“Dividends, Share Repurchases, and the Substitution Hypothesis”Grullon and MichaelyJournal of Finance, 57 (4), 1649-1684

Answers (cont’d)2. Share repurchases are being funded by potential

increases in dividendsEspecially for large, established firms

Grullon and Michaely believe Fama and French use incorrect measure of share repurchases

Market reaction to announcement of dividend reduction significantly less negative for firms who engage in share repurchases; implies substitution effect

“Dividends, Share Repurchases, and the Substitution Hypothesis”Grullon and MichaelyJournal of Finance, 57 (4), 1649-1684

Answers (cont’d)3. Share repurchases increase after passage of

Rule 10b-18 in 1982 Prior to this, no definite rules set by the SEC to

regulate share repurchase activity

Repurchasing firms faced risk of SEC investigation

“Are Dividends Disappearing? Dividend Concentration and the Consolidation of Earnings”DeAngelo, DeAngelo, and SkinnerForthcoming--Journal of Financial Economics

Fama and French report a decrease in the number and percentage of industrial firms that pay dividends over the period 1978 – 1998

But, real and nominal dividends paid by industrial firms have increased over this period Reduction in number and percentage of payers comes mainly from

loss of small firms Largest payers have significantly increased dividends “increase in real dividends paid by firms at the top of the dividend

distribution swamps the dividend reduction associated with the loss of many small payers at the bottom”

“Are Dividends Disappearing? Dividend Concentration and the Consolidation of Earnings”DeAngelo, DeAngelo, and SkinnerForthcoming--Journal of Financial Economics

High and increasing concentration of the dividend supply 2000: 75 firms pay 75% of agg. industrial dividends

Increasing concentration of earnings 2000: 56 firms with over $500 million in earnings

responsible for: 86.2 % of aggregate industrial earnings 61.4 % of aggregate industrial dividends

“Are Dividends Disappearing? Dividend Concentration and the Consolidation of Earnings”DeAngelo, DeAngelo, and SkinnerForthcoming--Journal of Financial Economics

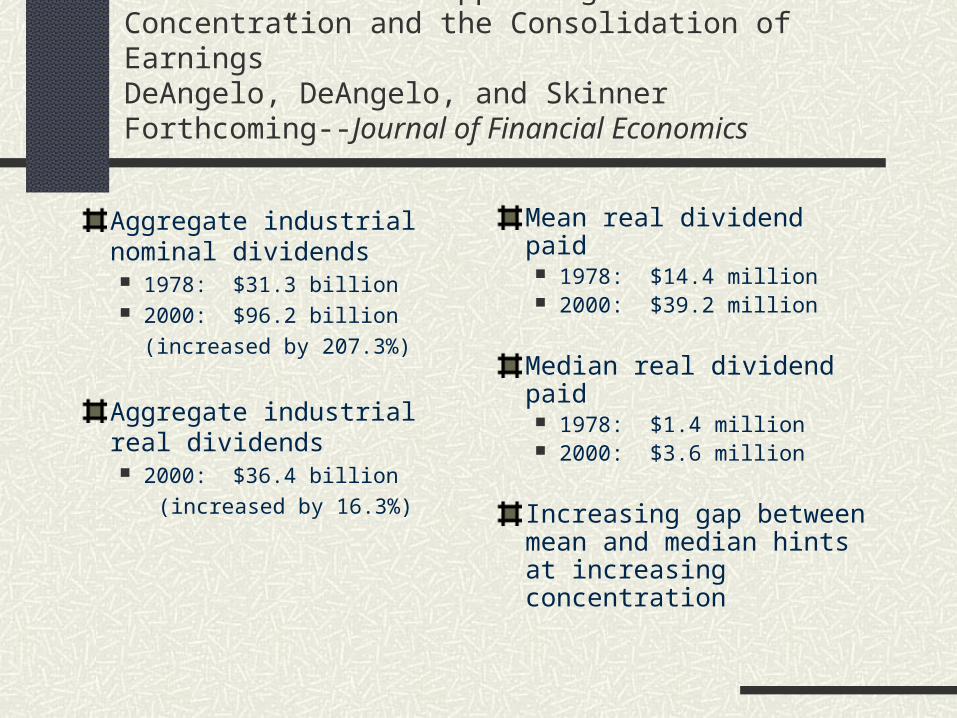

Aggregate industrial nominal dividends 1978: $31.3 billion 2000: $96.2 billion

(increased by 207.3%)

Aggregate industrial real dividends 2000: $36.4 billion

(increased by 16.3%)

Mean real dividend paid 1978: $14.4 million 2000: $39.2 million

Median real dividend paid 1978: $1.4 million 2000: $3.6 million

Increasing gap between mean and median hints at increasing concentration

What is Survival Analysis?

“a collection of statistical procedures for data analysis for which the outcome variable of interest is time until an event occurs” Kleinbaum, p. 4

Typical applications Biostatistics—study treatment effects in clinical

trials Industrial—study failure behavior of a machine

Functions of Interest in Survival Analysis

Survival/survivor function, S(t) Gives probability that a subject survives longer than

specified time t

S(t) = P(T > t) = 1 – P(T t) = 1 – F(t)

Properties Non increasing S(0) = 1; at the start of the study, all observations are alive S() = 0; if the study time were increased without limit,

eventually there would be no observations left alive

Functions of Interest in Survival Analysis

Hazard function, λ(t) λ(t) = limt0 P(t T < t + t | T t) / t

“Instantaneous potential per unit time for the event to occur, given that the individual has survived up to time t”

Conditional failure RATE (probability per unit time)

Typical Characteristic of Survival Analysis Data—Censoring

Exact survival time of a subject is unknown

Usually occurs at the right side of the follow-up period; but can have left or interval censoring

Typical reasons for right censoring:1. Subject does not experience the event before the study ends

2. Subject is lost to follow up during the study

3. Subject withdraws from the study

Why Apply Survival Analysis to this Question?

Outcome variable of interest = time to dividend initiation

Censoring present in data Some firms are yet to initiate dividends Some firms are lost during the study

Merge with other firms Go private Fail (go bankrupt)

My Hypothesis

Decision to initiate dividends depends in part on the age of the firm

Firm age should not be measured in terms of listing years, but instead should be measured from founding or incorporation

Market conditions of the 1980s and 1990s allowed firms to go public earlier in their lifecycles

My Hypothesis (cont’d)

Apparent decline in the propensity to pay is another example of the shift in population characteristics toward those of firms who have never paid dividends shift is toward younger, more immature firms

who have not yet reached the natural age of dividend initiation

Plan of Attack

Data: representative sample of 4711 firms Years of founding, incorporation, and listing for each

observation

Supplemental data from Compustat/CRSP Year of first dividend Annual data on market value, repurchase activity, earnings, etc.

Goal: fit Cox model with time-dependent covariates; include variable to pick up decreased propensity to pay; pray the variable is not significant

Challenges

Informed censoring Censoring mechanism assumed to be independent of failure

Probably not a valid assumption for firms that were censored due to bankruptcy

Probably valid for those that were merger targets

Left truncation Entry into the risk set at a time after 0

If time to dividends measured from incorporation, by our rules, the firm is not at risk to become a dividend payer until after it has listed