37 th conference of the directors of paying agencies riga, 6-8 may 2015 christina borchmann director...

TRANSCRIPT

37th Conference of the Directors of Paying Agencies

Riga, 6-8 May 2015

Christina BorchmannDirector

Directorate J: Audit of Agricultural ExpenditureDirectorate General for Agriculture & Rural Development

Annual Activity Report for 2014

Adjusted Error Rate

Market Intervention 3.87%

Direct Payments 2.54%EAGF 2.61%EAFRD 5.09%IPARD 3.19%CAP 3.10%

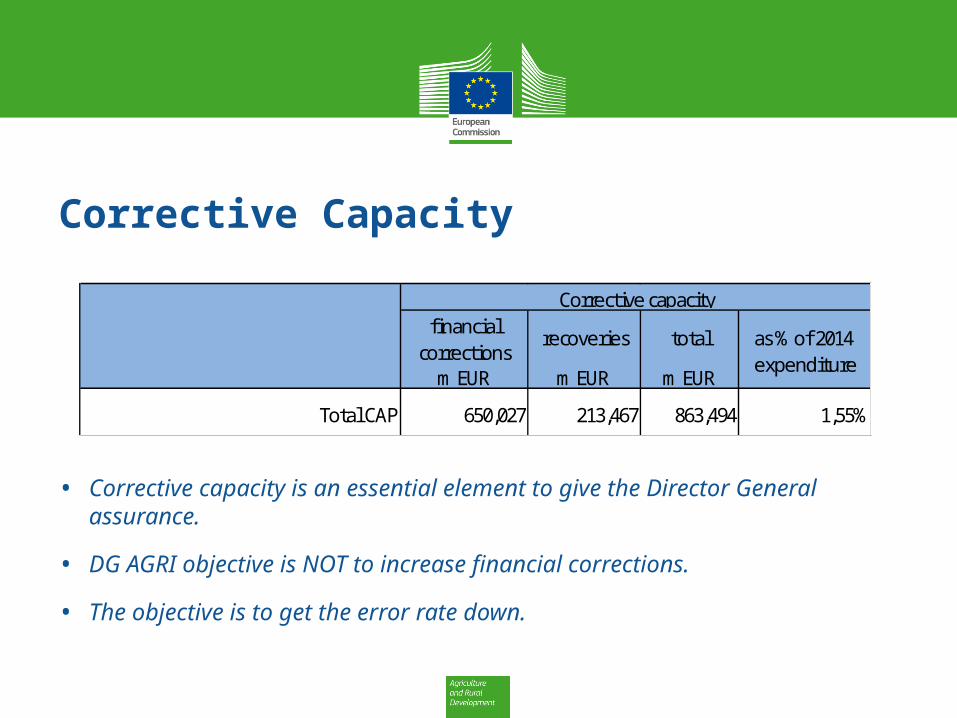

Corrective Capacity

• Corrective capacity is an essential element to give the Director General assurance.

• DG AGRI objective is NOT to increase financial corrections.

• The objective is to get the error rate down.

financial corrections

recoveries total

m EUR m EUR m EUR

Total CAP 650,027 213,467 863,494 1,55%

Corrective capacity

as % of 2014 expenditure

Reservation methodology

• Reservation necessary if error rate above 5% - unless amount at risk is below de minimis.

• Reservation necessary if error rate between 2 and 5% unless de minimis or mitigating factors apply:

• Deficiencies remedied,• 2014 expenditure covered by conformity clearance procedure

• No reservation if error rate for 2014 is below 2%.

• Where the amount of EU expenditure at risk is below the 1 million EUR de minimis threshold established in DG AGRI's materiality criteria, no reservation applies.

2014 financial clearance

• 30/04/2015: 81 letters to Paying Agencies

• 5 disjoined accounts for EAGF

• 7 disjoined accounts for EAFRD

• Reasons:• Late submission of accounts and of additional work

requested• Material error • Qualification of accounts by CB

Certification Bodies – Legality & Regularity

• 15 dedicated missions by DG AGRI

• Combination audits: include in the control sample some of the Certification Body checks carried out as well as those carried out by the Paying Agency.

Conformity Clearance – new deadlines

• Reg. 908/2014 includes a number of new mandatory legal deadlines for the Commission and for the MS at each stage of the procedure;

• Commission will need to apply the Regulation strictly to be able to meet the legal deadlines;

• A monitoring system is in place to ensure Commission meets deadlines;

• MS must request and justify deadline extensions where needed.

Conformity Clearance: new MS possibilities

• MS will be invited (in letter of findings) to calculate the risk to the EU budget.

• They are required to do this work at the beginning of the contradictory procedure.

• New information should come at the very latest at the time of commenting on the bilateral minutes (Reg. 908/2014, Art 34(3).

New financial correction guidelines

• Why are new guidelines necessary?

• Adapt existing rules to the new legal provisions (Art.52 of R. 1306/2013 and Art.12 of R. 907/2014)

• Improve clarity and transparency of the rules

• Take stock of experience gained/lessons learned

• New elements introduced:

• Calculated/Extrapolated corrections: more detailed instruction

• Additional levels of flat-rate financial corrections

• Entry into force of the new rules from 1.1.2015.

Key & ancillary controls• Definitions clarified, harmonised content & layout.

• Lists finalised (20)

• Future lists

• Application date: for conformity clearance procedures launched as from 1.1.2015

• Intention is to increase transparency - not to increase financial corrections

Cost of Control

• 4 billion EUR

• New information gathering exercise:

• Cost of control for how many controls• Keeping LPIS up to date• CAP reform implementation• IT systems• CB work

• Starts Autumn 2015.