296 fall 2012.pdf

TRANSCRIPT

HP Printer Case

Management in Engineering

November 14 2012 Dr Abbott Weiss Senior Lecturer

What do you recommend HP should do

Universal power supply raquo Yes raquo No

Why

111712 2

Mfg Eng

MktgController

HP managers around the table

Prod Design 111712 3

Measurements and Behavior

Five functional managers are discussed in the case

a) Marketing b) Product Design amp Development c) Finance d) Manufacturing Engineering e) Distribution

Distribution

How are they measured How does it influence their views on the universal power supply

111712 4

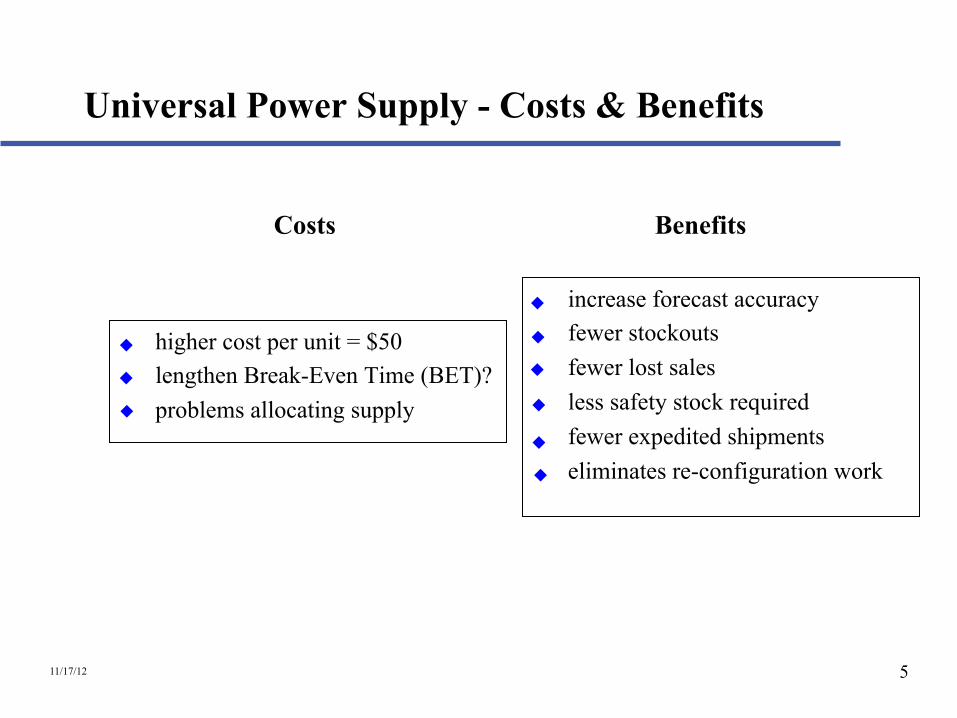

Universal Power Supply - Costs amp Benefits

Costs Benefits

higher cost per unit = $50 lengthen Break-Even Time (BET) problems allocating supply

increase forecast accuracy fewer stockouts fewer lost sales less safety stock required fewer expedited shipments eliminates re-configuration work

111712 5

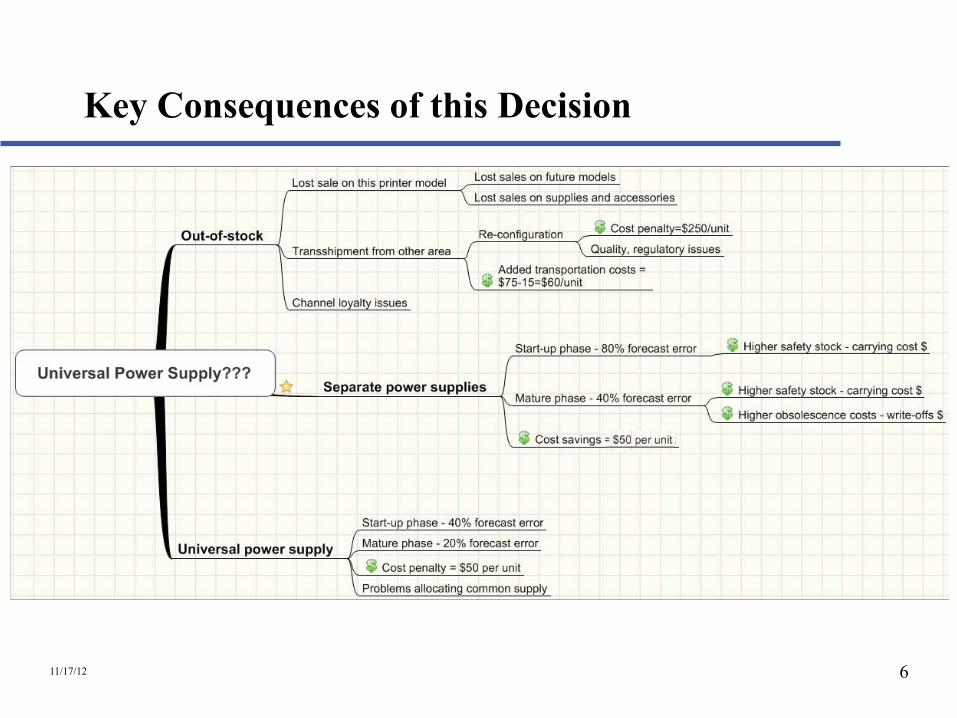

Key Consequences of this Decision

111712 6

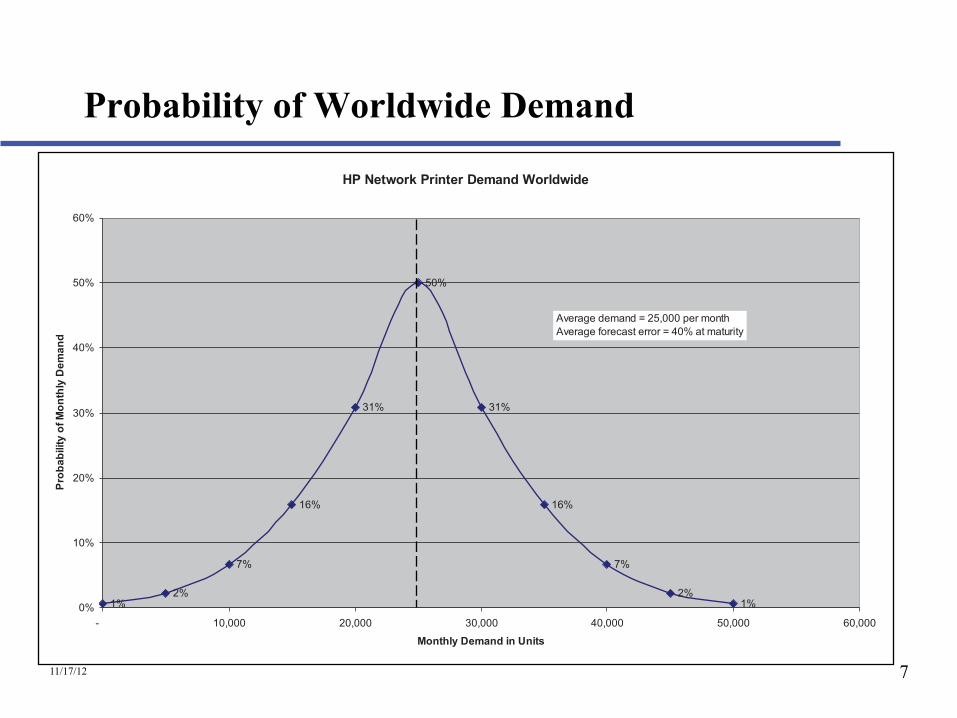

Probability of Worldwide Demand

HP Network Printer Demand Worldwide

60

50

40

30

20

10

0

50

Average demand = 25000 per month Average forecast error = 40 at maturity

31 31

16 16

1 2

7 7

2 1

- 10000 20000 30000 40000 50000 60000

Monthly Demand in Units

111712 7

Prob

abili

ty o

f Mon

thly

Dem

and

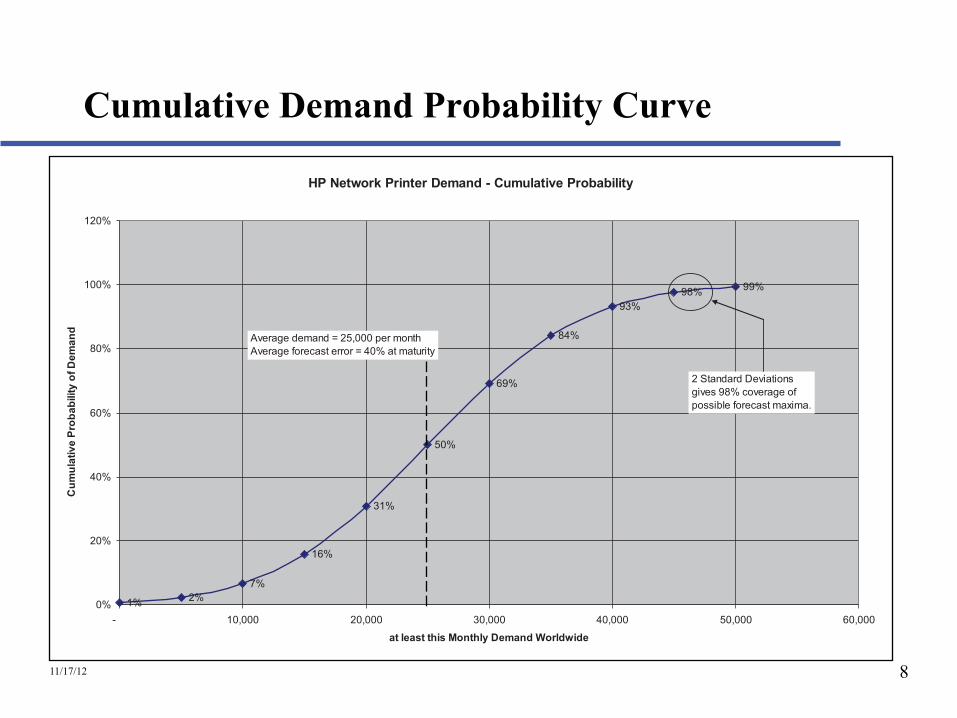

Cumulative Demand Probability Curve

HP Network Printer Demand - Cumulative Probability

1 2 7

16

31

50

69

84

93 98 99

0

20

40

60

80

100

120

- 10000 20000 30000 40000 50000 60000

at least this Monthly Demand Worldwide

Cum

ulat

ive

Prob

abili

ty o

f Dem

and

Average demand = 25000 per month Average forecast error = 40 at maturity

2 Standard Deviations gives 98 coverage of possible forecast maxima

111712 8

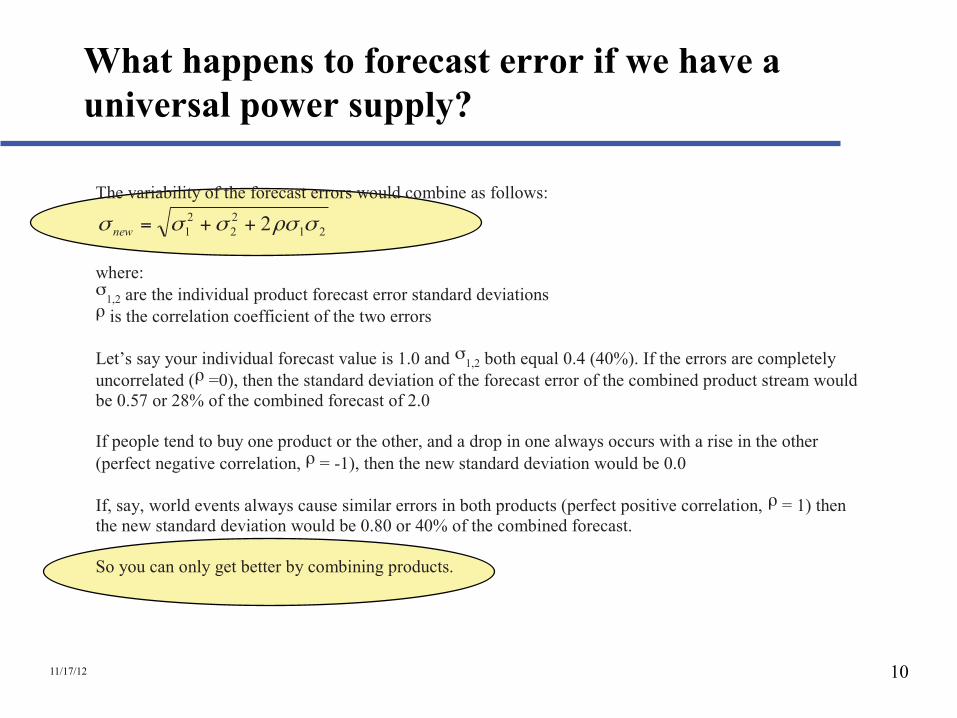

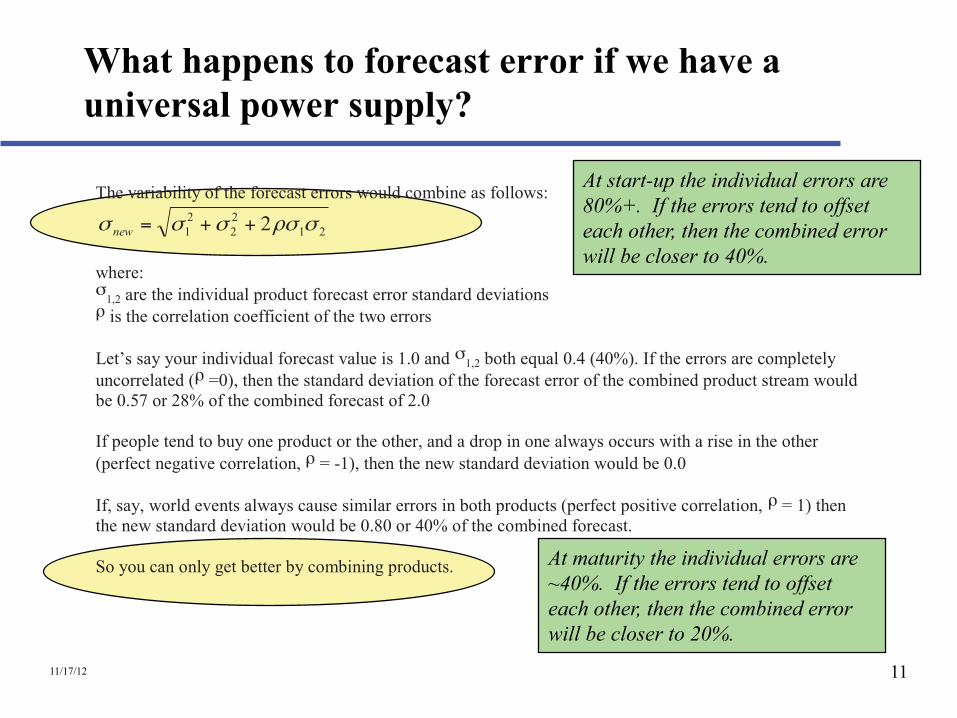

What happens to forecast error if we have a universal power supply

111712 9

What happens to forecast error if we have a universal power supply

The variability of the forecast errors would combine as follows

21 2 2

2 1 2 σρσσσσ ++= new

where σ

12 are the individual product forecast error standard deviations ρ is the correlation coefficient of the two errors

Letrsquos say your individual forecast value is 10 and σ 12 both equal 04 (40) If the errors are completely

uncorrelated (ρ =0) then the standard deviation of the forecast error of the combined product stream would be 057 or 28 of the combined forecast of 20

If people tend to buy one product or the other and a drop in one always occurs with a rise in the other (perfect negative correlation ρ = -1) then the new standard deviation would be 00

If say world events always cause similar errors in both products (perfect positive correlation ρ = 1) then the new standard deviation would be 080 or 40 of the combined forecast

So you can only get better by combining products

111712 10

What happens to forecast error if we have a universal power supply

The variability of the forecast errors would combine as follows

21 2 2

2 1 2 σρσσσσ ++= new

At start-up the individual errors are 80+ If the errors tend to offset each other then the combined error will be closer to 40

where σ

12 are the individual product forecast error standard deviations ρ is the correlation coefficient of the two errors

Letrsquos say your individual forecast value is 10 and σ 12 both equal 04 (40) If the errors are completely

uncorrelated (ρ =0) then the standard deviation of the forecast error of the combined product stream would be 057 or 28 of the combined forecast of 20

If people tend to buy one product or the other and a drop in one always occurs with a rise in the other (perfect negative correlation ρ = -1) then the new standard deviation would be 00

If say world events always cause similar errors in both products (perfect positive correlation ρ = 1) then the new standard deviation would be 080 or 40 of the combined forecast

So you can only get better by combining products At maturity the individual errors are ~40 If the errors tend to offset each other then the combined error will be closer to 20

111712 11

Key Learnings for Management in Engineering

Engineeringdesign decisions have major impact on operations and customer service

Consider all the costs especially when things do not go according to plan

Measurements and rewards change behavior influence how your company operates

111712 12

Key Takeaways

1 Forecasts are always wrong 2 How wrong (a) a lot or (b) an awful lot 3 Challenge for international markets power localization etc 4 Global supply lines mean long lead times aggravating the problem 5 Design can have a major impact on supply chain flexibility 6 Hard costs will lead you to specialized products Inventory

benefits can be very large but are Soft costs 7 Who is measured on inventory 8 Hidden costs are often invisible or occur much later than the key

decisions which can create them 9 Do the math Think again about what could change the answer 10 Remember that this is one of many decisions over time

111712 14

Key Learnings for Supply Chain Management

Value of postponement

Organizational roles and measurements

International dimensions

111712 15

Value of Postponement HP Network Printer Demand Worldwide

60

40

30Reduced cycle times 50

20

0 - 10000 20000 30000 40000 50000 60000

50

Average demand = 25000 per month Average forecast error = 40 at maturity

31 31

16 16

1 2

7 7

2 1

Monthly Demand in Units Lower forecast errors 10

Smaller safety stocksfewer stockouts Lower obsolescence costs Reduced penalty costsprofit drains

Prob

abili

ty o

f Mon

thly

Dem

and

raquo Reconfiguration and extra handling raquo Premium transportation raquo Prevent lost revenue and profit raquo Prevent loss of market share

Changes during product life cycle

111712 16

Organizational roles and Measurements

Marketing EngineeringDesignProduct Management Finance Manufacturing Procurement LogisticsDistribution General Managers Supplierpartner

111712 17

Organizational roles and Measurements

Accountability BET (Break-Even Time)

How to measure Who pays

Effects of regional PampLs

Costs raquo Product cost raquo Transportation raquo Inventory raquo Obsolescence raquo Stockouts

Net profit

111712 18

International Aspects

Product variety Distance and time for supply Power and regulatory requirements Labeling packaging Forecast complexities Supplier inflexibility Accountability and measurement

111712 19

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012 For information about citing these materials or our Terms of Use visit httpocwmiteduterms

Strategic Planning of RampD

- 2 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Outline

Risk Factors in RampD

Strategic Focus

Stage-Gate Process

Technology Choice Case

- 3 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Company Births and Deaths

1995 594000 births amp 497000 deaths

2002 580900 births amp 576200 deaths

2005 670058 births amp 599333 deaths

SBA Office of Advocacy

- 4 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Attrition Rate of New-Product Ideas

For every 11 serious ideas 3 enter development 13 are launched 1 succeeds

- 5 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Attempts to Start New Business

One success in ten

The odds are much poorer for new ideas

- 6 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

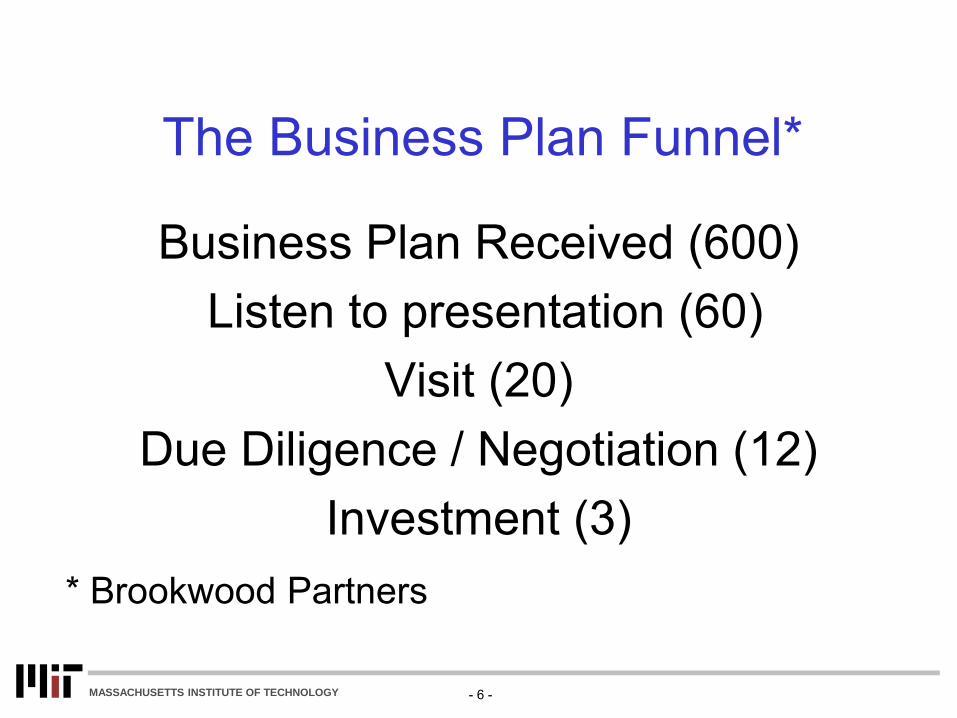

The Business Plan Funnel

Business Plan Received (600) Listen to presentation (60)

Visit (20) Due Diligence Negotiation (12)

Investment (3) Brookwood Partners

- 7 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

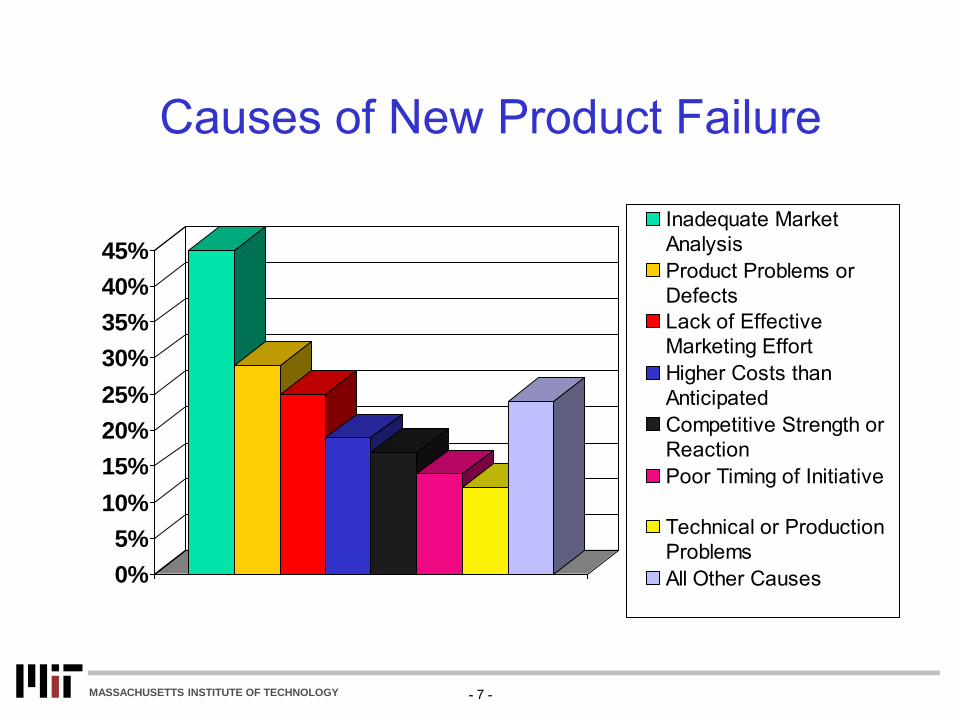

Causes of New Product Failure

0

5

10

15

20

25

30

35

40

45

Inadequate MarketAnalysisProduct Problems orDefectsLack of EffectiveMarketing EffortHigher Costs thanAnticipatedCompetitive Strength orReactionPoor Timing of Initiative

Technical or ProductionProblemsAll Other Causes

- 8 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Failures not merely negligence

Attributable to lack of minus understanding customer requirements

minus creating dramatic differences in current capabilities

minus understanding additional capabilities

- 9 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

The Suicide Square

New Technology

Inc

rea

se

d R

isk

- 10 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

The Suicide Square

New Product

New Technology

Inc

rea

se

d R

isk

- 11 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

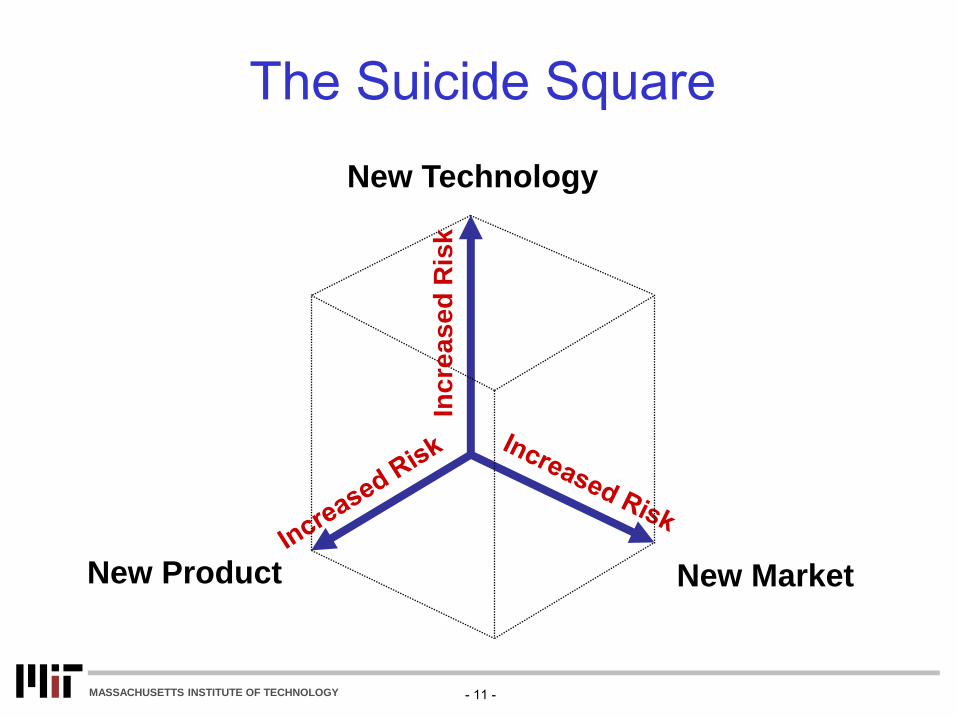

The Suicide Square

New Market New Product

New Technology

Inc

rea

se

d R

isk

- 12 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

The Suicide Square

New Market New Product

New Technology

Inc

rea

se

d R

isk

- 13 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

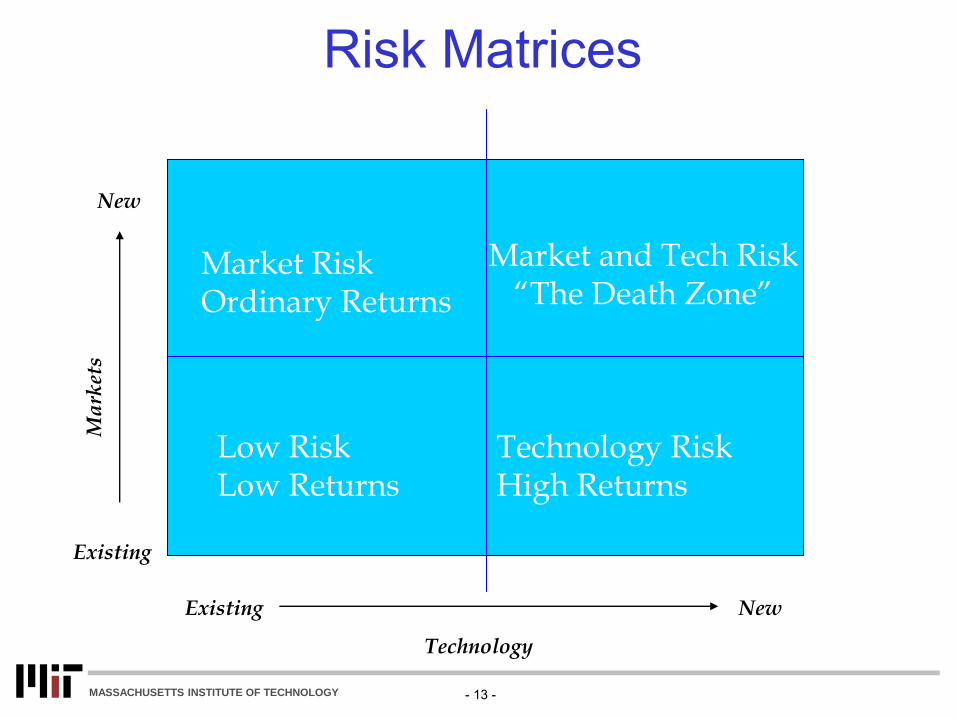

Risk Matrices

Existing New

Technology

Ma

rket

s

New

Existing

Low Risk Low Returns

Market Risk Ordinary Returns

Market and Tech Risk ldquoThe Death Zonerdquo

Technology Risk High Returns

- 14 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

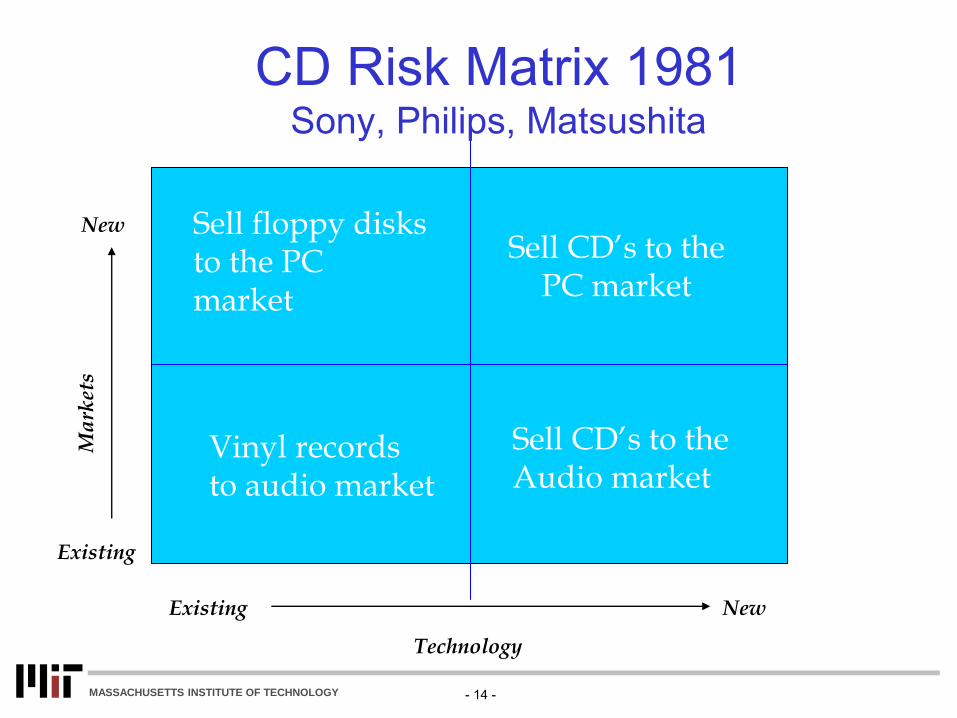

CD Risk Matrix 1981 Sony Philips Matsushita

Existing New

Technology

Ma

rket

s

New

Existing

Vinyl records to audio market

Sell floppy disks to the PC market

Sell CDrsquos to the PC market

Sell CDrsquos to the Audio market

- 15 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

CD Risk Matrix 1985-1996 Sony Philips Matsushita

Existing New

Technology

Ma

rket

s

New

Existing

Sell CDrsquos to the PC market

Sell CDrsquos to the Audio market

Sell DVDrsquos to the Video market

Sell DVDrsquos to the Video Game market

- 16 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Technology Management

Strategic focus

Business process

- 17 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Strategic Focus Choose attractive strategic markets or market

segments to participate in

Find ldquoBeaconsrdquo in selected markets and market segments

Identify core competencies needed to address products markets and applications

Plan a product market application competency succession strategy

- 18 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

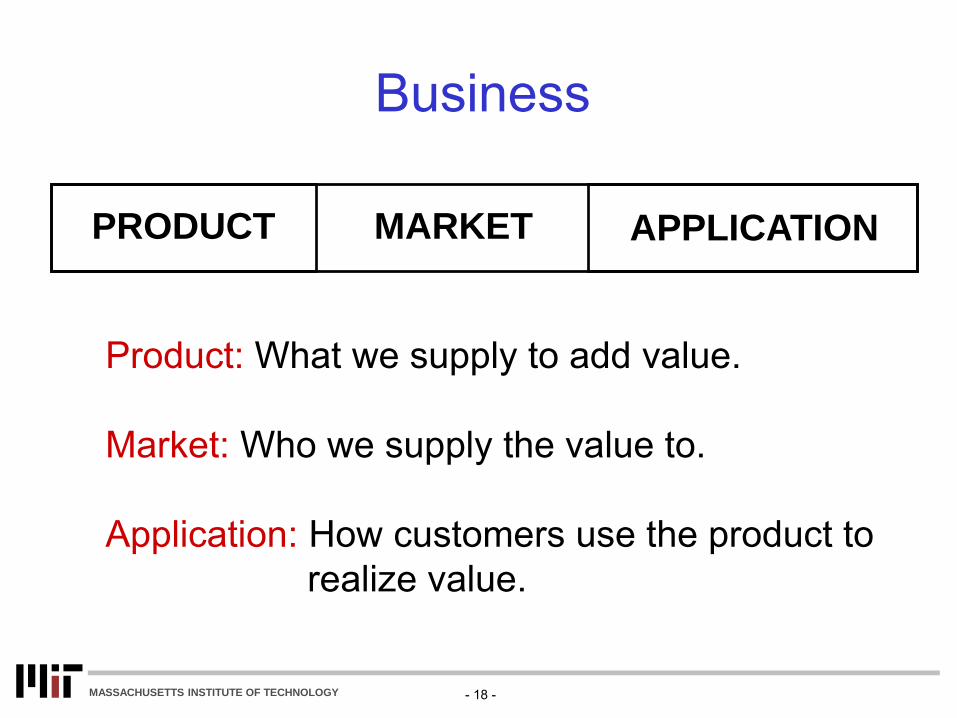

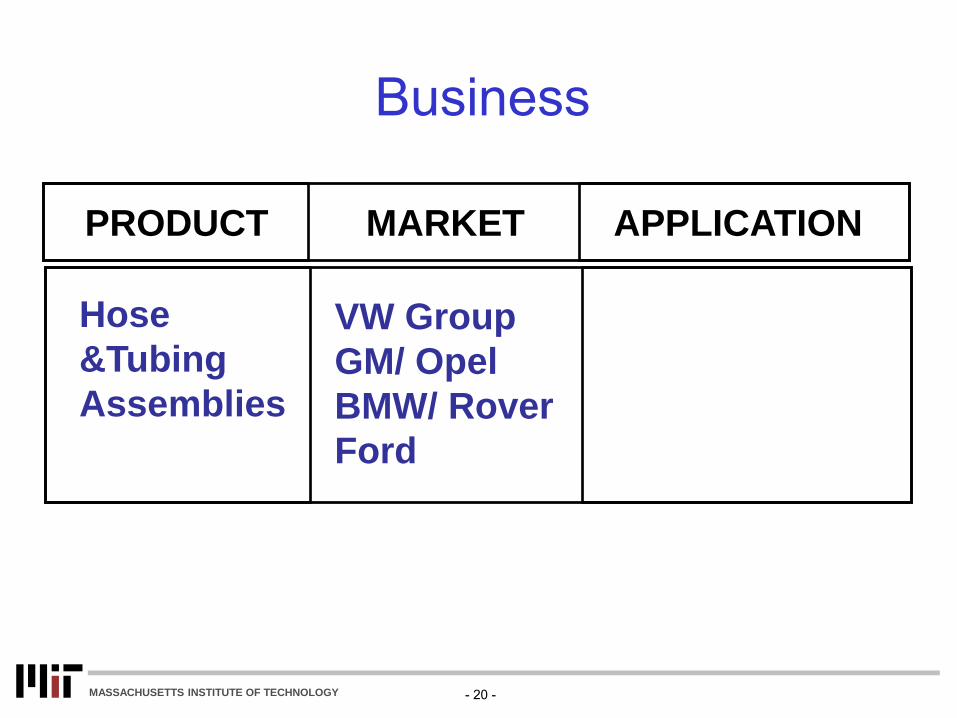

Business

PRODUCT MARKET APPLICATION

Product What we supply to add value Market Who we supply the value to Application How customers use the product to realize value

- 19 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Business

PRODUCT MARKET APPLICATION

Automotive

- 20 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

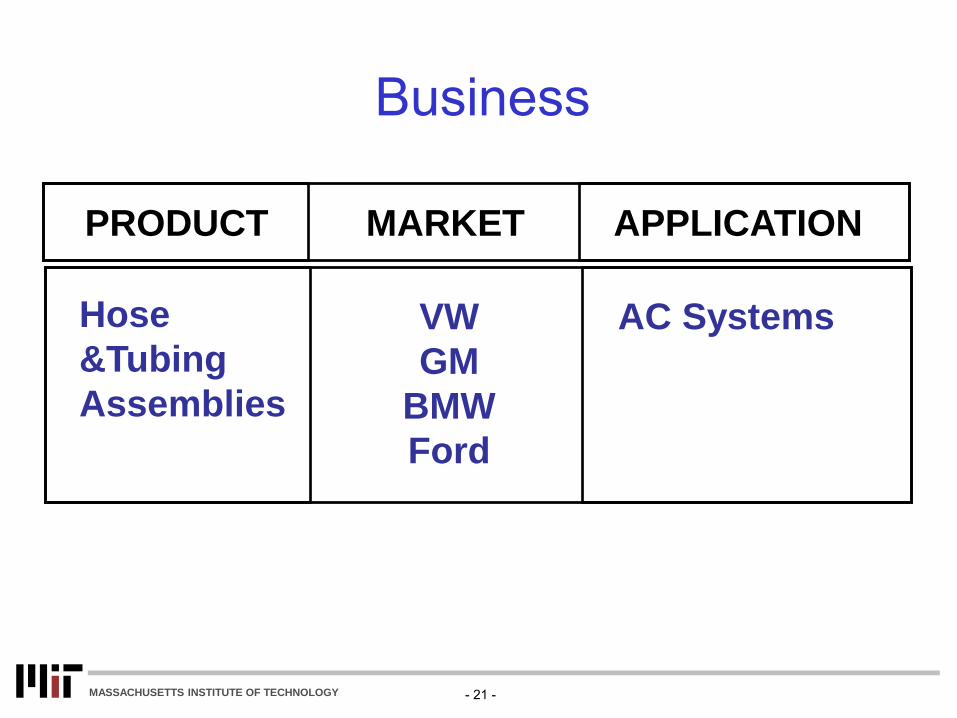

Business

PRODUCT MARKET APPLICATION

VW Group

GM Opel

BMW Rover

Ford

Hose

ampTubing

Assemblies

- 21 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Business

PRODUCT MARKET APPLICATION

VW

GM

BMW

Ford

Hose

ampTubing

Assemblies

AC Systems

- 22 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Technology Strategy vs Corporate Strategy

Identify the firmrsquos ldquoCore Competencyrdquo

Specify the types of products markets applications and technologies for focus

Specify the role technology innovation plays in achieving the firms overall objectives

- 23 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Strategic Resources Focus and Risk

Assign resources to reflect strategic focus

Assign resources according to the acceptable level of risk

Reconcile differences between the stated strategy and specified resources

- 24 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Stage ndash Gate Process

Develop Develop Launch

1st 2nd 3rd nthSTAGE

Ideas

Go No-Go Screen

Go No-Go Screen

Go No-Go Screen

Investigate

Modified Stage-Gate with Continuous Customer Interaction

Development New product

IDEA Strategic

focus

Customer

Customer

n-th Development

- 26 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Concurrent Business Development

Cross-disciplinary teams Knowledge must broaden

minus Engineers are ldquotechnicalrdquo experts but must understand the business

minus Managers are ldquobusinessrdquo experts but must understand the technology

- 27 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Case Study Technology Choice

Grumman Corporation

- 28 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Basic Factors in Evaluating a Technology

Will the technology satisfy a market sometime in the future (Market Need) minus Does it provide improved performance minus Does it reduce costs minus Is its market penetration rate acceptable

When will the product become significant (Timing)

- 29 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Basic Factors in Evaluating a Technology (cont)

Will the technology be commercially viable (Economics)

minus Does the market exist or will it be created minus Does the potential market size justify the

investment minus Is the production process feasible and practical minus Is the product profitable to manufacture

- 30 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

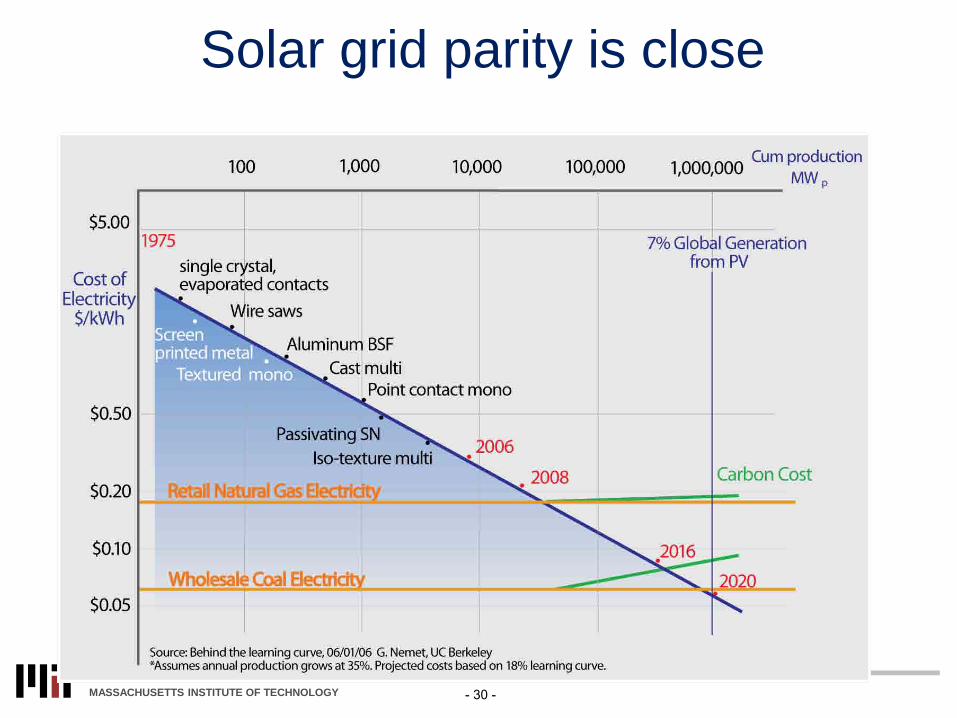

Solar grid parity is close

- 31 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

- 32 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Solarrsquos Challenge Scale

202 287 401 560 750 1256

1815 2536

4279

7910

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

MW

s

Global Cell Production

Despite record growth generation from PV still is only 02 of total global electricity

- 33 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

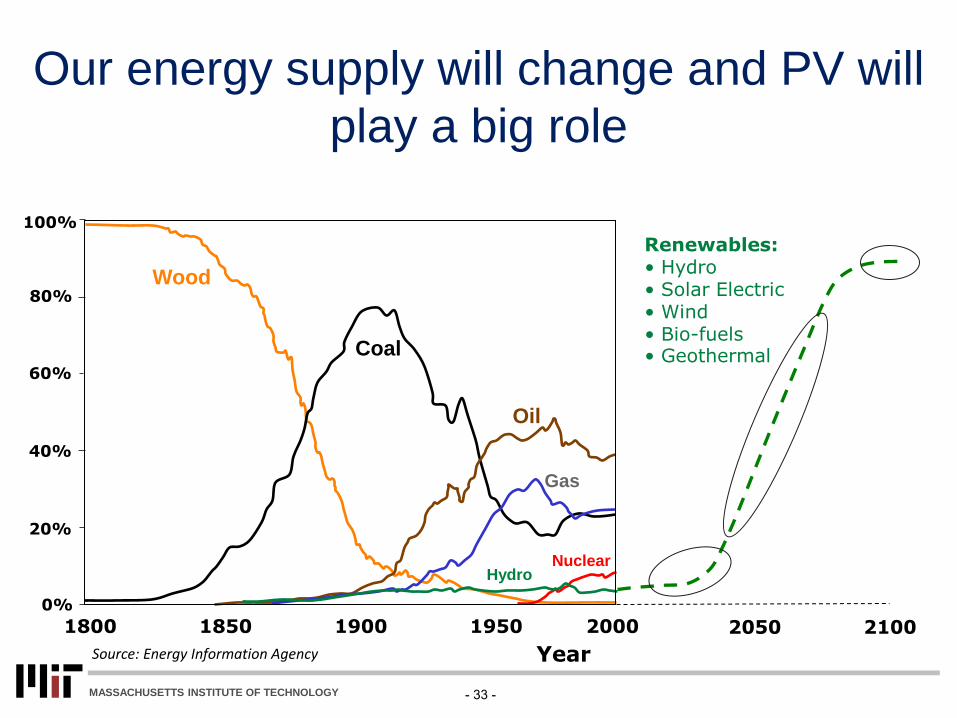

Our energy supply will change and PV will

play a big role

2050 2100

Renewables bull Hydro bull Solar Electric bull Wind bull Bio-fuels bull Geothermal

1800 1850 1900 1950 2000

Nuclear

Wood

Coal

Oil

Gas

100

80

60

40

20

0

Hydro

Year Source Energy Information Agency

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012 For information about citing these materials or our Terms of Use visit httpocwmiteduterms

You will often have a chance to develop or evaluate business propositions If you do

nothing else at least cover these elements

Presenting Business Opportunities Document Simply and Clearly

Customer Need

What unmet customer need exists that you are addressing Which customers What are

the characteristics of the need and those customers

Proposed Solution

How do you plan to fulfill the need described What alternatives are available (or could

be) to the customers and why is your solution preferred How is our solution better than

the competition What are the key elements of the solution proposed How do you plan

to implement When

Costs

What are the major costs and assets of delivering this solution Provide enough detail so

we understand them well

Price and Profit

What do we plan to charge the customer What are their expectations What are the

margins and the net profits

Risks

What are the important things that could go wrong What are our plans to minimize the

occurrence or the cost of those risks

Dr Abbott Weiss

Senior Lecturer

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

HP Printer Case Study amp Questions

Due Wednesday November 14 2012

Read Hewlett-Packard Company Universal Power Supply for Printer Design (p357)

The questions on the last page of the case study (p 365) are there to stimulate your thoughts as you analyze the case For the written assignment please answer the following questions in less than one page 1) What do you recommend HP do about the universal power supply and why 2) Five functional managers are discussed in the case a) Marketing b) Product Design amp Development c) Finance d) Manufacturing Engineering e) Distribution What do you believe are the primary measures of each departments performance and how do they affect the managerrsquos views about this decision

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

Self-Unloader Dry Bulk Ships Case Study amp Questions

Read the SUL Company case study For your written assignment I want you to calculate the premium (expressed as a percentage) that the self-unloader shipowner must charge compared to the owner of a standard bulker This premium should be evaluated for a ship that costs $60 million to build (includes an additional $12 million in vessel cost for the self-unloader) and has a daily operating cost (opex) of $8900 The premium must provide an equivalent return on capital (ROC) and return on equity (ROE) when compared to the original values for the standard bulker (See guidelines below as to how to do this) In class we will discuss

The above calculation assumes that the self-unloader spends the same time in port as a standard bulker What impact does it have that the self-unloader has a faster unloading rate and therefore a shorter time in port How do you quantify this impact

What should SUL Corsquos pricing policy be From a shipownerrsquos viewpoint what are the prorsquos and conrsquos of being a self

unloader shipowner Should SUL Co build the ship described in the case studyspreadsheet How does the down market affect SUL Corsquos decision

Guidelines for the SUL Mendoza Investment Model To modify capital costs Change cell F7 from a value of $48000000 to $60000000 To change operating expenses Change cell V8 from a value of $7000 to $8900 To change the time charter equivalent (TCE) rate Think of the TCE rate as the amount that the shipowner charges for the use of his ship each day To see the impact of increasing the TCE by X change cell F17 from 0 to X Hit ldquoEnterrdquo For your homework just state the PERCENTAGE PREMIUM plus 3 reasons why you think that SUL Co willmdashor will notmdashbe able to obtain this premium

This assignment sheet was prepared by Nathan L Pratt and Henry S Marcus as an introduction to working with the referenced investment model Some information in this spreadsheet (the inputs relating to TCE and interest rates in particular) has been disguised at the request of the author of the spreadsheet

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

Ethics ndash Group Homework Assignment

Read Ethics Scenarios (p 233)

For the written assignment please answer the following question in one paragraph as a group for your scenario

What would you do and why

If your entire group doesnrsquot agree on one answer you may add a paragraph with the minorityrsquos opinion

See the scenario assignments by group below

Team Scenario U01 1 U02 2 U03 3 U04 4 U05 5 U06 6 U07 7 U08 8 G01 9 G02 10 G03 11

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in Engineering Fall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

2962961 Management for Engineers

Fall 2011

Professor Henry Marcus Professor Jung-Hoon Chun

and Dr Abbott Weiss

Accounting Quiz

October 31 2011

DO NOT OPEN this quiz until instructed to do so This quiz is CLOSED BOOK Put your name on top of every pagemdashthese pages may be separated for grading Write your solutions in the space provided Should you need extra space write in

the back of the page with the problem Blue books will be provided for your own use but will not be graded Be neat and write legibly

Fill in your name and the names of the people sitting next to you If you are at the end of a row write ldquoXrdquo in the space provided

Your name Name of person to your left Name of person to your right

1 2 3 4 5

2962961 Quiz 1 Name______________________________________

Problem Grade Points 20 40 25 15 5

Total 105

2

2962961 Quiz 1 Name______________________________________

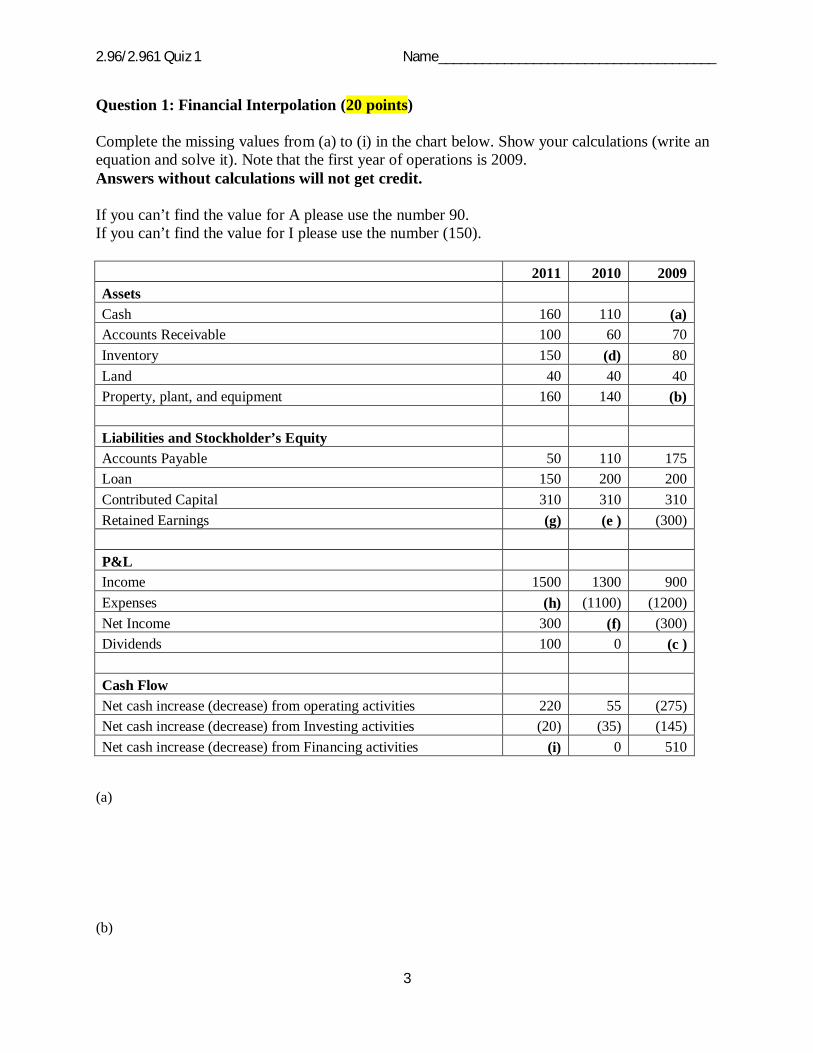

Question 1 Financial Interpolation (20 points)

Complete the missing values from (a) to (i) in the chart below Show your calculations (write an equation and solve it) Note that the first year of operations is 2009 Answers without calculations will not get credit

If you canrsquot find the value for A please use the number 90 If you canrsquot find the value for I please use the number (150)

2011 2010 2009 Assets Cash 160 110 (a) Accounts Receivable 100 60 70 Inventory 150 (d) 80 Land 40 40 40 Property plant and equipment 160 140 (b)

Liabilities and Stockholderrsquos Equity Accounts Payable 50 110 175 Loan 150 200 200 Contributed Capital 310 310 310 Retained Earnings (g) (e ) (300)

PampL Income 1500 1300 900 Expenses (h) (1100) (1200) Net Income 300 (f) (300) Dividends 100 0 (c )

Cash Flow Net cash increase (decrease) from operating activities 220 55 (275) Net cash increase (decrease) from Investing activities (20) (35) (145) Net cash increase (decrease) from Financing activities (i) 0 510

(a)

(b)

3

2962961 Quiz 1 Name______________________________________

(c)

(d)

(e)

(f)

(g)

(h)

(i)

4

2962961 Quiz 1 Name______________________________________

Question 2 Recording Transactions (40 points)

Test Corp (ldquothe Companyrdquo) made the following transactions during 2010 fiscal years (assume that they are listed in chronological order)

1 The business was started on January 1st by the owner when she contributed $10000 in cash 2 On January 1st the Company paid rent for two years in the total amount of $2400 3 On January 1st the Company purchased computers in the amount of $900 The computers

have a useful life of 3 years and a salvage value of 0 4 The Company provided service to customers and recognized $3000 revenue on account (did

not receive cash) 5 The Company Collected $1500 cash from customers 6 On July 1 the company borrowed $2000 from M-E Bank at an interest rate of 10 for 12

months The interest is payable on June 30 2011 7 On December 31 the Company distributed dividends in the amount of $600 to the owners

(a) Record ALL the effects of each of the events above on the table provided below Mark an increase with a + and a decrease with ( )

(b) Evaluate the effect of each transaction on the Leverage ratio (circle whether the ratio will increasenot changedecrease)

ASSETS LIABILITIES EQUITY Mark the effect on Leverage

Ratio Transaction Cash

Accounts Receivable (including

other)

Equipment Interest Payable Loan Shareholders

Equity

Increase Nochange decrease Increase Nochange decrease Increase Nochange decrease Increase Nochange decrease Increase Nochange

5

2962961 Quiz 1 Name______________________________________

ASSETS LIABILITIES EQUITY Mark the effect on Leverage

Ratio Transaction Cash

Accounts Receivable (including

other)

Equipment Interest Payable Loan Shareholders

Equity

decrease Increase Nochange decrease Increase Nochange decrease Increase Nochange decrease Increase Nochange decrease Increase Nochange decrease

6

2962961 Quiz 1 Name______________________________________

Question 3 Cash Flow Statement (25 points)

Use the balance sheet and income statement on the FOLLOWING PAGES (PAGE 8-9) to generate a cash flow statement for 2011 in the space below

CASH FLOW STATEMENT (2011) Cash Flow from Operating Activities

Cash Flow from Investing Activities

Cash Flow from Financing Activities

7

8

2962961 Quiz 1 Name______________________________________

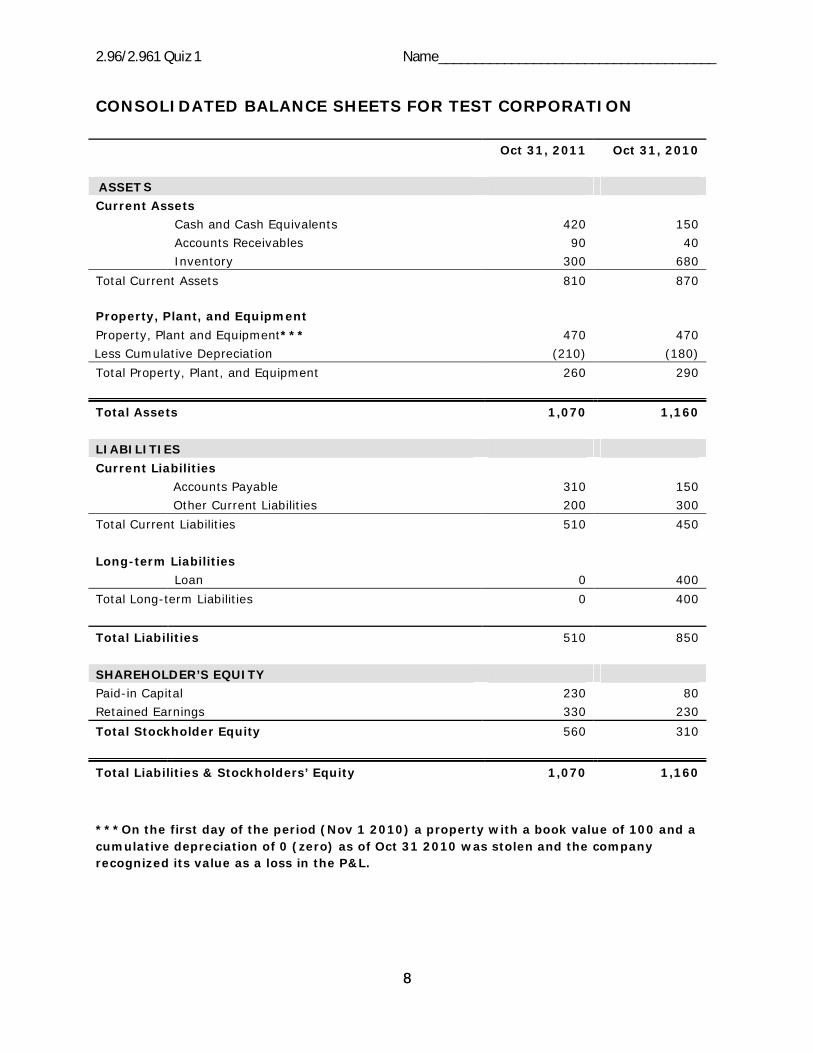

CONSOLIDATED BALANCE SHEETS FOR TEST CORPORATION

Oct 31 2011 Oct 31 2010

ASSETS Current Assets

Cash and Cash Equivalents 420 150 Accounts Receivables 90 40 Inventory 300 680

Total Current Assets 810 870 Property Plant and Equipment Property Plant and Equipment 470 470 Less Cumulative Depreciation (210) (180) Total Property Plant and Equipment 260 290

Total Assets 1070 1160 LIABILITIES Current Liabilities

Accounts Payable 310 150 Other Current Liabilities 200 300

Total Current Liabilities 510 450 Long-term Liabilities

Loan 0 400 Total Long-term Liabilities 0 400 Total Liabilities 510 850 SHAREHOLDERrsquoS EQUITY Paid-in Capital 230 80 Retained Earnings 330 230 Total Stockholder Equity 560 310

Total Liabilities amp Stockholdersrsquo Equity 1070 1160 On the first day of the period (Nov 1 2010) a property with a book value of 100 and a cumulative depreciation of 0 (zero) as of Oct 31 2010 was stolen and the company recognized its value as a loss in the PampL

8

ASSET

ASSETS

ASSETS

ASSETS

S

LIABILITIES

SHAREHOLDERrsquoS EQUITY

2962961 Quiz 1 Name______________________________________

CONSOLIDATED INCOME STATEMENT FOR TEST CORPORATION

Period Ending Oct 31 2011

Total Revenue 2000 Cost of Goods Sold 1225 Gross Profit 775

Research Development 250 Selling General and Administrative 170 Depreciation and amortization 30 Total Operating Expenses 450

Operating Income or Loss 425

Finance Expenses 25 Income Before Tax 400

Income Tax Expense 100 Net Income From Continuing Ops 200

Non-recurring Events

Loss from stolen property 100

Net Income 100

On the first day of the period (Nov 1 2010) a property with a book value of 100 and a cumulative depreciation of 0 (zero) as of Oct 31 2010 was stolen and the company recognized its value as a loss in the PampL

9

Operating Expenses

Non-recurring Events

2962961 Quiz 1 Name______________________________________

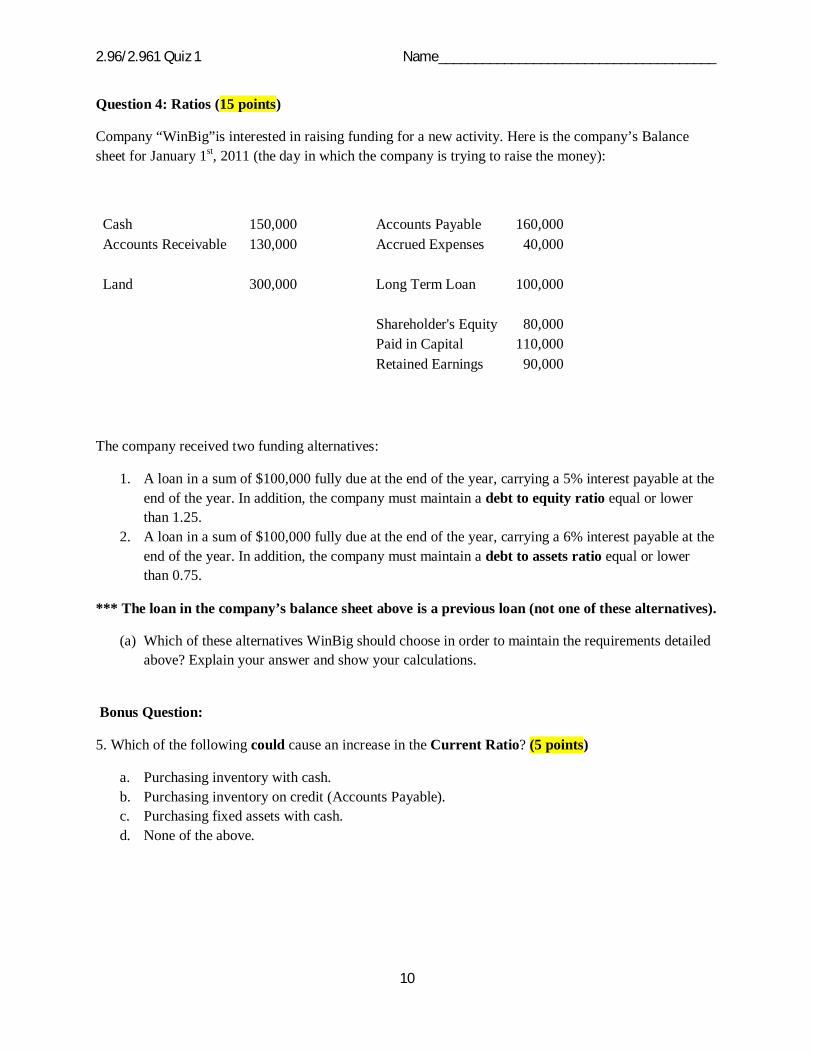

Question 4 Ratios (15 points)

Company ldquoWinBigrdquois interested in raising funding for a new activity Here is the companyrsquos Balance sheet for January 1st 2011 (the day in which the company is trying to raise the money)

Cash 150000 Accounts Payable 160000 Accounts Receivable 130000 Accrued Expenses 40000

Land 300000 Long Term Loan 100000

Shareholders Equity 80000 Paid in Capital 110000 Retained Earnings 90000

The company received two funding alternatives

1 A loan in a sum of $100000 fully due at the end of the year carrying a 5 interest payable at the end of the year In addition the company must maintain a debt to equity ratio equal or lower than 125

2 A loan in a sum of $100000 fully due at the end of the year carrying a 6 interest payable at the end of the year In addition the company must maintain a debt to assets ratio equal or lower than 075

The loan in the companyrsquos balance sheet above is a previous loan (not one of these alternatives)

(a) Which of these alternatives WinBig should choose in order to maintain the requirements detailed above Explain your answer and show your calculations

Bonus Question

5 Which of the following could cause an increase in the Current Ratio (5 points)

a Purchasing inventory with cash b Purchasing inventory on credit (Accounts Payable) c Purchasing fixed assets with cash d None of the above

10

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

2962961 Midterm Exam Answer Key Question 1 There are generally multiple valid equations to get to the correct answers These are just examples Also note the order of performing these calculations is not simply ai Up to -2 marks per error

a) Assets = Liabilities + Shareholder Equity a+70+80+40+b=175+200+310+(300) a = 90

b) Net Cash from Investing = (Incr in Land) + (Incr in PPE) (145) = (40) -b b = 105

c) REend = REbegin + NI - Dividends (300) = 0 + (300) - c c = 0

d) Assets = Liabilities + Shareholder Equity 110+60+d+40+140=110+200+310+e d=170

e) REend = REbegn + NI - Dividends e = (300)+f-0 e=(100)

f) NI = Income + Expenses f = 1300 + (1100) f = 200

g) REend = REbegin+NI-Dividends g = e + 300-100 g = 100

h) NI = Income + Expenses 300=1500+h h=(1200)

i) Net Cash from Financing = Incr in Cash - Net Cash from Operating - Net Cash from Investing i = 50-220-(20) i = (150)

1

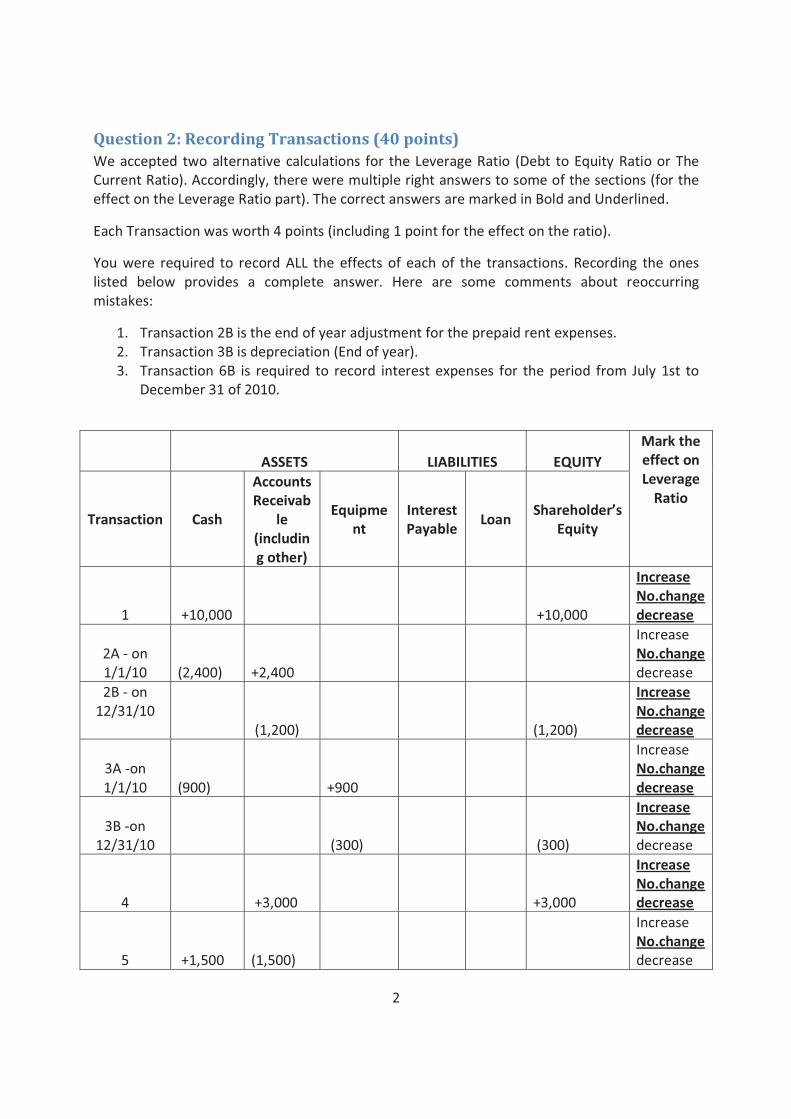

Question 2 Recording Transactions (40 points) We accepted two alternative calculations for the Leverage Ratio (Debt to Equity Ratio or The Current Ratio) Accordingly there were multiple right answers to some of the sections (for the effect on the Leverage Ratio part) The correct answers are marked in Bold and Underlined

Each Transaction was worth 4 points (including 1 point for the effect on the ratio)

You were required to record ALL the effects of each of the transactions Recording the ones listed below provides a complete answer Here are some comments about reoccurring mistakes

1 Transaction 2B is the end of year adjustment for the prepaid rent expenses 2 Transaction 3B is depreciation (End of year) 3 Transaction 6B is required to record interest expenses for the period from July 1st to

December 31 of 2010

ASSETS LIABILITIES EQUITY Mark the effect on Leverage

Ratio Transaction Cash

Accounts Receivab

le (includin g other)

Equipme nt

Interest Payable Loan Shareholders

Equity

1 +10000 +10000

Increase Nochange decrease

2A - on 1110 (2400) +2400

Increase Nochange decrease

2B - on 123110

(1200) (1200)

Increase Nochange decrease

3A -on 1110 (900) +900

Increase Nochange decrease

3B -on 123110 (300) (300)

Increase Nochange decrease

4 +3000 +3000

Increase Nochange decrease

5 +1500 (1500)

Increase Nochange decrease

2

ASSETS LIABILITIES EQUITY Mark the effect on Leverage

Ratio Transaction Cash

Accounts Receivab

le (includin g other)

Equipme nt

Interest Payable

Loan Shareholders

Equity

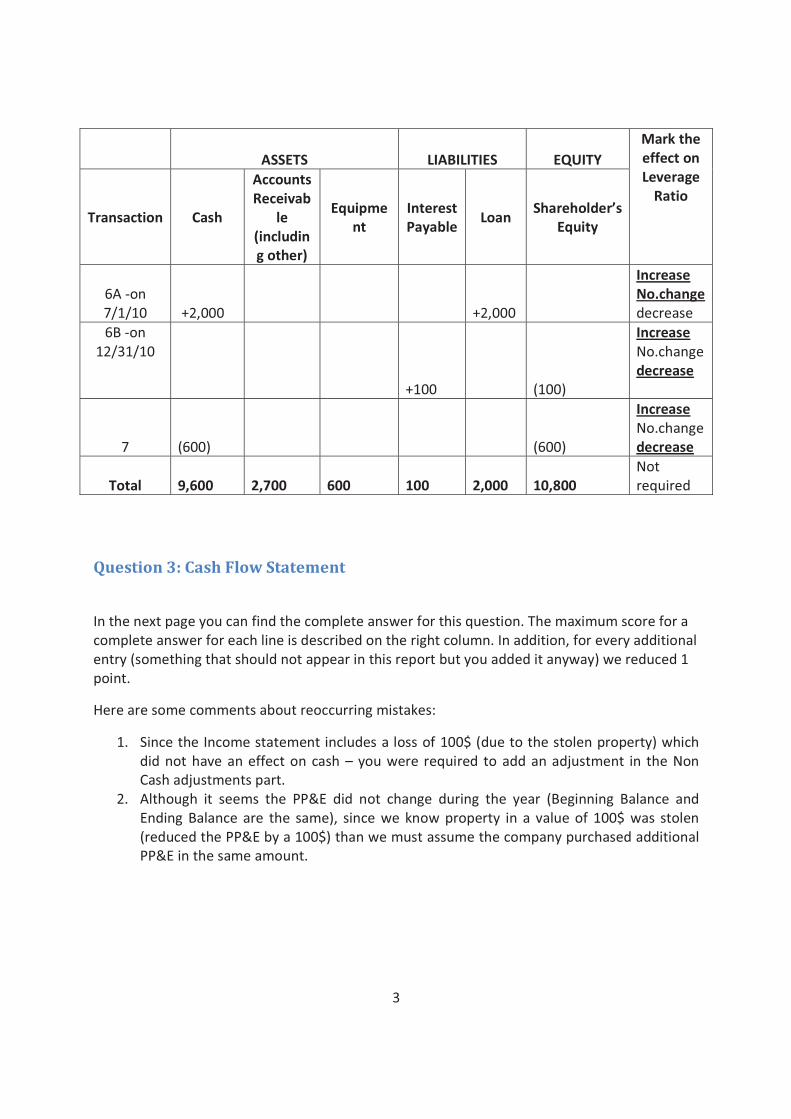

Increase 6A -on Nochange 7110 +2000 +2000 decrease 6B -on Increase

123110 Nochange decrease

+100 (100) Increase Nochange

7 (600) (600) decrease Not

Total 9600 2700 600 100 2000 10800 required

Question 3 Cash Flow Statement

In the next page you can find the complete answer for this question The maximum score for a complete answer for each line is described on the right column In addition for every additional entry (something that should not appear in this report but you added it anyway) we reduced 1 point

Here are some comments about reoccurring mistakes

1 Since the Income statement includes a loss of 100$ (due to the stolen property) which did not have an effect on cash - you were required to add an adjustment in the Non Cash adjustments part

2 Although it seems the PPampE did not change during the year (Beginning Balance and Ending Balance are the same) since we know property in a value of 100$ was stolen (reduced the PPampE by a 100$) than we must assume the company purchased additional PPampE in the same amount

3

Period Ending 3l-0ct-ll

Net Income l00

Non Cash Adjustments Increase in Cumulative Depreciation 30 Increase in Accounts Receivable -50 Decrease in Inventory 380 Increase in Accounts Payable 160 Decrease in Other Current Liabilities -100

Loss from stolen property 100

Max score

05

333331

2

Net Cash Increase from Operating Activities 620

Cash Flow from Investing Activities

Purchase of Property Plant and Equipment -100

Net Cash Decrease from Investing Activities -100

Cash Flow From Financing Activities Payment of Long Term Loan -400 3 Issuance of Stocks (Paid in Capital) 150 3 Net Cash Decrease from Financing Activities -250

Total Increase in Cash during the year 2011 270

Beginning Cash Balance 150

Ending Cash Balance 420

05

25 Total

4

Question 4 IShareholders Equity was meant to read IShare Capital such that you were supposed to add all three lines to get $280000 in Shareholder Equity However if you directly used Shareholder Equity of $80000 and made the correct conclusion given that choice you were not penalized Also if you elected to use long-term debt in these ratios instead of the more common total liabilities you should have realized that a one-year loan is not long-term debt In real life you would clarify these conditions with your debtors Also note that taking a loan provides cash assets in addition to showing up as a liability with interest Up to 5 marks per calculation 5 marks for conclusion There were 4 possible correct solutions

If equity is $80000 and debt is considered to be total liabilities WinBig should choose alternative 2 since it is the only possibility

Total Liabilities 160000+40000+100000+100000105 4050001 DE = = = = 506 gt 125 = FAIL Shareholder Equity 80000 80000

Total Liabilities 160000+40000+100000+100000106 406000 2 DA = = = = 060 lt 075 = OK Total Assets 150000+130000+300000+100000 680000

If equity is $80000 and debt is considered to be long-term debt WinBig should choose alternative 2 since it is the only possibility

Long-term Debt 100000 1 DE = = = 125 = 125 = FAIL Shareholder Equity 80000

Long-term Debt 100000 1000002 DA = = = = 015 lt 075 = OK Total Assets 150000+130000+300000+100000 680000

If equity is $280000 and debt is considered to be total liabilities WinBig should choose alternative 2 since it is the only possibility

Total Liabilities 160000+40000+100000+100000105 4050001 DE = = = = 145 gt 125 = FAIL Shareholder Equity 280000 280000

Total Liabilities 160000+40000+100000+100000106 406000 2 DA = = = = 060 lt 075 = OK Total Assets 150000+130000+300000+100000 680000

If equity is $280000 and debt is considered to be long-term debt WinBig should choose alternative 1 since both are possible but alternative 1 has a lower interest rate

Long-term Debt 100000 1 DE = = = 036 lt 125 = OK Shareholder Equity 280000

Long-term Debt 100000 1000002 DA = = = = 015 lt 075 = OK Total Assets 150000+130000+300000+100000 680000

5

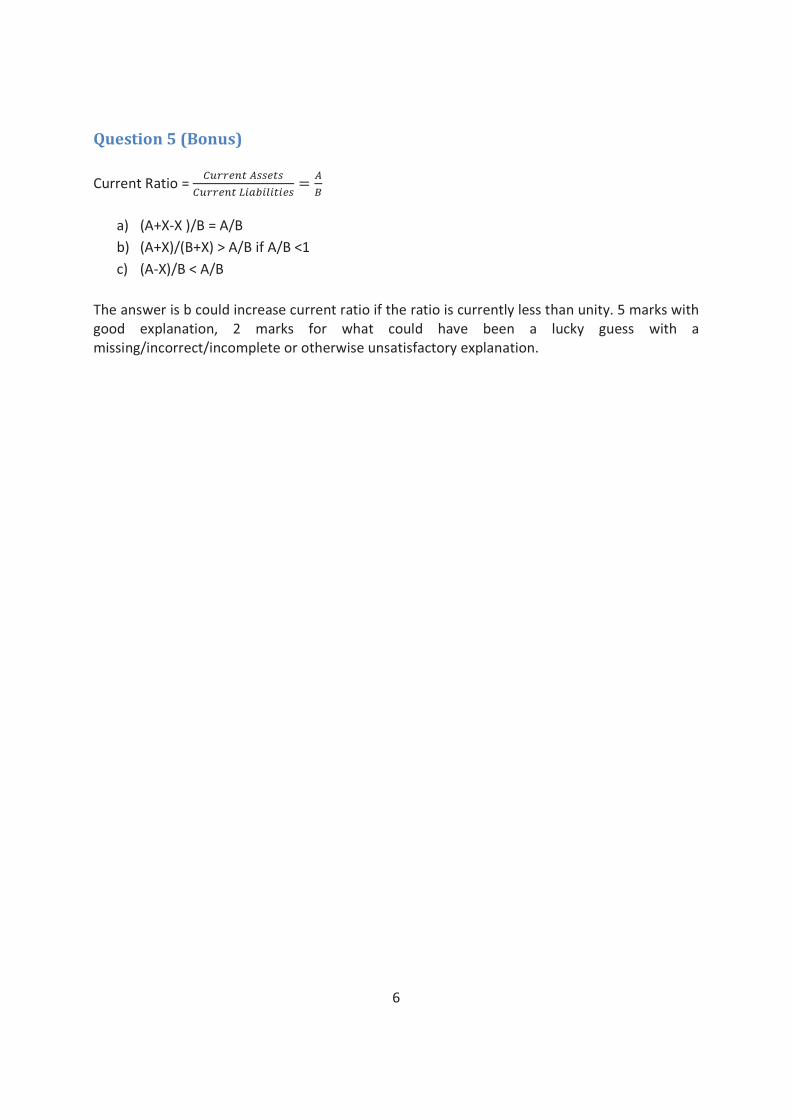

Question (onus)

urrent Assets ACurrent Ratio = = urrent Liabilities

a) (A+- )B = AB

b) (A+)(B+) AB if AB 1 c) (A-)B AB

The answer is b could increase current ratio if the ratio is currently less than unity 5 marks with good explanation 2 marks for what could have been a lucky guess with a missingincorrectincomplete or otherwise unsatisfactory explanation

6

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

2962961 Management for Engineers

Fall 2012

Professor Henry Marcus Professor Jung-Hoon Chun

Accounting Quiz

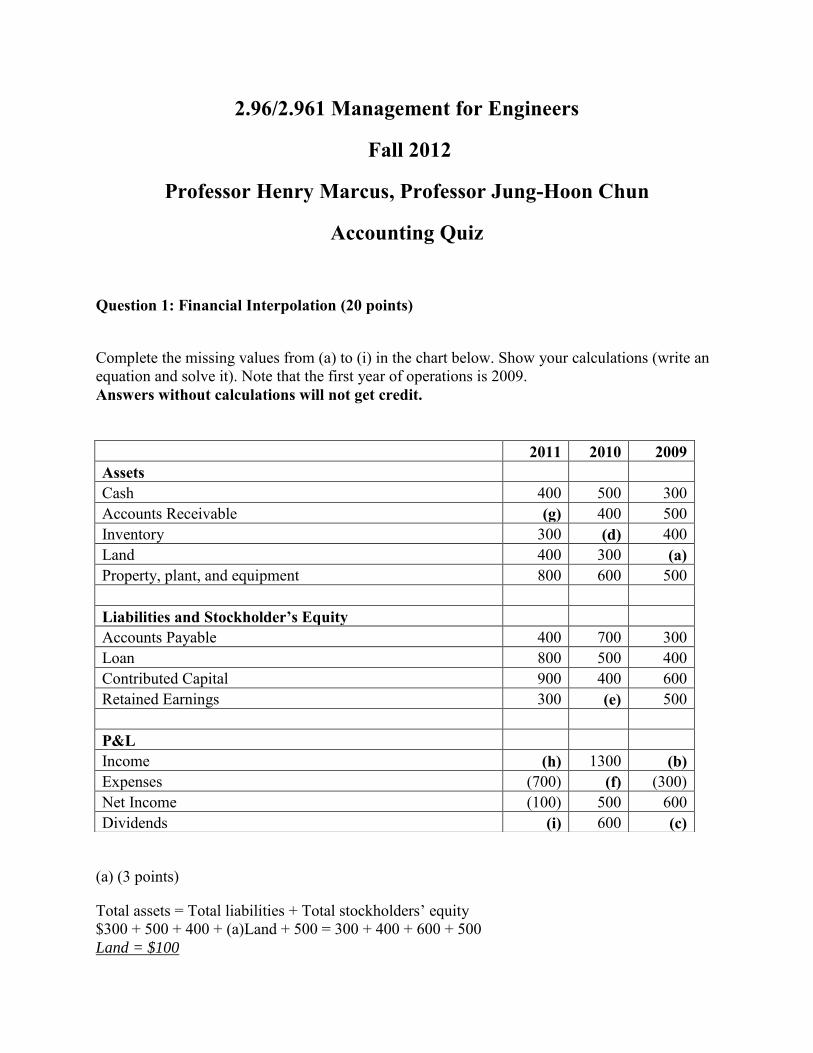

Question 1 Financial Interpolation (20 points)

Complete the missing values from (a) to (i) in the chart below Show your calculations (write an equation and solve it) Note that the first year of operations is 2009 Answers without calculations will not get credit

(a) (3 points)

Total assets = Total liabilities + Total stockholdersrsquo equity $300 + 500 + 400 + (a)Land + 500 = 300 + 400 + 600 + 500 Land = $100

2011 2010 2009

Assets Cash 400 500 300

Accounts Receivable (g) 400 500 Inventory 300 (d) 400 Land 400 300 (a) Property plant and equipment 800 600 500

Liabilities and Stockholderrsquos Equity Accounts Payable 400 700 300

Loan 800 500 400 Contributed Capital 900 400 600 Retained Earnings 300 (e) 500

PampL Income (h) 1300 (b)

Expenses (700) (f) (300) Net Income (100) 500 600 Dividends (i) 600 (c)

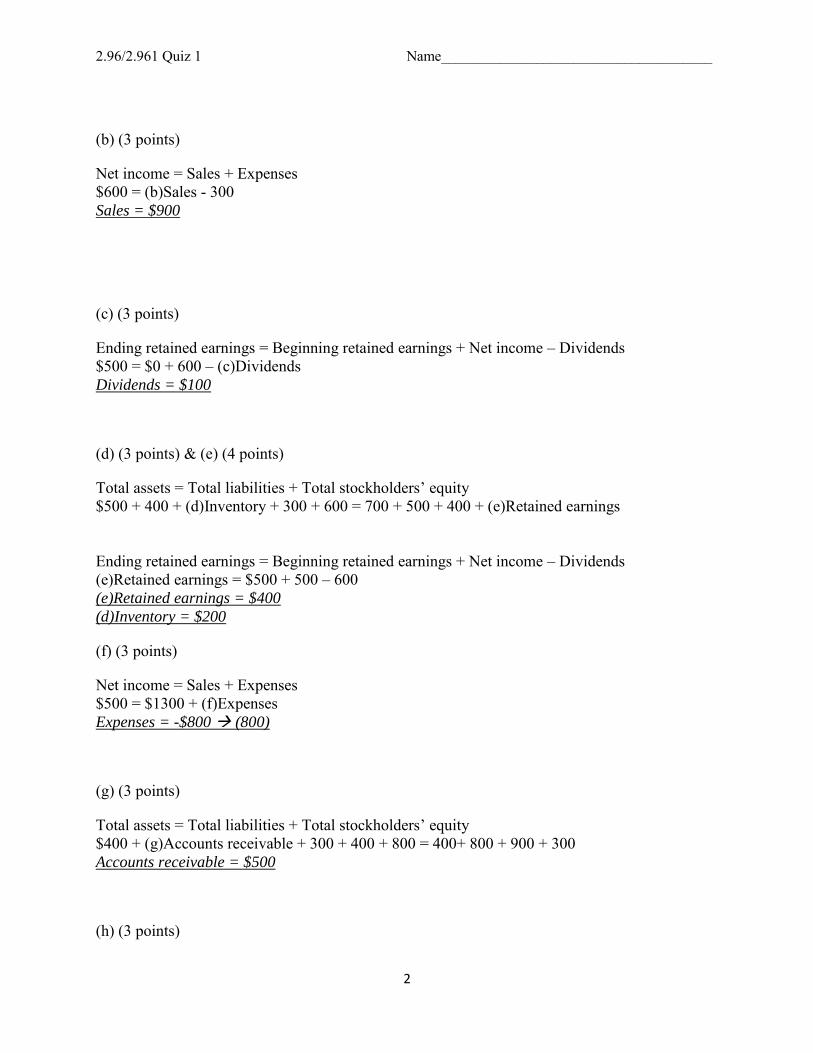

2962961 Quiz 1 Name_____________________________________

2

(b) (3 points)

Net income = Sales + Expenses $600 = (b)Sales - 300 Sales = $900

(c) (3 points)

Ending retained earnings = Beginning retained earnings + Net income ndash Dividends $500 = $0 + 600 ndash (c)Dividends Dividends = $100

(d) (3 points) amp (e) (4 points)

Total assets = Total liabilities + Total stockholdersrsquo equity $500 + 400 + (d)Inventory + 300 + 600 = 700 + 500 + 400 + (e)Retained earnings Ending retained earnings = Beginning retained earnings + Net income ndash Dividends (e)Retained earnings = $500 + 500 ndash 600 (e)Retained earnings = $400

(d)Inventory = $200

(f) (3 points)

Net income = Sales + Expenses $500 = $1300 + (f)Expenses Expenses = -$800 (800)

(g) (3 points)

Total assets = Total liabilities + Total stockholdersrsquo equity $400 + (g)Accounts receivable + 300 + 400 + 800 = 400+ 800 + 900 + 300 Accounts receivable = $500

(h) (3 points)

2962961 Quiz 1 Name_____________________________________

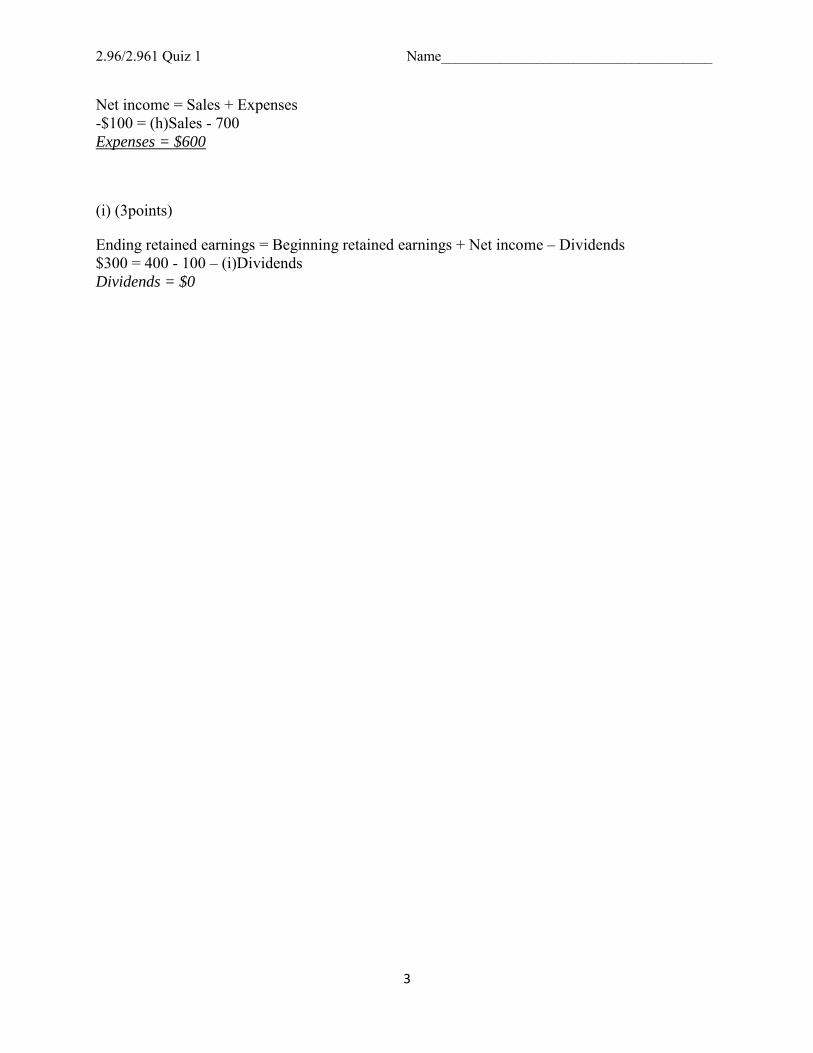

3

Net income = Sales + Expenses -$100 = (h)Sales - 700 Expenses = $600

(i) (3points)

Ending retained earnings = Beginning retained earnings + Net income ndash Dividends $300 = 400 - 100 ndash (i)Dividends Dividends = $0

2962961 Quiz 1 Name_____________________________________

4

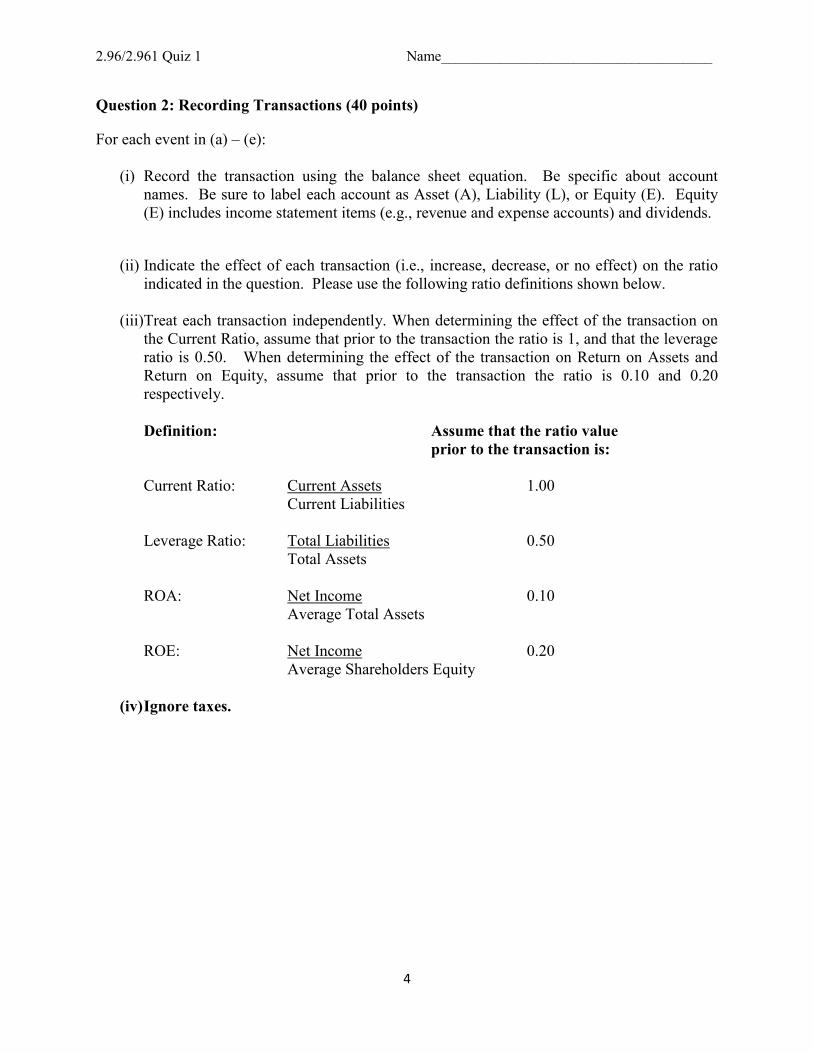

Question 2 Recording Transactions (40 points)

For each event in (a) ndash (e)

(i) Record the transaction using the balance sheet equation Be specific about account names Be sure to label each account as Asset (A) Liability (L) or Equity (E) Equity (E) includes income statement items (eg revenue and expense accounts) and dividends

(ii) Indicate the effect of each transaction (ie increase decrease or no effect) on the ratio indicated in the question Please use the following ratio definitions shown below

(iii)Treat each transaction independently When determining the effect of the transaction on

the Current Ratio assume that prior to the transaction the ratio is 1 and that the leverage ratio is 050 When determining the effect of the transaction on Return on Assets and Return on Equity assume that prior to the transaction the ratio is 010 and 020 respectively

Definition Assume that the ratio value

prior to the transaction is Current Ratio Current Assets 100 Current Liabilities Leverage Ratio Total Liabilities 050 Total Assets ROA Net Income 010 Average Total Assets ROE Net Income 020 Average Shareholders Equity

(iv) Ignore taxes

2962961 Quiz 1 Name_____________________________________

5

Question 2 Recording transactions (continued)

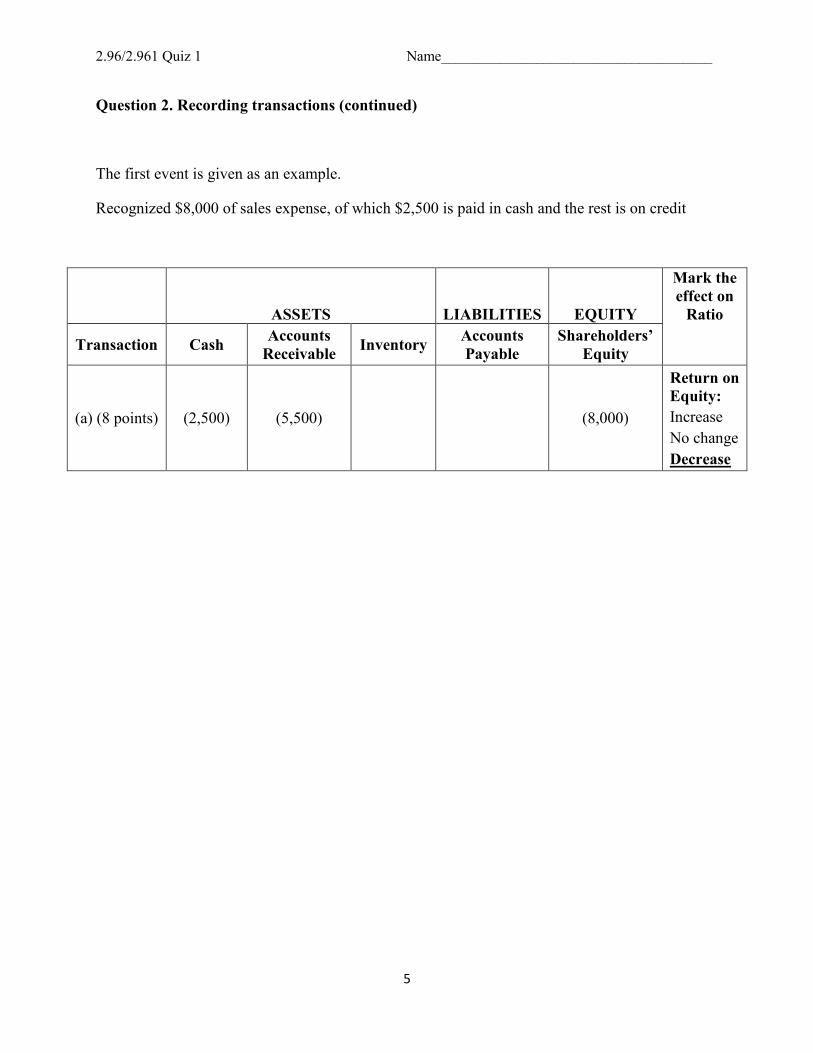

The first event is given as an example

Recognized $8000 of sales expense of which $2500 is paid in cash and the rest is on credit

ASSETS LIABILITIES EQUITY

Mark the effect on

Ratio

Transaction Cash Accounts Receivable Inventory Accounts

Payable Shareholdersrsquo

Equity

(a) (8 points) (2500) (5500) (8000)

Return on Equity Increase No change Decrease

2962961 Quiz 1 Name_____________________________________

6

Question 2 Recording transactions (continued)

(a) (8 points) Recorded $12000 in depreciation expense

(b) (8 points) Provided service to the customer and recognized $20000 revenue on account

(c) (8 points) Paid a $12000 dividend in cash

(d) (8 points) Received $12000 from a customer for a payment of accounts receivable

(e) (8 points) Purchased $10000 of inventory on account

ASSETS LIABILITIES EQUITY Mark the effect on

Ratio Transaction Cash Accounts Receivable Inventory Accounts

Payable Shareholdersrsquo

Equity

(a) (8 points) (12000) (12000)

Return on Assets Increase No change Decrease

(b) (8 points) 20000 20000

Leverage Ratio Increase No change Decrease

(c) (8 points) (12000) (12000)

Return on Equity Increase No change Decrease

(d) (8 points) 12000 (12000)

Current Ratio Increase No change Decrease

(e) (8 points) 10000 10000

Return on Assets Increase No change Decrease

2962961 Quiz 1 Name_____________________________________

7

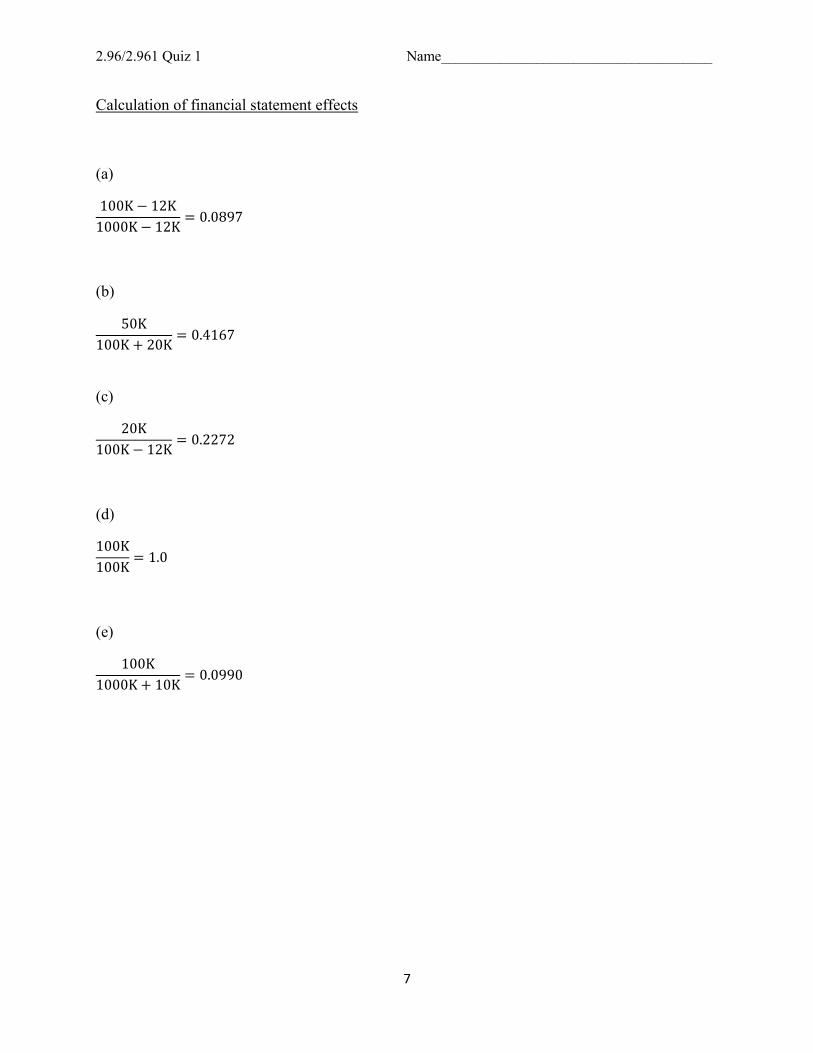

Calculation of financial statement effects

(a)

(b)

(c)

(d)

(e)

2962961 Quiz 1 Name_____________________________________

8

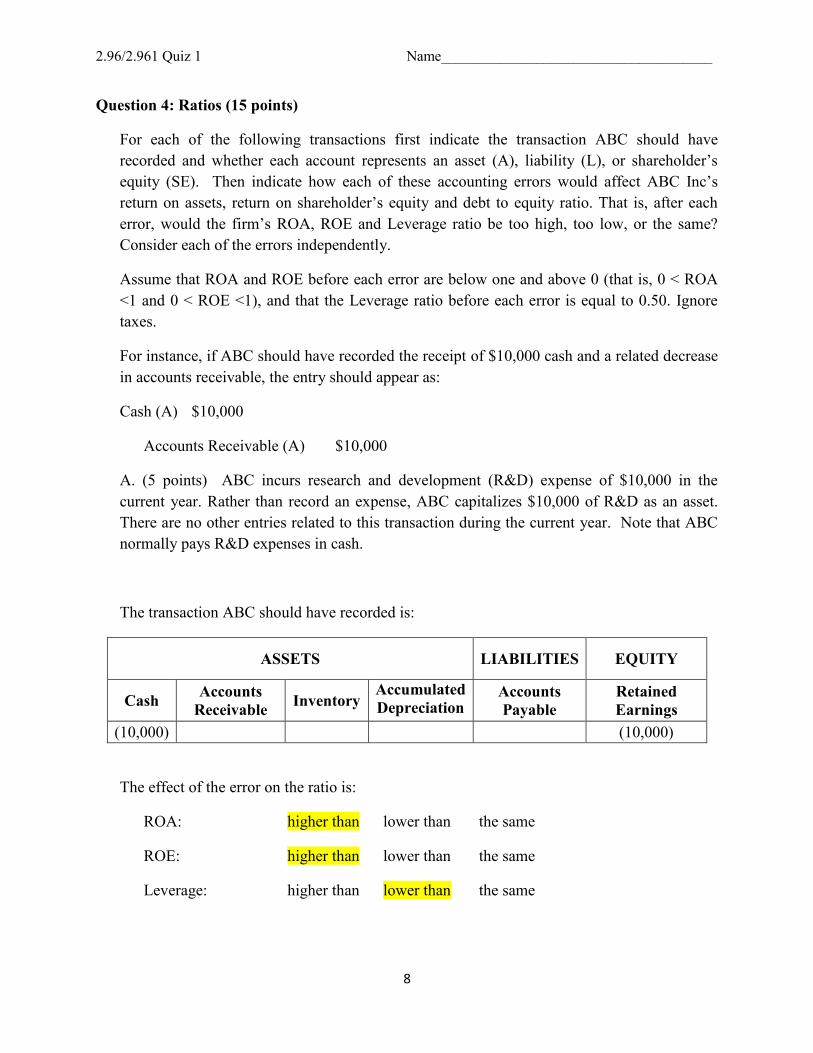

Question 4 Ratios (15 points)

For each of the following transactions first indicate the transaction ABC should have recorded and whether each account represents an asset (A) liability (L) or shareholderrsquos equity (SE) Then indicate how each of these accounting errors would affect ABC Incrsquos return on assets return on shareholderrsquos equity and debt to equity ratio That is after each error would the firmrsquos ROA ROE and Leverage ratio be too high too low or the same Consider each of the errors independently

Assume that ROA and ROE before each error are below one and above 0 (that is 0 lt ROA lt1 and 0 lt ROE lt1) and that the Leverage ratio before each error is equal to 050 Ignore taxes

For instance if ABC should have recorded the receipt of $10000 cash and a related decrease in accounts receivable the entry should appear as

Cash (A) $10000

Accounts Receivable (A) $10000

A (5 points) ABC incurs research and development (RampD) expense of $10000 in the current year Rather than record an expense ABC capitalizes $10000 of RampD as an asset There are no other entries related to this transaction during the current year Note that ABC normally pays RampD expenses in cash

The transaction ABC should have recorded is

ASSETS LIABILITIES EQUITY

Cash Accounts Receivable Inventory

Accumulated Depreciation

Accounts Payable

Retained Earnings

(10000) (10000)

The effect of the error on the ratio is

ROA higher than lower than the same

ROE higher than lower than the same

Leverage higher than lower than the same

2962961 Quiz 1 Name_____________________________________

9

B (5 points) ABC receives a loan in the amount of $20000 from the bank The company mistakenly records the loan as a common stock issuance

The transaction ABC should have recorded is

ASSETS LIABILITIES EQUITY

Cash Accounts Receivable Inventory

Accumulated Depreciation Loan Retained

Earnings 20000 20000

The effect of the error on the ratio is

ROA higher than lower than the same

ROE higher than lower than the same

Leverage higher than lower than the same

C (5 points) During a physical inventory count at yearend ABC realizes that 200 units of inventory costing $20000 are missing however ABC fails to update its accounting records

The transaction ABC should have recorded is

ASSETS LIABILITIES EQUITY

Cash Accounts Receivable Inventory

Accumulated Depreciation Loan Retained

Earnings (20000) (20000)

The effect of the error on the ratio is

ROA higher than lower than the same

ROE higher than lower than the same

Leverage higher than lower than the same

2962961 Quiz 1 Name_____________________________________

10

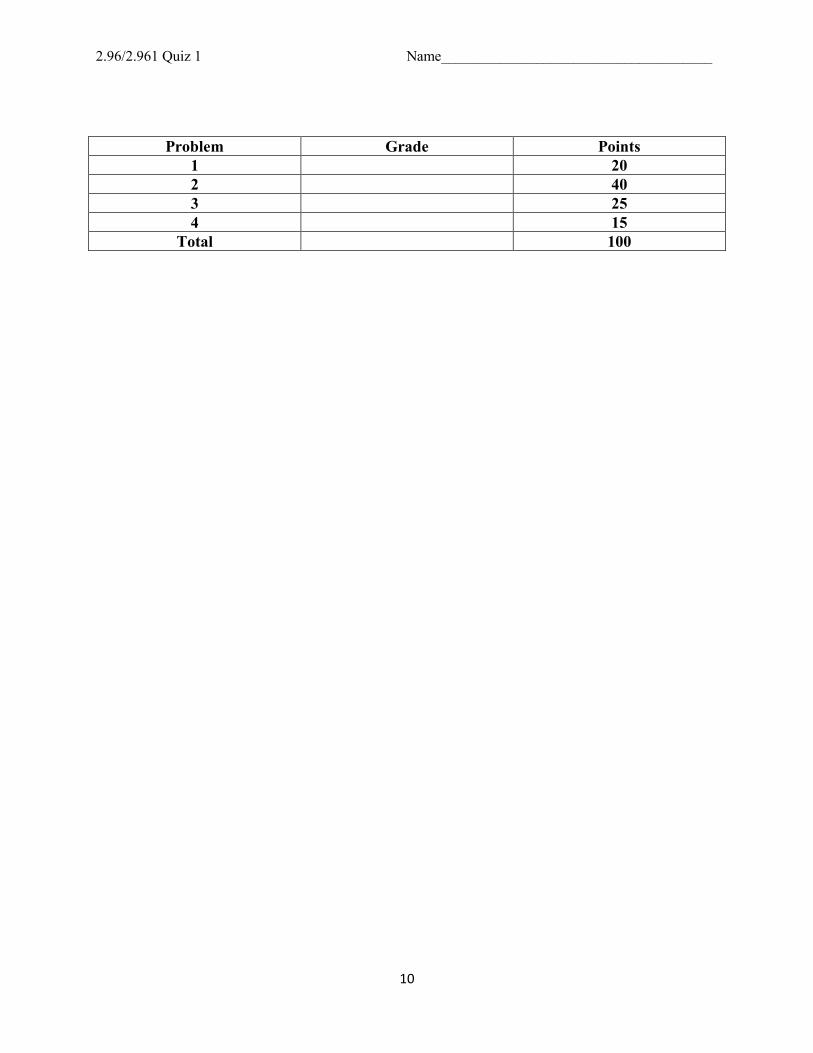

Problem Grade Points 1 20 2 40 3 25 4 15

Total 100

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

You will often have a chance to develop or evaluate business propositions If you do

nothing else at least cover these elements

Presenting Business Opportunities Document Simply and Clearly

Customer Need

What unmet customer need exists that you are addressing Which customers What are

the characteristics of the need and those customers

Proposed Solution

How do you plan to fulfill the need described What alternatives are available (or could

be) to the customers and why is your solution preferred How is our solution better than

the competition What are the key elements of the solution proposed How do you plan

to implement When

Costs

What are the major costs and assets of delivering this solution Provide enough detail so

we understand them well

Price and Profit

What do we plan to charge the customer What are their expectations What are the

margins and the net profits

Risks

What are the important things that could go wrong What are our plans to minimize the

occurrence or the cost of those risks

Dr Abbott Weiss

Senior Lecturer

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

What do you recommend HP should do

Universal power supply raquo Yes raquo No

Why

111712 2

Mfg Eng

MktgController

HP managers around the table

Prod Design 111712 3

Measurements and Behavior

Five functional managers are discussed in the case

a) Marketing b) Product Design amp Development c) Finance d) Manufacturing Engineering e) Distribution

Distribution

How are they measured How does it influence their views on the universal power supply

111712 4

Universal Power Supply - Costs amp Benefits

Costs Benefits

higher cost per unit = $50 lengthen Break-Even Time (BET) problems allocating supply

increase forecast accuracy fewer stockouts fewer lost sales less safety stock required fewer expedited shipments eliminates re-configuration work

111712 5

Key Consequences of this Decision

111712 6

Probability of Worldwide Demand

HP Network Printer Demand Worldwide

60

50

40

30

20

10

0

50

Average demand = 25000 per month Average forecast error = 40 at maturity

31 31

16 16

1 2

7 7

2 1

- 10000 20000 30000 40000 50000 60000

Monthly Demand in Units

111712 7

Prob

abili

ty o

f Mon

thly

Dem

and

Cumulative Demand Probability Curve

HP Network Printer Demand - Cumulative Probability

1 2 7

16

31

50

69

84

93 98 99

0

20

40

60

80

100

120

- 10000 20000 30000 40000 50000 60000

at least this Monthly Demand Worldwide

Cum

ulat

ive

Prob

abili

ty o

f Dem

and

Average demand = 25000 per month Average forecast error = 40 at maturity

2 Standard Deviations gives 98 coverage of possible forecast maxima

111712 8

What happens to forecast error if we have a universal power supply

111712 9

What happens to forecast error if we have a universal power supply

The variability of the forecast errors would combine as follows

21 2 2

2 1 2 σρσσσσ ++= new

where σ

12 are the individual product forecast error standard deviations ρ is the correlation coefficient of the two errors

Letrsquos say your individual forecast value is 10 and σ 12 both equal 04 (40) If the errors are completely

uncorrelated (ρ =0) then the standard deviation of the forecast error of the combined product stream would be 057 or 28 of the combined forecast of 20

If people tend to buy one product or the other and a drop in one always occurs with a rise in the other (perfect negative correlation ρ = -1) then the new standard deviation would be 00

If say world events always cause similar errors in both products (perfect positive correlation ρ = 1) then the new standard deviation would be 080 or 40 of the combined forecast

So you can only get better by combining products

111712 10

What happens to forecast error if we have a universal power supply

The variability of the forecast errors would combine as follows

21 2 2

2 1 2 σρσσσσ ++= new

At start-up the individual errors are 80+ If the errors tend to offset each other then the combined error will be closer to 40

where σ

12 are the individual product forecast error standard deviations ρ is the correlation coefficient of the two errors

Letrsquos say your individual forecast value is 10 and σ 12 both equal 04 (40) If the errors are completely

uncorrelated (ρ =0) then the standard deviation of the forecast error of the combined product stream would be 057 or 28 of the combined forecast of 20

If people tend to buy one product or the other and a drop in one always occurs with a rise in the other (perfect negative correlation ρ = -1) then the new standard deviation would be 00

If say world events always cause similar errors in both products (perfect positive correlation ρ = 1) then the new standard deviation would be 080 or 40 of the combined forecast

So you can only get better by combining products At maturity the individual errors are ~40 If the errors tend to offset each other then the combined error will be closer to 20

111712 11

Key Learnings for Management in Engineering

Engineeringdesign decisions have major impact on operations and customer service

Consider all the costs especially when things do not go according to plan

Measurements and rewards change behavior influence how your company operates

111712 12

Key Takeaways

1 Forecasts are always wrong 2 How wrong (a) a lot or (b) an awful lot 3 Challenge for international markets power localization etc 4 Global supply lines mean long lead times aggravating the problem 5 Design can have a major impact on supply chain flexibility 6 Hard costs will lead you to specialized products Inventory

benefits can be very large but are Soft costs 7 Who is measured on inventory 8 Hidden costs are often invisible or occur much later than the key

decisions which can create them 9 Do the math Think again about what could change the answer 10 Remember that this is one of many decisions over time

111712 14

Key Learnings for Supply Chain Management

Value of postponement

Organizational roles and measurements

International dimensions

111712 15

Value of Postponement HP Network Printer Demand Worldwide

60

40

30Reduced cycle times 50

20

0 - 10000 20000 30000 40000 50000 60000

50

Average demand = 25000 per month Average forecast error = 40 at maturity

31 31

16 16

1 2

7 7

2 1

Monthly Demand in Units Lower forecast errors 10

Smaller safety stocksfewer stockouts Lower obsolescence costs Reduced penalty costsprofit drains

Prob

abili

ty o

f Mon

thly

Dem

and

raquo Reconfiguration and extra handling raquo Premium transportation raquo Prevent lost revenue and profit raquo Prevent loss of market share

Changes during product life cycle

111712 16

Organizational roles and Measurements

Marketing EngineeringDesignProduct Management Finance Manufacturing Procurement LogisticsDistribution General Managers Supplierpartner

111712 17

Organizational roles and Measurements

Accountability BET (Break-Even Time)

How to measure Who pays

Effects of regional PampLs

Costs raquo Product cost raquo Transportation raquo Inventory raquo Obsolescence raquo Stockouts

Net profit

111712 18

International Aspects

Product variety Distance and time for supply Power and regulatory requirements Labeling packaging Forecast complexities Supplier inflexibility Accountability and measurement

111712 19

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012 For information about citing these materials or our Terms of Use visit httpocwmiteduterms

Strategic Planning of RampD

- 2 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Outline

Risk Factors in RampD

Strategic Focus

Stage-Gate Process

Technology Choice Case

- 3 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Company Births and Deaths

1995 594000 births amp 497000 deaths

2002 580900 births amp 576200 deaths

2005 670058 births amp 599333 deaths

SBA Office of Advocacy

- 4 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Attrition Rate of New-Product Ideas

For every 11 serious ideas 3 enter development 13 are launched 1 succeeds

- 5 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Attempts to Start New Business

One success in ten

The odds are much poorer for new ideas

- 6 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

The Business Plan Funnel

Business Plan Received (600) Listen to presentation (60)

Visit (20) Due Diligence Negotiation (12)

Investment (3) Brookwood Partners

- 7 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Causes of New Product Failure

0

5

10

15

20

25

30

35

40

45

Inadequate MarketAnalysisProduct Problems orDefectsLack of EffectiveMarketing EffortHigher Costs thanAnticipatedCompetitive Strength orReactionPoor Timing of Initiative

Technical or ProductionProblemsAll Other Causes

- 8 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Failures not merely negligence

Attributable to lack of minus understanding customer requirements

minus creating dramatic differences in current capabilities

minus understanding additional capabilities

- 9 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

The Suicide Square

New Technology

Inc

rea

se

d R

isk

- 10 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

The Suicide Square

New Product

New Technology

Inc

rea

se

d R

isk

- 11 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

The Suicide Square

New Market New Product

New Technology

Inc

rea

se

d R

isk

- 12 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

The Suicide Square

New Market New Product

New Technology

Inc

rea

se

d R

isk

- 13 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Risk Matrices

Existing New

Technology

Ma

rket

s

New

Existing

Low Risk Low Returns

Market Risk Ordinary Returns

Market and Tech Risk ldquoThe Death Zonerdquo

Technology Risk High Returns

- 14 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

CD Risk Matrix 1981 Sony Philips Matsushita

Existing New

Technology

Ma

rket

s

New

Existing

Vinyl records to audio market

Sell floppy disks to the PC market

Sell CDrsquos to the PC market

Sell CDrsquos to the Audio market

- 15 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

CD Risk Matrix 1985-1996 Sony Philips Matsushita

Existing New

Technology

Ma

rket

s

New

Existing

Sell CDrsquos to the PC market

Sell CDrsquos to the Audio market

Sell DVDrsquos to the Video market

Sell DVDrsquos to the Video Game market

- 16 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Technology Management

Strategic focus

Business process

- 17 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Strategic Focus Choose attractive strategic markets or market

segments to participate in

Find ldquoBeaconsrdquo in selected markets and market segments

Identify core competencies needed to address products markets and applications

Plan a product market application competency succession strategy

- 18 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Business

PRODUCT MARKET APPLICATION

Product What we supply to add value Market Who we supply the value to Application How customers use the product to realize value

- 19 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Business

PRODUCT MARKET APPLICATION

Automotive

- 20 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Business

PRODUCT MARKET APPLICATION

VW Group

GM Opel

BMW Rover

Ford

Hose

ampTubing

Assemblies

- 21 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Business

PRODUCT MARKET APPLICATION

VW

GM

BMW

Ford

Hose

ampTubing

Assemblies

AC Systems

- 22 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Technology Strategy vs Corporate Strategy

Identify the firmrsquos ldquoCore Competencyrdquo

Specify the types of products markets applications and technologies for focus

Specify the role technology innovation plays in achieving the firms overall objectives

- 23 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Strategic Resources Focus and Risk

Assign resources to reflect strategic focus

Assign resources according to the acceptable level of risk

Reconcile differences between the stated strategy and specified resources

- 24 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

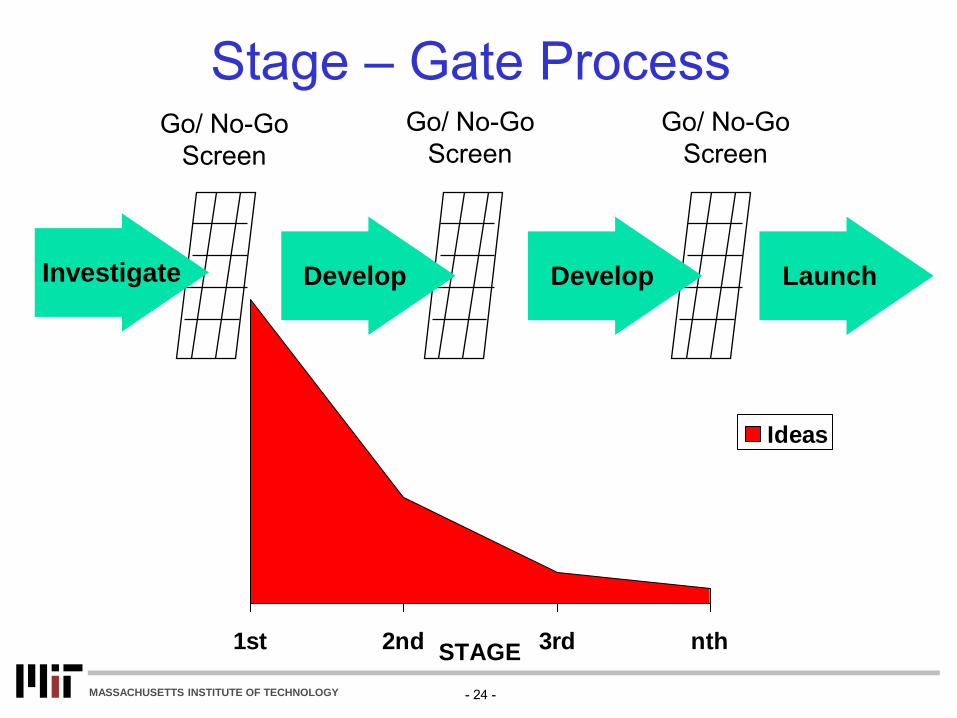

Stage ndash Gate Process

Develop Develop Launch

1st 2nd 3rd nthSTAGE

Ideas

Go No-Go Screen

Go No-Go Screen

Go No-Go Screen

Investigate

Modified Stage-Gate with Continuous Customer Interaction

Development New product

IDEA Strategic

focus

Customer

Customer

n-th Development

- 26 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Concurrent Business Development

Cross-disciplinary teams Knowledge must broaden

minus Engineers are ldquotechnicalrdquo experts but must understand the business

minus Managers are ldquobusinessrdquo experts but must understand the technology

- 27 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Case Study Technology Choice

Grumman Corporation

- 28 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Basic Factors in Evaluating a Technology

Will the technology satisfy a market sometime in the future (Market Need) minus Does it provide improved performance minus Does it reduce costs minus Is its market penetration rate acceptable

When will the product become significant (Timing)

- 29 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Basic Factors in Evaluating a Technology (cont)

Will the technology be commercially viable (Economics)

minus Does the market exist or will it be created minus Does the potential market size justify the

investment minus Is the production process feasible and practical minus Is the product profitable to manufacture

- 30 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Solar grid parity is close

- 31 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

- 32 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Solarrsquos Challenge Scale

202 287 401 560 750 1256

1815 2536

4279

7910

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

MW

s

Global Cell Production

Despite record growth generation from PV still is only 02 of total global electricity

- 33 - MASSACHUSETTS INSTITUTE OF TECHNOLOGY

Our energy supply will change and PV will

play a big role

2050 2100

Renewables bull Hydro bull Solar Electric bull Wind bull Bio-fuels bull Geothermal

1800 1850 1900 1950 2000

Nuclear

Wood

Coal

Oil

Gas

100

80

60

40

20

0

Hydro

Year Source Energy Information Agency

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012 For information about citing these materials or our Terms of Use visit httpocwmiteduterms

You will often have a chance to develop or evaluate business propositions If you do

nothing else at least cover these elements

Presenting Business Opportunities Document Simply and Clearly

Customer Need

What unmet customer need exists that you are addressing Which customers What are

the characteristics of the need and those customers

Proposed Solution

How do you plan to fulfill the need described What alternatives are available (or could

be) to the customers and why is your solution preferred How is our solution better than

the competition What are the key elements of the solution proposed How do you plan

to implement When

Costs

What are the major costs and assets of delivering this solution Provide enough detail so

we understand them well

Price and Profit

What do we plan to charge the customer What are their expectations What are the

margins and the net profits

Risks

What are the important things that could go wrong What are our plans to minimize the

occurrence or the cost of those risks

Dr Abbott Weiss

Senior Lecturer

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

HP Printer Case Study amp Questions

Due Wednesday November 14 2012

Read Hewlett-Packard Company Universal Power Supply for Printer Design (p357)

The questions on the last page of the case study (p 365) are there to stimulate your thoughts as you analyze the case For the written assignment please answer the following questions in less than one page 1) What do you recommend HP do about the universal power supply and why 2) Five functional managers are discussed in the case a) Marketing b) Product Design amp Development c) Finance d) Manufacturing Engineering e) Distribution What do you believe are the primary measures of each departments performance and how do they affect the managerrsquos views about this decision

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

Self-Unloader Dry Bulk Ships Case Study amp Questions

Read the SUL Company case study For your written assignment I want you to calculate the premium (expressed as a percentage) that the self-unloader shipowner must charge compared to the owner of a standard bulker This premium should be evaluated for a ship that costs $60 million to build (includes an additional $12 million in vessel cost for the self-unloader) and has a daily operating cost (opex) of $8900 The premium must provide an equivalent return on capital (ROC) and return on equity (ROE) when compared to the original values for the standard bulker (See guidelines below as to how to do this) In class we will discuss

The above calculation assumes that the self-unloader spends the same time in port as a standard bulker What impact does it have that the self-unloader has a faster unloading rate and therefore a shorter time in port How do you quantify this impact

What should SUL Corsquos pricing policy be From a shipownerrsquos viewpoint what are the prorsquos and conrsquos of being a self

unloader shipowner Should SUL Co build the ship described in the case studyspreadsheet How does the down market affect SUL Corsquos decision

Guidelines for the SUL Mendoza Investment Model To modify capital costs Change cell F7 from a value of $48000000 to $60000000 To change operating expenses Change cell V8 from a value of $7000 to $8900 To change the time charter equivalent (TCE) rate Think of the TCE rate as the amount that the shipowner charges for the use of his ship each day To see the impact of increasing the TCE by X change cell F17 from 0 to X Hit ldquoEnterrdquo For your homework just state the PERCENTAGE PREMIUM plus 3 reasons why you think that SUL Co willmdashor will notmdashbe able to obtain this premium

This assignment sheet was prepared by Nathan L Pratt and Henry S Marcus as an introduction to working with the referenced investment model Some information in this spreadsheet (the inputs relating to TCE and interest rates in particular) has been disguised at the request of the author of the spreadsheet

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

Ethics ndash Group Homework Assignment

Read Ethics Scenarios (p 233)

For the written assignment please answer the following question in one paragraph as a group for your scenario

What would you do and why

If your entire group doesnrsquot agree on one answer you may add a paragraph with the minorityrsquos opinion

See the scenario assignments by group below

Team Scenario U01 1 U02 2 U03 3 U04 4 U05 5 U06 6 U07 7 U08 8 G01 9 G02 10 G03 11

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in Engineering Fall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

2962961 Management for Engineers

Fall 2011

Professor Henry Marcus Professor Jung-Hoon Chun

and Dr Abbott Weiss

Accounting Quiz

October 31 2011

DO NOT OPEN this quiz until instructed to do so This quiz is CLOSED BOOK Put your name on top of every pagemdashthese pages may be separated for grading Write your solutions in the space provided Should you need extra space write in

the back of the page with the problem Blue books will be provided for your own use but will not be graded Be neat and write legibly

Fill in your name and the names of the people sitting next to you If you are at the end of a row write ldquoXrdquo in the space provided

Your name Name of person to your left Name of person to your right

1 2 3 4 5

2962961 Quiz 1 Name______________________________________

Problem Grade Points 20 40 25 15 5

Total 105

2

2962961 Quiz 1 Name______________________________________

Question 1 Financial Interpolation (20 points)

Complete the missing values from (a) to (i) in the chart below Show your calculations (write an equation and solve it) Note that the first year of operations is 2009 Answers without calculations will not get credit

If you canrsquot find the value for A please use the number 90 If you canrsquot find the value for I please use the number (150)

2011 2010 2009 Assets Cash 160 110 (a) Accounts Receivable 100 60 70 Inventory 150 (d) 80 Land 40 40 40 Property plant and equipment 160 140 (b)

Liabilities and Stockholderrsquos Equity Accounts Payable 50 110 175 Loan 150 200 200 Contributed Capital 310 310 310 Retained Earnings (g) (e ) (300)

PampL Income 1500 1300 900 Expenses (h) (1100) (1200) Net Income 300 (f) (300) Dividends 100 0 (c )

Cash Flow Net cash increase (decrease) from operating activities 220 55 (275) Net cash increase (decrease) from Investing activities (20) (35) (145) Net cash increase (decrease) from Financing activities (i) 0 510

(a)

(b)

3

2962961 Quiz 1 Name______________________________________

(c)

(d)

(e)

(f)

(g)

(h)

(i)

4

2962961 Quiz 1 Name______________________________________

Question 2 Recording Transactions (40 points)

Test Corp (ldquothe Companyrdquo) made the following transactions during 2010 fiscal years (assume that they are listed in chronological order)

1 The business was started on January 1st by the owner when she contributed $10000 in cash 2 On January 1st the Company paid rent for two years in the total amount of $2400 3 On January 1st the Company purchased computers in the amount of $900 The computers

have a useful life of 3 years and a salvage value of 0 4 The Company provided service to customers and recognized $3000 revenue on account (did

not receive cash) 5 The Company Collected $1500 cash from customers 6 On July 1 the company borrowed $2000 from M-E Bank at an interest rate of 10 for 12

months The interest is payable on June 30 2011 7 On December 31 the Company distributed dividends in the amount of $600 to the owners

(a) Record ALL the effects of each of the events above on the table provided below Mark an increase with a + and a decrease with ( )

(b) Evaluate the effect of each transaction on the Leverage ratio (circle whether the ratio will increasenot changedecrease)

ASSETS LIABILITIES EQUITY Mark the effect on Leverage

Ratio Transaction Cash

Accounts Receivable (including

other)

Equipment Interest Payable Loan Shareholders

Equity

Increase Nochange decrease Increase Nochange decrease Increase Nochange decrease Increase Nochange decrease Increase Nochange

5

2962961 Quiz 1 Name______________________________________

ASSETS LIABILITIES EQUITY Mark the effect on Leverage

Ratio Transaction Cash

Accounts Receivable (including

other)

Equipment Interest Payable Loan Shareholders

Equity

decrease Increase Nochange decrease Increase Nochange decrease Increase Nochange decrease Increase Nochange decrease Increase Nochange decrease

6

2962961 Quiz 1 Name______________________________________

Question 3 Cash Flow Statement (25 points)

Use the balance sheet and income statement on the FOLLOWING PAGES (PAGE 8-9) to generate a cash flow statement for 2011 in the space below

CASH FLOW STATEMENT (2011) Cash Flow from Operating Activities

Cash Flow from Investing Activities

Cash Flow from Financing Activities

7

8

2962961 Quiz 1 Name______________________________________

CONSOLIDATED BALANCE SHEETS FOR TEST CORPORATION

Oct 31 2011 Oct 31 2010

ASSETS Current Assets

Cash and Cash Equivalents 420 150 Accounts Receivables 90 40 Inventory 300 680

Total Current Assets 810 870 Property Plant and Equipment Property Plant and Equipment 470 470 Less Cumulative Depreciation (210) (180) Total Property Plant and Equipment 260 290

Total Assets 1070 1160 LIABILITIES Current Liabilities

Accounts Payable 310 150 Other Current Liabilities 200 300

Total Current Liabilities 510 450 Long-term Liabilities

Loan 0 400 Total Long-term Liabilities 0 400 Total Liabilities 510 850 SHAREHOLDERrsquoS EQUITY Paid-in Capital 230 80 Retained Earnings 330 230 Total Stockholder Equity 560 310

Total Liabilities amp Stockholdersrsquo Equity 1070 1160 On the first day of the period (Nov 1 2010) a property with a book value of 100 and a cumulative depreciation of 0 (zero) as of Oct 31 2010 was stolen and the company recognized its value as a loss in the PampL

8

ASSET

ASSETS

ASSETS

ASSETS

S

LIABILITIES

SHAREHOLDERrsquoS EQUITY

2962961 Quiz 1 Name______________________________________

CONSOLIDATED INCOME STATEMENT FOR TEST CORPORATION

Period Ending Oct 31 2011

Total Revenue 2000 Cost of Goods Sold 1225 Gross Profit 775

Research Development 250 Selling General and Administrative 170 Depreciation and amortization 30 Total Operating Expenses 450

Operating Income or Loss 425

Finance Expenses 25 Income Before Tax 400

Income Tax Expense 100 Net Income From Continuing Ops 200

Non-recurring Events

Loss from stolen property 100

Net Income 100

On the first day of the period (Nov 1 2010) a property with a book value of 100 and a cumulative depreciation of 0 (zero) as of Oct 31 2010 was stolen and the company recognized its value as a loss in the PampL

9

Operating Expenses

Non-recurring Events

2962961 Quiz 1 Name______________________________________

Question 4 Ratios (15 points)

Company ldquoWinBigrdquois interested in raising funding for a new activity Here is the companyrsquos Balance sheet for January 1st 2011 (the day in which the company is trying to raise the money)

Cash 150000 Accounts Payable 160000 Accounts Receivable 130000 Accrued Expenses 40000

Land 300000 Long Term Loan 100000

Shareholders Equity 80000 Paid in Capital 110000 Retained Earnings 90000

The company received two funding alternatives

1 A loan in a sum of $100000 fully due at the end of the year carrying a 5 interest payable at the end of the year In addition the company must maintain a debt to equity ratio equal or lower than 125

2 A loan in a sum of $100000 fully due at the end of the year carrying a 6 interest payable at the end of the year In addition the company must maintain a debt to assets ratio equal or lower than 075

The loan in the companyrsquos balance sheet above is a previous loan (not one of these alternatives)

(a) Which of these alternatives WinBig should choose in order to maintain the requirements detailed above Explain your answer and show your calculations

Bonus Question

5 Which of the following could cause an increase in the Current Ratio (5 points)

a Purchasing inventory with cash b Purchasing inventory on credit (Accounts Payable) c Purchasing fixed assets with cash d None of the above

10

MIT OpenCourseWarehttpocwmitedu

296 2961 6930 10806 16653 Management in EngineeringFall 2012

For information about citing these materials or our Terms of Use visit httpocwmiteduterms

2962961 Midterm Exam Answer Key Question 1 There are generally multiple valid equations to get to the correct answers These are just examples Also note the order of performing these calculations is not simply ai Up to -2 marks per error

a) Assets = Liabilities + Shareholder Equity a+70+80+40+b=175+200+310+(300) a = 90

b) Net Cash from Investing = (Incr in Land) + (Incr in PPE) (145) = (40) -b b = 105

c) REend = REbegin + NI - Dividends (300) = 0 + (300) - c c = 0

d) Assets = Liabilities + Shareholder Equity 110+60+d+40+140=110+200+310+e d=170

e) REend = REbegn + NI - Dividends e = (300)+f-0 e=(100)

f) NI = Income + Expenses f = 1300 + (1100) f = 200

g) REend = REbegin+NI-Dividends g = e + 300-100 g = 100

h) NI = Income + Expenses 300=1500+h h=(1200)

i) Net Cash from Financing = Incr in Cash - Net Cash from Operating - Net Cash from Investing i = 50-220-(20) i = (150)

1

Question 2 Recording Transactions (40 points) We accepted two alternative calculations for the Leverage Ratio (Debt to Equity Ratio or The Current Ratio) Accordingly there were multiple right answers to some of the sections (for the effect on the Leverage Ratio part) The correct answers are marked in Bold and Underlined

Each Transaction was worth 4 points (including 1 point for the effect on the ratio)

You were required to record ALL the effects of each of the transactions Recording the ones listed below provides a complete answer Here are some comments about reoccurring mistakes

1 Transaction 2B is the end of year adjustment for the prepaid rent expenses 2 Transaction 3B is depreciation (End of year) 3 Transaction 6B is required to record interest expenses for the period from July 1st to

December 31 of 2010

ASSETS LIABILITIES EQUITY Mark the effect on Leverage

Ratio Transaction Cash

Accounts Receivab

le (includin g other)

Equipme nt

Interest Payable Loan Shareholders

Equity

1 +10000 +10000

Increase Nochange decrease

2A - on 1110 (2400) +2400

Increase Nochange decrease

2B - on 123110

(1200) (1200)

Increase Nochange decrease

3A -on 1110 (900) +900

Increase Nochange decrease

3B -on 123110 (300) (300)

Increase Nochange decrease

4 +3000 +3000

Increase Nochange decrease

5 +1500 (1500)

Increase Nochange decrease

2

ASSETS LIABILITIES EQUITY Mark the effect on Leverage

Ratio Transaction Cash

Accounts Receivab

le (includin g other)

Equipme nt

Interest Payable

Loan Shareholders

Equity

Increase 6A -on Nochange 7110 +2000 +2000 decrease 6B -on Increase

123110 Nochange decrease

+100 (100) Increase Nochange

7 (600) (600) decrease Not

Total 9600 2700 600 100 2000 10800 required

Question 3 Cash Flow Statement

In the next page you can find the complete answer for this question The maximum score for a complete answer for each line is described on the right column In addition for every additional entry (something that should not appear in this report but you added it anyway) we reduced 1 point

Here are some comments about reoccurring mistakes

1 Since the Income statement includes a loss of 100$ (due to the stolen property) which did not have an effect on cash - you were required to add an adjustment in the Non Cash adjustments part

2 Although it seems the PPampE did not change during the year (Beginning Balance and Ending Balance are the same) since we know property in a value of 100$ was stolen (reduced the PPampE by a 100$) than we must assume the company purchased additional PPampE in the same amount

3

Period Ending 3l-0ct-ll

Net Income l00

Non Cash Adjustments Increase in Cumulative Depreciation 30 Increase in Accounts Receivable -50 Decrease in Inventory 380 Increase in Accounts Payable 160 Decrease in Other Current Liabilities -100

Loss from stolen property 100

Max score

05

333331

2

Net Cash Increase from Operating Activities 620

Cash Flow from Investing Activities