25-money supply process. commercial bank balance sheet assetsliabilitites loansdeposits u.s....

Post on 22-Dec-2015

215 views

TRANSCRIPT

25-Money Supply Process

Commercial Bank Balance Sheet

Assets Liabilitites

Loans Deposits

U.S. Bonds Borrowings from Banks

Foreign Bonds Borrowings from Fed

Reserves

Central Bank Balance Sheet

Central Bank Balance Sheet

Commercial Banks are required to hold reserves with the federal reserve system.

These exist electronically

When you write a check to Bob in Philadelphia, your bank doesn’t send cash to Bob’s bank in Philadelphia.

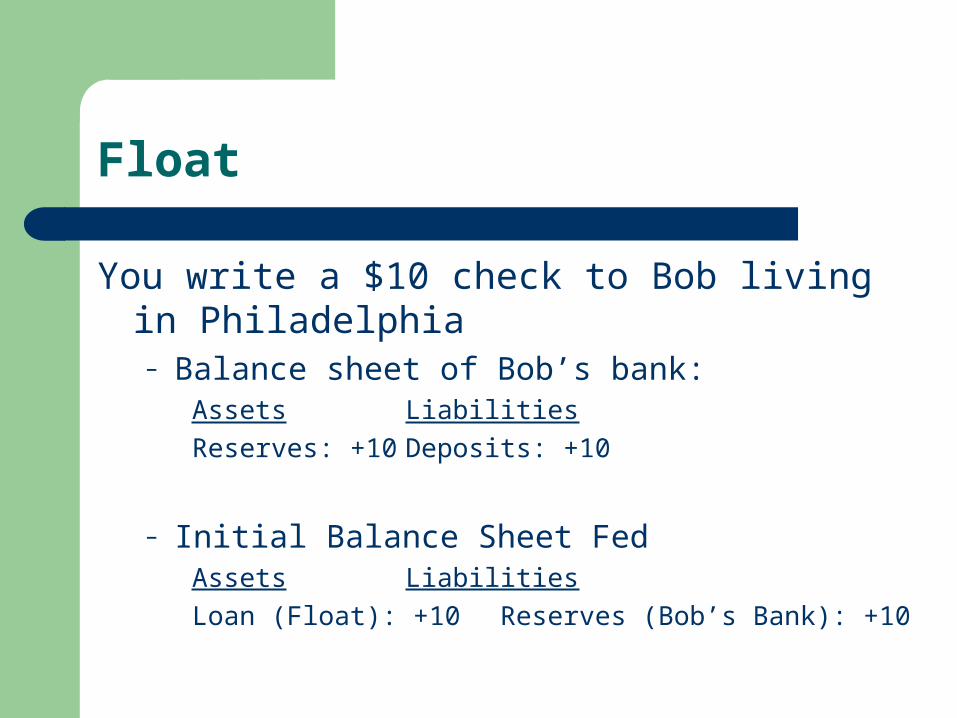

Float

You write a $10 check to Bob living in Philadelphia– Balance sheet of Bob’s bank:

Assets Liabilities

Reserves: +10 Deposits: +10

– Initial Balance Sheet FedAssets Liabilities

Loan (Float): +10 Reserves (Bob’s Bank): +10

Float

– Check is flown to your bank back in Utah

– Balance sheet of Your bank:Assets Liabilities

Reserves: -10 Deposits: -10

– Final Balance Sheet FedAssets Liabilities

Loan (Float): -10 Reserves (Your bank): -10

Central Bank Balance Sheet

The central bank differs from commercial banks in that it has full control over the size of its balance sheet– It can create liabilities (reserves)

Publication of Central bank balance sheet is essential component of transparency.– Value of reserves is backed by assets of bank– Central Bank on the gold standard

Transparency

Value of reserves is backed up by the bonds the Fed purchases.– Why do bonds (reserves) have value?

Government uses bonds to create services These services must be paid for by taxes (reserves)

– Our balance sheetAssets LiabilityGovernment Services Taxes (Reserves)

As long as we value government services, we will value the reserves we must use to pay for them, and hence, the bonds issued by the government.

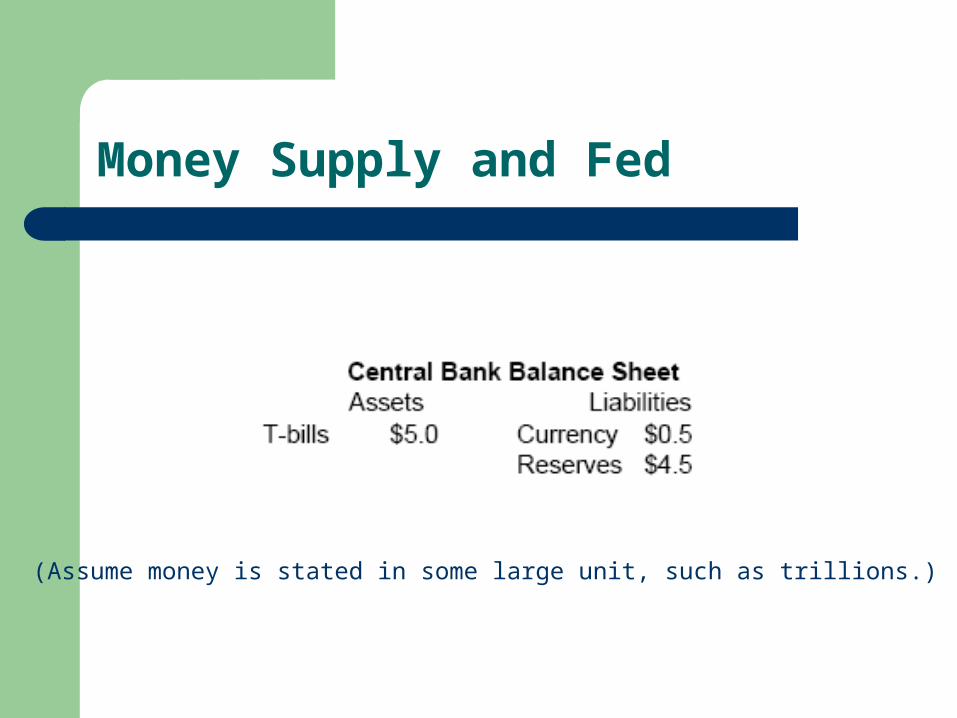

Money Supply and Fed

(Assume money is stated in some large unit, such as trillions.)

Money Supply and Fed

Assume required reserve-to-deposit ratio is 30%

Open Market Purchase

Assume Fed makes open market purchase of $1

OLD

NEW

Open Market Purchase

Assume Fed makes open market purchase of $1

OLD

INITIAL (Not end of the story)

Open Market Purchase

Reserve Deposit Ratio = 37% Bank will make loans

INITIAL

Open Market Purchase

Total reserves = 5.5 million Excess reserves are loaned out, spent, re-deposited,

spent, loaned out, redeposited . . .

Assume as deposits change, amount of currency held by public does not change.

– Deposits are not affected by a change in the demand for currency.

New Equilibrium: 5.5/D = 0.30

D=18.33

Open Market Purchase

NEW

Money Supply and the Fed

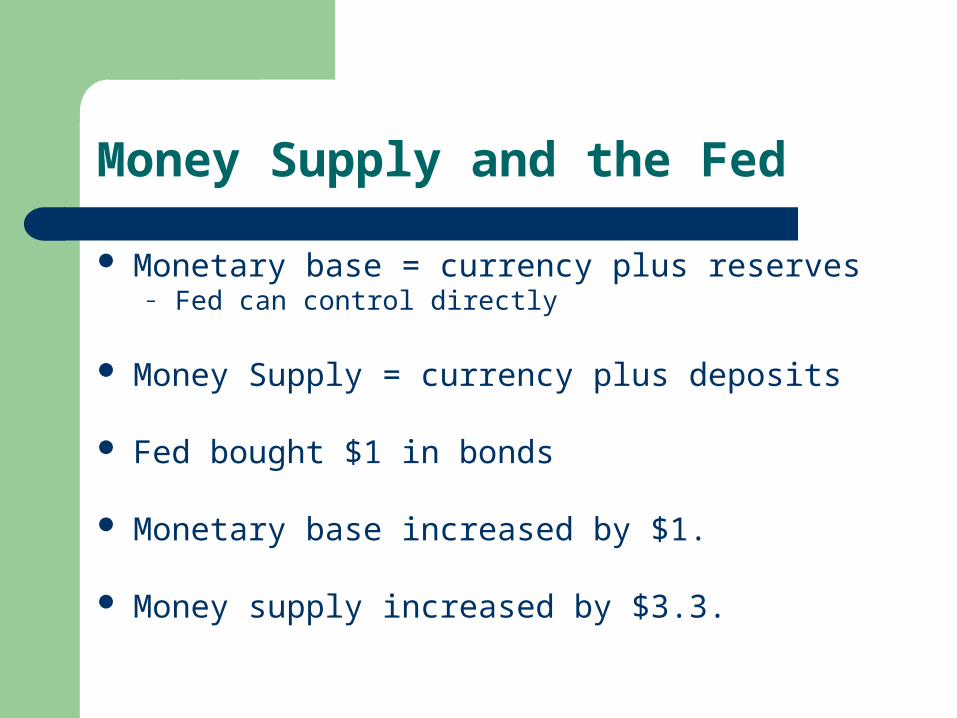

Monetary base = currency plus reserves– Fed can control directly

Money Supply = currency plus deposits

Fed bought $1 in bonds

Monetary base increased by $1.

Money supply increased by $3.3.

Simple Deposit Multiplier

Let rD = required reserve-to-deposit ratio Let R = amount of reserves D=deposits Assume no excess reserves are held

rD = R/D D = R/rD D = R/rD

In example– Change in reserves: +1– Change in deposits: +1/.30 = 3.33

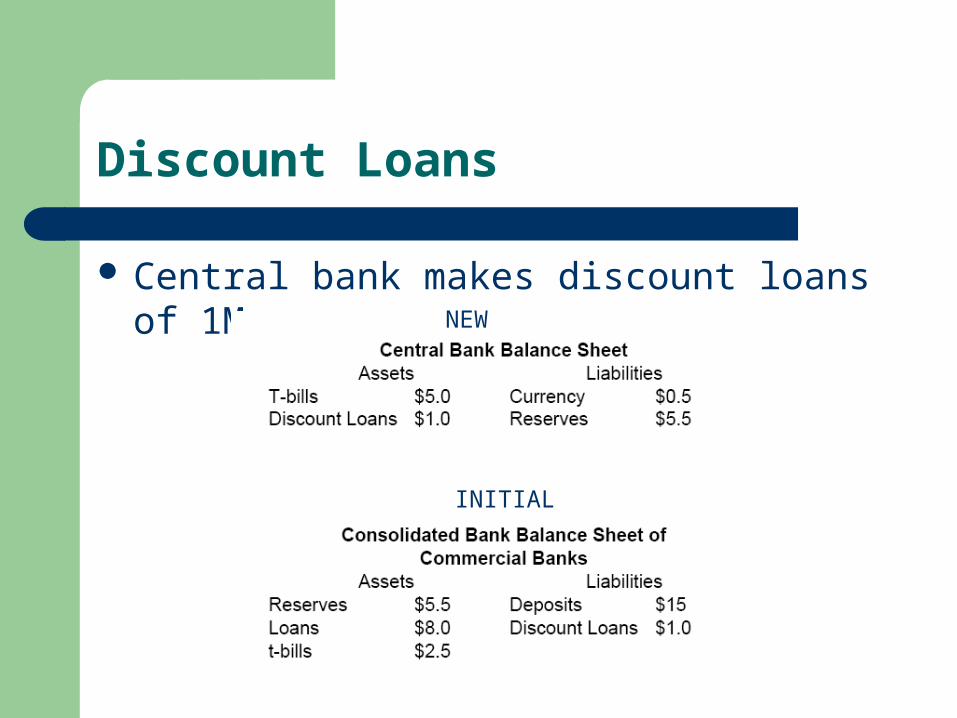

Discount Loans

Discount Loans

Central bank makes discount loans of 1MNEW

INITIAL

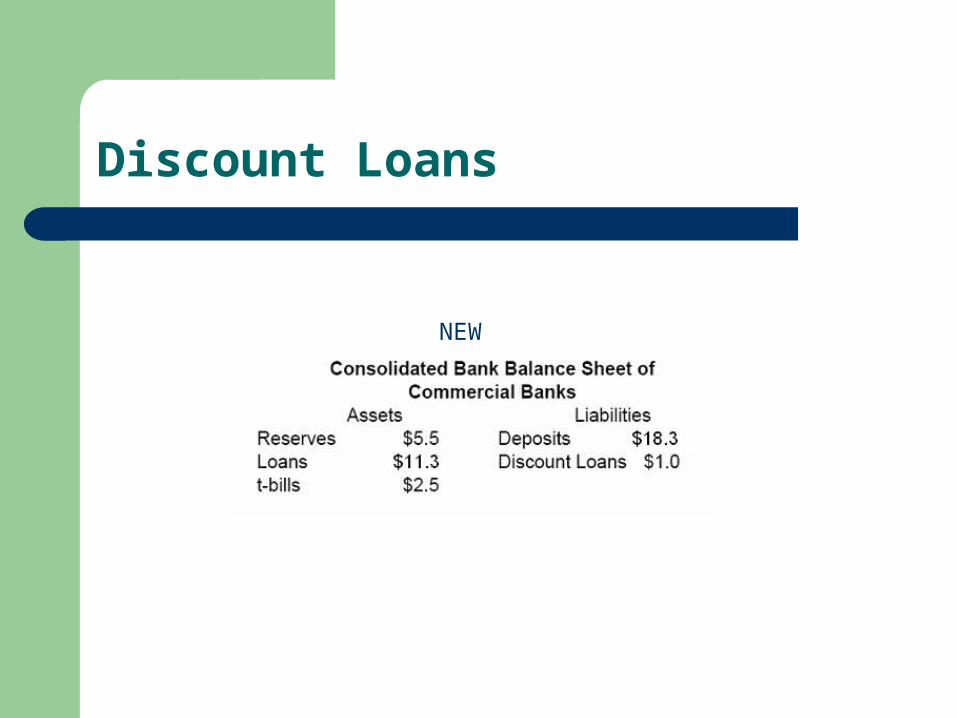

Discount Loans

NEW

Discount Loans

Open Market operations and discount loans both have the same effect on the monetary base and money supply:– Reserves increase by $1– MB=C+R increases by $1

– Deposits increase by 3.3– M=C+D increases by 3.3

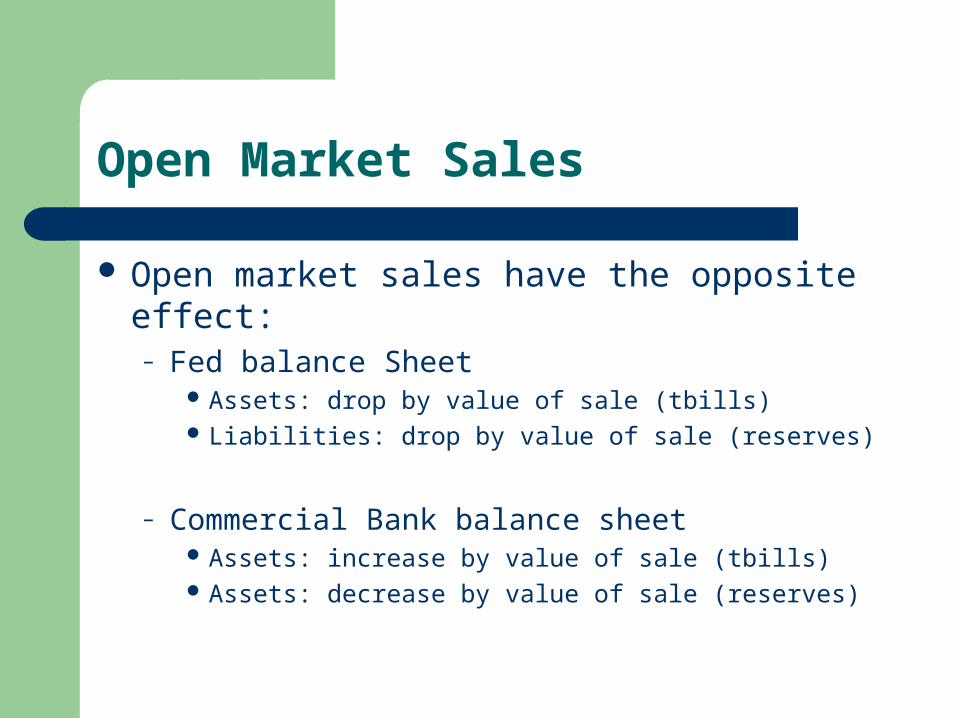

Open Market Sales

Open market sales have the opposite effect:– Fed balance Sheet

Assets: drop by value of sale (tbills) Liabilities: drop by value of sale (reserves)

– Commercial Bank balance sheet Assets: increase by value of sale (tbills) Assets: decrease by value of sale (reserves)

Open Market Purchase

In this case, reserves could drop below the required R/D ratio– Banks hold excess reserves as “insurance”– In the short run, banks with a shortage of

reserves can borrow from those with an excess– In long run, bank needs to either

acquire more reserves (Retire loans, or sell securities) reduce deposits (e.g. retire short-term CD liabilities)

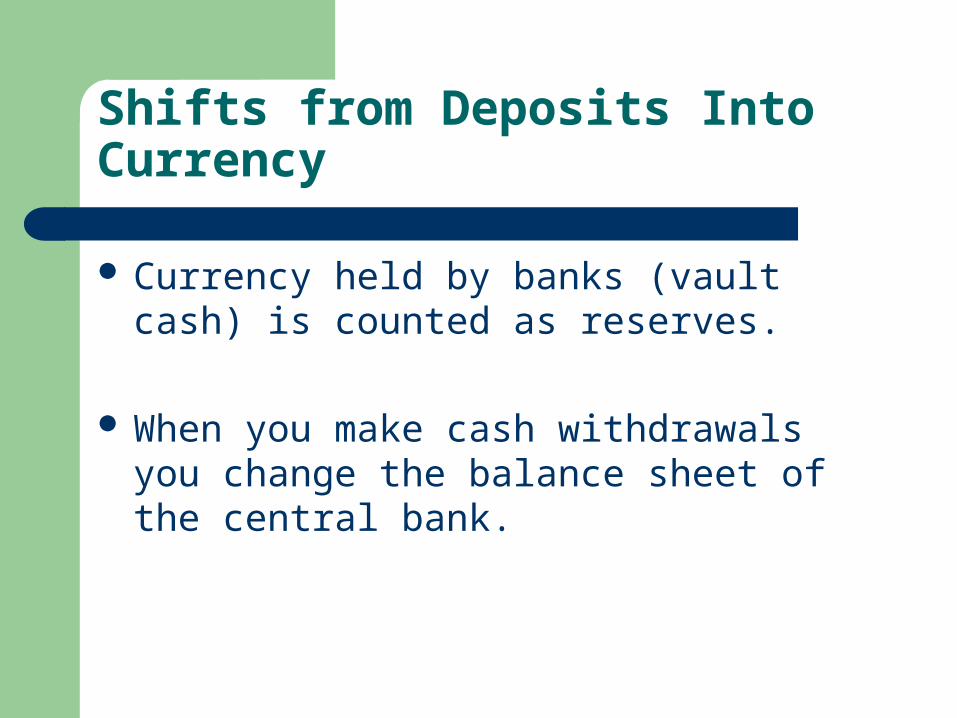

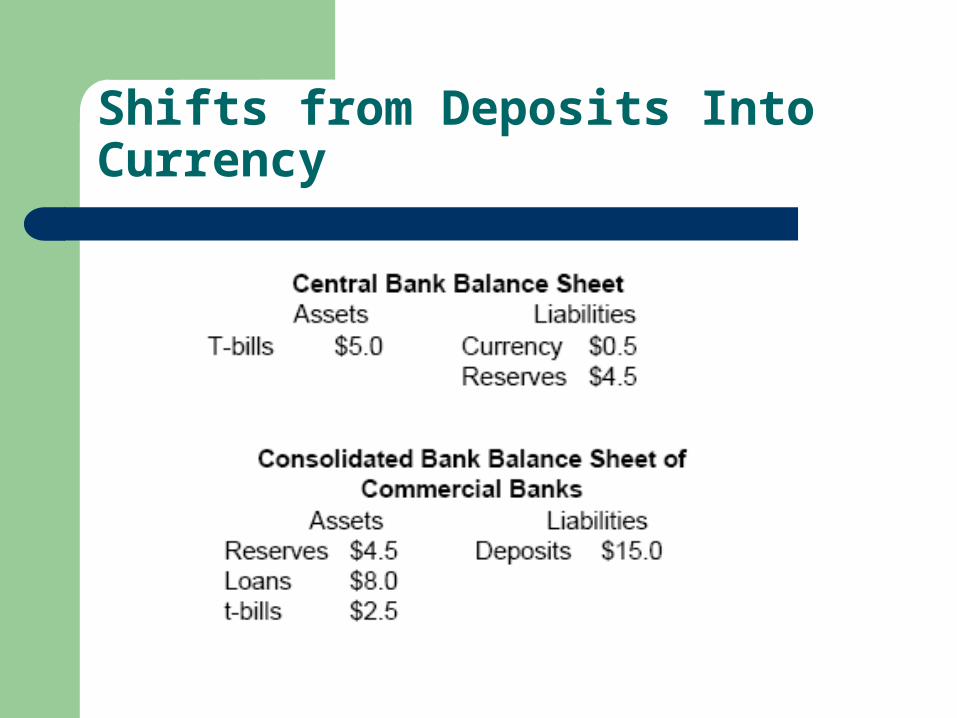

Shifts from Deposits Into Currency

Currency held by banks (vault cash) is counted as reserves.

When you make cash withdrawals you change the balance sheet of the central bank.

Shifts from Deposits Into Currency

Shifts from Deposits Into Currency

Suppose you withdraw $1 from an ATM

Your balance sheet

Shifts from Deposits Into Currency

Shifts from Deposits Into Currency

Change in Money Supply: – Currency: +2– Reserves: -2– Net effect =0

Change in Monetary Base:– Currency: +2– Deposits: -2– Net effect=0

Money Supply

As monetary base changes, what is impact on money supply?

Simple Deposit Multiplier– Assumes currency held by public is constant– Assumes banks only hold required reserves– Money supply changes with deposits D = R/rD

– Currency held doesn’t change, so M = D = R/rD

We will now relax these assumptions

Money Supply

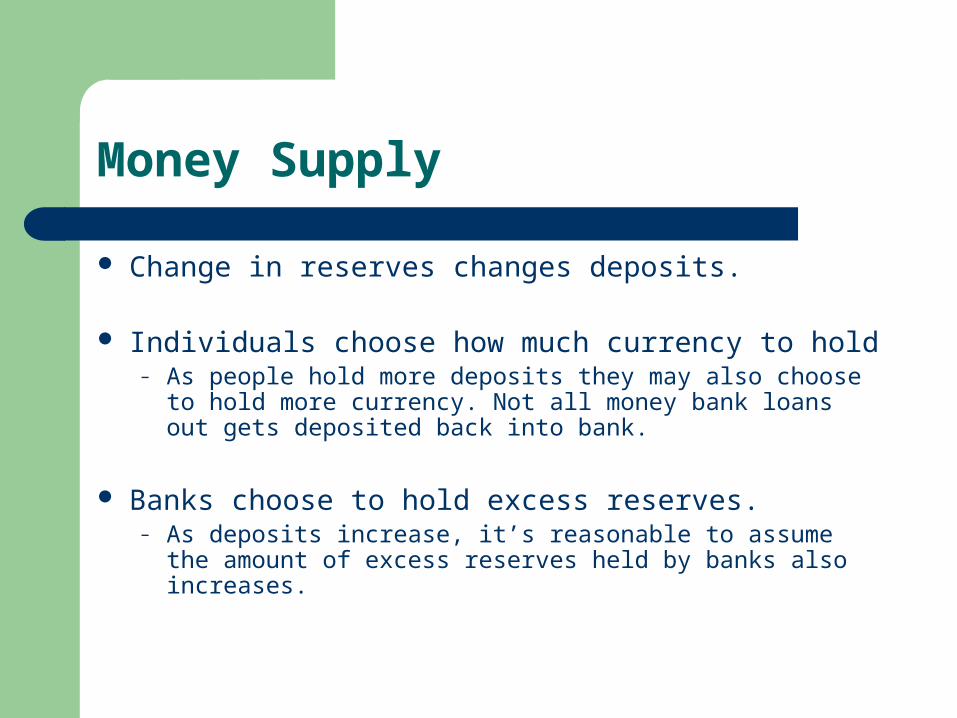

Change in reserves changes deposits.

Individuals choose how much currency to hold– As people hold more deposits they may also choose to hold

more currency. Not all money bank loans out gets deposited back into bank.

Banks choose to hold excess reserves.– As deposits increase, it’s reasonable to assume the amount

of excess reserves held by banks also increases.

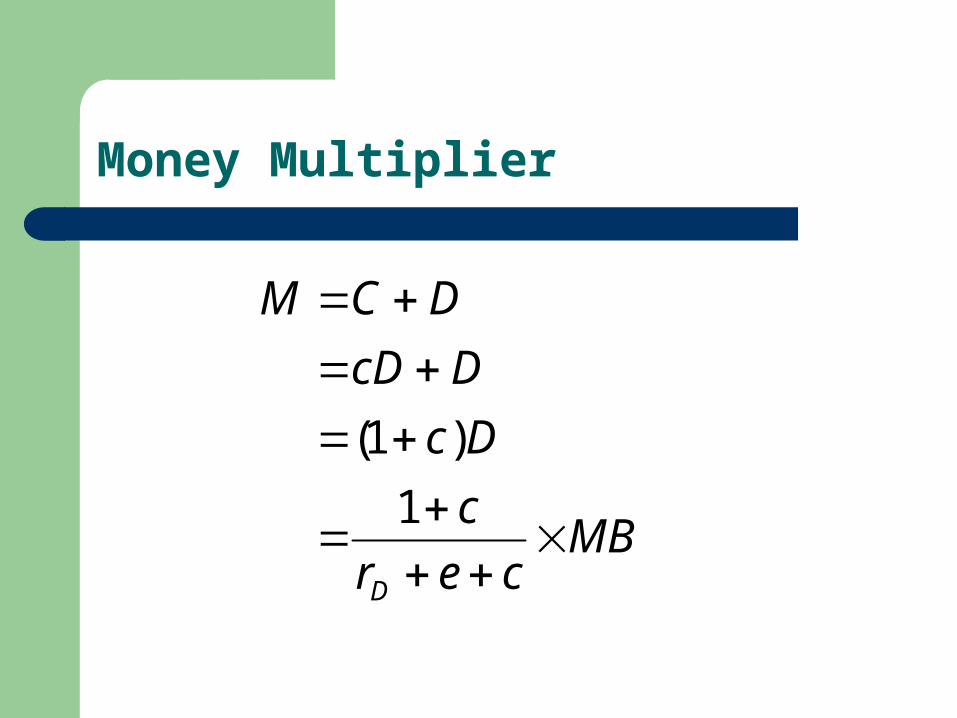

Money Multiplier

R=total reserves held RR=required reserves

– RR=rD*D rD=required reserve ratio

ER=excess reserves– ER=e*D e=excess reserve ratio

C=currency held by public– C=c*D c=currency ratio

Money Multiplier

cer

MBD

Dcer

cDeDDr

CERRR

CRMB

D

D

D

)(

Money Multiplier

MBcer

c

Dc

DcD

DCM

D

1

)1(

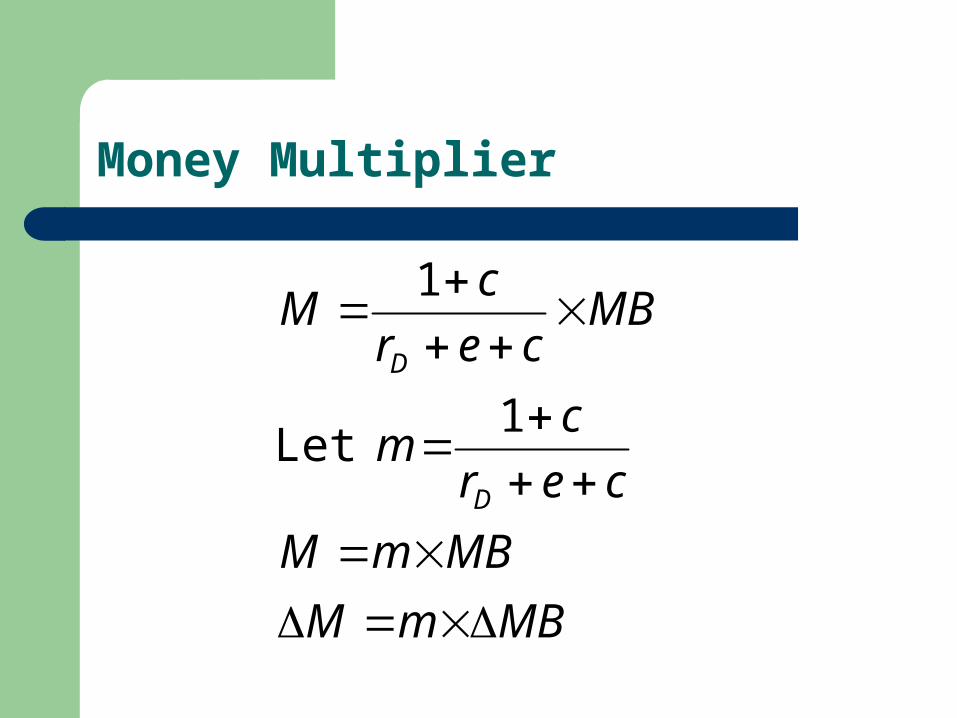

Money Multiplier

MBmM

MBmM

cer

cm

MBcer

cM

D

D

1

1

Let

Money Multiplier

Insight– m decreases as rD, e, and c increase

– A given change in the monetary base will have a smaller effect on the money supply as

The required reserve deposit ratio increases Banks desire to hold more excess reserves People desire to hold more cash

Money Multiplier as an Indicator

Central Bankers should keep an eye towards long-term money growth (determines inflation)

Fed View– Money Multiplier is too volatile and unpredictable

to exploit for short-run policy purposes