7.0 o bjective u nderstand ways to protect personal and family resources. 7.02 c-students will be...

TRANSCRIPT

7.0 OBJECTIVE UNDERSTAND WAYS TO PROTECT PERSONAL AND FAMILY RESOURCES.

7.02 C-students will be able to understand how to establish credit and maintain good credit

ESTABLISHING CREDIT

Creditors lend to people who can reasonably be expected to pay them back – all questions asked relate to “ability to repay”

Creditors look at credit-related information to determine if one is a good risk

A creditor’s evaluation of one’s ability and willingness to repay debts is a credit rating

ESTABLISHING CREDIT

Credit rating reflects the consumer’s credit history

Credit ratings are based on 3 Cs (review objective 6.03 housing options) Character---a person’s reputation for being honest

and their financial history Capacity---a person’s employment history and

ability to earn money Capital---a person’s financial worth

HOW TO ESTABLISH GOOD CREDIT

Take out a small, short term loan Make EVERY payment ON TIME! Pay off on time OR early Examples:

Low limit credit card – $500 MasterCard Car loan – may have to be co-signed by parent

Pay ALL your bills ON TIME! Rent to your landlord Premiums to your auto insurance Cell phone bill Utility bill Medical bills with doctor, hospital

CONSIDERATIONS WHEN SHOPPING FOR CREDIT Choosing the Right

Lender Annual fees to keep card Annual percentage rate

(APR)--- the amount whether it changes

Method used to calculate interest Previous balance Adjusted balance

Minimum payment amounts

Grace period Minimum finance

charge Any other fees

Cash advance Late fees

Credit limit Special features and

services Rebates, earning

points, free air miles

LOAN SOURCES Preferred lenders

Most reliable lenders Examples:

Banks Credit unions Savings & loan

associations Consumer finance

companies* May accommodate lower

credit rating for higher APR

Insurance policy loans Credit card companies Private loans**

Non-preferred lenders

May take advantage of people with poor credit; typically charge high interest rates

Examples: “payday” lenders Pawnbrokers loan sharks auto title loan lenders tax refund loan

*-usually higher interest rate**- if family, may cause tension

CREDIT DOCUMENT- THE CONTRACT

Credit contracts are legal binding documents that allow debtors to use credit to obtain goods and services.

READ the agreement BEFORE signing! Who is your best

advocate?

Know the content of the credit contract before signing such as: $ Amount of finance

charges Repairs covered Add-on features Reduction of finance

charge if contract paid in full prior to ending date

Receive a copy of the contract

Repossession conditions Know what you are signing!

JUMPSTART PRINCIPLE:

YOUR CREDIT PAST IS YOUR CREDIT FUTURE

What do you think this means?

PSA videos on http://www.ftc.gov/freereports PSA = Public Service Announcement

Go to http://www.ftc.gove/freereports Find information on how to obtain a credit report What are the 3 major credit reporting bureaus? What do they do?

Before approving loan, loan officer or underwriter will run credit report (credit check)

A credit report is like a report card of how people manage their credit

Report reflecting how well a person has used credit resources

Credit Reporting

Three national credit reporting agencies: Equifax Experian TransUnion

500- poor credit score 700+ good credit score

Provide information about employment history, credit accounts, balances, payment patterns

Consumers should check each of the three credit reports annually to verify accuracy

The Fair Credit Reporting Act---can get a free copy of credit reports every 12 months

The FTC site http://www.ftc.gov/freereports explains how to obtain the free reports

Credit Reporting

CAUTIONS WHEN SEEKING LOANS

Typically, must provide information related to ability to repay loan: Income Employment history Residence Credit history Savings

The lender will likely run a credit check (report).

If approved, borrowers may

have right to rescission (cancel) within three days if they choose; a provision of the Truth in Lending Act*

* How else does Truth In Lending Act protect consumers?

CAUTIONS WHEN SEEKING LOANS

Always “read the fine print” and know the terms of loans before signing watch for issues like balloon

payments

Consider if this would be wise or unwise use of credit

Remember that, once signed, borrowers are bound by the terms of the agreement

Consumers can apply for loans in person, online, over the telephone or in writing

WHAT DO YOU THINK?

How can having bad credit negatively affect a person?

If bills are not paid, what items can be repossessed?

If bills are not paid, what items can be foreclosed?

If bills are not paid, what items can be turned off?

http://whatsmyscore.org/contgest/videos.php

MAINTAINING GOOD CREDIT Evaluate the need to borrow

Can the purchase be avoided, delayed or bought on lay-away?

Identify and use the right type of credit for the intended purchase

Shop for the best terms Know how you will pay it back before you borrow Only use the amount of credit that you can afford to

repay Meet all the terms of credit contracts and agreements Keep accurate records of charges, statements, and

payments Consult creditors immediately if you cannot pay on time Resolve billing errors promptly

JUMPSTART PRINCIPLE:

Don’t borrow money that you can’t repay!

Create a tip sheet/brochure on: Credit card use Establishing and maintaining good credit Getting out of debt Knowing when and why to borrow

SIGNS OF A DEBT PROBLEM Consumers find

themselves stressed and constantly worrying over their finances

Having no savings Having reached the

credit limit on most of their credit cards

Skipping payments on some bills in order to pay others

Using cash advances on one credit card to pay another

Relying on credit cards to purchase day-to-day items like groceries and fast food

Relying on credit cards to pay monthly bills

Opening new credit card accounts in response to reaching the credit limit on others

Regularly receiving contacts from creditors/collection agencies trying to collect unpaid debts

video link: signs of debt problems

STRATEGIES FOR GETTING OUT OF DEBT

Actively deal with the problem; ignoring it will only make it worse

Get help from trained people---a credit counselor or credit counseling service

Develop a spending plan that includes living expenses and debt repayment funds

Learn to live within your budget!

Stop using credit; focus on repaying the debt owed

Contact creditors immediately, let them know your situation, ask to have credit terms adjusted

Get credit card with “teaser” rate

Pay bills automatically through EFTs!

Spend smarter!

video link: tips for getting out of debt

video link: credit counseling

BANKRUPTCY…A LAST RESORT

Legal relief or forgiveness from repaying certain debts

Try to deal with debts using ALL MEANS available before filing for bankruptcy

Bankruptcy carries serious, long-term consequences---part of one’s credit report for ten years! Chapter 7---must sell certain personal belongings, use

proceeds to repay debts Chapter 13---can retain most personal property, but

must propose a repayment plan, go to credit counseling, receive financial management education, and be employed

video link: when to file bankruptcy

BANKRUPTCY EXCLUSIONS

No Bankruptcy Forgiveness for: Taxes owed including fines & penalties Court ordered debt

Alimony Child support Liability from lawsuits

College loans

video link: filing personal bankruptcy

21

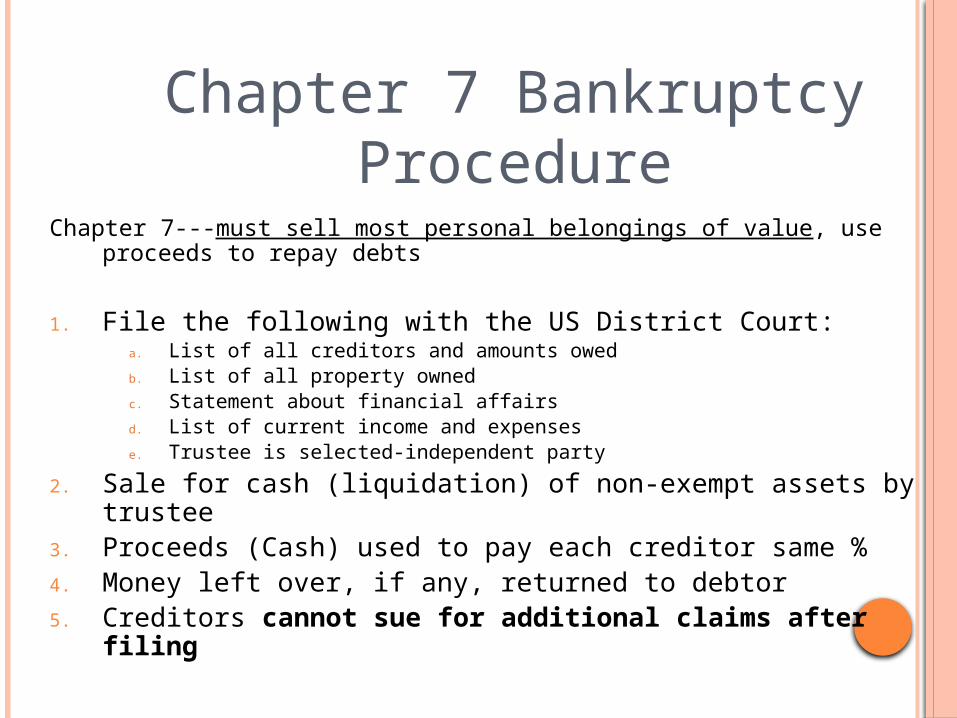

Chapter 7---must sell most personal belongings of value, use proceeds to repay debts

1. File the following with the US District Court:a. List of all creditors and amounts owedb. List of all property ownedc. Statement about financial affairsd. List of current income and expensese. Trustee is selected-independent party

2. Sale for cash (liquidation) of non-exempt assets by trustee3. Proceeds (Cash) used to pay each creditor same % 4. Money left over, if any, returned to debtor5. Creditors cannot sue for additional claims after filing

Chapter 7 Bankruptcy Procedure

22

CHAPTER 7: PROPERTY- EXEMPT & NON-EXEMPT

Exempt Property – can keep Up to $7500 equity in home Up to $1200 in vehicle Up to $500 in jewelry Up to $750 in tools of trade Up to $200 per item of household goods, max $4000 Rights to social security benefits All amounts in excess, subject to sale for cash

Nonexempt property- cannot keepeverything else included in liquidation and distribution to

creditors, examples: Bank Accounts Stocks Bonds

23

Extended Time Payment Plan or Reorganization Applies to individuals with regular income

(currently working) Trustee handles future earnings of debtor Trustee handles payment of bills Unsecured debts less than $250,000 and/or secured debts

of less than $750,000 Submit reasonable plan for repayment of debts within

three years May be extended to five years

CHAPTER 13 BANKRUPTCY

PRINCIPLES OF FINANCIAL PLANNINGFROM THE JUMP$TART COALITION

Map your financial future Money doubles by the “Rule of 72” Your credit past is your credit future Start saving young Stay insured Budget your money Don’t borrow what you can’t repay Don’t expect something for nothing High returns equal high risks Know your take-home pay Compare interest rates Pay yourself first

http://www.jumpstartcoalition.org/files2010/2010_J$_Calendar.pdf