5 th meeting of intosai knowledge sharing steering committee new delhi, 16 and 17 september 2013...

TRANSCRIPT

5th meeting of INTOSAI Knowledge Sharing Steering Committee

New Delhi, 16 and 17 September 2013

Progress report of INTOSAI Working Group Accountability for and Audit of Disaster-related Aid WG

AADAGijs de Vries

Chairman WG AADA,

Member, European Court of Auditors

INTOSAI Working Group AADA – Why?

2

2007 Mexico INCOSAI created Working Group – 23 members

•Solution to observed inadequacy of transparency and accountability arrangements•Guidance and good practice for SAIs auditing disaster-related aid

2010 South Africa INCOSAI encouraged Working Group to broaden the IFAF to cover all of humanitarian aid and to finalise the guidance and good practice

Present output to 2013 China INCOSAI:

•INTOSAI GOV 9250 on the IFAF•5500 series - 5 ISSAIs on auditing disaster-related aid

INTOSAI Working Group AADA – Why?

3

Since last KSC meeting:

•October 2012: 5 ISSAIs published as exposure drafts

•January 2013: ISSAIs modified to take account of

comments received from several SAIs but also many

international organisations such as UN organisations

(UN OCHA, UNDP, UNODC), World Bank, OECD, GHD,

European Commission and NGOs

•January 2013: INTOSAI GOV 9250 on IFAF published

as exposure draft

INTOSAI Working Group AADA – Why?

4

• April 2013: INTOSAI GOV modified to take account

of 30 sets of comments from international

organisations - UNDP, UNISDR, UNOIOS, World Bank,

European Commission, RIAS, HAP, IATI, NGOs, many

SAIs

• May and June 2013: adoption of final versions for

endorsement of ISSAIs and GOV by WG AADA

• June-Aug 2013: translation of endorsement

versions into French, German, Spanish and Arabic

INTOSAI Working Group AADA – Why?

5

• July 2013: adoption of endorsement versions of

ISSAIs and GOV by KSC and approval of GOV by the

PSC Subcommittee on Accounting and Reporting

• until Sept 2013: contacts with IDI on how to

promote training on the ISSAIs in the 5500 series

(training capacity and funding) and agreement to

include this issue in an upcoming IDI survey

INTOSAI Working Group AADA – Why?

6

The 5500 series of ISSAIs on auditing disaster-related aid is structured as follows:

Lead SAI

5500

Introduction to the 5500 series of ISSAIs and INTOSAI GOV 9250

ECA

5510

Audit of disaster risk reduction Turkey

5520

Audit of disaster-related aid Indonesia

5530

Adapting audit procedures to take account of the increased risk of fraud and corruption in the emergency phase following a disaster

ECA

5540

Geospatial information in auditing disaster management and disaster-related aid

Netherlands

INTOSAI Working Group AADA – Why?

Positive feedback on ISSAIs:

• ‘…drafts are extremely thorough and will be of great use to supreme audit institutions…’ - United Nations Office for the Coordination of Humanitarian Affairs (OCHA)•‘…drafts provide clarity on the auditors’ responsibility to highlight gaps in government disaster policy and action, and this is particularly welcome. Improving government performance in this area could be instrumental in saving lives and reducing economic losses from disaster.’ - OECD Development Assistance Committee•‘…documents are well written, structured to provide good understanding with many examples from real life, and lists of red flags for reference by SAI auditors…the result of multiple source input, good research and consultation.’ -Transparency International•‘All 5 guidelines are clear and comprehensive. When implemented these guidelines will help to promote more effective, accountable and transparent aid delivery to affected communities - Humanitarian Accountability Partnership (HAP)

7

INTOSAI Working Group AADA – Why?

8

INTOSAI GOV 9250: lead SAI ECA

«The Integrated Financial Accountability Framework (IFAF)»

Primarily directed at entities involved in providing and receiving humanitarian aid. Includes guidance and examples of how to prepare financial information and make it available as open data

INTOSAI Working Group AADA – Why?

Positive feedback on GOV:

•‘…will be a powerful mechanism to strengthen transparency and accountability.’ - World Bank•’IFAF is an important tool for enhancing accountability. DG ECHO looks forward to following them and promoting them within its partners’ community’ - European Commission•‘…recognises the value of IFAF. It provides audited ex-post final open data for a pre-defined financial period using simple, standardised tables.’ – United Nations Office for Internal Oversight Services•‘…appreciates the time and effort spent to achieve this high quality product…’ – United Nations Development Programme•‘…invaluable work: IFAF implementation will bring benefits to both donors and recipients of humanitarian aid…’ – United Nations International Strategy for Disaster Reduction•’…applauds the intent to achieve consistency, eliminate duplication and reduce costs.’ – Catholic Relief Services

9

INTOSAI Working Group AADA – Why?

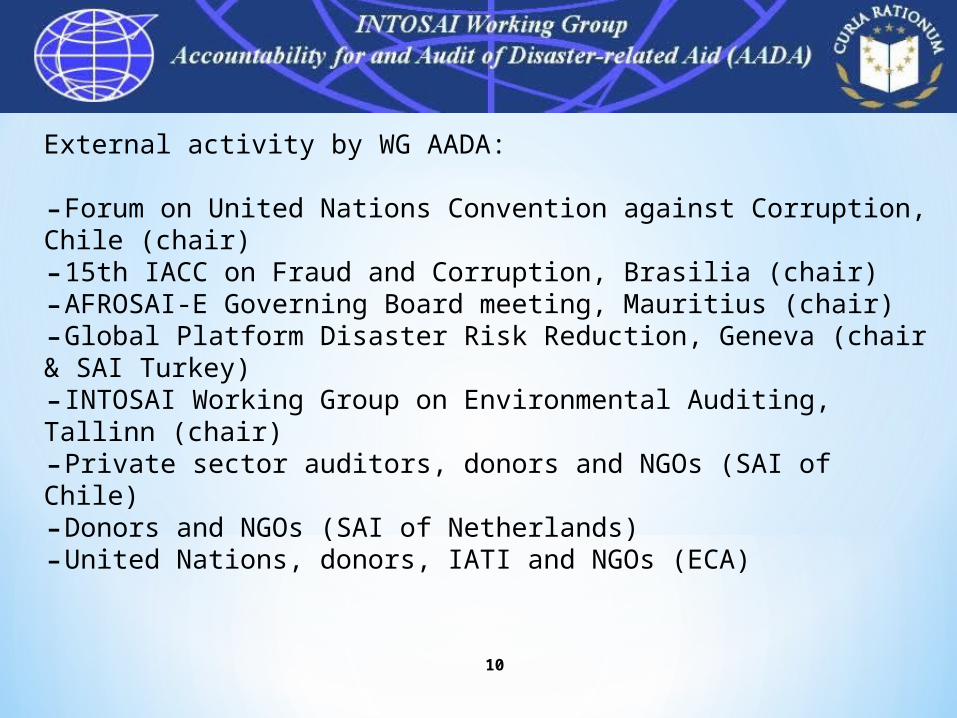

External activity by WG AADA:

-Forum on United Nations Convention against Corruption, Chile (chair)-15th IACC on Fraud and Corruption, Brasilia (chair)-AFROSAI-E Governing Board meeting, Mauritius (chair)-Global Platform Disaster Risk Reduction, Geneva (chair & SAI Turkey)-INTOSAI Working Group on Environmental Auditing, Tallinn (chair)-Private sector auditors, donors and NGOs (SAI of Chile)-Donors and NGOs (SAI of Netherlands)-United Nations, donors, IATI and NGOs (ECA)

10

INTOSAI Working Group AADA – Why?

Next steps

•Presentation to Governing Board in China

•Final endorsement by INCOSAI in China

•Dissolution of Working Group AADA

•Publication as ISSAIs and GOV on PSC website

•Use of ISSAIs by auditors and for training

•Possibly (upon request by SAIs) guidance for auditing

IFAF tables

•Review and update in time for INCOSAI 201911

12

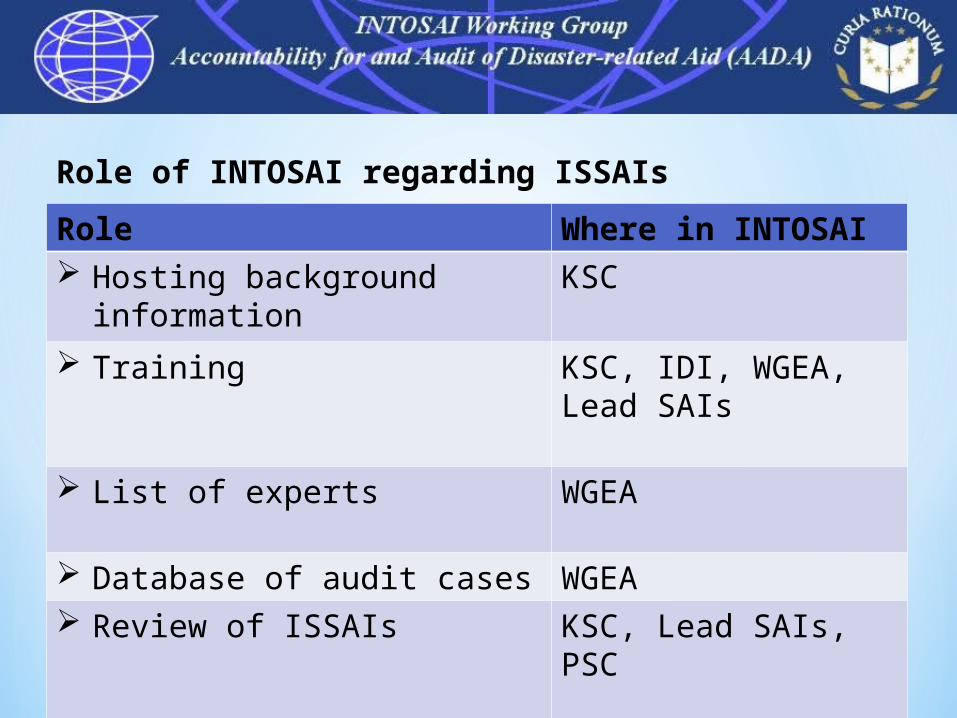

Role of INTOSAI regarding ISSAIs

INTOSAI Working Group AADA – Why?

Role Where in INTOSAI Hosting background

informationKSC

Training KSC, IDI, WGEA, Lead SAIs

List of experts WGEA

Database of audit cases WGEA Review of ISSAIs KSC, Lead SAIs, PSC

13

Role of INTOSAI regarding GOV

INTOSAI Working Group AADA – Why?

Role Where in INTOSAI Hosting background

information/FAQKSC

Providing contacts (postbox function)

IATI and KSC

Providing forum for IFAF users

IATI (technical), back up KSC (contents)

Review of GOV KSC, lead SAIs, PSC

14

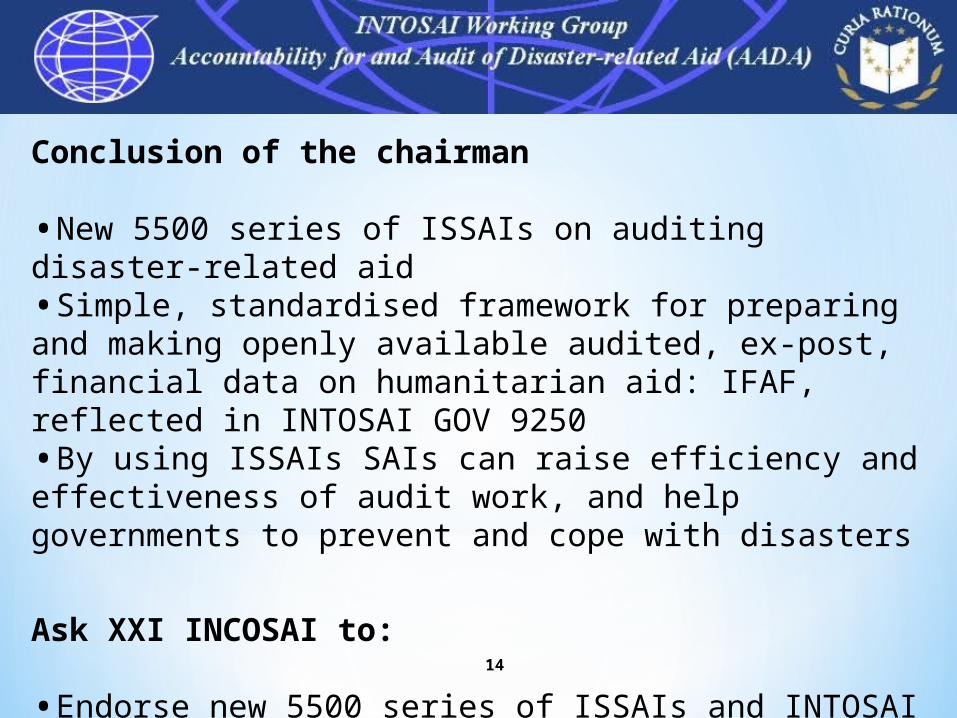

Conclusion of the chairman

•New 5500 series of ISSAIs on auditing disaster-related aid•Simple, standardised framework for preparing and making openly available audited, ex-post, financial data on humanitarian aid: IFAF, reflected in INTOSAI GOV 9250•By using ISSAIs SAIs can raise efficiency and effectiveness of audit work, and help governments to prevent and cope with disasters

Ask XXI INCOSAI to:

•Endorse new 5500 series of ISSAIs and INTOSAI GOV 9250, •Take note of Final Report of the Working Group, and •Disband the Working Group AADA

INTOSAI Working Group AADA – Why?

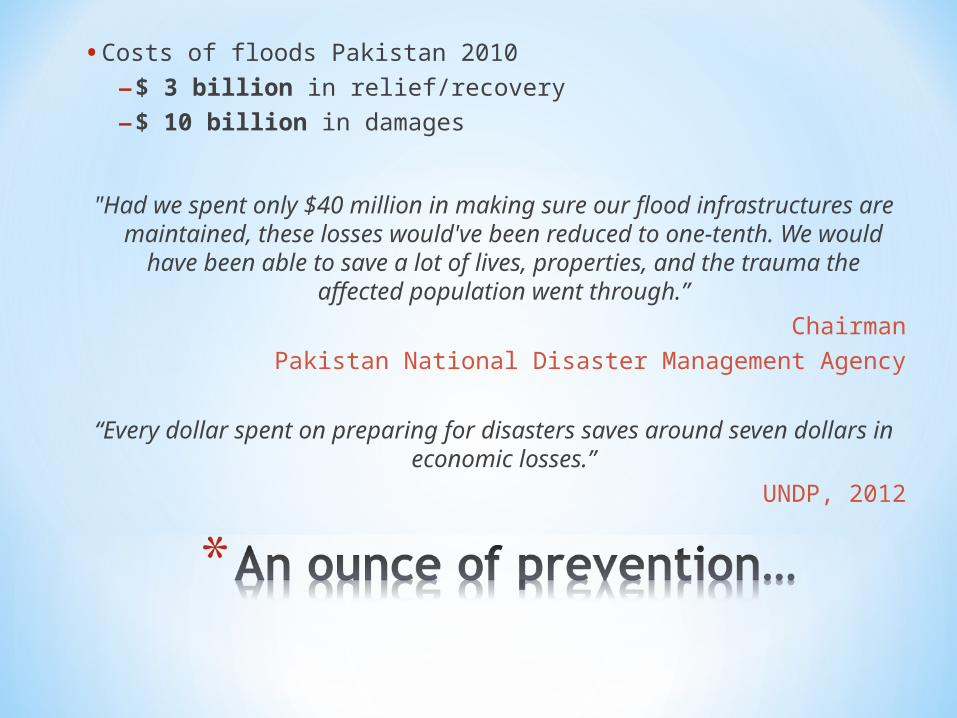

• Costs of floods Pakistan 2010

–$ 3 billion in relief/recovery

–$ 10 billion in damages

"Had we spent only $40 million in making sure our flood infrastructures are maintained, these losses would've been

reduced to one-tenth. We would have been able to save a lot of lives, properties, and the trauma the affected population went

through.”Chairman

Pakistan National Disaster Management Agency

“Every dollar spent on preparing for disasters saves around seven dollars in economic losses.”

UNDP, 2012

INTOSAI Working Group AADA – Why?

More information on the Working Group available at:

http://eca.europa.eu/intosai-aada